Embed Size (px)

Citation preview

An IMAPHIGH TECHNOLOGYReport

Computing & Internet Software Global Report — 2010

We’ve got connectionsall around the world.You are all about connecting the world, and so are we. For more than 35 years, IMAP has been helping to bring computer technology companies together via strategic cross-border mergers and acquisitions. Our vast experience in your industry has taught us that building a stable platform is fundamental to completing a successful M&A transaction, as well as to establishing a successful computing network. When you need to expand, invest, divest or restructure, you need an advisory that both knows your business and

has the global connections to ensure every opportunity is within your

reach. As these recent closings demonstrate, IMAP is that

advisory.

IMAP consists of independent advisory operations working together to execute cross-border M&A projects. Each IMAP office is independently owned and operated.

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 3

C O M P U T I N G A N D I N T E R N E T S O F T W A R E G L O B A L R E P O R T — 2 0 1 0

Contents2009 M&A activity in computing and Internet software ............................. 4Computing and Internet software sector .......................................................... 4

Shifting from capex to opex ........................................................................................................... 5

Alternative delivery model — SaaS ........................................................................................... 5

Industry-specific capabilities ........................................................................................................6

Vendor consolidation ..........................................................................................................................7

IT spending by central governments ..........................................................................................7

Trends across industry verticals ...................................................................................................7

Trends: Investment opportunities ..........................................................8Mobile applications and computing ...........................................................................................8

Internet-based models ......................................................................................................................9

Computing and Internet software industry outlook ...................................... 1 1

Statistical Reference (Appendices)Appendix A: Global Overview ......................................................................................................A-i

Appendix B: Summary of M&A Deals .....................................................................................B-i

Appendix C: Growth Drivers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C-i

Appendix D: Niche Focus Areas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . D-i

HOT

An IMAPHIGH TECHNOLOGY

Report

IMAP, Inc. is a Delaware corporation. Its regional firms are independently operating in various jurisdictions under a variety of legal forms of organization. References to IMAP transactions, offices, locations and other similar associations should not imply any form of IMAP ownership or agency over the local firms or cause any liability between the local firms and IMAP whatsoever.

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 4

The software sector, which contributed around 25 percent to IT spending in 2009 and mainly consists of the enterprise application market and application development market, generated revenues of $382 billion USD in 2009. The top few players, such as Microsoft, SAP, Oracle and Nintendo, generated more than 75 percent of total revenues from the software business segment in 2009.

2009 saw a decline in application software spending in all regions except Asia-Pacific. Despite the economy showing signs of a recovery in 2010, all industry verticals are still witnessing lower spending compared to pre-recessionary levels due to flat budget growth in the year. Furthermore, according to Forrester’s Enterprise and SMB

Global enterprise application software market working through bad-economy bugs

Large transactions led the way in sluggish 2009 M&A activityThe economic slowdown had an adverse impact on M&A activity in the software sector. The sector saw 1,131 transactions valued at $27.42 billion USD in twelve months (LTM) ending 1Q 2010, witnessing a year-over-year decline of 25.4 percent in terms of transaction value ($36.75 billion USD during the previous period with 2,417 transactions). Dollar volume in this period included one major deal (Sun Microsystems/Oracle), which represented $8.34 billion USD or nearly 28.1 percent of total dollar volume in the period. Excluding this transaction, the dollar volume would have been down 48 percent. During the previous period, the largest deal was the acquisition of NDS Group by Permira Advisers for $1.7 billion USD.

In terms of business segment, Internet software and services accounted for 30 percent of total transaction value followed by computer hardware and applications, which formed nearly 28 percent of the total.

In terms of country, the US saw the highest transaction value of $12.34 billion USD with a total of 501 transactions in this twelve month period while Japan came in second with a value of $9.12 billion USD through 15 transactions. Among regions, North America was the clear leader at $12.54 billion USD.

M&A Activities at a GlanceLTM ending 1Q 2009 LTM ending 1Q 2010

Transaction value (USD million) 36,752 27,415

Top 5 transactions (%) 20.1% 46.7%

Segment No. of transactions Value (USD mn)

Computer Hardware & Applications 1 8,341

Internet Software & Services 18 7,583

Application Software 838 5,412

IT Consulting and Others 10 4,218

Systems Software 199 1,464

Top 5 regions No. of transactions Value (USD mn)

North America 553 12,538

Asia 128 10,755

Europe 356 3,620

South America 19 194

Middle East 14 169

Top 5 countries No. of transactions Value (USD mn)

US 501 12,342

Japan 15 9,123

UK 78 1,386

China 50 1,374

Germany 47 964

Source: Capital IQ, IMAP

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 5

Software Survey, North America and Europe, Q4 2009, IT budgets are expected to remain unchanged in 2010. Nevertheless, revenues are expected to reach $419 billion USD in 2010, growing 9.7 percent year-over-year. This increase would reverse a 7.4 percent decline in 2009.

With just a moderate increase in IT spending overall, the enterprise application software market still remains vulnerable and enterprises are uncertain about near-term business prospects. However, the bright spot in the recovering economy is small- and medium-sized business (SMBs). As the economy emerges from the recession, SMBs will look for small-business software to automate their operations and scale up growth. In addition, large software vendors such as SAP and Oracle will continue to focus on the SMB market to reinvigorate their revenue growth in software license sales. The SMB enterprise application market is expected to reach $80.31 billion USD by 2012, representing a 10.6 percent CAGR for the period 2008-12.

Enterprises shifting from capex to opex

CIOs and COOs are expected to experience continued pressure to prove that the amount of investment in ERP systems is justified and generates a solid return on investment. As a result, the market will have more deliberate spending, more phased rollouts, buying of licenses only when needed, and hesitancy to invest in more expensive advanced enterprise software modules.

Accordingly, companies are directing much of their software investments to areas where they will definitely be implemented effectively and get more out of their existing enterprise investments. The need to more

1 IDC forecast

effectively manage organizational and business risk will likely result in a continuation of this trend in 2010.

Given the current risk averse environment, companies are less likely to try entirely new products or risky upgrades. As a result, vendors are more likely to invest in incremental product enhancements and tighter integration between modules rather than major changes to their software: operating expenditures versus capital expenditures.

Thus, going forward, vendors are expected to seek smaller deals from existing customers via add-on products and business intelligence tools because most customers are not yet ready to fund major enhancements or expansions.

Emergence of an alternative delivery model — SaaS

As companies are shying away from large capital investments in IT systems, software as a service (SaaS) is receiving a boost. SaaS is also being driven by SMBs that are looking to adopt this model as they typically find it difficult to afford on-premise systems. Moreover, considering that the tight credit markets will take time to thaw entirely, many SMBs are looking at SaaS-based services to help them minimize upfront capital IT costs.

Revenue Growth Comparison in 2009SaaS Vendors Traditional VendorsSuccessFactors (+36.8%) Manhattan Associates (-26.8%)

Salesforce.com (+21.2%) QAD (-18.3%)

Concur (+14.9%) Lawson (-11.1%)

Descartes (+11.7%) SAP AG (-7.8%)

Ariba (+3.3%) Microsoft (Business Division) (-0.2%)

Source: Bloomberg

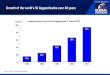

Global IT1 spending, which includes hardware, software and IT services, was estimated at $1.5 trillion USD in 2009, decreasing 8.9 percent compared to 2008. The decline turned out to be less than expected as the US market started recovering in 4Q 2009 while the Asia Pacific market, especially India, China and Australia, reported better performance. In 2010, it is expected to reach $1.6 trillion USD, indicating a year-over-year growth of 8.1 percent .2

1 Consists of spending on computer equipment, communication equipment, software, IT consulting and systems integration services, and IT sourcing

2 Forrester Research - US And Global IT Market Outlook: Q4 2009Source: Forrester Research, IMAP

Computer equipment Communications equipment

Software IT consulting services IT outsourcing

Global IT Spending, 2008-10 in USD Billions

1,750

1,500

1,250

1,000

750

500

250

02008

1,659

2009

1,512

2010

1,624

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 6

Considering these factors, most SaaS vendors reported better performance, with SaaS revenues overall growing 7.98 percent year-over-year in 2009. Deployment of SaaS increased in all areas from customer-relationship management (CRM) to human-capital management (HCM), as well as spend management. In fact, Salesforce.com posted revenues above $1.3 billion USD, which is a new high for the SaaS industry that was estimated to be $7.5 billion USD in 2009.

The increasing popularity of SaaS as a delivery model has not only led to increased revenues for SaaS vendors but also eaten into the revenue of traditional, on-premise vendors. However, the latter are still managing to maintain their operating margins as they rely on maintenance and support revenues, which are naturally recurring. For example, the ratio of maintenance revenue to new licenses of vendors such as CDC, Epicor, Exact, Lawson, Manhattan, Oracle, QAD and SAP increased as customers chose not to upgrade and purchase new licenses.

Industry-specific capabilities are crucial to remain competitive

In addition to preferring low-cost models such as SaaS, customers are expecting deeper industry expertise from their software providers to gain a more integrated application environment and end-to-end process automation. Hence, many companies have combined custom-built applications and customized industry packages to supplement their core software. This environment leads to a complex setup and ongoing integration challenges.

Large enterprise software vendors have added vertical depth and breadth. Both SAP and Oracle have invested heavily in industry solutions, each reportedly having capabilities in more than 20 verticals. This strategy to increase industry depth has driven many acquisitions, particularly for Oracle. SAP, on the other hand, is building industry functionality in-house but it has made several vertical acquisitions to accelerate time-to-market.

Second-tier software providers have found more success in offering deeper industry-specific functionalities compared with mega-vendors. Lawson, for example, has successfully targeted industries such as healthcare, food and fashion. Other vendors (e.g., Microsoft, Epicor and Sage) may choose to go down to sub-industry levels, often relying on partners to add the last mile of specialization.

Specialists focus on fewer or even single verticals. Some do not even provide the core accounting functionality, which is crucial to any ERP system. Nevertheless, these specialized plays are often compelling to customers and may also attract the attention of ERP vendors looking to partner or acquire. Specialist vendors offering comprehensive suites to particular verticals include Deltek (project-based businesses), Blackbaud (not-for-profit), Mincom (mining and asset-intensive businesses), QAD (manufacturing) and IBS (distribution). CGI Group gives ERP vendors stiff competition in the government sector, including US federal as well as state and local governments. Specialists dominate the lucrative healthcare market, particularly patient systems. Notable players include Cerner, Eclipsys, Epic Systems, McKesson and Siemens.

Source: Gartner Research, IMAP

Enterprise Application Market Spending by Region, 2009

Western Europe 30%

North America 46%

Asia/Pacific 9%

Japan 8%

Latin America 3%Eastern Europe 2%

Middle East & Africa 2%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 7

Functional expansion leading to vendor consolidation

With customers expecting deeper industry expertise from their software providers, many companies are combining custom-built applications and customized industry packages to supplement their core software. This environment leads to a complex setup. To overcome this challenge, vendors are looking to consolidate by becoming a one-stop shop for all functions. This consolidation trend is also fuelled by the rising competition between vendors and lower market valuations of struggling vendors because of the downturn.

Oracle has been a key proponent of vertical acquisitions, and SAP as well, though to a lesser extent. Possible plays for some vendors include acquiring breadth in horizontal areas such as HR. Peer-to-peer acquisitions among ERP vendors appear less likely. Vendors may also acquire adjacent technologies, such as enterprise content management tools.

Public administration represents the largest IT spending by central governments

After the economic crisis, which saw governments announcing massive stimulus packages, tax payers are now demanding funding cuts in the public service arena. There will be increased attention on how money is being spent at all levels of government.

At the same time, telecommunications and the Internet are increasingly recognized as critical to economies and service delivery. Governments are thus expected to make efforts to move the majority of citizen services to an online delivery model to increase transparency

Active Acquirers

ORACLE

INFOR

THE SAGE GROUP

Agresso

Deltek

Lawson Software

Regional Players

IFS

Intacct

Vertical Players

IBS Software

QADEpicor

NetSuiteExact Software

Source: Forrester Research, IMAP

Vendor Consolidation

Potential Acquirers

MICROSOFT

SAP

IBM

PRIVATE EQUITY

and create value for their constituents. To this end, investment across a wide variety of departments, functions and systems will be made. This will sustain investment in IT by governments in 2010, when the focus will be on rightsizing, underscored by government transformation or modernization.

Furthermore, by 2012, up to one in five government processes is expected to rely on crowd-sourced data due to the increasing influence of communities, individuals and groups in shaping the direction of businesses and markets. Thus, social media are becoming increasingly important as sources of public information, making them mission-critical for governments.

Trends across industry verticals

Most industries witnessed significant declines in IT spending in 2009. A majority of these cutbacks in tech purchases were driven by the fear of recession. These fears were more intense in some industries, such as retail, wholesale, transportation and logistics, and financial services, leading to a sharp cutback in IT spending. Since the situation is now easing and prices are rebounding, the pent-up demand in these industries for IT goods and services should bounce back in 2010.

Retail: Gartner expects to see many Tier 1 retailers pursue an m-commerce strategy mainly to avoid lagging on this front. They expect, however, to see only 20 percent of retailers succeeding in their m-commerce initiative. As many retailers have discovered with the Web, cross-channel shopping requires more than just launching an m-commerce presence to enable direct selling.

Manufacturing: By the end of 2011, manufacturers that prioritize future software investments in operational technologies such as product life-cycle management (PLM), manufacturing process management (MPM), manufacturing operations management (MOM) and quality management software (QMS), instead of traditional IT and ERP, could achieve a tenfold return on their investment .1

Education: By 2015, most local education agencies are expected to cut school construction by 50 percent by using virtual learning environments to better utilize existing facilities.

1 Gartner Research

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 8

Investment opportunities in mobile apps and Internet-based models

TrendsHOT

1: Mobile applications and computing

Despite the recession, the mobile application1 landscape performed well in 2009. There was continuous consumer demand for Apple’s proprietary ecosystem; Google acquired the mobile ad network AdMob for $750 million USD; and Internet service providers (ISPs) entered the mobile market (Iliad’s acquisition of France’s fourth 3G license, as an example).

The mobile application market was estimated to be $4.2 billion USD in 2009.2 The number of mobile application downloads was just over 7 billion in the same year. Going forward, the mobile application market is expected to reach $17.5 billion USD by 2012, representing an impressive three-year CAGR of 60.9 percent. The number of mobile application downloads is also estimated to grow to nearly 50 billion in 2012. This growth should be 1 A mobile application is a software application that runs in a handheld device such

as a smartphone. These applications are either pre-installed on phones during manufacture or downloaded by customers from app stores and other mobile software distribution platforms.

2 The GetJar study run by an independent consulting firm, Chetan Sharma Consulting

driven by increasing penetration of mobile Internet, more functionalities, rising adoption of smartphones, and increased and better integration of mobile hardware and software.

Within the mobile application segment, mobile enterprise application market is expected to be the next growth driver. Mobile enterprise applications are expected to see massive adoption in 2010 due to increased mobility of employees and demand for devices capable of these functionalities. Carriers and vendors are recognizing the enterprise as a high-value customer and actively working towards developing and promoting attractive mobile data solutions for enterprises.

The mobile enterprise application market was estimated to be $2.3 billion USD in North America in 2008.3 This market is made up of three types of vendors:

· Vendors focused on mobile operating systems that have developed broad mobile application development toolkits focused on a single platform (e.g. Microsoft, Apple and RIM)

3 http://www.cellular-news.com/story/38739.php

The economic slump had an adverse impact on most industries, including the software sector. Organizations shifted their IT spending from capital expenditure to operating expenditure to optimize costs. Various application markets such as enterprise resource planning (ERP), supply chain management (SCM) and customer relationship management (CRM) were badly hit in 2009. This gave an impetus to various Internet-based models such as Software-as-a-Service (SaaS), IT management, virtualization capabilities and open source software. Internet-based computing models in the enterprise software market requiring little or no implementation work on the customer side, are generally independent of operating systems and are offered on a subscription or pay-as-you-go basis. This translates into lower adoption barriers for new customers.

Mobile Application Market CAGR 60.9%

Source: GetJar Study, IMAP

Mobile Application Market in million USD

Europe North America South America Asia Middle East &South Africa

$10,000

$8,000

$6,000

$4,000

$2,000

$02009 2010 2011 2012

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 9

The worldwide market for IT services related to cloud computing and cloud services was worth almost $2.4 billion USD in 2009. By 2013, the market is expected to be worth almost $8.1 billion USD. By far, the largest component of the overall cloud service market is implementation, which represents 65 percent of the 2009 IT services market and is estimated to represent 64 percent by the end of 2013.

Smart computing — collaboration, unified communications and voice over IP:Smart computing is based on technologies such as service-oriented architecture, server and storage virtualization, cloud computing, and unified communications. It adds to existing technologies new capabilities of real-time situational awareness and automated analysis.

Smart computing will help companies optimize process results and returns from their balance sheets. Unlike the horizontal technologies of personal computing and network computing, smart computing will have a highly vertical industry focus.

Tech vendors have great growth opportunities in this new cycle but also big challenges in navigating the shift to smart computing. Accordingly, in the US alone, the share of the smart computing industry’s vertical solutions in the IT market will increase from 6 percent in 2008 to 23 percent in 2016.2 The market is expected to increase from $27 billion USD in 2009 to $213 billion USD in 2017 in the US.

Linux and open-source software (OSS):The phenomenon of OSS, which started 20 years back, has suddenly gained momentum as a possible alternative to expensive proprietary software. As the open source movement expands up the software stack, nearly all software markets are now being impacted in some way.

The OSS segment is experiencing slow but steady growth. The release of the open source Internet browser Firefox 3.0 by Mozilla in June 2008 was a major event for open source applications, with more than 8 million people downloading the new version of the software within the first 24 hours after its release. The Firefox browser has steadily been gaining market share, which had 24.2 percent of the overall browser market in February 2010 from 21.8 percent in February 2009.

2 Forrester Research: Smart Computing Drives The New Era Of IT Growth

· Mobile specialists with multichannel capability such as Sybase, IBM, Pyxis Mobile, Spring Wireless and Syclo

· Application suite vendors that have their own application suites, such as SAP and Oracle

Along with mobile ERP, enterprise mobile cloud applications (including thin clients and browser-based applications), SaaS, platform as a service (PaaS), and infrastructure as a service (IaaS) can fuel growth in this market. Going forward, the mobile enterprise application market in North America is estimated to reach $10.3 billion USD in 2013, a CAGR of 35 percent from 2008 to 2013.1

However, it should be noted that proving return on investment (ROI) is still a concern for vendors and service providers of mobile enterprise applications, because the market is in its nascent stages and customers are uncertain on whether they will fully obtain the potential benefits promised by these applications.

2) Internet-based models

Cloud-based application and infrastructure services:Cloud computing is currently emerging as a service offering that leverages Internet hosting capabilities and can be viewed as an evolution of SaaS. Cloud computing is generally regarded as IT infrastructure available on demand and it offers start-ups and SMBs flexible access to computing capabilities with minimum capital expenditure. Nevertheless, with Amazon.com’s spin-off Amazon Web Services (AWS) emerging as a leading provider of cloud computing services, cloud computing is expected to become more influential.

1 http://www.cellular-news.com/story/38739.php

Cloud Computing Spending CAGR 35.8%

Source: Gartner Research, IMAP

IT Spending in Cloud Computing in USD millions

Consulting Implementation Management

2009 2010 2011 2012

5,000

4,000

3,000

2,000

1,000

0

6,000

2013

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 10

In a Forrester Research report on enterprise interest for OSS, two-thirds of the 1,017 respondents at North American and European enterprises expressed some interest in open source deployment.

Virtualization: PC, server, and storage virtualization is growing and is being supported by the relatively tough economic conditions worldwide. Virtualization is introducing new ways of packaging client computing applications and capabilities. As a result, the choice of a particular PC hardware platform, and eventually the OS platform, becomes less critical. Thus, enterprises are proactively building a five- to eight-year strategic client computing roadmap outlining an approach to ownership and support, operating system and application selection, deployment and update, and management and security plans to manage diversity in the virtualization arena.

Spending on virtualization software technologies is forecast to grow at a 33.6 percent CAGR from 2009 to 2013. Growth would be driven by organizations looking to lower the total cost of ownership and to increase overall IT effectiveness.1

Business intelligence (BI) and analytical software: BI and specialized analytical software such as data mining and predictive analytics, video image analysis, pattern recognition, and artificial intelligence algorithms help businesses or governments analyze patterns or anomalies on a real-time basis. These functions make BI important in economically challenging times. As a result,

1 Gartner Research

the BI market was much less affected by the economic crisis than most other software markets.

All the big sellers of BI software are either parts of larger software vendor or private companies with the exception of pure-play BI public companies such as MicroStrategy and Actuate.

New categories of advanced analytics, including business performance solutions, text analytics, predictive analytics, and complex event processing, are expected to merge into the core BI market, thereby further fueling growth. The BI market is expected to reach $14 billion USD by 2014.2

Social CRM: Social CRM (also known as CRM 2.0) is a business strategy supported by a system and designed to engage the customer in a collaborative interaction that provides mutually beneficial value in a trusted and transparent business environment.

The industry has many participants and includes different types of players such as traditional CRM vendors, community platform and social media players, as well as brand monitoring players. Most of the players provide on-demand subscription-based offerings in social CRM.

Social CRM is most likely to be the next big trend in the entire CRM industry. According to one Gartner report, social CRM is expected to see significant growth, as more than 80 percent of the enterprise use of social networking tools in 2010 will be driven by customer engagement projects. In addition, Forrester mentions that by 2013, businesses will be spending almost $4.6 billion USD on Web 2.0 tools, which include advanced Internet technology and applications such as blogs, wikis,

really simple syndication (RSS), and social bookmarking. In an April 2008 report, the research group forecast

43 percent annual growth in the social media market for the so-called Enterprise 2.0 as

organizations are investing heavily in social networks.

2 Forrester Research: Market Overview: The Business Intel-ligence Software Market

IMAP’s Computing & Internet Software Industry Global Report — 2010: Page 11

Software Market Outlook, Quarterly, 2008-2010Global software vendors’ revenues by category of software (percentage change from prior year)

2008 2009 20101Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q* 1Q* 2Q* 3Q* 4Q*

Operating systems 3% 9% 6% -7% -15% -21% -20% 11% 17% 23% 22% 16%

Middleware 14% 19% 12% 3% 4% -4% -2% 3% 5% 5% 7% 6%

Applications 14% 17% 12% -3% -12% -16% -13% 2% 10% 12% 12% 12%

TOTAL 11% 16% 11% -1% -5% -12% -9% 4% 9% 10% 11% 10%

US software vendors’ revenues by category of software (percentage change from prior year)2008 2009 2010

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q* 1Q* 2Q* 3Q* 4Q*

Operating systems -3% 3% 1% -7% -14% -23% -20% 8% 10% 16% 16% 14%

Middleware 8% 13% 9% 7% 10% -1% 1% 3% 4% 6% 6% 5%

Applications 5% 7% 4% -4% -11% -15% -13% 0% 6% 9% 9% 9%

TOTAL 6% 9% 7% 1% -1% -9% -8% 3% 6% 8% 8% 8%

Source: 2008 and Q1, Q2, and Q3 2009 quarterly financial reports of 18 large, global software vendors1

1 BEA Systems (prior to acquisition by Oracle), BMC, Business Objects (prior to acquisition by SAP), CA, Cognos (prior to acquisition by IBM), Fujitsu, Hyperion (prior to acquisition by Oracle), EMC, Hewlett-Packard, Hitachi, IBM, Mercury Interactive (prior to acquisition by Hewlett-Packard), Microsoft, NEC, Oracle, SAP, Sun (prior to acquisition by Oracle), and Symantec.

The enterprise software market underwent a tumultuous phase during the economic slowdown of 2008-2009 and the recession that ensued. The sector overall faced pressure in terms of prices which in turn hampered margins. This led to vendors making structural changes in their technology and business model to adapt to the changing software demand space.

Most companies locked in their IT budgets for 2010 with a marginal increase in overall IT spending expected for the year. While spending is nowhere close to the depressed levels during the recession, it will be some time before spending reaches pre-recessionary levels. A meaningful recovery in spending is expected only in the second half of 2010. With the recession still fresh, companies are looking to convert their enterprise software needs from capex to opex. This means vendors with SaaS, virtualization capabilities and open-source strategy are poised to benefit in the near future.

This is not to say large vendors with non-SaaS capabilities will be left behind. Due to their sheer size and geographic diversification, they can price their products aggressively and also bundle offerings to make packages more attractive. Moreover, as legacy operators, most of their contracts are maintenance based, making revenues recurring in nature. This is

Computing and Internet software industry outlookunlike vendors in only one market or those without a wide geographical presence, whose revenues are highly dependent on new contract wins.

Geographical presence, in particular, cannot be under-estimated because North America still accounts for 45 percent of all software revenue, which by any standard is a large chunk. While the share of emerging markets is expected to increase to 20% by 2013, it is still a small share compared with North America. Hence, any future weakness in the US markets could have a material im-pact on revenue. Nevertheless, emerging markets will play a huge role in balancing revenues in the years to come because of their growing demand potential and underpenetrated nature.

The software sector has always accounted for the largest number of all technology related M&A transactions, over 40%. And, the value received is very much a function of finding the buyer that can best exploit the acquired technology. This requires advisors to conduct a global search effort, even for sellers with modest revenues.Ron Klammer, IMAP technology advisor, Southport, Connecticut

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-i

Appendix A: Global Overview of Computing & Internet Software (Enterprise Software Industry)

Value chain of the software marketAccording to IDC, the worldwide software market is composed of three primary software submarkets:

Software sector overview and trends

• System Infrastructure Software: System infrastructure software integrates a computer’s various capabilities but typically does not directly affect the performance of tasks that benefit end users. This market comes first in the value chain and operates as a foundation for the creation of various applications.

• Application Development and Deployment: AD&D is a process that includes the development of a software product, known as software life cycle. The AD&D market is second in the value chain; software development and deployment activity begins with system infrastructure as the base.

• Applications (Consumer and Enterprise): Application software, also known as software applications, is computer software designed to help the user perform a single or multiple tasks. This is one of the

biggest submarkets in the software industry; the applications market contributes roughly 60% to total software revenues. The applications market can be further classified as follows:

· enterprise application software, which includes content, communications and collaboration (CCC), customer relationship management (CRM), enterprise resource planning and supply chain management (ERP & SCM), office suites and digital content creation (DCC)

· enterprise infrastructure software such as middleware and databases

· information worker software · content access software · educational software · simulation software · media development software

Value chain of the enterprise application marketThe enterprise application market includes various secondary markets.

Sub-Applications Description

ERP

ERP integrates the data and processes of an organization on a cross-functional and enterprise-wide level into one single system. Usually ERP systems have many components including hardware and software to achieve integration. The two key components of an ERP system are a common database and a modular software design. Large ERP vendors include Oracle and SAP and middle-tier ERP vendors include Agresso, Epicor Software and Lawson Software.

SCM

SCM encompasses the planning and management of all activities involved in sourcing, procurement, conversion, and logistics management. It also includes the crucial components of coordination and collaboration with channel partners, which can be suppliers, intermediaries, third-party service providers, and customers.2 SCM also addresses issues related to distribution channels and inventory management. SAP, Oracle, Infor and Inspur are some of the large SCM vendors, while middle-tier vendors include 7Hills, Accellos, AdvanceWare Technologies, Fascor and Manhattan Associates.

CRM

CRM involves the use of technology to organize, automate and synchronize business processes—principally sales activities, but also those for marketing, customer service and technical support. CRM also helps in reducing the time required for sales cycles while hanging onto potential sales leads. Major CRM vendors include SAP and Oracle and midmarket-centric vendors include FrontRange Solutions, Maximizer Software and Sage Software. Salesforce.com and Netsuite are some software-as-a-service (SaaS)-based CRM application providers.

2 Definition by Council of Supply Chain Management Professionals (CSCMP)

1 IDC’s Software Taxonomy, 2010

• Global IT1 spending was estimated at $1.5 trillion USD in 2009, decreasing 8.9 percent compared to 2008. The decline, however, turned out to be less than expected as the US market started recovering in 4Q 2009 while the Asia-Pacific market, especially India, China and Australia, reported better performance in 2009. Global IT spending in 2010 is expected to reach $1.6 trillion USD, indicating a year-over-year growth of 8.1 percent.2

• Compared to pre-recessionary levels, all verticals have suffered from lower IT spending, which varies widely by region. The vast majority of enterprises are expected to continue experiencing almost flat budget growth in 2010. According to Forrester’s Enterprise and SMB Software

1 Consists of spending on computer equipment, communication equipment, software, IT consulting and systems integration services, and IT sourcing

2 Forrester Research - US And Global IT Market Outlook: 4Q 2009

Survey, North America and Europe, 4Q 2009, a high percentage of respondents expected to leave their IT budgets unchanged in 2010 and many enterprises remain vulnerable and are uncertain about near-term business prospects.3

• In terms of region, the strongest growth in 2010 should be in Western and Central Europe, where tech purchases are expected to rise 11.2 percent, boosted by the dollar’s decline against the euro. This would be followed by Canada at 9.9 percent, Asia-Pacific at 7.8 percent, and Latin America at 7.7 percent. Eastern Europe, the Middle East and Africa are expected to be the weakest market, rising by just 2.4 percent. With oil prices recovering from bottom levels but still below 2008 peak prices, oil-producing economies in the Middle East should perform slightly better, leading to a recovery in tech purchases in

3 Ovum Research

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-ii

their local currencies. However, their currencies in several cases have actually weakened against the dollar, bringing down dollar-denominated growth.1

• Shifting from regions to countries, the US remains, by a wide margin, the largest of the top 15 markets for IT goods and services. Purchases of IT goods and services in 2010 are expected to reach $568 billion USD—almost four times more than second place Japan (at $142 billion). China follows as third at $120 billion USD.

• The global software industry, which mainly consists of the AD&D market, is a major contributor to the overall IT industry. From 24 percent in 2004 to 25 percent in 2008, the contribution is expected to reach 25.7 percent in 2010. The software market generated revenues of $382 billion USD in 2009 and is expected to reach $419 billion USD in 2010, growing 9.7 percent year-over-year. This increase would reverse the 7.4 percent decline in 2009 and bring back software purchases above 2008 levels.

• The top few players, such as Microsoft, SAP, Oracle, and Nintendo, generated more than 75 percent of total revenues from the software business segment in 2009.

• As per an enterprise and small and medium size business (SMB) software survey by Forrester, firms in North America and Europe, despite the hype surrounding new technologies that were introduced in the market, are still devoting most of their spending on already installed technologies.

• According to Gartner, the enterprise application market weathered the economic crisis much better in 2009 than in 2001-02. This is because the market has evolved to become a matured market with more penetration, confidence of consumers in IT applications, and a well-balanced geographical and vertical mix.2

• The ERP market, however, was badly hit in 2009, with vendors see-ing dramatic drop-offs in license revenues and professional services. Recent Forrester survey data shows that the majority (67 percent) of ERP customers have put their ERP spending plans on hold for 2010 as well. Nevertheless, 29 percent of customers are planning to upgrade or expand existing ERP implementations (22 percent) or undertake new implementations (7 percent) in 2010.

• The SCM application market remained diverse in 2009, ranging from large-scale suite providers to innovative companies with value-adding capabilities. Although growth slowed down in 2009 and is expected to remain moderate during 2010, the market is estimated to post a CAGR of 10.6 percent until 2012. Growth would be fueled by supply chain organizations focusing on investments in areas of high business value, notably applications that help reduce costs, drive business growth, improve customer service and increase efficiency.

• While many CRM technology projects were deferred/cancelled in 2009, this is expected to reverse in 2010. Major trends to watch for in 2010 include the evolution of extended CRM application ecosystems, SaaS as the default choice for CRM, and mobile CRM becoming a must-have capability. In social media monitoring, an emerging trend in the CRM space, companies are expected to spend around $4.6 billion USD by 2013.

• Regarding strategy, organizations are likely to shift their IT spending from capital expenditure to operating expenditure to optimize costs. This is giving an impetus to SaaS, IT management, virtualization capabilities and open source software. Internet-based computing models in the enterprise software market require little or no implementation work on the customer side, are generally independent of operating systems, and are offered on a subscription or pay-as-you-go basis. This translates into lower adoption barriers for new customers.

Trends across function and tier• Functional expansion: Software vendors are continuing to add new

functionality to their software and are working to become a one-stop shop for all functions. This change is being facilitated by product development as well as acquisitions. This has led to several new

1 Forrester Research

2 www.zdnetasia.com/gartner-enterprise-software-sales-to-drop-in-europe-62052707.html

developments and inclusion of functionalities such as CRM, HR/payroll, and e-commerce.

• Tier 1 Vendors Moving to the Mid-Market: Because the number of Fortune 500 companies is limited, and most of them already have an ERP system, Tier 1 vendors such as Oracle and SAP have been expanding their marketing efforts downward to penetrate the middle market. In doing so, they have modified their strategies by offering scaled down, pre-configured versions of their applications, trying new methods of implementation, pursuing new distribution channels to sell and implement their software, and acquiring mid-market software. Some examples are the acquisition of Dynamics and Navision by Microsoft, Top Tier by SAP, and Tekton and Emdeon by Sage Software.

• Tier 3 & 4 Vendors Moving Upward: Software vendors that have traditionally focused on smaller organizations are moving their products upward to the tier 1 and 2 enterprise markets. These vendors have significantly improved functionality and scalability, allowing smaller companies to grow without having to change systems.

• ISVs marketing themselves as SaaS vendors: Due to the increased popularity of SaaS, many independent software vendors (ISVs) are trying to reinvent themselves as SaaS companies, using virtualization schemes to simulate multi-tenancy and provide them with a quick time-to-market solution. However, to capture the full benefits of SaaS, ISVs need to modify their business model accordingly in terms of architecture.3

Trends across industry vertical2010 is expected to see changes in the enterprise software market as businesses confront the challenge of cutting costs while dealing with a fundamentally restructured economy. This will require new business models and technologies because companies will need systems specifically designed for competitive advantage in their vertical. Companies are concentrating on turning back to innovation, strategic initiatives and development of new business operations that map to market demands. However, such initiatives will need to be funded from savings elsewhere as only few organizations are expected to increase their IT budgets.4

• Retail: Gartner expects to see many Tier 1 retailers pursue an m-commerce strategy mainly to avoid lagging on this front. This new strategy, however, will see only 20 percent of retailers succeeding in their m-commerce initiative. As many retailers have discovered with the Web, cross-channel shopping requires more than just launching an m-commerce presence to enable direct selling.

• Manufacturing: By the end of 2011, manufacturers that prioritize future software investments in operational technologies such as product life cycle management, manufacturing process management, manufacturing operations management and quality management software, instead of traditional IT and ERP, would achieve a tenfold return on their investment.5

• Government: Currently, most governments worldwide are focusing on providing as much public data as possible online to increase transparency and create value for constituents. The components of society ― which comprise individuals, groups, communities, markets and firms ― play a large role in shaping the direction of society and business. Hence, they will become a key component in how government entities will operate; by 2012, up to one in five government processes will rely on crowd-sourced data.

• Education: By 2015, most local education agencies are expected to cut school construction by 50 percent by using virtual learning environments to better utilize existing facilities.

3 http://www.interwest.com/venture-capital-funding/software-as-a-service-saas.html

4 Gartner Research - Top Industry Predictions 2010: The Recession’s Aftermath Proves Challenging

5 Gartner Research

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-iii

Thumbnail summaries of top 50 computing and internet software companies (enterprise software industry)

1: MICROSOFT CORP (US)

Brief description Developer cum manufacturer that licenses, sells and supports software products. Acquired Opalis Software Inc. in December 2009.

Products soldOperating systems for servers, computers and intelligent devices; server applications for distributed computing environments; information worker productivity applications; business solutions applications; computing applications; software development tools; video games.

Key brandsActive Accessibility, Active Desktop, ActiveMovie, ActiveStore, Azure, InfoPath, Inkseine, InPrivate, IntelliMirror, IntelliMorph, IntelliMouse, Microsoft Game Studios, MSN, Outlook, SQL Server, Visio, Visual Basic, Windows Media, Xbox 360

Markets covered Client, Server and Tools, Online Services Business, Microsoft Business Division, Entertainment and Devices

Geographic coverage (2009) US: 56.6%; Rest of world: 43.4%

Future plans Office 2010 Tech Guarantee program and YAHOO search partnership model to be launched in 2010

Financials (LTM)Revenue: 58.7 billion USD, year-over-year change: 3.3%Operating profit: 21.8 billion USD, year-over-year change: 8.0% Net income: 16.3 billion USD, year-over-year change: 17.6%

2: APPLE INC (US)

Brief description

Designs, manufactures and markets personal computers, mobile communication devices and portable digital music and video players. Also sells a variety of related software, services, peripherals and networking solutions. Sells its products worldwide through its online stores, retail stores, direct sales force and third-party wholesalers, resellers and value-added resellers. Acquired digital music service Lala in December 2009.

Products sold Portables, desktops, music-related products, software and services, iPhone, related products

Key brands AirTunes, Aperture, Apple, AppleCAT, AppleLink, Apple TV, Cocoa, iMovie, Inkwell, iPhone, iPhoto, Safari, Sand, WebScript, Xcode

Markets covered NA

Geographic coverage (2009) Americas: 44.1%; Europe: 27.5%; Rest of world: 28.4%

Future plans Focus on new product development and overcome challenges of the PC market

Financials (LTM)Revenue: 46.7 billion USD, year-over-year change: 14.4% Operating profit: 13.4 billion USD, year-over-year change: 41.0%Net income: 9.4 billion USD, year-over-year change: 34.6%

3: ORACLE CORP (US)

Brief description Develops, manufactures, markets, distributes and services database and middleware software as well as applications software. Acquired Silver Creek Systems and Sun Microsystems in January 2010.

Products soldSoftware business consists of two product segments: 1) new software licenses and 2) software license updates plus product support. Services business consists of three operating segments: consulting, on demand and education.

Key brandsApplications Unlimited, AutoVue, Case Exchange, JD Edwards EnterpriseOne, Oracle E-Business Suite, Oracle Enterprise Manager, Oracle Fusion, Oracle Transparent Gateway, Oracle Video Server, Oracleware, SQL Module

Markets covered Software and services represented 81% and 19% of its total revenues, respectively

Geographic coverage (2009) US: 43.8%; UK: 6.8%; Japan: 5.11%; Germany: 4.11% France: 3.6%; Canada: 3.17%; Rest of world: 33.3%

Future plans Plans to deliver a complete, open, integrated stack of hardware, software and business application solutions and optimize synergy benefits. Plans to form more attractive support plans.

Financials (LTM)Revenue: 24.2 billion USD, year-over-year change: 3.7%Operating profit: 9.3 billion USD, year-over-year change: 6.8% Net income: 5.7 billion USD, year-over-year change: 1.3%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-iv

4: RESEARCH IN MOTION INC. (Canada)

Brief description

Designs, manufactures and markets wireless solutions for the worldwide mobile communications market. Through the development of integrated hardware, software and services, RIM provides platforms and solutions for access to information, including e-mail, phone, SMS, Internet and intranet-based applications. Acquired Chalk Media Corp. and Certicom Corp in 2009.

Products sold Mobile applications and devices

Key brands BlackBerry

Markets covered Wireless business solutions

Geographic coverage (2009) US: 62.9%; Canada: 8.1%; UK: 6.4%; Rest of world: 22.6%

Future plans Build and operate strategies to handle the pricing pressures on mobile devices and other related services

Financials (LTM)Revenue: 14.95 billion USD, year-over-year change: 35.1% Operating profit: 3.1 billion USD, year-over-year change: NMNet income: 2.5 billion USD, year-over-year change: 29.8%

5: SAP AG (Germany)

Brief descriptionSells licenses for software solutions and related services; offers consulting, maintenance and training services for its software solutions. As of December 31, 2009, the company had more than 95,000 customers in over 120 countries and has 163 subsidiaries.

Products soldSAP Business Suite software and international corporations; SAP Business All-in-One solutions; SAP Business ByDesign solution; SAP Business One application for SMBs; SAP BusinessObjects portfolio which covers a variety of demands from small to large companies

Key brands NA

Markets covered Product, consulting and training

Geographic coverage (2009) EMEA: 52.9%; Americas: 33.9%; Asia Pacific: 13.2%

Future plans R&D focus on expanding on-demand offerings and mobility—delivering solutions on device; M&A focus is mainly on bolt-on acquisitions which will enhance its industry/technology product portfolios

Financials (LTM)Revenue: 14.9 billion USD, year-over-year change: 7.8%Operating profit: 3.9 billion USD, year-over-year change: 0.9% Net income: 2.4 billion USD, year-over-year change: 5.8%

6: COMPUTER ASSOCIATES (CA), INC. (US)

Brief descriptionIndependent IT management software company that develops and delivers software that help manage IT throughout complex computing environments. Addresses entire computing environment. Acquired Nimsoft, 3Tera, Inc., Cassatt, and Oblicore in 2010.

Products sold Products/services in mainframe and distributed environments spanning IT governance, management, security

Key brands Plans to acquire Nimsoft from which it would benefit from its strong presence with managed service providers (MSPs) and emerging enterprises solutions

Markets covered Infrastructure management, project and portfolio management, security management and data center automation and virtualization

Geographic coverage (2009) US: 58.7%; Europe: 26.4%; Rest of world: 14.9%

Future plans Restructuring efforts in Asia—shift in sales strategy from a direct sales force model to an indirect, partner-led model; plans to make acquisitions to achieve growth

Financials (LTM)Revenue: 4.3 billion USD, year-over-year change: 0.1% Operating profit: 1.3 billion USD, year-over-year change: 26.1% Net income: 742.0 million USD, year-over-year change: 38.8%

7: INTUIT INC (US)

Brief description Developer and marketer of business and financial management software solutions for SMBs, financial institutions, consumers and accounting professionals.

Products sold QuickBooks financial and business management software, payroll products for SMBs, merchant services, Lacerte and ProSeries professional tax products, outsourced online services

Key brandsBanknow, Checklock, Eclipse, Expensable, Intellicharge, Intuit, PC Access, Pocket Quicken, Pocket Quicken Connect, Proseries, Quickbooks Pro Quicken, Quickguide, Quickzoom, Tax Partner, The Tax Professional’s Choice, Turboforms

Markets covered Financial management solutions, employee management solutions, payments solutions, consumer tax solutions

Geographic coverage (2009) US: 100.0%

Future plans Focus on Mint.com (platform) rollout and reduce costs

Financials (LTM)Revenue: 3.2 billion USD, year-over-year change: 3.6% Operating profit: 718.5 million USD, year-over-year change: 5.5% Net income: 460.1 million USD, year-over-year change: 6.2%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-v

8: ADOBE SYSTEMS INC. (US)

Brief description

Diversified software company which offers creative, business, Web and mobile software and services used by creative professionals, knowledge workers, etc. for creating, managing, delivering and engaging with content and experiences across multiple operating systems, devices and media. Distributes products through a network of distributors, VARs, systems integrators, independent software vendors and OEMs, direct to end users and through its www.adobe.com. In 2009, it completed the acquisition of Omniture.

Products sold Prepackaged software

Key brands FRAME

Markets covered Creative solutions, knowledge worker, enterprise, print and publishing, platform, mobile and device solutions

Geographic coverage (2009) Americas: 46.9%; EMEA: 31.5%; Asia: 21.5%

Future plans Launch CS5 (new product) to increase portfolio offerings and focus more on the US market

Financials (LTM)Revenue: 3.0 billion USD, year-over-year change: 17.7%Operating profit: 700.1 million USD, year-over-year change: 31.0%Net income: 357.2 million USD, year-over-year change: 55.5%

9: SAGE GROUP (UK)

Brief descriptionDevelopment, distribution and support of business management software and related products and services for SMBs. Operates in 24 countries. Acquired Aytos CPD, S.L. (Aytos) and disposed of the Tax Compliance Services division in 2008. Disposed of Sage Pro-Concept S.A. in October 2009.

Products sold NA

Key brands NA

Markets covered Accounting; industry-specific; human resource (HR) and payroll; customer relationship management (CRM); payment processing

Geographic coverage (2009) North America: 40.0%; Mainland Europe: 36.2%; UK & Ireland: 16.8%; Rest of world: 7.0%

Future plans Reduce the cost base along with measures to improve license income

Financials (LTM)Revenue: 2.2 billion USD, year-over-year change: 11.1%Operating profit: 430.9 million USD, year-over-year change: 4.0% Net income: 293.7 million USD, year-over-year change: 14.0%

10: BMC SOFTWARE INC (US)

Brief description

Provides management solutions for mainframe and distributed information technology systems. Portfolio of software solutions spans enterprise systems, applications, databases and IT process management. Acquired MQSoftware and Tideway Systems Limited in 2009. Acquired Phurnace Software, a developer of automation software in January 2010.

Products sold Mainframe and distributed systems, applications, databases and information technology process management functions

Key brands ACSM, Assuring Business Availability, BMC Software, Cellular Event Processing Architecture, Mastercell, Mastervision

Markets covered Enterprise service management and mainframe service management

Geographic coverage (2009) US: 62.1%; and Rest of world: 37.9%

Future plans Focus on transformation of sales force

Financials (LTM)Revenue: 1.9 billion USD, year-over-year change: 8.1% Operating profit: 523.0 million USD, year-over-year change: 20.0%Net income: 370.6 million USD, year-over-year change: 24.1%

11: FUJI SOFT INC (Japan)

Brief description Independent software developer specializing in communications and machine control software, business application software for bank and insurance companies, and operating system software.

Products sold Embedded software, operation software and other software

Key brands NA

Markets covered Software for control and operational systems, cost saving measures by cutting SG&A expenses, expanding global footprint through acquisitions, strengthening collaboration within the group

Geographic coverage (2009) Japan: 100%

Future plans Promote cloud computing and on-premise businesses

Financials (LTM)Revenue: 1.6 billion USD, year-over-year change: 3.3% Operating profit: 53.0 million USD, year-over-year change: 2.7%Net income: 10.5 million USD, year-over-year change: 59.3%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-vi

12: CITRIX SYSTEMS (US)

Brief descriptionDesigns, develops and markets technology solutions that enable IT services to be delivered through its virtual computing infrastructure on demand, independent of location, device or network. Citrix served over 230,000 customers and over 100 million users in more than 100 countries in 2009.

Products sold Desktop solutions and datacenter/cloud solutions

Key brands XenDesktop, XenApp, GoToMeeting, GoToTraining, GoToAssist and GoToMyPC, CitrixXenServer, Citrix Essentials

Markets covered NA

Geographic coverage (2009) Americas: 43.1%; EMEA: 29.8%; Asia-Pacific: 8.0%; Rest of world: 19.1%

Future plans Focus on expanding XenDesktop 4 offerings both as long term and near term trade opportunities

Financials (LTM)Revenue: 1.6 billion USD, year-over-year change: 1.9% Operating profit: 210.9 million USD, year-over-year change: 32.1% Net income: 191.0 million USD, year-over-year change: 7.1%

13: SUMISHO COMPUTER (Japan)

Brief description Develops a variety of computer software, including software for business applications, electronic commerce, development tools, internet and financial industries. Industrial solutions form a major portion of revenues.

Products sold Industrial solutions, ERP solutions and platform solutions

Key brands NA

Markets covered Packaged software, software development, information services

Geographic coverage (2009) Japan: 100.0%

Future plans Focus on projects in the insurance and banking industries; allocating management resources to clients’ IT infrastructure development and certain R&D solutions

Financials (LTM)Revenue: 1.4 billion USD, year-over-year change: 2.1%Operating profit: 83.8 million USD, year-over-year change: 12.4%Net income: 32.6 million USD, year-over-year change: 26.9%

14: SALESFORCE.COM (US)

Brief descriptionProvides enterprise cloud computing applications; provides a technology platform for customers and developers to build and run business applications; offerings can be deployed, customized and integrated with other software applications; markets its service to businesses on a subscription basis.

Products sold NA

Key brands NA

Markets covered Customer and collaboration relationship management (CRM)

Geographic coverage (2009) Americas: 70.8%; Europe: 17.8%; Asia-Pacific: 11.4%

Future plans Focus on capturing opportunities in the area of enterprise software and may look to make an acquisition

Financials (LTM)Revenue: 1.3 billion USD, year-over-year change: 21.3% Operating profit: 115.3 million USD, year-over-year change: 80.8%Net income: 80.7 million USD, year-over-year change: 85.9%

15: MISYS PLC (UK)

Brief description

Engaged in the development, management and licensing of a variety of software products and solutions to customers in the financial services and healthcare industries; develops and delivers open source technologies. The merger to form Allscripts-Misys Healthcare Solutions, Inc. (Allscripts) was completed in October 2008. Misys PLC acquired a 56.8% interest in Allscripts.

Products sold NA

Key brands BankFusion universal banking solution

Markets covered Software solutions to banking, treasury & capital markets, Allscripts healthcare, central services

Geographic coverage (2009) Americas: 60.8%; Europe: 19.1%; Asia-Pacific: 7.15%; UK: 5.68%; Rest of world: 7.38%

Future plans Focus on upgrading existing customers along with new customers by selling BankFusion software and creating suitable sales support for BankFusion

Financials (LTM)Revenue: 1.2 billion USD, year-over-year change: 40.6% Operating profit: 186.9 million USD, year-over-year change: 35.4% Net income: 47.4 million USD, year-over-year change: 27.6%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-vii

16: SOFTWARE AG (Germany)

Brief descriptionProvides business infrastructure software solutions; products include solutions for managing data, enabling service-oriented architecture (SOA) and improving business processes; has more than 80 locations in 70 countries worldwide.

Products sold Enterprise transaction systems include software such as Adabas SQL Gateway, Event Replicator, Natural Business Services, Natural Engineer. Other web methods include webMethods Suite and CentraSite

Key brands NA

Markets covered Professional services, maintenance, licenses

Geographic coverage (2008) US: 28.6%; Germany: 11.28%; Spain: 10.9%; Rest of world: 49.2%

Future plans Integrate IDS Scheer (new platform from acquisition) along with cross-selling opportunities; cost control

Financials (LTM)Revenue: 1.2 billion USD, year-over-year change: 17.6% Operating profit: 300.1 million USD, year-over-year change: 30.8%Net income: 196.6 million USD, year-over-year change: 21.7%

17: SYBASE INC (US)

Brief description Delivers enterprise software and services to manage, analyze and mobilize information; provides open, cross-platform solutions that deliver information anytime and anywhere, providing decision-ready information.

Products sold Enterprise class database servers, integration and development products, mobile database, mobile enterprise solutions

Key brands Adaptive Server Enterprise, EDI Server, Information Anywhere, Jaguar CTS, Navigation Server, SQL Server, Sybase, Ultralite.net, Warehouse Studio

Markets covered Infrastructure platform and global services for mobile messaging interoperability and the management and distribution of mobile content

Geographic coverage (2008) North America: 50.2%; EMEA: 35.3%; Asia Pacific and Latin America: 14.6%

Future plans Explore new database architecture and software to power mobile devices; expand offerings in the software and architecture areas through acquisition

Financials (LTM)Revenue: 1.2 billion USD, year-over-year change: 3.4% Operating profit: 290.9 million USD, year-over-year change: 38.4%Net income: 164.0 million USD, year-over-year change: 27.9%

18: CHECK POINT SOFT (Israel)

Brief description

Develops, markets, and supports a range of software and combined hardware and software products and services for IT security; solutions operate under a unified security architecture that enables total end-to-end security with a single line of unified security gateways and allows a single agent for all endpoint security. Acquired Nokia Corporation’s security appliance business in April 2009.

Products sold NA

Key brands NA

Markets covered Network and gateway security solutions, data and endpoint security solutions, management solutions

Geographic coverage (2008) EMEA: 44.6%; Americas: 43.2%; Japan: 12.2%

Future plans Focus on share buyback, major focus on product revenues in the data security segment rather than maintenance support

Financials (LTM)Revenue: 924.4 million USD, year-over-year change: 14.3% Operating profit: 424.1 million USD, year-over-year change: 19.0% Net income 357.5 million USD, year-over-year change: 10.4%

19: MICROS SYSTEMS INC (US)

Brief descriptionDesigner, manufacturer, marketer and servicer of enterprise information solutions for the global hospitality and specialty retail industries. Acquired Fry, Inc., an e-commerce design, development and managed services provider August 2008.

Products sold Software encompassing property-based management systems (PMS), related property-specific modules and applications, central systems including central reservation systems (CRS)

Key brands Fidelio

Markets covered Enterprise solutions: hotel information systems, restaurant information systems, specialty retail information systems

Geographic coverage (2009) US: 51.6%; Rest of world: 48.4%

Future plans Focus on cost reduction and further improvement in margins

Financials (LTM)Revenue: 867.9 million USD, year-over-year change: 4.4% Operating profit: 145.3 million USD, year-over-year change: 3.2% Net income: 98.2 million USD, year-over-year change: 1.9%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-viii

20: OPEN TEXT CORPORATION (Canada)

Brief description

Provides enterprise content management (ECM) software solutions; Open Text ECM Suite enables corporations to manage traditional forms of content (images, office documents, graphics and drawings) as well as electronic content (Web pages, e-mail and video); offers solutions both as end-user standalone products and as fully integrated modules. Acquired Vizible Corporation and Vignette Corporation in 2009.

Products sold ECM software products

Key brands NA

Markets covered ECM software solutions

Geographic coverage (2009) North America: 50.4%; Europe: 42.6%; Others: 6.9%

Future plans Launch of a new series of products in mobile applications

Financials (LTM)Revenue: 854.6 million USD, year-over-year change: 8.3% Operating profit: 106.1 million USD, year-over-year change: 35.0%Net income: 64.5 million USD, year-over-year change: 7.4%

21: NOVELL INC (US)

Brief description Develops, sells and installs enterprise software positioned in the operating systems and infrastructure software layers of the IT industry worldwide.

Products soldSUSE Linux Enterprise Server, an open source server operating system; SUSE Linux Enterprise Desktop, a business desktop operating system; SUSE Studio that allows independent software vendors to build software appliances; SUSE Moblin, a Linux based open source operating system

Key brands Novell ZENworks and PlateSpin

Markets covered Linux and related solutions for enterprises; identity and security management; systems and resource management

Geographic coverage (2009) US: 49.3%; EMEA: 34.9%; Asia Pacific: 9.5%; Rest of world: 6.4%

Future plans Focus on improvement in top line in the next 12-18 months and improve fundamentals

Financials (LTM)Revenue: 849.7 million USD, year-over-year change: 9.9% Operating profit: 135.0 million USD, year-over-year change: 101.4% Net income: 203.0 million USD, year-over-year change: NM

22: RED HAT INC (US)

Brief description

Develops and provides open source software and services; offers information and news about open source software and provides an online community of open source software; collectively developed software is distributed under open source licenses, such as the GNU General Public License and GNU Lesser General Public License, permitting access to the human-readable software source code. Acquired Amentra, Inc., and Qumranet, Inc. in 2008.

Products sold Operating systems and software

Key brands Red Hat Linux operating system, JBoss Enterprise Middleware

Markets covered Core enterprise operating system platform, enterprise middleware platform and virtualization solutions

Geographic coverage (2009) Americas: 64.7%; EMEA: 21.7%; Asia Pacific: 13.6%

Future plans Focus on key go-to-market initiatives and achieve sustained earnings growth. In terms of technology strategy, it aims to promote Enterprise Linux 5.4 and virtualization

Financials (LTM)Revenue: 748.2 million USD, year-over-year change: 14.7% Operating profit: 109.1 million USD, year-over-year change: 32.2% Net income 87.3 million USD, year-over-year change: 10.8%

23: AUTONOMY CORP (UK)

Brief description

Developer cum manufacturer that licenses, sells and supports software products; also offers operating system software, server application software, business and consumer applications software, software development tools and Internet- based solutions. Acquired Interwoven, Inc. in March 2009 and MicroLink, LLC in February 2010.

Products sold Intelligence data operating layer (IDOL) server, IDOL platform, and IDOL protect products

Key brands TeamSite, LiveSite, Optimost, MediaBin, MetaTagger, OpenDeploy, ControlHub, Qfiniti Enterprise, Autonomy Explore

Markets covered Business solutions

Geographic coverage (2009) Americas: 69.9%; Rest of world: 30.1%

Future plans Expand through acquisition

Financials (LTM)Revenue: 739.7 million USD, year-over-year change: 47.0%Operating profit: 277.4 million USD, year-over-year change: 49.1% Net income 191.6 million USD, year-over-year change: 45.4%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-ix

24: LAWSON SOFTWARE (US)

Brief description

Provider of enterprise software, services and support targeting customers in specific industries, including equipment service management and rental, fashion, food and beverage, healthcare, manufacturing and distribution, public sector (US) and service industries, as well as the horizontal market for the strategic human capital management product line; provides software in 29 languages to more than 4,500 customers in 41 countries.

Products sold Software related to business processes, enterprise asset management, equipment service management, CRM, HCM

Key brands Business Begins With E, Drill Around, Lawson Ezupdate, Lawson Software, Lawson Suiteexpress Self-Evident Applications, The Information Office, Webtree

Markets covered Software applications and industry-specific solutions

Geographic coverage (2009) Americas: 58.1%; EMEA: 37.8%; Asia Pacific: 4.1%

Future plans Focus on expanding product portfolio, leveraging favorable spending trends in HCM, extending its products into the cloud computing application area

Financials (LTM)Revenue: 713.5 million USD, year-over-year change: 11.1% Operating profit: 77.6 million USD, year-over-year change: 28.5% Net income: 26.0 million USD, year-over-year change: 38.0%

25: QUEST SOFTWARE (US)

Brief description

Designs, develops, markets, distributes and supports enterprise systems management software products. In addition to perpetual software licenses, it sells time-based software licenses wherein customers pay a single fee for the right to use the software and receive maintenance for a defined period of time. Acquired PacketTrap Networks, Inc. in December 2009.

Products sold Big Brother, Deploydirector, Epurposing, Imagevue, IT Dad, Livereorg, NBSpool, Smartalarm, Spotlight, SQlab Xpert, SQL Navigator, Vista Plus

Key brands Foglight, InTrust, JProbe, MessageStats, SQL Navigator, Benchmark Factory, PowerGUI

Markets covered Software solution for application management, database management, windows management and virtualization management

Geographic coverage (2009) US: 62.5%; UK: 9.3%; Rest of world: 28.9%

Future plans Focus on Microsoft’s unified communications strategy

Financials (LTM)Revenue: 695.2 million USD, year-over-year change: 5.5% Operating profit: 102.5 million USD, year-over-year change: 1.5% Net income: 70.4 million USD, year-over-year change: 3.4%

26: ORACLE FINANCIAL (India)

Brief description Provides comprehensive IT solutions to the financial services industry worldwide; provides transaction processing and accounting software for banks, investment managers and mutual funds.

Products sold Product licenses and related activities (products); IT solutions and consulting services (services)

Key brands Flexcube suite, Reveleus, MicroBanker

Markets covered Financial services

Geographic coverage (2009) Europe: 34.2%; US: 29.1%; Asia Pacific: 19.9%; Middle East, India and Africa: 14.8%; Latin America and Caribbean: 2.1%

Future plans Improve its KPO business, which is currently a small part of revenues, and increase margins of maintenance services in light of the tough business climate

Financials (LTM)Revenue: 641.3 million USD, year-over-year change: 23.0% Operating profit: 151.3 million USD, year-over-year change: 74.1% Net income: 161.3 million USD, year-over-year change: 77.2%

27: NEUSOFT CORP (China)

Brief descriptionProvides software products such as HR management systems, group financial management systems, learning management systems, security operations centers, office management systems, network application monitoring and management systems, CRM systems; domestic and overseas markets.

Products sold NA

Key brands TalentBase, MPC, SkillBase, NetEye, UniOffice, NetPatrol

Markets covered Telecommunication, government, electric power, enterprise and electronic commerce, finance, education, traffic, medical equipment and health services

Geographic coverage (2008) China: 66.8%; Rest of world: 33.2%

Future plans Focus on outsourcing business

Financials (LTM)Revenue: 601.9 million USD, year-over-year change: 12.2% Operating profit: 69.8 million USD, year-over-year change: 16.8% Net income: 93.8 million USD, year-over-year change: 30.5%

IMAP’s Computing & Internet Software Industry Global Report — 2010: Appendix A-x

28: UNIT 4 AGRESSO NV (The Netherlands)

Brief description

Provides integrated business management software and internet and security solutions; provides information and communications technology products and services such as the design of e-commerce websites, implementation of security products (including anti-virus products, firewalls and e-mail content filters), ERP solutions and outsourcing of IT network management.

Products sold NA

Key brands NA

Markets coveredFinancial administration applications, applications for logistics and wholesale distribution, software to support production processes, project costing and invoicing systems, as well as software for information management and reporting

Geographic coverage (2009) Benelux: 32.9%; UK: 18.8%; Sweden: 13.5%; Spain: 10.6%; Norway: 8.0%; Germany: 4.5%; Rest of world: 11.7%

Future plans Focus on pipeline development and organic license sales

Financials (LTM)Revenue: 529.1 million USD, year-over-year change: 3.6% Operating profit: 52.4 million USD, year-over-year change: 14.7% Net income: 27.1 million USD, year-over-year change: 58.5%

29: TOTVS SA (Brazil)

Brief descriptionDevelops and markets software solutions including ERP software, CRM software and SCM software. Offers performance consulting; outsourcing of administrative processes, technology, and infrastructure; and distance education.

Products sold ERP software, CRM software, business intelligence software, SCM software

Key brands Logocenter, Totvs, Microsiga, RM Sistemas, TOTVS BMI

Markets covered NA

Geographic coverage (2009) Brazil: 100%

Future plans Focus on diversification of industry verticals to balance out seasonal effects, increase penetration in Brazil

Financials (LTM)Revenue: 501.3 million USD, year-over-year change: 45.7% Operating profit: 90.9 million USD, year-over-year change: 242.4% Net income: 61.0 million USD, year-over-year change: 149.5%

30: PROGRESS SOFTWARE CORPORATION (US)

Brief descriptionSupplier of application infrastructure software and services for the development, deployment, integration and management of business applications; develops, markets and distributes its products to businesses, industries and governments worldwide. Acquired Savvion, Inc. in January 2010.

Products sold Software solutions and services

Key brands OpenEdge, Orbix, ObjectStore, Apama, Sonic, Progress Actional and FUSE products, DataDirect Connect, DataDirect Shadow, DataXtend