Embed Size (px)

Citation preview

Journal of Economic LiteratureVol XLIII (June 2005) pp 437ndash479

Complementarities and Games New Developments

XAVIER VIVESlowast

437

lowast Vives INSEAD and ICREA-UPF I am grateful toTim Van Zandt two anonymous referees and the editorfor very helpful comments and to INSEAD for financialsupport

1 Introduction

Complementarities are pervasive in eco-nomics ranging from coordination

problems in macroeconomics and financeto pricing and product selection issues inindustrial organization At the heart ofcomplementarity is the notion due toEdgeworth that the marginal value of anaction or variable increases in the level ofanother action or variable

Complementarities have been a recurrentand somewhat contentious topic of study foreconomic analysis Indeed while Paul ASamuelson (1947) in his Foundations statedthat ldquoIn my opinion the problem of comple-mentarity has received more attention thanis merited by its intrinsic importancerdquo (at thestart of the section on complementarity p183 1979 edition) he later corrected himselfin this very journal in 1974 on the occasionof the fortieth anniversary of the HicksndashAllenrevolution in demand theory when he statedat the very beginning of his paper that

The time is ripe for a fresh modern look at theconcept of complementarity Whatever the

intrinsic merits of the concept forty years ago ithelped motivate Hicks and Allen to performtheir classical ldquoreconsiderationrdquo of ordinaldemand theory And as I hope to show the lastword has not yet been said on this ancient pre-occupation of literary and mathematical econo-mists The simplest things are often the mostcomplicated to understand fully

Complementarities have a deep connec-tion with strategic situations and the conceptof strategic complementarity is at the centerstage of game-theoretic analyses Examplesabound An arms race If the Soviet Unionincreased its spending on nuclear weapons itwould pay the United States to respond byincreasing its own spending A bank run Ifother customers of the bank that holds yoursavings withdraw their money it might payyou to also take your money out A currencycrisis If other investors attack the currency itmight pay me to do so as well An RampD raceIf my main rivals in the pharmaceuticalindustry increase their RampD spending doesit pay me to increase it also Technologyadoption My neighbors have introduced anew type of crop does it pay me to followLocation If a new store locates in the shop-ping mall does the mall become a moreattractive location for other stores

The modeling of complementaritiesincluding strategic situations has proved

jn05_Article 3 62205 100 PM Page 437

438 Journal of Economic Literature Vol XLIII (June 2005)

challenging The reason is that the tools athand were not attuned to deal with environ-ments where indivisibilities nonsmooth pay-offs and complex strategy spaces werenaturally the norm rather than the exceptionTo make matters worse multiple equilibriaare typical in the presence of complementar-ities and policy analysis is left orphanInstances of coordination failure with multi-ple equilibria abound bank runs debt runson a country low employmentactivity equi-libria revolutions and development trapsprovide some examples In all these situa-tions there are multiple self-fulfilling expec-tations of agents in the economy A key issueis how to build coherent models that are use-ful for policy analysis A challenging aspectof any crisis situation is to disentangle self-fulfilling from fundamentals-driven explana-tions that help answer questions such asWhat is the effect of an increase in theamount of central bank reserves on the prob-ability of a run on the currency What is theimpact of an increase in the solvency ratio onthe probability of failure of a bank What isthe effect of a change in foreign short-termdebt exposure on the probability of defaultof a small open economy

The appropriate toolbox to deal with com-plementarities and in particular with strate-gic situations is the theory of monotonecomparative statics and supermodulargames This theory provides the method formaking the analysis of complementarity sim-ple The basic idea of the theory is to exploitfully both order and monotonicity proper-ties The achievements of this approach areas follows First it provides a framework forthinking rigorously about complementari-ties identifying key parameters in the envi-ronment to look at (eg what are the criticalproperties of the payoffs and action spaces)Second it simplifies the analysis clarifyingthe drivers of the results (eg is the regular-ity condition really needed to obtain thedesired comparative static result) Third itencompasses the analysis of multiple equi-libria situations by ranking equilibria and

helping understand how potential equilibriamove with the parameters of interestFinally it easily incorporates complex strate-gy spaces such as those arising in dynamicgames and games of incomplete information

The paper provides an introduction to thetools of supermodular games and a range ofapplications to industrial organization(Cournot and Bertrand markets monopolis-tic competition RampD races multimarketoligopoly switching costs dynamic invest-ment games) macroeconomic models(menu costs search aggregate demandexternalities technology adoption adjust-ment costs) and finance (currency crisisbank runs) The next section presents theapproach in somewhat more detail as well asthe plan of the paper

2 Tools Results and Plan of the Paper

The basic theory was developed byDonald M Topkis (1978 1979) and furtherdeveloped and applied to economics byXavier Vives (1985a 1990a) and PaulMilgrom and John Roberts (1990a) Yet thetheory continues to be extended at the fron-tier of researchmdashfor example to dynamicgames and games of incomplete informa-tion The beauty of the approach is not itscomplexity but rather how much it simplifiesthe analysis and clarifies results In fact eventhe basic tools are not fully exploited byeconomists in current research

The theory of supermodular games andmonotone comparative statics based on lat-tice-theoretic methods has provided a pow-erful toolbox for analyzing the consequencesof complementarities in economicsMonotone comparative statics analysis pro-vides conditions under which optimal solu-tions to optimization problems movemonotonically with a parameter In this paperI provide an introduction to this methodologyand then apply it to the study of strategicinteraction in the presence of complementar-ities This approach exploits order and monot-onicity properties in contrast to classical

jn05_Article 3 62205 100 PM Page 438

Vives Complementarities and Games New Developments 439

convex analysis The central piece of attentionwill be games of strategic complementaritieswhere the best response of a player to theactions of rivals is increasing in their level

The purpose of this paper is to bring for-ward some recent applications of the lattice-theoretic methodology and at the same timeprovide an introduction to the toolbox Ishall demonstrate the usefulness of theapproach for

bull providing a common analytical frame tostudy complementarities

bull deriving new results andbull casting new light on old results by simpli-

fying proofs and discarding unnecessaryassumptions

Modeling strategic interaction presentsformidable problems A Nash equilibriummay not exist at least in pure strategies Orinstead there may be multiple equilibriaHow do players coordinate on one of themHow can the policymaker be sure thatchanging a parameter will have the desiredeffect Classical comparative statics analysisprovides ambiguous results in the presenceof multiple equilibria and imposes strongregularity conditions These regularity con-ditions become particularly strong whenapplied to games with complex functionalstrategy spaces such as dynamic or Bayesiangames We will see how complementaritiesare intimately linked to multiple equilibriaand how supermodular methods provide anatural tool for characterizing them

The class of games with strategic comple-mentarities and the tools to analyze themhave very nice properties

bull They allow very general strategy spacesincluding indivisibilities and functionalspaces such as those arising in dynamicor Bayesian games

bull They ensure the existence of equilibriumin pure strategies (without requiring quasiconcavity of payoffs smoothnessassumptions or interior solutions)

bull They allow a global analysis of the equi-librium set which has an order structurewith largest and smallest elements

bull Equilibria have useful stability proper-ties and there is an algorithm to computeextremal equilibria

bull Monotone comparative statics results areobtained with minimal assumptions byeither focusing on extremal equilibria orconsidering best-response dynamicsafter the perturbation

Furthermore as we shall see results canbe extended beyond the class of games withstrategic complementarities

Let me highlight here some examples ofhow the lattice-theoretic approach eitherobtains new results that are hard or impossi-ble to derive using the classical approach orimproves upon results already obtained bygetting rid of unnecessary assumptions orsimplifies and deepens our understanding ofthe proof of known results

bull Consider an RampD race where each firminvests continuously to obtain a break-through and where we want to knowwhat the effect is of increasing the num-ber of participants n in the race (TomLee and Louis L Wilde 1980) Undervery weak assumptions this game is oneof strategic complementarities and it willhave multiple equilibria The problem ofusing the classical approach is thatincreasing n may make some equilibriadisappear while others may appearClassical analysis will not help here butwith the lattice approach we obtain anunambiguous comparative statics resultincreasing n will necessarily increaseRampD effort provided that out-of-equi-librium adjustment dynamics are of ageneral adaptive form

bull Consider a dynamic monopolistic com-petition model with menu costs wherefirms interact repeatedly over an infinitehorizon and each firm receives an idio-syncratic demand or cost shock everyperiod Under what conditions doesthere exist a Markov perfect equilibri-um When is the current price of a firmincreasing in its past price and the dis-tribution of prices in the market The

jn05_Article 3 62205 100 PM Page 439

440 Journal of Economic Literature Vol XLIII (June 2005)

lattice approach provides the keyassumptions needed to answer thesequestions (Christopher Sleet 2001 andByoung Jun and Vives 2004)

bull Masahiro Okuno-Fujiwara AndrewPostlewaite and Kotaro Suzumura(1990) provided conditions under whichfully revealing equilibria obtain in duop-oly games of voluntary disclosure ofinformation when information is verifi-able The conditions involve restrictiveregularity assumptions such as concavityof payoffs interiority of equilibria andindependent types for the players Ourapproach allows us to omit these unnec-essary regularity assumptions highlightthe crucial ones (those related to monot-onicity conditions) and extend the resultto n-player games

bull Global games (Hans Carlsson and Ericvan Damme 1993) are games of incom-plete information with types determinedby each player observing a noisy signal ofthe state They are proving to be a popu-lar methodology for equilibrium selec-tion using iterated elimination ofdominated strategies and have wideapplications to currency and bankingcrises and macroeconomics (StephenMorris and Hyun Song Shin 2002)Global games are Bayesian games andthe lattice approach is particularly suitedto analyze them For example recentmajor advances in the difficult problem ofshowing the existence of Bayesian equi-librium in pure strategies have beenmade using the lattice-theoretic method-ology Furthermore by realizing thatglobal games are typically games of strate-gic complementarities we understandwhy and how iterated elimination of dom-inated strategies works and why andunder what conditions equilibrium selec-tion is successful Indeed we will see howequilibrium is unique precisely whenstrategic complementarities are weak andthat comparative statics results can bederived even for multiple equilibria

The methodology of supermodular gamesprovides the tools and an appropriate frame-work for satisfactorily confronting multipleequilibria and comparative statics Howeverwe should be aware also that the lattice-the-oretic approach is not a panacea and cannotbe applied to everything (Indeed theapproach builds on a set of assumptions) Togive an obvious example the approach can-not make equilibria appear in a game thathas no equilibrium to start with

We begin by introducing a simple class ofgames in section 3 where many of theimportant issues are highlighted The classincludes monopolistic competition searchand adoption games Section 4 provides anintroduction to the theory and basic resultsSection 5 provides applications to oligopolyand comparative statics in the context ofCournot Bertrand and RampD games includ-ing multimarket oligopoly competitionSection 6 deals with dynamic games therewe examine when increasing or decreasingdominance will obtain in investment gamesand we also characterize strategic incentivesin Markov games Applications to menuswitching and adjustment costs are providedas well Section 7 studies Bayesian gamescharacterizing equilibria in pure strategiesand comparative statics properties withapplications (among others) to games of vol-untary disclosure and global games includ-ing currency and banking crises Theappendix provides a brief recollection of themost important definitions and results of thelattice-theoretic method

3 A Simple Framework

Games of strategic complementarities arethose in which players respond to anincrease in the strategies of the rivals with anincrease in their own strategy This sectionpresents an example suggesting the flavor ofmany of the results that can be obtained withthe approach

Consider a game with a continuum ofplayers in which the payoff to a player is

jn05_Article 3 62205 100 PM Page 440

Vives Complementarities and Games New Developments 441

1 The analysis with n players is similar

π(aisimai) Here ai is the action of the playerlying in a (normalized) compact interval[01]sima is the average or aggregate actionand i is a (possibly idiosyncratic) payoff-relevant parameter1 I consider first the casewith homogeneous players and then laterthe case with heterogeneous players

31 Homogeneous Players

Consider the symmetric case where thepayoff to a player is given by π(aisima)Suppose that π is smooth in all argumentsand strictly concave in ai and let r be thebest response of an individual player toaggregate action sima In this framework equi-libria will be symmetric because given anyaggregate action sima there is a unique bestresponse r (sima) For interior solutions wewill have that

(r (sima)sima) = 0

If part2π(partai)2 lt 0 then r is continuously differ-

entiable and

Therefore sign r(~a) = signpart2πpartaipart~a andbest replies are increasing if part2πpartaipart~a ge 0 A symmetric equilibrium is characterized by r(a) = a Suppose also that part2πpartaipart ge 0so that an increase in increases the mar-ginal profit of the action of a player and hisbest response r

Two examples of the game are monopolis-tic competition and search In monopolisticcompetition (see Vives 1999 section 66)the action would be the price of a firm with~a the average price in the market and ademand or cost parameter We have

π(ai~a) = (ai minus )D(ai~a)

with D the demand function and the(common) marginal cost As we will see insection 4 for many demand systemspart2logDpartaipart~a gt 0 (meaning that the elasticity

prime( ) = minuspart part part

part part( )r a

a a

ai

i

~ ~

2

2 2

π

π

partpart

πai

of demand for product i is decreasing in theaverage price) and therefore part2logπpartaipart~a =part2logDpartaipart~a gt 0 Under this condition wewill have that r(~a) gt 0 because best repliesare invariant to an increasing transformationof the payoffs such as the logarithm In thesearch model (Peter A Diamond 1981) theaction ai is the effort of trader i in looking fora partner The benefit (probability of findinga partner) is proportional to own effort and isincreasing in the aggregate effort ~a of others

π(ai~a) = aig(~a) minus C(ai)

where gt 0 is the efficiency of the searchtechnology and where g and the cost ofeffort C are increasing functions In thiscase part2πpartaipart~a = g(~a) ge 0

In these examples it is easy to generatemultiple equilibria For instance in thesearch model let g(~a) equiv ~a and let C beincreasing with C(0) = 0 then ai = 0 for all iis always an equilibrium If C is smooth andstrictly convex with C(0) = 0 then there aretwo equilibria ai = 0 and ai = acirc gt 0 with acirc = C(acirc) for all i The latter equilibriumincreases strictly with and is Pareto supe-rior to the no-effort equilibrium Anotherpossibility is when g has an S-shaped func-tion and C(a) equiv a then there will be threeequilibria They will be the solutions (iea acirc and ndasha) to g(a) = a as depicted in figure 1 (lower branch) In this exampler(~a) = g(~a) Obviously equilibria are thesolution to r (a) = a and r(~a) = g(~a)

Several properties of the equilibria in thesearch example are worth noticing1 A sufficient condition to have multiple

equilibria is that strategic complementar-ities be sufficiently strongmdashnamely thatr(a) gt 1 for some candidate equilibriumr (a) = a (such as point acirc in figure 1)

2 The symmetric equilibria are orderedThere exits a largest (ndasha) and a smallest (ndasha)equilibrium (this follows trivially heregiven that actions are one-dimensional)and equilibria can be Pareto ranked Thisis a general property whenever π isincreasing in ~a (positive externalities)

jn05_Article 3 62205 100 PM Page 441

442 Journal of Economic Literature Vol XLIII (June 2005)

Figure 1 Best Response (with Homogenoues Players) and Multiple Equilibria

acirc a1

1

a a a

3 Extremal equilibria ndasha and ndasha are stablewith respect to the usual best-replydynamics Indeed it is immediate thatbest response dynamics starting at a = 0(resp a = 1) will converge to ndasha (resp ndasha)See figure 1

4 Iterated elimination of strictly dominatedstrategies defines two sequences that con-verge respectively to ndasha and ndasha For exam-ple let ndasha

0 = 0 Players will never use astrategy a lt r(0) because it is strictly dom-inated by ndasha

1 = r(0) Now knowing that noone will use a strategy in [0r(0)) theregion [0r(r(0))) will also be strictlydominated Let ndasha

2 = r(ndasha1) and define ndasha

k

recursively The sequence ndashak is increasing

and converges to ndasha (indeed it coincideswith best-reply dynamics starting at a =0) (See figure 1) This means that ratio-nalizable strategies will lie in the interval[ndashandasha] and if the equilibrium is uniquethen the game will be dominance solv-able That is the final outcome of theprocess of iterated elimination of strictly

2 Indeed at a stable equilibrium r lt 1 (or part2πi(partai)2 +part2πipartaipart~a lt 0) At equilibrium r(a) = a and therefore inthe vicinity of da d = (partrpart)(1 minus r) gt partrpart providedthat r gt 0 (or part2π partaipart~a gt 0)

dominated strategies is both unique andan equilibrium

5 An increase in the parameter will leadto an increased action in equilibriumgiven out-of-equilibrium best-responsedynamics and this increase will be overand above the direct effect of the increasein the parameter Indeed increasing will move r upward (as in figure 1) andthe equilibrium level of a will increaseStarting at a = ndasha the direct effect will leadus to r(ndasha) gt ndasha and the full equilibriumimpact to ndasha gt ndasha2 The consequences of a common shock (or for that matter an idiosyncratic shock) are amplifiedBecause of strategic complementaritiesthere is a multiplier effect Indeed thedirect effect of an increase in in theaction of an agent taking as given the

jn05_Article 3 62205 100 PM Page 442

Vives Complementarities and Games New Developments 443

3 Roger Guesnerie (1992) has shown this in a version ofthe model

4 See Satyajit Chatterjee and Cooper (1989) MarcoPagano (1989) or Philip H Dybvig and Chester S Spatt(1983) for related examples

average action is amplified by theincrease in the average action This hap-pens whether we focus on at extremal (orstable) equilibria or rather consider best-response dynamics after the perturbationEven starting at an unstable equilibriumor at an equilibrium that disappears once increases an increase in will result inan increase in a over and above the directeffect In figure 1 the unstable equilibri-um acirc disappears with the increase in moving r upward and best-replydynamics lead to the new equilibrium ndashaWith strategic substitutability among

strategies part2πpartaipart~a lt 0 there cannot bemultiple symmetric equilibria In this case itis immediate that there is a unique symmetricequilibrium (because

part2πi part2πi partπindashndashndashndash + ndashndashndash lt 0 and ndashndashndash (aa) = 0(partai)

2 partaipart~a partaiwill have a unique solution) It is easy to seethat when 0 gt r gt minus 1 (or |r| lt 1) thegame is dominance solvable3 This corre-sponds to the case where the symmetricequilibrium is stable according to the usualcobweb dynamics Equivalently in terms ofiterated elimination of strictly dominatedstrategies agents recognize that no one willtake an action larger than r(0) this starts theprocess of elimination of strategies nowwith alternating regions on both sides of thecandidate equilibrium

Models of aggregate demand externalitiesand models of Keynesian effects have a sim-ilar flavor to our simple model (see RussellCooper and Andrew John 1988) Themonopolistic competition model has beenused extensively in the growth developmentregional and international trade literaturesto generate complementarities and multipli-er processes (see Kiminori Matsuyama 1995for a survey) In all those instances the pres-ence of multiple Pareto rankable equilibria

multiplier effects and cumulative self-reinforcing processes is central to the analysis

32 Heterogeneous Players

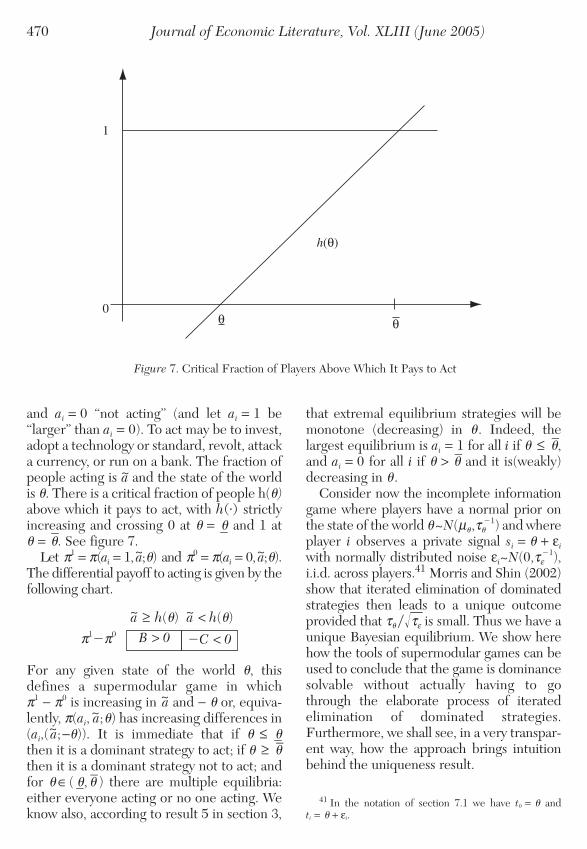

A variation of the search example encom-passes heterogeneous agents4 Suppose anagent must decide whether or not to adopt anew technology (or whether to ldquoinvestrdquoldquoactrdquo or ldquoparticipaterdquo) His action is ai = 0 ifthere is no adoption and is ai = 1 if there isadoption The cost of adoption is idiosyn-cratic and follows a distribution function Fon the interval [ndashndash ] The cost i for agent i isan independent draw from F The benefit ofadoption is g(~a) where ~a is the total massadopting (which will be between 0 and 1)and no adoption yields no benefit Therefore

π(ai~ai) = ai(g(~a) minus i)

The game is one of strict strategic comple-mentarities if g gt 0 It is worth noticingthat because of independence the adoptingmass ~a will be nonrandom Player i willadopt if g(~a) minus i ge 0 An equilibrium will begiven by an adoption threshold and anadopting mass ~a = F() such that g(~a) = and agent i will adopt if i le The aggregatebest reply to the adopting mass ~a is justF(g(~a)) or equivalently the best reply to athreshold used by other players is g(F())The equilibria can be depicted as in figure 1where on the horizontal axis we have ~a or and along the vertical axis the best-reply r(~a) = F(g(~a))or r () = g(F()) For examplelet g(~a) = ~a ndash lt 0 and ndash gt 1 Then for gt 0to adopt is a dominant strategy (ie it pays toadopt even if no one else adopts) for gt 1not to adopt is a dominant strategy (ie itdoes not pay to adopt even if everyone elseadopts) In equilibrium ~a = F() =

The equilibrium threshold solvesg(F()) minus = 0 The solution will be uniqueif gF minus 1 = gƒ minus 1 lt 0 where f is the den-sity of F It is thus immediate that if g lt 0(strategic substitutability) then the equilib-rium is unique The question is When dowe have a unique equilibrium with strategiccomplementarities

jn05_Article 3 62205 100 PM Page 443

444 Journal of Economic Literature Vol XLIII (June 2005)

5 Recall that if x~N(microσ 2) then f(micro) = (σradic2π)1 wheref is the density of x

It is instructive to think of the case wherei follows a normal distribution with mean micro

and variance σ 2 and where the costs of adop-

tion i and j (j ne i) are potentially correlat-ed with covariance σ 2

for isin[01) The case = 0 corresponds to the independent caseconsidered previously Suppose that playersadopt strategies with adoption threshold (In section 7 we will see that equilibriummust be of this form) From the point ofview of player i and given i the adoptingmass will be given by

where is the cumulative distributionfunction of the standard normal The agentwill adopt if and only if g(~ai) minus i ge 0 andthe equilibrium threshold will satisfy

where

The solution will be unique if (1 minus )(1 + )g minus 1 lt 0 where φ = is the density of the standard normal It isthen immediate that the equilibrium will beunique when (1 minus )(1 + )g2π lt 1where g equiv sup a[01] g(a)5 There will be aunique equilibrium when the degree ofstrategic complementarity is not too strongThis may happen either because payoff com-plementarities are weak (ndashg low) or becauseeach player ex ante faces a large cost uncer-tainty (σ high) or because the correlation ofthe costs is high ( close but not equal to 1)All three factors tend to lessen the strengthof strategic complementarities

Let g(~a) = ~a in order to illustrate theeffect of uncertainty If costs are perfectlycorrelated then there are multiple equilibria

Pr ˆ ˆˆ

θ θ θ θ ρρ

θ microσ

θ

θj ile = = minus

+minus

11

g j iPr ˆ ˆ ˆθ θ θ θ θle = ( ) minus = 0

ˆiθ ρθ ρ micro

σ ρθ

θ

=minus + minus( )( )

minus

1

1 2

~ Pr ˆai j i θ θ θle

6 What the two cases have in common is that the playerputs very little weight on prior information when σ 2

is verylarge because the prior is flat when is close to 1 becausethe type of the player predicts (almost) perfectly the typesof others

for isin(01) In this case there is completeinformation because a playermdashby knowinghis own costmdashknows the costs of any otherplayer However a little bit of imperfect costcorrelation ( close to 1) will yield a uniqueequilibrium Note for example that((1 minus )(1 + )( minus micro))) tends to 12either when rarrinfin or as rarr1 yielding theunique solution = 12 In figure 2 the case micro = 12 is displayed and = micro = 12is the equilibrium threshold Then if (1 minus )(1 + )2π gt 1 two more equi-libria appear

Either with a diffuse prior or when thecost of a player gives very precise informa-tion about the costs of others the (strategic)uncertainty of player i is maximal withrespect to the behavior of others Thisinduces a best response for the player whichis quite ldquoflatrdquo that is not very sensitive to thethreshold used by others6

33 How General Are the Results

The question arises of how far the niceresultsmdashabout existence and characteriza-tion of equilibria and comparative staticpropertiesmdashin our simple game of section31 extend to different specifications (what ifpayoffs are not concave and best responsesare not unique) or more general games withstrategic complementarities or evenbeyond As we will see in the next sectionmost of the properties generalize to multidi-mensional strategy spaces discrete or con-tinuous and even functional spaces as wellas to nonsmooth and nonconcave payoffsThe basic insight of the next section will bethat to obtain the desired results only themonotonicity properties of incremental pay-offs and the order properties of strategiesmatter Most of the regularity conditions typ-ically assumed will not be crucial In section7 we will study Bayesian games and see how

jn05_Article 3 62205 100 PM Page 444

Vives Complementarities and Games New Developments 445

Figure 2 Equilibrium Thresholds (with Heterogeneous Agents) and Multiple Equilibria

1

12

microθ = 12 1 θ

our intuitions concerning the game with het-erogeneous players of section 32 generalizeto equilibrium selection in global games Wewill see how the consideration of thresholdstrategies is in fact without loss of generalityand how the key to uniqueness will be aninformation structure (diffuse prior or thesignal of a player giving very precise infor-mation about the signals of others) thatweakens strategic complementarities Thegeneral principle is that in order to obtainuniqueness of equilibrium in the presence ofcomplementarities the degree of strategiccomplementarities must be weak

4 An Introduction to Games with Strategic Complementarities

In this section I provide first a briefintroduction to the tools and main resultsof the theory and then comment on thetheoryrsquos scope

41 Modeling Complementarities andResults

Complementarities are dealt with usingtools provided by the theory of monotonecomparative statics and supermodulargames Those tools are based on lattice-the-oretic results that exploit order and monoto-nicity properties of action sets and payoffsThe basis of the approach are monotonecomparative statics results developed byTopkis (1978) and the application of AlfredTarskirsquos (1955) fixed point theorem toincreasing functions In a game situationminimal assumptions are put on strategy setsand payoffs so that best responses areincreasing and move monotonically with theparameters of interest Then Tarskirsquos fixedpoint theorem delivers existence of equilib-ria as well as order properties of the equilib-rium set and comparative statics resultsfollow naturally

jn05_Article 3 62205 100 PM Page 445

446 Journal of Economic Literature Vol XLIII (June 2005)

7 The reader is referred to chapter 2 of Vives (1999) fora more thorough and general treatment of the theory aswell as proofs further references and applications

This approach provides a powerful analyt-ical tool that confronts the usual obstacleswhen analyzing a game existence of pure-strategy equilibria comparison of equilibriaand comparative statics In particular ingames of strategic complementarities thepresence of multiple equilibria need not bean obstacle to performing comparative stat-ics analysis

The emphasis of the exposition will be onintuition and not the technical details Thissection will provide the minimal backgroundnecessary for a reader to follow the rest ofthe paper and the appendix contains techni-cal definitions and intermediate resultsExamples will be developed to illustrate themethodology7

We will use the intuitive concept of agame of strategic complementarities (GSC)whenever the best responses of the playersin the game are increasing in the actions ofrivals The technical concept of supermodu-lar game (to be shortly defined below)defined provides sufficient conditions forbest responses to be increasing

I will provide a definition of a supermod-ular game in a smooth context in order tokeep the mathematical apparatus to a mini-mum but this is by no means the most gen-eral way to define it Consider the game (Aiπi i isin N) where N is the set of players i = 1hellip n Ai is the strategy set a compactcube in Euclidean space and πi the payoff ofplayer i isin N (defined on the cross productof the strategy spaces of the players A) Letai isin Ai and ai isin ΠjiAj (ie we denote byai the strategy profile (a1hellip an) exceptingthe ith element) Let aih denote the hth component of the strategy ai of player i

We will say that the game (Aiπi i isin N) issmooth supermodular if for all i

bull Ai is a compact cube in Euclidean spacebull πi(aiai) is twice continuously differen-

tiable

8 Continuity is needed to ensure the existence of bestreplies and the continuity requirement can also be weak-ened See the appendix for the general definitions of lat-tices supermodularity increasing differences andsupermodular game

9 Supermodularity and increasing differences can evenbe weakened to define an ldquoordinal supermodularrdquo gamerelaxing supermodularity to the weaker concept of quasi-supermodularity and increasing differences to a single-crossing property (see Milgrom and Chris Shannon 1994)However such properties (unlike supermodularity andincreasing differences) have no differential characteriza-tion and need not be preserved under addition or partialmaximization operations

1 supermodular in ai for fixed ai orpart2πipartaihpartaik ge 0 for all k ne h and

2 with increasing differences in (aiai)or part2πipartaihpartajk ge 0 for all j ne 1 and forall h and k

The game is smooth strictly supermodularif the inequality in (2) is strict

Condition (1) is the complementarityproperty (supermodularity) in own strate-gies It means that the marginal payoff to anystrategy of player i is increasing in the otherstrategies of the player Condition (2) is thestrategic complementarity property in rivalsrsquostrategies ai It means that the marginalpayoff to any strategy of player i is increasingin any strategy of any rival player This prop-erty of πi is termed increasing differences in(aiai) In the general formulation of asupermodular game strategy spaces needonly be ldquocomplete latticesrdquo only continuity(not differentiability) of payoffs is neededand properties (1) and (2) are stated in termsof increments8

In a supermodular game very generalstrategy spaces can be allowed These includeindivisibilities as well as functional strategyspaces such as those arising in dynamic orBayesian games (as we will see in section 62and section 7) Regularity conditions such asconcavity and interior solutions can be dis-pensed with The complementarity propertiesare robust in the sense that they are preservedunder addition or integration pointwise lim-its and maximization (with respect to a subsetof variables preserving supermodularity forthe remaining variables)9

jn05_Article 3 62205 100 PM Page 446

Vives Complementarities and Games New Developments 447

10 See chapter 6 of Vives (1999) However this is not auniversal result as we will see in section 42

11 See lemma 1 in the appendix for a precise statementof the result

Two leading oligopoly models fit in manyspecifications the complementarity assump-tions made A first example is a Cournot oli-gopoly with complementary products In thiscase the strategy sets are compact intervalsof quantities and the complementarityassumptions are natural (what MichaelSpence (1976) called ldquostrong comple-mentsrdquo) A second example is a Bertrand oli-gopoly with differentiated substitutableproducts where each firm produces a differ-ent variety The demand for variety i is givenby Di(pipi) where pi is the price of firm iand pi denotes the vector of the pricescharged by the other firms A linear demandsystem will satisfy the complementarityassumptions

The application of the theory can beextended by considering increasing transfor-mations of the payoff (which does notchange the equilibrium set of the game) Wesay that the game is log-supermodular if πi isnonnegative and if πi fulfills conditions (1)and (2) In the Bertrand oligopoly examplethe profit function πi = (pi minus ci)Di(pipi) offirm i where ci is the constant marginal costis log-supermodular in (pipi) wheneverpart2logDipartpipartpj ge 0 For firm i this holdswhenever the own-price elasticity ofdemand ηi is decreasing in pi as with con-stant elasticity logit or constant expendituredemand systems10

The key results of the theory are obtainedby a combination of monotone comparativestatics results due to Topkis and Tarskirsquos fixedpoint theorem The results by Topkis (1978)deliver monotone increasing best responseseven when πi is not quasi-concave in ai

The basic monotone comparative staticsresult states that the set of optimizers of afunction u(x t) that is parameterized by tsupermodular in x and with increasing dif-ferences in x and t has a largest and a smallestelement and that both are increasing in t11

12 This definition was used in Vives (1985a) who con-centrated attention on monotone increasing best respons-es as the defining characteristic of games with strategiccomplementarities See the appendix for a more formaldefinition along those lines

In a supermodular game this means thateach player i has a largest ndashψi(ai) = supψi(ai)as well as a smallest ndashψi(ai) = inf ψi(ai) bestreply and that they are increasing in thestrategies of the other players If the game isstrictly supermodular then any selectionfrom the best-reply correspondence isincreasing

Some intuition can be gained from thesimple framework of section 31 Weobserved that if part2πi(partai)

2 lt 0 then r(~a) = sign(part2πipartaipart~a) Now even when πi

is not quasi-concave the monotone com-parative statics result implies that if part2πipartaipart~a gt 0 then any selection from thebest-reply correspondence of player i (whichmay have jumps) is increasing in the averageaction

We could define also the (weaker) conceptof a game of strategic complementarities(GSC) under our maintained assumptionsas a game where (a) strategy sets are com-pact cubes (or ldquocomplete latticesrdquo) (b) thebest reply of any player has extremal (largestand smallest) elements and (c) those ele-ments are increasing in the strategies ofrivals Similarly we could define a game ofstrict strategic complementarities if in addi-tion any selection from the best reply of anyplayer is increasing in the strategies of therivals12 All the results stated hereafter willthen hold replacing (strictly) supermodulargame by GSC (game of strict SC)

The following results hold in a supermodu-lar game Let ndashψ = (ndashψ1hellipndashψn) and ndashψ =(ndashψ1hellipndashψn) denote the extremal best-replymaps

Result 1 Existence and order struc-ture (Topkis 1979) In a supermodulargame there always exist extremal equilibriaa largest element ndasha = supaisinA ndashψ(a) ge a anda smallest element ndasha = infaisinA ndashψ(a) le aof the equilibrium set

jn05_Article 3 62205 100 PM Page 447

448 Journal of Economic Literature Vol XLIII (June 2005)

13 The equilibrium set has additional order properties(see Vives 1985a Vives 1990a problem 25 in Vives(1999and Lin Zhou(1994)

14 Indeed if -a1 ne -a2 then because the game is symmet-ric (-a2 -a1 -a3hellip -an) will also be an equilibrium and there-fore because (--a1 -a2 -a3hellip -an) is the largest equilibrium -a1 ge -a2 ge -a1 and -a1 = -a2

The result is shown by applying Tarskirsquosfixed point theorem (which implies that anincreasing function from a compact cubeinto itself has a largest and a smallest fixedpoint see appendix) to the extremal selec-tions of the best-reply map ndashψ and ndashψ whichare monotone by the strategic complemen-tarity assumptions There is no reliance onquasi-concave payoffs and convex strategysets to deliver convex-valued best replies asis required when showing existence usingKakutanirsquos fixed point theorem13

In the Bertrand oligopoly for examplewhen the payoff is supermodular or log-supermodular then it follows that extremalprice equilibria do exist The results can beextended to convex costs and multiproductfirms and so provide a large class of Bertrandoligopoly cases for which the classical nonex-istence of equilibrium problem encounteredby Roberts and Hugo Sonnenschein (1977)does not arise

Result 2 Symmetric games For a sym-metric supermodular game (exchangeableagainst permutations of the players) the fol-lowing statements hold

bull Symmetric equilibria exist because theextremal equilibria ndasha and ndasha are symmet-ric14 Hence if there is a unique sym-metric equilibrium then the equilibriumis unique (since ndasha = ndasha) This result provesto be a very useful tool for showinguniqueness in symmetric supermodulargames For example in a symmetric ver-sion of a Bertrand oligopoly system withconstant elasticity of demand and con-stant marginal costs it is easy to see thatthere exists a unique symmetric equilib-rium Since the game is strictly log-supermodular we can conclude that theequilibrium is unique

15 See footnote 23 in Vives (1999) for a proof of thestatement

16 See section 231 in Vives (1999)17 Milgrom and Roberts (1994) also state and prove the

theorem with S = [01]18 The argument is simple Consider a symmetric game

with compact intervals as strategy spaces and let πi(aiai)= π(aiΣjneiaj) as in a Cournot game with homogeneousproduct and identical cost functions (or as in the game ofsection 3 with a continuum of players) Existence of sym-metric equilibria follows then from the stated result if thebest-reply Ψi of a player (identical for all i due to symme-try) has no jumps down This is in fact true if costs are con-vex in the Cournot game Symmetric equilibria are givenby the intersection of the graph of ai = Ψi(Σjneiaj) with theline ai = (Σjneiaj)(n minus 1)

bull If the strategy spaces of the players areone-dimensional (or more generallycompletely ordered) then a symmetricstrictly supermodular game has onlysymmetric equilibria15

For one-dimensional strategy spaces exis-tence of symmetric equilibria can beobtained by relaxing the monotonicityrequirement of best responses It is enoughthen that all jumps in the best reply of a play-er be up Existence follows from Tarskirsquosintersection point theorem16 The result iseasy to grasp considering a functionƒ [01]rarr[01] which when discontinuousjumps up but not down The function mustthen cross the 45˚ line at some point Indeedsuppose that it starts above the 45˚ line (oth-erwise 0 is a fixed point) then it either staysabove it (and then 1 is a fixed point) or itcrosses the 45˚ line Versions of this fixedpoint theorem have been derived by MMcManus (1962 1964) and Roberts andSonnenschein (1976) to show existence ofequilibria in symmetric Cournot games withconvex costs17 More generally In a sym-metric game where the strategy space ofeach player is a compact interval and thepayoff to a player depends only on her ownstrategy and the aggregate strategy of rivalsif the best reply of a player has no jumpsdown then symmetric equilibria exist Thisimplies in particular that for the game insection 31 under very weak assumptions asymmetric equilibrium will always exist18

jn05_Article 3 62205 100 PM Page 448

Vives Complementarities and Games New Developments 449

Figure 3 Cournot Tatocircnnement in a Supermodular Game with Best Reply Functions r1 r2

a2

A+

A+

Aminus

Aminus

a

a

a1

r2()

r1()

Result 3 Welfare (Milgrom andRoberts 1990a Vives 1990a) In a super-modular game if the payoff to a player isincreasing in the strategies of the other play-ers (positive externalities) then the largest(resp smallest) equilibrium point is thePareto best (resp worst) equilibrium Thisis a very simple result that is at the base offinding equilibria that can be Pareto rankedin many games with strategic complemen-tarities For example in the Bertrand oli-gopoly example the profits associated withthe largest price equilibrium are also thehighest for every firm

Result 4 Stability and rationalizabili-ty Consider a supermodular game with con-tinuous payoffs Then we have the following1 Simultaneous response best-reply

dynamics (Vives 1990a)bull Approach the ldquoboxrdquo [ndashandasha ] defined by

the smallest and the largest equilib-rium points of the game Hence ifthe equilibrium is unique then it isglobally stable

bull Converge monotonically downward(upward) to an equilibrium startingat any point in the intersection of

the upper (lower) contour sets of the largest (smallest) best replies ofthe players A+ equiv a isin A ndashψ(a) le a(A- equiv a isin A ndashψ(a) ge a) See figure 3

2 The extremal equilibria ndasha and ndasha corre-spond to the largest and smallest seriallyundominated strategies Therefore if theequilibrium is unique then the game isdominance solvable (Milgrom andRoberts 1990a)

This result implies that all relevant strate-gic action is happening in the box [ndashandasha ]defined by the smallest and largest equilib-rium points For example rationalizableoutcomes (B Douglas Bernheim 1984David G Pearce 1984) and supports ofmixed-strategy and correlated equilibriamust lie in the box [ndashandasha ] The argument forthe second part of result 41 is quite simplebecause for example starting at any pointin A+ (see figure 3) best-reply dynamicsdefine a monotone decreasing sequencethat converges to a point that must ( by con-tinuity of payoffs) be an equilibriumResults in 41 extend to a large class of adap-tive dynamics of which best-reply dynamicsare a particular case

jn05_Article 3 62205 100 PM Page 449

450 Journal of Economic Literature Vol XLIII (June 2005)

In fact starting at the largest (smallest)point of the strategy space Amdashrecall it is acubemdashbest-reply dynamics with the largest(smallest) best-response map ndashψ(ndashψ) will leadto the largest (smallest) equilibrium ndasha(ndasha )(Topkis 1979) For example starting atinf A (see figure 3) best-reply dynamicswith the smallest best reply map ndashψ definea monotone increasing sequence thatconverges to a point y that by continuityof payoffs must be an equilibriumFurthermore this must be the smallestequilibrium y = ndasha For any other equilibri-um x x ge inf A and iterating the best replymap ndashψ on both sides of the inequality yieldsx ge ndasha because ndashψ is increasing

Starting at an arbitrary point we cannotensure convergence because for instance acycle is possible For example in figure 3starting at a0 = (ndasha1ndasha 2) the simultaneousresponse best-reply dynamics cycle between(ndasha1ndasha 2) and (ndasha 1ndasha2)

In the Bertrand oligopoly example withlinear constant elasticity or logit demandsthe equilibrium is unique and so the game isdominance solvable and globally stable

Another interesting result is that properlymixed equilibria (ie Nash equilibria forwhich at least two playersrsquo strategies are notpure strategies) in strictly supermodulargames are unstable with respect to best-reply or more general adaptive dynamics(Federico Echenique and Aaron S Edlin2004) An example is the mixed-strategyequilibrium in the battle of the sexes

Result 5 Comparative staticsConsider a n-player supermodular gamewith payoff for firm i πi(aiai t) par-ameterized by a vector t = (t1hellip tn) If πi has increasing differences in (ai t)(part

2πipartaihparttj ge 0) for all h and j) thenwith an increase in t(i) the largest and smallest equilibrium

points increase and(ii) starting from any equilibrium best-

reply dynamics lead to a (weakly) largerequilibrium following the parameterchange

Furthermore the latter result can beextended to a class of adaptive dynamicsincluding fictitious play and gradient dynam-ics Continuous equilibrium selections thatdo not increase monotonically with t predictunstable equilibria (Echenique 2002) Thecomparative statics result is generalized inMilgrom and Shannon (1994)

An heuristic argument for the result is asfollows The largest best reply of player i isincreasing in t and from this it followsthat the largest equilibrium point (asdetermined by the largest best replies)also increases with t Indeed ndasha = supa isin A ndashψ(a t) ge a and ndashψ(a t) is increasingin t Obviously for an increase in the equi-librium to take place we need only forexample that the payoff to firm i be affect-ed by ti and not by any other tj An increasein t leaves the old equilibrium in A- (seefigure 3) and thus sets in motion viabest reply (or more generally via adap-tive dynamics) a monotone increasingsequence that converges to a larger equi-librium Increasing actions by one playerreinforce the desire of all other players toincrease their actions and the increasesare mutually reinforcing (ie they exhibitpositive feedback)

Another way to look at the feedback loopis to think in terms of multiplier effects Asstated in section 3 a multiplier effect inthe parameter tj obtains if the equilibriumreaction of each player to a change in theparameter is strictly larger than the reac-tion of the player keeping the strategies ofthe other players constant This will hap-pen for example in a smooth strictlysupermodular game with one-dimensionalstrategy spaces for which part2πipartaiparttj ge 0with strict inequality for at least one firm ifeither considering extremal equilibria orfollowing best-reply adjustment dynamicsafter a parameter change In figure 4where there is a unique equilibrium theeffect of an increase in t1 is to move out-ward the best reply of player 1 If player 2were to stay put at a0

2 then the best

jn05_Article 3 62205 100 PM Page 450

Vives Complementarities and Games New Developments 451

19 Martin Peitz (2000) gives sufficient conditions for aprice game to display multiplier effects

Figure 4 Effect of an Increase in Parameter t1

a2

a1acirc1 a1

r1 r2

a20

response of player 1 would be acirc1 but inequilibrium a1 gt acirc1

19

In games with strategic complementari-ties unambiguous monotone comparativestatics obtain if we concentrate on stableequilibria This is a multidimensional glob-al version of Samuelsonrsquos (1979) correspon-dence principle which links unambiguouscomparative statics with stable equilibriaand is obtained with standard calculusmethods applied to interior and stable one-dimensional models

As an example consider the (supermodu-lar or log-supermodular) Bertrand oligop-oly There extremal equilibrium pricevectors are increasing in an excise tax tIndeed we have that πi = (pi minus t minus ci)Di(p)and part2πipartpipartt = minuspartDipartpi gt 0

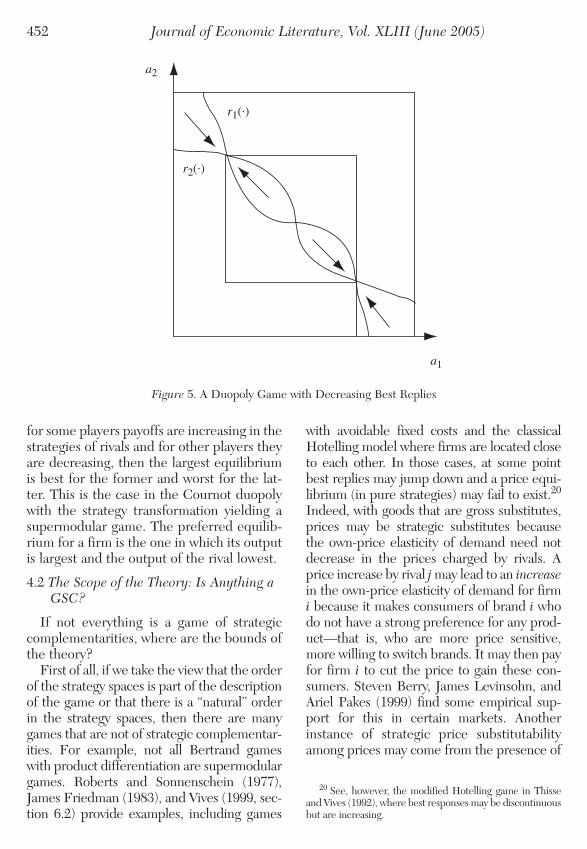

Result 6 Duopoly with strategic sub-stitutability (Vives 1990a) If n = 2 andthere is (a) strategic complementarity inown strategies with πi supermodular in ai

or part2πipartaihpartaik ge 0 for all k ne h and (b)strategic substitutability in rivalsrsquo strategieswith πi with decreasing differences in (aiaj)or part2πipartaihpartajk le 0 for all j ne i and for all hand k then the transformed game with newstrategies s1 = a1 and s2 = minusa2 is smoothsupermodular (See figure 5 and note thatthis is the mirror image of figure 3 withrespect to the ordinate axis) Therefore allthe results stated previously apply to thisduopoly game as well Unfortunately thetrick does not work for n gt 2 and the exten-sion to the strategic substitutability case forn players does not hold

A typical example of duopoly with strate-gic substitutability is a Cournot marketwhere usually best replies are decreasing Inthis case the welfare result is as follows If

jn05_Article 3 62205 100 PM Page 451

452 Journal of Economic Literature Vol XLIII (June 2005)

Figure 5 A Duopoly Game with Decreasing Best Replies

a2

r1()

r2()

a1

20 See however the modified Hotelling game in Thisseand Vives (1992) where best responses may be discontinuousbut are increasing

for some players payoffs are increasing in thestrategies of rivals and for other players theyare decreasing then the largest equilibriumis best for the former and worst for the lat-ter This is the case in the Cournot duopolywith the strategy transformation yielding asupermodular game The preferred equilib-rium for a firm is the one in which its outputis largest and the output of the rival lowest

42 The Scope of the Theory Is Anything aGSC

If not everything is a game of strategiccomplementarities where are the bounds ofthe theory

First of all if we take the view that the orderof the strategy spaces is part of the descriptionof the game or that there is a ldquonaturalrdquo orderin the strategy spaces then there are manygames that are not of strategic complementar-ities For example not all Bertrand gameswith product differentiation are supermodulargames Roberts and Sonnenschein (1977)James Friedman (1983) and Vives (1999 sec-tion 62) provide examples including games

with avoidable fixed costs and the classicalHotelling model where firms are located closeto each other In those cases at some pointbest replies may jump down and a price equi-librium (in pure strategies) may fail to exist20

Indeed with goods that are gross substitutesprices may be strategic substitutes becausethe own-price elasticity of demand need notdecrease in the prices charged by rivals Aprice increase by rival j may lead to an increasein the own-price elasticity of demand for firmi because it makes consumers of brand i whodo not have a strong preference for any prod-uctmdashthat is who are more price sensitivemore willing to switch brands It may then payfor firm i to cut the price to gain these con-sumers Steven Berry James Levinsohn andAriel Pakes (1999) find some empirical sup-port for this in certain markets Anotherinstance of strategic price substitutabilityamong prices may come from the presence of

jn05_Article 3 62205 100 PM Page 452

Vives Complementarities and Games New Developments 453

21 In a GSC as defined in this section there may be noequilibrium in pure strategies because strategy sets neednot be complete lattices

strong network externalities For example inthe logit model with network externalities(Simon Anderson Andre de Palma andJacques Franccedilois Thisse 1992 chapter 7)increasing the price set by a rival raises thevalue for consumers of the network of firm iso it may pay this firm to cut prices in order toenlarge this lead (although this will not hap-pen for small network externalities) To put itanother way in many games best responsesare simply nonmonotone For example theyare increasing in some portion of the strategyspace and decreasing in another

However we could also take the view thatthe order of the strategy sets of the players isa modeling choice at the convenience of theresearcher This is what we have done toextend the reach of the theory to duopolieswith strategic substitutes Then if we allowalso the construction of this order ex postwith knowledge of the equilibria of thegame then the answer to the question of thebounds of the theory is that most games areof strategic complementarities This meansthat complementarities alone in the weaksense stated do not have much predictivepower unless coupled with additional struc-ture (Echenique 2004a) Indeed define agame with strategic complementarities asone in which there is a partial order onstrategies (that can be chosen by the model-er) so that best responses are monotoneincreasing (and with strategy sets having alattice structure)21 Then (i) a game with aunique pure strategy equilibrium is a GSC ifand only if Cournot best-response dynamics(with unique or finite-valued best replies)have no cycles except for the equilibriumand (ii) a game with multiple pure strategyequilibria is always a GSC As a corollary (iii)2 times 2 games generically are either GSC orhave no pure strategy equilibria (like match-ing pennies) Result (i) in particular meansthat a game with a unique and globally stable 22 If a correspondence φ from X to X has two fixed

points a and b then define an order ge on X as follows Lety ge x if and only if any of the following is true x = y x = aor y = b Then φ is actually weakly increasing in the sensethat if y ge x then there is a z in φ and a z in φ(y) with z ge z (In fact (X ge ) is a complete lattice see appendix)

equilibrium is a GSC according to the defi-nition given An example is the strategic sub-stitutes case in the continuum of agentsmodel of section 2 when r gt minus 1 Note thatin this case the game is dominance solvable

Result (ii) is shown by taking one equilib-rium to be the largest and another thesmallest strategy profiles in a way that bestresponses are increasing22 Indeed a gamewith multiple equilibria always involves acoordination problem (ie coordinating onone equilibrium) We can then find an orderon strategies that makes the game one ofstrategic complementarities However notethat this is done with a priori knowledge ofthe equilibria and the defined orderindeed it may not be ldquonaturalrdquo at all

5 Oligopoly and Comparative Statics

This section reviews some of the basicapplications to oligopoly surveys very recentones and provides some new ones It devel-ops comparative statics results in Cournotmarkets (including entry) patent races andmultidimensional competition

The analysis illustrates several points thepotential pitfalls of classical analysis theextension of the methods to games that neednot display complementarities globally andthe isolation of the crucial assumptions driv-ing the results As an example of the firstissue classical analysismdashwhen studying theeffects of increasing the number of firms ninto a Cournot marketmdashignores that someequilibria may disappear (or appear) whenchanging n making any ldquolocalrdquo study mean-ingless (see Rabah Amir and Val E Lambson2000) An analysis of a multimarket oligopolycoming from two-sided competition willexemplify the second issue Using lattice-the-oretic methods conditions for ldquoperverserdquocomparative statics will be derived in a

jn05_Article 3 62205 100 PM Page 453

454 Journal of Economic Literature Vol XLIII (June 2005)

context where the underlying game is notsupermodular (Luis Cabral and Lluis Villas-Boas 2004) Finally an examination of a patentrace will isolate the crucial assumptionsbehind the comparative statics of RampD effortwith respect to the number of participants inthe race (Vives 1999) We deal in turn withcomparative statics in Cournot markets patentraces and multidimensional competition

51 Comparative Statics in Cournot Markets

The standard Cournot game displaysstrategic substitutability therefore thegame is supermodular only in the duopolycase (by changing the sign of the strategyspace of one player) as discussed in result 6However the lattice-theoretic approachdelivers results also with n firms I considerhere a symmetric market (see Amir 1996aand Vives 1999 for other results)

Consider a n-firm symmetric Cournotmarket in which the profit function of firm iis given by

πi = P(Q)qi minus C(qi)

Here P is the smooth inverse demandwith P lt 0Q is total output C is the costfunction of the firm and qi its output levelWe parameterize the cost function of firm iby and let C(qi) be smooth withpart2Cpartpartqi le 0

In the standard approach (Jesuacutes K Seade1980a 1980b Avinash K Dixit 1986) it isassumed that payoffs are quasi-concave andconditions

(n + 1)P(nq) + nP(nq)q lt 0 and C(q) minus P(nq) gt 0

are imposed so that there is a unique andlocally stable symmetric equilibrium qlowastThen standard calculus techniques showthat an increase in increases qlowast and thattotal output increases and profits per firmdecrease as n increases The comparativestatics of output per firm with respect to thenumber of firms are ambiguous

The classical approach has several prob-lems First of all it is silent about the

23 See Vives (1999 pp 42ndash43 93ndash96 section 431) fordetails

potential existence of asymmetric equilib-ria Second it is restrictive and may be mis-leading For example if the uniquenesscondition for symmetric equilibria does nothold and there are multiple symmetricequilibria changing n may either cause theequilibrium considered to disappear orintroduce more equilibria (as in figure 1)

In the lattice-theoretic approach (Amirand Lambson 2000 Vives 1999) it isassumed only that P lt 0 and C minus P gt 0Then it can be shown that a symmetricequilibrium (and no asymmetric equilibri-um) exists23 Furthermore at extremalCournot equilibria (or following out-of-equilibrium best-reply dynamics) individ-ual outputs are increasing in total outputis increasing in n and profits per firmdecrease with n Furthermore it can beshown that individual outputs decrease(increase) with n if demand is log-concave(log-convex and costs are zero) Thisapproach does away with the unnecessaryassumptions of the standard approach andderives new results

The approach here also delivers the con-ditions (in a differentiated product environ-ment) for Bertrand prices to be lower thanCournot prices as a corollary of the fact thatCournot prices must lie in region A+(figure3) when actions are prices (Vives 1985b1990a see also Vives 1999 section 63)

52 Patent Races

Suppose that n firms are engaged in amemoryless patent race and have access tothe same RampD technology (Lee and Wilde1980) An innovating firm obtains the prizeV and losers obtain nothing If a firm spendsx continuously then the (instantaneous)probability of innovating is given by h(x)where h is a smooth concave function withh(0) = 0 and h gt 0 limxrarrinfinh(x) = 0 h(0) = infin(a region of increasing returns for small x

jn05_Article 3 62205 100 PM Page 454

Vives Complementarities and Games New Developments 455

may be allowed) In the absence of innovat-ing the normalized profit of firms is zeroUnder these conditions the expected dis-counted profits (at rate r) of firm i investingx if rival j invests xj is given by

(see Lee and Wilde 1980 and JenniferReinganum 1989) Denote the bestresponse of a firm by xi = R(Σjih(xj) + r)this is well defined under the assump-tions Lee and Wilde (1980) restrict atten-tion to symmetric Nash equilibria of thegame and show that under a stability condition at a symmetric equilib-rium xlowast R((n minus 1)h(xlowast))(n minus 1)h(xlowast) lt 1 xlowast

increases with nHowever this approach suffers from the

same problems as the comparative statics ofentry in Cournot markets It requiresassumptions to ensure a unique and stablesymmetric equilibrium and cannot rule outthe existence of asymmetric equilibriaNonetheless the following mild assump-tions ensure that the game is strictly log-supermodular h(0) = 0 and h is strictlyincreasing in [0ndashx] with h(x)V minus x lt 0 for x ge ndashx gt 0 It follows then from result 2 thatequilibria exist and all are symmetric

Let xi = x and xj = y for j ne i Then logπi

has (strictly) increasing differences in (xn)for all y(y gt 0) and at extremal equilibriathe expenditure intensity xlowast is increasing inn Furthermore if h is smooth with h gt 0and h(0) = infin then partlogπi partxi is strictlyincreasing in n and (at extremal equilibria)xlowast is strictly increasing in n This followsbecause under our assumptions equilibriaare interior and must fulfill the first-orderconditions

As before starting at any equilibrium anincrease in n will raise the research intensitywith out-of-equilibrium adjustment accord-ing to best-reply dynamics This will be soeven if some equilibria disappear or newones appear as a result of increasing n

π ii i

i j i j

h x V xh x h x r

=( ) minus

( ) + ( ) +ne

53 Multidimensional Competition

Multidimensional competition providesanother fertile ground for application of theapproach which can readily handle multidi-mensional strategy spaces We will considerfirst an example with advertising and priceas strategies and then examine multimarketoligopoly situations

531 Advertising and Prices

Consider our Bertrand oligopoly examplewhere the demand Di(p ti) of firm i dependson advertising effort ti with partDipartti gt 0Suppose that goods are gross substitutespartDipartpj ge 0 for j ne i and that demand isdownward sloping partDipartpi lt 0 Let

πi = (pi minus ci)Di(p ti) minus Fi(ti)

here Fi is the cost of advertising with Fi gt 0The action of the firm is ai = (pi ti) with nat-ural upper bounds for pi and ti Profits πi arestrictly supermodular in ai = (pi t) if

A sufficient condition for the condition tohold is that part2Dipartpipartti ge 0 This amounts torequiring that advertising increases the cus-tomers willingness to pay Furthermore πi

has increasing differences in ((pi ti)(pi ti))if part2Dipartpipartpj ge 0 for j ne i (given thatpartDipartpiparttj = 0 j ne i) Under these assump-tions the game is supermodular and thelargest (smallest) equilibrium has the featureof having high (low) prices and advertisinglevels Multiple equilibria obtain with a sym-metric linear demand system where ti

increases the demand intercept if F is con-cave enough We have thus found conditionsunder which high prices are associated withhigh advertising levels

532 Multimarket Oligopoly

The previous example can be extendedreadily to multiproduct firms and even to

partpart part

= minus( ) partpart part

+partpart

gt2 2

0π i

i ii i

i

i i

i

ip tp c

Dp t

Dt

jn05_Article 3 62205 100 PM Page 455

456 Journal of Economic Literature Vol XLIII (June 2005)

24 See Mark Armstrong (2002) for a survey of two-sidedcompetition

pricing games which are neither supermod-ular nor log-supermodular For example inthe multiproduct logit model of Richard HSpady (1984) best responses are increasingand there is a unique Bertrand equilibriumdespite the fact that payoffs are single-peaked (not quasi-concave) and neithersupermodular or log-supermodular in ownactions or prices Even so strategic com-plementarity across prices of differentfirms holds

A multimarket mixed oligopoly featuringproducts demand complements within thefirm as well as substitutes across firms pro-vides another example This situation is typ-ical of two-sided markets where two groupsof market participants benefit from interac-tion via a platform or intermediaryIntermediaries compete for business fromboth groups and set prices Examples arenumerous and include readersviewers andadvertisers in media markets cardholdersconsumers and merchantsretailers in pay-ment systems such as credit cards con-sumers and shops in shopping malls authorsand readers in academic journals borrowersand depositors in banking ldquosubscription to anetworkrdquo and ldquonumber of calls made to anetworkrdquo in telecom markets and in generalbuyers and sellers put together with the helpof intermediaries (in real estate financialproducts or auction markets) The interac-tion between the two sides gives rise to com-plementarities or externalities betweengroups that are not internalized by endusers For example a consumer who uses acredit card does not internalize the benefitthat it confers to the other side of the market(the merchants)

Consider a situation of two-sided exclusiveintermediation with two groups of partici-pants (say columnists and readers datingbars workers and firms in a single regionconsumers and shops in a mall) where eachparticipant joins one of the two existingintermediaries and where the utility derivedby a member of a group from joining a par-ticular intermediary is increasing in the

number of members of the other group join-ing the same intermediary24 When lineardemands arise from Hotelling-type prefer-ences for the intermediaries the result isthat prices charged by intermediaries arestrategic complements across firms butstrategic substitutes within the firm Themultimarket oligopoly game is therefore nota supermodular game as defined in section4 However best replies will be increasing aslong as the demand complementarity amongthe products of the same firmintermediaryis not very strong In the context of the lineardemand game with small and symmetric net-work effects best replies are increasing andthere is a unique symmetric equilibrium

An interesting result in the Hotellinggame where total demand is inelastic is thatan increase in the cross-group network effect(ie an increase in the degree of demandcomplementarity of the ldquoproductsrdquo of theintermediary) reduces equilibrium profitsAn increase in the impact of the benefits thatone side of the market confers on the otherwhen they go to an intermediary has in facta detrimental equilibrium effect on profitsThe reason is that the externality increasehas no positive direct impact on demand at asymmetric equilibrium in which the wholemarket is covered and it motivates eachintermediary to cut prices Since totaldemand stays constant (because it is priceinelastic) equilibrium profits decrease Thisresult can be generalized whenever (a) thedirect effect of the externality on demand atsymmetric equilibria is small so that profitsfor any intermediary have decreasing differ-ences in the price charged to a group (and inconsequence the externality parameter andbest replies shift inward as the externalityparameter increases) and (b) total demand isfixed (or it is quite price inelastic) so that theequilibrium price decrease translates into aprofit decrease In those circumstances thestrategic pricing effect dominates the direct

jn05_Article 3 62205 100 PM Page 456

Vives Complementarities and Games New Developments 457

25 Peitz (forthcoming) uses supermodular methods tostudy the effects of asymmetric access price regulation intelecom markets

effect (Cabral and Villas-Boas 2004)Economies of scope have a similar effectthan demand externalities25

6 Dynamic Games

This section will take a look at dynamicissues building on comparative statics resultsfor supermodular games (like result 5) thatpredict movements of equilibrium variableswhen a parameter changes

I examine first the conditions under whichincreasing or decreasing dominance occursin oligopolymdashthat is whether leaders or lag-gards have more incentives to invest This isparticularly relevant in situations whereinvestment today which could be a largerfirm size if there are learning effects andoradjustment costs affects competitive condi-tions tomorrow This application will illus-trate the power of the approach to isolate thedrivers of results and extend them beyondGSC (Susan Athey and Armin Schmutzler2001) I deal afterwards with full-blowndynamic Markov games and Markov perfectequilibria (MPE) First I tackle how staticcomplementarities translate into dynamiccomplementarities and use the methodologyto characterize MPE Conditions are giventhat enable contemporaneous (intraperiod)strategic complementarity (SC) andintertemporal (interperiod) SC to obtainThe relationships between static and dynam-ic strategic substitutability and complemen-tarity are studied in alternating move games(Eric Maskin and Jean Tirole 1987 1988ab)and in games with adjustment costs (Jun andVives 2004) Finally the problem of exis-tence and characterization of Markov per-fect equilibria is addressed (Laurent OCurtat 1996 Sleet 2001)

The outcome of the analysis are newresults uncovered (characterization ofdynamic strategic complementarity linkage

between static and dynamic complementari-ty concepts existence of MPE) and isolationof crucial assumptions in known results(increasing dominance monotonicity ofdynamic reaction functions in alternatingmove games)

61 Increasing or Decreasing Dominance

Suppose that the payoff to player i is givenby πi(aiai t) with t = (t1hellip tn) The param-eter ti is to be interpreted as the state vari-able or initial conditions of player i in thegame Let both actions and state variables beone-dimensional We would like to find con-ditions under which if two firms differ onlyin their state variables if and ti gt tj then atany equilibrium we have ai(t) ge aj(t) withthe interpretation being that an initial domi-nance is reinforced by actions of the firmsFor example in the presence of a learningcurve the firm that has accumulated moreoutput has incentive to produce more

Suppose that πi(aiai t) has increasingdifferences in (aiaj) for i ne j (strategic com-plementarity) and increasing differences in(ai(ti minusti)) Assume also that all the playershave the same strategy set and that the pay-offs are exchangeable (players do not careabout the identity of their opponents onlyabout their actions and payoff-relevantparameters or state variables) This meansthat the payoffs of two players are the sameif actions and state variables are exchangedamong them Suppose also that payoffs arestrictly quasi-concave so there is a uniquebest-response function for any player andthat we have an equilibrium for which(without loss of generality) a1 lt a2 with t1 gt t2 Fix the actions of the players n = 3hellip n at their equilibrium levelsBecause of strict quasi-concavity andexchangeability we can write the bestresponse of firm 1 as r(a2 t1 t2) and that offirm 2 as r(a1 t2 t1) Because of strategiccomplementarity and a1 lt a2 we have a1 = r(a2 t1 t2) ge r(a1 t2 t1) Since t1 gt t2 andsince πi(aiai t) has increasing differ-ences in (ai(ti minusti)) it follows that

jn05_Article 3 62205 100 PM Page 457

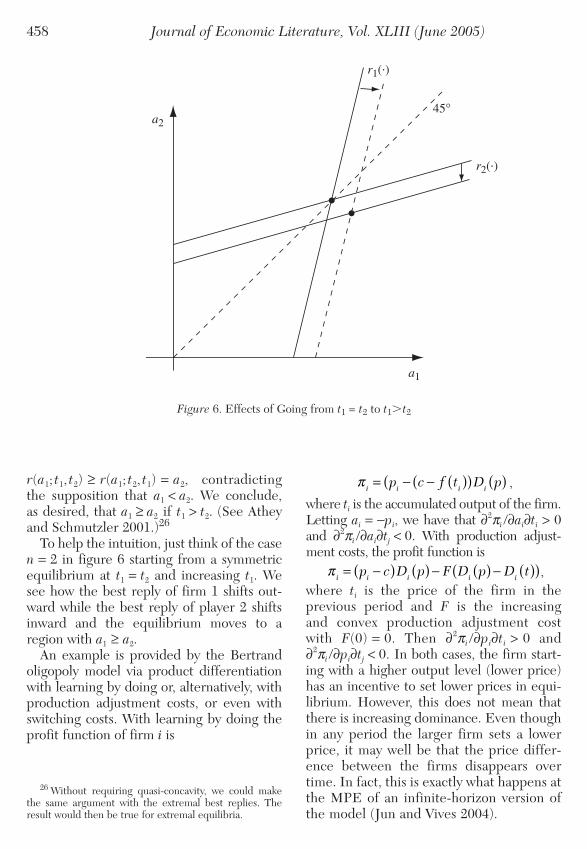

458 Journal of Economic Literature Vol XLIII (June 2005)

Figure 6 Effects of Going from t1 = t2 to t1t2

a2

r2()

r1()

45deg

a1

r(a1 t1 t2) ge r(a1 t2 t1) = a2 contradictingthe supposition that a1 lt a2 We conclude as desired that a1 ge a2 if t1 gt t2 (See Atheyand Schmutzler 2001)26

To help the intuition just think of the casen = 2 in figure 6 starting from a symmetricequilibrium at t1 = t2 and increasing t1 Wesee how the best reply of firm 1 shifts out-ward while the best reply of player 2 shiftsinward and the equilibrium moves to aregion with a1 ge a2

An example is provided by the Bertrandoligopoly model via product differentiationwith learning by doing or alternatively withproduction adjustment costs or even withswitching costs With learning by doing theprofit function of firm i is

where ti is the accumulated output of the firmLetting ai = minuspi we have that part2πi partaipartti gt 0and part2πi partaiparttj lt 0 With production adjust-ment costs the profit function is

where ti is the price of the firm in the previous period and F is the increasing and convex production adjustment costwith F(0) = 0 Then part2πi partpipartti gt 0 andpart2πi partpiparttj lt 0 In both cases the firm start-ing with a higher output level (lower price)has an incentive to set lower prices in equi-librium However this does not mean thatthere is increasing dominance Even thoughin any period the larger firm sets a lowerprice it may well be that the price differ-ence between the firms disappears overtime In fact this is exactly what happens atthe MPE of an infinite-horizon version ofthe model (Jun and Vives 2004)

π i i i i ip c D p F D p D t= minus( ) ( ) minus ( ) minus ( )( )

π i i i ip c f t D p= minus minus ( )(( ) ( )

26 Without requiring quasi-concavity we could makethe same argument with the extremal best replies Theresult would then be true for extremal equilibria

jn05_Article 3 62205 100 PM Page 458

Vives Complementarities and Games New Developments 459

27 This is so in the Avner Shaked and John Sutton(1982) model of vertical quality differentiation when themarket is covered However in the classical linearBertrand duopoly with product differentiation invest-ments in quality that raise the intercept of demand for theown product (Vives 1985a) or that increase the willingnessto pay by lowering the absolute value of the slope ofdemand |partDipartp|(Vives 1990b) are strategic complements

In the switching costs model (Alan WBeggs and Paul Klemperer 1992) firmscompete in prices and ti is the loyal customerbase of firm i In this case we have thatpart2πi partpipartti gt 0 because lowering prices ismore costly to a firm with a larger customerbase and part2πi partpiparttj lt 0 It then follows thata firm with a larger customer base will besofter in pricing This is to be interpreted asdecreasing dominance (and indeed theauthors show that at an MPE of the full-blown dynamic game initial asymmetries inmarket shares are eroded) However thereader is warned that in a dynamic gamefirms are forward looking and the continua-tion payoffs need not look like the static pay-offs Therefore the static dominance neednot translate in dominance in the dynamicgame We will show in the next section therelationships between static and dynamicproperties of payoffs

The result can be extended to the strategic substitutes case (where πi(aiai t)has decreasing differences in (aiaj) i ne j)with the restriction that minuspart2πi (partai)

2 gtpart2πi partaipartaj| i ne j (this implies that the profitfunction of any player is concave and that aduopoly game would have a unique equilib-rium) The conditions in the result for strate-gic substitutes are typically met when actionsare investments in cost reduction and also insome models of quality enhancement27

Then profits at the market stage as a functionof those investments display strategic substi-tutability both in Cournot and Bertrandmodels The result can also be used to showthat learning by doing in a Cournot marketleads to increasing dominance That is thefirm that is ahead of the learning curveremains ahead because it has incentives to

28 A similar example with product differentiation andnetwork demand externalities (Michael L Katz and CarlShapiro 1986) would have πi = (Pi(q) minus (c minus ƒ(ti))qi whereq is the vector of output levels of the firms and ti is the accumulated sales of product i

produce more Actions are current rates ofoutput and state variables are the inheritedaccumulated production of each firm Letthe profit function of firm i be given by

Here P is the inverse demand Q is totaloutput ƒ is the learning curve a differ-entiable and concave function of totalaccumulated output of the firm ti with ƒ gt0 and qi is its current output level Ifinverse demand is log-concave then bestreplies are downward sloping (strategicsubstitutes) Furthermore part2πi partqipartti =ƒ gt 0 and part2πi partqiparttj = 0 As a conse-quence ti gt tj implies that at the (unique)Cournot equilibrium qi(t) ge qj(t)

28

62 Markov Games

An important issue is how static comple-mentarities translate (or not) into dynamiccomplementarities In this section we willexplore the issue in the context of discretetime Markov games A Markov strategydepends only on (state) variables denoted ythat condense the direct effect of the past onthe current payoff Let the current payoff ofplayer i be πi(xy) where x is the currentaction profile vector and y is the state evolv-ing according to y = ƒ(xmacrymacr) where xmacr and ymacrare (respectively) the lagged action profilevector and the lagged state A Markov per-fect equilibrium (MPE) is a subgame-perfect equilibrium in Markov strategiesThat is an MPE is a set of strategies optimalfor any firm and for any state of systemgiven the strategies of rivals

What do we mean by dynamic strategiccomplementarity (SC) or dynamic strategicsubstitutability (SS) We can think of ldquocon-temporaneousrdquo SC when the value function atan MPE Vi(y) displays SC (Vi has increasingdifferences in (yiyndashi)) We can think of

π i i iP Q c f t q= ( ) minus minus ( )( )(

jn05_Article 3 62205 100 PM Page 459