Embed Size (px)

Citation preview

B104 (FORM 104) (08/07)

ADVERSARY PROCEEDING COVER SHEET (Instructions on Reverse)

ADVERSARY PROCEEDING NUMBER (Court Use Only)

PLAINTIFFS DEFENDANTS

ATTORNEYS (Firm Name, Address, and Telephone No.)

ATTORNEYS (If Known)

PARTY (Check One Box Only) � Debtor � U.S. Trustee/Bankruptcy Admin � Creditor � Other � Trustee

PARTY (Check One Box Only) � Debtor � U.S. Trustee/Bankruptcy Admin � Creditor � Other � Trustee

CAUSE OF ACTION (WRITE A BRIEF STATEMENT OF CAUSE OF ACTION, INCLUDING ALL U.S. STATUTES INVOLVED)

NATURE OF SUIT (Number up to five (5) boxes starting with lead cause of action as 1, first alternative cause as 2, second alternative cause as 3, etc.)

FRBP 7001(1) – Recovery of Money/Property � 11-Recovery of money/property - §542 turnover of property � 12-Recovery of money/property - §547 preference � 13-Recovery of money/property - §548 fraudulent transfer � 14-Recovery of money/property - other FRBP 7001(2) – Validity, Priority or Extent of Lien � 21-Validity, priority or extent of lien or other interest in property FRBP 7001(3) – Approval of Sale of Property � 31-Approval of sale of property of estate and of a co-owner - §363(h) FRBP 7001(4) – Objection/Revocation of Discharge � 41-Objection / revocation of discharge - §727(c),(d),(e) FRBP 7001(5) – Revocation of Confirmation � 51-Revocation of confirmation FRBP 7001(6) – Dischargeability � 66-Dischargeability - §523(a)(1),(14),(14A) priority tax claims � 62-Dischargeability - §523(a)(2), false pretenses, false representation, actual fraud � 67-Dischargeability - §523(a)(4), fraud as fiduciary, embezzlement, larceny

(continued next column)

FRBP 7001(6) – Dischargeability (continued) � 61-Dischargeability - §523(a)(5), domestic support � 68-Dischargeability - §523(a)(6), willful and malicious injury � 63-Dischargeability - §523(a)(8), student loan � 64-Dischargeability - §523(a)(15), divorce or separation obligation (other than domestic support) � 65-Dischargeability - other

FRBP 7001(7) – Injunctive Relief � 71-Injunctive relief – imposition of stay � 72-Injunctive relief – other FRBP 7001(8) Subordination of Claim or Interest � 81-Subordination of claim or interest FRBP 7001(9) Declaratory Judgment � 91-Declaratory judgment FRBP 7001(10) Determination of Removed Action � 01-Determination of removed claim or cause Other � SS-SIPA Case – 15 U.S.C. §§78aaa et.seq. � 02-Other (e.g. other actions that would have been brought in state court

if unrelated to bankruptcy case)

� Check if this case involves a substantive issue of state law � Check if this is asserted to be a class action under FRCP 23 � Check if a jury trial is demanded in complaint Demand $ Other Relief Sought

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 1 of 80

Brian A. Bash, Trustee for Fair Finance Company James F. Cochran and Susan J. Cochran

Alexis C. Osburn, Esq. - Baker & Hostetler, PNC Center,1900 East Ninth Street, Suite 3200, Cleveland, Ohio 44114-3482,216.621.0200

✔

✔

Complaint to Recover Fraudulent Transfer and Breach of Contract Claims

✔

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 2 of 80

UNITED STATES BANKRUPTCY COURTNORTHERN DISTRICT OF OHIO

EASTERN DIVISION

In re:

FAIR FINANCE COMPANY,

Debtor.

BRIAN A. BASH, CHAPTER 7 TRUSTEE,

Plaintiff,

vs.

JAMES F. COCHRAN13483 Marjac WayMcCordsville, Indiana 46055

and

SUSAN J. COCHRAN13483 Marjac WayMcCordsville, Indiana 46055,

Defendants.

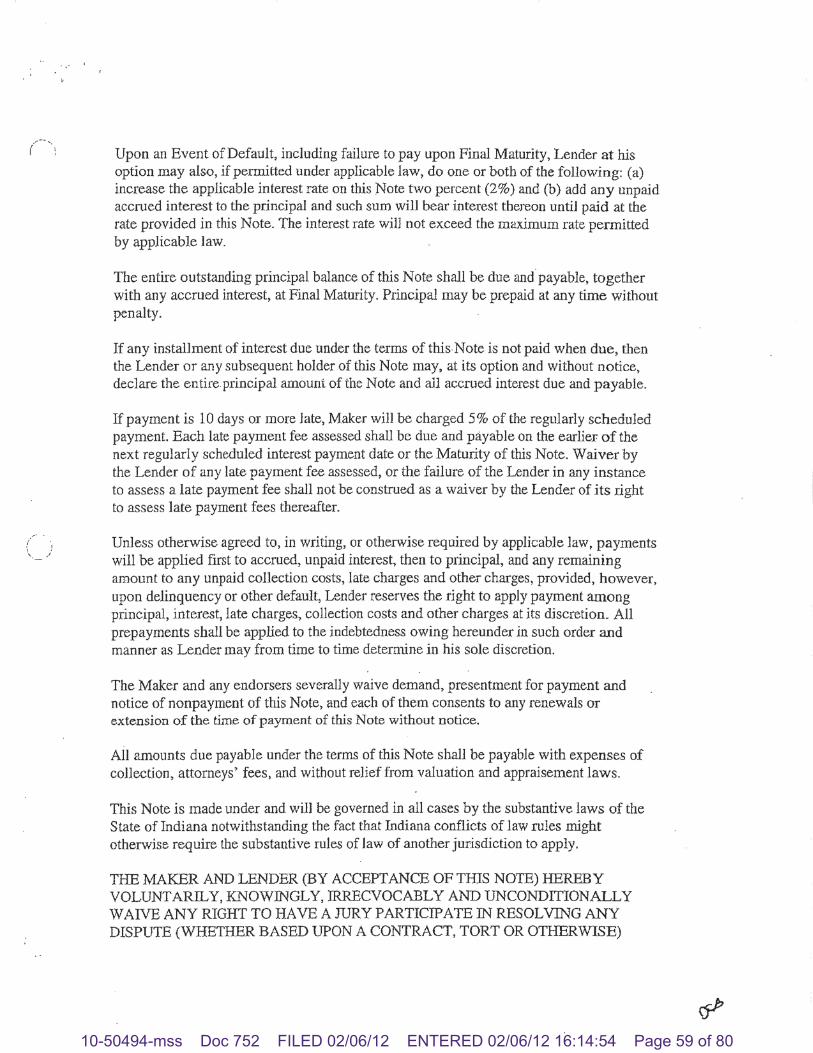

))))))))))))))))))))))))

Case No. 10-50494

Chapter 7

Judge Marilyn Shea-Stonum

Adv. Pro. No. _____________

COMPLAINT

Plaintiff Brian A. Bash (the “Trustee”), the duly appointed Chapter 7 trustee for Fair

Finance Company (“Fair Finance” or the “Debtor”) in the above-captioned case, hereby files

this Complaint against defendants James F. Cochran (“Cochran”) and Susan J. Cochran

(together with Cochran, the “Defendants”). In support of the requested relief, the Trustee states

the following, on information and belief, together and in the alternative:

PRELIMINARY STATEMENT

1. This adversary proceeding arises from a large Ponzi scheme perpetrated through

the Debtor by Timothy Durham (“Durham”), and other individuals, including Cochran. As a

result, Ohio residents who purchased Fair Finance V-Notes lost over $200 million. The Trustee

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 3 of 80

-2-

has diligently tried to unravel the Ponzi scheme involving the loans and transfers of the Debtor’s

assets, including the transfers discussed herein.

2. Durham and other individuals, including Cochran, funneled this money through

the Debtor’s parent and grandparent companies, Fair Holdings, Inc. (“Fair Holdings”) and DC

Investments LLC (“DCI,” and together with the Debtor and Fair Holdings, the “Fair Entities”).

Durham also funneled money to persons and entities affiliated with and/or owned or controlled

by Durham or Cochran (the “Related Parties”), including Obsidian Enterprises, Inc.

(“Obsidian”), as well as a number of officers and directors of those companies, including

himself, Cochran, Terry Whitesell and Jeffrey Osler, among other individuals. Durham and

Cochran have been charged by federal prosecutors for their role in the Fair Finance Ponzi

scheme, and they are awaiting federal criminal trial in Indiana.

3. Utilizing their insider positions at the involved companies, these individuals,

including Cochran, actively concealed and disguised their wrongful conduct and the transfers of

the Debtor’s assets, including the transfers and loans discussed herein, effectively preventing

their discovery until no earlier than the Petition Date.

4. The Defendants received money from the Fair Entities of more than $9 million in

loans or transfers. The Defendants also guaranteed loans made by the Fair Entities that are

currently in default. This action is brought to recover those monies for the benefit of the

Debtor’s estate.

JURISDICTION AND VENUE

5. This is an adversary proceeding commenced before the same Court in which the

Fair Finance bankruptcy case is pending – the Bankruptcy Court for the Northern District of

Ohio, Case No. 10-50494. This Court has jurisdiction over this adversary proceeding pursuant to

28 U.S.C. §§ 157(b) and 1334 and Rule 7001 of the Federal Rules of Bankruptcy Procedure.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 4 of 80

-3-

6. This matter is a core proceeding pursuant to 28 U.S.C. § 157(b).

7. Venue in this Court is proper pursuant to 28 U.S.C. § 1409.

PARTIES

8. Brian A. Bash is the duly appointed and acting Chapter 7 trustee for the Debtor.

9. Upon information and belief, defendant James F. Cochran is an individual

currently residing in McCordsville, Indiana. Cochran was a director and Chairman of the Board

of the Debtor at all times relevant to this Complaint. Cochran was also a director and officer of

Fair Holdings and a member of DCI at all times relevant to this Complaint.

10. Upon information and belief, defendant Susan J. Cochran is an individual

currently residing in McCordsville, Indiana. Upon information and belief, Mrs. Cochran is

Cochran’s wife.

PROCEDURAL BACKGROUND

11. On February 8, 2010 (the “Petition Date”), creditor-investors (the “Petitioning

Creditors”) filed a petition for involuntary bankruptcy against the Debtor.

12. On the Petition Date, the Petitioning Creditors also filed an “Emergency Motion

to Appoint Interim Trustee” (Dkt. No. 2) alleging that a trustee was needed to oversee the

operations of the Debtor because (i) the Debtor had failed to make timely payments on its debts,

including failing to redeem matured V-Notes and failing to pay interest on unmatured V-Notes;

(ii) the Debtor and several affiliated companies had been raided by the FBI in November of

2009; (iii) the Debtor had not been open to the public since the raid; and (iv) public records

revealed that the Debtor had made “unusually large” loans to insiders.

13. On February 19, 2010, this Court entered an Order directing the United States

Trustee to appoint an interim trustee (Dkt. No. 25).

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 5 of 80

-4-

14. On February 24, 2010, the Debtor filed notice that it consented to the entry of an

order for relief in the bankruptcy proceeding (Dkt. No. 35).

15. On March 2, 2010, the Court entered an Order granting the relief sought by the

Petitioning Creditors nunc pro tunc as of February 24, 2010 (Dkt. No. 40).

16. On March 2, 2010, the United States Trustee filed the Notice of Appointment of

Interim Chapter 7 Trustee nunc pro tunc, effective February 24, 2010 (Dkt. No. 41).

17. By agreements executed as of June 13, 2010, the Debtor’s parent entities, Fair

Holdings and DCI, each assigned to the Trustee all of their respective rights, title and interest in

and to their respective property, including, among other things, all accounts and notes receivable

(the “Assignments”).

18. On June 16, 2010, this Court entered an Order (the “Compromise Order”)

approving the Assignments between the Trustee, Fair Holdings and DCI (Dkt. No. 188).

19. As a result of the Assignments and the Compromise Order, the Trustee has the

right to enforce the Defendants’ obligations to DCI and Fair Holdings and to pursue DCI’s and

Fair Holdings’ claims against the Defendants for the benefit of the Debtor’s estate and its

creditors.

SIGNIFICANT NON-PARTIES

20. Fair Holdings is an Ohio corporation that had a principal place of business in

Akron, Ohio. Durham and Cochran formed Fair Holdings for the sole purpose of purchasing all

of the common shares of the Debtor. Fair Holdings is the sole shareholder of the Debtor.

21. DCI is an Indiana limited liability company that had a principal place of business

in Indianapolis, Indiana. DCI is the sole shareholder of Fair Holdings. Durham and Cochran

each own a 50% share of DCI.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 6 of 80

-5-

22. Fair Holdings and DCI primarily served as conduits for Durham and Cochran to

loan the Debtor’s money to themselves, their friends, privileged insiders, and Related Parties.

Fair Holdings and DCI had no significant source of income and conducted no business other than

drawing money out of the Debtor through purported “loans” and other transfers. In many cases,

the Debtor would purportedly “loan” money to Fair Holdings, which would, in turn, “loan”

money to DCI. The money siphoned from the Debtor, through Fair Holdings and DCI, was then

transferred out in more purported “loans” to others, mainly Related Parties, including loans to

Durham and Cochran.

23. Obsidian is a Delaware corporation that had a principal place of business in

Indianapolis, Indiana. Obsidian is a holding company founded and controlled by Durham. It

conducted no significant business other than to own subsidiaries controlled by Durham, borrow

money from the Fair Entities and lend those borrowed funds to Obsidian’s subsidiaries and

privileged insiders.

24. CLST Holdings, Inc. (“CLST”) is a Delaware corporation with a principal place

of business in Dallas, Texas. Durham has been Chairman of the Board and a significant

shareholder of CLST since 2007. Durham and Cochran benefited personally when CLST

purchased various accounts receivable from the Debtor.

THE FAIR FINANCE PONZI SCHEME

I. Durham and Cochran Purchase the Debtor to Siphon Money From the Debtor to Durham, Cochran and Durham’s Failing Business Ventures

25. The Debtor was founded in 1934 by Arthur Ray Fair and was operated by the Fair

family until its purchase by Durham and Cochran in 2002. Originally, the Debtor was an Akron,

Ohio-based factoring company that provided dealers and merchants with sales financing

services. To fund these services, the Debtor borrowed money by issuing V-Notes to local

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 7 of 80

-6-

individuals and used the proceeds to purchase accounts receivable. For simplicity, purchasers of

V-Notes will be referred to as “investors;” however, these investors held only debt, not equity.

26. Durham and Cochran established Fair Holdings to purchase the Debtor in January

of 2002. At all times relevant to this Complaint, Cochran was a director and Chairman of the

Board of the Debtor, a director and officer of Fair Holdings and a member of DCI.

27. Before Fair Holdings purchased the Debtor, the Debtor was very well capitalized,

with approximately $14 million of shareholder equity on its balance sheet, representing a healthy

25% asset to equity ratio.

28. After Durham and Cochran purchased the Debtor in 2002, they shifted the

Debtor’s primary business away from factoring, instead using the Debtor to make loans to Fair

Holdings and DCI. Fair Holdings and DCI would then make further loans to Related Parties,

such as Durham, Cochran, Obsidian and many other failed or failing businesses owned or

controlled by Durham.

29. Durham and Cochran used the Fair Entities to fund Durham’s failing businesses at

Obsidian and to fund their personal investments. Durham had steered Obsidian into dire straits

by the time he purchased the Debtor. According to Obsidian’s SEC filings, it lost $5.8 million in

the thirteen months before January 31, 2002. Obsidian never turned a profit thereafter.

30. Obsidian was able to pay for its unrelenting losses and its later acquisitions only

because Durham, who also was Obsidian’s CEO, Chairman of the Board and dominant

shareholder, purchased the Debtor and caused the Debtor to fund them. Within two days of

purchasing the Debtor, Durham caused the Fair Entities to extend a $3 million line of credit to

Obsidian with no payments due for several years. Within a year, Obsidian and its subsidiaries

incurred approximately $7.5 million in debts to the Fair Entities. The outstanding loans owed to

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 8 of 80

-7-

the Fair Entities grew to $30 million within fifteen months and $40 million within two years of

Durham’s and Cochran’s purchase of the Debtor.

II. Durham Runs the Debtor as a Ponzi Scheme

31. Starting in 2002, Durham used the Debtor’s funds to support his other businesses,

finance his own speculation in stocks, and finance his lavish lifestyle. Durham and Cochran

repeatedly ordered the transfer of significant sums of money from the Debtor to themselves,

either directly or through an insider or Related Party. For instance, in 2008 and 2009 alone,

Durham and Cochran authorized at least 200 requests to wire money from the Debtor to

Durham-related entities or Related Parties. Furthermore, Durham took millions of dollars in

personal, assumed and guaranteed loans through early 2010.

32. The outstanding balance of the various loans made by the Fair Entities to Durham

and Cochran since 2002 is in excess of $30 million and $10 million, respectively. Durham and

Cochran took these loans knowing they would never repay them, as evidenced by the fact that

they repeatedly caused the Fair Entities to raise the principal balance on their notes and extend

the maturity dates without requiring any payments of principal or interest.

33. According to a consolidated audit report drafted, but never issued, for fiscal year

2002, the Debtor and Fair Holdings lost money starting with Durham’s first year of control over

the Debtor. As of no later than 2003, Fair Holdings was in breach of its loan covenants with its

major lender because it, among other things, failed to provide timely audits, took on unapproved

debt, and purchased stock in related parties. The Debtor’s auditors, BGBC Partners, P.C.

(“BGBC”), refused to sign off on the Debtor’s financial statements after fiscal year 2002, and

were fired in 2005 without having completed audits for fiscal years 2003 and 2004. Those audits

were issued in the summer of 2005 by a different auditor, Somerset CPAs (“Somerset”), which

would not issue any further audit reports. After 2005, Durham decided the Debtor and Fair

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 9 of 80

-8-

Holdings would only submit to “reviews,” which relied on management’s assertions about the

condition of the companies.

34. By the end of 2005, at the latest, the Debtor was insolvent by at least $50 million

and Durham was operating the Debtor as a Ponzi scheme. By that point, if not significantly

earlier, the Debtor did not have the money to redeem or pay interest on existing V-Notes without

using proceeds from V-Notes purchased by new investors.

35. Despite the Debtor’s insolvency and the Fair Entities’ rapidly deteriorating

financial conditions, Durham did not stop using the Fair Entities to make loans to Related

Parties. Even after it became clear that the Debtor was doomed, Durham did not liquidate the

Debtor at a time when creditors could have realized a significant recovery. Instead, Durham

fired auditors who became too squeamish and operated the Debtor as a Ponzi scheme, enabling

Durham, Cochran and others to continue stealing money from innocent investors. Durham

himself admitted to the Debtor’s attorney in 2008 that between 89% and 93% of new money

brought in from investors was “used to repay” debts to other investors.

36. The FBI raided the Debtor on November 24, 2009, suspecting that the Debtor was

being operated as a Ponzi scheme. By the time the Trustee was appointed, the Debtor only had

approximately one-tenth of a cent in liquid assets for every dollar of unsecured debt.

THE FAIR ENTITIES MAKE INSIDER LOANS TO COCHRAN AND ENTITIES RELATED TO COCHRAN

I. DCI Extends a $10 Million Line of Credit to Cochran

A. The Cochran Note

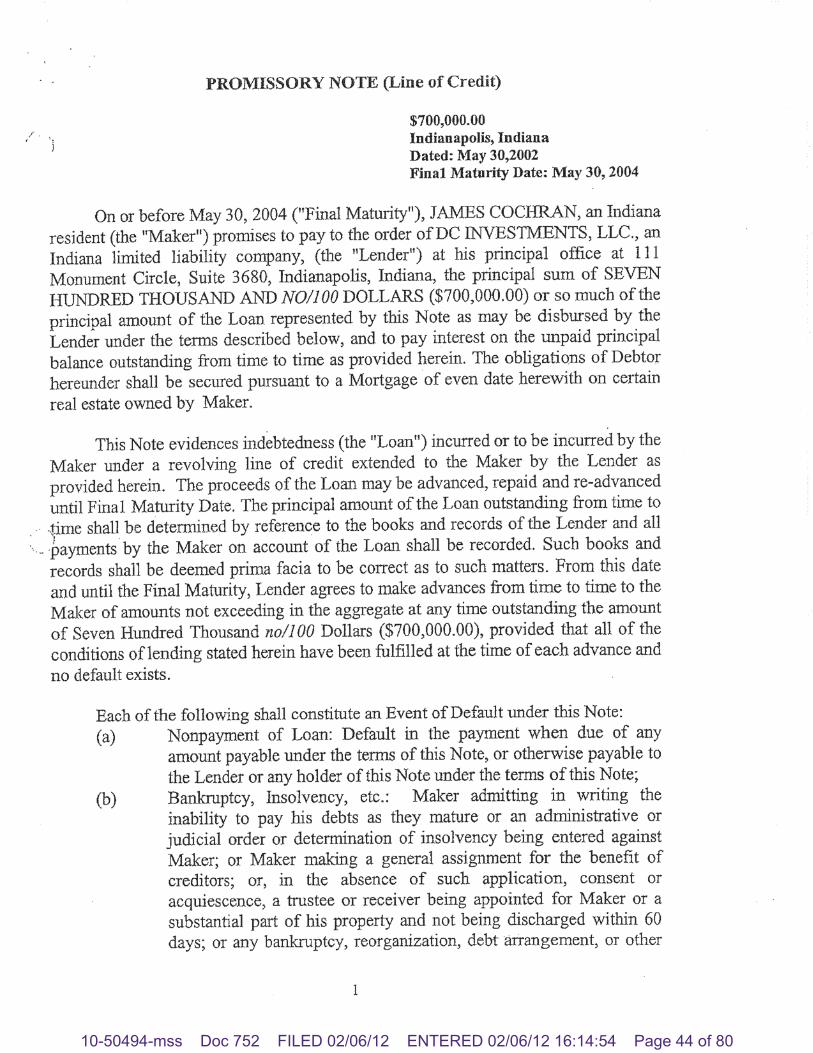

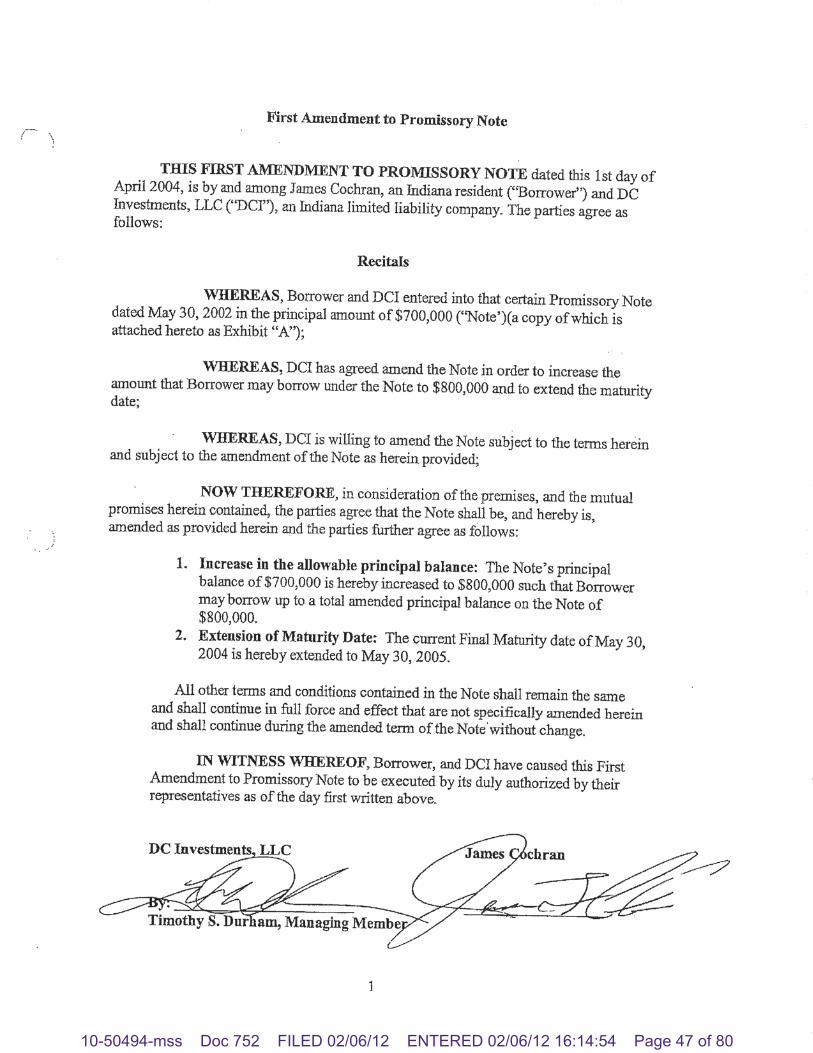

37. On or about May 30, 2002, Cochran executed a certain Promissory Note (Line of

Credit) in favor of DCI (the “Original Cochran Note”), pursuant to which DCI agreed to extend

Cochran a line of credit up to an original principal amount of $700,000. On or about April 1,

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 10 of 80

-9-

2004, Cochran executed a First Amendment to Promissory Note (the “First Amended Cochran

Note”), pursuant to which DCI increased the principal amount available under the Original

Cochran Note to $800,000 and extended the maturity date. On or about December 1, 2004,

Cochran executed a First (sic) Amendment to Promissory Note (the “Second Amended Cochran

Note”),1 pursuant to which DCI increased the principal amount available under the First

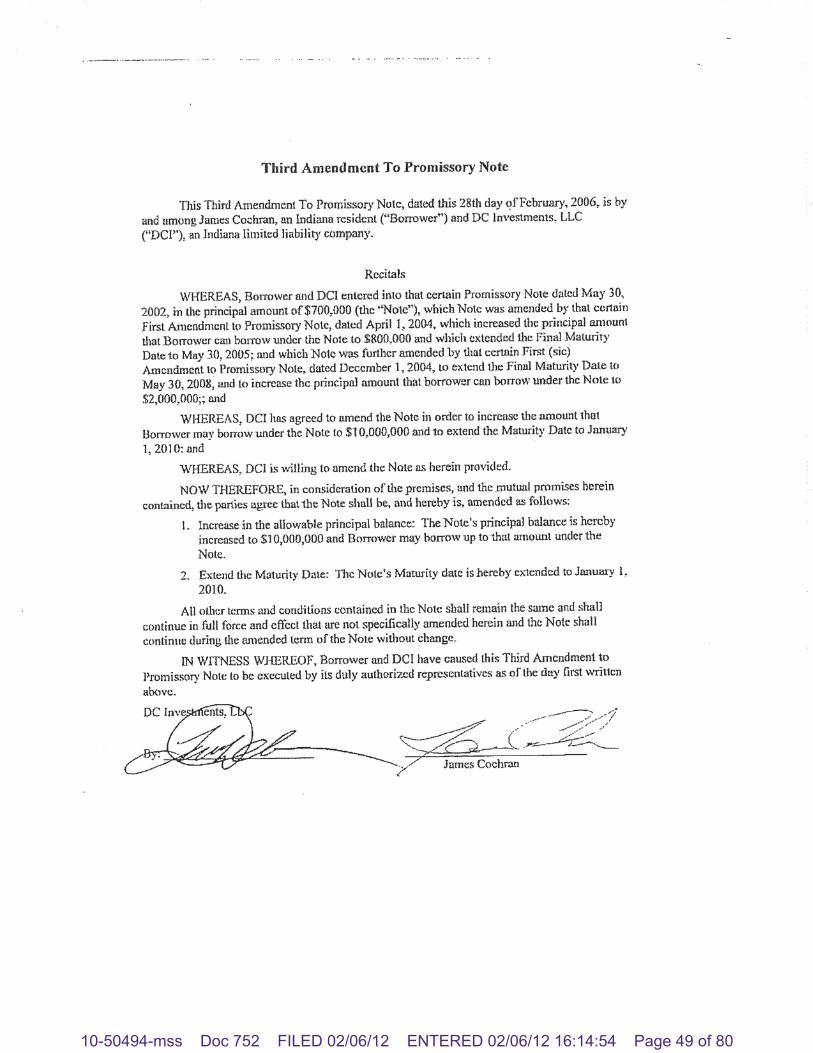

Amended Cochran Note to $2 million and extended the maturity date. On or about February 28,

2006, Cochran executed a Third Amendment to Promissory Note (the “Third Amended

Cochran Note,” and together with the Original Cochran Note, First Amended Cochran Note and

Second Amended Cochran Note, the “Cochran Note”), pursuant to which DCI increased the

principal amount available under the Second Amended Cochran Note to $10 million and

extended the maturity date. A true and correct copy of the Cochran Note, and all amendments

thereto, is attached to this Complaint as Exhibit A and is incorporated herein by reference.

38. Under the Cochran Note, the unpaid principal balance and accrued, unpaid

interest for the Cochran Note was due and payable on January 1, 2010 (the “Cochran Note

Maturity Date”).

39. Under the Cochran Note, the unpaid principal balance bears interest at 1% above

the interest rate being paid by the Debtor on its V-6 Notes. In the event of a default under the

Cochran Note, the unpaid principal balance bears interest at the default interest rate of 3% above

the interest rate being paid by the Debtor on its V-6 Notes. In the event of a default under the

1 The Second Amended Cochran Note is mistakenly titled First Amendment to Promissory Note when it should be titled Second Amendment to Promissory Note. This mistake is noted in the Third Amended Cochran Note (as defined herein), where the Second Amended Cochran Note is referred to as “that certain First (sic) Amendment to Promissory Note, dated December 1, 2004, to extend the Final Maturity Date to May 30, 2008, and to increase the principal amount that borrower can borrow under the Note to $2,000,000.” The fact that the Second Amended Cochran Note is mistitled does not affect Cochran’s obligations under the Second Amended Cochran Note.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 11 of 80

-10-

Cochran Note, any accrued and unpaid interest may be added to the principal, with the total sum

bearing interest at the default rate of interest identified in the Cochran Note.

40. Under the Cochran Note, payment of all accrued and unpaid interest was due and

payable monthly on the first day of the month beginning June 1, 2002, and continuing thereafter

until the Cochran Note Maturity Date. If any installment of interest due under the Cochran Note

is not paid when due, the entire principal amount and all accrued interest may be declared

immediately due and payable without notice.

41. Under the Cochran Note, Cochran expressly waived demand, presentment for

payment and notice of nonpayment of the Cochran Note.

42. Under the Cochran Note, Cochran agreed to pay all costs of collection, including,

but not limited to, reasonable attorneys’ fees.

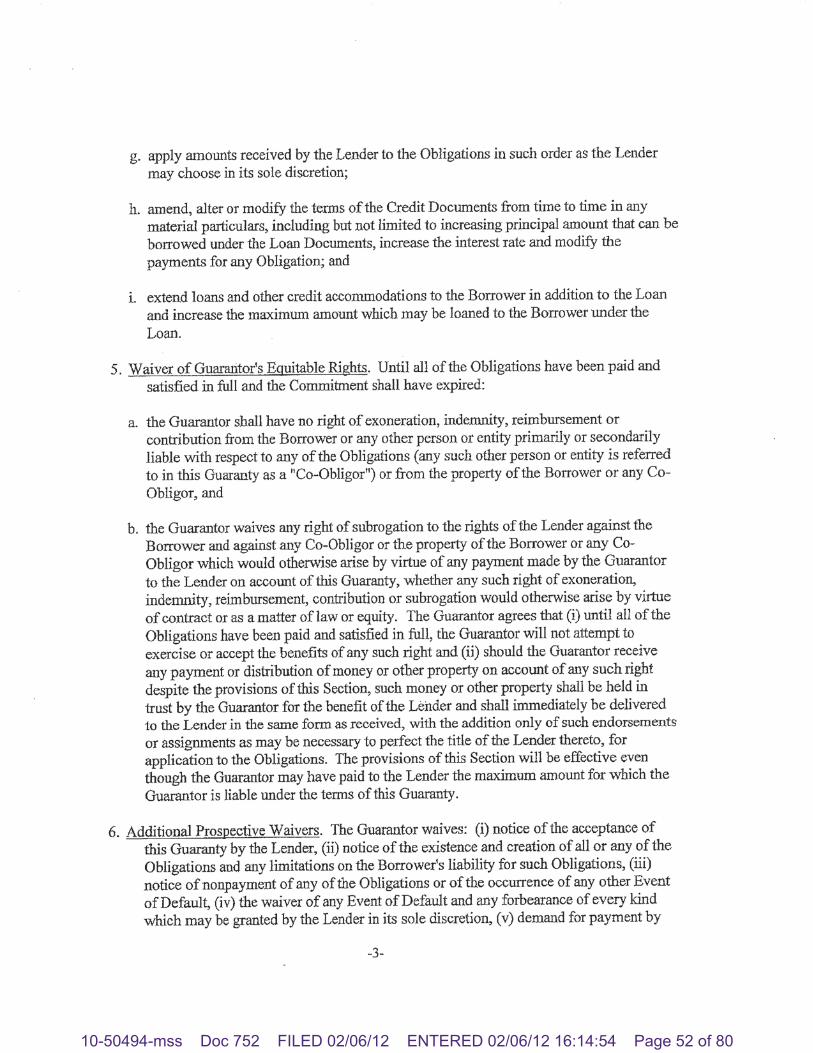

B. Mrs. Cochran Guaranties the Cochran Note

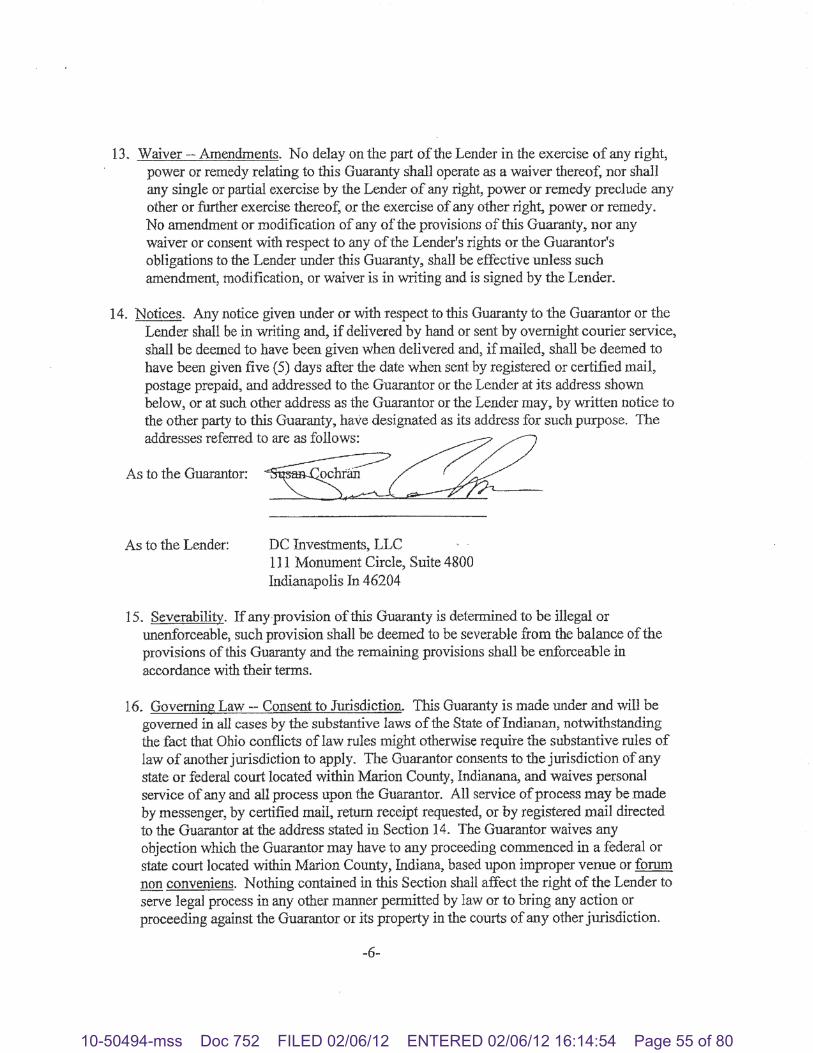

43. On or about December 1, 2004, Mrs. Cochran executed a Continuing Personal

Guaranty Agreement in favor of DCI (the “Cochran Note Guaranty”), pursuant to which Mrs.

Cochran unconditionally guaranteed all of the indebtedness and other obligations owing from

Cochran to DCI, including, but not limited to, the Cochran Note, existing or arising after the

execution of the Cochran Note Guaranty. A true and correct copy of the Cochran Note Guaranty

is attached to this Complaint as Exhibit B and is incorporated herein by reference.

44. Under the Cochran Note Guaranty, Mrs. Cochran expressly waived all rights to

indemnity, contribution and reimbursement from Cochran, notice of the existence or creation of

obligations under the Cochran Note, notice of nonpayment or an event of default under the

Cochran Note, and demand, presentment for payment and notice of nonpayment of the Cochran

Note or Cochran Note Guaranty.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 12 of 80

-11-

45. Under the Cochran Note Guaranty, Mrs. Cochran agreed to pay all costs of

collection, including, but not limited to, reasonable attorneys’ fees.

C. The Defendants Secure the Cochran Note with a Security Agreement and Mortgages

46. The Cochran Note is secured by a Security Agreement dated December 1, 2004

(the “Cochran Note Security Agreement”), pursuant to which the Defendants granted DCI a

security interest in “any and all assets of the [Defendants] owned now or in the future along with

any proceeds thereof.”

47. The Cochran Note is secured by two mortgages. It is secured by a Mortgage

dated April 16, 2003, as amended by an Amendment to Mortgage dated June 26, 2003, Second

Amendment to Mortgage dated April 1, 2004, and a Third Amendment to Mortgage dated

December 1, 2004 (together, the “Indiana Mortgage”). The Cochran Note is also secured by a

Mortgage dated December 1, 2004 (the “Florida Mortgage”).

II. The Defendants Guaranty a $234,666.75 Loan to HSE Hockey

A. The HSE Note

48. HSE Hockey Club, Inc. (“HSE Hockey”) is a non-profit corporation organized

under the laws of the State of Indiana. Upon information and belief, HSE Hockey is an

organization that sponsors youth hockey events. Upon information and belief, Cochran is, or

was at one time, on the board of HSE Hockey.

49. On or about July 14, 2004, HSE Hockey executed a Promissory Note in favor of

DCI (the “HSE Note”), pursuant to which DCI loaned HSE Hockey the principal amount of

$234,666.75. A true and correct copy of the HSE Note is attached to this Complaint as Exhibit

C and is incorporated herein by reference.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 13 of 80

-12-

50. On or about July 31, 2007, DCI assigned several outstanding loans, including the

HSE Note (together, the “DCI Loan Assignment Accounts”), to Fair Holdings, which

immediately transferred those loans to the Debtor (the “DCI Loan Assignment”). Upon

information and belief, Durham and Cochran caused DCI to assign the DCI Loan Assignment

Accounts to Fair Holdings, and Fair Holdings to assign those accounts to the Debtor, in order to

create the illusion that DCI and Fair Holdings were paying down their intercompany loan

balances. Prior to the DCI Loan Assignment, Fair Holdings was overdrawn on its $115 million

loan account with the Debtor by approximately $40 million. As part of the DCI Loan

Assignment, Fair Holdings was credited for the face value of the DCI Loan Assignment

Accounts. As a result, Fair Holdings was no longer overdrawn on its loan account with the

Debtor. Upon information and belief, while documents memorializing the DCI Loan

Assignment were drafted, Durham and Cochran never caused the Fair Entities to execute the

DCI Loan Assignment documents. Nonetheless, (i) the Fair Entities agreed that the DCI Loan

Assignment Accounts, including the HSE Note, were assigned to the Debtor, (ii) the Fair Entities

intended that the DCI Loan Assignment Accounts, including the HSE Note, be assigned to the

Debtor, (iii) the assignment of the HSE Note is reflected in the Fair Entities’ books, and (iv) the

Fair Entities treated the DCI Loan Assignment Accounts, including the HSE Note, as if they

were assigned.

51. Under the HSE Note, the unpaid principal balance and accrued, unpaid interest for

the HSE Note is due and payable on August 15, 2019 (the “HSE Note Maturity Date”).

52. Under the HSE Note, the unpaid principal balance bears interest at 5.25% per

annum. Upon an event of default under the HSE Note, which includes failure to make required

payments under the HSE Note, the unpaid principal balance bears interest at the default interest

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 14 of 80

-13-

rate of 7.25% per annum. After an event of default under the HSE Note, any accrued and unpaid

interest may be added to the principal, with the total sum bearing interest at the default rate of

interest identified in the HSE Note.

53. Under the HSE Note, payment of all accrued and unpaid interest is due and

payable annually on the first day of May, beginning May 1, 2005, and continuing thereafter until

the HSE Note Maturity Date. If any installment of interest due under the HSE Note is not paid

when due, the entire principal amount and all accrued interest may be declared immediately due

and payable without notice.

54. Under the HSE Note, HSE Hockey expressly waived demand, presentment for

payment and notice of nonpayment of the HSE Note.

55. Under the HSE Note, HSE Hockey agreed to pay all costs of collection, including,

but not limited to, reasonable attorneys’ fees.

B. The Defendants Guaranty the HSE Note

56. On or about August 1, 2004, the Defendants executed a Personal Guaranty

Agreement in favor of DCI (the “HSE Note Guaranty”), pursuant to which the Defendants

unconditionally guaranteed all of the indebtedness and other obligations owing from HSE

Hockey to DCI, including, but not limited to, the HSE Note, existing or arising after the

execution of the HSE Note Guaranty. A true and correct copy of the HSE Note Guaranty is

attached to this Complaint as Exhibit D and is incorporated herein by reference.

57. Under the HSE Note Guaranty, the Defendants expressly waived all rights to

indemnity, contribution and reimbursement from HSE Hockey, notice of the existence or

creation of obligations under the HSE Note, notice of nonpayment or an event of default under

the HSE Note, and demand, presentment for payment and notice of nonpayment of the HSE Note

or HSE Note Guaranty.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 15 of 80

-14-

58. Under the HSE Note Guaranty, the Defendants agreed to pay all costs of

collection, including, but not limited to, reasonable attorneys’ fees.

THE DEFENDANTS DEFAULT ON THEIR OBLIGATIONS TO THE FAIR ENTITIES

I. The Defendants Default Under the Cochran Note and Cochran Note Guaranty

59. The entire outstanding principal balance of the Cochran Note, together with all

accrued and unpaid interest, was due and payable on January 1, 2010, the Cochran Note Maturity

Date.

60. The Defendants defaulted under the terms of the Cochran Note and Cochran Note

Guaranty, by, among other things, failing to repay the entire indebtedness due under the Cochran

Note by the Cochran Note Maturity Date.

61. The principal balance due and owing on the Cochran Note is at least

$8,444,312.60. The outstanding accrued interest due and owing on the Cochran Note is at least

$2,161,804.74, as of December 31, 2011, and interest continues to accrue at the default interest

rate set forth in the Cochran Note.

II. The Defendants Default Under the HSE Note Guaranty

62. The payment of all accrued and unpaid interest on the HSE Note is due and

payable annually on the first day of May, beginning as of May 1, 2005 and continuing thereafter

until the HSE Note Maturity Date. If any installment of interest due under the HSE Note is not

paid when due, the entire principal amount and all accrued interest may be declared immediately

due and payable without notice

63. HSE Hockey defaulted under the terms of the HSE Note by, among other things,

failing to make annual interest payments required under the HSE Note. Pursuant to the terms of

the HSE Note, the Debtor declares the entire principal amount and all accrued interest

immediately due and payable without notice.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 16 of 80

-15-

64. The Defendants defaulted under the terms of the HSE Note Guaranty by, among

other things, failing to repay all outstanding amounts due under the HSE Note upon default.

65. The principal balance due and owing on the HSE Note is at least $144,145.54.

The outstanding accrued interest due and owing on the HSE Note is at least $13,982.83, as of

December 31, 2009, and interest continues to accrue at the default interest rate set forth in the

HSE Note.

THE TRANSFERS TO THE DEFENDANTS

I. The Debtor Transfers $108,000 Worth of Accounts to Cochran in Connection with the CLST Sale

66. CLST was a cell phone distributor until it sold substantially all of its assets in

2006. Since selling its assets, CLST has had few, if any, employees other than its directors.

CLST’s directors have effectively acted in managerial roles since 2007. Durham has been

Chairman of the Board and a significant shareholder of CLST since 2007.

67. In 2009, Durham engineered a sale (the “CLST Sale”) whereby the Debtor sold

certain accounts receivable with a face value of approximately $3.7 million to CLST in exchange

for cash payments, stock in CLST, and notes. CLST directly paid approximately 20% of the

purchase price to Durham and Cochran. Durham personally received $325,440 in cash, CLST

shares valued at $162,720, and notes valued at $162,720. Cochran personally received $54,000

in cash, CLST shares valued at $27,000, and two promissory notes in the aggregate principal

amount of $27,000.

68. Prior to the CLST Sale, neither Durham nor Cochran had any personal interest in

the accounts receivable sold to CLST. Upon information and belief, prior to closing the CLST

Sale, Durham and Cochran caused the Debtor to transfer some of the accounts that were to be

sold to CLST to Durham and Cochran (the transfer of accounts to Cochran individually, the

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 17 of 80

-16-

“Cochran CLST Transfer”) in exchange for promissory notes executed by Durham and

Cochran in favor of the Debtor (the loan to Cochran individually, the “Cochran CLST Loan,”

and together the loan to Durham, the “CLST Loans”). Upon information and belief, Durham

and Cochran never executed promissory notes memorializing the CLST Loans. Nonetheless, the

CLST Loans are reflected in the Debtor’s books and the terms of the CLST Sale identify Durham

and Cochran as “sellers” of at least some of the accounts being purchased.

II. The Fair Entities Transfer More Than $9 Million To or For the Benefit of the Defendants

69. In addition, or in the alternative, prior to the Petition Date, the Fair Entities made

payments or other transfers totaling more than $9 million either directly to the Defendants or to

other related persons or entities for the benefit of the Defendants (together, the “Fair Entities

Transfers,” as listed on Exhibit E to this Complaint). The Fair Entities made the Fair Entities

Transfers to or for the benefit of the Defendants, either directly or indirectly, as follows: (a) at

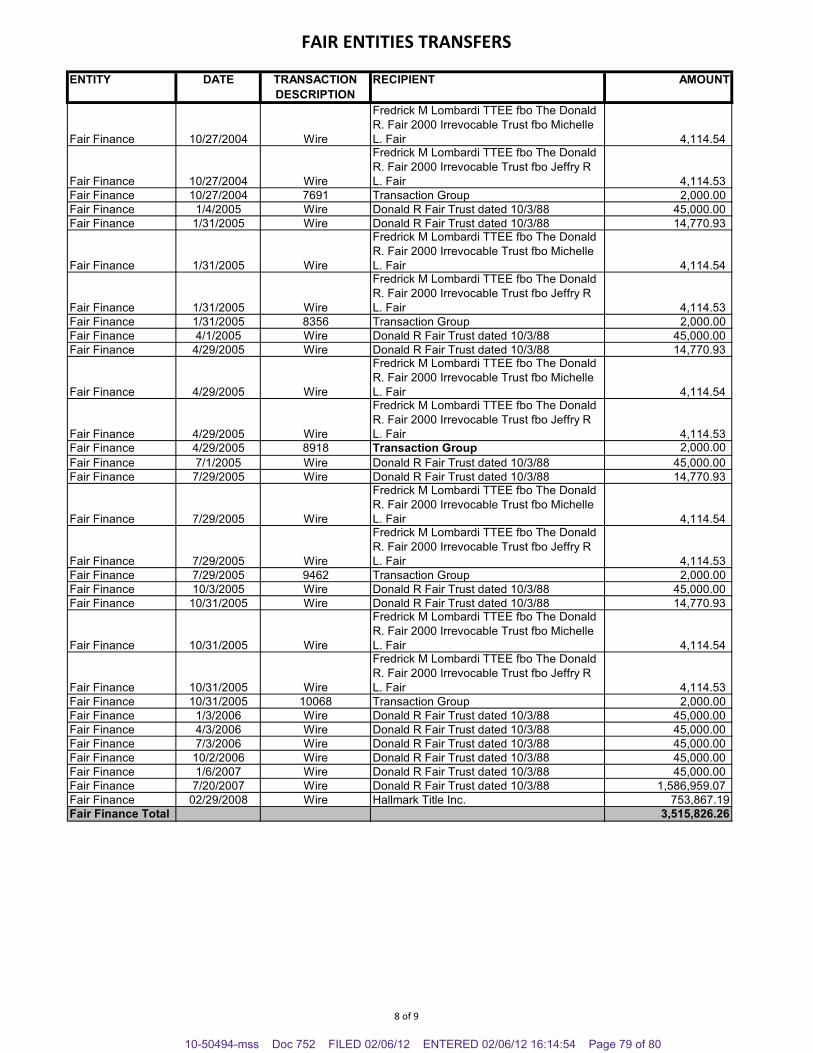

least $3,515,826.26 in the form of transfers from the Debtor (the “Fair Transfers,” as listed on

Exhibit E); (b) at least $5,659,111.93 in the form of transfers from DCI (the “DCI Transfers,”

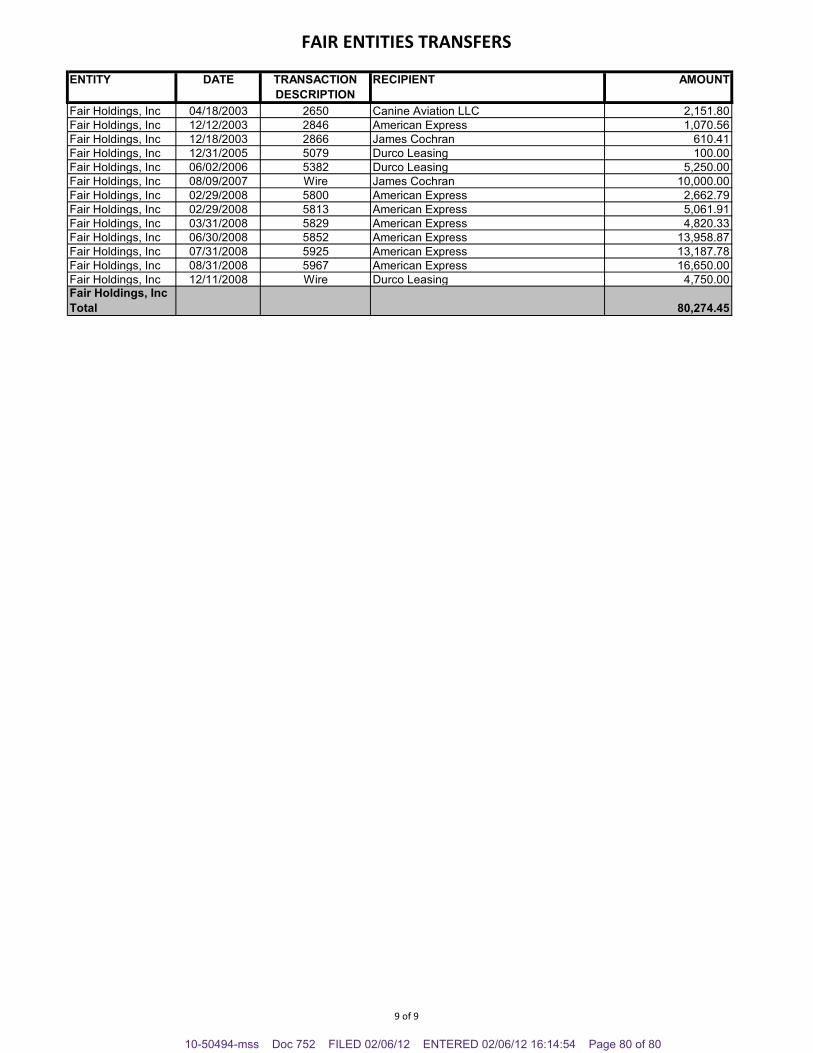

as listed on Exhibit E); and (c) at least $80,274.45 in the form of transfers from Fair Holdings

(the “Fair Holdings Transfers,” as listed on Exhibit E, and together with the DCI Transfers,

the “Fair Holdings/DCI Transfers”).

70. Cochran knew or should have known based on information available to him that

the Fair Entities were being used to perpetuate a Ponzi scheme, knew the Fair Entities were

insolvent and that the Fair Entities Transfers were made for a fraudulent purpose. Cochran

personally benefited from each of the Fair Entities Transfers, either directly or indirectly. The

Defendants did not furnish any consideration or value to the Fair Entities in exchange for the Fair

Entities.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 18 of 80

-17-

COUNT I – BREACH OF CONTRACT(COCHRAN NOTE)

71. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

72. Pursuant to the terms of the Cochran Note, Cochran was required to pay the entire

outstanding principal balance of the Cochran Note, together with accrued interest, on January 1,

2010, the Cochran Note Maturity Date.

73. Pursuant to the terms of the Cochran Note, Cochran was required to make

monthly payments of all accrued interest through the Cochran Note Maturity Date, and all

interest payments thereafter as accrued.

74. Cochran is in default of the Cochran Note and has breached his obligations under

the terms of the Cochran Note by, among other things, failing to repay all outstanding principal

and accrued interest by the Cochran Note Maturity Date.

75. By virtue of these defaults under the Cochran Note, all principal and accrued

interest under the Cochran Note is immediately due and payable.

76. Pursuant to the terms of the Cochran Note, interest has accrued and continues to

accrue on the unpaid principal balance at the default rate of 3% above the interest rate being paid

by the Debtor on its V-6 Notes.

77. Pursuant to the terms of the Cochran Note, the Trustee is entitled to recover his

costs of collection against Cochran, including reasonable attorney’s fees.

78. There is due and owing on the Cochran Note at least $8,444,312.60 in outstanding

principal and at least $2,161,804.74 in accrued and unpaid interest as of December 31, 2011, plus

interest accruing at the default rate set forth in the Cochran Note.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 19 of 80

-18-

79. As a direct and proximate cause of Cochran’s breach of the Cochran Note, the

Trustee is entitled to damages in an amount to be proven at trial, plus all reasonable attorneys’

fees and costs incurred by the Trustee to collect outstanding amounts.

COUNT II – BREACH OF CONTRACT(COCHRAN NOTE GUARANTY)

80. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

81. Pursuant to the terms of the Cochran Note Guaranty, Mrs. Cochran

unconditionally guaranteed all of the indebtedness and other obligations owing from Cochran to

DCI, including, but not limited to, the Cochran Note, existing or arising after the execution of the

Cochran Note Guaranty.

82. Cochran is in default of the Cochran Note and has breached his obligations under

the terms of the Cochran Note by, among other things, failing to repay all outstanding principal

and accrued interest by the Cochran Note Maturity Date.

83. Mrs. Cochran is in default of the Cochran Note Guaranty for, among other things,

failing to repay all outstanding principal and accrued interest by the Cochran Note Maturity

Date.

84. Pursuant to the terms of the Cochran Note Guaranty, the Trustee is entitled to

recover his costs of collection against Mrs. Cochran, including reasonable attorney’s fees.

85. There is due and owing on the Cochran Note Guaranty, by virtue of the Cochran

Note, at least $8,444,312.60 in outstanding principal and at least $2,161,804.74 in accrued and

unpaid interest, as of December 31, 2011, plus interest accruing at the default rate set forth in the

Cochran Note.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 20 of 80

-19-

86. As a direct and proximate cause of Mrs. Cochran’s breach of the Cochran Note

Guaranty, the Trustee is entitled to damages in an amount to be proven at trial, plus all

reasonable attorneys’ fees and costs incurred by the Trustee to collect outstanding amounts.

COUNT III – BREACH OF CONTRACT(HSE NOTE GUARANTY)

87. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

88. Pursuant to the terms of the HSE Note Guaranty, the Defendants unconditionally

guaranteed all of the indebtedness and other obligations owing from HSE Hockey to DCI,

including, but not limited to, the HSE Note, existing or arising after the execution of the HSE

Note Guaranty.

89. Pursuant to the terms of the HSE Note, HSE Hockey was required to make annual

payments of all accrued interest on the first day of May, beginning May 1, 2005 and continuing

thereafter until the HSE Note Maturity Date.

90. HSE Hockey is in default of the HSE Note and has breached its obligations under

the terms of the HSE Note by, among other things, failing to make annual payments of accrued

interest when due under the HSE Note. By virtue of these defaults under the HSE Note, all

principal and accrued interest under the HSE Note is immediately due and payable.

91. Pursuant to the terms of the HSE Note, interest has accrued and continues to

accrue on the unpaid principal balance at the default rate of 7.25% per annum.

92. The Defendants are in default of the HSE Note Guaranty for, among other things,

failing to repay all outstanding amounts due under the HSE Note upon default.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 21 of 80

-20-

93. There is due and owing on the HSE Note Guaranty, by virtue of the HSE Note, at

least $144,145.54 in outstanding principal and at least $13,982.83 in accrued and unpaid interest

through December 31, 2009, plus interest accruing at the default rate set forth in the HSE Note.

94. Pursuant to the terms of the HSE Note Guaranty, the Trustee also is entitled to

recover his costs of collection against the Defendants, including reasonable attorney’s fees.

95. As a direct and proximate cause of the Defendants’ breach of the HSE Note

Guaranty, the Trustee is entitled to damages in an amount to be proven at trial, plus all

reasonable attorneys’ fees and costs incurred by the Trustee to collect outstanding amounts.

COUNT IV – ACTUAL FRAUDULENT TRANSFER UNDER11 U.S.C. §§ 548(a)(1)(A), 550(a) AND 551

(COCHRAN CLST TRANSFER)

96. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

97. The Cochran CLST Transfer was made on or within two years before the Petition

Date.

98. The Cochran CLST Transfer constitutes a transfer of an interest of the Debtor in

property within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

99. The Cochran CLST Transfer was made with the actual intent to hinder, delay or

defraud some or all of the Debtor’s then existing or future creditors.

100. Accordingly, the Cochran CLST Transfer is a fraudulent transfer under 11 U.S.C.

§ 548(a)(1)(A), and the Trustee is entitled to judgment avoiding the Cochran CLST Transfer and

recovering the Cochran CLST Transfer, or the value thereof, from Cochran for benefit of the

estate pursuant to 11 U.S.C. § 550(a).

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 22 of 80

-21-

COUNT V – CONSTRUCTIVE FRAUDULENT TRANSFER UNDER11 U.S.C. §§ 548(a)(1)(B), 550(a) AND 551

(COCHRAN CLST TRANSFER)

101. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

102. The Cochran CLST Transfer was made on or within two years before the Petition

Date.

103. The Cochran CLST Transfer constitutes a transfer of an interest of the Debtor in

property within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

104. The Debtor received less than a reasonably equivalent value in exchange for the

Cochran CLST Transfer.

105. At the time of the Cochran CLST Transfer, the Debtor was insolvent, or became

insolvent as a result of the Cochran CLST Transfer.

106. At the time of the Cochran CLST Transfer, the Debtor was engaged in a business

or transaction, or was about to engage in a business or a transaction, for which any property

remaining with the Debtor was an unreasonably small capital.

107. At the time of the Cochran CLST Transfer, the Debtor intended to incur, or

believed that it would incur, debts that would be beyond the Debtor’s ability to pay as such debts

matured.

108. Accordingly, the Cochran CLST Transfer is a fraudulent transfer under 11 U.S.C.

§ 548(a)(1)(B), and the Trustee is entitled to judgment avoiding the Cochran CLST Transfer and

recovering the Cochran CLST Transfer, or the value thereof, from Cochran for benefit of the

estate pursuant to 11 U.S.C. § 550(a).

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 23 of 80

-22-

COUNT VI – FRAUDULENT TRANSFER UNDER OHIO REVISED CODE § 1336.04AND/OR IND. CODE § 32-18-2-14 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(b), AND 11 U.S.C. §§ 544, 550(a) AND 551(COCHRAN CLST TRANSFER)

109. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

110. At all times relevant to the Cochran CLST Transfer, there have been and are one

or more creditors who have held and still hold matured or unmatured unsecured claims against

the Debtor that were and are allowable under 11 U.S.C. § 502 or that were and are not allowable

only under 11 U.S.C. § 502(e) who would be entitled to avoid the Cochran CLST Transfer.

111. At all times relevant to the Cochran CLST Transfer, the Debtor had one or more

creditors with claims against the Debtor. One or more creditors of the Debtor were creditors of

the Debtor before the Cochran CLST Transfer and remain creditors up through to the present.

112. The Debtor has one or more creditors whose claims arose both before and after

the Cochran CLST Transfer was made.

113. The Debtor made the Cochran CLST Transfer with actual intent to hinder, delay,

or defraud some or all of the Debtor’s then existing or future creditors.

114. The Debtor made the Cochran CLST Transfer without receiving a reasonably

equivalent value in exchange for the Cochran CLST Transfer.

115. At the time of the Cochran CLST Transfer, the Debtor was engaged or was about

to engage in a business or transaction for which its remaining assets were unreasonably small in

relation to the business or transaction.

116. At the time of the Cochran CLST Transfer, the Debtor intended to incur, or

believed or reasonably should have believed that it would incur, debts beyond its ability to pay as

they became due.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 24 of 80

-23-

117. The Cochran CLST Transfer was made in the four-year period preceding the

Petition Date.

118. Accordingly, the Cochran CLST Transfer is a fraudulent transfer under Section

1336.04 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-14 and/or

Section 3304(b) of the Federal Debt Collection Procedures Act. As of the commencement of the

case, the Cochran CLST Transfer could be avoided under those provisions by numerous creditors

of the estate who were creditors at the time that the Cochran CLST Transfer was made and have

been continually since, and by other creditors of the estate, including the Internal Revenue

Service, or the hypothetical creditors provided by 11 U.S.C. §544(a)(1) and (2). The Trustee is

entitled to judgment avoiding the Cochran CLST Transfer and recovering the Cochran CLST

Transfer, or the value thereof, from Cochran for the benefit of the estate pursuant to Section

1336.07 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17 and/or

Federal Debt Collection Procedures Act § 3306, and 11 U.S.C. § 550(a).

COUNT VII – FRAUDULENT TRANSFER UNDER OHIO REVISED CODE § 1336.05AND/OR IND. CODE § 32-18-2-15 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(a), AND 11 U.S.C. §§ 544, 550(a) AND 551(COCHRAN CLST TRANSFER)

119. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

120. At all times relevant to the Cochran CLST Transfer, there have been and are one

or more creditors who have held and still hold matured or unmatured unsecured claims against

the Debtor that were and are allowable under 11 U.S.C. § 502 or that were and are not allowable

only under 11 U.S.C. § 502(e) who would be entitled to avoid the Cochran CLST Transfer.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 25 of 80

-24-

121. At all times relevant to the Cochran CLST Transfer, the Debtor had one or more

creditors with claims against the Debtor. One or more creditors of the Debtor were creditors of

the Debtor before the Cochran CLST Transfer and remain creditors up through to the present.

122. One or more of the Debtor’s creditors holds claims against the Debtor that arose

before the Cochran CLST Transfer was made.

123. The Debtor made the Cochran CLST Transfer without receiving a reasonably

equivalent value in exchange for the Cochran CLST Transfer.

124. The Debtor was insolvent at the time of the Cochran CLST Transfer, or became

insolvent as a result of the Cochran CLST Transfer. The Debtor was insolvent, or became

insolvent, because (i) the sum of its debts exceeded its assets at a fair valuation, and (ii) it was

unable to pay its debts as they became due.

125. The Cochran CLST Transfer was made in the four-year period preceding the

Petition Date.

126. Accordingly, the Cochran CLST Transfer is a fraudulent transfer under Section

1336.05 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-15 and/or

Section 3304(a) of the Federal Debt Collection Procedures Act. As of the commencement of the

case, the Cochran CLST Transfer could be avoided under those provisions by numerous creditors

of the estate who were creditors at the time that the Cochran CLST Transfer was made and have

been continually since, and by other creditors of the estate, including the Internal Revenue

Service, or the hypothetical creditors provided by 11 U.S.C. §544(a)(1) and (2). The Trustee is

entitled to judgment avoiding the Cochran CLST Transfer and recovering the Cochran CLST

Transfer, or the value thereof, from Cochran pursuant to Section 1336.07 of the Ohio Uniform

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 26 of 80

-25-

Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17 and/or Federal Debt Collection

Procedures Act § 3306, and 11 U.S.C. § 550(a).

COUNT VIII – ACTUAL FRAUDULENT TRANSFERS UNDER11 U.S.C. §§ 548(a)(1)(A), 550(a) AND 551

(FAIR TRANSFERS)

127. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

128. The Fair Transfers constitute transfers of an interest of the Debtor in property

within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

129. The Fair Transfers were made with the actual intent to hinder, delay or defraud

some or all of the Debtor’s then existing or future creditors.

130. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Transfers.

131. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Transfers. Utilizing his insider

position at the involved companies, Cochran concealed the fraud, effectively preventing the

discovery of the Fair Transfers until no earlier than the Petition Date.

132. Accordingly, the Fair Transfers are fraudulent transfers under 11 U.S.C. §

548(a)(1)(A), and the Trustee is entitled to judgment avoiding the Fair Transfers and recovering

the Fair Transfers, or the value thereof, from the Defendants for benefit of the estate pursuant to

11 U.S.C. § 550(a).

COUNT IX – CONSTRUCTIVE FRAUDULENT TRANSFERS UNDER11 U.S.C. §§ 548(a)(1)(B), 550(a) AND 551

(FAIR TRANSFERS)

133. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 27 of 80

-26-

134. The Fair Transfers constitute transfers of an interest of the Debtor in property

within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

135. The Debtor received less than a reasonably equivalent value in exchange for the

Fair Transfers.

136. At the time of the Fair Transfers, the Debtor was insolvent, or became insolvent

as a result of the Fair Transfers.

137. At the time of the Fair Transfers, the Debtor was engaged in a business or

transaction, or was about to engage in a business or a transaction, for which any property

remaining with the Debtor was an unreasonably small capital.

138. At the time of the Fair Transfers, the Debtor intended to incur, or believed that it

would incur, debts that would be beyond the Debtor’s ability to pay as such debts matured.

139. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Transfers.

140. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Transfers. Utilizing his insider

position at the involved companies, Cochran concealed the fraud, effectively preventing the

discovery of the Fair Transfers until no earlier than the Petition Date.

141. Accordingly, the Fair Transfers are fraudulent transfers under 11 U.S.C. §

548(a)(1)(B), and the Trustee is entitled to judgment avoiding the Fair Transfers and recovering

the Fair Transfers, or the value thereof, from the Defendants for benefit of the estate pursuant to

11 U.S.C. § 550(a).

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 28 of 80

-27-

COUNT X – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.04AND/OR IND. CODE § 32-18-2-14 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(b), AND 11 U.S.C. §§ 544, 550(a) AND 551(FAIR TRANSFERS)

142. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

143. At all times relevant to the Fair Transfers, there have been and are one or more

creditors who have held and still hold matured or unmatured unsecured claims against the Debtor

that were and are allowable under 11 U.S.C. § 502 or that were and are not allowable only under

11 U.S.C. § 502(e) who would be entitled to avoid the Fair Transfers.

144. At all times relevant to the Fair Transfers, the Debtor had one or more creditors

with claims against the Debtor. One or more creditors of the Debtor were creditors of the Debtor

before the Fair Transfers and remain creditors up through to the present.

145. The Debtor has one or more creditors whose claims arose both before and after

the Fair Transfers were made.

146. The Debtor made the Fair Transfers with actual intent to hinder, delay, or defraud

some or all of the Debtor’s then existing or future creditors.

147. The Debtor made the Fair Transfers without receiving a reasonably equivalent

value in exchange for the Fair Transfers.

148. At the time of the Fair Transfers, the Debtor was engaged or was about to engage

in a business or transaction for which its remaining assets were unreasonably small in relation to

the business or transaction.

149. At the time of the Fair Transfers, the Debtor intended to incur, or believed or

reasonably should have believed that it would incur, debts beyond its ability to pay as they

became due.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 29 of 80

-28-

150. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Transfers.

151. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Transfers. Utilizing his insider

position at the involved companies, Cochran concealed the fraud, effectively preventing the

discovery of the Fair Transfers until no earlier than the Petition Date.

152. Accordingly, the Fair Transfers are fraudulent transfers under Section 1336.04 of

the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-14 and/or Section

3304(b) of the Federal Debt Collection Procedures Act. As of the commencement of the case,

the Fair Transfers could be avoided under those provisions by numerous creditors of the estate

who were creditors at the time that the Fair Transfers were made and have been continually

since, and by other creditors of the estate, including the Internal Revenue Service, or the

hypothetical creditors provided by 11 U.S.C. §544(a)(1) and (2). The Trustee is entitled to

judgment avoiding the Fair Transfers and recovering the Fair Transfers, or the value thereof,

from the Defendants for the benefit of the estate pursuant to Section 1336.07 of the Ohio

Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17 and/or Federal Debt Collection

Procedures Act § 3306, and 11 U.S.C. § 550(a).

COUNT XI – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.05AND/OR IND. CODE § 32-18-2-15 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(a), AND 11 U.S.C. §§ 544, 550(a) AND 551(FAIR TRANSFERS)

153. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

154. At all times relevant to the Fair Transfers, there have been and are one or more

creditors who have held and still hold matured or unmatured unsecured claims against the Debtor

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 30 of 80

-29-

that were and are allowable under 11 U.S.C. § 502 or that were and are not allowable only under

11 U.S.C. § 502(e) who would be entitled to avoid the Fair Transfers.

155. At all times relevant to the Fair Transfers, the Debtor had one or more creditors

with claims against the Debtor. One or more creditors of the Debtor were creditors of the Debtor

before the Fair Transfers and remain creditors up through to the present.

156. One or more of the Debtor’s creditors holds claims against the Debtor that arose

before the Fair Transfers were made.

157. The Debtor made the Fair Transfers without receiving a reasonably equivalent

value in exchange for the Fair Transfers.

158. The Debtor was insolvent at the time of the Fair Transfers, or became insolvent as

a result of the Fair Transfers. The Debtor was insolvent, or became insolvent, because (i) the

sum of its debts exceeded its assets at a fair valuation, and (ii) it was unable to pay its debts as

they became due.

159. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Transfers.

160. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Transfers. Utilizing his insider

position at the involved companies, Cochran concealed the fraud, effectively preventing the

discovery of the Fair Transfers until no earlier than the Petition Date.

161. Accordingly, the Fair Transfers are fraudulent transfers under Section 1336.05 of

the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-15 and/or Section 3304(a)

of the Federal Debt Collection Procedures Act. As of the commencement of the case, the Fair

Transfers could be avoided under those provisions by numerous creditors of the estate who were

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 31 of 80

-30-

creditors at the time that the Fair Transfers were made and have been continually since, and by

other creditors of the estate, including the Internal Revenue Service, or the hypothetical creditors

provided by 11 U.S.C. §544(a)(1) and (2). The Trustee is entitled to judgment avoiding the Fair

Transfers and recovering the Fair Transfers, or the value thereof, from the Defendants pursuant

to Section 1336.07 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17

and/or Federal Debt Collection Procedures Act § 3306, and 11 U.S.C. § 550(a).

COUNT XII – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.04AND/OR IND. CODE § 32-18-2-14

(FAIR HOLDINGS/DCI TRANSFERS)

162. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

163. At all times relevant to the Fair Holdings/DCI Transfers, the Debtor was a

creditor with one or more claims against Fair Holdings and DCI by virtue of the loans and other

transfers described above.

164. The claims of the Debtor arose both before and after the Fair Holdings/DCI

Transfers were made.

165. Fair Holdings and DCI made the Fair Holdings/DCI Transfers with actual intent

to hinder, delay, or defraud the Debtor.

166. Fair Holdings and DCI made the Fair Holdings/DCI Transfers without receiving a

reasonably equivalent value in exchange for the Fair Holdings/DCI Transfers.

167. At the time of the Fair Holdings/DCI Transfers, Fair Holdings and DCI were

engaged or were about to engage in a business or transaction for which their remaining assets

were unreasonably small in relation to the business or transaction.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 32 of 80

-31-

168. At the time of the Fair Holdings/DCI Transfers, Fair Holdings and DCI intended

to incur, or believed or reasonably should have believed that they would incur, debts beyond

their ability to pay as they became due.

169. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

170. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

171. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under

Section 1336.04 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-14,

and the Trustee is entitled to judgment avoiding the Fair Holdings/DCI Transfers and recovering

the Fair Holdings/DCI Transfers, or the value thereof, from the Defendants for benefit of the

estate pursuant to Section 1336.07 of the Ohio Uniform Fraudulent Transfer Act and/or Ind.

Code § 32-18-2-17.

COUNT XIII – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.05AND/OR IND. CODE § 32-18-2-15

(FAIR HOLDINGS/DCI TRANSFERS)

172. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

173. At all times relevant to the Fair Holdings/DCI Transfers, the Debtor was a

creditor with one or more claims against Fair Holdings and DCI by virtue of the loans and other

transfers described above.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 33 of 80

-32-

174. The claims of the Debtor arose before the Fair Holdings/DCI Transfers were

made.

175. Fair Holdings and DCI made the Fair Holdings/DCI Transfers without receiving a

reasonably equivalent value in exchange for the Fair Holdings/DCI Transfers.

176. Fair Holdings and DCI were insolvent at the time of the Fair Holdings/DCI

Transfers, or became insolvent as a result of the Fair Holdings/DCI Transfers. Fair Holdings and

DCI were each insolvent, or became insolvent, because (i) the sum of their debts exceeded their

assets at a fair valuation, and (ii) they were unable to pay their debts as they became due.

177. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

178. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

179. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under

Section 1336.05 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-15,

and the Trustee is entitled to judgment avoiding the Fair Holdings/DCI Transfers and recovering

the Fair Holdings/DCI Transfers, or the value thereof, from the Defendants pursuant to Section

1336.07 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17.

COUNT XIV – ACTUAL FRAUDULENT TRANSFERS UNDER 11 U.S.C. § 548(a)(1)(A), 550(a) AND 551(FAIR HOLDINGS/DCI TRANSFERS)

180. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 34 of 80

-33-

181. The Fair Holdings/DCI Transfers were transfers of the Debtor’s funds, through

Fair Holdings and DCI, to or for the benefit of the Defendants, either directly or indirectly. The

Fair Holdings/DCI Transfers, whether direct or indirect, were made as part of a general scheme

to transfer funds from the Debtor to or for the Defendants’ benefit, either directly or indirectly.

182. Each of the Fair Holdings/DCI Transfers constitutes a transfer of an interest of the

Debtor in property within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

183. Each of the Fair Holdings/DCI Transfers was made with the actual intent to

hinder, delay or defraud some or all of the Debtor’s then existing or future creditors.

184. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

185. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

186. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under 11

U.S.C. § 548(a)(1)(A), and the Trustee is entitled to judgment avoiding the Fair Holdings/DCI

Transfers and recovering the Fair Holdings/DCI Transfers, or the value thereof, from the

Defendants pursuant to 11 U.S.C. § 550(a).

COUNT XV – CONSTRUCTIVE FRAUDULENT TRANSFERS UNDER 11 U.S.C. § 548(a)(1)(B), 550(a) AND 551(FAIR HOLDINGS/DCI TRANSFERS)

187. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 35 of 80

-34-

188. The Fair Holdings/DCI Transfers were transfers of the Debtor’s funds, through

Fair Holdings and DCI, to or for the benefit of the Defendants, either directly or indirectly. The

Fair Holdings/DCI Transfers, whether direct or indirect, were made as part of a general scheme

to transfer funds from the Debtor to or for the Defendants’ benefit, either directly or indirectly.

189. Each of the Fair Holdings/DCI Transfers constitutes a transfer of an interest of the

Debtor in property within the meaning of 11 U.S.C. §§ 101(54) and 548(a).

190. The Debtor received less than a reasonably equivalent value in exchange for each

of the Fair Holdings/DCI Transfers.

191. At the time of each of the Fair Holdings/DCI Transfers, the Debtor was insolvent,

or became insolvent as a result of the Fair Holdings/DCI Transfer in question.

192. At the time of each of the Fair Holdings/DCI Transfers, the Debtor was engaged

in a business or a transaction, or was about to engage in a business or a transaction, for which

any property remaining with the Debtor was an unreasonably small capital.

193. At the time of each of the Fair Holdings/DCI Transfers, the Debtor intended to

incur, or believed that it would incur, debts that would be beyond the Debtor’s ability to pay as

such debts matured.

194. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

195. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 36 of 80

-35-

196. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under 11

U.S.C. § 548(a)(1)(B), and the Trustee is entitled to judgment avoiding the Fair Holdings/DCI

Transfers and recovering the Fair Holdings/DCI Transfers, or the value thereof, from the

Defendants pursuant to 11 U.S.C. § 550(a).

COUNT XVI – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.04 AND/OR IND. CODE § 32-18-2-14 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(b), AND 11 U.S.C. §§ 544, 550(a) AND 551(FAIR HOLDINGS/DCI TRANSFERS)

197. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

198. The Fair Holdings/DCI Transfers were transfers of the Debtor’s funds, through

Fair Holdings and DCI, to or for the benefit of the Defendants, either directly or indirectly. The

Fair Holdings/DCI Transfers, whether direct or indirect, were made as part of a general scheme

to transfer funds from the Debtor to or for the Defendants’ benefit, either directly or indirectly.

199. At all times relevant to the Fair Holdings/DCI Transfers, there have been and are

one or more creditors who have held and still hold matured or unmatured unsecured claims

against the Debtor that were and are allowable under 11 U.S.C. § 502 or that were and are not

allowable only under 11 U.S.C. § 502(e) who would be entitled to avoid the Fair Holdings/DCI

Transfers.

200. At all times relevant to the Fair Holdings/DCI Transfers, the Debtor had one or

more creditors with claims against the Debtor. One or more creditors of the Debtor were

creditors of the Debtor before the Fair Holdings/DCI Transfers and remain creditors up through

to the present.

201. The Debtor has one or more creditors whose claims arose both before and after

the Fair Holdings/DCI Transfers were made.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 37 of 80

-36-

202. The Debtor made the Fair Holdings/DCI Transfers with actual intent to hinder,

delay, or defraud some or all of the Debtor’s then existing or future creditors.

203. The Debtor made the Fair Holdings/DCI Transfers without receiving a reasonably

equivalent value in exchange for the Fair Holdings/DCI Transfers.

204. At the time of the Fair Holdings/DCI Transfers, the Debtor was engaged or was

about to engage in a business or transaction for which its remaining assets were unreasonably

small in relation to the business or transaction.

205. At the time of the Fair Holdings/DCI Transfers, the Debtor intended to incur, or

believed or reasonably should have believed that it would incur, debts beyond its ability to pay as

they became due.

206. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

207. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

208. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under

Section 1336.04 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-14

and/or Section 3304(b) of the Federal Debt Collection Procedures Act. As of the

commencement of the case, the Fair Holdings/DCI Transfers could be avoided under those

provisions by numerous creditors of the estate who were creditors at the time that the Fair

Holdings/DCI Transfers were made and have been continually since, and by other creditors of

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 38 of 80

-37-

the estate, including the Internal Revenue Service, or the hypothetical creditors provided by 11

U.S.C. §544(a)(1) and (2). The Trustee is entitled to judgment avoiding the Fair Holdings/DCI

Transfers and recovering the Fair Holdings/DCI Transfers, or the value thereof, from the

Defendants for the benefit of the estate pursuant to Section 1336.07 of the Ohio Uniform

Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17 and/or Federal Debt Collection

Procedures Act § 3306, and 11 U.S.C. § 550(a).

COUNT XVII – FRAUDULENT TRANSFERS UNDER OHIO REVISED CODE § 1336.05 AND/OR IND. CODE § 32-18-2-15 AND/OR FEDERAL DEBT COLLECTION

PROCEDURES ACT § 3304(a), AND 11 U.S.C. §§ 544, 550(a) AND 551(FAIR HOLDINGS/DCI TRANSFERS)

209. The Trustee restates the allegations of all preceding paragraphs as if fully set forth

herein.

210. The Fair Holdings/DCI Transfers were transfers of the Debtor’s funds, through

Fair Holdings and DCI, to or for the benefit of the Defendants, either directly or indirectly. The

Fair Holdings/DCI Transfers, whether direct or indirect, were made as part of a general scheme

to transfer funds from the Debtor to or for the Defendants’ benefit, either directly or indirectly.

211. At all times relevant to the Fair Holdings/DCI Transfers, there have been and are

one or more creditors who have held and still hold matured or unmatured unsecured claims

against the Debtor that were and are allowable under 11 U.S.C. § 502 or that were and are not

allowable only under 11 U.S.C. § 502(e) who would be entitled to avoid the Fair Holdings/DCI

Transfers.

212. At all times relevant to the Fair Holdings/DCI Transfers, the Debtor had one or

more creditors with claims against the Debtor. One or more creditors of the Debtor were

creditors of the Debtor before the Fair Holdings/DCI Transfers and remain creditors up through

to the present.

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 39 of 80

-38-

213. One or more of the Debtor’s creditors holds claims against the Debtor that arose

before the Fair Holdings/DCI Transfers were made.

214. The Debtor made the Fair Holdings/DCI Transfers without receiving a reasonably

equivalent value in exchange for the Fair Holdings/DCI Transfers.

215. The Debtor was insolvent at the time of the Fair Holdings/DCI Transfers, or

became insolvent as a result of the Fair Holdings/DCI Transfers. The Debtor was insolvent, or

became insolvent, because (i) the sum of its debts exceeded its assets at a fair valuation, and (ii)

it was unable to pay its debts as they became due.

216. The Defendants personally benefited, either directly or indirectly, from each of

the Fair Holdings/DCI Transfers.

217. Cochran and other insiders described above actively concealed and disguised the

Ponzi scheme for their own financial gain, including the Fair Holdings/DCI Transfers. Utilizing

his insider position at the involved companies, Cochran concealed the fraud, effectively

preventing the discovery of the Fair Holdings/DCI Transfers until no earlier than the Petition

Date.

218. Accordingly, the Fair Holdings/DCI Transfers are fraudulent transfers under

Section 1336.05 of the Ohio Uniform Fraudulent Transfer Act and/or Ind. Code § 32-18-2-15

and/or Section 3304(a) of the Federal Debt Collection Procedures Act. As of the commencement

of the case, the Fair Holdings/DCI Transfers could be avoided under those provisions by

numerous creditors of the estate who were creditors at the time that the Fair Holdings/DCI

Transfers were made and have been continually since, and by other creditors of the estate,

including the Internal Revenue Service, or the hypothetical creditors provided by 11 U.S.C.

§544(a)(1) and (2). The Trustee is entitled to judgment avoiding the Fair Holdings/DCI

10-50494-mss Doc 752 FILED 02/06/12 ENTERED 02/06/12 16:14:54 Page 40 of 80

-39-

Transfers and recovering the Fair Holdings/DCI Transfers, or the value thereof, from the

Defendants for the benefit of the estate pursuant to Section 1336.07 of the Ohio Uniform

Fraudulent Transfer Act and/or Ind. Code § 32-18-2-17 and/or Federal Debt Collection

Procedures Act § 3306, and 11 U.S.C. § 550(a).

WHEREFORE, the Trustee respectfully requests the entry of an order:

(a) Granting the Trustee judgment against the Defendants on the Cochran Note,

Cochran Guaranty and HSE Guaranty in amounts to be proven at trial;

(b) Granting the Trustee compensatory and consequential damages in an amount to

be proven at trial;

(c) Granting the Trustee pre-judgment and post-judgment interest as permitted by

law;

(d) Granting the Trustee all the costs incurred in collecting the sums due under the

Cochran Note, Cochran Guaranty and HSE Guaranty, including, but not limited to, reasonable

attorneys’ fees and the costs of this action;

(e) Avoiding and authorizing the Trustee to recover the Cochran CLST Transfer and

Fair Entities Transfers, or the value thereof, to the extent necessary to satisfy the claims of the

Debtor;

(f) Attaching or garnishing the assets transferred or other property of the Defendants

in accordance with applicable state law;

(g) Granting injunctive relief against further disposition by the Defendants herein of

the assets transferred and other property; and