Embed Size (px)

Citation preview

Cott to Acquire Eden Springs

Expanding Our Home and Office Delivery Business and Platforms

Safe Harbor Statements

1

Forward Looking Statements: This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934 and applicable Canadian securities laws conveying management's expectations as to the future based on plans, estimates and projections at the time the Company makes the statements. Forward-looking statements involve inherent risks and uncertainties and the Company cautions you that a number of important factors could cause actual results to differ materially from those contained in any such forward-looking statement. The forward-looking statements contained in this presentation include, but are not limited to, statements related to the anticipated timing of the transaction, the completion of the transaction on the terms proposed, the financing of the transaction on terms currently anticipated, and the potential impact the acquisition will have on the Company. Management believes these assumptions to be reasonable but there is no assurance that they will prove to be accurate. Factors that could cause actual results to differ materially from those described in this presentation include, among others: (1) the ability to consummate the proposed transaction; (2) receipt of regulatory approvals without unexpected delays or conditions; (3) changes in estimates of future earnings and cash flows; (4) changes in expectations as to the closing of the transaction; (5) expected synergies and cost savings are not achieved or achieved at a slower pace than expected; (6) integration problems, delays or other related costs; (7) retention of customers and suppliers; (8) the cost of capital necessary to finance the transaction; and (9) unanticipated changes in laws, regulations, or other industry standards affecting the companies. The foregoing list of factors is not exhaustive. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Readers are urged to carefully review and consider the various disclosures, including but not limited to risk factors contained in the Company's Annual Report in the Form 10-K for the year ended January 2, 2016. The Company does not, except as expressly required by applicable law, undertake to update or revise any of these statements in light of new information or future events.

Non-GAAP Measures: The Company utilizes certain non-GAAP financial measures, including 2016 estimated Eden Springs adjusted EBITDA, to separate the impact of certain items from the underlying Eden Springs business. Management believes this supplemental information is useful to investors for their independent evaluation and understanding of the transaction with Eden Springs. Additionally, the Company supplements its reporting of net cash provided by (used in) operating activities determined in accordance with GAAP by excluding capital expenditures to present, free cash flow (on a stand-alone and pro forma basis), and by excluding acquisition, integration and transaction costs to present adjusted free cash flow (on a stand-alone and pro forma basis), which management believes provides useful information to investors. With respect to our expectations of performance of Eden as it is being integrated, reconciliations of free cash flow accretion and adjusted free cash flow accretion are not available, as we are unable to quantify certain amounts that would be required to be included in the relevant GAAP measures without unreasonable effort. We expect that the unavailable reconciling items, which primarily include foreign exchange impact, interest costs associated with yet to be issued debt and phasing of capex, could significantly affect our financial results. These items depend on highly variable factors and any such reconciliations would imply a degree of precision that would be confusing or misleading to investors. We expect the variability of these factors to have a significant, and potentially unpredictable, impact on our future GAAP financial results. The non-GAAP financial measures described above are in addition to, and not meant to be considered superior to, or a substitute for, the Company’s financial statements prepared in accordance with GAAP. In addition, the non-GAAP financial measures included in this presentation reflect management's judgment of particular items, and may be different from, and therefore may not be comparable to, similarly titled measures reported by other companies. A reconciliation of these non-GAAP measures may be found on www.cott.com.

Today’s Management Attendees

2

Jerry FowdenChief Executive Officer

Jay WellsChief Financial Officer

Tom HarringtonChief Executive Officer – DS Services

Jarrod LanghansHead of Investor Relations

Q&A

Strategic Rationale and Transaction Overview

Introduction

Today’s Agenda

3

Successfully integrate DS Services and Aquaterra to drive synergy capture

Stable, strong cash generation through 4Cs, supported by growth in contract manufacturing and Value Added Water offsetting PL CSD and SSJ declines

Continue to generate top-line growth

Small tuck-in acquisitions of $10 -$20 million in HOD Water/OCS businesses annually

DS Services Growth

Acquisition Synergy Capture

Mid-to-Larger Scale

Acquisitions

Traditional Business

Focus on cash generative HOD water, coffee and tea in growing and/or higher-margin beverage categories (cash-on-cash IRR greater than cost of equity)

Shareholder Value Creation

Create a more diversified higher margin and/or

growth-oriented company with annual EBITDA and

free cash flow expansion to drive increased

multiple/stock valuation.

Cott’s Vision – Create a More Diversified Higher Margin and/or Growth CompanyAcquisition of Eden Springs Builds Cott’s HOD Water, Coffee and Filtration Platform Across Europe

4

Eden Springs – Europe’s Leading Direct-to-Consumer (Home and Office) Water and Office Coffee Services Provider

2015 Revenue: €238mm ($266mm)

Water Services Office Coffee Services

2015 Revenue: €70mm ($77mm)

Filtration

2015 Revenue: €22mm ($24mm)

Retail

2015 Revenue: €37mm ($41mm) ___________________________Note: Figures converted at EUR:USD rate of 1.11 Source: Company information

5

2015 Revenue:

€367mm ($408mm)

Water Services

65%

Office Coffee

Services19%

Retail10%

Filtration6%

United Kingdom

18%

Israel17%

France15%

Russia9%

Switzerland8%

Germany7%

Poland6%

Nordics6%

Netherlands5%

Other(2)

9%

Eden Springs – Multiple Strong Leadership Positions and Platforms Across Europe

6

Leading Platforms Across Europe

3

1

1

1

1

1

12

2

2

2

11

2

1

2

2

2

Portugal Spain

France

Switzerland

Germany

UK Netherlands

Denmark

Norway

Sweden

Finland

Estonia

Latvia

Lithuania

Russia

IsraelEden geographic presence

BWC water position(3) Water activity Coffee activity

2015 Adj. EBITDA(1) By CountryBroad Spread of EBITDA Contribution

___________________________(1) Excludes corporate allocations. Adjustments to EBITDA include acquisition integration cost, restructuring charges, business development and establishment costs (2) Includes Baltics, Portugal and Spain(3) BWC represents total bottled water coolers but is not a market in and of itself as the HOD water business consists of coolers, bottled water as well as other products such as case pack water and single serve productsSource: Company information

Poland

Luxembourg

7

31

1

1

1

12

2

2

11

2

1

2

Portugal Spain

France Switzerland

Germany

UK Netherlands

Denmark

Norway

Sweden

Finland

Estonia

Latvia

Russia

Israel

Eden geographic presence

BWC water position(1)

1

1

1

1

1

1

1

1

1

1

1

1

1

2

2

2

2

2

3

3

___________________________(1) BWC represents total bottled water coolers but is not a market in and of itself as the HOD water business consists of coolers, bottled water as well as other products such as case pack water and single serve productsSource: Company information

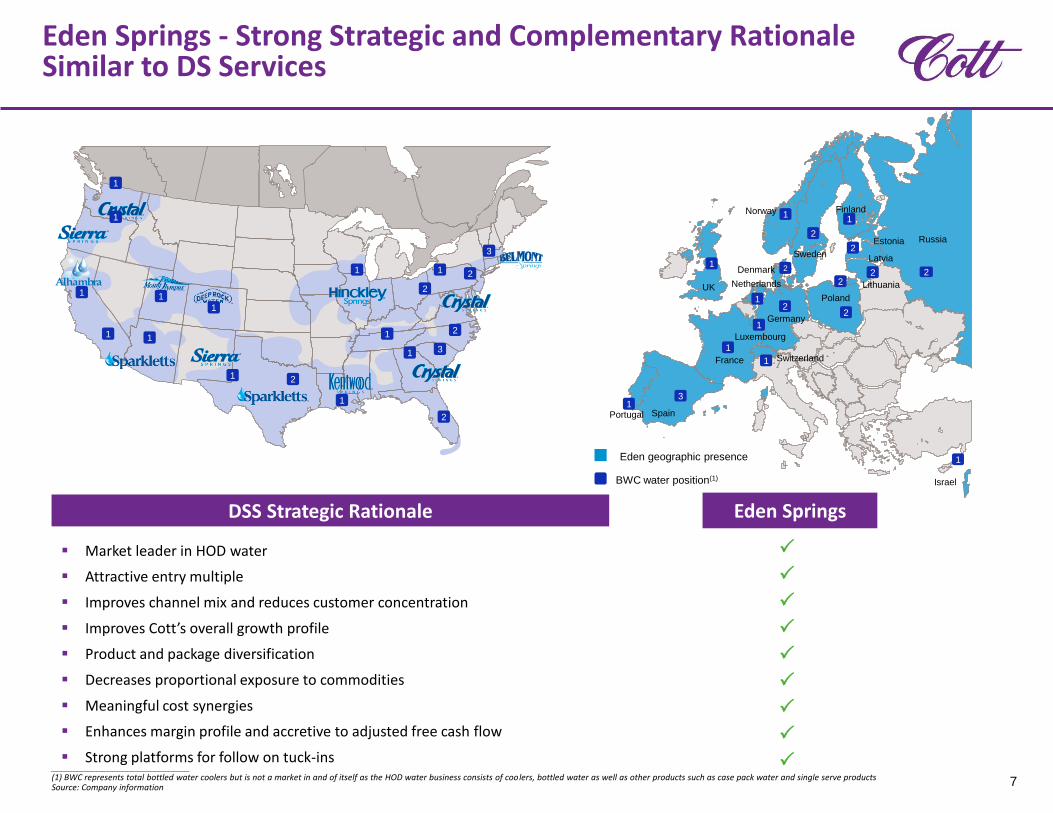

Eden Springs - Strong Strategic and Complementary Rationale Similar to DS Services

DSS Strategic Rationale

Market leader in HOD water

Attractive entry multiple

Improves channel mix and reduces customer concentration

Improves Cott’s overall growth profile

Product and package diversification

Decreases proportional exposure to commodities

Meaningful cost synergies

Enhances margin profile and accretive to adjusted free cash flow

Strong platforms for follow on tuck-ins

Eden Springs

2

Poland

2

Luxembourg

Lithuania

2

1

Q&A

Strategic Rationale and Transaction Overview

Introduction

Today’s Agenda

8

Cott’s Eden Springs Transaction Overview and Strategic Rationale

9

Improves product and channel mix while reducing exposure to Big Box retail and commodities, proportionally (Cott’s 2015 EBITDA from private label in large format retail is down to 31%)1

Creates a strong international HOD platform with multiple leading positions and further tuck-in opportunities 2

Meaningful scale across Europe with access to attractive end-markets with positive growth outlook (A leading European player with multiple value-creative tuck-in acquisition opportunities)3

Financially attractive and consistent with Cott’s acquisition and diversification strategy – clear synergy potential, accretive to adjusted EBITDA margins (Eden adjusted EBITDA margins ῀17% versus Cott ῀12%), adjusted free cash flow, and cash flow conversion(1)

5

Expands direct to consumer business – High-quality and loyal customer base (Combination of DS Services, Aquaterra and Eden has over 2 million direct to customer delivery points)

4

• Eden Springs to be acquired for approximately €470 million.

• The acquisition creates a business with ῀$3.3 billion in revenue and adds Europe's leading provider of water and coffee solutions while further enhancing Cott’s margins and free cash flow alongside product and channel diversification.

• Cott has received committed acquisition financing and the acquisition is expected to close in Q3 2016.

(1) FCF conversion defined as EBITDA less capex / EBITDA

CSD16%

Juice / Juice Drinks11%

Sparkling Waters

10%

HOD Water33%

Water8%

OCS6%

Other16%

CSD33%

Juice / Juice Drinks22%

Sparkling Waters

21%

Other24%

Better For You57%

Other43%

Better For You21%

Other79%

CSD13%

Juice / Juice Drinks

9%

Sparkling Waters

8%

HOD Water38%

Water8%

OCS8%

Other15%

Ch

an

ne

lsB

ette

r Fo

r Yo

u

Traditional Cott 2015 Adj. EBITDA Cott + DSS 2015 Adj. EBITDA Cott + DSS + Eden 2015 Adj. EBITDA

Improves Product and Channel Mix While Reducing Exposure to Big Box Retail and Commodities

10

Pro

du

cts

Better For You63%

Other37%

CSD + Juices = 55% CSD + Juices = 27% CSD + Juices = 22%Traditional Cott = 100% Traditional Cott = 48% Traditional Cott = 40%

1

___________________________Note: Financials based on FY 2015Adjustments to EBITDA include acquisition integration costs, unrealized foreign exchange gains, purchase accounting adjustments and restructuring and business development costsOther product category includes concentrates, Eden’s filtration services and other. Sparkling water includes mixers Other channels include contract packaging (except Cott standalone), office coffee services and otherBetter For You grouping includes HOD Water, Water, OCS and Sparkling Waters / MixersSource: Company information, Management estimates

Private Label Retail70%

Branded Retail15%

Contract Packaging

12%

Other3%

Private Label Retail37%

Branded Retail11%

HOD Water Delivery

33%

Other19%

Private Label Retail31%

Branded Retail11%

HOD Water Delivery

38%

Other20%

Creates a Strong International HOD Platform with Multiple Leading Positions and Further Tuck-In Acquisition Opportunities

11

Eden geographic presence

BWC water position(1)

1

1

1

1

1

11

1

1

1

1

1

1

2

2

2

2

2

3

3

___________________________Source: Company information, Management estimates(1) BWC represents total bottled water coolers but is not a market in and of itself as the HOD water business consists of coolers, bottled water as well as other products such as case pack water and single serve products

1 1

1

1

1

11

2

Eden4%

Other89%

Eden20%

Company A3%

Company B3%

Next 513%

Other61%

European HOD Water Players Revenue European Office Coffee Players Revenue

31

1

1

1

1

12

2

2

11

2

1

22

Israel

Company A

6%

Cott becomes a leading HOD player across North America and Europe. Opportunity exists for further accretive acquisitions

2

2

PortugalSpain

France

Switzerland

Germany

UK

Netherlands

Denmark

Norway

Sweden

Finland

Estonia

Latvia

Lithuania

Russia

Poland

Luxembourg

Meaningful Scale Across Europe with Access to Attractive End-Markets with Positive Growth Outlook

A Clear Leader in the European Market

12

3

Water Services Office Coffee Services Filtration

Fragmented market presents

multiple potential tuck-in

acquisition opportunities

Highly fragmented market provides tuck-

in acquisition and cross sell into water

customer opportunities

Small, but growing market with only

1 other large market participant

On-trend category with health &

wellness and environmental focus

Consumers increasingly expecting high-

quality, premium brand coffee at work

Strong growth and creating highly

synergistic opportunity

European Category Size: ~$1.1bn European Category Size: ~$1.8bn European Category Size: ~$280mm

___________________________Note: Figures converted as EUR:USD rate of 1.11. Source: Zenith International 2015, Euromonitor

More than 800,000 customers across Europe

Installed base of ~1 million water coolers and coffee machines

Clear leader in HOD water with largest competitor being a distant second

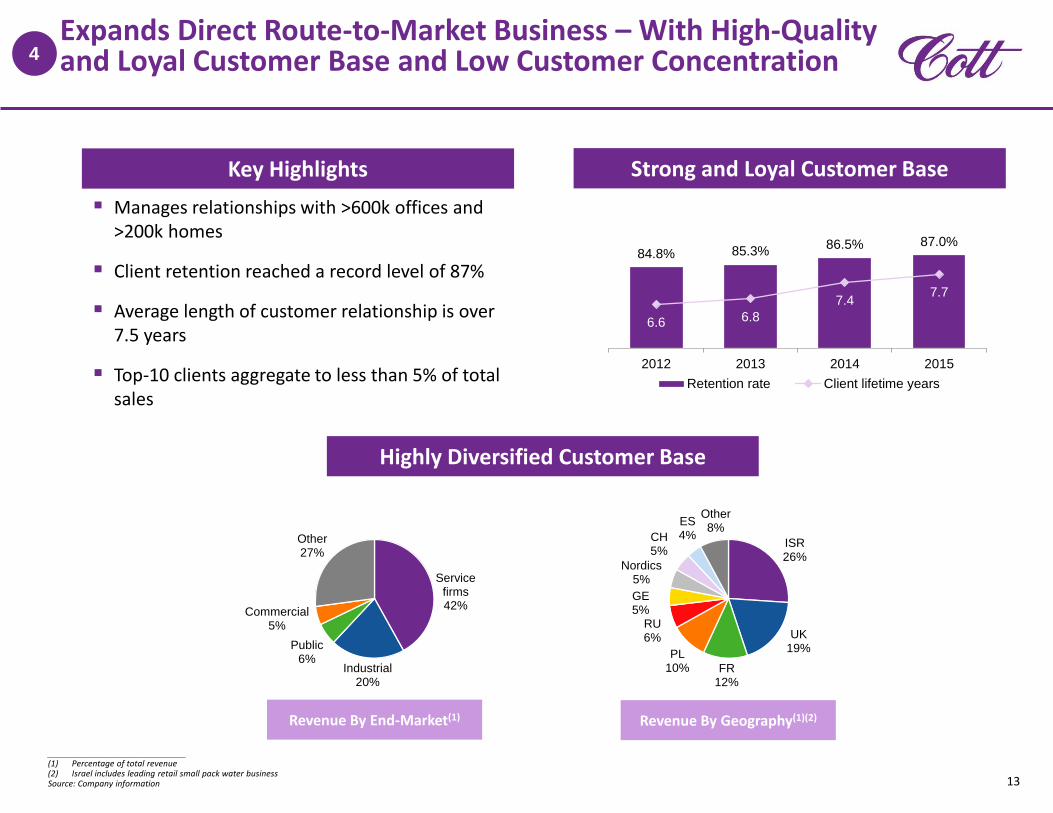

ISR26%

UK19%

FR12%

PL10%

RU6%

GE5%

Nordics5%

CH5%

ES4%

Other8%

Expands Direct Route-to-Market Business – With High-Quality and Loyal Customer Base and Low Customer Concentration

13

4

Service firms42%

Industrial20%

Public6%

Commercial5%

Other27%

Key Highlights Strong and Loyal Customer Base

Manages relationships with >600k offices and >200k homes

Client retention reached a record level of 87%

Average length of customer relationship is over 7.5 years

Top-10 clients aggregate to less than 5% of total sales

Highly Diversified Customer Base

84.8% 85.3% 86.5% 87.0%

6.6 6.8

7.47.7

2012 2013 2014 2015

Retention rate Client lifetime years

Revenue By End-Market(1) Revenue By Geography(1)(2)

___________________________(1) Percentage of total revenue(2) Israel includes leading retail small pack water businessSource: Company information

Financially Attractive and Consistent with Cott’s Acquisition Strategy

14

5

Purchase Price of ῀€ 470 million on a cash-free and debt-free basis representing a Mid-7x EBITDA purchase multiple

Estimated run rate adjusted 2016 EBITDA above €60 million

Approximately €10 million in synergies by the end of 2019

Estimated Mid-6x EBITDA post synergy multiple

Attractive long term cost of capital

Financial Impact

Eden’s ῀17% EBITDA margins are accretive to Cott’s overall EBITDA margin

Accretive to free cash flow in Year 1 (excluding acquisition, integration and transaction costs)

High free cash flow conversion(1) > 60% (capex ῀€20 to €25 million)

IRR in excess of cost of equity

___________________________Note: Figures converted as EUR:USD rate of 1.11 (1) FCF conversion defined as EBITDA less capex / EBITDASource: Management estimates

Attractive Multiple

Consistent with Cott’s

Acquisition Strategy

Improves channel diversification

Reduces customer concentration and exposure proportionally to large format retail

Low commodity exposure

Expands “Better For You” platform

Growing product categories and end-markets

Significant tuck-in acquisition opportunities at accretive multiples

Clear synergy potential across Cott, DS Services, Aimia Foods and Eden Springs

Strong international management team

Strategic Rationale and Transaction Overview

Introduction

Q&A

Today’s Agenda

15