Embed Size (px)

Citation preview

Cost• Fundamental Concept: Opportunity

cost—the value of the most highly valued forgone alternative.

• All costs are opportunity costs.

Opportunity Cost

Assumptions:•benefit of hiring ass’t = $80•assistant charges me $50

Hire

Don’thire

$80

$50

$50 is the opportunitycost of hiring theassistant

An Equivalent Tree

Assumptions:•benefit of hiring ass’t = $80•assistant charges me $50

Hire

Don’thire

$30 (= $80 - $50)

$0 (= $50 - $50)

So $50 is still theopportunity cost ofhiring the ass’t.

MBA 201a -- Lecture 4 -- Fall 2004

Page 1 of 18

Observation

• Subtracting a constant amount from allterminal nodes cannot change an expected-value maximizer’s decision.

What Does It Cost to Attend Haas?

Tuition (net aid)Books, fees, etc.Room & board

Total

What Does It Cost to Attend Haas?

Attend

Don’tAttend

benefit - room & board

- room & board+ net tuition+ books, fees, etc.+ salary

MBA 201a -- Lecture 4 -- Fall 2004

Page 2 of 18

Cost vs. Expense

Cost Expense

Tuition Tuition

Books, etc. Books, etc.

Salary —

— Room & Board

Difference between Cost & Expense

• Salary—an example of an imputed cost.• Imputed Cost: the opportunity cost

incurred when the owner of a factor employs that factor in one use rather than in its best alternative use.

• In this case, the factor is your time.

Difference between Cost & Expense

• Room & board—an example of a sunk expenditure.

• Sunk expenditure: an expenditure that will be made over the relevant decision-making horizon under both the considered course of action and the best alternative action.

MBA 201a -- Lecture 4 -- Fall 2004

Page 3 of 18

Difference between Cost & Expense

• Imputed costs do matter for decision making

• Sunk expenditures do not matter for decision making.

• Cost = Expenditure - Sunk Expenditures + Imputed Costs

Examples of Imputed Costs

• The cost of using a factor kept in inventory is its current market price, not its historical cost.– Apple Computers & memory chips.

• Wear & tear on machinery, vehicles, & other factors that reduces their resale value.

Test for Imputed Cost

If using a factor or asset changes its value, then there is an imputed cost.

MBA 201a -- Lecture 4 -- Fall 2004

Page 4 of 18

Examples of Sunk Expenditures

• The non-recoverable portion of irreversible expenditures made in the past.– the difference between what you paid for your

textbooks and the amount for which you can resell them.

• Expenditures to which you committed in the past (e.g., many debts).

Test for a Sunk Expenditure

If you can’t affect an expenditure over the relevant decision-making horizon, it’s a sunk expenditure.

A Cost Taxonomy

• Variable costs vs. overhead costs• Variable costs are those that vary with

each unit produced. Examples include– raw materials– direct labor

MBA 201a -- Lecture 4 -- Fall 2004

Page 5 of 18

A Cost Taxonomy

• Overhead costs are costs that do NOT vary with each unit produced. Examples include:– lease of machinery– supervisory staff salaries

• Caution: some expenditures that get labeled overhead by accountants are not overhead: either they are variable costs or they are sunk expenditures.

A Cost Taxonomy

• Total Cost: the cost of producing some number of units of output.

• Marginal Cost: the cost of producing the next unit.

• If C(n) is the total cost of producing nunits, then the marginal cost of the nth unit, MC(n), equals C(n) - C(n-1).

• Average Cost: C(n)/n.

Marginal Cost: Example 1

• $10 in labor per unit and $5 in raw materials per unit.

• MC = $15• AC = $15

MBA 201a -- Lecture 4 -- Fall 2004

Page 6 of 18

Marginal Cost: Example 2

• $10 in labor per unit, $5 in raw materials per unit, $100 to rent machine for the day.

• MC(1) = $115 and MC(n) = $15, n > 1.• Note: overhead increases the marginal

cost of the unit that triggers the overhead expenditure.

• AC(n) = $15 + $100/n > MC(n), n > 1.

Marginal Cost: Example 3

• $5 in raw materials per unit and $10 per unit in labor upto 20 units, but $15 (time & a half) per unit for all units beyond 20 units.

• MC(n) = $15 if n ≤ 20, but MC(n) = $20 if n> 20.

• If n > 20, then AC(n) = ($300 + $20(n-20))/n < $20 = MC(n).

Marginal Cost & Average Cost

• Marginal cost will sometimes equal average cost (e.g., example 1)

• Marginal cost will sometimes be less than average cost (e.g., example 2)

• Marginal cost will sometimes be greater than average cost (e.g., example 3)

• Moral: Average cost is often a poor estimate of marginal cost.

MBA 201a -- Lecture 4 -- Fall 2004

Page 7 of 18

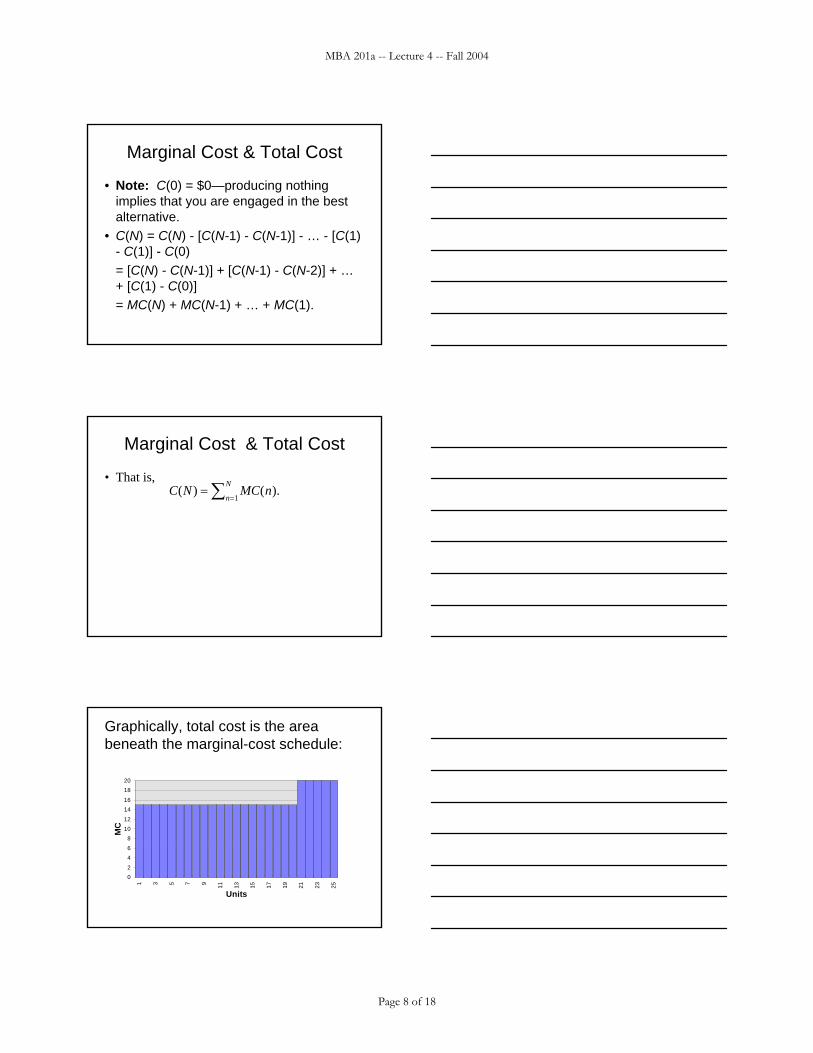

Marginal Cost & Total Cost

• Note: C(0) = $0—producing nothing implies that you are engaged in the best alternative.

• C(N) = C(N) - [C(N-1) - C(N-1)] - … - [C(1) - C(1)] - C(0)

= [C(N) - C(N-1)] + [C(N-1) - C(N-2)] + … + [C(1) - C(0)]

= MC(N) + MC(N-1) + … + MC(1).

Marginal Cost & Total Cost

• That is, C N MC n

n

N( ) ( ).==∑ 1

Graphically, total cost is the area beneath the marginal-cost schedule:

02

46

81012

1416

1820

1 3 5 7 9 11 13 15 17 19 21 23 25

Units

MC

MBA 201a -- Lecture 4 -- Fall 2004

Page 8 of 18

Going to the Continuum$/unit

units (x)

MC(x)

x1

C(x1)

x1+h

MC in the continuous context

This slide left blank intentionally

MBA 201a -- Lecture 4 -- Fall 2004

Page 9 of 18

MC in the continuous case

1. Approximation is

MC(x) =C(x + h) − C(x)

h.

2. Want h to be as small as possible:

MC(x) = limh→0

C(x + h) − C(x)h

, (Def’n MC )

where “lim” means the limit of that ratio as h goes toward zero.

3. Example:

C(x) = Ax, where A is a positive constant. Then

C(x + h) − C(x)h

=A(x + h) − Ax

h

=Ah

h= A .

Clearly, as the expression doesn’t depend on h, the limit as h goes to zerois A; that is, if C(x) = Ax, then MC(x) = A.

4. Example:

C(x) = Ax2 + Bx, where A and B are constants. Then

C(x + h) − C(x)h

=A(x2 + 2xh + h2) + B(x + h) − Ax2 − Bx

h

=2Axh + Ah2 + Bh

h= 2Ax + B + Ah .

As h goes to zero, this last expression clearly approaches 2Ax + B; thatis, if C(x) = Ax2 + Bx, then MC(x) = 2Ax + B.

5. Sometimes, there is an overhead cost associated with production.

(a) For instance, a chemical plant might have the following cost schedule:

C(x) ={

0 , if x = 0G(x) + F , if x > 0 ;

that is, if the firm decides to produce at all, then it incurs an overheadcost of F , F > 0, as well as a variable cost of G(x).

(b) This cost function is discontinuous at x = 0; hence MC(0) is notdefined.

MBA 201a -- Lecture 4 -- Fall 2004

Page 10 of 18

(c) Can define MC(x) for x > 0 using definition of MC above—the Fdoesn’t matter if x > 0:

MC(x) = limh→0

(G(x + h) + F

) − (G(x) + F

)h

= limh→0

G(x + h) − G(x)h

.

6. Another example:

Let C(x) = Ax2 +Bx+F , where A, B, and F are non-negative constants(i.e., each is greater than or equal to zero). Then MC(x) = 2Ax + B forx > 0. If F = 0, then MC(0) is defined and is equal to B.

7. Note that MC(x) = C ′(x) = dC(x)/dx.

Rest of this page intentionally left blank.

MBA 201a -- Lecture 4 -- Fall 2004

Page 11 of 18

Graphical Relations

• AC and MC. MC intersects AC at minimum of AC.

• C = x•AC• Area under MC is C

Cost of Capital

• Imputed cost of using an asset is the forgone return from selling asset and investing proceeds in next best alternative.

• Additional imputed cost is the wear and tear (reduction in resale value) of using the asset — depreciation

• Capital cost = forgone return + depreciation

This slide left blank intentionally

MBA 201a -- Lecture 4 -- Fall 2004

Page 12 of 18

Returns to Scale

1. A firm has increasing returns to scale if average cost, AC(x), is decreasingin output, x.

(a) Let β > 1

(b) Decreasing AC ⇒ AC(βx) < AC(x)

(c) Hence,

C(βx)βx

<C(x)

x; hence,

C(βx) < βC(x) .

That is, total costs must increase less than proportionally with anincrease in output if firm enjoys increasing returns to scale.

2. A firm has decreasing returns to scale if average cost is increasing in out-put.

(a) Let β > 1

(b) Increasing AC ⇒ AC(βx) > AC(x)

(c) Hence,

C(βx)βx

>C(x)

x; hence,

C(βx) > βC(x) .

That is, total costs must increase more than proportionally with anincrease in output if firm enjoys decreasing returns to scale.

3. A firm has constant returns to scaleif average cost remains constant asoutput increases.

(a) Let β > 1

(b) Constant AC ⇒ AC(βx) = AC(x)

(c) Hence,

C(βx)βx

=C(x)

x; hence,

C(βx) = βC(x) .

That is, total costs must increase proportionally with an increase inoutput if firm enjoys constant returns to scale.

4. What determines returns to scale?

MBA 201a -- Lecture 4 -- Fall 2004

Page 13 of 18

(a) Production processes

i. Some production processes require large overhead expenses (e.g.,building or maintaining a factory, engineering, corporate staffand other non-production-line workers, etc.)

ii. For example, suppose C(x) = F + cx for x > 0, where F > 0 isoverhead and c > 0 is a constant (note cx is the variable cost ofx units).

iii.AC(x) =

F

x+ c ,

which is clearly deceasing in x.iv. On the other hand, expansion could

• strain control mechanisms, leading to problems with quality(so number of saleable units per amount of inputs falls) orother inefficiencies.

• Running machines faster could increase their wear and tear(i.e., rate of depreciation) and increase the amount of main-tenance they require.

• For instance, if C(x) = x2, then AC(x) = x.

(b) Market for inputs

i. As a firm expands its output it finds it harder (i.e., more expen-sive) to acquire the necessary inputs (e.g., raw materials have tobe shipped from farther away, new workers need to be trained,etc.).

ii. If the firm is large enough, its increased demand for some inputscan drive up the market price of those inputs (e.g., General Mo-tors could not double its production of cars without driving upthe price of steel).

5. Sometimes, a firm enjoys IRS at low levels of output—dividing a largeamount of overhead over more units dominates any other effect—but suf-fers DRS at high levels of output. So initially, average cost is falling, thenit is increasing. Get U-shaped average cost curves.

MBA 201a -- Lecture 4 -- Fall 2004

Page 14 of 18

Scissors

• Review from page 57 of Lecture Notes for 201a

Red Pens and Blue Pens

• Firm makes red pens and blue pens• Each pen uses 15 cents of labor & raw

materials• Each pen goes through a machine that

costs $1000 per day to run regardless of number of pens that go through it

• First 5000 red pens can be sold at 30 cents/pen, additional red pens go for 20 cents/pen

More on Pens

• Firm can sell all the blue pens its wants at 25 cents/pen

• No more than 8000 pens/day• Firm produces 5000 red pens and 3000

blue pens per day• Daily profit is $50

50 = 5000 × (.30-.15) + 3000 × (.25-.15) - 1000

MBA 201a -- Lecture 4 -- Fall 2004

Page 15 of 18

Red Pens, Blue Pens, & Accounting& Accounting

• The $1000 in this problem is an example of shared overhead; i.e., overhead used by both products.

• A danger is that the accounting method will attempt to allocate this overhead to the two lines.

• Suppose allocated proportional to units produced.

Red Pens, Blue Pens, & & AccountingAccounting

• That is, $625 (= $1000 × 5/8) is allocated to red pens and the remainder, $375, is allocated to blue pens.

Product Red Pens Blue Pens TotalUnits 5000 3000 8000Price .30 for 5000 & .20 beyond 0.25 NARevenue 1500 750 2250Direct Cost 750 450 1200Indirect Cost 625 375 1000Profit 125 -75 50

Blue Line Shut

• This suggests blue line should be shutdown as unprofitable.

• But, then make only 8000 red pens. Profits are5000×(.30-.15) + 3000×(.20-.15) -1000

= -100

MBA 201a -- Lecture 4 -- Fall 2004

Page 16 of 18

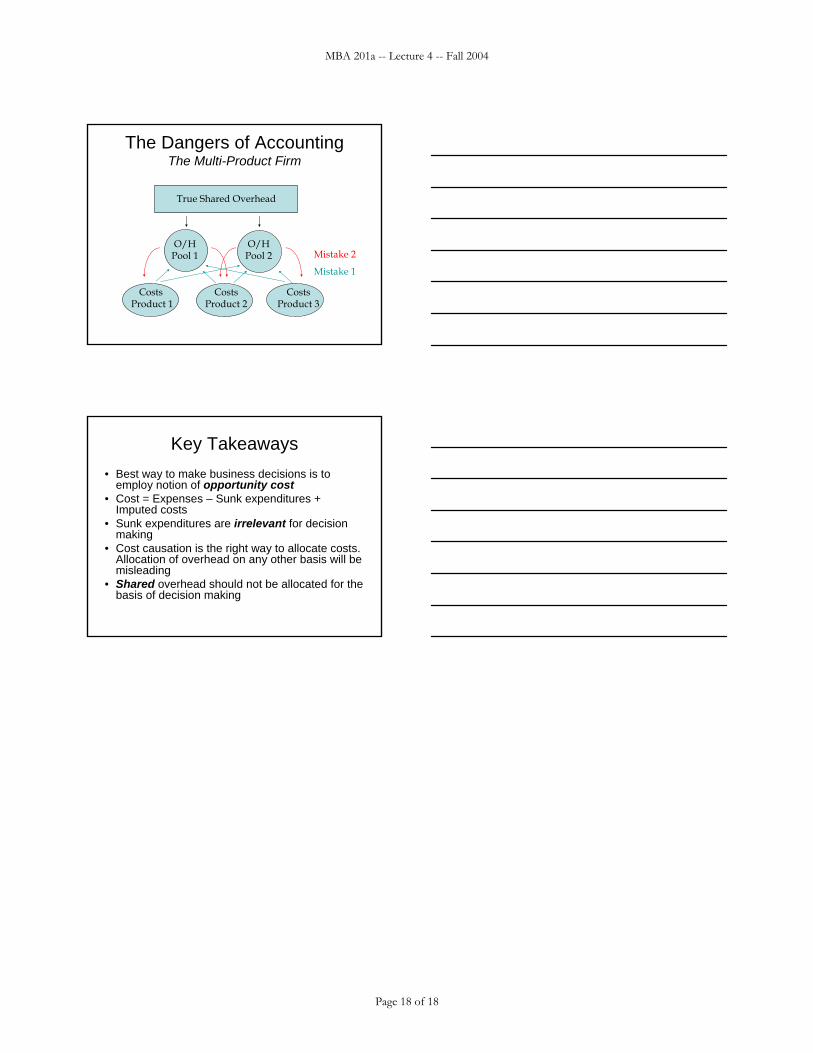

The Dangers of AccountingThe Multi-Product Firm

True Shared Overhead

CostsProduct 1

CostsProduct 2

CostsProduct 3

The Dangers of AccountingThe Multi-Product Firm

True Shared Overhead

CostsProduct 1

CostsProduct 2

CostsProduct 3

O/HPool 1

O/HPool 2

The Dangers of AccountingThe Multi-Product Firm

True Shared Overhead

CostsProduct 1

CostsProduct 2

CostsProduct 3

O/HPool 1

O/HPool 2

Mistake 1

MBA 201a -- Lecture 4 -- Fall 2004

Page 17 of 18

The Dangers of AccountingThe Multi-Product Firm

True Shared Overhead

CostsProduct 1

CostsProduct 2

CostsProduct 3

O/HPool 1

O/HPool 2

Mistake 1

Mistake 2

Key Takeaways• Best way to make business decisions is to

employ notion of opportunity cost• Cost = Expenses – Sunk expenditures +

Imputed costs• Sunk expenditures are irrelevant for decision

making• Cost causation is the right way to allocate costs.

Allocation of overhead on any other basis will be misleading

• Shared overhead should not be allocated for the basis of decision making

MBA 201a -- Lecture 4 -- Fall 2004

Page 18 of 18