Embed Size (px)

Citation preview

ConsolidatedFinancialReport

For the year ended June 30, 2007

Management’s Discussion and Analysis....................................................................................................... 2

Statement of Net Assets .............................................................................................................................17 Statement of Revenues, Expenses and Changes in Net Assets................................................................19 Statement of Cash Flows............................................................................................................................21

Note 1 – Summary of Significant Accounting Policies ................................................................................24 Note 2 – Change in Accounting Classifications ..........................................................................................27 Note 3 – Cash and Investments..................................................................................................................27 Note 4 – Accounts Receivable....................................................................................................................29 Note 5 – Notes Receivable from Students..................................................................................................30 Note 6 – Capital Assets...............................................................................................................................31 Note 7 – Long-term Liabilities .....................................................................................................................33 Note 8 – Operating Leases .........................................................................................................................35 Note 9 – Natural Classifications with Functional Classifications.................................................................35 Note 10 – Construction Commitments and Financing ................................................................................36 Note 11 – Pension Plan ..............................................................................................................................37 Note 12 – Donor Restricted Endowments...................................................................................................37 Note 13 – Federal Direct Lending and FFEL Programs .............................................................................37 Note 14 – Foundations and Affiliated Parties..............................................................................................38 Note 15 – Subsequent Events ....................................................................................................................38

NOTES TO FINANCIAL STATEMENTS

ANNUAL FINANCIAL STATEMENTS (UNAUDITED)

Mississippi State University Management’s Discussion and Analysis

Mississippi State University Consolidated Financial Report

Year Ended June 30, 2007

Overview Mississippi State University (referred to as the University) presents its financial statements for June 30, 2007 (end of the fiscal year) in accordance with Governmental Accounting Standards Board (GASB) Statement 34 as a special purpose government engaged solely in business-type activities (BTA). According to paragraphs 44 through 47 of GASB Statement 35 and related paragraph 67 of GASB Statement 34, the University is a public institution that regularly receives state appropriations and covers a major portion of its costs through external user charges for its services and is therefore allowed to report as a BTA. The University is one of eight universities under the direction of the Board of Trustees of Institutions of Higher Learning. The student population is 16,206 with the main campus in Starkville, Mississippi, and off-campus locations at Meridian and Vicksburg. Mississippi State University is a land-grant institution with strong ties to the U.S. Department of Agriculture and has County Extension Offices in eighty-two counties and eight Branch Experiment Stations. The following discussion and analysis of the University’s financial statements provide an overview of its financial activities for the year ending June 2007. Fiscal year 2006 data are presented for comparative purposes. The statements are composed of the statement of net assets, statement of revenues, expenses and changes in net assets, statement of cash flows (direct method), and notes to the financial statements.

2

Mississippi State University Management’s Discussion and Analysis

Statement of Net Assets The purpose of the Statement of Net Assets is to present at a point in time (end of the fiscal year) assets, liabilities and net assets of Mississippi State University. The University has chosen a net asset presentation. The statement uses a classified format presenting current and non-current assets and liabilities, as well as, three net asset categories (unrestricted, restricted and invested in capital assets).

FY 2007 FY 2006Assets:

Current Assets $107,866,890 $112,261,585Capital Assets Net 585,523,520 533,812,536Other Noncurrent Assets 97,734,709 102,510,742

Total Assets 791,125,119 748,584,863

Liabilities:Current Liabilities 42,956,108 48,954,071Noncurrent Liabilities 171,999,508 177,933,606

214,955,616 226,887,677Net Assets:

Invested in Capital Assets (net of related debt) 440,213,094 376,061,867Restricted-Nonexpendable Scholarships 17,783,585 12,106,647Restricted-Nonexpendable Research 5,364,033 4,783,218Restricted-Nonexpendable Other Purposes 239,789 239,789Restricted-Expendable Scholarships 2,705,233 2,884,590Restricted-Expendable Research 10,312,353 14,971,278Restricted-Expendable Loans 3,899,049 3,834,352Restricted-Expendable Capital Projects 2,700,962 14,787,375Restricted-Expendable Debt Service (3,646,109) 4,185,908Unrestricted 96,597,514 87,842,162

Total Net Assets $576,169,503 $521,697,186

Restricted-Nonexpendable

4%

Restricted-Expendable

3%

Unrestricted17%

Invested in Capital Assets

76%

Increase in net assets of $54,472,317

3

Mississippi State University Management’s Discussion and Analysis

Overall for the year the University improved its financial position with an increase in net assets of $54,472,317 or 10.4%. Much of this improvement in financial position was due to capital assets, net of related debt. The following overview discusses variances in both assets and liabilities as compared to fiscal year 2006 balances. While the discussion does not attempt to be all-inclusive, it does cover the major items for each category that exceed the variance limit of 5% determined by management to warrant further discussion. Current assets decreased for the year by $4,394,695 or 3.9%. The following lists the major items in this category experiencing at least a 5% variance:

• Cash and Cash Equivalents 25.0% Decrease – Working cash decreased by $7 million as a result of year-end activity for construction on campus and loan fund cash reclassified as Restricted Cash and Cash Equivalents.

• Short Term Investments 23.8% Decrease – A majority of the decrease is due to the

Educational Building Corporation 2005 bond funds in the amount of $13.5 million included in this category at the end of fiscal year 2006.

• Accounts Receivable, Net 25.4% Increase – General accounts receivables increased by

$3.8 million due to an increase in grant accruals at year-end. The MSU Foundation receivables increased by $4 million as a result of the McCool Hall addition. The Bulldog Club year-end accounts receivable increased by $1.6 million to support the University athletic program.

• Student Notes Receivable 13.3% Increase – Short term notes receivables for Perkins

Loans increased $500,000 due to principal collections for the current fiscal year exceeding the prior fiscal year.

• Inventories 12.6% Increase – Work-in-progress in Facilities Management increased

$211 thousand over the prior fiscal year end.

• Prepaid Expenses 35.7% Increase – Bureau of Building prepayment of $1.7 million was outstanding at year-end for the Colvard Student Union renovation.

Colvard Union

Construction

4

Mississippi State University Management’s Discussion and Analysis

Non-current assets increased by $46,934,951. Below are the line items in non-current assets that exceeded the 5% variance.

• Restricted Cash and Cash Equivalents 43.4% Increase – Loan fund cash of $1.8 million was reclassified from Current Cash and Cash Equivalents to achieve uniformity in presentation with other institutions in the state.

• Endowment Investments 28.9% Increase – Investment pool increased $5.4 million

mainly due to the creation of endowments devoted to academic excellence, faculty development, general scholarship and campus infrastructure.

• Other Long Term Investments 16.5% Decrease – Government Securities/Certificate of

Deposits maturing greater than one year decreased $10 million. Investments in Trinity Capital decreased $1.1 million.

• Capital Assets, Net of Accumulated Depreciation 9.7% Increase – Construction in

process increased $58.5 million consisting of the Colvard Student Union renovation, McCool Hall additions and renovations and the new residence halls phase II.

Current liabilities decreased $5,997,963 for the fiscal year. Line items included within current liabilities that varied more than 5% are presented below.

• Accounts Payable and

Accrued Liabilities 7.1% Increase – State retirement accrual increased $366 thousand due in part to a rate increase of 1.55% for the fiscal year. Accounts Payable invoicing increased $1.2 million mainly due to technology upgrades in process by the Extension Service at year-end.

• Deferred Revenues 11.6% Decrease – Deferred terminal leave decreased $795 thousand

due to the determination that the year end accrual of terminal leave should be based on the June 30 rate of pay rather than the July 1 rate used in prior fiscal years. Also the bond premium associated with the 2005 Educational Building Corporation issue decreased $295 thousand.

• Long Term Liabilities (Current Portion) 49.5% Decrease – The Educational Building

Corporation 1996 revenue bonds due within one year decreased $6 million.

Depot Welcome Center

5

Mississippi State University Management’s Discussion and Analysis

Statement of Revenues, Expenses and Changes in Net Assets The purpose of this statement is to present to the reader not only the revenues and expenses of the University but to also make a distinction between operating and nonoperating categories. Operating revenues are received for providing goods and services to the customers of the institution. Operating expenses are paid to acquire or produce goods and services provided in turn for operating revenues. Nonoperating revenue is revenue received for which goods and services are not provided. For example, state appropriations are nonoperating revenues since they are provided by the State of Mississippi Legislature to the Institutions of Higher Learning without the Legislature requiring a direct service in return.

FY2007 FY2006

Operating revenues $353,765,115 $305,747,079Operating expenses 526,885,392 476,456,043Operating loss (173,120,277) (170,708,964)

Nonoperating revenues and expenses 196,208,522 171,021,230

Income (loss) before other revenues, 23,088,245 312,266expenses, gains or losses

Other revenues, expenses, gains or losses 31,384,072 25,077,009

Increase in net assets 54,472,317 25,389,275

Net assets - beginning of year, as originally reported 521,697,186 496,307,911

Net assets - end of year $576,169,503 $521,697,186

The statement of revenues, expenses and changes in net assets reflects a positive year with an increase in net assets at the end of the year in the amount of $54,472,317. The following overview discusses variances that exceed 5% from FY 2006 totals: • Scholarship Allowance 8.4% Decrease – Scholarship allowances associated with auxiliary

enterprises were reallocated to the Auxiliary Enterprises section. Management deemed this presentation more appropriate to enable comparison with other state institutions. Tuition and required fees dedicated to University athletics and the Student Health Center were also reallocated to the Auxiliary Enterprise section of Operating Revenues.

6

Mississippi State University Management’s Discussion and Analysis

• Net Tuition and Fees 5.6% Increase – The University experienced an enrollment increase of 105 students over Fall 2005 in addition to a tuition increase of 6.6%.

• Federal Appropriations 9.1% Increase – Hatch federal appropriations increased 31% in

support of the Mississippi Agricultural Experiment Station and McIntire Stennis appropriations increased 25% in support of the Forestry and Wildlife Research Center.

• Federal Grants and Contracts 25.8% Increase – The University received several major

awards from the United States Department of Health and Human Services, from the University of Southern Mississippi through funding from NASA and from the United States Department of Energy. For fiscal year 2007 $15.4 million was realized from these awards.

• Nongovernmental Grants and

Contracts 11.4% Increase – The University received a major award from the Barksdale Reading Institute under the project title “Leaders in Literacy – Phase II”. Another large award was received from the Association of Southern Regional Extension Directors.

• Sales and Services of

Educational Departments 16.6% Increase – Sales increases observed were laboratory testing fees at the Veterinary Diagnostic lab and

the Center for Advanced Vehicular Systems MCASP Operations. Animal health care services also increased over the previous year. Riley Center conference activities also commenced during fiscal year 2007.

• Student Housing 15.5% Increase – Dorm rent revenue increased $1.8 million as a result of

an increase in rates effective Fall of 2006. • Bookstore 100% Increase – Bookstore royalty revenue was reclassified from Sales and

Services of Educational Departments to provide a more accurate comparison with other in state institutions.

• Athletic Sales 23.8% Increase – Required fees were reclassified from tuition and fees to

provide a more accurate comparison with other in-state institutions. • Other Auxiliary Revenues 32.1% Increase – Required fees for the Student Health Center

were reclassified from Tuition and Fees to provide a more accurate comparison with other in state institutions.

7

Mississippi State University Management’s Discussion and Analysis

• Auxiliary Enterprise Scholarship Allocations 100% Increase – Scholarship allowance

associated with Auxiliary required fees were reclassified from Scholarship Allowance to provide a more accurate comparison with other in-state institutions.

• Interest Earned on Loans to Students 12.3% Decrease – Investment income decreased

$32,000. • Other Operating Revenues 39.9% Increase – Miscellaneous income increased $483,000

with the largest increase showing in Coliseum parking revenue. • Salaries and Wages 8.3% Increase – University administration authorized a campus-wide

salary increase of 5% for the fiscal year. • Fringe Benefits 9.4% Increase – Retirement and health insurance rate increases were

incurred in addition to a salary increase. • Travel 16.3% Increase – In-state official travel increased 16.6% for the year. Out-of-state

conference travel increased 22.2%. • Contractual Services 12.9% Increase – Repair and maintenance of buildings and grounds

increased $4.9 million. Indirect cost recovery for overhead charges increased $4.4 million. • Utilities 23.8% Decrease – Electricity expenses declined 17% for the year due to a campus-

wide program to actively manage utility consumption. Natural gas expenses declined 26% as well.

• Scholarships and Fellowships 11.8%

Increase – Grants increased 15% for the year due to LEAP federal disaster awards continuing from the previous year as a result of Hurricane Katrina.

• Commodities 63.0% Increase – Equipment

titled to other agencies increased $5.9 million.

• State Appropriations 11.0% Increase – State appropriations increased $16 million over the

previous fiscal year. • Gifts and Grants 22.0% Increase – Gifts from foundations increased $7.3 million due in

large part to the gift for the McCool Hall addition. • Investment Income, Net of Investment Expense 80.4% Increase – A decrease in unrealized

loss on investments of $3.2 million was booked at year end.

Center for Advanced Vehicular Systems (CAVS) ChallengeX Car

8

Mississippi State University Management’s Discussion and Analysis

• Interest Expense on Capital Asset – Related Debt 31.2% Increase – Bond interest

payments increased 37.8% due in large part to the Educational Building Corporation 2005 bond issue for the new residence halls.

• Other Nonoperating Revenues 51.5% Decrease – This category consists of the fund balance

dedicated to outstanding check reserve. During the current fiscal year the outstanding check reserve was increased $49 thousand compared to the previous year’s increase of $102 thousand.

• Other Nonoperating Expenses 66.2% Decrease – Trustee fees decreased $571 thousand due

in large part to the previous year’s issuance of the 2005 new residence hall bonds. • Capital Grants and Gifts 96.1% Decrease – Capital gifts decreased $6.8 million due to the

previous fiscal year’s recognition of the capital gift of the Shira Field House. The reclassification of federal capital grants also decreased $4.3 million over the previous fiscal year.

Sanderson Center - Lakeside

9

Mississippi State University Management’s Discussion and Analysis

• State Appropriations Restricted for Capital Purposes 106.7% Increase – State

appropriations for capital purposes increased $14.8 million due in large part to the Colvard Student Union renovation.

• Other Additions 100.0% Increase – Gain on sale of assets increased $2.7 million due to a

land sale to Stateside Developers LLC. • Other Deletions 100.0% Decrease – No loss on sale of assets for FY07.

OPERATING REVENUES 2007

Net tuition and fees $70,703,098Federal appropriations 14,166,595Federal grants and contracts 163,690,056State grants and contracts 16,293,745Nongovernmental grants and contracts 11,925,364Sales and services 74,016,186Other 2,970,071Total operating revenues $353,765,115

OPERATING EXPENSES BY OBJECT 2007

Salaries and benefits $309,232,887Supplies and services 155,235,479Utilities 13,564,639Scholarships and fellowships 24,213,620Depreciation 24,638,767Total operating expenses $526,885,392

Nongovernmental Grants and

Contracts3%

Other1%

Net tuition and fees20%

Federal appropriations

4%

State grants and contracts

5%

Federal grants and contracts

46%

Sales and services

21%

Scholarships and

fellowships5%

Utilities3%

Supplies and services

29%

Salaries and benefits

58%

Depreciation5%

10

Mississippi State University Management’s Discussion and Analysis

Statement of Cash Flows

The purpose of this statement is to present information regarding cash receipts and cash payments during the year. Information is presented using the direct method and has four categories: operating activities, non-capital financing activities, capital financing activities and investing activities. The primary cash receipts from operating activities for fiscal year 2007 consists of tuition and fees in the amount of $69,728,787 and grants and contracts in the amount of $190,425,383. Cash outlays include payments to employees in the amount of $309,435,032. State appropriations are the primary source of non-capital financing in the amount of $161,159,492.

FY 2007 FY 2006Cash provided (used) by:

Operating activities ($150,743,385) ($146,881,342)Noncapital financing activities 187,459,783 176,138,844Capital financing activities (49,159,339) (53,362,210)Investing activities 4,872,237 6,735,260Net change in cash (7,570,704) (17,369,448)Cash, beginning of year 36,434,072 53,803,520

Cash, end of year $28,863,368 $36,434,072

Center for Advanced Vehicular Systems (CAVS)

at night

11

Mississippi State University Management’s Discussion and Analysis

Functional Classification of Operating Expenses

Year Ended June 30, 2007 Natural Classification

Functional Salaries Fringe Contractual Scholarships & DepreciationClassification & Wages Benefits Travel Services Utilities Fellowships Commodities Expense Total

Instruction $63,971,135 $17,542,138 $1,405,150 $5,107,923 $113,568 $1,036,605 $89,176,520Research 71,917,294 20,666,067 4,375,130 47,408,218 2,637,880 11,165,974 158,170,563Public Service 39,863,655 12,050,395 3,619,965 14,663,938 2,051,223 4,684,890 76,934,066Academic Support 15,387,098 3,952,642 564,417 4,278,847 213,193 2,195,874 26,592,071Student Services 6,831,927 1,900,816 320,444 1,873,880 (3,614) 492,047 11,415,500Institutional Support 15,694,084 1,897,745 210,238 24,564,915 (86,074) 11,328,498 53,609,406Operation of Plant 11,103,340 3,339,158 58,464 6,799,591 1,064,203 22,364,755Student Aid 895,012 2,041,772 7,178 367,198 $18,709,820 27,949 22,048,929Auxiliary Enterprises 16,198,195 3,980,416 2,375,523 9,244,822 1,838,873 5,503,800 2,793,186 41,934,815Depreciation $24,638,767 24,638,767

Total OperatingExpenses $241,861,738 $67,371,149 $12,936,509 $107,509,742 $13,564,639 $24,213,620 $34,789,228 $24,638,767 $526,885,392

Operating Expenses by Function

Depreciation5%

AuxiliaryEnterprises

8%Student Aid

4%

Operation of Plant4%

Institutional Support10%

Student Services2%

Academic Support5%

Public Service15%

Research30%

Instruction17%

12

Mississippi State University Management’s Discussion and Analysis

Significant Long-term Liability and Debt Activity During the current fiscal year the most significant debt activity involved the refunding of the Educational Building Corporation (EBC) 1996 revenue bonds. No new debt was issued by the EBC during fiscal year 2007. However, as of June 30, 2007 the University was in the final stages of issuing new debt in the amount of $6,100,000 for the Colvard Student Union renovation. Note seven of the Notes to Financial Statements provides more information on long-term debt. Trends

Total State Appropriations

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

147.7 145.6 161.6

2005 2006 2007

Millions

Full-time Resident Tuition and Required Fees

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

$4,106 $4,312 $4,595

2005 2006 2007

13

Mississippi State University Management’s Discussion and Analysis

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Race Gender Residency Level Age

Caucasian74%

African American20%

Other6%

Female48%

Male52%

Resident77%

Non-resident23%

Undergraduate78%

Graduate22%

Under 2571%

Over 2529%

Trends (continued)

Total Campus Student Enrollment

15,75015,80015,85015,90015,95016,00016,05016,10016,15016,20016,250

15,934 16,101 16,206

2005 2006 2007

Student Profile

14

Mississippi State University Management’s Discussion and Analysis

Financial Summary and Outlook Mississippi State University experienced growth and increased financial strength in FY 2007. As a result of broad-based energy conservation measures, most of the reserves expended in FY 2006 to cover sharply higher utility costs were returned to fund balance in FY 2007. Modest gains in student enrollment were realized despite a tuition rate increase. By the end of the fiscal year, the fourth new residence hall built since 1985 was occupied, and the renovation and expansion of our student union was well under way. Research contracts remained strong, even though universities across the nation faced sharply reduced funding from key federal agencies. In FY 2008, the Mississippi Legislature has planned to provide for increased operational appropriations to Mississippi State University. This increased funding will provide salary increases averaging 5 percent to university employees, along with the associated employer fringe benefit cost. Additional funding is planned for capital expenditures to renovate three campus buildings, although a significant backlog continues to exist. State of Mississippi revenues are expected to remain stable for the following fiscal year. We anticipate that our revitalized recruiting efforts will pay dividends beginning in FY 2008. Admittances for the fall term are up significantly from the prior year, and we expect matriculation levels to increase accordingly, producing additional net tuition revenue. Michael J. “Mike” McGrevey Chief of Staff and Chief Financial Officer

15

Financial Statements

2007 Chapel of Memories

June 302007 2006

AssetsCurrent Assets: Cash and Cash Equivalents $25,617,383 $34,170,264 Short Term Investments (note #3) 23,677,700 31,071,547 Accounts Receivable, Net (note #4) 46,680,006 37,227,752 Student Notes Receivable (note #5) 4,274,974 3,771,692 Inventories 2,691,640 2,390,447 Prepaid Expenses 4,925,187 3,629,883

Total Current Assets $107,866,890 $112,261,585

Non-Current Assets: Restricted Cash and Cash Equivalents $3,245,985 $2,263,808 Endowment Investments (note #3) 25,297,032 19,621,231 Other Long Term Investments (note #3) 56,057,589 67,163,514 Student Notes Receivable, Net (note #5) 13,134,103 13,462,189 Capital Assets, Net of Accumulated Depreciation (note #6) 585,523,520 533,812,536

Total Non-Current Assets $683,258,229 $636,323,278

Total Assets $791,125,119 $748,584,863

Liabilities and Net Assets

Current Liabilities: Accounts Payable and Accrued Liabilities $25,178,849 $23,518,314 Deferred Revenues 9,650,330 10,918,019 Accrued Leave Liabilities - Current Portion (note #7) 1,403,690 1,411,002 Long Term Liabilities - Current Portion (note #7) 6,498,611 12,877,395 Other Current Liabilities 224,628 229,341

Total Current Liabilities $42,956,108 $48,954,071

MISSISSIPPI STATE UNIVERSITYSTATEMENT OF NET ASSETS

17

(Continued)

2007 2006Non-Current Liabilities: Deposits Refundable (note #7) $85,490 $86,620 Accrued Leave Liabilities (note #7) 17,764,972 17,744,204 Long Term Liabilities (note #7) 138,813,912 144,873,273 Other Non-Current Liabilities (note #7) 15,335,134 15,229,509

Total Non-Current Liabilities $171,999,508 $177,933,606

Total Liabilities $214,955,616 $226,887,677

Net Assets: Invested in Capital Assets, Net of Related Debt $440,213,094 $376,061,867

Restricted for: Nonexpendable - Scholarships and Fellowships 17,783,585 12,106,647 Research 5,364,033 4,783,218 Other Purposes 239,789 239,789 Expendable - Scholarships and Fellowships 2,705,233 2,884,590 Research 10,312,353 14,971,278 Capital Projects 2,700,962 14,787,375 Debt Service (3,646,109) 4,185,908 Loans 3,899,049 3,834,352

Unrestricted 96,597,514 87,842,162

Total Net Assets $576,169,503 $521,697,186

Supplemental Information -- Academic Programs & Research $16,560,075 $11,777,895 -- Capital Projects 5,733,678 5,568,871 -- Repairs and Maintenance 6,070,600 7,683,511 -- Remaining Purposes 68,233,161 62,811,885

$96,597,514 $87,842,162

June 30

STATEMENT OF NET ASSETSMISSISSIPPI STATE UNIVERSITY

18

2007 2006Operating Revenues:

Tuition and Fees $91,928,814 $90,150,385Less: Scholarship Allowance (21,225,716) (23,168,265)

Net Tuition and Fees 70,703,098 66,982,120Federal Appropriations 14,166,595 12,982,886Federal Grants and Contracts 163,690,056 130,157,930State Grants and Contracts 16,293,745 16,859,379Nongovernmental Grants and Contracts 11,925,364 10,708,701Sales and Services of Educational Departments 28,405,674 24,363,102Auxiliary Enterprises:

Student Housing 12,473,629 10,801,156Food Services 5,683,364 5,770,470Bookstore 654,793 0Athletics 21,305,530 17,213,661Other Auxiliary Revenues 10,152,500 7,686,612 Less: Auxiliary Enterprise Scholarship Allowance (4,659,304) 0

Interest Earned on Loans to Students 231,698 264,149Other Operating Revenues 2,738,373 1,956,913

Total Operating Revenues $353,765,115 $305,747,079

Operating Expenses:Salaries and Wages $241,861,738 $223,328,995Fringe Benefits 67,371,149 61,600,070Travel 12,936,509 11,120,177Contractual Services 107,509,742 95,217,510Utilities 13,564,639 17,795,495Scholarships and Fellowships 24,213,620 21,662,336Commodities 34,789,228 21,344,487Depreciation Expense 24,638,767 24,386,973

Total Operating Expenses $526,885,392 $476,456,043

Operating Income (Loss) (173,120,277) (170,708,964)

June 30

MISSISSIPPI STATE UNIVERSITYSTATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETS

19

(Continued)2007 2006

Nonoperating Revenues (Expenses):State Appropriations $161,567,769 $145,588,753Gifts and Grants 32,774,410 26,861,905Investment Income, Net of Investment Expense 9,016,318 4,997,427Interest Expense on Capital Asset - Related Debt (6,725,743) (5,126,715)Other Nonoperating Revenues 49,434 101,835Other Nonoperating Expenses (473,666) (1,401,975)

Total Net Nonoperating Revenues (Expenses) $196,208,522 $171,021,230

Income (Loss) Before Other Revenues, $23,088,245 $312,266Expenses, Gains and Losses:

Capital Grants and Gifts 448,616 11,573,426State Appropriations Restricted for Capital Purposes 28,307,747 13,696,409Other Additions 2,627,709 0Other Deletions 0 (192,826)

Net Increase in Net Assets $54,472,317 $25,389,275

Net Assets - Beginning of Year, as Restated $521,697,186 $496,307,911

Net Assets - End of Year $576,169,503 $521,697,186

June 30

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETSMISSISSIPPI STATE UNIVERSITY

20

2007 2006

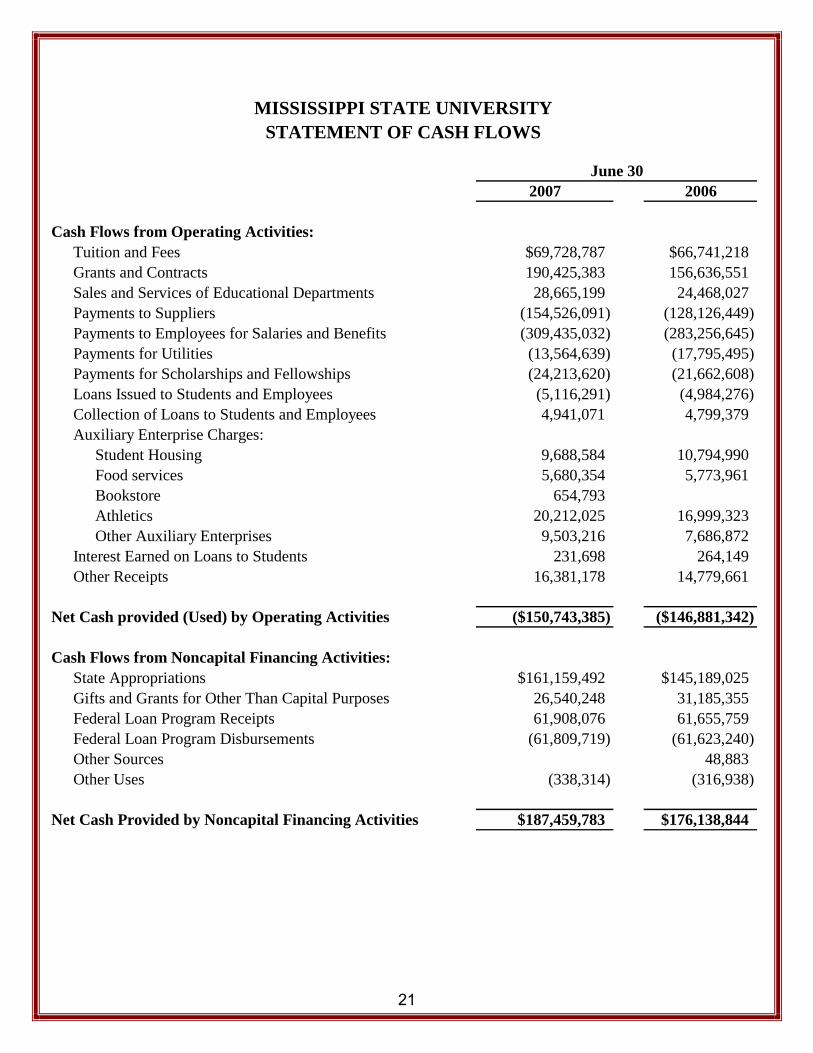

Cash Flows from Operating Activities:Tuition and Fees $69,728,787 $66,741,218Grants and Contracts 190,425,383 156,636,551Sales and Services of Educational Departments 28,665,199 24,468,027Payments to Suppliers (154,526,091) (128,126,449)Payments to Employees for Salaries and Benefits (309,435,032) (283,256,645)Payments for Utilities (13,564,639) (17,795,495)Payments for Scholarships and Fellowships (24,213,620) (21,662,608)Loans Issued to Students and Employees (5,116,291) (4,984,276)Collection of Loans to Students and Employees 4,941,071 4,799,379Auxiliary Enterprise Charges:

Student Housing 9,688,584 10,794,990Food services 5,680,354 5,773,961Bookstore 654,793Athletics 20,212,025 16,999,323Other Auxiliary Enterprises 9,503,216 7,686,872

Interest Earned on Loans to Students 231,698 264,149Other Receipts 16,381,178 14,779,661

Net Cash provided (Used) by Operating Activities ($150,743,385) ($146,881,342)

Cash Flows from Noncapital Financing Activities:State Appropriations $161,159,492 $145,189,025Gifts and Grants for Other Than Capital Purposes 26,540,248 31,185,355Federal Loan Program Receipts 61,908,076 61,655,759Federal Loan Program Disbursements (61,809,719) (61,623,240)Other Sources 48,883Other Uses (338,314) (316,938)

Net Cash Provided by Noncapital Financing Activities $187,459,783 $176,138,844

MISSISSIPPI STATE UNIVERSITYSTATEMENT OF CASH FLOWS

June 30

21

(continued)

2007 2006

Cash Flows from Capital Financing Activites:Proceeds from Capital Debt $58,846,499Cash Paid for Capital Assets ($50,413,426) (86,316,476)Capital Grants and Contracts Received 448,616 4,791,483Proceeds from Sales of Capital Assets 3,888,271 2,652,973Principal Paid on Capital Debt and Leases (12,985,234) (6,091,625)Interest Paid on Capital Debt and Leases (7,135,439) (5,245,216)Other Sources 17,333,369 3,281,967Other Uses (295,496) (25,281,815)

Net Cash used by Capital and Related Financing Activities ($49,159,339) ($53,362,210)

Cash Flows from Investing Activities:Proceeds from Sales and Maturities of Investments $25,373,135 $9,949,466Interest Received on Investments 4,991,199 5,785,794Purchases of Investments (25,492,097) (9,000,000)

Net Cash Provided by Investing Activities $4,872,237 $6,735,260

Net Increase (Decrease) in Cash and Cash Equivalents ($7,570,704) ($17,369,448)

Cash and Cash Equivalents - Beginning of the the Year 36,434,072 53,803,520

Cash and Cash Equivalents - End of the Year $28,863,368 $36,434,072

STATEMENT OF CASH FLOWS

June 30

MISSISSIPPI STATE UNIVERSITY

22

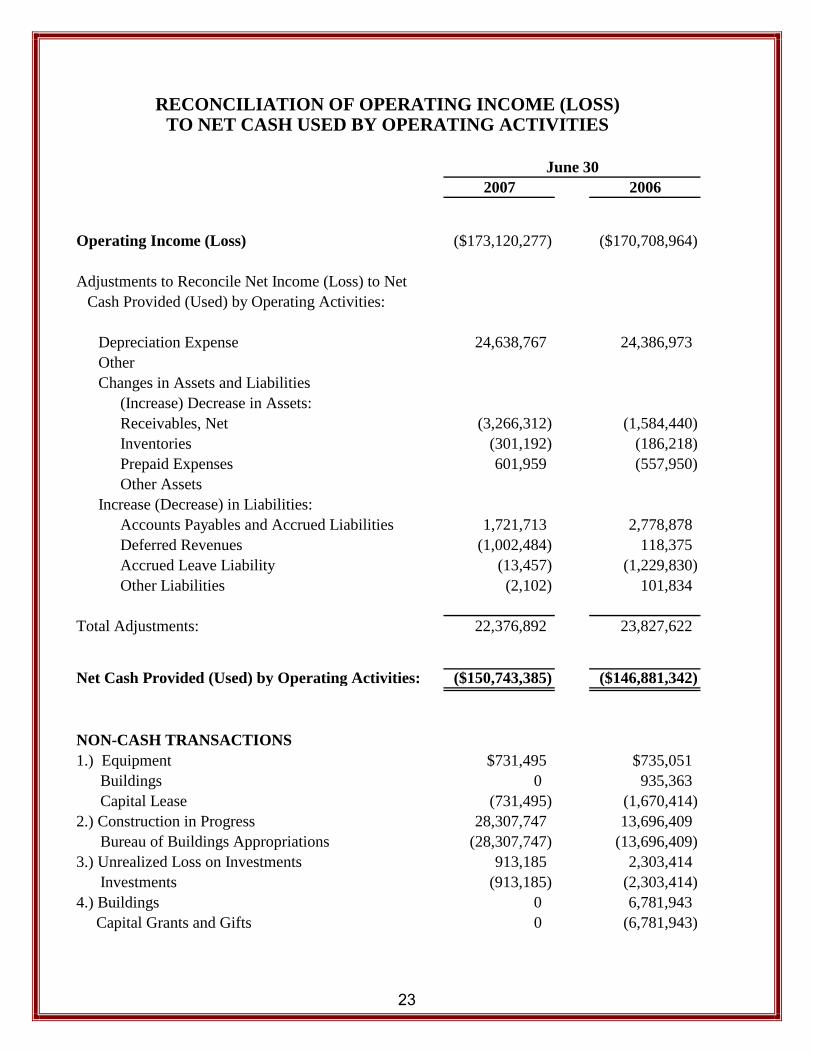

2007 2006

Operating Income (Loss) ($173,120,277) ($170,708,964)

Adjustments to Reconcile Net Income (Loss) to NetCash Provided (Used) by Operating Activities:

Depreciation Expense 24,638,767 24,386,973OtherChanges in Assets and Liabilities

(Increase) Decrease in Assets:Receivables, Net (3,266,312) (1,584,440)Inventories (301,192) (186,218)Prepaid Expenses 601,959 (557,950)Other Assets

Increase (Decrease) in Liabilities:Accounts Payables and Accrued Liabilities 1,721,713 2,778,878Deferred Revenues (1,002,484) 118,375Accrued Leave Liability (13,457) (1,229,830)Other Liabilities (2,102) 101,834

Total Adjustments: 22,376,892 23,827,622

Net Cash Provided (Used) by Operating Activities: ($150,743,385) ($146,881,342)

NON-CASH TRANSACTIONS1.) Equipment $731,495 $735,051 Buildings 0 935,363 Capital Lease (731,495) (1,670,414)2.) Construction in Progress 28,307,747 13,696,409 Bureau of Buildings Appropriations (28,307,747) (13,696,409)3.) Unrealized Loss on Investments 913,185 2,303,414 Investments (913,185) (2,303,414)4.) Buildings 0 6,781,943 Capital Grants and Gifts 0 (6,781,943)

June 30

RECONCILIATION OF OPERATING INCOME (LOSS)TO NET CASH USED BY OPERATING ACTIVITIES

23

Mississippi State University Notes to Financial Statements

Note 1 - Summary of Significant Accounting Policies Reporting Entity – The Mississippi Constitution was amended in 1943 to create a Board of Trustees of State Institutions of Higher Learning. This constitutional Board provides management and control of Mississippi’s system of public higher education. The constitution provides that the Board members be appointed by the Governor with the approval of the Senate. The Board of Trustees consists of twelve (12) members. Four (4) members of the Board of Trustees shall be appointed from each of the three (3) Mississippi Supreme Court districts and, as such vacancies occur, the Governor shall make appointments from the Supreme Court district having the smallest number of Board members until the membership includes four (4) members from each district. The members of the Board of Trustees as constituted on January 1, 2004, shall continue to serve until expiration of their respective terms of office. Appointments made to fill vacancies created by expiration of members’ terms of office occurring after January 1, 2004, shall be as follows: The initial term of the members appointed in 2004 shall be for eleven (11) years; the initial term of the members appointed in 2008 shall be for ten (10) years; and the initial term of the members appointed in 2012 shall be for nine (9) years. After the expiration of the initial terms, all terms shall be for (9) years. Mississippi State University has established its own educational building corporation (a nonprofit corporation incorporated in the State of Mississippi) in accordance with Section 37-101-61 of the Mississippi Code Annotated of 1972. The purpose of this corporation is for the acquisition, construction and equipping of facilities and land for the university. In accordance with Governmental Accounting Standards Board Statement Number 14, this educational building corporation is deemed a component unit of the State of Mississippi Institutions of Higher Learning and is included as a blended component unit in the general purpose financial statements. The State of Mississippi Institutions of Higher Learning is considered a component unit of the State of Mississippi reporting entity. Basis of Presentation – The financial statements have been prepared in accordance with generally accepted accounting principles as prescribed by the Governmental Accounting Standards Board (GASB), including Statement No. 34, Basic Financial Statements – and Management’s Discussion and Analysis – for State and Local Governments, and Statement No. 35, Basic Financial Statements and Management’s Discussion and Analysis of Public Colleges and Universities, issued in June and November, 1999. The university now follows the “business type activities” reporting requirements of GASB Statement No. 34 that provides a comprehensive one-look at the universities financial activities. Basis of Accounting – The financial statements of the university have been prepared on the accrual basis whereby all revenues are recorded when earned and all expenses are recorded when they have been reduced to a legal or contractual obligation to pay. All significant intra-agency transactions have been eliminated. Cash Equivalents – For purposes of the statement of cash flows, the university considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. Investments – The University accounts for its investments at fair value in accordance with GASB Statement No. 31, Accounting and Financial Reporting for Certain Investments and for External Investment Pools. Changes in unrealized gain (loss) on the carrying value of investments are reported as a component of investment income in the statement of revenues, expenses and changes in net assets. Investments for which there are no quoted market prices are not material.

24

Mississippi State University Notes to Financial Statements

Note 1 - Summary of Significant Accounting Policies (Continued) Accounts Receivable, Net – Accounts receivable consist of tuition and fee charges to students. Accounts receivable also include amounts due from federal and state governments, and nongovernmental sources, in connection with reimbursement of allowable expenses made pursuant to the university grants and contracts. Accounts receivable are recorded net of an allowance for doubtful accounts. Student Notes Receivable, Net – Student notes receivable consist of federal, state and institutional loans made to students for the purpose of paying tuition and fee charges. Loan balances that are expected to be paid during the next fiscal year are presented on the statement of net assets as current assets. Those balances that are either in deferment status or expected to be paid back beyond the next fiscal year are presented as non-current assets on the statement of net assets.

Inventories – Inventories consist of physical plant, agriculture, printing and food service supplies. These inventories are generally valued at the lower of cost or market, on either the first-in, first-out (“FIFO”) basis or the average cost basis.

Non-Current Cash and Investments – Cash and investments that are externally restricted to make debt service payments, maintain sinking or reserve funds, or to purchase or construct capital or non-current assets, are classified as non-current assets in the statement of net assets.

Capital Assets – Capital assets are recorded at cost at the date of acquisition, or, if donated, at fair market value at the date of donation. Livestock for educational purposes is adjusted at year-end to reflect market price. Renovations to buildings, and improvements other than buildings that significantly increase the value or extend the useful life of the structure are capitalized. Routine repairs and maintenance are charged to operating expense in the year in which the expense was incurred. Depreciation is computed using the straight-line method over the estimated useful life of the asset and is not allocated to the functional categories. See Note #6 for additional details concerning useful lives, salvage values and capitalization thresholds. Expenditures for construction in progress are capitalized as incurred. Interest expense relating to construction is capitalized net of interest income earned on resources set aside for this purpose. Certain maintenance and replacement reserves have been established to fund costs relating to residences and other auxiliary activity facilities.

Deferred Revenues – Deferred revenues include amounts received for tuition and fees and certain auxiliary activities prior to the end of the fiscal year but related to the subsequent accounting period. Deferred revenues also include amounts received from grant and contract sponsors that have not yet been earned.

Compensated Absences – Twelve-month employees earn annual personal leave at a rate of 12 hours per month for zero to three years of service; 14 hours per month for three to eight years of service; 16 hours per month for eight to 15 years of service; and from 15 years of service and over, 18 hours per month are earned. There is no requirement that annual leave be taken, and there is no maximum accumulation. At termination, these employees are paid for up to 240 hours of accumulated leave. Nine-month employees earn major medical leave at a rate of 13 1/3 hours per month for one month to three years of service; 14 1/5 hours per month for three to eight years of service; 15 2/5 hours per month for eight to 15 years of service; and from 15 years of service and over, 16 hours per month are earned are paid for up to 240 hours of accumulated major medical leave.

25

Mississippi State University Notes to Financial Statements

Note 1 - Summary of Significant Accounting Policies (Continued) Classification of Revenues – The University has classified its revenues as either operating or nonoperating revenues according to the following criteria:

Operating revenues: Operating revenues include activities that have the characteristic of exchange transactions, such as (1) student tuition, net of scholarship discounts and allowances, (2) sales and services of auxiliary enterprises, net of scholarship discounts and allowances, (3) most Federal, state and local grants and contracts and Federal appropriations, and (4) interest on institutional student loans. Gifts (pledges) that are received on an installment basis are recorded at net present value.

Nonoperating revenues: Non-Operating revenues include activities that have the characteristic of non-exchange transactions, such as gifts and contributions, and other revenue sources that are defined as non-operating revenues by GASB No. 9 Reporting Cash Flows of Proprietary and Nonexpendable Trust Funds and Governmental Entities That Use Proprietary Fund Accounting, and GASB No. 34 such as state appropriations and investment income.

Scholarship Discounts and Allowances – Financial aid to students is reported in the financial statements under the alternative method as prescribed by the National Association of College and University Business Officers (NACUBO). Certain aid such as loans, funds provided to students as awarded by third parties, and Federal Direct Lending is accounted for as a third party payment (credited to the student’s account as if the student made the payment). All other aid is reflected in the financial statements as operating expenses, or scholarship allowances, which reduce revenues. The amount reported as operating expenses represents the portion of aid that was provided to the student in the form of cash. Scholarship allowances represent the portion of aid provided to the student in the form of reduced tuition. Under the alternative method, these amounts are computed on a university basis by allocating the cash payments to students, excluding payments for services, on the ratio of total aid to the aid not considered to be third party aid.

Net Assets – GASB No. 34 reports equity as “Net Assets” rather than “Fund Balance”. Net assets are classified according to external donor restrictions or availability of assets for satisfaction of university obligations. Non-expendable restricted net assets are gifts that have been received for endowment purposes, the corpus of which cannot be expended. Expendable restricted net assets represent funds that have been gifted for specific purposes and funds held in Federal loan programs.

The unrestricted net asset balance of $96,597,514 at June 30, 2007 includes $16,560,075 reserved for academic programs and research, $5,733,678 reserved for capital projects, $6,070,600 reserved for repairs and maintenance, with $68,233,161 remaining for other purposes. University Foundation – Although the University is the exclusive beneficiary of the Foundation, the Foundation is independent of the University in all respects. The Foundation is not a subsidiary of the University and is not directly or indirectly controlled by the University. Moreover, the assets of the Foundation are the exclusive property of the Foundation and do not belong to the University. The University is not accountable for, and does not have ownership of, any of the financial and capital resources of the Foundation. The University does not have the power or authority to mortgage, pledge or encumber the assets of the Foundation. The trustees of the Foundation are entitled to make all decisions regarding the business and affairs of the Foundation, including, without limitation, distributions made to the University. Under state law, neither the principal nor income generated by the assets of the Foundation can be taken into consideration in determining the amount of State-appropriated funds allocated to the University. Third parties dealing with the University, the Mississippi State Board of Trustees and the State of Mississippi (or any agency thereof) should not rely upon the financial statements of the Foundation for any purpose without consideration of all of the foregoing conditions and limitations. 26

Mississippi State University Notes to Financial Statements

Note 2 – Change in Accounting Classifications Cash for loan funds was reclassified to restricted cash and cash equivalents on the Statement of Net Assets. Required fees for Athletics and Student Health Center were reclassified from tuition and fees to the appropriate auxiliary enterprise operation. A prorated share of the scholarship allowance was also reclassified. Note 3 - Cash and Investments Policies: A. Cash and Short-term Investments – Investment policies for cash and short-term investments as set forth by the

IHL Board of Trustees policy and state statute authorize the University to invest in demand deposits and interest-bearing time deposits such as savings accounts, certificates of deposit, money market funds, U.S. Treasury bills and notes, and repurchase agreements.

For purposes of the Statement of Cash Flows, the university considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. Cash equivalents representing endowment assets are included in non-current investments.

The collateral for public deposits in financial institutions is now held in the name of the State Treasurer under a program established by the Mississippi State Legislature and is governed by Section 27-105-5 of the Mississippi Code Annotated (1972). Under this program, the University’s funds are protected through a collateral pool administered by the State Treasurer. Financial institutions holding deposits of public funds must pledge securities as collateral against these deposits. In the event of failure of a financial institution, securities pledged by that institution would be liquidated by the State Treasurer to replace the public deposits not covered by the Federal Depository Insurance Corporation.

B. Investments – Investment policy at the university is governed by state statute (Section 27-105-33, MS Code

Ann. 1972) and the Uniform Management of Institutional Funds Act of 1998. The following table presents the fair value of investments by type at June 30, 2007:

Fair

Investment Type Value

U.S. Government Agency Obligations $71,523,734U.S. Treasury Obligations 1,756,939Certificates of Deposit 6,022,631Corporate Bonds 493,887Collateralized Mortgage Obligations 195,444Municipal Bonds 386,849Mutual Funds 3,538,924Asset Backed Securities 1,826,371Equity Securities 15,412,986International Obligations 3,634,767Landgrant 239,789

Total $105,032,321

27

Mississippi State University Notes to Financial Statements

Note 3 – Cash and Investments (Continued) Interest Rate Risk Per GASB Statement No. 40, Interest Rate Risk is defined as the risk a government may face should interest rate variances affect the fair value of investments. As of June 30, 2007, the institution had the following investments subject to Interest Rate Risk: Interest Rate Risk

Fair Investment Maturities (in years)Investment Type Value Less than 1 1 - 5 6 - 10 More than 10

U.S. Government Agency Obligations $71,213,669 $16,539,403 $45,891,958 $8,710,316 $71,992Repurchase AgreementsU.S. Treasury Obligations 1,756,829 973,272 783,557Corporate BondsCommercial Mortgage Backed SecuritiesCollateralized Mortgage ObligationsMunicipal Bonds 386,849 35,015 351,834Asset Backed SecuritiesInternational ObligationsCertificates of Deposit 6,022,631 6,022,631

Total $79,379,978 $23,570,321 $46,675,515 $9,062,150 $71,992 Credit Risk The State of Mississippi Institutions of Higher Learning System does not presently have a formal policy that addresses Credit Risk. As of June 30, 2007 the institution had the following investment credit profile:

FairValue

AAA $79,379,978Not Rated 25,652,343

Total $105,032,321

Rating Agency: S&P

28

Mississippi State University Notes to Financial Statements

Note 3 – Cash and Investments (Continued) Concentration of Credit Risk Per GASB Statement No. 40, Concentration of Credit Risk is defined as the risk of loss attributed to the magnitude of a government’s investment in a single issuer. The State of Mississippi Institutions of Higher Learning System does not presently have a formal policy that addresses Concentration of Credit Risk.

Concentration of Credit RiskFair % of Total

Issuer Value Investments

FHLB $27,921,554 35.17%FNMA 15,338,475 19.32%FHLMC 26,936,428 33.93%FFCB 945,221 1.19%GNMA Derivative 71,992 0.09%Treasury Bill 515,555 0.65%Treasury Note 499,688 0.63%Treasury Strip 741,585 0.93%Municipal Bond 386,849 0.49%Bank Certificate of Deposit 6,022,631 7.59%

Total $79,379,978

Note 4 - Accounts Receivable Accounts receivable consisted of the following at June 30, 2007:

June 30, 2007

Student Tuition $11,354,589Auxiliary Enterprises and Other operating activities 2,814,578Contributions and Gifts 7,529,149Federal, State, and Private Grants and Contracts 27,000,674State Appropriations 1,421,778Accrued Interest 543,637

Total Accounts Receivable $50,664,405

Less Allowance for Doubtful Accounts 3,984,399

Net Accounts Receivable $46,680,006

29

Mississippi State University Notes to Financial Statements

Note 5 - Notes Receivable from Students Notes receivable from students are payable in installments over a period of up to ten years, commencing three to twelve months from the date of separation from the institution. The following is a schedule of interest rates and unpaid balances for the different types of notes receivable held by the institution at June 30, 2007:

Interest Current Non-CurrentRates June 30, 2007 Portion Portion

Perkins Student Loans 3% to 9% $18,129,125 $4,000,000 $14,129,125Other Federal Loans 3% to 9%Institutional loans 0% to 9% 756,817 274,974 481,843

Total Notes Receivable $18,885,942 $4,274,974 $14,610,968

Less Allowance for Doubtful Accounts 1,476,865 1,476,865

Net Notes Receivable $17,409,077 $4,274,974 $13,134,103

30

Mississippi State University Notes to Financial Statements

Note 6 - Capital Assets A summary of changes in capital assets for the year ended June 30, 2007 is presented as follows:

July 1, 2006 Additions Deletions June 30, 2007Nondepreciable Capital Assets: Land $12,652,599 $0 $2,097 $12,650,502 Construction in Progress 132,993,466 61,140,422 2,634,273 191,499,615 Livestock 1,629,376 188,307 135,462 1,682,221

Total Nondepreciable Capital Assets $147,275,441 $61,328,729 $2,771,832 $205,832,338

Depreciable Capital Assets: Improvements Other Than Buildings $47,400,835 $3,615,579 $0 $51,016,414 Buildings 406,844,804 576,002 137,048 407,283,758 Equipment 116,359,314 10,973,732 7,421,365 119,911,681 Library Books 67,768,011 4,429,303 91,371 72,105,943 Total Depreciable Capital Assets $638,372,964 $19,594,616 $7,649,784 $650,317,796

Less Accumulated Depreciation for: Improvements Other Than Buildings $9,704,197 $1,908,085 $0 $11,612,282 Buildings 114,352,709 7,487,149 72,867 121,766,991 Equipment 78,219,314 11,094,386 5,683,784 83,629,916 Library Books 49,559,649 4,149,147 91,371 53,617,425

Total Accumulated Depreciation $251,835,869 $24,638,767 $5,848,022 $270,626,614

Capital Assets, Net $533,812,536 $56,284,578 $4,573,594 $585,523,520

31

Mississippi State University Notes to Financial Statements

Note 6 – Capital Assets (continued)

Depreciation is computed on a straight-line basis with the exception of the library books category, which is computed using a composite method. The following useful lives, salvage values and capitalization thresholds are used to compute depreciation:

Estimated Useful Lives

Salvage Value

Capitalization Threshold

Buildings 40 years 20% $50,000 Improvements Other than Buildings 20 years 20% 25,000 Equipment 3-15 years 1-10% 5,000 Library Books 10 years 0% 0

32

Mississippi State University Notes to Financial Statements

Note 7 - Long-term Liabilities Long-term liabilities of the university consist of notes and bonds payable, capital lease obligations and certain other liabilities that are expected to be liquidated at least one year from June 30, 2007. The various leases cover a period not to exceed five years. The university has the option to prepay all outstanding lease payments less any unearned interest to fully satisfy the obligation. There is also a fiscal funding addendum stating that if funds are not appropriated for periodic payment for any future fiscal period, the lessee will not be obligated to pay the remainder of the total payments due beyond the end of the current fiscal period.

Information regarding original issue amounts, interest rates and maturity dates for bonds, notes and capital leases included in the long-term liabilities balance at June 30, 2007, is listed in the following schedule. A schedule detailing the annual requirements necessary to amortize the outstanding debt is also provided.

Original Annual Due WithinDescription and Purpose Issue Interest Rate Maturity July 1, 2006 Additions Deletions June 30, 2007 One Year

Bonded DebtDormitory Revenue System $2,250,000 3.00% 2020 $1,165,000 $65,000 $1,100,000 $65,000Student Apartments 2,038,000 3.00% 2021 1,145,000 55,000 1,090,000 60,000EBC96 - Revenue Bonds 11,920,000 3.70%-5.00% 2008 7,990,000 7,410,000 580,000 580,000EBC98 - Revenue Bonds 31,865,000 3.75%-5.25% 2023 26,575,000 935,000 25,640,000 980,000EBC01 - Revenue Bonds 16,920,000 4.00%-5.50% 2026 14,115,000 775,000 13,340,000 805,000EBC04 - Revenue Bonds 17,000,000 2.00%-5.00% 2028 16,280,000 480,000 15,800,000 490,000EBC04A - Revenue Bonds 28,790,000 2.00%-5.00% 2029 27,890,000 925,000 26,965,000 950,000EBC05 - Revenue Bonds 58,965,000 4.00%-5.00% 2035 58,965,000 895,000 58,070,000 1,335,000

Total Bonded Debt $154,125,000 $0 $11,540,000 $142,585,000 $5,265,000

Capital Leases Farm Equipment $1,351,542 $365,612 $985,930 $365,750 Computer Equipment 1,282,687 337,604 695,982 924,309 567,697 Vehicles 99,963 58,643 41,320 23,772 Other 891,476 209,504 325,016 775,964 276,392Total Capital Leases $3,625,668 $547,108 $1,445,253 $2,727,523 $1,233,611

Other Long-term Liabilities - Accrued Leave Liabilities $19,155,206 $13,456 $19,168,662 $1,403,690 - Deposits Refundable 86,620 1,130 85,490Total Other Liabilities $19,241,826 $13,456 $1,130 $19,254,152 $1,403,690

Federal Portion of NDSL $15,229,509 $105,625 $15,335,134Total $192,222,003 $666,189 $12,986,383 $179,901,809 $7,902,301

Due Within One Year (7,902,301)

Total Long-term Liabilities $171,999,508

33

Mississippi State University Notes to Financial Statements

Note 7 – Long-term Liabilities (Continued)

Bonded CapitalFiscal Year Debt Leases Interest Total2008 $5,265,000 $1,233,611 $6,732,614 $13,231,2252009 5,430,000 927,484 6,474,254 12,831,7382010 5,365,000 455,748 6,230,645 12,051,3932011 5,560,000 98,427 5,980,190 11,638,6172012 5,770,000 12,253 5,725,498 11,507,7512013-2017 32,915,000 24,032,841 56,947,8412018-2022 30,170,000 16,356,464 46,526,4642023-2027 28,385,000 8,909,948 37,294,9482028-2032 14,695,000 3,776,690 18,471,6902033-2036 9,030,000 931,250 9,961,250Totals $142,585,000 $2,727,523 $85,150,394 $230,462,917

34

Mississippi State University Notes to Financial Statements

Note 8 - Operating Leases Leased property under operating leases is composed of office rent, land, computer software and equipment. The following is a schedule by years of the future minimum rental payments required under those operating leases:

Year Ending June 30 Amount

2008 $3,701,3772009 $3,701,3772010 $3,701,3772011 $3,701,3772012 $3,701,377

Total Minimum Payments Required $18,506,885

The total rental expense for all operating leases, except those with terms of a month or less that were not renewed, for the fiscal year ending June 30, 2007 was $3,701,377.

Note 9 - Natural Classifications with Functional Classifications The universities operating expenses by functional classification were as follows for the year ended June 30, 2007: Functional Salaries Fringe Contractual Scholarships & DepreciationClassification & Wages Benefits Travel Services Utilities Fellowships Commodities Expense Total

Instruction $63,971,135 $17,542,138 $1,405,150 $5,107,923 $113,568 $1,036,605 $89,176,520Research 71,917,294 20,666,067 4,375,130 47,408,218 2,637,880 11,165,974 158,170,563Public Service 39,863,655 12,050,395 3,619,965 14,663,938 2,051,223 4,684,890 76,934,066Academic Support 15,387,098 3,952,642 564,417 4,278,847 213,193 2,195,874 26,592,071Student Services 6,831,927 1,900,816 320,444 1,873,880 (3,614) 492,047 11,415,500Institutional Support 15,694,084 1,897,745 210,238 24,564,915 (86,074) 11,328,498 53,609,406Operation of Plant 11,103,340 3,339,158 58,464 6,799,591 1,064,203 22,364,755Student Aid 895,012 2,041,772 7,178 367,198 $18,709,820 27,949 22,048,929Auxiliary Enterprises 16,198,195 3,980,416 2,375,523 9,244,822 1,838,873 5,503,800 2,793,186 41,934,815Depreciation $24,638,767 24,638,767

Total OperatingExpenses $241,861,738 $67,371,149 $12,936,509 $107,509,742 $13,564,639 $24,213,620 $34,789,228 $24,638,767 $526,885,392

35

Mississippi State University Notes to Financial Statements

Note 10 - Construction Commitments and Financing

The university has contracted for various construction projects as of June 30, 2007. Estimated costs to complete the various projects and the sources of anticipated funding are presented below:

Total Costs Funded by Institutionalto Complete Federal Sources State Sources Funds Other

105-278 Lee Hall Renovation - Phase II $4,593,956 $4,593,956105-285 Colvard Student Union Preplanning 617,690 617,690105-294 Simulation Design Center 5,080,917 5,080,917105-303 2003 ADA Program (Replace Sidewalks) 402,116 402,116105-304 North MS R&E Center Expansion 925,941 925,941105-309 Colvard Student Union Renovation 22,676,435 16,676,435 $6,000,000105-310 Harned Hall Renovation - Phase I 2,698,172 2,698,172105-311 Communications - Sims/Design Center 340,000 340,000105-312 Communications - Colvard Union 5,000 5,000205-163 Band & Choral Rehearsal Hall 3,841,500 1,810,000 $2,031,500205-190 Mark Rothenburg Building & Opera House - Meridian 26,952,000 7,185,915 599,894 19,166,191205-191 Power Generation Plant 16,849,357 16,849,357205-199 McCool Hall Additions & Renovations 16,953,904 16,953,904205-205 Cullis Wade Welcome Center & Museum 8,957,904 8,086,989 870,915205-207 Roy Ruby Residence Hall (EBC 2004) 20,200,000 20,200,000205-208 Palmeiro Center 7,888,911 7,888,911205-210 New Residence Hall - Phase II (EBC 2005) 45,000,000 45,000,000Student Life Center 550,000 550,000Old Main Plaza 7,000,000 7,000,000Newberry Building 1,000,000 1,000,000113-097 Pace Seed Technology Building Reno 1,921,019 1,921,019113-099 MS Veterinary Diagnostic Lab (Phase I) 12,424,745 12,424,745113-102 Agricultural & Biological Engineering Bldg 9,430,435 9,430,435113-104 Communications Pace Seed Lab 117,710 117,710113-106 Landscaping Pace Seed Lab 37,689 37,689113-110 Pre-plan Wise Center Renovation 300,000 300,000113-111 Communications MS Vet Lab 1,145,940 1,145,940113-112 Communications Ag/Bio Eng 110,000 110,000113-113 Wise Center Fire Alarm/Security 549,167 549,167113-115 Lloyd-Ricks Renovation 3,357,970 3,248,210 109,760Stoneville Renovation 441,929 441,929Aquaculture Wetlab Expansion 335,000 335,000

Total $222,705,407 $10,876,054 $58,086,586 $106,720,256 $47,022,510

36

Mississippi State University Notes to Financial Statements

Note 11 - Pension Plan Plan Description. The State of Mississippi Institutions of Higher Learning participates in the Public Employees’ Retirement System of Mississippi (PERS), a cost-sharing multiple-employer defined benefit pension plan. PERS provides retirement and disability benefits, annual cost-of-living adjustments, and death benefits to plan members and beneficiaries. Benefit provisions are established by State law and may be amended only by the State of Mississippi Legislature. PERS issues a publicly available financial report that includes financial statements and required supplementary information which may be obtained by writing to the Public Employees’ Retirement System, PERS Building, 429 Mississippi Street, Jackson, MS 39201-1005 or by calling (601) 359-3589 or 1-800-444-PERS.

Funding Policy. PERS members are required to contribute 7.25% of their annual salary and the institution is required to contribute at an actuarially determined rate. The rate increased to 11.30% as of July 1, 2006 from 10.75%. The contribution requirement of PERS members are established and may be amended only by the State of Mississippi Legislature. The institutional contributions to PERS for the years ending June 30, 2007, 2006, and 2005 were $18,525,366, $16,468,674, and $14,922,385 respectively, and equal to the required contributions for each year. Vesting period – In 2007, the Mississippi Legislature amended the PERS plan to change the vesting period from four to eight years for members who entered the system after July 1, 2007. A member who entered the system prior to July 1, 2007 is still subject to the four-year vesting period provided that the member does not subsequently refund their account balance. PERS also administers an Optional Retirement Plan (ORP) whereby new faculty members may select from three investment companies. ORP contribution rates are identical to the PERS rates. University contributions for the years ending June 30, 2007, 2006, and 2005 were $5,579,208, $4,735,718, and $4,176,339 respectively. Note 12 - Donor Restricted Endowments The net depreciation on investments of donor restricted endowments that is available for authorization for expenditure decreased $90,657 to $2,924,788. This amount is included on the Statement of Net Assets as Restricted Expendable. Most endowments operate on the total-return concept as permitted by the Uniform Management of Institutional Funds Act (Sections 79-11-601 through 79-11-617, MS code, Ann. 1972) as enacted in 1998. The annual spending rate for these endowments is 5% of the three-year moving average of fiscal year end endowment fund market values using the most previous fiscal years, plus any funds available but not spent in previous fiscal years. Note 13 – Federal Direct Lending and FFEL Programs The University distributed $61,809,719 for the year ended June 30, 2007, for student loans through the U. S. Department of Education lending programs. These distributions and their related funding sources are included as “Non-Capital Financing Distributions” in the Cash Flows Statement.

37

Mississippi State University Notes to Financial Statements

Note 14 - Foundations and Affiliated Parties Mississippi State University Foundation (Foundation) is a legally separate, tax-exempt organization supporting Mississippi State University (University). The Foundation acts primarily as a fund-raising organization to supplement the resources that are available to the University in support of its programs. The 44-member board of the Foundation is self-perpetuating and consists of graduates and friends of the University. Although the University does not control the timing or amount of receipts from the Foundation, the majority of resources or income thereon that the Foundation holds and invests is restricted to the activities of the University by the donors. Because these restricted resources held by the Foundation can only be used by, or for the benefit of, the University, the Foundation is considered a component unit of the University and is discretely presented in the University’s financial statements. During the year ended June 30, 2007, the Foundation made distributions of $36,163,370 to or on behalf of the University for both restricted and unrestricted purposes. Immediately following this note are the financial statements for the Foundation. Any questions regarding the Foundation statements or requests for additional information may be addressed to the Administrative Office, Hunter Henry Center, P.O. Box 6149, Mississippi State, MS 39762.

Note 15 – Subsequent Events As of June 30, 2007 the University was in the final stages of issuing new debt in the amount of $6.1 million for the Colvard Student Union renovation. In August 2004 the University received permission by authority of the Directors of the Phil Hardin Foundation to remove the endowment restrictions from the $1 million Technology Enhancement portion of the Riley Education and Performing Arts Center Grant Agreement. The University reallocated the $1 million to the construction phase of the Newberry Building as part of the Riley Center Project. As part of the agreement with The Phil Hardin Foundation the University will fully fund the $1 million for the Technology Enhancement portion of the endowment from alternative fiscal sources during fiscal year 2008.

38

Mississippi State

University

Foundation, Inc.

Financial Statements

June 30, 2007 and 2006 (With Independent Auditors’ Report Thereon)

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Financial Statements

June 30, 2007 and 2006

(With Independent Auditors’ Report Thereon)

KPMG LLP Suite 1100 One Jackson Place 188 East Capitol Street Jackson, MS 39201

KPMG LLP, a U.S. limited liability partnership, is the U.S. member firm of KPMG International, a Swiss cooperative.

Independent Auditors’ Report

The Board of Directors Mississippi State University Foundation, Inc.:

We have audited the accompanying statements of financial position of Mississippi State University Foundation, Inc. (the Foundation) as of June 30, 2007 and 2006, and the related statements of activities and cash flows for the years then ended. These financial statements are the responsibility of the Foundation’s management. Our responsibility is to express an opinion on these financial statements based upon our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Foundation’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Foundation as of June 30, 2007 and 2006, and the changes in its net assets and its cash flows for the years then ended, in conformity with U.S. generally accepted accounting principles.

November 9, 2007

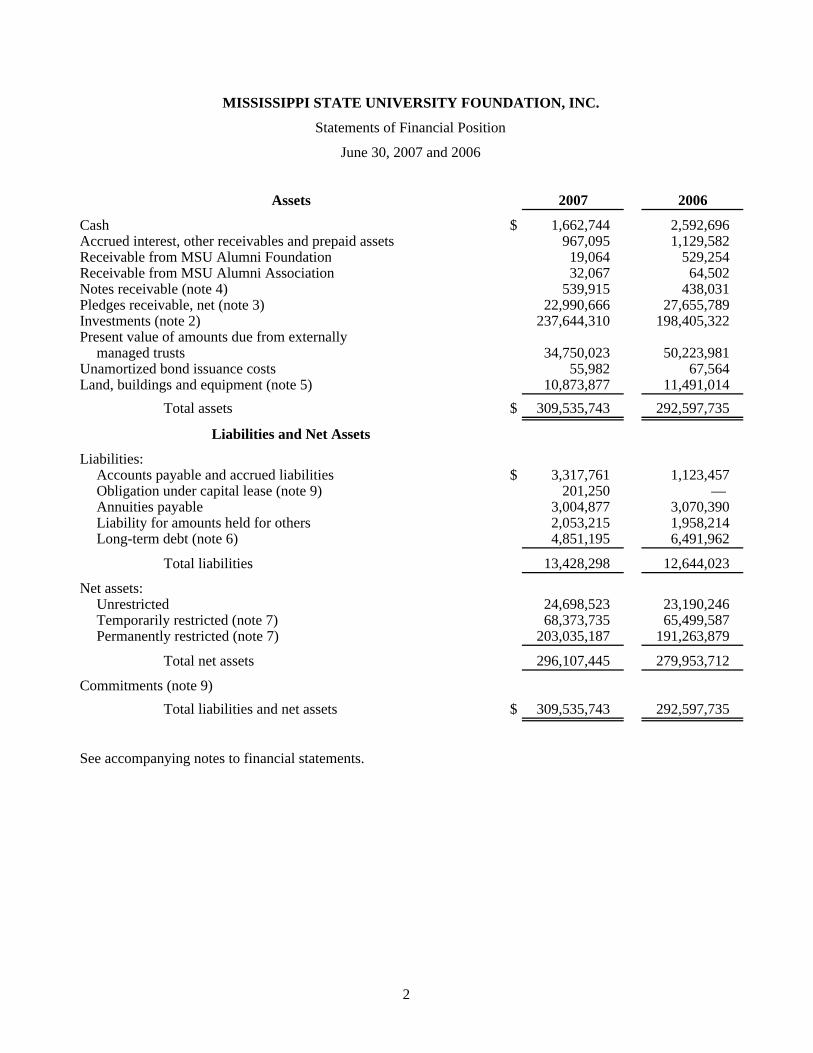

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Statements of Financial Position

June 30, 2007 and 2006

Assets 2007 2006

Cash $ 1,662,744 2,592,696 Accrued interest, other receivables and prepaid assets 967,095 1,129,582 Receivable from MSU Alumni Foundation 19,064 529,254 Receivable from MSU Alumni Association 32,067 64,502 Notes receivable (note 4) 539,915 438,031 Pledges receivable, net (note 3) 22,990,666 27,655,789 Investments (note 2) 237,644,310 198,405,322 Present value of amounts due from externally

managed trusts 34,750,023 50,223,981 Unamortized bond issuance costs 55,982 67,564 Land, buildings and equipment (note 5) 10,873,877 11,491,014

Total assets $ 309,535,743 292,597,735

Liabilities and Net Assets

Liabilities:Accounts payable and accrued liabilities $ 3,317,761 1,123,457 Obligation under capital lease (note 9) 201,250 — Annuities payable 3,004,877 3,070,390 Liability for amounts held for others 2,053,215 1,958,214 Long-term debt (note 6) 4,851,195 6,491,962

Total liabilities 13,428,298 12,644,023

Net assets:Unrestricted 24,698,523 23,190,246 Temporarily restricted (note 7) 68,373,735 65,499,587 Permanently restricted (note 7) 203,035,187 191,263,879

Total net assets 296,107,445 279,953,712

Commitments (note 9)Total liabilities and net assets $ 309,535,743 292,597,735

See accompanying notes to financial statements.

2

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Statement of Activities

Year ended June 30, 2007

Temporarily PermanentlyUnrestricted restricted restricted Total

Revenues and support:Contributions $ 7,323,813 7,315,406 17,719,486 32,358,705 Net investment income (note 2) 6,451,180 25,790,340 507,801 32,749,321 Change in value of split interest agreements — (2,234,450) (7,224,749) (9,459,199) Other 1,920,356 1,171,959 — 3,092,315 Net assets released from restrictions 28,400,337 (29,169,107) 768,770 —

Total revenues and support 44,095,686 2,874,148 11,771,308 58,741,142

Expenditures:Program services:

Contributions and support for MississippiState University 36,163,370 — — 36,163,370

Contributions and support for MSUAlumni Association 683,397 — — 683,397

Total program services 36,846,767 — — 36,846,767

Supporting services:General and administrative 2,891,380 — — 2,891,380 Fund raising 2,849,262 — — 2,849,262

Total supporting services 5,740,642 — — 5,740,642

Total expenditures 42,587,409 — — 42,587,409

Increase in net assets 1,508,277 2,874,148 11,771,308 16,153,733

Net assets at beginning of year 23,190,246 65,499,587 191,263,879 279,953,712 Net assets at end of year $ 24,698,523 68,373,735 203,035,187 296,107,445

See accompanying notes to financial statements.

3

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Statement of Activities

Year ended June 30, 2006

Temporarily PermanentlyUnrestricted restricted restricted Total

Revenues and support:Contributions $ 8,001,657 15,929,178 19,599,064 43,529,899 Net investment income (note 2) 6,728,565 10,913,334 111,642 17,753,541 Change in value of split interest agreements — 6,779,083 8,740,036 15,519,119 Other 2,024,660 1,006,058 — 3,030,718 Net assets released from restrictions 20,298,813 (20,501,878) 203,065 —

Total revenues and support 37,053,695 14,125,775 28,653,807 79,833,277

Expenditures:Program services:

Contributions and support for MississippiState University 25,631,242 — — 25,631,242

Contributions and support for MSUAlumni Association 600,000 — — 600,000

Total program services 26,231,242 — — 26,231,242

Supporting services:General and administrative 2,657,780 — — 2,657,780 Fund raising 2,428,259 — — 2,428,259

Total supporting services 5,086,039 — — 5,086,039

Total expenditures 31,317,281 — — 31,317,281

Increase in net assets 5,736,414 14,125,775 28,653,807 48,515,996

Net assets at beginning of year 17,453,832 51,373,812 162,610,072 231,437,716 Net assets at end of year $ 23,190,246 65,499,587 191,263,879 279,953,712

See accompanying notes to financial statements.

4

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Statements of Cash Flows

Years ended June 30, 2007 and 2006

2007 2006

Cash flows from operating activities:Increase in net assets $ 16,153,733 48,515,996 Adjustments to reconcile increase in net assets to cash used in

operating activities:Depreciation and amortization 978,766 945,269 Realized and unrealized gains on investments, net (25,349,015) (12,055,135) Loss on sale of building and equipment — 1,732 Present value adjustments to annuities 313,506 315,957 Fair value of donated assets (4,553,114) (4,298,912) Change in accrued interest, other receivables and prepaid assets 162,487 160,953 Change in pledges receivable, net 4,665,123 (10,687,297) Change in externally managed trusts 15,473,958 (11,887,100) Change in accounts payable and accrued liabilities 2,194,304 59,541 Change in liability for amounts held for others 95,001 45,371 Change in receivable from MSU Alumni Foundation 510,190 (507,427) Change in receivable from/payable to Mississippi State University — 1,176,128 Change in receivable from/payable to MSU Alumni Association 32,435 (193,961) Permanently restricted investment dividends and interest (1,205) (474) Permanently restricted contributions (17,719,486) (19,599,064)

Net cash used in operating activities (7,043,317) (8,008,423)

Cash flows from investing activities:Purchases of land, buildings and equipment (115,247) (38,840) Proceeds from sale of equipment — 375 Purchases of investments (9,400,000) (13,435,363) Proceeds from sales and maturities of investments 63,141 4,403,169 Advances on notes receivable (122,033) — Payments on note receivable 20,149 38,560

Net cash used in investing activities (9,553,990) (9,032,099)

Cash flows from financing activities:Principal payments on long-term debt (1,645,567) (651,945) Permanently restricted investment dividends and interest 1,205 474 Permanently restricted contributions 17,719,486 19,599,064 Investments subject to annuity agreements 117,302 139,085 Annuity payments (496,321) (481,534) Principal payments on capital lease obligation (28,750) —

Net cash provided by financing activities 15,667,355 18,605,144

Net increase (decrease) in cash (929,952) 1,564,622

Cash at beginning of year 2,592,696 1,028,074 Cash at end of year $ 1,662,744 2,592,696

Supplemental disclosure of cash flow information:Cash paid during the year for interest $ 128,407 122,239

Capital lease obligation for equipment $ 230,000 —

See accompanying notes to financial statements.

5

MISSISSIPPI STATE UNIVERSITY FOUNDATION, INC.

Notes to Financial Statements

June 30, 2007 and 2006

6 (Continued)

(1) Significant Accounting Policies

(a) Organization

Mississippi State University Foundation, Inc. (the Foundation) is a not-for-profit entity established to solicit and manage funds for the benefit of Mississippi State University (the University).

(b) Basis of Accounting

These financial statements, which are presented on the accrual basis of accounting, have been prepared to present balances and transactions according to the existence or absence of donor-imposed restrictions. This has been accomplished by classification of net assets and transactions into three classes – permanently restricted, temporarily restricted or unrestricted as follows:

Permanently restricted net assets – net assets subject to donor-imposed stipulations that they be maintained permanently by the Foundation. Generally, the donor of these assets permits the Foundation to use all or part of the income earned on related investments for general or specific purposes in support of the University.

Temporarily restricted net assets – net assets subject to donor-imposed stipulations that may or will be met by actions of the Foundation and/or the passage of time.

Unrestricted net assets – net assets which represent resources generated from operations or that are not subject to donor-imposed stipulations. Unrestricted net assets include contributions designated to a particular college or unit for which the use or purpose is unrestricted.

Revenues are reported as increases in unrestricted net assets unless use of the related assets is limited by donor-imposed restrictions. Expenditures are reported as decreases in unrestricted net assets. Gains and losses on investments and other assets or liabilities are reported as increases or decreases in unrestricted net assets unless their use is restricted by explicit donor stipulations or by law. Expirations of restrictions on net assets (i.e., the donor-stipulated purpose has been fulfilled and/or the stipulated time period has elapsed) are reported as reclassifications between the applicable classes of net assets.

Contributions, including unconditional promises to give, are recognized as revenues in the period received. Conditional promises to give are not recognized until they become unconditional, that is, when the conditions on which they depend are substantially met. Contributions of assets other than cash are recorded at their estimated fair value. Contributed goods and services are recorded as revenues and expenses in the statement of activities at estimated fair value.