Embed Size (px)

Citation preview

Copyright The Asian Banker 2009. All rights reserved 1

The Asian Banker

Discussion Point

“Avoiding the Icelandic crisis – the Asian response”

Emmanuel DanielPresident & CEOThe Asian Banker

Copyright The Asian Banker 2009. All rights reserved 2

I hope to discuss…

• The Icelandic crisis

• The evolution of the financial services industry

• The changing nature of the largest and strongest financial institutions

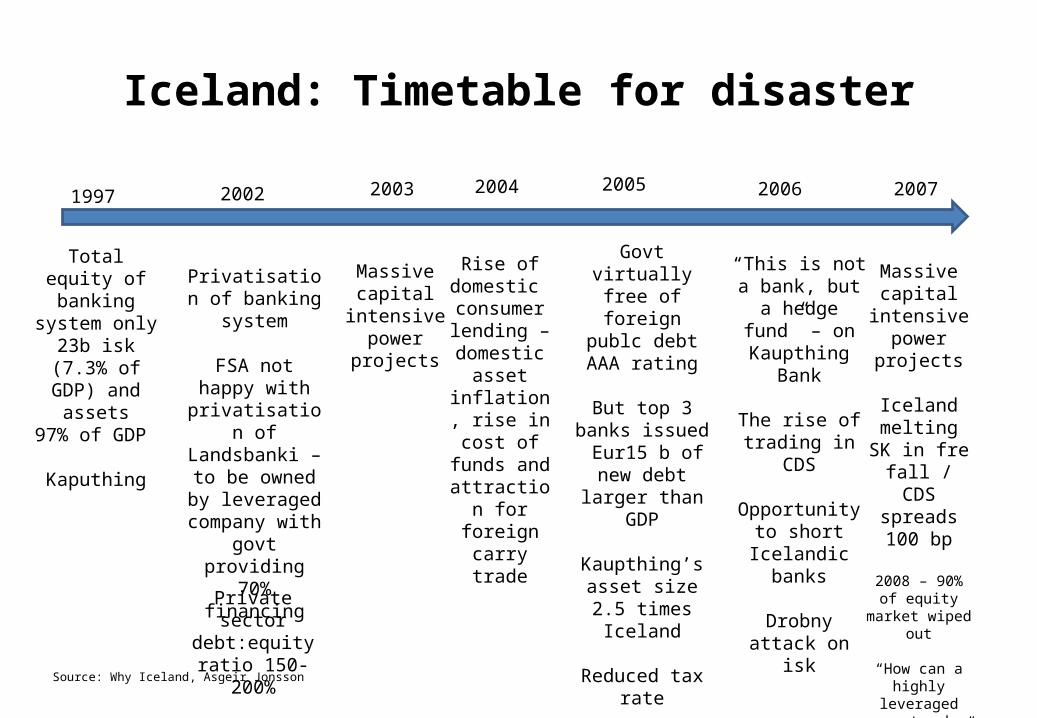

Iceland: Timetable for disaster

1997

Total equity of banking

system only 23b isk (7.3% of GDP) and

assets97% of GDP

Kaputhing

2005

Govt virtually free of foreign

publc debt AAA rating

But top 3 banks issued Eur15 b

of new debt larger than GDP

Kaupthing’s asset size 2.5 times Iceland

Reduced tax rate

Equity market booming

Glacier bonds

Private sector debt:equity ratio

150-200%

20032002

Privatisation of banking system

FSA not happy with

privatisation of Landsbanki – to

be owned by leveraged

company with govt providing 70% financing

2006

“This is not a bank, but a

hedge fund” – on Kaupthing

Bank

The rise of trading in CDS

Opportunity to short Icelandic

banks

Drobny attack on isk

Massive capital

intensive power

projects

2004

Rise of domestic consumer lending – domestic

asset inflation, rise

in cost of funds and

attraction for foreign carry

trade

2007

Massive capital

intensive power

projects

Iceland melting

SK in fre fall / CDS

spreads 100 bp

2008 – 90% of equity market

wiped out

“How can a highly leveraged country be AAA

rated?”Source: Why Iceland, Asgeir Jonsson

Copyright The Asian Banker 2009. All rights reserved 4

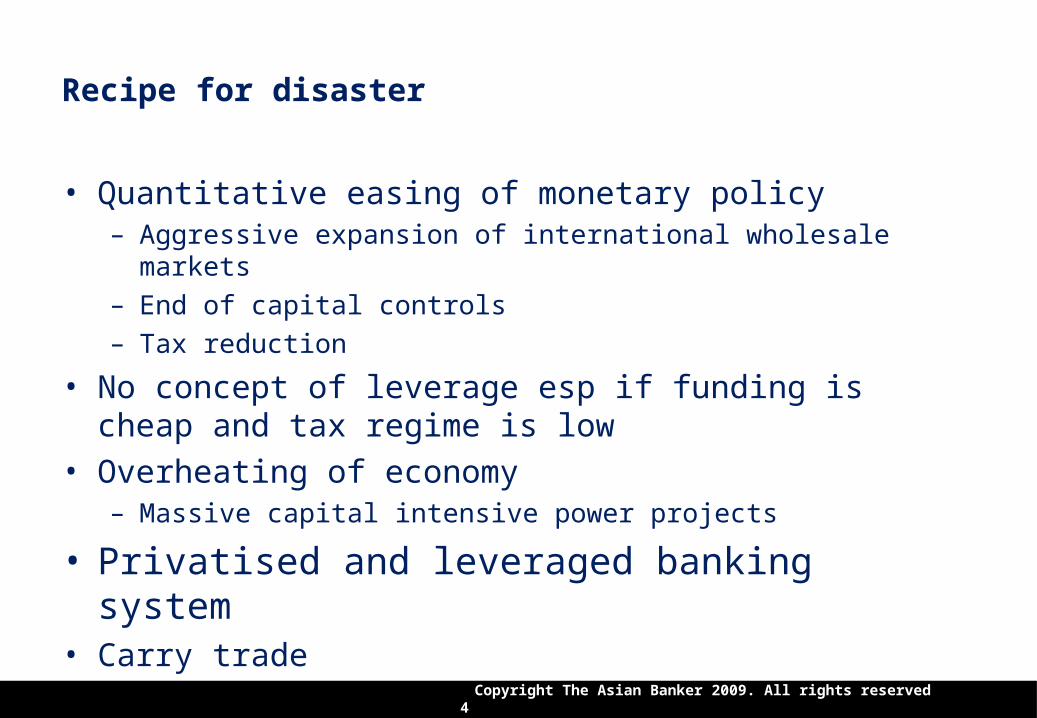

Recipe for disaster

• Quantitative easing of monetary policy– Aggressive expansion of international wholesale markets– End of capital controls– Tax reduction

• No concept of leverage esp if funding is cheap and tax regime is low

• Overheating of economy– Massive capital intensive power projects

• Privatised and leveraged banking system• Carry trade

Copyright The Asian Banker 2009. All rights reserved 5

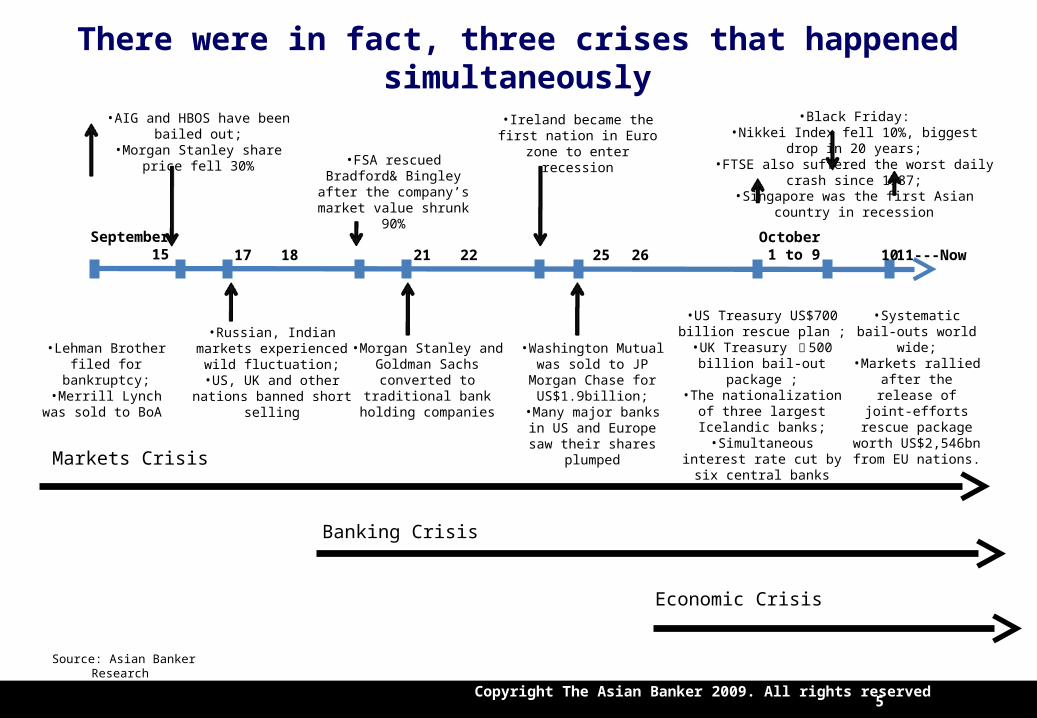

September 15 17 18 21 22 25 26

October 1 to 9 10 11---Now

•Lehman Brother filed for bankruptcy;

•Merrill Lynch was sold to BoA

•AIG and HBOS have been bailed out;

•Morgan Stanley share price fell 30%

•Russian, Indian markets experienced wild

fluctuation;•US, UK and other nations

banned short selling

•FSA rescued Bradford& Bingley after the company’s market value shrunk 90%

•Morgan Stanley and Goldman Sachs converted to traditional bank holding

companies

•Ireland became the first nation in Euro zone to enter

recession

•Washington Mutual was sold to JP Morgan Chase

for US$1.9billion;•Many major banks in US

and Europe saw their shares plumped

•US Treasury US$700 billion rescue plan ;

•UK Treasury £ 500 billion bail-out package ;

•The nationalization of three largest Icelandic banks;

•Simultaneous interest rate cut by six central banks

•Black Friday:•Nikkei Index fell 10%, biggest drop in 20 years;•FTSE also suffered the worst daily crash since

1987;•Singapore was the first Asian country in

recession

•Systematic bail-outs world wide;

•Markets rallied after the release of joint-

efforts rescue package worth

US$2,546bn from EU nations.

There were in fact, three crises that happened simultaneously

Source: Asian Banker Research

Markets Crisis

Banking Crisis

Economic Crisis

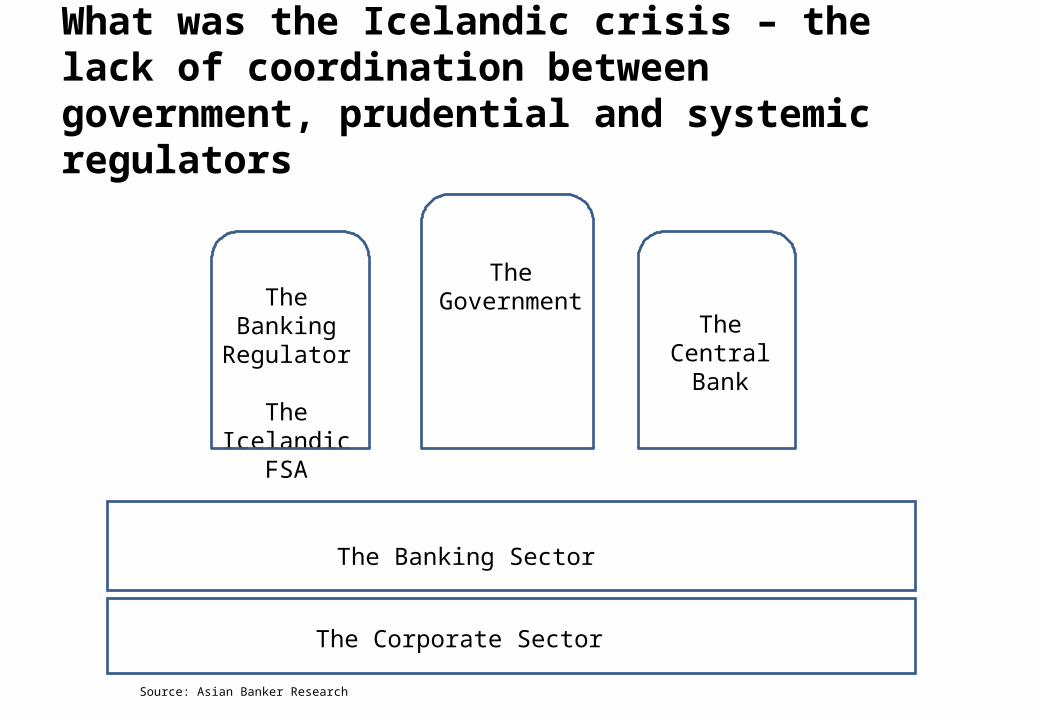

What was the Icelandic crisis – the lack of coordination between government, prudential and systemic regulators

The Banking Regulator

The Icelandic FSA

The Government

The Central Bank

The Banking Sector

The Corporate Sector

Source: Asian Banker Research

Copyright The Asian Banker 2009. All rights reserved 7

The relationship between the government, prudential and systemic regulators is so different in each country

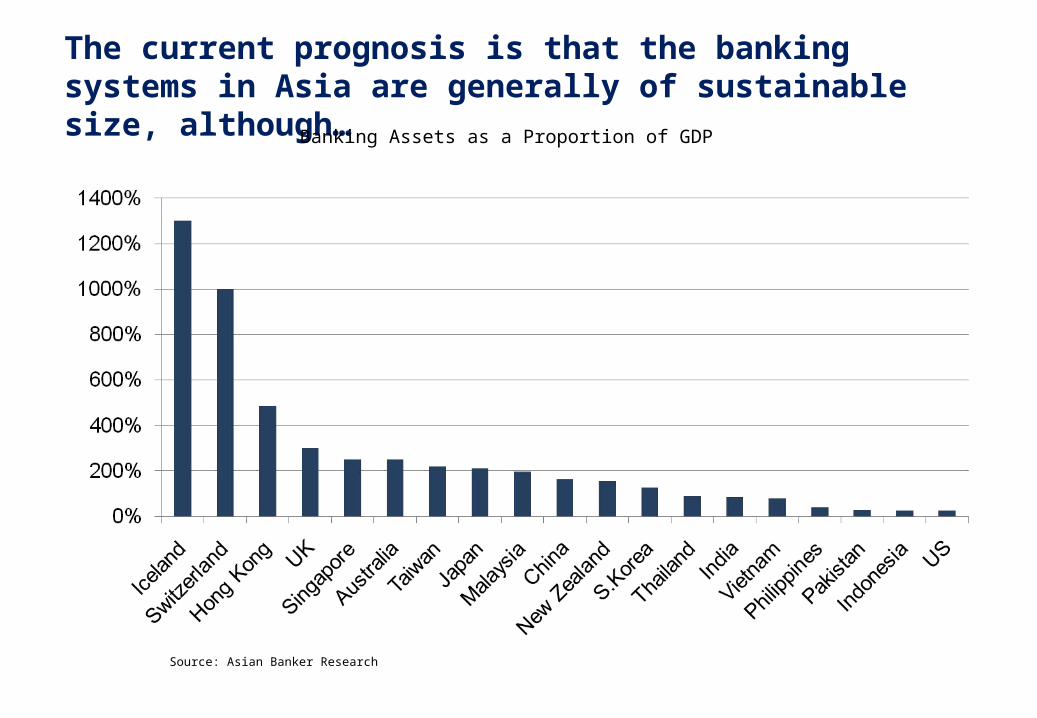

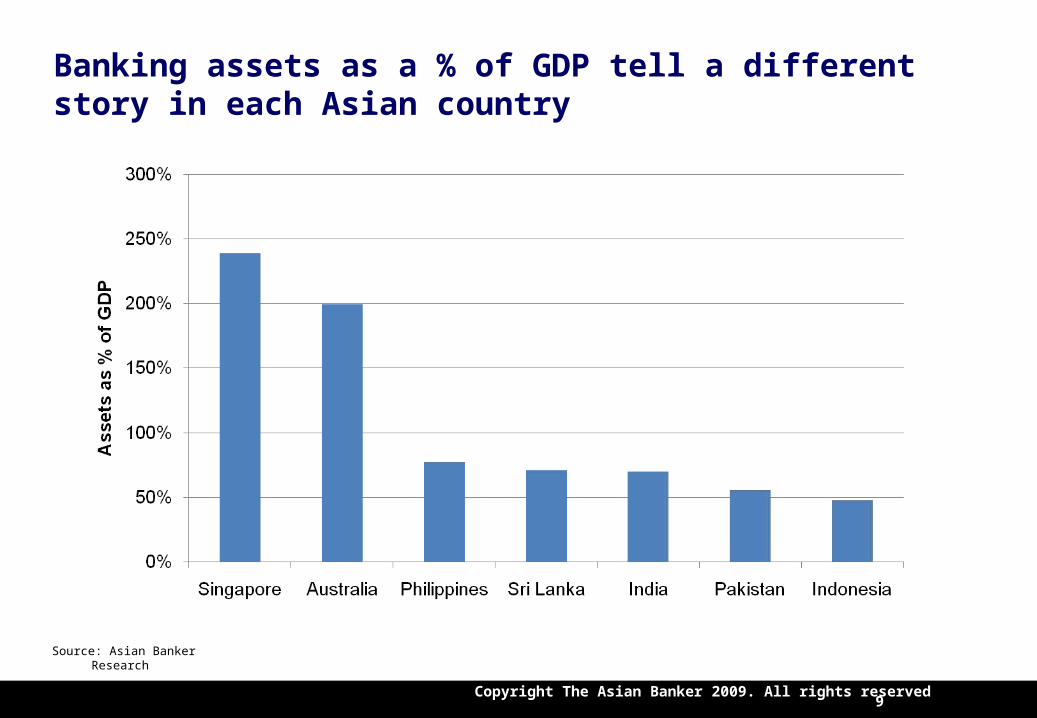

The current prognosis is that the banking systems in Asia are generally of sustainable size, although…

Banking Assets as a Proportion of GDP

Source: Asian Banker Research

Copyright The Asian Banker 2009. All rights reserved 9

Banking assets as a % of GDP tell a different story in each Asian country

Source: Asian Banker Research

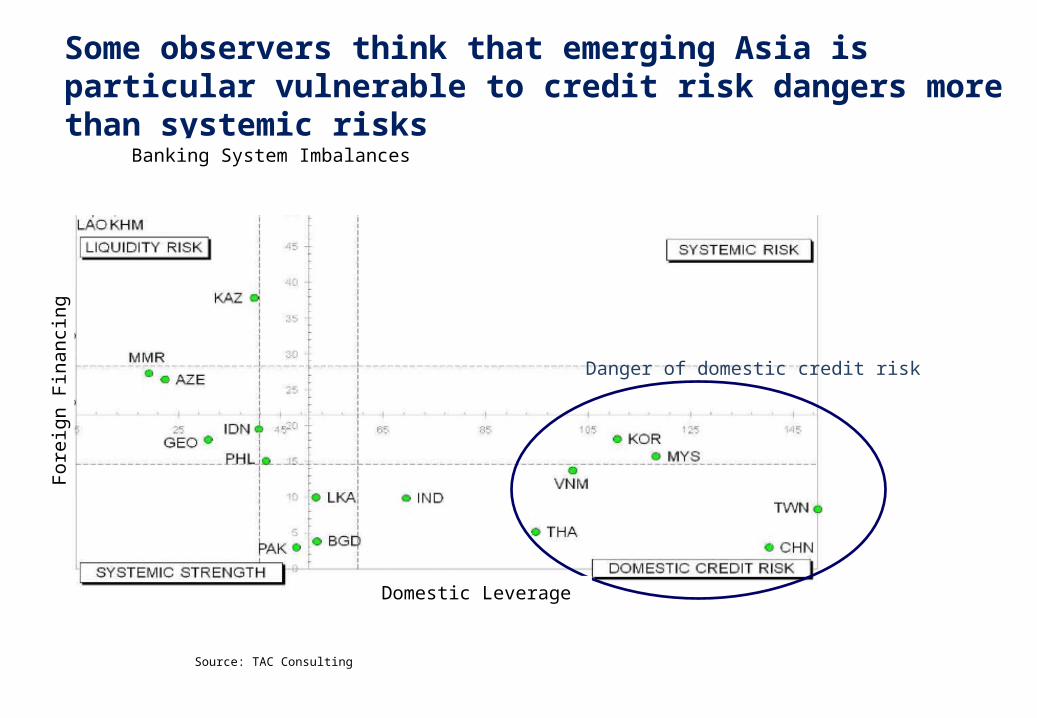

Some observers think that emerging Asia is particular vulnerable to credit risk dangers more than systemic risks

Danger of domestic credit risk

Banking System Imbalances

Domestic Leverage

For

eign

Fin

anci

ng

Source: TAC Consulting

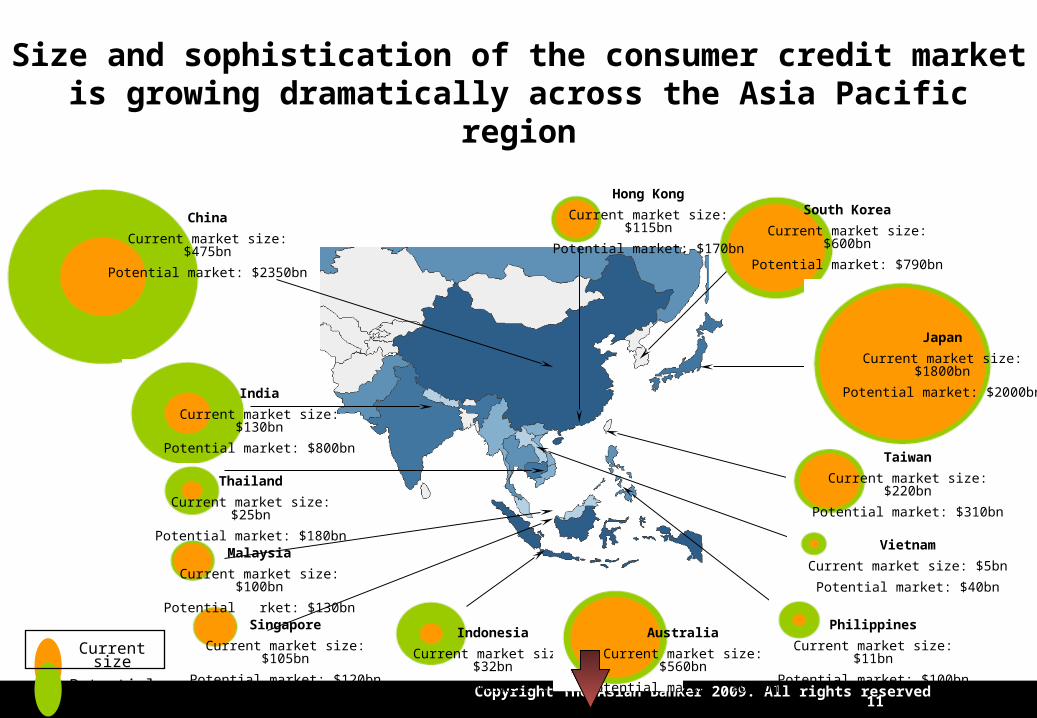

Copyright The Asian Banker 2009. All rights reserved 11 Source: Asian Banker Research

Current size

Potential size

Size and sophistication of the consumer credit market is growing dramatically across the Asia Pacific region

Thailand

Current market size: $25bn

Potential market: $180bn

Malaysia

Current market size: $100bn

Potential market: $130bn

Hong Kong

Current market size: $115bn

Potential market: $170bn

South Korea

Current market size: $600bn

Potential market: $790bn

India

Current market size: $130bn

Potential market: $800bn

Singapore

Current market size: $105bn

Potential market: $120bn

Indonesia

Current market size: $32bn

Potential market: $300bn

Philippines

Current market size: $11bn

Potential market: $100bn

Vietnam

Current market size: $5bn

Potential market: $40bn

Taiwan

Current market size: $220bn

Potential market: $310bn

Japan

Current market size: $1800bn

Potential market: $2000bn

China

Current market size: $475bn

Potential market: $2350bn

Australia

Current market size: $560bn

Potential market: $650bn

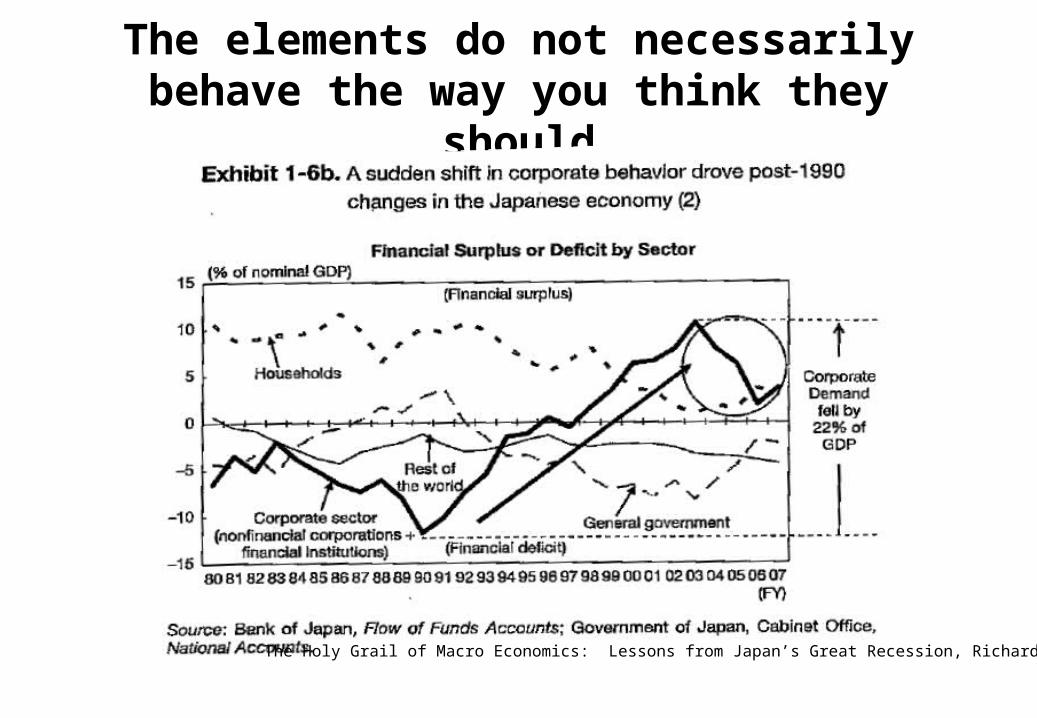

The elements do not necessarily behave the way you think they should

The Holy Grail of Macro Economics: Lessons from Japan’s Great Recession, Richard Koo

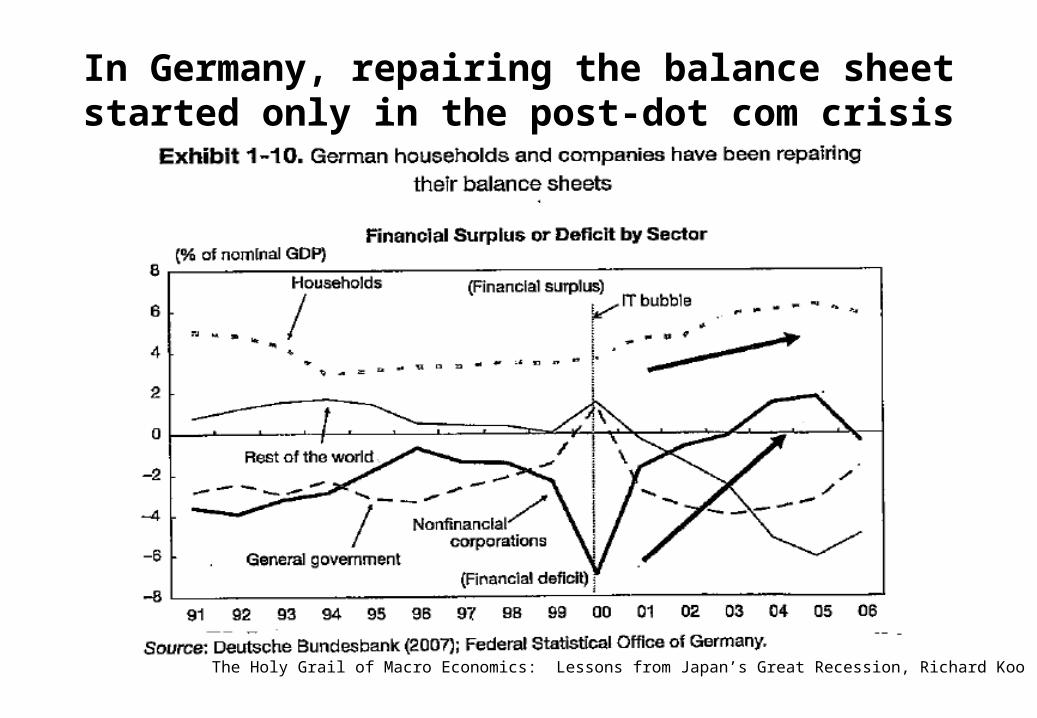

In Germany, repairing the balance sheet started only in the post-dot com crisis

The Holy Grail of Macro Economics: Lessons from Japan’s Great Recession, Richard Koo

Basel II was neither the cause nor the solution to the current crisis although weaknesses were exposed

Basel II implementation failures on parts of supervisors and banks, in particular the gap between best practices and actual practices.

‘Dynamic Provisioning’ in form of counter cyclical buffers in.

Formation of larger Asian supervisory colleges.

Tightened regulations in the treatment of off-balance sheet items and fair value accounting practices.

Reversion of mark-to-market accounting - Is MTM an improvement in the transparency of bank accounting?/ Does it reflect the intrinsic value to a bank of a loan or securities.

Source: Asian Banker Research

Copyright The Asian Banker 2009. All rights reserved 15

Source: Asian Banker Research

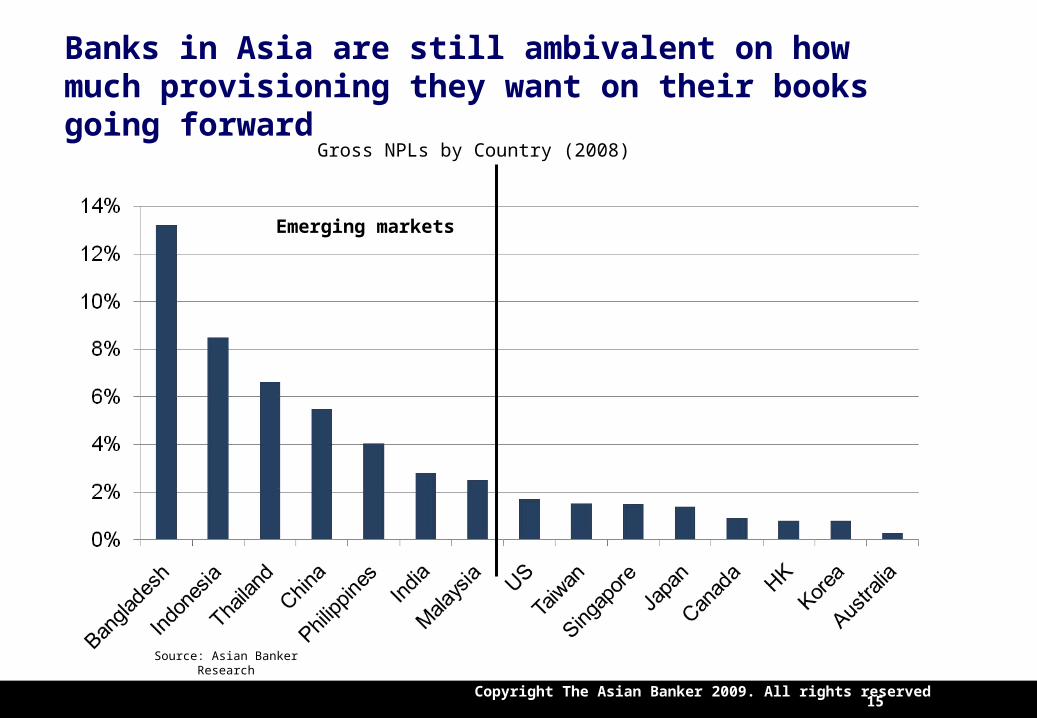

Banks in Asia are still ambivalent on how much provisioning they want on their books going forward

Gross NPLs by Country (2008)

Emerging markets

Copyright The Asian Banker 2009. All rights reserved 16

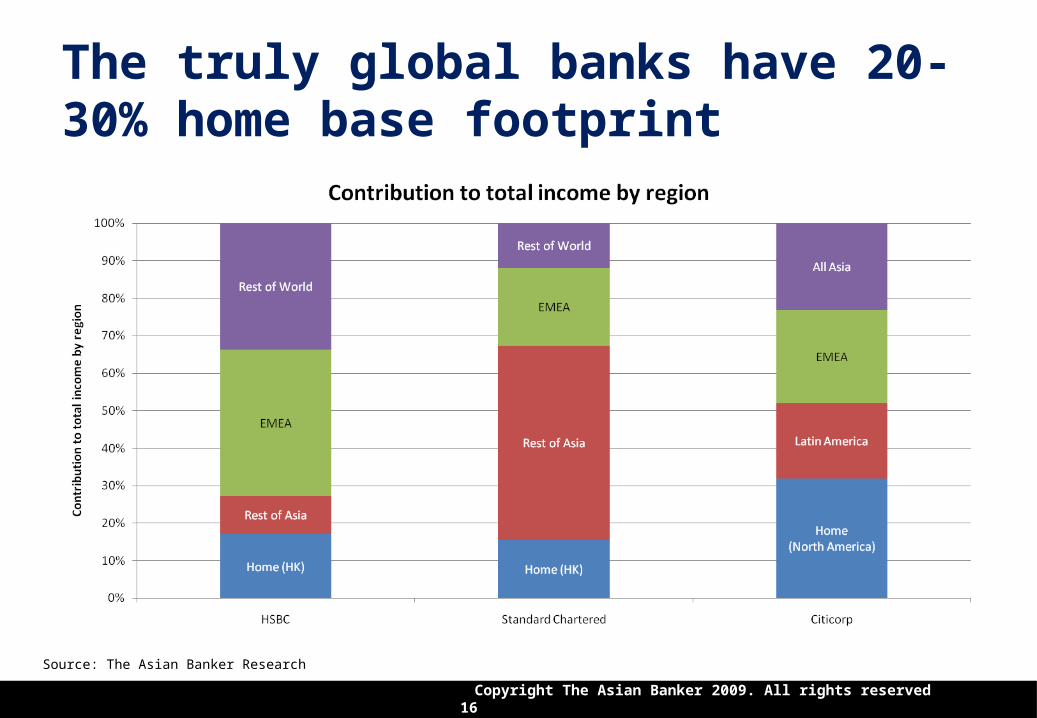

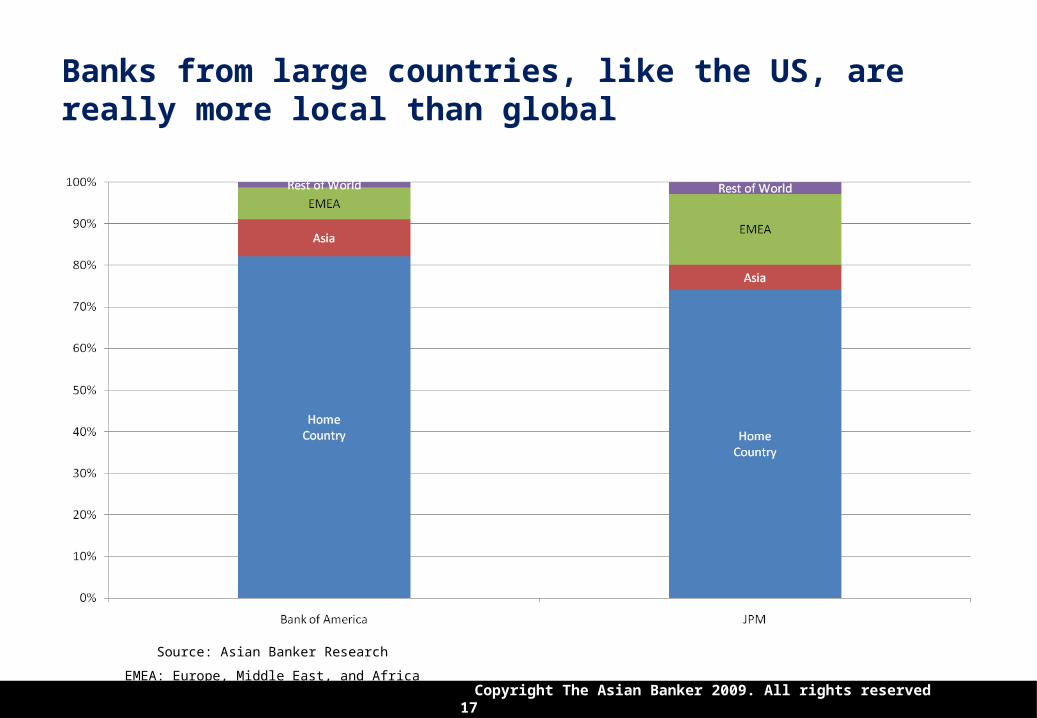

The truly global banks have 20-30% home base footprint

Source: The Asian Banker Research

Copyright The Asian Banker 2009. All rights reserved 17

Banks from large countries, like the US, are really more local than global

Source: Asian Banker Research

EMEA: Europe, Middle East, and Africa

Copyright The Asian Banker 2009. All rights reserved 18

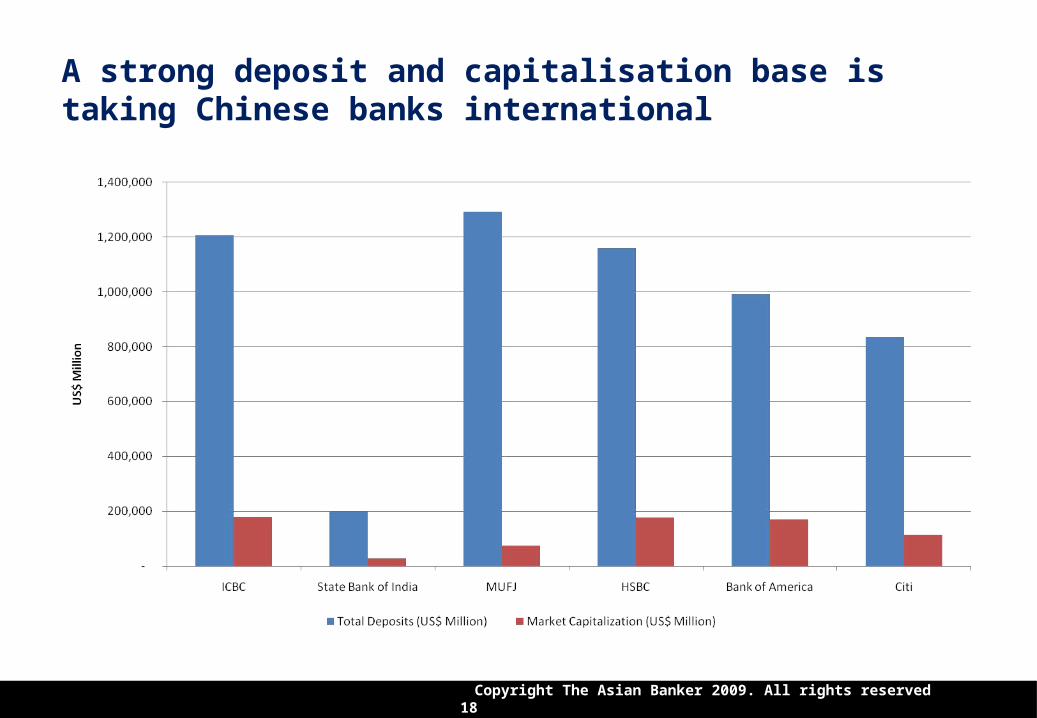

A strong deposit and capitalisation base is taking Chinese banks international

Copyright The Asian Banker 2009. All rights reserved 19

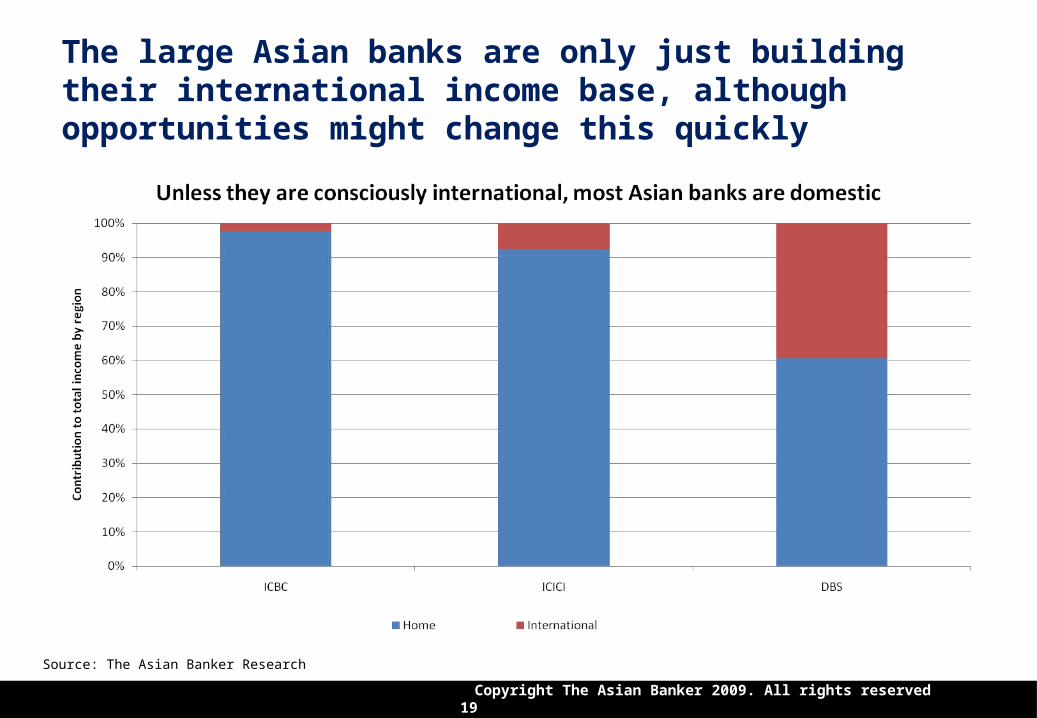

The large Asian banks are only just building their international income base, although opportunities might change this quickly

Source: The Asian Banker Research

Copyright The Asian Banker 2009. All rights reserved 20

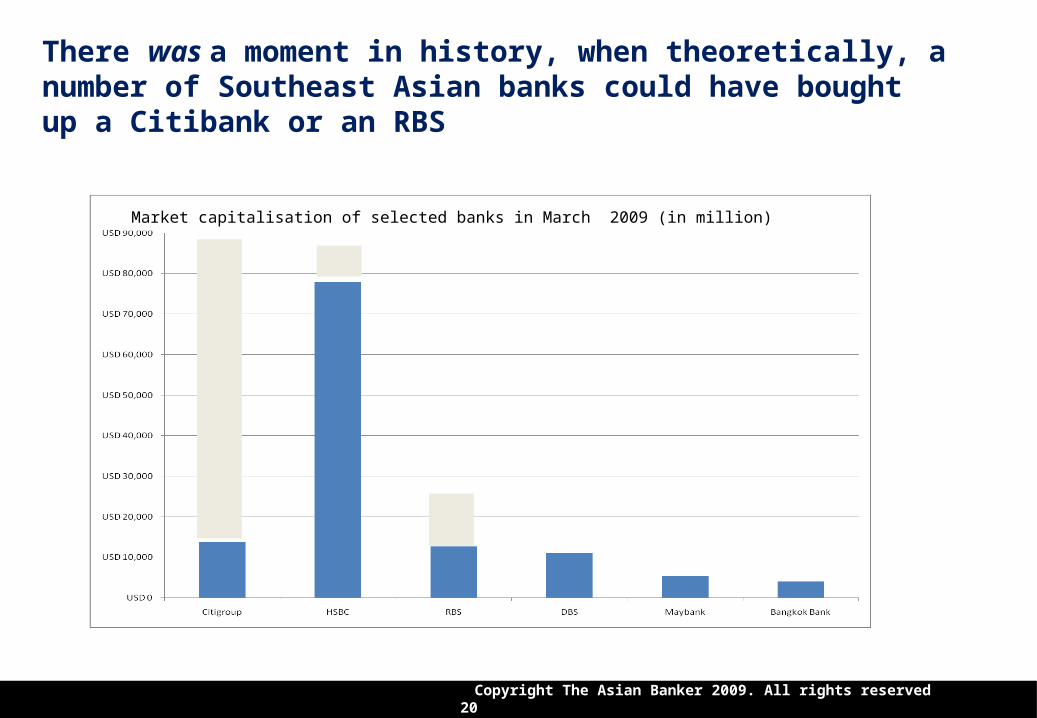

There was a moment in history, when theoretically, a number of Southeast Asian banks could have bought up a Citibank or an RBS

Market capitalisation of selected banks in March 2009 (in million)

Copyright The Asian Banker 2009. All rights reserved 21

Developing themes that could shape the safety of the financial industry, globally

• Price destruction on every product

• Inflation-independent “asset appreciation”

• Deleveraging

• Government stimulus write-downs

Financial services may become safer if reduced to regulated utilities

Copyright The Asian Banker 2009. All rights reserved 22

Subterfuge and more subterfuge

“I had 100-200 PhD’s at my disposal, and even I did not know what was going on”

- Alan Greenspan, on CNBC in March 2009