Embed Size (px)

Citation preview

COUNTRY REPORT ECID 8 TRAININGCOUNTRY REPORT ECID 8 TRAINING

AOTS, TOKYO KENSHU CENTREAOTS, TOKYO KENSHU CENTRE

TOKYO, JAPANTOKYO, JAPAN

DIRECTORATE GENERAL OF ELECTRICITY

MINISTRY OF ENERGY AND MINERAL RESOURCES

OUTLINE

� Overview of National Electricity Conditions (Current Status)

� Need for Private Power Participation

� Indonesian Power Sector Infrastructure

� Power Generation Current Condition

� Power Generation Development Planning

� Target of Energy Mix for Power Generation

� Opportunity of Investment

Overview of National Electricity Conditions

(Current Status)

� Total installed capacity (2012): 38,063 MW (PLN 76%, IPP 20%, and PPU 4%)

� Current electrification ratio: 72,95%.

� Several areas are facing critical condition (demand > supply)

� Energy mix in power generation: Coal 46%, Gas 26%, Oil 19%, Hydro 7%, Geothermal 2%.

� Power plants under construction (based on RUPTL 2011 – 2020) : PLN 5,372 MW and IPP:

1,505 MW

� Total investment in Power Sector (2011):

– Power Generation : USD 1,644 Million

– Transmission : USD 1,089 Million

– Distribution : USD 317 Million.

SUPPLY CHALLENGES

� Mismatch between primary energy resources versus population

density:

- 80% population located in Java-Bali;

- majority source of primary energy in other islands.

� Dependency on oil as primary energy for electricity generation :

- abundance coal reserve, but many electricity generations still use fuel

oil.

� Lack of supporting infrastructures:

- gas pipe networks;

- coal transportation and distribution;

- electricity transmission networks, especially in outer islands.

� Limited financial budget to develop electricity sector:

- Electrification ratio is still low;

- Funding is needed for the development of additional generation

capacity (crash programs), transmission and distribution networks.

POLICY ON POWER SECTOR DEVELOPMENT

� The electricity business is basically conducted by State and

carried out by state own enterprise (PLN).

� State Own Enterprise should has first right of refusal in

electricity supply.

� Other enterprises (e.g. Regional Own Enterprise (BUMD),

Private sector, Cooperation and Society) could participate

in electricity supply business.

� Electricity business could be conducted for own use or for

public use.

� Continually increase electrification ratio.

� Continuously increase new and renewable energy usage in

primary energy composition for electricity generation.

� Increase the ratio of electrification, 80% in 2014 (currently

67.2%) and continuously implementing short term, medium

and long term programs to overcome the electricity crises in

the provinces

� Improve the investment climate in the power sector. Promote

private power investment in the power sector

� Improve efficiency in the electricity demand and supply side

� Increase the local content (TKDN) in the power sector

� Enforce safety regulations in the power sector

� Encourage energy diversification program shifting away from

oil based sources and the utilization of renewable and more

environmentally friendly energy sources

POLICY ON POWER SECTOR DEVELOPMENT (2)

ELECTRICITY DEVELOPMENT PLAN MEDIUM & LONG TERM

� Transmission

- Java – Sumatera Interconnected;

- Transmission Development in Sumatera, Kalimantan and Sulawesi;

- Interconnection of Sumatera and Malaysia Peninsula;

- Interconnection of West Kalimantan and Serawak.

� Electric Power Generation

- Increase Gas Supply for Power Generation;

- Low Rank Coal Utilization for Power Generation;

- Replacement of Oil Power Plant with Non-Oil Power Plant;

� Increase Electrification Ratio (to reach 93% in 2025).

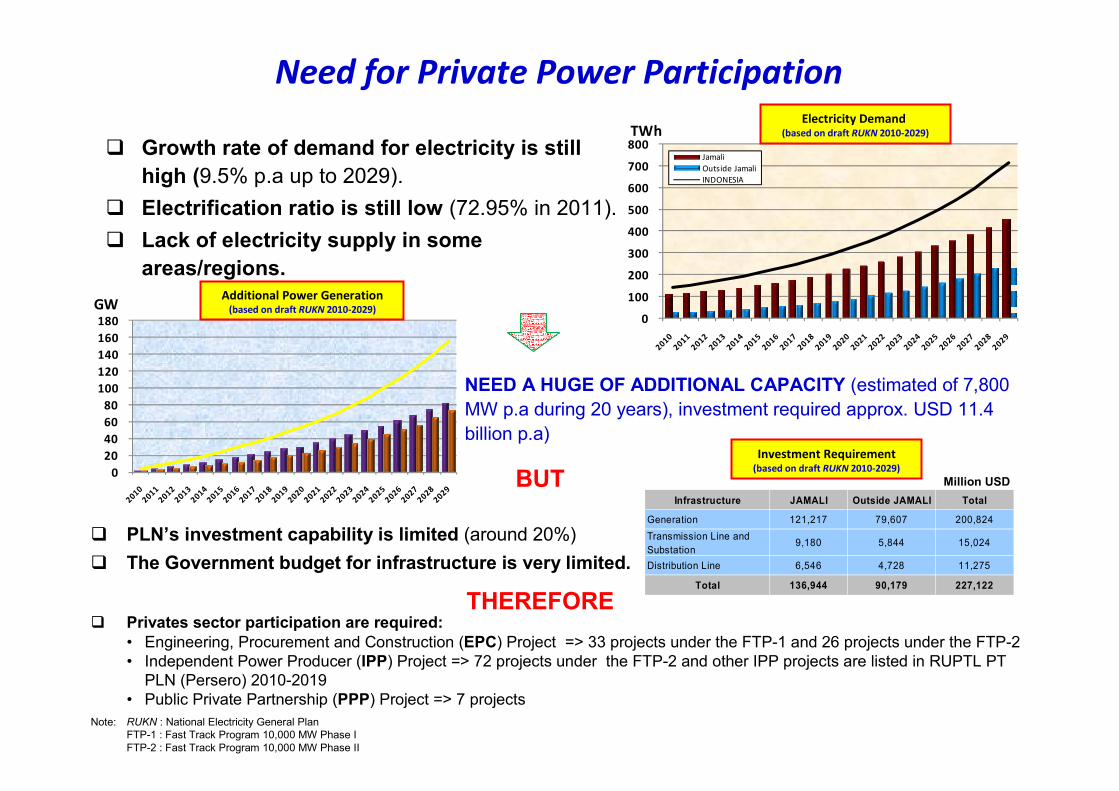

Need for Private Power Participation

� Growth rate of demand for electricity is still

high (9.5% p.a up to 2029).

� Electrification ratio is still low (72.95% in 2011).

� Lack of electricity supply in some

areas/regions.

NEED A HUGE OF ADDITIONAL CAPACITY (estimated of 7,800

MW p.a during 20 years), investment required approx. USD 11.4

billion p.a)

BUT

� PLN’s investment capability is limited (around 20%)

� The Government budget for infrastructure is very limited.

THEREFORE� Privates sector participation are required:

• Engineering, Procurement and Construction (EPC) Project => 33 projects under the FTP-1 and 26 projects under the FTP-2

• Independent Power Producer (IPP) Project => 72 projects under the FTP-2 and other IPP projects are listed in RUPTL PT

PLN (Persero) 2010-2019

• Public Private Partnership (PPP) Project => 7 projects

0

100

200

300

400

500

600

700

800 TWh

Jamali

Outside Jamali

INDONESIA

Electricity Demand (based on draft RUKN 2010-2029)

0

20

40

60

80

100

120

140

160

180

GWAdditional Power Generation

(based on draft RUKN 2010-2029)

Infrastructure JAMALI Outside JAMALI Total

Generation 121,217 79,607 200,824

Transmission Line and

Substation9,180 5,844 15,024

Distribution Line 6,546 4,728 11,275

Total 136,944 90,179 227,122

Investment Requirement(based on draft RUKN 2010-2029)

Million USD

Note: RUKN : National Electricity General Plan

FTP-1 : Fast Track Program 10,000 MW Phase I

FTP-2 : Fast Track Program 10,000 MW Phase II

Indonesian Power Sector Infrastructure

(Current Status) : Transmisi yang sudah ada

: Transmisi yang direncanakan

: Pembangkit Listrik

•• POWER GENERATION CAPACITYPOWER GENERATION CAPACITY : : 338.063 8.063 MWMW•• TRANSMISSION LENGTH :TRANSMISSION LENGTH :-- 500 KV : 500 KV : 4.923 kms4.923 kms-- 275 KV : 275 KV : 9.5059.505 kms kms -- 150 KV : 150 KV : 24.38024.380 kmskms-- 70 KV : 70 KV : 4.7244.724 kmskms

•• DISTRIBUTION LENGTHDISTRIBUTION LENGTH::-- JTM : 2JTM : 2775.613 kms5.613 kms-- JTR : JTR : 406.149 406.149 kmskms

SUMATERA : • Pembangkit: 5.909 MW (16%)• 275 kV : 1.011 kms• 150 kV : 8.382 kms• 70 kV : 332 kms• JTM : 75.382 kms• JTR : 83.827 kms

JAMALI : • Pembangkit: 28.101 MW (74%)• 500 kV : 4.923 kms• 275 kV : 8.494 kms• 150 kV : 12.126 kms• 70 kV : 3.437 kms• JTM : 137.354 kms• JTR : 256.156 kms

Nusa Tenggara:• Pembangkit: 282 MW (1%)• JTM : 7.836 kms• JTR : 7.794 kms

KALIMANTAN : • Pembangkit: 1.602 MW (4%)• 150 kV : 1.568 kms• 70 kV : 123 kms• JTM: 23.487 kms• JTR : 22.540 kms

SULAWESI : • Pembangkit: 1.625 MW (4%)• 150 kV : 2.304 kms• 70 kV : 833 kms• JTM : 24.482 kms• JTR : 29.722 kms

MALUKU :• Pembangkit:233 MW (1%)• JTM : 4.722 kms• JTR : 2.717 kms

PAPUA : • Pembangkit: 311 MW (1%)• JTM : 2.351 kms• JTR : 3.393 kms

10

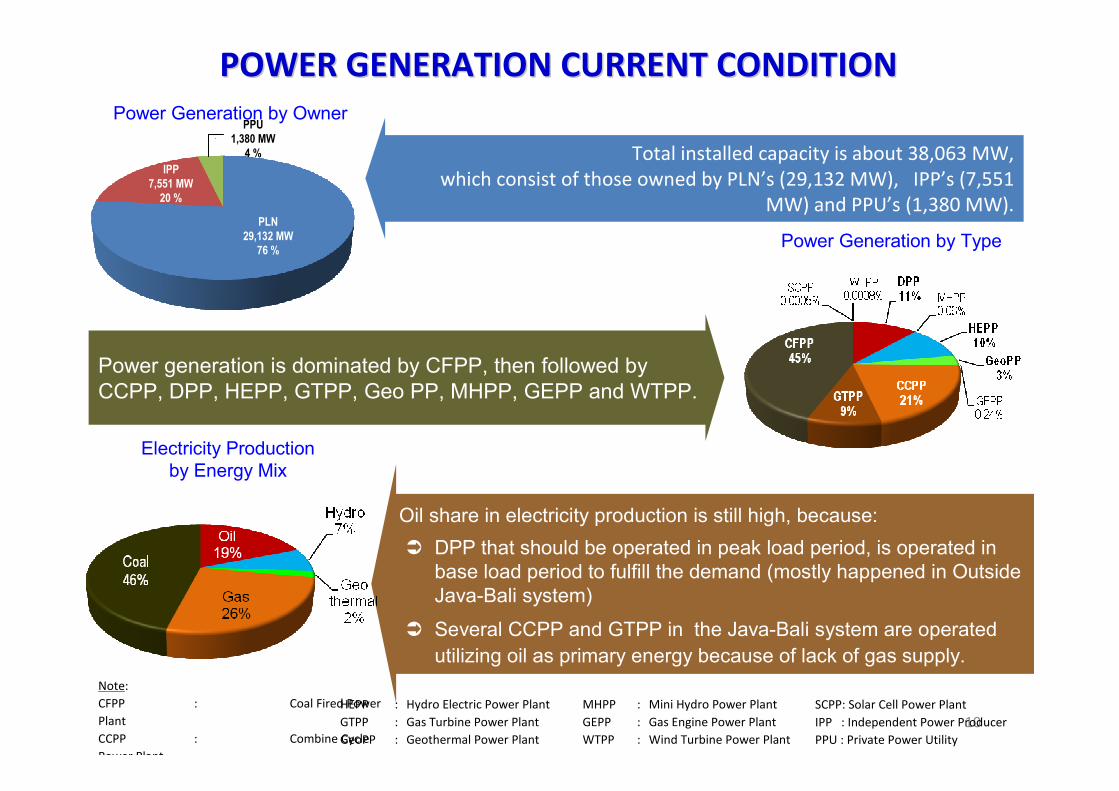

Oil share in electricity production is still high, because:

� DPP that should be operated in peak load period, is operated in

base load period to fulfill the demand (mostly happened in Outside

Java-Bali system)

� Several CCPP and GTPP in the Java-Bali system are operated

utilizing oil as primary energy because of lack of gas supply.

Total installed capacity is about 38,063 MW,

which consist of those owned by PLN’s (29,132 MW), IPP’s (7,551

MW) and PPU’s (1,380 MW).

POWER GENERATION CURRENT CONDITIONPOWER GENERATION CURRENT CONDITION

Power Generation by Owner

Power Generation by Type

Electricity Production

by Energy Mix

Power generation is dominated by CFPP, then followed by

CCPP, DPP, HEPP, GTPP, Geo PP, MHPP, GEPP and WTPP.

Note:

CFPP : Coal Fired Power

Plant

CCPP : Combine Cycle

Power Plant

HEPP : Hydro Electric Power Plant

GTPP : Gas Turbine Power Plant

GeoPP : Geothermal Power Plant

MHPP : Mini Hydro Power Plant

GEPP : Gas Engine Power Plant

WTPP : Wind Turbine Power Plant

SCPP: Solar Cell Power Plant

IPP : Independent Power Producer

PPU : Private Power Utility

PLN

29,132 MW

76 %

IPP

7,551 MW

20 %

PPU

1,380 MW

4 %

� Total power generation that will be developed from 2012 -2020 is about of 50 GW or in

average 5.5GW p.a

� PLN will develop about of 54% of the total capacity and the rest (46%) will be developed by

IPP/private

� Diesel Power Plant will still be developed, but only dedicated to isolated/remote area.

POWER GENERATION DEVELOPMENT PLANING (MW)POWER GENERATION DEVELOPMENT PLANING (MW)

2011 2019

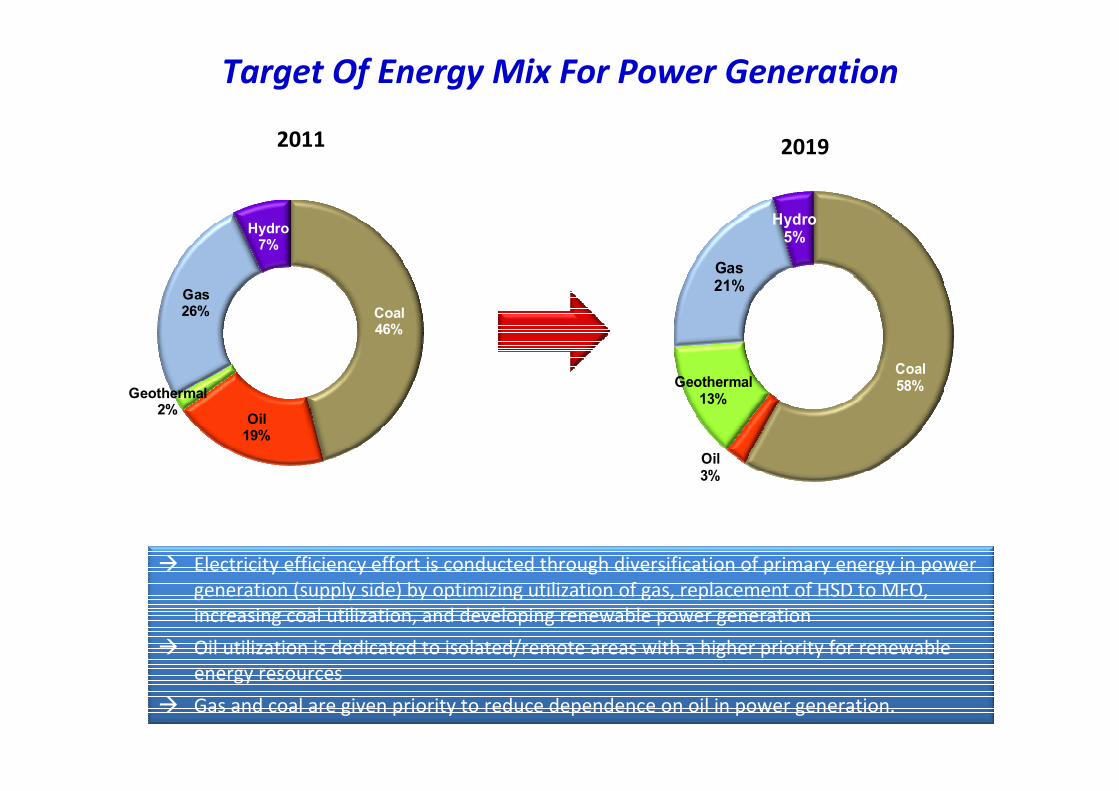

Target Of Energy Mix For Power Generation

Coal46%

Oil19%

Geothermal2%

Gas26%

Hydro7%

Coal58%

Oil3%

Geothermal13%

Gas21%

Hydro5%

� Electricity efficiency effort is conducted through diversification of primary energy in power

generation (supply side) by optimizing utilization of gas, replacement of HSD to MFO,

increasing coal utilization, and developing renewable power generation

� Oil utilization is dedicated to isolated/remote areas with a higher priority for renewable

energy resources

� Gas and coal are given priority to reduce dependence on oil in power generation.

OPPORTUNITY OF INVESTMENT

POWER 2012 2013 2014 2015 2016 2017 2018 2019 2020

Total

(MILLION

USD)

Generation 6.087,7 8.784,4 10.146,7 9.089,9 7.338,9 7.194,1 6.474,4 4.842,7 3.371,3 67.815,7

Transmission 2.531,4 1.701,2 1.907,8 2.389,3 1.375,1 717,6 480,7 331,0 79,8 14.928,0

Distribution 1.269,5 1.172,1 1.253,3 1.166,8 1.320,5 1.395,0 1.477,4 1.539,3 1.605,5 13.461,0

Grand Total 9.888,6 11.657,7 13.307,8 12.646,0 10.034,5 9.306,7 8.432,5 6.713,0 5.056,6 96.204,7

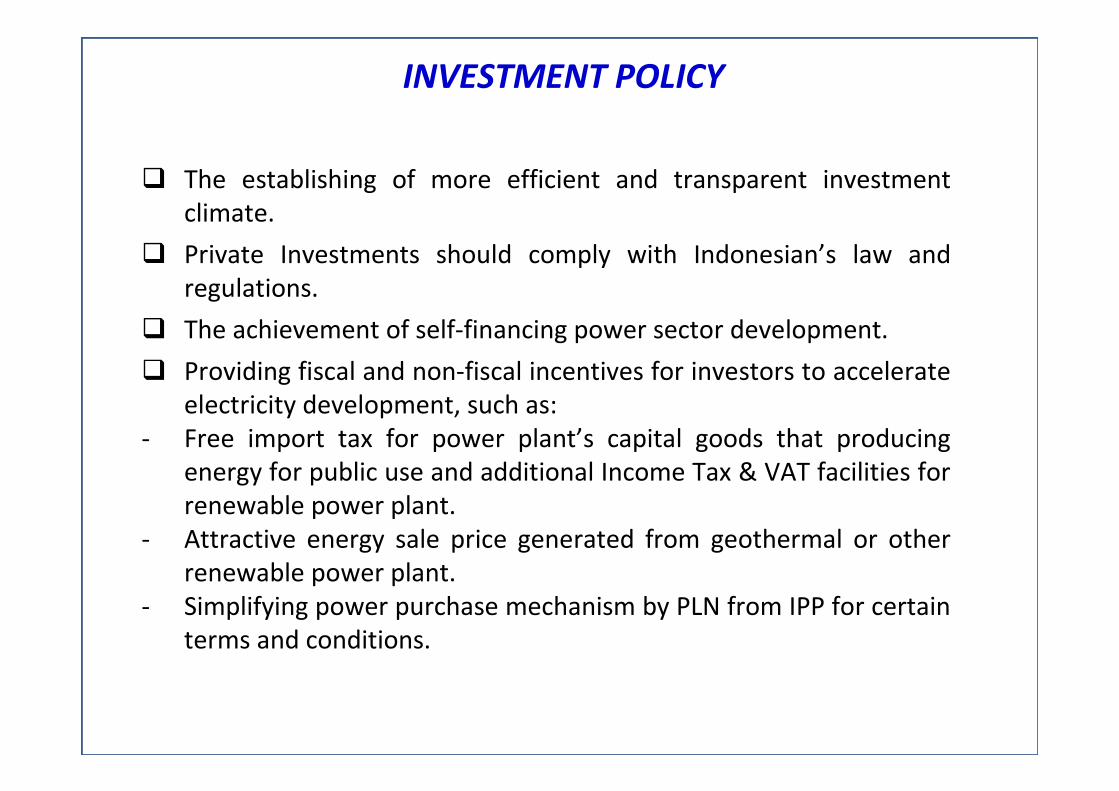

� The establishing of more efficient and transparent investment

climate.

� Private Investments should comply with Indonesian’s law and

regulations.

� The achievement of self-financing power sector development.

� Providing fiscal and non-fiscal incentives for investors to accelerate

electricity development, such as:

- Free import tax for power plant’s capital goods that producing

energy for public use and additional Income Tax & VAT facilities for

renewable power plant.

- Attractive energy sale price generated from geothermal or other

renewable power plant.

- Simplifying power purchase mechanism by PLN from IPP for certain

terms and conditions.

INVESTMENT POLICY

� Phase I

– Accelerated Program Phase I consist of 10.000 MW Coal Fired

Power Plant (37 projects) and approximately 1817 kms

transmission project as PLN’s projects, introduced in 2007.

– As PLN’s project, private sector participation as EPC contractor.

� Phase II

– Government has launched Accelerated Program Phase II (total

capacity approximately 10.000 MW) in the early 2010, consist of

93 power plant projects, with composition based on primary

energy: Hydro 11%, Geothermal 34% , Coal 40%, and , Gas

15%.

– PLN and Private could participate (through EPC or IPP as

well) in the development program.

ACCELERATED PROGRAM

16

Energy Conservation Program

on Electricity Sector 1)

NO PROGRAM DESCRIPTION / PROGRESS

1. Improving transmission and distribution system

� To reduce technical losses

� Currently, total electricity losses is more than 9%

2. Switch off fuel oil for power plant from HSD to MFO, natural gas, coal, geothermal and hydro,

� To reduce production cost of electricity

� To reduce dependency of oil

� To reduce CO2 emission

3 Utilization of advanced technology (cogeneration, clean coal technology, etc)

� To reduce energy consumption

� To reduce CO2 emission

4. Utilization of excess power from captive

Excess power from captive can be sold to PT.PLN

Supply Side

17

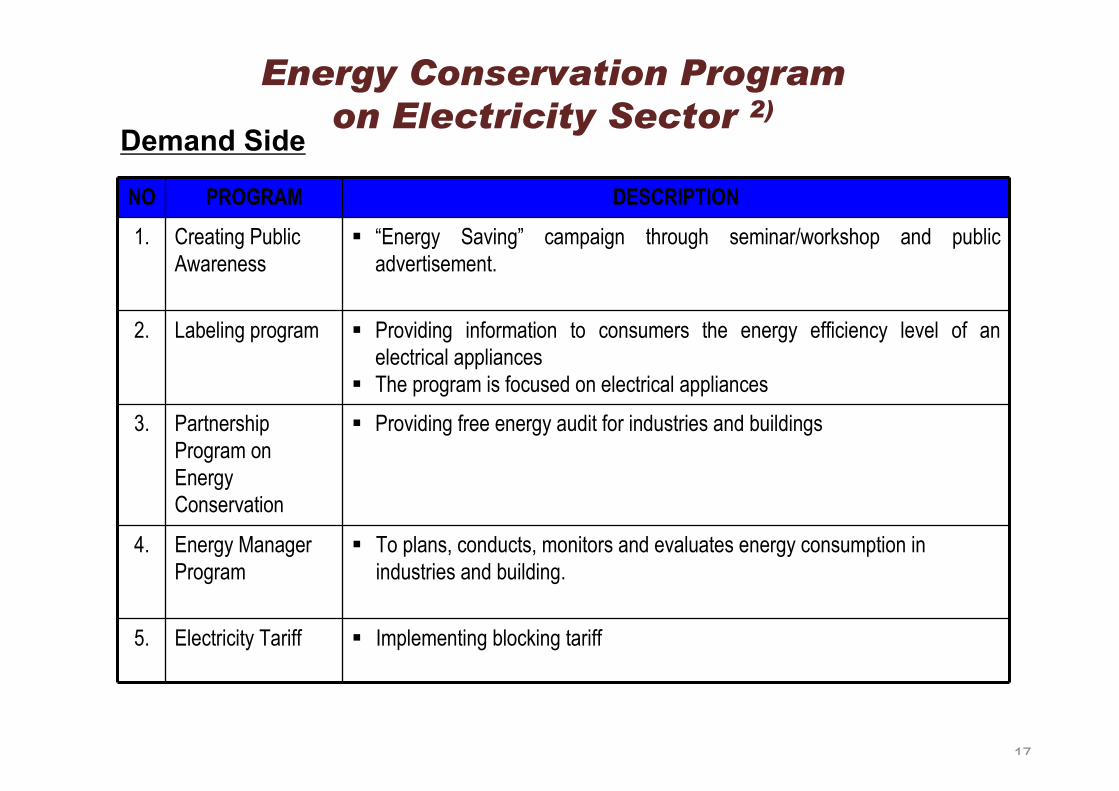

Energy Conservation Program

on Electricity Sector 2)

NO PROGRAM DESCRIPTION

1. Creating Public

Awareness

� “Energy Saving” campaign through seminar/workshop and public

advertisement.

2. Labeling program � Providing information to consumers the energy efficiency level of an

electrical appliances

� The program is focused on electrical appliances

3. Partnership

Program on

Energy

Conservation

� Providing free energy audit for industries and buildings

4. Energy Manager

Program

� To plans, conducts, monitors and evaluates energy consumption in

industries and building.

5. Electricity Tariff � Implementing blocking tariff

Demand Side

ありがとうございましたありがとうございましたありがとうございましたありがとうございました

![[Howto] Setup Local 3GS Restore Verification Server (ECID SHSH)](https://img.dokumen.tips/doc/110x75/577d221d1a28ab4e1e969c57/howto-setup-local-3gs-restore-verification-server-ecid-shsh.jpg)