ACCOUNTING CYCLES

REVENUE CYCLE

NOTE FROM TIM: This document I found on the web seems to have

some relevant CPA Exam Questions that are worth studying. I.

REVENUE CYCLE. As you will recall, the revenue cycle involves

accounting transactions resulting from economic events that produce

revenue for the accounting entity. The major events occurring in

the revenue cycle are: receiving and ordering from a customer,

delivering goods or services to the customer, requesting payment

from the customer, and receiving the payment. Understanding a cycle

involves familiarity with the documentation of the cycle.

Flowcharts, internal control questionnaires and narratives are

common methods of documentation. Fill in the flowcharts for revenue

(credit sales and cash sales and receipts).

Identify appropriate internal control procedures for the revenue

cycle using DAASI. (Reconciliation to ARCCS: D (Recorded) A

(Custody) A (Authorized) S (Seg of Duties) I (Comparison).)

D=

Prenumbered (and accounted for), multiple-copy SO, SD, SI

used

One copy of the SO, SD, SI filed in the department generated

Remittance advices used to post from

A/R subsidiary ledger, sales journals, cash receipts journal

Prenumbered cash receipt tickets, credit memos & bad debt

write-off forms

Aging prepared monthly

Prepare a prelisting of cash receipts

A=

Individuals with access to cash or goods should be bonded

Use of a lockbox

Cash deposited intact daily

Checks restrictively endorsed

Control over write-offs and collection of write-offs

Cash registers --internal tapes, locked drawers, correct change,

bell, window to

customer, assigned drawers, preprogrammed prices, drawers

reconciled

A=

Credit approved prior to shipment of goods

Monthly statements reviewed by supervisor before sent out

Appropriate credit policy

Approved sales price list with deviations authorized

Authorization of A/R write-offs

S=

Segregate the sales order function from the A) credit function

from the B) shipping

function from the C) billing function from the D) cash receipts

function

Segregate cash receipts from accounts receivable record

keeping

Segregate cash receipts from the credit function

Segregate accounts receivable subsidiary ledger from the general

ledger

I=

A/R general ledger reconciled to subsidiary ledger

Rotate duties between G/L and A/R subsidiary ledger (S/L)

clerks

Sendout monthly statements to customers

Compare SO, SD, & SI to ensure ordered goods were

shipped/shipped goods billed

Compare duplicate deposit slip with a) cash receipts journal,

and b) A/R sub ledger

Daily reconciliation of cash collections

Match credit memoranda and receiving report

II. Internal controls frequently missing in the revenue

cycle.

II. Credit granted by the credit department

II. Sales orders and invoices prenumbered and controlled

II. Sales return credit memoranda prenumbered and matched with

receiving reports

II. Subsidiary ledger reconciled to control ledger regularly

II. Individual who does not post accounts receivables reviews

monthly statements before sending to customer

II. Monthly statements sent to all customers

II. Write-offs approved by mgmt official independent of

recordkeeping responsibility

II. Cash receipts received in mail listed by individual(s) with

no recordkeeping responsibility; cash goes directly to cashier

II. Over-the-counter cash receipts controlled (cash register

tapes)

II. Cash deposited intact daily

II. Employees handling cash are bonded

II. Bank reconciliation prepared by individuals independent of

cash receipts recordkeeping

III. Internal control questionnaire designed using DAASI.

TITLE

Yes or No

D=

Are prenumbered SO, SD, and SI used and accounted for?

Is posting of the A/R S/L done from remittance advices?

Is a trial balance and aging of the A/R prepared monthly?A=

Is credit approved prior to shipment of goods?

Are monthly statements reviewed by the supervisor prior to

mailing?I=

Is the A/R G/L reconciled with the S/L on a regular basis?

Are sales invoices compared to sales orders and shipping

documents?

to determine that ordered goods were shipped and shipped goods

were

ordered?

NOTE: A NO answer on an I/C questionnaire indicates a

weakness.

The following questions are from the CPA Exam. You are given 15

- 25 minutes to answer each question. Each essay question is worth

10 points.

CPA EXAMPLE ESSAY #1

(Internal Controls for Cash Receipts) You have been asked by the

board of trustees of a local church to review its internal

controls. As a part of this review, you have prepared the following

comments relating to the collection made at weekly services and

recordkeeping for members pledges and contributions:

The churchs board of trustees has delegated responsibility for

financial management and audit of the financial records to the

finance committee. This group prepares the annual budget and

approves major disbursements, but is not involved in collections or

recordkeeping. No audit has been considered necessary in recent

years because the same trusted employee has kept church records and

has served as financial secretary for fifteen years.

The collection at the weekly service is taken by a team of

ushers. The head usher counts the collection in the church office

following each service. He then places the collection and a

notation of the amount counted in the church safe. Next morning,

the financial secretary opens the safe and recounts the collection.

She withholds about $100 to meet cash expenditures during the

coming week and deposits the remainder of the collection intact. In

order to facilitate the deposit, members who contribute by check

are asked to draw their checks to cash.

At their request, a few members are furnished prenumbered,

predated envelopes in which to insert their weekly contributions.

The head usher removes the cash from the envelopes to be counted

with the loose cash included in the collection and discards the

envelopes. No record is maintained of issuance or return of the

envelopes and the envelope system is not encouraged.

Each member is asked to prepare a contribution pledge card

annually. The pledge is regarded as a moral commitment by the

member to contribute a stated weekly amount. Based upon the amounts

shown on the pledge cards, the financial secretary furnishes a

letter to the members that supports the tax deductibility of their

contributions.

REQUIRED: Identify the internal control weaknesses apparent in

this scenario and recommendations for improvements.

CPA ESSAY ANSWER #1

WeaknessesRecommended Improvements

Financial secretary exercises too much control over

collections.

To the extent possible, financial secretarys responsibilities

should be confined to record-keeping.

Finance committee is not exercising its assigned responsibility

for collections.

Finance committee should assume a more active supervisory

role.

The auditing function has been assigned to the finance

committee, which also has responsibility for the administration of

the cash function. Moreover, the finance committee has not

performed the auditing function.

An audit committee should be appointed to perform periodic

auditing procedures or engage outside auditors.

The head usher has sole access to cash during the period of the

count. One person should not be left alone with the cash until the

amount has been recorded or control has been established in some

other way.

The number of counters should be increased to at least two, and

cash should remain under joint surveillance until counted and

recorded so that any discrepancy will be brought to attention.

The collection is vulnerable to robbery while it is being

counted and transported from the church safe to its deposit

bank.

The collection should be deposited in the banks night depository

immediately after the count. Physical safeguards, such as locking

and bolting the door during the period of the count, should be

instituted. Vulnerability to robbery will also be reduced by

increasing the number of counters.

The head ushers count lacks usefulness from a control standpoint

because he surrenders custody of both the cash and the record of

the count.

The financial secretary should receive a copy of the collection

report for posting to the financial records. The head usher should

maintain a copy of the report for use by the audit committee.

Contributions are not deposited intact. There is no assurance

that amounts withheld by the financial secretary for expenditures

will be properly accounted for.

Contributions should be deposited intact. If it is considered

necessary for the financial secretary to make cash expenditures, he

or she should be provided with a cash-working fund. The fund should

be replenished by check based upon satisfactory support and a

properly approved reimbursement request.

Members are asked to draw checks to cash thus making the checks

completely negotiable and vulnerable to misappropriation.

Members should be asked to make checks payable to the church. At

the time of the count, ushers should stamp the churchs restrictive

endorsement (For Deposit Only) on the back of the check.

The envelope system has not been encouraged. Control features

which it could provide have been ignored.

The envelope system should be encouraged. Ushers should indicate

on the outside of each envelope the amount contributed. Envelope

contributions should be reported separately and supported by the

empty collection envelopes. Prenumbered envelopes will permit ready

identification of the donor by authorized persons without general

loss of confidentiality.

CPA EXAMPLE ESSAY #2

Trapan Retailing Inc., has decided to diversify operations by

selling through vending machines. Trapans plans call for the

purchase of 312 vending machines which will be situated at 78

different locations within one city, and the rental of a warehouse

to store merchandise. Trapan intends to sell only canned beverages

at a standard price.

Management has hired an inventory control clerk to oversee the

warehousing functions, and two truck drivers who will periodically

fill the machines with merchandise, and deposit cash collected at a

designated bank. Drivers will be required to report to the

warehouse daily.

Required:

What internal controls should the auditor expect to find in

order to assure the integrity of the cash receipts and warehousing

functions?

The internal controls should provide for

S or IDrivers to count and then sign for all merchandise

received.

IDaily verification of each drivers ending inventory.

ACash to be deposited daily by each driver.

DDaily return of duplicate deposit slips by each driver.

IReconciliation of cash deposits with the daily net change in

inventory.

I Provision for explanation of overages and shortages.

IPeriodic independent surprise check of machines to verify

that

a. Machines contain only authorized Trapan-purchased

merchandise.

b. Machines are mechanically programmed to charge the authorized

prices.

c. Cash and merchandise in machines equal a predetermined

total.

ABonding of employees

I or AAlternate driver routes and required vacations.

ARestricting access to the warehouse.

SThe warehouseman to count and sign for all items.

D or IMaintenance of perpetual inventory records.

IPeriodic physical inventory count of merchandise in the

warehouse.

IAnalytical review of collections.

CPA EXAMPLE ESSAY #3

Taylor, CPA, has been engaged to audit the financial statements

of Johnson Coat Outlet, Inc., a medium-sized mail-order retail

store that sells a wide variety of coats to the public.

Required:Prepare the Shipments segment of Taylors internal

control questionnaire. Each question should elicit either a yes or

no response.

Do not prepare questions relating to the cash receipts, sales

returns and allowances, billing, inventory control, or other

segments.

Use the following format:

QuestionYesNo

JOHNSON COAT OUTLET, INC.

Shipments

Internal Control Questionnaire

QuestionYesNo

D or A 1. Are shipping documents prepared from sales orders

approved in accordance with managements authorization?

D 2. Are shipping documents prenumbered?

D 3. Are shipping documents periodically accounted for?

D 4. Are shipping documents recorded in a register, log, or

file?

D 5. Are copies of shipping documents forwarded to the

Billing department?Inventory control department?

I 6. Do shipping documents include cross reference to sales

orders; customer identity and address; description and

quantities of goods shipped; date; and other details?

S 7. Is the shipping function independent of

Sales orders?Credit approval?Billing and accounts

receivable?Cash receipts?Warehouse?Receiving?Inventory Control?

A 8. Is access to merchandise restricted and controlled

within

the shipping department?

I 9. Are type and quantities of goods withdrawn and packed

for

shipping verified by independent counts?

I10. Are receipts from carriers obtained and filed?

CPA EXAMPLE ESSAY #4

A CPAs audit working papers include the narrative description

below of the cash receipts and billing portions of the internal

controls of Parktown Medical Center, Inc. Parktown is a small

health care provider that is owned by a publicly held corporation.

It employs seven salaried physicians, ten nurses, three support

staff in a common laboratory, and three clerical workers. The

clerical workers perform such tasks as reception, correspondence,

cash receipts, billing, and appointment scheduling and are

adequately bonded. They are referred to in the narrative as office

manger, clerk #1, and clerk #2.

Most patients pay for services by cash or check at the time

services are rendered. Credit is not approved by the clerical

staff. The physician who is to perform the respective services

approves credit based on an interview. When credit is approved, the

physician files a memo with the billing clerk (clerk #2) to set up

the receivable from data generated by the physician.

The servicing physician prepares a charge slip that is given to

clerk #1 for pricing and preparation of the patients bill. Clerk #1

transmits a copy of the bill to clerk #2 for preparation of the

revenue summary and for posting in the accounts receivable

subsidiary ledger.

The cash receipts functions are performed by clerk #1, who

receives cash and checks directly from patients and gives each

patient a prenumbered cash receipt. Clerk #1 opens the mail and

immediately stamps all checks for deposit only and lists cash and

checks for deposit. The checks and cash are deposited daily by the

office manager. The list of cash and checks, together with related

remittance advices, are forwarded by clerk #1 to clerk #2. Clerk #1

also serves as receptionist and performs general correspondence

duties.

Clerk #2 prepares and sends monthly statements to patients with

unpaid balances. Clerk #2 also prepares the cash receipts journal

and is responsible for the accounts receivable subsidiary ledger.

No other clerical employee is permitted access to the accounts

receivable subsidiary ledger. Uncollectible accounts are written

off by clerk #2 only after the physician who performed the

respective services believes the account to be uncollectible and

communicates the write-off approval to the office manager. The

office manager then issues a write-off memo that clerk #2

processes.

The office manager supervises the clerks, issues write-off

memos, schedules appointments for the doctors, makes bank deposits,

reconciles bank statements, and performs general correspondence

duties.

Additional services are performed monthly by a local accountant

who posts summaries prepared by the clerks to the general ledger,

prepares income statements, and files the appropriate payroll forms

and tax returns. The accountant reports directly to the parent

corporation.

Required:

Based only on the information in the narrative, describe the

reportable conditions and one resulting misstatement that could

occur and not be prevented or detected by Parktowns internal

controls concerning the cash receipts and billing function. Do not

describe how to correct the reportable conditions and potential

misstatements. Use the format illustrated below.Reportable

conditionPotential misstatement

There is no control to verify that fees are recorded and billed

at authorized rates and terms.Accounts receivable could be

overstated and uncollectible accounts understated because of the

lack of controls.

CPA ESSAY ANSWER #4

The reportable conditions and resulting misstatements, in

addition to the example that could occur and not be prevented or

detected by Parktowns internal controls concerning the cash

receipts and billing functions include the following:

Reportable conditionPotential misstatement

The employees who perform services also are permitted to approve

credit without an external credit check.Uncollectible accounts

expense could be understated and accounts receivable could be

overstated because of the lack of an appropriate credit check.

There is no independent verification of the billing process.Fees

earned and accounts receivable may be understated because not all

services performed might be reported for billing.

or

Fees earned and accounts receivable may be either overstated or

understated because of the use of incorrect price or service data

or because of mathematical errors.

The employees who approve credit also approve write-offs of

uncollectible accounts.Accounts receivable could be understated and

uncollectible accounts expense overstated because write-offs of

accounts receivable could be approved for accounts that are, in

fact, collectible.

or

Accounts receivable could be overstated and uncollectible

accounts expense understated because write-offs of accounts

receivable might not be initiated for accounts that are

uncollectible.

Credit is not granted on the basis of established

limits.Uncollectible accounts expense could be either

understated or overstated because the lack of established credit

limits may make it more difficult to identify uncollectible

amounts.

The employee who initially handles cash receipts also prepares

billings.Fees earned and cash receipts or accounts receivable could

be understated because of omitted or inaccurate billing.

The employee who makes bank deposits also reconciles bank

statements.The cash balance per books may be overstated because not

all cash is deposited.

Uncollectible accounts are not determined on the basis of

established criteria.Uncollectible accounts expense could be either

understated or overstated because of the lack of established

write-off criteria.

Trial balances of the accounts receivable subsidiary ledger are

not prepared independently of, or verified and reconciled to, the

accounts receivable control account in the general ledger.Any of

fees earned, cash receipts, and uncollectible accounts expense

could be either understated or overstated because of undetected

differences between the subsidiary ledger and the general

ledger.

or Fees earned and cash receipts or accounts receivable could be

understated because of failure to record billing, cash receipts, or

write-offs accurately.

SMALLCO LUMBER ANSWERThe Weaknesses in Smallco Lumbers internal

controls are:

Warehouse ClerkA - Releases lumber prior to

authorization, for example, approval

of customers credit.

D - Copies of shipping advice should be

prepared and forwarded to

Bookkeeper #1.

D - Lacks documentation that lumber

was given to the carrier.

Bookkeeper #2S - Bookkeeper who maintains general

ledger should not be responsible for

footing and crossfooting of journals,

that is, sales and cash receipts

journals.

I - Subsidiary accounts receivable

ledger should be reconciled to

general ledger.

Bookkeeper #1A - Credit authorized by bookkeeper and

not a responsible officer.

I - Prepares and mails invoice without

knowledge of what was shipped.Collection ClerkS - Collection

clerk should not maintain

sales journal.

S - Collection clerk should not maintain

accounts receivable subsidiary

ledger.

D - Remittance advice not used as the

basis for posting collections.

A - Checks are not promptly endorsed by

the mail clerk.

A - Cash receipts are not promptly

deposited.

I - Deposit slips are not reconciled to

cash receipts journal or debits to

general ledger.

CHARTINGCharting, Inc. processes its sales and cash receipts

documents as follows:

Payment on account: The mail is opened each morning by a mail

clerk in the sales department. The mail clerk prepares a remittance

advice showing customer and amount paid if one is not received. The

checks and remittance advices are then forwarded to the sales

department supervisor who reviews each check and forwards the

checks and remittance advices to the accounting department

supervisor.

The accounting department supervisor, who also functions as

credit manager approving new credit and all credit limits, reviews

all checks for payments on past due accounts and then forwards the

checks and remittance advices to the A/R clerk, who arranges the

advices in alphabetical order. The remittance advices are posted

directly on the A/R ledger cards. The checks are endorsed by stamp

and totaled. The total is posted to the cash receipts journal. The

remittance advices are filed chronologically.

After receiving the cash from the previous days cash sales, the

A/R clerk prepares the daily deposit slip in triplicate. The third

copy of the deposit slip is filed by date, and the second copy and

the original accompany the bank deposit.

Sales: Sales clerks prepare sales invoices in triplicate. The

original & second copy go to the cashier. The third copy is

retained by the sales clerk in the sales book. For cash sales, the

customer pays the sales clerk, who presents the money to the

cashier with the invoice copies.

A credit sale is approved by the cashier from an approved credit

list after the sales clerk prepares the three-part invoice. After

receiving the cash or approving the invoice, the cashier validates

the original copy of the sales invoice and gives it to the

customer. At the end of each day, the cashier recaps the sales and

cash received and forwards the cash and the second copy of all

sales invoices to the accounts receivable clerk.

The A/R clerk balances the cash received with cash sales

invoices and prepares a daily sales summary. The sales invoices are

sent to the inventory control clerk in the sales department for

posting to the inventory control cards. After posting, the

inventory control clerk files all invoices numerically. The A/R

clerk posts the daily sales summary to the cash receipts journal

and sales journal and files the sales summaries by date. The clerk

also post the credit sales to the accounts receivable subsidiary

ledger account.

The cash sales and cash received on account make up the daily

bank deposit.

Bank deposits: The bank validates the deposit slip and returns

the second copy to the accounting department where it is filed by

date by the accounts receivable clerk.Monthly bank statements are

reconciled promptly by the accounting department supervisor and

filed by date.

REQUIRED:

1.Complete the flowchart on the following page by labeling the

appropriate symbols and indicating information flows. The chart is

complete as to symbols and document flows.

2.Identify weaknesses in Chartings internal controls.

CONTROL RISK ASSESSMENT CONSIDERATIONSCREDIT SALES

TRANSACTIONS

Potential

MisstatementNecessary

ControlPotential Testof Control

Sales may be made to un-authorized customers.Determination that

customer is on approved customer list.

Approved sales order form for each sale.Reperform procedure.

Examine approved sales order forms.

Sales may be made without credit approval.Credit department

credit check on all new customers.

Check on customers credit limit prior to each sale.Inquire about

procedures for checking credit on new customers.

Examine evidence of credit limit check prior to each sale.

Goods may be released from warehouse for unauthorized

orders.Approved sales order for all goods released to

shipping.Observe warehouse personnel filing orders.

Goods shipped may not agree with goods ordered.Independent check

by shipping clerks of agreement of goods received from warehouse

with approved sales order.Examine evidence of performance of

independent check.

Unauthorized shipments may be made.Segregation of duties filling

and shipping orders.

Preparation of shipping document for each shipment.Observe

segregation of duties.

Inspect shipping documents.

Billings may be made for fictitious transactions or duplicate

billings may be made.Matching shipping document and approved sales

order for each invoice.Vouch invoices to shipping documents and

approved sales orders.

Some shipments may not be billed.Matching sales invoice for each

shipping document.Trace shipping documents to sales invoices.

Sales invoices may have incorrect prices.Independent check on

pricing of invoices.Reperform check on accuracy of pricing.

Invoices may not be journalized or posted to customer

accounts.Independent check of agreement of sales journal entries

and amounts posted to customer accounts with control totals of

invoices.Review evidence of independent checks; re-perform

checks.

Invoices may be posted to wrong customer account.Mailing of

monthly statement to customers.Observe mailing of monthly

statements.

CONTROL RISK ASSESSMENT CONSIDERATIONCASH RECEIPTS

TRANSACTIONS

Potential

MisstatementNecessary

ControlPotential Test

of Control

Cash sales may not be registered.Use of cash registers or

point-of-sale devices.

Periodic surveillance of cash sales procedures.Observe cash

sales procedures.

Inquire of supervisors about results of surveillance.

Mail receipts may be lost or misappropriated after

receipt.Restrictive endorsement of checks immediately on

receipt.

Immediate preparation of prelist of mail receipts.Examine checks

for restrictive endorsement.

Observe preparation of prelists.

Cash and checks received for deposit may not agree with cash

count sheets and prelist.Independent check of agreement of cash and

checks with cash count sheets and prelist.Examine evidence of

independent check.

Cash may not be deposited intact daily.Independent check of

agreement of validated deposit slip with daily cash

summary.Reperform independent check.

Remittance advices may not agree with prelist.Independent check

of agreement or remittance advices with prelist.Examine evidence of

independent check.

Some receipts may not be recorded.Independent check of agreement

of amounts journalized and posted with daily cash summary.Reperform

independent check.

Errors may be made in journalizing receipts.Preparation of

periodic independent bank reconciliations.Examine bank

reconciliations.

Receipts may be posted to the wrong customer account.

Mailing of monthly statements to customers.Observe mailing of

monthly statements.

OOF QUESTION 2 (CPA, adapted) 15-25 minutes

Field, CPA, is auditing the financial statements of Miller

Mailorder, Inc. (MMI) for the year ended January 31, 1996. Field

has compiled a list of possible errors and fraud that may result in

the misstatement of MMI's financial statements and a corresponding

list of internal control activities that, if properly designed and

implemented, could assist MMI in preventing or detecting errors and

fraud.

Required

For each possible error and fraud numbered 1 through 15, select

one internal control activity from the answer list at right that,

if properly designed and implemented, most likely could assist MMI

in preventing or detecting the errors and fraud. Each response in

the list of internal control activities may be selected once, more

than once, or not at all.

Possible Errors and Frauds

1. Invoices for goods sold are posted to incorrect customer

accounts.

2. Goods ordered by customers are shipped but are not billed to

anyone.

3. Invoices are sent for shipped goods but are not recorded in

the sales journal.

4. Invoices are sent for shipped goods and are recorded in the

sales journal but are not posted to any customer account.

5. Credit sales are made to individuals with unsatisfactory

credit ratings.

6. Good are removed from inventory for unauthorized orders.

7. Goods shipped to customers do not agree with goods ordered by

customers.

8. Invoices are sent to allies in a fraudulent scheme, and sales

are recorded for fictitious transactions.

9. Customers' checks are received for less than the customers'

full account balances, but the customers full account balances are

credited.

10. Customers' checks are misappropriated before being forwarded

to the cashier for deposit.

11. Customers' checks are credited to incorrect customer

accounts.

12. Different customer accounts are each credited for the same

cash receipt.

13. Customers' checks are properly credited to customer accounts

and are properly deposited, but errors are made in recording

receipts in cash receipts journal.

14. Customers' checks are misappropriated after being forwarded

to the cashier for deposit.

15. Invalid transactions granting credit for sales returns are

recorded.

Internal Control ActivitiesA. Shipping clerks compare goods

received from the warehouse with the details on the shipping

documents.

B. Approved sales orders are required for goods to be released

from the warehouse.

C. Monthly statements are mailed to all customers with

outstanding balances.

D. Shipping clerks compare goods received from the warehouse

with approved sales orders.

E. Customer orders are compared with the inventory master file

to determine whether items ordered are in stock.

F. Daily sales summaries are compared with control totals of

invoices.

G. Shipping documents are compared with sales invoices when

goods are shipped.

H. Sales invoices are compared with the master price file.

I. Customer orders are compared with an approved customer

list.

J. Sales orders are prepared for each customer order.

K. Control amounts posted to the accounts receivable ledger are

compared with control totals of invoices.

L. Sales invoices are compared with shipping documents and

approved customer orders before invoices are mailed.

M. Prenumbered credit memos are used for granting credit for

goods returned.

N. Goods returned for credit are approved by the supervisor of

the Sales Department.

O. Remittance advices are separated from the checks in the mail

room and forwarded to the Accounting Department.

P. Total amounts posted to the accounts receivable ledger from

remittance advices are compared with the validated bank deposit

slip.

Q. The cashier examines each check for proper endorsement.

R. Validated deposit slips are compared with the cashier's daily

cash summaries.

S. An employee, other than the bookkeeper, periodically prepares

a bank reconciliation.

T. Sales returns are approved by the same employee who issues

receiving reports evidencing actual return of goods.

1. The correct answer is (C).DISCUSSION:Mailing monthly

statements to customers with outstanding accounts will detect

invoices posted to the wrong accounts. Customers whose accounts

were misposted for goods not ordered will contest the

statements.

2. The correct answer is (G).DISCUSSION:Each shipping document

should have a corresponding invoice when the goods are shipped. The

appropriate direction of testing is from the shipping documents to

the sales invoices.

3. The correct answer is (F).DISCUSSION:Daily sales summaries

are from the book of original entry--the sales journal. Comparing

the summaries with the total of invoices will detect failure to

record all invoices.

4. The correct answer is (K).DISCUSSION:Comparing control total

amounts posted to the accounts receivable (subsidiary) ledger with

the control total of all invoices for the same period should detect

invoices not posted.

5. The correct answer is (I).DISCUSSION:Credit approval should

be received before sales are made. Thus, shipping to customers on

an approved list should reduce the risk of sales to customers with

unsatisfactory credit.

6. The correct answer is (B).DISCUSSION:An approved sales order

should be presented to the storekeeper before release of goods from

the warehouse to prevent goods from being removed for unauthorized

orders.

7. The correct answer is (D).DISCUSSION:Requiring shipping

clerks to compare the amounts and type of goods received from the

warehouse with approved sales orders assures that goods shipped

agree with those ordered by customers.

8. The correct answer is (L).DISCUSSION:Comparing sales invoices

with shipping documents will assure that each invoice is supported

by a shipment. Fictitious sales, i.e., those for which no shipment

was made, should be detected.

9. The correct answer is (P).DISCUSSION: The total receipts

credited to customer accounts in the subsidiary ledger should equal

the total receipts deposited, given that daily receipts are

deposited intact.

10. The correct answer is (C).DISCUSSION:Checks misappropriated

(stolen) prior to forwarding to the cashier are not posted to

customer accounts (assuming that the remittance advices were stolen

as well). Thus, customers will complain when their payments fail to

be reflected in the balances on the monthly statements.

11. The correct answer is (C).DISCUSSION:Mailing monthly

statements to customers with outstanding accounts will detect

receipts posted to the wrong accounts. Customers whose accounts

were misposted will contest the statements.

12. The correct answer is (P).DISCUSSION:If more than one

customer account is credited for the same cash receipt, the error

will be detected when the total of the amounts posted to the

accounts receivable ledger is compared with the total cash

receipts.

13. The correct answer is (S).DISCUSSION:The bank reconciliation

will detect errors in recording cash receipts (and disbursements).

The balance in the ledger will not reconcile with the amount in the

bank statement.

14. The correct answer is (P).DISCUSSION- If the checks are

misappropriated (stolen) prior to deposit, the total of the amounts

posted to the accounts receivable ledger will be greater than the

validated bank deposit slip.

15. The correct answer is (N).DISCUSSION:Invalid sales returns

are prevented by requiring approval of returns by the Sales

Department supervisor.

REVENUE CYCLE MULTIPLE CHOICE

1.For effective internal control, the billing function should be

performed by the

a.Accounting department.

c.Shipping department.

b.Sales department.

d.Credit & collection department.

2.For good internal control, which of the following functions

should not be the

responsibility of the treasurers department?

a.Data processing.

c.Custody of securities.

b.Handling of cash.

d.Establishing credit policies.

3.When a customer fails to include a remittance advice with a

payment, it is

common practice for the person opening the mail to prepare

one.

Consequently, mail should be opened by which of the following

four company

employees?

a.Credit manager.

c.Sales manager.

b.Receptionist.

d.Account receivable clerk.

4.Which one of the following is not a universal rule for

achieving strong internal

control over cash?

a.Separate cash handling and the record keeping functions.

b.Decentralize the receiving of cash as much as possible.

c.Deposit each days cash receipts by the end of the day.

d.Have bank reconciliations performed by employees independent

with respect to handling cash.

5.The least crucial element of internal control over cash is

a.Separation of cash record keeping from custody of cash.

b.Preparation of the monthly bank reconciliation.

c.Batch processing of checks.

d.Separation of cash receipts from cash disbursements.

6.Which of the following sets of duties would ordinarily be

considered basically

incompatible in terms of good internal control?

a.Preparation of monthly statements to customers and maintenance

of the

accounts receivable subsidiary ledger.

b.Posting to the general ledger and approval of additions and

terminations

relating to the payroll.

c.Custody of unmailed signed checks and maintenance of expense

subsidiary

ledgers.

d.Collection of receipts on account and maintaining accounts

receivable

records.

7.Internal control over cash receipts is weakened when an

employee who

receives customer mail receipts also

a.Prepares initial cash receipts records.

b.Records credits to individual accounts receivable.

c.Prepares bank deposit slips for all mail receipts.

d.Maintains a petty cash fund.

8.Which of the following is an effective internal control over

accounts receivable?

a.Only persons who handle cash receipts should be responsible

for the

preparation of documents that reduce accounts receivable.

b.Responsibility for approval of the write-off of uncollectible

accounts should lie with sales personnel.

c.Balances in the subsidiary accounts receivable ledger should

be reconciled

to the G/L control account once a year, preferably at the year

end.

d.The billing function should be assigned to persons other than

those

responsible for maintaining accounts receivable subsidiary

records.

9.Smith Manufacturing Companys accounts receivable clerk has a

friend who is

also Smiths customer. The accounts receivable clerk, on

occasion, has issued

fictitious credit memorandums to his friend for goods supposedly

returned. The

most effective procedure for preventing this activity is to

a.Prenumber and account for all credit memorandums.

b.Require receiving reports to support all credit

memorandums.

c.Have the sales department independent of the A/R

department.

d.Mail monthly statements.

10.Salesmens commissions are based on gross sales. Sales

continue to increase; but uncollectible A/R are also increasing at

an alarming rate. The most effective procedure for preventing the

increase in uncollectible A/R is to

a.Have the sales manager review activity of individual

salesmen.

b.Age accounts receivable regularly.

c.Have the write-off of accounts properly approved.

d.Have the credit dept approve credit to customers before

shipment.

11.The sales department bookkeeper has been crediting

house-account sales to

her brother-in-law, an outside salesman. Commissions are paid on

outside

sales but not on house-account sales. This might have been

prevented by

requiring that

a.Sales order forms be prenumbered and accounted for by the

sales department bookkeeper.

b.Sales commission statements be supported by sales order forms

and

approved by the sales manager.

c.Aggregate sales entries be prepared by the general accounting

department.

d.Disbursement vouchers for sales commissions be reviewed by the

internal

audit department and checked to commission statements.

12.Which of the following control procedures may prevent the

failure to bill

customers for some shipments?

a.Each shipment should be supported by a prenumbered sales

invoice.

b.Each sales order should be approved by authorized

personnel.

c.Sales journal entries should be reconciled to daily sales

summaries.

d.Each sales invoice should be supported by a shipping

document.

13.To achieve good I/C which department should match shipping

documents with

sales orders and prepare daily sales summaries?

a.Billing.

c. Credit.

b.Shipping. d. Sales.

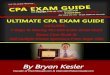

CPA ESSAY ON A COMPUTERIZED REVENUE CYCLE FLOWCHART

Required:The flowchart on the following page depicts part of a

revenue cycle. Some of the flowchart symbols are labeled to

indicate control procedures and records. For each symbol numbered 1

through 13, select one response from the answer lists below. Each

response in the lists may be selected once or not at all.

Operations and control procedures

A.Enter shipping data

B.Verify agreement of sales order and shipping document

C.Write off accounts receivable 1.

D.To warehouse and shipping department 2.

E.Authorize account receivable write-off 3.

F.Prepare aged trial balance 4.

G.To sales department 5.

H.Release goods for shipment 6.

I.To accounts receivable department 7.

J.Enter price data 8.

K.Determine that customer exists 9.

L.Match customer purchase order with sales order10.

M.Perform customer credit check11.

N.Prepare sales journal12.

O.Prepare sales invoice13.

Documents, journals, ledgers, and files

P.Shipping document

Q.General ledger master file

R.General journal

S.Master price file

T.Sales journal

U.Sales invoice

V.Cash receipts journal

W.Uncollectible accounts file

X.Shipping file

Y.Aged trial balance

Z.Open order file

CPA COMPUTERIZED REVENUE CYCLE FLOWCHART

DESCRIPTION OF ON-LINE ENTRY/BATCH PROCESSING FOR REVENUE

APPLICATION

Figure 1 shows a flowchart of an on-line batch entry processing

system that incorporates most of the controls discussed in the

preceding sections.

In the illustrated system, as orders are received sales order

clerks use on-line terminals and an order program to determine that

the customer has been approved, and that the order will not cause

the customer's balance to exceed the customer's authorized credit

limit. The program also checks the inventory master file to

determine that goods are on hand to fill the order. If the order is

accepted, the computer enters it into an open order file and a

multicopy sales order form is produced on a printer in the sales

order department. When an order is, not accepted, a message is

displayed on the terminal indicating the reason for rejection.

Copies of the approved sales order are forwarded to the

warehouse as authorization to release goods to shipping. In

shipping, personnel first makes an independent check on agreement

of the goods received with the accompanying sales order form. They

then use their on-line terminals and a shipping program to retrieve

the corresponding sales order from the open order file and add

appropriate shipping data. Next the computer transfers the

transaction from the open order file to a shipping file and

produces a shipping document on the printer in the shipping

department.

As matching shipping documents and sales order forms are

received in the billing department, they are batched and batch

totals are manually compared. Using their on-line terminals and a

billing program, billing department personnel first enter the

manually prepared batch totals. Next the previously entered order

and shipping data for each transaction is retrieved from the

shipping file and a sales invoice is generated using prices from

the master price file. As each billing is completed, the computer

enters it into a sales transactions file. After all the

transactions in a batch have been processed in this manner, the

billing program compares a computer generated batch total with the

manual batch total previously entered by the billing clerk.

Discrepancies are displayed on the terminal and corrected by the

billing clerks before processing continues. Finally, sales invoices

for the batch are printed in the EDP department and distributed as

shown in the flowchart.

The recording of sales transactions is completed at the end of

each day when the EDP department runs the master file update

program. As shown, this program updates three master files and

produces a sales journal and general ledger transaction summary

which are sent to accounting. The use of a separate program to

produce monthly customer statements is not shown in the

flowchart.

PAGE 1

_935322661.doc

Cash

Document

Cash Sales

Invoice

Supervisor

reading of

register daily

and

reconciliation

with cash

Supervisor

preparation of

Cash Count

Sheet

Document

Document

Cash

Document

Document

Register

Reading

Remittance Advice

Checks From

Customers

Remittance Advice

Checks

Prelist

Prelist

Prelist of

Mail Receipts

Register Reading

Count Sheet

Cash

Checks

Prelist

Cash and Checks

Prelist

Register Reading

Cash Count Sheet

Deposit Slip

Daily Cash Summary

Prelist

Daily Cash

Summary

Register Reading

Count Sheet

Deposit Slip

Daily Cash

Summary

Register Reading

Prelist

Prelist

Register Reading

Count Sheet

Deposit Slip

Daily Cash

Summary

1

2

1

2

1

2

To

Treasurer

1

2

3

To

Accounting

2

3

1

2

2

2

3

To Bank

To General

Accounting

1

2

2

2

2

3

2

2

1

2

3

2

SALES

CASHIER

CASH RECEIPTS FLOWCHART

A

_969213270.doc

Open

Mail

Write

Invoice For

Cust. Order

Checks

Remittance

Advice

Sales

Invoice

Sales

Invoice

Cash

Sales

Invoice

Post

Checks

Remittance

Advice

Prepare Remittance

Advice if Needed

2

1

2

3

Mail

Mail Clerk

Retained

In Sales

Book

From Customer

Customer

Inventory Control Clerk

File

N

1

2

Checks

Remittance

Advice

Accounts

Receivable

Ledger

Post

Checks

Remittance

Advice

Sales

Journal

Post

Sales Invoice

Cash

Post

Check

Total

Daily Sales

Summary

Endorse

Checks Total

Cash and

Prepare

Deposit Slip

2

File

D

To Bank

Validated

Deposit Slip

Monthly Bank

Statement

From

Bank

CLERKS

CASHIER

SALES SUPER.

A/R SUPER

ACCOUNTING DEPARTMENT/ACCOUNTS RECEIVABLE CLERK

SALES AND CASH RECEIPTS FOR CHARTING, INC.

Filed Third

Copy of

Deposit

Slip

Sales Clerks

A

B

C

D

E

F

G

H

I

J

K

L

M

N

O

P

Q

R

S

T

_921582673.doc

FIGURE 1

EXAMPLE OF ON-LINE ENTRY/BATCH PROCESSING FOR A REVENUE

APPLICATION

WAREHOUSE

BILLING

SHIPPING

EDP

SALES ORDER

N

N

To Customer

To Accounting

N

N

To Customer

2

3

4

2

3

2

1

2

1

Sales

Trans.

File

Shipping

File

Master

Price

File

Open

Order

File

General

Ledger

Master

File

Inventory

Master

File

Accts.

Rec.

Master

File

3

2

4

3

2

1

Shipping

Document

Sales Order

Enter Batch

Total; Prepare

Billing

Prepare

Batch

Total

Shipping

Document

Shipping Doc.

Shipping Doc.

Sales Order

Shipping Doc.

Enter

Shipping

Date

Check Agreement

of Goods and

Sales Order

Sales

Invoice

Sales Invoice

General Ledger

Transaction

Summary

Sales Journal

Retrieve Shipped Order Data;

Prepare Invoice; Accumulate

and Compare Batch Total;

Enter in Sales Transactions

File; Print Invoices

BILLING PROGRAM

Retrieve Open Orders;

Add Shipping Data;

Transfer to Shipping File;

Print Shipping Documents

SHIPPING PROGRAM

Update Master Files;

Print Sales Journal and

General Ledger

Transaction Summary

MASTER FILE

UPDATE PROGRAM

To

Shipping

with

Goods

Sales

Order

Sales Order

Release

Goods to

Shipping

Sales

Orders

Sales Order

Sales Order

Sales Order

Customer Order

From

Warehouse

Perform Edit and

Credit Checks;

Print Sales Orders

ORDER PROGRAM

Enter

Order

Data

Customer's

Order