Embed Size (px)

Citation preview

Page 1 CONFIDENTIAL

September 2017 Vantiv, LLC

Confidential Information Memorandum

$600MM Incremental Revolver $1,605MM Incremental Term Loan A

$1,270,000,000 Incremental Term Loan B $761MM Term Loan B Repricing

Special Notice Regarding Publicly Available Information

THE COMPANY HAS REPRESENTED THAT THE INFORMATION CONTAINED IN THIS CONFIDENTIAL

INFORMATION MEMORANDUM IS EITHER PUBLICLY AVAILABLE OR DOES NOT CONSTITUTE MATERIAL NON-

PUBLIC INFORMATION WITH RESPECT TO THE COMPANY OR ITS SECURITIES. THE RECIPIENT OF THIS

CONFIDENTIAL INFORMATION MEMORANDUM HAS STATED THAT IT DOES NOT WISH TO RECEIVE MATERIAL

NON-PUBLIC INFORMATION WITH RESPECT TO THE COMPANY OR ITS SECURITIES AND ACKNOWLEDGES

THAT OTHER LENDERS HAVE RECEIVED A CONFIDENTIAL INFORMATION MEMORANDUM THAT CONTAINS

ADDITIONAL INFORMATION WITH RESPECT TO THE COMPANY OR ITS SECURITIES THAT MAY BE MATERIAL.

NEITHER THE COMPANY NOR THE ARRANGER TAKES ANY RESPONSIBILITY FOR THE RECIPIENT'S DECISION

TO LIMIT THE SCOPE OF THE INFORMATION IT HAS OBTAINED IN CONNECTION WITH ITS EVALUATION OF THE

COMPANY AND THE FACILITY.

Vantiv, LLC

Revolver & Term Loan A Joint Lead Arrangers

Documentation Agents

Term Loan B Joint Lead Arrangers

Page 2 CONFIDENTIAL

September 2017 Vantiv, LLC

Notice to and Undertaking by Recipients

This Confidential Information Memorandum (the "Confidential Information Memorandum") has been prepared solely for informational purposes from

information supplied by or on behalf of Vantiv, LLC. (the "Company"), and is being furnished by Morgan Stanley (the "Arranger") to you in your capacity as

a prospective lender (the "Recipient") in considering the proposed Credit Facility described in the Confidential Information Memorandum (the "Facility").

ACCEPTANCE OF THIS CONFIDENTIAL INFORMATION MEMORANDUM CONSTITUTES AN AGREEMENT TO BE BOUND BY THE TERMS OF

THIS NOTICE AND UNDERTAKING AND THE SPECIAL NOTICE SET FORTH ON THE COVER PAGE HEREOF (THE “SPECIAL NOTICE”). IF THE

RECIPIENT IS NOT WILLING TO ACCEPT THE CONFIDENTIAL INFORMATION MEMORANDUM AND OTHER EVALUATION MATERIAL (AS

DEFINED HEREIN) ON THE TERMS SET FORTH IN THIS NOTICE AND UNDERTAKING AND THE SPECIAL NOTICE, IT MUST RETURN THE

CONFIDENTIAL INFORMATION MEMORANDUM AND ANY OTHER EVALUATION MATERIAL TO THE ARRANGER IMMEDIATELY WITHOUT

MAKING ANY COPIES THEREOF, EXTRACTS THEREFROM OR USE THEREOF.

I. Confidentiality

As used herein: (a) "Evaluation Material" refers to the Confidential Information Memorandum and any other information regarding the Company or the

Facility furnished or communicated to the Recipient by or on behalf of the Company in connection with the Facility (whether prepared or communicated by

the Arranger or the Company, their respective advisors or otherwise) and (b) "Internal Evaluation Material" refers to all memoranda, notes, and other

documents and analyses developed by the Recipient using any of the information specified under the definition of Evaluation Material.

The Recipient acknowledges that the Company considers the Evaluation Material to include confidential, sensitive and proprietary information and agrees

that it shall use reasonable precautions in accordance with its established procedures to keep the Evaluation Material confidential; provided however that

(i) it may make any disclosure of such information to which the Company gives its prior written consent and (ii) any of such information may be disclosed

to it, its affiliates and their respective partners, directors, officers, employees, agents, advisors and other representatives (collectively, "Representatives")

(it being understood that such Representatives shall be informed by it of the confidential nature of such information and shall be directed by the Recipient

to treat such information in accordance with the terms of the Notice and Undertaking and the Special Notice). The Recipient agrees to be responsible for

any breach of the Notice and Undertaking or the Special Notice that results from the actions or omissions of its Representatives.

The Recipient shall be permitted to disclose the Evaluation Material in the event that it is required by law or regulation or requested by any governmental

agency or other regulatory authority (including any self-regulatory organization) or in connection with any legal proceedings. The Recipient agrees that it

will notify the Arranger as soon as practical in the event of any such disclosure (other than at the request of a regulatory authority), unless such notification

shall be prohibited by applicable law or legal process.

The Recipient shall have no obligation hereunder with respect to any Evaluation Material to the extent that such information (i) is or becomes publicly

available other than as a result of a disclosure by the Recipient in violation of this agreement, or (ii) was within the Recipient's possession prior to its being

furnished pursuant hereto or becomes available to the Recipient on a non-confidential basis from a source other than the Company or its agents, provided

that the source of such information was not known by the Recipient to be bound by a confidentiality agreement with or other contractual, legal or fiduciary

obligation of confidentiality to the Company or any other party with respect to such information.

In the event that the Recipient of the Evaluation Material decides not to participate in the transaction described herein, upon request of the Arranger, such

Recipient shall as soon as practicable return all Evaluation Material (other than Internal Evaluation Material) to the Arranger or represent in writing to the

Arranger that the Recipient has destroyed all copies of the Evaluation Material (other than Internal Evaluation Material) unless prohibited from doing so by

the Recipient's internal policies and procedures.

II. Information

The Recipient acknowledges and agrees that (i) the Arranger received the Evaluation Material from third party sources (including the Company) and it is

provided to the Recipient for informational purposes, (ii) the Arranger and its affiliates bear no responsibility (and shall not be liable) for the accuracy or

completeness (or lack thereof) of the Evaluation Material or any information contained therein, (iii) no representation regarding the Evaluation Material is

made by the Arranger or any of its affiliates, (iv) neither the Arranger nor any of its affiliates has made any independent verification as to the accuracy or

completeness of the Evaluation Material, and (v) the Arranger and its affiliates shall have no obligation to update or supplement any Evaluation Material

or otherwise provide additional information.

The Evaluation Material has been prepared to assist interested parties in making their own evaluation of the Company and the Facility and does not

purport to be all-inclusive or to contain all of the information that a prospective participant may consider material or desirable in making its decision

to become a lender. Each Recipient of the information and data contained herein should take such steps as it deems necessary to assure that it has

the information it considers material or desirable in making its decision to become a lender and should perform its own independent investigation

and analysis of the Facility or the transactions contemplated thereby and the creditworthiness of the Company. The Recipient represents that it is

sophisticated and experienced in extending credit to entities similar to the Company. The information and data contained herein are not a substitute

for the Recipient's independent evaluation and analysis and should not be considered as a recommendation by the Arranger or any of its affiliates

that any Recipient enter into the Facility.

The Evaluation Material may include certain forward looking statements and projections provided by the Company. Any such statements and

projections reflect various estimates and assumptions by the Company concerning anticipated results. No representations or warranties are made

by the Company or any of its affiliates as to the accuracy of any such statements or projections. Whether or not any such forward looking

statements or projections are in fact achieved will depend upon future events some of which are not within the control of the Company. Accordingly,

actual results may vary from the projected results and such variations may be material. Statements contained herein describing documents and

agreements are summaries only and such summaries are qualified in their entirety by reference to such documents and agreements.

2

Page 3 CONFIDENTIAL

September 2017 Vantiv, LLC

III. General

It is understood that unless and until a definitive agreement regarding the Facility between the parties thereto has been executed, the Recipient will

be under no legal obligation of any kind whatsoever with respect to the Facility by virtue of this Notice and Undertaking except for the matters

specifically agreed to herein and in the Special Notice.

The Recipient agrees that money damages would not be a sufficient remedy for breach of this Notice and Undertaking or of the Special Notice, and

that in addition to all other remedies available at law or in equity, the Company and the Arranger shall be entitled to equitable relief, including

injunction and specific performance, without proof of actual damages.

This Notice and Undertaking and the Special Notice together embody the entire understanding and agreement between the Recipient and the

Arranger with respect to the Evaluation Material and the Internal Evaluation Material and supersedes all prior understandings and agreements

relating thereto. The terms and conditions of this Notice and Undertaking and the Special Notice shall apply until such time, if any, that the Recipient

becomes a party to the definitive agreements regarding the Facility, and thereafter the provisions of such definitive agreements relating to

confidentiality shall govern. If you do not enter into the Facility, the application of this Notice and Undertaking and the Special Notice shall terminate

with respect to all Evaluation Material on the date falling one year after the date of the Confidential Information Memorandum.

This Notice and Undertaking and the Special Notice shall be governed by and construed in accordance with the law of the State of New York,

without regard to principles of conflicts of law (except Section 5-1401 of the New York General Obligation Law to the extent that it mandates that the

law of the State of New York govern).

IV. No Offer or Solicitation

This Confidential Information Memorandum is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the

solicitation of an offer to buy any securities or a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in

which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

V. Forward-Looking Statements

This Confidential Information Memorandum contains forward-looking statements that are subject to risks and uncertainties. All statements other than

statements of historical fact or relating to present facts or current conditions included in this Confidential Information Memorandum are forward-

looking statements including any statements regarding guidance and statements of a general economic or industry specific nature. Forward-looking

statements give our current expectations and projections relating to our financial condition, results of operations, guidance, plans, objectives, future

performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These

statements may include words such as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “will,” “may,” “should,” “can have,”

“likely” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial

performance or other events.

The forward-looking statements contained in this Confidential Information Memorandum are based on assumptions that we have made in light of

our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are

appropriate under the circumstances. As you review and consider information presented herein, you should understand that these statements are

not guarantees of future performance or results. They depend upon future events and are subject to risks, uncertainties (many of which are beyond

our control) and assumptions. Although we believe that these forward-looking statements are based on reasonable assumptions, you should be

aware that many factors could affect our actual future performance or results and cause them to differ materially from those anticipated in the

forward-looking statements. Certain of these factors and other risks are discussed in the filings of the Company with the U.S. Securities and

Exchange Commission (the “SEC”) and include, but are not limited to: (i) our ability to adapt to developments and change in our industry; (ii)

competition; (iii) unauthorized disclosure of data or security breaches; (iv) systems failures or interruptions; (v) our ability to expand our market

share or enter new markets; (vi) our ability to identify and complete acquisitions, joint ventures and partnerships; (vii) failure to comply with

applicable requirements of Visa, MasterCard or other payment networks or changes in those requirements; (viii) our ability to pass along fee

increases; (ix) termination of sponsorship or clearing services; (x) loss of clients or referral partners; (xi) reductions in overall consumer, business

and government spending; (xii) fraud by merchants or others; (xiii) a decline in the use of credit, debit or prepaid cards; (xiv) consolidation in the

banking and retail industries; (xv) the effects of governmental regulation or changes in laws; (xvi) outcomes of future litigation or investigations; (xvii)

uncertainties as to the timing of the transaction; (xviii) uncertainties as to whether the transaction will be completed; (xix) the possibility that

shareholders or other third parties will file lawsuits challenging the transaction; (xx) potential operating costs, customer loss and business disruption

occurring prior to completion of the transaction or if the transaction is not completed; (xxi) the effect of the announcement of the transaction on our

business relationships, operating results and business generally; (xxii) the failure to satisfy conditions to completion of the transaction, including the

receipt of all required regulatory approvals; and (xxiii) difficulty in retaining certain key employees as a result of the transaction. Should one or more

of these risks or uncertainties materialize, or should any of these assumptions prove incorrect, our actual results may vary in material respects from

those projected in these forward-looking statements. More information on potential factors that could affect the Company’s financial results and

performance is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” sections of the Company’s periodic reports filed with the SEC, including the Company’s most recently filed Annual Report on Form 10-K

and its subsequent filings with the SEC.

Any forward-looking statement made by us in this Confidential Information Memorandum speaks only as of the date of this Confidential Information

Memorandum. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all

of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments

or otherwise, except as may be required by law.

3

Page 4 CONFIDENTIAL

September 2017 Vantiv, LLC

VI. Important Additional Information and Where to Find It

This Confidential Information Memorandum may be deemed to be solicitation material in respect of the acquisition (the “Acquisition”) of Worldpay

Group plc (“Worldpay”) by the Company, including the issuance of shares of the Company’s common stock in respect of the Acquisition. In

connection with the foregoing proposed issuance of the Company’s common stock, the Company expects to file a proxy statement on Schedule 14A

with the SEC. To the extent the Company effects the Acquisition of Worldpay as a Scheme of Arrangement under United Kingdom law, the issuance

of the Company’s common stock in the Acquisition would not be expected to require registration under the Securities Act of 1933, as amended (the

“Act”), pursuant to an exemption provided by Section 3(a)(10) under the Act. In the event that the Company determines to conduct the Acquisition

pursuant to an offer or otherwise in a manner that is not exempt from the registration requirements of the Act, it will file a registration statement with

the SEC containing a prospectus with respect to the Company’s common stock that would be issued in the Acquisition. INVESTORS AND

STOCKHOLDERS ARE URGED TO READ THE PROXY STATEMENT AND OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH

THE SEC CAREFULLY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE

COMPANY, THE ACQUISITION AND RELATED MATTERS. Investors and stockholders will be able to obtain free copies of the proxy statement

and other documents filed by the Company with the SEC at the SEC’s website at www.sec.gov. In addition, investors and stockholders will be able

to obtain free copies of the proxy statement and other documents filed by the Company with the SEC at http://investors.vantiv.com/.

VII. Participants in the Solicitation

The Company and its directors, officers and employees may be considered participants in the solicitation of proxies from the Company’s

stockholders in respect of the Acquisition. Information regarding the persons who may, under the rules of the SEC, be deemed participants in the

solicitation of the Company’s stockholders in connection with the Acquisition, including names, affiliations and a description of their direct or indirect

interests, by security holdings or otherwise, will be set forth in the proxy statement and other relevant materials to be filed with the SEC. Information

concerning the interests of the Company’s participants in the solicitation, which may, in some cases, be different than those of the Company’s

stockholders generally, is set forth in the materials filed by the Company with the SEC, including in the proxy statement for the Company’s 2017

Annual Meeting of Stockholders, which was filed with the SEC on March 15, 2017, as supplemented by other Company filings with the SEC, and will

be set forth in the proxy statement relating to the Acquisition when it becomes available.

VIII. Non-GAAP Financial Measures

This Confidential Information Memorandum contains estimated financial information that is unaudited and not presented in accordance with US

Generally Accepted Accounting Principles (GAAP).

Such information includes financial information presented in accordance with International Financial Reporting Standards (IFRS); information

relating to the combined financial data presented with the side-by-side financials; estimated efficiencies and run-rate savings; estimated synergies

and efficiencies; and adjusted earnings per share, which excludes non-cash amortization of intangible assets. This information has been provided

on a forward-looking basis pursuant to an exception for non-GAAP financial measures included in disclosures relating to a proposed business

combination transaction, the entity resulting from the business combination transaction or an entity that is a party to the business combination

transaction where the communication containing such disclosure is subject to the SEC’s rules relating to communications applicable to business

combination transactions. Investors should not place undue reliance on these measures and should carefully review the risks and uncertainties

described in the cautionary statement relating to “Forward-Looking Statements” contained herein.

IX. Representations

It is understood and acknowledged that any person's access to, and use of, any of the attached materials constitutes their overall acceptance of the

following: (1) none of Vantiv, Worldpay, the Company, or any other party involved in the preparation of the attached materials makes any

representation, warranty or claim that the materials and information contained therein is current or accurate; (2) by virtue of access to these

materials, no one shall be entitled to claim detrimental reliance on any information provided or expressed; (3) no person should rely on statements

or representations made within these materials nor should any person rely on the statements or representations made by any other source based

on these materials; and (4) neither Vantiv, Worldpay, the Company, nor any other party involved in the preparation of the attached materials shall

have any duty or liability to any person in connection with the attached materials.

4

Page 6 CONFIDENTIAL

September 2017 Vantiv, LLC

Table of Contents

1. Contact List 7

2. Transaction Timeline 15

3. Transaction Summary 16

4. Company Overviews 20

5. Strategic Rationale & Proposed Transaction Structure 23

6. Industry Overview 25

7. Credit Highlights 27

8. Historical Financial Results & Management’s Discussion and Analysis 38

9. Summary Terms and Conditions 49

1

2

3

4

5

6

7

8

9

6

Page 7 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

Vantiv 8500 Governors Hill Drive

Symmes Township, OH 45249

Name / Title Office E-mail

Stephanie Ferris Tel: +1 513 900 5131 [email protected]

Chief Financial Officer

Ned Greene Tel: +1 513 900 5200 [email protected]

Chief Legal Officer & Secretary

Tim Cooper Tel: +1 513 900 5181 [email protected]

Treasurer

Chris Thompson Tel: +1 513 900 5401 [email protected]

Chief Accounting Officer

Jared Warner Tel: +1 513 900 5263 [email protected]

Deputy General Counsel

Mark Wright Tel: +1 513 900 5183 [email protected]

Assistant Treasurer

7

Page 8 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

Morgan Stanley 1585 Broadway

New York, NY, 10036

Name / Title Office E-mail

IBD - Business Services Group

Seth Bergstein Tel: +1 212 761 7019 [email protected]

Head of Global Services Group Fax: +1 212 507 0257

Managing Director

Paul Wasinger Tel: +1 212 761 0687 [email protected]

Head of Payments and Processing Fax: +1 212 507 0084

Managing Director

Ryan Fernandes Tel: +1 212 761 4418 [email protected]

Vice President Fax: +1 718 233 0765

William Zapata Tel: +1 212 761 9210 [email protected]

Associate

Simon Osipov Tel: +1 212 761 0483 [email protected]

Analyst

Global Capital Markets – Credit Advisory

Brian Janiak Tel: +1 212-761-1282 [email protected]

Executive Director Fax: +1 212-507-3446

Maksim Rakhman Tel: +1 212-761-0755 [email protected]

Associate Fax: +1 212-507-0255

8

Page 9 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

Morgan Stanley (cont’d) 1585 Broadway

New York, NY, 10036

Name / Title Office E-mail

Leveraged Finance

Barry Price Tel: +1 212 761 3458 [email protected]

Managing Director Fax: +1 212 507 4738

Robbie Pearson Tel: +1 212 761 1132 [email protected]

Executive Director Fax: +1 201 633 4287

Jordan Ransom Tel: +1 212 761 0074 [email protected]

Associate

James Temple Tel: +1 212 761 3585 [email protected]

Analyst

Legal and Compliance

Jason Terrana Tel: +1 212 762 4814 [email protected]

Executive Director Fax: +1 212 507 6368

9

Page 10 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

Credit Suisse Eleven Madison Avenue

New York, NY, 10010

Name / Title Office E-mail

Technology Investment Banking

Brian Gudofsky Tel: +1 212 325 6571 [email protected]

Global Head of Technology Services

Managing Director

Gary Katz Tel: +1 212 538 8468 [email protected]

Director

Cyril Paleath Tel: +1 212 325 6446 [email protected]

Vice President

Chih-ya Tseng Tel: +1 212 538 3132 [email protected]

Associate

James Eisenstein Tel: +1 212 538 2791 [email protected]

Analyst

Leveraged Finance Origination & Restructuring

Jeb Slowik Tel: +1 212 538 0515 [email protected]

Managing Director

Jason Kulig Tel: +1 212 538 1319 [email protected]

Vice President

Kevin Johnston Tel: +1 212 538 1004 [email protected]

Associate

Daniel Eder Tel: +1 212 538 2161 [email protected]

Analyst

10

Page 11 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

MUFG 1221 Avenue of the Americas, 6th Floor

New York, NY 10020

Name / Title Office E-mail

Corporate Advisory Group

Robert Smock Tel: +1 212 782 4609 [email protected]

Managing Director

Joanita Ricketts Tel: +1 212 782 6564 [email protected]

Director

Gordon O’Brien Tel: +1 212 782 4966 [email protected]

Vice President

Leveraged Finance

James Gorman Tel: +1 212 405 7453 [email protected]

Managing Director

Yen Hua Tel: +1 212 405 7421 [email protected]

Director

Global Relationship Management

Scott Hagel Tel: +1 916 321 7602 [email protected]

Head of GI West & Midwest

Managing Director

Erin McNaughton Tel: +1 312 696 4681 [email protected]

Director

Carol Avila Tel: +1 312 696 4708 [email protected]

Vice President

Richard Benson Tel: +1 312 696 4665 [email protected]

Associate

11

Page 12 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

MUFG (cont’d) 1221 Avenue of the Americas, 6th Floor

New York, NY 10020

Name / Title Office E-mail

Portfolio Management Group

Victor Pierzchalski Tel: +1 312 696 4676 [email protected]

Managing Director

Thomas Danielson Tel: +1 312 696 4518 [email protected]

Director

Eric Hill Tel: +1 312 696 4587 [email protected]

Vice President

Colin O’Callaghan Tel: +1 312 696 4675 [email protected]

Associate

12

Page 13 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

Sidley – Company Counsel 2021 McKinney Ave, Suite 2000

Dallas, TX 75201

Name / Title Office E-mail

U.S. Finance

Kelly Dybala Tel: +1 214 981 3426 [email protected]

Partner

Sean Damm Tel: +1 214 981 3447 [email protected]

Associate

Tony Ortega Tel: +1 214 981 3421 [email protected]

Associate

U.K. Finance

James Crooks Tel: +44 20 7360 2040 [email protected]

Partner

Bryan Robson Tel: +44 20 7360 3717 [email protected]

Partner

Will Gwyn Tel: +44 20 7360 2047 [email protected]

Associate

13

Page 14 CONFIDENTIAL

September 2017 Vantiv, LLC

1. Contact List

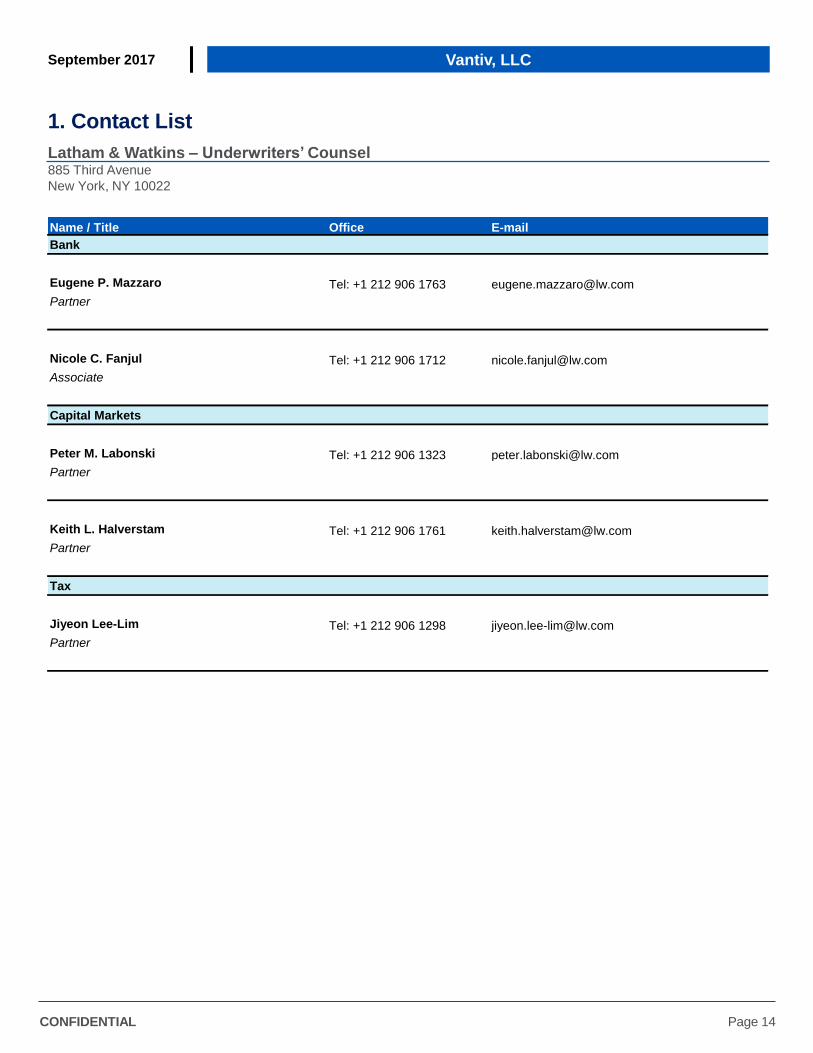

Latham & Watkins – Underwriters’ Counsel 885 Third Avenue

New York, NY 10022

Name / Title Office E-mail

Bank

Eugene P. Mazzaro Tel: +1 212 906 1763 [email protected]

Partner

Nicole C. Fanjul Tel: +1 212 906 1712 [email protected]

Associate

Capital Markets

Peter M. Labonski Tel: +1 212 906 1323 [email protected]

Partner

Keith L. Halverstam Tel: +1 212 906 1761 [email protected]

Partner

Tax

Jiyeon Lee-Lim Tel: +1 212 906 1298 [email protected]

Partner

14

Page 15 CONFIDENTIAL

September 2017 Vantiv, LLC

2. Transaction Timeline

Key event Federal holiday

September 2017

S M T W T F S

1 2

3 4 5 6 7 8 9

10 11 12 13 14 15 16

17 18 19 20 21 22 23

24 25 26 27 28 29 30

October 2017

S M T W T F S

1 2 3 4 5 6 7

8 9 10 11 12 13 14

15 16 17 18 19 20 21

22 23 24 25 26 27 28

29 30 31

Lender Call September 7th

Commitments Due September 18th

Close & Fund Term Loan B Week of October 16th

Close & Fund RCF & TLA-4 Q1 2018

15

Page 16 CONFIDENTIAL

September 2017 Vantiv, LLC

3. Transaction Summary

Notes: Assumes exchange rate of $1.2967:£1

1. PF LTM Adjusted EBITDA includes one-third of $200MM of run-rate synergies for illustrative purposes

2. Includes additional addbacks for Vantiv covenant EBITDA purposes; ~$40MM incremental addback as of 6/30/2017

3. Reflects balances expected at close

I. Transaction Overview

• Vantiv (the “Company”) is a leading, integrated payment processor and is the largest merchant and PIN debit acquirer in the U.S.,

based on number of transactions.

• On August 9, 2017, Vantiv and Worldpay announced that they reached agreement on the terms of a recommended combination,

which imply an enterprise value for Worldpay of approximately $12.0 billion (representing 18.6x LTM EBITDA without synergies).

• Worldpay is a leading payments technology company to approximately 400,000 clients worldwide. Using its network and technology,

Worldpay is able to process payments across 146 countries and in 126 currencies.

• In connection with the acquisition, Vantiv has completed an amendment to its existing credit facilities and has completed Agent-level

syndication on the acquisition financing comprised of a $600MM Incremental Revolver, $1,605MM Incremental Term Loan A-4,

$535MM Incremental Term Loan B-1, and $1,130MM of Senior Unsecured Notes

• In addition, Vantiv is seeking to reprice the existing $761MM Term Loan B and syndicate the $1,270MM Incremental Term Loan B

that was funded to complete the buyback of shares owned by Fifth Third Bank “Fifth Third” to reduce their ownership to ~4.9%

Pro forma 1st Lien and total net leverage of 4.1x and 4.8x, respectively, based on the Combined Company’s Pro Forma LTM 6/30/2017

EBITDA of $1,702MM(1)(2). The Combined Company has announced a target of de-levering to a 4.0x debt to EBITDA leverage ratio over

the next 12-18 months.

Sources & Uses and Pro Forma Capitalization

Sources ($MM) (3)

Equity Issuance 8,756

Rolled Vantiv Debt 3,304

Rolled Worldpay Debt 630

Incremental Term Loan A-4 1,605

Incremental Term Loan B-1 535

Incremental Unsecured Notes 1,130

Incremental Vantiv Term Loan B (Fifth Third) 1,270

Cash from Balance Sheet 76

Total 17,306

Uses ($MM) (3)

Equity Purchase Price 10,184

Rolled Vantiv Debt 3,304

Rolled Worldpay Debt 630

Refinanced Vantiv Debt –

Refinanced Worldpay Debt 1,568

Fifth Third Share Buyback 1,270

Provision for Transaction Expenses 350

Total 17,306

Capitalization ($MM) Current 6/30/17 Transaction-Related PF 6/30/17

Cash 120 466 586

Existing Vantiv Revolver 358 -- 358

Existing Vantiv Term Loan A 2,408 -- 2,408

Existing Vantiv Term Loan B 761 -- 761

Incremental Vantiv Term Loan B (Fifth Third) -- 1,270 1,270

Incremental Term Loan A-4 -- 1,605 1,605

Incremental Term Loan B-1 -- 535 535

Existing Vantiv Capital Leases & Leasehold Mortgages 43 -- 43

Rolled Worldpay Capital Leases -- 39 39

Total Secured Debt $3,570 $3,449 $7,019

Incremental Unsecured Notes -- 1,130 1,130

Rolled Worldpay Senior Unsecured Notes (€) -- 591 591

Total Debt $3,570 $5,170 $8,740

Net Debt $3,450 $4,703 $8,153

LTM Adjusted EBITDA

(1)(2) 991 1,702

Secured Leverage 3.6x 4.1x

Gross Leverage 3.6x 5.1x

Net Leverage 3.5x 4.8x

16

Page 17 CONFIDENTIAL

September 2017 Vantiv, LLC

3. Transaction Summary

II. Summary of Indicative Pro Rata Terms

Borrower: Vantiv, LLC (the “Borrower”)

Facility:

Amount $600MM Incremental Revolver

$1,605MM Incremental Term Loan A-4

Maturi ty 5 Years

Pricing

Opening at L+225 bps

RCF Undrawn: 37.5 bps with step-down

Total Leverage-based Pricing Grid:

4.50x+: L+225 bps

4.50x – 3.75x: L+200 bps

3.25x – 3.75x: L+175 bps

2.25x – 3.25x: L+150 bps

Below 2.25x: L+125 bps

Amortizat ion Revolver: None

Term Loan A: 5%/5%/5%/7.5%/10%

Use of

Proceeds:

Revolver: General corporate purposes

Term Loan A-4: To finance the acquisition of Worldpay, refinance existing Worldpay debt, and pay

related fees and expenses

Incremental

Facil ity:

Fixed Dollar Incremental Amount shall be $1,000,000,000 and the leverage ratios applicable to the Ratio-

Based Incremental Amount shall be set at the applicable leverage ratios on the Closing Date with ability

to incur non-USD incremental Term Loans.

Security: First lien on substantially all tangible and intangible assets, including stock of the Borrower and all

domestic restricted subsidiaries (Same as existing)

Guarantors: Vantiv Holding, LLC and the material domestic wholly-owned restricted subsidiaries of the Borrower

(Same as existing) (1)

Optional

Prepayments: Prepayable at Par

Mandatory

Prepayments:

Mandatory prepayments required from proceeds of:

100% net cash proceeds of non-ordinary course asset sale proceeds, with 12 month reinvestment

rights

100% of debt issuance proceeds (other than permitted debt)

50% of excess cash flow with leverage based stepdowns to 25% and 0% based on senior secured

leverage of 4.25x and 3.75x, respectively

(Same as existing)

Financial

Maintenance

Covenants:

Total Leverage Ratio: December 31, 2017 – September 30, 2018: 6.50 to 1.00

• December 31, 2018 – September 30, 2019: 5.75 to 1.00

• December 31, 2019 – September 30, 2020: 5.00 to 1.00

• December 31, 2020 and thereafter: 4.25 to 1.00

4.00 to 1.00 Interest Coverage Ratio

Negative

Covenants: To match Amended Existing Credit Facilities

Note

1. Worldpay US Subsidiaries expected to become guarantors post-closing

17

Page 18 CONFIDENTIAL

September 2017 Vantiv, LLC

3. Transaction Summary

III. Summary of Indicative Term Loan B Terms

Borrower: Vantiv, LLC (the “Borrower”)

Facility:

Amount $1,270MM Term Loan B

Maturi ty August 7, 2024

Amortizat ion 1.00% per annum

Use of

Proceeds: Share buyback of 19.8MM Vantiv shares to reduce Fifth Third’s stake to 4.9% post transaction

Incremental

Facil ity:

Fixed Dollar Incremental Amount shall be $1,000,000,000 and the leverage ratios applicable to the Ratio-

Based Incremental Amount shall be set at the applicable leverage ratios on the Closing Date with ability

to incur non-USD incremental Term Loans

Security: First lien on substantially all tangible and intangible assets, including stock of the Borrower and all

domestic restricted subsidiaries

Guarantors: Vantiv Holding, LLC and the material domestic wholly-owned restricted subsidiaries of the Borrower (1)

Optional

Prepayments: 101 Soft Call (6 months)

Mandatory

Prepayments:

Mandatory prepayments required from proceeds of:

100% net cash proceeds of non-ordinary course asset sale proceeds, with 12 month reinvestment

rights

100% of debt issuance proceeds (other than permitted debt)

50% of excess cash flow with leverage based stepdowns to 25% and 0% based on senior secured

leverage of 4.25x and 3.75x, respectively

Financial

Maintenance

Covenants:

None

Negative

Covenants: To match Amended Existing Credit Facilities

Note

1. Worldpay US Subsidiaries expected to become guarantors post-closing

18

Page 19 CONFIDENTIAL

September 2017 Vantiv, LLC

3. Transaction Summary

IV. Summary of Term Loan B Repricing

Borrower: Vantiv, LLC (the “Borrower”) (same as existing)

Facility:

Amount $761MM Term Loan B

Maturi ty October 14, 2023 (same as existing)

Amortizat ion 1.00% per annum (same as existing)

Use of

Proceeds: Reprice the existing Term Loan B

Incremental

Facil ity:

Fixed Dollar Incremental Amount shall be $1,000,000,000 and the leverage ratios applicable to the Ratio-

Based Incremental Amount shall be set at the applicable leverage ratios on the Closing Date with ability

to incur non-USD incremental Term Loans (same as existing)

Security: First lien on substantially all tangible and intangible assets, including stock of the Borrower and all

domestic restricted subsidiaries (Same as existing)

Guarantors: Vantiv Holding, LLC and the material domestic wholly-owned restricted subsidiaries of the Borrower

(same as existing) (1)

Optional

Prepayments: 101 Soft Call (6 months)

Mandatory

Prepayments:

Mandatory prepayments required from proceeds of:

100% net cash proceeds of non-ordinary course asset sale proceeds, with 12 month reinvestment

rights

100% of debt issuance proceeds (other than permitted debt)

50% of excess cash flow with leverage based stepdowns to 25% and 0% based on senior secured

leverage of 4.25x and 3.75x, respectively

(Same as existing)

Financial

Maintenance

Covenants:

None (same as existing)

Negative

Covenants: To match Amended Existing Credit Facilities (same as existing)

Note

1. Worldpay US Subsidiaries expected to become guarantors post-closing

19

Page 20 CONFIDENTIAL

September 2017 Vantiv, LLC

4. Company Overviews

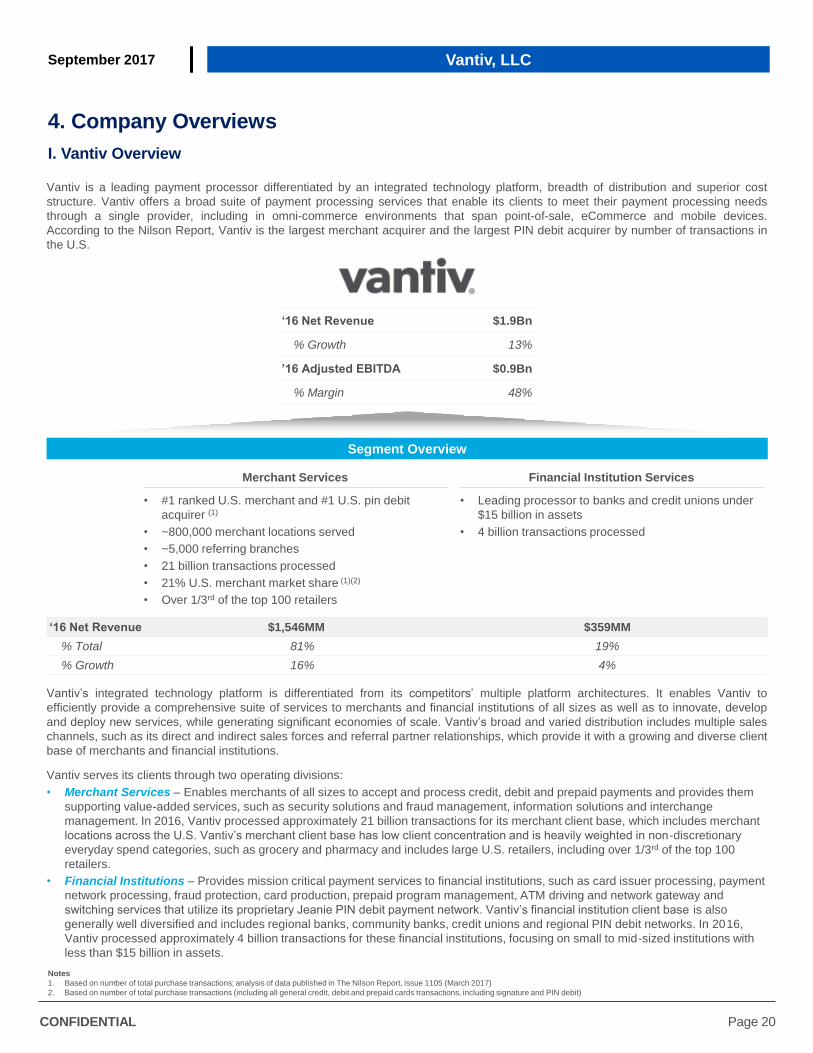

I. Vantiv Overview

Vantiv is a leading payment processor differentiated by an integrated technology platform, breadth of distribution and superior cost

structure. Vantiv offers a broad suite of payment processing services that enable its clients to meet their payment processing needs

through a single provider, including in omni-commerce environments that span point-of-sale, eCommerce and mobile devices.

According to the Nilson Report, Vantiv is the largest merchant acquirer and the largest PIN debit acquirer by number of transactions in

the U.S.

Notes

1. Based on number of total purchase transactions; analysis of data published in The Nilson Report, issue 1105 (March 2017)

2. Based on number of total purchase transactions (including all general credit, debit and prepaid cards transactions, including signature and PIN debit)

Vantiv’s integrated technology platform is differentiated from its competitors’ multiple platform architectures. It enables Vantiv to

efficiently provide a comprehensive suite of services to merchants and financial institutions of all sizes as well as to innovate, develop

and deploy new services, while generating significant economies of scale. Vantiv’s broad and varied distribution includes multiple sales

channels, such as its direct and indirect sales forces and referral partner relationships, which provide it with a growing and diverse client

base of merchants and financial institutions.

Vantiv serves its clients through two operating divisions:

• Merchant Services – Enables merchants of all sizes to accept and process credit, debit and prepaid payments and provides them

supporting value-added services, such as security solutions and fraud management, information solutions and interchange

management. In 2016, Vantiv processed approximately 21 billion transactions for its merchant client base, which includes merchant

locations across the U.S. Vantiv’s merchant client base has low client concentration and is heavily weighted in non-discretionary

everyday spend categories, such as grocery and pharmacy and includes large U.S. retailers, including over 1/3rd of the top 100

retailers.

• Financial Institutions – Provides mission critical payment services to financial institutions, such as card issuer processing, payment

network processing, fraud protection, card production, prepaid program management, ATM driving and network gateway and

switching services that utilize its proprietary Jeanie PIN debit payment network. Vantiv’s financial institution client base is also

generally well diversified and includes regional banks, community banks, credit unions and regional PIN debit networks. In 2016,

Vantiv processed approximately 4 billion transactions for these financial institutions, focusing on small to mid-sized institutions with

less than $15 billion in assets.

‘16 Net Revenue $1.9Bn

% Growth 13%

’16 Adjusted EBITDA $0.9Bn

% Margin 48%

Segment Overview

• Leading processor to banks and credit unions under

$15 billion in assets

• 4 billion transactions processed

Financial Institution Services

• #1 ranked U.S. merchant and #1 U.S. pin debit

acquirer (1)

• ~800,000 merchant locations served

• ~5,000 referring branches

• 21 billion transactions processed

• 21% U.S. merchant market share (1)(2)

• Over 1/3rd of the top 100 retailers

Merchant Services

‘16 Net Revenue $1,546MM $359MM

% Total 81% 19%

% Growth 16% 4%

20

Page 21 CONFIDENTIAL

September 2017 Vantiv, LLC

Worldpay serves a diverse set of merchants across a variety of end-markets, sizes and geographies. On an average day, it processes

over 40 million transactions worldwide (including mobile, online and in-store), offering over 300 payment methods in 126 transaction

currencies across 146 countries, while supporting approximately 400,000 clients, including large enterprises, domestic corporates and

small and medium sized businesses. Globally, Worldpay also partners with innovative and fast-growing eCommerce businesses

including many of the world’s most renowned and dynamic online brands.

Worldpay serves its clients through its three operating divisions:

• Global eCom — Global eCom provides a wide range of online and mobile multi-currency payment acceptance, validation and

settlement services for its client book of large and fast growing internet-led multinationals. The vast majority of Global eCom’s clients

sit within five priority industry verticals: Digital Content, Global Retail, Airlines, Regulated Gambling and Travel. Global eCom

accounted for 46 percent of the Worldpay Group’s business unit contribution in 2016

(4).

• WPUK — WPUK has the number one market share in the U.K., accounting for ~40 percent of the U.K. merchant market as

measured by estimated volume of transactions in 2016. It provides a strong proposition of in-store, phone, online and mobile

payment acceptance solutions for ~300,000 U.K. and Ireland-based clients, from SMBs to major retailers (including Tesco, Asda and

Next). WPUK accounted for 42 percent of the Worldpay Group’s business unit contribution in 2016

(4).

• WPUS — WPUS provides in-store, online and mobile payment acceptance solutions for U.S.-based clients, with a focus on

developing omni-commerce and integrated payment solutions for its ~100,000 SMB clients and vertical-specific solutions for ~15,000

enterprise clients in the grocery, petroleum, restaurant and retail industries. WPUS accounted for 17 percent of the Worldpay

Group’s business unit contribution in 2016

(4).

4. Company Overviews

II. Worldpay Overview

Worldpay is a leader in global payments. Worldpay provides a broad range of technology-led solutions to its merchant clients to allow

them to accept payments of almost any type, across multiple payment channels, nearly anywhere in the world. Worldpay is one of the

few global businesses able to offer functionality in most aspects of payment acceptance, whether in-store, online or on a mobile device,

by providing access to a global payments network through an agile, integrated, secure, reliable and highly scalable proprietary global

payments platform.

Source: Nilson Report, issues 1105 (March 2017) and 1110 (May 2017)

Notes: Assumes exchange rate of $1.2967:£1

1. Worldpay net revenue reflects reported gross profit for comparable reporting conventions to Vantiv, for illustrative purposes, estimated by allocating total gross profit using reported net revenue % of total

2. Underlying EBITDA shown for Worldpay, margin shown after taking into effect net revenue to gross profit adjustment

3. Assumes corporate costs of £25MM are allocated pro rata across segments by Worldpay reported net revenue

4. Corporate costs of £25MM account for (5)% of Group underlying EBITDA

‘16 Net Revenue (1) $1.3Bn

% Growth 15%

’16 Adjusted EBITDA (2) $0.6Bn

% Margin (2) 47%

Segment Overview

U.S.

• #7 merchant acquirer in US

• ~100,000 SME clients and ~15,000

enterprise clients

• Vertical-specific enterprise

solutions: Grocery, Petroleum,

Restaurant and Retail

U.K.

• #1 merchant acquirer in UK

• ~40% share of UK merchant

market by volume

• ~300,000 UK and Ireland-based

clients ranging from SMEs to major

retailers

• Online and mobile multi-currency

payments for multi-national retailers

• ~1,200 clients including some of

the largest, global online merchants

• Verticals: Digital Content, Global

Retail, Airlines, Gaming and Travel

Global eCom

‘16 Net Revenue (1) $439MM $498MM $340MM

% Total 34% 39% 27%

CC Growth 22% 8% 2%

‘16 Adj. EBITDA (2)(3) $273MM $247MM $94MM

% Margin (2)(3) 62% 50% 28%

21

Page 22 CONFIDENTIAL

September 2017 Vantiv, LLC

III. Combined Company Overview

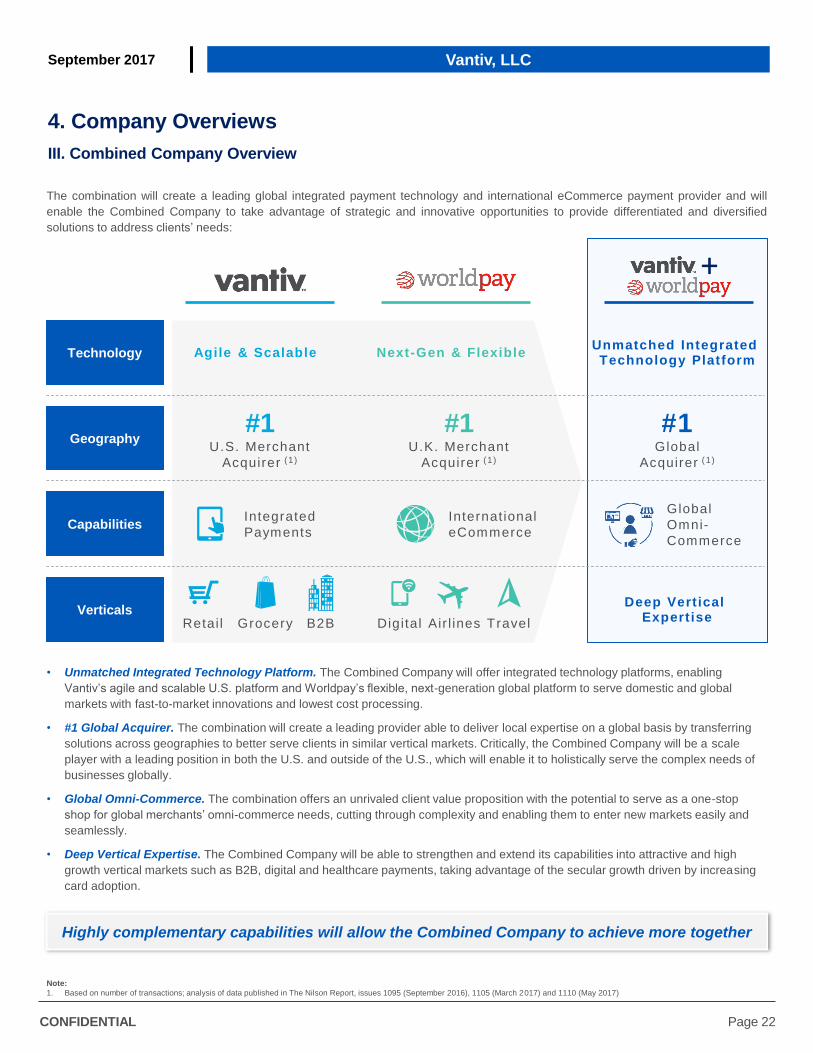

The combination will create a leading global integrated payment technology and international eCommerce payment provider and will

enable the Combined Company to take advantage of strategic and innovative opportunities to provide differentiated and diversified

solutions to address clients’ needs:

• Unmatched Integrated Technology Platform. The Combined Company will offer integrated technology platforms, enabling

Vantiv’s agile and scalable U.S. platform and Worldpay’s flexible, next-generation global platform to serve domestic and global

markets with fast-to-market innovations and lowest cost processing.

• #1 Global Acquirer. The combination will create a leading provider able to deliver local expertise on a global basis by transferring

solutions across geographies to better serve clients in similar vertical markets. Critically, the Combined Company will be a scale

player with a leading position in both the U.S. and outside of the U.S., which will enable it to holistically serve the complex needs of

businesses globally.

• Global Omni-Commerce. The combination offers an unrivaled client value proposition with the potential to serve as a one-stop

shop for global merchants’ omni-commerce needs, cutting through complexity and enabling them to enter new markets easily and

seamlessly.

• Deep Vertical Expertise. The Combined Company will be able to strengthen and extend its capabilities into attractive and high

growth vertical markets such as B2B, digital and healthcare payments, taking advantage of the secular growth driven by increasing

card adoption.

4. Company Overviews

Note:

1. Based on number of transactions; analysis of data published in The Nilson Report, issues 1095 (September 2016), 1105 (March 2017) and 1110 (May 2017)

Technology

Verticals

Geography

Capabilities

Agile & Scalable

Integrated

Payments

Internat ional

eCommerce

Global

Omni-

Commerce

Grocery Retai l Digital Air l ines

Next-Gen & Flexible Unmatched Integrated

Technology Platform

Deep Vertical Expertise B2B

#1 U.K. Merchant

Acquirer

(1)

#1 U.S. Merchant

Acquirer

(1)

#1 Global

Acquirer

(1)

Travel

+

Highly complementary capabilities will allow the Combined Company to achieve more together

22

Page 23 CONFIDENTIAL

September 2017 Vantiv, LLC

5. Strategic Rationale & Proposed Transaction Structure

I. Strategic Rationale for the Transaction

This transaction joins two highly complementary businesses and will allow the Combined Company to achieve more together than either

could on its own. The Combined Company will be well-positioned to offer more innovative and flexible technology and payment

solutions to merchants in a large and fast growing market, creating a strategic omni-commerce partner for merchants of all sizes across

industries.

Creating a leading global payment provider to power omni-commerce. Consumers continue to expect and demand more from

merchants. The global consumer has become accustomed to transacting across the channels and in the geographies of their choosing

in a way that is seamless, simple and secure. Merchants therefore require a payments provider that is able to provide a comprehensive

omni-commerce solution that can deliver a unified consumer experience on a global basis as well as the tools to help them manage and

grow their businesses. By combining the companies’ respective strengths in integrated payments, eCommerce and traditional merchant

offerings, the Combined Company will be able to enable commerce through a unified and global product suite that is in-store, online,

mobile, multi-currency and spanning geographies.

Unique combination of scale and global presence. The Combined Company will become a leading international eCommerce

payment provider, a leading U.S. payment provider and a leading U.K. and European payment provider, processing approximately $1.5

trillion in payment volume and 40 billion transactions through more than 300 payment methods in 146 countries and 126 currencies, with

a combined net revenue of over $3.2 billion (on a pro forma basis, assuming the combination had completed on 31 December 2016).

The Combined Company will benefit from enhanced economies of scale, leveraging its combined operations, technology infrastructure

and data and analytics capabilities to deliver services that are cost efficient and provide superior value to clients.

Ability to capitalize on strategic and high-growth verticals. Completion of the combination will bring together two complementary

partners to create a market leader in payment technology, positioned to capitalize on strategic and high-growth verticals in the most

attractive global markets. The combination will create a leading global eCommerce provider by adding Worldpay’s leading global

eCommerce capabilities to Vantiv’s existing U.S. eCommerce capabilities. The combination will also enable the Combined Company to

export Vantiv’s integrated payments technological know-how and capabilities to Worldpay’s global merchant base. The combination will

enhance the ability of the Combined Company to strengthen and extend its capabilities into attractive and high growth vertical markets

such as B2B, digital and healthcare payments, taking advantage of the secular growth driven by increasing card adoption.

Integrated technology platforms built for innovation and to manage complexity. The Combined Company will have

complementary technology assets that will provide a strong, integrated foundation for innovation and growth, enabled by Vantiv’s agile

and scalable U.S. platform and Worldpay’s flexible, next generation global platform. The combination will enhance the ability of the

Combined Company to serve domestic and global markets and the Combined Company is also expected to benefit from a reduction in

capital expenditure by harmonizing Vantiv’s and Worldpay’s U.S. technology platforms. These U.S. and global technology platforms will

be developed, secured and optimized by one of the industry’s largest pools of engineering and technology talent.

Powerful business model and financial profile. The Combined Company will benefit from an attractive business model and financial

profile, the hallmarks of which are recurring revenue, scalability and significant operating margins. On a pro forma basis, assuming the

combination had completed on 31 December 2016, the Combined Company would have $1.5 billion of adjusted EBITDA, an EBITDA

margin of 48 percent and free cash flow generation of over $1.0 billion with 78 percent free cash flow conversion. It is expected that the

Combined Company, with its strong credit profile and attractive cash flow, will seek to reduce leverage on a consistent basis over the

medium term, including a target of de-levering to a 4.0x debt to EBITDA leverage ratio over the next 12-18 months.

Cost synergies will deliver significant value creation. The Combined Company is expected to benefit from synergies that could not

be achieved independent of the combination. Annual recurring pre-tax cost synergies of approximately $200 million are expected to be

fully realized by the end of the third year following completion of the combination. The majority of these cost synergies will be generated

by harmonizing the Combined Company’s U.S. platforms and streamlining corporate costs.

23

Page 24 CONFIDENTIAL

September 2017 Vantiv, LLC

5. Strategic Rationale & Proposed Post-Closing Structure

II. Proposed Simplified Transaction Structure Summary

Proposed post-closing structure summary subject to legal requirements and ongoing tax and structuring analysis –

subject to change

Fifth Third Bank Vantiv, Inc.

Vantiv Holding U.S.

Subsidiaries

Vantiv

Shareholders

Worldpay

U.S. Subsidiaries

Vantiv U.K.

Payments Ltd. (U.K.)

Vantiv U.K.

Solutions LTD (U.K.)

Vantiv, LLC.

(Delaware)

Vantiv

Holding, LLC.

(Delaware)

Vantiv

Cayman Holdings

Ltd. (Cayman Islands)

Vantiv U.K.

Group Ltd. (U.K.)

Worldpay Group

PLC (U.K.)

Worldpay Finance

PLC (U.K.)

Vantiv

U.K. Ltd. (U.K.)

Worldpay

Non-U.S. Subsidiaries

New Acquisition

Debt & Existing

Vantiv Debt

Existing

Worldpay Unsecured

Notes

24

Page 25 CONFIDENTIAL

September 2017 Vantiv, LLC

Electronic Payments

Electronic payments globally have evolved into a large and growing market with favorable secular trends that continue to increase the

adoption and use of card-based payment services, such as those for credit, debit and prepaid cards.

This growth is driven by the shift from cash and checks towards card-based and other electronic forms of payment due to their greater

convenience, security, enhanced services and rewards and loyalty features. Changing demographics and emerging trends, such as the

adoption of new technologies and business models, including eCommerce, mobile commerce and prepaid services, will also continue to

drive growth in electronic payments.

Payment Processing Industry

The payment processing industry is comprised of various processors that create and manage the technology infrastructure that enables

electronic payments. Payment processors help merchants and financial institutions develop and offer electronic payment solutions to

their customers, facilitate the routing and processing of electronic payment transactions and manage a range of supporting security,

value-added and back office services. In addition, many large banks manage and process their card accounts in-house. This is

collectively referred to as the payment processing value chain.

Many payment processors specialize in providing services in discrete areas of the payment processing value chain, which can result in

merchants and financial institutions using payment processing services from multiple providers. A limited number of payment

processors have capabilities or offer services in multiple parts of the payment processing value chain. The Combined Company will

provide solutions across the payment processing value chain as a merchant acquirer, payment network and as an issuer processor,

primarily by utilizing the integrated technology platform to enable clients to easily access a broad range of payment processing services

as illustrated below:

Payment processing value chain encompasses three key types of processing:

• Merchant Acquiring Processing. Merchant acquiring processors sell electronic payment acceptance, processing and supporting

services to merchants and third-party resellers. These processors route transactions originated by consumer transactions with the

merchant, including in omni-channel environments that span point-of-sale, ecommerce and mobile devices, to the appropriate

payment networks for authorization, known as “front-end” processing and then ensure that each transaction is appropriately cleared

and settled into the merchant’s bank account, known as “back-end” processing. Many of these processors also provide specialized

reporting, back office support, risk management and other value-added services to merchants. Merchant acquirers charge

merchants based on a percentage of the value of each transaction on a per transaction basis. Merchant acquirers pay the payment

network processors a routing fee per transaction and pass through interchange fees to the issuing financial institution.

• Payment Network Processing. Payment network processors, such as Visa, MasterCard and PIN debit payment networks, sell

electronic payment network routing and support services to financial institutions that issue cards and merchant acquirers that provide

transaction processing. Depending on their market position and network capabilities, these providers route credit, debit and prepaid

card transactions from merchant acquiring processors to the financial institution that issued the card and they ensure that the

financial institution’s authorization approvals are routed back to the merchant acquiring processor and that transactions are

appropriately settled between the merchant’s bank and the card-issuing financial institution. These providers also provide specialized

risk management and other value-added services to financial institutions. Payment networks charge merchant acquiring processors

and issuing financial institutions routing fees per transaction and monthly or annual maintenance fees and assessments.

• Issuer Card Processing. Issuer card processors sell electronic payment issuing, processing and supporting services to financial

institutions. These providers authorize transactions received from the payment networks and ensure that each transaction is

appropriately cleared and settled from the originating card account. These companies also provide specialized program

management, reporting, outsourced customer service, back office support, risk management and other value-added services to

financial institutions. Card processors charge issuing financial institutions fees based on the number of transactions processed and

the number of cards that are managed.

6. Industry Overview

Payment Processing Value Chain

M er chant M er chant Acqui r e r

P aym en t Ne twor k

I ssuer P r ocessor

Financ i a l Ins t i tu t i o n

Co

ns

um

er C

on

su

me

r

25

Page 26 CONFIDENTIAL

September 2017 Vantiv, LLC

Competition

U.S. Merchant Services

In the U.S. merchant services market, the Combined Company will hold the number one market position as measured by number of

transactions in 2016 according to the Nilson Report

(1). Its competitors include financial institutions and well-established payment

processing companies, including Bank of America Merchant Services, Chase Paymentech Solutions, Inc., Elavon Inc. (a subsidiary of

U.S. Bancorp), First Data Corporation, Global Payments, Inc. and Total System Services, Inc. Furthermore, the Combined Company is

facing new competitive pressure from non-traditional payments processors and other parties entering the payments industry, such as

Alibaba, Amazon, Apple, Google and PayPal, who may compete in one or more of the functions performed in processing merchant

transactions.

U.K. Merchant Services

In the U.K. merchant services market, the Combined Company will hold the number one market position as measured by number of

transactions in 2016 according to the Nilson Report

(2). Its two largest competitors in the U.K. by number of transactions are Barclays

PLC and Global Payments, Inc. In Europe and the Asia Pacific regions, financial institutions remain the primary providers of payment

processing services to merchants, although outsourcing is becoming more prevalent.

eCommerce

In the Global eCommerce market, the combination will encounter a number of niche specialists, which are typically gateway-led and

offer specific vertical, channel, geographic and/or segment solutions and compete on specific expertise and partnership coverage.

These include companies such as Adyen B.V., Braintree and Stripe, Inc. The Combined Company will also encounter a number of

global payments partners in the eCommerce market, including Elavon Inc., Ingenico Group and Wirecard AG.

U.S. Financial Institution Services

In the U.S. financial institution services market, competitors to the Combined Company include Fidelity National Information Services,

Inc., First Data Corporation, Fiserv, Inc., Total System Services, Inc. and Visa Debit Processing Service. In addition to competition with

direct competitors, the Combined Company also competes with the capabilities of many larger potential clients to conduct their key

payment processing applications in-house. The most significant competitive factors in this segment are price, system performance and

reliability, breadth of services and functionality, data security, scalability, flexibility of infrastructure and servicing capability.

6. Industry Overview

Notes:

1. The Nilson Report (March 2017, Issue 1105)

2. The Nilson Report (May 2017, Issue 1110)

26

Page 27 CONFIDENTIAL

September 2017 Vantiv, LLC

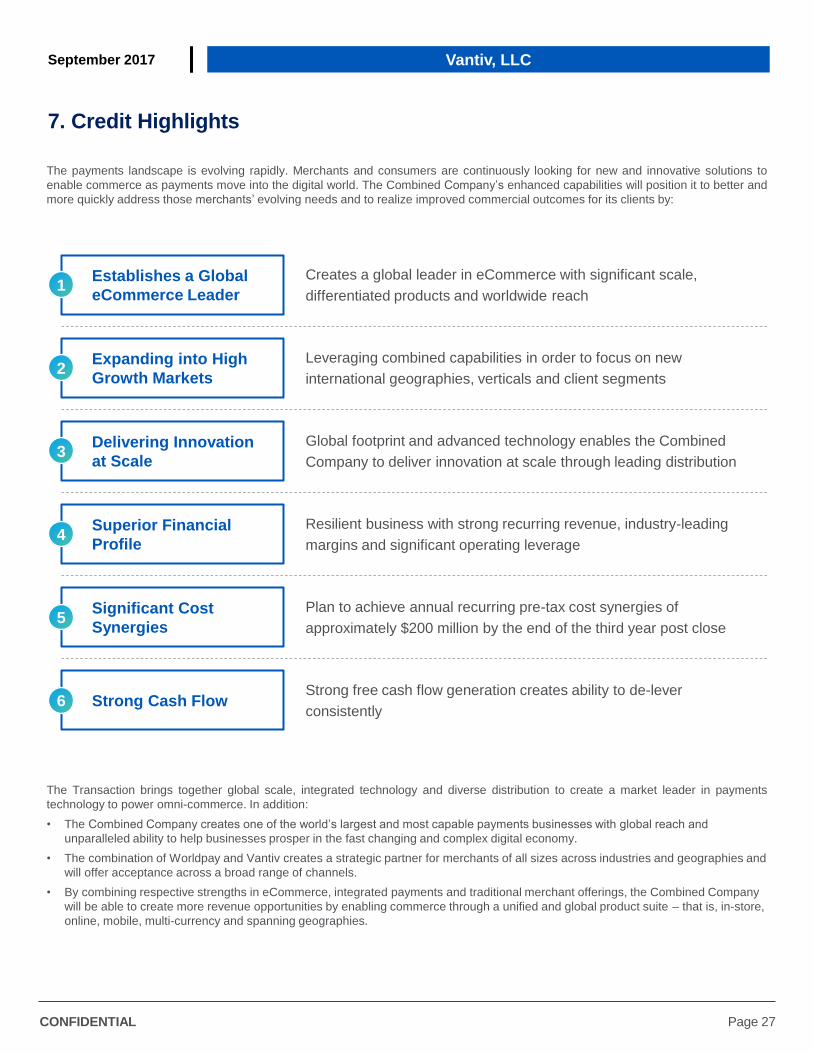

The payments landscape is evolving rapidly. Merchants and consumers are continuously looking for new and innovative solutions to

enable commerce as payments move into the digital world. The Combined Company’s enhanced capabilities will position it to better and

more quickly address those merchants’ evolving needs and to realize improved commercial outcomes for its clients by:

The Transaction brings together global scale, integrated technology and diverse distribution to create a market leader in payments

technology to power omni-commerce. In addition:

• The Combined Company creates one of the world’s largest and most capable payments businesses with global reach and

unparalleled ability to help businesses prosper in the fast changing and complex digital economy.

• The combination of Worldpay and Vantiv creates a strategic partner for merchants of all sizes across industries and geographies and

will offer acceptance across a broad range of channels.

• By combining respective strengths in eCommerce, integrated payments and traditional merchant offerings, the Combined Company

will be able to create more revenue opportunities by enabling commerce through a unified and global product suite – that is, in-store,

online, mobile, multi-currency and spanning geographies.

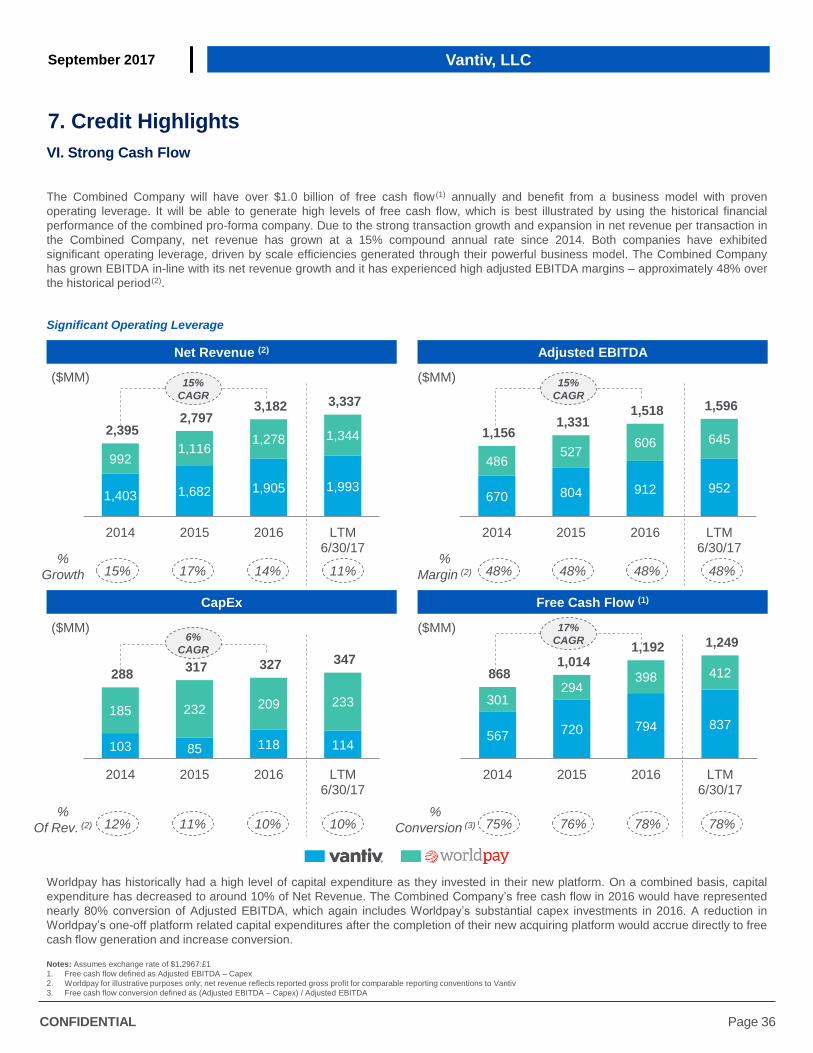

7. Credit Highlights

Establishes a Global

eCommerce Leader

Creates a global leader in eCommerce with significant scale,

differentiated products and worldwide reach 1

Expanding into High

Growth Markets

Leveraging combined capabilities in order to focus on new

international geographies, verticals and client segments 2

Delivering Innovation

at Scale

Global footprint and advanced technology enables the Combined

Company to deliver innovation at scale through leading distribution 3

Strong Cash Flow Strong free cash flow generation creates ability to de-lever

consistently 6

Significant Cost

Synergies

Plan to achieve annual recurring pre-tax cost synergies of

approximately $200 million by the end of the third year post close 5

Superior Financial

Profile

Resilient business with strong recurring revenue, industry-leading

margins and significant operating leverage 4

27

Page 28 CONFIDENTIAL

September 2017 Vantiv, LLC

I. Creates a Global Leader in eCommerce

The ubiquity of the internet has increasingly driven commerce to be conducted online, with the decreasing costs of technology creating

the opportunity for merchants to deploy eCommerce and mobile commerce solutions. In addition, commerce is continuing to evolve into

a global activity as merchants utilize these online methods to connect with consumers in geographic markets outside their own.

Technology and the internet continue to transform global commerce:

• The rapid growth of eCommerce and its progressively international nature is increasing complexity for merchants everywhere. From

complying with local and international regulations, to minimizing costs inherent in cross-border trade, to integrating businesses that

operate both offline in brick-and-mortar and online in eCommerce, merchants require solutions that help them manage complexity.

• The constant evolution of technology via new form factors and device types, coupled with increasing interconnectedness and

continuous new threats to security, requires that merchants adopt nimble, secure and future-proof payment solutions.

Digital Revolution Creates Opportunity

These rapidly changing consumer expectations and technology developments are difficult for merchants to address with existing

payment solutions and are difficult for traditional payment processors to support.

7. Credit Highlights

Helping clients navigate increasing complexity

and drive commerce through payments…

…as technology drives global

eCommerce growth

Seamless

Real-time

Scalable

Secure

Insights

Alternative

Payments

Developer-

Friendly

APIs

Business

Optimization

Integrated

Multi-Currency

0101 1010

Automated

+

Global eCommerce Market ($Tn) (1)

2.0

4.0 – 4.5

2015 2020F

~16%

CAGR 2x+

Note:

1. Based on McKinsey & Company research

28

Page 29 CONFIDENTIAL

September 2017 Vantiv, LLC

I. Creates a Global Leader in eCommerce (cont’d)

Vantiv’s robust U.S. eCommerce and omni-channel offering provides leading capabilities to domestic merchants. Worldpay’s

international online and multi-currency payment offering serves some of the world’s largest eCommerce merchants outside of the U.S.

Worldpay is one of the few global players to have the full eCommerce product set, across payment gateway services, fraud prevention

services, global and local card acquiring, local and alternative payment products, treasury management services, and analytics

services.

The combination creates a leading global eCommerce provider by adding Worldpay’s leading global eCommerce capabilities to Vantiv’s

existing U.S. eCommerce capabilities. A global eCommerce offering will create value for its clients by providing insights into the markets

they operate in and their consumers’ payment behavior. Offering the full range of products will also create profitable cross-sell and up-

sell opportunities for the combination’s existing clients.

The combination will be able to provide an end-to-end set of products and services across geographies which act as a key differentiator

to similar payment processors in driving simplicity and profitability in its payment solutions for merchants. The Combined Company will

have an unrivaled client value proposition with the potential to serve as a one-stop shop for global merchants’ omni-commerce needs,

cutting through complexity and enabling them to enter new markets easily and seamlessly.

eCommerce Leader Spanning U.S. + U.K. and Rest of World

7. Credit Highlights

One-stop shop for all

omni-commerce needs

Unified view of data

globally across all channels

Enable clients to

access new geographies

and markets

Empower merchants

to cut through complexity

Global network and reach

supporting 300+ payment

types across 146 countries

and 126 currencies

Consumer insights through

data & analytics and value

added services

Proven ability to partner with

merchants to drive revenue

growth

Differentiated and

advanced technology

Combination extends

ability to support

eCommerce clients

worldwide

29

Page 30 CONFIDENTIAL

September 2017 Vantiv, LLC

II. Expanding into Strategic and High-Growth Markets

Completion of the combination will bring together two complementary partners to create a market leader in payment technology

positioned to capitalize on strategic and high-growth verticals in the most attractive global markets. The Combined Company will be able

to:

• Export Vantiv’s integrated payments technological know-how and capabilities to Worldpay’s global merchant base. This will allow the

Combined Company to penetrate Worldpay’s deep SMB client base in the U.K. and expand further internationally.

• In addition, the Combined Company will continue to leverage Vantiv’s existing integrated payments capability in the U.S. and

increase its SMB client base in the U.S.

Expanding Integrated Payments

The combination will create a leading global integrated payment technology provider and will enable the Combined Company to take

advantage of strategic and innovative opportunities to provide differentiated and diversified solutions to address clients’ needs:

• This will allow the Combined Company to deliver local expertise on a global basis by transferring solutions across geographies to

better serve clients in similar vertical markets. Critically, the Combined Company will be a scale player with a leading position in both

the U.S. and outside of the U.S., which will enable it to holistically serve the complex needs of businesses globally. The Combined

Company will also be able to bring economies of scale to benefit clients with shared geographies, end-markets or technology needs.

7. Credit Highlights

VANTIV INTEGRATED

PAYMENTS ECOSYSTEM

Products &

Technology

Developers

Dealers

Accelerating adoption of integrated

payments continues to drive strong

growth in the U.S.

Pioneer in integrated payments with leading capabilities

Continue to grow business with SMBs in the U.S.

Follow Vantiv’s U.S. clients and partners as they

expand overseas

Penetrate Worldpay’s deep SMB client base in the

U.K.

Springboard to expand presence across Europe

30

Page 31 CONFIDENTIAL

September 2017 Vantiv, LLC

II. Expanding into Strategic and High-Growth Markets (cont’d)

• Enhances the ability of the Combined Company to strengthen and extend its capabilities into attractive and high growth vertical

markets such as B2B, digital and healthcare payments, taking advantage of the secular growth driven by increasing card adoption.

For example, the Combined Company will be able to faster deploy Vantiv’s B2B enterprise payment capabilities into their large ly

untapped and combined client base.

Enhancing Deep Vertical Expertise

• The combination also provides the ability for the Combined Company to extend its capabilities into new and high-growth emerging

markets, including Latin America and Asia/Pacific, which offer significant growth potential. Worldpay is already active in these

markets, offering e-commerce solutions to global merchants. The Combined Company plans to build on its presence in these

markets over time and transact locally in many of these markets, further expanding its global revenue base. Emerging markets are

expected to drive 75% of all global card volume growth over the next 10 years and the Combined Company would be better

positioned as a leader in the deepest and most attractive global markets as a platform to capture this growth.

A Leader in the Deepest and Most Attractive Markets

7. Credit Highlights

Increasing card adoption driving secular growth with anticipated

outsized benefits in high growth verticals

Leading capabilities with deep expertise

across a broad range of key verticals

Aggressively expanding into high growth verticals (e.g., B2B, Digital, Health) B2B

DIGITAL

HEALTH

RETAIL

AIRLINES

RESTAURANT

GROCERY DRUG

Focus on expansion

in high growth

verticals

Emerging markets will drive 75% of global card volume growth over the next 10 years

U.S. &

Canada Europe Asia

Pacific

+

Middle East / Africa Latin

America

$5.2Tn

~7% CAGR

‘15 PURCHASE VOLUME

’15-’25 CAGR %

$0.6TN

~8% CAGR

$0.3TN

~14% CAGR

$11.4TN

~12% CAGR

$3.0TN

~9% CAGR

Source: The Nilson Report (January 2017, issue 1102), McKinsey & Company

31

Page 32 CONFIDENTIAL

September 2017 Vantiv, LLC

III. Delivering Innovation at Scale

The Combined Company will offer integrated technology platforms, enabling Vantiv’s agile and scalable U.S. platform and Worldpay’s

flexible, next-generation global platform to serve domestic and global markets with fast-to-market innovations and lowest cost

processing.

The Combined Company will have the ability to:

• Offer comprehensive and differentiated payment solutions with significant strategic and operational benefits. These platforms are

configurable for almost any geography, currency, region or combination and are built to seamlessly accommodate alternative

payments and support a fully omni-commerce transaction environment.

• Leverage existing deep knowledge in technology and commerce to offer solutions that reduce complexity for both high growth

segment merchants and traditional merchants, regardless of size or channel.

• Enhance the ability of the Combined Company to innovate with fast-to-market developments and proven record of M&A integration

to develop industry-leading solutions to meet emerging new client needs as the payment landscape continues to evolve.

• Access the widest set of distribution channels, ranging from large merchants and financial institutions to small and medium business

and eCommerce merchants of all sizes. This will solidify the Combined Company’s presence in high-growth channels (including

integrated payments, eCommerce and merchant bank), with 37 percent of the Combined Company focused on these fast growing

and highly profitable market segments. This will enable it to reach clients with highly complementary strategies in a manner that is

cost-effective and efficient regardless of size, type or industry vertical.

• Benefit from a reduction in capital expenditure by harmonizing Vantiv’s and Worldpay’s U.S. technology platforms.

The U.S. and global technology platforms will be developed, secured and optimized by one of the industry’s largest pools of engineering

and technology talent. Whether a local, small merchant requires an integrated payment solution to help manage their business, or a

multi-national enterprise would like to connect and transact with consumers online or cross-border, the Combined Company’s

comprehensive suite of solutions will enable them to do so seamlessly. The graphic below illustrates the platform and technology

attributes:

7. Credit Highlights

G L O B A L P A R T N E R O F C H O I C E

SEAMLESS INTEGRATED TECHNOLOGY

COMPREHENSIVE DIFFERENTIATED SOLUTION SET

#1 Global acquirer (1) | ~$1.5Tn in payments volume | Leading cost eff iciency

Next-Gen Flexible Integrated Scalable Secure

Agile

Best-in-class Security

Customer Insights through

Data Analytics

0101

1010

Omni- Channel

Online Connectivity

Alternative Payments

Multi- Currency

Revenue Opportunities

Back-office Automation

UNMATCHED SCALE

Note: