Embed Size (px)

Citation preview

333(University(Ave,(Suite(160(•(Sacramento,(CA(95825Phone:(d916l(561-0890(•(Fax:(d916l(561-0891

www.goodwinconsultinggroup.net

CITY AND COUNTY OF SAN FRANCISCO

COMMUNITY FACILITIES DISTRICT NO. 2014-1 (TRANSBAY TRANSIT CENTER)

CFD TAX ADMINISTRATION REPORT FISCAL YEAR 2020-21

September 17, 2020

Community Facilities District No. 2014-1 CFD Tax Administration Report

TABLE OF CONTENTS

Section Page Executive Summary ............................................................................................................. i I. Introduction ..........................................................................................................................1 II. Purpose of Report ................................................................................................................2 III. Special Tax Requirement .....................................................................................................3 IV. Special Tax Levy .................................................................................................................4 V. Development Status .............................................................................................................5 VI. Prepayments .........................................................................................................................6 VII. State Reporting Requirements .............................................................................................7 Appendix A - Fiscal Year 2020-21 Base Special Tax Rates Appendix B – Summary of Fiscal Year 2020-21 Special Tax Levy Appendix C – Fiscal Year 2020-21 Special Tax Levy for Individual Assessor’s Parcels Appendix D – Amended and Restated Rate and Method of Apportionment of Special Tax Appendix E – Boundary Map of Community Facilities District No. 2014-1 Appendix F – Assessor’s Parcel Maps for Fiscal Year 2020-21

City and County of San Francisco i Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

EXECUTIVE SUMMARY The following summary provides a brief overview of the main points from this report regarding the City and County of San Francisco Community Facilities District No. 2014-1 (Transbay Transit Center) (“CFD No. 2014-1” or “CFD”): Fiscal Year 2020-21 Special Tax Levy

Number of Taxed Parcels Total Special Tax Levy

212 $28,902,239 For further detail regarding the special tax levy, or special tax rates, please refer to Section IV of this report. Development Status for Fiscal Year 2020-21

Land Use Square Feet

For-Sale Residential Square Footage 632,527 Square Feet

Rental Residential Square Footage 1,033,993 Square Feet

Office Square Footage 2,650,625 Square Feet

Hotel Square Footage 0 Square Feet

Retail Square Footage 63,411 Square Feet

For more information regarding the status of development in CFD No. 2014-1, please see Section V of this report.

City and County of San Francisco ii Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

Outstanding Bonds Summary

Bonds Original Principal

Amount Retired*

Current Amount Outstanding*

Special Tax Bonds, Series 2017A (Federally Taxable) $36,095,000 $665,000 $35,430,000

Special Tax Bonds, Series 2017B (Federally Taxable – Green Bonds) $171,405,000 $3,130,000 $168,275,000

Special Tax Bonds, Series 2019A (Federally Taxable) $33,655,000 $650,000 $33,005,000

Special Tax Bonds, Series 2019B (Federally Taxable – Green Bonds) $157,310,000 $3,000,000 $154,310,000

2020B Special Tax Bonds (Federally Taxable – Green Bonds) $81,820,000 $0 $81,820,000

* As of the date of this report.

City and County of San Francisco 1 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

I. INTRODUCTION Community Facilities District No. 2014-1 On September 23, 2014, the City and County of San Francisco (the “City”) adopted Resolution No. 350-14, the Resolution of Formation of CFD No. 2014-1. In a landowner election held on December 29, 2014, the then-qualified landowner electors within CFD No. 2014-1 authorized the levy of a Mello-Roos special tax. The landowners also voted to incur bonded indebtedness in an amount not to exceed $1,400,000,000. The initial boundaries of CFD No. 2014-1 are comprised of 17 parcels located in downtown San Francisco. Approximately 12 development projects are anticipated on these parcels. The CFD also includes a Future Annexation Area, which is generally bounded by Stuart Street to the north, Folsom Street on the east, Market Street on the west, and 3rd Street to the south. As of June 30, 2020, four annexations have occurred in CFD No. 2014-1. The types of facilities to be funded by special tax revenues generally include streetscape and pedestrian improvements, transit and other transportation improvements, public open space, and other transit center district public improvements. The Mello-Roos Community Facilities Act of 1982 The reduction in property tax revenue that resulted from the passage of Proposition 13 in 1978 required public agencies and real estate developers to look for other means to fund public infrastructure. The funding available from traditional assessment districts was limited by certain requirements of the assessment acts, and it became clear that a more flexible funding tool was needed. In response, the California State Legislature approved the Mello-Roos Community Facilities Act of 1982 (the “Act”), which provides for the levy of a special tax within a defined geographic area, namely a community facilities district, if such a levy is approved by two-thirds of the qualified electors in the area. Community facilities districts can generate funding for a broad range of facilities, and special taxes can be allocated to property in any reasonable manner other than on an ad valorem basis. A community facilities district is authorized to issue tax-exempt bonds that are secured by land within the district. If a parcel does not pay the special tax levied on it, a public agency can foreclose on the parcel and use the proceeds of the foreclosure sale to ensure that bondholders receive interest and principal payments on the bonds. Because bonds issued by a community facilities district are land-secured, there is no risk to a public agency’s general fund or taxing capacity. In addition, because the bonds are tax-exempt, they typically carry an interest rate that is lower than conventional construction financing.

City and County of San Francisco 2 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

II. PURPOSE OF REPORT This CFD Tax Administration Report (the “Report”) presents findings from research and financial analysis performed by Goodwin Consulting Group, Inc. to determine the fiscal year 2020-21 special tax levy for CFD No. 2014-1. The Report is intended to provide information to interested parties regarding CFD No. 2014-1, including the current financial obligations of the CFD and special taxes to be levied in fiscal year 2020-21. The Report also summarizes development activity as well as other pertinent information (e.g., prepayments) for CFD No. 2014-1. The Report is organized into the following sections:

• Section III identifies the financial obligations of CFD No. 2014-1 for fiscal year 2020-21. • Section IV provides a summary of the methodology that is used to apportion the special

tax among parcels in the CFD.

• Section V summarizes the status of development within the CFD.

• Section VI identifies parcels, if any, that have prepaid their special tax obligation.

• Section VII provides a summary of state reporting requirements.

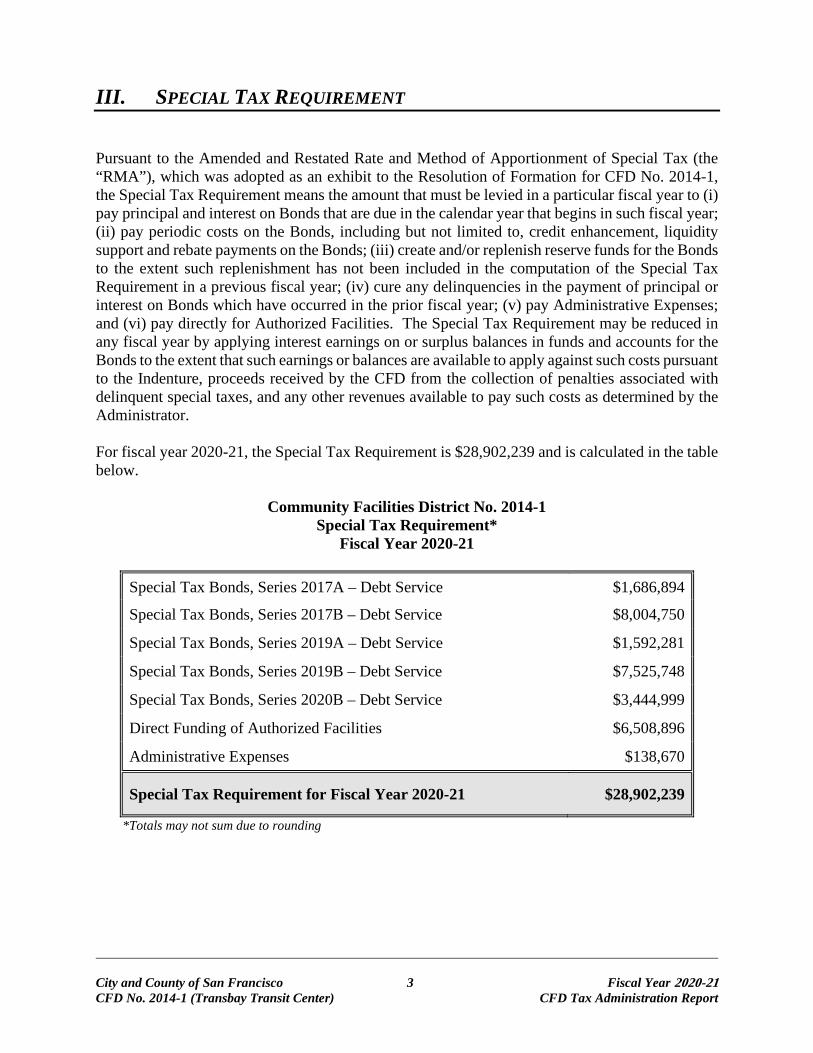

City and County of San Francisco 3 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

III. SPECIAL TAX REQUIREMENT Pursuant to the Amended and Restated Rate and Method of Apportionment of Special Tax (the “RMA”), which was adopted as an exhibit to the Resolution of Formation for CFD No. 2014-1, the Special Tax Requirement means the amount that must be levied in a particular fiscal year to (i) pay principal and interest on Bonds that are due in the calendar year that begins in such fiscal year; (ii) pay periodic costs on the Bonds, including but not limited to, credit enhancement, liquidity support and rebate payments on the Bonds; (iii) create and/or replenish reserve funds for the Bonds to the extent such replenishment has not been included in the computation of the Special Tax Requirement in a previous fiscal year; (iv) cure any delinquencies in the payment of principal or interest on Bonds which have occurred in the prior fiscal year; (v) pay Administrative Expenses; and (vi) pay directly for Authorized Facilities. The Special Tax Requirement may be reduced in any fiscal year by applying interest earnings on or surplus balances in funds and accounts for the Bonds to the extent that such earnings or balances are available to apply against such costs pursuant to the Indenture, proceeds received by the CFD from the collection of penalties associated with delinquent special taxes, and any other revenues available to pay such costs as determined by the Administrator. For fiscal year 2020-21, the Special Tax Requirement is $28,902,239 and is calculated in the table below.

Community Facilities District No. 2014-1 Special Tax Requirement*

Fiscal Year 2020-21

Special Tax Bonds, Series 2017A – Debt Service $1,686,894

Special Tax Bonds, Series 2017B – Debt Service $8,004,750

Special Tax Bonds, Series 2019A – Debt Service $1,592,281

Special Tax Bonds, Series 2019B – Debt Service $7,525,748

Special Tax Bonds, Series 2020B – Debt Service $3,444,999

Direct Funding of Authorized Facilities $6,508,896

Administrative Expenses $138,670

Special Tax Requirement for Fiscal Year 2020-21 $28,902,239

*Totals may not sum due to rounding

City and County of San Francisco 4 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

IV. SPECIAL TAX LEVY Special Tax Categories Special taxes within CFD No. 2014-1 are levied pursuant to the methodology set forth in the RMA. Among other things, the RMA establishes various special tax categories against which the special tax may be levied, the maximum special tax rates, and the methodology by which the special tax is applied. On or after July 1 of each Fiscal Year, the Administrator shall identify the current Assessor’s Parcel numbers for all Taxable Parcels in the CFD. In order to identify Taxable Parcels, the Administrator shall confirm which Buildings in the CFD have been issued both a Tax Commencement Authorization and a COO. The Administrator shall also work with the Zoning Authority to confirm: (i) the Building Height for each Taxable Building, (ii) the For-Sale Residential Square Footage, Rental Residential Square Footage, Office/Hotel Square Footage, and Retail Square Footage on each Taxable Parcel, (iii) if applicable, the number of BMR Units and aggregate Square Footage of BMR Units within the Building, (iv) whether any of the Square Footage on a Parcel is subject to a Certificate of Exemption, and (v) the Special Tax Requirement for the Fiscal Year. (Unless otherwise indicated, capitalized terms shall have the same meaning set forth in the RMA, which is included in Appendix D of this Report.) Maximum Special Tax Rates The base special tax rates and maximum special tax rates applicable to each Taxable Parcel in CFD No. 2014-1 are set forth in Section C of the RMA. The base special tax rates shall be used to calculate the maximum special tax for each Taxable Parcel in a Taxable Building for the first fiscal year in which the building is a Taxable Building. Appendix A of this Report contains a full summary of the base special tax rates for fiscal year 2020-21. The percentage of the maximum special tax rates that will be levied on each land use category in fiscal year 2020-21 are determined by the method of apportionment included in Section E of the RMA. The table in Appendix B identifies the fiscal year 2020-21 maximum special taxes and actual special taxes for CFD No. 2014-1.

Apportionment of Special Taxes The amount of special tax that is apportioned to each parcel is determined through application of Section E of the RMA. Once the Special Tax Requirement for the fiscal year is determined, the following step determines the amount of special tax each property will be taxed. Each fiscal year, the special tax shall be levied proportionately on each Taxable Parcel up to 100% of the maximum special tax for each parcel for such fiscal year until the amount levied on each Taxable Parcels is equal to the Special Tax Requirement. The special tax roll, which identifies the special tax to be levied against each parcel in CFD No. 2014-1 in fiscal year 2020-21, is provided in Appendix C.

City and County of San Francisco 5 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

V. DEVELOPMENT STATUS As of June 30, 2020, there are nine Conditioned Projects that have issued Tax Commencement Authorizations, for the fiscal year 2020-21 special tax levy. Based on the current status of development in CFD No. 2014-1, the following table summarizes the amount of taxable square footage by land use:

Community Facilities District No. 2014-1 Land Uses Within Taxable Parcels

Fiscal Year 2020-21

Land Use Square Feet

For-Sale Residential Square Footage 632,527 Square Feet

Rental Residential Square Footage 1,033,993 Square Feet

Office Square Footage 2,650,625 Square Feet

Hotel Square Footage 0 Square Feet

Retail Square Footage 63,411 Square Feet

City and County of San Francisco 6 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

VI. PREPAYMENTS As of June 30, 2020, no property owner in CFD No. 2014-1 has prepaid his/her special tax obligation; therefore, all parcels of taxable property are subject to the special tax levy for fiscal year 2020-21 pursuant to the RMA.

City and County of San Francisco 7 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

VII. STATE REPORTING REQUIREMENTS Senate Bill No. 165 On September 18, 2000, former Governor Gray Davis signed Senate Bill 165 which enacted the Local Agency Special Tax and Bond Accountability Act. In approving the bill, the Legislature declared that local agencies need to demonstrate to the voters that special taxes and bond proceeds are being spent on the facilities and services for which they were intended. To further this objective, the Legislature added Sections 50075.3 and 53411 to the California Government Code setting forth annual reporting requirements relative to special taxes collected and bonds issued by a local public agency. Pursuant to the Sections 50075.3 and 53411, the “chief fiscal officer” of the public agency will, by January 1, 2002, and at least once a year thereafter, file a report with the City setting forth (i) the amount of special taxes that have been collected and expended; (ii) the status of any project required or authorized to be funded by the special taxes; (iii) if bonds have been issued, the amount of bonds that have been collected and expended; and (iv) if bonds have been issued, the status of any project required or authorized to be funded from bond proceeds. Assembly Bill No. 1666

On July 25, 2016, Governor Jerry Brown signed Assembly Bill No. 1666, adding Section 53343.2 to the California Government Code (“GC”). The bill enhances the transparency of community facilities districts by requiring that certain reports be accessible on a local agency’s web site. Pursuant to Section 53343.2, a local agency that has a web site shall, within seven months after the last day of each fiscal year of the district, display prominently on its web site the following information: Item (a): A copy of an annual report, if requested, pursuant to GC Section 53343.1. The report required by Section 53343.1 includes CFD budgetary information for the prior fiscal year and is only prepared by a community facilities district at the request of a person who resides in or owns property in the community facilities district. If the annual report has not been requested to be prepared, then a posting to the web site would not be necessary. Item (b): A copy of the report provided to the California Debt and Investment Advisory Commission (“CDIAC”) pursuant to GC Section 53359.5. Under Section 53359.5, local agencies must provide CDIAC with the following: (i) notice of proposed sale of bonds; (ii) annual reports on the fiscal status of bonded districts; and (iii) notice of any failure to pay debt service on bonds, or of any draw on a reserve fund to pay debt service on bonds. Item (c): A copy of the report provided to the State Controller’s Office pursuant to GC Section 12463.2. This section refers to the parcel tax portion of a local agency’s Financial Transactions Report that is prepared for the State Controller’s Office annually. Note that school districts are not subject to the reporting required by GC Section 12463.2.

City and County of San Francisco 8 Fiscal Year 2020-21 CFD No. 2014-1 (Transbay Transit Center) CFD Tax Administration Report

Assembly Bill No. 1483 On October 9, 2019, Governor Gavin Newsom signed Assembly Bill No. 1483, adding Section 65940.1 to the California Government Code. The law requires that a city, county, or special district that has an internet website, maintain on its website a current schedule of fees, exactions, and affordability requirements imposed by the public agency on all housing development projects. Pursuant to Section 65940.1, the definition of an exaction includes a special tax levied pursuant to the Mello-Roos Community Facilities Act. Assembly Bill No. 1483 defines a housing development project as consisting of (a) residential units only; or (b) mixed-use developments consisting of residential and non-residential land uses with at least two-thirds of the square footage designated for residential use; or (c) transitional housing or supportive housing. Assembly Bill No. 1483 also requires a city, county, or special district to update this information on their website within 30 days of any changes made to the information.

APPENDIX A

Fiscal Year 2020-21 Base Special Tax Rates

For Sale Rental Office/Residential Residential Hotel Retail

Building Square Square Square Square Height Footage Footage Footage Footage

1 - 5 Stories $6.20 $5.83 $4.54 $4.186 - 10 Stories $6.61 $6.05 $4.68 $4.18

11 - 15 Stories $8.07 $6.12 $5.30 $4.1816 - 20 Stories $8.42 $6.16 $5.45 $4.1821 - 25 Stories $8.70 $6.22 $5.59 $4.1826 - 30 Stories $8.90 $6.29 $5.74 $4.1831 - 35 Stories $9.05 $6.36 $5.88 $4.1836 - 40 Stories $9.21 $6.41 $6.03 $4.1841 - 45 Stories $9.36 $6.47 $6.17 $4.1846 - 50 Stories $9.54 $6.55 $6.32 $4.18

> 50 Stories $9.69 $6.62 $6.46 $4.18

Source: Goodwin Consulting Group, Inc.

Fiscal Year 2020-21 Base Special Taxes

per Square Foot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)

APPENDIX B

Summary of Fiscal Year 2020-21 Special Tax Levy

FY 2020-21 FY 2020-21Maximum Actual

Special SpecialLand Use Category Tax Levy Tax Levy

For-Sale Residential 632,527 sq. ft. $5,899,653 $5,899,653Rental Residential 1,033,993 sq. ft. $6,436,334 $6,436,334Office 2,650,625 sq. ft. $16,308,216 $16,308,216Hotel 0 sq. ft. $0 $0Retail 63,411 sq. ft. $258,036 $258,036

Total Fiscal Year 2020-21 Special Tax Levy $28,902,239

Goodwin Consulting Group, Inc.

Footage

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy Summary

Square

APPENDIX C

Fiscal Year 2020-21 Special Tax Levy for Individual Assessor’s Parcels

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special Tax

3710 - 017 350 Mission $269,795 $269,7953718 - 027 Block 5 -- --3718 - 038 Block 5 -- --3718 - 039 Block 5 -- --3718 - 040 Block 5 $4,611,464 $4,611,4643719 - 450 181 Fremont $2,706,018 $2,706,0183719 - 452 181 Fremont $4,658 $4,6583719 - 453 181 Fremont $3,754 $3,7543719 - 454 181 Fremont $5,636 $5,6363719 - 455 181 Fremont $6,652 $6,6523719 - 456 181 Fremont $7,323 $7,3233719 - 457 181 Fremont $6,987 $6,9873719 - 458 181 Fremont $5,254 $5,2543719 - 459 181 Fremont $5,860 $5,8603719 - 460 181 Fremont $6,186 $6,1863719 - 461 181 Fremont $5,403 $5,4033719 - 462 181 Fremont $5,329 $5,3293719 - 463 181 Fremont $6,335 $6,3353719 - 464 181 Fremont $18,959 $18,9593719 - 465 181 Fremont $21,148 $21,1483719 - 466 181 Fremont $14,953 $14,9533719 - 467 181 Fremont $17,189 $17,1893719 - 468 181 Fremont $18,735 $18,7353719 - 469 181 Fremont $20,775 $20,7753719 - 470 181 Fremont $14,953 $14,9533719 - 471 181 Fremont $17,012 $17,0123719 - 472 181 Fremont $18,474 $18,4743719 - 473 181 Fremont $20,431 $20,4313719 - 474 181 Fremont $14,953 $14,9533719 - 475 181 Fremont $16,797 $16,7973719 - 476 181 Fremont $18,176 $18,1763719 - 477 181 Fremont $20,058 $20,0583719 - 478 181 Fremont $14,953 $14,9533719 - 479 181 Fremont $16,592 $16,5923719 - 480 181 Fremont $17,850 $17,8503719 - 481 181 Fremont $19,564 $19,5643719 - 482 181 Fremont $14,953 $14,9533719 - 483 181 Fremont $16,285 $16,2853719 - 484 181 Fremont $18,549 $18,5493719 - 485 181 Fremont $22,238 $22,2383719 - 486 181 Fremont $11,832 $11,8323719 - 487 181 Fremont $15,502 $15,5023719 - 488 181 Fremont $18,279 $18,2793719 - 489 181 Fremont $21,837 $21,8373719 - 490 181 Fremont $11,832 $11,8323719 - 491 181 Fremont $15,307 $15,3073719 - 492 181 Fremont $18,008 $18,0083719 - 493 181 Fremont $21,362 $21,3623719 - 494 181 Fremont $11,832 $11,8323719 - 495 181 Fremont $15,176 $15,1763719 - 496 181 Fremont $17,729 $17,729

Block and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

Page 1 of 6

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special TaxBlock and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

3719 - 497 181 Fremont $20,822 $20,8223719 - 498 181 Fremont $11,832 $11,8323719 - 499 181 Fremont $15,111 $15,1113719 - 500 181 Fremont $17,291 $17,2913719 - 501 181 Fremont $20,356 $20,3563719 - 502 181 Fremont $11,832 $11,8323719 - 503 181 Fremont $14,738 $14,7383719 - 504 181 Fremont $17,170 $17,1703719 - 505 181 Fremont $19,862 $19,8623719 - 506 181 Fremont $11,832 $11,8323719 - 507 181 Fremont $14,533 $14,5333719 - 508 181 Fremont $22,564 $22,5643719 - 509 181 Fremont $23,934 $23,9343719 - 510 181 Fremont $16,378 $16,3783719 - 511 181 Fremont $22,369 $22,3693719 - 512 181 Fremont $23,254 $23,2543719 - 513 181 Fremont $16,276 $16,2763719 - 514 181 Fremont $31,806 $31,8063719 - 515 181 Fremont $30,464 $30,4643719 - 516 181 Fremont $31,489 $31,4893719 - 517 181 Fremont $30,082 $30,0823719 - 518 181 Fremont $64,665 $64,6653720 - 009 Salesforce Tower $8,811,740 $8,811,7403721 - 016 Parcel F -- --3721 - 134 Parcel F -- --3721 - 135 Parcel F -- --3721 - 136 Parcel F -- --3721 - 137 Parcel F -- --3721 - 138 Parcel F -- --3736 - 190 41 Tehama $1,448,331 $1,448,331

3736A - 001 Block 9 $888,182 $888,1823736A - 002 Block 9 -- --3736A - 003 Block 9 $7,750 $7,7503736A - 004 Block 9 $5,407 $5,4073736A - 005 Block 9 $10,604 $10,6043736A - 006 Block 9 -- --3736A - 007 Block 9 -- --3736A - 008 Block 9 -- --3736A - 009 Block 9 -- --3736A - 010 Block 9 -- --3736A - 011 Block 9 -- --3736A - 012 Block 9 -- --3736A - 013 Block 9 -- --3736A - 014 Block 9 -- --3736A - 015 Block 9 -- --3736A - 016 Block 9 -- --3736A - 017 Block 9 -- --3736A - 018 Block 9 -- --3736A - 019 Block 9 -- --3736A - 020 Block 9 -- --3736A - 021 Block 9 -- --

Page 2 of 6

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special TaxBlock and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

3736A - 022 Block 9 -- --3736A - 023 Block 9 -- --3736A - 024 Block 9 -- --3736A - 025 Block 9 -- --3736A - 026 Block 9 -- --3736A - 027 Block 9 -- --3736A - 028 Block 9 -- --3736A - 029 Block 9 -- --3736A - 030 Block 9 -- --3736A - 031 Block 9 -- --3736A - 032 Block 9 -- --3736A - 033 Block 9 -- --3736A - 034 Block 9 -- --3736A - 035 Block 9 -- --3736A - 036 Block 9 -- --3736A - 037 Block 9 -- --3736A - 038 Block 9 -- --3736A - 039 Block 9 -- --3736A - 040 Block 9 -- --3736A - 041 Block 9 -- --3736A - 042 Block 9 -- --3736A - 043 Block 9 -- --3736A - 044 Block 9 -- --3736A - 045 Block 9 -- --3736A - 046 Block 9 -- --3736A - 047 Block 9 -- --3736A - 048 Block 9 -- --3736A - 049 Block 9 -- --3736A - 050 Block 9 -- --3736A - 051 Block 9 -- --3736A - 052 Block 9 -- --3736A - 053 Block 9 -- --3736A - 054 Block 9 -- --3736A - 055 Block 9 -- --3736A - 056 Block 9 -- --3736A - 057 Block 9 -- --3736A - 058 Block 9 -- --3736A - 059 Block 9 -- --3736A - 060 Block 9 -- --3736A - 061 Block 9 -- --3736A - 062 Block 9 -- --3736A - 063 Block 9 -- --3736A - 064 Block 9 -- --3736A - 065 Block 9 -- --3736A - 066 Block 9 -- --3736A - 067 Block 9 -- --3736A - 068 Block 9 -- --3736A - 069 Block 9 -- --3736A - 070 Block 9 -- --3736A - 071 Block 9 -- --3736A - 072 Block 9 -- --

Page 3 of 6

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special TaxBlock and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

3736A - 073 Block 9 $1,162,068 $1,162,0683737 - 041 Exempt -- --3737 - 042 Block 8 $1,242,293 $1,242,2933737 - 044 Block 8 $4,207 $4,2073737 - 045 Block 8 -- --3737 - 046 Block 8 -- --3737 - 047 Block 8 -- --3737 - 048 Block 8 -- --3737 - 049 Block 8 $349 $3493737 - 050 Block 8 $1,276 $1,2763737 - 051 Block 8 $5,245 $5,2453737 - 052 Block 8 $5,241 $5,2413737 - 053 Block 8 $7,108 $7,1083737 - 054 Block 8 $4,350 $4,3503737 - 055 Block 8 $4,350 $4,3503737 - 056 Block 8 $20,903 $20,9033737 - 057 Block 8 $20,899 $20,8993737 - 058 Block 8 $8,692 $8,6923737 - 059 Block 8 $14,818 $14,8183737 - 060 Block 8 $16,148 $16,1483737 - 061 Block 8 $19,501 $19,5013737 - 062 Block 8 $18,029 $18,0293737 - 063 Block 8 $8,692 $8,6923737 - 064 Block 8 $14,666 $14,6663737 - 065 Block 8 $15,949 $15,9493737 - 066 Block 8 $9,157 $9,1573737 - 067 Block 8 $19,501 $19,5013737 - 068 Block 8 $18,029 $18,0293737 - 069 Block 8 $8,673 $8,6733737 - 070 Block 8 $14,685 $14,6853737 - 071 Block 8 $15,949 $15,9493737 - 072 Block 8 $9,157 $9,1573737 - 073 Block 8 $20,898 $20,8983737 - 074 Block 8 $18,029 $18,0293737 - 075 Block 8 $8,673 $8,6733737 - 076 Block 8 $14,685 $14,6853737 - 077 Block 8 $15,892 $15,8923737 - 078 Block 8 $10,601 $10,6013737 - 079 Block 8 $20,850 $20,8503737 - 080 Block 8 $18,058 $18,0583737 - 081 Block 8 $8,701 $8,7013737 - 082 Block 8 $14,666 $14,6663737 - 083 Block 8 $15,892 $15,8923737 - 084 Block 8 $11,864 $11,8643737 - 085 Block 8 $20,850 $20,8503737 - 086 Block 8 $18,058 $18,0583737 - 087 Block 8 $8,701 $8,7013737 - 088 Block 8 $14,666 $14,6663737 - 089 Block 8 $15,892 $15,8923737 - 090 Block 8 $11,864 $11,8643737 - 091 Block 8 $18,371 $18,371

Page 4 of 6

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special TaxBlock and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

3737 - 092 Block 8 $17,934 $17,9343737 - 093 Block 8 $8,749 $8,7493737 - 094 Block 8 $14,714 $14,7143737 - 095 Block 8 $15,692 $15,6923737 - 096 Block 8 $10,848 $10,8483737 - 097 Block 8 $18,371 $18,3713737 - 098 Block 8 $17,934 $17,9343737 - 099 Block 8 $8,749 $8,7493737 - 100 Block 8 $14,714 $14,7143737 - 101 Block 8 $15,692 $15,6923737 - 102 Block 8 $10,848 $10,8483737 - 103 Block 8 $18,371 $18,3713737 - 104 Block 8 $17,934 $17,9343737 - 105 Block 8 $8,749 $8,7493737 - 106 Block 8 $14,714 $14,7143737 - 107 Block 8 $15,692 $15,6923737 - 108 Block 8 $10,848 $10,8483737 - 109 Block 8 $18,371 $18,3713737 - 110 Block 8 $17,934 $17,9343737 - 111 Block 8 $8,749 $8,7493737 - 112 Block 8 $14,714 $14,7143737 - 113 Block 8 $15,692 $15,6923737 - 114 Block 8 $10,848 $10,8483737 - 115 Block 8 $18,371 $18,3713737 - 116 Block 8 $17,934 $17,9343737 - 117 Block 8 $8,749 $8,7493737 - 118 Block 8 $14,714 $14,7143737 - 119 Block 8 $15,692 $15,6923737 - 120 Block 8 $10,848 $10,8483737 - 121 Block 8 $18,371 $18,3713737 - 122 Block 8 $17,934 $17,9343737 - 123 Block 8 $8,749 $8,7493737 - 124 Block 8 $14,714 $14,7143737 - 125 Block 8 $15,692 $15,6923737 - 126 Block 8 $10,848 $10,8483737 - 127 Block 8 $18,371 $18,3713737 - 128 Block 8 $17,934 $17,9343737 - 129 Block 8 $8,749 $8,7493737 - 130 Block 8 $14,714 $14,7143737 - 131 Block 8 $15,692 $15,6923737 - 132 Block 8 $10,848 $10,8483737 - 133 Block 8 $20,508 $20,5083737 - 134 Block 8 $19,606 $19,6063737 - 135 Block 8 $17,402 $17,4023737 - 136 Block 8 $9,376 $9,3763737 - 137 Block 8 $17,203 $17,2033737 - 138 Block 8 $20,508 $20,5083737 - 139 Block 8 $19,606 $19,6063737 - 140 Block 8 $17,402 $17,4023737 - 141 Block 8 $9,376 $9,3763737 - 142 Block 8 $17,203 $17,203

Page 5 of 6

FY 2020-21 FY 2020-21Maximum Actual

Project Name Special Tax Special TaxBlock and Lot

City and County of San FranciscoCommunity Facilities District No. 2014-1

(Transbay Transit Center)Fiscal Year 2020-21 Special Tax Levy

3737 - 143 Block 8 $20,508 $20,5083737 - 144 Block 8 $19,606 $19,6063737 - 145 Block 8 $17,402 $17,4023737 - 146 Block 8 $9,376 $9,3763737 - 147 Block 8 $17,203 $17,2033737 - 148 Block 8 $20,508 $20,5083737 - 149 Block 8 $19,606 $19,6063737 - 150 Block 8 $17,402 $17,4023737 - 151 Block 8 $9,376 $9,3763737 - 152 Block 8 $17,203 $17,2033737 - 153 Block 8 $20,508 $20,5083737 - 154 Block 8 $19,606 $19,6063737 - 155 Block 8 $17,402 $17,4023737 - 156 Block 8 $9,376 $9,3763737 - 157 Block 8 $17,203 $17,2033737 - 158 Block 8 $20,508 $20,5083737 - 159 Block 8 $19,606 $19,6063737 - 160 Block 8 $17,402 $17,4023737 - 161 Block 8 $9,376 $9,3763737 - 162 Block 8 $17,203 $17,2033737 - 163 Block 8 $20,508 $20,5083737 - 164 Block 8 $19,606 $19,6063737 - 165 Block 8 $17,402 $17,4023737 - 166 Block 8 $9,376 $9,3763737 - 167 Block 8 $17,203 $17,2033737 - 168 Block 8 $39,668 $39,6683737 - 169 Block 8 $40,960 $40,9603737 - 170 Block 8 $39,668 $39,6683737 - 171 Block 8 $40,960 $40,9603737 - 172 Block 8 $39,668 $39,6683737 - 173 Block 8 $40,960 $40,9603737 - 174 Block 8 $39,611 $39,6113737 - 175 Block 8 $40,960 $40,9603738 - 016 Block 6 $1,722,319 $1,722,3193738 - 017 Exempt -- --3738 - 018 Block 7 -- --3739 - 008 Block 4 -- --3740 - 027 Block 1 $1,778,325 $1,778,3253740 - 029 Block 1 $170,338 $170,3383740 - 030 Block 1 $451,963 $451,9633740 - 031 Block 1 $408,810 $408,8103740 - 032 Block 1 $6,814 $6,8143741 - 045 75 Howard -- --

Total Special Tax Levy for Fiscal Year 2020-21 $28,902,239

Goodwin Consulting Group, Inc.

Page 6 of 6

APPENDIX D

Amended and Restated Rate and Method of Apportionment of Special Tax

San Francisco CFD No. 2014-1 1 September 5, 2014

EXHIBIT B

CITY AND COUNTY OF SAN FRANCISCO COMMUNITY FACILITIES DISTRICT NO. 2014-1

(TRANSBAY TRANSIT CENTER)

AMENDED AND RESTATED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX A Special Tax applicable to each Taxable Parcel in the City and County of San Francisco Community Facilities District No. 2014-1 (Transbay Transit Center) shall be levied and collected according to the tax liability determined by the Administrator through the application of the appropriate amount or rate for Square Footage within Taxable Buildings, as described below. All Taxable Parcels in the CFD shall be taxed for the purposes, to the extent, and in the manner herein provided, including property subsequently annexed to the CFD unless a separate Rate and Method of Apportionment of Special Tax is adopted for the annexation area. A. DEFINITIONS The terms hereinafter set forth have the following meanings: “Act” means the Mello-Roos Community Facilities Act of 1982, as amended, being Chapter 2.5, (commencing with Section 53311), Division 2 of Title 5 of the California Government Code. “Administrative Expenses” means any or all of the following: the fees and expenses of any fiscal agent or trustee (including any fees or expenses of its counsel) employed in connection with any Bonds, and the expenses of the City and TJPA carrying out duties with respect to CFD No. 2014-1 and the Bonds, including, but not limited to, levying and collecting the Special Tax, the fees and expenses of legal counsel, charges levied by the City Controller’s Office and/or the City Treasurer and Tax Collector’s Office, costs related to property owner inquiries regarding the Special Tax, costs associated with appeals or requests for interpretation associated with the Special Tax and this RMA, amounts needed to pay rebate to the federal government with respect to the Bonds, costs associated with complying with any continuing disclosure requirements for the Bonds and the Special Tax, costs associated with foreclosure and collection of delinquent Special Taxes, and all other costs and expenses of the City and TJPA in any way related to the establishment or administration of the CFD. “Administrator” means the Director of the Office of Public Finance who shall be responsible for administering the Special Tax according to this RMA. “Affordable Housing Project” means a residential or primarily residential project, as determined by the Zoning Authority, within which all Residential Units are Below Market Rate Units. All Land Uses within an Affordable Housing Project are exempt from the Special Tax, as provided in Section G and are subject to the limitations set forth in Section D.4 below.

San Francisco CFD No. 2014-1 2 September 5, 2014

“Airspace Parcel” means a parcel with an assigned Assessor’s Parcel number that constitutes vertical space of an underlying land parcel. “Apartment Building” means a residential or mixed-use Building within which none of the Residential Units have been sold to individual homebuyers. “Assessor’s Parcel” or “Parcel” means a lot or parcel, including an Airspace Parcel, shown on an Assessor’s Parcel Map with an assigned Assessor’s Parcel number. “Assessor’s Parcel Map” means an official map of the County Assessor designating Parcels by Assessor’s Parcel number.

“Authorized Facilities” means those public facilities authorized to be funded by the CFD as set forth in the CFD formation proceedings. “Base Special Tax” means the Special Tax per square foot that is used to calculate the Maximum Special Tax that applies to a Taxable Parcel pursuant to Sections C.1 and C.2 of this RMA. The Base Special Tax shall also be used to determine the Maximum Special Tax for any Net New Square Footage added to a Taxable Building in the CFD in future Fiscal Years. “Below Market Rate Units” or “BMR Units” means all Residential Units within the CFD that have a deed restriction recorded on title of the property that (i) limits the rental price or sales price of the Residential Unit, (ii) limits the appreciation that can be realized by the owner of such unit, or (iii) in any other way restricts the current or future value of the unit. “Board” means the Board of Supervisors of the City, acting as the legislative body of CFD No. 2014-1. “Bonds” means bonds or other debt (as defined in the Act), whether in one or more series, issued, incurred, or assumed by the CFD related to the Authorized Facilities. “Building” means a permanent enclosed structure that is, or is part of, a Conditioned Project. “Building Height” means the number of Stories in a Taxable Building, which shall be determined based on the highest Story that is occupied by a Land Use. If only a portion of a Building is a Conditioned Project, the Building Height shall be determined based on the highest Story that is occupied by a Land Use regardless of where in the Building the Taxable Parcels are located. If there is any question as to the Building Height of any Taxable Building in the CFD, the Administrator shall coordinate with the Zoning Authority to make the determination. “Certificate of Exemption” means a certificate issued to the then-current record owner of a Parcel that indicates that some or all of the Square Footage on the Parcel has prepaid the Special Tax obligation or has paid the Special Tax for thirty Fiscal Years and, therefore, such Square Footage shall, in all future Fiscal Years, be exempt from the levy of Special Taxes in the CFD. The Certificate of Exemption shall identify (i) the Assessor’s Parcel number(s) for the Parcel(s)

San Francisco CFD No. 2014-1 3 September 5, 2014

on which the Square Footage is located, (ii) the amount of Square Footage for which the exemption is being granted, (iii) the first and last Fiscal Year in which the Special Tax had been levied on the Square Footage, and (iv) the date of receipt of a prepayment of the Special Tax obligation, if applicable. “Certificate of Occupancy” or “COO” means the first certificate, including any temporary certificate of occupancy, issued by the City to confirm that a Building or a portion of a Building has met all of the building codes and can be occupied for residential and/or non-residential use. For purposes of this RMA, “Certificate of Occupancy” shall not include any certificate of occupancy that was issued prior to January 1, 2013 for a Building within the CFD; however, any subsequent certificates of occupancy that are issued for new construction or expansion of the Building shall be deemed a Certificate of Occupancy and the associated Parcel(s) shall be categorized as Taxable Parcels if the Building is, or is part of, a Conditioned Project and a Tax Commencement Letter has been provided to the Administrator for the Building. “CFD” or “CFD No. 2014-1” means the City and County of San Francisco Community Facilities District No. 2014-1 (Transbay Transit Center). “Child Care Square Footage” means, collectively, the Exempt Child Care Square Footage and Taxable Child Care Square Footage within a Taxable Building in the CFD. “City” means the City and County of San Francisco. “Conditioned Project” means a Development Project that is required to participate in funding Authorized Facilities through the CFD. “Converted Apartment Building” means a Taxable Building that had been designated as an Apartment Building within which one or more Residential Units are subsequently sold to a buyer that is not a Landlord. “Converted For-Sale Unit” means, in any Fiscal Year, an individual Market Rate Unit within a Converted Apartment Building for which an escrow has closed, on or prior to June 30 of the preceding Fiscal Year, in a sale to a buyer that is not a Landlord. “County” means the City and County of San Francisco. “CPC” means the Capital Planning Committee of the City and County of San Francisco, or if the Capital Planning Committee no longer exists, “CPC” shall mean the designated staff member(s) within the City and/or TJPA that will recommend issuance of Tax Commencement Authorizations for Conditioned Projects within the CFD. “Development Project” means a residential, non-residential, or mixed-use development that includes one or more Buildings, or portions thereof, that are planned and entitled in a single application to the City.

San Francisco CFD No. 2014-1 4 September 5, 2014

“Exempt Child Care Square Footage” means Square Footage within a Taxable Building that, at the time of issuance of a COO, is determined by the Zoning Authority to be reserved for one or more licensed child care facilities. If a prepayment is made in association with any Taxable Child Care Square Footage, such Square Footage shall also be deemed Exempt Child Care Square Footage beginning in the Fiscal Year following receipt of the prepayment. “Exempt Parking Square Footage” means the Square Footage of parking within a Taxable Building that, pursuant to Sections 151.1 and 204.5 of the Planning Code, is estimated to be needed to serve Land Uses within a building in the CFD, as determined by the Zoning Authority. If a prepayment is made in association with any Taxable Parking Square Footage, such Square Footage shall also be deemed Exempt Parking Square Footage beginning in the Fiscal Year following receipt of the prepayment. “Fiscal Year” means the period starting July 1 and ending on the following June 30. “For-Sale Residential Square Footage” or “For-Sale Residential Square Foot” means Square Footage that is or is expected to be part of a For-Sale Unit. The Zoning Authority shall make the determination as to the For-Sale Residential Square Footage within a Taxable Building in the CFD. For-Sale Residential Square Foot means a single square-foot unit of For-Sale Residential Square Footage. “For-Sale Unit” means (i) in a Taxable Building that is not a Converted Apartment Building: a Market Rate Unit that has been, or is available or expected to be, sold, and (ii) in a Converted Apartment Building, a Converted For-Sale Unit. The Administrator shall make the final determination as to whether a Market Rate Unit is a For-Sale Unit or a Rental Unit. “Indenture” means the indenture, fiscal agent agreement, resolution, or other instrument pursuant to which CFD No. 2014-1 Bonds are issued, as modified, amended, and/or supplemented from time to time, and any instrument replacing or supplementing the same. “Initial Annual Adjustment Factor” means, as of July 1 of any Fiscal Year, the Annual Infrastructure Construction Cost Inflation Estimate published by the Office of the City Administrator’s Capital Planning Group and used to calculate the annual adjustment to the City’s development impact fees that took effect as of January 1 of the prior Fiscal Year pursuant to Section 409(b) of the Planning Code, as may be amended from time to time. If changes are made to the office responsible for calculating the annual adjustment, the name of the inflation index, or the date on which the development fee adjustment takes effect, the Administrator shall continue to rely on whatever annual adjustment factor is applied to the City’s development impact fees in order to calculate adjustments to the Base Special Taxes pursuant to Section D.1 below. Notwithstanding the foregoing, the Base Special Taxes shall, in no Fiscal Year, be increased or decreased by more than four percent (4%) of the amount in effect in the prior Fiscal Year. “Initial Square Footage” means, for any Taxable Building in the CFD, the aggregate Square Footage of all Land Uses within the Building, as determined by the Zoning Authority upon issuance of the COO.

San Francisco CFD No. 2014-1 5 September 5, 2014

“IPIC” means the Interagency Plan Implementation Committee, or if the Interagency Plan Implementation Committee no longer exists, “IPIC” shall mean the designated staff member(s) within the City and/or TJPA that will recommend issuance of Tax Commencement Authorizations for Conditioned Projects within the CFD. “Land Use” means residential, office, retail, hotel, parking, or child care use. For purposes of this RMA, the City shall have the final determination of the actual Land Use(s) on any Parcel within the CFD. “Landlord” means an entity that owns at least twenty percent (20%) of the Rental Units within an Apartment Building or Converted Apartment Building. “Market Rate Unit” means a Residential Unit that is not a Below Market Rate Unit. “Maximum Special Tax” means the greatest amount of Special Tax that can be levied on a Taxable Parcel in the CFD in any Fiscal Year, as determined in accordance with Section C below. “Net New Square Footage” means any Square Footage added to a Taxable Building after the Initial Square Footage in the Building has paid Special Taxes in one or more Fiscal Years. “Office/Hotel Square Footage” or “Office/Hotel Square Foot” means Square Footage that is or is expected to be: (i) Square Footage of office space in which professional, banking, insurance, real estate, administrative, or in-office medical or dental activities are conducted, (ii) Square Footage that will be used by any organization, business, or institution for a Land Use that does not meet the definition of For-Sale Residential Square Footage Rental Residential Square Footage, or Retail Square Footage, including space used for cultural, educational, recreational, religious, or social service facilities, (iii) Taxable Child Care Square Footage, (iv) Square Footage in a residential care facility that is staffed by licensed medical professionals, and (v) any other Square Footage within a Taxable Building that does not fall within the definition provided for other Land Uses in this RMA. Notwithstanding the foregoing, street-level retail bank branches, real estate brokerage offices, and other such ground-level uses that are open to the public shall be categorized as Retail Square Footage pursuant to the Planning Code. Office/Hotel Square Foot means a single square-foot unit of Office/Hotel Square Footage. For purposes of this RMA, “Office/Hotel Square Footage” shall also include Square Footage that is or is expected to be part of a non-residential structure that constitutes a place of lodging, providing temporary sleeping accommodations and related facilities. All Square Footage that shares an Assessor’s Parcel number within such a non-residential structure, including Square Footage of restaurants, meeting and convention facilities, gift shops, spas, offices, and other related uses shall be categorized as Office/Hotel Square Footage. If there are separate Assessor’s Parcel numbers for these other uses, the Administrator shall apply the Base Special Tax for Retail Square Footage to determine the Maximum Special Tax for Parcels on which a restaurant, gift shop, spa, or other retail use is located or anticipated, and the Base Special Tax for Office/Hotel Square Footage shall be used to determine the Maximum Special Tax for Parcels on

San Francisco CFD No. 2014-1 6 September 5, 2014

which other uses in the building are located. The Zoning Authority shall make the final determination as to the amount of Office/Hotel Square Footage within a building in the CFD. “Planning Code” means the Planning Code of the City and County of San Francisco, as may be amended from time to time. “Proportionately” means that the ratio of the actual Special Tax levied in any Fiscal Year to the Maximum Special Tax authorized to be levied in that Fiscal Year is equal for all Taxable Parcels. “Rental Residential Square Footage” or “Rental Residential Square Foot” means Square Footage that is or is expected to be used for one or more of the following uses: (i) Rental Units, (ii) any type of group or student housing which provides lodging for a week or more and may or may not have individual cooking facilities, including but not limited to boarding houses, dormitories, housing operated by medical institutions, and single room occupancy units, or (iii) a residential care facility that is not staffed by licensed medical professionals. The Zoning Authority shall make the determination as to the amount of Rental Residential Square Footage within a Taxable Building in the CFD. Rental Residential Square Foot means a single square-foot unit of Rental Residential Square Footage. “Rental Unit” means (i) all Market Rate Units within an Apartment Building, and (ii) all Market Rate Units within a Converted Apartment Building that have yet to be sold to an individual homeowner or investor. “Rental Unit” shall not include any Residential Unit which has been purchased by a homeowner or investor and subsequently offered for rent to the general public. The Administrator shall make the final determination as to whether a Market Rate Unit is a For-Sale Unit or a Rental Unit. “Retail Square Footage” or “Retail Square Foot” means Square Footage that is or, based on the Certificate of Occupancy, will be Square Footage of a commercial establishment that sells general merchandise, hard goods, food and beverage, personal services, and other items directly to consumers, including but not limited to restaurants, bars, entertainment venues, health clubs, laundromats, dry cleaners, repair shops, storage facilities, and parcel delivery shops. In addition, all Taxable Parking Square Footage in a Building, and all street-level retail bank branches, real estate brokerages, and other such ground-level uses that are open to the public, shall be categorized as Retail Square Footage for purposes of calculating the Maximum Special Tax pursuant to Section C below. The Zoning Authority shall make the final determination as to the amount of Retail Square Footage within a Taxable Building in the CFD. Retail Square Foot means a single square-foot unit of Retail Square Footage. “Residential Unit” means an individual townhome, condominium, live/work unit, or apartment within a Building in the CFD. “Residential Use” means (i) any and all Residential Units within a Taxable Building in the CFD, (ii) any type of group or student housing which provides lodging for a week or more and may or may not have individual cooking facilities, including but not limited to boarding houses,

San Francisco CFD No. 2014-1 7 September 5, 2014

dormitories, housing operated by medical institutions, and single room occupancy units, and (iii) a residential care facility that is not staffed by licensed medical professionals. “RMA” means this Rate and Method of Apportionment of Special Tax. “Special Tax” means a special tax levied in any Fiscal Year to pay the Special Tax Requirement. “Special Tax Requirement” means the amount necessary in any Fiscal Year to: (i) pay principal and interest on Bonds that are due in the calendar year that begins in such Fiscal Year; (ii) pay periodic costs on the Bonds, including but not limited to, credit enhancement, liquidity support and rebate payments on the Bonds, (iii) create and/or replenish reserve funds for the Bonds to the extent such replenishment has not been included in the computation of the Special Tax Requirement in a previous Fiscal Year; (iv) cure any delinquencies in the payment of principal or interest on Bonds which have occurred in the prior Fiscal Year; (v) pay Administrative Expenses; and (vi) pay directly for Authorized Facilities. The amounts referred to in clauses (i) and (ii) of the preceding sentence may be reduced in any Fiscal Year by: (i) interest earnings on or surplus balances in funds and accounts for the Bonds to the extent that such earnings or balances are available to apply against such costs pursuant to the Indenture; (ii) in the sole and absolute discretion of the City, proceeds received by the CFD from the collection of penalties associated with delinquent Special Taxes; and (iii) any other revenues available to pay such costs as determined by the Administrator. “Square Footage” means, for any Taxable Building in the CFD, the net saleable or leasable square footage of each Land Use on each Taxable Parcel within the Building, as determined by the Zoning Authority. If a building permit is issued to increase the Square Footage on any Taxable Parcel, the Administrator shall, in the first Fiscal Year after the final building permit inspection has been conducted in association with such expansion, work with the Zoning Authority to recalculate (i) the Square Footage of each Land Use on each Taxable Parcel, and (ii) the Maximum Special Tax for each Taxable Parcel based on the increased Square Footage. The final determination of Square Footage for each Land Use on each Taxable Parcel shall be made by the Zoning Authority. “Story” or “Stories” means a portion or portions of a Building, except a mezzanine as defined in the City Building Code, included between the surface of any floor and the surface of the next floor above it, or if there is no floor above it, then the space between the surface of the floor and the ceiling next above it. “Taxable Building” means, in any Fiscal Year, any Building within the CFD that is, or is part of, a Conditioned Project, and for which a Certificate of Occupancy was issued and a Tax Commencement Authorization was received by the Administrator on or prior to June 30 of the preceding Fiscal Year. If only a portion of the Building is a Conditioned Project, as determined by the Zoning Authority, that portion of the Building shall be treated as a Taxable Building for purposes of this RMA.

San Francisco CFD No. 2014-1 8 September 5, 2014

“Tax Commencement Authorization” means a written authorization issued by the Administrator upon the recommendations of the IPIC and CPC in order to initiate the levy of the Special Tax on a Conditioned Project that has been issued a COO. “Taxable Child Care Square Footage” means the amount of Square Footage determined by subtracting the Exempt Child Care Square Footage within a Taxable Building from the total net leasable square footage within a Building that is used for licensed child care facilities, as determined by the Zoning Authority. “Taxable Parcel” means, within a Taxable Building, any Parcel that is not exempt from the Special Tax pursuant to law or Section G below. If, in any Fiscal Year, a Special Tax is levied on only Net New Square Footage in a Taxable Building, only the Parcel(s) on which the Net New Square Footage is located shall be Taxable Parcel(s) for purposes of calculating and levying the Special Tax pursuant to this RMA. “Taxable Parking Square Footage” means Square Footage of parking in a Taxable Building that is determined by the Zoning Authority not to be Exempt Parking Square Footage. “TJPA” means the Transbay Joint Powers Authority. “Zoning Authority” means either the City Zoning Administrator, the Executive Director of the San Francisco Office of Community Investment and Infrastructure, or an alternate designee from the agency or department responsible for the approvals and entitlements of a project in the CFD. If there is any doubt as to the responsible party, the Administrator shall coordinate with the City Zoning Administrator to determine the appropriate party to serve as the Zoning Authority for purposes of this RMA. B. DATA FOR CFD ADMINISTRATION On or after July 1 of each Fiscal Year, the Administrator shall identify the current Assessor’s Parcel numbers for all Taxable Parcels in the CFD. In order to identify Taxable Parcels, the Administrator shall confirm which Buildings in the CFD have been issued both a Tax Commencement Authorization and a COO. The Administrator shall also work with the Zoning Authority to confirm: (i) the Building Height for each Taxable Building , (ii) the For-Sale Residential Square Footage, Rental Residential Square Footage, Office/Hotel Square Footage, and Retail Square Footage on each Taxable Parcel, (iii) if applicable, the number of BMR Units and aggregate Square Footage of BMR Units within the Building, (iv) whether any of the Square Footage on a Parcel is subject to a Certificate of Exemption, and (v) the Special Tax Requirement for the Fiscal Year. In each Fiscal Year, the Administrator shall also keep track of how many Fiscal Years the Special Tax has been levied on each Parcel within the CFD. If there is Initial Square Footage and Net New Square Footage on a Parcel, the Administrator shall separately track the duration of the Special Tax levy in order to ensure compliance with Section F below.

San Francisco CFD No. 2014-1 9 September 5, 2014

In any Fiscal Year, if it is determined by the Administrator that (i) a parcel map or condominium plan for a portion of property in the CFD was recorded after January 1 of the prior Fiscal Year (or any other date after which the Assessor will not incorporate the newly-created parcels into the then current tax roll), and (ii) the Assessor does not yet recognize the newly-created parcels, the Administrator shall calculate the Special Tax that applies separately to each newly-created parcel, then applying the sum of the individual Special Taxes to the Assessor’s Parcel that was subdivided by recordation of the parcel map or condominium plan. C. DETERMINATION OF THE MAXIMUM SPECIAL TAX 1. Base Special Tax Once the Building Height of, and Land Use(s) within, a Taxable Building have been identified, the Base Special Tax to be used for calculation of the Maximum Special Tax for each Taxable Parcel within the Building shall be determined based on reference to the applicable table(s) below:

FOR-SALE RESIDENTIAL SQUARE FOOTAGE

Building Height

Base Special Tax Fiscal Year 2013-14*

1 – 5 Stories $4.71 per For-Sale Residential Square Foot 6 – 10 Stories $5.02 per For-Sale Residential Square Foot 11 – 15 Stories $6.13 per For-Sale Residential Square Foot 16 – 20 Stories $6.40 per For-Sale Residential Square Foot 21 – 25 Stories $6.61 per For-Sale Residential Square Foot 26 – 30 Stories $6.76 per For-Sale Residential Square Foot 31 – 35 Stories $6.88 per For-Sale Residential Square Foot 36 – 40 Stories $7.00 per For-Sale Residential Square Foot 41 – 45 Stories $7.11 per For Sale Residential Square Foot 46 – 50 Stories $7.25 per For-Sale Residential Square Foot

More than 50 Stories $7.36 per For-Sale Residential Square Foot

San Francisco CFD No. 2014-1 10 September 5, 2014

RENTAL RESIDENTIAL SQUARE FOOTAGE

Building Height

Base Special Tax Fiscal Year 2013-14*

1 – 5 Stories $4.43 per Rental Residential Square Foot 6 – 10 Stories $4.60 per Rental Residential Square Foot 11 – 15 Stories $4.65 per Rental Residential Square Foot 16 – 20 Stories $4.68 per Rental Residential Square Foot 21 – 25 Stories $4.73 per Rental Residential Square Foot 26 – 30 Stories $4.78 per Rental Residential Square Foot 31 – 35 Stories $4.83 per Rental Residential Square Foot 36 – 40 Stories $4.87 per Rental Residential Square Foot 41 – 45 Stories $4.92 per Rental Residential Square Foot 46 – 50 Stories $4.98 per Rental Residential Square Foot

More than 50 Stories $5.03 per Rental Residential Square Foot

OFFICE/HOTEL SQUARE FOOTAGE

Building Height

Base Special Tax Fiscal Year 2013-14*

1 – 5 Stories $3.45 per Office/Hotel Square Foot 6 – 10 Stories $3.56 per Office/Hotel Square Foot 11 – 15 Stories $4.03 per Office/Hotel Square Foot 16 – 20 Stories $4.14 per Office/Hotel Square Foot 21 – 25 Stories $4.25 per Office/Hotel Square Foot 26 – 30 Stories $4.36 per Office/Hotel Square Foot 31 – 35 Stories $4.47 per Office/Hotel Square Foot 36 – 40 Stories $4.58 per Office/Hotel Square Foot 41 – 45 Stories $4.69 per Office/Hotel Square Foot 46 – 50 Stories $4.80 per Office/Hotel Square Foot

More than 50 Stories $4.91 per Office/Hotel Square Foot

RETAIL SQUARE FOOTAGE

Building Height

Base Special Tax Fiscal Year 2013-14*

N/A $3.18 per Retail Square Foot * The Base Special Tax rates shown above for each Land Use shall escalate as set forth in

Section D.1 below. 2. Determining the Maximum Special Tax for Taxable Parcels Upon issuance of a Tax Commencement Authorization and the first Certificate of Occupancy for a Taxable Building within a Conditioned Project that is not an Affordable Housing Project, the

San Francisco CFD No. 2014-1 11 September 5, 2014

Administrator shall coordinate with the Zoning Authority to determine the Square Footage of each Land Use on each Taxable Parcel. The Administrator shall then apply the following steps to determine the Maximum Special Tax for the next succeeding Fiscal Year for each Taxable Parcel in the Taxable Building: Step 1. Determine the Building Height for the Taxable Building for which a

Certificate of Occupancy was issued. Step 2. Determine the For-Sale Residential Square Footage and/or Rental Residential

Square Footage for all Residential Units on each Taxable Parcel, as well as the Office/Hotel Square Footage and Retail Square Footage on each Taxable Parcel.

Step 3. For each Taxable Parcel that includes only For-Sale Units, multiply the

For-Sale Residential Square Footage by the applicable Base Special Tax from Section C.1 to determine the Maximum Special Tax for the Taxable Parcel.

Step 4. For each Taxable Parcel that includes only Rental Units, multiply the Rental

Residential Square Footage by the applicable Base Special Tax from Section C.1 to determine the Maximum Special Tax for the Taxable Parcel.

Step 5. For each Taxable Parcel that includes only Residential Uses other than

Market Rate Units, net out the Square Footage associated with any BMR Units and multiply the remaining Rental Residential Square Footage (if any) by the applicable Base Special Tax from Section C.1 to determine the Maximum Special Tax for the Taxable Parcel.

Step 6. For each Taxable Parcel that includes only Office/Hotel Square Footage,

multiply the Office/Hotel Square Footage on the Parcel by the applicable Base Special Tax from Section C.1 to determine the Maximum Special Tax for the Taxable Parcel.

Step 7. For each Taxable Parcel that includes only Retail Square Footage, multiply

the Retail Square Footage on the Parcel by the applicable Base Special Tax from Section C.1 to determine the Maximum Special Tax for the Taxable Parcel.

Step 8. For Taxable Parcels that include multiple Land Uses, separately determine

the For-Sale Residential Square Footage, Rental Residential Square Footage, Office/Hotel Square Footage, and/or Retail Square Footage. Multiply the Square Footage of each Land Use by the applicable Base Special Tax from Section C.1, and sum the individual amounts to determine the aggregate Maximum Special Tax for the Taxable Parcel for the first succeeding Fiscal Year.

San Francisco CFD No. 2014-1 12 September 5, 2014

D. CHANGES TO THE MAXIMUM SPECIAL TAX

1. Annual Escalation of Base Special Tax The Base Special Tax rates identified in Section C.1 are applicable for fiscal year 2013-14. Beginning July 1, 2014 and each July 1 thereafter, the Base Special Taxes shall be adjusted by the Initial Annual Adjustment Factor. The Base Special Tax rates shall be used to calculate the Maximum Special Tax for each Taxable Parcel in a Taxable Building for the first Fiscal Year in which the Building is a Taxable Building, as set forth in Section C.2 and subject to the limitations set forth in Section D.3. 2. Adjustment of the Maximum Special Tax After a Maximum Special Tax has been assigned to a Parcel for its first Fiscal Year as a Taxable Parcel pursuant to Section C.2 and Section D.1, the Maximum Special Tax shall escalate for subsequent Fiscal Years beginning July 1 of the Fiscal Year after the first Fiscal Year in which the Parcel was a Taxable Parcel, and each July 1 thereafter, by two percent (2%) of the amount in effect in the prior Fiscal Year. In addition to the foregoing, the Maximum Special Tax assigned to a Taxable Parcel shall be increased in any Fiscal Year in which the Administrator determines that Net New Square Footage was added to the Parcel in the prior Fiscal Year. 3. Converted Apartment Buildings If an Apartment Building in the CFD becomes a Converted Apartment Building, the Administrator shall rely on information from the County Assessor, site visits to the sales office, data provided by the entity that is selling Residential Units within the Building, and any other available source of information to track sales of Residential Units. In the first Fiscal Year in which there is a Converted For-Sale Unit within the Building, the Administrator shall determine the applicable Base Maximum Special Tax for For-Sale Residential Units for that Fiscal Year. Such Base Maximum Special Tax shall be used to calculate the Maximum Special Tax for all Converted For-Sale Units in the Building in that Fiscal Year. In addition, this Base Maximum Special Tax, escalated each Fiscal Year by two percent (2%) of the amount in effect in the prior Fiscal Year, shall be used to calculate the Maximum Special Tax for all future Converted For-Sale Units within the Building. Solely for purposes of calculating Maximum Special Taxes for Converted For-Sale Units within the Converted Apartment Building, the adjustment of Base Maximum Special Taxes set forth in Section D.1 shall not apply. All Rental Residential Square Footage within the Converted Apartment Building shall continue to be subject to the Maximum Special Tax for Rental Residential Square Footage until such time as the units become Converted For-Sale Units. The Maximum Special Tax for all Taxable Parcels within the Building shall escalate each Fiscal Year by two percent (2%) of the amount in effect in the prior Fiscal Year. 4. BMR Unit/Market Rate Unit Transfers

If, in any Fiscal Year, the Administrator determines that a Residential Unit that had previously been designated as a BMR Unit no longer qualifies as such, the Maximum Special Tax on the

San Francisco CFD No. 2014-1 13 September 5, 2014

new Market Rate Unit shall be established pursuant to Section C.2 and adjusted, as applicable, by Sections D.1 and D.2. If a Market Rate Unit becomes a BMR Unit after it has been taxed in prior Fiscal Years as a Market Rate Unit, the Maximum Special Tax on such Residential Unit shall not be decreased unless: (i) a BMR Unit is simultaneously redesignated as a Market Rate Unit, and (ii) such redesignation results in a Maximum Special Tax on the new Market Rate Unit that is greater than or equal to the Maximum Special Tax that was levied on the Market Rate Unit prior to the swap of units. If, based on the Building Height or Square Footage, there would be a reduction in the Maximum Special Tax due to the swap, the Maximum Special Tax that applied to the former Market Rate Unit will be transferred to the new Market Rate Unit regardless of the Building Height and Square Footage associated with the new Market Rate Unit. 5. Changes in Land Use on a Taxable Parcel If any Square Footage that had been taxed as For-Sale Residential Square Footage, Rental Residential Square Footage, Office/Hotel Square Footage, or Retail Square Footage in a prior Fiscal Year is rezoned or otherwise changes Land Use, the Administrator shall apply the applicable subsection in Section C.2 to calculate what the Maximum Special Tax would be for the Parcel based on the new Land Use(s). If the amount determined is greater than the Maximum Special Tax that applied to the Parcel prior to the Land Use change, the Administrator shall increase the Maximum Special Tax to the amount calculated for the new Land Uses. If the amount determined is less than the Maximum Special Tax that applied prior to the Land Use change, there will be no change to the Maximum Special Tax for the Parcel. Under no circumstances shall the Maximum Special Tax on any Taxable Parcel be reduced, regardless of changes in Land Use or Square Footage on the Parcel, including reductions in Square Footage that may occur due to demolition, fire, water damage, or acts of God. In addition, if a Taxable Building within the CFD that had been subject to the levy of Special Taxes in any prior Fiscal Year becomes all or part of an Affordable Housing Project, the Parcel(s) shall continue to be subject to the Maximum Special Tax that had applied to the Parcel(s) before they became part of the Affordable Housing Project. All Maximum Special Taxes determined pursuant to Section C.2 shall be adjusted, as applicable, by Sections D.1 and D.2. 6. Prepayments If a Parcel makes a prepayment pursuant to Section H below, the Administrator shall issue the owner of the Parcel a Certificate of Exemption for the Square Footage that was used to determine the prepayment amount, and no Special Tax shall be levied on the Parcel in future Fiscal Years unless there is Net New Square Footage added to a Building on the Parcel. Thereafter, a Special Tax calculated based solely on the Net New Square Footage on the Parcel shall be levied for up to thirty Fiscal Years, subject to the limitations set forth in Section F below. Notwithstanding the foregoing, any Special Tax that had been levied against, but not yet collected from, the Parcel is still due and payable, and no Certificate of Exemption shall be issued until such amounts are fully paid. If a prepayment is made in order to exempt Taxable Child Care Square Footage on a Parcel on which there are multiple Land Uses, the Maximum Special Tax for the Parcel shall be recalculated based on the exemption of this Child Care Square Footage which shall, after such prepayment, be designated as Exempt Child Care Square Footage and remain exempt in all Fiscal Years after the prepayment has been received.

San Francisco CFD No. 2014-1 14 September 5, 2014

E. METHOD OF LEVY OF THE SPECIAL TAX Each Fiscal Year, the Special Tax shall be levied Proportionately on each Taxable Parcel up to 100% of the Maximum Special Tax for each Parcel for such Fiscal Year until the amount levied on Taxable Parcels is equal to the Special Tax Requirement. F. COLLECTION OF SPECIAL TAX The Special Taxes for CFD No. 2014-1 shall be collected in the same manner and at the same time as ordinary ad valorem property taxes, provided, however, that prepayments are permitted as set forth in Section H below and provided further that the City may directly bill the Special Tax, may collect Special Taxes at a different time or in a different manner, and may collect delinquent Special Taxes through foreclosure or other available methods. The Special Tax shall be levied and collected from the first Fiscal Year in which a Parcel is designated as a Taxable Parcel until the principal and interest on all Bonds have been paid, the City’s costs of constructing or acquiring Authorized Facilities from Special Tax proceeds have been paid, and all Administrative Expenses have been paid or reimbursed. Notwithstanding the foregoing, the Special Tax shall not be levied on any Square Footage in the CFD for more than thirty Fiscal Years, except that a Special Tax that was lawfully levied in or before the final Fiscal Year and that remains delinquent may be collected in subsequent Fiscal Years. After a Building or a particular block of Square Footage within a Building (i.e., Initial Square Footage vs. Net New Square Footage) has paid the Special Tax for thirty Fiscal Years, the then-current record owner of the Parcel(s) on which that Square Footage is located shall be issued a Certificate of Exemption for such Square Footage. Notwithstanding the foregoing, the Special Tax shall cease to be levied, and a Release of Special Tax Lien shall be recorded against all Parcels in the CFD that are still subject to the Special Tax, after the Special Tax has been levied in the CFD for seventy-five Fiscal Years. Pursuant to Section 53321 (d) of the Act, the Special Tax levied against Residential Uses shall under no circumstances increase more than ten percent (10%) as a consequence of delinquency or default by the owner of any other Parcel or Parcels and shall, in no event, exceed the Maximum Special Tax in effect for the Fiscal Year in which the Special Tax is being levied. G. EXEMPTIONS Notwithstanding any other provision of this RMA, no Special Tax shall be levied on: (i) Square Footage for which a prepayment has been received and a Certificate of Exemption issued, (ii) Below Market Rate Units except as otherwise provided in Sections D.3 and D.4, (iii) Affordable Housing Projects, including all Residential Units, Retail Square Footage, and Office Square Footage within buildings that are part of an Affordable Housing Project, except as otherwise provided in Section D.4, and (iv) Exempt Child Care Square Footage.

San Francisco CFD No. 2014-1 15 September 5, 2014

H. PREPAYMENT OF SPECIAL TAX The Special Tax obligation applicable to Square Footage in a building may be fully prepaid as described herein, provided that a prepayment may be made only if (i) the Parcel is a Taxable Parcel, and (ii) there are no delinquent Special Taxes with respect to such Assessor’s Parcel at the time of prepayment. Any prepayment made by a Parcel owner must satisfy the Special Tax obligation associated with all Square Footage on the Parcel that is subject to the Special Tax at the time the prepayment is calculated. An owner of an Assessor’s Parcel intending to prepay the Special Tax obligation shall provide the City with written notice of intent to prepay. Within 30 days of receipt of such written notice, the City or its designee shall notify such owner of the prepayment amount for the Square Footage on such Assessor’s Parcel. Prepayment must be made not less than 75 days prior to any redemption date for Bonds to be redeemed with the proceeds of such prepaid Special Taxes. The Prepayment Amount for a Taxable Parcel shall be calculated as follows:

Step 1: Determine the Square Footage of each Land Use on the Parcel. Step 2: Determine how many Fiscal Years the Square Footage on the Parcel has paid

the Special Tax, which may be a separate total for Initial Square Footage and Net New Square Footage on the Parcel. If a Special Tax has been levied, but not yet paid, in the Fiscal Year in which the prepayment is being calculated, such Fiscal Year will be counted as a year in which the Special Tax was paid, but a Certificate of Exemption shall not be issued until such Special Taxes are received by the City’s Office of the Treasurer and Tax Collector.

Step 3: Subtract the number of Fiscal Years for which the Special Tax has been paid

(as determined in Step 2) from 30 to determine the remaining number of Fiscal Years for which Special Taxes are due from the Square Footage for which the prepayment is being made. This calculation would result in a different remainder for Initial Square Footage and Net New Square Footage within a building.

Step 4: Separately for Initial Square Footage and Net New Square Footage, and

separately for each Land Use on the Parcel, multiply the amount of Square Footage by the applicable Maximum Special Tax that would apply to such Square Footage in each of the remaining Fiscal Years, taking into account the 2% escalator set forth in Section D.2, to determine the annual stream of Maximum Special Taxes that could be collected in future Fiscal Years.

Step 5: For each Parcel for which a prepayment is being made, sum the annual

amounts calculated for each Land Use in Step 4 to determine the annual Maximum Special Tax that could have been levied on the Parcel in each of the remaining Fiscal Years.

San Francisco CFD No. 2014-1 16 September 5, 2014

Step 6. Calculate the net present value of the future annual Maximum Special Taxes that were determined in Step 5 using, as the discount rate for the net present value calculation, the true interest cost (TIC) on the Bonds as identified by the Office of Public Finance. If there is more than one series of Bonds outstanding at the time of the prepayment calculation, the Administrator shall determine the weighted average TIC based on the Bonds from each series that remain outstanding. The amount determined pursuant to this Step 6 is the required prepayment for each Parcel. Notwithstanding the foregoing, if at any point in time the Administrator determines that the Maximum Special Tax revenue that could be collected from Square Footage that remains subject to the Special Tax after the proposed prepayment is less than 110% of debt service on Bonds that will remain outstanding after defeasance or redemption of Bonds from proceeds of the estimated prepayment, the amount of the prepayment shall be increased until the amount of Bonds defeased or redeemed is sufficient to reduce remaining annual debt service to a point at which 110% debt service coverage is realized.

Once a prepayment has been received by the City, a Certificate of Exemption shall be issued to the owner of the Parcel indicating that all Square Footage that was the subject of such prepayment shall be exempt from Special Taxes.

I. INTERPRETATION OF SPECIAL TAX FORMULA The City may interpret, clarify, and revise this RMA to correct any inconsistency, vagueness, or ambiguity, by resolution and/or ordinance, as long as such interpretation, clarification, or revision does not materially affect the levy and collection of the Special Taxes and any security for any Bonds.

J. SPECIAL TAX APPEALS

Any taxpayer who wishes to challenge the accuracy of computation of the Special Tax in any Fiscal Year may file an application with the Administrator. The Administrator, in consultation with the City Attorney, shall promptly review the taxpayer’s application. If the Administrator concludes that the computation of the Special Tax was not correct, the Administrator shall correct the Special Tax levy and, if applicable in any case, a refund shall be granted. If the Administrator concludes that the computation of the Special Tax was correct, then such determination shall be final and conclusive, and the taxpayer shall have no appeal to the Board from the decision of the Administrator. The filing of an application or an appeal shall not relieve the taxpayer of the obligation to pay the Special Tax when due. Nothing in this Section J shall be interpreted to allow a taxpayer to bring a claim that would otherwise be barred by applicable statutes of limitation set forth in the Act or elsewhere in applicable law.

APPENDIX E

Boundary Map of Community Facilities District No. 2014-1

N

1"= 250'

GCGGOODWIN CONSULTING GROUP

SHEET 1 OF 2

State of California

City and County of San Francisco

(Transbay Transit Center)

2. I hereby certify that the within map showing proposed boundaries of

City and County of San Francisco Community Facilities District No.

2013-1 (Transbay Transit Center), State of California, was approved by

the Board of Supervisors of the City and County of San Francisco, at a

meeting thereof, held on the_________day of ___________, 20___, by its Resolution No. _________.

3. Filed this __________day of ______________, 20___, at the hour of

____o'clock___.m, in Book _____________of Maps of Assessment

and Community Facilities Districts at Page __________in the office of

the County Assessor-Recorder in the City and County of San Francisco, State of California.

Community Facilities District No. 2014-1

1. Filed in the office of the Clerk of the Board of Supervisors of the City and County of San Francisco this ___________ day of _______________, 20____.

County Recorder

Clerk of the Board of Supervisors

County Clerk

City and County of San Francisco

Proposed Boundaries of

MARKET STREET

MISSION STREET

HOWARD STREET

FOLSOM STREET

2 ND

STREET

BEALE

STREET

MA

IN STREET

SPEAR

STREET

STEUART

STREET

FREMONT

STREET

1 ST

STREET

FREMONT

STREET

FOLSOM STREET

MINNA STREET

NATOMA STREET

1 ST

STREET

37403739

1

33