Embed Size (px)

Citation preview

The Franco-German regional bankDie deutsch-französische Regionalbank

Corporate Report 2012

Foresight THROUGH PROXIMITY

2

CONTENTS

Foreword from the Board of Management .................................................. 6

Group Management Report – Overview ......................................................13

SaarLB consolidated financial statements 2012 .......................................58

Consolidated statement of comprehensive income .................................59

Consolidated balance sheet .........................................................................60

Schedule of changes in equity .....................................................................62

Cash flow statement .....................................................................................63

Group Notes to the consolidated financial statements 2012 ..................64

Board of Administration ............................................................................. 142

Board of Management ................................................................................ 143

Independent Auditors’ Report ................................................................... 150

Report of the Board of Administration ..................................................... 151

Organisational Chart ................................................................................... 152

Shareholders ................................................................................................ 153

“Wortsegel” (“Wordsail”)

Steel plastic in Tholey-Sotzweiler, by Heinrich Popp

3

CORPORATE REPORT 2012 | CONTENTS

Take our word for it

As a regional bank with Franco-German

roots, we have grown with the region.

Thanks to our experience and dedication,

knowledge of the regional economy and

culture, we work with our customers to find

the right solutions for present and future

challenges. Take our word for it.

4

At a glance (IFRS)

* Including security repurchase transactions and interests in entities valued at equity

** Including shares of profits in associated companies accounted for using the equity method

*** Change in the figure from 2011

1. BALANCE SHEET 31 DEC. 2012 EUR MILLION

31 DEC. 2011 EUR MILLION

CHANGE IN %

Total assets 18,740 19,761*** -5.2

Business volumes 19,713 20,912 -5.7

Loans and advances to banks 3,246 4,106 -20.9

Loans and advances to customers 9,039 8,607 5.0

Assets held for trading 518 432 19.9

Investments* 5,271 6,531 -19.3

Liabilities to banks 6,000 8,008 -25.1

Liabilities to customers 5,898 5,905 -0.1

Securitised liabilities 5,115 4,329 18.2

Liabilities held for trading 645 544 18.6

Shareholders’ equity 559 461 21.3

Liable capital in acc. with Sec. 10 KWG/Banking Act

932 976 -4.5

2. PROFIT AND LOSS ACCOUNT

Net interest and commission income** 146.1 133.8 9.2

Gains or losses on fair value measurement 37.0 -16.2 >100.0

Administrative expenses 72.4 78.5 -7.8

Earnings before taxes 82.1 18.4*** >100.0

Consolidated net income/loss for the year 59.4 22.2*** >100.0

5

SaarLB’s earnings were exceptional in 2012.

This is proof of the very good collaboration

with our customers and partners in the region

– and the further expansion of our position.

CORPORATE REPORT 2012 | AT A GLANCE (IFRS)

6

Ladies and Gentlemen,Dear Business Partners,

7

We are pleased to present SaarLB’s annual

report for 2012. It was a very successful finan-

cial year that we can look back on, with an af-

ter-tax profit of EUR 59.4 million. There were

multiple reasons for this.

On the one hand, it was due to a constant

improvement in our core business. Both the

volume of business and earnings are steadily

growing.

Growth in the regional economy may have

been weaker than in 2011 and 2010, but we

also saw increasing demand for loans in seg-

ments such as Corporate Customers or Ger-

man Real Estate – and were able to expand

our volume of business here.

Thomas Christian Buchbinder

Corporate Development, Market 2

Corporate Development, Savings Banks, Institutionals

and High Net Worth Individuals, Treasury and Portfolio

Management, LBS Market and Risk Office, Internal Audit

CORPORATE REPORT 2012 | FOREWORD FROM THE BOARD OF MANAGEMENT

8

The real estate business in France and the pro-

ject financing (above all for renewable energy)

performed well. It was the same with strong

municipality business on both the German

and French side. Furthermore, we were able

to further reduce the non-core business –

which is why the balance sheet total fell to

EUR 18.7 billion.

The fact that SaarLB enjoys a very good rep-

utation as an issuer can be seen from the

strong demand for our own issues in the past

year – which let the funding of the bank be

achieved at attractive conditions.

The most important reason for our success is

the mostly long-term business relationships

with our customers. But SaarLB is much more

than “just” a lender: We are advisers in all fi-

nancial questions, an engine for investments

and innovations and promoters of cross-bor-

der business.

Here we would like to present four of our

customers as examples. They are well-known

names in the region. Wendelin von Boch

elaborates on why sustainable business was

always important for him as an entrepreneur

– and why he now built a solar power plant for

this reason. Dr. Guido Colsman and Bruno P.

Proietti from the company Ludwig Schokolade

explain how a Saarland family-run company

with a passion for cocoa products became an

economic success story. Prof. Dr. Peter Theiss

describes how he turned his father’s small

pharmacy into a successful company on five

continents – with natural cosmetics. And Dr.

Karlheinz Blessing makes it clear why the suc-

cessful work in Dillinger Hütte or at Saarstahl

AG has much in common with good harmony

in an orchestra – and why qualified actors, i.e.

employees, guarantee our success.

9

Frank Eloy

Market 1

Corporate Customers,

Real Estate and Projects,

Central Sales Management

SaarLB is much more than “just” a lender.

CORPORATE REPORT 2012 | FOREWORD FROM THE BOARD OF MANAGEMENT

10

Education and training play a major role for us.

The subject of education and training also

plays a major role for SaarLB. It is very impor-

tant that the future generation profits from

experienced colleagues. We will also describe

how well this works at SaarLB in this annual

report. Going beyond the area of education,

we would like to thank all our employees at

this point for their tremendous dedication

yet again in the past year.

Werner Severin

Bank Management/Operations

Overall Bank Management,

Risk Office, Services, Compliance,

Data Protection

11

Good collaboration with our partners in the region is another of the bank’s major “secrets of

success.” SaarLB benefits from the cross-border character of the region. At the same time, it

gives a lot back to the region through its dedication. We support the arts, culture, and science.

We have been an important taxpayer for a long time. The bank offers more than 500 profes-

sional jobs. For the purchasing of products or services, the bank mostly awards contracts to

companies in the area.

Last but not least, we would like to express our particular thanks to our shareholders both in

and outside the region. Their tremendous commitment to the bank will also serve as the basis

for its success in the future.

Werner SeverinThomas Christian Buchbinder Frank Eloy

CORPORATE REPORT 2012 | FOREWORD FROM THE BOARD OF MANAGEMENT

12

13

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

OVERVIEW

ECONOMIC ENVIRONMENT

The German economy enjoyed a strong start

to 2012. In the Summer and increasingly dur-

ing the rest of the year, growth slowed on ac-

count of the poor performance of the global

economy and the difficult situation in the

euro zone. In the fourth quarter, economic

output actually even declined. Overall, real

gross domestic product (GDP) rose by 0.7% in

2012, and foreign trade remained a bright spot

despite the foreign trade environment, as ex-

ports were the strongest driver of growth.

However, on account of weaker demand

from the euro zone, export activity declined

in the last few months of the year. Domestic

demand, which fell overall in real terms, de-

veloped unevenly. Private and government

consumption may have increased and stimu-

lated growth, but investments did not make

a positive contribution for the first time since

the economic crisis in 2009. Construction in-

vestments and capital expenditures declined,

although a positive development is that most

companies kept their employees despite the

hesitancy to make investments. The number

of employed people reached a new record

high in 2012. Government budgets continued

to be reduced, and measured in terms of gross

domestic product (GDP), there was a small

general government surplus of 0.1%.

In the course of 2012, the recovery in the Saar-

land economy weakened substantially. The

reason for this was the development of the

global economy, which had a corresponding

impact on some important export markets.

Demand fell substantially in the steel indus-

try, a significant sector for the Saarland econ-

omy. Machine building also saw a decline in

incoming orders, whereby there was still an

increase in sales. The automotive industry,

on the other hand, performed better. Despite

a decline in economic activity, Saarland and

Germany as a whole achieved a record high

number of employed people.

Economic growth in Rhineland-Palatinate

was primarily fuelled by the service sectors in

the first half of the year. As compared to previ-

ous years, manufacturing made only a minor

contribution. But here, too, companies’ busi-

ness expectations dimmed toward the end of

the year due to the euro crisis.

The French economy did not grow in 2012,

and economic output actually contracted in

the fourth quarter of the past year, although

private consumption and exports had a stabi-

lising impact. Industrial production was quite

volatile over the course of the year, fluctuat-

ing very unevenly within various industrial ar-

eas. The inconsistent business environment

led to a slight overall decline in investment ac-

tivity by companies. Despite a deterioration

in the financial position of companies and

uncertainty with regard to the overall devel-

opment of the economy, the investment ratio

remained on a high level. However, unemploy-

ment continued to rise and, together with a

rise in taxes in the second half of the year, had

a negative impact on the purchasing power of

private households. Private consumption was

helped by the savings of private households.

The Lorraine economy faced a difficult envi-

ronment in 2012. Business activity declined

significantly due to the poor business cli-

mate. Gross domestic product fell by an esti-

mated 0.4%. The investment rate dropped no-

ticeably. There were many lay-offs, especially

in industry, as a result of which unemploy-

ment rates continued to rise. Exports also fell

sharply.

Alsace also suffered an economic slowdown

in 2012, contracting by an estimated 0.3%.

The stagnating economic output forecast for

the second quarter was not confirmed. Small

and medium-sized enterprises (SMEs) had to

withstand a decline in their business activi-

ties. The liquidity situation and earnings fell

as expected. However, the investment rate re-

mained stable despite the negative business

climate in 2012. The number of unemployed

people also increased in Alsace.

Group Management Report

14

FINANCIAL SECTOR

The critical factor on German financial mar-

kets in 2012 was again the European sover-

eign debt crisis, which resulted in a turbulent

year. After the crisis initially spread and also

reached large economies such as Spain and

Italy, massive efforts by central banks in the

second half of the year ensured an improve-

ment. In June 2012, the European Central Bank

(ECB) lowered the interest rate for deposit fa-

cilities to 0.0% p.a. and decided to reduce the

main refinancing rate to 0.75% p.a.

The decision by euro member states to form a

bank union should also stabilise the markets.

The plan for the bank union includes uniform

bank supervision by the ECB, a collective un-

winding and restructuring mechanism and a

European system of deposit insurance. The

establishment of a European bank superviso-

ry authority is a requirement for the direct re-

capitalisation of banks by the European Sta-

bility Mechanism (ESM) and is being forced by

some member states against this backdrop.

The significant regulatory measures that are

usually combined under the description of Ba-

sel III or CRD IV have not been implemented

yet. In contrast to the original plan, coordina-

tion and passage on the European level will

still take some time, which means that these

measures did not enter into force on 1 Janu-

ary 2013. In 2013, additional, currently not

yet completed amendments are waiting for

passage and/or implementation. They include

the separation of investment and commercial

banks and the financial transaction tax. With

regard to its risk-bearing capacity, the Ger-

man banking system is stronger than it was

before the financial market crisis.

SAARLB

SaarLB’s strategic objective is to be a region-

al bank with a focus on corporate customer

lending, real estate business and advisory

services for institutional investors, public sec-

tor/municipalities and high net worth private

customers (wealth management). In recent

years, the Bank has distinguished itself as

a special financier for projects in the area of

renewable energy throughout Germany and

France.

Landesbausparkasse Saar (LBS), part of Saar-

LB, finances primarily residential real estate

through its home loan savings business.

The Bank’s business model depends heavily

on the awarding of long-term loans and is to

be harmonised with respect to the coming

strict requirements of Basel III (particularly

with regard to the core capital ratio and li-

quidity management) by passing through a

control process with supervisory guidelines.

On account of its history and its ownership

structure, SaarLB is an integral part of the

savings banks finance group [Sparkassen-

Finanzgruppe] and places a high priority on

networking work, particularly with the Saar-

land savings banks, while simultaneously con-

centrating on core competencies. SaarLB is a

central bank for the savings banks and is the

principal bank for Saarland.

SaarLB’s ownership structure did not change

from 2011 and took the following form at the

end of 2012:

Saarbrücken 14.9%

SaarLB and its shareholders have each agreed

to commitments that are expected to ensure

the long-term independence of the Bank and

its further development as a Franco-German

regional bank. There is also a framework

agreement with the Sparkassen-und Girover-

band [German Savings Bank Association] on

the principles for collaboration between the

Saarland savings banks and SaarLB. The com-

mitments and the framework agreement set

15

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

forth fundamental framework conditions.

The binding form is determined by the Bank’s

risk strategy.

The SaarLB Group’s target market is made up

of the core market Saarland and the regional

market, which consists of the surrounding

regions in south-west Germany, France and

Luxembourg.

The objective for business financing is funda-

mentally business with target customers that

have their headquarters in the Bank’s target

market or, if their business’s headquarters is

outside of the target market, then at least

the business’s sales are primarily made in the

Bank’s target market.

The requirements for the business objective

in real estate and project financing and LBS

[Landesbausparkasse : subsidiary of savings

bank offering collective real estate savings

products and providing low-interest residen-

tial mortgage loans] are met if the financed

object or project is in Germany or France. For

real estate (with the exception of LBS), the

following criteria must be met:

a) the borrower/investor/asset manager must

be based in the target market or

b) the financed object must be in the target

market.

Portfolio financing is a business objective

if the focus of the portfolio is classified as a

business objective.

Customer relationship management is usu-

ally handled according to the so-called re-

lationship management approach, i.e each

customer has a primary contact who works in

a problem- and service-oriented way. For spe-

cial questions (e.g. interest and currency man-

agement), the customer manager receives

support from internal product specialists.

Depending on the significance (monetary/

ideas) of the customer for the Bank, he is in-

cluded in the senior coverage model. As a re-

sult, the customer relationship management

is handled by the respective manager of the

organisational unit, division head or Board of

Management.

On the product side, SaarLB primarily con-

centrates on marketable and standardised

products. Project financing is, however, an ex-

ception on account of the business structure.

Over the long term, complex products and

services that require substantial advice are

primarily handled by cooperation partners.

As a member of the Saarland Sparkassen-Fi-

nanzgruppe, SaarLB and Landesbausparkasse

Saar are heavily involved in the syndication

business and as an arranger with the region’s

savings banks. SaarLB is also a centre of ex-

cellence, particularly for project financing,

corporate financing, foreign commercial busi-

ness and interest and currency management.

SaarLB is the largest bank in Saarland and

feels a particular connection and obligation

to the region. SaarLB has deep roots in the

region and actively shapes economic life,

makes an important contribution to cultural

diversity and promotes the sciences in the

greater region. This is seen, among others, in

the promotion of science and culture through

the awarding of the SaarLB science prize and

countless permanent loans to the Saarland

museum.

EARNINGS

The SaarLB Group’s net interest income (in-

cluding the results of the companies valued

at equity) increased by EUR 16.6 million, from

EUR 122.2 million in 2011 to EUR 138.8 million

in 2012. This is an increase of 13.6%. The de-

cline in interest income from EUR 834.3 mil-

lion in 2011 to EUR 765.4 million in 2012 (-8.3%)

was more than compensated by the decline in

interest expenses from EUR 712.3 million in

2011 to EUR 626.7 million (-12.0%). The decline

in interest income is mainly due to a decrease

of roughly EUR 0.9 million in the portfolio

of investments and the current low interest

16

rates. The drop in interest expenses also re-

flects the advantageous refinancing costs for

SaarLB. In addition, the change in net interest

income is defined by one-off effects from the

receipt of prepayment penalties on interest

derivatives (approx. EUR 5.0 million).

Interest income from credit and money mar-

ket transactions fell slightly from the previ-

ous year (-1.3%).

As in previous years, increases in interest mar-

gin contributions in the corporate custom-

ers business and in real estate and project

financing explained the rise in the net inter-

est income. Thus falling income from other

budgeted reductions in the no longer strate-

gic portfolio from Treasury and Portfolio Man-

agement could be more than compensated

again.

The maturity transformation/treasury gains/

losses totalled EUR 14.8 million in 2012, thus

roughly on the high level of 2011 (EUR 15.8 mil-

lion).

The Landesbausparkasse’s net interest in-

come also increased in comparison to 2011.

The interest expenses for subordinated and

hybrid capital were EUR 19.5 million in 2012,

slightly below the amount in 2011 (EUR 20.1

million).

Expenses for risk provisions in the credit busi-

ness rose substantially, by EUR 14.4 million,

from EUR 18.9 million in 2011 to EUR 33.3 mil-

lion in 2012, but were still below the expected

amount in the budget for 2012.

The increase in the risk provisions is mainly due

to the valuation of the Treasury and Portfolio

Management segment in which the reduction

portfolio of non-strategic assets is managed.

Approx. 62.6% of the individual risk provisions

created for all segments, including provisions

for off-balance-sheet transactions, are repre-

sented by this segment. This was countered

by the risk provision requirement in the area of

corporate customers, which was significantly

reduced to roughly 4.4% of the net newly cre-

ated provisions. 29.7% of the risk provisions

for individual transactions can be attributed

to the real estate financing segment.

An additional negative impact was made by

the net additions to portfolio risk provisions

in the credit business for a total of EUR 2.4

million in 2012. This was also offset by a re-

lease of EUR 3.7 million in 2011.

Net commission income totalled EUR 7.3 mil-

lion and did not remain on the level from 2011

(EUR 11.5 million).

The decline in the net commission income is

primarily due to a drop in the commission in-

come from the credit and home loan savings

business.

The commission income in the credit busi-

ness was EUR 0.2 million below the level from

2011, despite good new business of EUR 12.9

million. The commission expenses totalled

EUR 1.6 million, in part due to significantly

higher than planned brokerage commissions,

and were EUR 0.8 million above the level from

2011 as a result.

The commission income from the home loan

savings business rose 2.5% to EUR 4.3 mil-

lion and was therefore roughly on the level

of the previous year. Commission expenses

increased 19.1% and reflect the substantial

rise in closing fees for home loan savings

contracts and the related brokerage commis-

sions.

Future increases in net interest income can be

viewed in comparison to the commission ex-

penses for the brokerage of credit and home

loan savings business, which were above the

level from the previous year.

The net commission income in the securi-

ties business declined from the previous

year to EUR -0.7 million (2011: EUR 1.5 mil-

lion) and is mainly due to lower year-on-year

17

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

commission income from EUREX transactions

of EUR 1.1 million. This is due to changes in the

investment habits of special funds, for which

SaarLB assumes the custodian bank function.

The gains on fair value measurement and

hedge accounting totalled EUR 36.9 million in

2012 and greatly exceeded the amount from

2011 (EUR -16.1 million). The improvement of

EUR 53.0 million is primarily comprised of

positive, planned maturity effects related

to interest swaps (EUR 4.8 million), the posi-

tive market development of credit deriva-

tives (EUR 5.4 million) and the very positive

valuation effects from securities measured

at fair value (EUR 24.8 million). Alone roughly

EUR 16.0 million are attributable to securities

invested in special funds; another roughly

EUR 9.0 million are due to securities that

were invested as part of the LCR portfolio.

The losses on hedge accounting totalled

EUR -0.2 million in the year under review and

were at the level of the previous year and in-

significant.

The gains on investments were EUR 3.2 mil-

lion in 2012, which reflected an increase of EUR

3.7 million from the level in 2011. The gains in

2012 were affected by disposal losses for Greek

bank bonds of EUR 5.9 million, which could

largely be compensated by the release of the

portfolio risk provision created for this in 2011

and amounting to a total of EUR 4.9 million.

Furthermore, another EUR 1.5 million in port-

folio risk provisions were released and had a

positive impact on income from investments.

The decline in gains/losses on the dispos-

al amount of EUR 11.7 million in 2011 to

EUR -3.7 million in 2012 is mainly due to a

special effect in 2011 related to the sale of the

DEKA bank shares (EUR + 12.3 million) and the

disposal losses on Greek bank bonds.

The write-down of debt securities and other

fixed income securities was EUR 0.7 million

and thus significantly below the amount from

the previous year (EUR 12.3 million).

Administrative expenses incl. the deprecia-

tion of property, plant and equipment and

the amortisation of other intangible assets

totalled EUR 72.4 million on 31 December 2012

and was EUR 6.7 million lower than planned

and also EUR 6.1 million below the amount in

2011 (EUR 78.5 million).

Personnel expenses rose slightly by

EUR 1.8 million year on year. On the other

hand, other administrative expenses fell

by EUR 8.4 million as compared to 2011

(EUR 37.6 million). This is mainly due to the

high one-off IT expenses (approx. EUR 8.5 mil-

lion) in 2011, which were connected with the

system migration to OSPlus. The depreciation

of property, plant and equipment and the am-

ortisation of other intangible assets totalled

EUR 2.6 million and was slightly above the

level from 2011 (EUR 2.2 million).

Other income amounted to EUR 1.6 million in

2012 (2011: EUR -1.3 million).

Other income rose from EUR 4.0 million in 2011

to EUR 5.1 million in 2012. It mainly includes

rental income from investment property

(EUR 1.3 million; 2011: EUR 1.4 million), income

from the release of provisions (EUR 0.9 mil-

lion; 2011: EUR 1.2 million) and other income

(EUR 1.8 million; 2011: EUR 0.8 million).

Other expenses totalled EUR 3.5 million in

2012, which was EUR 1.7 million below the

level from 2011 (EUR 5.2 million). The offset-

ting expenses with partnerships were critical

here and amounted to EUR 1.0 million (2011:

EUR 1.5 million).

In total, there was a consolidated net profit

before taxes of EUR 82.1 million in financial

year 2012 (2011: EUR 18.5 million).

After taking into account the tax expenses

of EUR 22.7 million (2011: EUR +3.8 million),

SaarLB had a consolidated net profit after

taxes of EUR 59.4 million (2011: EUR 22.2

million). The tax expenses consist of an ac-

tual tax expense of EUR 15.7 million and an

18

expense for deferred taxes of EUR 7.0 mil-

lion.

The SaarLB Group will service its hybrid capi-

tal in full in 2012, similar to previous years.

EUR 9.7 million (2011: EUR 10.7 million) will

be distributed on the equity component of

the hybrid capital. A dividend on the share-

holder capital of SaarLB will not be paid in

2012. As a result, the total consolidated profit

of EUR 49.7 million will remain (2011: EUR 11.3

million).

The cost income ratio (CIR) fell from 59.3% in

2011 to 49.0% in 2012. The cost income ratio

is calculated for the respective financial year

on the basis of the administrative expenses

in relation to the Bank’s income (net interest

income, net commission income and net trad-

ing income less additions to risk provisions).

The lower administrative expenses alongside

a substantial rise in income had a major im-

pact on the CIR in 2012.

On account of the very positive course of busi-

ness in 2012, the return on equity, which is

based on the consolidated profit before taxes

in relation to the currently available equity,

rose by 11.0 percentage points, from 3.0% in

2011 to 14.0% in 2012.

19

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

FINANCIAL POSITION

The SaarLB Group’s financial position re-

mained good in 2012. The inflow of liquid-

ity over the next few years is ensured on ac-

count of the current refinancing structures.

The flow of liquidity from the asset business

can be used again to refinance new business.

The expansion of the mortgage collateral real

estate business in 2012 continued to back

the surplus cover in SaarLB’s collateral pool

and the collateral pool for Pfandbriefe, and

remains on a high level, even if it fell slightly

from 2011. The lower surplus cover is mainly

due to an increase in the issuing of mortgage

Pfandbriefe and declining cover funds for

public sector Pfandbriefe.

The situation on the capital market, from the

perspective of the SaarLB Group, substan-

tially improved again as compared to finan-

cial year 2011. With just under EUR 2.3 billion

(2011: EUR 0.7 billion), the placed volumes

in 2012 rose significantly again year on year,

whereby the total volume solely took place

as part of private placements with custom-

ers and financial partners. As a result, SaarLB

was largely independent of capital markets

in 2012. In the process, the SaarLB Group also

succeeded in refinancing itself primarily via

uncollateralized issuances with long maturi-

ties.

In order to ensure solvency at all times, Saar-

LB deposited securities amounting to roughly

EUR 1.4 billion at the ECB, as in 2011. Payment

obligations could therefore be met indepen-

dently of other sources of refinancing.

The SaarLB Group’s ability to meet its pay-

ment obligations was thus ensured at all

times in the 2012 financial year.

The SaarLB Group’s access to money markets

and capital markets is supported by the credit

ratings of two international rating agencies.

The two rating agencies Moody’s Investor

Service and Fitch Ratings confirmed SaarLB’s

credit rating as an issuer in the past financial

year.

Rating Moody’s Fitch

Long-term rating (uncollateralised)

with government liability Aa1 AAA

without government liability A3 A

Short-term rating (uncollateralised) P-2 F1

Financial strength/viability rating D BB+

20

ASSETS

The SaarLB Group’s total assets fell by 5.2%

to EUR 18.7 billion as of 31 December 2012 (31

December 2011: EUR 19.8 billion). The decline

mainly results from a substantially lower

portfolio of investments, which is due to the

planned decrease in the reduction portfolio

for the most part. Furthermore, short-term

loans and advances to banks decreased sub-

stantially in comparison to the treasury-

related high level on 31 December 2011. The

increase in loans and advances to customers

by some EUR 0.4 billion in the core segments

of the Bank more than compensated for this.

In terms of liabilities, this decrease was pri-

marily reflected in a decline in short-term

bank liabilities. Scheduled maturities for

profit participation rights and subordinated

liabilities led to a further decrease in subordi-

nated capital.

The SaarLB Group’s equity increased to

EUR 558.8 million (2011: EUR 462.0 million)

in the year under review. This was primarily a

result of the increase in revaluation reserves

and the consolidated net income generated

in 2012.

The credit volume of the SaarLB Group – simi-

lar to total assets – fell by 9.2% from EUR 20.3

billion to EUR 18.4 billion in the 2012 financial

year.

Loans and advances to banks made a signifi-

cant contribution, declining year on year by

some EUR 0.9 billion to EUR 3.2 billion. The

decrease in invested excess liquidity in 2011 is

responsible for this.

Another major driver of the declining credit

volume was investments (including securities

repurchase transactions) that fell by EUR 1.3

billion, from EUR 6.5 billion to EUR 5.3 billion

(-19.3%) in the past financial year. The reasons

for this include the repayment of bank securi-

ties and investments in international corpo-

rates that do not belong to the core business.

PORTFOLIO PERFORMANCE

Change

in EUR million 31 Dec. 2012 31 Dec. 2011 Δ in EUR million Δ in %

Loans and advances to banks 3,246.1 4,105.6 -859.5 -20.9 %

Investments 5,271.3 6,531.2 -1,259.9 -19.3 %

of which

Interests in associated companies 2.9 2.8 0.1 4.1 %

Investments 4,698.4 5,574.2 -875.8 -15.7 %

Securities repurchase transactions 570.0 954.2 -384.2 -40.3 %

Loans and advances to customers 9,039.0 8,607.2 431.8 5.0 %

Contingent liabilities 274.3 290.2 -15.8 -5.5 %

Irrevocable credit commitments 592.9 756.7 -163.8 -21.6 %

Total credit volume 18,423.6 20,290.9 -1,867.2 -9.2 %

21

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

A slightly different development was seen in

loans and advances to customers, which are

mainly influenced by the Bank’s core business

segments. Loans and advances to customers

increased by EUR 0.4 billion to EUR 9.0 billion

in 2012 (2011: EUR 8.6 billion), primarily in the

long-term maturity area.

Contingent liabilities totalled EUR 0.3 bil-

lion in 2012 (2011: EUR 0.3 billion), while ir-

revocable credit commitments amounted to

EUR 0.6 billion and were 21.6% below the pre-

vious year (2011: EUR 0.8 billion).

The credit portfolio performance is reflected –

as illustrated in the following – in the busi-

ness segments of the SaarLB Group:

Corporate Customers services corporate cus-

tomers in Germany and corporate customers,

municipalities and municipally owned com-

panies in France. The target markets in Ger-

many include Saarland, Rhineland-Palatinate

and the surrounding regions. In France, the

SaarLB Group concentrates on the Grand Est

and here in particular on the neighbouring Al-

sace-Lorraine where the Bank is represented

by its SaarLB France branch at the offices in

Metz and Strasbourg.

In the past financial year, the positive trend

from 2010 continued. Both in our target mar-

kets of Saarland, Rhineland-Palatinate and

the surrounding regions, including the French

side, and particularly Alsace and Lorraine,

it was possible to significantly increase the

credit volume reported at the end of the year.

This is, among others, due to the increased us-

age of cross-border consulting and financial

services, which has let the SaarLB Group use

and further expand its unique selling point

among French and German customers. The

SaarLB Group also benefits, on the German

side, from long-term customer relationships

that were in turn the basis for the structur-

ing and financial support of numerous in-

vestment projects in 2012. The revaluation

of the entire Corporate Customers business

segment amounts to EUR 420 million (2010:

EUR 196 million), whereby roughly 55% is at-

tributable to Germany and 45% to France. The

margins on the French market increased no-

ticeably year on year, while in Germany it was

possible to maintain the high level from the

previous year. Risk premiums can be charged

increasingly better on the market in France.

Furthermore, the quality of the portfolio

continued to improve on account of the thor-

oughly better than planned ratings in new

business. Overall, the credit volume in the

business segment as of 31 December 2012 was

EUR 2.1 billion, and thus EUR 0.2 billion above

the level from the prior year.

Real Estate is responsible for the financing of

commercial real estate in the SaarLB Group.

The regional focus is also on the German tar-

get market already defined for the Corporate

Customers segment and the French Grand

Est, with a focus on the Île-de-France. The

management of French real estate financiers

is also handled from the offices in Paris. Addi-

tionally, Real Estate monitors public private

partnership measures (PPP) for investments

in infrastructure and education as well as

other public sector construction measures in

the German regional market. In Real Estate,

roughly EUR 447 million was revalued/extend-

ed in 2012 (2011: EUR 631 million) of which

EUR 202 million was in France and EUR 245

million in Germany. On the German market,

the budgeted targets for the past financial

year were substantially exceeded, by roughly

70%. The French business, on the other hand,

was roughly 40% below the budget, which is

mainly due to the stronger competition in

the conditions for high-quality business. The

targeted margins in both segments are above

the budget. In France, the missed targets

in volume were overcompensated by higher

margins. In total, the credit volume in the

segment amounts to EUR 2.8 billion, which is

EUR 0.2 billion above the level from the prior

year.

The Projects segment is responsible for the

financing of projects in the SaarLB Group,

especially in the renewable energy sector,

22

but also in the area of public private partner-

ship (PPP) on the French market. The regional

business also focuses on the target markets

already defined in the Corporate Customers

segment. In Project Financing subsegment,

loans for renewable energies were valued at

EUR 393 million (2011: EUR 561 million). Of this

amount, as in the previous year, almost 90%

was attributable to the French market, which

again underscores the substantial market po-

sition and the structuring and legal expertise

of the SaarLB Group as the Franco-German

regional bank. The planned volumes could be

slightly exceeded, which is primarily due to

the French business with renewable energies.

In total, the credit volume of EUR 1.5 billion in

the segment as of 31 December 2011 increased

by roughly EUR 0.3 billion to EUR 1.8 billion as

of 31 December 2012. In the PPP France sub-

segment, the Group was able to expand its

market position. The total volume here was

EUR 83 million in 2012, as compared to EUR 53

million in the previous year.

Privately used real estate was financed, in

close collaboration with the Saarland sav-

ings banks, exclusively through Landesbau-

sparkasse Saar, which belongs to the SaarLB

Group. The customer credit volume for the

Landesbausparkasse was a good EUR 0.5 bil-

lion as of 31 December 2012, that is, slightly

above the level in 2011.

Savings Banks, Institutionals and High Net

Worth Individuals provides asset advice and

management for savings banks, institutional

investors and high net worth individuals. The

focus of Savings Banks and Institutionals is

on increasing existing customer connections

and expanding contacts with insurance com-

panies and pension funds in the region and

the business relationships to savings banks

in Rhineland-Palatinate. It also deals with the

financing of the region’s savings banks and

municipalities. The credit volume – primarily

from the financing of municipalities in the re-

gion – fell slightly from roughly EUR 2.1 billion

to roughly EUR 2.0 billion year on year. New

business in the municipal sector successively

improved, particularly for the securing of the

low interest rates, while the loan volume in

this subsegment was roughly at the level of

the previous year, although margins increased

from 6 bp to 9 bp year on year. The good liquid-

ity situation at savings banks kept a lid on de-

mand, resulting in a drop in loan volumes by

EUR 131 million to EUR 744 million in the 2012

financial year.

The non-portfolio related business with insti-

tutional investors improved significantly year

on year due to the very successful placement

of SaarLB issues.

In the business with high net worth individu-

als, SaarLB continues to see risk aversion due

to the ongoing discussions surrounding the

debt crisis. The low interest rates also lead to

a decrease in margins in the asset area. In ad-

dition to the cooperation between the SaarLB

Group and Berenberg Bank, Hamburg, which

has existed since the end of 2009, we im-

proved high net worth individuals’ perception

of the SaarLB Group through the creation of

a specialized team for wealth management in

2012 and strengthened our image in this seg-

ment. Volumes with high net worth clients

increased even more here.

The Treasury and Portfolio Management seg-

ment handles the active management of all

the portfolios of the SaarLB Group that no

longer belong to the core business. This in-

cludes both the so-called reduction portfo-

lios (mainly the investments in international

banks and corporates outside the core of

Europe, the international commercial real es-

tate financing, the securitisations and diverse

smaller subportfolios that the SaarLB Group

would like to dispose of in the medium term)

and liquidity portfolios. They comprise the

Securities Account A, which is held primarily

according to strict liquidity criteria (securi-

ties portfolio with a focus on European com-

panies in the investment grade area) and the

LCR portfolio, which serves to expand the

qualified assets in accordance with Basel III.

While the reduction portfolios fell in 2012 by

23

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

roughly EUR 0.9 billion to EUR 2.8 billion in

accordance with the strategic orientation of

the Group, the corresponding volume in the

Securities Account A remained, at EUR 2.3 bil-

lion, on the level of the previous year due to

the required structure and asset parameters.

In consideration of Basel III, the building of a

corresponding LCR portfolio was begun at the

end of 2011. The portfolio of securities in com-

pliance with Basel III totalled roughly EUR 0.3

billion as of 31 December 2012.

Furthermore, this business segment is re-

sponsible for the liquidity and asset-liability

management of the Group, for which the

Bank’s derivative business is mainly used. The

derivative business is mainly used to hedge

interest rate risks. The nominal volume was

EUR 16.5 billion, roughly on the level from the

previous year (2011: EUR 16.5 billion). Broken

down by type of business, 80.6% of this is at-

tributable to interest rate swaps.

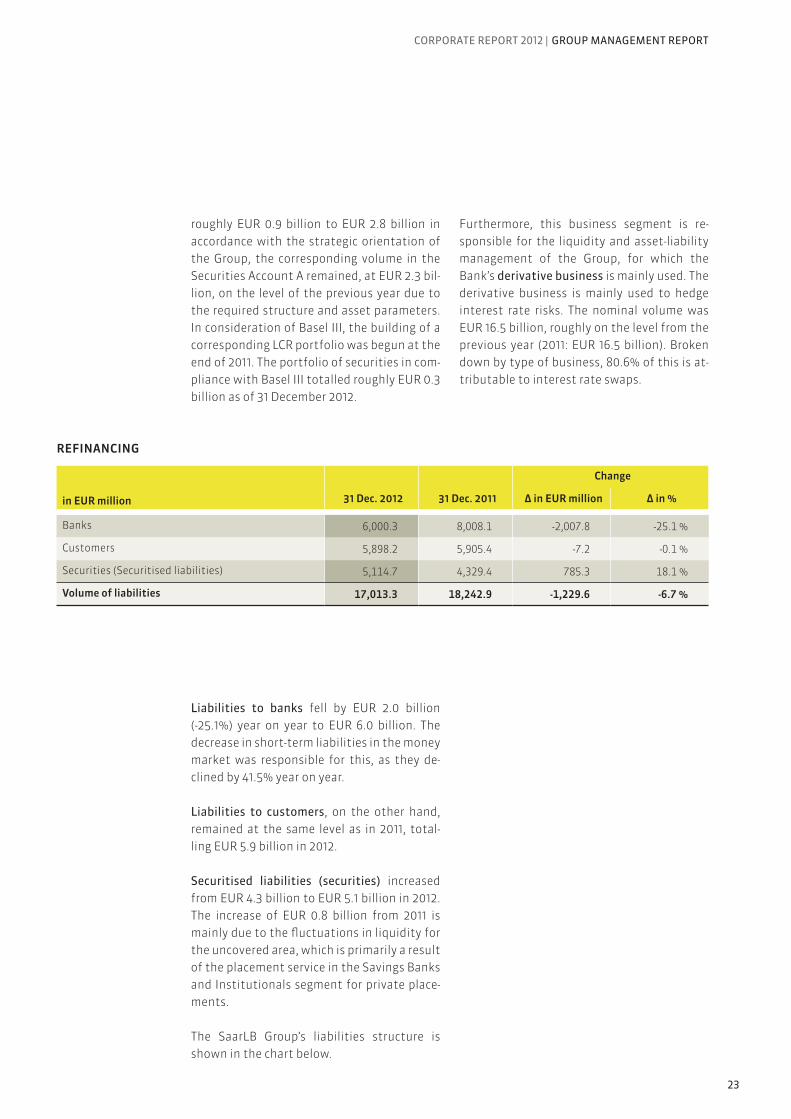

Liabilities to banks fell by EUR 2.0 billion

(-25.1%) year on year to EUR 6.0 billion. The

decrease in short-term liabilities in the money

market was responsible for this, as they de-

clined by 41.5% year on year.

Liabilities to customers, on the other hand,

remained at the same level as in 2011, total-

ling EUR 5.9 billion in 2012.

Securitised liabilities (securities) increased

from EUR 4.3 billion to EUR 5.1 billion in 2012.

The increase of EUR 0.8 billion from 2011 is

mainly due to the fluctuations in liquidity for

the uncovered area, which is primarily a result

of the placement service in the Savings Banks

and Institutionals segment for private place-

ments.

The SaarLB Group’s liabilities structure is

shown in the chart below.

REFINANCING

Change

in EUR million 31 Dec. 2012 31 Dec. 2011 Δ in EUR million Δ in %

Banks 6,000.3 8,008.1 -2,007.8 -25.1 %

Customers 5,898.2 5,905.4 -7.2 -0.1 %

Securities (Securitised liabilities) 5,114.7 4,329.4 785.3 18.1 %

Volume of liabilities 17,013.3 18,242.9 -1,229.6 -6.7 %

24

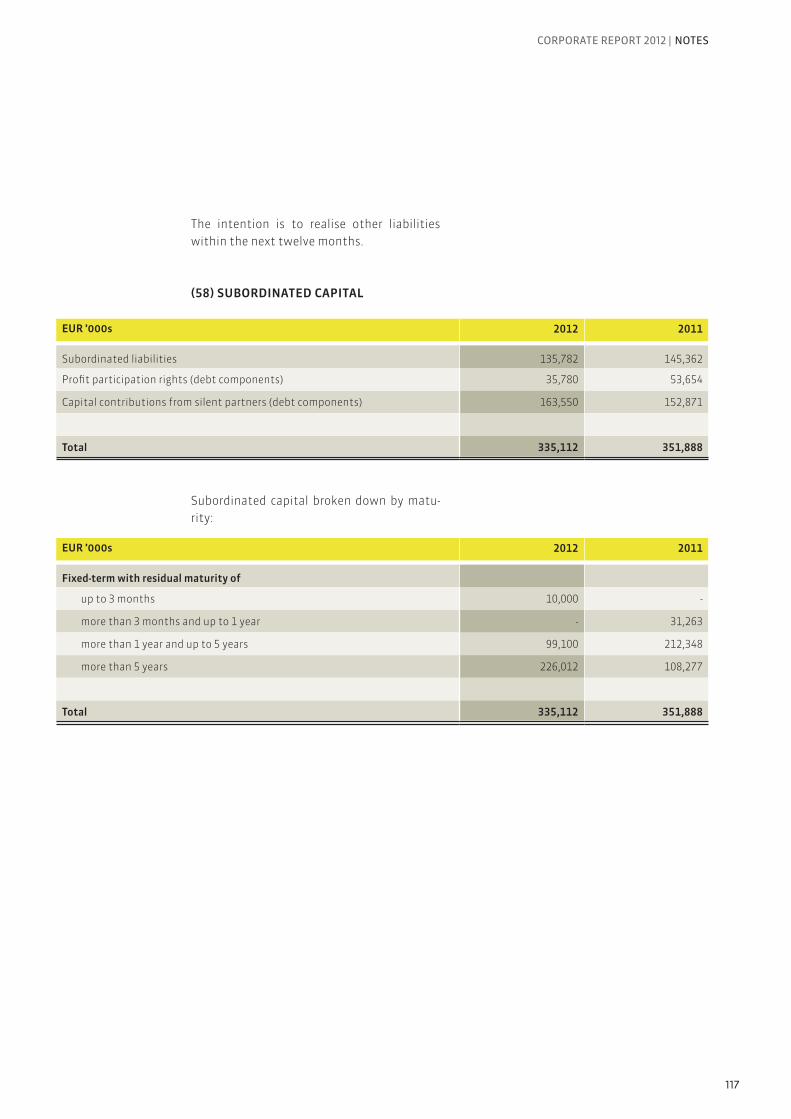

SUBORDINATED CAPITAL

The subordinated capital fell from EUR 351.9

million to EUR 335.1 million in the past finan-

cial year. A planned run-off of subordinated

liabilities and profit participation rights for a

total of EUR 27.5 million was not replaced. The

debt component of silent reserves increased

by EUR 10.7 million in 2012 due to the shorter

maturities as part of the split accounting in

2012.

REPORTED EQUITY

Reported equity rose by EUR 96.8 million,

from EUR 462.0 million to EUR 558.8 million.

The change is, on the one hand, due to an in-

crease in the revaluation reserve from EUR

-11.6 million in 2011 to EUR 43.6 million in 2012

and, on the other, due to a significant rise in

the retained profit of EUR 49.7 million, which

is EUR 38.4 million above the previous year.

REGULATORY CAPITAL

SaarLB’s equity in accordance with regulatory

requirements [Solvency Ordinance : SolvV] as

of the reporting deadline 31 December 2012

fell from EUR 865.2 million as of 31 December

2011 to EUR 845.4 million. The reason for this

is a decrease in the profit participation rights

capital in accordance with Section 10 (5) KWG

[German Banking Act] of EUR 30.0 million and

a decrease in the dated silent reserves of EUR

10.0 million. Both capital components may no

longer be assigned to capital on account of

the remaining maturities. On account of the

use of the exemption provisions pursuant to

Section 31 KWG [German Banking Act], SaarLB

has not prepared a regulatory group report.

The core capital – before the items that are

subject to a 50% deduction from core capi-

tal – fell by some EUR 10.1 million to EUR 812.1

million. The reason for this includes two silent

reserves with fixed terms that may no longer

be assigned to capital on account of the ma-

turity date.

The supplementary capital – before the items

that are subject to a 50% deduction from sup-

plementary capital – totalled EUR 139.4 mil-

lion (2011: EUR 173.0 million) on account of the

regulatory subordinated liabilities and profit

participation rights that ceased to be eligible.

The decrease in the eligibility of the profit par-

ticipation rights was material.

The value adjustment shortfalls, which

must be deducted fifty-fifty from core and

EUR billion

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

Banks Customers Securities

2012 2011 2010

25

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

supplementary capital, fell by EUR 22.1 million

to EUR 87.0 million. This amount results from

the difference between the actual value ad-

justments made in accordance with economic

standards and those that must be forecast

based on prudent regulatory requirements.

Likewise, the items, which must be deduct-

ed fifty-fifty from core and supplementary

capital, decreased slightly for investments to

EUR 19.1 million (2011: EUR 20.9 million).

The risk positions of the SaarLB Group fell –

similar to the development of the balance

sheet total – by EUR 437 million to EUR 7.2 bil-

lion as of 31 December 2012 (2011: EUR 7.6 bil-

lion). A reduction in the risk positions was

primarily driven by a reduction in the non-

strategic business.

As of the reporting deadline 31 December

2012, the core capital ratio was 10.6% and thus

significantly above the level from 2011 (9.9%),

while the solvency coefficient improved from

11.4% in 2011 to 11.8% in 2012.

With the approval of the annual financial

statements (German Commercial Code) of

the Group’s parent company SaarLB, the core

capital of SaarLB will be strengthened by EUR

30.3 million through the increase in reserves

pursuant to Section 340 g of the German Com-

mercial Code.

The Bank has been engaged in intense ne-

gotiations with the shareholders since the

beginning of 2013 in order to strengthen the

silent reserves of Saarland savings banks to

meet the stricter capital requirements in ac-

cordance with Basel III. The negotiations have

been moving ahead positively and the objec-

tive is to have the Saar Association of Savings

Banks increase its share of the voting share-

holder capital of SaarLB to 25.1% by means

of converting the previous silent reserves of

Saarland savings banks, effective 30 Septem-

ber 2013. Furthermore, the plan is to grant,

to the remaining silent reserves of Saarland

savings banks in SaarLB, the right to request

conversion to solid core capital as of 1 January

2016, if need be.

Irrespective of this, the Bank continued to im-

plement the regulatory changes under Basel

III/CRD IV and CRR and determine the imple-

mentation measures required in 2013 by con-

ducting a commensurate concept study.

SUPPLEMENTARY REPORT

There have been no events of special signifi-

cance since the end of the year under review.

RISK REPORT

RISK MANAGEMENT AND MONITORING

PRINCIPLES

The SaarLB Group manages and monitors its

risks on the basis of uniform principles. All in-

formation given below relates to the SaarLB

Group unless expressly stated otherwise.

Management of subsidiaries and companies

valued at equity takes place as part of invest-

ment controlling.

The key risk management and monitoring

principles are laid down in SaarLB’s risk strat-

egy. In accordance with the business strategy,

the Board of Management sets the policy for

dealing with counterparty risk (counterparty

default risks and credit spread risks), market

price risk, liquidity risk, operational risk, risks

from unexpected behaviour of savers, real es-

tate risk, strategic risks / business risks and

reputation risks, which are the key risk types

for SaarLB. It is responsible for and monitors

the implementation of these guidelines.

Generating a reasonable and sustainable re-

turn after allowing for risk is the ultimate aim

of all SaarLB’s business activities. Risks may

only be entered into to the extent permitted

by SaarLB’s risk-bearing capacity.

26

Suitable limits for the key risk types have

therefore been set and appropriate proce-

dures for identifying, measuring and monitor-

ing them defined as part of the risk strategy.

The tasks, competencies and responsibilities

of the staff involved are based on clearly de-

fined organisational structures and process-

es. Organisational structures take account of

the regulatory requirements under the Mini-

mum Requirements for Risk Management

[MaRisk] and the Solvency Ordinance [SolvV]

on the division of functions between Sales

and Trading (business segments) on the one

hand and Risk Office, Settlement and Risk

Controlling on the other.

While business areas are based around Saar-

LB’s business model, core competencies have

been combined in the organisation of the Risk

Office and Settlement.

Global Risk Management is in charge of risk

controlling of all risk types at the portfolio

level. Risk Office is responsible for managing

and monitoring counterparty risk at the indi-

vidual exposure and sub-portfolio level. This

involves integrated risk reporting of all risk

types as part of a joint MaRisk risk report.

Internal Audit reports directly to the Board of

Management and is answerable to its Chair-

man. It is an independent internal division that

audits and assesses, on the basis of a risk-ori-

ented audit approach, all activities and process-

es within SaarLB, including the internal control

system and risk management and controlling.

This also applies for outsourced activities and

processes. Internal Audit acts in accordance

with legal and regulatory requirements such as

KWG [German Banking Act], MaRisk [Minimum

Requirements for Risk Management].

With the publication of the 4th MaRisk

amendment on 14 December 2012, SaarLB im-

mediately began the implementation of the

new requirements and completed them in ac-

cordance with the requirements at the end of

2013.

CAPITAL MANAGEMENT

The regulatory requirements set out in the

Solvency Ordinance [SolvV] are key for SaarLB

when assessing and managing capital ad-

equacy as well as maintaining economic risk-

bearing capacity.

REGULATORY CAPITAL

SaarLB has applied the relevant rules on cal-

culating capital requirements under the Sol-

vency Ordinance since obtaining approval

from the German Federal Financial Supervi-

sory Authority (BaFin) to use the Internal Rat-

ings Based Approach (IRBA) on 1 January 2007.

Regulatory capital – i.e. equity – comprises

core capital (essentially nominal capital, si-

lent partner contributions and reserves, in-

cluding the reserves under Section 340 g of

the Commercial Code) plus supplementary

capital (essentially profit participation rights

and long-term subordinated liabilities) after

deductible items.

The overall ratio – the ratio of capital to risk

positions calculated under Solvency Ordi-

nance rules – must not fall below 8.0% from a

regulatory point of view. SaarLB has specified

a stricter target ratio of 10.0% for its Group

figure and a core capital target ratio of 8.0%

in its internal management. The latter is the

ratio of core capital (after deductible items)

to risk exposures.

Target values are constantly maintained by

means of medium-term planning over a five-

year timeframe. The Corporate Development

segment is responsible for the strategic plan-

ning process. On the basis of the economic

conditions determined in this process, each

business area performs its own risk exposure

planning for this time period. Their figures

are then aggregated at the Group level by

Controlling – the department in charge of the

quantitative aspects of medium-term plan-

ning – and compared with the equity available

in the planning period. Finally, the measures

27

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

needed to procure capital or scale back pro-

posed business area budgeting are defined to

ensure the targets are met.

An overview of the key Solvency Ordinance

data as of the balance sheet date of 31

December 2012 and the corresponding fig-

ures from the previous year are given below.

SaarLB stopped preparing regulatory group

reports in the middle of 2011. To this extent,

the figures only include the single institute.

The key figures for SaarLB increased noticea-

bly year on year due to the drop in risk assets.

SaarLB complied with the minimum regula-

tory ratio during the entire reporting period

at all times as well as its stricter target ratios.

Good overall capital adequacy ratios were

also reflected in the results of the required

regulatory stress tests: Based on the assump-

tion of economic weakness, the equity ratio

at the Group level was 10.0% and the core

capital ratio was 9.0% as of 31 December 2012.

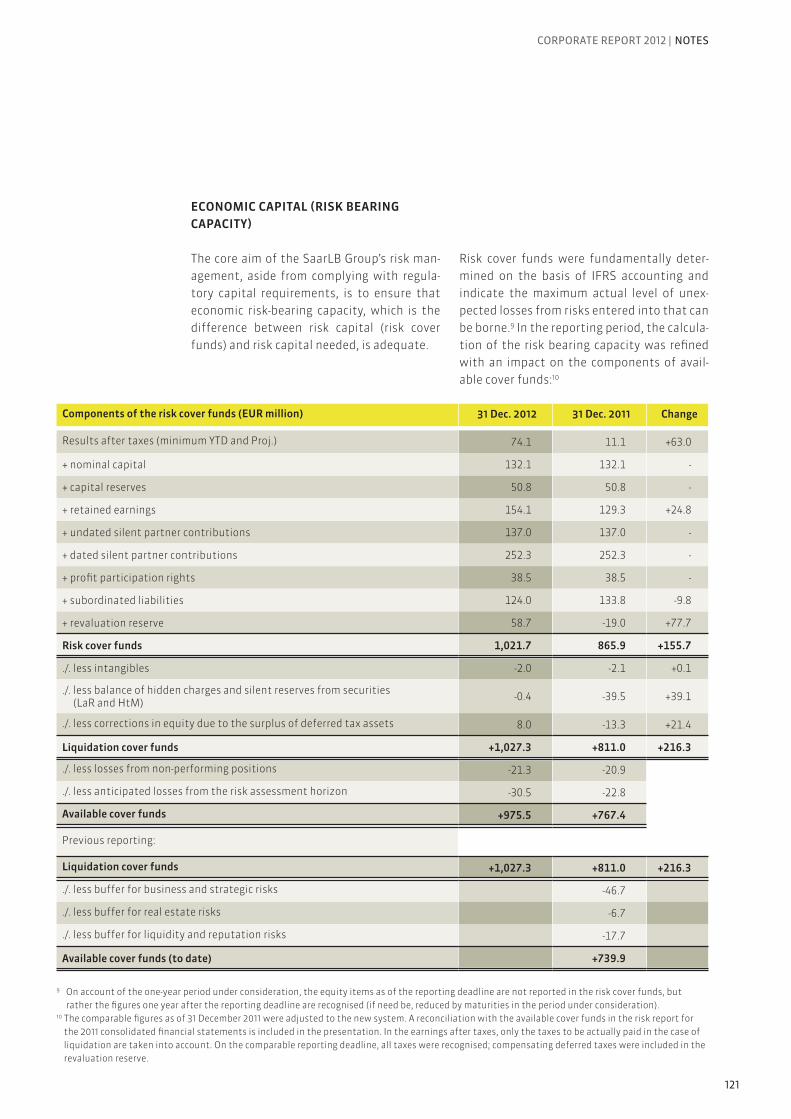

ECONOMIC CAPITAL (RISK BEARING

CAPACITY)

The core aim of the SaarLB Group’s risk man-

agement, aside from complying with regula-

tory capital requirements, is to ensure that

the economic risk-bearing capacity, which is

the difference between risk capital (risk cover

funds) and risk capital needed, is adequate.

Risk cover funds are fundamentally deter-

mined on the basis of IFRS accounting and

indicate the maximum actual level of unex-

pected losses from risks entered into that can

be borne.1 In the reporting period, the calcula-

tion of the risk bearing capacity was refined

with an impact on the components of avail-

able cover funds:2

Key Solvency Ordinance (SolvV) data 31 Dec. 2012 31 Dec. 2011

Risk exposure (EUR million) 7,181 7,618

Equity (EUR million) 845 865

of which: core capital (EUR million) 759 757

Equity ratio (Group level in %) 11.8 % 11.4 %

Core capital ratio (in %) 10.6 % 9.9 %

1 On account of the one-year period under consideration, the equity items as of the reporting deadline are not reported in the risk cover funds, but rather

the figures (if need be, reduced by maturities in the period under consideration) one year after the reporting deadline are recognised.2 The comparable figures as of 31 December 2011 were adjusted to the new system. A reconciliation with the available cover funds in the risk report for

the 2011 consolidated financial statements is included in the presentation. In the earnings after taxes, only the taxes to be actually paid in the case of

liquidation are taken into account. On the comparable reporting deadline, all taxes were recognised; compensating deferred taxes were included in the

revaluation reserve.

28

Components of the risk cover funds (EUR million) 31 Dec. 2012 31 Dec. 2011 Change

Results after taxes (minimum YTD and Proj.) 74.1 11.1 +63.0

+ nominal capital 132.1 132.1 -

+ capital reserves 50.8 50.8 -

+ retained earnings 154.1 129.3 +24.8

+ undated silent partner contributions 137.0 137.0 -

+ dated silent partner contributions 252.3 252.3 -

+ profit participation rights 38.5 38.5 -

+ subordinated liabilities 124.0 133.8 -9.8

+ revaluation reserve 58.7 -19.0 +77.7

Risk cover funds 1,021.7 865.9 +155.7

./. less intangibles -2.0 -2.1 +0.1

./. less balance of hidden charges and silent reserves from securities (LaR and HtM)

-0.4 -39.5 +39.1

./. less corrections in equity due to the surplus of deferred tax assets 8.0 -13.3 +21.4

Liquidation cover funds +1,027.3 +811.0 +216.3

./. less losses from non-performing positions -21.3 -20.9

./. less anticipated losses from the risk assessment horizon -30.5 -22.8

Available cover funds +975.5 +767.4

Previous reporting:

Liquidation cover funds +1,027.3 +811.0 +216.3

./. less buffer for business and strategic risks -46.7

./. less buffer for real estate risks -6.7

./. less buffer for liquidity and reputation risks -17.7

Available cover funds (to date) +739.9

29

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

The risk cover funds rose significantly in com-

parison to the previous deadline primarily due

to the higher earnings, an addition to profit

reserves and due to positive effects from the

revaluation reserve, while slight declines in

subordinated liabilities were overcompensat-

ed as a result.3 The available risk cover funds

result from the risk cover funds due to the re-

ductive consideration of other effects:

-

ducted from the cover funds, which might not

retain their value in the case of a liquidation.

cover funds are also deducted over a one-year

assessment horizon, which will not be explic-

itly considered in the future modelling of the

economic risk bearing capacity calculation.

As part of economic risk capital management,

SaarLB monitors its risk profile and ensures

its risk-bearing capacity is always adequate

by comparing each month the risk capital al-

located to the available cover funds and risk

capital needed. Risk capital needed is deter-

mined by analysing all significant risk types

in a consistent manner.4 The risks from across

the Group are collated into an overall assess-

ment of the risk existing. In ICAAP, the value at

risk (VaR) method based on a confidence level

of 99.95% is used to determine risk capital

needed. The limits are set at the level of the

individual risk types and collectively through

the (total) allocated risk capital. Assumptions

and results of the risk quantification are to be

validated at least once a year.

3 In 2013 – i.e. over a one-year assessment horizon – some EUR 10 million of subordinated liabilities will fall due.4 Besides the previously considered risk types, the new system also includes the following risks: unexpected behaviour by savers, real estate risk, strate-

gic risk / business risks and reputation risks.

30

The ICAAP risk-bearing capacity as of 31 De-

cember 2012 is illustrated in the following

overview:5

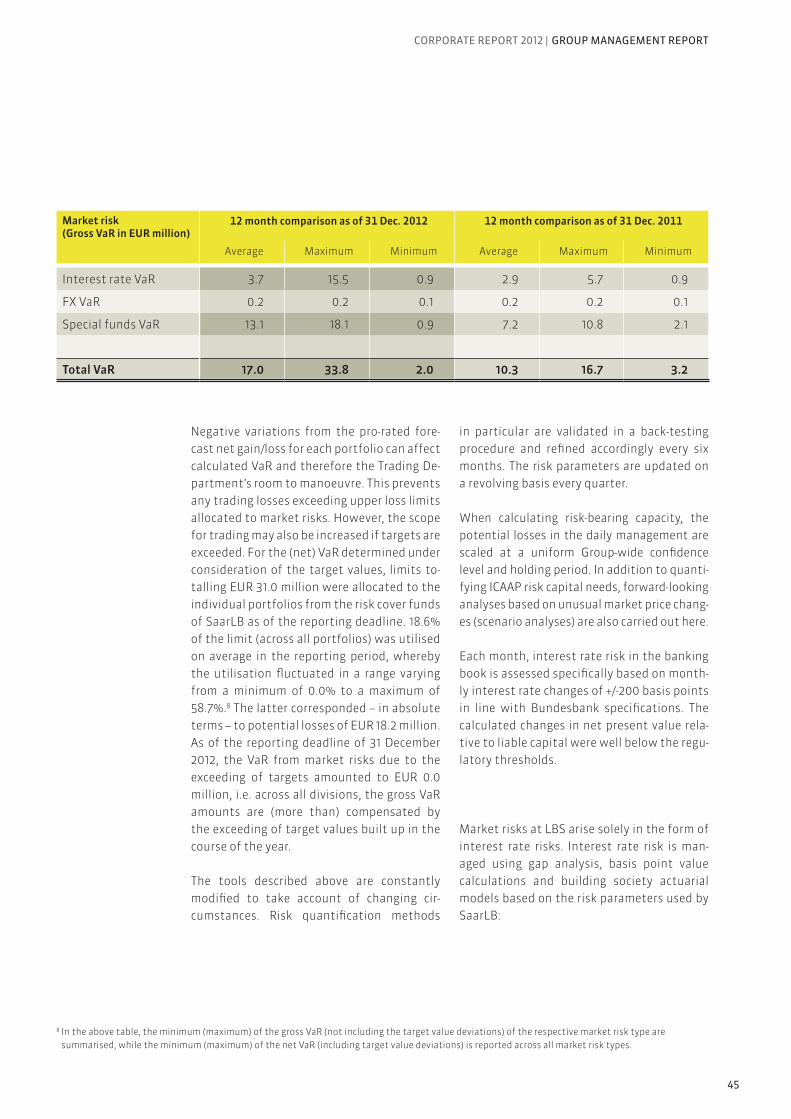

Economic RBC (ICAAP)(EUR million)

31 Dec. 2012 31 Dec. 2011

Capitalneeded

Limit Range Capitalneeded

Limit Range

Counterparty risk 331.1 430.0 77.0 % 338.5 430.0 78.7 %

of which default risk (141.2) (180.0) 78.4 % (136.2) (180.0) 75.7 %

of which credit spread risk (189.9) (250.0) 75.9 % (202.2) (250.0) 80.9 %

Market risk 32.2 90.0 35.8 % 12.0 90.0 13.3 %

Operational risk 2.6 5.0 51.1 % 2.1 5.0 41.8 %

Reputation risk 0.0 2.0 0.0 % 0.0 2.0 0.0 %

Unexp. behaviour by savers 0.6 3.0 19.7 % 1.0 3.0 32.5 %

Real estate risk 13.3 15.0 88.5 % 13.3 15.0 88.5 %

Strategic risk / business risk 72.7 85.0 85.5 % 68.1 85.0 80.1 %

Total 452.4 630.0 71.8 % 434.8 630.0 69.0 %

Available cover funds 975.5 767.4

Free econ. cover funds 523.1 332.5

5 The refinement of the risk bearing capacity calculation was retroactively applied to the comparable reporting deadline of 31 December 2011. In comparison

to the system outlined in the report for the previous year, credit spread risks (EUR +169.9 million) and market risks (EUR +4.6 million) are quantified higher

in the comparable figures as of 31 December 2011 as a result. In the credit spread risks, significantly higher divergence in spreads is anticipated on the basis

of the experiences in the financial crisis; a holding period of 10 days is no longer generally assumed for market price risks; instead, the losses expected

within a year are to be quantified. On the other hand, no longer regulatory, but expected capital needed due to economic performance is counted (EUR

-20.7 million). The utilisation of the limits allocated at the reporting deadline is also illustrated as of 31 December 2011.

The SaarLB Group’s risk bearing capacity was

ensured at all times without qualification

throughout the reporting period (both in to-

tal and on the level of individual types of risk).

Besides the ICAAP risk capital needed, the risk

capital needed in multiple scenarios, was cal-

culated among others in the case of serious

economic weakness across all risk types under

consistent assumptions. With regard to coun-

terparty risks, a sector-specific deterioration

of the credit portfolio and a further increase

in credit spreads are assumed, and for all oth-

er types of risk, more stringent assumptions

also apply.

31

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

While the capital needed fell slightly overall,

the free economic cover funds rose year on

year and significantly exceeded the capital

needed as of the reporting deadline.6

COUNTERPARTY RISK (CREDIT RISK)

Under counterparty risk (credit risk), SaarLB

combines counterparty default risk and credit

spread risks. SaarLB defines counterparty de-

fault risk as the risk that the credit quality of

a business partner will deteriorate to such an

extent that it is unable to meet its payment

or contractual obligations towards the Bank

either in full and/or on time. Counterparty

default risk traditionally covers credit risk

but also includes issuer risk, borrower risk,

country risk and investment risk. Other coun-

terparty risks (credit spread risks) result from

credit-related changes in prices for the securi-

ties portfolio (including credit derivatives and

securitisation).

The risk strategy sets out the framework for

taking on counterparty default risks. A limit

on them, calculated from the risk-bearing

capacity, is then set in the annual strategy

process. To manage and monitor concentra-

tion risks and for operationalisation purpos-

es, limits are also imposed according to the

credit quality of borrowers, transactions, geo-

graphical markets and sectors.

The entire credit business chain, including

management and monitoring systems, is de-

scribed in detail in the SaarLB Lending Man-

ual. The master processes defined here apply

Bank-wide and are implemented uniformly in

all Risk Office areas. The Lending Manual is

constantly updated to take account of chang-

ing internal and external requirements.

Counterparty default risk is initially assessed

at individual borrower and (regulatory) bor-

rower unit level using the rating procedures

of RSU Rating Service Unit GmbH & Co. KG,

Munich, for banks, corporate customers (in-

cluding municipally-owned companies), inter-

national public authorities, leasing entities

(leasing companies and real estate leasing),

insurers, international commercial real es-

tate, project financing, country and transfer

6 In the presentation of the stress scenarios as of 31 December 2011 calculated according to the new system for comparative purposes, the direct eco-

nomic impact of the scenario would have been manageable, but the simultaneous occurrence of the 2000 year ICAAP loss would no longer have been

covered. From a regulatory point of view, both the scenario losses and an additional SolvV stress would have been covered as of 31 December 2011.

Serious economic weakness(EUR million)

31 Dec. 2012 31 Dec. 2011

Capital needed Capital needed

Counterparty risk 306.8 332.0

of which default risk (155.8) (166.0)

of which credit spread risk (151.0) (166.0)

Market risk 12.2 9.6

Operational risk 1.3 1.0

Reputation risk 0.0 0.0

Unexp. behaviour by savers 0.5 0.8

Real estate risk 10.2 10.2

Strategic risk / business risk 38.3 36.0

Total capital needed 369.3 389.7

Free econ. cover funds 523.1 332.5

32

risk, and the DSGV liability association. These

procedures are backed up by the savings

banks standard rating and the savings bank

real estate rating modules from Sparkassen

Rating und Risikosysteme GmbH, Berlin. All

these rating procedures have been approved

by the German Federal Financial Supervisory

Authority (BaFin) for use within the Internal

Ratings Based Approach (IRBA) to calculate

capital requirements in accordance with the

Solvency Ordinance. They are validated an-

nually by the Bank in cooperation with these

partners on the basis of the current credit

portfolio.

Significant input parameters for the quan-

titative part of the credit rating analysis

performed in the rating process come from a

balance sheet analysis system that supports

the major accounting standards (among oth-

ers HGB, IFRS, US-GAAP) and facilitates peer

groups and industry comparisons. In addition

to borrowers’ credit ratings, the risk assess-

ment also takes into account, where required,

property and project risks as well as country

and transfer risks. Finally, borrowers are allo-

cated to a specific rating category on a 25-tier

rating scale based on the probability of de-

fault. Rating categories are therefore compa-

rable regardless of the rating procedure used.

In accordance with SaarLB’s requirements,

standard forms of bank collateral – particular-

ly mortgage liens, pledges, assignments, chat-

tel mortgages, and debt undertakings – are

accepted by the Bank to reduce risks. Collater-

al is processed and valued in accordance with

the Collateral Manual. The procedure used to

calculate and determine collateral value must

be clearly documented. In the case of deriva-

tives trading, master agreements are conclud-

ed for the purpose of close-out netting. Collat-

eral agreements have been made with certain

business partners limiting the risk of default

in each case to an agreed maximum.

Exposures that may be at risk are identified

using an appropriately constructed early

warning system – for example by means of

annually revised ratings – and transferred for

intensive support. As with problem loan han-

dling, this falls within the remit of the Risk

Office.

Counterparty default risks from trading are

monitored daily by Settlement to take ac-

count of MaRisk. In particular, all derivatives

business is monitored (counterparty risk). All

trading business conducted with each cus-

tomer is counted towards the borrower lim-

its – including settlement limit – set for that

specific customer in a system-supported and

uniform Bank-wide process and in accordance

with the requirements on market valuation

methods under the Solvency Ordinance.

The internal rating is key for managing and

monitoring counterparty default risks at the

overall Bank level; collateral is currently taken

into account only at individual exposure level

as part of reaching decisions. In particular

for the calculation of the capital adequacy

under the Solvency Ordinance [SolvV], col-

lateral (through the credit risk mitigation

techniques) is largely not taken into account.

Gross exposure limits for borrower units

based on rating categories, markets and cus-

tomer types derived from the business strat-

egy are clearly defined in the risk strategy.

In addition, to strengthen individual sector

portfolios, only selected new business may

be conducted in the risk sectors identified by

the Bank. A strict ancillary condition requires

risk-oriented pricing supported by a suitable

calculation tool.

The relevant Sales and Risk Office areas moni-

tor each individual credit decision to ensure

compliance with the risk strategy.

The quarterly MaRisk risk report for the Board

of Management, Board of Administration and

the SaarLB Risk Committee contains both an

analysis of the credit portfolio – particularly

in relation to rating categories, sectors and

countries – as well as a summary target/ac-

tual comparison with the risk strategy.

33

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

SaarLB uses the CreditRisk+ credit portfolio

model – particularly in calculating risk-bear-

ing capacity – to analyse risks at the portfo-

lio level. The credit portfolio model takes ac-

count of the SaarLB Group’s entire receivables

portfolio exposed to counterparty default

risk, weighted by the specific probability of

default for each borrower derived from the

rating categories. A key variable is credit val-

ue at risk, which breaks down into expected

loss – which the risk-oriented pricing takes ac-

count of – and unexpected loss. Both the ex-

pected and unexpected loss must be covered

by risk capital in the risk-bearing capacity cal-

culation.

PORTFOLIO ANALYSIS (ECONOMIC)

The presentation in the following sections ti-

tled “Portfolio analysis (economic)” and “Sub-

portfolios with elevated risk profiles” is based

on the internal risk management (manage-

ment approach) according to which there was

a maximum credit risk of EUR 20,139 million

on the reporting deadline (as of 31 December

2011: EUR 21,896 million). Minor deviations

from the balance sheet approach (see section

“Portfolio analysis (balance sheet)”) are due,

among others, to consideration given to add-

ons in the determination of the exposure of

derivative financial instruments according to

the market valuation method, counterparty

risks from securities repurchase transactions

and the recognition of credit derivatives at

nominal values.

34

Around 81% of exposure is in the investment

grade bracket (rating categories 1 to 5 ac-

cording to the DSGV scale). In comparison to

2011, this share has increased by around three

percentage points due in particular to the de-

crease in exposure in rating category 1.

SaarLB uses a value-added and risk-orientated

grouping code for the purposes of economic

management and strategic alignment of the

sector exposure, breaking down exposure

into 32 sector groups. Sector group exposure

(excluding the low-risk Banks sector group,

which is shown separately in the following

and comprises just under 42% of total expo-

sure) can be broken down as follows:

Exposure by rating category (EUR million)

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

DSGV scale 1 2 - 5 6 - 12 13 - 15 16 - 18(Landesbanks

scale:0-7 8-11 12-18 19-21 22-24)

31 Dec. 2011 31 Dec. 2012

Customer exposure by sector (EUR million)

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Real Estate SovereignsRenewable

EnergyUtilities Automotive

Construc-tion

SteelWholesale +retail trade

Food +Beverages

ABSRetail

customersOther

sectors

31 Dec. 2011 31 Dec. 2012

35

CORPORATE REPORT 2012 | GROUP MANAGEMENT REPORT

SaarLB’s sector portfolio – particularly the

corporates portfolio – continues to be well-

diversified. Real estate, the largest individual

sector (besides banks), comprises roughly 17%

of the total exposure (including banks) after

amounting to 15% in 2011.

In the year under review, the exposure in the

target industry of renewable energy signifi-

cantly increased again by EUR 448 million,

while primarily exposure to the bank sector

fell (by EUR 2,097 million).

SaarLB uses the official Bundesbank codes to

give a breakdown of its exposure in a uniform

manner for each individual country. Regions

are then grouped on the basis of global and

regional economic ties. The focus of SaarLB’s

country portfolio is in its defined target mar-

kets of Germany and France, which amount

to a share of around 85% (as of 31 December

2011: 84%). Another 12% (as of 31 December

2011: 13%) concerns exposure in the rest of Eu-

rope, whereby the exposure in Ireland and in

the southern European countries of Greece,

Italy, Spain and Portugal amounts to a total