Embed Size (px)

Citation preview

Creating great

everyday experiences

Re-structuring

Accelerating innovation and growth

2016 -

2018

2012

2022

Consistently creating value to all stakeholders

2

2014

2019

Orientingfor growth

Digital Experience acceleration

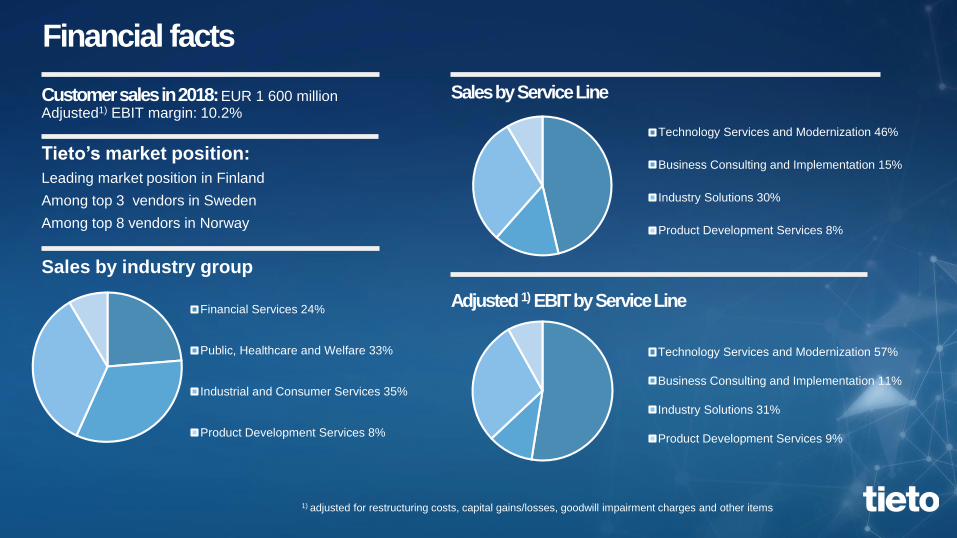

Financial Services 24%

Public, Healthcare and Welfare 33%

Industrial and Consumer Services 35%

Product Development Services 8%

Technology Services and Modernization 46%

Business Consulting and Implementation 15%

Industry Solutions 30%

Product Development Services 8%

Technology Services and Modernization 57%

Business Consulting and Implementation 11%

Industry Solutions 31%

Product Development Services 9%

Adjusted 1) EBIT by Service Line

Customer sales in 2018: EUR 1 600 millionAdjusted1) EBIT margin: 10.2%

Tieto’s market position:

Leading market position in Finland

Among top 3 vendors in Sweden

Among top 8 vendors in Norway

Sales by Service Line

Sales by industry group

1) adjusted for restructuring costs, capital gains/losses, goodwill impairment charges and other items

Financial facts

2018 as a continuation of our multi-year performance improvement

-5%

0%

5%

10%

15%

-100

-50

0

50

100

150

200

2014 2015 2016 2017 2018

EBIT, EUR million EBIT %

-6%

-4%

-2%

0%

2%

4%

-1000

-500

0

500

1000

1500

2000

2014 2015 2016 2017 2018

Net Sales, EUR million Growth %

2015 2016 2017 2018

2015 2016 2017 2018

CUSTOMER EXPERIENCE / NPS

EMPLOYEE ENGAGEMENT SCORE

REVENUE GROWTH, %

OPERATING MARGIN, %

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

2014 2015 2016 2017 2018

DIVIDEND/SHARE, EUR

Base dividend Additional dividend

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

1,0

2014 2015 2016 2017 2018

NET DEBT / EBITDA

Market opportunity and

strategy 2019

5

Personalized

experiences

Data-driven value

Cross-industry

ecosystems

Agile and adaptive

TIME

VALUE

CREATIONTODAY

Omnichannel

Industry 4.0

Servitization

Realtime

payments

Predictive

healthcare

Smart cities

Sustainability

IoT

Digital

citizen

services

Connected

vehicles

Industry

clouds

Connected

consumer

products

Designed experiences and data-driven services

Agile business models, services and ways of working

Make my product / service better, faster and cheaper

Definite products, processes and technologies

Customer agenda for driving competitiveness

Changing industry paradigm with new data-driven experiences

and business models

6

Data at the core of innovation and value creation

Adaptenterprise

architecture

Data and insights

Design and experience

Renewapplications

Agile

Hybrid Infrastructure

Cloud first Connected products Agile

AI Ecosystems Platforms

Cyber security

ML/NLP/RPA

Automation

Microservices

Agile sprints

co-creating

business

outcomes for

customers

Active innovation agenda

in the market

Design and data led

Agility driving both

innovation and efficiency

Faster time to market

7

Services enabling

customers’

competitiveness

Networked ways

of working

and leadership

Context-rich

customer

engagement

Leading CX in the market

Most engaging workplace

Upgraded financial ambition

We aim to make customers more competitiveStrategy 2019 choices and ambition

8

Digital

Experience

Hybrid Infra

Industry

Software

Product

Development

Services

Enable new business models and

experiences for customers.

Capability uplift

Agile at scale

Ensure customer’s business continuity,

efficiency and unified service experience.

Multi-cloud and scale

Automation and quality

Drive customer’s business critical

processes and functions.

Common R&D practices

Expansion

Making customers products connected with

world-class engineering.

New industry segments

Global expansion

Services enabling customers’ competitivenessTieto Service portfolio

9

© Tieto Corporation

Key markets: Finland, Sweden and Norway

Building on strong global delivery capabilities and long term

off-shore development

Focus on Nordic enterprises and the public sector

Selective international expansion of Industry Software

Longer term ambition for broader Tieto expansion

in European markets

PDS continues to grow its global customer base -

focusing on software R&D

Global delivery capabilities:China, Czech, India and Poland

Nordic focus, serving customers globally – with a global Tieto team

10Employing 15 000+

experts globally Serving customers in over

90 countries world-wide

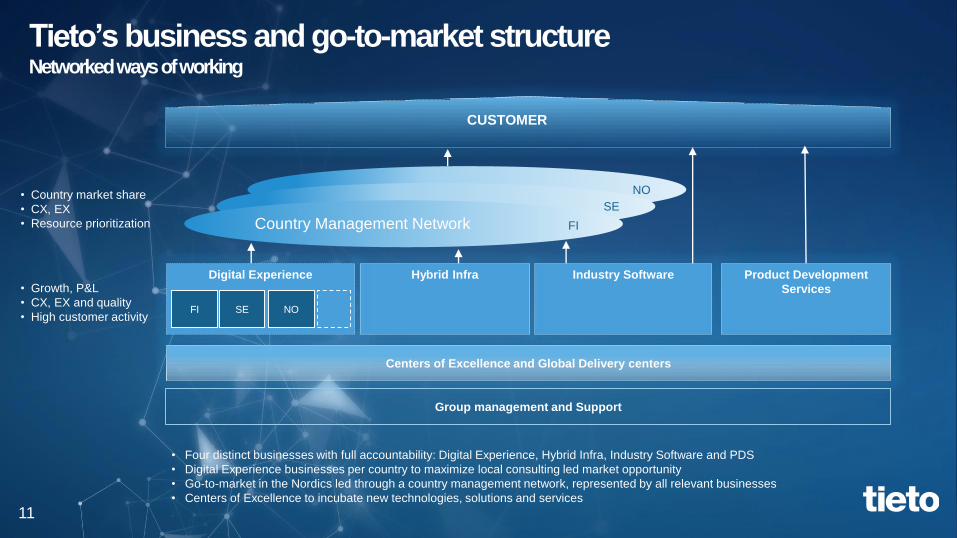

Country Management Network

Industry SoftwareHybrid Infra Product Development

Services

Digital Experience

CUSTOMER

• Country market share

• CX, EX

• Resource prioritization

• Growth, P&L

• CX, EX and quality

• High customer activity

FI

SE

NO

Group management and Support

Centers of Excellence and Global Delivery centers

• Four distinct businesses with full accountability: Digital Experience, Hybrid Infra, Industry Software and PDS

• Digital Experience businesses per country to maximize local consulting led market opportunity

• Go-to-market in the Nordics led through a country management network, represented by all relevant businesses

• Centers of Excellence to incubate new technologies, solutions and services

FI SE NO

Tieto’s business and go-to-market structureNetworked ways of working

11

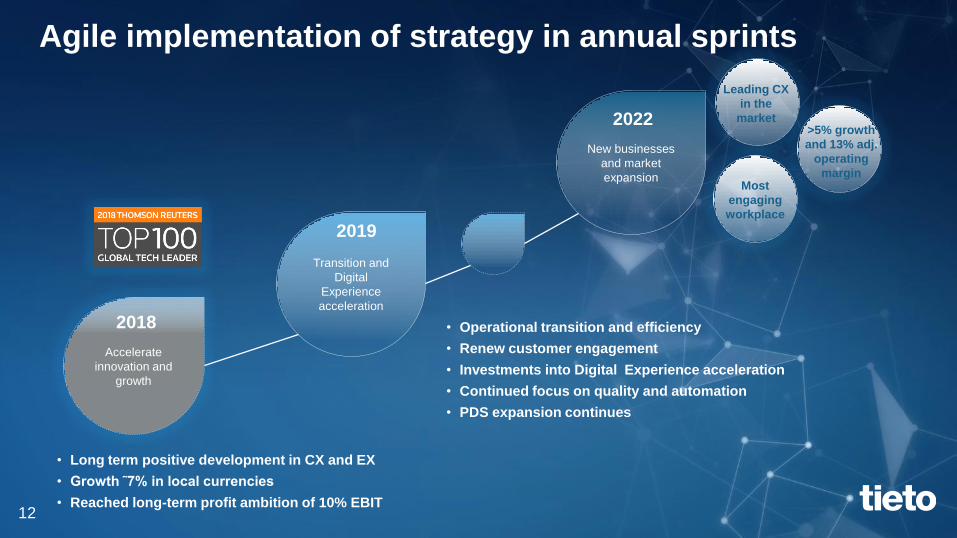

Agile implementation of strategy in annual sprints

• Operational transition and efficiency

• Renew customer engagement

• Investments into Digital Experience acceleration

• Continued focus on quality and automation

• PDS expansion continues

Transition and

Digital

Experience

acceleration

2019

New businesses

and market

expansion

2022

Accelerate

innovation and

growth

Leading CX

in the

market

Most

engaging

workplace

>5% growth

and 13% adj.

operating

margin

2018

• Long term positive development in CX and EX

• Growth ˜7% in local currencies

• Reached long-term profit ambition of 10% EBIT12

Value creation

13

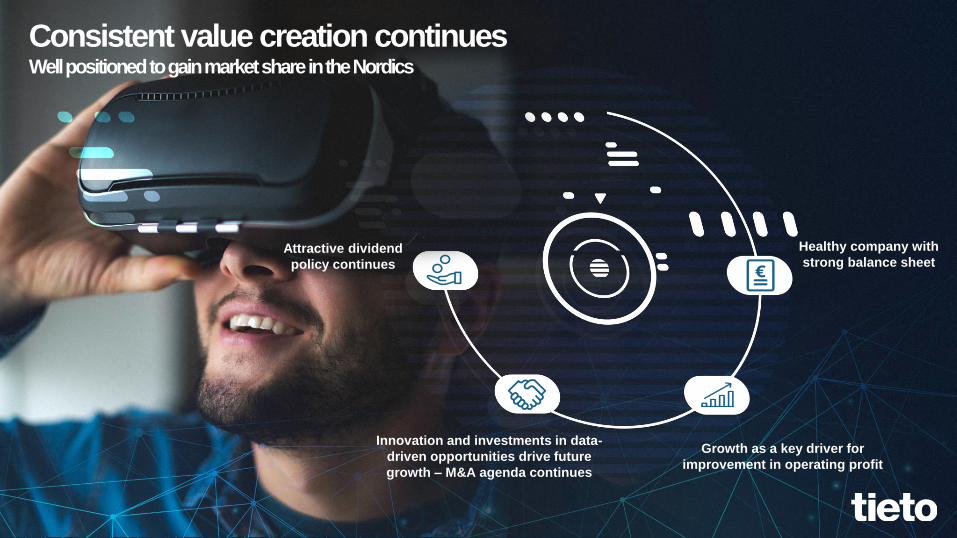

Consistent value creation continuesWell positioned to gain market share in the Nordics

Healthy company with

strong balance sheet

Innovation and investments in data-

driven opportunities drive future

growth – M&A agenda continues

Growth as a key driver for

improvement in operating profit

Attractive dividend

policy continues

Higher growth and profit ambitions while maintaining attractive dividend policy

Ambition 2022

Growth over 5% (CAGR 2019–2022)

Adjusted operating margin (EBIT) 13%1)

1) Adjusted for amortization of acquisition-related intangible assets, restructuring costs, capital

gains/losses, goodwill impairment charges and other items affecting comparability

In accordance with IFRS 16, taking effect on 1 Jan 2019 2) In accordance with IFRS 16, taking effect on 1 Jan 2019 – equals to around 1.5 prior to IFRS 16

Aim is to increase base dividend

annually in absolute terms

Net debt/EBITDA below 2.0

in the long term2)

• Temporarily may exceed 2.0 during the period

• CAPEX expected to remain below 4% of sales

• Strong cash flow driving attractive dividend profile

• Continued active M&A in addition to organic growth

• Main drivers include growth, simplified operations

and automation

15

Profitability

Product Development

Services

Industry

Software

Hybrid Infra

Growth

Digital Experience• Consulting-led market demand

• Active investments into capabilities

• Agile ways of working

Share of sales

... ...

...

.

Performance drivers

..

..

..

.

All businesses contributing to Tieto’s growth and profitability ambition by 2022

• Investments into service experience

• Customer base and partnerships

• Automation activities

• Best-in-class competitive software

• Software functionality and SaaS

• Common practices and knowledge

• Demand for connected products and 5G

• Knowledge in connectivity domain

• Global customer reach and delivery

. ...ContributionLow High

✓ Businesses as the

reportable segments

✓ Updated segment

reporting effective

as of Q2 2019

Businesses

16

Investments focusing on accelerating digital capabilities and

software business expansion

Investment focus

• Accelerate digital capabilities e.g. Design, AI, Public cloud

• Incubate future technologies e.g. Blockchain

• Solution accelerators, data assets and platforms

• Ongoing renewals in Healthcare, Utilities and Payments

• Expand functionality to drive competitiveness

• Selective international expansion and SaaS models

• Infra service experience and multi-cloud orchestration

• Enable PDS customer base expansion

• Skill renewal and learning as a Lifestyle

Investment drivers

Total investment level

to be maintained at

˜5% of revenues

Digital Experience

Industry Software

Other

70-80% of

investments

17

Summary

• Strategy to make customers more competitive focusing on• Digital Experience

• Renewed customer engagement

• Simplified operations

• Digital Experience as the main growth driver, while all businesses expected to grow above market

• Investments to build data-driven services and capabilities - addition of 2500-3000 people during the

strategy period to drive growth

• Operational simplification potentially impacting ˜700 roles globally, resulting in annualized savings

of 30-35M€

• Upgraded financial ambition growth >5%, adjusted operating margin 13%, attractive dividend policy

maintained

• Gradual transition to the new structures during Q2’19

18

Q4, 2018 and

outlook for 2019

19

2018 key figures

Full-year net sales up by 4%› EUR 1 600 (1 543) million› Growth in local currency 7%› Organic growth in local currencies 4%

Full-year EBIT› EBIT EUR 154.7 (139.1) million, 9.7% (9.0%)› Adjusted1) EBIT EUR 162.8 (161.4) million, 10.2%

(10.5%)› Investments in offering development up by

EUR 6 million, of which EUR 3.6 million capitalized

› Currency impact EUR 8 million› Includes EUR 5.2 (4.3) million in amortization

of acquisition-related intangible assets

Dividend proposal› Proposed dividend EUR 1.45 per share

› Base dividend EUR 1.25 (1.20) › Additional dividend EUR 0.20 (0.20)

› Dividend yield 6.1%

3) Base dividend

2) Additional dividend

1,00 1,10 1,15 1,20 1,25

0,30 0,25 0,22 0,20 0,20

0,0

0,5

1,0

1,5

2014 2015 2016 2017 2018

Dividend/share, EUR

3)

2)

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

© Tieto Corporation

2015 2020

Traditional services Emerging services

Two-fold development with strong growth in growth services and

continued decline in infrastructure services

WE AIM TO GROW FASTER THAN THE MARKET*

*IT market growth expectation (CAGR

2015–2020) for the Nordics at 2–3%

SHARE OF IT SERVICES 2018

Growth

businesses**

Other services and

solutions***

Traditional services42%

GROWTH 2018

7%

19%

1%

* Application services growth in local currencies 7%, incl. in traditional services

** Growth solution portfolio described on the next slide

*** Including Avega

41%

17%EMERGING SERVICES

TRADITIONAL SERVICES

© Tieto Corporation

Selected industry solutions

Customer Experience

ManagementData-Driven Businesses Cloud services Security services

Investments supporting continuous renewal and growthUp by 7% in local currencies in 2018

+16% +15% +16%+120%

+3%

Lifecare

Payments

Credit solutions

Case management

Production excellence

SmartUtilities

Hydrocarbon

management

392 384 353 408 393 392 358 411

1 22

2 13 129

11

9,0 9,2

11,612,0

9,08,6

11,311,8

0

2

4

6

8

10

12

14

0

100

200

300

400

500

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

Net of divestment and acquisitions

Customer sales adjusted

Adjusted1) EBIT, %

Q4 2018 key figures

Net sales up by 3%› EUR 421.9 (409.6) million› Growth in local currencies 5%› Organic growth in local currencies 3%

EBIT margin 10.8% (11.7%)› EBIT EUR 45.7 (47.9) million› Adjusted1) EBIT EUR 49.8 (49.2) million,

11.8% (12.0%)› Includes EUR 1.2 (1.2) million in amortization of

acquisition-related intangible assets› EUR 1.9 million of offering development costs

capitalized

Order backlog EUR 1 698 (1 849) million› Negative currency impact› Order backlog provides support for the 2019

growth ambition› Book-to-bill 1.3 (1.3)

MEUR %

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

79,7

-6,110,8

66,6 61,5 12,3 18,7 81,7

-9,3-16,9

-9,1 -11,6 -8,2 -11,4 -8,7 -16,7

-25

-5

15

35

55

75

95

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

Net cash flow from operations and capital expenditure

Net cash from operations Capital expenditure

13822 13754 13851 14329 14581 14956 15109 15190

48,6 49,0 49,6 48,7 49,4 49,8 50,6 50,6

0

10

20

30

40

50

60

0

5000

10000

15000

20000

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

Number of full-time employees and offshore ratio

Number of personnel Offshore ratio

Quarterly development

Number of personnel up by a net amount of 861

Offshore ratio: IT services 48.2% (46.2%) PDS 71.5% (69.8%)

%

MEUR

Employees

MEUR

392 384 353 408 393 392 358 411

1 2 22 13 12 9

11

0100200300400500

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

Net sales

Net of divestment and acquisitionsCustomer sales adjusted

0,2

0,90,8 0,8

0,5

1,0 1,0

0,7

0

0,5

1

1,5

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

Net debt/EBITDA

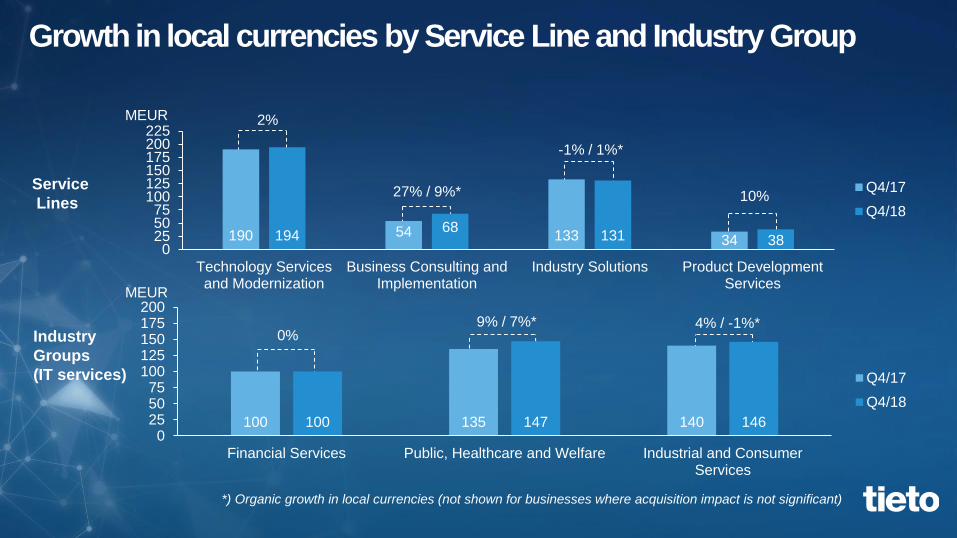

Growth in local currencies by Service Line and Industry Group

4% / -1%* 9% / 7%*0%

10%

-1% / 1%*

27% / 9%*

2%

Service

Lines

Industry

Groups

(IT services)

*) Organic growth in local currencies (not shown for businesses where acquisition impact is not significant)

MEUR

MEUR

100 135 140100 147 1460

255075

100125150175200

Financial Services Public, Healthcare and Welfare Industrial and ConsumerServices

Q4/17

Q4/18

190 54 133 3419468

131 380

255075

100125150175200225

Technology Servicesand Modernization

Business Consulting andImplementation

Industry Solutions Product DevelopmentServices

Q4/17

Q4/18

Service Lines

Technology Services and Modernization

Industry Solutions

Industrial and

Consumer ServicesPublic, Healthcare

and WelfareFinancial Services

Product Development Services

New

data-driven

businesses *)

*) Reported in Industry Solutions

Business Consulting and Implementation

Support Functions

Technology Services and Modernization

189 186 172 190 189 187 173 190

1110,4

11,7

13,512,8

11,012,3

13,813,0

0

2

4

6

8

10

12

14

16

0

50

100

150

200

250

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

%MEUR

Net of divestment and acquisitions

Customer sales adjusted

Adjusted1) EBIT, %

Customer sales in Q4› EUR 190 (190) million, growth at Q4 2017 level, or

+2% in local currencies

EBIT› Adjusted1) EBIT EUR 24.8 (24.3) million, 13.0%

(12.8)

Q4 highlights› Growth (in local currencies) driven by infrastructure

cloud and application services – up by 15% and 7% in full year, respectively

› Decline in traditional infrastructure services continued, down by 3% in full year

› Operating margin somewhat improved, mainly owing to good Application Services development

› Q1 adjusted operating margin is anticipated to be below Q1/2018 level, which was supported by the efficiency programme

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

Business Consulting and Implementation

Customer sales Q4› EUR 67 (54) million, +24%, or +27% in local currencies› Organic growth in local currencies +9%

EBIT› Adjusted1) EBIT EUR 5.5 (4.3) million, 8.2% (8.1)

Q4 highlights› Growth supported by the acquisition of Avega and

Meridium› Organic growth driven by CEM› Adjusted operating profit improved, mainly due to good

volume development and the acquisitions› Q1 adjusted operating margin is anticipated to be at or

above Q1/2018 level

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

51 49 42 54 49 52 44 57

13 12

8

99,2

7,78,2 8,1

8,79,8

2,8

8,2

0

2

4

6

8

10

12

0

10

20

30

40

50

60

70

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

%MEUR

Net of divestment and acquisitions

Customer sales adjusted

Adjusted1) EBIT, %

Industry Solutions

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

Customer sales Q4› EUR 129 (133) million, -3%, or -1% in local

currencies› Organic growth in local currencies 1%

EBIT› Adjusted1) EBIT EUR 20.4 (20.8) million, 15.8%

(15.7)

Q4 highlights› Strong growth in Hydrocarbon Management and

Payments solutions› Architectural renewal continued to affect

SmartUtilities› Lifecare growth somewhat affected by the reform in

the Finnish healthcare segment and the solution renewal

› Technology renewal continues in selected solutions

› Offering development costs up by EUR 3 million as planned

› EUR 1.9 million related to platform development capitalized

› Q1 adjusted operating margin expected to be close to Q1/2018 level

121 118 110 131 121 119 110 129

1 22

2

8,19,4

14,115,7

7,5

4,9

14,315,8

0

2

4

6

8

10

12

14

16

18

0

50

100

150

Q1/17Q2/17Q3/17Q4/17Q1/18Q2/18Q3/18Q4/18

%MEUR

Net of divestment and acquisitions

Customer sales adjusted

Adjusted1) EBIT, %

Product Development Services

Customer sales Q4› EUR 36 (34) million, +6%, or +10% in local

currencies

EBIT› Adjusted1) EBIT EUR 3.7 (3.5) million, 10.1%

(10.1)

Q4 highlights› Strong volume development with the largest key

customers and good development in automotive› EBIT margin remained at a healthy level while

improvement somewhat curbed by negative currency effects

› Q1 adjusted operating margin is anticipated to be below Q1/2018 level

32 31 29 34 34 34 32 36

13,4

8,07,2

10,1

12,7

8,79,9 10,1

0

2

4

6

8

10

12

14

16

0

5

10

15

20

25

30

35

40

Q1/17Q2/17Q3/17Q4/17Q1/18Q2/18Q3/18Q4/18

%MEUR

Net of divestment and acquisitions

Customer sales adjusted

Adjusted1) EBIT, %

1) adjusted for restructuring costs, capital gains/losses,

goodwill impairment charges and other items

Industry Groups

Business Consulting

& Implementation

Technology Services and Modernization

Industry Solutions

Product Development Services

New

data-driven

businesses *)

Public, Healthcare

and WelfareFinancial Services

Industrial and

Consumer Services

*) Reported in Industry Solutions

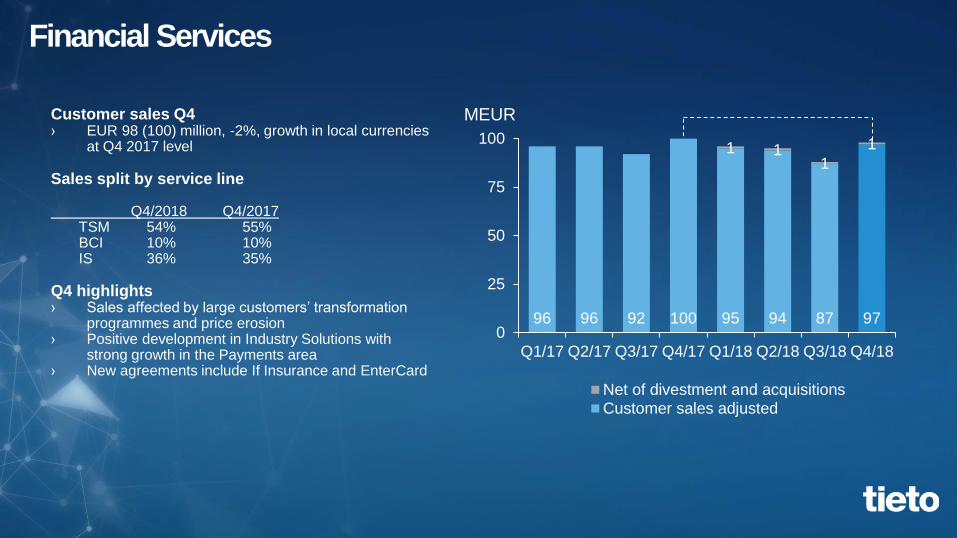

Financial Services

Customer sales Q4› EUR 98 (100) million, -2%, growth in local currencies

at Q4 2017 level

Sales split by service line

Q4/2018 Q4/2017TSM 54% 55%BCI 10% 10%IS 36% 35%

Q4 highlights› Sales affected by large customers’ transformation

programmes and price erosion› Positive development in Industry Solutions with

strong growth in the Payments area› New agreements include If Insurance and EnterCard

96 96 92 100 95 94 87 97

1 11

1

0

25

50

75

100

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

MEUR

Net of divestment and acquisitions

Customer sales adjusted

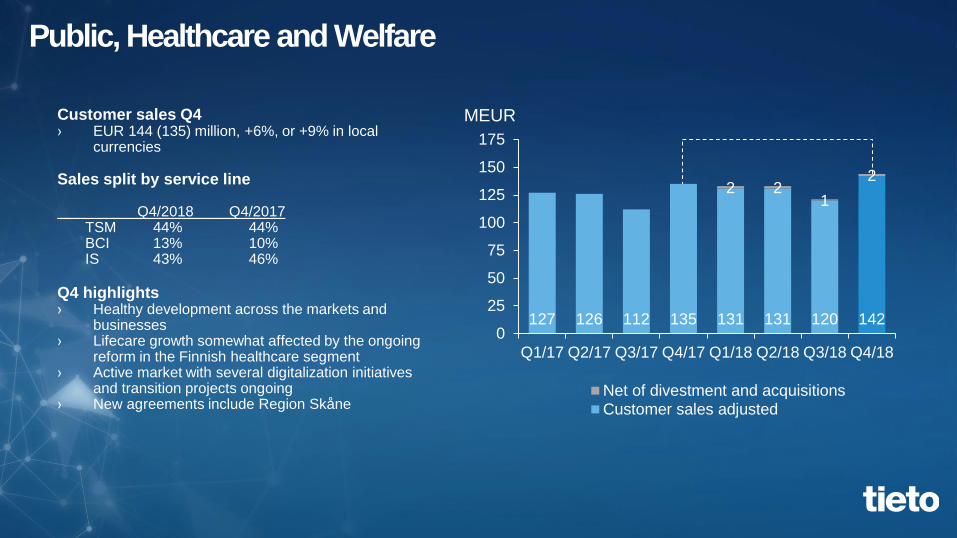

Public, Healthcare and Welfare

Customer sales Q4› EUR 144 (135) million, +6%, or +9% in local

currencies

Sales split by service line

Q4/2018 Q4/2017TSM 44% 44%BCI 13% 10%IS 43% 46%

Q4 highlights› Healthy development across the markets and

businesses› Lifecare growth somewhat affected by the ongoing

reform in the Finnish healthcare segment› Active market with several digitalization initiatives

and transition projects ongoing › New agreements include Region Skåne

127 126 112 135 131 131 120 142

2 21

2

0

25

50

75

100

125

150

175

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

MEUR

Net of divestment and acquisitionsCustomer sales adjusted

Industrial and Consumer Services

Customer sales Q4› EUR 144 (140) million, +3%, or +4% in local

currencies› Organic growth in local currencies -1%

Sales split by service line

Q4/2018 Q4/2017TSM 52% 54%BCI 26% 21%IS 22% 25%

Q4 highlights› Growth supported by the acquisition of Avega› Healthy growth especially in Hydrocarbon

Management whereas sales development in SmartUtilities negative due to the ongoing large-scale renewal

› New agreements include SSAB and Volvo Car Dealers

137 130 121 139 133 133 119 136

11

1

1 10 97

8

0

25

50

75

100

125

150

175

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

MEUR

Net of divestment and acquisitionsCustomer sales adjusted

Performance drivers in 2019

› Growth above the market

› Offering development costs around 5% of Group sales

› Efficiency and productivity improvement measures,

incl. automation, optimized subcontracting, offshoring,

management of competence pyramid

› Salary inflation over EUR 30 million

› New strategy to enhance competitiveness launched

› Operational simplification anticipated to affect

around 700 roles globally

› Annualized gross savings of EUR 30–35 million,

partially affecting performance in 2019

© Tieto Corporation

Guidance for 2019

› Tieto expects its full-year adjusted1)

operating profit (EBIT) to increase

from the previous year’s level

(EUR 168.0 million2) in 2018)

1) adjusted for amortization of acquisition-related intangible

assets, restructuring costs, capital gains/losses, goodwill

impairment charges and other items affecting comparability

2) not restated for IFRS 16

Appendix

© Tieto Corporation

Key customersTop 10 customers account for 29% of sales

Financial Services Public, Healthcare and Welfare Industrial and Consumer Services

Tieto has around 900 customers across industry groups. According to the terms and

conditions of the customer agreements, Tieto is able to introduce only part of them.

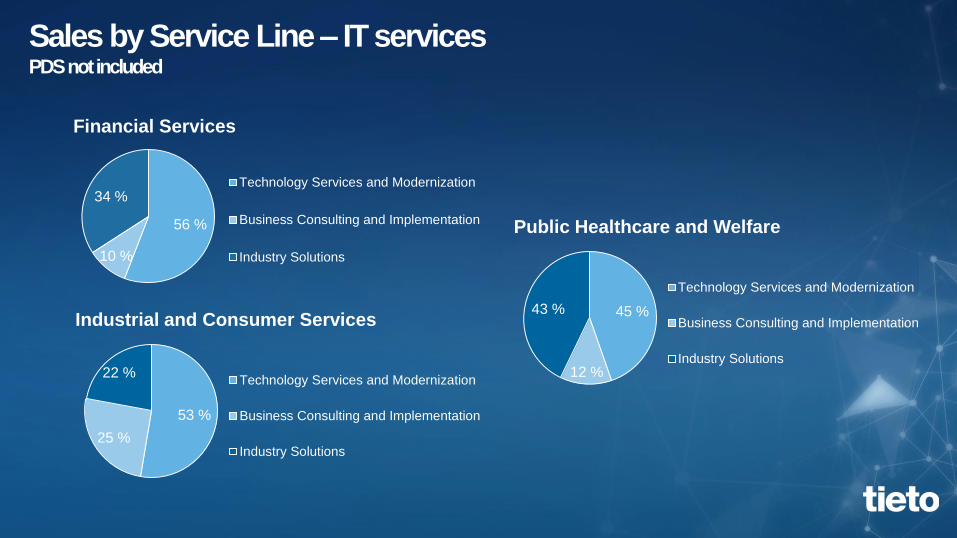

Sales by Service Line – IT services PDS not included

56 %

10 %

34 %

Financial Services

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

45 %

12 %

43 %

Public Healthcare and Welfare

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

53 %

25 %

22 %

Industrial and Consumer Services

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

Sales by Industry Group – IT servicesPDS not included

29 %

32 %

39 %

Technology Services and Modernization

Financial Services

Public, Healthcare & Welfare

Industrial and Consumer Services

27 %

47 %

26 %

Industry Solutions

Financial Services

Public, Healthcare & Welfare

Industrial and Consumer Services

16 %

27 %57 %

Business Consulting and Implementation

Financial Services

Public, Healthcare & Welfare

Industrial and Consumer Services

Sales by Service Line

46 %

15 %

30 %

9 %Tieto

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

Product Development Services39 %

17 %

28 %

16 %

Sweden

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

Product Development Services

67 %

15 %

17 %1 %

Finland

Technology Services and Modernization

Business Consulting and Implementation

Industry Solutions

Product Development Services

Sales by Industry Group

24 %

33 %

35 %

8 %Tieto

Financial Services

Public Healthcare and Welfare

Industrial and Consumer Services

Product Development Services

25 %

35 %

39 %

1 %Finland

Financial Services

Public Healthcare and Welfare

Industrial and Consumer Services

Product Development Services

22 %

36 %

26 %

16 %

Sweden

Financial Services

Public Healthcare and Welfare

Industrial and Consumer Services

Product Development Services

All information in this material is for informational purposes only.

The opinions and viewpoints regarding, inter alia, the future of the

company and markets are of Tieto and may not actually materialize.

This information should not be construed as an investment recommendation or

investment advice. All information expressed herein is subject to change without

notice. Neither Tieto nor its officers nor employees shall have any liability for any loss

sustained by anyone who has relied on the information provided.