Embed Size (px)

Citation preview

Contributionto Literature

Model

Results

Comments

Conclusion

Discussion of "Financial Globalization andMonetary Transmission" by Simone Meier

Pedro Gete

Georgetown University

Contributionto Literature

Model

Results

Comments

ConclusionI Paper makes interesting contribution toimportant policy question

I Let me start with the question

Contributionto Literature

Model

Results

Comments

Conclusion

Dallas Fed President Richard Fisher (2006)

I "The literature on globalization is large. Theliterature on monetary policy is vast. But theliterature examining the combination of the twois surprisingly small."

I "The old models simply no longer apply in ourglobalized, interconnected and expandedeconomy."

Contributionto Literature

Model

Results

Comments

Conclusion

Bernanke (2007), Gonzalez-Paramo (2007), Mishkin(2007), Papademos (2007), Rogoff (2006), Weber(2007), Yellen (2006)...

I Globalization has had or will soon havedramatic consequences for the nature of themonetary transmission mechanism

I It may threaten the ability of national centralbanks to control output and in�ation withintheir borders

Contributionto Literature

Model

Results

Comments

Conclusion

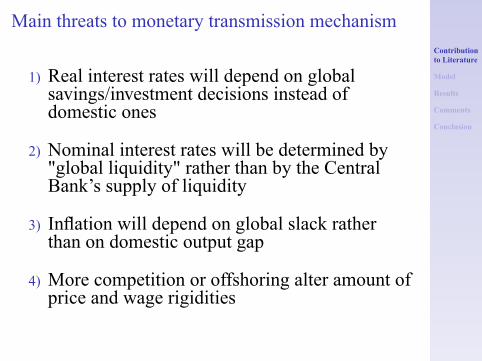

Main threats to monetary transmission mechanism

1) Real interest rates will depend on globalsavings/investment decisions instead ofdomestic ones

2) Nominal interest rates will be determined by"global liquidity" rather than by the CentralBank's supply of liquidity

3) In�ation will depend on global slack ratherthan on domestic output gap

4) More competition or offshoring alter amount ofprice and wage rigidities

Contributionto Literature

Model

Results

Comments

Conclusion

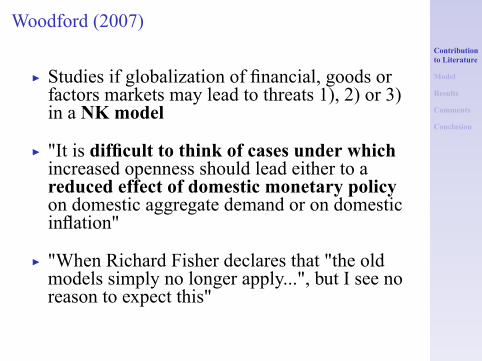

Woodford (2007)

I Studies if globalization of �nancial, goods orfactors markets may lead to threats 1), 2) or 3)in a NK model

I "It is dif�cult to think of cases under whichincreased openness should lead either to areduced effect of domestic monetary policyon domestic aggregate demand or on domesticin�ation"

I "When Richard Fisher declares that "the oldmodels simply no longer apply...", but I see noreason to expect this"

Contributionto Literature

Model

Results

Comments

Conclusion

But...

I Woodford's analysis of �nancial globalizationbuilds on Cole and Obstfeld (1991):

I unit elasticity of substitution betweendomestic and foreign goods, and identicalpreferences in the two countries,

I then �nds the result that the degree ofinternational integration of �nancialmarkets is irrelevant:

I the same allocation of resources and systemof asset prices represents an equilibrium forany cost of asset trade or incompleteness ofinternational �nancial markets under anymonetary policy.

Contributionto Literature

Model

Results

Comments

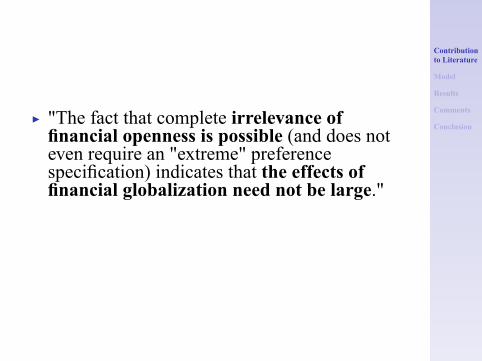

ConclusionI "The fact that complete irrelevance of�nancial openness is possible (and does noteven require an "extreme" preferencespeci�cation) indicates that the effects of�nancial globalization need not be large."

Contributionto Literature

Model

Results

Comments

Conclusion

Meier (2012)

I Extend Woodford's analysis to a model with aricher structure in �nancial markets.

I Study the effects of monetary policy ondomestic output and in�ation for different costsof international asset trading and levels of grossforeign asset holdings

I Both forms of �nancial globalization can affectthe monetary transmission mechanism in a NKmodel.

Contributionto Literature

Model

Results

Comments

Conclusion

I While some channels of transmission may beweaker, other channels will be stronger. Thecombined impact is a priori ambiguous.

I Simulations of the model show that none of theanalyzed forms of �nancial globalizationundermine the impact of monetary policy onoutput and in�ation.

I Simone claims that Woodford (2007) resultsare con�rmed:

I "It is dif�cult to construct scenarios inwhich �nancial integration or an interactionof �nancial with other forms of integrationmaterially weaken the impact of monetarypolicy"

Contributionto Literature

Model

Results

Comments

Conclusion

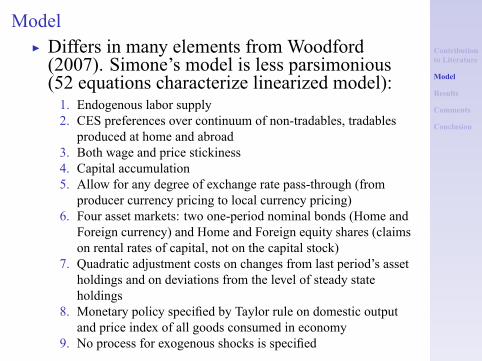

ModelI Differs in many elements from Woodford(2007). Simone's model is less parsimonious(52 equations characterize linearized model):1. Endogenous labor supply2. CES preferences over continuum of non-tradables, tradablesproduced at home and abroad

3. Both wage and price stickiness4. Capital accumulation5. Allow for any degree of exchange rate pass-through (fromproducer currency pricing to local currency pricing)

6. Four asset markets: two one-period nominal bonds (Home andForeign currency) and Home and Foreign equity shares (claimson rental rates of capital, not on the capital stock)

7. Quadratic adjustment costs on changes from last period's assetholdings and on deviations from the level of steady stateholdings

8. Monetary policy speci�ed by Taylor rule on domestic outputand price index of all goods consumed in economy

9. No process for exogenous shocks is speci�ed

Contributionto Literature

Model

Results

Comments

Conclusion

I Parameterized model (26 parameters) is solvedby linearization around an exogenous steadystate asset portfolio

I Compares IRs after unexpected positivemonetary shock for different parameter valuesof1. foreign transaction costs2. levels of gross foreign steady state assetholdings

3. Interactions of 1) and 2) with lower shareof home traded goods

Contributionto Literature

Model

Results

Comments

Conclusion

Main results

I Interest rate channel of monetary policy isweaker when agents have better access to risksharing with another country.

I After an increase in domestic rates, agentssell assets instead of reducing consumption.

I Exchange rate channel is stronger when assetmarkets are more integrated: capital �owsenhance reaction of exchange rates.

I Consequences for imports/exports.I Larger role for valuation effects.

Contributionto Literature

Model

Results

Comments

Conclusion

Comments on the results

I Goal of paper is to make a contribution tomonetary theory. We need more results onwhat controls strength of policy effects

I Tackle Woodford's conclusion: can we think ofcases under which increased openness shouldlead to a reduced effect of domestic monetarypolicy on either domestic aggregate demand ordomestic in�action?

I Local currency pricing? Slow pass-through of exchange-ratechanges to import/export prices reduces the size of the effecton in�ation

Contributionto Literature

Model

Results

Comments

ConclusionI Monetary policy is effective because rigiditiesallow monetary policy to affect real variables,how does �nancial globalization affect therigidities?

Contributionto Literature

Model

Results

Comments

Conclusion

Comments on the solution technique

I Devereux and Sutherland (2006) show thattime variation in portfolio shares is mostlyirrelevant for all questions regarding the�rst-order responses of macroeconomicvariables like consumption, output, realexchange rates, etc. Only a solution for theSteady State portfolio is required.

I Here we linearize, assume an exogenousSteady State portfolio and impose portfolioadjustment costs to ensure stationarity aroundthe exogenously chosen SS

Contributionto Literature

Model

Results

Comments

Conclusion

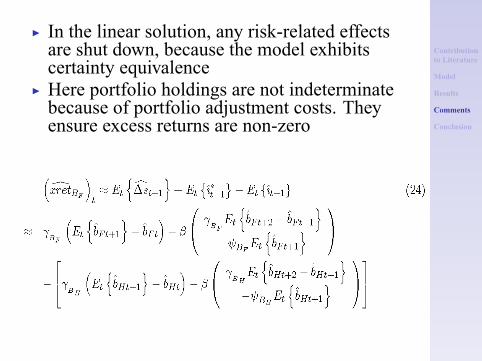

I In the linear solution, any risk-related effectsare shut down, because the model exhibitscertainty equivalence

I Here portfolio holdings are not indeterminatebecause of portfolio adjustment costs. Theyensure excess returns are non-zero

Contributionto Literature

Model

Results

Comments

Conclusion

I The asset holding dynamics are then drivenexclusively by transaction costs, which seemsimplausible.

I Holdings should depend, among other things,on agents' attitudes towards risk, the structureof shocks, and the impact of different shockson the risk of agents' portfolios

I Monetary policy affects risk premiums (E.g.Diebold, Piazzesi and Rudebusch 2005,Palomino 2012), and �nancial globalizationmay alter how

Contributionto Literature

Model

Results

Comments

Conclusion

A doubtI Exogenous steady State has zero net foreignasset positions

I NFA and related variables do not seem toreturn to initial Steady State

Contributionto Literature

Model

Results

Comments

Conclusion

Some comments that imply changing the model

I Does the model give a picture of thetransmission of monetary policy through�nancial markets that is consistent with thedynamics observed in the data?

I When we study �nancial integration without a�nancial sector, what are we missing?

I For example, the model assumes the centralbank has no problem controlling the interestrate that matters for consumption/savingsdecisions. Empirically we know this is notalways true. I'd say it's a main effect ofglobalization on the monetary transmissionchannel

Contributionto Literature

Model

Results

Comments

Conclusion

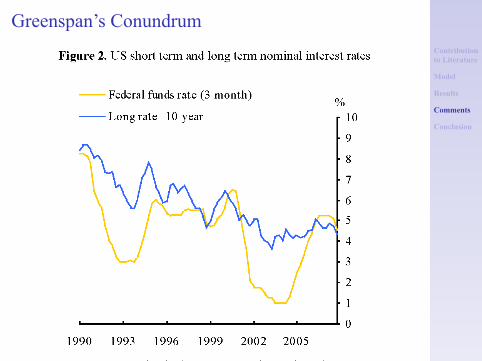

Greenspan's Conundrum

Contributionto Literature

Model

Results

Comments

Conclusion

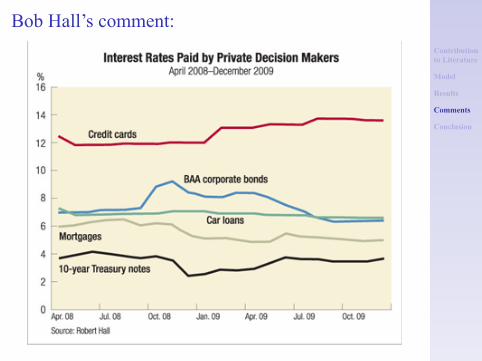

Bob Hall's comment:

Contributionto Literature

Model

Results

Comments

Conclusion

The recent crisis illustrates some other effects of�nancial globalization:

I Fire sales of assets may transmit a shock fromthe US to the euro area if institutions that needliquidity in the US sell assets in Europe. Andthe ECB may �nd it harder to control theeconomies of the euro area when there is acrisis in the US.

I Large gross positions increase balance-sheetrisks, like liquidity problems in the dollardenominated market in Europe that promptedthe central bank swaps in 2008.

Contributionto Literature

Model

Results

Comments

Conclusion

Should we agree with Woodford (2007)?

I "Increased international trade in �nancialassets, consumer goods and factors ofproduction should lead to quantitativechanges in the magnitudes of various keyresponse elasticities relevant to thetransmission mechanism for monetary policy,but should not require fundamentalreconsideration of the framework ofmonetary policy analysis."