Embed Size (px)

Citation preview

*«»

COULEE CROCHE FIRE PROTECTIONDISTRICT NO. FOUKCANKTON, LOUISIANA

ANNUAL FINANCIAL REPORTFOR THE YEARS ENDED DECEMBER 31, 2006̂ 0̂ 2005

Under provisions cf stats law, this report is a publicdocument. A copy of the report has been submitted tothe entity and oth&r appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date

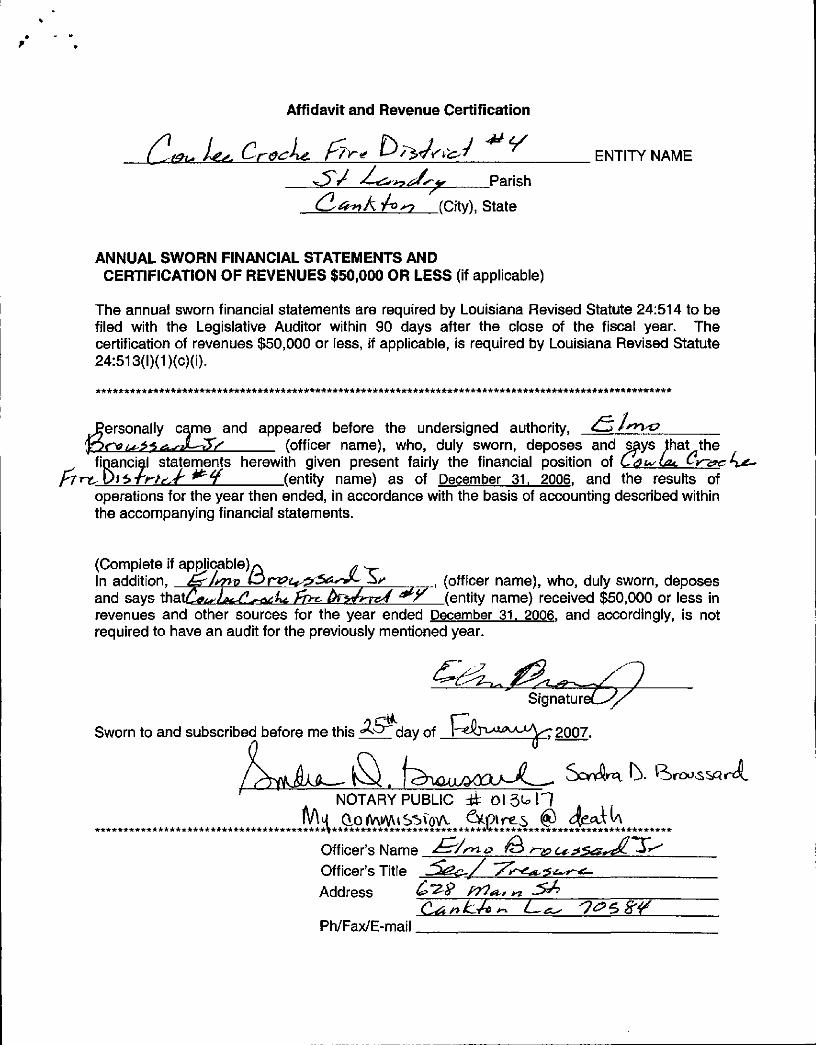

Affidavit and Revenue Certification

X"1 / r I f D^ J -/ ̂ ^

(City). State

ENTITY NAME

Parish

ANNUAL SWORN FINANCIAL STATEMENTS ANDCERTIFICATION OF REVENUES $50,000 OR LESS (if applicable)

The annual sworn financial statements are required by Louisiana Revised Statute 24:514 to befiled with the Legislative Auditor within 90 days after the close of the fiscal year. Thecertification of revenues $50,000 or less, if applicable, is required by Louisiana Revised Statute24:513(l)(1)(c)(i).

ersonally came and appeared before the undersigned authority,^*A^a)L~3V (officer name), who, duly sworn, deposes and says that the

financial statements herewith given present fairly the financial position of C0i*La± Cy-&c/>-?£,/ **^*f (entity name) as of December 31. 2006. and the results of

operations for the year then ended, in accordance with the basis of accounting described withinthe accompanying financial statements.

(Complete if applicable)^In addition, &Jtfr*v & r&i*s>556* x (officer name), who, duly sworn, deposesand says that£*^/A^^~a^ fir*^ br*drrd *^r (entity name) received $50,000 or less inrevenues and other sources for the year ended December 31. 2006. and accordingly, is notrequired to have an audit for the previously mentioned year.

SignatureC /̂

Sworn to and subscribed before me this ̂ °"day of e v ^ ^ ^ 2007.~

b.

NOTARY PUBLIC it

Officer's NameOfficer's Title

Address

Ph/Fax/E-mail

T A B L E O F C O N T E N T S

PAGE

Accountant's Compilation Report 1

Combined Balance Sheet - All Fund Types and Account Groups -December 31, 2006 2

Combined Balance Sheet - All Fund Types and Account Groups -December 31, 2005 3

Statements of Revenues, Expenditures, and Changes in FundBalances - Governmental Fund Type - General Fund -For the Years Ended December 31, 2006 and 2005 4

Statement of Revenues and Expenditures,- Budget and Actual (Non-GAAP Basis) -General Fund - For the Year Ended December 31, 2006 5

Statement of Revenues and Expenditures- Budget and Actual (Non-GAAP Basis) -General Fund - For the Year Ended December 31, 2005 6

Notes to Financial Statements 7-12

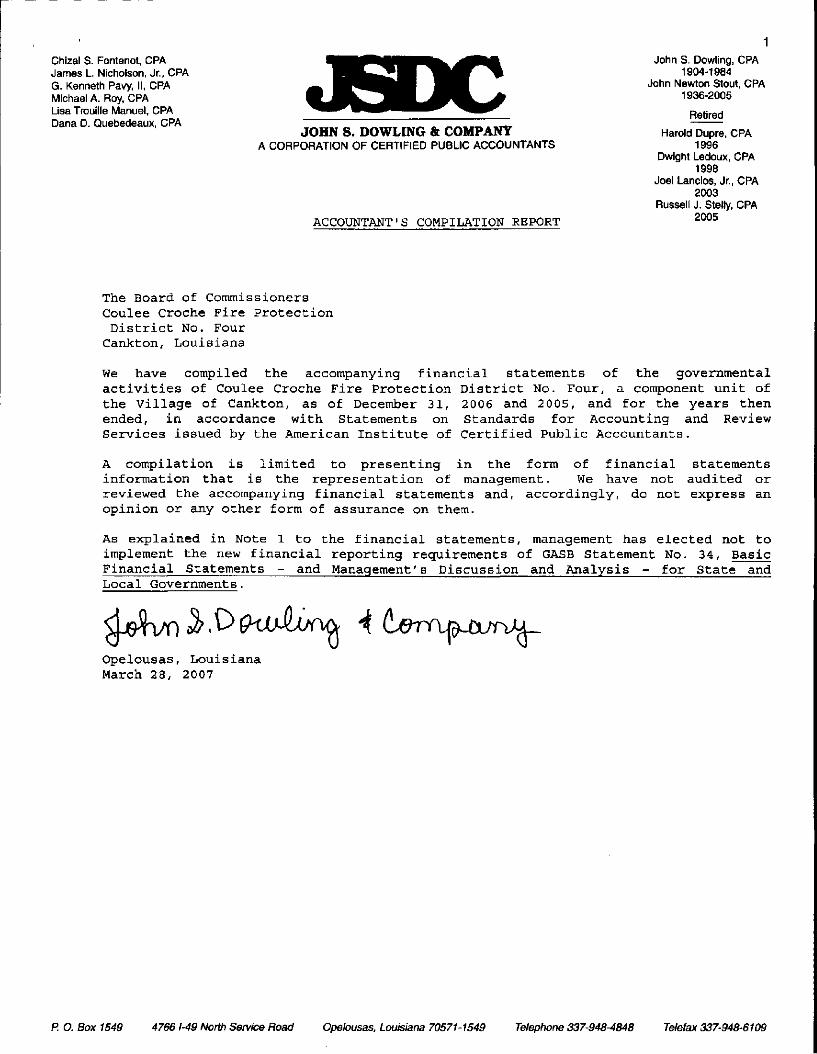

Chizal S. Fontenot, CPAJames L. Nicholson, Jr., CPAG. Kenneth Pavy, II, CPAMichael A. Roy, CPALisa Trouille Manuel, CPADana D. Quebedeaux, CPA

JOHN S. DOWLING & COMPANYA CORPORATION OF CERTIFIED PUBLIC ACCOUNTANTS

ACCOUNTANT'S COMPILATION REPORT

1

John S. Dowling, CPA1904-1984

John Newton Stout, CPA1936-2005

Retired

Harold Dupre, CPA1996

Dwight Ledoux, CPA1998

Joel Lanclos, Jr., CPA2003

Russell J. Stelly, CPA2005

The Board of CommissionersCoulee Croche Fire ProtectionDistrict No. FourCankton, Louisiana

We have compiled the accompanying financial statements of the governmentalactivities of Coulee Croche Fire Protection District No. Four, a component unit ofthe Village of Cankton, as of December 31, 2006 and 2005, and for the years thenended, in accordance with Statements on Standards for Accounting and ReviewServices issued by the American Institute of Certified Public Accountants.

A compilation is limited to presenting in the form of financial statementsinformation that is the representation of management . We have not audited orreviewed the accompanying financial statements and, accordingly, do not express anopinion or any other form of assurance on them.

As explained in Note 1 to the financial statements, management has elected not toimplement the new financial reporting requirements of GASB Statement No. 34, BasicFinancial Statements - and Management's Discussion and Analysis - for State andLocal Governments .

Opelousas , LouisianaMarch 28, 2007

P. O. Box 1549 47661-49 North Service Road Opelousas, Louisiana 70571-1549 Telephone 337-948-4848 Telefax 337-948-6109

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

COMBINED BALANCE SHEET - ALL FUND TYPES AND ACCOUNT GROUPSDECEMBER 31, 2006

GOVERNMENTALFUND TYPEGENERAL

ACCOUNT GROUPGENERALFIXEDASSETS

TOTAL(Memorandum

Only)2006

ASSETS

CashCertificate of depositTaxes receivableLess allowance for doubtfulaccountsProperty and equipment

Total assets

$27,54133,17916,888

(1,351)

76,257

$163,900

163,900

$27,54133,17916,888

(1,351)163,900

240,157

LIABILITIES AND FUND EQUITY

LIABILITIES

FUND EQUITYInvestment in general fixedassetsFund balanceUnreservedUndesignated

Total fund equity

Total liabilities andfund equity

-0-

$76,25776,257

76,257

-0-

$163,900

163,900

163,900

-0-

$163,900

76,257240,157

240,157

See accompanying notes and accountant's report.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

COMBINED BALANCE SHEET - ALL FUND TYPES AND ACCOUNT GROUPSDECEMBER 31, 2005

GOVERNMENTALFUND TYPEGENERAL

ACCOUNT GROUPGENERALFIXEDASSETS

TOTAL(Memorandum

Only)2005

ASSETS

CashCertificate of depositTaxes receivableLess allowance for doubtfulaccountsProperty and equipment

Total assets

$20,40242,40914,715

(1,177)

76,349

$152,162

152,162

$20,40242,40914,715

(1,177)152,162

228^511

LIABILITIES AND FUND EQUITY

LIABILITIES

FUND EQUITYInvestment in general fixedassetsFund balanceUnreservedUndesignated

Total fund equity

Total liabilities andfund equity

-0-

$76,34976,349

76,349

-0-

$152,162

152,162

152,162

-0-

$152,162

76,349228,511

228^511

See accompanying notes and accountant's report.

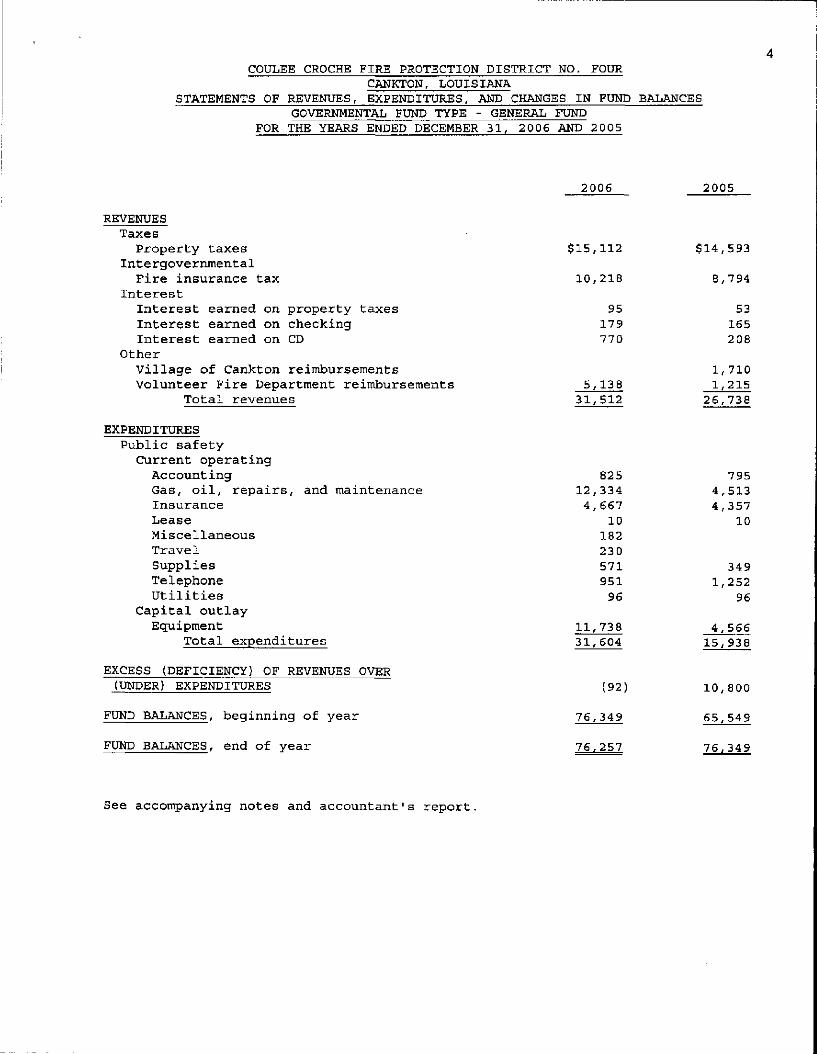

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

STATEMENTS OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCESGOVERNMENTAL FUND TYPE - GENERAL FUND

FOR THE YEARS ENDED DECEMBER 31, 2006 AND 2005

2006 2005

REVENUESTaxesProperty taxes

IntergovernmentalFire insurance tax

InterestInterest earned on property taxesInterest earned on checkingInterest earned on CD

OtherVillage of Cankton reimbursementsVolunteer Fire Department reimbursements

Total revenues

EXPENDITURESPublic safetyCurrent operatingAccountingGas, oil, repairs, and maintenanceInsuranceLeaseMiscellaneousTravelSuppliesTelephoneUtilities

Capital outlayEquipment

Total expenditures

EXCESS (DEFICIENCY) OF REVENUES OVER(UNDER) EXPENDITURES

FUND BALANCES, beginning of year

FUND BALANCES, end of year

$15,112

10,218

95179770

5,13831,512

82512,3344,667

1018223057195196

11,73831,604

(92)

76,349

76,257

$14,593

8,794

53165208

1,7101,215

26,738

7954,5134,357

10

3491,252

96

4,56615,938

10,800

65,549

76,349

See accompanying notes and accountant's report,

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

STATEMENT OF REVENUES AND EXPENDITURESBUDGET AND ACTUAL (NON-GAAP BASIS) - GENERAL FUND

FOR THE YEAR ENDED DECEMBER 31, 2006

GENERAL FUND

REVENUESTaxesProperty taxes

IntergovernmentalFire insurance tax

InterestInterest earned on property taxesInterest earned on checkingInterest earned on CD

OtherVillage of Cankton reimbursementsVolunteer Fire Departmentreimbursements

Total revenues

EXPENDITURESPublic safetyCurrent operatingAccountingGas, oil, repairs, and maintenanceInsuranceLeaseSuppliesTelephoneUtilitiesMiscellaneousTravelCapital outlayEquipment

Total expenditures

EXCESS (DEFICIENCY) OF REVENUESOVER (UNDER) EXPENDITURES

BUDGET

$12,

10,

5,28,

8,4,

15,29,

(1,

590

218

85167659

138857

825054667104695196153

170972

115)

ACTUAL

$13,112

10,218

95179770

5,13829,512

82512,3344,667

1057195196182230

11,73831,604

(2,092)

VARIANCEFAVORABLE

(UNFAVORABLE)

$522

1012111

655

(4,280)

(525)

(29)(230)

3,432(1,632)

(977)

See accompanying notes and accountant's report.

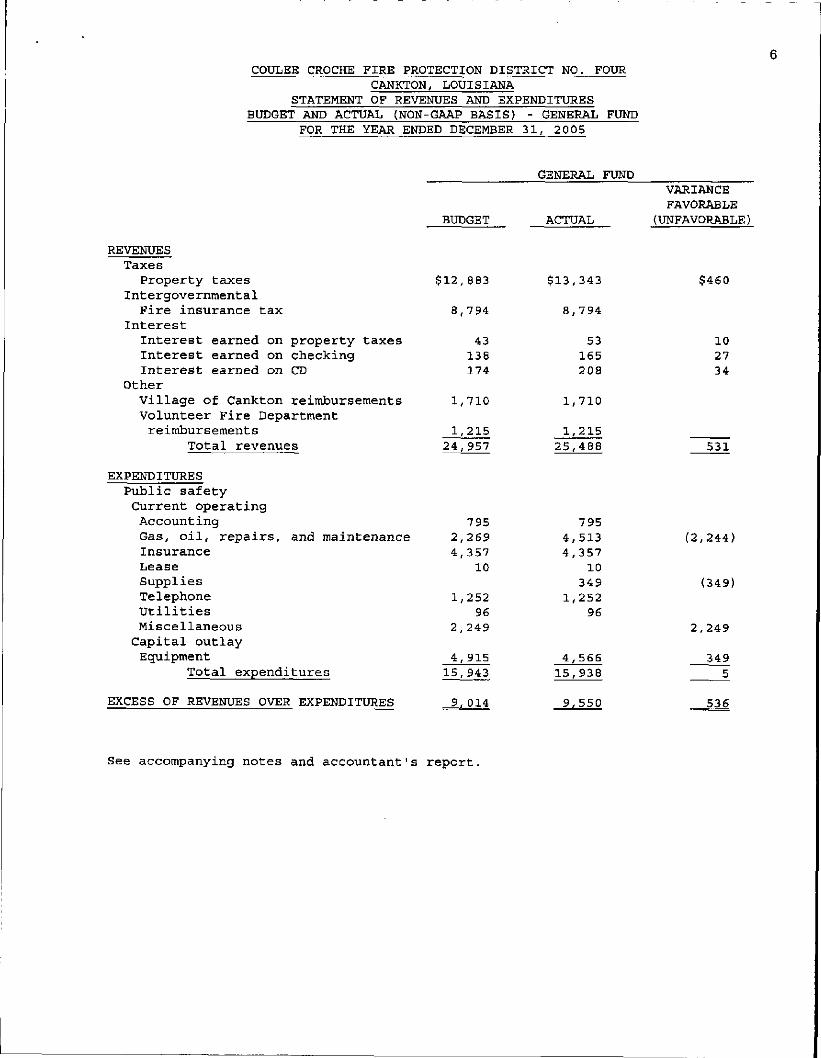

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

STATEMENT OF REVENUES AND EXPENDITURESBUDGET AND ACTUAL (NON-GAAP BASIS)

FOR THE YEAR ENDED DECEMBER

REVENUESTaxesProperty taxes

IntergovernmentalFire insurance tax

InterestInterest earned on property taxesInterest earned on checkingInterest earned on CD

OtherVillage of Cankton reimbursementsVolunteer Fire Departmentreimbursements

Total revenues

EXPENDITURESPublic safetyCurrent operatingAccountingGas, oil, repairs, and maintenanceInsuranceLeaseSuppliesTelephoneUtilitiesMiscellaneousCapital outlayEquipment

Total expenditures

EXCESS OF REVENUES OVER EXPENDITURES

BUDGET

$12,883

8,794

43138174

1,710

1,21524,957

7952,2694,357

10

1,25296

2,249

4,91515,943

9, 014

- GENERAL FUND31, 2005

GENERAL FUND

ACTUAL

$13,343

8,794

53165208

1,710

1,21525,488

7954,5134,357

10349

1,25296

4,56615,938

9,550

VARIANCEFAVORABLE

(UNFAVORABLE)

$460

102734

531

(2,244)

(349)

2,249

3495

536

See accompanying notes and accountant's report.

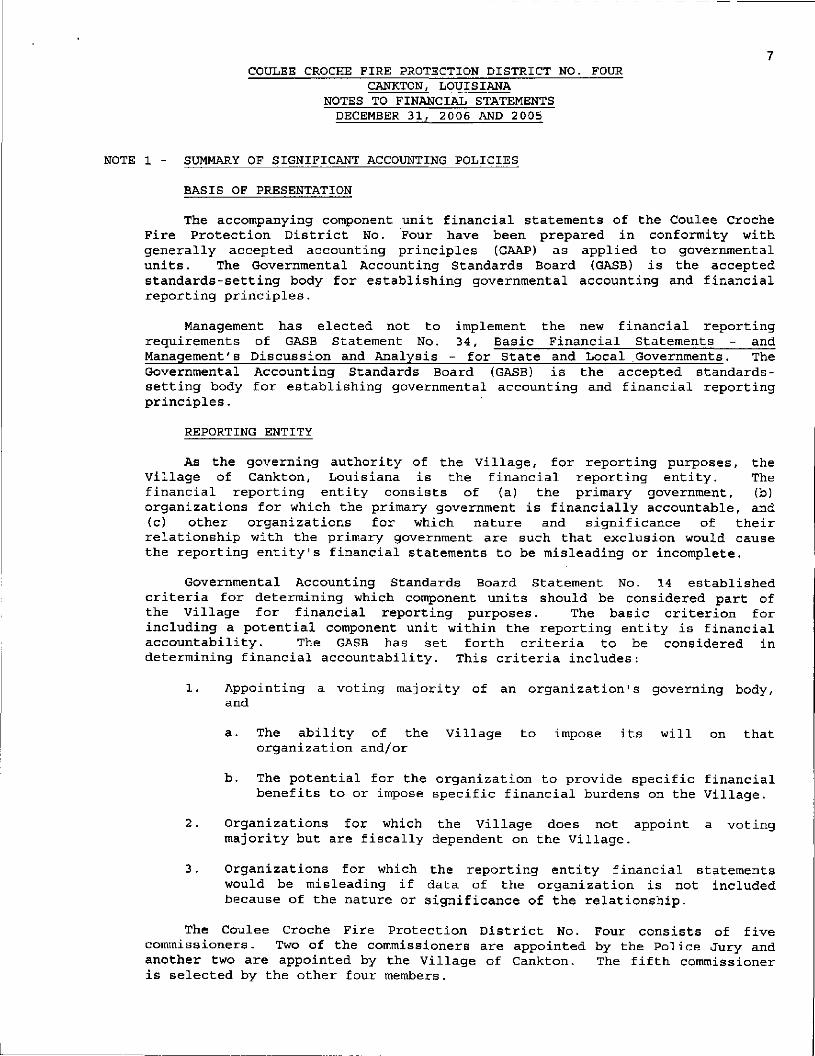

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2005

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PRESENTATION

The accompanying component unit financial statements of the Coulee CrocheFire Protection District No. Four have been prepared in conformity withgenerally accepted accounting principles (GAAP) as applied to governmentalunits. The Governmental Accounting Standards Board (GASB) is the acceptedstandards-setting body for establishing governmental accounting and financialreporting principles.

Management has elected not to implement the new financial reportingrequirements of GASB Statement No. 34, Basic Financial Statements - andManagement's Discussion and Analysis - for State and Local Governments. TheGovernmental Accounting Standards Board (GASB) is the accepted standards-setting body for establishing governmental accounting and financial reportingprinciples.

REPORTING ENTITY

As the governing authority of the Village, for reporting purposes, theVillage of Cankton, Louisiana is the financial reporting entity. Thefinancial reporting entity consists of (a) the primary government, (b)organizations for which the primary government is financially accountable, and(c) other organizations for which nature and significance of theirrelationship with the primary government are such that exclusion would causethe reporting entity's financial statements to be misleading or incomplete.

Governmental Accounting Standards Board Statement No. 14 establishedcriteria for determining which component units should be considered part ofthe Village for financial reporting purposes. The basic criterion forincluding a potential component unit within the reporting entity is financialaccountability. The GASB has set forth criteria to be considered indetermining financial accountability. This criteria includes:

1. Appointing a voting majority of an organization1s governing body,and

a. The ability of the Village to impose its will on thatorganization and/or

b. The potential for the organization to provide specific financialbenefits to or impose specific financial burdens on the Village.

2. Organizations for which the Village does not appoint a votingmajority but are fiscally dependent on the Village.

3. Organizations for which the reporting entity financial statementswould be misleading if data of the organization is not includedbecause of the nature or significance of the relationship.

The Coulee Croche Fire Protection District No. Four consists of fivecommissioners. Two of the commissioners are appointed by the Police Jury andanother two are appointed by the Village of Cankton. The fifth commissioneris selected by the other four members.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2Q05

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

REPORTING ENTITY - Continued

Coulee Croche Fire Protection District No. Four leases land from theVillage of Cankton under a 99 year lease for $10 per year. Because theDistrict receives a reimbursement from the Village of Cankton, leases landfrom the Village and the Village appoints two commissioners, the District isconsidered to be a component unit of the Village of Cankton, the financialreporting entity. The accompanying financial statements present informationonly on the funds maintained by the District and do not present information onthe Village of Cankton, the general government services provided by thatgovernment unit, or the other governmental units that comprise the financialreporting entity.

FUND ACCOUNTING

The accounts of the District are organized on the basis of funds andaccount groups, each of which is considered a separate accounting entity. Theoperations of each fund are accounted for with a separate set of self -balancing accounts that comprise its assets, liabilities, fund equity,revenues, and expenditures or expenses, as appropriate. Government resourcesare allocated to and accounted for in individual funds based upon the purposesfor which they are to be spent and the means by which spending activities arecontrolled. The fund presented in the financial statements in this report isdescribed as follows:

Governmental Fund

General Fund. The General Fund is the general operating fund of theDistrict. It is used to account for all financial resources except thoserequired to be accounted for in another fund.

BASIS OF ACCOUNTING

The accounting and financial reporting treatment applied to a fund isdetermined by its measurement focus. All governmental funds and expendabletrust funds are accounted for using a current financial resources measurementfocus. With this measurement focus, only current assets and currentliabilities generally are included on the balance sheet. Operating statementsof these funds present increases (i.e., revenues and other financing sources)and decreases (i.e., expenditures and other financing uses) in net currentassets.

Basis of accounting refers to when revenues and expenditures or expensesare recognized in the accounts and reported in the financial statements.Basis of accounting relates to the timing of the measurements made, regardlessof the measurement focus applied.

All governmental funds are accounted for using the modified accrual basisof accounting. Their revenues including grants, entitlements and sharedrevenues, are recognized when they become measurable and available as netcurrent assets. Property taxes are recognized as revenue at the time thatthey are assessed. All other income is recognized as revenue when received.

COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOURCANKTON, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2005

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

BASIS OF ACCOUNTING - Continued

Expenditures are generally recognized under the modified accrual basis ofaccounting when the related fund liability is incurred. An exception to thisgeneral rule is for principal and interest on general long-term debt which isrecognized when due.

Expenditures for insurance and similar services, which extend over morethan one accounting period, are accounted for as expenditures in the period ofacquisition.

Purchases of operating supplies are regarded as expenditures at the timepurchased and inventories of such supplies (if any) are not recorded as assetsat the close of year-end.

CASH AND INVESTMENTS

Cash and investments are recorded at cost, which approximates market.Louisiana statutes authorize the District to invest in United States bonds,treasury notes or certificates, time certificates of deposit in state andnational banks, or any other federally insured investment.

FIXED ASSETS

All items of property, plant, and equipment (including infrastructuregeneral fixed assets) are recorded in the General Fixed Assets Account Group.Such assets are maintained on the basis of original cost (cash paid plustrade-in allowance, if applicable) and no depreciation is computed or recordedthereon. All fire hydrants are capitalized by the Village of Cankton.

The account group is not a "fund." It is concerned only with themeasurement of financial position. It is not involved with measurement ofresults of operations.

Construction period interest is capitalized if material amounts ofinterest resulting from borrowings in the course of the construction of fixedassets is incurred. No interest was capitalized for the years ended December31, 2006 or 2005.

BUDGETARY ACCOUNTING

Annually, the Fire District prepares and adopts a budget for the GeneralFund. Formal budget integration is not employed as a part of the accountingsystem; however, routine budget comparisons are made prior to expending funds.Budgets are prepared on a cash basis of accounting, and appropriations lapseat year-end. The budgeted amounts of the General Fund in the accompanyingfinancial statements are from the amended budget which was adopted.

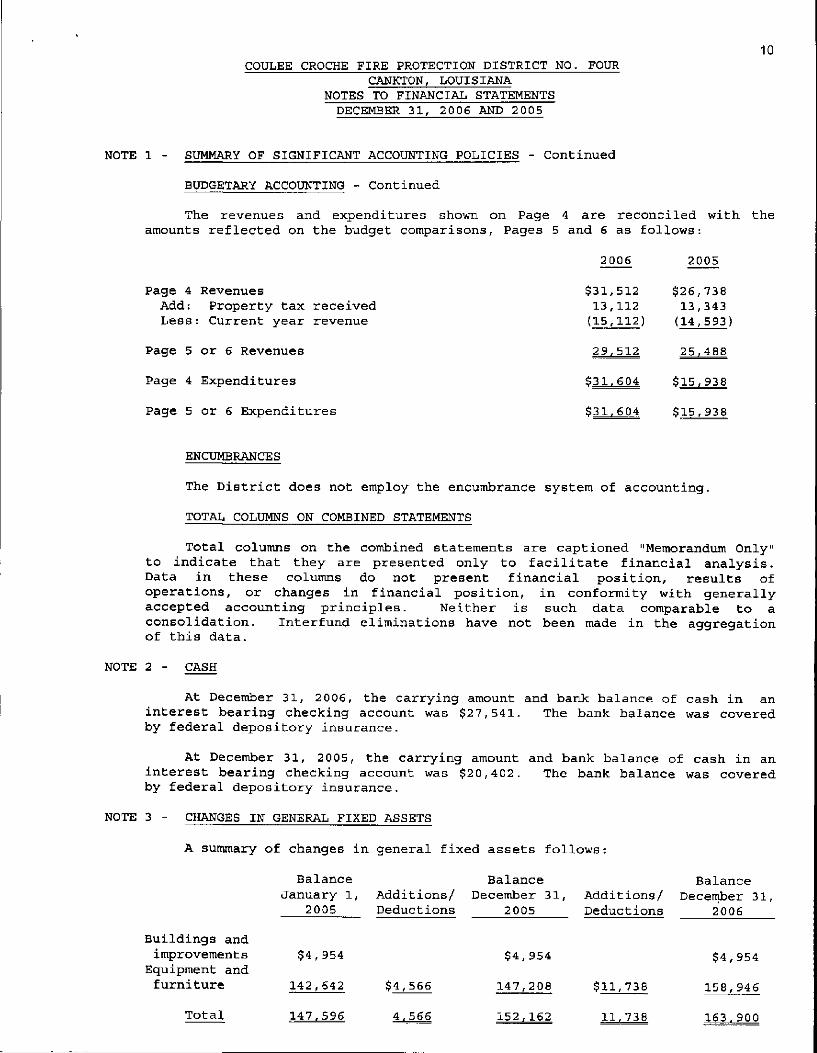

10COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR

CANKTON, LOUISIANANOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2005

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

BUDGETARY ACCOUNTING - Continued

The revenues and expenditures shown on Page 4 are reconciled with theamounts reflected on the budget comparisons. Pages 5 and 6 as follows:

2006 2005

Page 4 Revenues $31,512 $26,738Add: Property tax received 13,112 13,343Less: Current year revenue (15,112) (14,593)

Page 5 or 6 Revenues 29,512 25,488

Page 4 Expenditures $31,604 $15,938

Page 5 or 6 Expenditures $31,604 $15,938

ENCUMBRANCES

The District does not employ the encumbrance system of accounting.

TOTAL COLUMNS ON COMBINED STATEMENTS

Total columns on the combined statements are captioned "Memorandum Only"to indicate that they are presented only to facilitate financial analysis.Data in these columns do not present financial position, results ofoperations, or changes in financial position, in conformity with generallyaccepted accounting principles. Neither is such data comparable to aconsolidation. Interfund eliminations have not been made in the aggregationof this data.

NOTE 2 - CASH

At December 31, 2006, the carrying amount and bank balance of cash in aninterest bearing checking account was $27,541. The bank balance was coveredby federal depository insurance.

At December 31, 2005, the carrying amount and bank balance of cash in aninterest bearing checking account was $20,402. The bank balance was coveredby federal depository insurance.

NOTE 3 - CHANGES IN GENERAL FIXED ASSETS

A summary of changes in general fixed assets follows:

Balance Balance BalanceJanuary 1, Additions/ December 31, Additions/ December 31,

2005 Deductions 2005 Deductions 2006

Buildings andimprovements $4,954 $4,954 $4,954

Equipment andfurniture 142,642 $4,566 147,208 $11,738 158,946

Total 147,596 4,566 152,162 11,738 163,900

11COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR

CANKTON, LOUISIANANOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2005

NOTE 4 - AD VALOREM TAXES

The District's ad valorem tax is collected by an intermediary governmentand remitted on a monthly basis. The intermediary government maintains thetax roll for ad valorem taxes for the District. The District levied a generaltax of 3.09 mills which was approved by voters on November 3, 1998.

The District's ad valorem tax, levied for the calendar year, is due on orbefore December 31 and becomes delinquent on January 1. A tax sale is usuallyheld in September of the following year.

The Coulee Croche Fire Protection District No. Four called an election onMay 7, 2002. The two propositions on the ballot were ® renewal of the 1.03mills property tax for 10 years and © levy of an additional 2.06 millsproperty tax for 10 years for the purpose of constructing, acquiring,improving, maintaining and operating the District's fire protection facilitiesand paying the cost of obtaining equipment and water for fire protectionpurposes. Both propositions were approved by the voters. The additional 2.06mills tax is effective with the 2002 property tax roll.

The 2004 tax year was a reassessment year; as a result the Districtassessed 2.96 mills.

Ad valorem taxes receivable at December 31, 2006 and 2005 were asfollows:

Taxes PerTax Roll

RetirementContribut ions

ReceiptsNovember andDecember

Estimated Net TaxesUncollectiable Receivable

20052006

$15,82317,473

$176585

$932 $1,1771,351

$13,53815,537

The estimated allowance for uncollectiable ad valorem tax is based onprior years' experience.

NOTE 5 - PER DIEM

Members of the governing board are not paid compensation or per diem.

NOTE 6 - FUND BALANCE

For the years ended December 31, 2006 and 2005, Coulee Croche FireProtection District No. Four did not have a deficit fund balance and the fundbalance was unreserved.

NOTE 7 - COST-SHARING AGREEMENT

On November 7, 2000 the Board entered into an agreement with the Villageof Cankton and the Cankton Volunteer Fire Department to share the cost equallyof all vehicles used in the control of fires within the Fire District. Thesevehicles consist of the two pumper trucks owned by Coulee Croche FireProtection District No. Four. The costs include all repairs, operating costs,maintenance and insurance for said vehicles.

12COULEE CROCHE FIRE PROTECTION DISTRICT NO. FOUR

CANKTON, LOUISIANANOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006 AND 2005

NOTE 7 - COST-SHARING AGREEMENT - Continued

It was further resolved that the Coulee Croche Fire Protection DistrictNo. Four will pay the monthly bills for the operation, etc., of thesevehicles. The two other entities will reimburse their one-third share once ayear on or about October 31, upon the submission of a statement from theDistrict of the expenses for the year.