Embed Size (px)

DESCRIPTION

Classification of Cost

Citation preview

Cost Classifications

Chapter 1

Classification of cost

According to:

1. Elements

2. Nature

3. Function

4. Normality

5. Control-ability

6. Time

7. Decision making

The Product

Materials Labour Expense

Elements of Costs

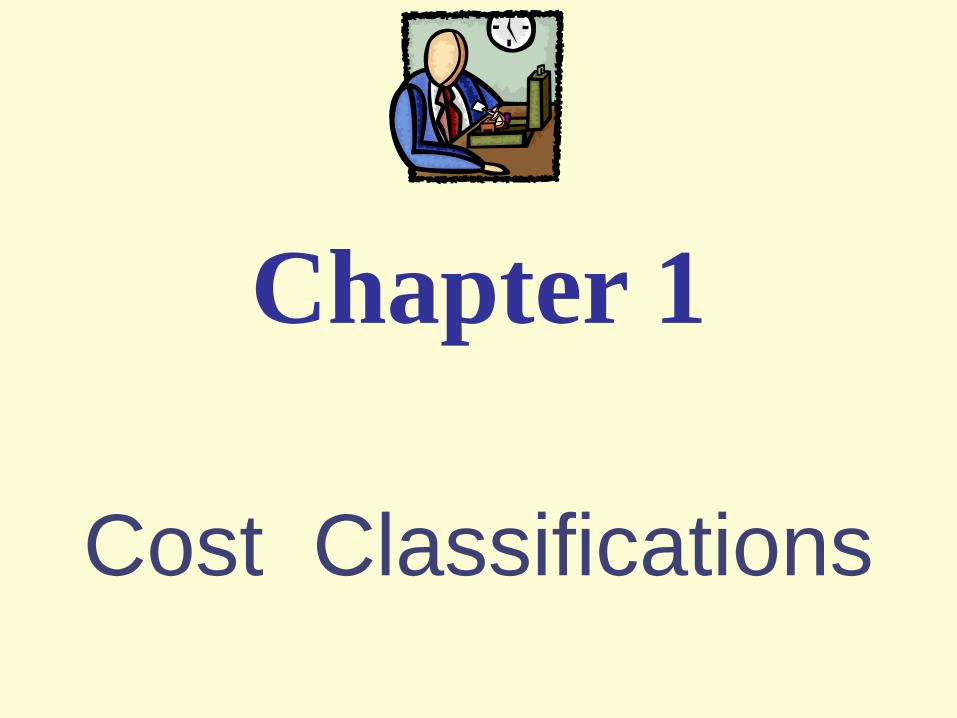

Direct Materials

Those materials that become an integral part of the product and that can be conveniently

traced directly to it.

Example: A radio installed in an automobile

Indirect Material

Those materials that do not become an

integral part of the product but which

helps in production.

Example: indirect materials

Materials used to support the production process. Examples: lubricants and

cleaning supplies used in the automobile assembly plant.

Direct Labor

Those labor costs that can be easily traced to individual units of product.

Example: Wages paid to automobile assembly workers

Indirect Labour

Those labor costs that cannot be easily

traced to individual units of product.

Examples: Indirect labor

Wages paid to employees who are not directly

involved in production work.

Examples: maintenance workers, janitors and security

guards.

Expense

Expenses are of two types:

Direct expense

Indirect expense

Expense

Direct expense is an expense which is incurred with manufacture of a product.

Eg: Purchase of raw materials, factory labour, factory wages, electricity

Indirect expense also called as overhead are additional expenses which are incurred on bringing a product to final customer.

Eg: Sales and Distribution, Office Salary, office electricity, office water, printing and stationery, outsourcing expenses, advertising expenses etc.

Direct and Indirect cots

Direct costs

Costs that can be easily and conveniently traced to a unit of product or other cost objective.

Examples: direct material and direct labor

Indirect costs

Costs cannot be easily and conveniently traced to a unit of product or other cost object.

Example: manufacturing overhead

Cost Behavior( nature)- fixed/

variable

How a cost will react to changes in the level of business activity.

Total variable costs change when activity changes.

Total fixed costs remain unchanged when activity changes.

Cost Classifications by

Predicting Cost Behaviour

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remains

as activity level changes. the same over wide ranges

of activity.

Fixed Total fixed cost remains Fixed cost per unit goes

the same even when the down as activity level goes up.

activity level changes.

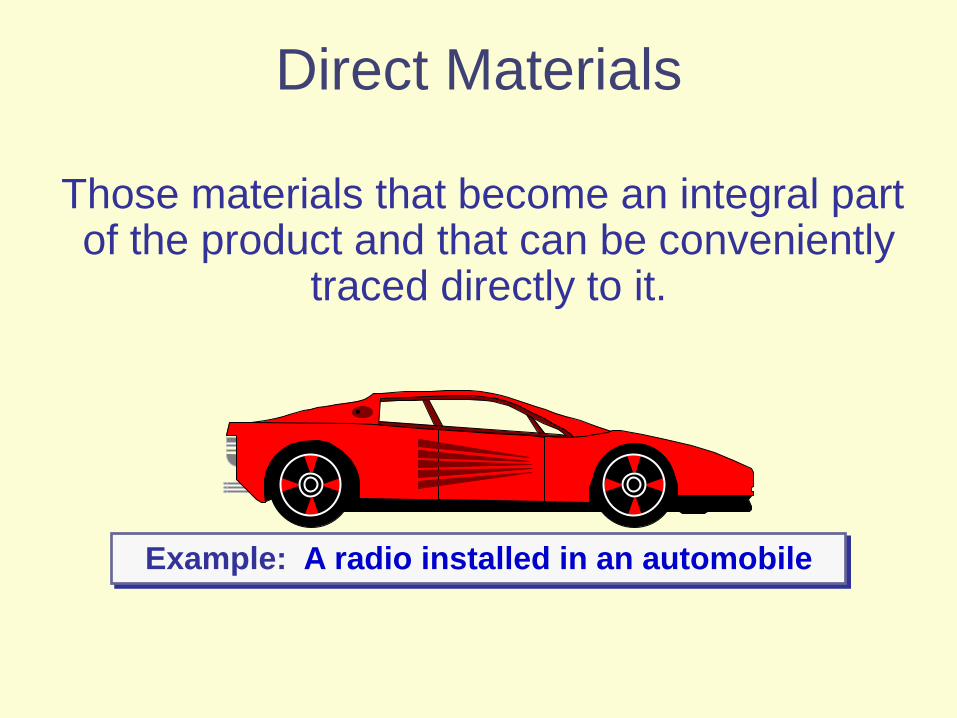

Variable Cost Per Unit

Per KBs used

Per

Min

ute

Te

lep

ho

ne

Ch

arg

e

The cost per KB of DATA is constant. For

example, Re.5 per KB.

DA

TA

CO

ST

Per

KB

Us

ed

Total Variable Cost

Your total DATA cost is based on how

many KB you use..

DATA used

Tota

l D

ATA

CO

ST

on

your

Cell

ph

one

Bill

Total Fixed Cost

Your monthly basic cellphone bill does not change when you make more calls.

Number of Local Calls

Mo

nth

ly B

asic

Tele

ph

one

Bill

NTT DoCoMo's wristwatch-style

cellphone

Fixed Cost Per Unit

Number of Local Calls

Mon

thly

Ba

sic

Tele

pho

ne

Bill

pe

r Lo

cal C

all

The average cost per call decreases as more

local calls are made.

Quick Check Variable/Fixed Costs

Which of the following costs would be variable

with respect to the number of cones sold at a

Baskins & Robbins shop? (There may be more

than one correct answer.)

A. The cost of lighting the store.

B. The wages of the store manager.

C. The cost of ice cream.

D. The cost of Tissue for customers.

E. Rent of the store

F. Cost of Chocolate sauce

Quick Check Variable/Fixed Costs

Which of the following costs would be variable

with respect to the number of cones sold at a

Baskins & Robbins shop? (There may be more

than one correct answer.)

A. The cost of lighting the store.

B. The wages of the store manager.

C. The cost of ice cream.

D. The cost of tissue for customers.

E. Rent of the store

F. Cost of Chocolate sauce

Quick Check Variable/Fixed Costs

Which of the following costs would be variable

with respect to the number of people who buy a

ticket for a show at a movie theater? (There

may be more than one correct answer.)

A. The cost of renting the film.

B. Royalties on ticket sales.

C. Wage and salary costs of theater

employees.

D. The cost of cleaning up after the show.

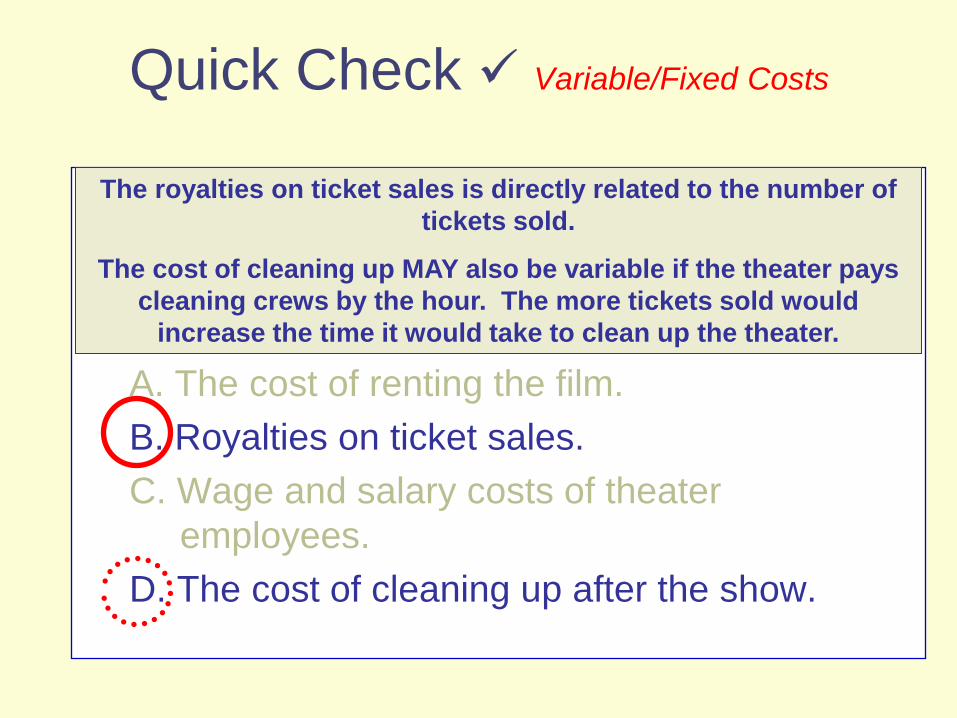

Quick Check Variable/Fixed Costs

Which of the following costs would be variable

with respect to the number of people who buy a

ticket for a show at a movie theater? (There

may be more than one correct answer.)

A. The cost of renting the film.

B. Royalties on ticket sales.

C. Wage and salary costs of theater

employees.

D. The cost of cleaning up after the show.

The royalties on ticket sales is directly related to the number of

tickets sold.

The cost of cleaning up MAY also be variable if the theater pays

cleaning crews by the hour. The more tickets sold would

increase the time it would take to clean up the theater.

By Function

Marketing and

Selling Cost

Costs necessary to get the

order and deliver the

product.

Administrative

Cost

All executive,

organizational, and

clerical costs.

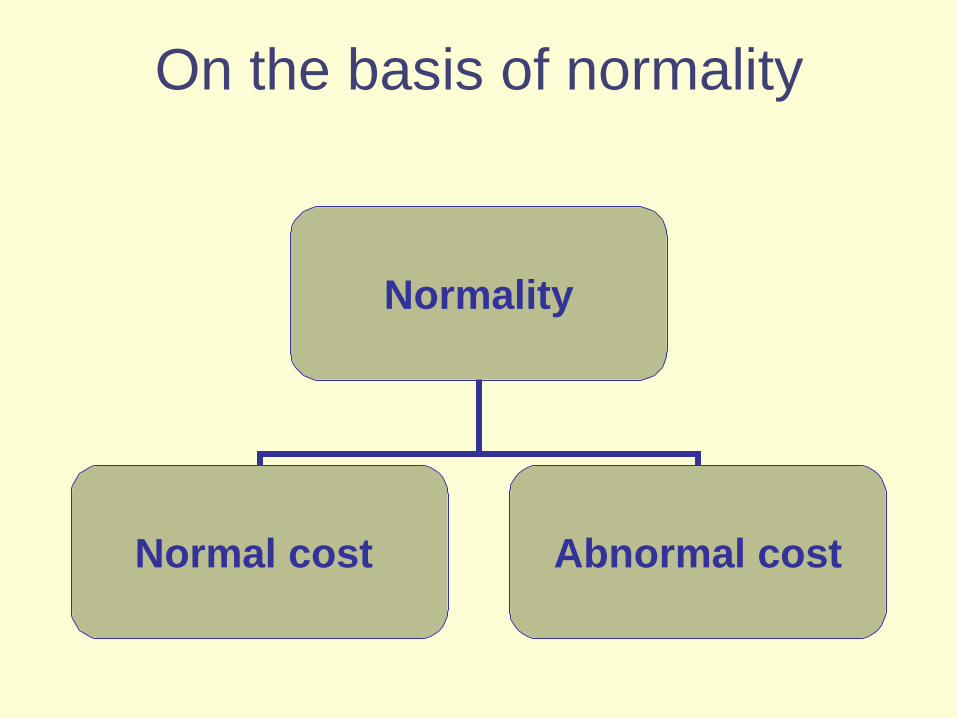

On the basis of normality

Normality

Normal cost Abnormal cost

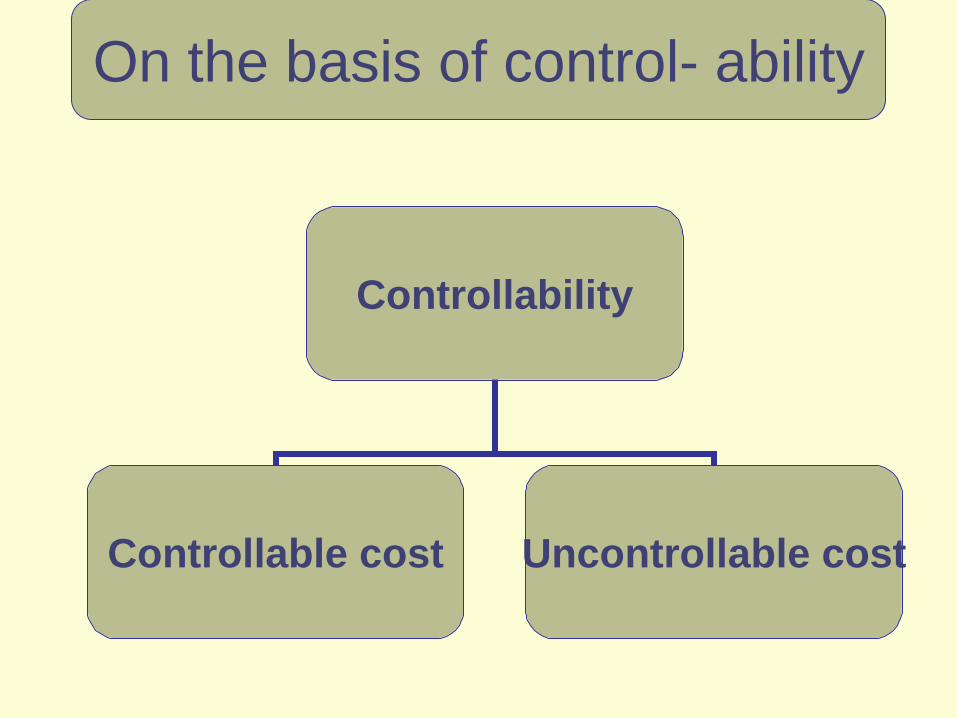

On the basis of control- ability

Controllability

Controllable cost Uncontrollable cost

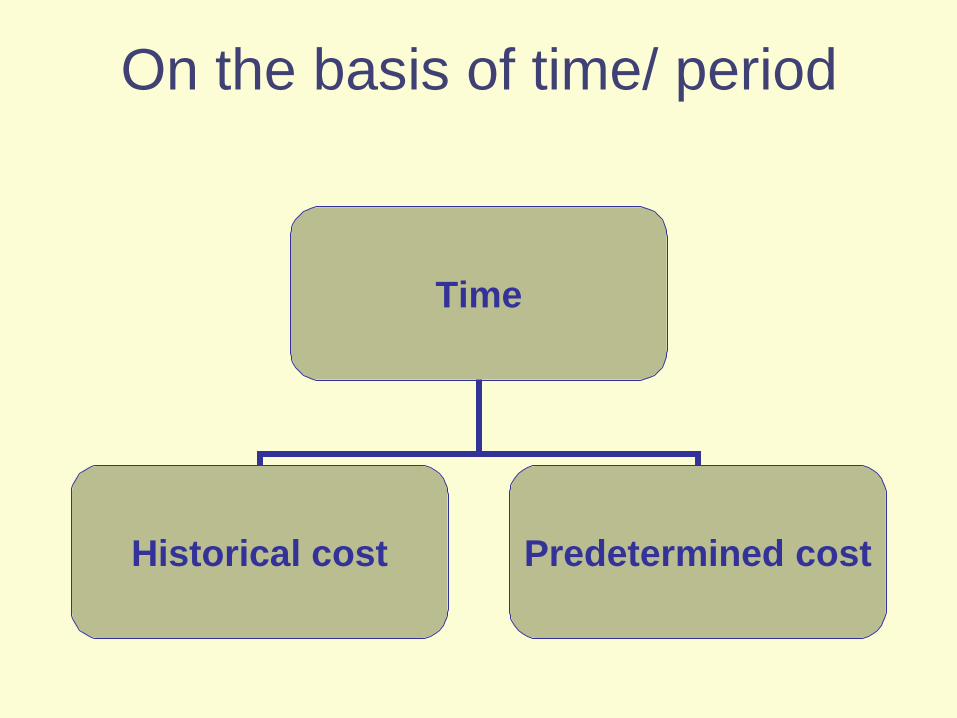

On the basis of time/ period

Time

Historical cost Predetermined cost

Product Costs Versus Period

Costs

Product costs include

direct materials, direct

labour, and

manufacturing

overhead.

Period costs are not

included in product

costs. They are

expensed on the

income statement.

Quick Check Period vs. Product Costs

Which of the following costs would be

considered a period rather than a product cost

in a manufacturing company?

A. Manufacturing equipment depreciation.

B. Property taxes on corporate headquarters.

C. Direct materials costs.

D. Electrical costs to light the production

facility.

Quick Check Period vs. Product Costs

Which of the following costs would be

considered a period rather than a product cost

in a manufacturing company?

A. Manufacturing equipment depreciation.

B. Property taxes on corporate headquarters.

C. Direct materials costs.

D. Electrical costs to light the production

facility.

On the basis of decision

making

Planning & Control

Standard cost Budgeted Cost

Differential Costs and

Revenues

Costs and revenues that differ among

alternatives. Example: You have a job paying Rs1,500 per month in

your hometown. You have a job offer in a neighboring

city that pays Rs 2,000 per month. The commuting

cost to the city is $300 per month.

Differential revenue is:

Rs2,000 – Rs1,500 = Rs500

Differential cost is:

Rs300

Decision-making-

Opportunity Costs The potential benefit that is

given up when one alternative

is selected over another.

Example: If you were

not attending college,

you could be earning

Rs15,000 per year.

Your opportunity cost

of attending college for

one year is Rs15,000.

© The McGraw-Hill Companies, Inc., 2003 McGraw-Hill/Irwin

Decision making-

Marginal cost

Marginal cost – cost of producing an

additional unit or output or service

Marginal costing differentiates the fixed

and variable costs

© The McGraw-Hill Companies, Inc., 2003 McGraw-Hill/Irwin

Decision making-

Replacement cost

Cost of replacing an asset

At current market price

Replacement Cost value is the amount

it would cost to repair or replace an item

with one of the same kind and quality as

the original — in today’s market.

Quick Check -Relevant -Irrelevant Cost

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly.

Is the cost of the pizza you ate last night relevant

in this decision? In other words, should the cost

of the pizza affect the decision of whether you

drive or take the train to Chenna?

A. Yes, the cost of the pizza is relevant.

B. No, the cost of the pizza is not relevant.

Quick Check Relevant -Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the cost of the pizza you ate last night relevant

in this decision? In other words, should the cost

of the pizza affect the decision of whether you

drive or take the train to Chenna?

A. Yes, the cost of the pizza is relevant.

B. No, the cost of the pizza is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the cost of the train ticket relevant in this

decision? In other words, should the cost of the

train ticket affect the decision of whether you

drive or take the train to Chenna?

A. Yes, the cost of the train ticket is relevant.

B. No, the cost of the train ticket is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the cost of the train ticket relevant in this

decision? In other words, should the cost of the

train ticket affect the decision of whether you

drive or take the train to Chennai?

A. Yes, the cost of the train ticket is relevant.

B. No, the cost of the train ticket is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the annual cost of licensing your car relevant in

this decision?

A. Yes, the licensing cost is relevant.

B. No, the licensing cost is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the annual cost of licensing your car relevant in

this decision?

A. Yes, the licensing cost is relevant.

B. No, the licensing cost is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the depreciation on your car relevant in this

decision?

A. Yes, the depreciation is relevant.

B. No, the depreciation is not relevant.

Quick Check Relevant Irrelevant Costs

Suppose you are trying to decide whether to

drive or take the train to Chennai to attend a

concert. You have ample cash to do either, but

you don’t want to waste money needlessly. Is

the depreciation on your car relevant in this

decision?

A. Yes, the depreciation is relevant.

B. No, the depreciation is not relevant.

Depreciation that

is a function of miles driven

would be relevant.

Depreciation that is a

function of the passage of

time would not be relevant.

Sunk Costs

Sunk costs cannot be changed by any decision. They are not differential costs and should be

ignored when making decisions.

Example: You bought an automobile that cost

Rs100,000 two years ago. The Rs100,000 cost

is sunk because whether you drive it, park it,

trade it, or sell it, you cannot change the

Rs100,000 spent

Quick Check Sunk Costs

Suppose that your car could be sold now for

Rs50,000. Is this a sunk cost?

A. Yes, it is a sunk cost.

B. No, it is not a sunk cost.

Quick Check Sunk Costs

Suppose that your car could be sold now for

Rs.50,000. Is this a sunk cost?

A. Yes, it is a sunk cost.

B. No, it is not a sunk cost.