Embed Size (px)

Citation preview

COMPLETION OF THE ACCOUNTING CYCLE

- Closing Entries -

CHAPTER

10

Account Titles Debit Credit Debit Credit Debit Credit Debit Credit Debit CreditBalance SheetTrial Balance Adjustments Adjusted Trial Balance Income Statement

1. Prepare trial balance

on the worksheet.

2. Enter adjustment

data.

3. Enter adjusted balances

4. Extend adjusted balance to appropriate

columns.5. Calculate income/loss

and complete the worksheet.

Worksheet Over View

The final stage of the accounting cycle is to prepare the accounts for the next fiscal period.

To do this, you must understand which accounts have balances that continue from one period to the next and which do not.

Closing Entry Concepts

When a new accounting period begins, the revenue and expense accounts should show zero balances so that they contain only data that refer to the new period.

This allows the calculation of net income according to the matching principle, which states:

Revenue for each accounting period is matched with expenses for that accounting period to determine the net income or net loss.

Closing Entry Concepts Continued

1. Updates the owner’s capital account in the ledger by transferring net income (loss) and owner’s drawings to owner’s capital.

2. Prepares the temporary accounts (revenue, expense, drawings) for the next period’s postings by reducing their balances to zero.

Purpose of Closing Entries

The revenue and expense accounts are reduced to zero by a process called closing the books.

Closing the books is the process by which revenue and expense accounts are reduced to zero of the end of each accounting period.

Closing the accounts is sometimes called clearing the accounts.

Closing Entries

Real Accounts and Nominal Accounts

All asset and liability accounts, as well as the owner's capital account, are considered to be real accounts.

Real accounts have balances that continue into the next fiscal period.

Examples of real accounts are Bank, Trucks, and Accounts Payable.

Real Accounts

Nominal accounts (Revenue, Expense, and Drawings) have balances that do not continue into the next fiscal period.

Nominal accounts, with the exception of the Drawings account, are related to the income statement, and the income statement deals only with a single fiscal period.

All nominal accounts begin each fiscal period with a nil balance.

Nominal Accounts

Real Accounts and Nominal Accounts

A special nominal account, called the Income Summary account, is used only during the closing entry process.

The Income Summary account summarizes the revenues and expenses of the period.

The temporary balance in this account represents either the amount of net income or the amount of net loss.

Real Accounts and Nominal Accounts

Income Summary

Other names for REAL and NOMINAL accounts are Permanent and TEMPORARY accounts.

These alternative terms help you remember which accounts will continue to have balances (PERMANENT) and which will be closed out (TEMPORARY).

Real Accounts and Nominal Accounts

Temporary Versus Permanent

TEMPORARY (NOMINAL) PERMANENT (REAL) These accounts are closed These accounts are not closed

All revenue accounts All asset accounts

All expense accounts All liability accounts

Owner’s drawings Owner’s capital account

(Balance Sheet Accounts)(Income Statement / Drawings Accounts)

(INDIVIDUAL) REVENUES

1

Diagram of the Closing Process

1 Debit each revenue account for its balance, and credit the owner’s capital account for total revenues.

2 Debit the owner’s capital account for total expenses, and credit each expense account for its balance.

1 Debit each revenue account for its balance, and credit the owner’s capital account for total revenues.

2 Debit the owner’s capital account for total expenses, and credit each expense account for its balance.

(INDIVIDUAL)EXPENSES

Normal Dr. Balance

Normal Cr. Balance

Cr. to close Dr. to close

- 0 - - 0 -

OWNER’SCAPITAL

Expenses Revenues

Opening Balance

2

3

3 Debit owner’s capital for the balance in the owner’s drawings account and credit owner’s drawings for

the same amount.

3 Debit owner’s capital for the balance in the owner’s drawings account and credit owner’s drawings for

the same amount.

OWNER’SDRAWINGS

Normal Dr. Balance

Cr. to close

- 0 -

OWNER’SCAPITAL

Expenses

Revenues

Opening BalanceDrawings

Ending Balance

Diagram of the Closing Process

Summary

In summary, there are four steps involved in closing the books:

1. Close the revenue accounts into Income Summary.

2. Close the expense accounts into Income Summary.

3. Close Income Summary into Capital.

4. Close Drawings into Capital.

12

3

4

Journalizing and Posting the Closing Entries

Closing Entry No. 1

Don’t forget to post to the General Ledger

Journalizing and Posting the Closing Entries

Closing Entry No. 2

Don’t forget to post to

the General Ledger

Journalizing and Posting the Closing Entries

Closing Entry No. 3

Don’t forget to post to the General Ledger

Journalizing and Posting the Closing Entries

Closing Entry No. 4

Don’t forget to post to the General Ledger

STOP AND CHECK

1. Does the balance in your Owner’s Capital account equal the ending capital balance reported in the Balance Sheet and Statement of Owner’s Equity?

2. Are all of your temporary account balances zero?

Closing Entries

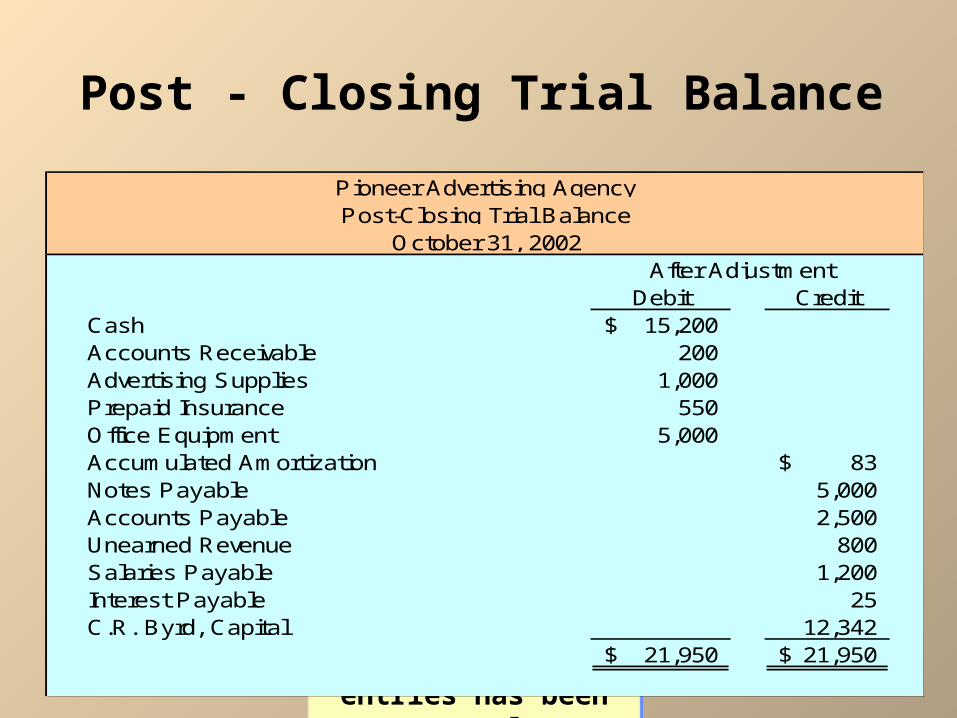

After all closing entries have been journalized and posted, a post-closing trial balance is prepared.

The purpose of this trial balance is to prove the equality of the permanent (balance sheet) account balances that are carried forward into the next accounting period.

Post - Closing Trial Balance

Debit CreditCash 15,200$ Accounts Receivable 200 Advertising Supplies 1,000 Prepaid Insurance 550 Office Equipment 5,000 Accumulated Amortization 83$ Notes Payable 5,000 Accounts Payable 2,500 Unearned Revenue 800 Salaries Payable 1,200 Interest Payable 25 C.R. Byrd, Capital 12,342

21,950$ 21,950$

After Adjustment

Pioneer Advertising AgencyPost-Closing Trial Balance

October 31, 2002

The post-closing trial balance is prepared from the permanent

accounts in the ledger.

The post-closing trial balance is prepared from the permanent

accounts in the ledger.

The post-closing trial balance provides evidence that the journalizing and posting of closing entries

has been properly completed.

The post-closing trial balance provides evidence that the journalizing and posting of closing entries

has been properly completed.

Post - Closing Trial Balance

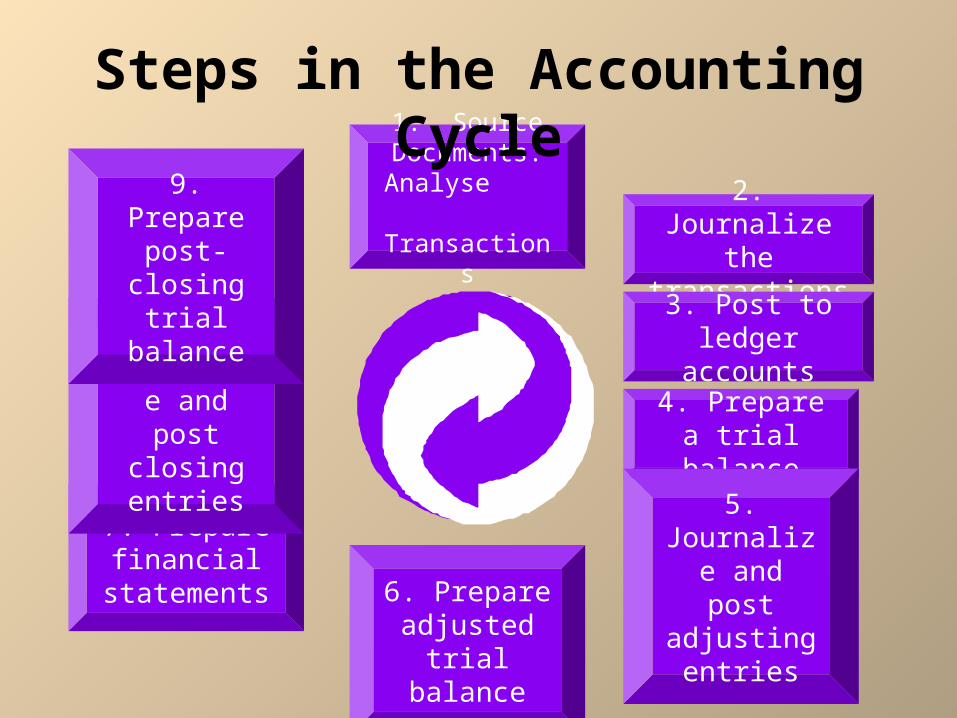

1. Source Documents:

Analyse Transactions

2. Journalize the transactions

3. Post to ledger accounts

4. Prepare a trial balance

5. Journalize and post adjusting entries

6. Prepare adjusted trial

balance

7. Prepare financial

statements

8. Journalize and post

closing entries

9. Prepare post-closing trial balance

Steps in the Accounting Cycle