Embed Size (px)

Citation preview

Corporate Responsibility Report 2005

Responsiblebanking

Responsible banking

Contents

Introduction

IFC Our businesses1 Group Chief Executive’s statement2 Corporate Responsibility

Director’s statement 2a Summary of targets and

achievements

Responsible banking

3 Customer service8 Financial inclusion

14 Responsible lending17 Dealing with environmental

and social issues in commercial lending

22 Carbon trading and renewable energy finance

24 Barclays in Africa

Inside Barclays

29 How we treat our people33 How we manage our

environmental impact36 Out in the community40 Where we stand on

key issues

Other information

44 Data tables48 External assurance statement

and commentaryIBC GRI summary and contact

information

UK Banking

UK Banking delivers bankingsolutions to retail and businessbanking customers in the UnitedKingdom, through a variety ofchannels comprising the branchnetwork, cash machines, telephonebanking, online banking andrelationship managers. It ismanaged through two businessareas, UK Retail Banking and UKBusiness Banking.

UK Retail Banking aims to build broaderand deeper relationships with bothexisting and new customers. It provides a wide range of products and services to retail customers, including currentaccounts, savings, mortgages, andgeneral insurance; banking services forsmall businesses and banking, investmentproducts and advice to affluentcustomers.

UK Business Banking provides relationshipbanking to larger and medium businesscustomers in the United Kingdom via a network of relationship and industrysector specialist managers; offers accessto the products and expertise of otherbusinesses in the Group, particularlyBarclays Capital; and provides assetfinancing and leasing solutions through a specialist business.

Barclays Capital

Barclays Capital is a leading globalinvestment bank which provideslarge corporate, institutional andgovernment clients with solutionsto their financing and riskmanagement needs.

Barclays Capital services a wide variety of client needs, from capital raising andmanaging foreign exchange, interest rate,equity and commodity risks, through toproviding technical advice and expertise.Activities are organised into three principalareas: Rates, which includes fixed income,foreign exchange, commodities, emergingmarkets, money markets sales, tradingand research, prime services and equityproducts; Credit, which includes primaryand secondary activities for loans andbonds for investment grade, high yieldand emerging market credits, as well as hybrid capital products, asset basedfinance, commercial mortgage backedsecurities, credit derivatives, structuredcapital markets and large asset leasing;and Private Equity.

Barclays GlobalInvestorsBarclays Global Investors (BGI)is one of the world’s largest assetmanagers and a leading globalprovider of investment managementproducts and services.

BGI offers structured investmentstrategies such as indexing, global asset allocation and risk-controlled active products, including hedge funds. BGI also provides related investmentservices such as securities lending, cashmanagement and portfolio transitionservices. In addition, BGI is the globalleader in assets and products in theexchange traded funds business, withover 140 funds for institutions andindividuals trading in eleven marketsglobally. BGI’s investment philosophy is founded on managing all dimensions of performance: a consistent focus on controlling risk, return and cost.

We

Weafflucorbanstocfinama

Privaand wortinclustruOffsbanislanmanexpain thexecAsseadviadviservas sFinaand pensplanservcust

“We touch the lives of manypeople around the world andour success as a business is inextricably linked with that of our customers, employees,suppliers and the strength of the communities in which we live and work.”

Alastair CampCorporate Responsibility Director Barclays

Our businesses

UK • 1• 1

c

Bar• U

is

Bar• U

m

PerCent ClubWe are a member of the Business in the Community PerCent Club – a group of companies undertakingto ensure that donations to thecommunity over time amount to at least 1% of UK pre-tax profit.

Wealth Management

Wealth Management servesaffluent, high net worth andcorporate clients, providing privatebanking, offshore banking,stockbroking, asset management,financial planning services andmanages the closed life fund.

Private banking offers bespoke bankingand investment solutions to high networth individuals in the UK and abroad,including investment and wealthstructuring advice and banking services.Offshore banking serves the corporatebanking needs of clients in the offshoreislands and overseas together with wealthmanagement and banking services forexpatriates and non-UK nationals living in the UK & overseas. Stockbroking offersexecution only stockbroking services.Asset management provides bespokeadvisory and discretionary investmentadvice and multi-manager investmentservices to mass affluent clients as well as some high net worth individuals.Financial Planning provides tailored and impartial financial advice on life,pensions, investments and inheritanceplanning including estates & trustsservices to both personal and businesscustomers.

Barclaycard

Barclaycard is a multi-brandinternational credit card andconsumer lending business; it is one of the leading credit cardbusinesses in Europe.

In the UK, Barclaycard manages theBarclaycard branded credit cards andother non-Barclaycard branded cardportfolios including Monument, SkyCardand Solution Personal Finance. Inconsumer lending, Barclaycard managesboth secured and unsecured loanportfolios, through Barclays brandedloans, mostly Barclayloan, and alsothrough the FirstPlus and ClydesdaleFinancial Services businesses.

Outside the UK, Barclaycard providescredit cards in the United States throughBarclaycard US (previously Juniper),Germany, Spain, Greece, Italy, Portugaland a number of other countries. In the Nordic region, Barclaycard operatesthrough Entercard, a joint venture withFöreningsSparbanken (Swedbank).

Barclaycard Business processes cardpayments for retailers and issuespurchasing and credit cards to businesscustomers and to the UK Government.

Barclaycard works closely with other partsof the Group, including UK Retail Banking,UK Business Banking and InternationalRetail and Commercial Banking, toleverage their distribution capabilities.

International Retail andCommercial BankingInternational Retail andCommercial Banking (IRCB)provides Barclays internationalpersonal and corporate customerswith banking services. It includesthe Absa Group in South Africa inwhich Barclays acquired a majoritystake on 27th July 2005.

IRCB provides a range of banking services,including current accounts, savings,investments, mortgages and loans topersonal and corporate customers across Spain, Portugal, France, Italy, theCaribbean, Africa and the Middle East.

It works closely with other parts of theGroup, including Barclaycard, UK Banking,Barclays Capital and Barclays GlobalInvestors, to leverage synergies fromproduct and service propositions.

Absa Group Limited is one of SouthAfrica’s largest financial servicesorganisations serving personal, commercialand corporate customers predominantly inSouth Africa. Absa serves retail customersthrough a variety of distribution channelsand offers a full range of banking services,including basic bank accounts, mortgages,instalment finance, credit cards,bancassurance products and wealthmanagement services; for commercial and large corporate customers Absa offers customised business solutions. As at 31st December 2005, Barclays owned 56.6% of Absa Group Limited’sordinary shares and has voting control.

UK Banking• 11.1 million Current Accounts.• 183,000 Business Banking

customers.

Barclays Capital• US$329.2bn loans and bonds

issued on behalf of clients.

Barclays Global Investors• US$1.5 trillion assets under

management.

Wealth Management• £78.3 billion of customers’ funds.

Barclaycard• 11.2 million UK customers.• 4.3 million international cards

in issue.

International Retail andCommercial Banking• 1,516 international branches,

including Absa.

1Barclays PLC Corporate Responsibility Report 2005

Group Chief Executive’s introduction

What is responsible banking?

“Responsible banking is an integral part of the way we do business, and a central element of ouroverall strategy to makeBarclays one of the world’sleading banks.”

In December 2005, the Daily Telegraphpublished their ‘Corporate Responsibility’supplement. In Barclays we havedevoted a lot of time and resource todeveloping our corporate responsibilityprinciples and activities. But my pride in our achievements to date deflatedsomewhat when I read in the article that“Sectors such as…banks are generallymuch further behind on CSR”*. It wasclear to me that, despite our efforts inthe past, we still had a lot more to do to convince our stakeholders that we are absolutely serious about corporateresponsibility. The best way I cantransmit this is to say that everything wedo under the ‘corporate responsibility’banner is directly relevant to ourbusiness goals. For too long, the term‘corporate responsibility’ has hadsomething of an abstract quality to it,with few people knowing what it looked

like in practice. In Barclays, our objective is to make it recognisable and meaningful which is why we writeabout it in some detail in this report.

By incorporating CR principles intoeverything that we do, we aim to beleaders, not followers, in corporateresponsibility. In support of thisapproach, we have recently appointedAlastair Camp as our CorporateResponsibility Director. Alastair hassuccessfully run a number of businessesin Barclays and his appointmentdemonstrates our commitment toprovide leadership in the CR arena.

We firmly believe that we make ourgreatest contribution to society bybeing good at what we do, and doing it in a responsible way – providingproducts and services that helpcustomers realise their financial goals,that drive economic growth, and thatsustain a healthy financial system. Thisis the context in which a major bank like Barclays has its most important role to play. Areas such as financialinclusion, responsible lending, and thefinancing of large-scale developmentprojects are questions of acute socialinterest – and rightly so. And they arealso areas where Barclays can make a significant and enduring impact.

To take two examples, I am proud of the fact that Barclays has one of themost extensive financial inclusionprogrammes in the UK. And we werealso one of the four banks that helped to develop the Equator Principles, which

have transformed the way in which thebanking sector as a whole approachesproject finance across the world. Wethink of this as ‘responsible banking’,and I believe it gets to the heart of whatit means to run a bank at once profitablyand in a responsible way. Responsiblebanking is an integral part of the way we do business, and a central elementof our overall strategy to make Barclaysone of the world’s leading banks. It alsounderpins the way we have presentedthis year’s report: the following pagesdescribe what we have achieved in2005, but they also set out what wemean by responsible banking, and how we seek to make it real for ourcustomers, for our colleagues and for the communities we serve.

Ranked 32nd in the Business in the CommunityCorporateResponsibilityIndex.

Member of the 2005 Dow JonesSustainabilityIndex. Ranked in the top quartile of thebanking sector.

Member of the2005 FTSE4GoodIndex.

John VarleyGroup Chief Executive

2

Corporate Responsibility Director’s statement

Putting it into practice

“Having looked at the feedbackwe received last year, we have aimed to make thisreport more readable, moreaccessible, and with a muchbroader international focus.”

This year’s report represents somethingof a change in both tone and style.Having looked at the feedback wereceived last year, we have aimed tomake this report more readable, moreaccessible and with a much broaderinternational focus. And as John Varleysaid, we have set it out as a clear storyin which we describe not only what wedo, but the context in which we do it,all under the overarching theme of‘responsible banking’.

The public debate about environmentaland ethical issues has continued toevolve in the last year, and ourunderstanding of the issues has beeninformed by the dialogue we have hadwith customers, employees, investors,governments, politicians, the voluntarysector and Non-GovernmentalOrganisations (NGOs).

We realise that many of thesestakeholders are less interested in how we spend our profits than in how we make them. Fine judgementsare often required but every decisionwe make is underpinned by our basic belief in treating customers,employees and other stakeholdersfairly, acting with integrity, honouringthe commitments we make, andrespecting people’s rights.

Coming new to this role, having runvarious Barclays businesses in the UK and overseas, I understand theimportance of CR and how it shouldinfluence business decisions. I can see that we made progress last year,especially in the areas of financial

inclusion, climate change andenvironmental practice, and in ourwork on human rights. Customerservice is a vital area where we haveachieved a good deal, but still havework to do, so it continues to be a top priority. The issue of consumerdebt is a growing concern in manydeveloped countries, and we talkabout this in more detail in thechapter on responsible lending. From an international perspective, our acquisition of a majority stake in Absa in South Africa means thatone-third of our employees are nowbased in Africa, and we recognise that this enhanced presence bringswith it additional responsibilities.

Listening to feedback

After we published last year’s report we carried out an extensiveconsultation programme withinvestors, NGOs, the voluntarysector, consumer groups,government, media and corporateresponsibility specialists.In particular, we were asked to:

• Explain more clearly whycorporate responsibility isimportant to us. Our new focus on ‘responsible banking’concentrates on the issues thatmatter to us, making corporateresponsibility inextricable from our strategic goals.

• Give more of the context aroundour key issues and initiatives. Again,the focus on responsible bankingaims to meet this requirement.

• Broaden the content internationally.In this report we have includedmuch more about our operationsaround the world.

• Clarify our commitments. We have made progress on this,and have brought our targets and achievements together in one section.

• Make the report more accessible.This year’s report is designed tobe more visually appealing, andeasier to read.

Alastair CampCorporate Responsibility Director

Page Issue Targets for 2005

3 Customer service Launch Barclays Global Investors iShares socially responsible exchange-traded fund

–

Meet the needs of our increasingly diverse customer base by adapting appropriate products and services

8 Financial inclusion Launch a programme of financial inclusion support for one-parent families in the UK

Extend the reach of basic banking to reduce the number of people in the UK without bank accounts

Play a leading role in the Money Advice Gateway to increase free independent money advice in the UK

14 Responsible lending –

–

17 Dealing with environmental and –social issues in commercial lending

–

22 Carbon trading and renewable energy finance –

24 Barclays in Africa –

29 How we treat our people Embed shared values and revitalise employee perceptions of the brand

Build leadership succession across all of our businesses

Continue work to encourage employees to focus on customer needs

Reduce turnover among new recruits

Continue embedding equality and diversity in people policies and practices

33 How we manage our environmental impact Meet 2005 targets for energy, water and paper consumption

Set new environmental targets for 2006 and beyond

Expand our EMS to key Barclays businesses worldwide

Develop environmental standards for office refurbishments

Expand recycling facilities at our main office sites in the UK

36 Out in the community Develop online facilities to handle employee volunteering and donations

Use branches and other channels to communicate our programme more effectively

Achieve greater synergies between community and commercial operations

Ensure donation and employee support meets stakeholder needs

Increase the international scope of our community involvement

40 Where we stand on key issues Strengthen ethical, social and environmental supplier-screening policies

Continue participation in Business Leaders’ Initiative on Human Rights (BLIHR)

–

Responsible bankingSummary of targets and achievements

2a

2b

How we are doing Objectives for 2006

iShares KLD Select Social Index Fund launched and gaining momentum Develop a new electronic payments service, ready for launch by end 2007

– Continue to improve customer satisfaction in UK Retail Banking

Improved products launched (e.g. Barclays Additions current account) Continue development of online banking security featuresSummary information added to Personal Card/Loan statements

Launched Barclaycard Horizons to support 50,000 disadvantaged lone Encourage a strong UK community finance sector through a focusedparents and their families with practical support including money management, programme of funding and supportadvice, training and help to get back to work

379,000 Cash Card Accounts opened since launch. We are working Review our UK basic banking proposition to ensure it meets the needsclosely with partners to help ‘hard-to-reach’ groups of a diverse customer base

The Gateway is on course for piloting in 2006 Embed the Ghanaian microbanking programme and apply learning todevelop further microfinance initiatives

– Encourage increase in the number of organisations sharingcredit information

– Pilot programme to identify and help customers who may be approaching financial difficulty

– –

– Improve understanding of social issues relating to Equator Principles andinclude in updated sectoral guidelines

– Commence trading in carbon options. Develop weather and floodmanagement products. Investigate the feasibility of carbon managementservices for SMEs, personal customers and staff

– Expand branch and cash machine network in South Africa. Increase take-upof Mzansi basic bank account in South Africa. Further develop HIV/AIDSawareness and participation in employee welfare programmes

‘Guiding Principles’ developed, and being shared across Barclays –

Employee survey shows 76% of employees feel proud to be associated Further improvement in key Employee Opinion Survey scoreswith Barclays (up from 71%)

We have invested in developing talent, including external recruitment. Acquire and develop talent with increased momentum via a systematic Employee survey shows a rise to 58% (from 51%) in Perceptions of Leadership talent management approach

Customer Orientation was 65% in the Employee Opinion Survey (up from 60%) Ensure line managers in Barclays have the tools they need to meet the‘Best People’ Guiding Principle

Resignation rates for UK employees with less than 12 months’ service –have fallen by 10%

8th placed organisation in Race for Opportunity; ranked 20th in –Stonewall’s Workplace Equality Index 2005; Barclays Capital US Employerof The Year (by National Business & Disability Council)

Water consumption and recycled paper targets achieved. Good progress made –in energy and overall paper consumption

New targets set for 2006-2010 including new measures for waste and Meet specific 2006 environmental improvement targets. Put in place thecarbon emissions processes necessary to achieve carbon neutrality for our UK operations

ISO 14001 achieved in Barclaycard. Absa in South Africa is working Implement our Environmental Management System in Italy and South Africatowards ISO 14001

New opportunities identified to increase the amount of recycled materials –used in office refurbishments

Achieved a 95% recycling rate during a trial at One Churchill Place and –improved waste data collection

66% of UK matched funding requests now online (2004: 42%). Ten other –countries now registered on our online system

Community investment programmes promoted through better profiling Launch programmes with NCH and Help the Aged, to support core themesin local branches, worldwide of ‘Financial Futures’, ‘Getting to Work’ and ‘Stronger Communities’

Launched Barclaycard Horizons, linked to Barclaycard’s commitment to Develop a co-ordinated global community investment programmeresponsible lending and ‘Barclays Spaces for Sports’, linked to our Premiershipfootball sponsorship

Community employee programmes redeveloped and launched Increase participation in UK and international employee community programmes (skills-based volunteering, matched funding)

Launched Barclays Miles Ahead involving 7,000 employees across the –UK, continental Europe and Africa, increasing participation in Barclaycard International, Barclays Capital (Asia Pacific) and the Americas, and Barclaysin the Middle East and Egypt

New supplier screening tool developed and now being implemented Review the supply chain using enhanced screening tool and build into new supplier contracts

Continued participation in BLIHR with input to debate and publications Support the continuing development of BLIHR

– Develop and launch an integrated Code of Ethics

����

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

��

�

3Barclays PLC Corporate Responsibility Report 2005

Responsible bankingCustomer service

We make our greatest contribution tosociety by supporting economic growtharound the world, and being responsibleabout how we do this. Our products and services give businesses the support they need to grow, help people managetheir everyday lives more efficiently, and invest for the future.

Better, fairer, safer

Treating customers fairlyThe UK banking sector as a whole has often been taken to task for notgiving customers good enough service, and some of this criticism has beenjustified. But in recent years the picturehas changed quite significantly. A greatdeal of effort and investment has goneinto improving our products, andgiving our customers better service,but more still remains to be done.

Treating customers fairly is both a toppriority and an absolute commitment.We are giving people more and betterinformation before they buy, so thatthey can make more informed decisionsand take more responsibility for theirown finances. In this, we share theFinancial Services Authority’s objectivesunder the ‘Treating Customers Fairly’approach and have a programme inplace to ensure that it is fully embeddedinto all aspects of our business. We have just appointed a former seniorregulator to the role of ‘ConsumerChampion’, reporting directly to theChief Executive of UK Retail Banking.

Better serviceOur Business Banking division in the UK has consistently received some of the highest customer satisfactionscores in the industry, as has BarclaysCapital. Absa in South Africa, and ourbusinesses in Botswana, Ghana, andKenya have the highest Brand Healthscores in their markets. The ‘touch pad’initiative in Botswana gives customersthe opportunity to leave instantfeedback at the counter, and this ishelping to strengthen our quality ofservice even further. In Portugal wewere the top-rated bank for counterservice, and in International Retail andCommercial Banking our overall clientnumbers were up 7% in 2005, withparticular increases in France, Portugal,and Absa in South Africa.

We have faced bigger challenges in UK Retail Banking. Having reached a low point in 2004, our customersatisfaction scores rose by 10% in2005, and our customers’ willingnessto recommend us increased 20%during the same period. This ranks

us alongside our major competitors,but our next ambition is to lead thefield on this measure, as part of ouroverall strategy to build the best bankin the UK. As part of this we have:

• Put 700 new cashiers and personal bankers in place.

• Raised entry-level salaries to ensure both a better rate and to help recruit the best.

• Invested heavily in training. • Introduced new technology

to speed up the time it takes to process transactions.

BranchesCustomers increasingly want flexibility in the way they deal with us – through branches, over the telephone and on the internet.Branches remain very important to us because they are important to our customers – our researchshows that nearly 80% of ouraccount-holders use branches at least some of the time. Hence thesubstantial investment that is goinginto upgrading the branch network.

This investment is already showingresults. Queuing times have been cutby an average of one-third, and thenumber of people who say they are‘completely satisfied’ with our serviceis up by 16%. Branch managers havebeen given more power to run theirbranch in the way that best suits theirneighbourhood, including deciding on their own opening hours. Somebranches now open on Saturdays,

“Our duty is to listen tocustomers, and to create a service which addresseswhat they want today.”

John VarleyGroup Chief ExecutiveBarclays

“The marketplace in which we operate is highlycompetitive. If we are tosucceed we must put thecustomer at the centre of our business. We mustdeliver propositions thatdemonstrate value andservice that sees us gettingthings right first time,every time.”

Deanna OppenheimerChief ExecutiveBarclays UK Retail Banking

Responsible bankingCustomer service

4

5Barclays PLC Corporate Responsibility Report 2005

for example, and others open at 8amand close at 6pm, to allow people todo their banking before or after work. We have also made a conscious effortto recruit store managers from leadingretailers so that we can combine ourown banking expertise with the sort ofconsumer understanding that comesfrom the best in retailing.

At the same time, if a branch becomesvery under used, or if there are highsecurity risks about its location, it may no longer be economic to keep itrunning. We appreciate that the issueof branch closures is an emotive oneso we have made a commitment notto close ‘the last bank in town’. If wedo have to close a branch we alwaysabide by the Banking Code.

In France our branches are mostlyconcentrated in Paris and the othermain urban areas, so we are investingin upgrading our online service, andthe Barclays France site now offers full banking facilities in both Frenchand English – a first in the Frenchbanking sector.

Cash machinesAnother area we have focused on isour cash machines – nearly 3,800 ofthem in the UK. Using our machines is free, and we currently have no plansto change that. Our customers canalso use over 30,000 LINK machines,get cash-back at shop tills, and usePost Office counters, all free of charge.Self-service kiosks are also beinginstalled in over 500 branches, and

our online service is being extended,giving people the chance to do alltheir banking in one place.

ComplaintsThe way we deal with complaints isvery much within the scope of our‘Treating Customers Fairly’ agenda.Our Group Complaints Programme,implemented across the businessthroughout 2005, has enabled us withmuch greater clarity to identify and,more importantly, address areas ofcustomer dissatisfaction. In the UK we now have teams of dedicatedcomplaint handling specialists whosupport our customers and colleagueswhen things do go wrong. The new ITsystem we introduced provides moretimely and better quality informationthan we have ever had before.

Six of our major African businesseshave developed their own service

improvement plan, which includesbetter staff training, faster complaint-handling and quicker turnaroundtimes for transactions. In Europe, Italy,Portugal and France all exceeded theirtargets on dealing with customercomplaints in 2005.

Fairer dealsThe way we market and sell ourproducts is a key element ofresponsible banking. It is importantthat our customers have all theinformation they need to make the right decisions for their owncircumstances.

Responsible sellingWe no longer have product-basedsales targets for individual members of staff. We have replaced theminstead with a system that we think isfairer for our customers: there is oneoverall financial goal for each branch,

Working withStonewallLeading up to the change in UK lawin December 2005 we worked withStonewall, the UK gay and lesbiancampaigning organisation, toproduce Getting Hitched – a Plain-English Guide to Civil Partnership,giving them the resources to producea print run of 300,000 rather than the initial 25,000 copies. We alsoworked with Stonewall on a parallel

series of seminars across the country.

In February 2005 Barclays was voted ‘Best Financial Institution’ in the annual poll of readers of thePink Paper.

Call centre of the year

Our contact centre in Cheshire wasvoted European Call Centre of theYear 2005 by Call Centre Focusmagazine.

6

but an equally important paralleltarget relating to local customersatisfaction levels. Our UK branchemployees are rewarded on that basis.

Transaction timesOne of the recurrent issues that allbanks face in the media is the amountof time it takes to clear payments. We offer personal customersimmediate access to their money: our free Instant Banking service allowscustomers to withdraw up to £1,000immediately, without waiting for thecheque to clear. Further progress onreducing the traditional clearing cyclewill come from our collaboration with

the other banks in the Association forPayment Clearing Services (APACS).We are working to provide betterelectronic payment services by theend of 2007.

Overdraft chargesWe know that some customersslip into overdraft by accident, and we now allow people to do this onceevery 12 months without chargingthem. Half a million customers havebenefited so far.

Payment Protection InsuranceAnother industry-wide issue hittingthe headlines is Payment Protection

Insurance, or PPI. These are policiesthat are sold alongside a loan to coverpayments if the borrower has anaccident, falls ill, or is made redundant.The Citizens Advice Bureau made asuper-complaint about PPI to the Officeof Fair Trading (OFT) in September2005. The OFT then looked at themarket as a whole and decided toundertake a formal market study,commencing in March 2006, andexpected to take nine months. The FSA is also monitoring how PPI is sold. Our view is that PPI is a goodproduct as long as it is sold in the rightway, to people who need it. Barclayscustomers do not have to buy PPIwhen they take out a loan and if theydo buy PPI from us we make sure theyhave a clear summary of the policy anda separate breakdown of the costs ofthe loan and the PPI (some providershave been criticised for lumping thesenumbers together). Customers thenhave 30 days to change their mind.

StatementsOur statements have been redesignedto make them clearer, easier tounderstand, and more informative. For example, we now notify people ofchanges to charges on the statementitself, rather than in a separate leaflet.

Unclaimed balancesDormant bank accounts are an issuefor the whole banking industry. We welcome the UK Government’srecognition that some deposits mayappropriately be left to lie in bankaccounts for long periods of time,

Responsible bankingCustomer service

Helping disabledcustomersWe have spent over£78m on makingour services moreaccessible todisabled people, and 93% of our UKbranch network is now accessible.There are planning issues toovercome with the remaining 7% butour eventual target is for all our UKbranches to have accessible features.

92% of Barclays and Woolwichcash machines are at a height thatsuits wheelchair users, and two-thirds of the remainder will bemade accessible by the end of

2007. Every branch has inductionloops for those who are hard ofhearing. All our printed materials inthe UK are also produced in audio,large-text and Braille, includingstatements, letters and productinformation.

We are helping people with learningdisabilities get equal access, partlyby funding ‘It’s Your Money’, abooklet from the Employers’ Forumon Disability which explainsbanking in clear terms.

You can find more information by going towww.barclays.com/responsibilityand clicking ‘services for disabledcustomers’.

7Barclays PLC Corporate Responsibility Report 2005

but that these should be classified as dormant if they are unclaimed for 15 years. We do everything we can to find the rightful owners ofaccounts like this, and we willcontinue to work with the BritishBankers’ Association and theGovernment on the best approach to this issue. We support theGovernment’s proposal to reinvestdormant funds in the community, particularly its focus on financialeducation, financial inclusion andyouth services.

Safer bankingWe take the problem of fraud veryseriously. All Barclays outdoor cashmachines are now protected by ‘anti-skimming’ technology (up from 44% at the end of 2004) which prevents fraudsters tamperingwith cash machines. There are also new security messages on all our cash machines.

Chip and PIN is increasingly making credit and debit cards easier and safer to use, and more improvementsare being made to make online

banking safer.

Customers are naturallyconcerned aboutthe security of

online banking.We areintroducingmore security

messages on

our online site, and a safer two-phaseauthentication process, which willwork alongside an expert transactionprofiling system designed to interceptsuspicious transactions. Thesechanges are designed to enhancefurther the security of online bankingwithout reducing ease of access byour customers; all these changes are in line with the requirements of theDisability Discrimination Act. We are working with other banks andspecialist anti-virus companies to dealwith Trojans and ‘phishing’, and wecollaborate with the authorities toclose down phishing sites as soon as they are identified.

For more details on online security and steps you can take to protect yourself, visitwww.barclays.co.uk/security

Anti-money launderingWe observe high standards of customer identification andverification, wherever we operatearound the world. We work closelywith all the relevant authorities,

and use sophisticated IT systems to monitor and report suspicioustransactions.

We have set out our 2005 targetsand achievements for customerservice, and our new goals for 2006,in the fold-out table behind page 2.

$85bnBarclays Global Investors manages$85bn in ethical funds on behalf ofour clients.

iShares

Barclays Global Investors iSharesKLD Select Social Index Fund,

available in the US, invests in largecapitalisation companies that have a positive social and environmentalrecord. The fund had grown from$20m under management inJanuary 2005, to $117m byDecember 2005.

8

Responsible bankingFinancial inclusion

A bank account is something manypeople take for granted, but billions of people around the world do not have one. Lack of access to banking isa big problem in developing countriesand contributes to exclusion even in adeveloped country like the UK.

Into themainstream

9Barclays PLC Corporate Responsibility Report 2005

The United Kingdom“Two million families have no bankaccount. It costs them more to paytheir bills. Credit costs more. It makesit harder for them to get a job.”

This is UK Chancellor of theExchequer, Gordon Brown, in December 2004, announcing thecreation of a Government taskforceand £120m fund to tackle financialexclusion. Over a year on and thisissue is still high on the Government’slist of priorities. A key aim is to workwith banks to halve the number of UK households that have no bankaccount by the end of 2006. This is a challenging target for all concerned,but as a leading UK bank we recognisethat we have an important role to play.

Bringing ‘unbanked’ people into themainstream of financial services is anintegral part of responsible banking.Basic bank accounts have a part toplay in this, but they are only oneelement of a complex equation.

A business opportunityThinking about financial inclusion in both social and commercial terms is a good mindset to have and weapproach this issue as we would anyother business challenge. This means

“Barclays is the bank that hasdone the most to advanceboth thinking and action onfinancial inclusion in the UK,and its efforts put it ahead of other banks assessedworldwide.”

ANZ BankFinancial Literacy & Inclusion –Global Benchmarking ReportSeptember 2005

Microfinance in Ghana

Less than 10% of the population in Ghana has a bank account.However, the majority of the peopleuse traditional forms of banking that go back centuries.

Barclays is working with Ghana’sSusu collectors who look after thedaily spare income of their clients,who are mainly market traders. Thisis then returned by the Susu collectorat the end of each month, minus oneday’s deposit as exchange for thegreater security provided. Thougheach individual client’s deposit is too small for high street banking,collectively they amount to a £75m economy.

Barclays has invested 2.4 billion cedis(£150,000) into its Microbanking

initiative, providing Susu collectorswith deposit accounts and loans toon-lend, as well as providing trainingfor these Susu collectors andfinancial education for the traders.

As Dominic Bruynseels, ManagingDirector of Barclays Africa and Middle East, says: “This is aboutaccess to capital for market traders and smallindigenousprivate sectoroperators. We are learningabout how wemight operate – and how differentcultures handle the issue ofmicrocredit.”

having a full understanding of theneeds of the people we are trying toreach and taking a creative approachto addressing whatever barriers arestanding in their way. But in the caseof financial exclusion the causes arecomplex and especially sensitive. It is not just about the availability ofproducts and services but about a lackof confidence, a lack of understandingand many other practical issues thatare not always immediately obvious.Some people are not ready or willingto join mainstream banking and there

are some services that high streetbanks like Barclays simply are not set up to provide.

This is why we have to be realisticabout what we can do ourselves, and what can better be done by the Government, or communityorganisations. The key here is gettingall these groups to work together,which is why we put so muchemphasis on collaborations andpartnerships when we are dealing with this problem.

10

ABC – advice, banking, creditHowever complicated the causes ofexclusion, the areas that need to beaddressed are clear enough. Tacklingthe ‘ABC’ of financial inclusion meansgiving people better access to advice,banking, and credit. There are clearlywider questions that also need to beconsidered – including savings andpensions – but the ABC issues,underpinned by better financialeducation, are the real priorities if we are to help people out of cycles of exclusion and debt.

AdviceThere are two facets to this. Peoplestruggling with debt need specificguidance about how to manage it but there is also a broader need forbasic financial education so that fewer people get into problems in the first place. We have a part to playin both of these areas – both as alender to our own customers and as a supporter of organisations whospecialise in providing general adviceand information. Improving the overalllevel of financial literacy is a biggerchallenge, and the main responsibilityfor this has to lie with governments –not least because it has to start asearly as primary school.

Providing clear information and advice to our customers is an integral

part of responsible banking. We have been working hard to do this better,and to give customers more support if they get into difficulties. But peoplewho are financially excluded tend to have little experience of using financial services, which means thereis an even greater need for down-to-earth information and advice. That is why, for example, we supportedCitizens Advice’s recent successfulpilot researching ways to makefinancial advice more available tothose on low income, and since 2000 have been actively leading anumber of projects designed to tackle financial exclusion. And it isalso why we have been working with independent debt adviceorganisations like the Money AdviceTrust National Debtline, CitizensAdvice, and the Consumer CreditCounselling Service for over ten years (including contributing £3.15m in 2005 alone).

Appealing to young peopleIn the last year we have put particularemphasis on initiatives aimed atyoung people. These include:

• The ‘Thrifty Squid Challenge’ with the youth charity Kikass.

• Ker’ching, a project for 9 to 10 year olds in 75 Londonschools which has also involvedBarclays volunteers.

• Supporting the Personal FinanceEducation Group to support work in Pupil Referral Units.

Barclaycard HorizonsAlongside work like this, we have set up Barclaycard Horizons, a £3mprogramme to help over-indebtedlone parents. Research repeatedlyshows that they are at the greatestrisk of slipping into financialdifficulties. One Parent Families,Citizens Advice, Parentline Plus andthe Family Welfare Association are all supporting the programme, andcombining their skills to help 50,000struggling lone parents and theirchildren with practical support,including money management advice,training and help to get back to work.

In 2006, we will also be launching‘Financial Futures’, a scheme that will involve us working with NCH and Help the Aged.

There is more on all of these projects on our website atwww.barclays.com/community.

BankingWe believe that every high street bankhas a responsibility to provide a basicbank account for people who want itand we take this responsibilityseriously. Our version is the Cash CardAccount, introduced in 2000, andwhich now has over 379,000customers, with over 11.9% of themin more deprived neighbourhoods.

The Cash Card Account is a no-frillscurrent account that gives peoplebasic banking, without allowing themto become overdrawn. It has been

“I congratulate and applaudBarclaycard for the way it is bringing businesses andcharities together. This willmake a very real difference to the emotional and financial hardship that many lone parents and their children face.”

Rt Hon Gordon Brown MPUK Chancellor of the Exchequerat the launch of BarclaycardHorizons, July 2005

Responsible bankingFinancial inclusion

11Barclays PLC Corporate Responsibility Report 2005

designed to be accessible and easy tomanage, but even so there will alwaysbe some groups who will be hard toreach for a mainstream bank. Forexample, homeless people may lackthe standard forms of identification.

With this in mind, in summer 2005 we completed a pilot project with ThePassage, a centre for homeless peoplein London. It was a great success, andhas been developed into an ongoingarrangement. By the end of 2005, 150 of their clients had opened a Cash Card Account.

Easier accessWe have made some importantchanges to the Cash Card Accountthis year. For example, we halved directdebit unpaid fees to reflect the factthat these customers have very lowincome or are on benefits. Followingfeedback from organisations includingThe Passage and SAFE (a Toynbee Halladult advice and education initiative), we have also introduced a moreflexible process for identification andverification, and the account pack isprominently displayed in our branches.These changes are also a response to

some of the points raised in the annual Banking Code Standards Board‘mystery shopper’ survey. They said we needed to raise the visibility of theaccount and make identification andverification easier. Moving forward we know there is more we still need to do to make this account genuinelyaccessible to everyone.

Alongside our own basic bank accountwe are continuing our support for theGovernment’s Universal Bankingprogramme and the Post Office CardAccount, which gives people another

“People come to us for amultitude of reasons, but inmany cases homelessness isconnected with losing a job. And to be employed in the 21stcentury you simply must have a bank account. The Passage isdeeply grateful to Barclays andtheir support with their basicbank account – with their helpmany homeless and unemployedpeople are returning toemployment and, from there, in time, to a normal home life.”

Sister Ellen FlynnDirector The Passage

Support for small businesses in deprived areas(a) of the UKAs at 31st December 2005The figures below refer to firms with a debit turnover of less than £1 million

All Deprived % share % shareBarclays areas 2005 2004(c)

Number of business current accounts 672,533 34,392 5.1 5.0

% in overdraft 24.0 24.4 5.2 5.0

Number of business deposit accounts 276,218 11,850 4.3 4.4

Number of loans 107,394 4,567 4.3 4.1

Loan and overdraft balances (£m) 9,021 356 4.0 4.4

Current and deposit balances (£m) 9,793 512 5.2 5.0

Number of business start-ups during 2005 92,648 7,236 7.8 6.9

2005 start-ups as a % of end-year business customers(b) 15.1 24.1

Ratio of savings to lending 1.09 1.44

Notes(a) ‘Deprived areas’ are those areas defined as such by the Bank of England in its report ‘Finance for small businesses in deprived communities’, November 2000. The term ‘small businesses’ refers to

businesses so defined by the British Bankers’ Association.(b) Business customers are all small businesses (companies, partnerships and sole traders) holding a business current account.(c) Definitional changes agreed by the Bank of England, British Bankers’ Association and contributing banks mean that data contained in this table cannot be compared with that previously supplied

by Barclays for 2000, 2001 and 2002. Data for 2004 has been revised to meet the new definitions.

UK Community Finance Organisations £546,000 Microbanking in Africa£150,000

Community placements £211,000 Research £56,600 Other £25,500

Global investment in financial inclusion 2005

12

option. Barclays is contributing £30mtowards the running costs of thisscheme over five years (2003-2008).

And it is not only in the UK that we are doing this sort of work. In SouthAfrica, Absa has been one of thepioneers of the basic ‘Mzansi’ bankaccount (there is more detail on thison page 25).

Affordable creditWe have a responsibility to provide fair access to loans and our lendingdecisions are based on a customer’sability to repay. We publish our lendingdata (see tables) to encourage widertransparency on lending in deprivedareas – we are currently the only bankto disclose the data for both personaland small business lending.

However, a high street bank likeBarclays is not always the mostappropriate organisation for some typesof loans. For example, high volumes ofvery low value loans, particularly forthose with limited credit histories, donot fit easily into our business. However,we realise that there is a need for thesetype of loans, and that is why wesupport other organisations that arebetter set up to do this.

Community financeWe are a major supporter ofcommunity finance organisations.These include Credit Unions, whichoffer basic savings facilities and loansfor individuals, and CommunityDevelopment Finance Institutions

(CDFIs), which lend to smallbusinesses, social enterprises andindividuals. In fact, Barclays is currentlythe biggest single corporate supporterof the Association of British CreditUnions Limited (ABCUL), the mainnational trade association for CreditUnions, and we have just agreed afurther two years support for the‘PEARLS’ IT system, which we havefunded since its introduction in 2002.This is a practical tool that can helpCredit Unions develop their business,and reach more excluded people.

As Peter Kelly, Head of BarclaysFinancial Inclusion team, says: “CreditUnions and CDFIs can play a crucialrole. It is important that communityfinance organisations develop scale andwe will continue to work in partnershipwith the sector to help make thishappen. Quite simply we need viablealternatives to high-cost lenders toprovide more choice to the mostdisadvantaged in society. The socialimpact of what we are doing is key. For instance, 17 of the organisationswe supported in 2005 provided 4,900loans worth over £10m, collectedsavings of over £1.2m and created orprotected almost 3,000 jobs in the UK.Naturally we hope that some peoplewill then graduate into mainstreambanking, so it makes good businesssense for us to be involved too.”

You can find more information on our website atwww.barclays.com/financialinclusion

Supporting community financeWe funded 35 community financeorganisations in disadvantaged areasacross the UK in 2005. Total supportin the UK amounted to £839,000,including community placements,research, loans and direct grants via two funds.

The Barclays Partnership Fundfocuses on development andongoing costs for organisationsworking in the area of financialinclusion, such as Lincolnshire Credit Union, and Fair Finance in East London.

The Barclays Financial InclusionFund supports smaller initiativesencouraging innovation. In 2005,we supported ten organisationswith a total of almost £130,000. All of the initiatives being fundedinvolved organisations workingtogether in partnerships to tackleexclusion – examples includeSouthwark Credit Union’scollaboration with the BlackfriarsAdvice Centre, and LASA CreditUnion working with local schools in Swansea, Wales.

Responsible bankingFinancial inclusion

“Barclays has played a uniquerole in facilitating many of the changes under way in the credit union movement.Their far-sighted sponsorshipof PEARLS has been a keycatalyst for change.”

Mark LyonetteChief Executive Association of British CreditUnions Limited

Social housing

We committed more than £1.2bn of new loans to regenerate socialhousing in 2005 and we have also been supporting communityfinance projects such as CHANGE,which is working with 14 housingassociations in London, helping togive their tenants better access tofinancial services and information.

13Barclays PLC Corporate Responsibility Report 2005

Commercial opportunitiesWorking with community financeorganisations on a commercial basisopens up new opportunities for bothof us. One example is the growingnumber of cross-referrals between our Local Business Teams and CDFIs – in some situations where we couldnot offer a business loan ourselves wereferred the customer on to their localCDFI. In many cases the customer had been unaware this option even existed.

This is working well in a number ofcases, as it has with The EnterpriseFund in Manchester: our LocalBusiness Team has made 21 referralsto them since May 2005. In 2006 we have the challenge of turning this

into a more robust bank-wide process, but progress is definitelybeing made.

Another initiative that has a positivesocial impact as well as a soundcommercial rationale is the ‘StartRight’ seminar programme. We ranover 300 of these seminars with theNational Federation of EnterpriseAgencies in 2005, which helped morethan 5,000 entrepreneurs start theirfirst business and 10% of thesebusiness people came from deprived areas.

Involving our staffAs part of our wider communityprogramme, we have supportedBarclays volunteers and funded

former staff in community financeroles. This makes a lot of sense as it helps improve their awareness of the problems of financial exclusion,and their specialist skills can be veryuseful to the host organisations. At the end of 2005 there were eight ex-staff working in community finance organisations, including one who has worked in Africa and the Philippines for OpportunityInternational, an internationalmicrofinance organisation.

We have set out our 2005 targetsand achievements on financialinclusion, and our new goals for2006, in the fold-out table behindpage 2.

“Now that I have moved awayfrom the front line in Barclays,it does help me to maintainthose skills gained in retailand business banking –meeting members of thepublic and dealing with real-life issues and theirconsequences. It keeps megrounded and makes me feelI’m making a difference.”

Anne HussainBarclays volunteer at theClockwise Credit Union in Leicester

Support for personal customers in deprived areas(a) of the UKAs at 31st December 2005

2005 Analysis 2004 AnalysisAll Deprived All Deprived % share % share

Barclays areas Barclays areas 2005 2004

Number of current accounts(b) 11,093,000 627,000 10,709,000 592,000 5.7% 5.5%

Number of Cash Card Accounts(b) 379,000 45,000 309,100 36,000 11.9% 11.6%

Cash Cards as % of all current accounts 3.4% 7.2% 2.9% 6.1%

Unsecured loans and OD balances (£m) 11,100 630 10,500 570 5.6% 5.4%

Mortgage lending (£m) 59,600 1,970 61,800 2,060 3.3% 3.3%

Deposit and current account balances (£m) 67,300 2,140 63,000 2,040 3.2% 3.2%

Ratio of deposits to lending 0.95 0.82 0.87 0.78

Notes(a) ‘Deprived areas’ are those areas defined as such by the Bank of England in its report ‘Finance for small businesses in deprived communities’, November 2000.(b) Data in 2005 reflects account numbers rather than customer numbers. 2004 data has been restated to reflect this for comparison.

Reaching outLincolnshire Credit Union andSalford Money Line, two of thecommunity finance organisationssupported by Barclays in 2005

14

Responsible bankingResponsible lending

Over the last decade UK consumerdebt has grown to over £1 trillion.Exercising responsibility in lending has never been more important.

Sensible limits

15Barclays PLC Corporate Responsibility Report 2005

“The problems of people wehelp arise substantially frompenalties and charges. In thiscontext Barclaycard’s newinitiative…represents a moreintelligent approach by lenderswhich offers consumers a helpful choice.”

The Consumer Credit Counselling Service

Summary boxes on statements

Consumer lendingThere can be no arguing with thefigures, or the problems this level ofborrowing can cause – bankruptcyfilings rose by around 30% in 2005,indicating that a number of thosealready struggling to manage theirborrowing effectively are finding itincreasingly challenging. It is hardlysurprising that many commentators,politicians and campaigners areblaming the banks for being over-ready to lend money to people whocannot repay it, or who already havemounting debts from other lenders.

Bad debts are a cost to us as abusiness, so it is hardly in our intereststo lend money if there is no chance of getting it back. As far as we areconcerned, offering transparent,competitive deals is not irresponsiblein itself. Responsible lending meansproviding straightforward informationthat makes the terms of the loan orcredit agreement absolutely clear, sothat the customer understands the full implications for them. And thenapplying strict, sensible criteria abouthow much we lend to any individual.

Prevention is better than cureBarclaycard introduced ‘summaryboxes’ on its statements in 2004. They are relevant here because theyclearly set out the interest rates thatapply and what a customer has to doto manage their account. In addition, the financial consequences of makingonly the minimum repayment everymonth are spelled out on customerstatements. We have now extendedthis idea to our personal loanmarketing material, so new customers are given exactly the same sort ofinformation about the costs andimplications of taking on newborrowing before they sign up for it.

The criteria we use for granting loansis under constant review, and atpresent we typically turn down 55%of the people who come to us for new credit cards. When we lend to a customer who has never had a facility like this before, their initialcredit limits are set at a low level. The typical starting amount is £400 and this will only increase if the customer develops a good track record, and can cope with theincreased borrowing. Even then, thetypical increase is usually only £150,and there will only be one rise in thefirst year. We also reduce customers’credit limits if we become aware thatthey may be getting into difficulties.Early warning signs include regularcash withdrawals and only payingback the minimum amount everymonth – 200,000 accounts had theirlimits reduced in 2005.

This common-sense approach pays off: nearly 50% of Barclaycardcustomers settle their balance in full every month and pay no interest at all. Likewise nearly 70% of personalloans are repaid early.

Sharing informationWe can do more to prevent peoplefrom getting into difficulties in the first place if we pool more informationwith other banks and loan providers.The Government and the Bank ofEngland have put their weight behindthis idea, and in December 2005 wewere a prime mover behind a newindustry-wide scheme to share moreinformation about how people aremanaging their accounts. This willenable us to make better lendingdecisions and help us to spotcustomers who may be starting to have difficulties managing theirborrowing.

This builds on similar existingschemes, and by mid 2006 it will helpall the lenders involved to identify

“Barclaycard has written to100,000 customers offering an experimental product,Barclaycard Combinations, thatcombines features of a creditcard and a loan. Barclaycardsays Combinations is designedto help customers save moneyand reduce debts more quickly.”

The Daily Telegraph*2nd April 2005

Responsible bankingResponsible lending

customers in difficulties more quickly.Levels of debt are important but it isalso about how well customers arecoping with that debt. Frequent cashwithdrawals may be one sign thatthings may be going wrong, as somepeople will take cash from one card to pay another.

If customers do get into difficulties we have a number of ways of helping them deal with their debt. A structured repayment plan is oneoption, another is to reduce theminimum payments and suspend the interest charges until the loan is under control. We also work withthird parties like the Consumer CreditCounselling Service and CitizensAdvice. There is more on this in the chapter on financial inclusion. See page 10 for more detail.

New ideasIn the last year a range of newproducts has been introduced that are specifically designed to helppeople manage their borrowing more effectively.

The BarclaycardFlexi Rate is

the first creditcard thatoffers areduced rate

for customerswho pay off

more than theminimum eachmonth. There are

three levels of interest rate on the card and the more you pay off, thelower the rate on the remainder. Some have called it a gimmick, butorganisations like the Consumer Credit Counselling Service haverecognised that it is a genuine attempt to address a complicatedsocial problem.

We have also been piloting the UK’sfirst combined credit card and loan.Barclaycard Combinations works byshifting the balances that build up on the credit card element over to theloan. This helps cardholders managetheir money more efficiently andminimises the amount of interest they pay.

The third new idea this year ispersonalised messages on loan andcard statements. These allow us towarn customers in advance that theymay be slipping into difficulties, sothat they can take action immediately:debt advisers always advise people to take action as early as possible,which can often prevent thingsreaching a crisis point. Examples ofthese messages are provided in the box above.

Following a test last year we are usingour experience to create a computermodel that will help us identifycustomers who may be getting intofinancial difficulties. The aim will be to offer help and advice at a muchearlier stage. A pilot project started in January 2006.

Personalised messages

Business customersWe have a specialist business supportteam which works with Barclaysrelationship managers whenever oneof their business clients gets intofinancial difficulties. This combinedexpertise is applied to understandingthe problem, and developing robustand creative ways to address it. 853new cases were referred to BusinessSupport over the year and 78% ofcases were referred to the turnaroundteam. The turnaround team’s record is impressive – the team’s success ratein returning customers to financialstability was 80% during 2005.

We have set out our new goals for2006 in the fold-out table behindpage 2.

16

17Barclays PLC Corporate Responsibility Report 2005

Responsible bankingDealing with environmental and social issues in commercial lending

On 4th June 2003, ten internationalbanks came to an agreement inWashington D.C. At first sight hardlyground-breaking news, but this particularagreement has been called “a shiningbeacon for responsible banking”, and ithas revolutionised the way our sectorapproaches project finance.

A differentenvironment

18

“Even if you use anextremely conservativeestimate [the EquatorPrinciples] will change the rules of the road forover $100bn in globalinvestment over the nextten years.”

Peter WoickeFormer Executive Vice-President International FinanceCorporation (IFC)

Responsible bankingDealing with environmentaland social issues incommercial lending

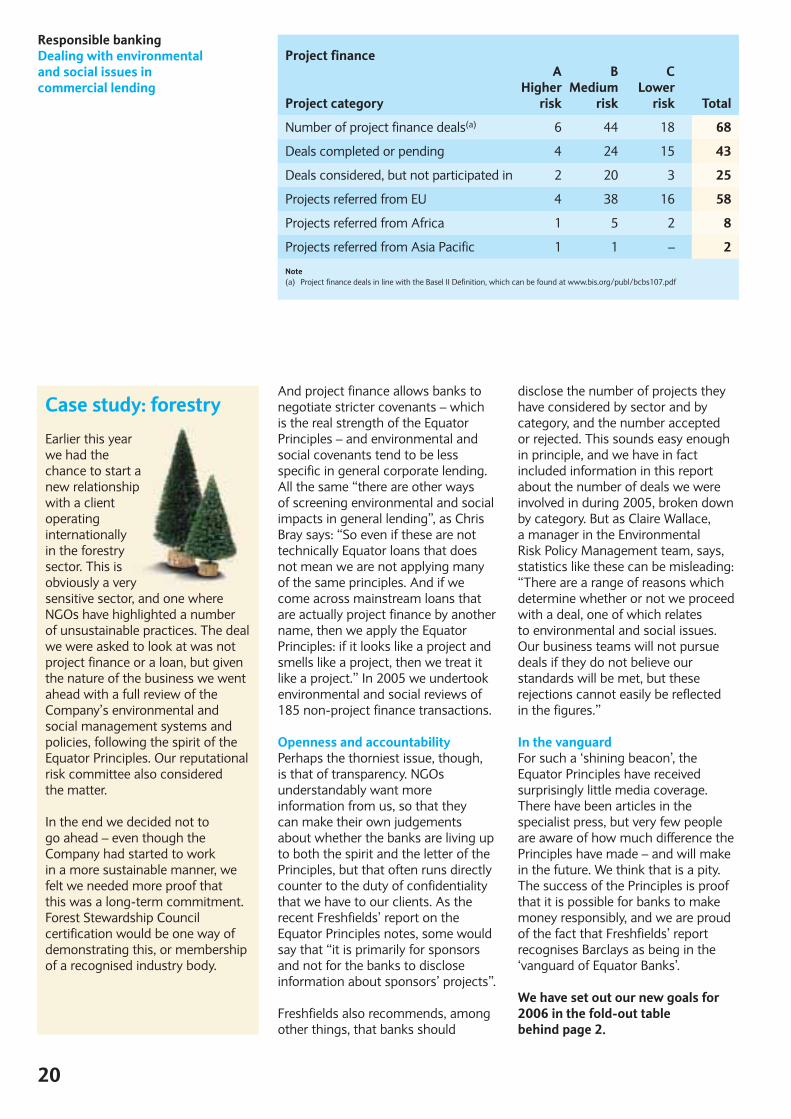

Project financeProject finance has always been oneof the more difficult and contentiousareas of bank lending, partly because it deals with big developmentschemes like dams, mines andpipelines, and partly because itrequires a balance between theadvantages of economic developmentand social and environmentalconcerns. Banks which have adoptedthe Equator Principles make avoluntary commitment to fund onlythose projects that can be “developedin a manner that is socially responsibleand reflects sound environmentalmanagement practices”.

A founder memberBarclays is the third largest projectfinance lender in the world, and we were among the first to develop a robust and structured approach to dealing with these issues. Westarted assessing and managingenvironmental risks in 1997, and five years down the line we were one of the first banks to recognise thatthere was a need to raise standards

across the whole sector. That was a bold step in itself, since projectfinance is a fiercely competitive field,but judging by the progress that hasbeen made it was clearly an ideawhose time had come.

In 2002, when the Equator discussionsfirst started, it was Chris Bray, our Head of Environmental Risk PolicyManagement, who was one of the four‘founding fathers’ of the agreement.He was Barclays representative on thefour-bank team that came up with the initial shape and scope of thePrinciples, based on their own bank’sexpertise and experience. By the timewe adopted the agreement there weresix more banks involved, and another30 have followed since.

Principles in practice Our own commitment to the EquatorPrinciples stems from a combinationof ethical and commercialmotivations: minimising a project’ssocial and environmental impact isunquestionably the right thing to do,but it also makes good commercialsense. As Gerard Holden, ManagingDirector of Barclays Capital’s Miningand Metals team observes: “In thesector we cover, the Equator Principlesare a key element of the businessdynamic, and we believe they are good for business. Not only must allour projects meet the letter of thePrinciples, but the team also worksdiligently to ensure there is realcompliance after the loan is signed.Taking a leading role in this area has

also attracted new business, becauseour team can assist clients as theydevelop their own mining projectsaround the world.”

Adopting the Equator Principles wasnot such a step change for us as it has been for some banks, because we were doing so much in this areaalready. But it has given us a newfocus, and prompted us to changesome of our decision-makingprocesses, and develop new ones.Something we have done this year is to create a new tool to categoriseprojects under the Equator system(see the box for more on this).

We have also spent a great deal oftime and effort on training, whicheveryone agrees is key to the realsuccess of the Principles. Top levelcommitment is crucial, but it is thepeople on the ground who make thepractical decisions. We focused inparticular on Asia this year, holding a seminar for staff from eight localoffices and Australia. Overall, wecoached over 350 people from 16 different locations in 2005,including staff from the lending, risk and legal departments in Barclays Capital and UK Banking.

Internal guidelinesWe also have guidelines that deal with the specific risks and industrypractices affecting 32 of the mostsensitive sectors. These includeairports, forestry and logging, dams,mining, oil and gas, pipelines,

19Barclays PLC Corporate Responsibility Report 2005

“Integrating environmentaland broader social issuesinto [banks’] core creditrisk management isessential to managingcredit risk in the 21st century.”

Reed HuppmanPartner Environmental ResourcesManagement Washington D.C.

How the EquatorPrinciples work in practice…

The Equator Principles cover projectsin all sectors of industry, and anydeal over $50m in size. An EquatorBank must do a full environmentalassessment for any project coveredby these parameters, to evaluatewhether the scheme is high, mediumor low risk (Category A, B or C).Category A projects must then carryout a full public consultation aroundthe proposed site, and prepare anenvironmental management plan.But regardless of category, allEquator projects must observe locallaws, World Bank guidelines, and theInternational Finance Corporation’spollution prevention rules. Indeveloping countries there are alsostrict IFC Safeguard policies on issuessuch as habitat, indigenous people,involuntary resettlement and forestry.

…and at Barclays

We go beyond the basics of theEquator Principles by applying thesame standards to every A or Bcategory project, whatever its size.And when we categorise a project as A, B or C we always getindependent confirmation from anoutside expert, to avoid any dangerof a high-risk project slipping into a lower tier.

Our deal teams work side by sidewith the credit team, and the mainenvironmental and social risk teamto evaluate new loans. We also have a panel of top independentconsultants who undertakeenvironmental assessments for us.

For more information, go to:www.personal.barclays.co.uk/PFS/A/content/files/environment.and.social.risk.pdf

“When working to Barclays requirements [forenvironmental assessments],URS is always aware that theexpected scope is regularlyupdated and extended by the Bank to reflect currentconsultancy thinking…

…Such assignments presenttheir own unique challengesgiven the range of issues whichmust be addressed.”

Robert FitzsimmonsManaging Principal ConsultantURS London

of meetings with leading companies,government departments, and someof the key Non-GovernmentalOrganisations (NGOs). Most of thesegroups have supported the Principlesas a powerful force for positivechange, but it is fair to say that theapplause has not been universal.

Addressing the issuesSome NGOs criticise the Principlesbecause the social angle is not as welldeveloped as the environmental one.We accept that our environmentalexpertise is currently more developedthan our understanding of socialissues, and this will be a major area of focus for us in 2006. We will beupdating our sector guidelines toinclude more social risk, and makingmore extensive use of specialistconsultants to help us identify andmanage these issues.

Other NGOs criticise the Principlesbecause they only apply to deals over $50m capital cost, and only to project finance. In Barclays case we do not restrict ourselves to the $50m threshold, which means thatany sensitive project will get the full Equator treatment. But thelimitation of the Principles to project finance is more complicated to resolve. The nature of project finance suits the Equator Principlesbecause the banks have far greaterinfluence over the way funds are allocated during the life of the loan.

electricity production and wastemanagement. Wherever we can wemake use of international best practicein these briefings – for example, wefollow the Forest Stewardship Councilguidelines in the forestry guidancenote. In 2006 we will be revising all the guidance notes to take the newInternational Finance Corporation (IFC)Performance Standards into account

(the IFC is the private sectordevelopment arm of the World Bank).

Next stepsThe Principles are now being reviewed by the Equator Banks, in parallel with the IFC’s work toupgrade its Safeguard Policies intoPerformance Standards. As part of this process we have held a number

20

And project finance allows banks tonegotiate stricter covenants – which is the real strength of the EquatorPrinciples – and environmental andsocial covenants tend to be lessspecific in general corporate lending.All the same “there are other ways of screening environmental and socialimpacts in general lending”, as ChrisBray says: “So even if these are nottechnically Equator loans that doesnot mean we are not applying manyof the same principles. And if wecome across mainstream loans thatare actually project finance by anothername, then we apply the EquatorPrinciples: if it looks like a project andsmells like a project, then we treat itlike a project.” In 2005 we undertookenvironmental and social reviews of185 non-project finance transactions.

Openness and accountabilityPerhaps the thorniest issue, though, is that of transparency. NGOsunderstandably want moreinformation from us, so that they can make their own judgements about whether the banks are living upto both the spirit and the letter of thePrinciples, but that often runs directlycounter to the duty of confidentialitythat we have to our clients. As therecent Freshfields’ report on theEquator Principles notes, some wouldsay that “it is primarily for sponsorsand not for the banks to discloseinformation about sponsors’ projects”.

Freshfields also recommends, amongother things, that banks should

disclose the number of projects theyhave considered by sector and bycategory, and the number accepted or rejected. This sounds easy enoughin principle, and we have in factincluded information in this reportabout the number of deals we wereinvolved in during 2005, broken downby category. But as Claire Wallace, a manager in the Environmental Risk Policy Management team, says,statistics like these can be misleading:“There are a range of reasons whichdetermine whether or not we proceedwith a deal, one of which relates to environmental and social issues.Our business teams will not pursuedeals if they do not believe ourstandards will be met, but theserejections cannot easily be reflected in the figures.”

In the vanguardFor such a ‘shining beacon’, theEquator Principles have receivedsurprisingly little media coverage.There have been articles in thespecialist press, but very few peopleare aware of how much difference thePrinciples have made – and will makein the future. We think that is a pity.The success of the Principles is proofthat it is possible for banks to makemoney responsibly, and we are proudof the fact that Freshfields’ reportrecognises Barclays as being in the‘vanguard of Equator Banks’.

We have set out our new goals for2006 in the fold-out table behind page 2.

Project financeA B C

Higher Medium LowerProject category risk risk risk Total

Number of project finance deals(a) 6 44 18 68

Deals completed or pending 4 24 15 43

Deals considered, but not participated in 2 20 3 25

Projects referred from EU 4 38 16 58

Projects referred from Africa 1 5 2 8

Projects referred from Asia Pacific 1 1 – 2

Note(a) Project finance deals in line with the Basel II Definition, which can be found at www.bis.org/publ/bcbs107.pdf

Case study: forestry

Earlier this yearwe had thechance to start anew relationshipwith a clientoperatinginternationally in the forestrysector. This isobviously a verysensitive sector, and one whereNGOs have highlighted a number of unsustainable practices. The dealwe were asked to look at was notproject finance or a loan, but giventhe nature of the business we wentahead with a full review of theCompany’s environmental andsocial management systems andpolicies, following the spirit of theEquator Principles. Our reputationalrisk committee also considered the matter.

In the end we decided not to go ahead – even though theCompany had started to work in a more sustainable manner, wefelt we needed more proof that this was a long-term commitment.Forest Stewardship Councilcertification would be one way ofdemonstrating this, or membershipof a recognised industry body.

Responsible bankingDealing with environmentaland social issues incommercial lending

21Barclays PLC Corporate Responsibility Report 2005

“Barclays have real in-houseenvironmental assessment expertise and leading projectfinance practices, but have less well-developed expertise in theassessment of social impacts.”

Banking on ResponsibilityFreshfields Bruckhaus DeringerJuly 2005

Non-project finance

Generalpurpose Leveraged Relationship Other

Review type lending deals review facilities(a) Total

No. of reviews 108 35 32 10 185

Note(a) Including letters of credit and bonds.

Case study: mining

We have been appointed projectadviser to a new, long-term miningdevelopment in Asia. This iscurrently at the ‘feasibility study’stage, which means that we arehelping the client to map out thescope of the project in line with the requirements of the EquatorPrinciples. As a result, the mine will be built and operated tointernationally accepted standardsand practices.

Partnerships with local and nationalgovernment will ensure thatsustainable benefits are deliveredduring the life of the project andbeyond. This demonstrates aresponsible approach to the ‘legacyissues’ that are often associated withmining projects, and which are nowa key focus of the InternationalCouncil of Mining and Metals‘Resource Endowment Project’.

As Martin Horgan, AssociateDirector in Barclays Capital Miningand Metals team says: “This minewill act as an engine of sustainablegrowth for the local communityand its surrounding region creating

many new long-term jobopportunities in what is currently a relatively underdeveloped area. In fully addressing the social andenvironmental aspects of the projectprior to development, not only doesthe community in which the mineoperates benefit, but the projectowners benefit through minimising,and where possible mitigating, thesocial and environmental risks oftenassociated with mining operations. Inreducing the project risks by utilisingthe Equator Principles, the mine willmost likely attract more sources offunding and at preferential rates thanan equivalent non-Equator Principlecompliant mining development.”

22

Responsible bankingCarbon trading and renewable energy finance

An important step towards a worldwidemarket in greenhouse gas emissions wasmade in January 2005, when the EU’sinternational emissions trading schemewent live. This will see 2.2 billiontradable carbon allowances given outannually across the 25 member states.

The business ofclimate change

23Barclays PLC Corporate Responsibility Report 2005

Barclays was the first UK bank to setup a dedicated carbon trading desk to help companies and institutionsaccess this market. We made aconscious decision to get into themarket early, because we wanted tohelp shape its development, and thatcovered everything from the creationof standard contracts to the sharing of our trading experience with othernewer players. We also see this marketas an important new business for us, and one where the investmentbanking skills of Barclays Capital can give our clients new tools and techniques to manage theiremissions risks.

One year on from the opening of themarket and we are now the biggestbanking participant and one of themost active institutions in the market.Carbon trading has been integratedinto our other mainstream dealingoperations, and we have pioneeredsome of the key milestones in thedevelopment of carbon trading as aviable and increasingly mature marketin its own right. We did the very firstspot trade in the European market in March 2005, and were the firstbank to take physical delivery ofcarbon allowances. We were also the first bank to do a forward-datedemissions trade using the standarddocumentation used by the financialderivatives market. And in May 2005we did the first trade using the newLondon Energy Brokers’ Carbon Indexas the reference price.

It was to recognise all theseachievements that we were awardedthe Gold Award for Excellence inEmissions Trading at the 2005 EnergyBusiness Awards. Looking ahead, wewill start carbon options trading in2006, and we are already developingweather and flood risk managementproducts. We will also be exploring the possibility of offering ‘over the counter’ carbon services so that smaller businesses, personalcustomers and our own staff can take their own stand against climate change.

RenewablesWe have also played an active part in the development of the market in renewable energy. Our NaturalResources team has provided thelong-term finance behind over2,500MW of new renewablegenerating capacity, including onshore windfarms, landfill gasextraction plants, small-scalehydroelectric projects, biomass

plants and biodiesel conversion plants. Overall, this generates enoughelectricity to power nearly 1.4 millionhouseholds for a year, or a city the size of Los Angeles, California. We are also actively involved in the futuredevelopment of the renewables sector– we support the European WindEnergy Association, the EnvironmentalServices Association, the ScottishRenewables Forum, and we arerepresented on the UK Government’sRenewables Advisory Board and NewTechnologies Committee.