Embed Size (px)

DESCRIPTION

Arthur Worsley - Container Freight Derivatives Broker - Tel / +44 (0) 20 7090 1120 - Mob / +44 (0) 75 9565 7672 - Fax / +44 (0) 20 7090 1121 - Freight Investor Services, 80 Cannon Street, London, EC4N 6HL, United Kingdom

Citation preview

5 August, 2010

Introduction to

Container Swaps

Introduction to Container Swaps http://bit.ly/get-reports

Agenda

Introduction to Container Swaps http://bit.ly/get-reports

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

Global Container Trade (2010)Distribution of 144 Million TEUs of Global Container Trade

Container Shipping

19% [ 27 ]

27% [ 32 ]

7% [ 9 ]

9% [ 11 ]

38% [ 55 ] East >> East

East >> West

West >> East

West >> West

Rest of World

http://bit.ly/get-reportsIntroduction to Container Swaps

Container Market Volatility

Container Market Volatility (CCFI)

http://bit.ly/get-reportsIntroduction to Container Swaps

600.00

800.00

1000.00

1200.00

1400.00

1600.00

1800.00

2000.00

2200.00

05 Jan 07 05 May 07 05 Sep 07 05 Jan 08 05 May 08 05 Sep 08 05 Jan 09 05 May 09 05 Sep 09 05 Jan 10 05 May 10

IND

EX P

OIN

TS

European Service Mediterranean Service American Service (West Coast) American Service (East Coast)

1200.00

1400.00

1600.00

1800.00

2000.00

2200.00

Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10

USD

/ T

EU

Shanghai >> Europe (USD/TEU) Shanghai >> Mediterranean (USD/TEU)

Container Box-Rate Volatility

http://bit.ly/get-reportsIntroduction to Container Swaps

+ 152%

Container ‘Box-Rate’ Volatility (SCFI)

+ 149%

+ 179%

Container Shipping

• Containers are like any commodity

• Key price drivers include– Intermodal container and container ship supply

– Consumer spending and consumer goods demand

• Containers are traded in substantial volumes

• Container box-rates are highly volatile

• Clear requirements for price risk management

• The FIS cash settled container swaps market is establishing itself and growing rapidly

Introduction to Container Swaps http://bit.ly/get-reports

Agenda

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

Introduction to Container Swaps http://bit.ly/get-reports

What are Container Swaps

• Container Swaps– Are cash-settled wagers

– Agreed between two counterparties

– To ship a precise volume of containers

– On a particular trade route

– Over a specified period

– At a box-rate agreed today

Introduction to Container Swaps http://bit.ly/get-reports

Why Use Container Swaps

-600

-400

-200

200

400

600

800 1000 1200 1400 1600 1800

Pro

fit

/ Lo

ss (

USD

)

Box-Rate ( USD / TEU )

Physical Position Swap Position

Introduction to Container Swaps http://bit.ly/get-reports

Purchasing a container swap with the opposite profit/loss profile to your physical position causes the profits/losses from each position to cancel each other out.

Whether box rates increase or decrease, the net box-rate you pay/receive is thus fixedrelative to the spot market

The position can be flexibly escaped (closed out) by taking a second swap position that is equal and opposite to your first swap position.

Who Uses Container Swaps

• For End-Users and Commodity Traders– Container swaps are used to offset (hedge) the risk of

increasing box-rate costs in a rising physical market

• For Shipping Liners and Operators– Container swaps are used to offset (hedge) the risk of

decreasing box-rate revenues in a falling physical market

• For Trading Desks and Speculators– Container swaps can be used to profit by using complex

quantitative and qualitative analysis to speculate on the direction of box-rate fluctuations

Introduction to Container Swaps http://bit.ly/get-reports

Indirect Hedging with Container Swaps

Composite SCFI vs AP Moller-Maersk (Share Price)Container Swaps are Used to Hedge Indirectly Against Highly Correlated Commodities

Introduction to Container Swaps

34000

36000

38000

40000

42000

44000

46000

48000

50000

1000.00

1100.00

1200.00

1300.00

1400.00

1500.00

1600.00

Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10

Comprehensive Index Ap Moller - Maersk (Share Price)

http://bit.ly/get-reports

Composite SCFI

Agenda

Introduction to Container Swaps http://bit.ly/get-reports

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

The SCFI

• The Shanghai Containerised Freight Index (SCFI)is published weekly on a Friday at 15:00 Shanghai Time and is administrated by the Shanghai Shipping Exchange (SSE)

• 30 Volunteer Panellists– 15 Global Shipping Companies (Net Long the Underlying)

– 15 Local Freight Forwarders (Net Short the Underlying)

• 15 Indexed Shanghai Export Routes– The SCFI provides a fair and faithful representation of container

Box-Rates across constituent routes• BAF/FAF, EBS/EBA, CAF/YAS, PSS, WRS, PCS, SCS/SCF/PTF/PCC included

Introduction to Container Swaps http://bit.ly/get-reports

The SCFI : Panelists

• 30 Volunteer principals– Account for over 60% of trade volume on indexed routes

Introduction to Container Swaps http://bit.ly/get-reports

Shanghai • Europe (base ports)

• Mediterranean (base ports)

• US West Coast (base ports)

• US East Coast (base ports)

• Persian Gulf (Dubai)

• Australia / New Zealand (Melbourne)

• West Africa (Lagos)

• South Africa (Durban)

• South America (Santos)

• West Japan (base ports)

• East Japan (base ports)

• Southeast Asia (Singapore)

• Korea (Pusan)

• Taiwan (Kaohsiung)

• Hong Kong (Hong Kong)

The SCFI :: Routes

Introduction to Container Swaps http://bit.ly/get-reports

Europe• Hamburg / Antwerp / Felixstowe / Le Havre

Mediterranean• Barcelona / Valencia / Genoa / Naples

US West Coast• Los Angeles / Long Beach / Oakland

US East Coast• New York / Savannah / Norfolk / Charleston

West Japan• Osaka / Kobe

East Japan• Tokyo / Yokohama

The SCFI :: Sample

Introduction to Container Swaps http://bit.ly/get-reports

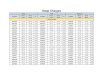

The Shanghai Containerized Freight Index (SCFI) – Sample Data

Date Composite IndexShanghai>> Europe

(USD / TEU)Shanghai >> Mediterranean

(USD / TEU)Shanghai >> US West Coast

(USD / FEU)Shanghai >> US East Coast

(USD / FEU)

30 Jul 10 1555.3 1890 1838 2787 4085

23 Jul 10 1563.97 1895 1859 2779 4012

16 Jul 10 1579.16 1903 1886 2794 3988

09 Jul 10 1581.85 1901 1910 2816 3987

02 Jul 10 1583.18 1887 1919 2833 3962

25 Jun 10 1576.84 1870 1906 2823 3960

18 Jun 10 1569.04 1868 1908 2810 3897

11 Jun 10 1543.72 1874 1906 2743 3822

Agenda

Introduction to Container Swaps http://bit.ly/get-reports

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

LCH.Clearnet

• LCH.Clearnet sits in the middle of a trade and acts as the legal counterparty to each side

– Minimises credit risk

– Maintains trading anonymity

– Maximises processing efficiencies

• principals must trade through one of LCH’s general clearing members (GCMs)

Introduction to Container Swaps http://bit.ly/get-reports

FFA Clearing

• In 2006 cleared FFA trades made up 15% of the total market• In 2009 that figure rose to a staggering 93%• A clearing account is essential to trading container swaps

Introduction to Container Swaps

34%49%

69%

90% 97%

0%

20%

40%

60%

80%

100%

2H 2007 1H 2008 2H 2008 1H 2009 2H 2009

OTC Cleared

http://bit.ly/get-reports

Swap Buyer(Front Office)

Swap Buyer(Back Office)

Swap Seller(Back Office)

Swap Seller(Front Office)

Clearing Member(Back Office)

Broker(FIS)

Clearing Member(Back Office)

Clearing House(LCH.Clearnet)

Introduction to Container Swaps http://bit.ly/get-reports

Clearing Process

1 1

2

3 3

4 4

E X

E C

U T

I O

NC

L E

A R

I N

G

LCH Cleared Container Swaps

Tradable Routes Pricing Contract Size LCH Contract Code

Shanghai >> Europe USD / TEU 1 TEU CNW

Shanghai >> Mediterranean USD / TEU 1 TEU CMD

Shanghai >> US West Coast USD / FEU 1 FEU CSW

Shanghai >> US East Coast USD / FEU 1 FEU CSE

Introduction to Container Swaps http://bit.ly/get-reports

• LCH currently clears contracts against the four major SCFI settled Shanghai export routes

Tradable Periods Months Quarter Calendar Year

Contracts Available M / M + 1 / M + 2 Q / Q + 1 / Q +2 / Q +3 Cal + 1

E.g. On 01 Apr 2010 Apr / May / JunQ3 2010 / Q4 2010Q1 2011 / Q2 2011

Cal 2011

Initial Margin

• The initial margin is a returnable deposit placed at the start of a trade in respect of the estimated risk of a party’s net open positions

– LCH reviews several factors on a monthly basis to estimate this risk

• The initial margin protects LCH against significant financial loss in the case of counterparty default

• For container swaps initial margins are approx 10 – 15% of the value of a position

Introduction to Container Swaps http://bit.ly/get-reports

Variation (Maintenance) Margin

• Each day the profit and loss is calculated on a party’s positions against the end of day price as supplied by a panel of container swaps brokers

• A party’s clearing member account is creditedwhen the position is ‘in the money’– New funds in excess of your initial margin may be withdrawn

• A party’s clearing member’s account is debited when the position is ‘out of the money’– Additional funds must be deposited to maintain your initial margin

Introduction to Container Swaps http://bit.ly/get-reports

LCH Cash Settlement & Costs

• Contracts are Cash Settled Monthly

– The settlement price is the average of the SCFI route prices published during the contract period

• Clearing Costs

– $6 (approx.) per swap contract

• $3 initial clearing house fee

• Approx. $3 additional clearing member surcharge – Full clearing fee is subject to individual terms negotiated with your clearing member

Introduction to Container Swaps http://bit.ly/get-reports

Agenda

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

Introduction to Container Swaps http://bit.ly/get-reports

SCFI rates fall to $1,600 / TEU during FEB 2010

In JAN ABC becomes concerned that market is falling rather than rising as expected

On Jan 15th, ABC sells 100 CNW FEB contracts at spot market price of $1,750 USD

ABC’s net swap position is closed out at a loss of $5,000. This is $35,000 less than holding on to the contracts until settlement. ABC once again exposes itself to physical box-rates alone.

Physical Position / ABC pays $240,000 during FEB to ship 100 TEUs [100 TEUs x $2,400]

Paper Position / ABC settles its 100 CNW FEB swaps on MAR 1st, receiving $60,000[ 100 TEUs x ($2,400 – $1,800) ]

Net Position / ABC successfully hedges their costs. ABC pays $60,000 less for FEB transport relative to spot-market trading competitors

Hedging :: Market Example

Introduction to Container Swaps

Position

“ABC” supermarket knows it needs to ship 100 containers in FEB 2010 and is worried that box prices from Shanghai >> Europe will rise in response to increased consumer demand

On DEC 10th 2009 ABC buys 100 CNW FEB swap contracts at the current spot price of $1,800 / TEU• ABC posts an initial margin deposit of $18,000 (N.B. Total position value $180,000)

SCFI rates rise to $2,400 / TEU during FEB 2010

http://bit.ly/get-reports

Agenda

1. The Underlying: Container Shipping

2. The Product: Container Swaps

3. The Index : The SCFI

4. The Clearer : LCH.Clearnet

5. Case Study : ABC Supermarket

6. The Broker : FIS

Introduction to Container Swaps http://bit.ly/get-reports

Who are FIS?

Freight & Commodity Derivatives BrokerageLeading players in the global FFA marketsGlobal network of offices, brokers & clients

London / Athens / Dubai / Singapore / Shanghai / Tokyo / New York

Consistent, measured, annual growthFSA (London) /MAS (Singapore) Regulated

http://bit.ly/get-reportsIntroduction to Container Swaps

The Role of Brokers

• Freight Investor Services

– Facilitates & Negotiates trades between buyers and sellers of FFAs; generating market liquidity

– Advises clients on moment to moment market movements and sentiment

– Disseminates market reports and daily forward rate curves to keep clients informed

– Maintains high standards of trading within the market place and protects client anonymity

Introduction to Container Swaps http://bit.ly/get-reports

Some FIS FFA Clientsship broking, dry bulk, iron ore, steel, fertilizers

http://bit.ly/get-reportsIntroduction to Container Swaps

Container Swaps :: SUMMARY

• Container swaps are the single greatest development in containerization since the first standardization of intermodal containers

• Container swaps allow for flexible, cost-effective risk-management, universal pricing stability, price transparency & price discovery

• Container swaps trading is simple. It can and should be effortlessly integrated within an existing operational and corporate structure

Introduction to Container Swaps http://bit.ly/get-reports

Next Steps

Get our free container market reports + price curvesby email | [email protected]

online | http://bit.ly/get-reports

Contact Arthur for a telephone or personal consultationin person | 80 Cannon Street, London, EC4N 6HL

by telephone | +44 (0) 207 090 1120online | http://bit.ly/more-information

1st

2nd

Thank you for your time. We look forward to hearing from you soon.

Arthur Worsley [ + 44 (0) 7595 657 672 ]Container Freight Derivatives Broker