Embed Size (px)

Citation preview

Corporate & Institutional Banking

Dr Bob EdgarManaging Director

Australia and New Zealand Banking Group Limited 20 July 2001

Page 2

The relationship gateway to our corporate customer base

• Financial performance

• Strong customer focus

• Conservative risk management

• Growth focused on fee-based investment banking style products

• Goals for Corporate & Institutional Banking

Page 3

Corporate & Institutional Banking

Institutional Banking

• Middle market companies with $10 - $100m turnover

• 5500 customers & targets• Geographic relationship

management model with 21 regions across Australia & New Zealand

• Regional Credit Executives located with relationship

• Management of overall customer relationship & profitability

• Balance sheet management

• Navigation, co-ordination & solutions development between product areas for our customers

Corporate Banking

Key Responsibilities

• Top end corporates in with $100m plus turnover

• Has ~1000 customers & targets, in Australia and New Zealand

• 9 Specialised Industry Segments

• Supported by Credit Products Group

Page 4

Institutional Banking continues to perform strongly

Mar-01

422

435430

350

375

400

425

450

475

500

Mar-00 Sep-00

FTE

6770

88

40

50

60

70

80

90

100

Profit After Tax

Mar-00 Sep-00 Mar-01

31% Growth176

209

171

100

120

140

160

180

200

220

Mar-00 Sep-00 Mar-01

Operating Income

22% Growth

$m $m

Mar-01

21.123.922.2

0

10

20

30

40

50

Mar-00 Sep-00

Cost Income%

Page 5

Corporate Banking performance has been more subdued

34.638.0

35.0

20

30

40

50

60

70

Mar-00 Sep-00 Mar-01

Cost Income%

Mar-01

756769762

650670690710730750770790810830850

Mar-00 Sep-00 Mar-01

FTE

183187 188

160

165

170

175

180

185

190

195

200

Mar-00 Sep-00

Operating Income

3% Growth

$m

6160

65

50

55

60

65

70

Profit After Tax

Mar-00 Sep-00 Mar-01

7% Growth

$m

Page 6

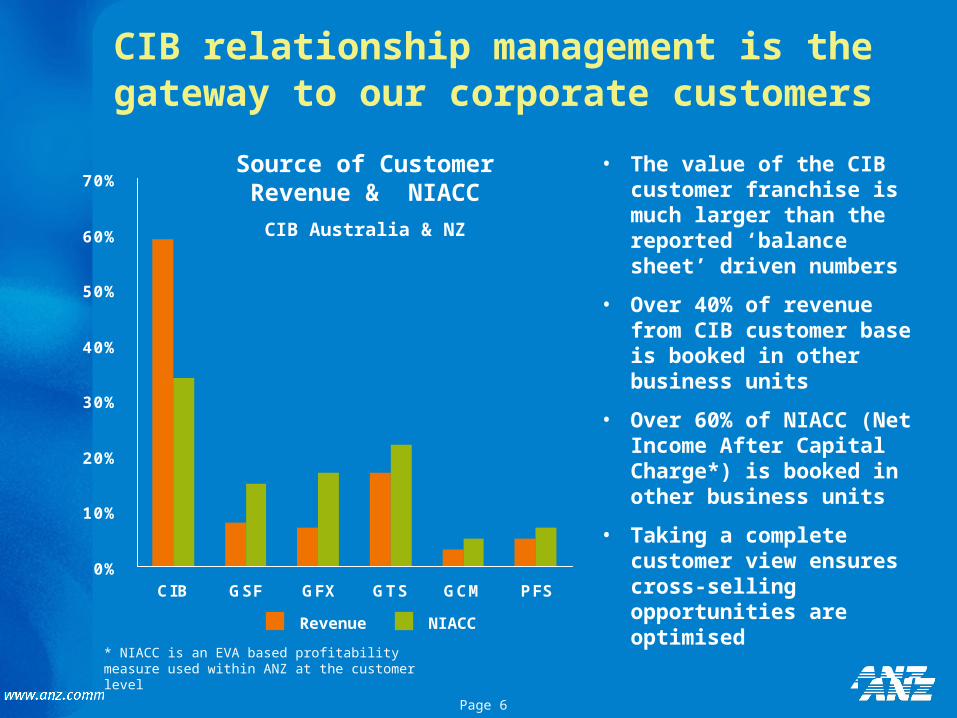

CIB relationship management is the gateway to our corporate customers

0%

10%

20%

30%

40%

50%

60%

70%

CIB GSF GFX GTS GCM PFS

• The value of the CIB customer franchise is much larger than the reported ‘balance sheet’ driven numbers

• Over 40% of revenue from CIB customer base is booked in other business units

• Over 60% of NIACC (Net Income After Capital Charge*) is booked in other business units

• Taking a complete customer view ensures cross-selling opportunities are optimised

* NIACC is an EVA based profitability measure used within ANZ at the customer level

Revenue NIACC

Source of Customer Revenue & NIACC

CIB Australia & NZ

Page 7

CIB drives for continuous change to be a high performing customer business

•Distribution StrategyRole clarityProcess improvement

• Customer Profitability tool• Product specialists in regions

• e-Transformation • Outsourcing / centralisation - CTSC - Securities

• Industry specialisation in IB

NIACC $130mCTI 36%ELP 53bp

NIACC $460mCTI 28%ELP 37bp

1998 1999 2000 2001

• Corporate Banking portal CARBe Impact

Page 8

We are a leader in customer relationship management

0% 20% 40% 60%

#2

=1

=1

=1

=1

Overall Satisfaction with Bank(Corporate Bank)

7.67.5

7.67.4

6.97.0

7.1

6.46.0

6.5

7.0

7.5

8.0

1997 1998 1999 2000

ANZ NAB CBA WBC

Source: Roberts Research Group

8.1 8.1 8.1 8.38.0

7.47.5

6.8

7.4 7.4

6

6.5

7

7.5

8

8.5

1995 1996 1997 1998 1999

Satisfaction with Relationship Manager(Corporate Bank)

2000

8.4

7.0

0% 20% 40% 60% 80%

#2

#1

#1 Total customers

Significant Bank R’ships

Lead bank customers

Market Position(Institutional Bank)

Relationship Management(Institutional Bank)

Overall satisfaction

Quality of account management

Level of ideas & initiatives

Understanding and knowledge of business

Prompt follow-up

Source: Greenwich Associates

Page 9

Risk profile and management stance remain conservative

• Risk grades 7D-10 [ie B to D external credit ratings agency equivalents] are less than 4% of total book

• This reflects a substantial improvement in book quality

• Risk grades 5-7C [ie BB+ to well secured B] improved from 54.3% to 43% of book.

Risk Profile

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10

CCR

Ass

ets

(%)

Page 10

For key asset quality indicators, CIB has a solid record - no systemic credit issues

Risks actively managed

• Enhanced credit management processes reducing expected loss rates in the business, (eg ‘one-up’ reviews)

• Whilst net specific provisions have increased during the first half year, the loss rate is still well below ELP rate

• At this stage of the credit cycle, we expect specific provisions to increase towards ELP

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

Mar-98 Mar-99 Mar-00 Mar-01

ELP Rate

SP Rate

% o

f Len

din

g A

ssets

ELP is a key measure of

portfolio quality

Page 11

Growth is increasingly being driven by investment banking style products…

Traditional Income – lending, transaction, deposit & trade products

Other - principally products from the Personal portfolio

34

100

1671

32

80

90

100

110

120

130

140

150

160

170

180

11

4

100

117

2

80

85

90

95

100

105

110

115

120

Institutional Corporate

Traditional Income

Inv. Bank products

Other

Mar-00 Mar-01

Traditional Income

Wall St to Main St

Other

Mar-00 Mar-01

Index Index

Page 12

What do our customers want? - their top 3 needs are

CB to focus on:

• Wall St to Main St

• Cross sell products from the Personal businesses into our customer base:

• Corporate portal to lower cost to serve

Corporate Banking

• ‘Balance Sheet’ on reasonable terms

• Partner & trusted advisor• Smart products / customised

solutions

Institutional Banking

• Industry Knowledge• Creative ideas and solutions• High quality service proposition

IB’s focus will be:• Leverage the success of

Industry Specialisation to our institutional customers

• Client servicing• Corporate Portal – helps

customers streamline operations

Page 13

…supported by world class customer value management systems like MARS

Management Analysis Reporting System

Relationship expense

Transaction details

Product & pricing details

Risk profile

Key Inputs Key Outputs

Customer profitability

“What if” scenarios

Product profitability

Risk based pricing

Share of overheads

Page 14

Summary

• The pre-eminent domestic corporate banking franchise

• Our cross sell focus is embedded in the sales network, driven to growing non-balance sheet product solutions for customers

• Optimising overall customer value is driving new revenue opportunities

• The business will continue to build industry specialisation

Goals• Double digit earnings

growth

• Continue growth and

diversification of

customer revenue

mix

• Maintain customer

satisfaction ratings

• Performing loans

remain at 99% of

total book

Page 15

Copy of presentation available on

www.anz.com