Embed Size (px)

Citation preview

© ICSA, 2010 Page 1 of 18

Corporate Financial Management June 2010

Suggested answers and examiner’s comments Important notice When reading these answers, please note that they are not intended to be viewed as a definitive ‘model’ answer, as in many instances there are several possible answers/approaches to a question. These answers indicate a range of appropriate content that could have been provided in answer to the questions. They may be a different length or format to the answers expected from candidates in the examination. Examiner’s general comments The pass rate for this examination was 52%, broadly in line with recent exams. There was a wide variation in the marks earned for different questions in Section A. This seems to have been due, in part, to candidates concentrating their studies and revision on the most frequently examined topics, rather than covering the whole syllabus. Questions 1(b) – on the adjusted present value method of investment appraisal, 1(d) – on the calculation and use of the beta value of a share, and 1(f) – on operational gearing, were often not well answered. Questions 1(d), 1(f) and 1(h) – on the proceeds of a share issue, also illustrated another common weakness: calculation questions were often poorly done, particularly when they were on less frequently examined calculations or when the question did not specify how the calculations should be done. It is understandable that candidates who are preparing for examinations under all kinds of pressures may find it difficult to cover the whole syllabus or to do a lot of practice in a wide range of different calculations. A fair number of marks are given for questions that can be answered using standard theory and by doing calculations that have appeared before in a similar form. But the whole syllabus is liable to be examined, and candidates cannot rely on all calculations being in a form with which they are familiar. There is no short cut to adequate preparation. Perhaps partly because a number of candidates could not make serious attempts at all parts of Question 1, there was little evidence of candidates spending too much time on Section A and not leaving enough time for the Section B questions. Most candidates seem to have had enough time to write fairly complete answers to all the questions that they attempted. Or, at least, when there were gaps in answers, these tended to be found at any point in the script, rather than in the last question answered. However, there were a number of scripts where it appeared that candidates did not know the answer to a question and wasted time by writing irrelevant points. All of the Section B questions involved some calculations. Questions 2 and 5 were much less popular than Questions 3, 4 and 6. This could have been because, in Questions 2 and 5, candidates needed

© ICSA, 2010 Page 2 of 18

to decide for themselves how to go about the calculations. It may have been easier to see from the wording of Questions 3, 4 and 6 how the Examiner expected the calculations to be tackled. More detailed comments on individual questions are given below:

Section A 1. (a) State the primary corporate purpose that underlies corporate financial

management in a public limited company, and give three reasons why the managers of companies tend to act in furtherance of this purpose. (4 marks)

Suggested answer The primary corporate purpose of most public companies is to maximise the return to shareholders. This may not be the only purpose, but it is usually the reason why ordinary shareholders, the owners of the company, buy and hold the shares. Reasons why companies act in furtherance of this purpose include:

The directors owe a legal duty to the shareholders to safeguard their interests as owners of the company.

The audit is designed to ensure that the shareholders, regulators, advisors and other interested parties can rely on the financial statements to give them a true and fair view of the company’s affairs.

Directors have to report to shareholders at the annual general meeting.

Analysts and other advisors use professional knowledge and skills in evaluating performance, and identifying strengths and weaknesses.

The Combined Code on Corporate Governance sets out good practice to protect the interests of shareholders, and companies are required by law to confirm that they are complying with the Code, or say why they are not.

Many companies have management incentive schemes designed to encourage managers to focus on the maximisation of shareholder value.

Competitive markets for capital and for management jobs tend to encourage managers to act so as to meet shareholder objectives.

Examiner’s comments Almost all answers correctly identified the corporate purpose of a public limited company. While most answers identified reasons related to overcoming the agency problem to explain why managers tend to act in furtherance of the shareholders' interests, a fair number of answers gave, as a reason, that it is an expected part of their job. This was accepted as a valid reason.

(b) Explain how adjusted present value can offer special advantages in terms of

representing the cost of capital. (4 marks) Suggested answer Discounted cash flow techniques for capital investment appraisal, such as net present value (NPV) and internal rate of return, discount cash flows using a discount rate that represents the cost of capital. In many capital appraisal situations, these methods take account adequately of the cost of capital. A more detailed approach may be needed if the cost of capital for a particular project differs from the risk or cost of capital for the generality of a company’s investment projects. The cost of capital may vary from the company average due to special funding arrangements that are specific to a particular project (for example, if an investment is funded using subsidised loans) or special tax treatment (if tax allowances are available in connection with a particular

© ICSA, 2010 Page 3 of 18

project, or a project involves overseas investment or operations). Variations in the cost of capital may be needed if a project is large, and has an effect on the average cost of capital for the whole company. Adjusted present value can deal with problems of this kind by calculating a ‘base case’ NPV, using the like ungeared cost of equity to discount cash flows, and then adjusting the base case NPV to reflect the effects of factors such as a different interest rate, an atypical level of risk or cash flows arising from taxation. Examiner’s comments Many answers were very brief, indicating candidates did not know what adjusted present value was. Time was wasted by some candidates writing answers that were wide of the mark.

(c) Give four reasons why a small, recently established company might prefer to

have its shares listed on the Alternative Investment Market rather than on the main market. (4 marks)

Suggested answer Advantages of the Alternative Investment Market (AIM) include:

No requirements as to size, profitability, track record or proportion of shares in public hands (unlike the main market).

Less stringent regulation.

Lower costs.

The use of Nominated Advisors (‘Nomads’), who provide a flexible way of getting advice on a company’s obligations under the AIM rules.

Possible tax benefits for shareholders, since AIM quoted shares are treated as unquoted by the UK tax authorities.

Examiner’s comments This question was generally very well answered.

(d) The following information is provided about a share:

Standard deviation of the return on the share: 10% Standard deviation of the return on the market portfolio: 8% Coefficient of correlation between the return on the share and the return on the market portfolio:

- 0.6

Calculate the beta of the share, and calculate, showing your working, by how much the return on the share would be expected to change if the market return increased from 8% to 12%. (4 marks)

Suggested answer

m

sms

s

= 10% x (-0.6)/8% = -0.75

© ICSA, 2010 Page 4 of 18

Change in the expected return: = -0.75 x change in market return = -0.75 x (12% - 8%) = -3%

Examiner’s comments This question was poorly answered by many candidates. Few answers gave a correct figure for beta, and fewer used it correctly. Many answers confused the standard deviation of the return on the market portfolio (used in calculation beta) with the market return (used in calculating the expected return on the share).

(e) Explain why ‘capital gearing’ is of interest to shareholders. (4 marks)

Suggested answer Capital gearing is the ratio of debt to shareholders’ funds in the long-term capital of a company. A high geared company has a high ratio. The expression ‘highly geared’ may imply, depending on the context, that the level of borrowing is such as to cause a significant risk of insolvency. The level of gearing at which this happens depends on the nature of the business and, in particular, the steadiness of operating cash flow from which to pay interest. The level of gearing of a company is significant because the interest on debt is payable whatever the operating profit of a company. Whereas, dividends on ordinary share capital can only be paid when there are sufficient distributable profits, and can be passed (not paid) or reduced if the directors think it sufficiently important to conserve funds. The effect of the fixed cost represented by debt interest is that profits after interest are more variable than profits before interest and, therefore, riskier. The risk arising from gearing is financial risk. Shareholders are interested in gearing since they are interested in risk and, in particular, the level of risk affects the return they require. Examiner’s comments This question was generally well answered.

(f) The following information is provided about a company:

£ million Operating revenue 120 Variable operating costs 80 Fixed operating costs 30 Profit before interest and tax 10

Calculate the operating gearing for this company (showing the definition of operating gearing that you use), and explain why operating gearing provides a measure of risk. (4 marks)

Suggested answer Operating gearing = Fixed operating costs/Total operating costs = £30m/(£30m + £80m) = .273 = 27.3% Alternatively: Operating gearing = Contribution/Operating profit before interest and tax = £40m/£10m = 4.0

© ICSA, 2010 Page 5 of 18

Whichever definition is used, higher operating gearing usually means that fixed costs are more important in relation to variable costs. This has the same significance for risk as financial gearing: since fixed costs have to be covered before a profit is made, companies with higher operating gearing have greater volatility in their profits – and therefore greater risk - as a result of variations in the volume of business. Examiner’s comments This question was poorly answered by many candidates. Few answers gave an acceptable definition, though variants were accepted, and fewer explained its significance. Many answers tried to calculate and comment on capital gearing.

(g) Explain the relevance of the efficient market hypothesis for financial

management. (4 marks)

Suggested answer According to the efficient market hypothesis, prices in securities markets reflect relevant information concerning securities. They do this in different ways, depending on the different versions of the hypothesis. The strong form states that all relevant information, published and unpublished, is taken into account. The semi-strong form states that prices reflect all published information. The weak form states that only past price information is reflected. The main implications for financial management are: (i) Since the market values a company’s shares using all the information available to it, it

would be misleading to take decisions on the assumption that the shares are under or over-valued. This means that, in decisions on such things as the timing of share issues or prices for mergers and acquisitions, there is no ‘best’ time for issuing or valuing shares, since any future changes will be caused by factors that are as yet unknown.

(ii) Markets can ‘see through’ any attempts at manipulating profits and so a firm’s share price cannot be boosted by ‘creative accounting’.

(iii) In efficient markets, the ‘intrinsic value’ of a share is reflected in the market price. This means that the impact of management actions can be seen by managers as well as investors.

(iv) Managers should, therefore, focus on actions that will increase shareholders’ wealth.

Examiner’s comments Answers to this question were generally acceptable, or better. Most gave an acceptable statement of the efficient market hypothesis, but fewer answers explained its significance for financial management, though both aspects are standard bookwork. However, some candidates took the question as a cue to explain the efficiency frontier in portfolio theory.

(h) A company is issuing 218 million additional ordinary shares with a nominal value

of 5 pence each. The first dividend on the new shares will be paid in one year’s time. The current dividend is 12 pence, and dividends are expected to grow at an annual rate of 10%. The annual return required by purchasers of the shares is 14%. The expenses of the issue are expected to be 18% of the funds raised. Calculate the amount in £, after expenses, that the issue will raise. (4 marks)

Suggested answer

Po = g- Ke

g) + (1 do =

0.10- 0.14

0.10) + (1 12 = 330 pence

Total proceeds of issue: = 218 million x 330 pence x (1 – 0.18) = £589.908 million

© ICSA, 2010 Page 6 of 18

Examiner’s comments Many candidates did not use the correct formula to find the issue price. Many tried to use the formula linking the company's cost of capital to the share price and the issue expenses, though the rate of return given in the question was the investors’ expected rate of return, and not the company's cost of capital. A number of answers based the calculation on the nominal value of the shares.

(i) Name four different jobs in which the person fulfilling the role would be involved

in corporate financial management and would report to a finance director. For each job, state a task in corporate financial management with which the job is concerned. (4 marks)

Suggested answer Possible jobs reporting to the finance director, and activities involved in these jobs, could include:

Financial controller – capital budgeting, investment appraisal, stock control, credit control, selection of short-term investments and audit.

Financial accountant – recording transactions concerned with investment, procurement of funds or payment of dividends and preparation of management reports concerned with similar matters.

Management accountant – provision of management information in areas concerned with corporate financial management and dealing with decision making, planning and control.

Treasurer/cashier – budgeting for cash flows, providing and using liquid funds, ensuring the physical security of cash and foreign currency management including risk management.

Financial strategist – procuring and managing funds and organising communications with external bodies and groups of stakeholders such as government and investors.

Examiner’s comments This question was straightforward, and many answers earned high marks. However, a number of answers identified the jobs of people who would probably not report to a finance director, as required by the question, even though they might provide information and services to do with corporate financial management. Latitude was allowed in the answers that were accepted.

(j) A company issued ordinary shares with a nominal value of £1 each in an initial

public offering three years ago. Since then, it has made losses every year and its operating cash flows have been consistently negative. The company’s management is honest and competent. The company’s financial statements have been audited by an accounting firm of unblemished reputation, using experienced professional staff, and the auditor’s reports have been unqualified. The shares were issued at a price of £2.75, and are now valued at £8.23 (even though, over the past three years, the price index for the whole market has fallen). Suggest how this price increase could have occurred. (4 marks)

Suggested answer Any market values shares on the basis of its expectations about the future benefits that can be received by shareholders, usually on the basis of future business performance. The past activities that have contributed to expectations about the future performance of this company have incurred high costs, greater than any income, and operating activities have absorbed cash. This is typical of a company that is spending heavily to develop the potential for future profitable activities. Such spending is often on research and development of new and innovative products, for example, in biotechnology and other technology-dependent businesses. Though the research

© ICSA, 2010 Page 7 of 18

has not yet led to the profitable marketing of new products, the market believes that progress is satisfactory, and that it will. Examiner’s comments This required a little speculative imagination, and, on the whole, candidates rose well to the challenge.

Section B 2. Playmex plc (‘Playmex’), a distributor of children’s toys, has recently introduced an

incentive scheme offering its managers bonuses linked to the gross level of turnover achieved. Playmex currently allows a maximum credit period of 30 days to all customers, and does not offer any early payment discount. In practice, only 60% of customers pay on 30 days, and 40% delay payment by an extra 10 days on average. Playmex is considering whether it should relax its credit policy in order to attract more customers, so as to increase the company’s turnover and market share.

The changes that are under consideration are: (i) to offer a discount of 4% to customers who pay on 15 days; and (ii) to extend the maximum credit period allowed from 30 days to 60 days.

The Marketing Director believes that these changes will increase sales turnover before discounts and bad debts from £100 million to £150 million. If the changes are made as outlined above, 50% of customers are expected to pay on 15 days to qualify for the discount, and 40% are expected to take the new longer credit period. 10% are expected to delay payment, by an average of 15 days, beyond the new maximum allowed period of 60 days. Playmex’s variable cost ratio (variable operating costs as a percentage of sales) is currently 86%, and the company funds working capital with a bank overdraft on which it pays 10% interest. The company’s fixed costs are £5 million per annum. There are no bad debts at present, and the company does not expect there to be any if the new credit policy is adopted. REQUIRED

(a) (i) Evaluate the impact of the revised credit policy on the amount of working

capital (in £) invested in debtors, and on the company’s profit before tax. (10 marks)

(ii) Use the results of your work in (a)(i) above, to provide advice concerning

the company’s credit policy decision. (3 marks)

Suggested answer

(i) Old debtors = (0.60 X 30/365 x £100m) + (0.40 X 40/365 x £100m) = £9,315,068 New debtors = (0.50 x 15/365 x 0.96 x £150m) + (0.40 x 60/365 x £150m) + (0.10 x 75/365 x £150m) = £15,904,110 Extra working capital investment = £6,589,042

© ICSA, 2010 Page 8 of 18

Old debtors interest cost = 0.10 x £9,315,068 = £931,507 New debtors interest cost = 0.10 x £15,904,110 = £1,590,411

Discounts under new credit policy = 0.04 x 0.50 x £150,000,000

= £3,000,000

Old credit policy New credit policy

Gross sales 100,000,000 150,000,000

Variable cost of sales (86%) 86,000,000 129,000,000

Discounts - 3,000,000

Fixed costs 5,000,000 5,000,000

PBIT 9,000,000 13,000,000

Debtors interest cost 931,507 1,590,411

Profit before tax 8,068,493 11,409,589

Increase in profit before tax 3,341,096

(ii) On the basis of the stated assumptions, Playmex should change its credit terms, since profit before tax would increase from £8,068,493 to £11,409,589. However, the increase in the profit depends on assumptions about hypothetical factors, perhaps most importantly, how much sales can be increased and whether the new customers will pay promptly (or at all). These assumptions should be tested, if possible, and the sensitivity of the profit figures to possible changes in the assumptions should be calculated.

(b) Discuss how far managerial incentive schemes based on share options and profit

targets ensure that managers pursue the goal of maximising shareholder wealth. (7 marks)

Suggested answer Maximising shareholder wealth involves a combination of share price growth and dividend income, taking account of risk and the timing of returns. To achieve goal congruence between shareholders and managers, many companies have management incentive schemes based on share price performance: Share options give managers the right to purchase shares at a pre-determined price at some future date. If the actual price is higher than the pre-determined exercise price, the difference allows a manager who exercises his options to make a capital gain, and this serves as a powerful incentive to maximise the share price. Share options can encourage managers to take actions that maximise profits up to the point in time when options are exercised, but have adverse effects in the longer-term. Because share prices are also affected by factors that affect the market as a whole and are outside the control of the company’s managers, rewards based on share prices do not reflect only the actions taken by managers. This may be seen when share prices are depressed by adverse market movements and managers press for new options, rebased with lower exercise prices, since there is little prospect of existing options being profitable. Managers' salaries and other benefits are often linked to profits. Managers may, therefore, be interested in maximising profits, often in the short-term. Short-term profit maximisation will not necessarily maximise shareholder wealth. Activities that are profitable in the medium or long-term do not necessarily make profits straight away, and actions to improve profitability in the short-term, particularly by cutting costs, can damage investments made for the longer-term. Growth in profits may not increase shareholder value if it is achieved with an unacceptable

© ICSA, 2010 Page 9 of 18

increase in the level of risk, or so much new share capital is required that existing shareholders’ holdings are diluted and the earnings per share reduced. Examiner’s comments Question 2 was not popular, although the calculations required in part (a) were straightforward. Those candidates who attempted the calculations, on the whole, did them reasonably well. The discussion of the effectiveness of share options and profit targets required in part (b) was, generally, fairly well done.

3. Sunshine Deluxe plc (‘SD’) is a UK-based food manufacturer that is expanding its

operations through foreign direct investment. It is currently constructing a plant in Poland to produce vegetable and fruit extracts and purees, and a final payment of Polish Zloty 12 million is due to be paid to a Polish contractor in three months’ time.

Current rates in the foreign exchange and money markets are:

Foreign exchange market Zloty/£ Spot 4.9095 – 4.9148 1 month forward 18 – 22 basis points discount 3 months’ forward 75 – 84 basis points discount

Money Market Borrowing Deposit Sterling 5% 2% Zloty 7% 3%

REQUIRED

(a) Suggest reasons why a company may undertake foreign direct investment.

(8 marks)

Suggested answer Possible motives for foreign direct investment include:

(i) To establish new markets and attract new demand. (ii) To avoid tariffs and trade restrictions. (iii) To gain access to low-cost materials, labour or fixed assets. (iv) To gain access to special skills. (v) To gain access to raw materials. (vi) To benefit from grants and subsidies offered by foreign governments. (vii) To achieve economies of scale. (viii) To gain access to new overseas markets when access is restricted to companies based in

the countries concerned, or when imports are restricted by tariffs or quotas. (ix) To take advantage of what is perceived to be an undervalued or overvalued foreign

currency. (x) To exploit competitive advantages arising from the firm’s possession and control of

information, technology, marketing or other commercial expertise.

(b) Calculate the cost to SD, in £, in three months’ time, of the final payment to the contractor if SD uses a forward purchase in the foreign exchange market to hedge the currency risk. (3 marks)

Suggested answer SD needs to pay Zloty 12 million in 3 months’ time.

© ICSA, 2010 Page 10 of 18

Forward rate for purchase of Zloty: 4.9095 + 0.0075 = Zloty 4.9170:£ The cost in £ in three months using forward contract: Zloty 12m/(Zloty 4.9170:£) = £2,440,512.51

(c) Calculate the amount in £ that SD will have to pay in three months’ time if it

hedges the foreign exchange risk of the payment to the contractor by the following actions:

(i) Borrows sterling today and converts this into Zloty at the spot rate. (ii) Deposits the Zloty to earn interest for three months. (iii) Uses the deposit, together with interest earned, to pay the amount due in

three months’ time. (iv) Pays back with interest in three months’ time the sterling borrowed today.

(4 marks)

Suggested answer To provide Zloty 12m in three months, SD needs to deposit: 12m/(1 + .03/4) = Zloty 11,910 669.98 today Cost in £ today = Zloty 11,910,669.98/(Zloty 4.9095:£) = £2,426,045.42 If £2,426,045.42 is borrowed today, the amount repaid in three months’ time with interest = £2,426,045.42 x (1 + .05/4) = £2,456,370.99

(d) SD has been advised that it might get a better exchange rate than would apply in

3(b) above, if it undertook a forward contract with a bank. Explain how commercial companies, with which the bank makes such contracts, are paying a premium to reduce or remove risk, while the bank may be able to make a risk-free profit from the very same contracts. (5 marks)

Suggested answer If SD undertakes today to buy Zloty in three months’ time, it will receive Zloty 4.9170 for each £. If another company undertakes a forward contract to sell Zloty in three months’ time, it will have to give Zloty 4.9148 + .0084 = Zloty 4.9232 for each £. If both companies undertake forward contracts with the same bank, the difference between Zloty 4.9232 and Zloty 4.9170 will be the amount that they pay between them for each £ to remove uncertainty about the exchange rate. If both contracts are for the same amount, the bank will make a profit with no foreign exchange risk (though it will still have counterparty risk) and will make a risk free profit. Forward contracts undertaken by the bank with commercial companies will not necessarily involve buying and selling the same amount of each foreign currency, but contracts to buy and sell a given currency will, to some extent, balance each other out (and if the bank wants to eliminate its foreign exchange risk altogether, it can undertake contracts with other banks).

Examiner’s comment Part (a) was a very straightforward question and was generally very well answered by the large number of candidates who attempted Question 3. The forward purchase calculation in part (b) was well done by a fair number of candidates. The money market hedge calculation in part (c) was rather less well done, and some candidates who answered Question 3 did not do this part.

© ICSA, 2010 Page 11 of 18

Part (d) required an explanation of how banks can make a risk-free profit from forward currency transactions. The part of the answer to do with the role of a bank's customer was reasonably well answered, but the part to do with the bank's risk and return was often much less well done.

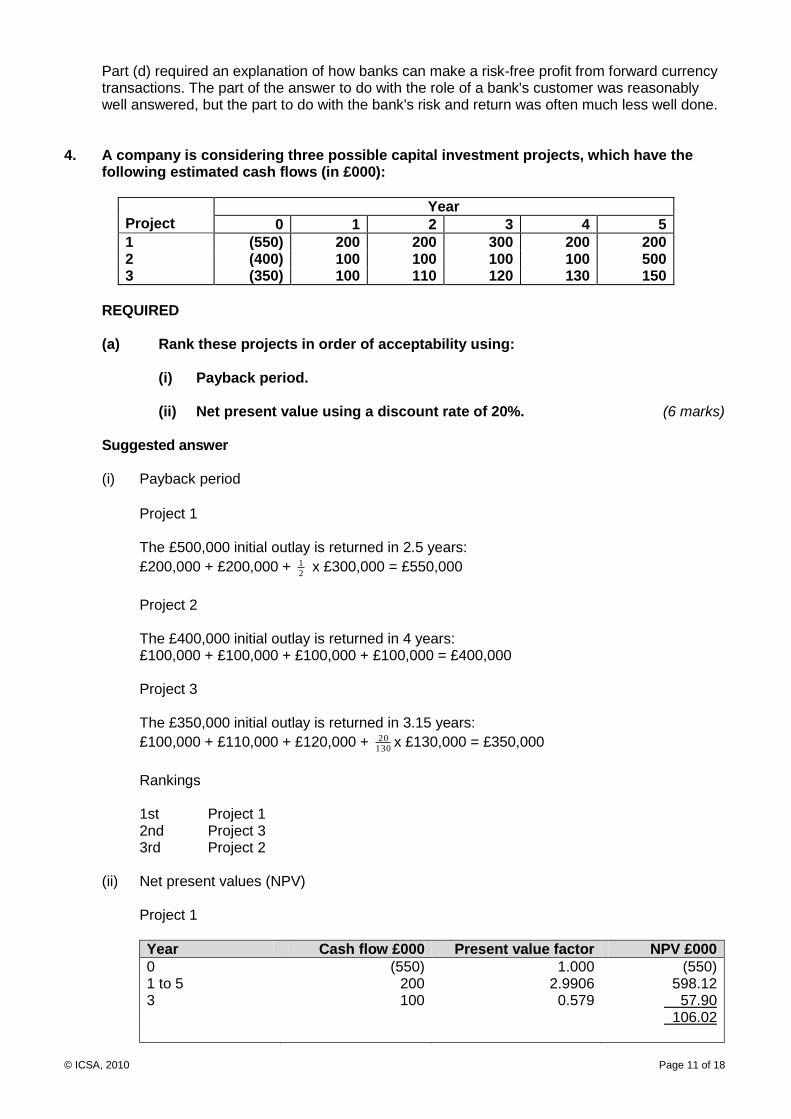

4. A company is considering three possible capital investment projects, which have the

following estimated cash flows (in £000):

Project

Year

0 1 2 3 4 5

1 (550) 200 200 300 200 200 2 (400) 100 100 100 100 500 3 (350) 100 110 120 130 150

REQUIRED

(a) Rank these projects in order of acceptability using:

(i) Payback period.

(ii) Net present value using a discount rate of 20%. (6 marks)

Suggested answer (i) Payback period

Project 1 The £500,000 initial outlay is returned in 2.5 years:

£200,000 + £200,000 + 21 x £300,000 = £550,000

Project 2 The £400,000 initial outlay is returned in 4 years: £100,000 + £100,000 + £100,000 + £100,000 = £400,000 Project 3 The £350,000 initial outlay is returned in 3.15 years:

£100,000 + £110,000 + £120,000 + 13020 x £130,000 = £350,000

Rankings 1st Project 1 2nd Project 3 3rd Project 2

(ii) Net present values (NPV)

Project 1

Year Cash flow £000 Present value factor NPV £000

0 (550) 1.000 (550) 1 to 5 200 2.9906 598.12 3 100 0.579 57.90 106.02

© ICSA, 2010 Page 12 of 18

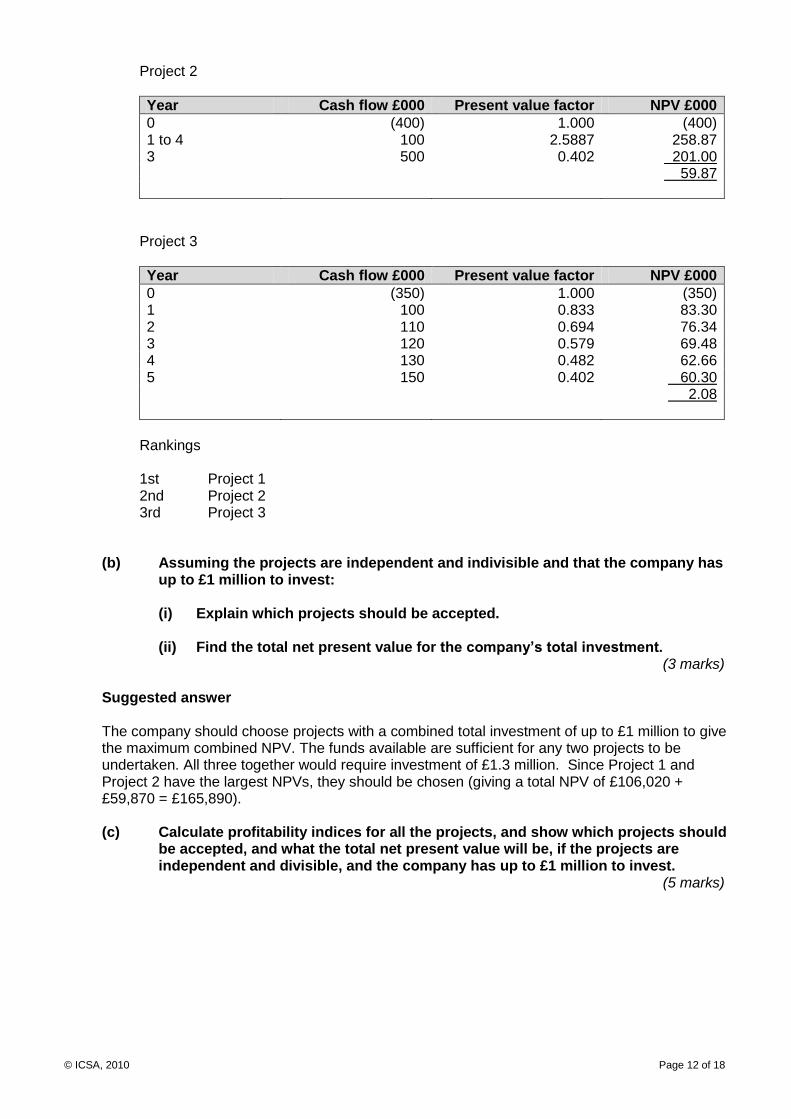

Project 2

Year Cash flow £000 Present value factor NPV £000

0 (400) 1.000 (400) 1 to 4 100 2.5887 258.87 3 500 0.402 201.00 59.87

Project 3

Year Cash flow £000 Present value factor NPV £000

0 (350) 1.000 (350) 1 100 0.833 83.30 2 110 0.694 76.34 3 120 0.579 69.48 4 130 0.482 62.66 5 150 0.402 60.30 2.08

Rankings 1st Project 1 2nd Project 2 3rd Project 3

(b) Assuming the projects are independent and indivisible and that the company has up to £1 million to invest:

(i) Explain which projects should be accepted. (ii) Find the total net present value for the company’s total investment. (3 marks)

Suggested answer The company should choose projects with a combined total investment of up to £1 million to give the maximum combined NPV. The funds available are sufficient for any two projects to be undertaken. All three together would require investment of £1.3 million. Since Project 1 and Project 2 have the largest NPVs, they should be chosen (giving a total NPV of £106,020 + £59,870 = £165,890).

(c) Calculate profitability indices for all the projects, and show which projects should

be accepted, and what the total net present value will be, if the projects are independent and divisible, and the company has up to £1 million to invest. (5 marks)

© ICSA, 2010 Page 13 of 18

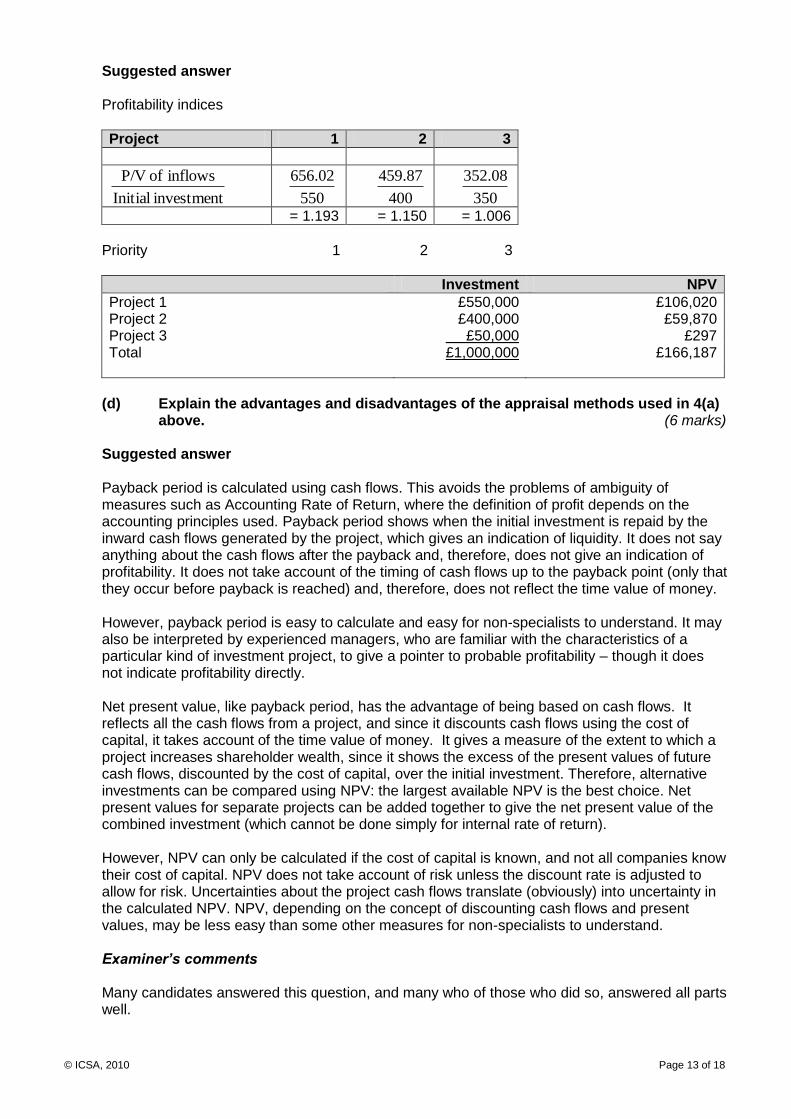

Suggested answer Profitability indices

Project 1 2 3

investment Initial

inflows of P/V

550

02.656

400

87.459

350

08.352

= 1.193 = 1.150 = 1.006

Priority 1 2 3

Investment NPV

Project 1 £550,000 £106,020 Project 2 £400,000 £59,870 Project 3 £50,000 £297 Total £1,000,000 £166,187

(d) Explain the advantages and disadvantages of the appraisal methods used in 4(a)

above. (6 marks)

Suggested answer Payback period is calculated using cash flows. This avoids the problems of ambiguity of measures such as Accounting Rate of Return, where the definition of profit depends on the accounting principles used. Payback period shows when the initial investment is repaid by the inward cash flows generated by the project, which gives an indication of liquidity. It does not say anything about the cash flows after the payback and, therefore, does not give an indication of profitability. It does not take account of the timing of cash flows up to the payback point (only that they occur before payback is reached) and, therefore, does not reflect the time value of money. However, payback period is easy to calculate and easy for non-specialists to understand. It may also be interpreted by experienced managers, who are familiar with the characteristics of a particular kind of investment project, to give a pointer to probable profitability – though it does not indicate profitability directly. Net present value, like payback period, has the advantage of being based on cash flows. It reflects all the cash flows from a project, and since it discounts cash flows using the cost of capital, it takes account of the time value of money. It gives a measure of the extent to which a project increases shareholder wealth, since it shows the excess of the present values of future cash flows, discounted by the cost of capital, over the initial investment. Therefore, alternative investments can be compared using NPV: the largest available NPV is the best choice. Net present values for separate projects can be added together to give the net present value of the combined investment (which cannot be done simply for internal rate of return). However, NPV can only be calculated if the cost of capital is known, and not all companies know their cost of capital. NPV does not take account of risk unless the discount rate is adjusted to allow for risk. Uncertainties about the project cash flows translate (obviously) into uncertainty in the calculated NPV. NPV, depending on the concept of discounting cash flows and present values, may be less easy than some other measures for non-specialists to understand. Examiner’s comments Many candidates answered this question, and many who of those who did so, answered all parts well.

© ICSA, 2010 Page 14 of 18

5. Financial Support Services plc (‘FSS’) is planning to issue £100 million nominal of 8% redeemable loan stock at a price of £95 per £100 nominal. The stock will be redeemed at par four years from now. Interest will be paid annually, with the first payment at the end of the first year. FSS is making substantial profits, and expects to continue to do so for the foreseeable future. It pays corporation tax at 28%, and the timing of tax and loan stock interest payments is expected to be such that one half of the tax relief on interest will be received in the year in which interest is paid and one half in the following year.

REQUIRED

(a) Find the after-tax cost of the loan stock capital. (16 marks)

Suggested answer

Cash flows for £100 nominal of 8% loan stock

Cash flow Years from

present

Cash flow

Discount factor

(8%)

Present value (8%)

Discount factor

(6%)

Present value (6%)

£ £ £

Received from subscribers

0 95.00

Net cash flow (Year 0) 0 95.00 1.000 95.00 1.0 95.00

Interest (Year 1) 1 (8)

Tax relief (Year 1) 1 1.12

Net cash flow (Year 1) 1 (6.88) 0.926 (6.37088) 0.943 (6.48784)

Interest (Year 2) 2 (8)

Tax relief (Year 2) 2 2.24

Net cash flow (Year 2) 2 (5.76) 0.857 (4.93632) 0.890 (5.1264)

Interest (Year 3) 3 (8)

Tax relief (Year 3) 3 2.24

Net cash flow (Year 3) 3 (5.76) 0.794 (4.57344) 0.840 (4.8384)

Interest (Year 4) 4 (8)

Tax relief (Year 4) 4 2.24

Redemption (Year 4) 4 (100.00)

Net cash flow (Year 4) 4 (105.76) 0.735 (77.7336) 0.792 (83.76192)

Tax relief (Year 5) 5 1.12 0.681 0.76272 0.747 0.83664

Total 2.14848 (4.37792)

Workings

Received in year Received in following year

Tax relief for Years 1 to 4: 28% of £8 = £2.24 £1.12 £1.12

IRR = lowrate +

)lowrate - highrate(

e)NPVhighrat - e(NPVlowrat

NPVlowrate

= 6% +

%)6%8(

2.14848 -) (4.37792

(4.37792)

= 7.3%

This is the cost of loan capital.

© ICSA, 2010 Page 15 of 18

(b) State, with reasons, whether you would expect the cost of FSS’s ordinary share capital to be higher or lower than the cost of the loan stock capital. (4 marks)

Suggested answer Loan capital is less risky for investors because the company has a legal obligation to pay the interest, and to repay the principal at the redemption date, whatever its financial situation. Equity capital carries no such obligations. Dividends can only be paid if distributable profits are available and, in the event of a winding up, the ordinary shareholders are last in priority to have their capital repaid, and get their capital back only if all other claims have been met. Investors therefore, expect a higher return on equity than on debt to compensate them for the greater risk of equity. Conversely, since equity carries a smaller risk for the company than debt capital, the company expects to pay a higher return to equity investors because of the lower risk to the company. Companies can deduct loan stock interest when calculating taxable profits, which reduces the after-tax cost of loan capital, whereas dividends are paid out of taxed profits, so that there is no corresponding reduction in the cost of equity. (The rates of taxation of interest and dividends in the hands of investors depends on their tax status, but there is no such clearly consistent difference in the taxation treatment of dividends and interest for investors as there is for companies.) Examiner’s comments This question was not popular. Discounted cash flow calculations are usually popular, as were those in Question 4, but they are much less popular when they involve tax. When, as here, candidates have to decide what approach to take, rather than being told to calculate NPVs or IRRs, they are even less popular. Most of the few candidates who answered this question did the calculations at least tolerably well, and comments were generally good.

6. You have recently been appointed to work for a company that manages several

investment funds, and have been asked to review the performance of two investment portfolios. Your company is planning to liquidate one of these portfolios in order to raise funds for a new investment. You have been asked to advise on which of the two portfolios below should be liquidated:

Portfolio O

Share Beta of share

Actual Return over last year (%)

Amount invested (£ million)

Banks plc 1.3 15 17.4 Charlton plc 0.1 7 13.6 Moore plc 0.9 12 8.8 Stiles plc 1.6 16 10.2

Portfolio N

Share Beta of share

Actual Return over last year (%)

Amount invested (£ million)

Beckham plc 1.0 14 21.0 Cole plc 0.4 11 10.8

Heskey plc 1.8 21 25.5 Lampard plc 0.2 10 17.7

The risk-free rate of return is 5.5% and the market risk premium is estimated to be 8%.

© ICSA, 2010 Page 16 of 18

REQUIRED

(a) Explain the principle of portfolio diversification and its relevance to the capital asset pricing model. Include in your answer a comment on what the ‘beta’ of a share represents, and how it is determined. (10 marks)

Suggested answer Combining stocks in a portfolio reduces portfolio risk, because non-systematic risk, which arises from factors that are special to individual companies, affects individual shares in ways that are not related between companies. Consequently, non-systematic risks tend to balance each other out, and this effect becomes greater as more shares are included in a portfolio. It is often found that a portfolio of about 15 to 20 stocks the effect of non-systematic risk is substantially removed. The amount of reduction of non-systematic risk depends on the degree of correlation between the returns on the different investments in the portfolio. The greatest risk reduction occurs when the correlations between the returns on different securities are negative. Most securities tend to be positively correlated, limiting the scope for risk reduction. Because non-systematic risk tends to be removed by diversification in a portfolio, the total risk of a security held in isolation is more than that of the same security held as part of a portfolio. The non-systematic risk for an individual security is called specific risk, because it arises from factors that are specific to that company, or diversifiable risk, because its effects are reduced by diversification in a portfolio. Systematic risk affects all the securities in the market, and is associated with factors such as economic conditions, political events and general market sentiment. Systematic risk is also called market risk or undiversifiable risk. Diversified investors are concerned about the systematic risk of a security – not the specific risk, which can be diversified away. The ‘market portfolio’ refers to a hypothetical portfolio of all the shares in the market, weighted according to market capitalisation. By its nature, the market portfolio is well diversified, but it is not unique in this. The market portfolio is unique in that it gives the biggest return (measured by the excess of the return over the return from a risk free investment such as short dated government stock) per unit of risk (measured by the standard deviation of the portfolio return). Market indices like the FTSE 100 share index in London and the S&P 500 share index in New York are taken as proxies for the market portfolio. The beta of a share is the slope of a regression line of the historical returns on the share against the returns on the market portfolio. It measures the change in the share’s return that is ‘explained’ by change in the return on the market portfolio, and thus provides a measure of the share’s systematic risk. Given the return on the market portfolio and the risk-free return, the expected return on any share (the return that is required to compensate for share’s systematic risk but not for its diversifiable risk) can be estimated using the share’s beta. The capital asset pricing model (CAPM) relates the return required on an investment to the systematic risk of the investment measured by the investment’s beta:

Rs = Rf + ß (Rm Rf) Where: Rs = The required return. Rf = The risk-free rate. ß = The investment’s beta.

© ICSA, 2010 Page 17 of 18

Rm = The expected return on the market portfolio.

(b) Using the capital asset pricing model, carry out calculations to show which of the two portfolios has performed better, and which should be liquidated, and comment on the validity of your conclusions. (10 marks)

Suggested answer Expected and actual portfolio returns: Portfolio O Portfolio beta = (1.3 x 17.4/50) + (0.1 x 13.6/50) + (0.9 x 8.8/50) + (1.6 x 10.2/50) = 0.9644 Expected return = 5.5 + (8 x 0.9644) = 13.22% Actual return of the portfolio over the last year: (15 x 17.4/50) + (7 x 13.6/50) + (12 x 8.8/50) + (16 x 10.2/50) = 12.50% Portfolio O has under-performed, since its actual return has been less than the return expected on the basis of the CAPM to compensate for the level of systematic risk, measured by the portfolio beta. Portfolio N Portfolio beta = (1.0 x 21.0/75) + (0.4 x 10.8/75) + (1.8 x 25.5/75) + (0.2 x 17.7/75) = 0.9968 Expected return = 5.5 + (8 x 0.9968) = 13.47% Actual return of the portfolio over the last year: (14 x 21.0/75) + (11 x 10.8/75) + (21 x 25.5/75) + (10 x 17.7/75) = 15.00% Portfolio N has over-performed. Conclusion According to the CAPM, Portfolio N has performed better. Portfolio O, which has underperformed, should be liquidated. Validity of conclusions A portfolio of only four investments is unlikely to be well diversified, and would still have some non-systematic risk as well as systematic risk. Alternative portfolios with a greater degree of diversification should be considered. The CAPM theory is based on assumptions about perfect markets that may not hold true. This can affect the validity of conclusions based on CAPM.

© ICSA, 2010 Page 18 of 18

CAPM oversimplifies reality by making the expected return on a particular share depend on only one parameter that is special to that share: its beta. Betas are calculated using series of returns on individual shares and on the market portfolio. The parameters of the regression equations of the security return on the market return depend on the period of time over which the series are taken, and can vary. Market indices used in CAPM calculations to represent the performance of the market portfolio do not exactly represent the whole market, which includes all possible investments. Examiner’s comments This question was popular, and the discursive part which required standard bookwork was well done by many candidates. The calculations, which involved calculating portfolio weighted returns, partly using the CAPM, were less complete. Most answers did calculations to find the expected returns, though many answers treated the risk premium, which was given in the question, as the market return. A number of answers did not calculate the actual returns on the portfolios. Most answers gave some comment on the results of the calculations.

The scenarios included here are entirely fictional. Any resemblance of the information in the scenarios to real persons or organisations, actual or perceived, is purely coincidental.