Embed Size (px)

Citation preview

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

Flexible Budgets,Overhead Cost Variances,

andManagement Control

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

1. Explain the similarities and differences in planning variable and fixed overhead costs

2. Develop budgeted variable and fixed overhead cost rates

3. Compute the variable overhead flexible-budget variance, the variable overhead efficiency variance and the variable overhead spending variance

4. Compute the fixed overhead flexible-budget variance, the fixed overhead spending variance and the fixed overhead production-volume variance

8-2

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

5. Show how the 4-variance analysis approach reconciles the actual overhead incurred with the overhead amounts allocated during the period

6. Explain the relationship between the sales-volume variance and the production-volume variance

7. Calculate variances in activity-based costing

8. Examine the use of overhead variances in nonmanufacturing settings

8-3

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

To effectively plan variable overhead costs, managers should focus on activities that add value and eliminate those that do not.

Fixed overhead planning is similar ~ plan only for essential activities and plan to be as efficient as possible.

8-4

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

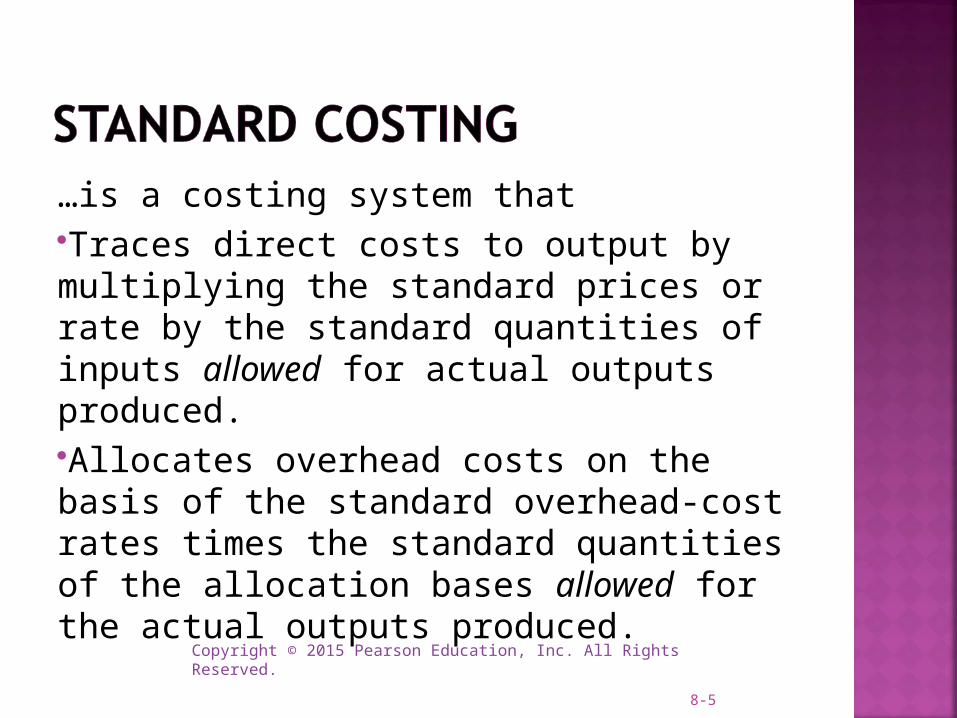

…is a costing system thatTraces direct costs to output by multiplying the standard prices or rate by the standard quantities of inputs allowed for actual outputs produced.Allocates overhead costs on the basis of the standard overhead-cost rates times the standard quantities of the allocation bases allowed for the actual outputs produced.

8-5

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

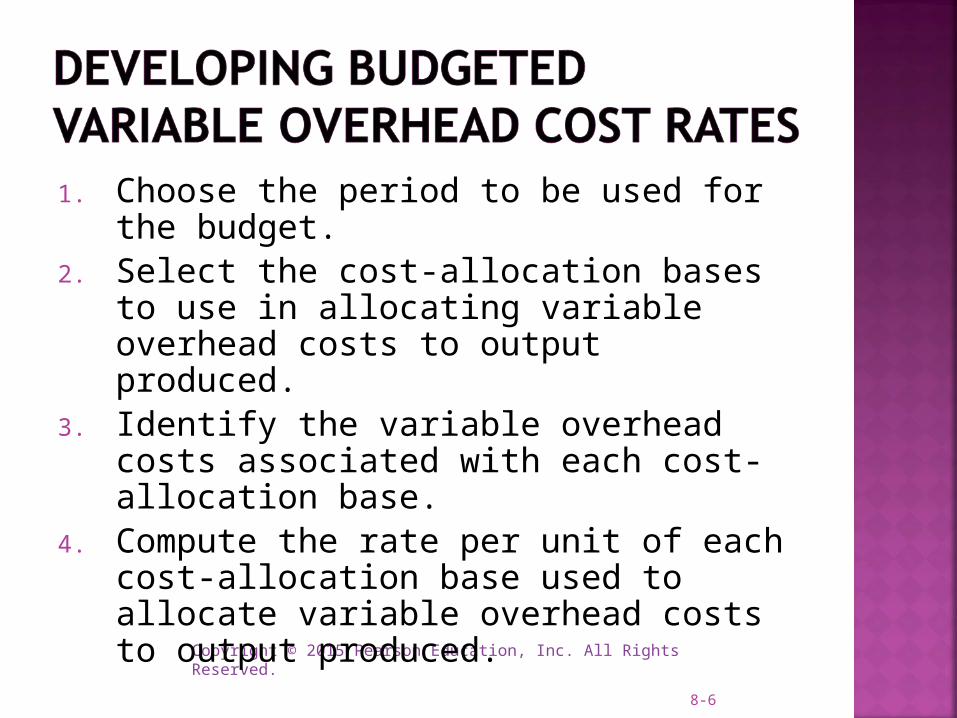

1. Choose the period to be used for the budget.

2. Select the cost-allocation bases to use in allocating variable overhead costs to output produced.

3. Identify the variable overhead costs associated with each cost-allocation base.

4. Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

8-6

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

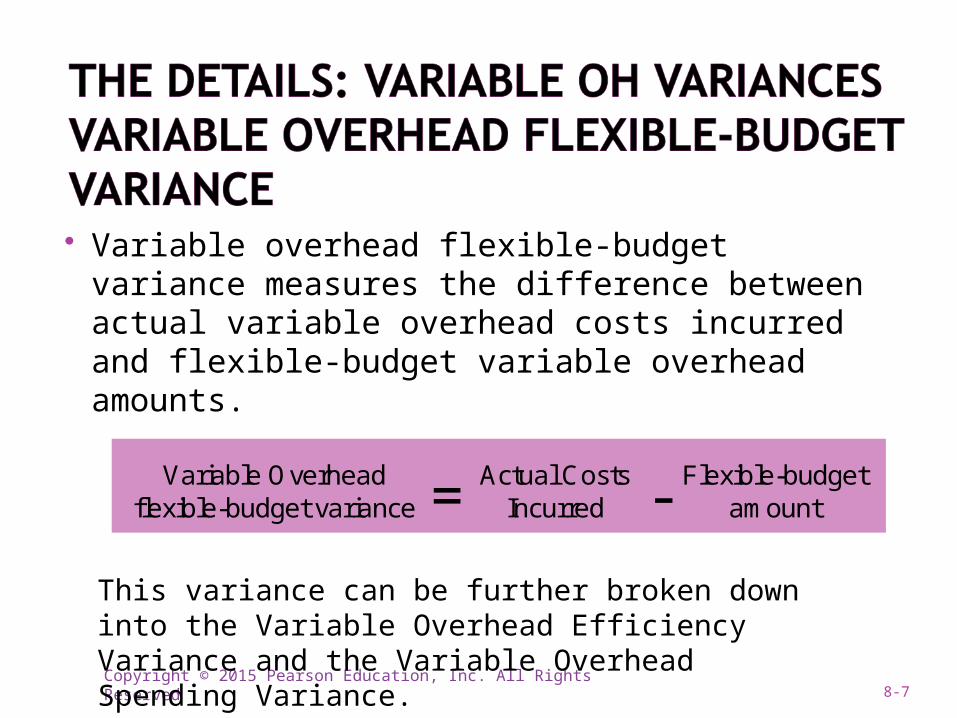

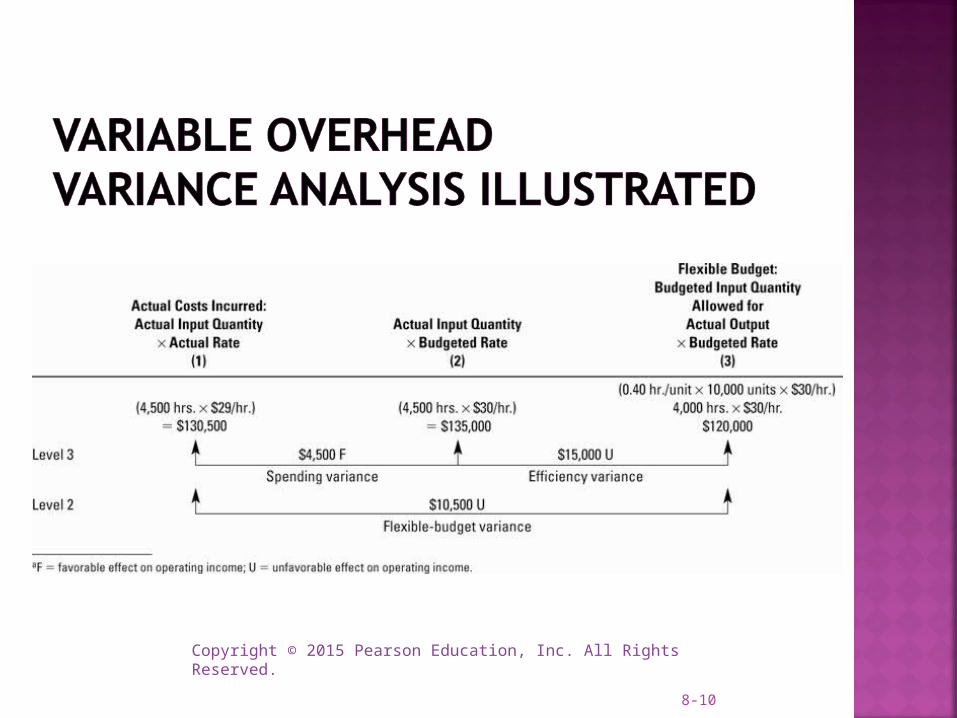

Variable overhead flexible-budget variance measures the difference between actual variable overhead costs incurred and flexible-budget variable overhead amounts.

Variable Overhead Actual Costs Flexible-budgetflexible-budget variance Incurred amount= -

This variance can be further broken down into the Variable Overhead Efficiency Variance and the Variable Overhead Spending Variance.

8-7

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

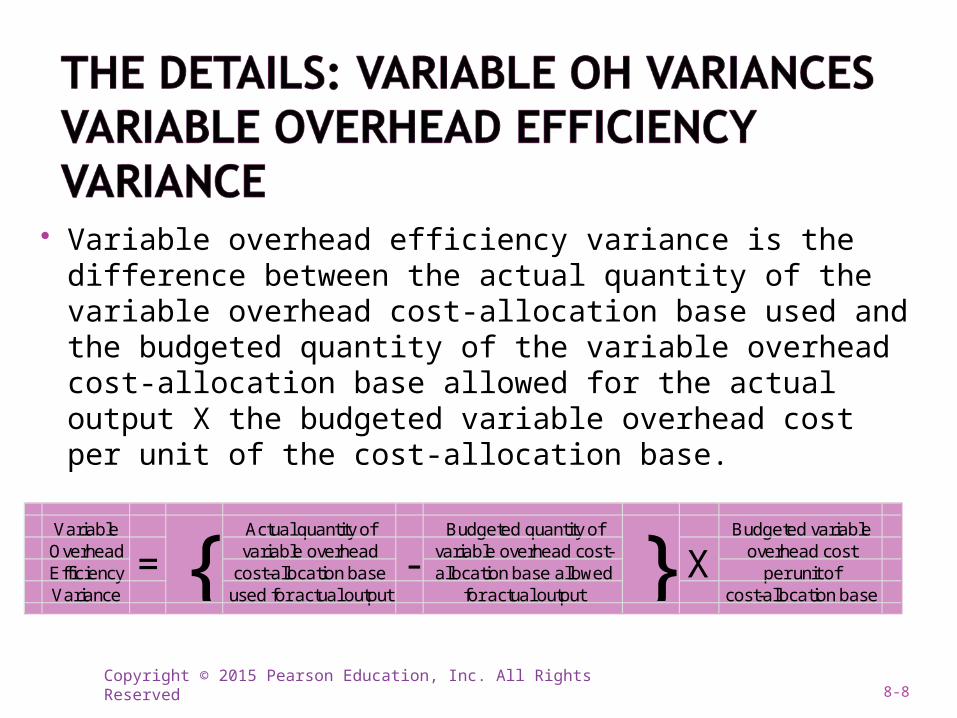

Variable overhead efficiency variance is the difference between the actual quantity of the variable overhead cost-allocation base used and the budgeted quantity of the variable overhead cost-allocation base allowed for the actual output X the budgeted variable overhead cost per unit of the cost-allocation base.

Variable Actual quantity of Budgeted quantity of Budgeted variableOverhead variable overhead variable overhead cost- overhead costEfficiency cost-allocation base allocation base allowed per unit ofVariance used for actual output for actual output cost-allocation base

} X= { -

8-8

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

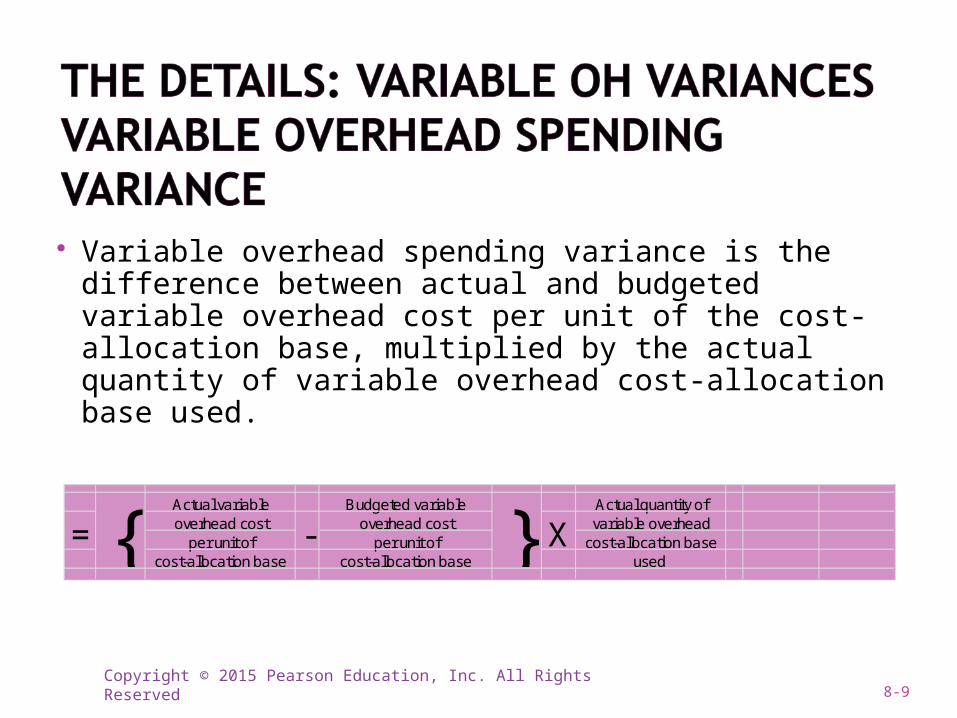

Variable overhead spending variance is the difference between actual and budgeted variable overhead cost per unit of the cost-allocation base, multiplied by the actual quantity of variable overhead cost-allocation base used.

Actual variable Budgeted variable Actual quantity ofoverhead cost overhead cost variable overhead

per unit of per unit of cost-allocation basecost-allocation base cost-allocation base used

= { }- X

8-9

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

8-10

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

Fixed overhead costs are, by definition, a lump sum of costs that remain unchanged for a given period despite potentially wide changes in activity within the relevant range. These costs are fixed in the sense that, unlike variable costs, fixed costs do not automatically increase or decrease with the level of activity within the relevant range.

8-11

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

1. Choose the period to be used for the budget.

2. Select the cost-allocation bases to use in allocating fixed overhead costs to output produced.

3. Identify the fixed overhead costs associated with each cost-allocation base.

4. Compute the rate per unit of each cost-allocation base used to allocate fixed overhead costs to output produced.

8-12

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

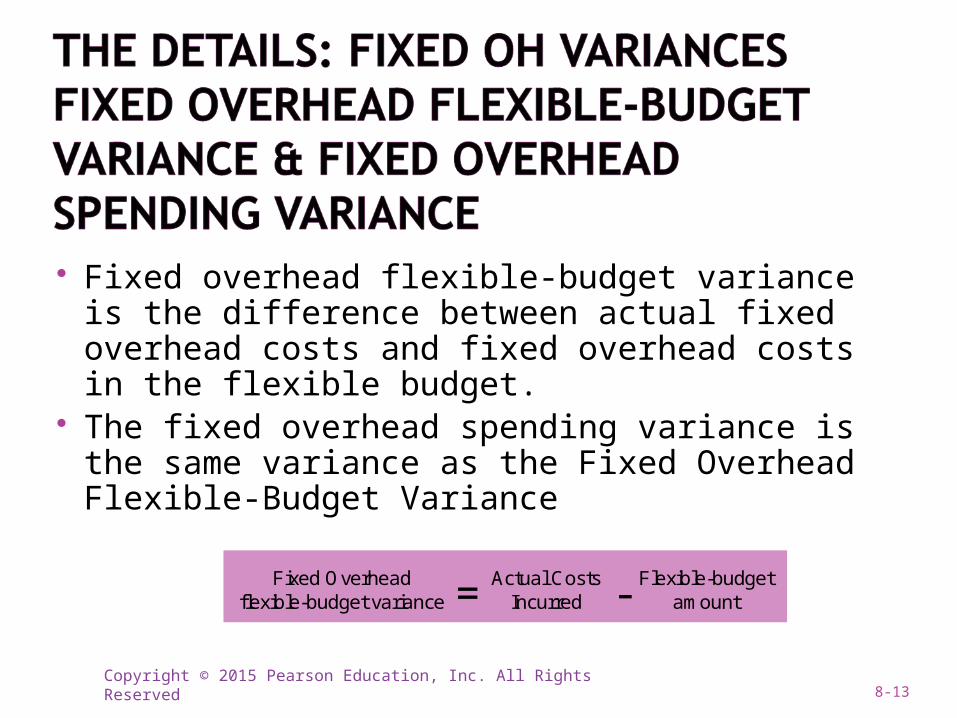

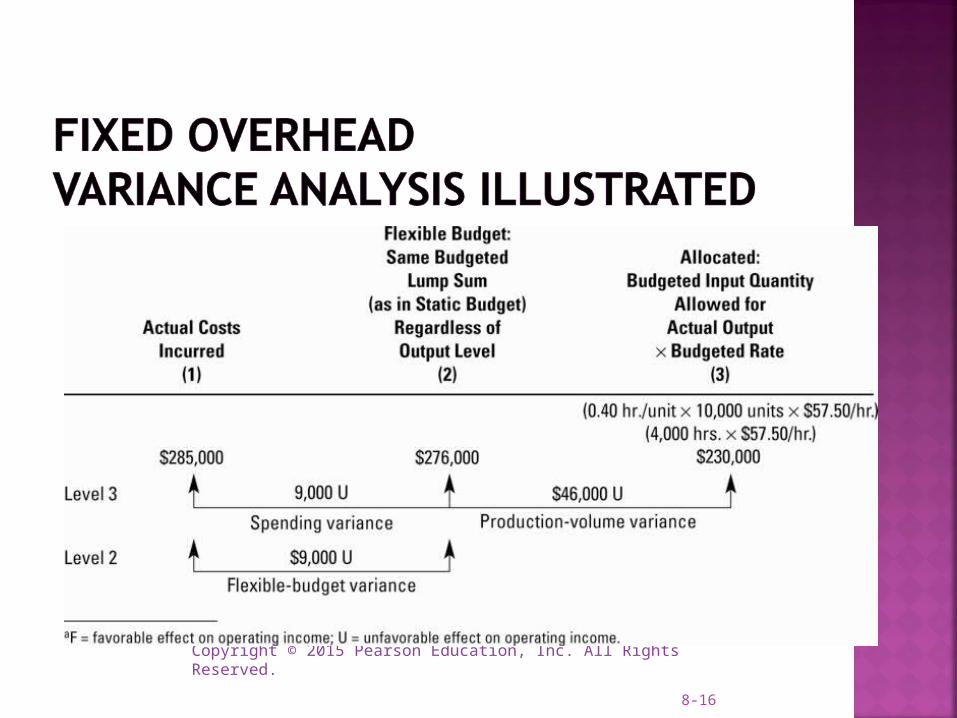

Fixed overhead flexible-budget variance is the difference between actual fixed overhead costs and fixed overhead costs in the flexible budget.

The fixed overhead spending variance is the same variance as the Fixed Overhead Flexible-Budget Variance

Fixed Overhead Actual Costs Flexible-budgetflexible-budget variance Incurred amount= -

8-13

Copyright © 2015 Pearson Education, Inc. All Rights Reserved

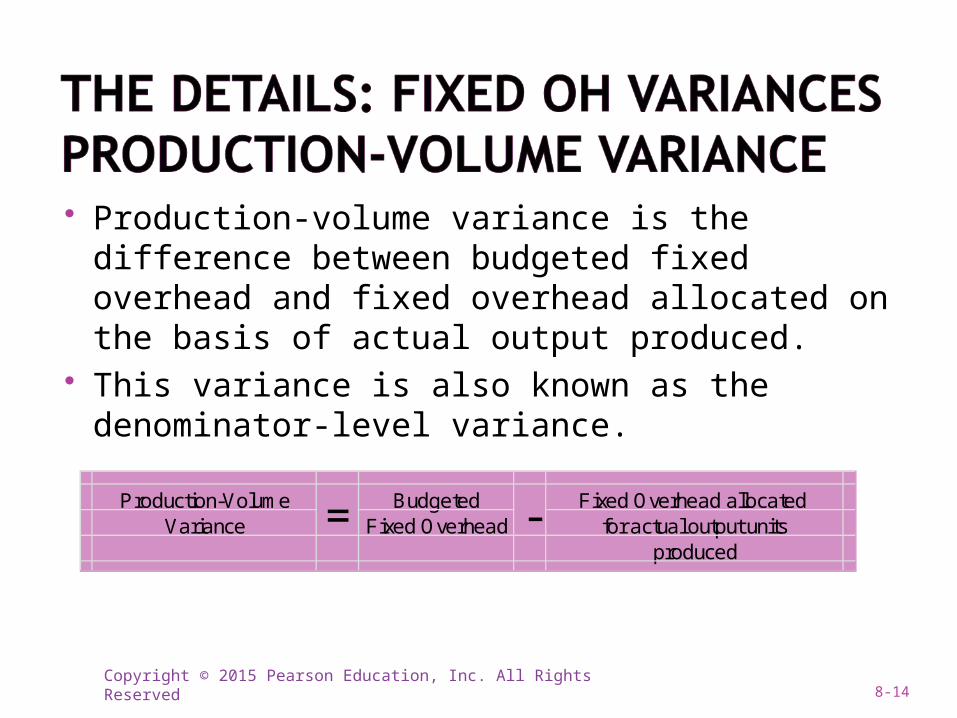

Production-volume variance is the difference between budgeted fixed overhead and fixed overhead allocated on the basis of actual output produced.

This variance is also known as the denominator-level variance.

Production-Volume Budgeted Fixed Overhead allocated Variance Fixed Overhead for actual output units

produced

= -

8-14

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

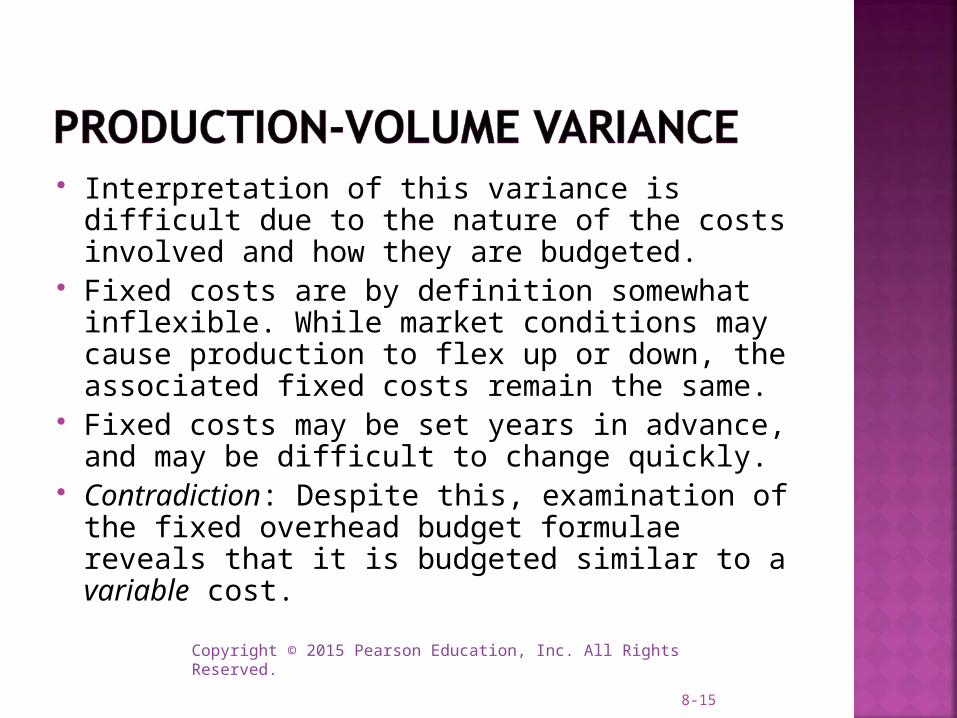

Interpretation of this variance is difficult due to the nature of the costs involved and how they are budgeted.

Fixed costs are by definition somewhat inflexible. While market conditions may cause production to flex up or down, the associated fixed costs remain the same.

Fixed costs may be set years in advance, and may be difficult to change quickly.

Contradiction: Despite this, examination of the fixed overhead budget formulae reveals that it is budgeted similar to a variable cost.

8-15

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

8-16

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

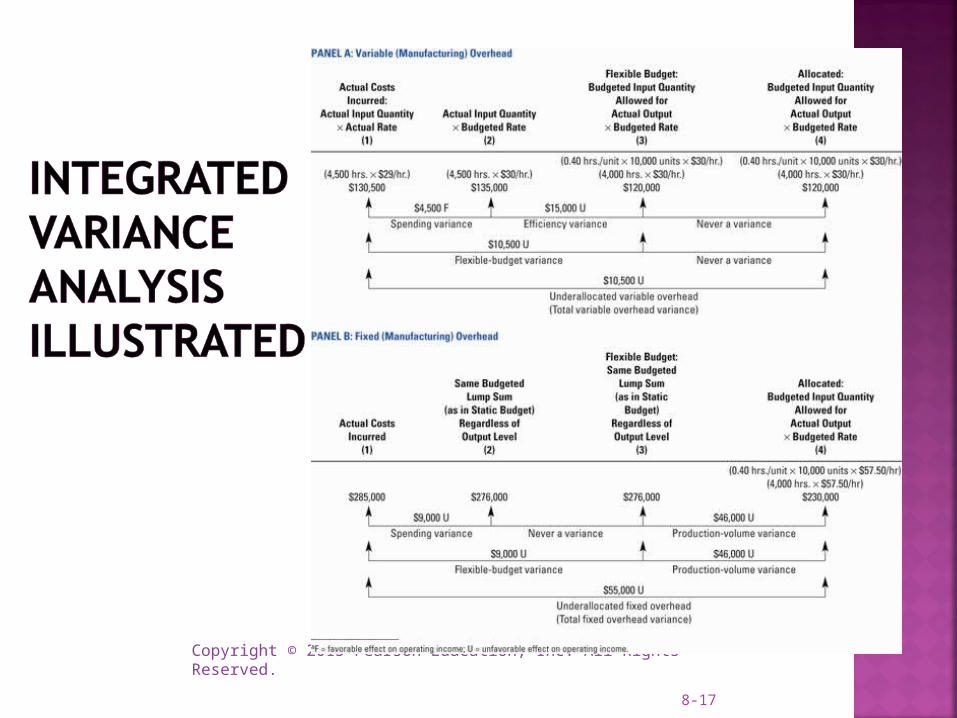

8-17

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

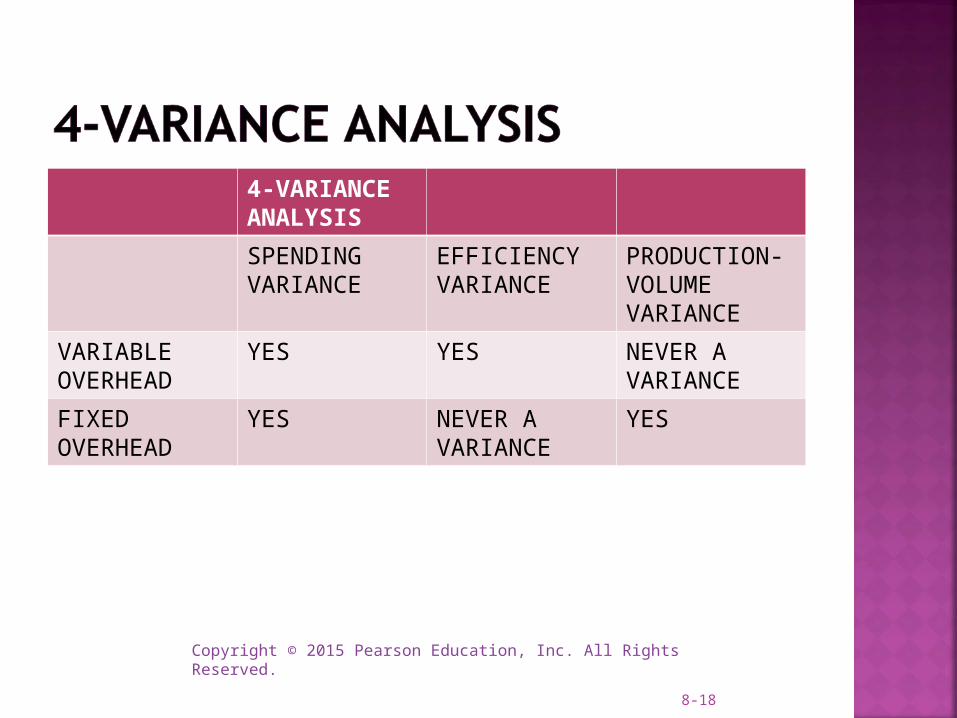

4-VARIANCE ANALYSIS

SPENDING VARIANCE

EFFICIENCY VARIANCE

PRODUCTION-VOLUME VARIANCE

VARIABLE OVERHEAD

YES YES NEVER A VARIANCE

FIXED OVERHEAD

YES NEVER A VARIANCE

YES

8-18

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

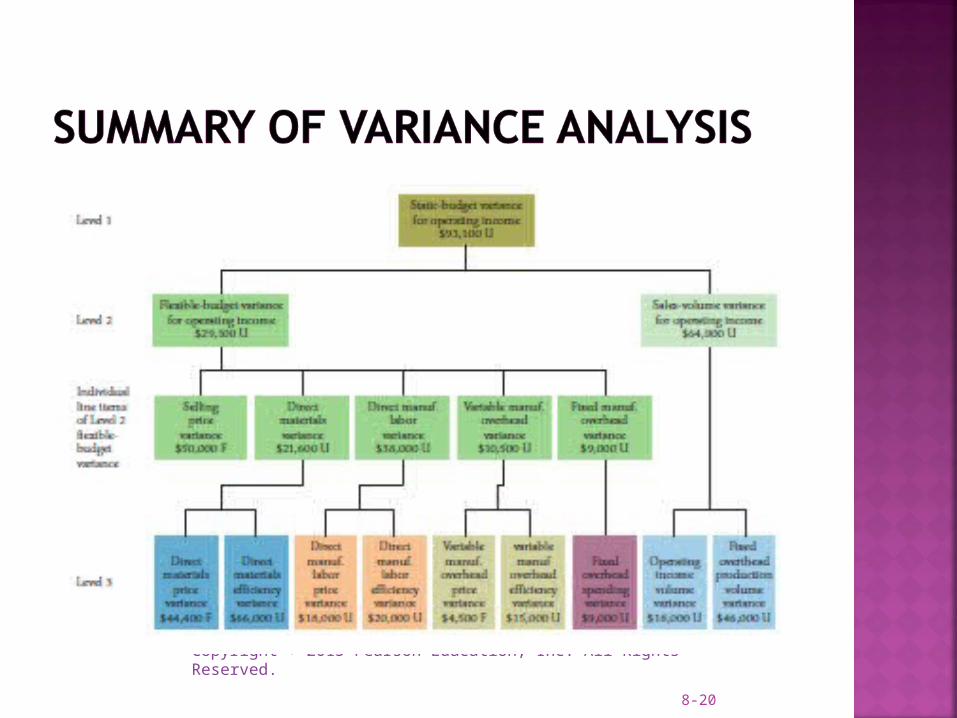

You may recall from chapter 7 that the static budget variance (the difference between the static budget and the actual results) was $93,100 Unfavorable for Webb Company, our sample company.The sales-volume variance (the difference between the flexible budget and the static budget) was $64,000 Unfavorable.The sales-volume variance consists of two components: The operating-income volume variance and the production-volume variance.

8-19

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

8-20

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

Activity-based costing systems focus on individual activities as the fundamental cost objects.

Variances are calculated for each activity

8-21

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

Nonmanufacturing companies can benefit from overhead variances just as manufacturing companies can.

Variance analysis can be used to examine overhead costs and make decisions about pricing, managing costs and the mix of products.

Output measures will be different and can be passenger-miles flown, patient days provided, rooms-days occupied, ton-miles of freight hauled, etc.

8-22

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

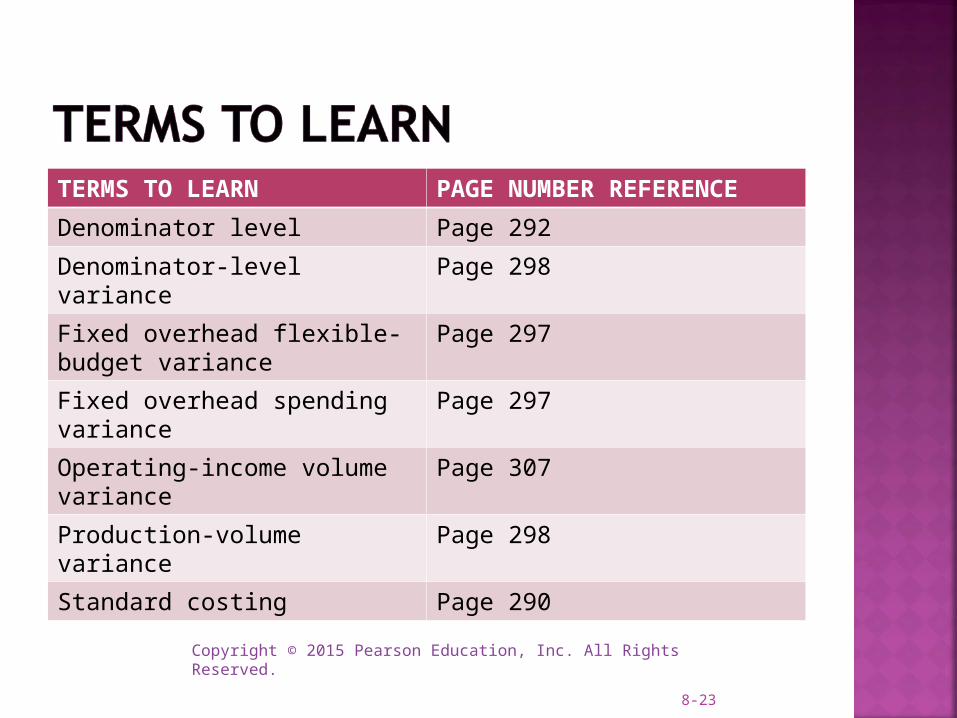

TERMS TO LEARN PAGE NUMBER REFERENCE

Denominator level Page 292

Denominator-level variance Page 298

Fixed overhead flexible-budget variance

Page 297

Fixed overhead spending variance

Page 297

Operating-income volume variance

Page 307

Production-volume variance Page 298

Standard costing Page 290

8-23

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

TERMS TO LEARN PAGE NUMBER REFERENCE

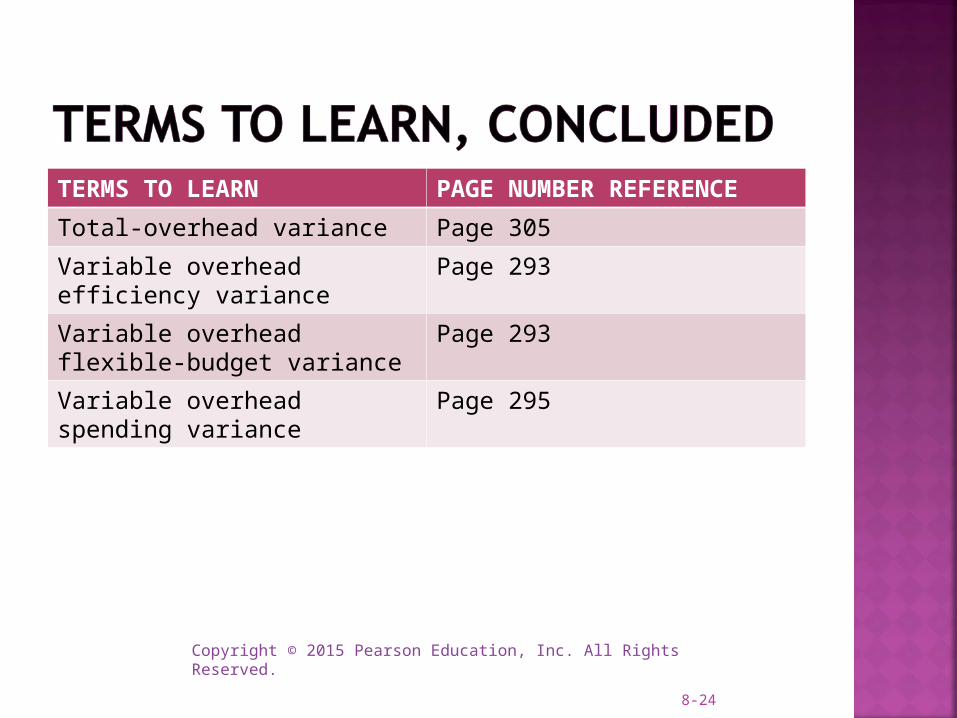

Total-overhead variance Page 305

Variable overhead efficiency variance

Page 293

Variable overhead flexible-budget variance

Page 293

Variable overhead spending variance

Page 295

8-24

Copyright © 2015 Pearson Education, Inc. All Rights Reserved.

25