Embed Size (px)

Citation preview

www.complianceonlie.com©2010 Copyright

© 2015 ComplianceOnline

This training session is sponsored by

1

Developing an Effective Fraud Risk Management Program

This Training is Brought to you by ComplianceOnline.

Presenter: Craig M. Taggart

www.complianceonline.com©2015 Copyright

Areas Covered in the Webinar: Identify fraud risks and the factors that influence them Analyze existing risk management frameworks and

their application to managing fraud risk Develop and implement the necessary components of

a successful fraud risk management program Identify the elements of a strong ethical corporate

culture Conduct a cost effective fraud risk assessment

2

www.complianceonline.com©2015 Copyright

Agenda

3

The risk of fraud is just one of the many types of risks to be managed by an organization. But to let this risk fall out of focus can bring catastrophic results. Building an effective fraud risk management program to combat organizational fraud requires solid understanding of how and why fraud is perpetrated. This course will discuss the components of a fraudulent act, different types of fraud schemes and the impact fraud has on organizations. It will also analyze why individuals commit fraud and why the threat of punishment alone doesn’t deter potential fraudsters

www.complianceonline.com©2015 Copyright

Definition of Fraud source Wikipedia

In law, fraud is deliberate deception to secure unfair or unlawful gain. Fraud is both a civil wrong (i.e., a fraud victim may sue the fraud perpetrator to avoid the fraud and/or recover monetary compensation) and a criminal wrong (i.e., a fraud perpetrator may be prosecuted and imprisoned by governmental authorities). The purpose of fraud may be monetary gain or other benefits, such as obtaining a drivers license by way of false statements. A hoax is a distinct concept that involves deception without the intention of gain or of materially damaging or depriving the victim.

4

www.complianceonline.com©2015 Copyright

5

Instructor Profile: Craig Taggart has almost a decade of experience in the fields of mergers and acquisitions and

business financing. Mr. Taggart works strategically with his clients to achieve the highest value for their business within the capital markets. His experience with BCC Capital Partners in the M&A industry has greatly contributed to his understanding of transaction structure, strategic

placement of buyers, and the attainment of maximum market value for his clients. He has represented and sold many businesses in a number of different industries and has significant experience working with companies in: continuing education, transportation, software and professional services. Mr. Taggart is currently working in the clean energy sector that covers multiple initiatives within M&A and corporate development.

He is a certified merger and acquisition advisor, accredited valuation analyst as well as an active member of Alliance of Mergers and Acquisition, and The National Association of Certified Valuators and Analysts (NACVA). Mr. Taggart has been a certified fraud examiner since 2011 and has owned an investigative franchise business, which focused on fraud based cases involving insurance, asset searches, surveillance, witness statements

He earned his MBA from the San Diego State University specializing in financial management. Mr. Taggart graduated from the California State University Northridge with a bachelor’s degree majoring in organizational psychology.

www.complianceonline.com©2015 Copyright

Agenda

6

Why Should You Attend:The field of risk management has attracted increased mainstream attention in the wake of the economic meltdown as the public has begun to comprehend the negative effects of uncontained risk. Unfortunately, many risk management professionals tend to underestimate the role of fraud in the scope of their professional duties.

www.complianceonline.com©2015 Copyright

With organizations losing an estimated 5 percent of their annual revenues to fraud, Applied to the estimated 2013 gross world product, this figure translates to a potential total fraud loss of more than $3.5 trillion (U.S.). The need for a strong anti-fraud stance and proactive, comprehensive approach to combating fraud is clear. As organizations increase their focus on fraud, they should take the opportunity to consider, enact and improve measures to detect, deter and prevent fraud. Without clear, defined objectives, a fraud risk management program cannot be effective.

7

www.complianceonline.com©2015 Copyright

Common Fraud Schemes source FBI

Telemarketing Fraud Identity Theft Advance Fee Schemes Health Care Fraud / Health Insurance Fraud Redemption / Strawman / bond Fraud Nigerian Letter or “419” Fraud

8

www.complianceonline.com©2015 Copyright

9

www.complianceonline.com©2015 Copyright

Whether in your individual role or in a team setting, you are taking on a process of determining current or future acts of fraud. The process at a larger organizational level or within a function, the fraud assessment process is basically the same. Here is the top down approach:

Review Business Objectives Review current assessed fraud & fraud categories Review core processes tied to the objectives Brainstorm fraud that can affect your organization

The Fraud Assessment Process

10

www.complianceonline.com©2015 Copyright

Determine criteria or (possibility and impact) to develop ranking acts of fraud into critical, important and not important as it pertains to specific organization

Determine whether the controls in place are efficient and effective

Action plans and more testing where needed

11

www.complianceonline.com©2015 Copyright

Corruption, embezzlement, fraud, these are all characteristics which exist everywhere. It is regrettably the way human nature functions, whether we like it or not. What successful economies do is keep it to a minimum. No one has ever eliminated any of that stuff.

Alan Greenspan former Chairman of the Federal Reserve of the United States from 1987 to 2006

12

www.complianceonline.com©2015 Copyright

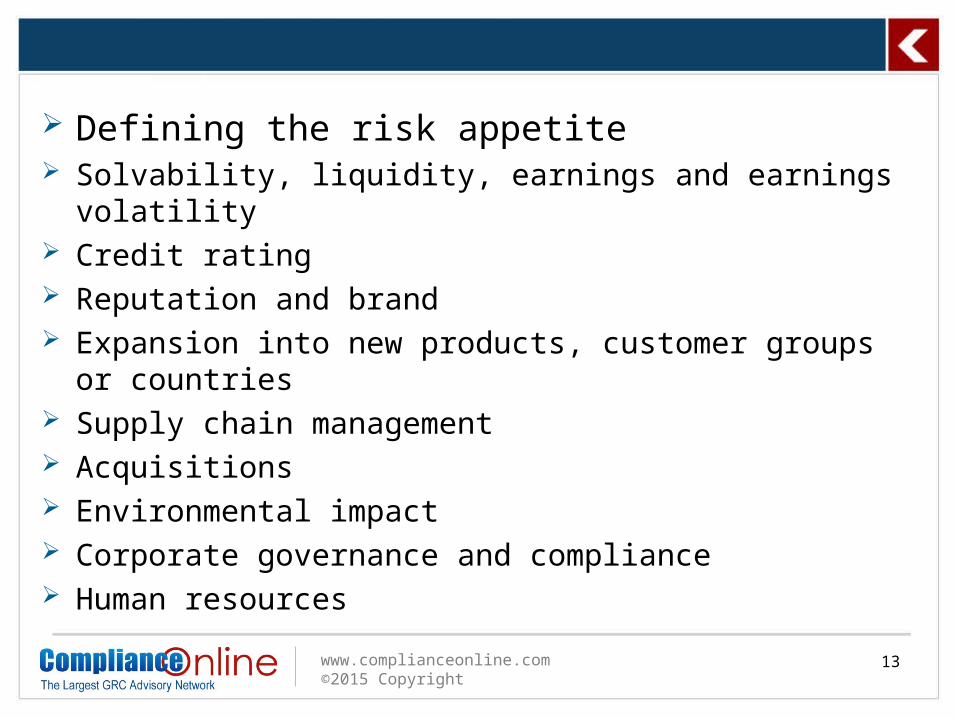

Defining the risk appetite Solvability, liquidity, earnings and earnings volatility Credit rating Reputation and brand Expansion into new products, customer groups or countries Supply chain management Acquisitions Environmental impact Corporate governance and compliance Human resources

13

www.complianceonline.com©2015 Copyright

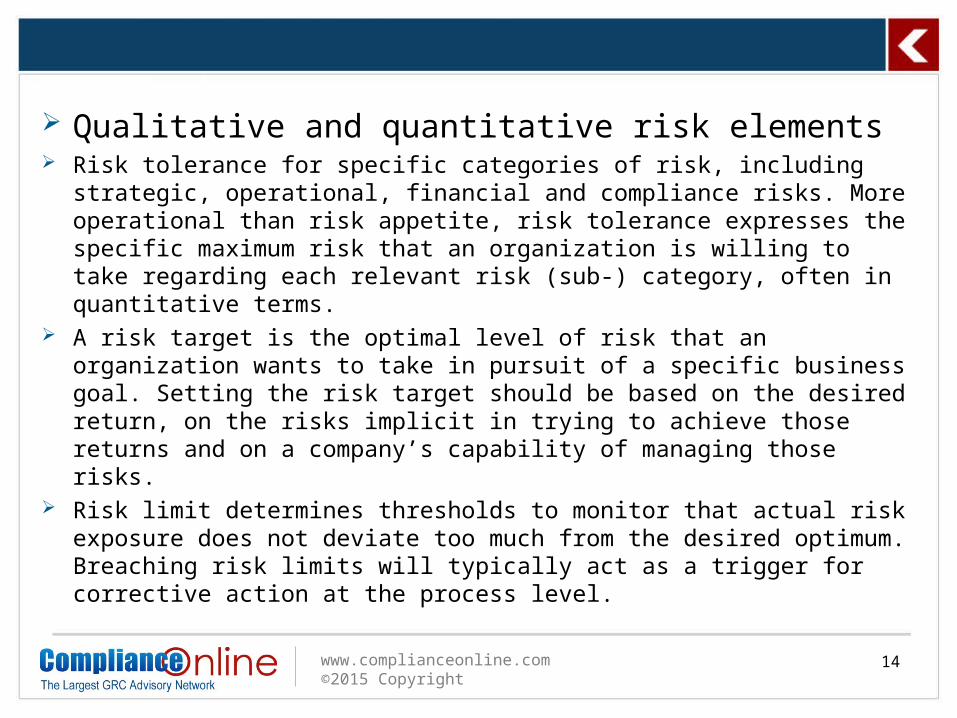

Qualitative and quantitative risk elements Risk tolerance for specific categories of risk, including strategic, operational,

financial and compliance risks. More operational than risk appetite, risk tolerance expresses the specific maximum risk that an organization is willing to take regarding each relevant risk (sub-) category, often in quantitative terms.

A risk target is the optimal level of risk that an organization wants to take in pursuit of a specific business goal. Setting the risk target should be based on the desired return, on the risks implicit in trying to achieve those returns and on a company’s capability of managing those risks.

Risk limit determines thresholds to monitor that actual risk exposure does not deviate too much from the desired optimum. Breaching risk limits will typically act as a trigger for corrective action at the process level.

14

www.complianceonline.com©2015 Copyright

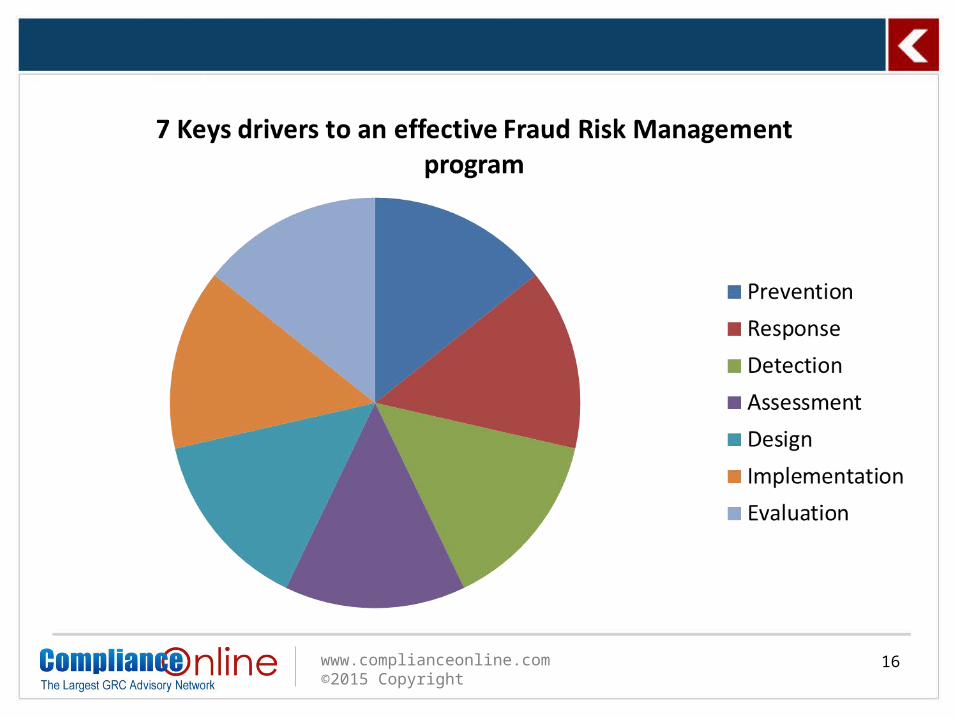

Developing a fraud risk management program As mentioned previously, an effective fraud and

misconduct risk management approach is one that focuses on three objectives: establishing policies, programs, and controls designed to reduce the risk of fraud and misconduct from occurring; detecting it when it occurs; and taking appropriate corrective action to remedy the harm caused by integrity breakdowns.

15

www.complianceonline.com©2015 Copyright

16

www.complianceonline.com©2015 Copyright

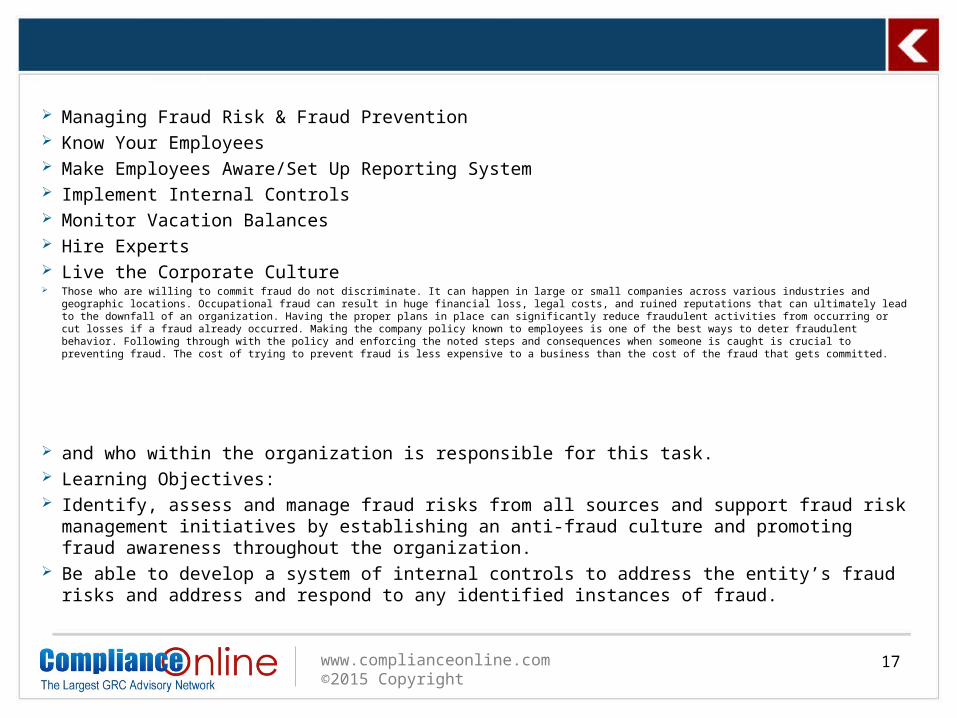

Managing Fraud Risk & Fraud Prevention Know Your Employees Make Employees Aware/Set Up Reporting System Implement Internal Controls Monitor Vacation Balances Hire Experts Live the Corporate Culture Those who are willing to commit fraud do not discriminate. It can happen in large or small companies across various industries and geographic locations. Occupational fraud can result

in huge financial loss, legal costs, and ruined reputations that can ultimately lead to the downfall of an organization. Having the proper plans in place can significantly reduce fraudulent activities from occurring or cut losses if a fraud already occurred. Making the company policy known to employees is one of the best ways to deter fraudulent behavior. Following through with the policy and enforcing the noted steps and consequences when someone is caught is crucial to preventing fraud. The cost of trying to prevent fraud is less expensive to a business than the cost of the fraud that gets committed.

and who within the organization is responsible for this task. Learning Objectives: Identify, assess and manage fraud risks from all sources and support fraud risk management initiatives by

establishing an anti-fraud culture and promoting fraud awareness throughout the organization. Be able to develop a system of internal controls to address the entity’s fraud risks and address and

respond to any identified instances of fraud.

17

www.complianceonline.com©2015 Copyright

Techniques used for fraud detection fall into two primary classes: statistical techniques and artificial intelligence.[3] Examples of statistical data analysis techniques are:

Data preprocessing techniques for detection, validation, error correction, and filling up of missing or incorrect data.

Calculation of various statistical parameters such as averages, quantiles, performance metrics, probability distributions, and so on. For example, the averages may include average length of call, average number of calls per month and average delays in bill payment.

18

www.complianceonline.com©2015 Copyright

Models and probability distributions of various business activities either in terms of various parameters or probability distributions.

Computing user profiles. Time-series analysis of time-dependent data. Clustering and classification to find patterns and associations

among groups of data. Matching algorithms to detect anomalies in the behavior of

transactions or users as compared to previously known models and profiles. Techniques are also needed to eliminate false alarms, estimate risks, and predict future of current transactions or users.

19

www.complianceonline.com©2015 Copyright

THANK YOU FOR YOUR ATTENTION

20

For more information on Live Webinars and any Other Training Requirements please email us [email protected] or Call us at this Toll Free Number: 1- 888-717-2436