Embed Size (px)

Citation preview

Consolidated Financial Statements Financial year 2012

Approved by the Board of Directors March 13th, 2013

3

MANAGEMENT REPORTS AND FINANCIAL STATEMENTS

Group Structure and bank shareholdings 9

Reference Scenario 13

Management Report 21

The Group in 2012 23

Key indicators of Cattolica Group business performance 26

Ways in which the Group image and information are disclosed 33

Business performance for the period 35

A brief outline of the business performance 37

Insurance business and other sectors of activities 41

Financial and asset management 54

Risk management 59

Risk management 61

Insurance risk – non-life business 61

Insurance risk – life business 62

Market risk 64

Operating, legal and reputational risk 68

Employees and sales network 71

Human resources 73

Sales network 74

Significant events and other information 77

Significant transactions carried out during the year 79

Other information 87

Significant events during the first few months of 2013 92

Outlook for business activities 93

Consolidated Financial Statements 95

Statement of Financial Position 97

Income statement 99

Statement of comprehensive income 100

Statement of cash flows 102

Statement of changes in equity 103

Reconciliation statement of the result of the period and shareholders’ equity of the Group

and the Parent Company 107

Index

4

Notes to the accounts 113

Part A – Basis of presentation and consolidation area 115

Part B – Accounting principles 125

Part C – Information on the consolidated statement of financial position and income

statement 149

Part D – Other information 193

Certification of the Executive appointed to draw up the corporate accounting documents 197 Independent Auditors’ Report 199

5

TABLES

Table 1 – Key economic indicators 27

Table 2 – Key equity indicators 27

Table 3 – Sales network and headcount 28

Table 4 – Reclassified consolidated statement of financial position 29

Table 5 – Reclassified consolidated income statement 30

Table 6 – Reclassified consolidated income statement by segment of activities 31

Table 7 – Key indicators 32

Table 8 - Total premiums written 45

Table 9 – Life premiums written 46

Table 10 – Group exposure to re-insurers by rating category 62

Table 11 – Stratification of the portfolio on the basis of the maturity date 66

Table 12 – Stratification of the bond portfolio by rating 67

Table 13 – Group headcount 74

Table 14 - Ratios for share in circulation 92

Table 15 – Scope of consolidation (ISVAP Regulation No. 7 dated July 13th, 2007) 121

Table 16– Statement of financial position by sector of activities (ISVAP Regulation No. 7 dated July 13th, 2007) 151

Table 17 – Intangible assets 152

Table 18 - Goodwill – changes during the period 152

Table 19 – Other intangible assets – changes during the period 155

Table 20 – Tangible assets 157

Table 21 – Property and other tangible assets – changes during the period 158

Table 22 – Analysis of technical provisions – reinsurance amount (ISVAP Regulation No. 7 dated July 13th, 2007) 159

Table 23 - Investments 159

Table 24 – Investment property – changes during the period 160

Table 25 – Analysis of tangible and intangible assets (ISVAP Regulation No. 7 dated July 13th, 2007) 161

Table 26 - Investments in subsidiaries, associates and joint ventures 161

Table 27 – Analysis of non-consolidated equity investments (ISVAP Regulation No. 7 dated July 13th, 2007) 162

Summary index of tables

6

Table 28 – Summary data of non consolidated subsidiary and associated companies and joint ventures 162

Table 29 - Financial investments 163

Table 30 – Analysis of financial assets (ISVAP Regulation No. 7 dated July 13th, 2007) 163

Table 31 - Fair value of held to maturity investments and of loans and receivables 164

Table 32 - Financial assets at fair value through profit or loss 165

Table 33 - Exposure in Greek Government debt securities 166

Table 34 - Exposure in government debt securities issued by EU zone countries - Available for sale financial assets 166

Table 35 - Exposure in government debt securities issued by EU zone countries - Financial assets at fair value through profit or loss 167

Table 36 - Exposure in government debt securities issued by EU zone countries - Held to maturity investments 167

Table 37 – Analysis of financial assets and liabilities by level (ISVAP Regulation No. 7 dated July 13th, 2007) 168

Table 38 – Analysis of changes in level 3 financial assets and liabilities (ISVAP Regulation No. 7 dated July 13th, 2007) 168

Table 39- Analysis of assets and liabilities relating to contracts issued by insurance companies where the investment risk is borne by the policyholders and deriving from pension fund management (ISVAP Regulation No. 7 dated July 13th, 2007) 169

Table 40 - Sundry receivables 169

Table 41 – Other asset items 170

Table 42 - Other assets 171

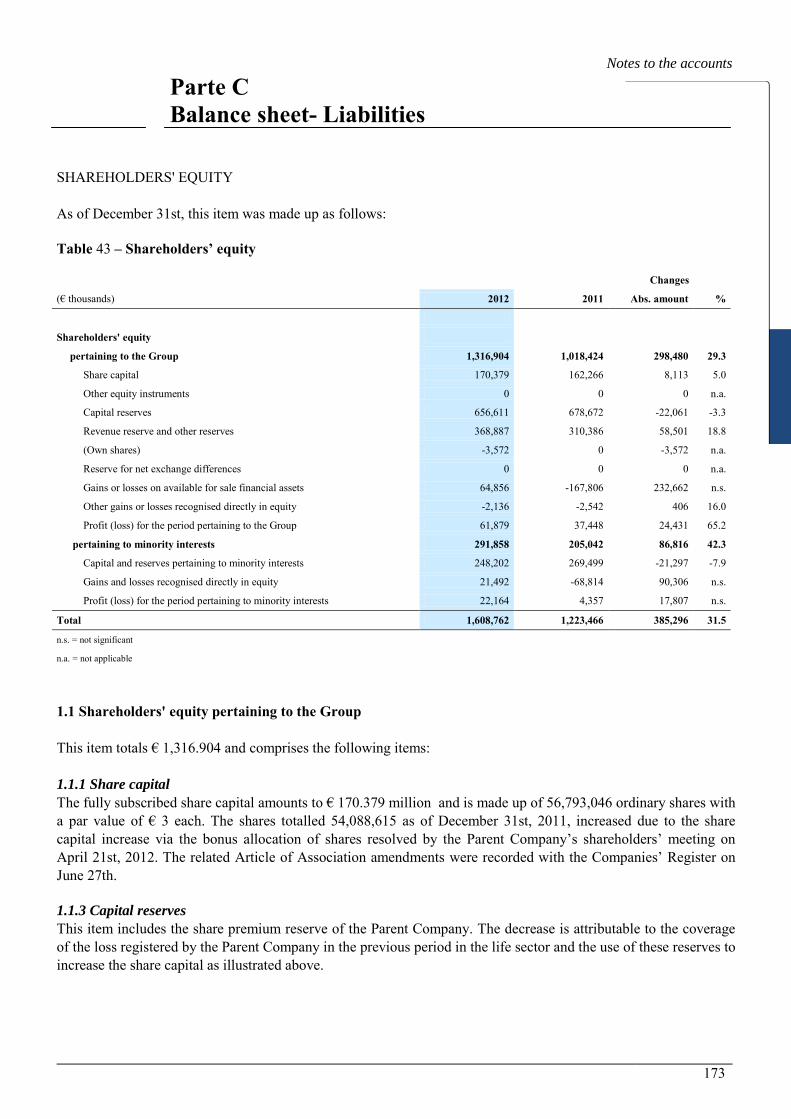

Table 43 – Shareholders’ equity 173

Table 44 – Provisions and allowances 174

Table 45 – Provisions and allowances – changes during the period 174

Table 46 – Analysis of technical provisions (ISVAP Regulation No. 7 dated July 13th, 2007) 176

Table 47 – Financial liabilities 177

Table 48 – Analysis of financial liabilities (ISVAP Regulation No. 7 dated July 13th 2007) 178

Table 49 - Payables 179

Table 50 – Employee severance indemnity and length-of-service bonus 180

Table 51 – Other liability items 180

Table 52 - Other liabilities 181

7

Table 53– Breakdown of direct and indirect gross premiums written class and by geographic area 183

Table 54 - Insurance business 184

Table 55 - Analysis of insurance operating expenses 184

Table 56 - Financial operations 185

Table 57 - Financial and investment income and charges (ISVAP Regulation No. 7 dated July 13th, 2007) 186

Table 58 – Income taxes for the year 188

Table 59 – Reconciliation of the tax rate – analysis 189

Table 60 - Analysis of the statement of other comprehensive income – net amounts (ISVAP Regulation No. 7 dated July 13th, 2007) 189

Table 61 – Income statement by sector of activities (ISVAP Regulation No. 7 dated July 13th, 2007) 190

Table 62 – Analysis of technical insurance items (ISVAP Regulation No. 7 dated July 13th, 2007) 191

Table 63 – Analysis of insurance operating expenses (ISVAP Regulation No. 7 dated July 13th, 2007) 191

Table 64 - Transactions with related parties 196

Group Structure and bank shareholdings

Key:

(*) Tua Assicurazioni wholly owns Tua Retail.

(**) 0.005% of the share capital of Cattolica Services is held individually by ABC Assicura, BCC Assicurazioni, BCC Vita, Berica Vita, Cattolica

Previdenza, C.P. Servizi Consulenziali, Duomo Uni One, Lombarda Vita, Risparmio & Previdenza and TUA Assicurazioni.

(***) Up until February 25th, 2013, the company name was Car Full Service.

Non-Life Operating services Life Banks Agricultural-real estate

property sector

49%

82%

BCC Vita

Berica Vita

Cattolica Life

Cattolica Previdenza

Lombarda Vita

Risparmio & Previdenza

ABC Assicura

BCC Assicurazioni

Duomo Uni One Assicurazioni

TUA Assicurazioni (*)

As at December 31st, 2012

Cattolica Immobiliare

Cattolica Services (**)

Cattolica Services Sinistri (***)

C. P. Servizi Consulenziali

Cassa di Risparmio di San Miniato

Prisma

Cattolica Agricola

Cattolica Beni Immobili

100%

25.07%

20%

100%

100%

99.95%

51%

NON LIFE LIFE OTHER

99.99%

97%

60%

51%

51%

60%

60%

100%

60%

97.58%

Cassa di Risparmio di Fabriano e Cupramontana

Banca Popolare S. Angelo

Emil Banca

UBI Banca

Banca di Valle Camonica

Banca Popolare di Vicenza

As at December 31st, 2012

BANK SHAREHOLDINGS

17.42%

0.42%

0.08%

0.92%

6.38%

0.46%

Reference Scenario

15

Macro-economic scenario

During the year, the crisis continued to weigh heavily on global markets, especially in Europe where the economic recession, aggravated by the policies for containing budget costs and by the rise in the costs of refinancing the public deficit became increasingly pressing. This was joined by the implicit default of Greece which further eroded the confidence of investors and contributed towards heavily reducing the economic growth estimates. In order to contrast the deteriorating situation, the European Central Bank initially increased the liquidity extraordinary measures for the banking system by means of a second LTRO transaction (long-term refinancing operation) over 3 years. The worsening of the crisis and the difficulty of the European authorities to provide swift responses, forced the board to adopt an expansive monetary policy during the Summer, cutting the rates in the second quarter by 25 bp, taking them to the all time low of 0.75% and launching additional extraordinary liquidity measures for the banking system. The most important of these measures was the OMT (Outright Monetary Transaction) or rather the programme for the repurchase of short-term government securities of countries in difficulty, subject to the signing of a memorandum with the manoeuvres for the containment of the debt which the rescued government will have to implement. In Italy, the crisis deteriorated further, with a collapse in the confidence indexes and a significant reduction in industrial production which pushed the country into a deep recession. Despite the efforts linked to the containment of the public deficit, the concern of international investors with regard to the staying power of the single currency brought the levels of the spread to the all-time high values already seen in 2011. Only the intervention of the European Central Bank and the completion of a series of important reforms on the employment market carried out by the Monti government made it possible to temporarily brighten up the situation. The US economy disclosed a trend in line with expectations, featuring under potential economic growth. Positive contributions came from internal demand, aided by the increase in employment level in the private sector, from the real estate property market (even if still at contained levels) and from the cycle of stock of the manufacturing sector. At the same time however, industrial activities slowed down even further due to the reduction in exports and the November elections curbed the budget adjustment manoeuvres. Therefore, the Federal Reserve continued its expansive monetary policy, launching two additional repurchase operations on g overnment securities in order to ensure the system ample liquidity and changing the tax policy targets for the coming years. In Japan, the economy suffered a heavy slowdown in consequence of the reduction in Chinese demand. The new prime minister declared a new expansive policy so as to keep the Japanese economy competitive. By contrast, among emerging countries an essential slowdown was seen in economic activities, mainly due to the considerable re-balancing of the budget flows (China and South East Asia), the lack of structural reforms (India) and the crisis in the main economic sector (Brazil). Global inflation disclosed significant symptoms of a slowdown. Bond markets Despite the numerous downgrades registered on global governmental issues, on t he bond market the return on ten-year government securities of the core countries (Germany, USA and UK) remained at minimum levels, albeit with a partial recovery in the second half of the year,

Reference Scenario

16

both for the US (1.77%) and for the German (1.38%) yield curve, while the short-term maturities reported close to zero nominal rates and in some cases even negative ones. Volatility was high in 2012, following the mentioned above policy delays. After an initial part of the year when the effect of the abundant liquidity on markets led to a significant contraction in the returns of the curves, the second and third quarters saw an abnormal trend involving a widening of the spread between the return on government securities of the peripheral European countries with respect to German Bunds, with record levels on all the curves. From August onwards, the intervention of the European Central Bank and greater concreteness of the Eurogroup decisions, for the purpose of achieving a fiscal and banking union, led to a contraction on the spreads close to record lows for the year. In contrast, the attention of the operators was concentrated above all else on the corporate bonds market which saw an explosion at record levels of the issues both for the investment grade component and for the high-yield market, with an increase in the portfolio risk. Stock markets The stock markets saw great volatility, guided above all else by the economy trend expectations and the European crisis. The share lists maintained a fluctuating trend for the whole of the first half of the year, while from June onwards the evident underweight of the investors and the conviction of the operators that the Euro Zone could tangibly resolve the problems led buyers to return in a more decisive manner to the market attracted by high dividends paid. On an annual basis, in the USA, the S&P 500 i ndex closed at +13.40% and the Nasdaq at +15.90%, while in Europe the Dax closed at +29.06%, the Eurostoxx50 at +13.79% and the FTSEMIB at +7.84%. In Asia, the Hang Seng index rose 22.9% and the Nikkei closed with a gain of 22.94%. Foreign exchange market The fears of an economic recession in Europe led the Euro to lose value both against the Dollar, with depreciation of 3%, and against the Yen, which gained 8.74% on the single currency. The Fed’s decision to keep the market extremely liquid for a long period made it possible for the Dollar to devaluate also against the Japanese currency by 5.91%.

17

Insurance industry

The graphs below show certain summary figures published by ANIA1 for the insurance industry for the period 2007-2011.

4.7%

-2.9%

3.0%

-0.5%

-3.0%

5.5%

-2.2%

3.4%

-0.6%

-3.4%-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2007 2008 2009 2010 2011

Key indicatorsInsurance sector

%

Technical result/direct and indirect premiums Net income/direct and indirect premiums On the basis of the IVASS Statistics on gross premiums written through the fourth quarter of 2012, published on March 6th, 2013, overall premiums written in the life and non-life classes by Italian insurance companies and by representative agencies in Italy of companies from outside the E.E.A. during 2012 amounted to € 105,109.4 million, with a decrease of 4.6% with respect to 2011 (-7.4% in real terms), which follows the -12.5% registered in that year with respect to 2010 (when the amount of the premiums written had reached an all-time high).

1 Source ANIA - L’assicurazione italiana nel 2011-2012, page 317, publication dated June 25th, 2012.

61,555 54,829

81,409 90,592

73,869

35,471

34,327

33,790

33,054

36,363

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2007 2008 2009 2010 2011

Direct and indirect Life premiums Direct and indirect Nonlife premiums

Key economic indicatorsof the Insurance sector

€/millions

18

In detail, life premiums, equating to € 69,707.2 million, reported a decrease of 5.6% (-8.4% in real terms), and an incidence on the overall life and non-life portfolio which came to 66.3% (67% in 2011); the non-life portfolio, which came to 35,402.2 million, decreased 2.6% (-5.5% in real terms), with an incidence of 33.7% on the overall portfolio (33% in 2011). The same changes calculated on a consistent basis (or rather also excluding from the 2011 total premiums written the ones of three companies which left the Italian direct business portfolio in 2012), reveal - for the Italian insurance companies and representative agencies in Italy of companies from outside the E.E.A. - a drop in total premiums written (life and non-life), for the life classes and the non-life classes equating, respectively, to 4.3%, 5.5% and 1.9% (in real terms the reduction on a consistent basis in premiums written came to 7.1%, 8.3% and 4.8%). Premiums written as a percentage of GDP in 2012 came to 6.71% (down with respect to the 6.98% in 2011); in detail, the drop was attributable to the life classes, where the percentage of GDP came to 4.45% (4.68% in 2011), while it came to 2.26% for the non-life classes (down slightly with respect to the 2.30% in 2011). With regard to the figures relating to premiums written in the life classes, Class I (insurance on the duration of human life) with € 51,087.5 million, reported a decrease of 9.7% compared with 2011; Class III (insurance whose main benefits are directly linked to the value of UCIT units or internal funds or indexes or other reference values) with € 13,799.9 million, increased 10.5% with respect to 2011; premiums written for Class V (capitalization transactions) amounted to € 2,814.4 million, a decrease of 10.1%. These classes as a percentage of total life premiums represent 73.3%, 19.8% and 4% respectively (76.6%, 16.9% and 4.2% respectively in 2011). With regard to the remaining classes, the premiums of Class VI (pension funds: € 1,85 5.7 million, involving a decrease of 22.7% when compared with 2011) represented 2.7% of the life portfolio (2% in 2011). Premiums written relating to Class IV insurance (Long-term non-cancellable health insurance: € 43.2 million) and supplementary insurance (€ 106.6 million) in conclusion represented the remaining 0.2% of total life premiums (as in 2011). With reference to assets managed for pension funds, overall these came to € 11,696.1 million, involving an increase of 17.2% with respect to the end of 2011. The breakdown by sales channels of premiums written discloses that bank and post office branches broker 48.6% of the life portfolio (down by around six percentage points with respect to the 54.8% in 2011), financial advisors 23.3% (up by five percentage points with respect to the 18.3% in 2011), agencies with mandate 16.3% (stable with respect to the 16.4% in 2011), agencies managed directly and subsidiaries 10.3% (compared with 9.2% in the same period of 2011), brokers 1.1% (compared with 1% as in 2011) and other forms of direct sale 0.4% (compared with 0.3%, as in 2011). With reference to the trend of the non-life classes, the premiums portfolio of the TPL land motor vehicles and TPL ships (sea and inland water vessels) classes amounted in total to € 17,576.1 million, presenting a drop of 1.2% with respect to 2011, with an incidence of 49.6% on total non-life classes (48.9% in 2011) and 16.7% on total premiums (16.1% in 2011). With regard to the other classes, those with the highest business, and therefore the highest percentage in terms of the total, are: accident and injury, with 8.4% (as in 2011), TPL general,

19

with 8.3% (8.1% in 2011), land vehicle hulls, with 7.5% (8% in 2011), other damage to assets, with 7.4% (7.3%), fire and natural forces, with 6.5% (6.4% in 2011) and health, with 6% (as in 2011). Analysis by distribution channel continues to highlight the preponderance of premiums written via agencies with mandate, even if these continue to drop slightly with respect to previous figures. In conclusion, this channel places 81.3% of the non-life portfolio (81.6% in 2011) and 87.2% of the portfolio relating to just the motor TPL class (88% in 2011). Lastly, mention should be made of the slight rise in the portion brokered by other forms of direct sale, both with regard to the non-life portfolio (5.2% compared with 4.7% in 2011), and with reference to just the motor TPL class (7.9% compared with 6.9% in 2011). On the basis of the afore-mentioned figures, the Group’s market share in the non-life sector would rise from 4.5% to 4.8% and in the life sector would drop from 3.1% to 2.8%.

4.5 4.8

3.12.8

3.6 3.5

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2011 2012

Total Group market share%

Non life Life Total

Management Report

Management Report The Group in 2012 Business performance for the period Risk management Employees and sales network Significant events and other information

Management Report

25

The Cattolica Group closed the year with consolidated profit of € 84 million compared with € 41.8 million in the previous year. The Group’s net result came to € 61.9 million (€ 37.4 million at December 31st, 2011). Excluding the extraordinary effects, the consolidated profit would have come to € 95 million, and the Group net result € 78 million. Despite the continuation of the difficult economic situation and the instability of the financial markets in the Euro Zone due to heavy tension on sovereign debts, the improvement in business operations of the non-life classes continued with a combined ratio of retained business which dropped from 96.9% in December 2011 to 95.7%; the latter figure, excluding the effects of the earthquake which hit Emilia Romagna in May, came to 94.7%. Premiums written for the direct non-life business classes rose by 3.6% also due to the on-going productive commitment of the agencies confirming the strategy implemented over the last few years, enhancing and consolidating the sales network as the backbone for the Group’s growth. Life premiums written were affected by the decrease in the market and dropped 14.8%, passing from € 2,319.2 million to € 1,976 m illion, with premiums in the traditional segment for € 1,307.6 million, unit and index-linked premiums for € 203.5 million, capitalisation for € 318.7 million and pension funds for € 146.2 million. Financial operations2 closed with a result, gross of the tax effects, amounting to € 542.2 million as against € 259 .5 million in the previous year, mainly as a result of the additional income interest from which rose from € 410.3 m illion to € 432.7 million, of the increase in other net incomes realised which rose from € 12.8 million to € 89.6 m illion and of the reduction in losses from valuation on financial assets from € 181.1 million to € 21.9 million. Overall, this consolidated result was affected by € 48 million in impairment losses on the financial investments portfolio3 and on goodwill. As at December 31st, investments amounted to € 15,938.7 million (€ 15,094.5 million as at December 31st, 2011) and technical provisions net of the reinsurance amount together with financial liabilities relating to investment contracts came to € 15,010.9 m illion (€ 14,945.5 million as at December 31st, 2011). Consolidated shareholders’ equity amounted to € 1,608.8 million (€ 1,223.5 million as at December 31st, 2011) and the Group’s solvency margin came to 1.61 times the regulatory minimum4 compared with 1.25 times as at December 31st, 2011.

*****

2With the exclusion of investments whose risk is borne by the policyholders and the change in other financial liabilities. 3 Net of tax effects and shadow accounting. 4 Prior to the Parent Company’s dividend payment proposal. It is hereby disclosed that the Parent Company does not apply the IVASS anti-crisis regulations. Taking into account the dividend proposal, the solvency margin comes to 1.55 times the regulatory minimum.

The Group in 2012

26

Significant corporate events which characterised 2012 included the purchase, for a value of € 76 million, of the agricultural-real estate complex “Tenuta Cà Tron”, covering a surface area of more than 1,000 hectares, via two specifically-created companies, Cattolica Agricola and Cattolica Beni Immobili, and the renewal in December of the strategic partnership agreement with Banca Popolare di Vicenza, extending the expiry date until 2022. The renewed agreement, linked to the changed market context, confirms and consolidates the collaboration launched between the two Groups in 2007, focusing on the growth of the insurance companies in the partnership. The agreement confirms the exclusive commitments in force for the distribution of Cattolica Group products via the network of the Banca Popolare di Vicenza Group, which at December 31st, had 640 branches.

KEY INDICATORS OF CATTOLICA GROUP BUSINESS PERFORMANCE

The tables which follow show the most significant performance indicators, the figures concerning employees and the sales network, the reclassified consolidated statement of financial position and income statement, the consolidated income statement reclassified by segment of activities and the key indicators as co mpared to those of the previous year, respectively, in accordance with the international accounting standards. In these consolidated financial statements, the term “premiums written” means the sum total of the insurance premiums (as defined by IFRS 4) and the amounts relating to investment contracts (as defined by IFRS 4 which refers the related discipline to IAS 39).

Management Report

27

Table 1 – Key economic indicators

Changes

(€ thousands) 2012 2011 Abs. amount %

Total premiums written 3,676,670 3,960,534 -283,864 -7.2

of which

Gross premiums written 3,539,070 3,778,268 -239,198 -6.3

Direct business - non-life 1,685,444 1,626,769 58,675 3.6

Direct business – life 1,838,422 2,136,936 -298,514 -14.0

Indirect business - non-life 15,103 14,453 650 4.5

Indirect business – life 101 110 -9 -8.2

of which

Investment contracts 137,600 182,266 -44,666 -24.5

Consolidated net profit for the period 84,043 41,805 42,238 n.s.

Group net profit for the period 61,879 37,448 24,431 65.2

n.s. = not significant

Table 2 – Key equity indicators

Changes

(€ thousands) 2012 2011 Abs. amount %

Investments 15,938,701 15,094,533 844,168 5.6

Technical provisions net of reinsurance amount 14,054,067 13,941,214 112,853 0.8

Financial liabilities relating to investment contracts 956,861 1,004,277 -47,416 -4.7

Consolidated shareholders' equity 1,608,762 1,223,466 385,296 31.5

28

Table 3 – Sales network and headcount

Changes

(number) 2012 2011 Abs. amount %

Direct network:

Agencies 1,391 1,398 -7 -0.5%

including non-exclusive agencies 349 331 18 5.4%

Partner networks:

Bank branches 5,967 5,990 -23 -0.4%

Financial advisors 879 973 -94 -9.7%

Welfare and pension product advisors 30 46 -16 -34.8%

C.P. Servizi Consulenziali subagents 295 217 78 35.9%

Headcount prior to BPVI Fondi SGR spin-off (*) 1,451 1,470 -19 -1.3%

Employees acquired with BPVI Fondi SGR spin-off 9 0 9

Total headcount 1,460 1,470 -10 -0.7%

Full-Time Equivalent headcount prior to BPVI Fondi SGR spin-off (*) 1,397 1,410 -13 -0.9%

FTE employees acquired with BPVI Fondi SGR spin-off 9 0 9

FTE headcount 1,406 1,410 -4 -0.3%

(*) on March 14th, the deed for the partial non-proportionate spin-off of BPVI Fondi SGR within Cattolica Immobiliare was finalised; the business segment was subsequently spun-off to Cattolica Assicurazioni with effect as at December 31st, 2012.

Management Report

29

Table 4 – Reclassified consolidated statement of financial position

Changes Items from obligatory

statements (*) (€ thousands) 2012 2011 Abs. amount %

Assets

Investment property 172,935 157,958 14,977 9.5 4.1

Property 94,747 18,778 75,969 n.s. 2.1

Investments in subsidiaries, associates and joint ventures 82,197 103,108 -20,911 -20.3 4.2

Loans and receivables 1,239,353 1,516,516 -277,163 -18.3 4.4

Held to maturity investments 287,193 285,481 1,712 0.6 4.3

Available for sale financial assets 9,739,824 8,512,235 1,227,589 14.4 4.5

Financial assets at fair value through profit or loss 3,714,741 4,093,219 -378,478 -9.2 4.6

Cash and cash equivalents 607,711 407,238 200,473 49.2 7

Investments 15,938,701 15,094,533 844,168 5.6

Intangible assets 310,467 327,612 -17,145 -5.2 1

Technical provisions - reinsurance amount 673,367 640,453 32,914 5.1 3

Sundry receivables, other tangible assets and other asset items 1,525,999 1,858,993 -332,994 -17.9 (**)

TOTAL ASSETS 18,448,534 17,921,591 526,943 2.9

Liabilities and shareholders' equity

Group capital and reserves 1,255,025 980,976 274,049 27.9

Group profit for the year 61,879 37,448 24,431 65.2 Shareholders' equity pertaining to the Group 1,316,904 1,018,424 298,480 29.3 1.1

Capital and reserves pertaining to minority shareholders 269,694 200,685 69,009 34.4

Profit for the period pertaining to minority shareholders 22,164 4,357 17,807 n.s. Net shareholders' equity pertaining to minority shareholders 291,858 205,042 86,816 42.3 1.2

Total capital and reserves 1,608,762 1,223,466 385,296 31.5 1

Provision for unearned premiums 701,539 625,694 75,845 12.1

Provision for outstanding claims 2,312,178 2,331,070 -18,892 -0.8

Gross technical provisions - non-life 3,013,717 2,956,764 56,953 1.9 3

Gross technical provisions - life 11,365,658 11,298,929 66,729 0.6 3

Other gross non-life technical provisions 2,202 2,300 -98 -4.3 3

Other gross life technical provisions 345,857 323,674 22,183 6.9 3

Financial liabilities 1,264,398 1,254,072 10,326 0.8 4 of which deposits from policyholders 956,861 1,004,277 -47,416 -4.7

Allowances, payables and other liability items 847,940 862,386 -14,446 -1.7 (***)

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 18,448,534 17,921,591 526,943 2.9 (*) Indicates the items of the statements in the consolidated financial statements as per ISVAP regulation No. 7 of July 13th, 2007 (**) Sundry receivables, other asset items, and other tangible assets (balance sheet items under assets = 5 + 6 + 2.2) (***) Allowances, payables and other liability items (balance sheet items under liabilities = 2 + 5 + 6) n.s. = not significant

30

Table 5 – Reclassified consolidated income statement

Changes Items from obligatory

statements (*) (€ thousands) 2012 2011 Abs. amount % Net premiums 3,161,876 3,439,405 -277,529 -8.1 1.1

Net charges relating to claims -3,218,839 -3,194,241 -24,598 -0.8 2.1

Operating expenses -441,160 -441,508 348 0.1 of which commission and other acquisition costs -304,786 -305,869 1,083 0.4 2.5.1 of which other administrative expenses -136,374 -135,639 -735 -0.5 2.5.3

Other revenues net of other costs (other technical income and charges) -48,183 -9,897 -38,286 n.s. 1.6 - 2.6 Net income deriving from financial instruments at fair value through profit or loss 227,864 26,935 200,929 n.s. 1.3

of which class D 214,041 16,843 197,198 n.s. Net income deriving from investments in subsidiaries, associates and joint ventures -3,662 -15,693 12,031 76.7 1.4 - 2.3

Net income deriving from other financial instruments and investment property 567,871 280,993 286,878 n.s. 1.5 - 2.4

of which net interest 432,729 410,308 22,421 5.5 1.5.1 - 2.4.1 of which other income net of other charges 47,674 36,404 11,270 31.0 1.5.2 - 2.4.2 of which net profits realised 89,629 12,777 76,852 n.s. 1.5.3 - 2.4.3 of which net valuation profits on financial assets -21,894 -181,114 159,220 87.9 1.5.4 - 2.4.4 of which changes in other financial liabilities 19,733 2,618 17,115 n.s. 1.5.4 - 2.4.4

Commission income net of commission expense -27 1,132 -1,159 n.s. 1.2 - 2.2

Operating expenses relating to investments -16,120 -14,382 -1,738 -12.1 2.5.2 RESULT OF INSURANCE BUSINESS AND FINANCIAL OPERATIONS 229,620 72,744 156,876 n.s.

Other revenues net of other costs (excluding other technical income and charges included under insurance operations)

-70,781 -51,759 -19,022 -36.8 1.6 - 2.6

PRE-TAX PROFIT FOR THE PERIOD 158,839 20,985 137,854 n.s.

Taxation -74,796 20,804 -95,600 n.s. 3

NET PROFIT FOR THE PERIOD 84,043 41,789 42,254 n.s.

PROFIT (LOSS) FROM DISCONTINUED OPERATIONS 0 16 -16 -100.0 4

CONSOLIDATED PROFIT (LOSS) FOR THE PERIOD 84,043 41,805 42,238 n.s.

Profit for the period pertaining to minority shareholders 22,164 4,357 17,807 n.s.

PROFIT FOR THE PERIOD PERTAINING TO THE GROUP 61,879 37,448 24,431 65.2 n.s. = not significant

Management Report

31

Table 6 – Reclassified consolidated income statement by segment of activities

NON-LIFE LIFE OTHER TOTAL

(€ thousands) 2012 2011 2012 2011 2012 2011 2012 2011

Net premiums 1,374,395 1,362,054 1,787,481 2,077,351 0 0 3,161,876 3,439,405

Net charges relating to claims -946,102 -990,681 -2,272,737 -2,203,560 0 0 -3,218,839 -3,194,241

Operating expenses -337,954 -328,504 -103,206 -113,001 0 -3 -441,160 -441,508 of which commission and other acquisition costs -247,123 -236,031 -57,663 -69,838 0 0 -304,786 -305,869 of which other administrative expenses -90,831 -92,473 -45,543 -43,163 0 -3 -136,374 -135,639

Other revenues net of other costs (other technical income and charges) -31,670 -230 -16,513 -9,667 0 0 -48,183 -9,897

Net income deriving from financial instruments at fair value through profit or loss -8,065 1,551 235,929 25,384 0 0 227,864 26,935

of which class D 214,041 16,843 214,041 16,843

Net income deriving from investments in subsidiaries, associates and joint ventures -372 -9,430 -3,290 -6,263 0 0 -3,662 -15,693

Net income deriving from other financial instruments and investment property 93,580 21,773 468,089 252,620 6,202 6,600 567,871 280,993

Commission income net of commission expenses -16 -57 -11 1,189 0 0 -27 1,132 Operating expenses relating to investments -3,211 -3,523 -7,037 -6,444 -5,872 -4,415 -16,120 -14,382 RESULT OF INSURANCE BUSINESS AND FINANCIAL OPERATIONS 140,585 52,953 88,705 17,609 330 2,182 229,620 72,744 Other revenues net of other costs (excluding other technical income and charges included under insurance operations) -46,283 -35,638 -24,852 -15,792 354 -329 -70,781 -51,759

PRE-TAX PROFIT FOR THE PERIOD 94,302 17,315 63,853 1,817 684 1,853 158,839 20,985

Taxation -47,460 23,227 -27,302 -2,531 -34 108 -74,796 20,804

NET PROFIT FOR THE PERIOD 46,842 40,542 36,551 -714 650 1,961 84,043 41,789 PROFIT (LOSS) FROM DISCONTINUED OPERATIONS 0 16 0 0 0 0 0 16

CONSOLIDATED PROFIT (LOSS) FOR THE PERIOD 46,842 40,558 36,551 -714 650 1,961 84,043 41,805

32

Table 7 – Key indicators

2012 2011

Non-life ratios for retained business Claims ratio (Net charges relating to claims / Net premiums) 68.8% 72.7% G&A ratio (Other administrative expenses / Net premiums) 6.6% 6.8% Commission ratio (Acquisition costs / Net premiums) 18.0% 17.3% Total Expense ratio (Operating expenses / Net premiums) 24.6% 24.1% Combined ratio (1 - (Technical balance / Net premiums)) 95.7% 96.9% Non-life ratios for direct business Claims ratio (Net charges relating to claims / Premiums for the period) 69.5% 72.4% G&A ratio (Other administrative expenses / Premiums for the period) 5.6% 5.8% Commission ratio (Acquisition costs / Premiums for the period) 18.9% 18.5% Total Expense ratio (Operating expenses / Premiums for the period) 24.5% 24.2% Combined ratio (1 - (Technical balance / Premiums for the period) 96.1% 96.8% Life ratios G&A ratio (Other administrative expenses / Premiums written) 2.3% 1.9% Commission ratio (Acquisition costs / Premiums written) 2.9% 3.0% Total Expense ratio (Operating expenses/ Premiums written) 5.2% 4.9% Total ratios G&A ratio (Other administrative expenses / Premiums written) 3.7% 3.4% Note: "Total premiums written" in the life business refer to the amount of gross insurance premiums and of the investment contracts

Management Report

33

WAYS IN WHICH THE GROUP IMAGE AND INFORMATION ARE DISCLOSED

The Social report

Each year the Company publishes the Social Report which is drawn up in accordance with the GBS standard. The first section (identity) proposes the distinctive values of the Company. In the second section (economic data), the Group’s corporate activities are represented in quantitative terms. The crux of the social report is found in the third section (corporate relationship), where a detailed map of the stakeholders outlines the overall picture of the corporate relations.

The Investor Relations Division

The Investor Relations Division maintained an on-going dialogue with the financial community, involving relations marked by clarity and transparency, in order to ensure the market visibility on the results and on the strategies of the Group. There are four companies which follow and publish analysis and reports on Cattolica stock; individual meetings are periodically organised with the analysts so as to look in-depth at the economic-business trend. On July 11th, Carlo Ferraresi was appointed as the new Finance Director and Investor Relations Manager of the Cattolica Group. Mr. Ferraresi comes from Crédit Agricole Corporate & Investment Bank where he covered the role of Managing Director and gained important technical and managerial experience. He has covered important roles both in the finance field and in the insurance and reinsurance sectors in Italy and in the UK.

Rating In January, Standard & Poor’s lowered the ratings of 16 countries in the Euro Zone, including Italy with a decrease of two notches from A to BBB+ with a negative outlook. Consequently, the agency adopted the same rating action for 15 European insurance companies including the Cattolica Group. On January 27th, the agency in fact took the Group’s rating to “BBB” with a negative outlook in line with its view that the persistence of an unfavourable economic and financial market trend in Italy and the Euro Zone could influence the capitalisation of the company. On October 3rd, the rating agency confirmed Cattolica’s rating as BBB, confirming the strong operating performance of the non-life business, the maintenance of a consolidated market position and the ability of management to achieve the results. The outlook remains negative given the continuation of a still uncertain economic and financial context.

Management Report The Group in 2012 Business performance for the period Risk management Employees and sales network Significant events and other information

Management Report

37

A BRIEF OUTLINE OF THE BUSINESS PERFORMANCE

The Group by main financial statement aggregates

Sectors of business

The Group’s activities are divided up into three business segments: life, non-life and other. The core business of the Group, headed up by Cattolica Assicurazioni, a company which is involved in both life and non-life business, is divided up between the non-life segment (ABC Assicura, BCC Assicurazioni, Car Full Service, C.P. Servizi Consulenziali for the Cattolica and TUA Assicurazioni mandate, Duomo Uni One Assicurazioni, hereinafter “Duomo Uni One”, and TUA Assicurazioni) and the life segment (BCC Vita, Berica Vita, Cattolica Life, Cattolica Previdenza, C.P. Servizi Consulenziali for the Cattolica Previdenza Vita mandate, Lombarda Vita, Risparmio & Previdenza). The other activities include the agricultural-real estate services of Cattolica Agricola and Cattolica Beni Immobili and the operating services of Cattolica Services and Cattolica Immobiliare, instrumental in the performance of the Group’s activities. For an analysis of the result by segment of business, reference should be made to Table 6, where each segment is represented net of the intersectorial adjustments. The notes to the accounts contain tables relating to the operating segments envisaged by ISVAP Regulation No. 7 dated July 13th, 2007 (gross of eliminations between sectors).

Profit for the year

The year closed with consolidated net profit of € 84 million, of which € 46.8 million attributable to the non-life business (€ 40.6 million in 2011), € 36.6 million attributable to the life business (€ 714 thousand loss in 2011), and € 650 t housand pertaining to the “other” segment (€ 2 million in 2011). The Group’s net profit came to € 61.9 million (€ 37.4 million in 2011).

Premiums Gross consolidated premiums (which therefore comply with the definition of insurance policy as per IFRS 4) at the end of the accounting period amounted to € 3,539.1 million. Also taking into account investment contracts, total premiums written came to € 3,676.7 m illion, disclosing a decrease of € 283.9 million (-7.2%) compared with the previous year, attributable to life premiums.

Business performance for the period

38

1,627 1,686

2,319

1,976

15 15 0

400

800

1,200

1,600

2,000

2,400

2,800

2011 2012

Direct Non life premiums Direct Life premiums Indirect premiums (Life and Non life)

Direct Life and Non life premiums, indirect premiums

€/millions

Gross direct non-life premiums totalled € 1,685.4 million, registering an increase of 3.6% and account for 47.8% of total direct premium business (43.2% in 2011). Gross direct life premiums totalled € 1,83 8.4 million (€ 2,136.9 million in 2011); total premiums written amounted to € 1,976 million (-14.8%). Life insurance policies represented the majority share of total direct business (52.2% in 2012 compared with 56.8% in 2011).

Direct premiums written are divided up as follows by sales channel: agencies 47.6%, banks 35.2%, brokers 7%, welfare and pension product advisors 0.3%, financial advisors 0.2% and other channels 9.7%.

1,743

1,289

255 18

356

Agencies Banks Brokers Financial & Pension Advisors Other channels

Direct premiums by channel€/millions

Other administrative expenses

Other administrative expenses amount to € 136.4 million compared with € 135.6 million, essentially in line with the previous year. The ratio of other administration expenses to total insurance premiums written came to 3.7%, compared with 3.4% in 2011, mainly as a result of the drop in premiums written.

Management Report

39

The Group by segments

Non-life business

The non-life business ended the period with net premiums of € 1,374.4 million, compared with € 1,362.1 million last year (+0.9%). The combined ratio net of reinsurance dropped to 95.7%, compared with 96.9% as at December 31st, 2011 and was characterised by the decrease in the claims ratio which fell from 72.7% to 68.8%, despite the negative effects deriving from the earthquake in Emilia Romagna and the decrease in the incidence of other administrative expenses which fell from 6.8% to 6.6% in 2011. Financial operations were characterised by net income deriving from other financial instruments and investment property for € 93.6 million, compared with € 21.8 million in 2011, involving an increase in income on sales which amounted to € 26.6 m illion compared with -€ 1.8 million in 2011, w ith net losses from valuation which rose from € 44.5 m illion to € 6. 1 million and net interest which increased from € 61.8 million to € 68.8 million. The non-life business ended the period with a profit of € 46.8 million, compared with € 40.6 million as at December 31st, 2011.

Life business Life business was characterised by a decrease in net life premiums which fell from € 2,077.4 million to € 1,787.5 million (-14%) and by the result of financial operations5 which improved, passing from € 247 million to € 459.9 million. Financial operations were characterised by net income deriving from other financial instruments and investment property for € 468.1 million, compared with € 252.6 million in 2011, involving an increase in income on sales which amounted to € 63.1 million compared with € 14 .5 million in 2011, with net income from valuation which rose from € -131.9 million to € 6.9 million and net interest which increased from € 351.3 million to € 366.9 million. The life business ended the period with a profit of € 36.6 million, compared with a loss of € 714 thousand as at December 31st, 2011.

Other business The result relating to the other segment at the end of the accounting period came to € 650 thousand, compared with € 2 million in 2011.

Sectors by geographic area

Written premiums, which are taken in Italy, are mainly concentrated in Central-Northern Italy, an area similar in terms of risk and return and therefore not significant for the purposes of the secondary segmentation envisaged by IFRS 8.

Investments Investments which include investment property, equity investments in subsidiaries, associates and joint ventures, loans and receivables, held to maturity investments, available for sale financial assets, financial assets at fair value through profit or loss, cash & cash equivalents and property used for operating purposes), amounted to € 15 ,938.7 million at year end compared with € 15,094.5 million in 2011 (+5.6%). In detail, investment property and properties used for operating activities amounted to € 267.7 million compared with € 176.7 million in 2011; equity investments in Group companies fell from € 103.1 m illion to € 82.2 million (-20.3%), mainly due to the B.P.Vi. Fondi SGR spin-off. Loans and receivables fell from € 1,516.5 m illion to € 1,239.4 million (-18.3%), held to maturity investments amounted to € 287.2 million (in line with December 31st, 2011),

5 With the exclusion of investments whose risk is borne by the policyholders and the change in other financial liabilities.

40

available for sale financial assets rose from € 8,512.2 million to € 9,739.8 million (+14.4%) and financial assets at fair value through profit or loss decreased from € 4,093.2 million to € 3,714.7 million (-9.2%). The result of financial operations, with the exclusion of investments whose risk is borne by the policyholders and gross of the tax effects and the change in other financial liabilities, came to € 542.2 million, compared with € 259.5 million in 2011.

Net income relating to other financial instruments and investment property amounted to € 567.9 million (€ 281 million as of December 31st, 2011), mainly due to the capital losses from valuation for € 21.9 million compared with € 181.1 million as at December 31st, 2011, net income from sales which passed from € 12.8 million to € 89.6 million and net interest which rose from € 410.3 million to € 432.8 million.

Technical provisions

Non-life technical provisions (premiums and claims) amounted to € 3,013.7 million, compared with € 2,956.8 million last year (+ 1.9%).

2,957 3,014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012

Non life technical provisions€/millions

Life technical provisions (mathematical provisions inclusive of shadow accounting) totalled €

11,365.7 million, compared with € 11,299 million at the end of the previous year. Also taking into account financial liabilities relating to investment contracts, the technical provisions and deposits relating to life business amounted to € 12,322.5 million, involving a decrease on 2011 of 0.2%.

11.299 11.366

1.004 957

0

3.500

7.000

10.500

14.000

17.500

2011 2012

Life technical provisions Life investment policies

12.303 12.323

Life technical provisions and investment contracts

€/millions

Management Report

41

Life technical provisions include the shadow accounting provision which takes into account the share of latent gains and losses on assets in segregated funds ascribable to policyholders.

Shareholders' equity

Consolidated shareholders’ equity at the end of the accounting period came to € 1, 608.8 million as against € 1,223.5 million in 2011. The Group’s shareholders’ equity amounts to € 1,316.9 million compared with € 1,018.4 million in 2011 (+29.3%) and includes gains on available for sale financial assets amounting to € 64.9 million, compared with losses for € -167.8 million at the end of the previous year. Portions of shareholders’ equity pertaining to minority shareholders amounted to € 291 .9 million compared with € 205 million last year and include gains on available for sale financial assets amounting to € 21.5 million, compared with € -68.8 million at the end of the previous year.

INSURANCE BUSINESS AND OTHER SECTORS OF ACTIVITIES

Summary of the activities carried out by the Group companies

At December 31st, the scope of consolidation comprised the insurance Parent Company, ten insurance companies, four service companies, two companies which carry out agricultural-real estate activities, three real estate property investment funds and one mutual equity fund. During the year, San Miniato Previdenza was merged by incorporation into the Parent Company and Cattolica Business School was merged by incorporation into Cattolica Services. The scope of consolidation includes Fondo Perseide for the first time, a closed-end real estate property mutual investment fund, and the two newcos, Cattolica Agricola and Cattolica Beni Immobili.

Società Cattolica di Assicurazione – Società Cooperativa, which operates throughout Italy in the life and non-life businesses, ideally targeting the medium/high range of the personal segment. It is the Parent Company of the following companies:

Non-life insurance companies

• ABC Assicura, is authorized to carry out non-life business and distributes its products using the network of branches of the Banca Popolare di Vicenza Group. The Parent Company holds 60% of the share capital;

• BCC Assicurazioni, is authorized to carry out non-life business and distributes its products

using the network of branches of the ICCREA Group. The Parent Company holds 51% of the share capital;

• Duomo Uni One Assicurazioni, is authorised to carry out non-life business. Following the

spin-off into Cattolica, which took place in April 2011, the insurance portfolio relating to an agency, the key account policy portfolio and the portfolio relating to indirect business remained with the company. The Parent Company holds 99.99% of the share capital;

• TUA Assicurazioni, carries out insurance activities in the non-life segment, offering the

42

market a sp ecialist range of insurance and financial products/services able to meet the needs of personal line customers. The Parent Company holds 97% of the share capital.

Life assurance companies

• BCC Vita is authorized to carry out life insurance activities and distributes its products via the branches of the ICCREA Group. It is controlled by Cattolica via a 51% holding;

• Berica Vita, is authorized to carry out life insurance activities and distributes its products

using the network of branches of the Banca Popolare di Vicenza Group. The Parent Company holds 60% of the share capital;

• Cattolica Life Limited, is a l ife insurance company with registered office in Dublin,

Ireland, specialised in the structuring of index and unit linked policies by customer segments. The Parent Company holds 60% of the share capital;

• Cattolica Previdenza. The company is authorised to carry out life insurance activities and

non-life activities in relation to just the accident, injury and health classes within the sphere of pension & welfare products and collective assistance. It avails itself of leading brokerage firms, 30 pe nsion and welfare product consultants and, with the launch of C.P. Servizi Consulenziali’s activities, a network of 321 sub-agents. On May 15th, with reference to the provisions originally agreed on, the Parent Company acquired the residual holding of 19.86% from Intesa Sanpaolo Vita thereby achieving complete possession of the share capital;

• Lombarda Vita. The company is authorised to carry out life insurance activities,

distributing them via the network of branches of the UBI Banca Group. The Parent Company holds 60% of the share capital;

• Risparmio & Previdenza, carries out life insurance activities and is active in the non-life

segment, limited to accident and injury and health, in order to offer a complete range of pension and welfare products, availing itself of the branches of the UBI Banca Group, Banca di Torre del Greco and other banks. It is owned by Cattolica which has a holding of 97.58%, following the acquisition in May of a further holding of 2.4% from Banco di Brescia.

Companies of the other segment

Agricultural-real estate property companies

• Cattolica Agricola, was established on September 28th, by Cattolica, the sole shareholder, with initial capital of € 120 thousand fully paid, within the sphere of the purchase of the property complex known as “Tenuta Ca’ Tron”. It is a single-member limited liability company which has the exclusive purpose of carrying out agricultural activities pursuant to Article 2135 of the Italian Civil Code;

• Cattolica Beni Immobili, was established on September 28th, by Cattolica, the sole

shareholder, with initial capital of € 120 thousand fully paid-in, within the sphere of the purchase of the property complex known as “T enuta Ca’ Tron”. It is a si ngle-member limited liability company which is destined to manage the properties not used for

Management Report

43

agricultural activities existing on the land.

Closed-end real estate property funds

• Fondo Euripide, is a cl osed-end real estate property mutual investment fund to which Cattolica Immobiliare transferred all the properties and which, in December, acquired Palazzo Biandrà in Piazza Cordusio, Milan. Cattolica holds an interest of 41.63%, Berica Vita 10.18%, Cattolica Previdenza 2.04%, Lombarda Vita 45.47%, and Tua Assicurazioni 0.68%;

• Fondo Macquarie Office Italy, is a cl osed-end real estate property mutual investment

fund which was wholly acquired by the Group companies. It owns the property complex City Central in Via Lepetit, Milan. Cattolica holds an interest of 61.83%, BCC Vita 10.36%, Cattolica Previdenza 4.14%, Lombarda Vita 17.75%, and Risparmio & Previdenza 5.92%;

• Fondo Perseide, is a m utual fund dedicated to investment in renewable energies. On

October 4th, it acquired the first two photovoltaic plants for a value of € 9.35 million.

Closed-end equity funds

• Fondo Networth, is a closed-end mutual investment equity fund reserved for qualified investors who invests mainly in companies active on the market of energy production from renewable sources. Cattolica has a holding of 99.76%.

Service companies

• Cattolica Immobiliare carries out consulting and management activities for the real estate property assets. On April 1st, the partial, non-proportionate spin-off of B.P.Vi. Fondi SGR into Cattolica Immobiliare was finalised; the latter consequently changed its corporate name intto Cattolica Gestione Investimenti S.p.A.. On May 15th, Cattolica’s Board of Directors approved the partial spin-off project for the spin-off of Cattolica Gestione Investimenti in favour of the same. The transaction, having obtained the necessary authorisations from the competent authorities and the legal deadlines having elapsed, was finalised on December 27th and was effective since December 31st with the consequent return to its previous name. It is wholly-owned by Cattolica;

• Car Full Service, is the Group company dedicated to the development of the products and services linked to the motor industry including the repair activities supporting the settlement of claims. Cattolica Services owns 82%. On December 21st, 2012 a n outline agreement was settled between Cattolica Service, Car Full Service and the minority shareholders of the same; following the finalisation of the same and as from February 28th, 2013, Cattolica, via Cattolica Services, owns 100% of the former Car Full Service (which, as at February 25th, 2013, adopted the name Cattolica Services Sinistri s.p.a.) inclusive of the claims management activities;

• Cattolica Services, a consortium company which carries out service activities for the

Group. A division of the company handles planning, implementation and management of IT applications and operating processes, along with the services relating to telecommunications services; another deals with the settlement of Group claims with the exception of the security, hail and transport areas. During the year it acquired the new division “Fabbrica Life” from the Parent Company. On December 31st it absorbed Cattolica Assicurazioni Business School, a consortium company, set up in November 2010, as a training hub suitable for utilising the skills developed within in favour of all those who

44

work with the Group. Cattolica Services is 99.95% owned by Cattolica, while the remaining investment is held by other Group companies (ABC Assicura, BCC Assicurazioni, BCC Vita, Berica Vita, Cattolica Previdenza, C.P. Servizi Consulenziali, Duomo Uni One, Lombarda Vita, Risparmio & Previdenza and TUA Assicurazioni) to an equal extent (0.005%);

• C. P. Servizi Consulenziali, received an agency mandate in 2011 from Cattolica, Cattolica

Previdenza and TUA Assicurazioni. As from May 2012, besides the life business solely under Cattolica Previdenza mandate, it carries out non-life premium business activities (with TUA and Cattolica products) also availing itself of sub-agents, previously welfare and pension fund advisors, of Cattolica Previdenza. It is 51% owned by Cattolica and 49% owned by Cattolica Previdenza.

Management Report

45

Insurance business

Insurance premiums are shown in the table below, with indication of the percentage in relation to total direct business and percentage changes as compared with the previous year, together with investment contracts.

Table 8 - Total premiums written

Classes Changes

(€ thousands) 2012 % of total 2011 % of total Abs. amount % 01 - Accident and injury 124,503 3.5 131,755 3.5 -7,252 -5.5

02 – Health 97,656 2.8 101,935 2.7 -4,279 -4.2

03 - Land vehicle hulls 107,653 3.1 109,761 2.9 -2,108 -1.9

07 - Goods in transit 6,165 0.2 6,612 0.2 -447 -6.8

08 - Fire & natural forces 106,598 3.0 112,415 3.0 -5,817 -5.2

09 - Other damage to assets 139,631 4.0 123,314 3.3 16,317 13.2

10 - TPL - Land motor vehicles 868,158 24.6 817,175 21.7 50,983 6.2

13 - TPL –General 157,594 4.5 144,058 3.8 13,536 9.4

14 – Credit 797 n.s. 424 n.s. 373 88.0

15 – Suretyship 12,408 0.4 13,233 0.4 -825 -6.2

16 - Sundry financial losses 24,596 0.7 28,505 0.8 -3,909 -13.7

17- Legal protection 11,293 0.3 11,835 0.3 -542 -4.6

18 – Assistance 24,856 0.7 20,830 0.6 4,026 19.3

Other classes (1) 3,536 n.s. 4,917 n.s. -1,381 -28.1

Total non-life classes 1,685,444 47.8 1,626,769 43.2 58,675 3.6

Insurance on the duration of human life - class I 1,307,649 37.1 1,351,931 35.9 -44,282 -3.3 Insurance on the duration of human life linked to investment funds - class III 199,799 5.7 379,197 10.1 -179,398 -47.3

Health insurance - class IV 44 n.s. 89 n.s. -45 -50.6

Capitalisation transactions - class V 318,686 9.1 393,316 10.5 -74,630 -19.0

Pension funds - class VI 12,244 0.3 12,403 0.3 -159 -1.3

Total life classes 1,838,422 52.2 2,136,936 56.8 -298,514 -14.0

Total direct business 3,523,866 100.0 3,763,705 100.0 -239,839 -6.4

Indirect business 15,204 14,563 641 4.4

Total insurance premiums 3,539,070 3,778,268 -239,198 -6.3 Insurance on the duration of human life linked to investment funds - class III 3,675 2.7 18,505 10.2 -14,830 -80.1

Pension funds - class VI 133,925 97.3 163,761 89.8 -29,836 -18.2

Total investment contracts 137,600 100.0 182,266 100.0 -44,666 -24.5

TOTAL PREMIUMS WRITTEN 3,676,670 3,960,534 -283,864 -7.2

n.s. = not significant (1) includes railway rolling stock, aircraft, sea and inland water vessels/hulls and TPL aircraft and sea and inland water vessels.

In particular, life premiums written are divided by insurance class (taking account of both

insurance premiums and investment contracts) as follows:

46

Table 9 – Life premiums written

Life business Changes

(€ thousands) 2012 % of total 2011 % of total Abs. amount % Insurance on the duration of human life - class I 1,307,649 66.2 1,351,931 58.3 -44,282 -3.3 Insurance on the duration of human life linked to investment funds - class III 203,474 10.3 397,702 17.1 -194,228 -48.8

Health insurance - class IV 44 n.s. 89 n.s. -45 -50.6

Capitalisation transactions - class V 318,686 16.1 393,316 17.0 -74,630 -19.0

Pension funds - class VI 146,169 7.4 176,164 7.6 -29,995 -17.0

Total life premiums - direct business 1,976,022 100.0 2,319,202 100.0 -343,180 -14.8

n.s. = not significant

Non-life business – written Premiums

Direct non-life premiums written rose from € 1,626.8 million to € 1,685.4 million, disclosing an increase of 3.6%. Indirect premiums rose from € 14.5 million to € 15.1 million, (+4.5%).

The trend in non-life premiums written saw growth of 5.3% in the motor classes and 1.4% in the non-motor classes: in detail; premiums relating to other damage to assets increased, amounting to € 139.6 million (+13.2%), along with those relating to general TPL which totalled € 157.6 m illion (+9.4%) and those relating to assistance amounting to € 24.9 m illion (+19.3%).

817

110 144 123

868

108 158 140

0

100

200

300

400

500

600

700

800

900

1,000

TPL - Land motor vehicles Land vehicle hulls TPL-General Accident and injury

2011 2012

Main Non life classes, direct premiums€/millions

Direct non-life premiums written were generated as follows: the agency channel with € 1,523.4 million (+4.1%), the banking channel with € 46.2 million (-12.3%), brokers with € 83.1 million (+48.7%), welfare and pension product advisors with € 4 thousand and other channels with € 32.7 million (-39.5%). Non-life premiums attributable to the Parent Company totalled € 1,4 68.3 million, € 19. 1 million to ABC Assicura, € 19.5 million to BCC Assicurazioni, € 1.1 m illion to Duomo Uni One, € 158.4 million to TUA Assicurazioni, in addition to accident/injury and health premiums written by the companies Cattolica Previdenza and Risparmio & Previdenza amounting to €

Management Report

47

15.5 million and € 3.5 million respectively.

Non-life business - R&D activities: new products

Within the framework of the progressive renewal of the product catalogue and the standardisation of the same at Group level, the following activities were carried out. The Parent Company During the year, marketing commenced of new products within the retail and corporate sphere: Retail products ”Cattolica&Salute INFORTUNI” was launched in March with innovative coverage for the accident/injury market and again with the retail sphere “Cattolica&Famiglia”, a new line of clear, simple and immediate products, so as to protect the main areas of the personal and family sphere at a contained cost. Corporate products During the Spring, “Cattolica&Impresa INDUSTRIA” was launched, the new Group product dedicated to small and medium-sized industrial companies, conceived to help the various local manufacturing entities and further enhance the link between the Group and the business world and to develop the area in which they operate. The new “Cattolica&Professionisti RC TECNICI, PROGETTISTI AGRONOMI E FORESTALI” policy came out in October, in order to more fully satisfy the different insurance needs of professionals who operate in agronomic/forestry section by means of simple and adaptable solutions. The year ended with the launch of “Cattolica&Impresa ARTIGIANO E PICCOLA INDUSTRIA” which completes the Group’s range dedicated to the segment of manufacturing businesses.

ABC Assicura During the year, the company consolidated the personal line range of products already on sale within banks, taking steps to overhaul part of the existing catalogue and introducing five new products: • a specific product for mortgages taken out in the past so as to meet the insurance needs of

customers for the event linked to demise, disability and loss of employment. The product was created in collaboration with Berica Vita;

• a multi-risk family policy, to protect the family from serious events which may affect them and which comprises, in a single solution, the following coverage: reimbursement of major surgery, third party liability in private life and legal protection;

• a multi-risk home policy which is intended to cover risks pertaining to the home. The product is not linked to the disbursement of loans and has been developed in complementary units which can be chosen by the customer providing protection for one’s properties, with maximum flexibility and completeness;

• a policy, which is the first health product of ABC Assicura, which envisages a daily convalescence allowance. A simple product with regard to coverage and particularly abundant in terms of protection which proposes an indemnity in the event of hospital stays

48

which may compromise the ability to generate income for a freelance workers or which have eroded the resources of the household in the event of a dependent employee.

Placement of the product “CREDITOR PROTECTION CARTE DI CREDITO” under contract with Compass s.p.a was launched by Banca Popolare di Vicenza and Banca Nuova and particular attention was dedicated to the study and development of the pharmacy multirisk product, a product with a wide range of specific coverage for this commercial category.

BCC Assicurazioni During 2012, the Company made a number of changes envisaged by ISVAP Instruction No. 2946/2011, in force as from April 2nd, 2012, on t he following products: “Formula Fotovoltaico”,“Pro Fabbricato”,“Pro Agricoltura”,“Pro Agriturismo”, “Pro-Artigianato”, “Pro Commercio” and “Formula Domus”. Other changes were made to ““Socio in salute”, a new product which offers the shareholders of the lending co-operative different forms of protection linked to the family sphere in one single package. This policy offers the subscribers three important types of coverage such as the reimbursement of health costs due to important surgery, the protection of property from damage caused to third parties and support for sorting out legal matters linked to major surgery.

TUA Assicurazioni In January, TUA Assicurazioni launched the new policy “TUA Salute MAXXI”, aspiring to the French GAV, which provides wide coverage in the event of serious disability or demise. In July, the “TUA Famiglia” product, a head-of-the-household TPL and multi-risk for the home policy, was overhauled and modernised: inclusion of new and exclusive coverage (stalking, protection of personal data on the internet and assistance for electrical household appliances) and definition of a number of made-to-measure solutions for the various types of homes which aimed to facilitate and speed up the activities of the financial advisor (despite maintaining the possibility of intervening intact, varying the insured amounts, limits and coverage). In conclusion, during the second half of the year, the “TUA Professione” solution was extended by including among the options third party and administrative/accounting liability of public employees.

Life business - Premiums

Direct life business premiums came to € 1,838.4 million and indirect life premiums totalled € 101 thousand. Premiums relating to investment contracts amounted to € 137.6 million. Total direct life premiums written amounting to € 1,976 million, were down by 14.8% when compared with the € 2,319.2 million at the end of 2011. The life segment disclosed a decrease in premiums written for traditional type contracts which, in a situation of heavy competition on t he returns offered by other alternative forms of investment, saw their appeal decrease. The trend in premiums for linked products, especially index linked products disclosed renewed interest from investors who show preference for coupon flows and who are heedful of the

Management Report

49

variable return mechanism linked to the performance of one or more reference indexes. The attention which the Group pays to the pension and welfare component has led to the development of accumulation plans and supplementary welfare products. Direct life business premiums were generated by the agency channel with € 220 million (+0.8%), the banking channel with € 1,243.1 million (-19.6%), brokers with € 171.8 million (-20%), pension and welfare product consultants with € 11.5 million (-71.4%), financial advisors with € 6.4 million and other channels with € 323.2 million, mainly represented by pensions funds (+20.3%). Life premiums attributable to the Parent Company totalled € 612.5 million (€ 644.8 million in 2011), BCC Vita € 184.7 million (€ 190.5 million in 2011), Berica Vita € 198.1 million (€ 282.5 million in 2011), Cattolica Previdenza € 110.8 million (€ 85.3 million in 2011), Lombarda Vita € 705.7 million (€ 893.3 million in 2011), Risparmio & Previdenza € 18.9 million (€ 35.1 million in 2011) and Cattolica Life € 145.3 million (€ 187.7 million in 2011).

In class I (insurance on the duration of human life), the Group recorded a decrease in insurance

premiums from € 1,351.9 million to € 1,307.6 million (-3.3%). This result was affected by the heavy competition on returns offered by other alternative forms of investment which benefited from the significant growth in returns on government securities. Total Class III premiums written amounted to € 203.5 million, compared with € 397.7 million in 2011. Premiums for linked products, especially index linked products, as already reported, were met with enthusiasm by investors who show preference for coupon flows and who are heedful of the variable return mechanisms linked to the performance of reference indexes. Total Class V premiums written (capitalisation) amounted to € 318.7 million, compared with € 393.3 million in 2011. No investment policies were issued during the year. Class VI premiums written (pension funds) decreased from € 176.2 m illion to € 146.2 million, due primarily to investment policies from € 163.8 million to € 133.9 million.

1,352

398 393

176

1,308

203

319

146

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Class I Class III Class V Class VI

2011 2012

Main Life classes, direct premiums€/millions

50

Life business - R&D activities: new products

During the year new Class I products were marketed, of which 18 for the Parent Company, 1 for Lombarda Vita, 5 for Berica Vita and 4 for Cattolica Previdenza. With regard to the range of capitalisation products, a new class V product was created for Lombarda Vita. With regard to Class III products, two single premium unit-linked products were developed for Lombarda Vita: one addressing retail-type customers linked to a single internal flexible fund, the other by contrast dedicated to mass affluent customers and linked to 58 external funds. The catalogue was extended, creating products specifically dedicated to customer insurance, protection and savings/investment needs.

Parent Company, Cattolica Previdenza, Lombarda Vita and Risparmio & Previdenza Product activities were focused on the consolidation of that already achieved in the previous year, while product innovation specifically concerned the segment of protection, savings and investment products, by means of the restyling of the current products and the development of a new model for approaching the segment business linked to both investment and protection coverage, working on new insurance solutions. Furthermore, given the current situation of the markets and in line with the matters envisaged by the strategic business plan, long-term investment products were developed which pay out a minimum guaranteed annual rate of return exclusively when maturing and nil redemption penalties for “welfare” reasons”. In detail, the insurance offer placed by the Parent Company’s agency distribution network was expanded with the development of three Class I products, created with the purpose of offering a competitive mix of products in the catalogue. In fact, three mixed insurance products with single premium and annual revaluation of capital and additional benefit in the event of death have been created; one of these offers scheduled benefits each year under the form of payment coupons so as to permit the planning of the financial flows of the product subscriber. With regard to the banking network of the Parent Company and the other subsidiary companies, as well as the network of welfare and pension product advisors and insurance brokers, the insurance range saw the development of new Class I products of various types: • three mixed insurance products with single premium and annual revaluation of capital and

additional benefit in the event of demise; • one single premium insurance product with deferred capital which also envisages the

payment of a bonus on maturity; • two mixed insurance products with single premium which annually make a scheduled pay

out in the form of a coupon and which provide benefits which can be revalued on maturity, as well as additional benefits in the event of demise;

• two temporary insurance products for the event of demise: one with capital and constant annual premium following demise due to accident; the other with decreasing capital and a limited constant annual premium;

Management Report

51

• a temporary insurance in the event of demise with decreasing capital and a single premium. With a view to completing the range dedicated to protection, in conclusion a specific product has been developed with a constant annual premium dedicated to the coverage of the risk of non-self sufficiency (so-called long term care). The range of Class V products for the banking network saw the creation of a product with a sole premium and additional single premiums which makes it possible to establish capital which can be revalued annually in relation to the return obtained from the internal segregated fund which the policy is linked to. Various capitalization products have been developed dedicated to investors-institutional contracting parties, which makes it possible to establish capital which can be revalued annually in relation to the return obtained by the internal segregated fund; in this case as well, the company guarantees a minimum return and the consolidation of the revalued capital. Furthermore, numerous insurance products were created for the sales networks of the Parent Company, linked to the funding of loans and other financing agreements with related insurance coverage in the event of demise and other events; for such purposes, temporary insurance in the event of demise with decreasing capital was developed for which the company, in the event the insured party dies during the terms of the contract, undertakes to settle the envisaged insured sum on the beneficiaries. Towards the end of the year, steps were taken to up-date the product catalogue for the entire Cattolica Assicurazioni Group, with the aim of adapting it to the matters envisaged by Directive 2004/113/EC, which establishes the general principle of equal treatment of men and women in the insurance sphere and prohibits any form of discrimination based on gender when accessing and supplying goods and services.

BCC Vita This insurance company continued the activities carried out in 2012 studying traditional Class I insurance solutions linked to the situation of the financial markets with the issue of products with specific funding of the assets, which in a second phase of the product will rejoin the BCC Vita Garantita separate fund. These products will permit a saving for the purpose of both the safety of the capital and the payment of the coupons. During the year, with regard to individual products, the insurance company issued: • “BCC Vita - Concreta. 5/2012 & 6/2012”, products with specific funding of assets, full life

single premium with insurance in the event of demise, with coupons for a pre-established amount, annual revaluation of the capital for the period and an additional pay out in the event of demise;

• “BCC Vita - Concreta. 10/2012 5 anni" and "BCC Vita - Concreta. 10/2012 3 anni" , products, created as per the specific funding of assets formula with underlying Iccrea Banca bonds; these are insurance products for the event of demise with full life single premium, with coupons for a pre-established amount until the end of the third or fifth year (first phase), annual revaluation of the capital for the subsequent period (second phase) and an additional pay out in the event of demise;

52

“BCC Vita - Concreta. 12/2012 4 anni" , a product, again structured as specific funding of assets with an underlying Iccrea Banca bond; this is an insurance product for the event of demise with full life single premium, with coupons for a pre-established amount until the end of the fourth year (first phase), annual revaluation of the capital for the subsequent period (second phase) and an additional pay out in the event of demise; With regard to collective products, the company launched “Protezione Fido”, a product which provides coverage for the event of demise and total disability. The premium is once a year. This product is intended to cover bank credit facilities (opening of current account credit, advances on invoices and collection with due reserve) care of Banche di Credito Cooperativo.

Berica Vita The line dedicated to protection, savings and investments was enhanced, creating five new products: • three full life policies in the event of demise featuring a single premium and additional

single premiums, with revaluation and an additional benefit in the event of demise; • a mixed insurance product with single premium and additional single premiums with annual

revaluation of capital and additional benefit in the event of death; • a temporary insurance in the event of demise with decreasing capital and a single premium.