Embed Size (px)

Citation preview

Corporate Social Responsibility and Stakeholder Governance

Around the World

Hoje Jo*, Moon H. Song**, and Albert Tsang***

*Gerald and Bonita Wilkinson Professor of Finance and Department Chair

Leavey School of Business, Santa Clara University

**Professor of Finance

College of Business Administration, San Diego State University

***Assistant Professor of Accounting

School of Accountancy, Chinese University of Hong Kong

October 7, 2014

Abstract In this paper, we examine the impact of stakeholder governance on corporate social

responsibility (CSR) around the world to determine whether CSR is employed as a

mechanism to mitigate conflicts of interest between managers and diverse stakeholders, or

used as managerial perquisites. To examine this relation properly, we not only employ a

large and extensive sample of international firms, but also control for endogeneity by using

dynamic panel generalized method of moments (GMM), propensity score matching, and

difference-in-difference approach. Our results suggest that stakeholder governance

positively influences firms’ CSR engagement with a greater magnitude than board

governance after controlling for endogeneity and other confounding factors of traditional

corporate governance mechanisms, firm characteristics and national factors. Stakeholders’

influence in CSR engagement is more prevalent when investor protections and board

governance are relatively weak.

Keywords: Corporate Social responsibility; Stakeholder Governance; Board

Governance; Conflict resolution; Management Perquisite

* Jo (corresponding author) is in the Department of Finance, Leavey School of Business,

Santa Clara University, 500 El Camino Real, Santa Clara, CA 95053-0388, (408) 554-4779,

(408) 554-5206 (fax), Email: [email protected]. We thank Ye Cai, Sandra Dow, Joseph T.

Mahoney, Niki Den Nieuwenboer, Maretno A. Harjoto, Hellen Jo, Woo Chan Kim, Yongtae

Kim, Tammy Madsen, Jungbien Moon, Carrie Pan, Lawrence C. Rose, Chamu

Sundaramurthy, Lorne Switzer, Yulia Veld-Merleoulova, and Demir Yener and Korea

University Business School (KUBS) for many valuable comments. We also appreciate

Sebastian Brinkmann of MSCI ESG for generously providing us the ESG IVA database and

research assistance provided by Jinhua Cui and Hyunil Lim at Korea University Business

School (KUBS). This study was initiated while Jo was visiting KUBS.

1

Introduction

Corporate governance takes up a central role in many academic disciplines.

Management, accounting, business law, economics, and finance scholars, among others,

examine the relation between parties of interest to corporations. To date, these collective

efforts have centered on agency theory (Dalton et al. 2007), which emphasizes the conflicts

of interest among diverse stakeholders arising from the separation of ownership and control

in corporations (Jensen and Meckling 1976; Eisenhardt 1989). While corporate governance

aims to minimize the conflicts of interest, these agency conflicts cannot be removed

completely by a firm’s governance mechanisms. Thus the debates related to our

understanding and conceptualization of the agency problem and related governance

mechanisms continuously grow.

The theoretical foundations of these debates relate to the primacy of the various

stakeholders 1 in the corporation. First, the so-called shareholder primacy model re-

emphasizes that shareholders, as the legal owners, hold residual claim of the firm, and thus

hold primacy over any other stakeholder in the corporation (Eisenhardt 1989; Bebchuk 2005;

2006). Second, the alternative model, dubbed the stakeholder primacy model (Bainbridge

2003), highlights that all stakeholders join in team production; thus, the objective of the firm

is to maximize the risk-adjusted returns to all participants (Lan and Heracleous 2010). While

the shareholder primacy view advocates value creation for the shareholder, the stakeholder

primacy model promotes value creation for the corporation as a whole.

Well-designed corporate governance systems according to the stakeholder primacy

model should align managers' incentives with those of nonfinancial stakeholders, and reduce the

conflicts of interest between management and stakeholders; not only do good stakeholder

relations help firms to gain performance advantages, but they enable those performance

advantages to persist (Choi and Wang 2009). Kacperczyk (2009) also contends that catering

to non-shareholding stakeholders contributes to the long-term value of the firm. Freeman

(1984) argues that firms can use corporate social responsibility (CSR) as an extension of

1 Mahoney (2012) defines stakeholders as “…those persons and groups who contribute to the wealth-

creating potential of the firm and are its potential beneficiaries and/or those who voluntarily or

involuntarily become exposed to risk from the activities of a firm…Thus, stakeholders include shareholders,

holders of options issued by the firm, debt holders, employees (especially those investing firm-specific

human capital), local communities, environment as latent stakeholders, regulatory authorities, the

government, inter-organizational alliance partners, customers and suppliers”.

2

effective governance mechanisms to resolve conflicts between managers and non-investing

stakeholders, and Mannix (2003) maintains that conflict resolution and conflict management

should be an essential part of a group’s strategic management decision-making process. On

the other hand, Zajac and Westphal (1994) claim that there are costs associated with

governance mechanisms, and top managers prefer to take value in the form of perks. Baron

(2009) asserts that managers can opportunistically invest in CSR as a management perquisite.

In this paper, we examine the relation between stakeholder governance and firms’ CSR

activities across countries to determine whether CSR is employed as a mechanism to mitigate

the conflicts of interest between managers and stakeholders, or used as management perks. To

the best of our knowledge, there is little evidence for an international set of firms on the

significance or economic magnitude of this CSR-stakeholder governance relation. Thus, our

study pertains not only to the literature on how conflict resolution or management perquisite

influences corporate strategy but also provides a novel empirical lens on the increasingly

important context of CSR. Previous studies have empirically examined the role of CSR

across a broad set of countries (e.g., Maignan and Ralston 2002; Chapple and Moon 2005;

Jackson and Apostolakou 2010) or the empirical determinants of CSR based on social and

environmental metrics (Ioannou and Serafeim 2012). Their main focus, however, is not on

stakeholder governance.

While board governance is extensively documented, shareholder governance is

relatively less examined, and there is no universally accepted definition of stakeholder

governance. 2 We define stakeholder governance as the stakeholder orientation of corporate

governance pertaining system of checks and balances that trade off benefits and costs of firm

decisions and that provide various incentives, controls, and regulations to minimize conflicts

of interest between firms and stakeholders, to maintain financial stability, and to prevent

potential corruption and fraud. Despite the lack of a universally agreed-upon definition of

stakeholder governance, we are keenly interested in the impact of incremental contribution of

2 Spitzeck and Hansen (2010) define stakeholder governance mechanisms as the system of how

stakeholders influence corporate decision making and help align the worldviews of those inside and outside

the firm. Böhling (2011) defines stakeholder governance as the system of how multiple stakeholders bring

diverse stakeholders together, negotiate collectively on regulatory arrangements for the provision of

stability, and provide a means to accommodate competing interests in decision-making in the global

economy. We closely follow the MSCI ESG IVA’s definition of stakeholder governance as multi-

stakeholder initiated strategic governance (see more details in data, measurement, and research design

section as well as Appendices I and II).

3

stakeholder governance on CSR engagement after controlling for board governance, CEO

ownership, analysts’ indirect monitoring, institutional investor ownership, auditor monitoring,

and other confounding firm and national factors.3

CSR has continued to be highly popular, but contentious subjects over the previous

thirty-year history of academic research. Corporations across the globe have become more

alert to CSR issues since CSR can be considered important non-financial information

(Dhaliwal et al. 2011, 2012). Although an increasing number of firms are engaged in a

serious effort to define and integrate CSR into various aspects of their businesses, the

discussions pertaining CSR continue to grow without a clear consensus on its meaning or

value to stakeholders. Many studies suggest that while the definitions of CSR vary, it

generally refers to serving people, communities, and the environment in ways that go above

and beyond what is legally required of a firm (McWilliams and Siegel 2001; Margolis and

Walsh 2003; Orlitzky et al. 2003; Ioannou and Serafeim 2012; Jo and Harjoto 2011, 2012,

2014).

Our findings reveal several empirical regularities. First, without controlling for

endogeneity, our empirical results suggest that CSR is significantly and positively associated

with both stakeholder governance and board governance, but stakeholder governance reveals

a much higher significance than board governance after controlling for various firm and

international characteristics, suggesting that stakeholder governance is more important in

engaging CSR activities across countries than board and other governance mechanisms. This

finding is generally supportive of Jensen (1993) who claims that internal board governance is

not the most effective during the last decade, and therefore other external governances

become more important.

Second, the engagement of CSR activities in different countries is also found to be

affected by country-level institutions, especially in countries characterized by weak investor

protections and weak board governance. Stakeholders play a more salient role in CSR

activities when board governance and/or legal environments are relatively weak, presumably

3 While multi-stakeholder initiatives in CSR engagement from NGOs, corporations, scientific communities,

governments and international organizations are quite prolific, there are significant shortcomings in

practices of stakeholder governance. Stakeholder inclusion and governance, unfortunately, is neither

representative nor balanced, decision-making procedures fall short of transparency, and monitoring

mechanisms are largely unexplored (Böhling 2011).

4

because the stakeholder governance complements the weak board governance and investor

protections in international CSR markets.

Third, when we control for endogeneity4 using dynamic GMM, while the positive

association between CSR and stakeholder governance is still preserved, CSR-board

governance relation becomes insignificant. This insignificant relation between CSR and

board governance is supportive of Wintoki et al. (2012) who find that board independence is

insignificantly related to financial performance when they control for endogeneity by

employing dynamic panel GMM. Our results remain robust even after we control for the

endogeneity of the selection between CSR and stakeholder governance using propensity

score matching. Based on the difference-in-difference approach following Bertrand and

Mullainathan (2003), we further find that the impact of stakeholder governance on CSR is

growing after the global financial crisis, indicating more demand for stakeholder governance

after crisis, due to internal governance breakdown.

The remainder of the paper is organized as follows. We briefly discuss related

literature and develop two hypotheses of conflict resolution vs. management perquisite under

resource constraint in Section 2. We discuss the sample and measurement of CSR and CG as

well as our research design in Section 3. Section 4 presents the empirical results and

additional analyses. Section 5 summarizes our conclusions, the limitation of this study and

potential future research avenue.

Hypotheses Development

In this paper, we study the empirical determinants of international CSR engagement

with a particular emphasis on stakeholder governance (hereafter, SGOV). Specifically, we

examine the following hypotheses that relate SGOV and CSR engagement of firms around

the world.

4 Potential sources of cause and effect problems in CSR-governance studies could include the omission of

some important variables, reverse causality, and measurement error in the variables of interest (Roberts and

Whited 2011; Reeb et al. 2012). To examine properly the relation between stakeholder governance and

CSR across countries, we control for endogeneity as well as serial autocorrelation of CSR scores by using

dynamic panel generalized method of moments (GMM) that are known to cure both endogeneity and

autocorrelation problems reasonably well (Reeb et al. 2012; Wintoki et al. 2012). To further control for

endogeneity, we also employ propensity score matching (PSM) method following the seminal work of

Rosenbaum and Rubin (1983) as well as differences-in-differences approach following Bertrand and

Mullainathan (2003).

5

Conflict-Resolution Hypothesis

The stakeholder position that raises the most controversy takes into account the degree

to which firms should allocate limited resources to satisfy the needs and demands of a broad

group of stakeholders beyond and above what is necessary for the normal stakeholder

inclusion and participation (i.e., Harrison and Freeman 1999; Jensen 2001; Harrison et al.

2010). Some firms allocate both firm resources and decision-making influence widely across

diverse stakeholder networks (Sisodia et al. 2007). This sort of firm behavior is called as

‘managing for stakeholders’ (Freeman et al. 2007; Harrison et al. 2010). Mahoney (2012)

summarizes the benefits of stakeholder management and suggests that modern property rights

stakeholder theory recognizes the role each of these stakeholder groups plays in the creation

and distribution of the economic value.5 This stakeholder management approach is in sharp

contrast to the shareholder wealth maximization goal (Friedman 1962; Jensen 2001).

In rapidly changing modern organizations, conflict is an inevitable phenomenon that

hinders performance over the entirety of firm life (Mannix 2003).6 Corporate governance

literature identifies various settings for conflicts within stakeholder groups or intra-

stakeholder conflicts, such as those among owners (Bergloff and von Thadden 1994;

Hoskisson et al. 2002) or creditors. While there are several compelling explanations for inter-

stakeholder conflicts, such as agency theory (Jensen and Meckling 1976; Eisenhardt 1989) or

class politics (Roe 1994, 2003), there is a dearth of intra-stakeholder conflict examined in the

prior literature (Carney et al. 2011).

According to Freeman’s (1984) stakeholder theory, firms could use CSR to resolve

conflicts between managers and non-investing stakeholders. While it may not be completely

possible to satisfy all related stakeholders, there is a growing CSR literature on conflict

resolution based on stakeholder theory (e,g., Jensen 2002; Calton and Payne 2003; Sherer et

al. 2006; Cespa and Cestone 2007; Jo and Harjoto 2011; 2012), in which the role of the

5 Clearly, while there are potential problems in moving towards a stakeholder perspective, such as potential

increased discretion on the part of management and increased costs of corporate decision-making (Tirole

2001), there are potential benefits of moving to the stakeholder view.

6 The field of conflict and conflict resolution stems from a strong theoretical focus, initiated by the

groundwork of Walton and McKersie’s (1965) study on labor relations and bargaining, Deutsch’s (1973)

work on competition and cooperation in the resolution of conflict, and Rubin and Brown’s (1975)

explication of the social psychology of negotiation.

6

corporation is to serve the interests of non-investing stakeholders. Cespa and Cestone (2007),

in particular, propose a theoretical model investigating the conflicts of interest among

managers, shareholders, and other non-investing stakeholders, when managers are not

performing. In addition, management also considers firms’ fiduciary responsibilities toward

stakeholders (Del Guercio 1996; Jensen 2002; Aguilera et al. 2007). From the stakeholder

theory perspective, stakeholder governance needs to give a voice to diverse stakeholders to

secure their contribution to the success of the firm and stakeholder management should lead

to improved shareholder value creation (Hillman and Keim 2001; Ulrich 2008).

Top management also could use CSR to address social pressure that originates from

various stakeholders (Baron 2009). There is a consensus that corporations engage in CSR as

a response to social or stakeholder pressures. Indeed, stakeholder pressures may come from

many different forms, including pressures from investors’ preference for social giving

(DellaVigna et al. 2012), from community stakeholder groups regarding environmental issues

(Kassinis and Vafeas 2006), from consumers (Besley and Ghatak 2007), from the

competitive market structure (Fisman et al. 2008), and from non-governmental organizations

(NGOs) from the society (Baron 2009). Hong and Kacperczyk (2009) find that firms with

products that are considered harmful to the society (alcohol, tobacco and gambling) are

followed by less number of analysts and held less by institutional investors who are norm-

constrained. Thus, those sinful industry firms receive social pressures from reduced analyst

coverage and shrunken institutional ownership.

Resolving conflicts-of-interest and/or relieving stakeholder pressure are consistent with

stakeholder theory in which firms undertake social activities to balance the conflicts-of-

interest or to mitigate competing pressures from stakeholders. CSR undertaken to lessen the

conflicts-of-interest or the threat of social pressure are also strategic (Porter and Krammer,

2002, 2006). For instance, when activists have provided negative coverage on oil spill by

large oil companies such as BP and Exxon, 7 putting indirect, but additional pressure on firms,

7 Nye (2012) suggests that “the U.S. Department of Justice has accused British oil giant BP of gross

negligence, incompetence and a 'culture of corporate recklessness' in the 2010 Gulf of Mexico oil spill - in

a legal filing which could result in a massive $25 billion fine. In a federal court submission last Friday

(August 30, 2012), the Department of Justice (DOJ) offered its clearest signal that it will press for the

maximum possible penalties in a court of law against the British multinational, which is the fourth largest

firm of any company listed on the London Stock Exchange. BP has indicated that it will defend itself

against any action brought by the DOJ, but the threat of larger than anticipated compensation payments

caused BP's shares to drop four percent on Wednesday, wiping more than three percent or $4.77 from its

7

and consequently, firms either attempt to be more careful and reduce their irresponsible

activities or provide strategic CSR. In addition, firms often engage in normative CSR

activities that are not required by laws and regulations. For instance, Johnson and Johnson

strategically launch its Project Phoenix to help cooperatives in Brazil to enhance workers

conditions, although not required by law (Johnson and Johnson Annual Repot 2011).

In accordance with the conflict-resolution hypothesis, to the extent that firms use CSR

engagement as an effective communicative mechanism to resolve conflicts between

managers and stakeholders, CSR engagement should be positively related to SGOV. Because

conflict resolution is considered to be a dynamic part of a group’s interaction process

(Mannix 2003), cross-cultural and/or international settings in conflict resolution could also

provide strategic value of CSR activities. Taken together, we expect the following;

Hypothesis 1: To the extent that CSR is used as a mechanism for conflict resolution between

managers and stakeholders, we expect a positive association between CSR and SGOV around

the world.

Management Perquisites Hypothesis

Scholars have debated the attributes of management perquisites for more than three

decades. Jensen and Meckling (1976) maintain that CEO perks can be viewed as an agency

problem between managers and shareholders, because managers not only have greater

incentive to consume corporate resources for their own personal private benefit, but also have

more inducement to adversely affect the value of the firm through low percentages of

managerial ownership. Fama (1980) suggests that perks can be a motivational tool as a part

of optimal compensation contract to enhance shareholder value. Zajac and Westphal (1994)

claim that executives may prefer to take value in the form of perks. Few scholars, however,

believe that CEO perquisites represent an efficient way to monitor or influence executives.

Recent studies show that the relation between perks and short-run abnormal return is negative

(Rajan and Wulf 2006; Yermack 2006; Grinstein et al. 2011). Grinstein et al. (2011), in

particular, find that perks are positively related to CEO power and free cash flow, while

negatively associated with a firm’s growth opportunities.

market value.” (Read more: http://www.dailymail.co.uk/news/article-2199064/BP-labelled-incompetent-

Gulf-oil-spill-U-S-Department-Justice-threatens-British-firm-25-billion fine.html#ixzz2GZtKkAoj).

8

Baron (2009) similarly argues that managers could undertake CSR activities because of

their own personal interests. That is, social activities could be perquisites for managers based

on their own moral, warm glow, or self-interested preferences. Managers could enjoy the

social accolades that can come from pressure groups and NGOs or receive moral satisfaction

from benefitting others. CSR as a perquisite should depend on the discretion managers have

to serve their own interests and on the resources available to managers; i.e., the financial

resources of the firm.

In addition, managers may have a myopic view and a shorter time horizon (short

termism) than shareholders and in their pursuit of promotion may aim at early returns and

fast rewards even at the cost of shareholders’ as well as stakeholders’ long-term interests

(Jensen & Meckling 1976). Furthermore, although the objective of the firm is to maximize

shareholders’ wealth under the standard shareholder wealth maximization (SWM) model,

managers may use corporate resources to provide themselves with various perquisites.

Obviously, there is a separation between ownership and control, and there is no reason to

believe that managers will always act in the best interest of the shareholders and diverse

stakeholders. Pandher and Currie (2013) argue that the CEO and other firm stakeholders

compete over the firm’s resource surplus as utility-maximizing claimants based on their

relative bargaining power. Consequently, stakeholders will monitor managerial decisions to

make sure that management makes every decision in a way that maximizes firm value and

will put in place incentives that align managerial interests with those of stakeholders. Cheng,

et al. (2014) provide evidence that both better stakeholder engagement and transparency

around CSR performance are important in reducing capital constraints. Because the firms’

financial resources are typically limited in difficult economic period and any returns from

implementing CSR programs usually have a longer time horizon, non-shareholding

stakeholders will be more likely to monitor and enforce managers to focus on the long-term

value of the firm, but not to engage in CSR as a perquisite (Kacperczyk 2009). Thus, the

management perquisite hypothesis based on agency theory will predict the following;

Hypothesis 2: To the extent that CSR is used as a tool for management perquisite, we expect

an inverse association between CSR and SGOV around the world.

Clearly, the null hypothesis for the above two hypotheses is that CSR engagement is not

associated with SGOV mechanisms.

9

Data, Measurement and Research Design

Data

The data set is assembled from MSCI Environmental, Social, and Governance (ESG)

Intangible Value Assessment (IVA) Database. The IVA universe coverage currently

comprises the following: Top 1,500 companies of the MSCI World Index; Top 25 companies

of the MSCI Emerging Markets Index; Top 275 companies by market cap of the FTSE 100

and the FTSE 250 excluding investment trusts; and ASX 200 across 36 countries or districts.

And they provide ratings of 1,859 companies in their active universe and archived ratings for

an additional 658 previously rated companies. From ESG IVA database, we obtain various

measures of CSR as well as BGOV and SGOV. We choose MSCI ESG IVA database

because they specifically provide multi-stakeholder initiated strategic governance ratings.

We obtain the number of analysts following the firm (ANAL) from the I/B/E/S database.

In addition, because we use various accounting and financial information, we require that

sufficient Compustat domestic and global databases and firm risk measured by the standard

deviation of monthly stock price returns from Worldscope/Datastream data are available for our

tests. Other governance and monitoring mechanisms, such as, institutional ownership (IIOWN),

CEO ownership (CEO), and Big four auditor or not (BIG4) are compiled from Capital IQ, and

block holders (BLOCK) are proxied by the number of large shareholders from Compustat

domestic and global databases. This sample procedure produces a combined sample of 5,072

firm-year observations from 2006 to 2011.8 Actual samples used in the analyses are slightly

different because the data availability is different for each regression analysis.

Dependent Variable: CSR Measurement

MSCI ESG database provides three main Intangible value Assessment (IVA) variables

of human capital, environmental issues, and stakeholder capital.9 Our main measure of CSR

8 While MSCI ESG IVA (former Innovest) database is available from 1999, MSCI ESG provided us the

2006-2011 period of sample that are more complete than the earlier period of relatively incomplete 1999-

2005 sample. ESG IVA database is used by several previous studies (see, e.g., Derwall et al. 2005; Aktas et

al. 2011; Vasia and King 2012 to name a few).

9 Human capital is comprised by workplace practices, labor relations, and health and safety issues.

Workplace practices include workforce diversity, policies and programs to promote diversity, work/life

10

index (CSRIDX) is the arithmetic average of all 26 IVA social ratings subsets of human

capital, environmental issues, and stakeholder capital (see appendix I for the details of the 26

CSR dimensions). We compute CSRIDX such that the highest CSRIDX scoring firm gets a 10

while the lowest-scoring company obtains a 0. 10

Main Independent variable: Stakeholder Governance

While collecting firm-level CG information across countries is difficult, mainly due to

differences in the quality of disclosure across countries, ESG IVA provides firm-level

partnership in multi-stakeholder initiatives (SGOV) information across countries. ESG IVA

multi-stakeholder initiated SGOV key issues include four specific areas including (i)

corruption and instability, (ii) financial instability, (iii) business ethics and fraud, and (iv)

anti-competitive practices. 11 Specifically, first, SGOV issues encompass corruption and

instability issues evaluating the extent to which companies are at risk of suffering operational

disruptions or loss of market access due to violence, property destruction or sabotage,

political instability, demands for bribes, and costly litigation related to corrupt practices.

Companies that have programs, guidelines, and clear policies to avoid corrupt business

dealings, that have strong partnerships with local communities, one of important stakeholders,

and that have high level of disclosure and transparency score higher on this key issue.

benefits, discrimination-related controversies. Labor relations contain labor management issues related to

policies, programs, benefits, employee-related controversies, union relations. Health and safety (H&S)

issues include policies and systems, implementation and monitoring of those systems, performance (injury

rate, etc.), safety-related incidents and controversies.

10

Our second measure of CSR index (CSRIDX_I) is the arithmetic average of three main Intangible value

Assessment (IVA) variables of human capital, environmental issues, and stakeholder capital. We also

compute CSRIDX_I such that the highest CSRIDX_I scoring firm gets a 10 while the lowest-scoring

company obtains a 0. Our third measure of CSR index (CSRIDX_II) is the aggregated CSR score coded

directly from CSR rating assigned by Intangible Value Assessment (IVA), CSR rating of AAA, AA, A,

BBB, BB, B, CCC, and CC are coded as 8, 7, 6, 5, 4, 3, 2, and 1, respectively. The results of CSRIDX-

SGOV, and other CSRIDX-independent variable regressions to be presented later in empirical results

section are qualitatively very similar when we use CSRIDX_I and CSRIDX_II as dependent variables. To

conserve the space, we only report results when we use the CSRIDX as dependent variable.

11

One caveat of SGOV scores reported in ESG IVA database is not detailed enough to reveal how each

specific stakeholder initiates the above four particular key issues. Nevertheless, we consider that ESG

IVA’s multiple-stakeholder initiated strategic governance scores provide important first-step SGOV

information to understand the empirical association between CSR and stakeholder initiated strategic

governance because international SGOV information was not empirically available in the prior CSR and

CG literature.

11

Companies with a history of community opposition, that face security problems, and lack

transparency in ESG and financial information score lower on this key issue.

Second, SGOV covers firm-level financial stability that evaluates the extent to which a

company institutes strong governance structures, demonstrates a high level of transparency,

and avoids large scale controversy score well on this key issue. Companies that are large and

deeply interconnected to other financial institutions (as creditors that are other important

stakeholders), but have limited checks and balances in their governance structures and have

incentives for short-term risk-taking at the expense of long-term economic value creation

score poorly on this key issue.

Third, SGOV addresses business ethics and fraud that evaluates the extent to which

companies face regulatory and legal risks or loss of investor confidence due to ethical issues.

Ethics and fraud includes a wide range of ethical and criminal violations, some of which

relate closely to CG issues, including but not limited to insider trading and dealings;

securities and accounting fraud; securities litigation; criminal behavior of directors or top

executives; and options backdating. Notice that Government agencies such as SEC also are a

part of stakeholders. Companies that have avoided controversies in these areas score higher

on this key issue, while companies that have faced moderate or severe controversies over the

past three years score lower. Fourth and last, SGOV contains anti-competitive practices that

evaluate the extent to which companies face regulatory risks relating to anti-competitive

practices. Notice that regulatory agencies also are a part of stakeholders. Companies that

have avoided controversies in this area score higher on this key issue, while companies that

have faced moderate or severe controversies over the past three years score lower (see MSCI

ESG IVA manual, 2012). The highest SGOV scoring firm also receives a 10 while the

lowest-scoring company receives a 0.

To check the robustness of our results, we replace our current SGOV variable with

variable which can be more directly linked to the ex-ante stakeholder commitment rather than

the ex-post measure. ASSET4 database differentiate between the ex-ante measure of CSR

driver and the ex-post measure of CSR outcome across environmental and social dimension,

and the ex-ante CSR driver consists of policy, implementation, monitoring and improvement

(variables measuring the ex-ante stakeholder commitment to certain dimensions). Thus, we

use the ASSET4’s ex-ante measure of CSR driver variables related to stakeholder governance

as a robustness check, which could be more appropriate measure of ex-ante stakeholder

governance (SGOV), to replace our SGOV variables to measure stakeholder governance.

12

Another Important Independent variable: Board Governance

MSCI ESG IVA provides firm-level BGOV information across countries. In particular,

MSCI ESG provides key issue score for corporate governance derived from a combination of

two data sources: the Governance Risk Indicators (GRId) provided by Institutional

Shareholder Services (ISS), an MSCI company, and the MSCI ESG Impact Monitor. The

GRId scores focus on four key areas including (i) board structure, (ii) shareholder rights, (iii)

compensation and remuneration, and (iv) auditing practices and controversies. Among those,

BGOV is based upon board independence, board diversity, compensation practices,

controversies involving executive compensation and governance, and the management of

CSR issues. The highest BGOV scoring firm receives a 10 while the lowest-scoring company

receives a 0.

Other Governance and Monitoring Mechanisms

To control for additional external monitoring, we employ the number of analysts

following the firm (ANAL) as a measure of analyst monitoring from the I/B/E/S database

during the same time period (Chung and Jo 1996; Yu 2008). Since the number of analysts

following the firm is highly skewed to the right (Lim 2001; Bushman et al. 2005), we

measure analyst coverage with the natural logarithm of one plus the number of analysts

following the firm (ANAL).

Monitoring by large shareholders has been considered an important governance

mechanism to mitigate agency problems (Berle and Means 1932; Demsetz 1986; Shleifer and

Vishny 1997). We employ international institutional ownership data compiled from Capital

IQ to measure large shareholder monitoring (Shleifer and Vishny 1986; 1997) by institutional

ownership (IIOWN).12

CEO ownership is also important as another internal governance mechanism in terms

of incentive alignment between managers and stakeholders (Jensen 1993). Previous studies,

12 In addition, as more number of shares outstanding (CSHO compustat variable) and less number of

shareholders (CSHR compustat variable) indirectly represent greater percentage of larger blockholder

holding, we use log(CSHO/CSHR) as a second-best proxy of log(blockholders). Although log(blockholders)

variable is not an accurate measure of large shareholder monitoring, we report the results in our empirical

analyses. Our main results (to be followed in empirical results section) of the positive association between

CSRIDX and SGOV (as well as BGOV) remain intact when we include or exclude the imperfect measure

of log (blockholders) variable (BLOCK) in our analyses.

13

however, typically focus on individual country and the impact of CEO ownership on

international CSR engagement is relatively under explored. Thus, we compile CEO

ownership (CEO) from Capital IQ as additional governance mechanism.

Viewing that major accounting scandals and global financial crisis associated with

massive accounting frauds, strengthening accounting transparency can be an effective way of

alleviating the agency problems. We include the existence of Big 4 auditing as a proxy of

accounting transparency, and measure accounting transparency based on whether the auditor

is one of the Big 4 auditors (BIG4) (PricewaterhouseCoopers (PwC), Ernst & Young, KPMG,

and Delloitte) or not (a dummy variable). Big4 is also compiled from Capital IQ.

Measurement of Firm Control Variables

We obtain financial variables from Compustat domestic as well as Compustat Global

databases, and we compute the firm risk proxied by the standard deviation of monthly stock

price returns from Worldscope/Datastream database. Other firm characteristics as control

variables generally follow Jo and Harjoto (2011, 2012) that include firm size measured by the

natural log of total assets (LOGTA), R&D expenditures divided by sales revenue (RNDR),

total debt divided by total assets (LEV), capital expenditure divided by sales revenue

(CAPXR), firm profitability by return on assets (ROA), sales growth (GROW), growth

opportunities measured by Tobin’s Q (TOBINQ), and firm risk measured by the standard

deviation of monthly stock returns (DEVRET).

Information transparency is known to be important for the development of a sustained

economy as it provides a viable disclosure mechanism for both investors and firms. We

anticipate that firm’s earnings management inversely influences CSR engagement because

information transparency tends to reduce earnings management (Jo and Kim 2007). Thus, we

measure earnings management using performance-adjusted discretionary total accruals

(ACCRUAL) following Kothari et al. (2005).13

Earnings management is also less likely for firms that disclose more information on a

persistent basis because the increased transparency lowers information asymmetry and helps

investors recognize earnings management. Conversely, incentives for earnings management

are likely to be high for firms when information asymmetry is high. Thus, we expect that

13 Our main results remain intact when we measure discretionary accruals based on modified Jones (1991)

model or discretionary total accruals as suggested by Hribar and Collins (2002) or by discretionary current

accruals following Rangan (1998).

14

CSR is an increasing function of information transparency across firms and a decreasing

function of the firm-level earnings management. Thus we proxy firm-level information

transparency based on analyst forecast error (FERROR).

Measurement of National Variables

With respect to national factors, it is well established in prior literature that information

transparency, legal environment, cultural, geographical, and other various types of distance

play important roles in international business, respectively. First, to measure country-level

transparency, existing cross-country research has relied to a larger extent on the Center for

International Financial Analysis Research (CIFAR) index of transparency, introduced by La

Porta et al. (1998). We follow La Porta et al. (1998) and Bushman et al. (2004), and employ

the CIFAR Index created by examining and rating companies’ 1995 annual reports on their

inclusion or omission of 90 items. These items fall into seven categories: general information,

income statements, balance sheets, funds flow statement, accounting standards, stock data,

and special items.

Second, country legality is shown to be an important prerequisite for economic

development in a country and it impacts firm performance in emerging economies. La Porta

et al. (1997, 1998, 1999), in their series of seminal papers, show that the legality of a specific

country, including the following factors: civil versus common law systems, efficiency of

judicial system, rule of law, corruption, risk of expropriation, risk of contract repudiation, and

shareholder rights measure, are important for economic development in a country. We expect

that investor protection is positively related to the better legal system, and therefore, we first

measure the influence of legality using the rule of law (RULELAW) that measures the extent

to which agents have confidence in and abide by the rules of society in year 2000. These

include perceptions of the incidence of both violent and non-violent crime, the effectiveness

and predictability of the judiciary, and the enforceability of contracts (La Porta et al. 2006).

The source for the data on the rule of law is from Kaufmann et al. (2003).

We also assess the legal environment of a country in protecting labor rights based on

the measure of STAKELAW. It is the average rank score of the following four indices, with

the first three from Botero et al. (2004) and the fourth from La Porta et al. (2004):

15

Employment laws, social security laws, collective relations laws, and human rights law. In

addition, we measure the common (COMMON) vs. civil law on CSR engagement.14

While international business researchers have examined various types of distances and

their effects, many international business scholars recognize that distance is not a uni-

dimensional concept, but rather multiple-dimensions construct that captures various types of

distance between countries. For instance, international business scholars have studied various

types of distance and their effects, including cultural distance, geographic distance,

administrative distance, economic distance, psychic distance, and institutional distance.

Following Campbell et al. (2012), we consider that the four distances including the cultural,

geographical, administrative, and economic distances are relevant to our CSR-SGOV context.

Research Design

As we seek to investigate the relation between CSR and SGOV, we first regress the CSR

indices, constructed from ESG IVA data, on the level of stakeholder initiated governance

measures of SGOV, board corporate governance (BGOV), along with other governance and

monitoring mechanisms as well as firm control variables including firm size, profitability,

firm risk, R&D, capital expenditure (measure of investment), growth opportunities, firm’s

earnings management, and country level information transparency, investor protection by

legality, and other international distance factors including culture, geographical,

administration, and economic distance.

CSRit = α0 + α1 SGOVit + α2 BGOVit +

n

j

j

3

CONTROL VARIABLESit + εit (1)

Endogeneity issue arises due to the dynamic nature of the CSR-SGOV relation. Thus,

in order to address the endogeneity issue, we adopt a well-developed dynamic panel

generalized method of moment (GMM) estimator following Wintoki et al. (2012), and

employ the method for the determinants of CSR, and compare the results to those obtained

from traditional OLS.

14 We also measure the legality of a specific country as the weighted average of the above-mentioned seven

factors based on Dai et al. (2012) and find our main results remain intact. A higher value of legality index

indicates a “better” legal system.

16

CSRit = α0 + α1 SGOVit + α2 BGOVit + α3 CSRit-1 + α4 CSRit-2 +

n

j

j

5

CONTROL

VARIABLESit + εit (2)

We also include year dummy and industry dummy variables to control for fluctuations

to macroeconomic and industry conditions, which may affect the incentives of firms’ CSR

engagement. We further conduct propensity score matching (PSM) method as well as the

difference-in-difference approach to address any remaining endogeneity problems.

Results

Descriptive Statistics and Bivariate Correlations

Panel A of Table 1 presents summary statistics by country. The mean CSR indices

(CSRIDX, CSRIDX_I, and CSRIDX_II) for various countries range from 2.985 to 6.17 where

the highest score is 10. International institutional ownership (IIOWN) ranges from 17.27%

(Hong Kong) to 76.28% (U.S.). The mean stakeholder governance, SGOV (board governance,

BGOV) ranges from 3.50 (3.51) to 6.44 (6.75). STAKELAW (RULELAW) scores range from

3.13 (-0.37) to 26.88 (2.22). CIFAR scores range from 56 to 85. Those numbers, in general,

reveal enough variation for empirical analysis. Our data covers more than 5,000 observations

in 31 countries during the 2006-2011 period.

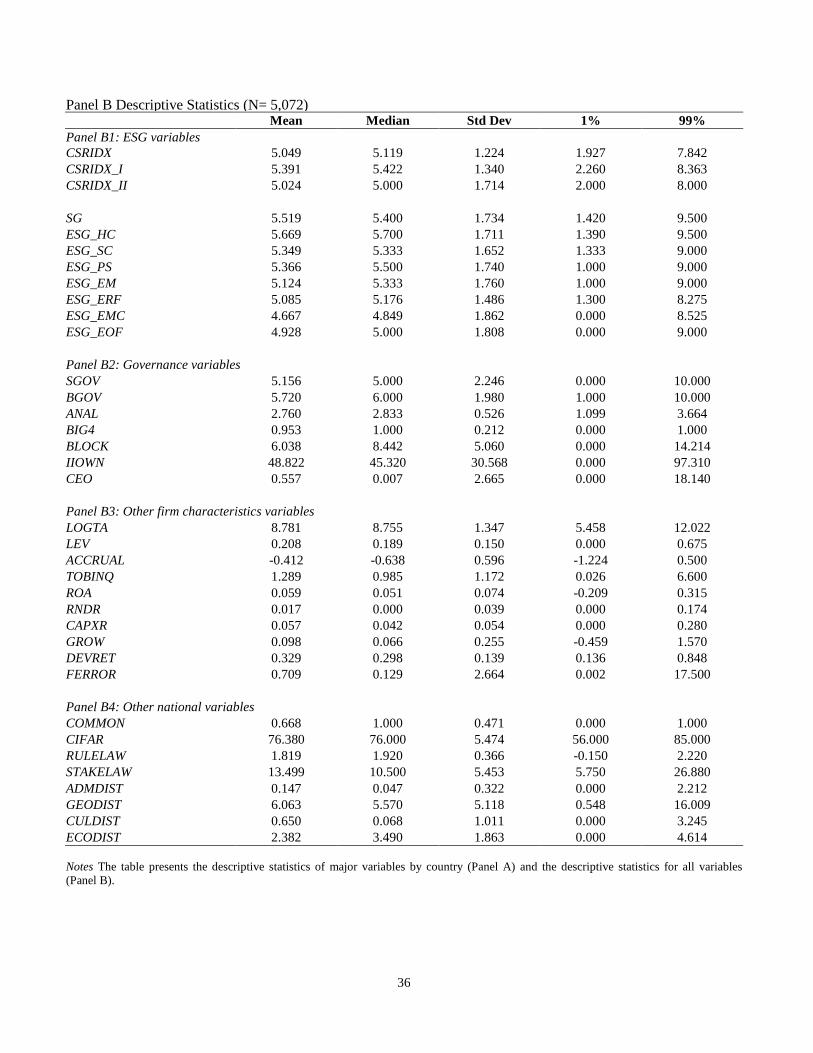

Panel B of Table 1 presents mean, median, standard deviation, 1% and 99% of all

variables that we employ. Three CSR indices show similar mean (around 5.00) and median

(around 5.00) numbers with close standard deviation ranging 1.224 to 1.714. Both the mean

and median scores of SGOV (5.16 and 5.00) and BGOV (5.72 and 6.00) seem closely related

to the mean and median numbers of CSR indices, suggesting the possible positive association.

[Table 1 about here]

Table 2 presents the Spearman correlation matrices among various CSR measures,

governance variables, and firm characteristics. We notice that both SGOV and BGOV are

significantly and positively correlated with both CSR measures. Most notably, SGOV is

mostly highly and positively correlated to CSRIDX_I (0.62) and CSRIDX (0.60) measures,

respectively. BGOV also is highly and positively related to CSRIDX_II (0.31) and CSRIDX

(0.28) measures, respectively. We also notice that other governance variables and firm

characteristics, such as the number of analyst following (ANAL), big four audit company

17

affiliation (BIG4), and firm size variables are positively correlated with CSR indices. Other

firm characteristics, i.e., R&D and volatility (DEVRET) which have been documented to

impact CSR also have significant correlation coefficients with our CSR measures.

We also conduct multicollinearlity diagnostics using a linear regression model and find

that all the individual variable’s variance inflation factor (VIF) values were below 6 (mean

VIF was below 3 for all models), suggesting that multicollinearlity does not significantly

influence our results. Due to the panel structure of our data, we also employ the Hausman

test to select between a fixed-effects and a random-effects model. The test suggests the use of

the random-effects OLS modeling. Below, we proceed to a multivariate test to examine the

incremental effect of SGOV and BGOV on CSR indices.

[Table 2 about here]

Baseline Regression Results

Table 3 presents our baseline regressions results using the ordinary least squares

methodology with clustered (at the firm level) and robust standard errors and year fixed

effects. All t-values are robust to heteroskedasticity and adjusted for two-way clustering at

the firm and year level. Consistent with the bivariate correlation results, we find that the

coefficients on SGOV are significantly and positively associated with CSRIDX with the

highest t-values of 19.68-20.53 among all independent variables, indicating that stakeholder

governance provides the critical role in international CSR market. 15 These results are

supportive of our conflict-resolution. The coefficients on BGOV also are positive and

significant at the one-percent level, but with relatively lower t-values of 4.60-5.09 than those

on SGOV. The positive coefficients on BGOV are also consistent with the conflict-resolution

hypothesis. 16 Our untabulated results using ASSET4’s ex-ante measure of CSR driver

15 When we employ country-effect regressions as well as firm-fixed effect regressions for robustness check,

the results are qualitatively identical to OLS regressions adjusted for two-way clustering at the firm and

year level.

16

Board governance is important because the market reacts based on directors’ characteristics

(Sundarmurthy et al. 1997). Board governance is also crucial because the board’s human and social capital

provides the firm with the critical knowledge and network access (Hillman and Dalziel 2003). When there

are convergent expectations, it is more likely for management to build mutual trust with the board and less

likely to maintain impression management and ingratiation tactics (Forbes and Milliken 1999; Westphal

1998). When the CEO is more receptive of board involvement in strategic CSR development, the board can

develop a more positive attitude and respect for the CEO’s CSR decision. This mutual respect can enhance

the cooperation within the board in a sound way (Forbes and Milliken 1999). It will also encourage the

18

variables related to stakeholder governance reveal qualitatively similar results of the positive

CSR-SGOV association after replacing our SGOV variables by these ASSET4 CSR driver

variables.

CSR engagements are also positively (negatively) associated with firm size (firm

leverage measured by LEV), consistent with U.S. findings of Jo and Harjoto (2011; 2012).

We also find a negative association between CSRIDX and risk measure of DEVRET at the

one percent level, consistent with earlier findings of McGuire et al. (1988), Godfrey et al.

(2009), Oikonomou et al. (2010). Thus, this evidence adds to the validity of our empirical

results.

In addition, we find that the coefficients on STAKELAW, common law (COMMON),

and administrative distance (ADMDIST) are negatively associated with CSR engagement.

Lopez-de-Silanes et al. (1998) suggest that English common law countries tend to offer the

strongest investor protection. Thus, the negative coefficients on COMMON suggest that CSR

engagements are more prevalent in civil law countries where investor protection is relatively

weak. Similarly, the negative coefficients on STAKELAW suggest that CSR engagements are

more rampant when labor rights are relatively weak. If compliance with host-country

regulations is more difficult for firms from more distant home countries, then the costs of

CSR should rise with greater ADMDIST between home and host countries. Thus, observed

inverse association between CSRIDX and ADMDIST is consistent with our anticipation. The

coefficient on economic distance (ECODIST) and RULELAW are positively related to

CSRIDX. The positive coefficients on RULELAW indicate that CSR engagements are more

ubiquitous in countries where the quality of law enforcement, as measured by RULELAW, is

relatively higher. The positive coefficients on ECODIST indicate that CSR engagements are

more prevailing in countries where the real GDP per capita difference between U.S. and a

firm’s home country is higher. This positive CSR-ECODIST association seems a bit puzzling

because the smaller the economic distance, the more similar the countries are in terms of their

income and wealth profiles, and thus, the more likely the non-U.S. firm is to engage in CSR

CEO to feel more comfortable in seeking the board’s input and advice (Westphal 1999). If the board

considers CEO’s CSR decision as a conflict resolution between the firm and stakeholders, we expect a

positive association between CSR engagement and BGOV.

19

in a firm’s home country (Campbell et al. 2012). 17 The coefficients on CULDIST and

GEODIST, however, are insignificant.

[Table 3 about here]

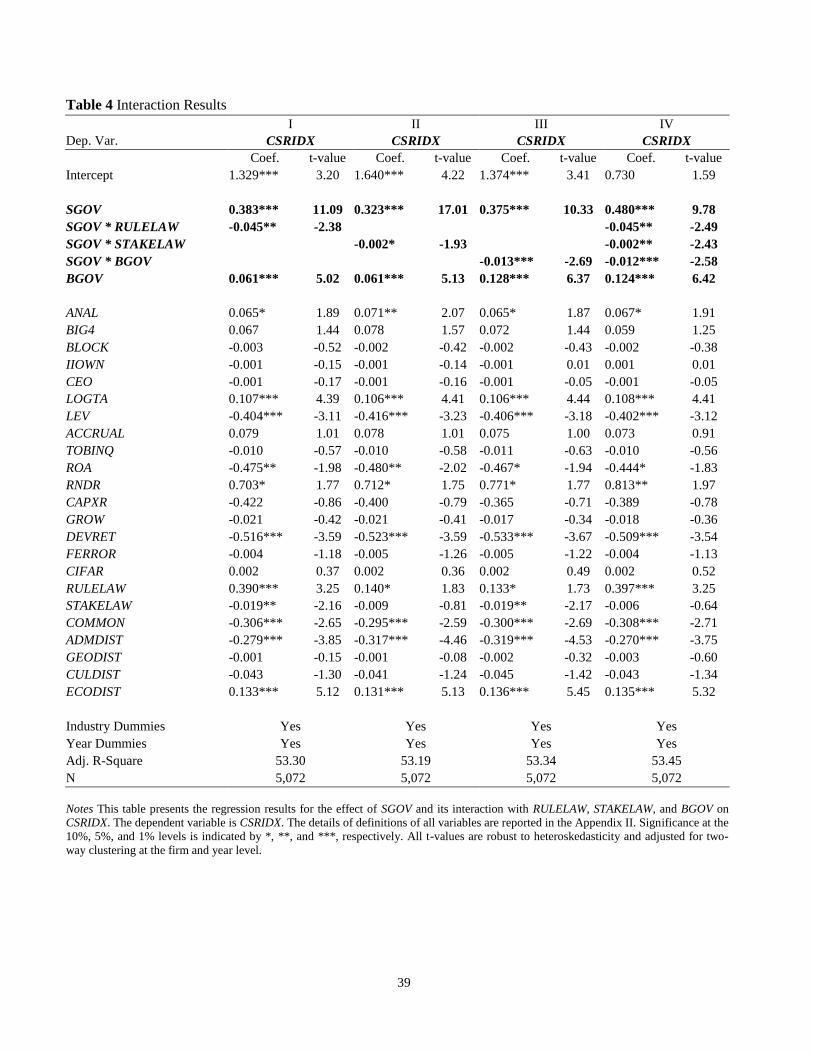

Table 4 presents the results with the effects of various legality issues and BGOV

interacted with SGOV. While the coefficients on SGOV remain highly significant at the one-

percent level, the coefficients on the interaction variables of SGOV*RULELAW and

SGOV*STAKELAW are significantly negative, suggesting that when investor protection is

relatively weak in terms of labor rights and social justice, SGOV plays more important role in

international CSR engagement. In addition, the coefficient on SGOV*BGOV is significantly

negative, suggesting that when corporate board (stakeholder) governance is relatively weak,

SGOV (BGOV) plays pivotal role in international CSR engagement. Other results remain

similar to those reported in Table 3.

[Table 4 about here]

Endogeneity Control

Previous studies suggest that endogeneity problem is quite serious in governance

(Wintoki et al. 2012) and CSR studies (Jo and Harjoto 2011; 2012; Reeb et al. 2012; Ioannou

and Serafeim 2014). Thus, we control for endogeneity using the following two

methodologies. First, we employ a well-developed dynamic panel GMM estimator, which

mitigates the biases of OLS and fixed effect regressions, as well as specification tests of the

validity of our dynamic panel assumptions to control for dynamic endogeneity. 18 This

dynamic panel GMM estimator alleviates endogeneity concerns in the effect of SGOV on

CSR and the determinants of CSR. Second, we use propensity score matching method to

tackle the endogeneity of selection. The method of propensity score matching has been

17 We conjecture that the positive CSR-ECODIST relation is partially because we use GDP per capital

instead of country-level GDP. GDP per capita takes a country's production, as measured by GDP, and

divides it by the country's total population. Hence, it is the output of a country's economy per person. A

country with larger ECODIST may confront with higher pressures from stakeholders, leading to potentially

higher demand for more CSR activities.

18

The term‘‘dynamic endogeneity’’ has been used to refer to the type of endogeneity that arises from the

possibility that a firm’s current actions will affect its control environment and future performance, which

will in turn affect its future control environment; see, for example, Durlauf and Quah (1999) and Asada, et

al. (2006).

20

receiving increasing attention in social studies mainly for dealing with the endogeneity issues

since the seminal work of Rosenbaum and Rubin (1983). Third and last, we perform the

differences-in-differences test for the change in CSR before and after global financial crisis,

following Bertrand and Mullainathan (2003).

First, to deal with any remaining dynamic endogeneity issue, we conduct a dynamic

panel generalized method of moments (GMM) regression following Wintoki et al. (2012).

The dynamic GMM enables us to estimate CSR-SGOV relation while including both past

CSR ratings and fixed-effects to account for the dynamic aspects of the CSR-SGOV relation

and time-invariant unobservable heterogeneity, respectively. Table 5 presents the regression

results of dynamic GMM. Due to our sample availability of 2006-2011, we lose more than

half of our observations because of dynamic GMM’s two lag period requirements.

Nonetheless, the results show that when we include fixed-effects in a dynamic model and

estimate via system GMM, the coefficients on SGOV in CSR regressions are still significant

and positive at the one percent level (t-values range from 4.19 to 4.40). Although statistical

significance gets a bit weaker than those of OLS regressions (t-values range from 19.68 to

20.53), it still seems that firms initiated and/or pressured by diverse stakeholders tend to

engage in more CSR activities, further lending support for our conflict-resolution hypothesis.

Notably, CSR-BGOV relation, however, becomes insignificant. This lack of significance

between CSR and BGOV supports the insignificant board independence of Wintoki et al.

(2012) based on dynamic panel GMM, although their focus is not on CSR.

We also report the results of two specification tests in Table 5—the AR(2) second-

order serial correlation tests and the Hansen J test of over-identification tests. The first AR(2)

test yields a p-value of 0.416-0.445, suggesting that the null hypothesis of no second-order

serial correlation cannot be rejected. The second test also reveals the Hansen J-statistic with a

p-value of 0.361-0.368. Thus, we cannot reject the hypothesis that our instruments are valid.

In addition, we report the results from a test of the exogeneity of a subset of our instruments.

The system GMM estimator makes an additional exogeneity assumption such that any

correlation between our endogenous variables and the unobserved (fixed) effect is constant

over time. This assumption enables us to include the levels equations in our GMM estimates

and use lagged differences as instruments for these levels. Eichenbaum et al. (1988) and

Wintoki et al. (2012) suggest that this assumption can be directly tested based on a

difference-in-Hansen test of exogeneity. This test also yields a J-statistic which is distributed

χ2 under the null hypothesis that the subsets of instruments in the levels equations are

21

exogenous. The results show a p-value of 0.142-0.247 for the J-statistic produced by the

difference-in-Hansen test. This suggests that we cannot reject the null hypothesis that the

additional subset of instruments used in the system GMM estimates is exogenous. Overall,

our dynamic GMM results support the conflict-resolution hypothesis, but not the

management perquisite hypothesis.

[Table 5 about here]

Second, the method of propensity score matching (PSM) has been receiving glowing

attention in social studies mainly for dealing with the endogeneity issues since the seminal

work of Rosenbaum and Rubin (1983). There are several steps involved. The first step is to

estimate the conditional probability of a specific SGOV type given the observable

characteristics with a probit regression. The independent variables we include in the probit

regression are the same firm characteristics and country level control variables at the firm

level. The second step is to estimate the conditional probability or the propensity score for

each observation from the probit model. As a third step, we use various matching techniques,

such as the nearest neighbor matching, radius matching, and the Kernel matching to form

sub-groups of observations with different SGOV type but with equal or close propensity

scores. As a final step, we compute the likelihood of CSR engagements for these sub-groups.

The differences in the likelihood of CSR engagement then reflect the contribution to the CSR

engagement by different SGOV type after controlling for the endogeneity of selection.

As shown in Table 6, firms initiated and/or pressured by stakeholders consistently

outperform those less initiated/pressured by stakeholders no matter which matching

technique we apply. The findings of propensity score matching further underline the results

from our multivariate regression analysis in Tables 3 and 4 without endogeneity control, and

dynamic GMM results with endogeneity control reported in Table 5, implying that

stakeholder governance is an effective mechanism to make firms engage in various CSR

activities when firms explore their CSR opportunities in the international CSR market.

[Table 6 about here]

A remaining potential limitation of the pooled cross-sectional regressions is that the

results may reflect the impact of uncontrolled omitted variables rather than the causal effect

of SGOV on CSR engagement. To further address this concern, we investigate whether CSR

engagement changes around global financial crisis. Specifically, we examine the change in

CSR around financial crisis between banking vs. non-banking industries during our sample

period because banking and financial industries are more seriously affected by financial crisis.

22

Table 7 shows the effect of global financial crisis on CSR engagement. Panel A of

Table 7 presents the differences in CSR for one year before and three years after crisis. To

avoid any confounding effect, the CSRIDX in the crisis years (2007-2008) are not included.19

In banking and financial industries, CSRIDX declines from year t-1 (2006) to year t+1 (2009),

but CSRIDX does not decline during the same period in non-banking industries. The

difference test in Panel A indicates that CSRIDX caused by exogenous shocks results in

differential CSR engagement between bank vs. non-bank industries. Specifically, while

CSRIDX of non-bank industries increases from year t-1 to year (t+1, t+3), CSRIDX of

banking and financial industries are statistically insignificant during the same period.

Next, we perform the differences-in-differences test for the change in CSR before and

after crisis, following Bertrand and Mullainathan (2003). Panel B of Table 7 presents the

results. To investigate the dynamic effect of crisis on CVSIDX, we estimate a regression with

four interaction variables (SGOV*Year(t-1), SGOV*Year(t+1), SGOV*Year(t+2),

SGOV*Year(t+3)) as well as CRISIS (one for 2007-2008 and 0 for other period). The

coefficients on CRISIS are significant and negative as anticipated. As shown in model (2) of

Panel B, the coefficients on SGOV*Year(t+1) and SGOV*Year(t+2) are statistically

indifferent from zero, but the coefficients on SGOV*Year(t-1) and SGOV*Year(t+3) are

significantly negative and positive, respectively. CSR engagements begin to decline one year

before crisis, but increases three years after crisis, suggesting the possibility that post-crash

effects of disciplining managers to reengage in CSR take time. The results shown in model

(3) of Panel B suggest that the impact of SGOV on CSRIDX is less (more) substantial in

non-banking (banking) industries while the overall impact of SGOV on CSRIDX remains

positive. Combined together, both results from the simple difference tests reported in Panel A

and those from the differences-in-differences test reported in Panel B are supportive of the

conflict-resolution hypothesis.

[Table 7 about here]

Additional Tests

To further check the robustness of our main results, we verify whether the positive

CSR-SGOV relation remains intact if we construct CSR index based on other international

19 This result remains intact when we examine the global finance crisis based on 2008-2009 period instead

of 2007-2008.

23

CSR data such as ASSET4 using the same sample period. Table 8 presents the regression

results for the effect of SGOV and BGOV on CSR_ASSET4. The dependent variable

CSR_ASSET4 is measured by the CSR performance data provided by ASSET4 ESG database.

Specifically, CSR_ASSET4 is calculated as the mean performance score of environmental

(EN) and social (SO) pillars. The environmental pillar (EN) measures a company's impact on

living and non-living natural systems, including the air, land, water, and complete ecosystems.

It reflects how well a company uses the best management practices to avoid environmental

risks and capitalize on environmental opportunities in order to generate long-term

shareholder value. It covers three categories including resource reduction, emission reduction,

and product innovation. The social pillar (PO) measures a company's capacity to generate

trust and loyalty with its workforce, customers and society, through its use of best

management practices. It is a reflection of the company's reputation and the health of its

license to operate, which are key factors in determining its ability to generate long term

shareholder value. It covers a total of seven categories including Employment Quality, Health

& Safety, Training and Development, Diversity and Opportunity, Human Rights,

Communities, and Product Responsibility. Both EN and SO are ranged from 0-1 with higher

value for better performance.

Our results reported in Table 8 suggest a significant and positive association between

CSR_ASSET4 and SGOV with t-values of 9.71-10.90, and between CSR_ASSET4 and BGOV

with t-values ranging 1.95-1.98. Thus, CSR_ASSET4-SGOV relation is quite close to our

main results of the positive CSRIDX-SGOV relation. A positive (negative) association

between CSR_ASSET4 and firm size (DEVRET) also remains similar to our previous results.

Based on the above results, we conclude that our main results of a positive association

between CSR indices and stakeholder governance is not primarily driven by our usage of the

same MSCI ESG IVA database both for CSR indices construction and SGOV scores. 20

[Table 8 about here]

20 Due to the non-disclosure agreement (NDA) requirement specifying that we should not combine the

MSCI ESG IVA database with other CSR rating data provided by other CSR rating agency, such as

ASSET4, we cannot combine ASSET4 and ESG IVA in our main analysis. We report Table 8 only for the

robustness cross-check purpose to verify whether our findings of a positive CSR-SGOV relation remains

intact if we construct CSR index based on ASSET4. In addition, we find a positive and significant CSR-

SGOV association when we construct the ex-ante measure of stakeholder governance from CSR driver of

ASSET4 (unreported).

24

In addition, we examine whether there exist any differences in stakeholder influence

on the relation between CSR and SGOV between various regions, i.e., between U.S. and.

non-U.S., between U.S. and Europe, between U.S. and Asia, between Europe and non-

Europe, and between Asia and non-Asia. Our unreported Chow test results suggest that while

the coefficients on SGOV in CSRIDX regressions are all significant at the one percent level,

they are insignificantly different each other, indicating that the impact of stakeholder

governance on CSR are world-wide, but not just region-specific phenomena.

Furthermore, we investigate whether the impact of stakeholder governance and

pressures is less substantial for firms with substantial CEO influence, measured by CEO

ownership. When we examine firms with CEO ownership higher than 10%, our untabulated

results indicate that the coefficients on SGOV become insignificant, suggesting the

possibility that CEO power and stakeholder governance are substitutes in CSR engagement.

Discussion and Conclusion

A few number of prior studies have examined what empirical factors affect

international CSR engagement (e.g. McWilliams and Siegel 2001; Campbell 2007; Ioannou

and Serafeim 2012) yet no empirical studies have investigated the empirical association

between CSR engagement and stakeholder-initiated governance around the world. In this

paper, we provide empirical evidence of the important role that stakeholder governance play

in explaining the CSR variation as measured by our constructed CSR index. In doing so, we

utilize a global MSCI ESG IVA database from MSCI ESG Research covering more than

5,000 observations in 31 countries during the 2006-2011 period.

Drawing from Freeman’s (1984) stakeholder theory, we maintain that conflict-

resolution is one important incentive behind recent CSR movement following Jensen (2002)

and others, and firms are strategically engaging in CSR activities (Porter and Krammer 2002,

2006) or reducing socially irresponsible activities to reduce conflicts of interest between

firms and non-investing stakeholders. Empirically, our paper is the first one that shows a

positive association between CSR and stakeholder-initiated (strategic) governance covering a

large number of CSR observations, countries, industries, and firms. Our empirical models,

with and without controlling for endogeneity, are able to explain 47-53% of the variance in

international CSR engagement with observable characteristics.

International CSR and SGOV are significantly and positively correlated without and

with endogeneity control. The influence of stakeholder governance, however, is less

25

ascendant when investor protection and board governance are relatively strong. While

international CSR and BGOV are positively correlated without endogeneity control, CSR-

BGOV nexus is insignificantly related with endogeneity control. The coefficients and

corresponding t-values of SGOV are, in general, higher than those of BGOV. The

coefficients on the other governance and monitoring variables are mostly insignificant. It

seems that the incremental monitoring effect of SGOV is non-trivial, and greater than that of

BGOV as well as those from other governance and monitoring mechanisms.

Given that there is no prior evidence on the relation between stakeholder governance and

CSR across countries, this study provides the first-step empirical evidence regarding the impact

of stakeholder governance on firms’ CSR after controlling for endogeneity and other

confounding factors. This study is different from Ioannou and Serafeim (2012) who

investigate the empirical determinants of CSR, but do not address corporate governance

issues. Our study is also not particularly limited to specific country or economic region like

Maignan and Ralston (2002) who examine CSR in Europe and the U.S. or Chapple and

Moon (2005) who investigate CSR in Asia. Instead, our study examines the relation between

stakeholder governance and CSR around the world.

One caveat is that a significant relation between international CSR and our SGOV

metrics does not necessarily imply that any managers who choose not to engage in CSR is

behaving irrationally. A majority manager of an international firm can rationally measure

private benefits of CSR engagement versus related costs of CSR. A future study with better

international data may be able to examine the choice against CSR engagement.

26

References

Aguilera, R.V., Ganapathi, J., Rupp, D.E., & Williams, C.A. (2007). Putting the S back in

corporate social responsibility: A multilevel theory of social change in organizations.

Academy of Management Review, 32(3), 836-863.

Aktas, N., Bodt, E., & Cousin, J. (2011). Do financial markets care about SRI? Evidence from

mergers and acquisitions. Journal of Banking and Finance, 35(7), 1753-1761.

Asada, T., Chen, P., Chiarella, C., & Flaschel, P. (2006). Keynesian dynamics and the wage–price

spiral: a baseline disequilibrium model. Journal of Banking and Finance, 28, 90–130.

Bainbridge, S. (2006). Director primacy and shareholder disempowerment. Harvard Law Review,

119, 1735–1758.

Baron, D.P. (2009). A positive theory of moral management, social pressure, and corporate

social performance. Journal of Economics and Management Strategy, 18, 7-43.

Bebchuk, L.A. (2005). The case for increasing shareholder power. Harvard Law Review, 118,

833–914.

Bebchuk, L.A. (2006). Letting shareholders set the rules. Harvard Law Review, 119, 1784–1813.

Bergloff, E., von Thadden, E.L. (1994). Short term vs. long term interest: Capital structure with

multiple investors. Quarterly Journal of Economics, 109, 1055–1084.

Berle, A.A., & Means, G.C. (1932). The modern corporation and private property. New York:

Commerce clearing house.

Bertrand, M., & Mullainathan, S. (2003). Enjoying the quiet life? Corporate governance and

managerial preferences. Journal of Political Economy, 111, 1043-1075.

Besley, T., & Ghatak, M. (2007). Retailing public goods: The economics of corporate social

responsibility. Journal of Public Economics, 91, 1645-1663

Böhling, K. (2011). Emergence of stakeholder governance in the United Nations: an outcome of

institutional work? Working paper. Technische Universität München (TUM).

Botero, J., Djankov, S., La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2004). The regulation

of labor. Quarterly Journal of Economics, 119(4), 1339-1382.

Bushman, R., Piotroski, J., & Smith, A. (2004). What determines corporate transparency? Journal

of Accounting Research, 42(2), 207-252.

Bushman, R., Piotroski, J., & Smith, A. (2005). Insider trading restrictions and analysts’

incentives to follow firms. Journal of Finance, 60, 35-66.

Calton, J., & Payne, S. (2003). Coping with paradox. Business and Society, 42, 7-42.

Campbell, J.L. (2007). Why would corporations behave in socially responsible ways? An

institutional theory of corporate social responsibility. Academy of Management Review,

32(3), 946.

Campbell, J.L., Eden, L., & Miller, S. (2012). Multinationals and corporate social responsibility in

host countries: Does distance matter? Journal of International Business Studies, 43(1), 84-106.

Carney, M., Gedajlovic, E., & Sur, S. (2011). Corporate governance and stakeholder conflict.

Journal of Management & Governance, 15, 483-507.

Cespa, G., & Cestone, G. (2007). Corporate social responsibility and managerial entrenchment.

Journal of Economics & Management Strategy, 16, 741-771.

Chapple, W., Moon, J. (2005). Corporate social responsibility (CSR) in Asia: a seven-country

study of CSR web site reporting. Business & Society, 44(4), 415-441.

Cheng, B., I. Ioannou, & Serafeim, G. (2014). Corporate social responsibility and access to

finance. Strategic Management Journal, 35(1), 1-23.

Choi. J., & Wang, H. (2009). Stakeholder relations and the persistence of corporate financial

performance. Strategic Management Journal, 30, 895-907.

Chung, K., & Jo, H. (1996). The impact of security analysts’ monitoring and marketing functions on

the market value of firms. Journal of Financial and Quantitative Analysis, 31, 493-512.

27

Dai, N., Jo, H., & Kassicieh, S. (2012). Cross-border venture capital investments in Asia:

Selection and exit performance. Journal of Business Venturing, 27, 666-684.

Dalton, D.R., Hitt, M.A., Certo, S.T., & Dalton, C.M. (2007). The fundamental agency problem

and its mitigation. Academy of Management Annals, 1, 1–64.

Del Guercio, D. (1996). The distorting effect of the prudent man law on equity investments.

Journal of Financial Economics, 40, 31-62.

DellaVigna, S., List, J., Malmendier, U. (2012), Testing for altruism and social pressure in

charitable giving. Quarterly Journal of Economics, 127, 1-56.

Demsetz, H. (1986). Corporate Control, Insider Trading, and Rates of Return. American

Economic Review, 76, 313-317.

Derwall, J., Guenster, N., Bauer, R., & Koedijk, K. (2005). The eco-efficiency premium puzzle.

Financial Analyst Journal, 61(2), 51-63.

Deutsch, M. (1973). The resolution of conflict. New Haven, CT: Yale University.

Dhaliwal, D., Oliver, L., Tsang, A., & Yang, G.Y. (2011). Voluntary nonfinancial disclosure and

the cost of equity capital: The initiation of corporate social responsibility reporting.

Accounting Review, 86(1), 59-100.

Dhaliwal, D., Radhakrishnan, S., Tsang, A., & Yang, G.Y. (2012). Nonfinancial disclosure and

analyst forecast accuracy: International evidence on corporate social responsibility (CSR)

disclosure. Accounting Review, 87(3), 723-759.

Dharwadkar, R., Goranova, M., Brandes, P., & Khan, R. (2008). Institutional ownership and

monitoring effectiveness: It's not just how much but what else you own. Organization

Science, 19(3), 419-440.

Durlauf, S.N., & Quah, D.T. (1999). The new empirics of economic growth. In: Taylor, J.B.,

Woodford, M. (Eds.), Handbook of Macroeconomics, 1, Elsevier, North Holland, 235–308.

(Chapter 4).

Eichenbaum, M.S., Hansen, L.P., & Singleton. K.J. (1988). A time series analysis of

representative agent models of consumption and leisure choice under uncertainty. Quarterly

Journal of Economics, 103, 51–78.

Eisenhardt, K.M. (1989). Agency theory: An assessment and review. Academy of Management

Review, 14(1), 57–74.

Fama, E.F. (1980). Agency problems and the theory of the firm. Journal of Political Economy, 88,

288-307.

Fisman, R., Geoffrey, H., & Vinay, B.N. (2008). A model of corporate philanthropy. Working