Embed Size (px)

Citation preview

The investment management industry’s revenue growth will continue to slow, with net flows accounting for less than 1% of annual growth worldwide between now and 2017, compared to organic growth rates of between 6% and 7% per annum before the crisis.

Nevertheless, there will be substantial opportunities in key segments and strategies. Five key drivers will account for virtually all positive impact on revenue growth during the next five years:

• Continuing “democratization” of alternative investments

• Increasing popularity of customized and packaged investmentsolutions

• Globalizing portfolios

• Growing assets of wealthy individuals

• The rise of investors in emerging markets

Nearly 90% of new industry revenues between now and 2017 will accrue to a select group of firms able to capably deliver one or more of four key value propositions to investors:

• High-alpha active management

• Cost-efficient beta

• Asset allocation expertise

• Solutions-led distribution

A substantial portion of the industry’s current competitors face the threat of irrelevance unless they undertake substantive change. Firms that do not offer any of the four key value propositions will only attract 10% of the industry’s net new revenues and lose significant market share between now and 2017.

Today’s asset managers can transform themselves into tomorrow’s Complete Firms by:

• Delivering investments leadership in a “difficult to differentiate” environment

• Organizing well-led and resourced sales/marketing efforts that foster growth

• Building a technically skilled client interface for client cultivation and retention

• Implementing incentives that aggressively attract and retain talent

• Instituting governance and ownership practices that support long-termdynamism

The Complete Firm 2013:Competing for the 21st Century Investor

CaseyQuirk by Deloitte.

The Complete Firm 2013: Competing for the 21st Century Investor 1

Table of Contents

1. Introduction:

A Changing, Maturing Industry ....................2

2. Slowing Revenue Growth ............................3

3. A Concentrating Industry ............................11

4. Prologue to the Complete Firm....................15

5. The Complete Firm 2013 ..........................20

6. Conclusion ..............................................30

Authorship

Authors:Kevin P. Quirk, PrincipalBenjamin F. Phillips, Investment Management Lead Strategist - Consulting

Contributors:John F. Casey, former Chairman at Casey QuirkDaniel Celeghin, Head of Wealth Management Strategy Asia-PacificYariv Itah, Casey Quirk Global Practice LeaderJonathan H. Feldman, former Director of Research at Casey QuirkJeffrey A. Levi, Principal

Supporting Team:Michael D. Chia, former Manager at Casey QuirkDan Neeman, former Senior Associate at Casey QuirkJacob F. Walker, former Senior Associate at Casey QuirkSheryle D. Wells, former Marketing Associate at Casey Quirk

Casey Quirk by Deloitte helps clients develop broad business growth strategies, improve investment/product appeal and growth prospects, evaluate new market and product opportunities, and enhance incentive alignment structures. Our unparalleled industry knowledge and experience, detailed proprietary data, and global network of relationships make Casey Quirk by Deloitte a leading advisor to the owners and senior executives of investment management firms in the world.

CaseyQuirk by Deloitte.

The Complete Firm 2013: Competing for the 21st Century Investor 2

Introduction: A Changing, Maturing Industry

The global asset management industry remains vibrant and profitable, generating an estimated

$350 billion of revenue and more than $100 billion of earnings worldwide in 2012. The 2008

financial crisis, however, loudly marked the end of the industry’s adolescent growth spurt. Going

forward, four key changes to the operating environment will define opportunity and challenge in

the global asset management industry:

• Organic industry growth will slow, with expansion from net new flows dropping from

between 6% and 7% annually before the crisis to less than 1% for each of the next five years.

Changing investor sentiments and shifting asset allocations will define opportunity going

forward. The resulting changes in competitive dynamics will favor select products and client

segments, and transform others into turnover-driven takeaway games.

• Investors will concentrate their business with asset management firms that add value

in one of four clear ways, reflecting growing investor concern over outcomes rather than

benchmarks in an increasingly low-return environment, as well as a desire for global

portfolios less correlated to the broader market.

• Competition will become even fiercer, with a larger number of industry laggards falling

further behind a select group of successful competitors. Winners will differ in scale,

and comprise both new entrants and (some) existing market leaders, but will share a

few common characteristics related to their operating and ownership principles.

• Finally, given oversupply in the industry, asset management firms that fail to execute five

strategic initiatives will become increasingly irrelevant to investors and stakeholders.

Those that do succeed will be investment management businesses we call Complete Firms —

able to meet increasingly high client and stakeholder expectations regarding not only

investments, but also distribution and business management.

Exhibit 1

Key White Paper Sections

1 Revenue

Growth Slows

• Exogenous factors re-shape the industry

• New revenue opportunities will be targeted

2A Concentrating

Industry

• Complete Firms consolidate new revenue share

• Challenged firms increasingly less relevant

• Four primary value propositions

3 Success

Factors Evident

• Factors correlating more strongly with higher growth and/or profitability…

• …show the potential path forward

4The Complete

Firm 2013

• Five strategic initiatives for success

• The Complete Firm 2013 Checklist

• Charting the path to success

The Complete Firm 2013: Competing for the 21st Century Investor 3

Subsequent sections of this white paper will describe each of these changes in detail, outlining

how asset management firms can, and should, transform themselves into tomorrow’s market

leaders. The success principles in this paper are often extensions of concepts first introduced in

our earlier Success in Investment Management series, but reflect the fact that the operating

environment has changed dramatically in the last 10 years.

Slowing Revenue Growth

The 2008 financial crisis and its aftermath accelerated a number of secular trends that have

been dampening the industry’s long-term revenue growth.

Exhibit 2

Exogenous Pressures on Long-Term Asset Management Industry Revenue Growth

These exogenous forces are very long-term in nature and already familiar to many

readers; five of them can be summarized as follows:

1. Diverging investor and client demographics. Post-war baby boomers in major developed

markets are retiring, withdrawing their accumulated savings from pension and welfare

systems that states and corporations are increasingly unwilling to fund for younger

generations with less aggregate savings to deploy. New flows in developed markets will come

from investors who have grown up in less attractive market conditions than their baby-

boomer parents did; in emerging markets, younger investors making their first foray into

investments will drive organic growth. Both demographic trends will impact product demand.

Evolving intermediaries

Slower industryrevenuegrowth

Diverging investor/

client demographics

Low return/volatile capital

markets

Shifting product/

investment demand

New investment frameworks

The Complete Firm 2013: Competing for the 21st Century Investor 4

2. Evolving intermediaries. The number of intermediaries for asset management products and

services — retail and private banks, insurers, brokerages, and asset consultants — continues to

shrink as aftershocks from the financial crisis spur weaker players to consolidate. More

importantly, as other lines of business (such as investment banking) become less lucrative for

large global financial conglomerates, they have placed greater emphasis on operations that

generate asset-based, non-cyclical cash flows — such as distributing asset management

products and offering wealth management services. Intermediaries globally are becoming

professional buyers: more selective in the asset managers they choose to distribute, more

competitive in terms of the asset allocation advice they provide, and more expensive in terms

of revenue-sharing and retrocessions.

3. Low return/volatile capital markets. Between 1988 and 2000, fueled by bull markets in

global equities, the average global 60/40 balanced portfolio grew 10% compounded annually.

Since 2000, as interest rates tumbled to historic lows in major economies and stock markets

gyrated amid uncertain macroeconomic signals, a similar 60/40 portfolio has only appreciated

5% compounded annually, with higher volatility. The mighty tailwind that propelled industry

growth for much of its modern history is now sputtering.

4. New investment frameworks. In the emerging low-return environment, institutional

investors and professional buyers are re-examining the approach they take to strategic asset

allocation. Relative return is necessary but not sufficient; less correlated, more absolute, risk-

adjusted performance increasingly characterizes an investor’s evaluation criteria. Investors also

now design components of their portfolios around objectives such as growth or liability

management, rather than simply around asset classes such as equities and bonds. This new

perspective will continue to blur lines of demarcation between traditional and alternative

managers, as both attempt to provide the outcomes clients seek. This also means that more

complex offerings create new challenges in educating, and communicating with, investors.

5. Shifting product demands. Implementing these new investment frameworks has led many

advisors to consider hiring asset managers with different investment skills, and deploying

those capabilities within the portfolio in different ways. The changing product set will include

more passive instruments, a wider use of hedging strategies and illiquid investments, and

greater reliance on more tactical approaches to asset allocation.

The Complete Firm 2013: Competing for the 21st Century Investor 5

All five forces already have started to constrict net inflows into the global asset management

industry. In the years immediately preceding the crisis, the industry’s assets under management

grew between 6% and 7% a year organically, before accounting for market gains or losses. But

between year-end 2007 and 2011, assets expanded less than 1% from net new money, and will

grow less than 1% a year between now and 2017.

Exhibit 3

Estimated Global Asset Management Industry Net New Flows

2005

6.3%

Net

Flo

ws

as %

of B

egin

ning

AU

M

-2%

0%

2%

3%

5%

6%

8%

9%

2006 2007

6.9% 6.9%

E

Sources: Morningstar Direct, Strategic Insight, eVestment, HFR, Casey Quirk by Deloitte Global Demand Model

7%

4%

1%

-1%

2008 2009 2010 2011 2012–2017

-1.3%

0.4%1.0%

0.5% 0.6%

These five trends also have reshaped portfolios

worldwide, as investors continue to execute broad,

strategic shifts in their investment philosophies and

outlook. New money will favor more innovative

investment strategies and capabilities, while competition

within traditional asset classes will create a turnover-

driven takeaway game.

New money will favor more innovative investment strategies and capabilities, while competition within traditional asset classes will create a turnover-driven takeaway game.

The Complete Firm 2013: Competing for the 21st Century Investor 6

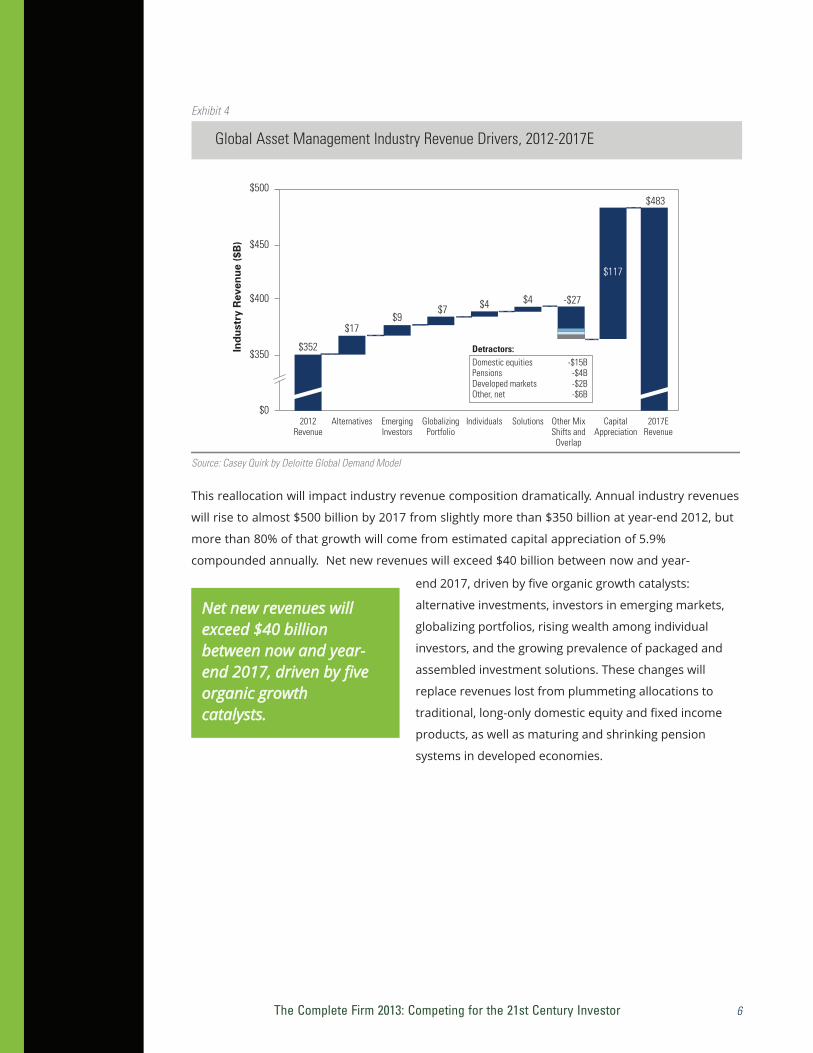

Exhibit 4

Global Asset Management Industry Revenue Drivers, 2012-2017E

Source: Casey Quirk by Deloitte Global Demand Model

2012Revenue

Indu

stry

Rev

enue

($B

)

$0

$350

$400

$450

$500

Alternatives EmergingInvestors

GlobalizingPortfolio

Individuals Solutions CapitalAppreciation

$352

$17$9

$7 $4 $4

$117

Other MixShifts andOverlap

-$27

2017ERevenue

$483

Detractors:Domestic equities -$15BPensions -$4BDeveloped markets -$2BOther, net -$6B

This reallocation will impact industry revenue composition dramatically. Annual industry revenues

will rise to almost $500 billion by 2017 from slightly more than $350 billion at year-end 2012, but

more than 80% of that growth will come from estimated capital appreciation of 5.9%

compounded annually. Net new revenues will exceed $40 billion between now and year-

end 2017, driven by five organic growth catalysts:

alternative investments, investors in emerging markets,

globalizing portfolios, rising wealth among individual

investors, and the growing prevalence of packaged and

assembled investment solutions. These changes will

replace revenues lost from plummeting allocations to

traditional, long-only domestic equity and fixed income

products, as well as maturing and shrinking pension

systems in developed economies.

Net new revenues will exceed $40 billion between now and year-end 2017, driven by five organic growth catalysts.

The Complete Firm 2013: Competing for the 21st Century Investor 7

Exhibit 5

Global Asset Management Industry Revenue Opportunity by Asset Class, 2012-2017E

2012

Global AUM 2012

Alternatives

SolutionsPassive Fixed

Passive Equity

Global Equity

Global Fixed

Local Fixed

Local Equity

($T)

15%

7%5%

10%

15%

6%

22%

20%

NetWinners37%

Global21%

Domestic42%

Global Net New Flows

Projected 2013 –2017E

Alternatives

Solutions

Passive Fixed

Passive Equity

Global/Intl Equity

Global/Intl Fl

EMD

EME

Local Other Fl

Local High Yield

Local Core/Core Plus

Local Equity

-$4 -$3 -$2 -$1 $0 $1 $2

Global Revenue Opportunity

Projected 2013 –2017E

-$50 -$0 -$50 -$100 $150

($B)■ Flows ■ Turnover

% of Total

37%

38%

25%

Note: Revenue opportunity is the sum of revenue available each year from manager turnover and net flows. Source: Casey Quirk by Deloitte Global Demand Model

1. Alternative investments. Investors increasingly regard “alternative” investments — including

unlisted securities, hedging strategies, derivatives and innovative structuring — as mainstream,

better described as the result of evolving skills in active asset management. Alternative asset

managers increasingly will compete with their long-only counterparts for larger core mandates

from institutional investors focused on reducing correlation and portfolios designed around

desired outcomes. Importantly, professional buyers will help further “democratize” alternative

and hedge fund strategies, with mass-affluent and high-net-worth investors representing most

of the growth in alternative investments assets between now and 2017.

The Complete Firm 2013: Competing for the 21st Century Investor 8

Exhibit 6

Global Alternatives AUM CAGR, 2012-2017E

Source: Casey Quirk by Deloitte Global Demand Model

7.7%

Mass Affluent Individuals

9.3%

10.2%

High-Net-Worth Individuals

Institutional

Total Industry 8.6%

2. Investors from emerging markets. Institutional and particularly individual investors in

emerging markets are the asset management industry’s newest and fastest-growing

customers, benefiting immediately from post-crisis global shifts in capital, but largely driven

by long-term demographics. Asset management marketplaces in developed economies will

remain large but fail to grow, and competitive dynamics will become more zero-sum as a

result.

The Complete Firm 2013: Competing for the 21st Century Investor 9

Exhibit 7

Global Revenue Opportunity by Region and Client Type, 2012-2017E

5-Ye

ar N

et N

ew F

low

as

% o

f Beg

inni

ng A

UM

-15%

5%

10%

15%

20%

25%

30%

35%

$0

40%

Note: DC markets broken out of institutional for U.S., Europe and Australia only. DC in other markets resides in institutional. Source: Casey Quirk by Deloitte Global Demand Model

0%

-5%

-10%

$5 $10 $15 $20 $25 $30 $35 $40 $45 $50 $55 $60 $130 $135

Latin America Indiv.

Latin America Instl.

Asia ex-Japan Instl.

Europe DC

Australia DC Middle East Indiv.

Australia Instl.

Australia Indiv.

Middle East Instl.

Japan Indiv.

Japan Instl.

Europe Instl.

Europe Indiv.

Asia ex-Japan Indiv.

N. America DC

N. America Instl.

N. America Indiv.

Manager Turnover Revenue Opportunity ($B)

●● Institutional ●● Individual ●● DC

Size of Bubble: 2013-2017Revenue Opportunity

Manager Turnover-driven Markets

Flows-driven Markets

●● = $5 billion

3. Globalizing portfolios. Institutional investors and professional buyers worldwide continue

to move toward global benchmarks and asset allocation structures, seeking to diversify

geographically to maximize appreciation and yield, as well as tap faster-growing emerging

markets as investment destinations. This shift will come at the expense of lower-fee

single-country portfolios that largely focus on domestic securities, particularly affecting

U.S. asset managers without global or international product sets.

4. Wealthy individuals. Individuals, not institutions, will drive future revenue growth. Wealth-

management clients with between $5 million and $30 million of investable assets will shape

opportunities for the next five years, as boomers remove accumulated savings from pension

plans in developed economies, estate transfers rise in frequency and size, and newly minted

entrepreneurs and business owners in developing economies sell their family businesses and

reinvest the proceeds. Four-fifths of new industry revenues between 2012 and 2017 will come

from individuals.

The Complete Firm 2013: Competing for the 21st Century Investor 10

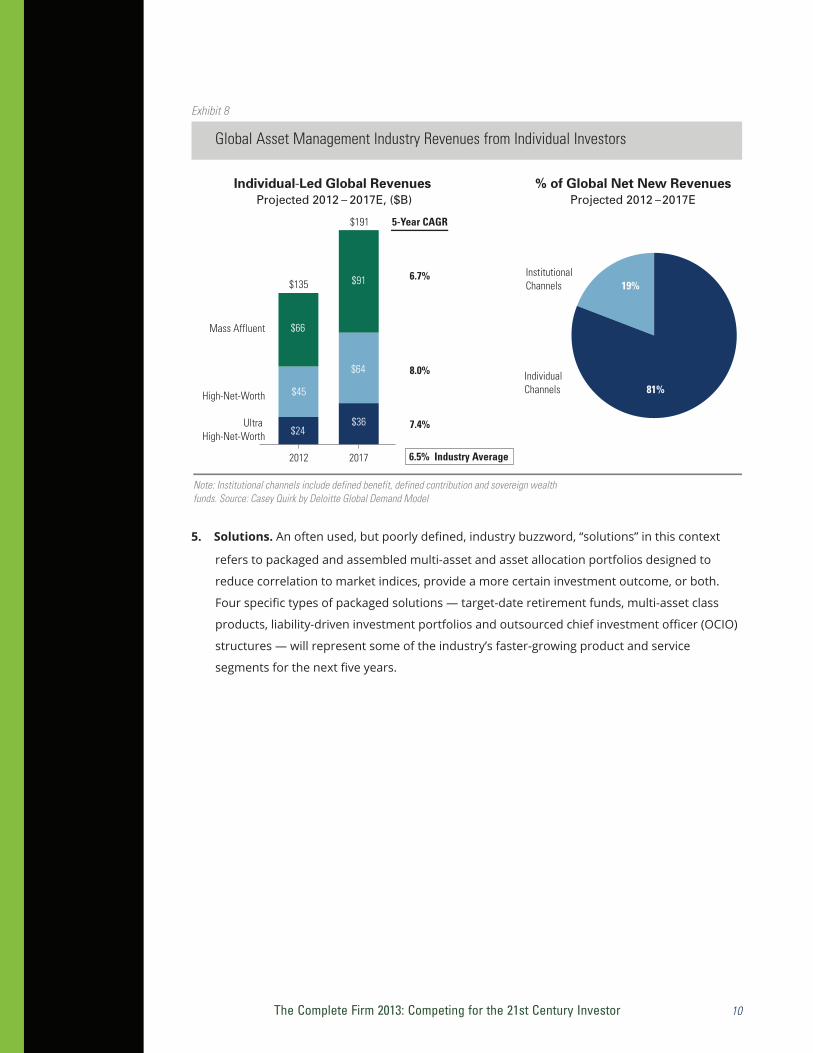

Exhibit 8

Global Asset Management Industry Revenues from Individual Investors

2012

$135

Individual-Led Global Revenues Projected 2012 – 2017E, ($B)

2017

$191

% of Global Net New Revenues Projected 2012 –2017E

Mass Affluent

High-Net-Worth

Ultra High-Net-Worth

$66

$45

$24

$91

$64

$36

5-Year CAGR

6.7%

8.0%

7.4%

6.5% Industry Average

Institutional Channels 19%

IndividualChannels 81%

Note: Institutional channels include defined benefit, defined contribution and sovereign wealth funds. Source: Casey Quirk by Deloitte Global Demand Model

5. Solutions. An often used, but poorly defined, industry buzzword, “solutions” in this context

refers to packaged and assembled multi-asset and asset allocation portfolios designed to

reduce correlation to market indices, provide a more certain investment outcome, or both.

Four specific types of packaged solutions — target-date retirement funds, multi-asset class

products, liability-driven investment portfolios and outsourced chief investment officer (OCIO)

structures — will represent some of the industry’s faster-growing product and service

segments for the next five years.

The Complete Firm 2013: Competing for the 21st Century Investor 11

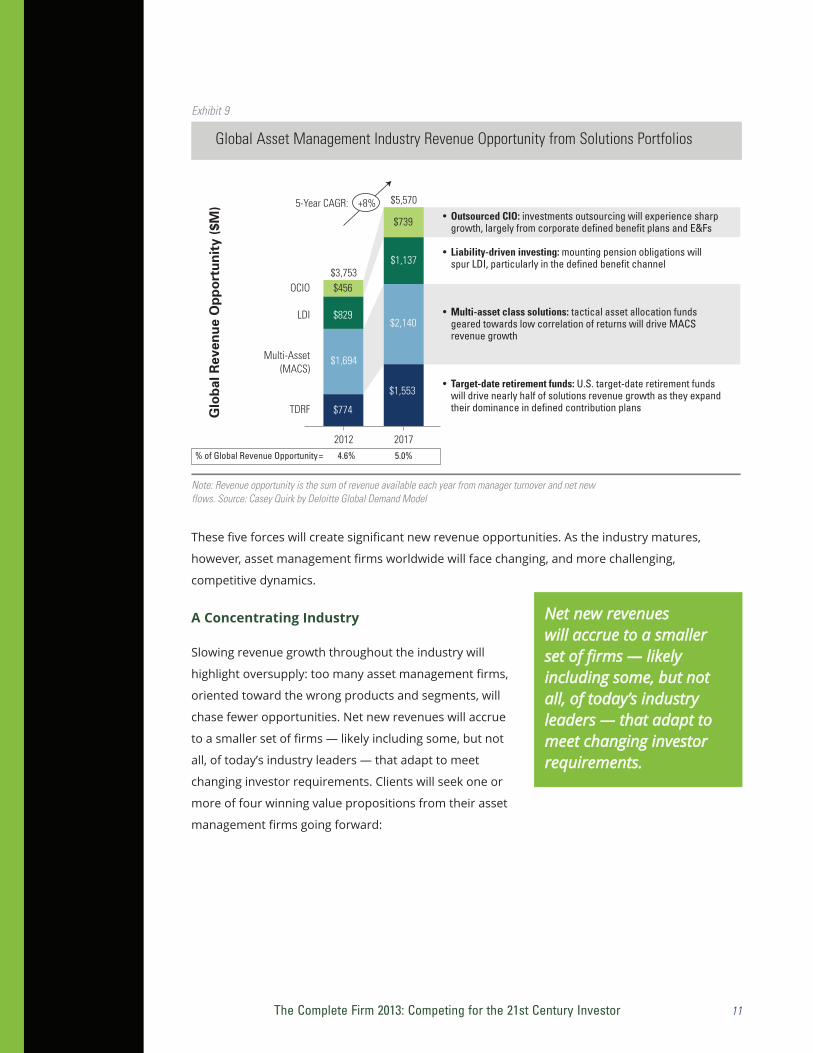

2012

$3,753

Glo

bal R

even

ue O

ppor

tuni

ty ($

M)

2017

OCIO

LDI

Multi-Asset(MACS)

TDRF

$829

$1,694

$774

$1,137

$2,140

$1,553

% of Global Revenue Opportunity= 4.6% 5.0%

$456

$739 • Outsourced CIO: investments outsourcing will experience sharp growth, largely from corporate defined benefit plans and E&Fs

• Liability-driven investing: mounting pension obligations will spur LDI, particularly in the defined benefit channel

• Multi-asset class solutions: tactical asset allocation funds geared towards low correlation of returns will drive MACS revenue growth

• Target-date retirement funds: U.S. target-date retirement fundswill drive nearly half of solutions revenue growth as they expand their dominance in defined contribution plans

$5,5705-Year CAGR: +8%

E

Note: Revenue opportunity is the sum of revenue available each year from manager turnover and net new flows. Source: Casey Quirk by Deloitte Global Demand Model

Exhibit 9

Global Asset Management Industry Revenue Opportunity from Solutions Portfolios

These five forces will create significant new revenue opportunities. As the industry matures,

however, asset management firms worldwide will face changing, and more challenging,

competitive dynamics.

A Concentrating Industry

Slowing revenue growth throughout the industry will

highlight oversupply: too many asset management firms,

oriented toward the wrong products and segments, will

chase fewer opportunities. Net new revenues will accrue

to a smaller set of firms — likely including some, but not

all, of today’s industry leaders — that adapt to meet

changing investor requirements. Clients will seek one or

more of four winning value propositions from their asset

management firms going forward:

Net new revenues will accrue to a smaller set of firms — likely including some, but not all, of today’s industry leaders — that adapt to meet changing investor requirements.

The Complete Firm 2013: Competing for the 21st Century Investor 12

Exhibit 10

Valid Value Propositions

1. High-alpha active management: offering at-scale, relatively uncorrelated, high-tracking-

error investment skills and capabilities, often designed for sheer outperformance in a low-

growth environment. Elusive, uncorrelated alpha still will attract most of a client’s fee budget

and, therefore, represents the industry’s most substantial revenue opportunity. Generating

less-correlated alpha increasingly requires investment skills that support more complex

portfolios (i.e., less liquid, global, with multiple legal, tax and accounting dimensions), favoring

the continued growth of alternative investments. The size of the opportunity for strong long-

only liquid portfolio providers remains vast for those asset management firms that can

provide sustainable returns.

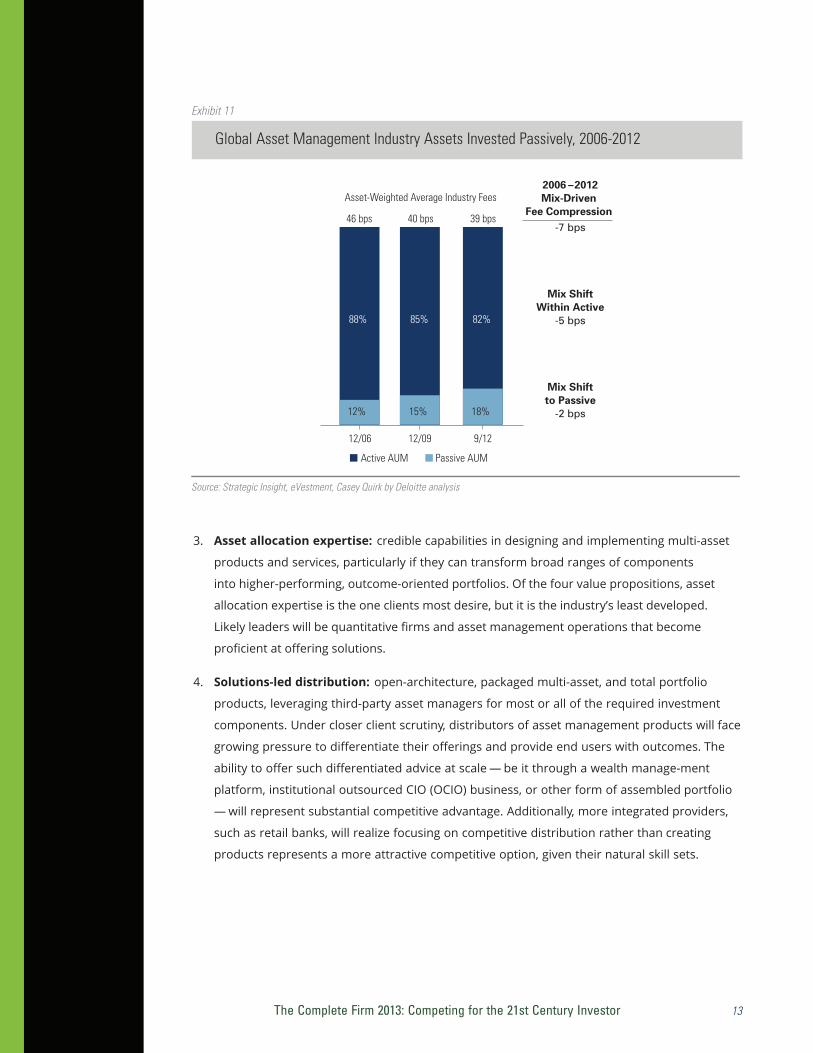

2. Cost-efficient beta: benchmark returns at competitive fees and/or within innovative

packaging, such as exchange-traded funds (ETFs). ETF proliferation underscores the true cost

of beta, which makes the market for index returns highly efficient, favoring scale players able

to maximize their operating leverage. In the six years since December 2006, investors have

raised their exposure to passive portfolios and ETFs to 18% from 12%, helping to spur a 15%

compression in long-only fees within the global asset management industry.

1 High-Alpha

Active Management

At-scale provider of relatively uncorrelated, high-tracking-error equity, or fixed income products, and/or alternatives capabilities

Undifferentiatedactive managers

ValueProposition

Definition

ChallengedFirms

2 Cost-Efficient

Beta

At-scale provider of ETF or index products at competitive fees

Expensive beta

3 Asset

Allocation Expertise

Credible manufacturer of multi-asset class products and services (e.g., MACS, LDI, TDRF, OCIO)

Siloed capabilities

4 Solutions-Led Distributors

Firm specializing in distributing open-architecture multi-asset class products, allocation products, and allocation services (limited to no manufacturing)

Undifferentiated distributors

The Complete Firm 2013: Competing for the 21st Century Investor 13

Exhibit 11

Global Asset Management Industry Assets Invested Passively, 2006-2012

3. Asset allocation expertise: credible capabilities in designing and implementing multi-asset

products and services, particularly if they can transform broad ranges of components

into higher-performing, outcome-oriented portfolios. Of the four value propositions, asset

allocation expertise is the one clients most desire, but it is the industry’s least developed.

Likely leaders will be quantitative firms and asset management operations that become

proficient at offering solutions.

4. Solutions-led distribution: open-architecture, packaged multi-asset, and total portfolio

products, leveraging third-party asset managers for most or all of the required investment

components. Under closer client scrutiny, distributors of asset management products will face

growing pressure to differentiate their offerings and provide end users with outcomes. The

ability to offer such differentiated advice at scale — be it through a wealth manage-ment

platform, institutional outsourced CIO (OCIO) business, or other form of assembled portfolio

— will represent substantial competitive advantage. Additionally, more integrated providers,

such as retail banks, will realize focusing on competitive distribution rather than creating

products represents a more attractive competitive option, given their natural skill sets.

Source: Strategic Insight, eVestment, Casey Quirk by Deloitte analysis

12/06

46 bps

12/09 9/12

40 bps 39 bps

■ Active AUM ■ Passive AUM

2006 –2012Mix-Driven

Fee Compression -7 bps

Mix ShiftWithin Active

-5 bps

Mix Shiftto Passive

-2 bps

88% 85% 82%

12% 15% 18%

Asset-Weighted Average Industry Fees

The Complete Firm 2013: Competing for the 21st Century Investor 14

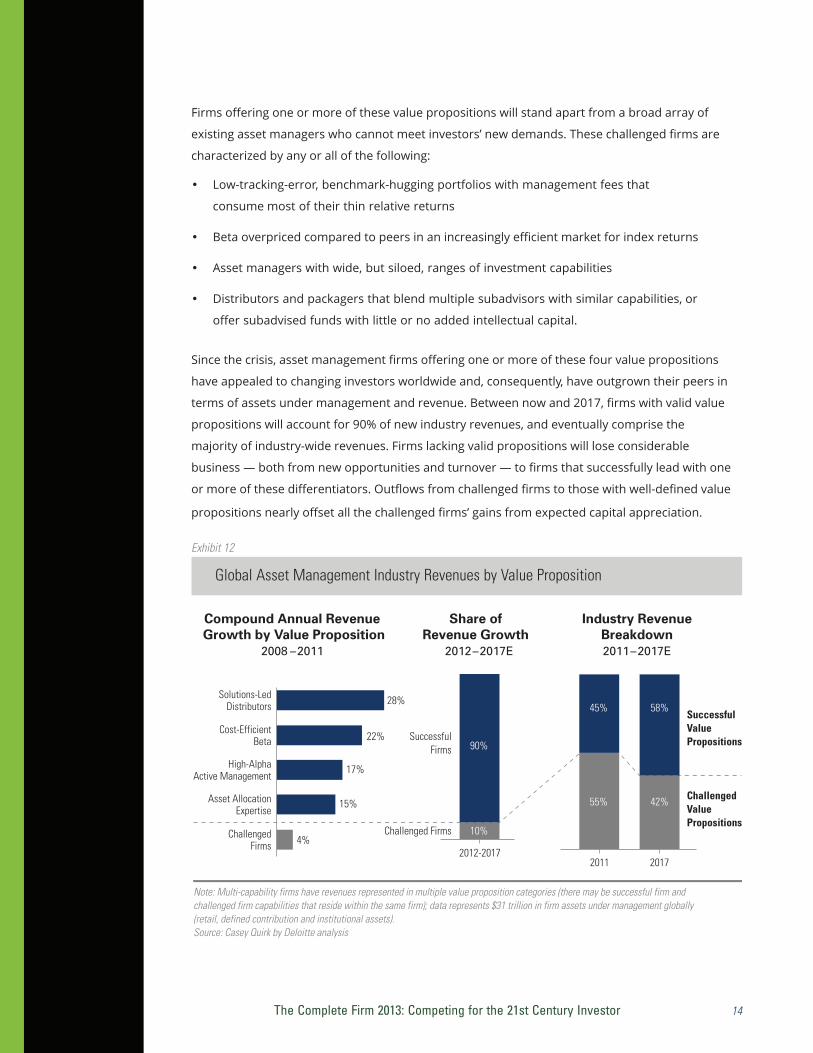

Firms offering one or more of these value propositions will stand apart from a broad array of

existing asset managers who cannot meet investors’ new demands. These challenged firms are

characterized by any or all of the following:

• Low-tracking-error, benchmark-hugging portfolios with management fees that

consume most of their thin relative returns

• Beta overpriced compared to peers in an increasingly efficient market for index returns

• Asset managers with wide, but siloed, ranges of investment capabilities

• Distributors and packagers that blend multiple subadvisors with similar capabilities, or

offer subadvised funds with little or no added intellectual capital.

Since the crisis, asset management firms offering one or more of these four value propositions

have appealed to changing investors worldwide and, consequently, have outgrown their peers in

terms of assets under management and revenue. Between now and 2017, firms with valid value

propositions will account for 90% of new industry revenues, and eventually comprise the

majority of industry-wide revenues. Firms lacking valid propositions will lose considerable

business — both from new opportunities and turnover — to firms that successfully lead with one

or more of these differentiators. Outflows from challenged firms to those with well-defined value

propositions nearly offset all the challenged firms’ gains from expected capital appreciation.

Exhibit 12

Global Asset Management Industry Revenues by Value Proposition

4%

2011

Compound Annual Revenue Growth by Value Proposition

2008 –2011

2017

Industry Revenue Breakdown 2011–2017E

45%

55%

58%

42%

SuccessfulValue Propositions

ChallengedValue Propositions

Note: Multi-capability firms have revenues represented in multiple value proposition categories (there may be successful firm and challenged firm capabilities that reside within the same firm); data represents $31 trillion in firm assets under management globally (retail, defined contribution and institutional assets).Source: Casey Quirk by Deloitte analysis

Share of Revenue Growth

2012–2017E

Solutions-LedDistributors

Cost-EfficientBeta

High-AlphaActive Management

Asset AllocationExpertise

ChallengedFirms

2012-2017

SuccessfulFirms

Challenged Firms

90%

10%

28%

22%

17%

15%

The Complete Firm 2013: Competing for the 21st Century Investor 15

Industry economics will consolidate around skill, not

necessarily scale, going forward. In fact, smaller, younger

firms, built solely around valid value propositions, will

eclipse some current industry leaders hobbled by large,

legacy books of business centered on outmoded products

and less attractive client segments. More importantly, only

a subset of the industry’s firms will have the operating

model elements required to successfully support one, or

several, valid value propositions going forward.

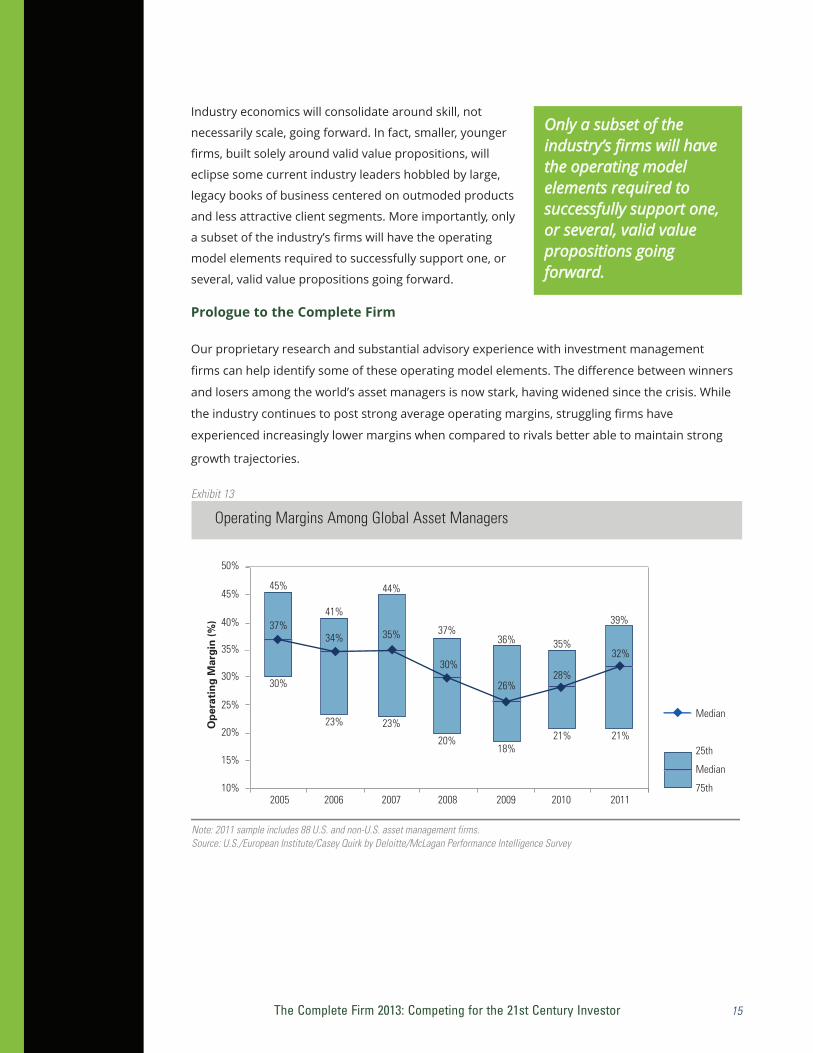

Prologue to the Complete Firm

Our proprietary research and substantial advisory experience with investment management

firms can help identify some of these operating model elements. The difference between winners

and losers among the world’s asset managers is now stark, having widened since the crisis. While

the industry continues to post strong average operating margins, struggling firms have

experienced increasingly lower margins when compared to rivals better able to maintain strong

growth trajectories.

Exhibit 13

Operating Margins Among Global Asset Managers

Only a subset of the industry’s firms will have the operating model elements required to successfully support one, or several, valid value propositions going forward.

45%

Ope

rati

ng M

argi

n (%

)

10%

15%

20%

25%

30%

35%

40%

45%

50%

Note: 2011 sample includes 88 U.S. and non-U.S. asset management firms. Source: U.S./European Institute/Casey Quirk by Deloitte/McLagan Performance Intelligence Survey

2005 2006 2007 2008 2009 2010 2011

41%

44%

37%36% 35%

39%

30%

23% 23%

20%18%

21% 21%

◆◆ ◆

◆

◆◆

◆

37%34% 35%

30%

26%28%

32%

Median

25th

Median

75th

◆

The Complete Firm 2013: Competing for the 21st Century Investor 16

Successful asset management firms share five key ingredients, success factors that we believe are

likely to persist going forward, and form the foundation for the prescriptive framework that

follows. They are:

Factor 1: Investment brand strength. In a relative-return meritocracy, brand matters less;

in the more complicated world of the future, it may matter more, as investors begin to look

toward products in development, rather than products on the shelf. Firms with greater

perceived than actual performance secured a sizable amount of business from U.S.

institutional investors. These firms grew just as fast as firms that actually offered competitive

performance — but lacked the perception of doing so. Additionally, brand will play a key role

in attracting business from individual investors, which (as described earlier) represent most

of the industry’s revenue opportunity for the next five years.

Exhibit 14

Impact of Performance and Investments Brand on Growth, U.S. Institutional Marketplace

Factor 2: Appropriate sales staffing. The previous conventional wisdom held that sales

productivity — i.e., the same person selling more business — drove top-line growth, implying

asset management was a highly scalable business. Successful firms, however, realized that

more complicated client needs and the need to tap more labor-intensive revenue

opportunities meant manpower would provide a critical advantage. Since the crisis, firms with

large numbers of salespeople have substantially outgrown rivals with smaller distribution

groups, and even outpaced the growth of highly efficient sales and marketing organizations.

10%

20%

35%

% of Firms Performance Avg. 3-Year Flows as % of BoP AUM

Note: Perceived performance based on survey of 600 U.S. institutional investors asked to rate 36 managers on investment performance. Actual performance calculated as % of AUM in top 30% ranked products and weighted as a blend of 1-, 3,- and 5-year peer group % rank (25%, 60%, 15%) for the three-year period ended 6/30/12. Sources: Cogent Research, eVestment, Pensions & Investments, Casey Quirk by Deloitte analysis

-5%

87%

45%

43%

35%

StarPerformers

InvestmentSpecialists

StrongBrand

UnderPerformers

Perceived

High

Low

High

Low

Actual

High

High

Low

Low

% GroupFlows

23%

38%

46%

-7%

100%

The Complete Firm 2013: Competing for the 21st Century Investor 17

Exhibit 15

Average Annual AUM Growth Rate by Key Efficiency Ratios, 2009-2011

Factor 3: Proper incentives. Franchise-value currency reflecting the asset

management organization, not any parent bank or insurer, has been a success factor

across multiple samples and timeframes. Firms that award equity, either real or

synthetic, in asset management operations handily outgrow competitors.

BottomQuartile

1.2%

Avg

AU

M G

row

th (%

)

By Sales Staffing Sales Professionals % of Total Front O�ce

0%

1%

2%

3%

4%

5%

6%

7%

Middle 50% TopQuartile

3.0%

6.1%

BottomQuartile

3.1%

Avg

AU

M G

row

th (%

)

By Sales Productivity Gross Sales/Sales Professionals

0%

1%

2%

3%

4%

5%

6%

7%

Middle 50% TopQuartile

4.3% 4.3%

Source: U.S./European Institute/Casey Quirk by Deloitte/McLagan Performance Intelligence

The Complete Firm 2013: Competing for the 21st Century Investor 18

Exhibit 16

Median AUM CAGR by Incentive Scheme Format, 2001-2011

Factor 4: A global platform. Firms gathering more than one-third of their client assets from

outside their home region grow much faster than single-region counterparts. Perhaps more

importantly, in recent years these fully globalized firms have posted higher profit margins than

their less global counterparts, as long-term investments in business infrastructure begin to

bear fruit. Many asset management firms have relied on existing operating leverage in their

globalization efforts. Those with broad foreign client bases, however, have built a sustainable,

profitable business over time by investing in the regional products and distribution support

that allow them to compete more effectively with local competitors.

Note: Based on 125 firms with outside owners and over $10B in AUM. AUM excludes cash and liquidity products. Manager-Level Equity: Firms with equity programs in the asset management firm.Parent-Level Equity: Firms with an equity program– typically at the owner level–but no equity in the asset management firm. Long-Term (no equity): Firms with long-term incentives (i.e., deferred comp or profit-sharing) and no equity program.Short-Term: Firms with no long-term incentive programs.Sources: eVestment, Casey Quirk by Deloitte analysis

8.1%

Manager-Level Equity

8.4%

10.7%

Parent-Level Equity

Long-Term (no equity)

Short-Term 6.2%

0% 2% 4% 6% 8% 10% 12%

The Complete Firm 2013: Competing for the 21st Century Investor 19

Exhibit 17

Key Metrics of Asset Management Firms by Proportion of Foreign Clients

Factor 5: Operating autonomy. The crisis has emphasized the competitive advantages

of pure-play asset managers, over the partially or fully owned subsidiaries of larger

financial institutions. They can offer the more competitive incentives described earlier and,

consequently, appeal to professional buyers. Data show that subsidiary asset managers

can overcome these challenges, but only with innovative compensation systems coupled

with empowered enterprise-wide leadership.

Regional<5%

foreign-client AUM

–1.3%

Rev

enue

on

Net

New

Flo

ws

(% o

f Beg

inni

ng)

Revenue on Net New Flows 2007 through 2011

-5%

0%

5%

10%

15%

20%

25%

30%

Partially Global5-33% foreign-

client AUM

Fully Global>33%

foreign-client AUM

2.3%

25.2%

Regional<5%

foreign-client AUM

28.9%

Ope

rati

ng M

argi

n (%

)

Operating Margins As of 2011

Partially Global5-33% foreign-

client AUM

Fully Global>33%

foreign-client AUM

32.3%

37.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Sources: eVestment, Casey Quirk by Deloitte analysis

The Complete Firm 2013: Competing for the 21st Century Investor 20

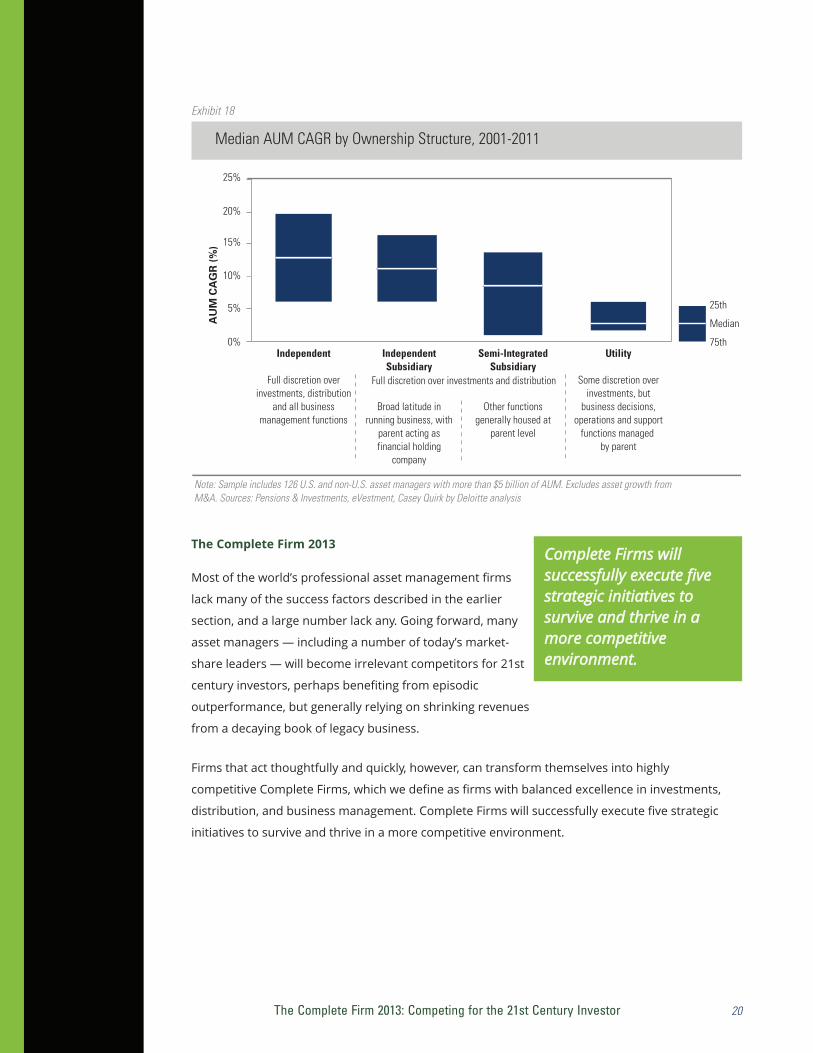

Exhibit 18

Median AUM CAGR by Ownership Structure, 2001-2011

The Complete Firm 2013

Most of the world’s professional asset management firms

lack many of the success factors described in the earlier

section, and a large number lack any. Going forward, many

asset managers — including a number of today’s market-

share leaders — will become irrelevant competitors for 21st

century investors, perhaps benefiting from episodic

outperformance, but generally relying on shrinking revenues

from a decaying book of legacy business.

Firms that act thoughtfully and quickly, however, can transform themselves into highly

competitive Complete Firms, which we define as firms with balanced excellence in investments,

distribution, and business management. Complete Firms will successfully execute five strategic

initiatives to survive and thrive in a more competitive environment.

Complete Firms will successfully execute five strategic initiatives to survive and thrive in a more competitive environment.

AU

M C

AG

R (%

)

0%

5%

10%

15%

20%

25%

Note: Sample includes 126 U.S. and non-U.S. asset managers with more than $5 billion of AUM. Excludes asset growth from M&A. Sources: Pensions & Investments, eVestment, Casey Quirk by Deloitte analysis

Independent

Full discretion overinvestments, distribution

and all businessmanagement functions

25th

Median

75thIndependentSubsidiary

Broad latitude inrunning business, with

parent acting asfinancial holding

company

Semi-IntegratedSubsidiary

Other functionsgenerally housed at

parent level

Utility

Some discretion overinvestments, but

business decisions,operations and support

functions managed by parent

Full discretion over investments and distribution

The Complete Firm 2013: Competing for the 21st Century Investor 21

Exhibit 19

Strategic Initiatives to Create the Complete Firm

Initiative 1: Deliver investments leadership in a “difficult to differentiate” environment.

As professional buyers become more influential, they will use outcomes and absolute

performance, rather than return relative to benchmarks, to evaluate asset management firms.

Additionally, volatile capital markets will render past performance even less relevant in

manager selection. Investors and their intermediaries will favor investment firms that can

support their performance records with four elements of “investments leadership”:

• Credible, market-leading investment capabilities, highly differentiated from those

offered by rivals and supported by a compelling philosophy, evidence of the ability to

perform, and strong teams. Firms meeting best practices standards in this area will

rigorously test and continuously validate their value

proposition in the market to ensure they meet

market-leading status versus their competitors.

• A strong investments quality brand, which

emphasizes that success is repeatable and

sustainable. Best practices for building such

a brand include regularly benchmarking

investment processes to ensure they still resonate

with professional buyers, as well as creating

positioning and marketing strategies that are market-tested.

Investments leadership A brand built on a clear investment philosophy supported by well-articulated process, macroeconomic worldview, and innovative thought leadership

Well-led and organizedsales and marketing

Properly resourced, organized and led sales and marketing that alignscapabilities effectively with market demand

Technically skilled client interface

Client-facing officers proficient with portfolios, investments, and assetallocation to support persistent, multiproduct relationships

Ability to competefor talent

Well-designed incentive programs that attract, retain, and motivate talent

Clear governance andownership

Relative autonomy for investment operations, balanced with a clear growthstrategy and a plan for multi-generational succession planning

1

2

3

4

5

Investors and their intermediaries will favor investment firms that can support their performance records with four elements of“investments leadership”

The Complete Firm 2013: Competing for the 21st Century Investor 22

• Innovative thought leadership, capably delivered to institutional investors and

intermediaries for individuals. Professional buyers will favor asset managers that provide

intellectual capital supporting portfolio strategy and development, rather than simply

products. Firms focused on best practices build internal thought leadership creation and

delivery processes that support a steady, regular output of ideas and help for investors.

• Capacity management and rationing that ensures performance objectives are met and

favors strategic client relationships. Too many active managers today do not fully

understand their capacity limitations and have not developed a clear approach to

addressing the issue. Best practices firms will develop clear strategies regarding capacity,

including a thoughtful analysis of limits, clear messages to clients and prospects regarding

their approach, and asset-gathering strategies that support sustainable firm-level

profitability.

Exhibit 20

Complete Firm Checklist #1: Investments Leadership

Initiative 2: Organize well-led and resourced sales/marketing efforts that foster growth.

Increasingly, there will be fewer new flows for which an overcrowded asset management

industry can compete. Consequently, successful asset-gathering — driven by quality sales and

marketing — must focus efforts on the best revenue opportunities going forward, rather than

cover legacy clients and product sets that no longer represent growth. Sales and marketing

organizations of successful asset managers will have the following elements:

• A thoughtful, market-driven distribution strategy that rigorously identifies and

prioritizes target client segments and distribution channels, focusing resources and

efforts where opportunities are greater and the firm enjoys a competitive advantage.

Best practices include developing a multi-year new business growth plan that properly

identifies and sequences the pursuit of key revenue opportunities worldwide.

Furthermore, successful firms will take extra measures to fully understand client priorities

and adapt their engagement models to deepen relationships.

Investments Leadership

❏ Credible, market-leading investment capabilities

❏ Ability to articulate competitive advantagein investments

❏ Innovative thought leadership

❏ Capacity rationing

The Complete Firm 2013: Competing for the 21st Century Investor 23

• Strong, experienced, empowered sales

leadership. Winning asset management firms

will seek and retain aggressive distribution

leaders that prioritize growth. These leaders will

implement clear positioning strategies based on

well-researched views regarding future market

opportunities. Successful sales leaders will

actively drive product and service innovation, and

build strong sales and relationship functions. Best

practices firms will empower and appropriately

incentivize their sales leadership teams. Experienced

leaders will prioritize opportunities and objectives

to match long-term strategic goals.

• A distribution organization appropriate in size and quality to the firm’s growth

ambitions, and structured to best support the firm’s competitive advantages. Many

of today’s firms maintain sales organizations that either lack the appropriate size to

effectively compete, deploy their resources without appropriate regard to the best

future opportunities, or both. Best practices asset management firms thoughtfully tier

their clients and prospects, model their sales and servicing coverage ratios, and build their

organizations accordingly.

• Demand-driven product development that balances input from a firm’s investment

and distribution organizations. Asset management firms no longer have the luxury,

in time or cost, of developing products no one will buy. Best practices will include

developing rigorous product-lifecycle management, including unflinching product

rationalization processes.

Exhibit 21

Complete Firm Checklist #2: Well-Led and Organized Sales and Marketing

Well-Led and Organized Sales and Marketing

❏ Market-driven global distribution strategy

❏ Strong, experienced, empowered sales leadership

❏ Distribution organization of appropriate sizeand quality

❏ Demand-driven product development

Successful asset-gathering — driven by quality sales and marketing — must focus efforts on the best revenue opportunities going forward, rather than cover legacy clients and product sets that no longer represent growth.

The Complete Firm 2013: Competing for the 21st Century Investor 24

Initiative 3: Build a technically skilled client interface for client cultivation and retention. Competitive client service, historically a critical differentiator among asset

management firms, will be essential going forward. In the new operating environment,

however, firms with an ability to bring investment and technical expertise closer to the client

will enjoy an outsized advantage over their peers who do not. Firms with client-facing officers

that can engage proactively with clients regarding their entire portfolio will have a significant

competitive advantage in retaining clients for the long term, as well as growing firm

relationships. Successful asset management businesses will support technically proficient

client interfaces with the following elements:

• A clearly articulated client relations strategy

designed to add value, not simply serve

administrative requirements. Complete Firms

view client service as an ongoing relationship

development function, imparting technical

content and intellectual capital, often based on a

total-portfolio perspective, from their investment

professionals to the client. This additional advice

can create a form of “distribution alpha” that

strengthens the overall relationship by finding

additional ways to improve outcomes. It also brands the firm as one of a limited number

of trusted advisors to which investors gravitate amid more challenging capital markets.

Best practices firms will develop a strategy that clearly articulates the value added to the client

from client relations.

• Well-defined client relations roles that clearly outline the responsibilities and

required expertise for client-facing officers, articulating their added value to the client.

As client-facing organizations become a central differentiator for leading firms, roles will

increasingly require technical skill sets that typically have not resided at scale within this

part of the organization. Best practices firms will develop clear and detailed role profiles

with optimal desired professional skill sets, as well as networks within the best pools of such

talent , to execute successfully on building their team.

• Appropriate technical and relationship talent balance. Many of today’s firms

find themselves out-of-balance in their client relations function, often long on

relationship/administrative skills and short on technical expertise. Best practices

firms will center on ensuring an appropriate mix of investment specialists among client

relations teams and will build clear client engagement processes that optimize the use

of relationship managers and investment specialists.

The new operating environment, however, firms with an ability to bring investment and technical expertise closer to the client will enjoy an outsized advantage.

The Complete Firm 2013: Competing for the 21st Century Investor 25

Initiative 4: Implement incentives that aggressively attract and retain talent. As

demonstrated in the previous section, the structure, duration, and currency of incentive

compensation is highly correlated to success in

investment management. Extending competitive

incentives across multiple functions and seniority

levels within an asset management firm reduces

personnel turnover and prioritizes value-creating

behavior, which attracts professional buyers and

raises revenues. Competitive incentive compensation

schemes vary widely, but tend to share these

common denominators:

• Performance metrics talent can directly influence.

This is a standard characteristic among any firm successfully motivating human capital;

people work best when they strive to achieve goals directly related to their job and clearly

align with the firm’s stated objectives. Best practices involve regularly benchmarking

compensation schemes to ensure that they are not only competitive, but also link to

proper metrics at the individual, team, and firm levels.

• Alignment with asset management P&L and strategy. Asset management markedly

differs from banking, insurance or capital markets. Financial conglomerates that provide

the bulk of incentive compensation in shares of their overall enterprise — rather than a

stake in the usually more valuable, in terms of multiples, asset management operation —

tend to lose key people. Additionally, incentives are powerful tools with which to shape

strategic direction. Best practices firms develop incentives linked tightly with asset

management’s results and long-term strategic goals.

Exhibit 22

Complete Firm Checklist #3: Technically Skilled Client Interface

The duration and currency of incentive compensation is highly correlated to success in investment management.

Technically Skilled Client Interface

❏ Clearly articulated client relations strategydesigned to add value

❏ Well-defined client service roles

❏ Proper servicing models balancing technical and relationship talent

The Complete Firm 2013: Competing for the 21st Century Investor 26

• A clear path to employee participation in franchise value. Executives among successful

investment management firms accrue most of their long-term net worth through their

stake in their asset management operation’s franchise value, regardless of whether the

currency is true ownership or an instrument that replicates equity. Best practices firms

employ equity schemes that are meaningful and will use creative currencies (real equity,

phantom equity, option-like, and deferred compensation) as necessary.

• Long-term incentives. Professional buyers prize tenure among investment, distribution

and business management executives at asset management firms. Many firms today rely

far too heavily on near-term incentives and, as a result, risk the loss of critical

professionals. Best practices firms will employ compensation systems that significantly

weight long-term incentives within their overall scheme to better ensure personnel stability.

Exhibit 23

Complete Firm Checklist #4: Ability to Compete for Talent

Initiative 5: Institute governance and ownership practices that support long-term

dynamism. Asset management is no longer a simple business. Institutionalizing success —

trapping the lightning in the bottle — is difficult, particularly as firms change ownership,

either organically through generational succession, or inorganically through a transaction. In

the long term, thoughtful consideration of ongoing governance and ownership ideals will

separate competitive asset managers from firms that founder during a transfer of

leadership. Well-tested governance and ownership principles among successful investment

manage-ment firms include the following:

• Strong, empowered, and experienced business leadership. Asset management

operations function best when run as commercial operations, not utilities for broader

Ability to Compete for Talent

❏ Performance metrics talent can directly influence

❏ Aligned with asset management P&L and strategy

❏ Clear path to employee participation infranchise value

❏ Long-term incentives

The Complete Firm 2013: Competing for the 21st Century Investor 27

financial services offers. Best practices involve

hiring dedicated people with appropriate industry

experience managing and leading a strong

asset management firm and empowering the

leadership to effect serious change and

continuously improve the business.

• Ability to execute on asset managementindustry best practices, not simply those of the

parent bank or insurer. Professional buyers

rightfully shun subsidiary asset managers where

an ownercan influence or compromise decisions

that may be in the best interest of the asset management operation, particularly given

its fiduciary obligations to clients. A critical best practice for good owners of asset

management firms is understanding the key principles of success in asset management

(which often differ dramatically from an owner’s core business) and then allowing

leadership the ability to execute on those practices.

• Accountability for value creation. While it is critical for asset management leadership

to be empowered to implement industry best practices, it is similarly critical for owners to

agree to clear goals with leadership and then hold executives accountable for results.

Structuring the economic relationship between shareholders and the asset manager’s

executive leadership is a critical part of this exercise. Best practices asset management

firm owners hire strong executive teams, grant autonomy, set clear financial and growth

goals, and hold leadership accountable to meet those goals.

• Clarity regarding generational transition. This is the most underrated element of clear

governance and ownership. Few investment management firms find ways to smoothly

transition ownership between generations because they begin too late. The more

desperately founders need liquidity, the greater the chances of agreeing to a poorly

designed transaction that encourages personnel turnover and destroys long-term value.

A well-designed succession plan centered on a funding mechanism — often involving

permanent, patient capital — that helps younger executives buy out older ones separates

Complete Firms from their less competitive rivals. In private partnership situations,

continuously recycling equity or dynamic recapitalization is a time-tested industry

best practice.

Thoughtful consideration of on-going governance and ownership ideals will separate competitive asset managers from firms that founder during a transfer of leadership.

The Complete Firm 2013: Competing for the 21st Century Investor 28

Exhibit 24

Complete Firm Checklist #5: Clear Governance and Ownership

Creating a strategic plan and business model that supports execution of these five initiatives will

separate winners from losers in the asset management industry of the next decade. Complete

Firms likely will comprise a variety of different, innovative business models. A number of existing

asset management businesses in particular, however, will struggle to transform themselves into

successful competitors without strong, proactive leadership armed with a blueprint for reform:

• Bank-owned asset management firms, which will need to reconcile the perceived

constraints of a bank (such as cultural aversion to autonomy, inability to implement effective

asset management-focused incentives, and heightened regulation) with success requirements

—and higher multiples — of a successful asset management subsidiary. Transformation will

require innovative incentive schemes and a clear decision, shared at multiple levels of

management, about whether the group’s primary function in asset management is

manufacturing, distribution, or both. Some banks will choose to address the success

requirements head-on, and some will exit the business altogether, either via a proactive

exit or through client attrition.

Clear Governance and Ownership

❏ Strong, empowered, experienced businessleadership

❏ Executives that promote asset managementbest practices

❏ Accountability for value creation

❏ Clarity regarding succession transition

The Complete Firm 2013: Competing for the 21st Century Investor 29

• Multi-affiliates — firms built through serial acquisition of smaller, often specialist, asset

managers — have unique challenges. The inorganic growth that buoyed many during the

industry’s heyday is gone, thanks to less M&A activity among asset management firms.

Additionally, the markets and products in favor require multi-asset cooperation and central

distribution, functions with which multi-affiliates struggle to reach consensus among their

stakeholders and, therefore, often trail rivals in terms of efficiency. Many multi-affiliates today

lag the growth and financial performance of the industry at large. The majority of those firms

are stuck with muddled operating models that are neither financial holding companies nor

integrated asset managers. Multi-affiliates can become Complete Firms by clarifying their

governance and operating model, as well as conducting a disciplined review of their affiliate

portfolio, to ensure all their capabilities are truly competitive. For some, this will entail

integrating and rationalizing firms, while working to put substantial quality improvements into

place. For others, it will entail creating more autonomous accountable affiliates on the one

hand and exiting other affiliates, on the other.

• First-generation partnerships benefit from employee ownership and focused governance,

until their founders either seek an exit or are no longer effective for clients. Many of

these partnerships never reach a second generation because the founders fail to begin a

generational transition plan far enough in advance and build no mechanisms to thoughtfully

make the transition. Partnerships that create generational transition plans and introduce

dynamic recapitalization systems to transfer ownership deliberately over time, often via their

annual compensation process, will create real franchise value and have a much higher

chance of enjoying a multi-generational existence.

• Finally, the most challenged firms may be undifferentiated active managers, who provide

their clients with beta-like returns at alpha-like prices. Even implementing all five strategic

initiatives described in this section will not be enough if an asset manager cannot credibly

provide clients with any of the four value propositions described at the heart of this

white paper. Reform for challenged players must be revolutionary and involve substantial

transfusions of talent and product, likely resulting in significant changes to operating

platforms and business models.

The Complete Firm 2013: Competing for the 21st Century Investor 30

Conclusion

In as soon as five years, league tables of industry leaders

already will look different. Most large firms today, saddled

with the costs of serving slower-growing legacy client

segments and unable to redirect resources toward newer,

better opportunities, will struggle to maintain their

historical growth trajectories. Many will shrink, losing

business to newer entrants that have custom-built their

operating model for this new, less forgiving, environment.

Some of today’s leaders, however, can survive these

changes and improve revenues and earnings substantially, augmenting their existing competitive

advantages with new ones. Becoming a Complete Firm will involve rapid, and deep, business

transformation, driven by enlightened business leaders and supported by a thoughtful, strategic

approach to change management. Each firm will pursue its own definition of boldness, but speed

(not haste) will be a critical differentiator. Complete Firms will set the standard for success in

investment management.

Becoming a Complete Firm will involve rapid, and deep, business transformation, driven by enlightened business leaders and supported by a thoughtful, strategic approach to change management.

The Complete Firm 2013: Competing for the 21st Century Investor

Jeffrey A. [email protected] +1 203 899 3035

Kevin P. [email protected] +1 203 899 3033

Benjamin F. Phillips Investment Management Lead Strategist - Consulting New [email protected] US +1 347 269 1324

Kevin P. Quirk, PrincipalYariv Itah, Casey Quirk Global Practice LeaderDaniel Celeghin, Head of Wealth Management Strategy Asia-PacificGrace Cicero, Chief of StaffJeb B. Doggett, DirectorJonathan L. Doolan, PrincipalJeffrey A. Levi, PrincipalBenjamin F. Phillips, Investment Management Lead Strategist - ConsultingJeffrey B. Stakel, PrincipalJustin R. White, Principal

Casey Quirk by Deloitte helps clients develop broad business growth strategies, improve investment/product appeal and growth prospects, evaluate new market and product opportunities, and enhance incentive alignment structures. Our unparalleled industry knowledge and experience, detailed proprietary data, and global network of relationships make Casey Quirk by Deloitte a leading advisor to the owners and senior executives of investment management firms in the world.

To discuss this white paper, please contact:

This publication contains general information only and none of the member firms of Deloitte Touche Tohmatsu Limited or their respective related entities is, by means of this publication, rendering business, financial, investment, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. None of the member firms of Deloitte Touche Tohmatsu Limited or their respective related entities shall be responsible for any loss sustained by any person who relies on this publication.

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2016 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited

Supporting Team: Michael D. Chia, Jacob F. Walker, Dan Neeman, Sheryle D. Wells

CaseyQuirk by Deloitte.