Embed Size (px)

Citation preview

174

V. Comparative Value Chain and Economic

Analysis of the Furniture/Wood Processing

Sector (Chairs) in Ethiopia, Tanzania, Zambia,

China and Vietnam

175

V.1. Wood Products Analysis: Objectives

The purpose of the wood products analysis is to assess the current competitiveness of the

subsector and the main opportunities for moving from the current relative inefficiency

and low competitiveness to reach a competitive production level in the medium term

future. To do this, a typical product (wooden chair) is analyzed in the following manner:

Examine important issues and trends in the world wood products market;

Review the structures of the Ethiopian, Tanzanian, Zambian, Chinese and

Vietnamese wood products markets;

Assess the key features, strengths and weaknesses of the existing supply chain for

wood products in Ethiopia, Tanzania, Zambia, China and Vietnam;

Assess the overall economic efficiency of domestic wood products production in

relation to world prices (based primarily on Chinese prices) using alternative cost

projection scenarios to establish current and medium-term competitiveness;

Taking the economic efficiency result as a starting point, analyze the wood

products (wooden chair) value chain to identify key strengths, weaknesses and

opportunities or needs for investment, expansion or contraction to move towards

international competitiveness at the business strategy and business process levels;

and

Provide possible policy options and recommendations to help stimulate growth

and improve competitiveness in the sector.

V.2. Product Selection Method

Following a review of the first product screening in which 40 products were selected for

consideration for the value chain analysis and feasibility study, the World Bank (WB)

and Global Development Solutions (GDS)/HQ teams immediately agreed on seven out of

the ten products needed for the analysis. The seven products selected by the teams were

as follows:

1. Apparel:

a. Polo shirt; and

b. Underwear

2. Agribusiness:

a. Milk; and

b. Wheat milling

3. Leather:

a. High-end sheepskin loafers

4. Wood:

a. Windows/French windows and frames

176

5. Metal:

a. Padlocks.

To finalize the selection of the remaining products from the wood, metal and leather

sectors, based on the Africa Competitiveness: Phase 1.1 - Preliminary Product Screening

in Ethiopia report (July 2010), the WB and GDS/HQ teams chose six products as

potential candidates to be included in the list of the final ten products to be the target

products for the value chain analysis and feasibility study. The six products included the

following:

1. Wood products:

a. Wooden doors; and

b. Wooden chairs (not upholstered).

2. Leather products:

a. Leather golf gloves; and

b. Sports footwear of leather.

3. Metal products:

a. Metal doors, window-frame (security window frame); and

b. Aluminum doors and windows.

In order to screen the final six products, a product screening survey was developed which

revolved around six factors:

1. Whether these products are currently produced by companies with less than

50 employees;

2. If companies identified in #1 above can be set up with less than US$100,000

in investment capital;

3. The minimum level of skills and know-how required to produce the products;

4. Whether the products produced by the companies in #1 are being exported;

5. Whether products produced by companies in #1 are consolidated by brokers

or other intermediaries for exports; and

6. Whether companies identified in #1 can readily access raw material inputs in

the market to produce the products.

These questions were posed to the wood, metal and leather sector associations in both

China and Vietnam. Following interviews with sector associations, additional interviews

were conducted at the firm level to identify specifically the level of investments and

minimum level of technical skills required for an entrepreneur or existing SMEs to set up

a production operation. These questions were posed to existing operators in China and

Vietnam to identify whether:

177

Barriers to market entry, particularly from a financial and skills

requirement, were sufficiently low to allow entrepreneurs and SMEs in

Ethiopia to easily establish operations; and

These products are currently being produced by SMEs in China and

Vietnam, and are effectively being sold in local and export markets.

The product screening survey identified the following products as viable candidates to be

targeted for the value chain and feasibility analysis.

1. Wood product:

a. Wooden chairs (soft wood); and

b. Wooden door (semi-solid).

Although French windows and their frames made of wood had originally been

preselected for analysis, a decision was made to opt to analyze both wooden

chairs and wooden doors. This decision stemmed from the fact that French

windows require glass thus introducing an outside factor that could influence

the manufacturing of the final product. Wooden doors (without glass) and

wooden chairs (without upholstery) are more representative of wood

processing exclusively.

2. Leather products: Leather golf gloves or sports glove of comparable structure

and weight.

3. Metal products: Both the pre-selected products (security window frame; and

aluminum doors and windows) were screened out of the selection due to

various factors including high initial investment requirements. As a result,

further analyses of products identified during the preliminary product

screening were conducted. Interviews with metal sector associations and

enterprises currently operating in China and Vietnam, as well as interviews

with existing operators in the fabricated metal products sector in Ethiopia

identified crown corks (bottle caps) as a viable candidate to be targeted for

value chain analysis. Crown corks currently are produced in four of the five

countries, but Ethiopia continues to import substantial volumes of this product,

including imports from China. As a result, crown corks have been chosen as

the final fabricated metal product to be the focus of a value chain analysis in

the target countries.

178

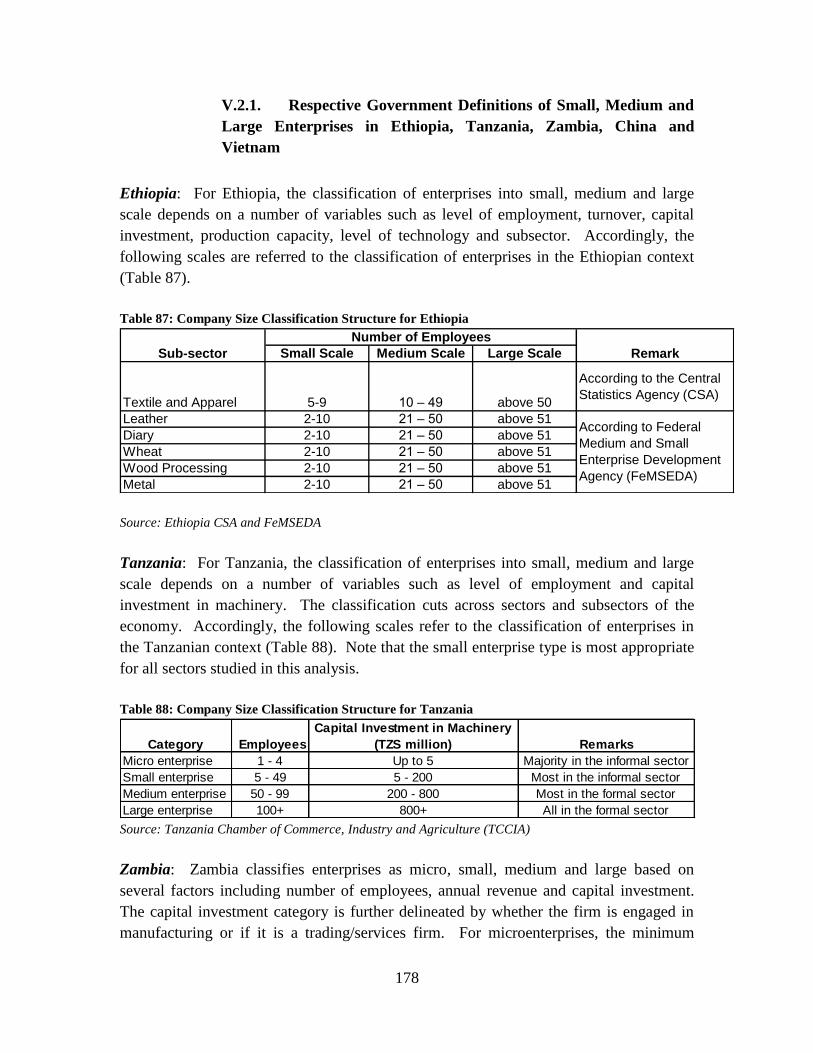

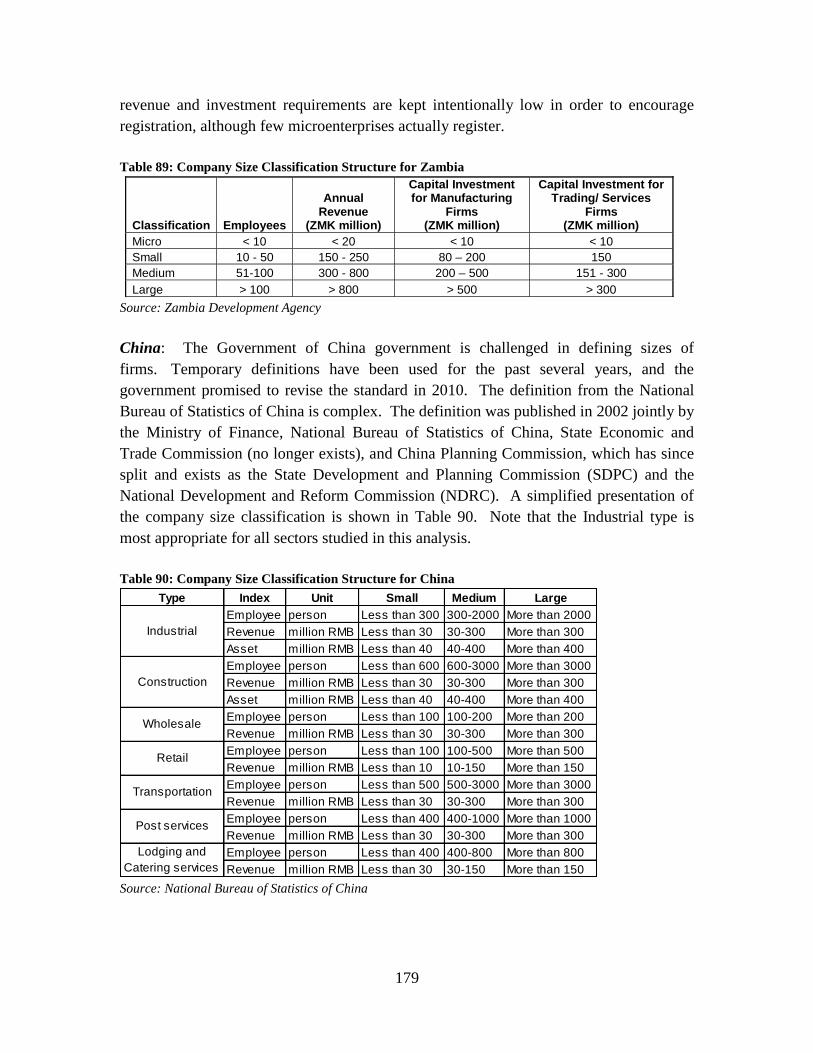

V.2.1. Respective Government Definitions of Small, Medium and

Large Enterprises in Ethiopia, Tanzania, Zambia, China and

Vietnam

Ethiopia: For Ethiopia, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment, turnover, capital

investment, production capacity, level of technology and subsector. Accordingly, the

following scales are referred to the classification of enterprises in the Ethiopian context

(Table 87).

Table 87: Company Size Classification Structure for Ethiopia

Small Scale Medium Scale Large Scale

Textile and Apparel 5-9 10 – 49 above 50

According to the Central

Statistics Agency (CSA)

Leather 2-10 21 – 50 above 51

Diary 2-10 21 – 50 above 51

Wheat 2-10 21 – 50 above 51

Wood Processing 2-10 21 – 50 above 51

Metal 2-10 21 – 50 above 51

According to Federal

Medium and Small

Enterprise Development

Agency (FeMSEDA)

Sub-sector Remark

Number of Employees

Source: Ethiopia CSA and FeMSEDA

Tanzania: For Tanzania, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment and capital

investment in machinery. The classification cuts across sectors and subsectors of the

economy. Accordingly, the following scales refer to the classification of enterprises in

the Tanzanian context (Table 88). Note that the small enterprise type is most appropriate

for all sectors studied in this analysis.

Table 88: Company Size Classification Structure for Tanzania

Category Employees

Capital Investment in Machinery

(TZS million) Remarks

Micro enterprise 1 - 4 Up to 5 Majority in the informal sector

Small enterprise 5 - 49 5 - 200 Most in the informal sector

Medium enterprise 50 - 99 200 - 800 Most in the formal sector

Large enterprise 100+ 800+ All in the formal sector Source: Tanzania Chamber of Commerce, Industry and Agriculture (TCCIA)

Zambia: Zambia classifies enterprises as micro, small, medium and large based on

several factors including number of employees, annual revenue and capital investment.

The capital investment category is further delineated by whether the firm is engaged in

manufacturing or if it is a trading/services firm. For microenterprises, the minimum

179

revenue and investment requirements are kept intentionally low in order to encourage

registration, although few microenterprises actually register.

Table 89: Company Size Classification Structure for Zambia

Classification Employees

Annual Revenue

(ZMK million)

Capital Investment for Manufacturing

Firms (ZMK million)

Capital Investment for Trading/ Services

Firms (ZMK million)

Micro < 10 < 20 < 10 < 10

Small 10 - 50 150 - 250 80 – 200 150

Medium 51-100 300 - 800 200 – 500 151 - 300

Large > 100 > 800 > 500 > 300

Source: Zambia Development Agency

China: The Government of China government is challenged in defining sizes of

firms. Temporary definitions have been used for the past several years, and the

government promised to revise the standard in 2010. The definition from the National

Bureau of Statistics of China is complex. The definition was published in 2002 jointly by

the Ministry of Finance, National Bureau of Statistics of China, State Economic and

Trade Commission (no longer exists), and China Planning Commission, which has since

split and exists as the State Development and Planning Commission (SDPC) and the

National Development and Reform Commission (NDRC). A simplified presentation of

the company size classification is shown in Table 90. Note that the Industrial type is

most appropriate for all sectors studied in this analysis.

Table 90: Company Size Classification Structure for China

Type Index Unit Small Medium Large

Employee person Less than 300 300-2000 More than 2000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 600 600-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 100 100-200 More than 200

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 100 100-500 More than 500

Revenue million RMB Less than 10 10-150 More than 150

Employee person Less than 500 500-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-1000 More than 1000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-800 More than 800

Revenue million RMB Less than 30 30-150 More than 150

Lodging and

Catering services

Industrial

Construction

Wholesale

Retail

Transportation

Post services

Source: National Bureau of Statistics of China

180

Vietnam: A small firm has less than 50 laborers, while a medium-size firm has 51-200

laborers. Within the small and medium-size classifications, there are some detailed

categories depending on the purpose of research and management. For instance, a firm

with less than 10 laborers is called a super small-size firm. Such a regulation is in line

with Social Insurance Law.75

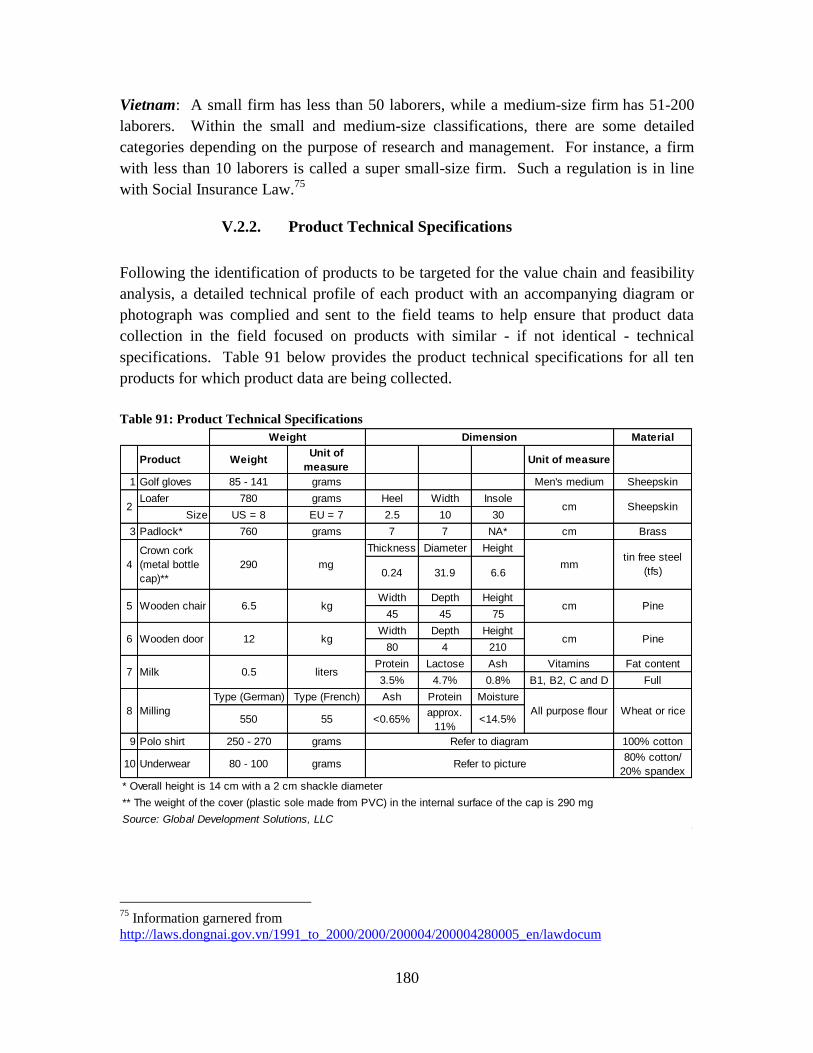

V.2.2. Product Technical Specifications

Following the identification of products to be targeted for the value chain and feasibility

analysis, a detailed technical profile of each product with an accompanying diagram or

photograph was complied and sent to the field teams to help ensure that product data

collection in the field focused on products with similar - if not identical - technical

specifications. Table 91 below provides the product technical specifications for all ten

products for which product data are being collected.

Table 91: Product Technical Specifications

Material

Product WeightUnit of

measureUnit of measure

1 Golf gloves 85 - 141 grams Men's medium Sheepskin

Loafer 780 grams Heel Width Insole

Size US = 8 EU = 7 2.5 10 30

3 Padlock* 760 grams 7 7 NA* cm Brass

Thickness Diameter Height

0.24 31.9 6.6

Width Depth Height

45 45 75

Width Depth Height

80 4 210

Protein Lactose Ash Vitamins Fat content

3.5% 4.7% 0.8% B1, B2, C and D Full

Type (German) Type (French) Ash Protein Moisture

550 55 <0.65%approx.

11%<14.5%

9 Polo shirt 250 - 270 grams 100% cotton

10 Underwear 80 - 100 grams80% cotton/

20% spandex

* Overall height is 14 cm with a 2 cm shackle diameter

** The weight of the cover (plastic sole made from PVC) in the internal surface of the cap is 290 mg

Source: Global Development Solutions, LLC

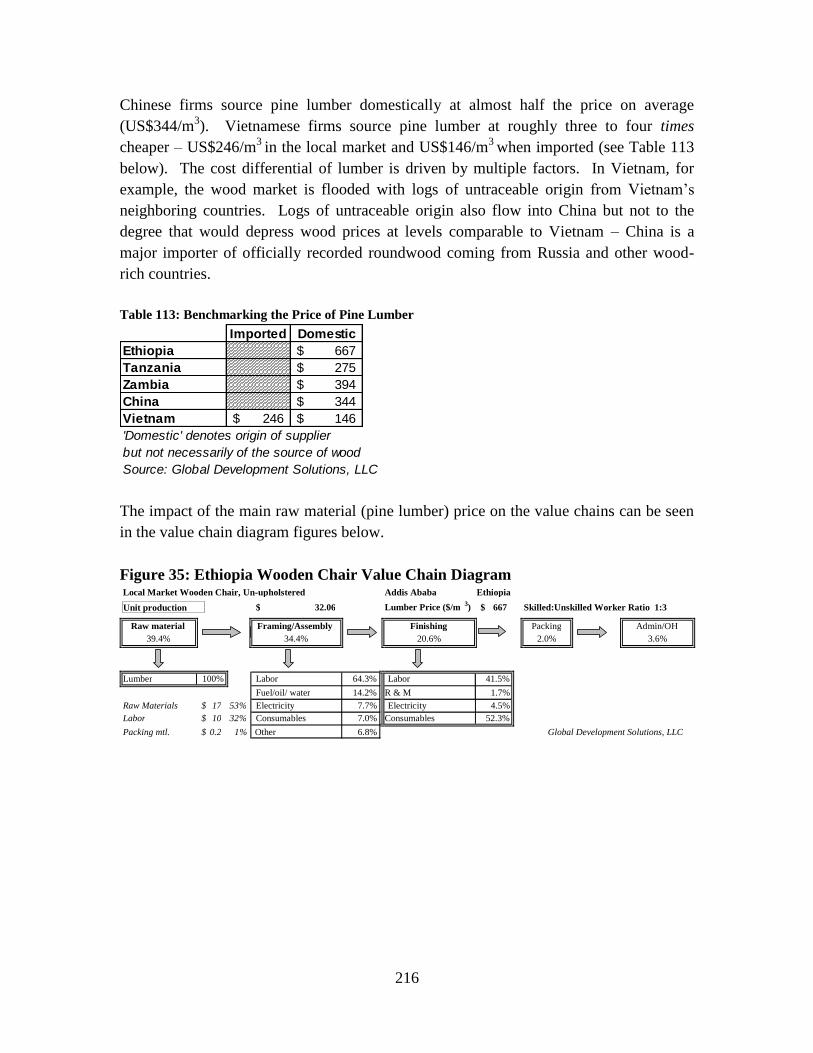

Pine

Wheat or rice

Dimension

All purpose flour

cm

Refer to diagram

Weight

cm

mm

cm

tin free steel

(tfs)

Sheepskin

Pine

mg

kg

kg

liters

Refer to picture

Crown cork

(metal bottle

cap)**

Wooden chair

Wooden door

Milk

Milling

290

6.5

12

0.5

2

4

5

6

7

8

75

Information garnered from

http://laws.dongnai.gov.vn/1991_to_2000/2000/200004/200004280005_en/lawdocum

181

V.3. Global Wood Products Market

Market Trends:76

In 2009, the international trade in wood and articles of wood

amounted to US$90 billion, down by US$20 billion from a year earlier and by US$35

billion from the 2007 peak. The largest segment of the global trade in wood and articles

of wood is sawn wood, accounting for over a quarter (26 percent) of the international

trade in wood, followed by builders‘ joinery and carpentry, as well as plywood, wood in

the rough, and fiberboard.

The largest exporters of wood and articles of wood in 2009 were Germany (US$8.5

billion), China (US$7.7 billion) and Canada (US$6.5 billion). The Russian Federation

and the USA are also among top exporters of wood with roughly US$5.5 billion annual

exports each, followed by Austria, Sweden and Malaysia with roughly US$4 billion

annual exports each. Many countries that lead in exports also are large importers of

wood. China, for example, was the third largest importer of wood and wood products in

2009 (US$7.2 billion). Among the largest net importers of wood and wood products are

Japan (US$8.5 billion net imports in 2009), followed by USA (US$5 billion in 2009), the

UK (US$3.7 billion) and Italy (US$2.8 billion).

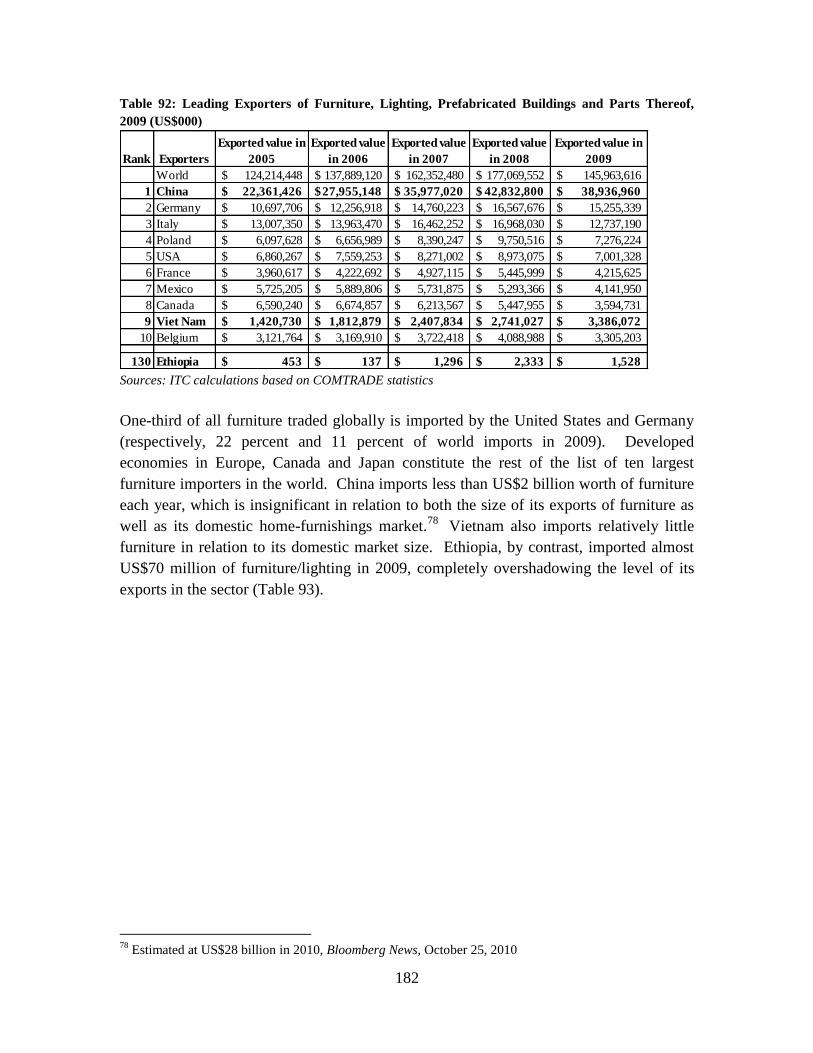

The international trade in furniture, lighting and prefabricated buildings and parts thereof

also decreased; from US$177 billion in 2008 to US$145 billion in 2009.77

The largest

segment of the global furniture/lighting trade is wooden furniture for office, bedroom,

and kitchen (valued at roughly US$45 billion or 31 percent of the global furniture trade),

followed by the trade in wooden seats and seat parts valued at US$28 billion in 2009,

and lamps and lighting fittings (US$24 billion).

The leading exporters of furniture, lighting and parts thereof are China, Germany and

Italy (Table 92). Vietnam has been one of the few countries among the top exporters

where exports grew even in the face of the current downturn in global demand. Today,

the country is the second largest Asian exporter of furniture, lightings and prefabricated

buildings. With its current export growth trend, Vietnam is likely to overtake Canada,

Mexico and France in the near future to reach the status of the sixth largest exporter of

furniture in the world. Ethiopia, Tanzania and Zambia, by contrast, do not have any

significant exports in the sector.

76

Section based on COMTRADE data as reported by the International Trade Center. 77

Includes furniture and furniture parts made of wood, metal, plastic, cane/bamboo and other materials.

182

Table 92: Leading Exporters of Furniture, Lighting, Prefabricated Buildings and Parts Thereof,

2009 (US$000)

Rank Exporters

Exported value in

2005

Exported value

in 2006

Exported value

in 2007

Exported value

in 2008

Exported value in

2009

World 124,214,448$ 137,889,120$ 162,352,480$ 177,069,552$ 145,963,616$

1 China 22,361,426$ 27,955,148$ 35,977,020$ 42,832,800$ 38,936,960$

2 Germany 10,697,706$ 12,256,918$ 14,760,223$ 16,567,676$ 15,255,339$

3 Italy 13,007,350$ 13,963,470$ 16,462,252$ 16,968,030$ 12,737,190$

4 Poland 6,097,628$ 6,656,989$ 8,390,247$ 9,750,516$ 7,276,224$

5 USA 6,860,267$ 7,559,253$ 8,271,002$ 8,973,075$ 7,001,328$

6 France 3,960,617$ 4,222,692$ 4,927,115$ 5,445,999$ 4,215,625$

7 Mexico 5,725,205$ 5,889,806$ 5,731,875$ 5,293,366$ 4,141,950$

8 Canada 6,590,240$ 6,674,857$ 6,213,567$ 5,447,955$ 3,594,731$

9 Viet Nam 1,420,730$ 1,812,879$ 2,407,834$ 2,741,027$ 3,386,072$

10 Belgium 3,121,764$ 3,169,910$ 3,722,418$ 4,088,988$ 3,305,203$

130 Ethiopia 453$ 137$ 1,296$ 2,333$ 1,528$ Sources: ITC calculations based on COMTRADE statistics

One-third of all furniture traded globally is imported by the United States and Germany

(respectively, 22 percent and 11 percent of world imports in 2009). Developed

economies in Europe, Canada and Japan constitute the rest of the list of ten largest

furniture importers in the world. China imports less than US$2 billion worth of furniture

each year, which is insignificant in relation to both the size of its exports of furniture as

well as its domestic home-furnishings market.78

Vietnam also imports relatively little

furniture in relation to its domestic market size. Ethiopia, by contrast, imported almost

US$70 million of furniture/lighting in 2009, completely overshadowing the level of its

exports in the sector (Table 93).

78

Estimated at US$28 billion in 2010, Bloomberg News, October 25, 2010

183

Table 93: Leading Importers of Furniture, Lighting, Prefabricated Buildings and Parts Thereof,

2009 (US$000)

Rank Importers

Imported value

in 2005

Imported value

in 2006

Imported value

in 2007

Imported value

in 2008

Imported value

in 2009

World $ 135,283,168 $ 148,901,024 $ 172,813,680 $ 181,705,136 $ 148,292,160

1 USA $ 41,234,684 $ 43,932,048 $ 44,882,684 $ 41,919,408 $ 32,472,700

2 Germany $ 12,062,649 $ 12,917,532 $ 13,710,198 $ 15,082,178 $ 15,613,344

3 France $ 8,014,874 $ 8,496,198 $ 10,284,960 $ 11,384,802 $ 9,517,121

4 United Kingdom $ 8,794,791 $ 9,427,094 $ 11,601,876 $ 11,124,282 $ 8,198,500

5 Canada $ 5,706,644 $ 6,631,483 $ 7,477,628 $ 7,804,628 $ 6,235,172

6 Japan $ 5,699,028 $ 5,867,036 $ 6,018,743 $ 6,366,192 $ 5,595,712

7 Netherlands $ 3,226,264 $ 3,541,261 $ 4,388,216 $ 4,891,634 $ 5,070,640

8 Belgium $ 3,755,435 $ 3,937,880 $ 4,686,212 $ 4,975,811 $ 4,082,581

9 Spain $ 3,473,062 $ 3,826,734 $ 5,305,650 $ 5,301,387 $ 3,704,743

10 Switzerland $ 2,889,740 $ 3,092,232 $ 3,728,420 $ 4,086,876 $ 3,599,410

17 China $ 820,527 $ 944,845 $ 1,299,778 $ 1,526,475 $ 1,841,701

55 Viet Nam $ 70,745 $ 95,814 $ 128,735 $ 160,296 $ 302,665

95 Ethiopia $ 46,132 $ 61,094 $ 71,666 $ 70,081 $ 66,381 Sources: ITC calculations based on COMTRADE statistics

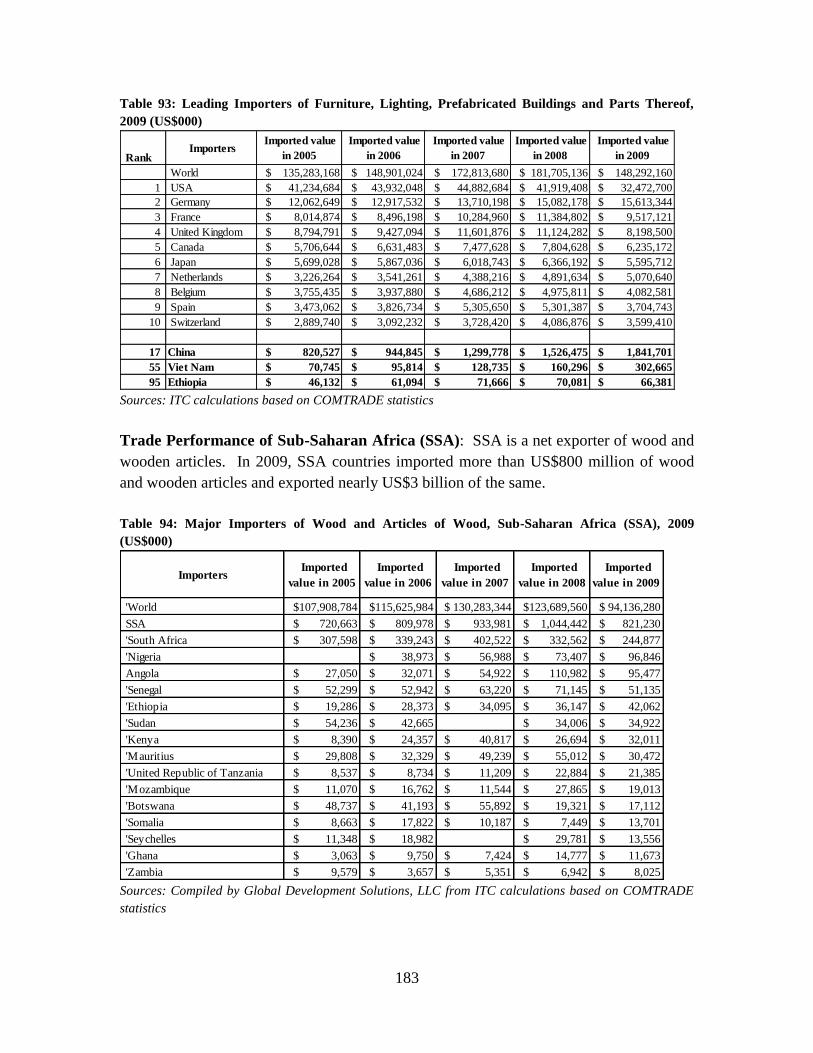

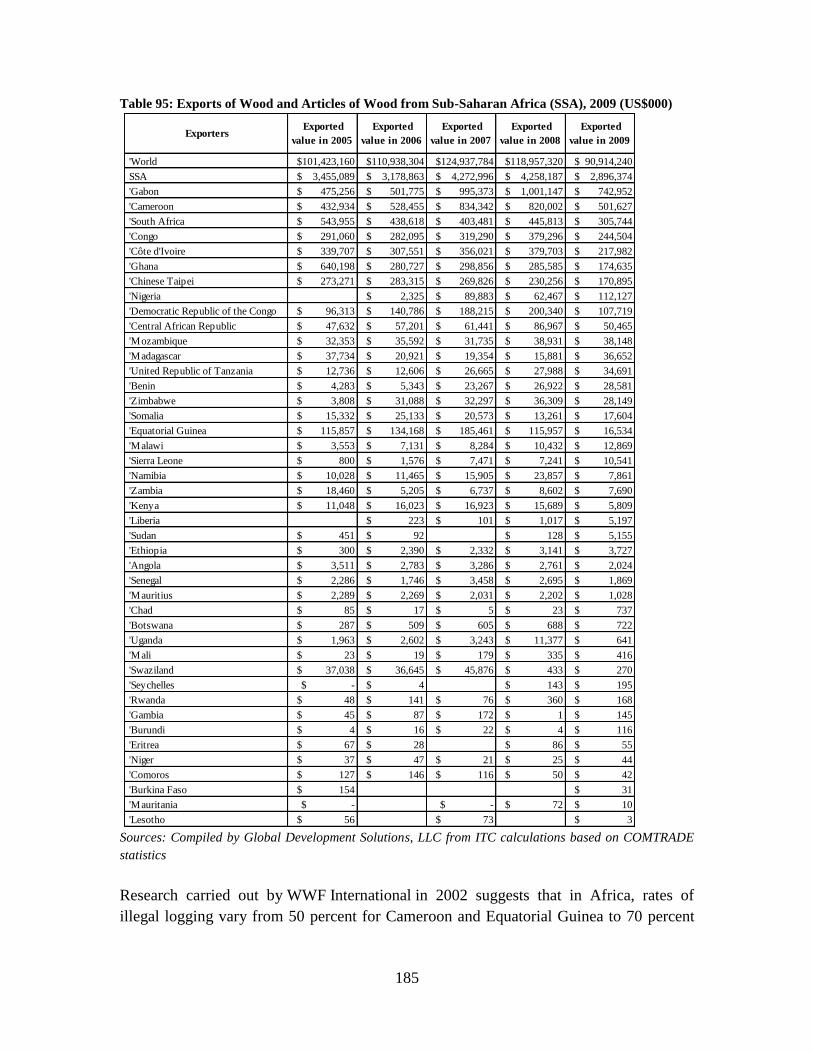

Trade Performance of Sub-Saharan Africa (SSA): SSA is a net exporter of wood and

wooden articles. In 2009, SSA countries imported more than US$800 million of wood

and wooden articles and exported nearly US$3 billion of the same.

Table 94: Major Importers of Wood and Articles of Wood, Sub-Saharan Africa (SSA), 2009

(US$000)

Importers Imported

value in 2005

Imported

value in 2006

Imported

value in 2007

Imported

value in 2008

Imported

value in 2009

'World $107,908,784 $115,625,984 $ 130,283,344 $123,689,560 $ 94,136,280

SSA $ 720,663 $ 809,978 $ 933,981 $ 1,044,442 $ 821,230

'South Africa $ 307,598 $ 339,243 $ 402,522 $ 332,562 $ 244,877

'Nigeria $ 38,973 $ 56,988 $ 73,407 $ 96,846

Angola $ 27,050 $ 32,071 $ 54,922 $ 110,982 $ 95,477

'Senegal $ 52,299 $ 52,942 $ 63,220 $ 71,145 $ 51,135

'Ethiopia $ 19,286 $ 28,373 $ 34,095 $ 36,147 $ 42,062

'Sudan $ 54,236 $ 42,665 $ 34,006 $ 34,922

'Kenya $ 8,390 $ 24,357 $ 40,817 $ 26,694 $ 32,011

'Mauritius $ 29,808 $ 32,329 $ 49,239 $ 55,012 $ 30,472

'United Republic of Tanzania $ 8,537 $ 8,734 $ 11,209 $ 22,884 $ 21,385

'Mozambique $ 11,070 $ 16,762 $ 11,544 $ 27,865 $ 19,013

'Botswana $ 48,737 $ 41,193 $ 55,892 $ 19,321 $ 17,112

'Somalia $ 8,663 $ 17,822 $ 10,187 $ 7,449 $ 13,701

'Seychelles $ 11,348 $ 18,982 $ 29,781 $ 13,556

'Ghana $ 3,063 $ 9,750 $ 7,424 $ 14,777 $ 11,673

'Zambia $ 9,579 $ 3,657 $ 5,351 $ 6,942 $ 8,025 Sources: Compiled by Global Development Solutions, LLC from ITC calculations based on COMTRADE

statistics

184

South Africa, with its relatively developed wood processing industry and housing market,

is the largest SSA importer of wood, followed by Nigeria and Angola (Table 94 above).

Most SSA countries import limited amounts and are net exporters of wood.

In terms of exports, five countries export 90 percent (US$2 billion) of all wood and

articles of wood from SSA each year: Gabon, Cameroon, South Africa, Congo and Ivory

Coast. Illegal logging is rife in SSA and export figures are generally considered to reflect

only a portion of actual wood exports from the region.

185

Table 95: Exports of Wood and Articles of Wood from Sub-Saharan Africa (SSA), 2009 (US$000)

Exporters Exported

value in 2005

Exported

value in 2006

Exported

value in 2007

Exported

value in 2008

Exported

value in 2009

'World $101,423,160 $110,938,304 $124,937,784 $118,957,320 $ 90,914,240

SSA $ 3,455,089 $ 3,178,863 $ 4,272,996 $ 4,258,187 $ 2,896,374

'Gabon $ 475,256 $ 501,775 $ 995,373 $ 1,001,147 $ 742,952

'Cameroon $ 432,934 $ 528,455 $ 834,342 $ 820,002 $ 501,627

'South Africa $ 543,955 $ 438,618 $ 403,481 $ 445,813 $ 305,744

'Congo $ 291,060 $ 282,095 $ 319,290 $ 379,296 $ 244,504

'Côte d'Ivoire $ 339,707 $ 307,551 $ 356,021 $ 379,703 $ 217,982

'Ghana $ 640,198 $ 280,727 $ 298,856 $ 285,585 $ 174,635

'Chinese Taipei $ 273,271 $ 283,315 $ 269,826 $ 230,256 $ 170,895

'Nigeria $ 2,325 $ 89,883 $ 62,467 $ 112,127

'Democratic Republic of the Congo $ 96,313 $ 140,786 $ 188,215 $ 200,340 $ 107,719

'Central African Republic $ 47,632 $ 57,201 $ 61,441 $ 86,967 $ 50,465

'Mozambique $ 32,353 $ 35,592 $ 31,735 $ 38,931 $ 38,148

'Madagascar $ 37,734 $ 20,921 $ 19,354 $ 15,881 $ 36,652

'United Republic of Tanzania $ 12,736 $ 12,606 $ 26,665 $ 27,988 $ 34,691

'Benin $ 4,283 $ 5,343 $ 23,267 $ 26,922 $ 28,581

'Zimbabwe $ 3,808 $ 31,088 $ 32,297 $ 36,309 $ 28,149

'Somalia $ 15,332 $ 25,133 $ 20,573 $ 13,261 $ 17,604

'Equatorial Guinea $ 115,857 $ 134,168 $ 185,461 $ 115,957 $ 16,534

'Malawi $ 3,553 $ 7,131 $ 8,284 $ 10,432 $ 12,869

'Sierra Leone $ 800 $ 1,576 $ 7,471 $ 7,241 $ 10,541

'Namibia $ 10,028 $ 11,465 $ 15,905 $ 23,857 $ 7,861

'Zambia $ 18,460 $ 5,205 $ 6,737 $ 8,602 $ 7,690

'Kenya $ 11,048 $ 16,023 $ 16,923 $ 15,689 $ 5,809

'Liberia $ 223 $ 101 $ 1,017 $ 5,197

'Sudan $ 451 $ 92 $ 128 $ 5,155

'Ethiopia $ 300 $ 2,390 $ 2,332 $ 3,141 $ 3,727

'Angola $ 3,511 $ 2,783 $ 3,286 $ 2,761 $ 2,024

'Senegal $ 2,286 $ 1,746 $ 3,458 $ 2,695 $ 1,869

'Mauritius $ 2,289 $ 2,269 $ 2,031 $ 2,202 $ 1,028

'Chad $ 85 $ 17 $ 5 $ 23 $ 737

'Botswana $ 287 $ 509 $ 605 $ 688 $ 722

'Uganda $ 1,963 $ 2,602 $ 3,243 $ 11,377 $ 641

'Mali $ 23 $ 19 $ 179 $ 335 $ 416

'Swaziland $ 37,038 $ 36,645 $ 45,876 $ 433 $ 270

'Seychelles $ - $ 4 $ 143 $ 195

'Rwanda $ 48 $ 141 $ 76 $ 360 $ 168

'Gambia $ 45 $ 87 $ 172 $ 1 $ 145

'Burundi $ 4 $ 16 $ 22 $ 4 $ 116

'Eritrea $ 67 $ 28 $ 86 $ 55

'Niger $ 37 $ 47 $ 21 $ 25 $ 44

'Comoros $ 127 $ 146 $ 116 $ 50 $ 42

'Burkina Faso $ 154 $ 31

'Mauritania $ - $ - $ 72 $ 10

'Lesotho $ 56 $ 73 $ 3 Sources: Compiled by Global Development Solutions, LLC from ITC calculations based on COMTRADE

statistics

Research carried out by WWF International in 2002 suggests that in Africa, rates of

illegal logging vary from 50 percent for Cameroon and Equatorial Guinea to 70 percent

186

in Gabon and 80 percent in Liberia.79

What generally is known is that the bulk of exports

from SSA are in the form of rough unprocessed logs (roundwood). Mirror trade data

from Gabon, for example, show that 75 percent (US$550 million) of the officially

recorded exports are in the form of rough wood. Almost 90 percent of Cameroon‘s

officially recorded exports are in the form of rough or sawn wood form.

The most valued forms of wood exports, such as builder‘s joinery and carpentry of wood

(includes doors, windows, flooring, etc.), are done in limited scale in only a few SSA

countries. South Africa, for example, exported US$30 million of builders‘ joinery in

2009 (US$20 million of which are doors and their frames), down from US$80 million in

2005. The next SSA countries to export valuable builder‘s joinery can be found at the

very bottom of the list of exporters: Zimbabwe and Ivory Coast, each with roughly US$2

million of builder‘s joinery exports in 2009.

The inability of SSA countries to add value to their wood resources is further exemplified

by the furniture trade. South Africa alone exports roughly 90 percent of all furniture and

lighting products from SSA (in value terms). All the rest of SSA countries combined

exported US$61 million worth of furniture and related articles of all types; only 0.04

percent of the world exports.

Table 96: Leading SSA Exporters of Furniture, Lighting, Prefabricated Buildings and Parts Thereof,

2009 (US$000)

Exporters Exported

value in 2005

Exported

value in 2006

Exported

value in 2007

Exported

value in 2008

Exported

value in 2009

'World $ 124,214,448 $ 137,889,120 $ 162,352,480 $ 177,069,552 $ 145,963,616

SSA $ 670,836 $ 631,158 $ 719,545 $ 724,320 $ 519,253

'South Africa $ 594,544 $ 539,386 $ 605,587 $ 588,922 $ 457,511

'Nigeria $ 96 $ 925 $ 2,358 $ 8,936

'Kenya $ 15,532 $ 22,646 $ 21,303 $ 21,349 $ 7,341

'Malawi $ 2,554 $ 3,484 $ 1,874 $ 3,121 $ 5,687

'Angola $ 90 $ 88 $ 672 $ 229 $ 5,318

'Mauritius $ 3,293 $ 3,165 $ 3,365 $ 4,031 $ 4,780

'Ghana $ 8,595 $ 14,018 $ 6,305 $ 8,518 $ 3,895

Tanzania $ 876 $ 1,864 $ 2,897 $ 27,381 $ 2,693

'Burkina Faso $ 1,616 $ 2,413

'Mozambique $ 298 $ 1,012 $ 432 $ 6,271 $ 2,272

'Sierra Leone $ 3,576 $ 2,711 $ 2,902 $ 1,400 $ 2,104

'Cameroon $ 968 $ 502 $ 1,562 $ 2,120 $ 2,092

'Zambia $ 210 $ 709 $ 20,206 $ 631 $ 1,992

'Senegal $ 1,485 $ 1,985 $ 3,272 $ 2,791 $ 1,904

'Botswana $ 2,403 $ 2,447 $ 3,256 $ 1,333 $ 1,814

'Côte d'Ivoire $ 8,354 $ 5,496 $ 8,045 $ 2,432 $ 1,808

'Rwanda $ 97 $ 9 $ 50 $ 421 $ 1,799

'Ethiopia $ 453 $ 137 $ 1,296 $ 2,333 $ 1,528

79

The Timber Footprint of G8 and China, WWF International, 2002.

187

Sources: Compiled by Global Development Solutions, LLC from ITC calculations based on COMTRADE

statistics

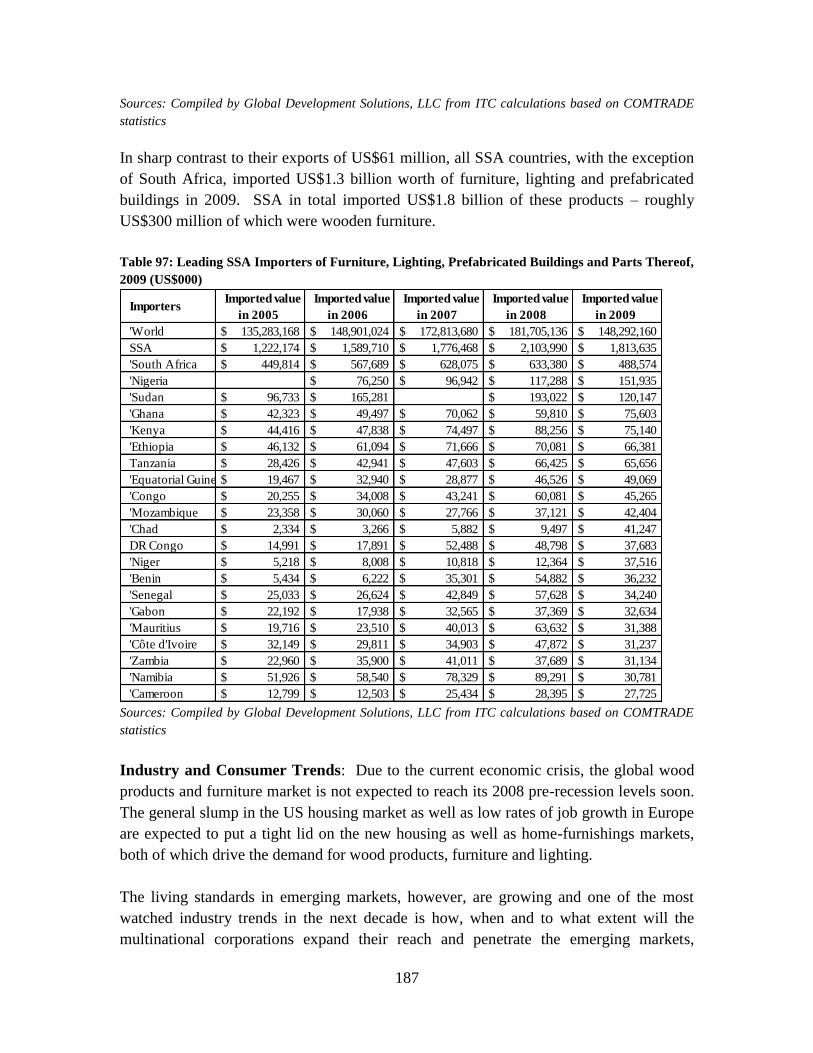

In sharp contrast to their exports of US$61 million, all SSA countries, with the exception

of South Africa, imported US$1.3 billion worth of furniture, lighting and prefabricated

buildings in 2009. SSA in total imported US$1.8 billion of these products – roughly

US$300 million of which were wooden furniture.

Table 97: Leading SSA Importers of Furniture, Lighting, Prefabricated Buildings and Parts Thereof,

2009 (US$000)

Importers Imported value

in 2005

Imported value

in 2006

Imported value

in 2007

Imported value

in 2008

Imported value

in 2009

'World $ 135,283,168 $ 148,901,024 $ 172,813,680 $ 181,705,136 $ 148,292,160

SSA $ 1,222,174 $ 1,589,710 $ 1,776,468 $ 2,103,990 $ 1,813,635

'South Africa $ 449,814 $ 567,689 $ 628,075 $ 633,380 $ 488,574

'Nigeria $ 76,250 $ 96,942 $ 117,288 $ 151,935

'Sudan $ 96,733 $ 165,281 $ 193,022 $ 120,147

'Ghana $ 42,323 $ 49,497 $ 70,062 $ 59,810 $ 75,603

'Kenya $ 44,416 $ 47,838 $ 74,497 $ 88,256 $ 75,140

'Ethiopia $ 46,132 $ 61,094 $ 71,666 $ 70,081 $ 66,381

Tanzania $ 28,426 $ 42,941 $ 47,603 $ 66,425 $ 65,656

'Equatorial Guinea $ 19,467 $ 32,940 $ 28,877 $ 46,526 $ 49,069

'Congo $ 20,255 $ 34,008 $ 43,241 $ 60,081 $ 45,265

'Mozambique $ 23,358 $ 30,060 $ 27,766 $ 37,121 $ 42,404

'Chad $ 2,334 $ 3,266 $ 5,882 $ 9,497 $ 41,247

DR Congo $ 14,991 $ 17,891 $ 52,488 $ 48,798 $ 37,683

'Niger $ 5,218 $ 8,008 $ 10,818 $ 12,364 $ 37,516

'Benin $ 5,434 $ 6,222 $ 35,301 $ 54,882 $ 36,232

'Senegal $ 25,033 $ 26,624 $ 42,849 $ 57,628 $ 34,240

'Gabon $ 22,192 $ 17,938 $ 32,565 $ 37,369 $ 32,634

'Mauritius $ 19,716 $ 23,510 $ 40,013 $ 63,632 $ 31,388

'Côte d'Ivoire $ 32,149 $ 29,811 $ 34,903 $ 47,872 $ 31,237

'Zambia $ 22,960 $ 35,900 $ 41,011 $ 37,689 $ 31,134

'Namibia $ 51,926 $ 58,540 $ 78,329 $ 89,291 $ 30,781

'Cameroon $ 12,799 $ 12,503 $ 25,434 $ 28,395 $ 27,725 Sources: Compiled by Global Development Solutions, LLC from ITC calculations based on COMTRADE

statistics

Industry and Consumer Trends: Due to the current economic crisis, the global wood

products and furniture market is not expected to reach its 2008 pre-recession levels soon.

The general slump in the US housing market as well as low rates of job growth in Europe

are expected to put a tight lid on the new housing as well as home-furnishings markets,

both of which drive the demand for wood products, furniture and lighting.

The living standards in emerging markets, however, are growing and one of the most

watched industry trends in the next decade is how, when and to what extent will the

multinational corporations expand their reach and penetrate the emerging markets,

188

especially in China, Russia, and India. China‘s home-furnishings market, for example, is

estimated at US$28 billion in 2010 and is growing with the prosperity of its workforce

and attracting major investments by multinationals. Ikea, for example, plans to more than

double the number of its outlets in China to 18 by 2015, thus making a total investment of

nearly US$1.5 billion in the country. Investment by Ikea and other retailers in Russia,

India, Brazil, etc., also are increasing.

The wood/furniture industry also is seeing significant trends in the direction of:

Increased awareness among consumers on issues related to sustainable forestry,

chain of custody and other good forest-to-furniture industry practices; and

Increased regulatory interventions in the EU and North America, especially in the

direction of laws for elimination of formaldehyde in wood products and laws

against illegal exploitation of wood.

The last point warrants further explanation as it relates indirectly to Sub-Saharan Africa

and its timber exports. The Lacey Act, which stipulates that wood products in the USA

must have certification showing they are legal, came into effect in April 2010 in the USA.

Unlike previous related legislation, this statute is fact-based rather than document-based.

If a product imported into the US turns out be of illegal (logging) origin, this fact will

override any statement or document to the contrary. In addition, under the EU Due

Diligence Regulation, which will be mandatory from January 2012, everyone selling

timber to the EU will have to use a ‗checking‘ system to ensure that wood is not illegal.

As a result of these developments, many furniture and wood processing firms throughout

the world are increasingly implementing chain of custody supply chain management

policies to avoid sanctions and safeguard their prestige. In Vietnam, for example, almost

200 wood processing firms use chain of custody management practice. Chain of custody

is being used increasingly more in China although precise figures are not available.

The chain of custody measures implemented by wood processing firms globally are

anticipated to affect negatively Sub-Saharan Africa (SSA). SSA is a big supplier of

tropical timber to wood processing firms worldwide, but the region is known and

suspected to have high rates of illegal logging. The region‘s ability to maintain its

exports of timber is most likely to be challenged by the recent regulations in the main

consumer markets in the EU and USA. The degree to which SSA exports will be

challenged by recent regulations in the USA and EU currently is not known. What is

known is that, notwithstanding the regulations, identification of illegally logged or traded

wood is technically difficult. In this respect, in the short-term, recent regulations are

likely to adversely impact (depress) prices of wood coming from SSA more than the

actual volume of wood coming from SSA.

189

V.4. Comparative Sector Profiles: Wood Products Sector

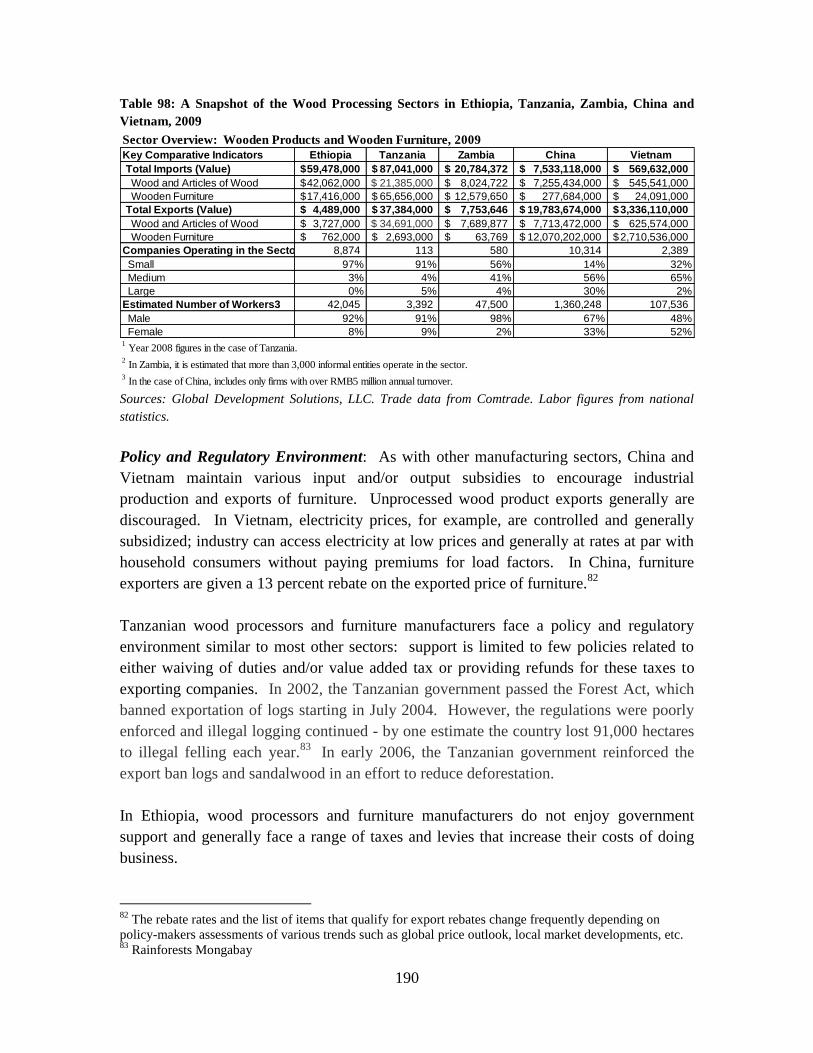

Key Indicators: Similar to most other sectors, China‘s presence in the furniture industry

has grown significantly over the last decade. Chinese furniture exports increased by 335

percent from 1994 to 2001, and by 545 percent from 2001 to 2009 when the total export

value of furniture reached US$25.6 billion. According to the official Chinese Bureau of

Statistics, the wood processing and furniture industry employed roughly 1.3 million

people in almost 11,000 firms in 2008. This statistic, however, covers only a certain size

of firms (those with reported revenues of RMB5 million), which leaves many small and

medium firms out of the official statistics. According to some estimates, the furniture

industry alone employs over 5 million people. Approximately 30 percent of the total

shipments and 50 percent of the export of furniture are from one south China province:

Guangdong.

In Ethiopia, roughly 9,000 firms employing 42,000 people operate in the wooden

products and furniture sector. The vast majority of firms in the sector are small and most

workers in the industry are male. The situation is almost identical in Tanzania: roughly

90 percent of the workers in the sector are male and work in small firms.80

In Zambia, a

higher percentage of the more than 47,000 workers are male (approximately 98 percent)

and a higher percentage of the firms are of medium size (41 percent) (Table 98).81

In

Vietnam and China, there is a mix of enterprises in terms of their size. Since the official

Chinese statistics do not capture enterprises with turnover less than RMB5 million, the

share of small firms in the industry is most probably much higher than the 14 percent

reported by the official statistics.

80

Data for Tanzania does not include micro/small enterprises employing less than 10 people. Data for such

firms, such as small workshops, repair shops, etc, are not available – an estimated 95 percent of all

manufacturing firms belong in this unregistered category of firms. 81

As is the case with Tanzania, Zambia has a significant informal sector and it is not known how much

these unregistered companies are accounted for in the statistics.

190

Table 98: A Snapshot of the Wood Processing Sectors in Ethiopia, Tanzania, Zambia, China and

Vietnam, 2009

Sector Overview: Wooden Products and Wooden Furniture, 2009

Key Comparative Indicators Ethiopia Tanzania Zambia China Vietnam

Total Imports (Value) 59,478,000$ 87,041,000$ 20,784,372$ 7,533,118,000$ 569,632,000$

Wood and Articles of Wood 42,062,000$ $ 21,385,000 8,024,722$ 7,255,434,000$ 545,541,000$

Wooden Furniture 17,416,000$ 65,656,000$ 12,579,650$ 277,684,000$ 24,091,000$

Total Exports (Value) 4,489,000$ 37,384,000$ 7,753,646$ 19,783,674,000$ 3,336,110,000$

Wood and Articles of Wood 3,727,000$ $ 34,691,000 7,689,877$ 7,713,472,000$ 625,574,000$

Wooden Furniture 762,000$ 2,693,000$ 63,769$ 12,070,202,000$ 2,710,536,000$

Companies Operating in the Sector1,2,3 8,874 113 580 10,314 2,389

Small 97% 91% 56% 14% 32%

Medium 3% 4% 41% 56% 65%

Large 0% 5% 4% 30% 2%

Estimated Number of Workers3 42,045 3,392 47,500 1,360,248 107,536

Male 92% 91% 98% 67% 48%

Female 8% 9% 2% 33% 52%1 Year 2008 figures in the case of Tanzania.

2 In Zambia, it is estimated that more than 3,000 informal entities operate in the sector.

3 In the case of China, includes only firms with over RMB5 million annual turnover.

Sources: Global Development Solutions, LLC. Trade data from Comtrade. Labor figures from national

statistics.

Policy and Regulatory Environment: As with other manufacturing sectors, China and

Vietnam maintain various input and/or output subsidies to encourage industrial

production and exports of furniture. Unprocessed wood product exports generally are

discouraged. In Vietnam, electricity prices, for example, are controlled and generally

subsidized; industry can access electricity at low prices and generally at rates at par with

household consumers without paying premiums for load factors. In China, furniture

exporters are given a 13 percent rebate on the exported price of furniture.82

Tanzanian wood processors and furniture manufacturers face a policy and regulatory

environment similar to most other sectors: support is limited to few policies related to

either waiving of duties and/or value added tax or providing refunds for these taxes to

exporting companies. In 2002, the Tanzanian government passed the Forest Act, which

banned exportation of logs starting in July 2004. However, the regulations were poorly

enforced and illegal logging continued - by one estimate the country lost 91,000 hectares

to illegal felling each year.83

In early 2006, the Tanzanian government reinforced the

export ban logs and sandalwood in an effort to reduce deforestation.

In Ethiopia, wood processors and furniture manufacturers do not enjoy government

support and generally face a range of taxes and levies that increase their costs of doing

business.

82

The rebate rates and the list of items that qualify for export rebates change frequently depending on

policy-makers assessments of various trends such as global price outlook, local market developments, etc. 83

Rainforests Mongabay

191

In Zambia, because the wood sector is considered a non-traditional product (NTE), the

government grants some incentives for the wood and wood processing sector. Incentives

include reduced income tax for net exporters (35 percent reduced to 15 percent), 1/7th

reduction of income tax for rural enterprises in the first five years after establishment, and

reduced duties (5 percent - 15 percent) on various inputs and machinery. However, lack

of regulations/control at the forestry level was evidenced in interviews with larger

companies, suggesting that there is illegal trade in timber occurring in the industry. This

is attributed to lack of control and policies where things are left to traditional leaders to

charge royalties especially for the open area forests.

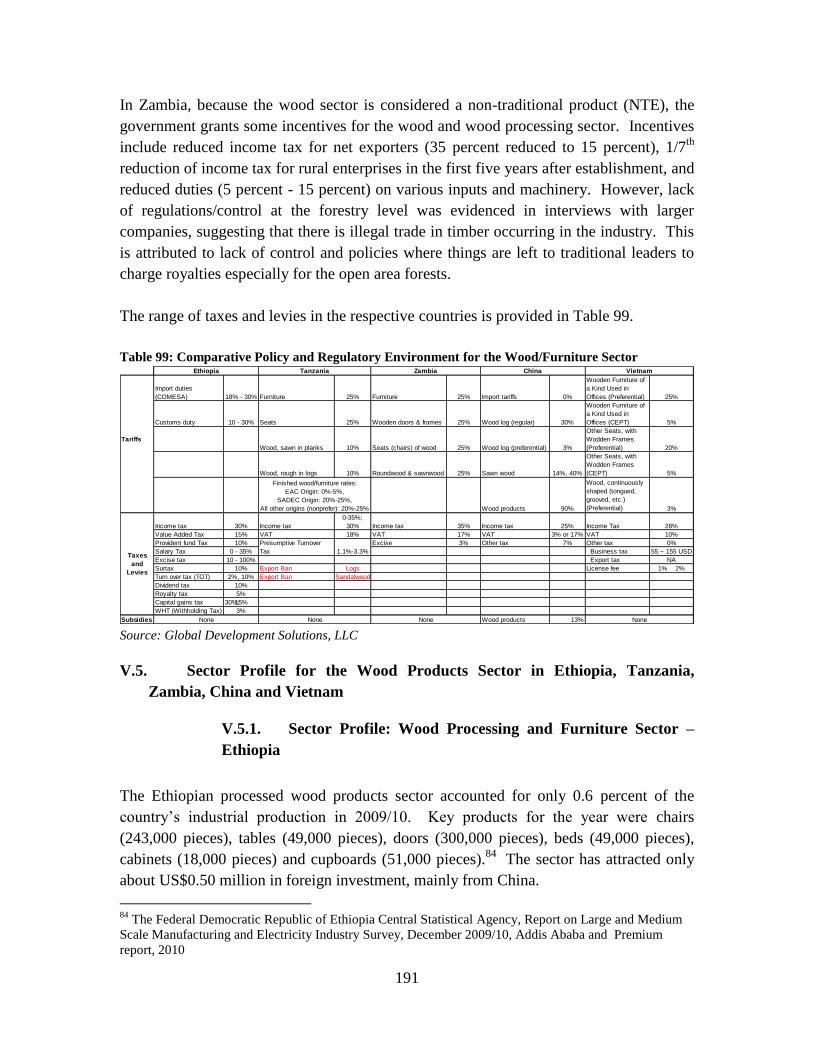

The range of taxes and levies in the respective countries is provided in Table 99.

Table 99: Comparative Policy and Regulatory Environment for the Wood/Furniture Sector

Import duties

(COMESA) 18% - 30% Furniture 25% Furniture 25% Import tariffs 0%

Wooden Furniture of

a Kind Used in

Offices (Preferential) 25%

Customs duty 10 - 30% Seats 25% Wooden doors & frames 25% Wood log (regular) 30%

Wooden Furniture of

a Kind Used in

Offices (CEPT) 5%

Tariffs

Wood, sawn in planks 10% Seats (chairs) of wood 25% Wood log (preferential) 3%

Other Seats, with

Wodden Frames

(Preferential) 20%

Wood, rough in logs 10% Roundwood & sawnwood 25% Sawn wood 14%, 40%

Other Seats, with

Wodden Frames

(CEPT) 5%

Wood products 90%

Wood, continuously

shaped (tongued,

grooved, etc.)

(Preferential) 3%

Income tax 30% Income tax

0-35%;

30% Income tax 35% Income tax 25% Income Tax 28%

Value Added Tax 15% VAT 18% VAT 17% VAT 3% or 17% VAT 10%

Provident fund Tax 10% Excise 3% Other tax 7% Other tax 0%

Salary Tax 0 - 35% Business tax 55 ~ 155 USD

Excise tax 10 - 100% Export tax NA

Surtax 10% Export Ban Logs License fee 1% 2%

Turn over tax (TOT) 2%, 10% Export Ban Sandalwood

Dividend tax 10%

Royalty tax 5%

Capital gains tax 30%;15%

WHT (Withholding Tax) 3%

Subsidies Wood products 13%

China Vietnam

NoneNoneNone

ZambiaEthiopia Tanzania

Finished wood/furniture rates:

EAC Origin: 0%-5%,

SADEC Origin: 20%-25%,

All other origins (nonprefer): 20%-25%

None

Presumptive Turnover

Tax 1.1%-3.3%Taxes

and

Levies

Source: Global Development Solutions, LLC

V.5. Sector Profile for the Wood Products Sector in Ethiopia, Tanzania,

Zambia, China and Vietnam

V.5.1. Sector Profile: Wood Processing and Furniture Sector –

Ethiopia

The Ethiopian processed wood products sector accounted for only 0.6 percent of the

country‘s industrial production in 2009/10. Key products for the year were chairs

(243,000 pieces), tables (49,000 pieces), doors (300,000 pieces), beds (49,000 pieces),

cabinets (18,000 pieces) and cupboards (51,000 pieces).84

The sector has attracted only

about US$0.50 million in foreign investment, mainly from China.

84

The Federal Democratic Republic of Ethiopia Central Statistical Agency, Report on Large and Medium

Scale Manufacturing and Electricity Industry Survey, December 2009/10, Addis Ababa and Premium

report, 2010

192

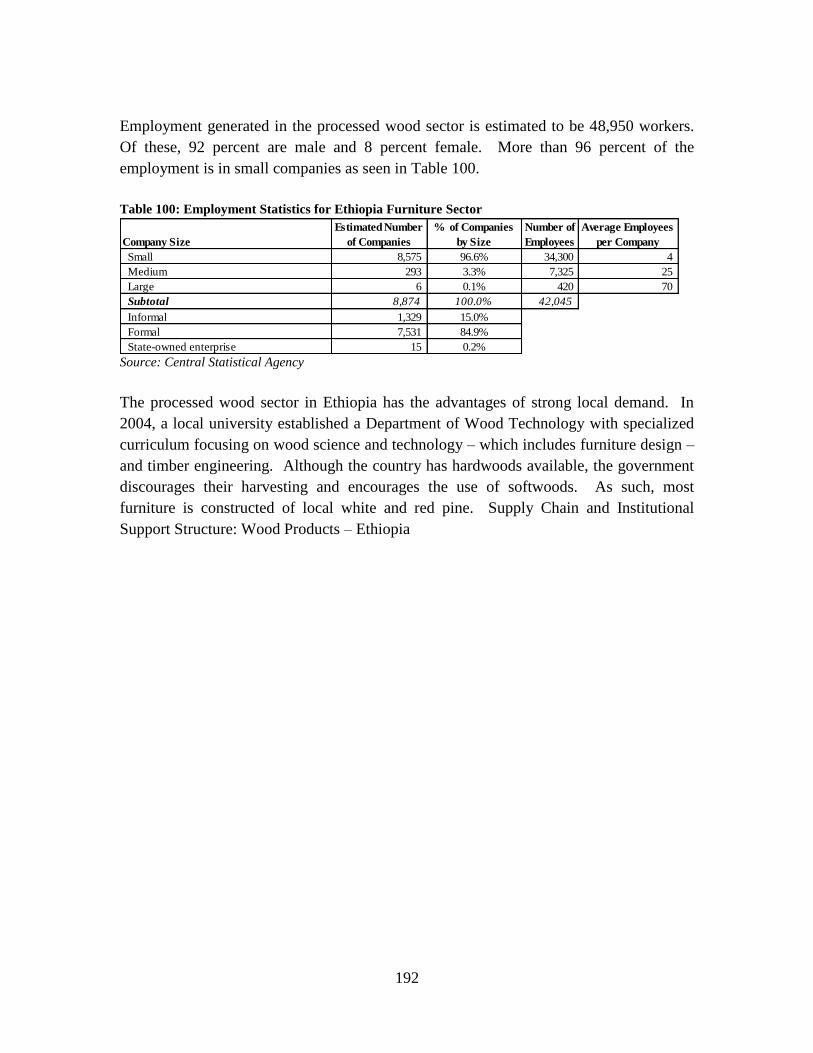

Employment generated in the processed wood sector is estimated to be 48,950 workers.

Of these, 92 percent are male and 8 percent female. More than 96 percent of the

employment is in small companies as seen in Table 100.

Table 100: Employment Statistics for Ethiopia Furniture Sector

Company Size

Estimated Number

of Companies

% of Companies

by Size

Number of

Employees

Average Employees

per Company

Small 8,575 96.6% 34,300 4

Medium 293 3.3% 7,325 25

Large 6 0.1% 420 70

Subtotal 8,874 100.0% 42,045

Informal 1,329 15.0%

Formal 7,531 84.9%

State-owned enterprise 15 0.2% Source: Central Statistical Agency

The processed wood sector in Ethiopia has the advantages of strong local demand. In

2004, a local university established a Department of Wood Technology with specialized

curriculum focusing on wood science and technology – which includes furniture design –

and timber engineering. Although the country has hardwoods available, the government

discourages their harvesting and encourages the use of softwoods. As such, most

furniture is constructed of local white and red pine. Supply Chain and Institutional

Support Structure: Wood Products – Ethiopia

193

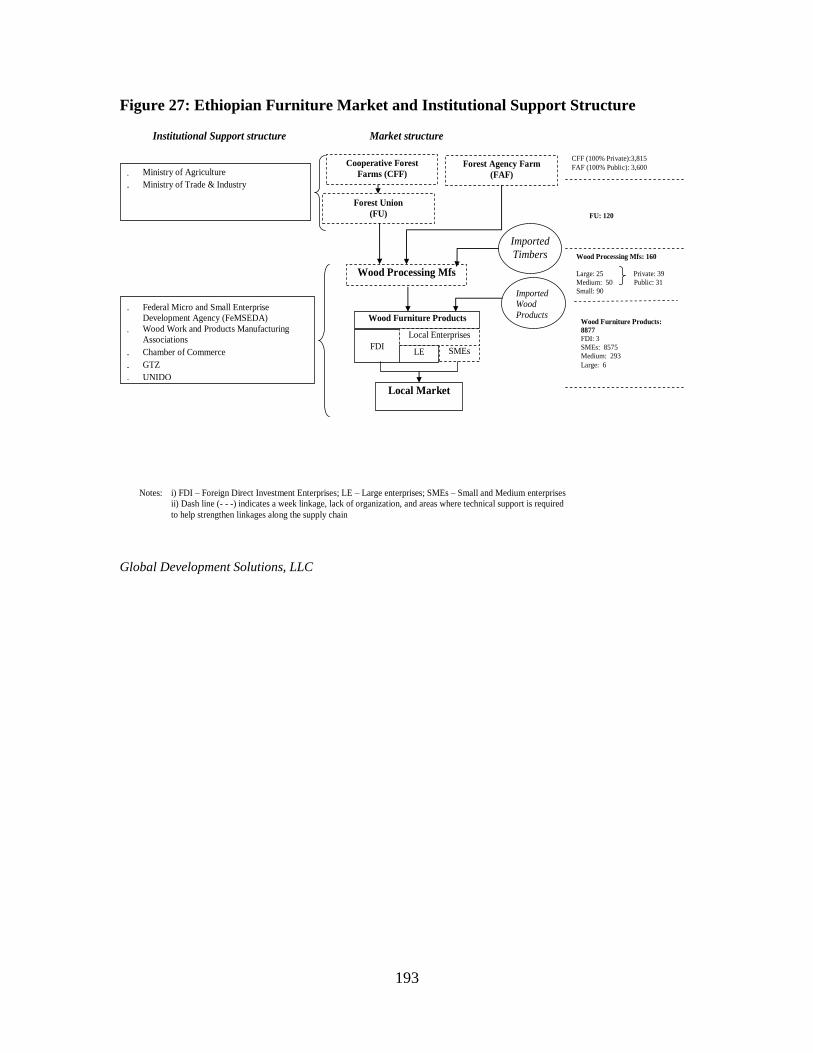

Figure 27: Ethiopian Furniture Market and Institutional Support Structure Ethiopian Furniture Market and Institutional Support Structure

Market structure Institutional Support structure

Cooperative Forest Farms (CFF)

- Ministry of Agriculture

- Ministry of Trade & Industry

Wood Processing Mfs

Imported

Timbers

Wood Furniture Products

FDI LE SMEs

Local Market

- Federal Micro and Small Enterprise

Development Agency (FeMSEDA) - Wood Work and Products Manufacturing

Associations

- Chamber of Commerce

- GTZ

- UNIDO

Notes: i) FDI – Foreign Direct Investment Enterprises; LE – Large enterprises; SMEs – Small and Medium enterprises

ii) Dash line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required

to help strengthen linkages along the supply chain

Local Enterprises

CFF (100% Private):3,815

FAF (100% Public): 3,600

Wood Furniture Products:

8877

FDI: 3

SMEs: 8575

Medium: 293

Large: 6

Forest Agency Farm

(FAF)

Forest Union

(FU)

Imported

Wood

Products

FU: 120

Wood Processing Mfs: 160

Large: 25 Private: 39

Medium: 50 Public: 31

Small: 90

Global Development Solutions, LLC

194

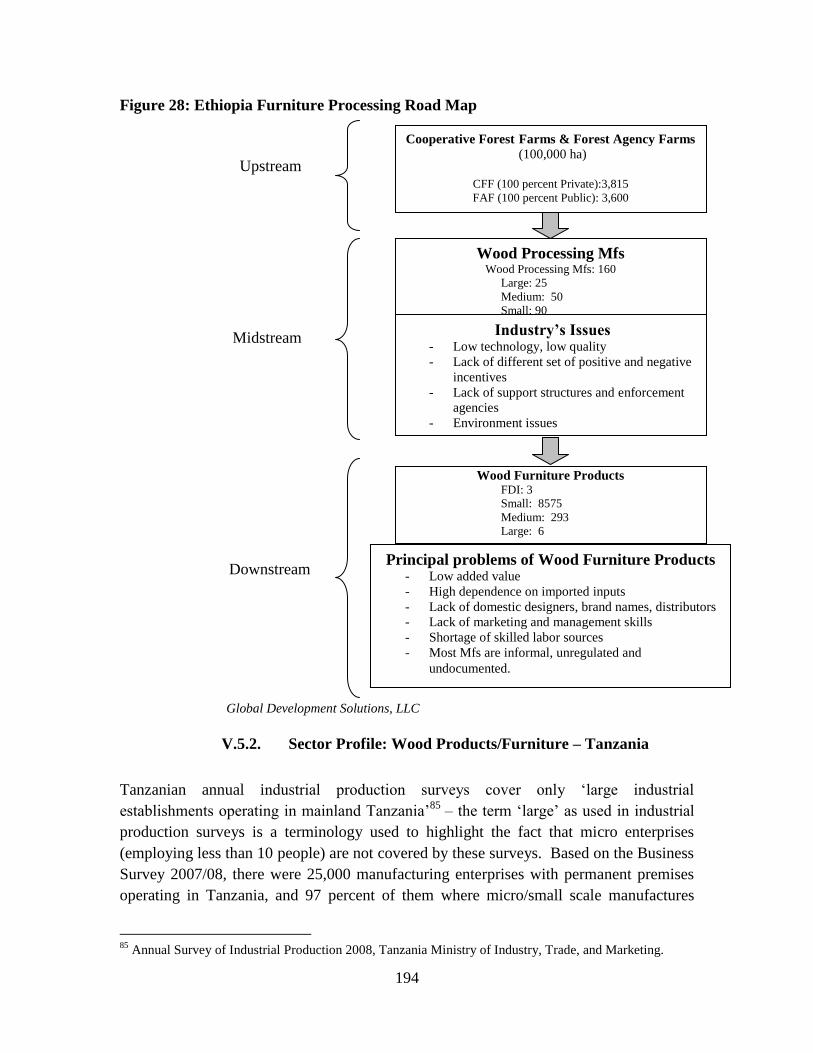

Figure 28: Ethiopia Furniture Processing Road Map

Global Development Solutions, LLC

V.5.2. Sector Profile: Wood Products/Furniture – Tanzania

Tanzanian annual industrial production surveys cover only ‗large industrial

establishments operating in mainland Tanzania‘85

– the term ‗large‘ as used in industrial

production surveys is a terminology used to highlight the fact that micro enterprises

(employing less than 10 people) are not covered by these surveys. Based on the Business

Survey 2007/08, there were 25,000 manufacturing enterprises with permanent premises

operating in Tanzania, and 97 percent of them where micro/small scale manufactures

85

Annual Survey of Industrial Production 2008, Tanzania Ministry of Industry, Trade, and Marketing.

Cooperative Forest Farms & Forest Agency Farms (100,000 ha)

CFF (100 percent Private):3,815

FAF (100 percent Public): 3,600

Wood Processing Mfs Wood Processing Mfs: 160

Large: 25

Medium: 50

Small: 90

Industry’s Issues - Low technology, low quality

- Lack of different set of positive and negative

incentives

- Lack of support structures and enforcement

agencies

- Environment issues

Wood Furniture Products FDI: 3

Small: 8575

Medium: 293

Large: 6

Upstream

Downstream Principal problems of Wood Furniture Products

- Low added value

- High dependence on imported inputs

- Lack of domestic designers, brand names, distributors

- Lack of marketing and management skills

- Shortage of skilled labor sources

- Most Mfs are informal, unregulated and

undocumented.

Midstream

195

with less than 10 workers. 86

Virtually no official data is kept on micro/small scale

manufacturing enterprises, as such this sector profile covers only firms employing 10 or

more people, officially recorded as ‗industrial enterprises/manufacturing establishments‘

under national statistics.

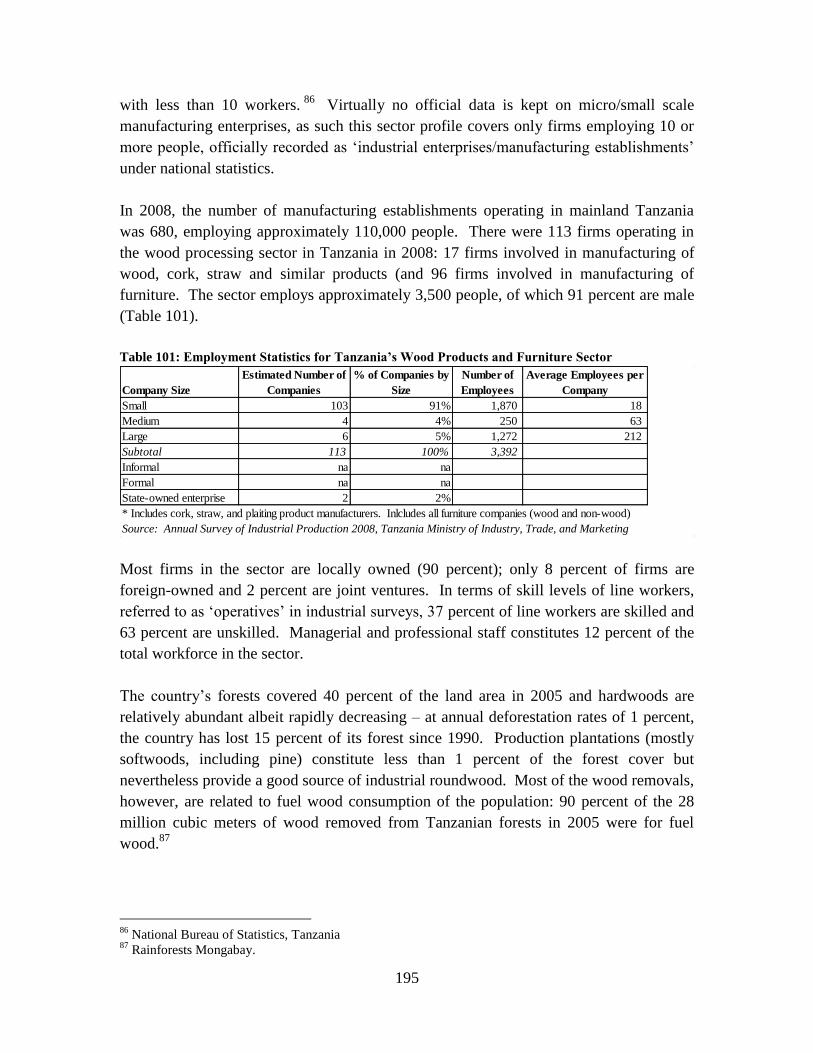

In 2008, the number of manufacturing establishments operating in mainland Tanzania

was 680, employing approximately 110,000 people. There were 113 firms operating in

the wood processing sector in Tanzania in 2008: 17 firms involved in manufacturing of

wood, cork, straw and similar products (and 96 firms involved in manufacturing of

furniture. The sector employs approximately 3,500 people, of which 91 percent are male

(Table 101).

Table 101: Employment Statistics for Tanzania’s Wood Products and Furniture Sector

Company Size

Estimated Number of

Companies

% of Companies by

Size

Number of

Employees

Average Employees per

Company

Small 103 91% 1,870 18

Medium 4 4% 250 63

Large 6 5% 1,272 212

Subtotal 113 100% 3,392

Informal na na

Formal na na

State-owned enterprise 2 2%

* Includes cork, straw, and plaiting product manufacturers. Inlcludes all furniture companies (wood and non-wood)

Source: Annual Survey of Industrial Production 2008, Tanzania Ministry of Industry, Trade, and Marketing

Most firms in the sector are locally owned (90 percent); only 8 percent of firms are

foreign-owned and 2 percent are joint ventures. In terms of skill levels of line workers,

referred to as ‗operatives‘ in industrial surveys, 37 percent of line workers are skilled and

63 percent are unskilled. Managerial and professional staff constitutes 12 percent of the

total workforce in the sector.

The country‘s forests covered 40 percent of the land area in 2005 and hardwoods are

relatively abundant albeit rapidly decreasing – at annual deforestation rates of 1 percent,

the country has lost 15 percent of its forest since 1990. Production plantations (mostly

softwoods, including pine) constitute less than 1 percent of the forest cover but

nevertheless provide a good source of industrial roundwood. Most of the wood removals,

however, are related to fuel wood consumption of the population: 90 percent of the 28

million cubic meters of wood removed from Tanzanian forests in 2005 were for fuel

wood.87

86

National Bureau of Statistics, Tanzania 87

Rainforests Mongabay.

196

According to local experts, even though precise figures are not known, the bulk of

industrial roundwood consumption of softwoods is destined for the construction industry.

The furniture sector consumes very limited quantities of mostly hard industrial

roundwood. Softwood applications for joinery (doors, windows, etc), seats (chairs) or

furniture are not popular among Tanzanian consumers – most wood-based products

manufactured in Tanzania are from hardwoods.

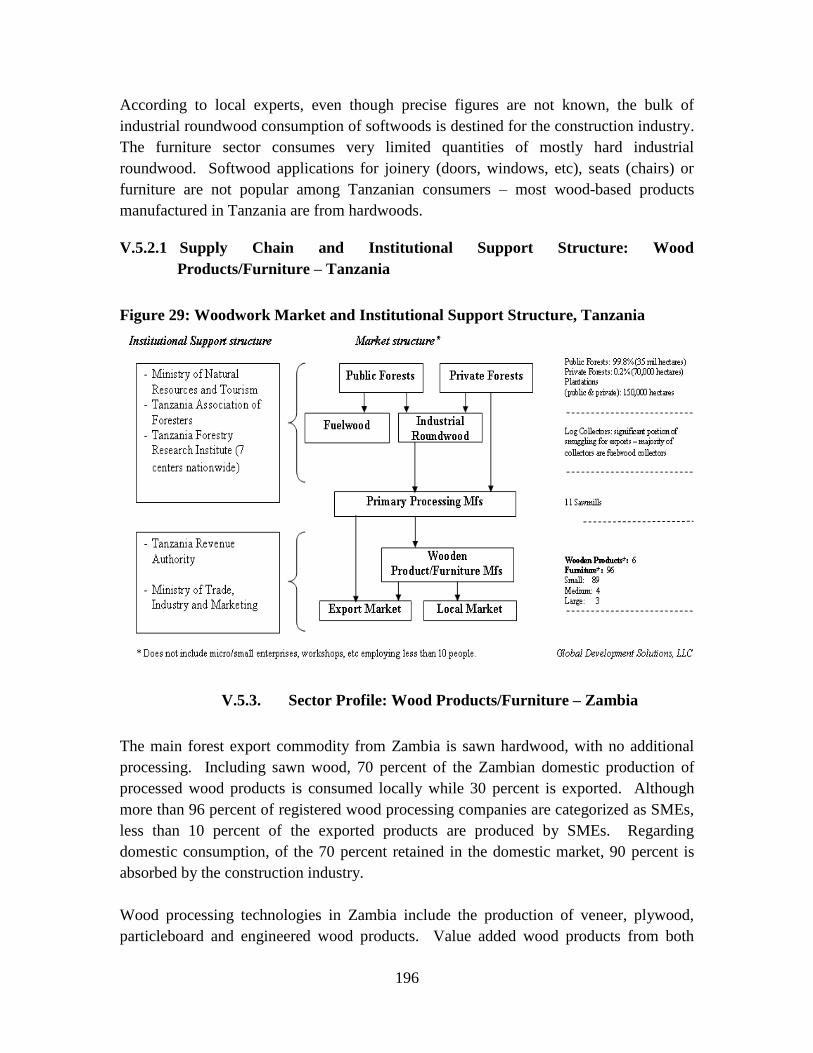

V.5.2.1 Supply Chain and Institutional Support Structure: Wood

Products/Furniture – Tanzania

Figure 29: Woodwork Market and Institutional Support Structure, Tanzania

V.5.3. Sector Profile: Wood Products/Furniture – Zambia

The main forest export commodity from Zambia is sawn hardwood, with no additional

processing. Including sawn wood, 70 percent of the Zambian domestic production of

processed wood products is consumed locally while 30 percent is exported. Although

more than 96 percent of registered wood processing companies are categorized as SMEs,

less than 10 percent of the exported products are produced by SMEs. Regarding

domestic consumption, of the 70 percent retained in the domestic market, 90 percent is

absorbed by the construction industry.

Wood processing technologies in Zambia include the production of veneer, plywood,

particleboard and engineered wood products. Value added wood products from both

197

softwood and hardwoods are produced within Zambia. However, the wood processing

industry overall is typified by small and informal companies (more than 3,000 informal

companies, 588 SMEs and only 22 large firms).

Table 102: Company and Employment Statistics for Zambian Wood Processing Sector

All Wood Processing

Firms (Incl. sawmills,

furniture, joinery, etc)

% of

Companies

by Size

% of Wooden

Furniture (Doors/

Chairs) Manufacturers

Wooden Furniture

(Doors/ Chairs)

Manufacturers

Company Size

Small 322 56% 50.0% 166

Medium 236 41% 9.0% 20

Large 22 4% 45.0% 7

Subtotal 580 100% 193

Informal > 3,000

Formal 580

State-owned enterprise 1 1 1

Est. no. workers employed in the sector 47,500

% Male 98%

% Female 2% Source: Zambia Forestry and Forest Industrial Corporation (ZAFFICO)

Table 103 below shows the exports and imports in Zambia‘s wood furniture sector for the

three years from 2008 to 2010. Note that furniture exports have declined rapidly (88

percent) in the three year span from 2008 – 2010. By 2010, furniture imports outweighed

exports by more than a factor of 400 times. Factors contributing to the uncompetitive

nature of the sector are indicated in the bulleted list below.

The Democratic Republic of Congo (DRC) accounts for 89 percent of Zambian wood

furniture exports. Although insignificant compared to the DRC, other export destinations

for Zambian wood furniture include Burundi, Botswana, South Africa and Uganda.

Table 103: Zambia Wood Furniture Imports and Exports, 2008 - 2010

Import Export

2010 6,199,422$ 14,102$

2009 4,205,011$ 63,769$

2008 5,999,914$ 112,948$

Wood furniture

Source: UN COMTRADE

The main sources of wood furniture imports into Zambia are South Africa (46 percent),

China (18.2 percent) and Malaysia (10.2 percent) with various other countries comprising

the balance.

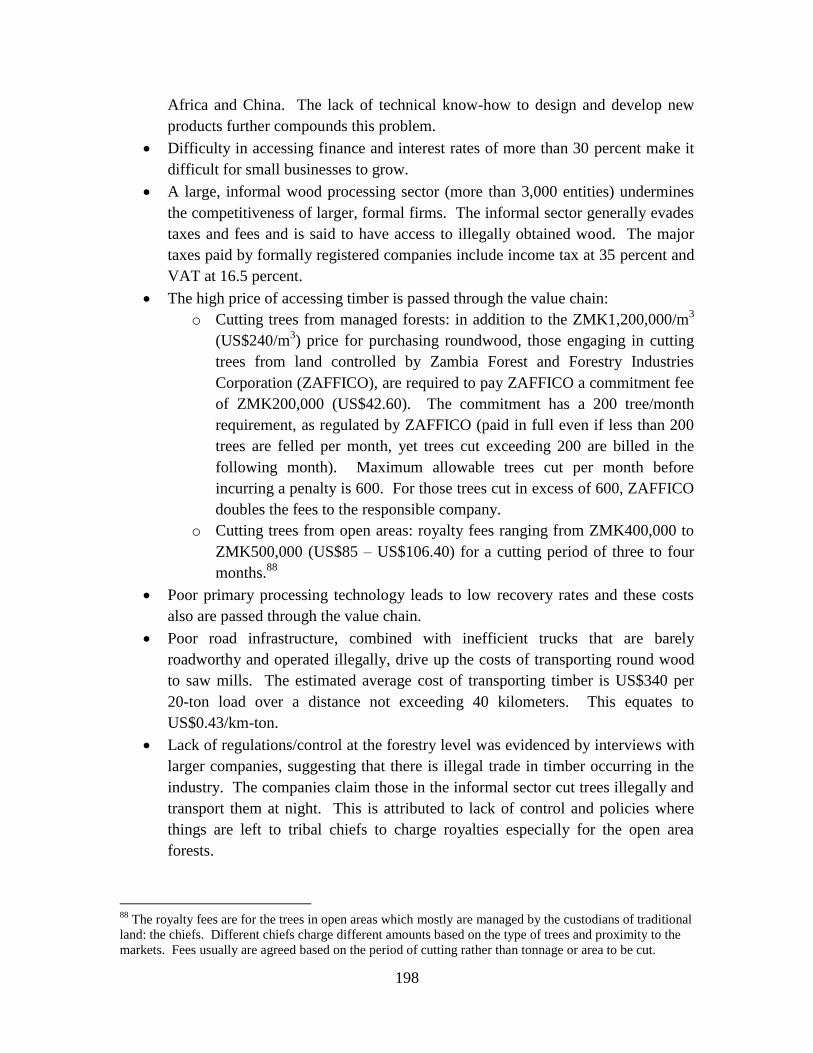

The major issues in the wood processing industry are:

Low level of technology and know-how leading to high production cost thus

making it difficult to compete against imported products, especially from South

198

Africa and China. The lack of technical know-how to design and develop new

products further compounds this problem.

Difficulty in accessing finance and interest rates of more than 30 percent make it

difficult for small businesses to grow.

A large, informal wood processing sector (more than 3,000 entities) undermines

the competitiveness of larger, formal firms. The informal sector generally evades

taxes and fees and is said to have access to illegally obtained wood. The major

taxes paid by formally registered companies include income tax at 35 percent and

VAT at 16.5 percent.

The high price of accessing timber is passed through the value chain:

o Cutting trees from managed forests: in addition to the ZMK1,200,000/m3

(US$240/m3) price for purchasing roundwood, those engaging in cutting

trees from land controlled by Zambia Forest and Forestry Industries

Corporation (ZAFFICO), are required to pay ZAFFICO a commitment fee

of ZMK200,000 (US$42.60). The commitment has a 200 tree/month

requirement, as regulated by ZAFFICO (paid in full even if less than 200

trees are felled per month, yet trees cut exceeding 200 are billed in the

following month). Maximum allowable trees cut per month before

incurring a penalty is 600. For those trees cut in excess of 600, ZAFFICO

doubles the fees to the responsible company.

o Cutting trees from open areas: royalty fees ranging from ZMK400,000 to

ZMK500,000 (US$85 – US$106.40) for a cutting period of three to four

months.88

Poor primary processing technology leads to low recovery rates and these costs

also are passed through the value chain.

Poor road infrastructure, combined with inefficient trucks that are barely

roadworthy and operated illegally, drive up the costs of transporting round wood

to saw mills. The estimated average cost of transporting timber is US$340 per

20-ton load over a distance not exceeding 40 kilometers. This equates to

US$0.43/km-ton.

Lack of regulations/control at the forestry level was evidenced by interviews with

larger companies, suggesting that there is illegal trade in timber occurring in the

industry. The companies claim those in the informal sector cut trees illegally and

transport them at night. This is attributed to lack of control and policies where

things are left to tribal chiefs to charge royalties especially for the open area

forests.

88

The royalty fees are for the trees in open areas which mostly are managed by the custodians of traditional

land: the chiefs. Different chiefs charge different amounts based on the type of trees and proximity to the

markets. Fees usually are agreed based on the period of cutting rather than tonnage or area to be cut.

199

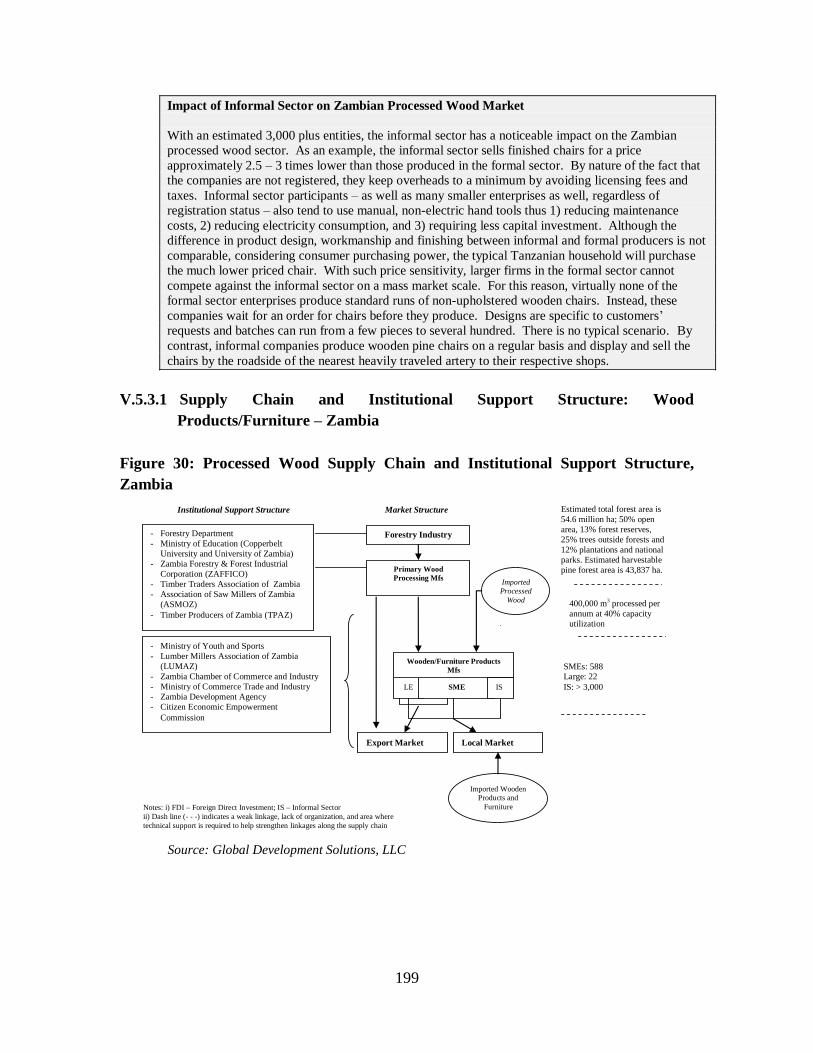

Impact of Informal Sector on Zambian Processed Wood Market

With an estimated 3,000 plus entities, the informal sector has a noticeable impact on the Zambian

processed wood sector. As an example, the informal sector sells finished chairs for a price

approximately 2.5 – 3 times lower than those produced in the formal sector. By nature of the fact that

the companies are not registered, they keep overheads to a minimum by avoiding licensing fees and

taxes. Informal sector participants – as well as many smaller enterprises as well, regardless of

registration status – also tend to use manual, non-electric hand tools thus 1) reducing maintenance

costs, 2) reducing electricity consumption, and 3) requiring less capital investment. Although the

difference in product design, workmanship and finishing between informal and formal producers is not

comparable, considering consumer purchasing power, the typical Tanzanian household will purchase

the much lower priced chair. With such price sensitivity, larger firms in the formal sector cannot

compete against the informal sector on a mass market scale. For this reason, virtually none of the

formal sector enterprises produce standard runs of non-upholstered wooden chairs. Instead, these

companies wait for an order for chairs before they produce. Designs are specific to customers‘

requests and batches can run from a few pieces to several hundred. There is no typical scenario. By

contrast, informal companies produce wooden pine chairs on a regular basis and display and sell the

chairs by the roadside of the nearest heavily traveled artery to their respective shops.

V.5.3.1 Supply Chain and Institutional Support Structure: Wood

Products/Furniture – Zambia

Figure 30: Processed Wood Supply Chain and Institutional Support Structure,

Zambia

- Forestry Department

- Ministry of Education (Copperbelt

University and University of Zambia)

- Zambia Forestry & Forest Industrial

Corporation (ZAFFICO)

- Timber Traders Association of Zambia

- Association of Saw Millers of Zambia

(ASMOZ)

- Timber Producers of Zambia (TPAZ)

- Ministry of Youth and Sports

- Lumber Millers Association of Zambia

(LUMAZ)

- Zambia Chamber of Commerce and Industry

- Ministry of Commerce Trade and Industry

- Zambia Development Agency

- Citizen Economic Empowerment

Commission

Institutional Support Structure Estimated total forest area is

54.6 million ha; 50% open

area, 13% forest reserves,

25% trees outside forests and

12% plantations and national

parks. Estimated harvestable

pine forest area is 43,837 ha.

Market Structure

Forestry Industry

Primary Wood

Processing Mfs

400,000 m3 processed per

annum at 40% capacity

utilization

Export Market Local Market

LE SME

Wooden/Furniture Products

Mfs

IS

Imported

Processed

Wood

SMEs: 588 Large: 22

IS: > 3,000

Imported Wooden

Products and

Furniture Notes: i) FDI – Foreign Direct Investment; IS – Informal Sector

ii) Dash line (- - -) indicates a weak linkage, lack of organization, and area where

technical support is required to help strengthen linkages along the supply chain

Source: Global Development Solutions, LLC

200

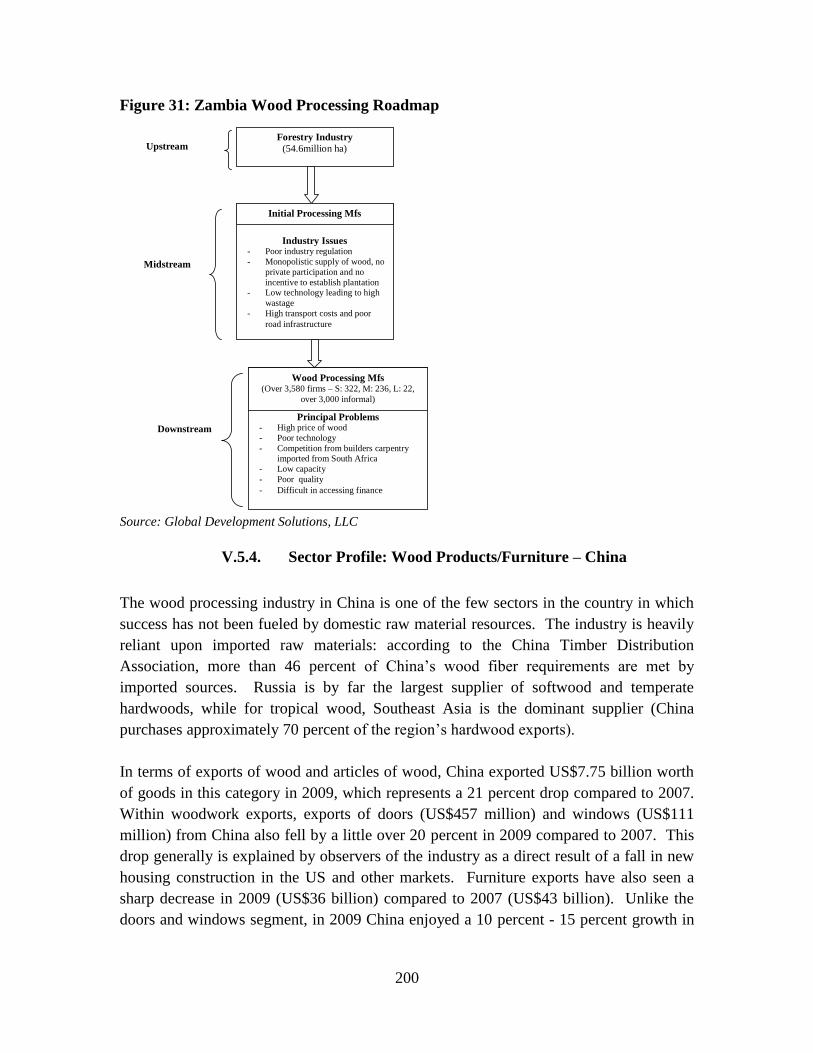

Figure 31: Zambia Wood Processing Roadmap

Forestry Industry

(54.6million ha)

Upstream

Industry Issues

- Poor industry regulation

- Monopolistic supply of wood, no

private participation and no

incentive to establish plantation - Low technology leading to high

wastage

- High transport costs and poor

road infrastructure

Initial Processing Mfs

Midstream

Industry Issues

Principal Problems - High price of wood

- Poor technology

- Competition from builders carpentry imported from South Africa

- Low capacity

- Poor quality

- Difficult in accessing finance

Wood Processing Mfs (Over 3,580 firms – S: 322, M: 236, L: 22,

over 3,000 informal)

Downstream

Source: Global Development Solutions, LLC

V.5.4. Sector Profile: Wood Products/Furniture – China

The wood processing industry in China is one of the few sectors in the country in which

success has not been fueled by domestic raw material resources. The industry is heavily

reliant upon imported raw materials: according to the China Timber Distribution

Association, more than 46 percent of China‘s wood fiber requirements are met by

imported sources. Russia is by far the largest supplier of softwood and temperate

hardwoods, while for tropical wood, Southeast Asia is the dominant supplier (China

purchases approximately 70 percent of the region‘s hardwood exports).

In terms of exports of wood and articles of wood, China exported US$7.75 billion worth

of goods in this category in 2009, which represents a 21 percent drop compared to 2007.

Within woodwork exports, exports of doors (US$457 million) and windows (US$111

million) from China also fell by a little over 20 percent in 2009 compared to 2007. This

drop generally is explained by observers of the industry as a direct result of a fall in new

housing construction in the US and other markets. Furniture exports have also seen a

sharp decrease in 2009 (US$36 billion) compared to 2007 (US$43 billion). Unlike the

doors and windows segment, in 2009 China enjoyed a 10 percent - 15 percent growth in

201

exports of chairs (US$4.45 billion) and bedroom, kitchen and office wooden furniture

(US$7.59 billion).

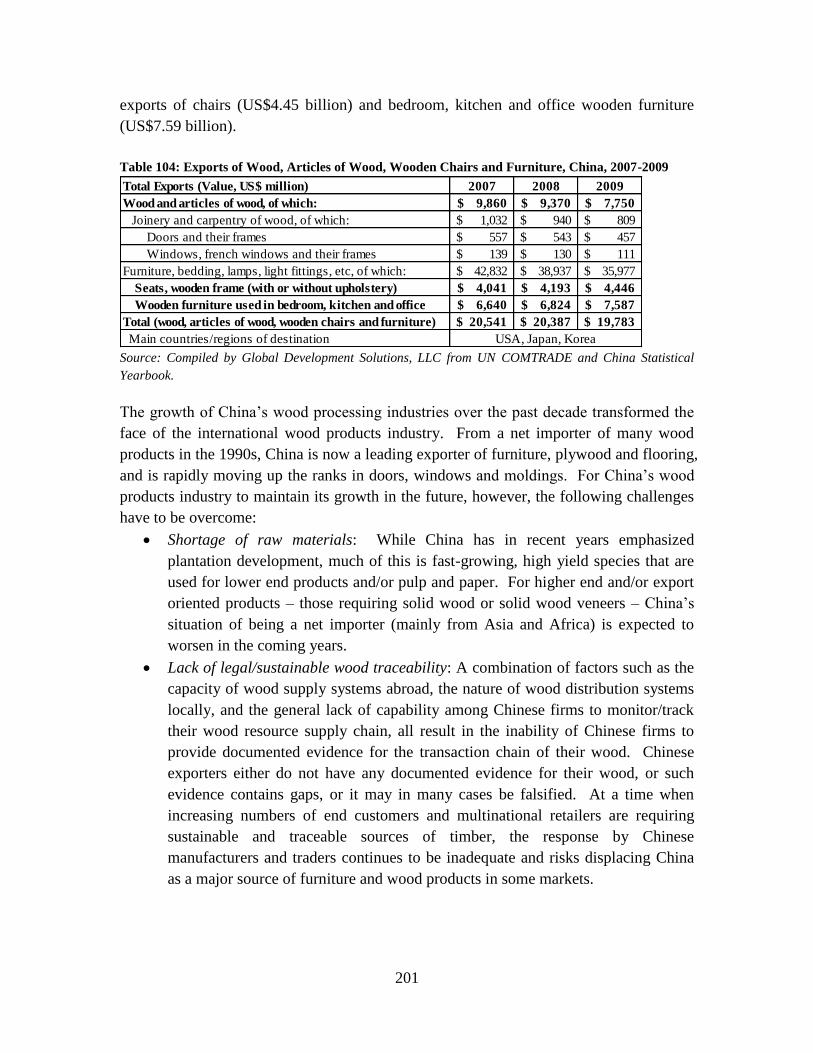

Table 104: Exports of Wood, Articles of Wood, Wooden Chairs and Furniture, China, 2007-2009

Total Exports (Value, US$ million) 2007 2008 2009

Wood and articles of wood, of which: 9,860$ 9,370$ 7,750$

Joinery and carpentry of wood, of which: 1,032$ 940$ 809$

Doors and their frames 557$ 543$ 457$

Windows, french windows and their frames 139$ 130$ 111$

Furniture, bedding, lamps, light fittings, etc, of which: 42,832$ 38,937$ 35,977$

Seats, wooden frame (with or without upholstery) 4,041$ 4,193$ 4,446$

Wooden furniture used in bedroom, kitchen and office 6,640$ 6,824$ 7,587$

Total (wood, articles of wood, wooden chairs and furniture) 20,541$ 20,387$ 19,783$

Main countries/regions of destination USA, Japan, Korea Source: Compiled by Global Development Solutions, LLC from UN COMTRADE and China Statistical

Yearbook.

The growth of China‘s wood processing industries over the past decade transformed the

face of the international wood products industry. From a net importer of many wood

products in the 1990s, China is now a leading exporter of furniture, plywood and flooring,

and is rapidly moving up the ranks in doors, windows and moldings. For China‘s wood

products industry to maintain its growth in the future, however, the following challenges

have to be overcome:

Shortage of raw materials: While China has in recent years emphasized

plantation development, much of this is fast-growing, high yield species that are

used for lower end products and/or pulp and paper. For higher end and/or export

oriented products – those requiring solid wood or solid wood veneers – China‘s

situation of being a net importer (mainly from Asia and Africa) is expected to

worsen in the coming years.

Lack of legal/sustainable wood traceability: A combination of factors such as the

capacity of wood supply systems abroad, the nature of wood distribution systems

locally, and the general lack of capability among Chinese firms to monitor/track

their wood resource supply chain, all result in the inability of Chinese firms to

provide documented evidence for the transaction chain of their wood. Chinese

exporters either do not have any documented evidence for their wood, or such

evidence contains gaps, or it may in many cases be falsified. At a time when

increasing numbers of end customers and multinational retailers are requiring

sustainable and traceable sources of timber, the response by Chinese

manufacturers and traders continues to be inadequate and risks displacing China

as a major source of furniture and wood products in some markets.

202

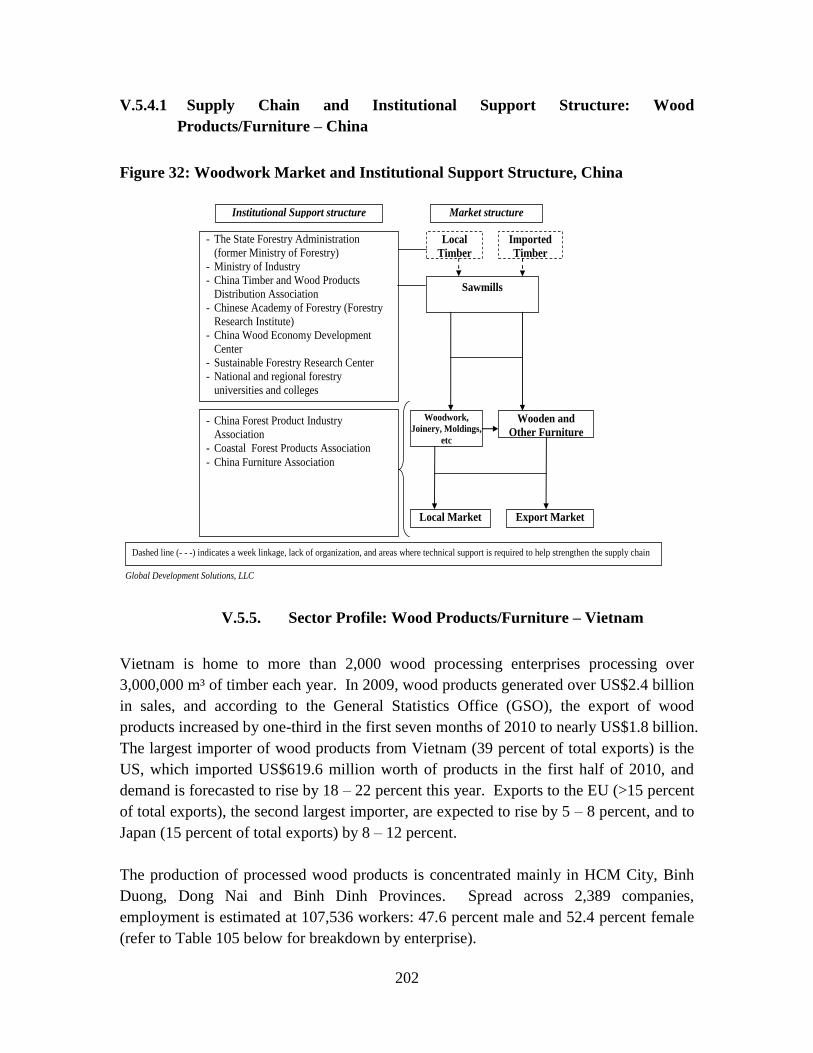

V.5.4.1 Supply Chain and Institutional Support Structure: Wood

Products/Furniture – China

Figure 32: Woodwork Market and Institutional Support Structure, China

Woodwork Market and Institutional Support Structure, China

Market structure Institutional Support structure

- The State Forestry Administration

(former Ministry of Forestry)

- Ministry of Industry

- China Timber and Wood Products

Distribution Association

- Chinese Academy of Forestry (Forestry

Research Institute)

- China Wood Economy Development

Center

- Sustainable Forestry Research Center

- National and regional forestry

universities and colleges

- China Forest Product Industry

Association

- Coastal Forest Products Association

- China Furniture Association

Dashed line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required to help strengthen the supply chain

Local

Timber

Sawmills

Woodwork,

Joinery, Moldings,

etc

Wooden and

Other Furniture

Local Market Export Market

Imported

Timber

Global Development Solutions, LLC

V.5.5. Sector Profile: Wood Products/Furniture – Vietnam

Vietnam is home to more than 2,000 wood processing enterprises processing over

3,000,000 m³ of timber each year. In 2009, wood products generated over US$2.4 billion

in sales, and according to the General Statistics Office (GSO), the export of wood

products increased by one-third in the first seven months of 2010 to nearly US$1.8 billion.

The largest importer of wood products from Vietnam (39 percent of total exports) is the

US, which imported US$619.6 million worth of products in the first half of 2010, and

demand is forecasted to rise by 18 – 22 percent this year. Exports to the EU (>15 percent

of total exports), the second largest importer, are expected to rise by 5 – 8 percent, and to

Japan (15 percent of total exports) by 8 – 12 percent.

The production of processed wood products is concentrated mainly in HCM City, Binh

Duong, Dong Nai and Binh Dinh Provinces. Spread across 2,389 companies,

employment is estimated at 107,536 workers: 47.6 percent male and 52.4 percent female

(refer to Table 105 below for breakdown by enterprise).

203

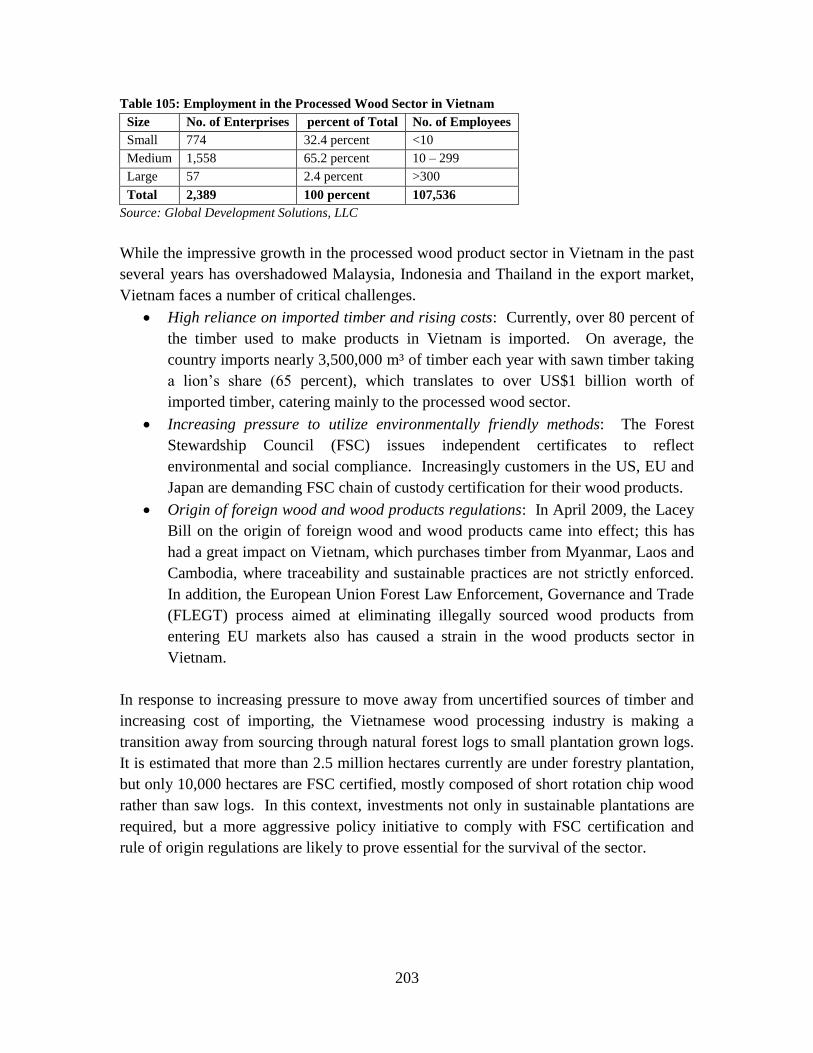

Table 105: Employment in the Processed Wood Sector in Vietnam

Size No. of Enterprises percent of Total No. of Employees

Small 774 32.4 percent <10

Medium 1,558 65.2 percent 10 – 299

Large 57 2.4 percent >300

Total 2,389 100 percent 107,536

Source: Global Development Solutions, LLC

While the impressive growth in the processed wood product sector in Vietnam in the past

several years has overshadowed Malaysia, Indonesia and Thailand in the export market,

Vietnam faces a number of critical challenges.

High reliance on imported timber and rising costs: Currently, over 80 percent of

the timber used to make products in Vietnam is imported. On average, the

country imports nearly 3,500,000 m³ of timber each year with sawn timber taking

a lion‘s share (65 percent), which translates to over US$1 billion worth of

imported timber, catering mainly to the processed wood sector.

Increasing pressure to utilize environmentally friendly methods: The Forest

Stewardship Council (FSC) issues independent certificates to reflect

environmental and social compliance. Increasingly customers in the US, EU and

Japan are demanding FSC chain of custody certification for their wood products.

Origin of foreign wood and wood products regulations: In April 2009, the Lacey

Bill on the origin of foreign wood and wood products came into effect; this has

had a great impact on Vietnam, which purchases timber from Myanmar, Laos and

Cambodia, where traceability and sustainable practices are not strictly enforced.

In addition, the European Union Forest Law Enforcement, Governance and Trade

(FLEGT) process aimed at eliminating illegally sourced wood products from

entering EU markets also has caused a strain in the wood products sector in

Vietnam.

In response to increasing pressure to move away from uncertified sources of timber and

increasing cost of importing, the Vietnamese wood processing industry is making a

transition away from sourcing through natural forest logs to small plantation grown logs.

It is estimated that more than 2.5 million hectares currently are under forestry plantation,

but only 10,000 hectares are FSC certified, mostly composed of short rotation chip wood

rather than saw logs. In this context, investments not only in sustainable plantations are

required, but a more aggressive policy initiative to comply with FSC certification and

rule of origin regulations are likely to prove essential for the survival of the sector.

204

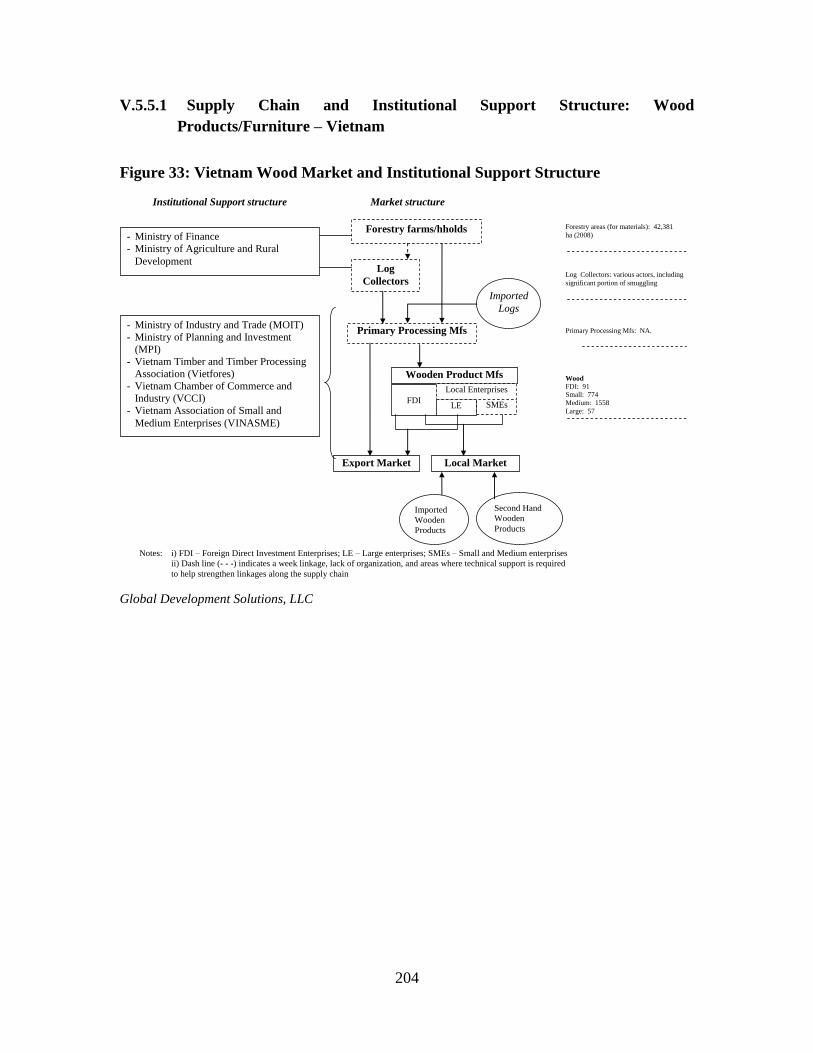

V.5.5.1 Supply Chain and Institutional Support Structure: Wood

Products/Furniture – Vietnam

Figure 33: Vietnam Wood Market and Institutional Support Structure Vietnam Wood Market and Institutional Support Structure

Market structure Institutional Support structure

Forestry farms/hholds - Ministry of Finance

- Ministry of Agriculture and Rural

Development Log

Collectors

Primary Processing Mfs

Imported

Logs

Wooden Product Mfs

FDI LE SMEs

Export Market Local Market

- Ministry of Industry and Trade (MOIT)

- Ministry of Planning and Investment

(MPI)

- Vietnam Timber and Timber Processing

Association (Vietfores)

- Vietnam Chamber of Commerce and

Industry (VCCI)

- Vietnam Association of Small and

Medium Enterprises (VINASME)

Notes: i) FDI – Foreign Direct Investment Enterprises; LE – Large enterprises; SMEs – Small and Medium enterprises

ii) Dash line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required

to help strengthen linkages along the supply chain

Second Hand

Wooden

Products

Imported

Wooden

Products

Local Enterprises

Forestry areas (for materials): 42,381

ha (2008)

Log Collectors: various actors, including

significant portion of smuggling

Primary Processing Mfs: NA.

Wood

FDI: 91 Small: 774

Medium: 1558

Large: 57

Global Development Solutions, LLC

205

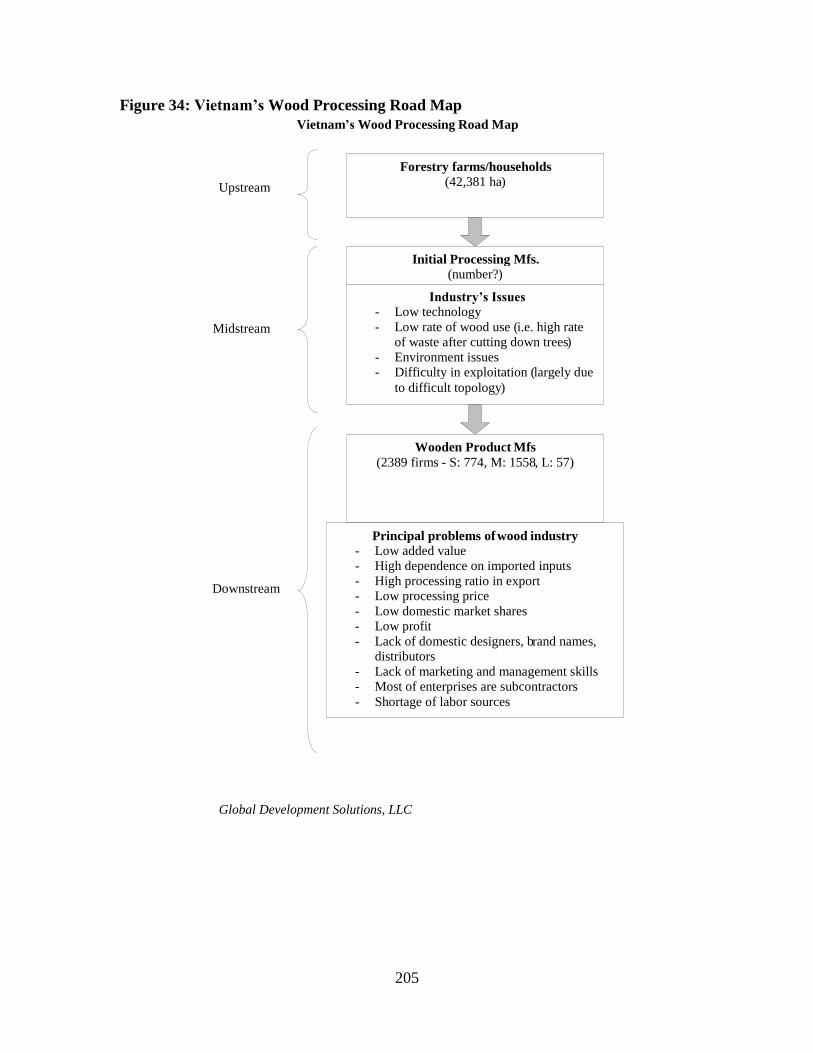

Figure 34: Vietnam’s Wood Processing Road Map

Global Development Solutions, LLC

Vietnam ’s W ood Processing Road Map

Forestry farms/households (42,381 ha )

I nitial Processing Mfs. ( number? )

Industry’s Issues - Low technology - Low rate of wood use ( i.e. high rate

of waste after cutting down trees ) - Environment issues - Difficulty in exploitation ( largely due

to difficult topology )

Wooden Product Mfs (2389 firms - S: 774, M: 1558 , L: 57 )

Upstream

Downstream

Principal problems of wood industry - Low added value - High dependence on imported inputs - High processing ratio in export - Low processing price - Low domestic market shares - L ow pr of it - Lack of domestic designers, b rand names,

distributors - Lack of marketing and management skills - Most of enterprises are subcontractors - Shortage of labor sources

Midstream

206

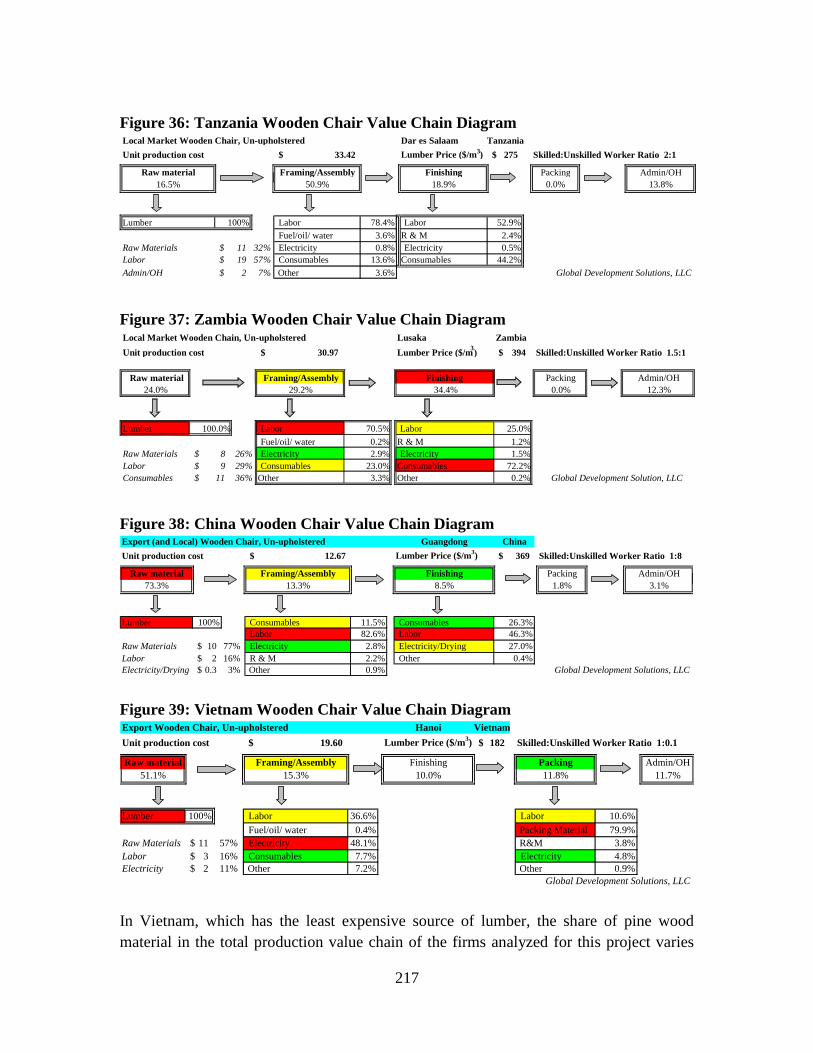

V.6. Economic Efficiency and Competitiveness of Wood Products/Furniture –

Chairs

V.6.1. Ethiopia: Wood Chairs

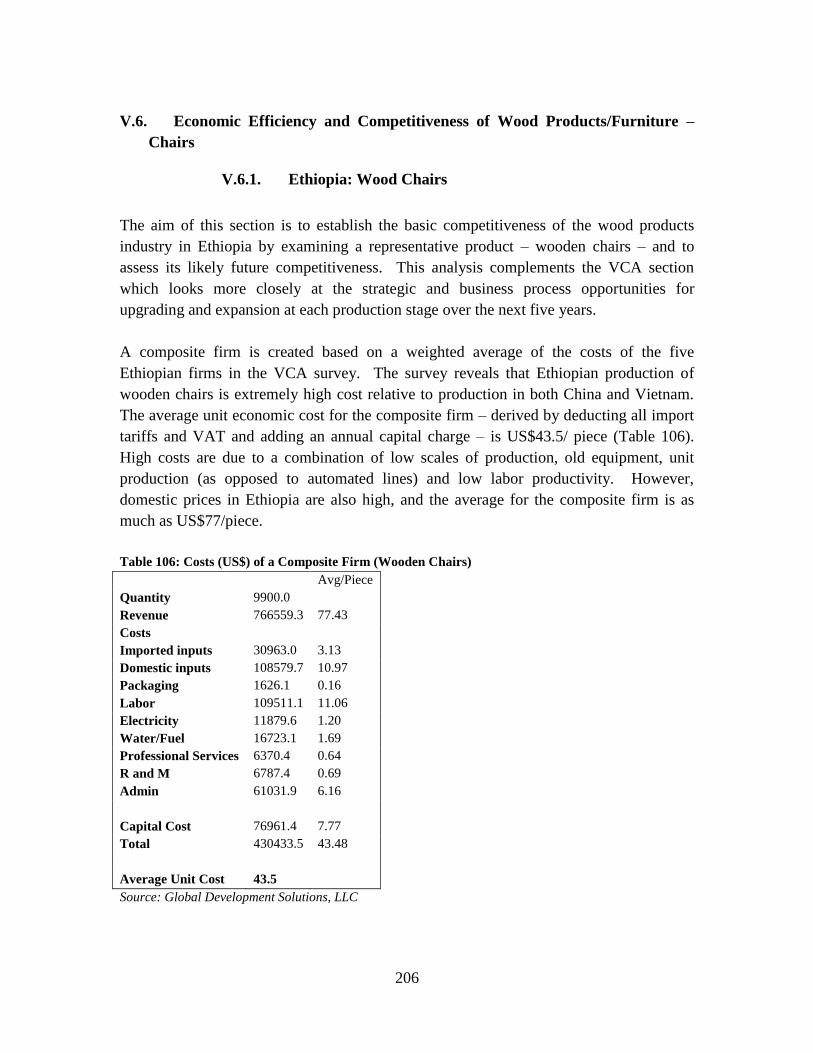

The aim of this section is to establish the basic competitiveness of the wood products

industry in Ethiopia by examining a representative product – wooden chairs – and to

assess its likely future competitiveness. This analysis complements the VCA section

which looks more closely at the strategic and business process opportunities for

upgrading and expansion at each production stage over the next five years.

A composite firm is created based on a weighted average of the costs of the five

Ethiopian firms in the VCA survey. The survey reveals that Ethiopian production of

wooden chairs is extremely high cost relative to production in both China and Vietnam.

The average unit economic cost for the composite firm – derived by deducting all import

tariffs and VAT and adding an annual capital charge – is US$43.5/ piece (Table 106).

High costs are due to a combination of low scales of production, old equipment, unit

production (as opposed to automated lines) and low labor productivity. However,

domestic prices in Ethiopia are also high, and the average for the composite firm is as

much as US$77/piece.

Table 106: Costs (US$) of a Composite Firm (Wooden Chairs)

Avg/Piece

Quantity 9900.0

Revenue 766559.3 77.43

Costs

Imported inputs 30963.0 3.13

Domestic inputs 108579.7 10.97

Packaging 1626.1 0.16

Labor 109511.1 11.06

Electricity 11879.6 1.20

Water/Fuel 16723.1 1.69

Professional Services 6370.4 0.64

R and M 6787.4 0.69

Admin 61031.9 6.16

Capital Cost 76961.4 7.77

Total 430433.5 43.48

Average Unit Cost 43.5

Source: Global Development Solutions, LLC

207

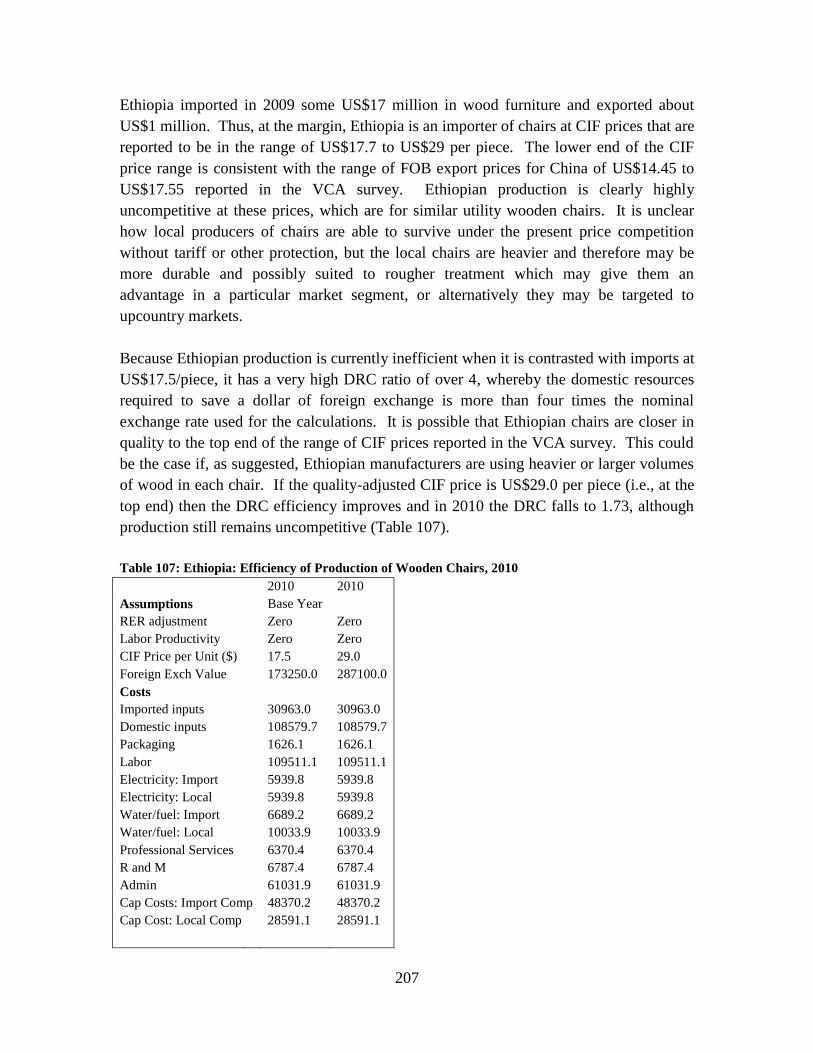

Ethiopia imported in 2009 some US$17 million in wood furniture and exported about

US$1 million. Thus, at the margin, Ethiopia is an importer of chairs at CIF prices that are

reported to be in the range of US$17.7 to US$29 per piece. The lower end of the CIF

price range is consistent with the range of FOB export prices for China of US$14.45 to

US$17.55 reported in the VCA survey. Ethiopian production is clearly highly

uncompetitive at these prices, which are for similar utility wooden chairs. It is unclear

how local producers of chairs are able to survive under the present price competition

without tariff or other protection, but the local chairs are heavier and therefore may be

more durable and possibly suited to rougher treatment which may give them an

advantage in a particular market segment, or alternatively they may be targeted to

upcountry markets.

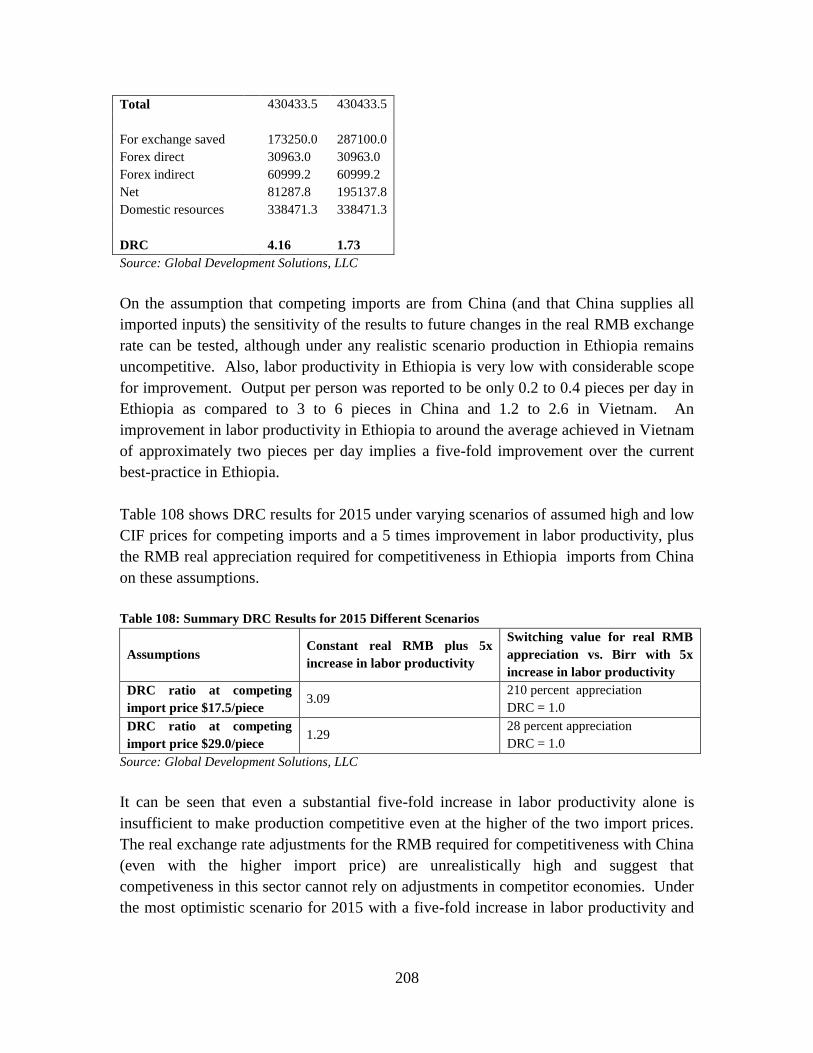

Because Ethiopian production is currently inefficient when it is contrasted with imports at

US$17.5/piece, it has a very high DRC ratio of over 4, whereby the domestic resources

required to save a dollar of foreign exchange is more than four times the nominal

exchange rate used for the calculations. It is possible that Ethiopian chairs are closer in

quality to the top end of the range of CIF prices reported in the VCA survey. This could

be the case if, as suggested, Ethiopian manufacturers are using heavier or larger volumes

of wood in each chair. If the quality-adjusted CIF price is US$29.0 per piece (i.e., at the

top end) then the DRC efficiency improves and in 2010 the DRC falls to 1.73, although

production still remains uncompetitive (Table 107).

Table 107: Ethiopia: Efficiency of Production of Wooden Chairs, 2010

2010 2010

Assumptions Base Year

RER adjustment Zero Zero

Labor Productivity Zero Zero

CIF Price per Unit ($) 17.5 29.0

Foreign Exch Value 173250.0 287100.0

Costs

Imported inputs 30963.0 30963.0

Domestic inputs 108579.7 108579.7

Packaging 1626.1 1626.1

Labor 109511.1 109511.1

Electricity: Import 5939.8 5939.8

Electricity: Local 5939.8 5939.8

Water/fuel: Import 6689.2 6689.2

Water/fuel: Local 10033.9 10033.9

Professional Services 6370.4 6370.4

R and M 6787.4 6787.4

Admin 61031.9 61031.9

Cap Costs: Import Comp 48370.2 48370.2

Cap Cost: Local Comp 28591.1 28591.1

208

Total 430433.5 430433.5

For exchange saved 173250.0 287100.0

Forex direct 30963.0 30963.0

Forex indirect 60999.2 60999.2

Net 81287.8 195137.8

Domestic resources 338471.3 338471.3

DRC 4.16 1.73

Source: Global Development Solutions, LLC

On the assumption that competing imports are from China (and that China supplies all

imported inputs) the sensitivity of the results to future changes in the real RMB exchange

rate can be tested, although under any realistic scenario production in Ethiopia remains