Embed Size (px)

Citation preview

Distribution or sharing of this material is strictly prohibited and may result in the assignment of a failing grade and/or termination of membership in the Institute for Professionals in Taxation®.

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL

Cornerstone 2 – Basic Valuation of Machinery and Equipment

Learning Objectives At the end of this section, the learner will be able to: Recognize the basic fundamentals of valuation Know the three approaches of valuation applied to personal property Apply the cost approach to valuation of personal property Calculate potential tax savings and apply valuation methods to defend and

challenge your value

Reference Materials Commerce Clearing House (CCH), Wolters Kluwer, Various state reporting instruction pamphlets and IPT publications. www.cchgroup.com

The American Society of Appraisers, (Machinery and Technical Specialties Committee of the American Society of Appraisers, July 25, 2010). www.appraisers.org

American Society of Appraisers. Valuing Machinery and Equipment: The Fundamentals of Appraising Machinery and Technical Assets, Third Edition. American Society of Appraisers, Washington D.C.: 2011.

IPT Personal Property Tax School Valuation – Machinery and Equipment

1

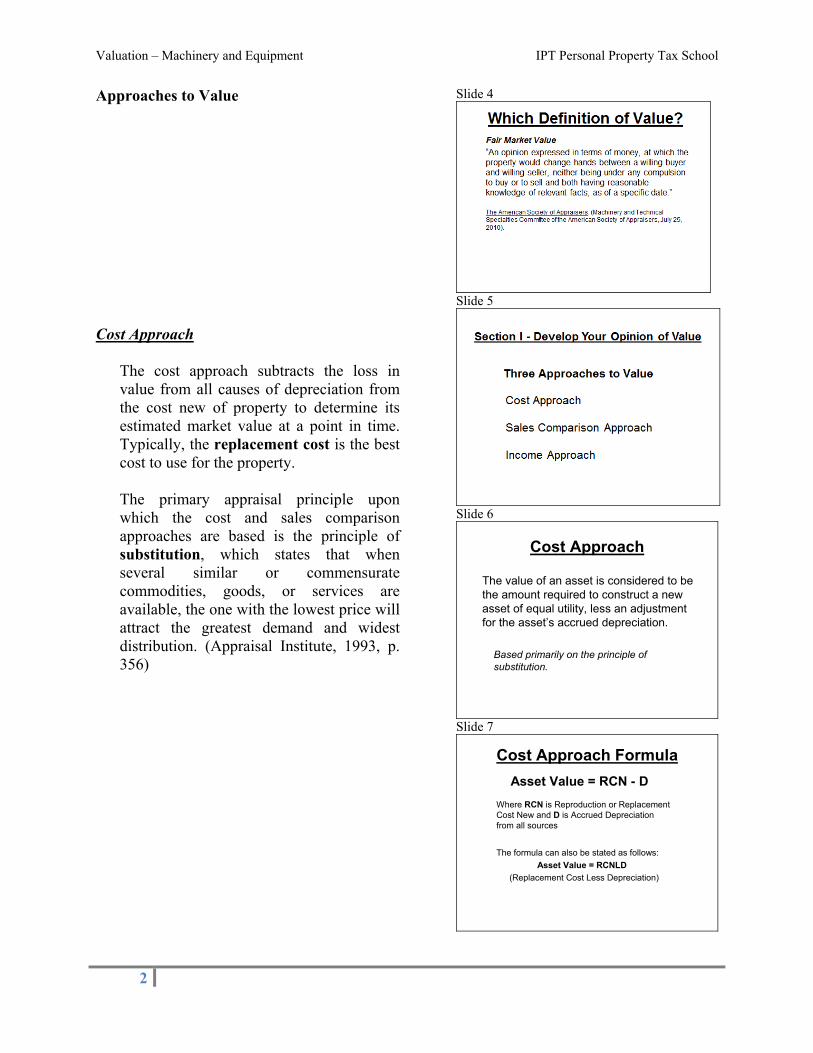

Basic Fundamentals of Machinery and Equipment Valuation Section I – Develop Your Opinion of Value In the valuation and reporting of personal property, we are concerned with Fair Market Value versus Net Book Value or the Assessor’s Value which may only include Cost less Physical Depreciation. All forms of Depreciation must be considered to arrive at Fair Market Value.

Slide 1

Slide 2

Slide 3

Valuation – Machinery and Equipment IPT Personal Property Tax School

2

Approaches to Value

Cost Approach

The cost approach subtracts the loss in value from all causes of depreciation from the cost new of property to determine its estimated market value at a point in time. Typically, the replacement cost is the best cost to use for the property.

The primary appraisal principle upon which the cost and sales comparison approaches are based is the principle of substitution, which states that when several similar or commensurate commodities, goods, or services are available, the one with the lowest price will attract the greatest demand and widest distribution. (Appraisal Institute, 1993, p. 356)

Slide 4

Slide 5

Slide 6

Intermediate Personal Property Tax S chool

Cost Approach

The value of an asset is considered to be the amount required to construct a new asset of equal utility, less an adjustment for the asset’s accrued depreciation.

Based primarily on the principle of substitution.

Slide 7

Intermediate Personal Property Tax S chool

Cost Approach Formula

Asset Value = RCN - D

Where RCN is Reproduction or Replacement Cost New and D is Accrued Depreciationfrom all sources

The formula can also be stated as follows:

Asset Value = RCNLD

(Replacement Cost Less Depreciation)

IPT Personal Property Tax School Valuation – Machinery and Equipment

3

Types of Costs

Replacement Cost - Replacement cost is the cost today to replace property with property of like kind and utility. The materials to construct the property will be the most modern and cost efficient available. It will not include inherent obsolescence. It does not have to be an exact replica. This is the cost that should be used when valuing property. Replacement cost includes material, labor, capitalized interest, entrepreneurial profit, installation and sales tax. This cost is referred to as Replacement Cost New (RCN) Reproduction Cost - Reproduction cost is the cost to reproduce an exact replica of a piece of property as of a specified point in time using current pricing. Generally, the point in time is the current time or in the case of an assessment, the assessment date. An exact replica will include exact materials and workmanship. It will also use exact technology, which may be outdated. The replica will include inherent obsolescence. In practice, assessors generally use reproduction cost as the starting point in the valuation process. This cost is referred to as Reproduction Cost New (RCN)

Slide 8

Intermediate Personal Property Tax S chool

Types of Costs Associated with Valuation Process

Replacement Cost

Reproduction Cost

Indexed Cost aka Trended Cost

Slide 9

Slide 10

Valuation – Machinery and Equipment IPT Personal Property Tax School

4

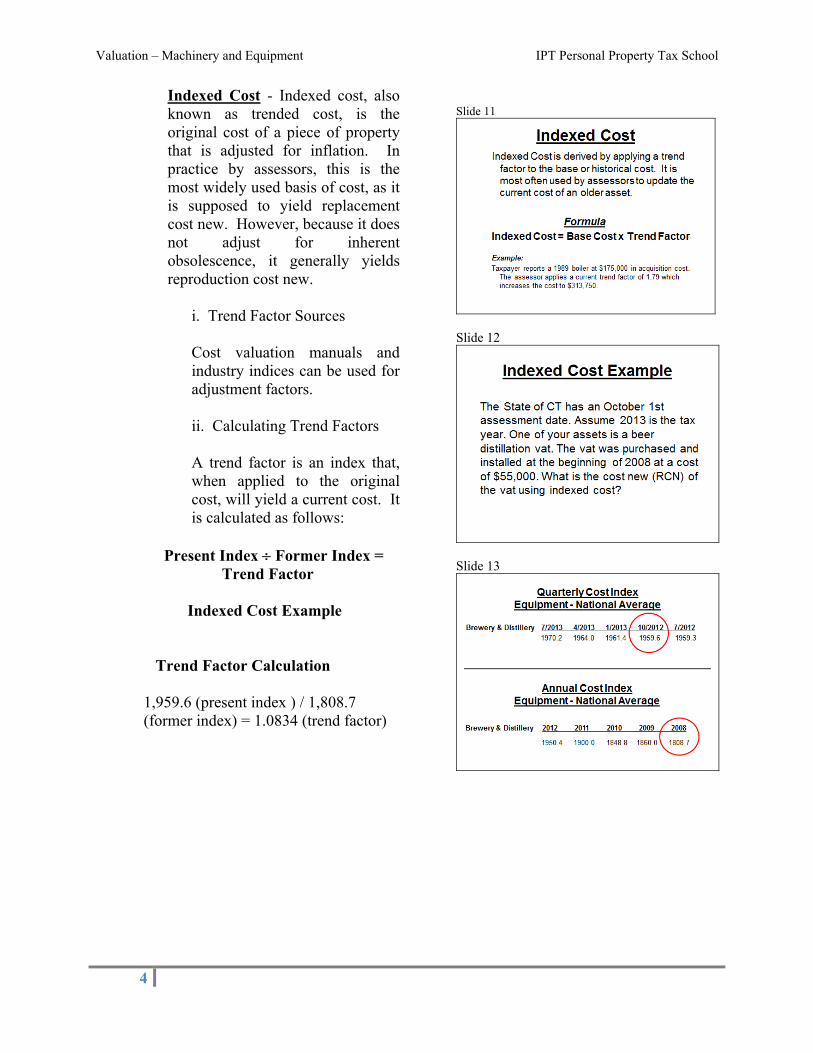

Indexed Cost - Indexed cost, also known as trended cost, is the original cost of a piece of property that is adjusted for inflation. In practice by assessors, this is the most widely used basis of cost, as it is supposed to yield replacement cost new. However, because it does not adjust for inherent obsolescence, it generally yields reproduction cost new.

i. Trend Factor Sources

Cost valuation manuals and industry indices can be used for adjustment factors.

ii. Calculating Trend Factors

A trend factor is an index that, when applied to the original cost, will yield a current cost. It is calculated as follows:

Present Index Former Index =

Trend Factor Indexed Cost Example

Trend Factor Calculation 1,959.6 (present index ) / 1,808.7 (former index) = 1.0834 (trend factor)

Slide 11

Slide 12

Slide 13

IPT Personal Property Tax School Valuation – Machinery and Equipment

5

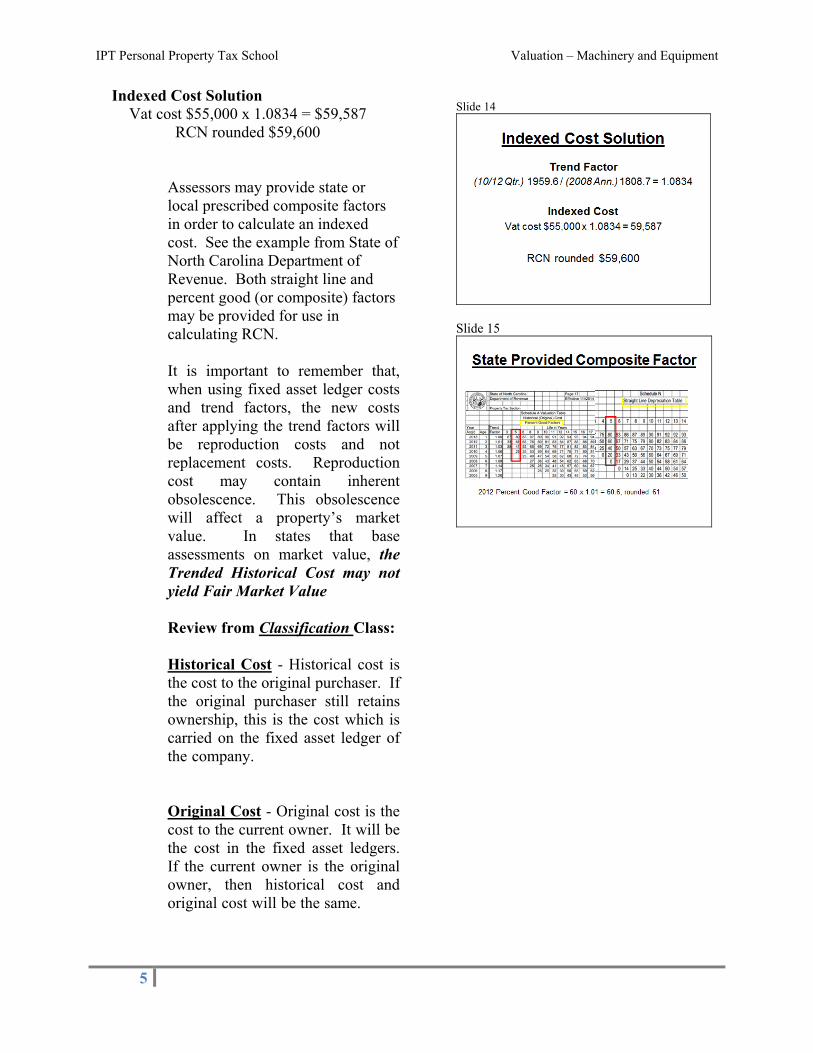

Indexed Cost Solution Vat cost $55,000 x 1.0834 = $59,587

RCN rounded $59,600 Assessors may provide state or local prescribed composite factors in order to calculate an indexed cost. See the example from State of North Carolina Department of Revenue. Both straight line and percent good (or composite) factors may be provided for use in calculating RCN. It is important to remember that, when using fixed asset ledger costs and trend factors, the new costs after applying the trend factors will be reproduction costs and not replacement costs. Reproduction cost may contain inherent obsolescence. This obsolescence will affect a property’s market value. In states that base assessments on market value, the Trended Historical Cost may not yield Fair Market Value

Review from Classification Class:

Historical Cost - Historical cost is the cost to the original purchaser. If the original purchaser still retains ownership, this is the cost which is carried on the fixed asset ledger of the company. Refer to definitions in Listing Section Original Cost - Original cost is the cost to the current owner. It will be the cost in the fixed asset ledgers. If the current owner is the original owner, then historical cost and original cost will be the same. Refer to definitions in Classification Section

Slide 14

Slide 15

Valuation – Machinery and Equipment IPT Personal Property Tax School

6

When entire businesses are acquired, often the assets of the business will be increased or decreased to reflect the value of the entire business. These revised costs are known as Stepped Up or Stepped Down Costs.

Types of Depreciation

Physical Depreciation(also known as Physical Deterioration) - is the loss in

value due to wear and tear. An example would be the tires of an automobile. As the vehicle is driven, the tires wear to a point where they need to be replaced. Physical deterioration is “an element of accrued depreciation” and may be either curable or incurable. (Appraisal Institute, 1993, p. 265)

Sources & Causes

Age - When valuing property, age can refer to physical (actual) age or effective age.

Actual Age - Actual age is the physical time period that has passed since the asset was acquired or constructed.

Effective Age - Effective age is the estimated age that the asset is displaying. The effective age can be greater or less than the actual age of the asset.

Use - If a property is heavily used, it may wear quicker than a property in normal use. Equipment that runs year round 24 hours a day may not wear at the same rate as equipment only run 5 days a week for 8 hours as day.

Slide 16

Intermediate Personal Property Tax S chool

Types of Depreciation

Physical Depreciation

Functional Obsolescence

External Obsolescence

Depreciation from all three sources is referred to as an asset’s Accrued Depreciation

Slide 17

Intermediate Personal Property Tax S chool

Physical Depreciation

Loss in value due to physical wear and tear during usage and/or from the forces of nature.

Physical Depreciation is also known as Physical Deterioration

Slide 18

Intermediate Personal Property Tax S chool

Causes & Sources ofPhysical Depreciation

Age – Actual versus Effective

Frequency of Operating Usage

Regular or Deferred Maintenance

Exposure to Elements

IPT Personal Property Tax School Valuation – Machinery and Equipment

7

Maintenance - If a maintenance schedule is not adhered to or is loosely followed, it may have an effect on the wear and tear of the property. Action of the Elements - This is the result of the effects of mother nature or effects of a hostile environment. Other Physical Factors - These are other actions, intentional or unintentional, that affect the physical condition of property. One example would be damage sustained to a machine from a fork lift striking it.

Curable vs. Incurable

Curable - This is deterioration that is economically feasible to cure, because the value of the property added by the cure exceeds the cost of the cure. In addition, the cure will generally extend the life of the property or enable the property to complete its life as expected. An example would be the replacing of worn tires on an automobile. Usually, the addition of the tires will extend the life of the asset, and the cost of the repair does not exceed the value added by the repair. Curable physical deterioration is “a curable defect caused by deferred maintenance.” (Appraisal Institute, 1993, p. 86)

Slide 19

Intermediate Personal Property Tax S chool

Physical DepreciationCurable vs. Incurable

– Curable deterioration is economicallyfeasible to cure through repair or replacement since the value added by the cure exceeds the cost of the cure.

– Incurable deterioration is not economicallyfeasible to cure through repair or replacement since the value added by the cure does not exceed the cost of the cure.

Valuation – Machinery and Equipment IPT Personal Property Tax School

8

Incurable - This is deterioration that is not economically feasible to cure since the value added by the cure does not exceed its cost. An example is an old vehicle that may only be worth $500. If it were to require a new or rebuilt engine that would cost $1,500, the cost to cure would exceed the value of the vehicle. Although the cure would extend the life of the vehicle, other factors may not justify the expense. Incurable physical deterioration is “a defect caused by physical deterioration that cannot be practically or economically corrected.” (Appraisal Institute, 1993, p. 180)

Methods of Calculation

Straight-line – uniform annual depreciation based on age of property vs. expected life.

Slide 20

Intermediate Personal Property Tax S chool

Methods of Calculating Physical Depreciation

Straight-line percentage based on age

Actual lump sum cost to cure

Age/Life percentage based on condition

Slide 21

Intermediate Personal Property Tax S chool

Straight Line Depreciation

Straight line depreciation is calculated by spreading the cost of an asset out over its useful life in uniform increments.

Example:

An asset deemed to have a useful life of 15 years would receive 6.6% depreciation per year over this period.

Note: This method does not mirror the motivations and actions of buyers and sellers in determining fair market value.

IPT Personal Property Tax School Valuation – Machinery and Equipment

9

Actual cost to cure – determine cost to cure defect, such as cost to replace worn out gears.

Age/Life Method

Total Economic Life - period of anticipated profitable use of the property. Effective Age - Effective age is the estimated age that the asset is displaying. The effective age can be greater or less than the actual age of the asset.

Age / Life Example 1 Age/ Life Example 2

Slide 22

Intermediate Personal Property Tax S chool

Age/Life Depreciation

Physical DPR = EA ÷ TEL

EA = Effective Age of property

TEL = Total expected Economic Life

Slide 23

Intermediate Personal Property Tax S chool

Age/Life Example 1

A pneumatic press that is 7 years old has an estimated economic life of 20 years. Due to superior maintenance, the estimated effective age of the press is only 5 years. What is the amount of accrued physical deterioration?

Actual Age = 7 years, Effective Age = 5 yearsTotal Economic Life = 20 years

Physical = 5 / 20 = 25%

Slide 24

Intermediate Personal Property Tax S chool

Age/Life Example 2 A computer controlled robotic arm is

expected to operate for 5 years. After

3 years the owner upgraded the computer controls, which eliminated 50% of the

asset’s depreciation. What is the actual

age and effective age of the asset?

Actual Age: (3 EA/5 TEL) = 60%

Effective Age: (60% Old Dpr x 50% Reduced Dpr) x 5 years = 1.5 years.

Valuation – Machinery and Equipment IPT Personal Property Tax School

10

Cost Approach Example 1 Cost Approach Example 2 Advanced Depreciation Concepts

Slide 25

Intermediate Personal Property Tax S chool

Cost Approach Example 1

The cost new of a K32 front-end loader is $200,000. The total economic life is 15 years. The subject K32 front end loader has an effective age of 5 years. What is the value of the asset based on the cost approach?

RCN $200,000

D (5 EA/15 TEL = .33) $200,000 x.33 -$66,000

RCN-D $134,000

Slide 26

Intermediate Personal Property Tax S chool

Cost Approach Example 2The current cost new of a milling machine is $90,000. It cost $5,500 to install. The current sales tax rate is 5%. We have a milling machine that has a total accrued depreciation of 20%. What is the RCNLD of our asset?

Cost $90,000

Installation +5,500

Sales tax (90,000 x .05) +4,500

RCN $100,000

Depreciation (100,000 x .20) -20,000

RCNLD $80,000

Slide 27

Intermediate Personal Property Tax S chool

Advanced Depreciation Concepts

In addition to physical deterioration, there are two other forms of depreciation to be considered in the valuation process:

Functional Obsolescence

External Obsolescence

Note: Assessors do not generally apply obsolescence unless it is brought to their attention by the taxpayer

IPT Personal Property Tax School Valuation – Machinery and Equipment

11

Functional Obsolescence is “an element of accrued depreciation resulting from deficiencies or superadequacies in the structure.” (Appraisal Institute, 1993, p. 154) Similar to physical deterioration, it may be either curable or incurable.

External obsolescence is “an element of accrued depreciation; a defect, usually incurable, caused by negative influences outside a site and generally incurable on the part of the owner, landlord, or tenant” (Appraisal Institute, 1993, p. 128). The most severe external obsolescence results in plant closure or business termination due to slack markets, excessive expenses or excessive investment to meet government standards.

Both functional and external obsolescence will be discussed in greater detail in another section this week.

Sales Comparison Approach

The three types of depreciation are inherently captured in this approach: Physical, Functional, and External.

Slide 28

Intermediate Personal Property Tax S chool

Functional Obsolescence

Loss in value due to the inability of the asset to perform adequately the function for which it is used - can be considered a deficiency or a super-adequacy.

Example

A nail manufacturing unit cannot run at full capacity due to a lower-rated sorter at the end of the line.

Slide 29

Slide 30

Intermediate Personal Property Tax S chool

Sales Comparison Approach The value of an asset is estimated based on

adjusted sale prices of similar assets. Adjusted asking prices for similar assets are also instructive.

Based primarily on the principle of supply and demand and the principle of substitution.

The question to be answered is, “What does the market indicate as a reasonable value for the asset?”

Valuation – Machinery and Equipment IPT Personal Property Tax School

12

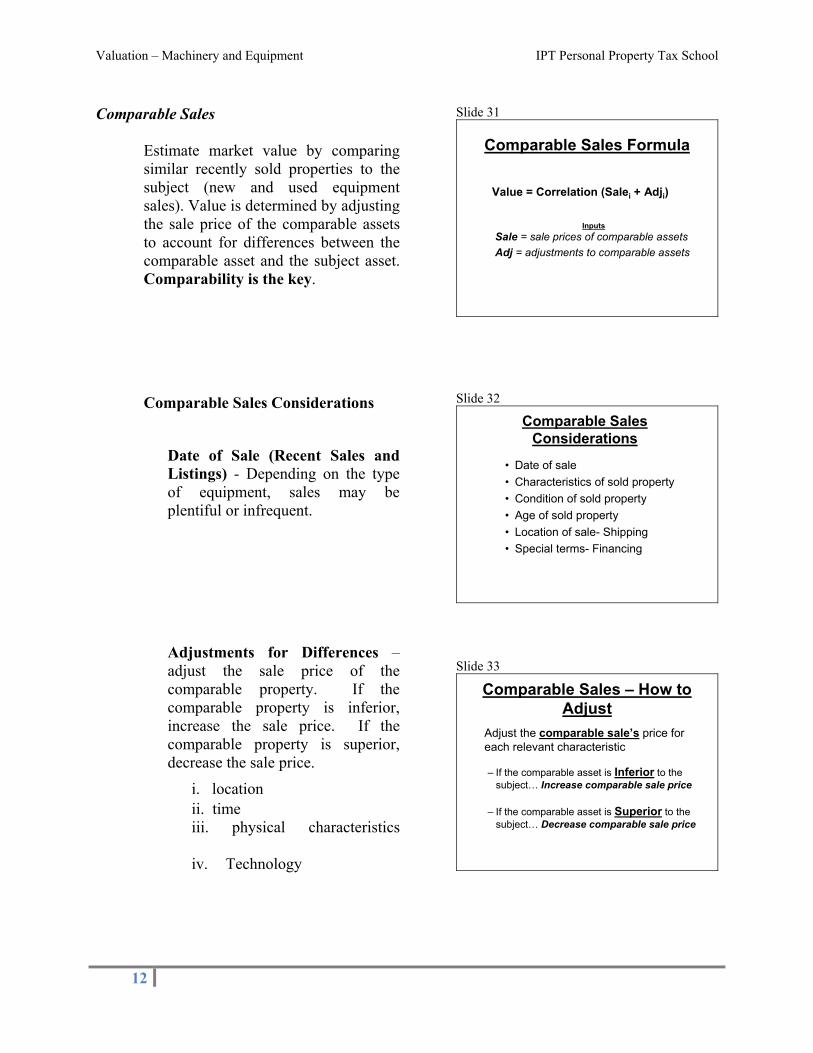

Comparable Sales

Estimate market value by comparing similar recently sold properties to the subject (new and used equipment sales). Value is determined by adjusting the sale price of the comparable assets to account for differences between the comparable asset and the subject asset. Comparability is the key.

Comparable Sales Considerations

Date of Sale (Recent Sales and Listings) - Depending on the type of equipment, sales may be plentiful or infrequent.

(a nuclear power plant or coal dragline sale vs. a personal computer sale)

Adjustments for Differences – adjust the sale price of the comparable property. If the comparable property is inferior, increase the sale price. If the comparable property is superior, decrease the sale price.

i. location ii. time iii. physical characteristics (size) iv. Technology (throughput, automated vs. mechanical, utility usage)

Slide 31

Intermediate Personal Property Tax S chool

Comparable Sales Formula

Value = Correlation (Salei + Adji)

Inputs

Sale = sale prices of comparable assets

Adj = adjustments to comparable assets

Slide 32

Intermediate Personal Property Tax S chool

Comparable Sales Considerations

• Date of sale

• Characteristics of sold property

• Condition of sold property

• Age of sold property

• Location of sale- Shipping

• Special terms- Financing

Slide 33

Intermediate Personal Property Tax S chool

Comparable Sales – How to Adjust

Adjust the comparable sale’s price for each relevant characteristic

– If the comparable asset is Inferior to the subject… Increase comparable sale price

– If the comparable asset is Superior to the subject… Decrease comparable sale price

IPT Personal Property Tax School Valuation – Machinery and Equipment

13

Income Approach

The income approach is based on estimating market value by calculating the present worth of future benefits (income). It takes into consideration both the rate of return ON the investment, which is the yield or profit and the rate of return OF the investment which is the recovery of invested capital.

Direct Capitalization - This method extracts a capitalization rate from market transactions when the sale price and income of the property are known. It uses a simple formula known as IRV. Each element of the formula stands for one of the three elements which make up the direct capitalization method. I - Annual Net Operating Income, R - Capitalization Rate and V - Market Value. The formula is interchangeable and can be written in the forms I / R=V, R x V=I, I / V = R. Having knowledge of any two of the elements, the third can be determined using the IRV formula. This method is best suited when the income stream is fairly constant from year to year.

Slide 34

Intermediate Personal Property Tax S chool

Income Approach

The value of an asset is represented by the present worth of future financial benefits derived from ownership.

Based primarily on the principle of anticipation and the principle of substitution.

The question to answer is, “What is an investor willing to pay for an asset today in order to obtain annual rental income over future years?”

Slide 35

Intermediate Personal Property Tax S chool

Income Approach Methods

Direct Capitalization

Discounted Cash Flow

Slide 36

Valuation – Machinery and Equipment IPT Personal Property Tax School

14

Direct Capitalization Examples:

Slide 37

Slide 38

Slide 39

IPT Personal Property Tax School Valuation – Machinery and Equipment

15

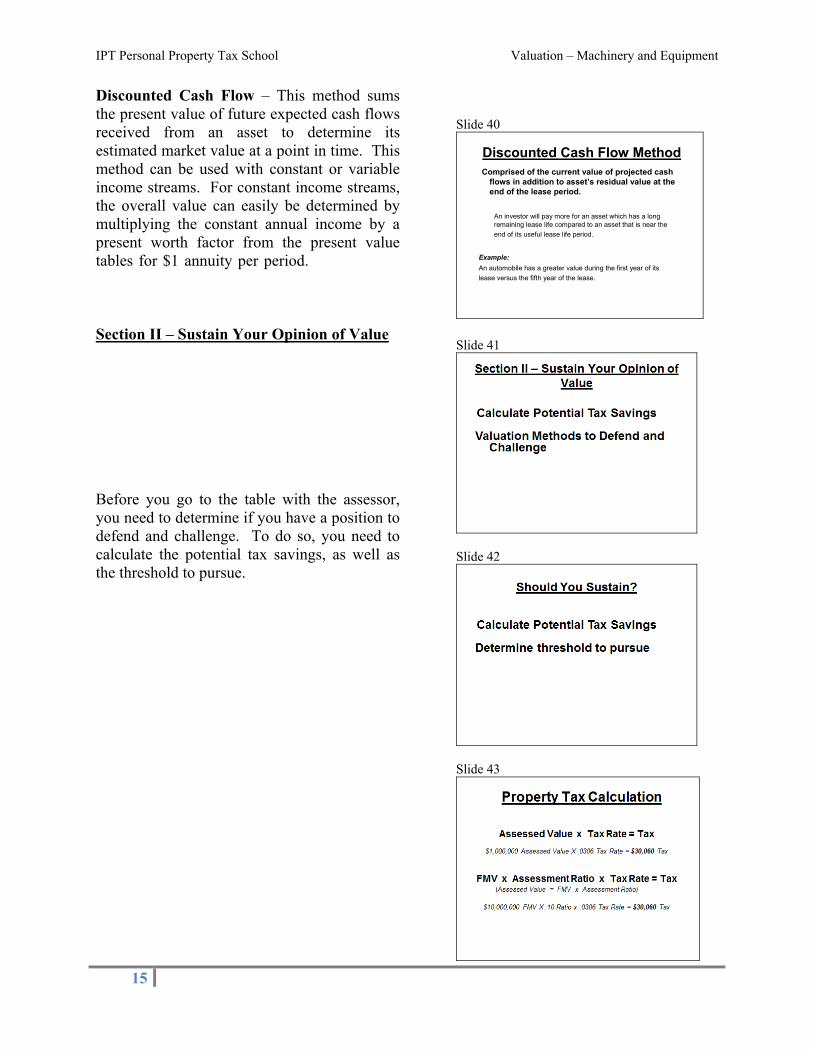

Discounted Cash Flow – This method sums the present value of future expected cash flows received from an asset to determine its estimated market value at a point in time. This method can be used with constant or variable income streams. For constant income streams, the overall value can easily be determined by multiplying the constant annual income by a present worth factor from the present value tables for $1 annuity per period. (See present value table exhibit at the end of Student Reference Manual.) Section II – Sustain Your Opinion of Value With respect to the three approaches to value, in practice most assessors estimate market value by applying the cost approach. Before you go to the table with the assessor, you need to determine if you have a position to defend and challenge. To do so, you need to calculate the potential tax savings, as well as the threshold to pursue.

Slide 40

Intermediate Personal Property Tax S chool

Discounted Cash Flow MethodComprised of the current value of projected cash

flows in addition to asset’s residual value at the end of the lease period.

An investor will pay more for an asset which has a long remaining lease life compared to an asset that is near the

end of its useful lease life period.

Example:

An automobile has a greater value during the first year of its

lease versus the fifth year of the lease.

Slide 41

Slide 42

Slide 43

Valuation – Machinery and Equipment IPT Personal Property Tax School

16

Now that you have your tax savings calculated, you can determine if it fits within the threshold to defend. Is this savings significant? What is the savings vs. your cost to defend? Does your client have a taste to pursue beyond administrative hearings?

Slide 44

Slide 45

Slide 46

IPT Personal Property Tax School Valuation – Machinery and Equipment

17

Section III – Sustain Your Opinion of Value Value Positions to Challenge and Defend Cost

1. Company booked costs

Historical vs. original vs. stepped up costs. 2. Industry Costs or Published Costs 3. Exclude (when allowable) Installation, Freight, Sales Tax

Classification

1. Moving assets to shorter life categories 2. Moving assets to non-taxable categories

Useful life

1. Disposal records 2. Industry Studies 3. In-house experts and suppliers

Trend Factors in Cost Approach

1. Cost Indexes sources

Depreciation

1. Percent good / depreciation factor 2. Residual percentage good (Floor percentage)

3. Actual and effective age 4. Customized Depreciation Tables 5. Include calculations for Obsolescence

Slide 47

Slide 48

Slide 49

Slide 50

Valuation – Machinery and Equipment IPT Personal Property Tax School

18

Market Data to Supplement Cost Approach

1. Challenge cost approach using market approach

a. similar equipment from various suppliers b. equipment pricing guides c. liquidation advertisements and industrial periodicals

2. Challenge cost approach using income approach

a. income and expenses b. capitalization rate

Uniformity

1. Equipment of like kind 2. Compare to other jurisdictions 3. Compare to competitors

(When checking uniformity, check costs used, depreciation allowed and where applicable level of assessments.)

Slide 51

Slide 52

Slide 53

Slide 54

IPT Personal Property Tax School Valuation – Machinery and Equipment

19

By the conclusion of this cornerstone, you should understand the basic fundamentals of valuation and how to apply the three approaches of valuation to personal property. Specifically, you should understand how to apply the cost approach to the valuation of machinery and equipment. And finally, you can calculate your potential tax savings and apply valuation methods to defend and challenge your value to the assessor.

Slide 55

Slide 56

Slide 57

Valuation – Machinery and Equipment IPT Personal Property Tax School

20

NOTES