Embed Size (px)

Citation preview

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed|Must Read Apr. 7, 2016 9:04 AM ET10 comments

by: Lester Goh

Summary• Shares of CPI Aerostructures have sold off following the government's

announcement of the early retirement of the military's A-10 attack jet program in 2014.

• This led to the Company incurring a ~$47m charge to earnings in 2014, highlighted the fragility of business model, and depressed gross margins by a significant amount.

• However, it appears that a positive black swan is going unnoticed – the Pentagon recently announced that the A-10 retirement will be pushed back to 2022.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 1 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

• While there are opportunities for the Company to win contracts, especially in commercial aerospace, further A-10 work is higher-probability bet. Lenders seem to share this sentiment.

• Assuming zero multiple expansion/A-10 contract wins, shares see ~80% upside. The Company is the natural winner for future A-10 orders. An announcement to that effect would be incremental upside.

ThesisContract manufacturing is a mediocre business model at best. When things go well, returns are acceptable but not great. When things hit the fan, all hell breaks loose. The latter situation exemplifies what CPI Aerostructures (NYSEMKT:CVU) ("CPI", "CVU", or the "Company") has gone through in 2014.

Reasons for the opportunity: anticipated loss of a major contract, optically bad financials, limited Street coverage, limited daily liquidity

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 2 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

Shares of CVU sold off sharply from $15 to ~$8 when a proposal for early retirement of the A-10 attack jet program surfaced in 2014. This not only highlighted the fragility of the business model, but depressed gross margins by a significant amount in subsequent quarters and led to a ~$47m charge in 2014. The sharp sell-off was likely a function of limited daily liquidity. The market also seems to be giving CVU no credit for the dramatic improvement in cost structure, instead apparently choosing to focus on the effects of the early retirement of the A-10 program.However, good news is likely on the horizon for CPI - rendering the previously-warranted sell-off unwarranted. Although the Company likely has numerous contract opportunities in commercial aerospace, military contract wins - especially the A-10 program- are likely more probable. Lenders seem to share the same sentiment.In my view, the Company shares could be worth significantly greater than what they are worth right now when the reversal of the 2014 situation flows through the financials. Using the Company's A-10 estimates prior to the cancellation and historical net income margins suggest that CVU is trading at ~7x 2016 earnings assuming zero new A-10 business wins. Assuming that CVU trades to its trailing p/e multiple of ~13x - i.e. no multiple expansion, shares see ~80% upside from current levels.Given that these wins have not surfaced on the Company's books, this makes extremely likely that the market is missing this near-term catalyst. Recent share price action certainly suggest that the aforementioned positive black swan is going unnoticed.Background to the A-10 attack jet program, proposed retirement, and impact on financialsIn 2008, the Company won a contract to produce assemblies for wings of the A-10 attack jet. It received orders for 173 wings and no further orders. In early 2014, a proposal to retire the A-10 attack jet had surfaced.The A-10 attack jet program was one of the Company's largest programs. Eventually, management concluded that the A-10 program would not continue to its full capacity and projected that the program would be terminated sometime during 2015.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 3 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

This anticipated termination led to the Company taking a charge of ~$47m in 2Q '14, of which ~$45m was allocated to a negative adjustment in revenue, and ~$3m was an adjustment to cost of sales. This had a huge impact on financials, resulting in negative margins for 1H '14. Given the large-scale nature of the A-10 program (total Company revenues were only ~$100m), shares unsurprisingly sold off sharply from $15 to around the current price of $8.This eventually resulted in a CEO change. The new CEO embarked on programs to improve margins through reducing costs and improving productivity. These initiatives drastically improved the Company's cost structure largely through reducing factory overhead - factory overhead rates has been reduced by over 5,000bp (i.e. halving overhead) since 2014.This massive reduction in overhead is sustainable given that it was achieved through investing in automation, affording the company a lower fixed cost structure. Workforce reductions also helped - G&A has been reduced by 50bps since 2014. Opex leverage appears to be kicking in, as evident by incremental revenues requiring less per-dollar opex.The market appears to be giving zero credit to these improvements, instead choosing to focus myopically on the effects of the A-10 situation. This is unsurprising given that the margin improvement is somewhat disguised with the Company booking A-10 revenues at zero gross margin. Management appears focused to continue these improvements, as seen below.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 4 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

Source: February Investor PresentationAs the Company chose to record A-10 revenue at zero gross margins, the metric has been artificially depressed by a significant amount. 1H '15 gross margins were ~18%. Excluding the impact of the A-10 program, these margins were ~23% instead, a 500bps difference.Notably, these ~23% gross margins were a significant y/y improvement from 1H '14 (also excluding the A-10 impact) where the metric was ~20%, good for a 300bps improvement. This margin improvement was driven by higher production rates on certain commercial programs and should continue as these programs continue to ramp.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 5 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

This also invalidates one major leg of the bear thesis, which suggested that the Company's leading win-rate of ~13% vs industry peers at ~5% was due to CVU undercutting on price for the sake of revenue growth. If one does not adjust for the booking of A-10 orders at zero gross margins, he would quite severely understate the Company's profitability.Moreover, given the amount of costs that has been cut since the new CEO came on board, it seems quite clear that the problem was cost-related, not sales-related. If one simply looks at the Company's margins before the cost cuts occurred, and also saw that sales were growing fast, he may erroneously conclude that CVU was bidding aggressively on unprofitable contracts. As discussed, this is not the case. Per 2015 results, the Company's ~8% net income margins (understated as it does not adjust for the A-10 zero gross margin situation) are not out of the norm, given the relatively commoditized nature of its operations.Positive Black Swan Going UnnoticedLady Luck appears to have been smiling on CVU recently. A black swan-like situation occurred in early February - the Pentagon announced that it would delay the retirement of the A-10 until 2022. According to the report, it appears that the primary reason for this delay is due to the emergence of ISIS. Given the appearance of a valid threat against US, this delay is unlikely to be reversed, in my view. Terrorism appears to be on the rise as well, if the recent attacks are any indication.The press report also mentions that the A-10 is instrumental in missions involving Islamic State militants, increased Russian aggression, and in taming North Korea. None of these are going to be eliminated in the near- or medium-term, which reinforces my belief that a subsequent withdrawal of A-10 funding is unlikely in future annual budgets.Martha McSally, a former A-10 pilot, also mentioned that "no other plane can perform the tasks for which the A-10 is uniquely suited", further supporting my assertion. Notably, shares of CVU continue to trade at ~$8, suggesting that the positive black swan event is going unnoticed.Interestingly, CVU did not issue any press release related to this matter. In my view, the Company is likely keeping the matter under wraps until a deal is finalized. Management lost credibility with investors due to the A-10 situation in '14/'15 and

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 6 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

thus new management is unlikely in a hurry to make the same mistake; they would likely only issue a press release when they are absolutely sure about things. Given the lack of a press release from the Company itself, it appears that the market is unaware of this new development - recent price action certainly supports this theory.Note: The stock sold off in March due to an inability to file a timely 10-K, but this situation has been rectified - the 10-K has been filed.So what impact does this have on CVU? Essentially, it is very likely that CVU can continue supplying wing replacements for the A-10 and actual orders can be booked at appropriate gross margins. Recall that they received orders for 173 wings - the Company continues to fulfil these orders, but at zero gross margins. While actual numbers are hard to come by, management's estimates are a helpful starting point.As a contract manufacturer, CVU uses percent-of-completion accounting as its contracts tend to be multi-year and require upfront working capital investment. Revenue is only recognized when two things are present - 1) costs are incurred and 2) contracts are funded (i.e. annual govt budget allocates funding for a contract, thus assuring collection). Essentially, if CVU incurs 20% of the cost of a contract in a quarter and the contract is funded, 20% of the revenue will be recognized in that quarter. Revenue and costs are management's best estimates.Typically, estimates will be need to be re-visited every reporting period (in this case, every quarter) to see if adjustments are needed. Adjustments are needed when estimates were too pessimistic or when contracts are cancelled/have the potential to be cancelled due to the withdrawal of funding, and vice versa.In the prior section, I mentioned that management took a ~$45m negative adjustment to revenue as a result of the anticipated termination of the A-10 program. When adjustments are required for the revenue of a contract, these adjustments are made with an inception-to-date effect in the current period. Thus, when the budget request called for a withdrawal of funding for the A-10, this essentially means that no further revenue for CVU as the contract is no longer funded - i.e. the second criteria discussed earlier is unfulfilled. As a result, CVU reduced its revenue estimates for this contract, resulting in negative revenue in 2Q '14 - the period during which the estimates were made.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 7 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

The recent Pentagon announcement would require a re-estimation of revenues by the Company. Put simply, the Pentagon announcement calls for funding for CVU's A-10 contracts, and hence the Company will be able to recognize their revenue - recall that revenue is recognized when two things are present, costs incurred and funding. Costs have been (and continue to be) incurred as CVU is still fulfilling the contract, and the Pentagon announcement fulfils the second criteria - funding.The Company would likely re-visit their estimates within the current fiscal year and adjust for the ~$45m in revenue that is now funded. My expectation regarding the timing of this reversal is supported by the fact that the 2014 announcement which called for no further funding for the A-10 occurred in March 2014 and the Company adjusted its estimates (i.e. reversed previously-recognized revenue) as soon as practicable - 2Q '14.If we assume that CVU would be able to make ~7% net margins (slightly lower than historicals, and also understated as it is unadjusted for the A-10 zero gross margin situation) on this revenue, this adds ~$3.2m in incremental net income for 2016.Moreover, CVU is likely to be the natural winner of further A-10 orders. As discussed, CVU received only 173 wing orders. Given the Company's prior experience with the program, it appears very likely that the remaining orders would be allocated to CVU, which would add substantially to revenues and earnings. After all, it does not make any economic sense for the USAF to sub-contract the orders to others, as other contractors do not have the prior manufacturing experience with the A-10 and would likely experience delays.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 8 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

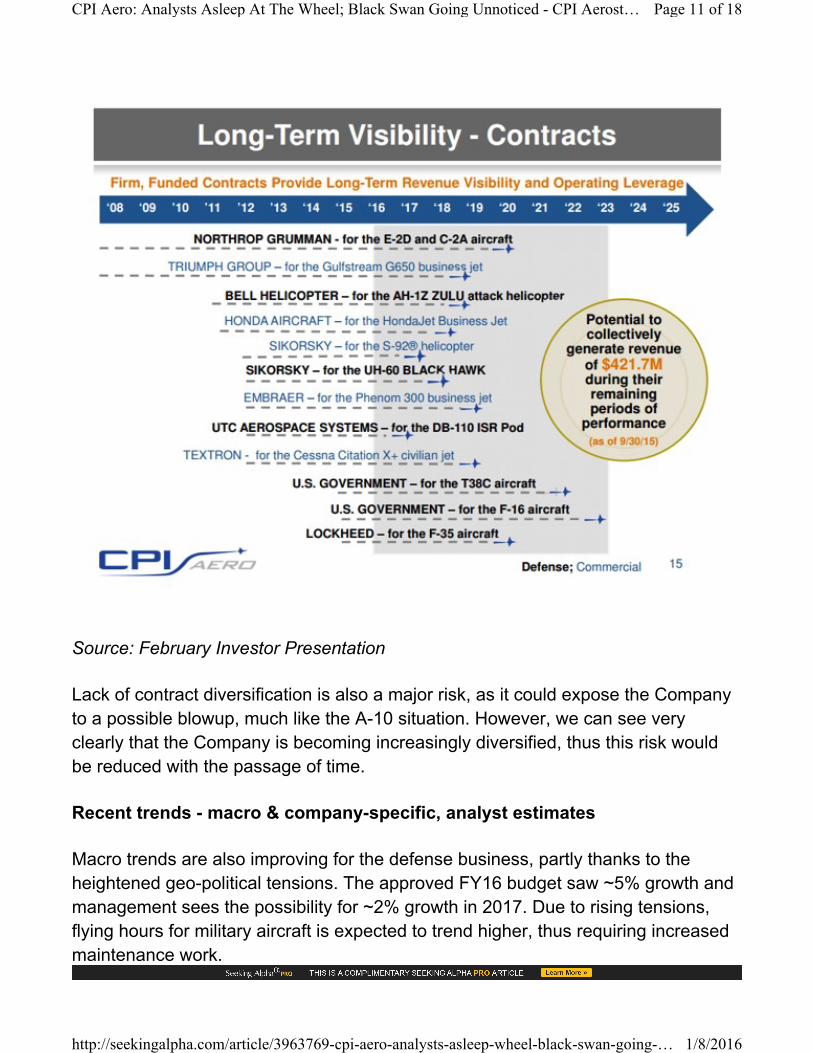

Source: February Investor PresentationThe above slide by management essentially confirms my thesis. Note that although the slides were released a day after the Pentagon announcement, they do not discuss said announcement, suggesting that the slides may have been prepared at a much earlier date. In my view, potential longs might have seen the investor presentation and concluded that there was significant near-term uncertainty associated with the A-10 program, unaware that this uncertainty has already been lifted.Lenders to the Company appear to share my bullish sentiment. On March 24, CVU entered into a refinancing and paid off its $4.5m term loan and ~$24m existing revolving credit facility using part of the proceeds. The new lender, Bank United, provided the Company with a $10m term loan (up from $4.5m) and a $30m

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerostr… Page 9 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

revolving credit facility (down from $35m). Additionally, the rates of the Company's credit facilities appear to have lowered. Under the previous lenders - CVU was paying 1m LIBOR + 3%, now CVU will pay a 2%-2.75% spread over LIBOR.In my view, this refinancing is essentially a vote of confidence for the Company by its lenders. After all, lenders are unlikely to finance a company - especially one as small as CVU - if they are not convinced that their money would be safe and that the Company has decent prospects.In addition, the new credit facilities provides the Company with an incremental ~$11m in liquidity, which supports the near-term possibility of a major contract win - companies/the USAF wants to ensure that contractors have ample liquidity to carry out orders, and this increase in liquidity for CVU could presage a major win. Stated simply, the new credit facilities is likely geared to showing customers that the Company can support a higher level of business activity. There is simply no other significant reason (aside from a slight decrease in interest rates) for this.Diversifying away from military and reducing single-contract relianceThe proposed retirement of the A-10 program also appears to have given management a fright. Management is now looking for new opportunities on the commercial aerospace side, presumably due to the relatively lower volatility in contract cancellations - OEMs such as Boeing and Airbus are not subject to government budget revisions after all.Moreover, commercial aerospace seems set to grow for many years given record OEM backlogs at Boeing/Airbus, low oil prices aiding airline profitability and financing fleet growth, and high passenger load factors indicating strong consumer demand and incentivizing airlines to continue buying new aircraft.Stated simply, commercial aerospace is a better place to be as compared to the military space, something that CVU's management appear to have woken up to. While this diversification would no doubt take a while - current backlog is ~70% defense and ~30% commercial - it is encouraging that management at least is taking the step in the right direction.The Company has also focused on diversifying its contract base to reduce single-contract exposure and prevent another situation similar to the A-10, as seen below.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 10 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

Source: February Investor PresentationLack of contract diversification is also a major risk, as it could expose the Company to a possible blowup, much like the A-10 situation. However, we can see very clearly that the Company is becoming increasingly diversified, thus this risk would be reduced with the passage of time.Recent trends - macro & company-specific, analyst estimatesMacro trends are also improving for the defense business, partly thanks to the heightened geo-political tensions. The approved FY16 budget saw ~5% growth and management sees the possibility for ~2% growth in 2017. Due to rising tensions, flying hours for military aircraft is expected to trend higher, thus requiring increased maintenance work.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 11 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

Recent contracts wins such as the T-38C ($49m contract from 2015-2021), F-35A ($10.6m contract from 2015-2021), and E-2D ($25m-$30m contract from 2016-2019) are also in the process of ramping up, suggesting that margins could continue to expand going forward as production increases. These recent wins also reinforces my belief that the macro picture is improving.Analysts also appear to be asleep at the wheel, according to estimates compiled by Yahoo. They are looking for ~$100m in revenue for 2016 and ~$6.6m in net income, which does account for the recent contract wins but neither accounts for the reversal of the A-10 situation, nor any incremental A-10 orders. This lack of attention to detail is not surprising given that CVU is a fairly small company - the sell-side tends to focus on more on larger companies due to the potential for much higher fees.Valuation; zero multiple expansion suggests ~85% upsideCVU currently trades at ~13x earnings. For 2016, I am merely modeling the positive effect of the reversal in the A-10 program and excluding the effects of any other new A-10 business wins - which appear very likely. Management sees potential for another 120 A-10 orders, compared to the current 173.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 12 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 13 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 14 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 15 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

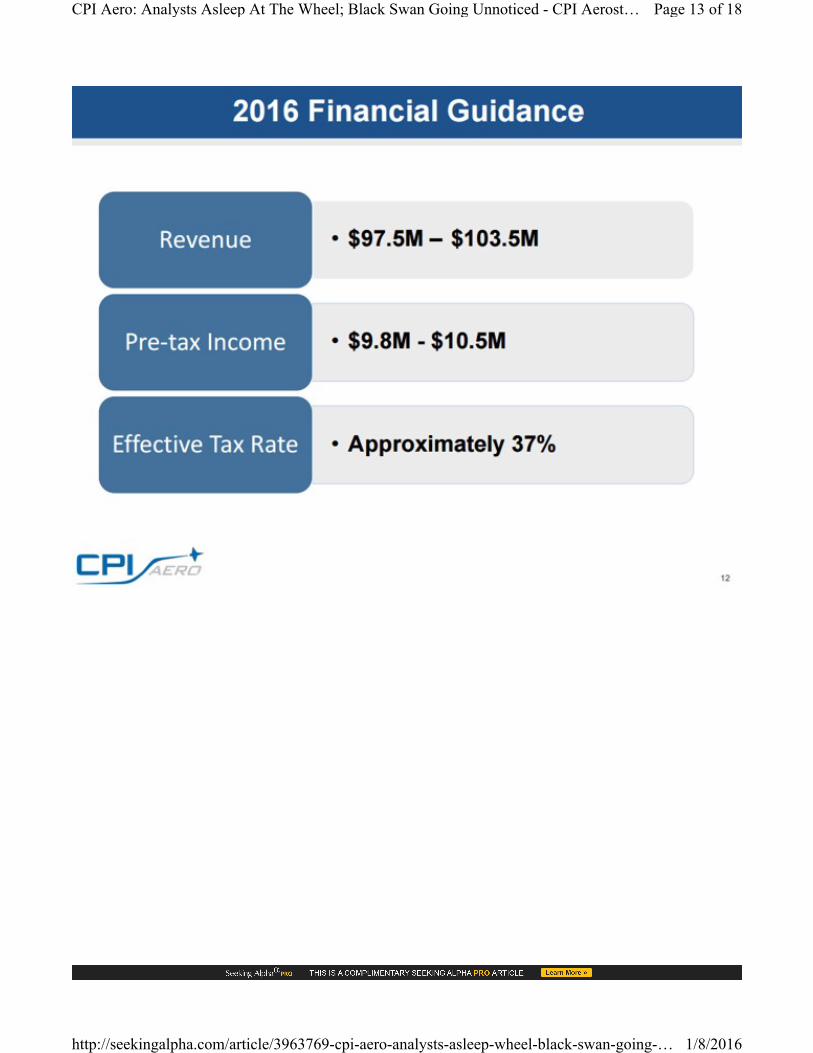

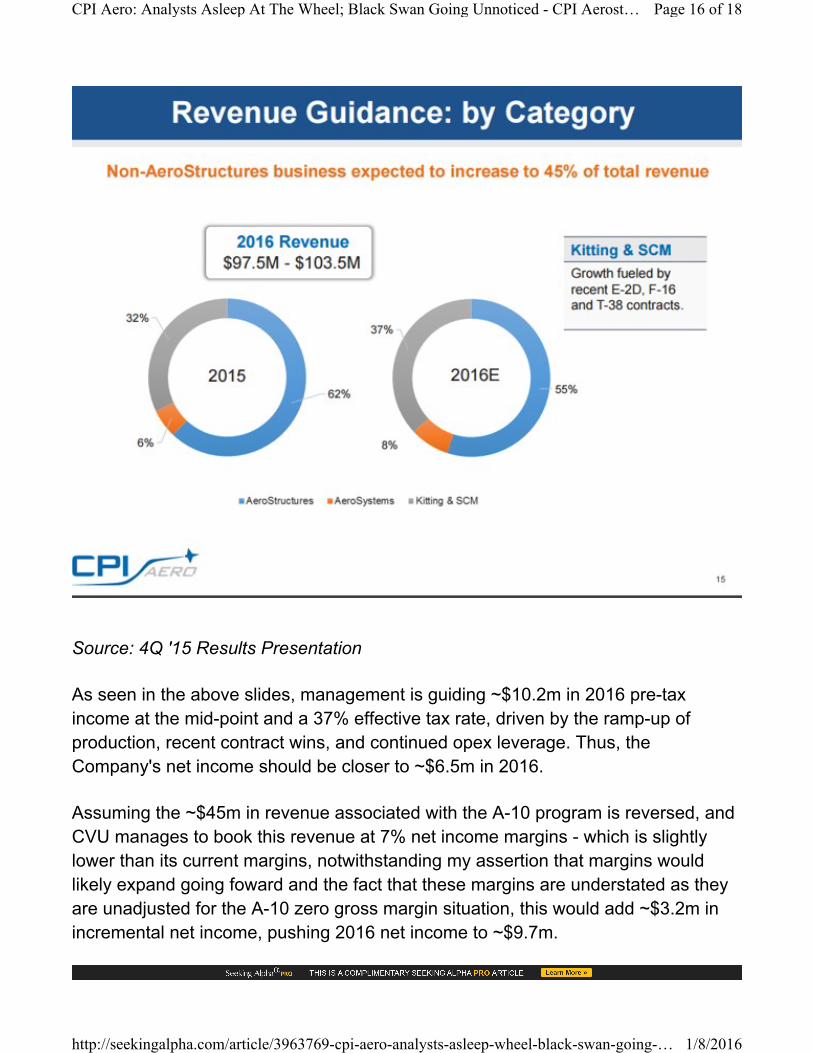

Source: 4Q '15 Results PresentationAs seen in the above slides, management is guiding ~$10.2m in 2016 pre-tax income at the mid-point and a 37% effective tax rate, driven by the ramp-up of production, recent contract wins, and continued opex leverage. Thus, the Company's net income should be closer to ~$6.5m in 2016.Assuming the ~$45m in revenue associated with the A-10 program is reversed, and CVU manages to book this revenue at 7% net income margins - which is slightly lower than its current margins, notwithstanding my assertion that margins would likely expand going foward and the fact that these margins are understated as they are unadjusted for the A-10 zero gross margin situation, this would add ~$3.2m in incremental net income, pushing 2016 net income to ~$9.7m.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 16 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

If we assume zero multiple expansion - i.e. CVU continues trading at 13x earnings, shares should be worth ~$126m, implying ~80% upside from current levels.Catalysts

• Reversal of the A-10 program• Additional orders on the remaining 120 A-10s - As the Company recorded a

~$45m negative adjustment to revenue for 173 wing orders, which comprised of ~41% of A-10 contract revenue per the 10-K, an additional 120 A-10 orders would amount to a ~$76m contract, by my rough math.

• Gross margin expansion as the Company proceeds to book A-10 gross margins at appropriate amounts.

Risks

• Adverse budget revision - Mitigant: Given the emergence of ISIS and recently elevated levels of terrorist attacks, any budget revision seems likely to be skewed to the upside and would probably be in CVU's favor.

ConclusionShares of CVU are compelling due to 1) an undemanding valuation at ~7x my estimate of 2016 net income; 2) a sell-off in shares that was previously warranted but is now unjustifiable; and 3) the presence of a major catalyst just around the corner. Simply assuming zero multiple expansion, shares see ~80% upside from current levels - possibly more if additional A-10 orders come in, substantially boosting the Company's growth trajectory.Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 17 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

Additional disclosure: The author's reports contain factual statements and opinions. He derives factual statements from sources which he believes are accurate, but neither they nor the author represent that the facts presented are accurate or complete. Opinions are those of the the author and are subject to change without notice. His reports are for informational purposes only and do not offer securities or solicit the offer of securities of any company. Mr. Goh ("Lester") accepts no liability whatsoever for any direct or consequential loss or damage arising from any use of his reports or their content. Lester advises readers to conduct their own due diligence before investing in any companies covered by him. He does not know of each individual's investment objectives, risk appetite, and time horizon. His reports do not constitute as investment advice and are meant for general public consumption. Past performance is not indicative of future performance.Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

CPI Aero: Analysts Asleep At The Wheel; Black Swan Going Unnoticed - CPI Aerost… Page 18 of 18

http://seekingalpha.com/article/3963769-cpi-aero-analysts-asleep-wheel-black-swan-going-… 1/8/2016

![An Unnoticed Struggle - Japanese American Citizens … Unnoticed Struggle: A Concise History of Asian American Civil Rights Issues CHINESE EXCLUSION “ [The Chinese are] swarming](https://img.dokumen.tips/doc/110x75/5b07a9957f8b9ad1768e7ca0/an-unnoticed-struggle-japanese-american-citizens-unnoticed-struggle-a-concise.jpg)

![PRESS RELEASE 07 Janek Schaefer Asleep at the wheel Web pix/Asleep Press Release.pdfMDTS 07 PRESS RELEASE “Asleep at the wheel…” [#audiOh!34] is a free to download ‘Audiofile](https://img.dokumen.tips/doc/110x75/5ccdb00688c993ca688c3956/press-release-07-janek-schaefer-asleep-at-the-wheel-web-pixasleep-press-releasepdfmdts.jpg)