Embed Size (px)

DESCRIPTION

Corporate Finance

Citation preview

Investment, Cash Flow, and Corporate Hedging

Deshmukh, S, and S. C. Vogt, 2005, “Investment, cash flow, and corporate hedging”, Journal of Corporate Finance 11, 628-644

Afriyanti H/ M10324057Aulia Annisa I/ M10324055Dina Yeni M/ M10324060Dimas Sumitra D/Endah Dwi K /

Fiesty Utami / M10324061Leni Nurpratiwi /Randy Heriyanto /Sugih Sutrisno P /

Group I

Introduction

The motivation for hedging stems from the

existence of market imperfections.

External funds are more costly than internal

funds.

Testable Hypothesis

If firms hedge to reduce both their reliance on external funds and the volatility of internal cash flow, then their investment spending should be less sensitive to internal cash flow in the presence of hedging.

Parsial Simultan

the sensitivity of investment spending to cash flow is lower when the extent of hedging is higher.

Literature Review

1. Mayers and Smith (1982) and Smith and Stulz (1985)

hedging can reduce the expected tax liability of a firm in the presence of a convex tax schedule.

2. Smith and Stulz (1985)

hedging can reduce the costs of financial distress.

3. Stulz (1984) and Smith and Stulz (1985)provide a rationale for hedging based on managerial risk aversion

Literature Reference

4. Breeden and Viswanathan (1996) and DeMarzo and Duffi (1995)

Focus on asymmetric information between managers and outside investors and on managers’ reputations

5. Stulz (1990), Lessard (1990), and Froot et al. (1993)

Focus on investment policy to provide a rationale for corporate hedging. Their models are based on the premise than external funds are more costly than internal funds.

,

Literature Reference

4. Tufano (1998) exception hedging may involve costs if it isolates managers from the scrutiny of external capital markets.

Underinvestment Rationale and Hypothesis Development

Froot et al. (1993) market imperfections cause external funds to be more costly than internal funds.

firm is faced with a two-period, investment-financing decision.

underinvestment results from the random nature of the first-period wealth w and the existence of the deadweight costs of external finance.

Underinvestment Rationale and Hypothesis Development

The issue of hedging arises because w is random. The firm wants to maximize its expected profits

(or its net present value).

Froot et al. argue :that for hedging to be beneficial, the level of internal wealth w must have a positive impact on the optimal level of investment chosen by the firm.if a firm does not hedge, the variability in the cash flow from assets in place can cause variability in both investment spending and/or external funds raised.

Data and Variables

sample of hedgers/derivative users from the Database of Users of Derivatives, published by Swaps Monitor Publications, New York covers period 1992-1996

Collect annual data from Compustat

Focus on manufacturing firms (SIC 2000-3999)

Data and Variables

Depedent VariableInvestment spending Ratio of Investment to beginning of- year gross plant and equipment

Independent Variablecash flow variablea proxy for investment or growth opportunities (Q)

Data and Variables

Cash Flow Measures :1. CF Mesure 1 =

2. CF Measure 2 =

3. CF Measure 3 =

4. CF Measure 4 =

5. CF Measure 5 =

Operating Income (OI) before deprecitionBeginning of year Gross plant & equipment

Sales – COGS – SGA - NWCBeginning of year Gross plant & equipment

Income before Extraordinary item + D&A- NWC

Beginning of year Gross plant & equipmentOI before depreciatio –income taxes paid-

NWCBeginning of year Gross plant & equipmentOI before depreciation - NWCBeginning of year Gross plant & equipment

`

Empirical Result

`

Empirical Result

`

Empirical Result

Table 3

`

Empirical Result

Table 4

`

Empirical Result

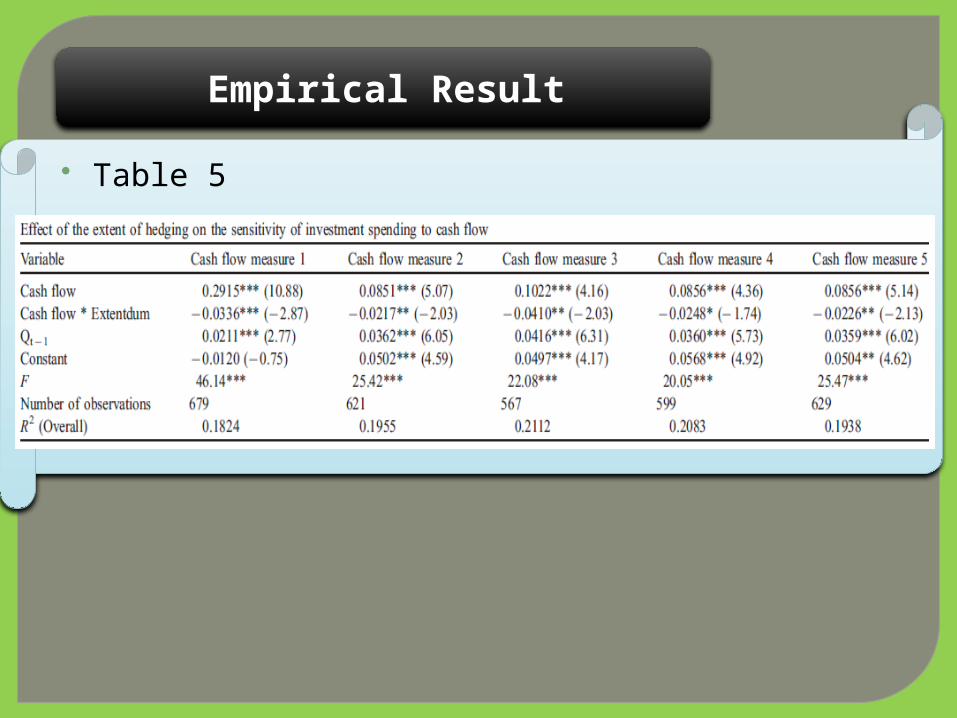

Table 5

Summary and Conclusions

1. The results are consistent with this hypothesis in that the investment spending of hedgers is less sensitive to prehedged cash flow than is that of nonhedgers.

2. Among hedgers, the sensitivity of investment spending to cash flow is lower when the extent of hedging is higher.

THANK YOUFOR YOUR ATTENTION