Embed Size (px)

Citation preview

COMPANION TO THE DRAFT FOREST SECTOR TRANSFORMATION CHARTER

FIRST DRAFT FOR PRESENTATION TO STAKEHOLDERS

MAY 2007

Prepared by the Charter Steering Committee

Launched for public comment at the Forest Sector BBBEEE Indaba held on

25 June 2007

�

Table of ContentsAcronyms 2

1 Chronology of the Development of the Forest Sector Transformation Charter 3

2 Profile of the Forest Sector 6

3 Current State of Empowerment in the Sector 9

�.1 EquityOwnership 9�.2 ManagementControlandEmploymentEquity 10�.� OtherKeyElements 10�.4 Conclusions 11

4 Sector Challenges 12

4.1 Increaseroundwoodsupply 124.2 Sustainablesupplyandbetterutilisationofsawlogs 1�4.3 Localbeneficiationinandthroughthefibreproductionsub-sector 134.4 Equityintheforestryvaluechain 1�4.5 Empowermentandsustainabilityofsmallforestsectorenterprises 144.6 Linkingforestrywithpovertyalleviationandlocaleconomicdevelopment 15

5 Details on Undertakings in the Charter 16

5.1 Streamlineandexpediteafforestationlicensingprocedures 16

5.2 SawloggrowingstrategyandprogrammeforSouthAfrica 17

5.� Forestprotectionservices 18

5.4 CharterCouncil 19

6 Explanatory notes to the Charter 22

6.1 CalculationofoverallOwnershipProfilefortheSector 22

6.2 ComparisonbetweenScorecardfortheForestSectorandtheGenericScorecard 2�

6.� FurtherdetailsonSkillsDevelopmentStrategy/Plan 25

6.4 FurtherdetailsonIndustryCodesofConductonContractingandEmployment 27

6.5 Motivationtofundand/orsubsidisetheinterestburdentodevelopemergingforestry

enterprises ��

6.6 Motivationforseedfundingtodevelopfireinsuranceschemesforemergingforestry

enterprises �6

7 Financial requirements for Forest Sector Transformation 36

7.1 IndustryCosts �6

7.2 GovernmentCosts 40

8 Key Outcomes of the Forest Sector Transformation Process 44

9 Charter Implementation Plan 45

Appendix: Forestry Funding models

4

Acronyms

ABET AdultBasicEducationandTraining

ASGI-SAAcceleratedandSharedGrowthInitiativeforSouthAfrica

B-BBEE Broad-basedBlackEconomicEmpowerment

BEE Broad-basedBlackEconomicEmpowerment

CEPPWAWU Chemical,Energy,Paper,Printing,WoodandAlliedWorkers’Union

CRLR CommissiononRestitutionofLandRights

DEAT DepartmentofEnvironmentalAffairsandTourism

DoA DepartmentofAgriculture

DLA DepartmentofLandAffairs

DoL DepartmentofLabour

DPLG DepartmentofProvincialandLocalGovernment

DoT DepartmentofTransport

DTI DepartmentofTradeandIndustry

DWAF DepartmentofWaterAffairsandForestry

EAP EconomicallyActivePopulation

ESMEs ExemptedMicro-Enterprises

FAWU FoodandAlliedWorkers’Union

FIETA ForestIndustryEducationandTrainingAuthority

GDP GrossDomesticProduct

IDC IndustrialDevelopmentCorporation

ITAC InternationalTradeAdministrationCommission

MOU MemorandumofUnderstanding

NSF NationalSkillsFund

NPAT NetProfitafterTax

NSF NationalSkillsFund

SALGA SouthAfricanLocalGovernmentAssociation

OSHA OccupationalSafetyandHealthAct

PGDS ProvincialGrowthandDevelopmentStrategy

QSE’s QualifyingSmallEnterprises

SAFCOL SouthAfricanForestryCompanyLtd

SALGA SouthAfricanLocalGovernmentAssociation

SANAS SouthAfricanNationalAccreditationSystem

SAQA SouthAfricanQualificationAuthority

SETA SectorEducationandTrainingAuthority

SFRA StreamFlowReductionActivity

SGB StandardsGeneratingBody

QSE QualifyingSmallEnterprise

WfW WorkingforWater

5

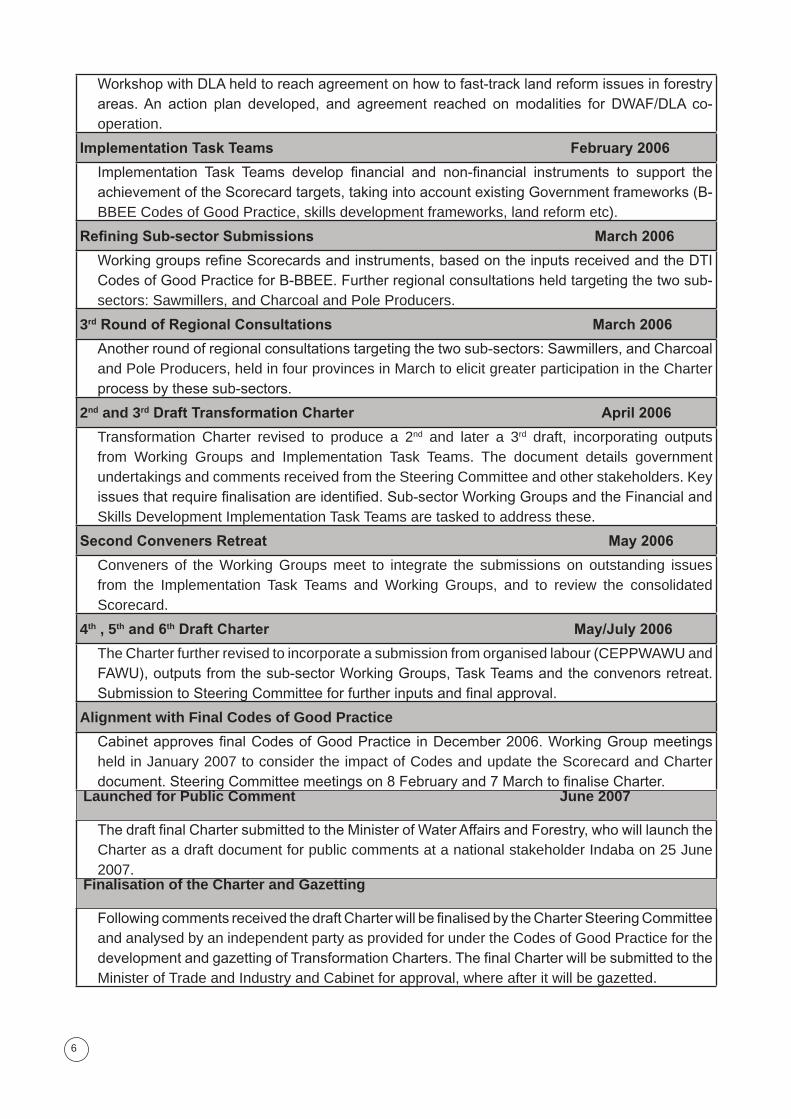

1.ChronologyoftheDevelopmentoftheForest SectorTransformationCharter

Launch 18 April 2005

Charterofficially launchedby theMinisterofWaterAffairsandForestryatan indabaheld inMidrand.StakeholderspresentagreementtodevelopaB-BBEECharter,andestablishaCharterSteering Committee assisted by Working Groups to drive the process.The Minister acceptsnominationsandappointstheSteeringCommittee.

Working Groups 1st Tasks June/November 2005

Four sub-sector Working Groups established: Growers, Forestry Contractors, Sawmillers, Char-coal and Treated Pole Producers, and a group to examine the Sector delineation. Working Group tasks were to:

• DevelopaChartervisionforeachsub-sector;

• IdentifykeyprinciplestoguidetheCharter;

• Determinethecurrentstatusofempowermentineachsub-sector;and

•Determine the challenges facing each sub-sector and recommend solutions to thesechallenges.

Regional Public Consultation September 2005

ThefindingsoftheWorkingGroupspresentedatregionalpublicconsultationmeetingsinEastLondon,DurbanandNelspruit.InputsreceivedfromstakeholdersusedbytheWorkingGroupstoupdatetheirsubmissions.

Draft Charter – Preliminary Sections

WorkingGroupsubmissionsformthebasisforthedraftingofthepreliminarysectionsofthedraftCharter,withtheSteeringCommitteeplayinganoversightrole.

Working Groups 2nd Tasks October/November 2005

A5thWorkingGroup,theFibreWorkingGroup,established.TheSteeringCommitteedevelopsguidelinesfordevelopmentofScorecardsbyeachsub-sectorWorkingGroup.WorkingGrouptasksinclude:

• DevelopingScorecardsforeachsub-sector;and

• IdentifyinginstrumentsrequiredforachievingScorecardtargets.

Regional Public Consultation – 2nd Round November/December 2005

AsecondroundofregionalpublicconsultationmeetingsheldtoreviewthedraftScorecardsandinstruments. InputsreceivedusedtoupdatetheWorkingGroupsubmissions,whicharethenusedasabasisforcompilingtheremainingsectionsoftheDraftTransformationCharter.

First Conveners Retreat January 2006

Conveners of theSteeringCommittee andWorkingGroupsmeet to cross-check sub-sectorScorecardsanddevelopTORfortaskteamstoexaminecross-cuttinginstrumentstosupporttheachievementofScorecardtargets.

DWAF/DLA Workshop January 2006

6

WorkshopwithDLAheldtoreachagreementonhowtofast-tracklandreformissuesinforestryareas.An action plan developed, and agreement reached onmodalities for DWAF/DLA co-operation.

Implementation Task Teams February 2006

Implementation Task Teams develop financial and non-financial instruments to support theachievementoftheScorecardtargets,takingintoaccountexistingGovernmentframeworks(B-BBEECodesofGoodPractice,skillsdevelopmentframeworks,landreformetc).

Refining Sub-sector Submissions March 2006

WorkinggroupsrefineScorecardsandinstruments,basedontheinputsreceivedandtheDTICodesofGoodPracticeforB-BBEE.Furtherregionalconsultationsheldtargetingthetwosub-sectors:Sawmillers,andCharcoalandPoleProducers.

3rd Round of Regional Consultations March 2006

Anotherroundofregionalconsultationstargetingthetwosub-sectors:Sawmillers,andCharcoalandPoleProducers,heldinfourprovincesinMarchtoelicitgreaterparticipationintheCharterprocessbythesesub-sectors.

2nd and 3rd Draft Transformation Charter April 2006

Transformation Charter revised to produce a 2nd and later a �rd draft, incorporating outputsfrom Working Groups and Implementation Task Teams. The document details governmentundertakingsandcommentsreceivedfromtheSteeringCommitteeandotherstakeholders.Keyissuesthatrequirefinalisationareidentified.Sub-sectorWorkingGroupsandtheFinancialandSkillsDevelopmentImplementationTaskTeamsaretaskedtoaddressthese.

Second Conveners Retreat May 2006

Conveners of the Working Groups meet to integrate the submissions on outstanding issuesfrom the Implementation Task Teams and Working Groups, and to review the consolidatedScorecard.

4th , 5th and 6th Draft Charter May/July 2006

TheCharterfurtherrevisedtoincorporateasubmissionfromorganisedlabour(CEPPWAWUandFAWU),outputsfromthesub-sectorWorkingGroups,TaskTeamsandtheconvenorsretreat.SubmissiontoSteeringCommitteeforfurtherinputsandfinalapproval.

Alignment with Final Codes of Good Practice

CabinetapprovesfinalCodesofGoodPractice inDecember2006.WorkingGroupmeetingsheldinJanuary2007toconsidertheimpactofCodesandupdatetheScorecardandCharterdocument.SteeringCommitteemeetingson8Februaryand7MarchtofinaliseCharter.

Launched for Public Comment June 2007

ThedraftfinalChartersubmittedtotheMinisterofWaterAffairsandForestry,whowilllaunchtheCharterasadraftdocumentforpubliccommentsatanationalstakeholderIndabaon25June2007.

Finalisation of the Charter and Gazetting

FollowingcommentsreceivedthedraftCharterwillbefinalisedbytheCharterSteeringCommitteeandanalysedbyanindependentpartyasprovidedforundertheCodesofGoodPracticeforthedevelopmentandgazettingofTransformationCharters.ThefinalCharterwillbesubmittedtotheMinisterofTradeandIndustryandCabinetforapproval,whereafteritwillbegazetted.

7

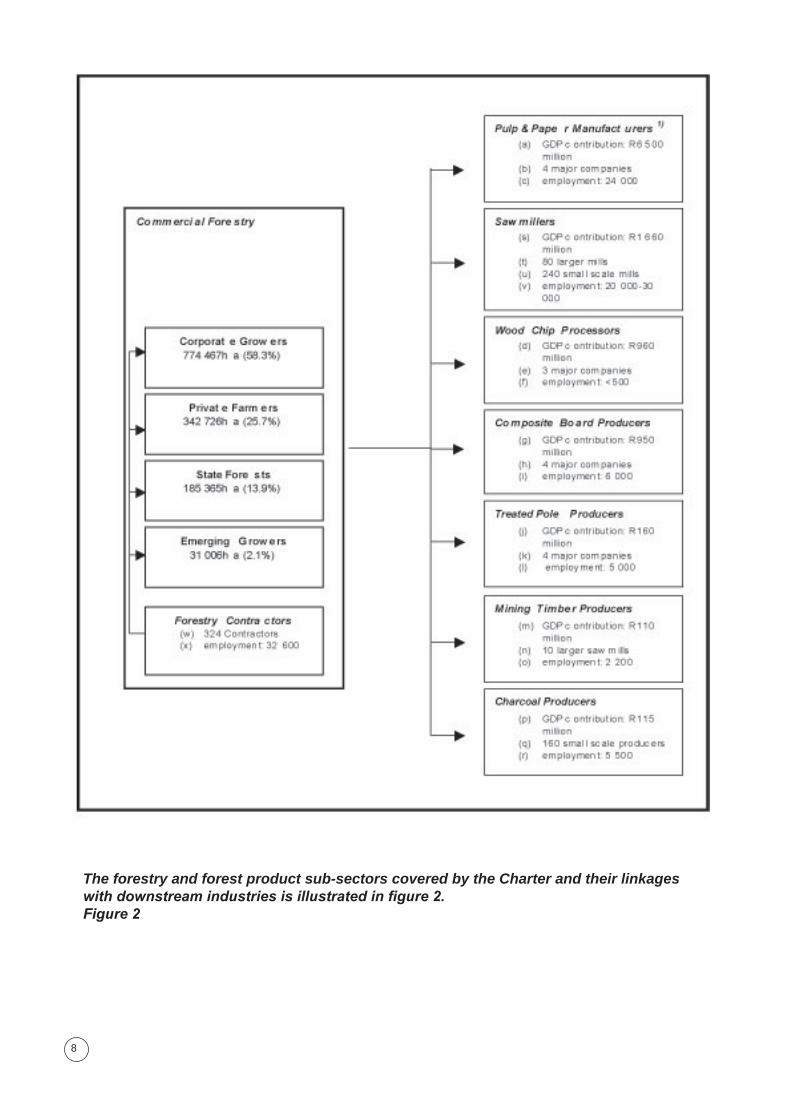

2 ProfileoftheForestSectorTheForestSectormakesamajorcontributiontotheSouthAfricaneconomy.Thecommercialplantationresourceofsome1.33millionhectaresformsthebasisforawell-developed,highlyintegratedanddiversifiedforestproductsindustryinSouthAfrica(Figure1).

Thefibresub-sectorisdominatedbyasmallnumberoflarge,corporateenterprisesthatareinvolvedinthecapital-intensivepulp,paperandcompositeboardindustries.Theseindustriesarecharacterisedbytheirbackwardlinkagesintoplantationforestry,motivatedbytheneedtosecurereliableroundwoodsupply.These,togetherwithasmallnumberinvolvedinsawmilling,own58.8%oftheplantationforestresource.Alargernumberofmediumandemergingenterprisesislocatedinthesub-sectorsofgrowers,forestrycontractors,sawmilling,poletreatment,charcoalmanufacturingandpaperprocessing.

Contribution to GDP

ThecontributionoftheSectortoGDPfor2006wasaboutR14.0billion.Thisequatestoabout1%contributiontothetotalRSAGDP.

ContributiontoForeignTrade

Theforestproductsindustryranksamongstthetopexportingindustriesinthecountry.Onaverageoverthepastfewyears,sectorexportsamountedtoR11.0billionperannum,which,afterdeductionofimportsofforestproductsofR4.0billiongaveanetforeignexchangeearningtothecountryofR7.0billionperannum.TheForestSectorcontributed15.6%ofthecountry’stradebalance.

ContributiontoEmployment

TheForestSectorgeneratesemploymentformorethan170000workers,ofwhich6�%areincommercialforestry,whichincludesthesub-sectorsofgrowersandforestrycontractors.TotalremunerationamountedtoR4.6billionin2006.Mostofthejobscreatedareinruralandremoteareaswhereunemploymentishighandalternativeemploymentopportunitiesscarce.

Includingfamilydependants,anestimated870000peoplerelyontheSectorfortheirlivelihood.

Contributiontolivelihoodsubsistenceandinformaltrade

ThemajorityofSouthAfrica’sruralpoormakeextensiveuseofforestproductsfromwoodlandsandplantationsfordailyconsumptionandsmall-scaletrade.Firewood,buildingpoles,medicinalplantsandediblefruitsarecriticaltolivelihoodsofthepoorandprovideasafetynettothemostvulnerablehouseholds.

ThemajorchallengetogrowthandsustainableequityintheForestSectoristheshortageinroundwoodsupply,whichisnotkeepingpacewiththeincreaseinthelocaldemandforforestproducts.Ifthischallengeisnotaddressed,growthandemploymentprospectsandopportunitiesfortransformationintheForestSectorwillbeseriouslyconstrained.

8

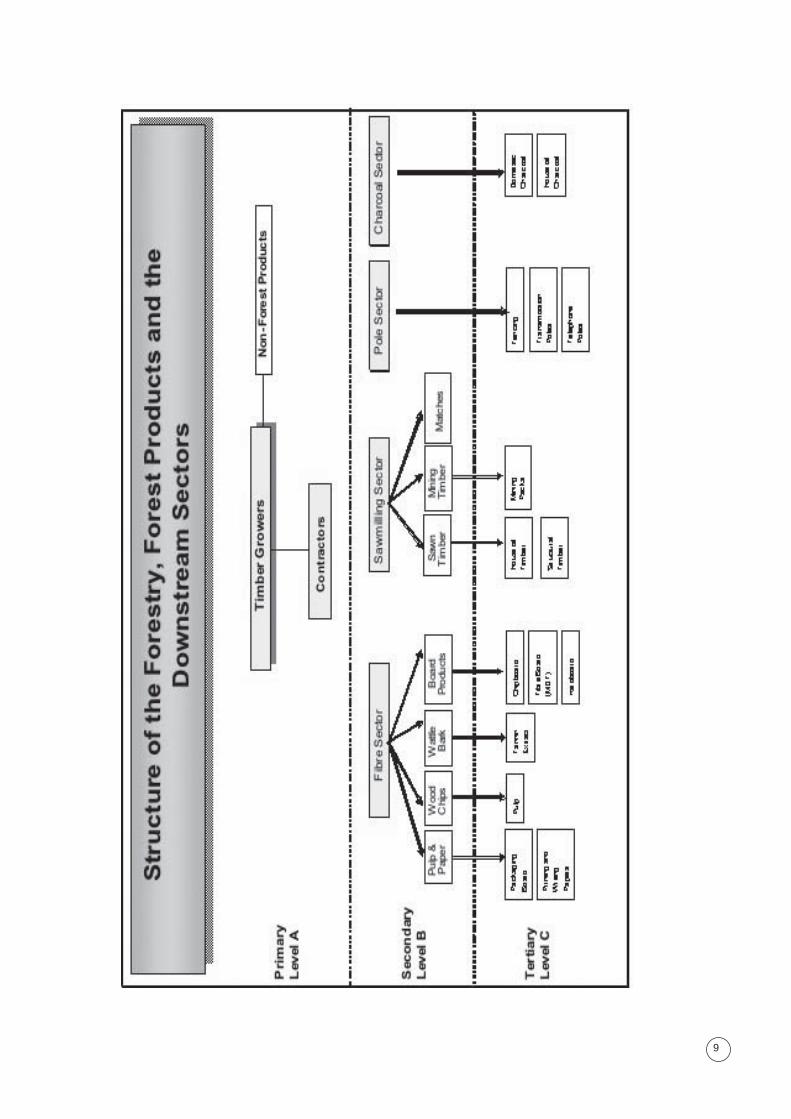

The forestry and forest product sub-sectors covered by the Charter and their linkages with downstream industries is illustrated in figure 2. Figure 2

9

10

�.CurrentStateofEmpowermentintheSector

Thefollowingtablespresentanoverviewofthecurrentsstateofbroad-basedblackeconomicempowermentintheSectorwithregardtokeyelementscoveredbytheSectorScorecard.TheinformationintheTablebelowisfromasurveyofenterprisesineachsub-sectorduring2006.

�.1 EquityOwnership

Sub-sectorWeighted Average

Black Total Black Women

PlantationGrowers

- Corporate

- PrivateFarmers2)

- EmergingGrowers2)

8,0%1)

<5%

>95%

0,1%1)

<5%

>80%

Fibre[Pulp,PaperandCompositeBoardProducers]

10,5% 0,0%

Sawmilling

- LargeMillers

- MediumMillers

- SmallMillers2)

20,1%

5,1%

>80%

0,�%

2,1%

<20%

PoleProducers 7,6% 0,5%

CharcoalProducers

- Corporate

- SmallProducers2)

1,�%

>80%

0,0%

>50%

ForestryContractors �9,8% 6,7%

1) Figuresestimatedfromsurveydataoffibreandlargesawmillinggroups(i.e.integrated forestryandforestproductsprocessingcompanies)

2) Estimated

Note: The fibre sub-sector comprises a number of large groups with international share-holding and asset profiles (e.g. Sappi, Steinhoff, Sonae, Masonite). The sawmilling sub-sector has large sawmilling participants that are wholly or partly state-owned (SAFCOL, Komatiland Forests (Pty) Ltd, MTO Forestry (Pty) Ltd, Singisi Forest Products (Pty) Ltd, Siyaqhubeka Forests (pty) Ltd, Amathole Forestry Company (Pty) Ltd) or owned by a trust (Hans Merensky Holdings). All other sub-sectors mostly comprise medium-sized or emerg-ing enterprises in private hands.

11

�.2ManagementControlandEmploymentEquity

Sub-sectors

Board LevelExecutive

Management LevelMiddle Management

Level

Black Total

Black Women

Black Total

Black Women

Black Total

Black Women

PlantationGrowers1) 2�,0%1) �,8%1) 1�,0%1) 2,7%1) 17,6%1) 4,7%1)

Fibre[Pulp,PaperandCompositeBoardProducers]

26,7% 6,7% 18,5% 0,4% 19,8% 2,1%

Sawmilling-LargeMillers

-MediumMillers

19,6%

8,6%

�,9%

2,5%

20,5%

5,7%

7,0%

1,2%

�0,5%

�0,7%

9,8%

1,2%

PoleProducers 0,0% 0,0% 1,6% 1,1% 4,7% 0,5%

CharcoalProducers 1,�% 0,0% 47,0% 15,8% 8�,8% �1,4%

ForestryContractors ��,0% 7,1% ��,8% 12,�% 52,9% 14,2%

1) Figures estimated from survey data of fibre and large sawmilling groups (i.e. integrated forestry and forest products processing companies)

�.�OtherKeyElements

Sub-sectorSkills

Development1

Preferential

Procurement2

Enterprise

Development3

Social

Investment4

PlantationGrowers 1,4% �1,0% n/a n/a

Fibre[Pulp,PaperandCompositeBoardProducers]

2,4% 19,8% 0,6% 4,2%

Sawmilling

- LargeMillers

- MediumMillers

1,0%

1,0%

n/a

n/a

n/a

n/a

n/a

n/a

PoleProducers 0,8% 7,5% 0,0% 0,5%

CharcoalProducers 0,5% 25,0% n/a n/a

ForestryContractors n/a n/a n/a n/a

12

1) SkillsDevelopment:Investmentaspercentageofpayroll

2) PreferentialProcurement:Discretionaryprocurementspendonblacksuppliers

3) EnterpriseDevelopment:Investmentinenterprisedevelopmentaspercentageofnetprofit

aftertax

4) SocialInvestment:Investmentinsocial/economicdevelopmentaspercentageofnetprofit

aftertax

Note: The high level of ‘not available’ data is mostly a reflection of the inability by companies to access/ gather reliable data due to lack of systems and that the data provided in the survey forms is not compatible with the Scorecard definition. Only in the case of larger companies in the fibre sector can the data be regarded as representative.

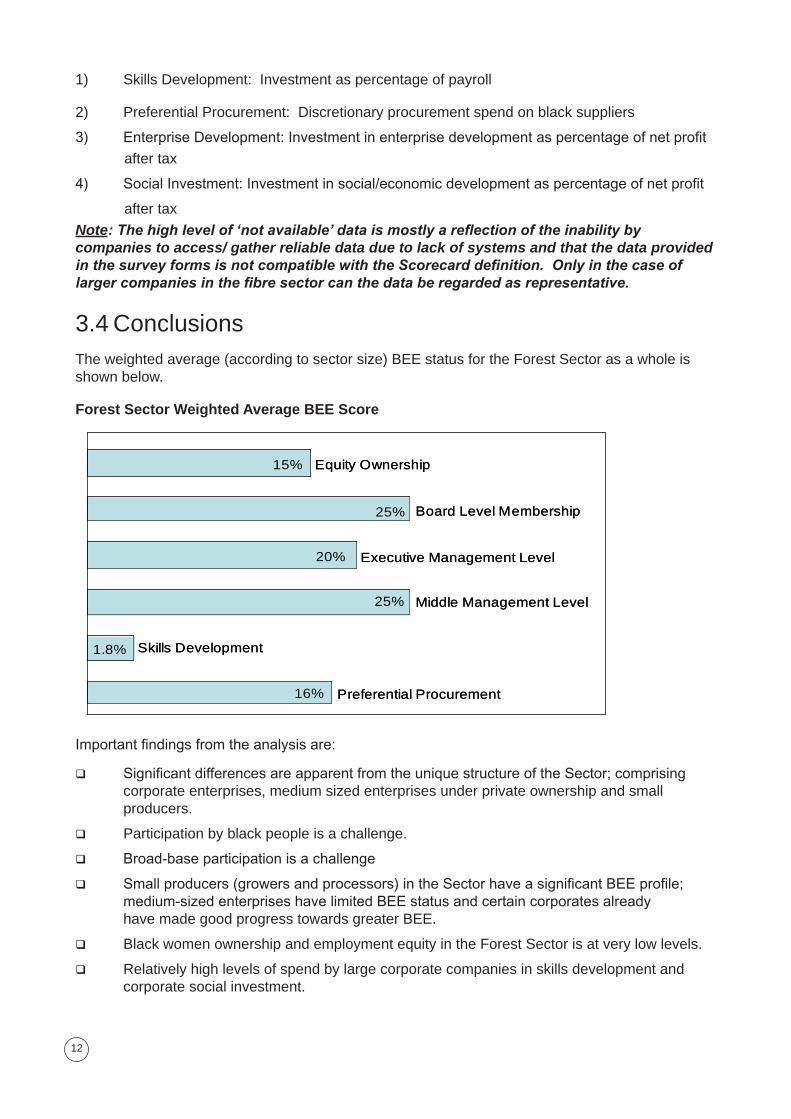

�.4ConclusionsTheweightedaverage(accordingtosectorsize)BEEstatusfortheForestSectorasawholeisshownbelow.

Forest Sector Weighted Average BEE Score

EquityOwnership

BoardLevelMembership

ExecutiveManagementLevel

MiddleManagementLevel

SkillsDevelopment

PreferentialProcurement

15%

25%

20%

25%

1.8%

16%

EquityOwnership

BoardLevelMembership

ExecutiveManagementLevel

MiddleManagementLevel

SkillsDevelopment

PreferentialProcurement

15%

25%

20%

25%

1.8%

16%

Importantfindingsfromtheanalysisare:

q SignificantdifferencesareapparentfromtheuniquestructureoftheSector;comprising corporateenterprises,mediumsizedenterprisesunderprivateownershipandsmall producers.

q Participationbyblackpeopleisachallenge.

q Broad-baseparticipationisachallenge

q Smallproducers(growersandprocessors)intheSectorhaveasignificantBEEprofile; medium-sizedenterpriseshavelimitedBEEstatusandcertaincorporatesalready havemadegoodprogresstowardsgreaterBEE.

q BlackwomenownershipandemploymentequityintheForestSectorisatverylowlevels.

q Relativelyhighlevelsofspendbylargecorporatecompaniesinskillsdevelopmentand corporatesocialinvestment.

1�

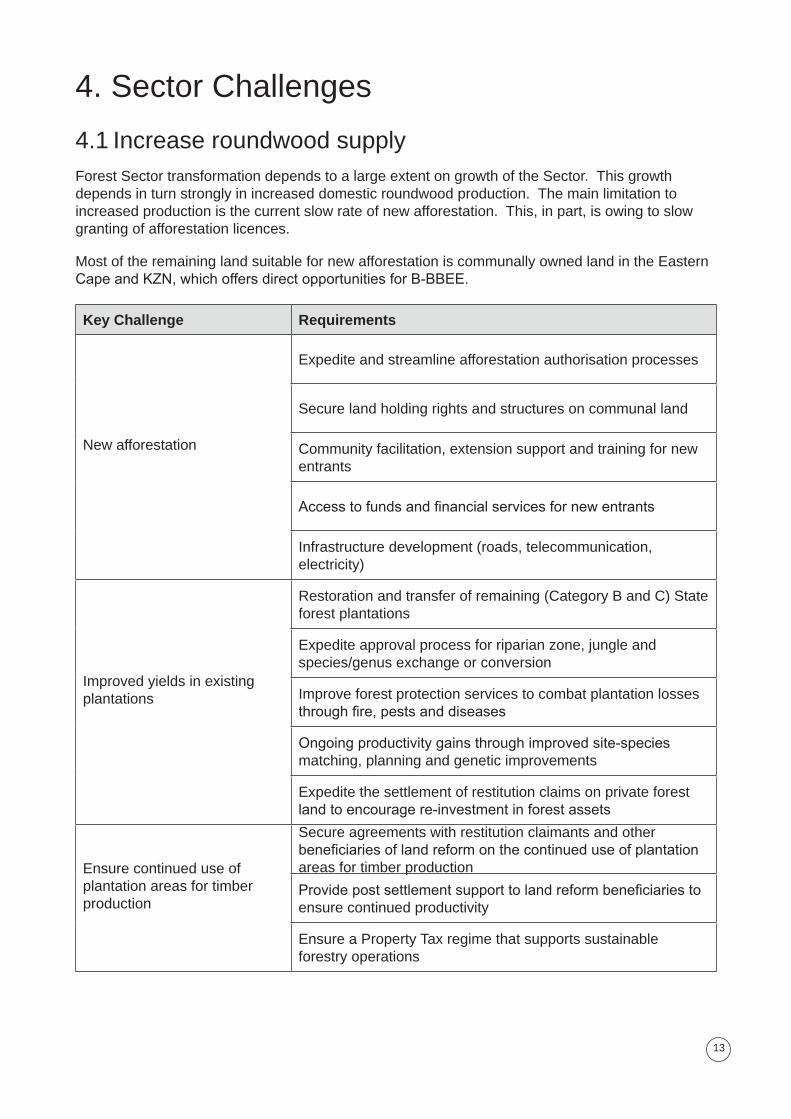

4.SectorChallenges

4.1IncreaseroundwoodsupplyForestSectortransformationdependstoalargeextentongrowthoftheSector.Thisgrowthdependsinturnstronglyinincreaseddomesticroundwoodproduction.Themainlimitationtoincreasedproductionisthecurrentslowrateofnewafforestation.This,inpart,isowingtoslowgrantingofafforestationlicences.

MostoftheremaininglandsuitablefornewafforestationiscommunallyownedlandintheEasternCapeandKZN,whichoffersdirectopportunitiesforB-BBEE.

Key Challenge Requirements

Newafforestation

Expediteandstreamlineafforestationauthorisationprocesses

Securelandholdingrightsandstructuresoncommunalland

Communityfacilitation,extensionsupportandtrainingfornewentrants

Accesstofundsandfinancialservicesfornewentrants

Infrastructuredevelopment(roads,telecommunication,electricity)

Improvedyieldsinexistingplantations

Restorationandtransferofremaining(CategoryBandC)Stateforestplantations

Expediteapprovalprocessforriparianzone,jungleandspecies/genusexchangeorconversion

Improveforestprotectionservicestocombatplantationlossesthroughfire,pestsanddiseases

Ongoingproductivitygainsthroughimprovedsite-speciesmatching,planningandgeneticimprovements

Expeditethesettlementofrestitutionclaimsonprivateforestlandtoencouragere-investmentinforestassets

Ensurecontinueduseofplantationareasfortimberproduction

Secureagreementswithrestitutionclaimantsandotherbeneficiariesoflandreformonthecontinueduseofplantationareasfortimberproduction

Providepostsettlementsupporttolandreformbeneficiariestoensurecontinuedproductivity

EnsureaPropertyTaxregimethatsupportssustainableforestryoperations

14

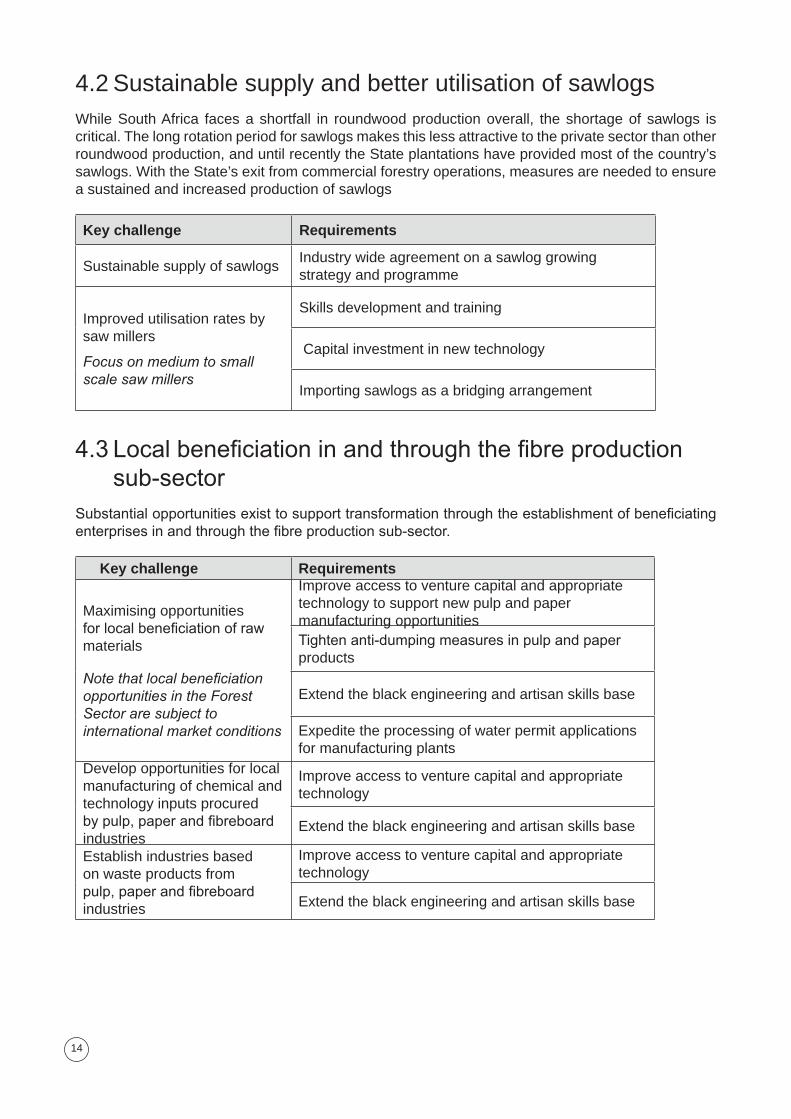

4.2SustainablesupplyandbetterutilisationofsawlogsWhileSouthAfrica facesashortfall in roundwoodproductionoverall, theshortageof sawlogs iscritical.Thelongrotationperiodforsawlogsmakesthislessattractivetotheprivatesectorthanotherroundwoodproduction,anduntilrecentlytheStateplantationshaveprovidedmostofthecountry’ssawlogs.WiththeState’sexitfromcommercialforestryoperations,measuresareneededtoensureasustainedandincreasedproductionofsawlogs

Key challenge Requirements

SustainablesupplyofsawlogsIndustrywideagreementonasawloggrowingstrategyandprogramme

Improvedutilisationratesbysawmillers

Focus on medium to small scale saw millers

Skillsdevelopmentandtraining

Capitalinvestmentinnewtechnology

Importingsawlogsasabridgingarrangement

4.3Localbeneficiationinandthroughthefibreproductionsub-sector

Substantialopportunitiesexisttosupporttransformationthroughtheestablishmentofbeneficiatingenterprisesinandthroughthefibreproductionsub-sector.

Key challenge Requirements

Maximisingopportunitiesforlocalbeneficiationofrawmaterials

Note that local beneficiation opportunities in the Forest Sector are subject to international market conditions

ImproveaccesstoventurecapitalandappropriatetechnologytosupportnewpulpandpapermanufacturingopportunitiesTightenanti-dumpingmeasuresinpulpandpaperproducts

Extendtheblackengineeringandartisanskillsbase

Expeditetheprocessingofwaterpermitapplicationsformanufacturingplants

Developopportunitiesforlocalmanufacturingofchemicalandtechnologyinputsprocuredbypulp,paperandfibreboardindustries

Improveaccesstoventurecapitalandappropriatetechnology

Extendtheblackengineeringandartisanskillsbase

Establishindustriesbasedonwasteproductsfrompulp,paperandfibreboardindustries

Improveaccesstoventurecapitalandappropriatetechnology

Extendtheblackengineeringandartisanskillsbase

15

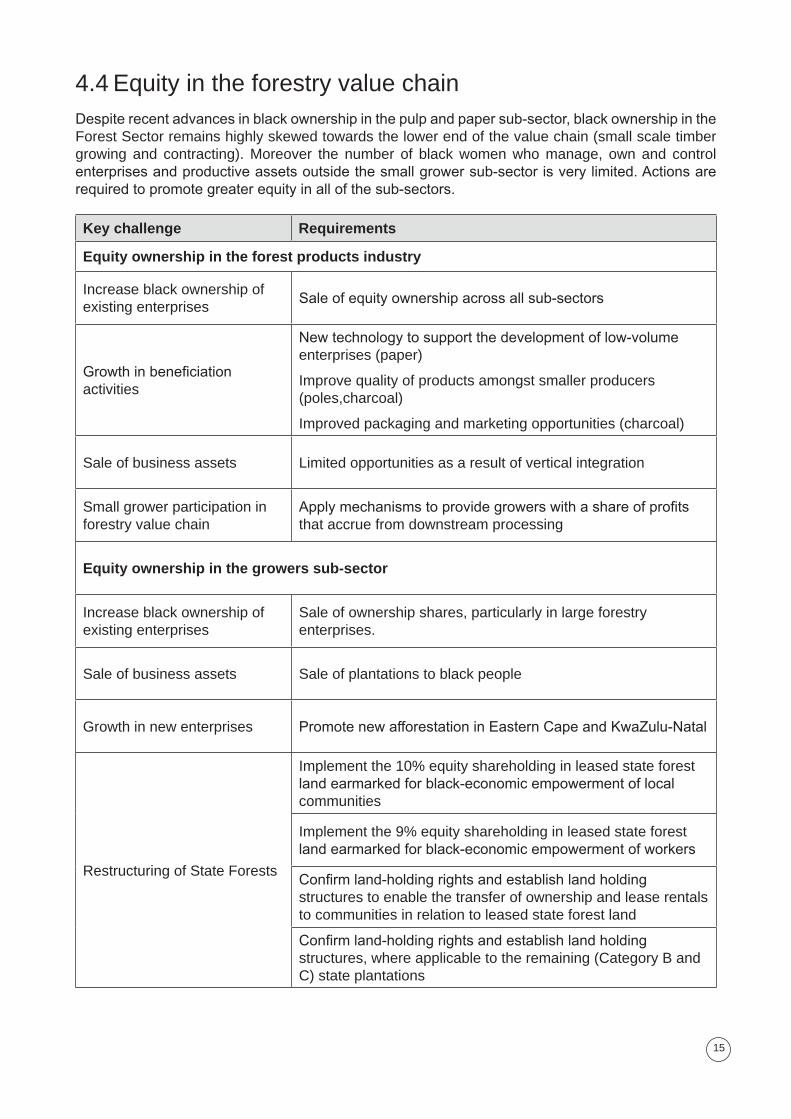

4.4EquityintheforestryvaluechainDespiterecentadvancesinblackownershipinthepulpandpapersub-sector,blackownershipintheForestSectorremainshighlyskewedtowardsthelowerendofthevaluechain(smallscaletimbergrowing and contracting). Moreover the number of black women who manage, own and controlenterprisesandproductiveassetsoutsidethesmallgrowersub-sectorisverylimited.Actionsarerequiredtopromotegreaterequityinallofthesub-sectors.

Key challenge Requirements

Equity ownership in the forest products industry

Increaseblackownershipofexistingenterprises

Saleofequityownershipacrossallsub-sectors

Growthinbeneficiationactivities

Newtechnologytosupportthedevelopmentoflow-volumeenterprises(paper)

Improvequalityofproductsamongstsmallerproducers(poles,charcoal)

Improvedpackagingandmarketingopportunities(charcoal)

Saleofbusinessassets Limitedopportunitiesasaresultofverticalintegration

Smallgrowerparticipationinforestryvaluechain

Applymechanismstoprovidegrowerswithashareofprofitsthataccruefromdownstreamprocessing

Equity ownership in the growers sub-sector

Increaseblackownershipofexistingenterprises

Saleofownershipshares,particularlyinlargeforestryenterprises.

Saleofbusinessassets Saleofplantationstoblackpeople

Growthinnewenterprises PromotenewafforestationinEasternCapeandKwaZulu-Natal

RestructuringofStateForests

Implementthe10%equityshareholdinginleasedstateforestlandearmarkedforblack-economicempowermentoflocalcommunities

Implementthe9%equityshareholdinginleasedstateforestlandearmarkedforblack-economicempowermentofworkers

Confirmland-holdingrightsandestablishlandholdingstructurestoenablethetransferofownershipandleaserentalstocommunitiesinrelationtoleasedstateforestland

Confirmland-holdingrightsandestablishlandholdingstructures,whereapplicabletotheremaining(CategoryBandC)stateplantations

16

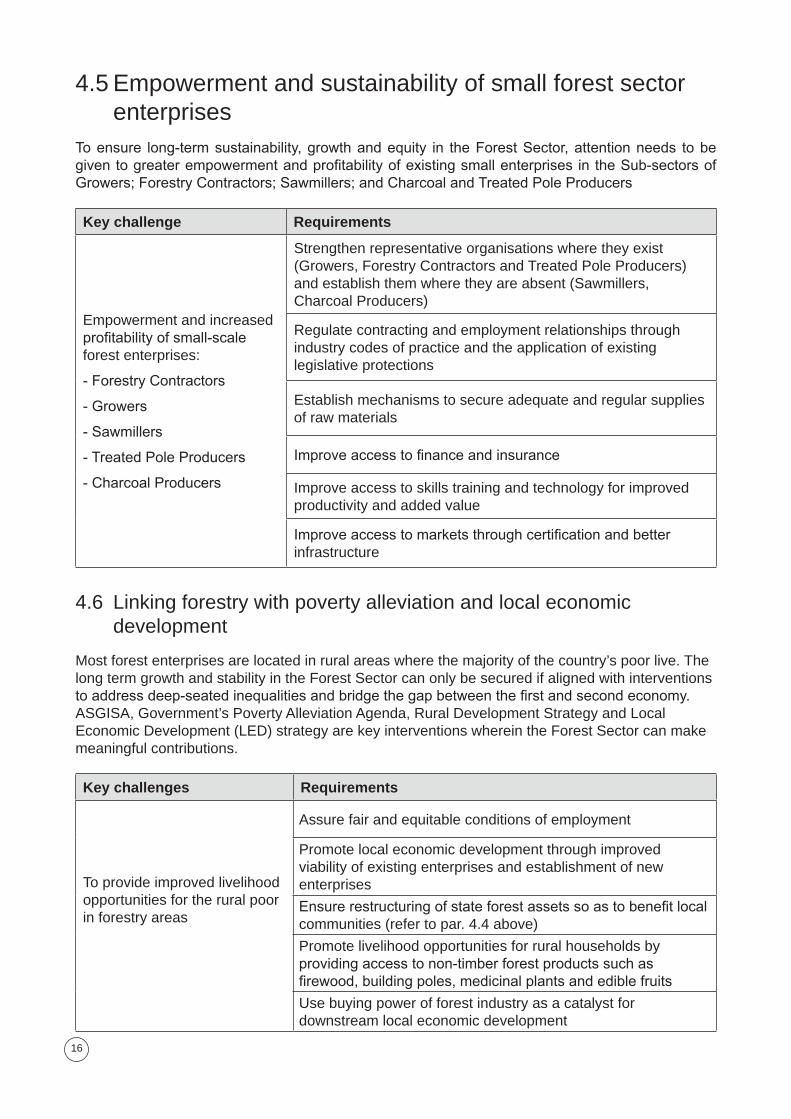

4.5Empowermentandsustainabilityofsmallforestsectorenterprises

Toensure long-termsustainability,growthandequity in theForestSector,attentionneeds tobegiventogreaterempowermentandprofitabilityofexistingsmallenterprises intheSub-sectorsofGrowers;ForestryContractors;Sawmillers;andCharcoalandTreatedPoleProducers

Key challenge Requirements

Empowermentandincreasedprofitabilityofsmall-scaleforestenterprises:

-ForestryContractors

-Growers

-Sawmillers

-TreatedPoleProducers

-CharcoalProducers

Strengthenrepresentativeorganisationswheretheyexist(Growers,ForestryContractorsandTreatedPoleProducers)andestablishthemwheretheyareabsent(Sawmillers,CharcoalProducers)

Regulatecontractingandemploymentrelationshipsthroughindustrycodesofpracticeandtheapplicationofexistinglegislativeprotections

Establishmechanismstosecureadequateandregularsuppliesofrawmaterials

Improveaccesstofinanceandinsurance

Improveaccesstoskillstrainingandtechnologyforimprovedproductivityandaddedvalue

Improveaccesstomarketsthroughcertificationandbetterinfrastructure

4.6 Linkingforestrywithpovertyalleviationandlocaleconomicdevelopment

Mostforestenterprisesarelocatedinruralareaswherethemajorityofthecountry’spoorlive.ThelongtermgrowthandstabilityintheForestSectorcanonlybesecuredifalignedwithinterventionstoaddressdeep-seatedinequalitiesandbridgethegapbetweenthefirstandsecondeconomy.ASGISA,Government’sPovertyAlleviationAgenda,RuralDevelopmentStrategyandLocalEconomicDevelopment(LED)strategyarekeyinterventionswhereintheForestSectorcanmakemeaningfulcontributions.

Key challenges Requirements

Toprovideimprovedlivelihoodopportunitiesfortheruralpoorinforestryareas

Assurefairandequitableconditionsofemployment

Promotelocaleconomicdevelopmentthroughimprovedviabilityofexistingenterprisesandestablishmentofnewenterprises

Ensurerestructuringofstateforestassetssoastobenefitlocalcommunities(refertopar.4.4above)

Promotelivelihoodopportunitiesforruralhouseholdsbyprovidingaccesstonon-timberforestproductssuchasfirewood,buildingpoles,medicinalplantsandediblefruits

Usebuyingpowerofforestindustryasacatalystfordownstreamlocaleconomicdevelopment

17

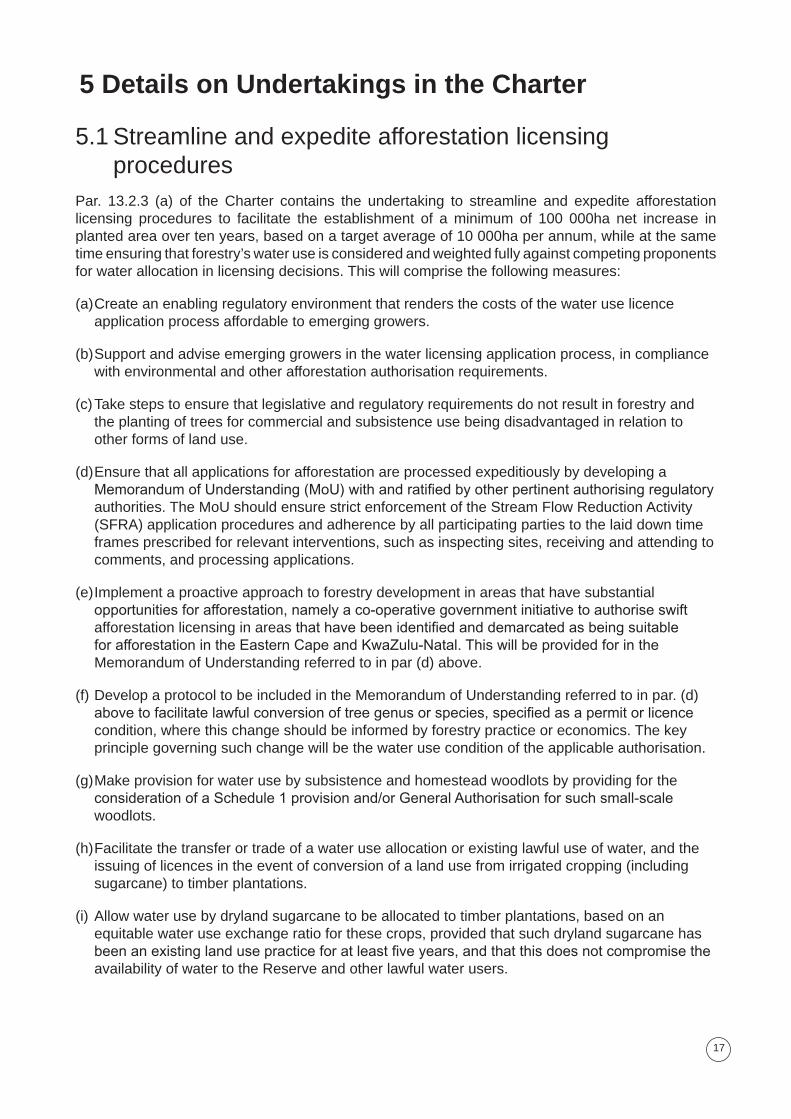

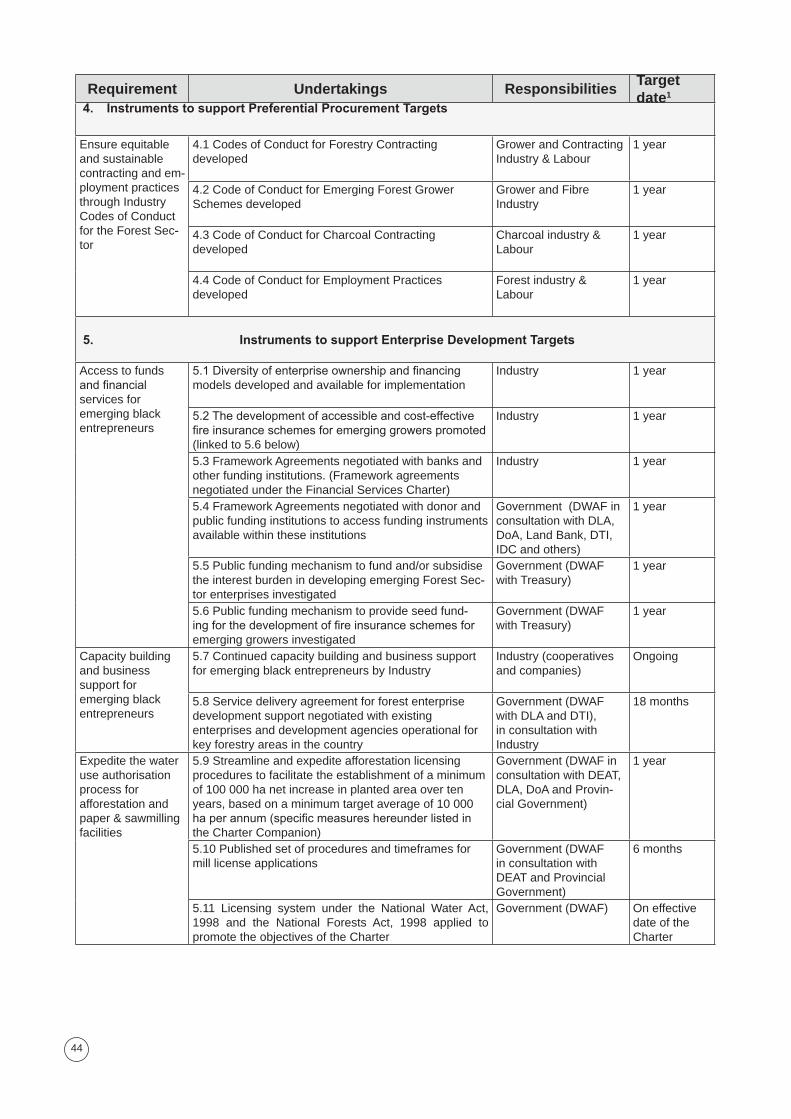

5 Details on Undertakings in the Charter

5.1Streamlineandexpediteafforestationlicensingprocedures

Par. 1�.2.� (a) of the Charter contains the undertaking to streamline and expedite afforestationlicensing procedures to facilitate the establishment of a minimum of 100 000ha net increase inplantedareaovertenyears,basedonatargetaverageof10000haperannum,whileatthesametimeensuringthatforestry’swateruseisconsideredandweightedfullyagainstcompetingproponentsforwaterallocationinlicensingdecisions.Thiswillcomprisethefollowingmeasures:

(a)Createanenablingregulatoryenvironmentthatrendersthecostsofthewateruselicenceapplicationprocessaffordabletoemerginggrowers.

(b)Supportandadviseemerginggrowersinthewaterlicensingapplicationprocess,incompliancewithenvironmentalandotherafforestationauthorisationrequirements.

(c)Takestepstoensurethatlegislativeandregulatoryrequirementsdonotresultinforestryandtheplantingoftreesforcommercialandsubsistenceusebeingdisadvantagedinrelationtootherformsoflanduse.

(d)EnsurethatallapplicationsforafforestationareprocessedexpeditiouslybydevelopingaMemorandumofUnderstanding(MoU)withandratifiedbyotherpertinentauthorisingregulatoryauthorities.TheMoUshouldensurestrictenforcementoftheStreamFlowReductionActivity(SFRA)applicationproceduresandadherencebyallparticipatingpartiestothelaiddowntimeframesprescribedforrelevantinterventions,suchasinspectingsites,receivingandattendingtocomments,andprocessingapplications.

(e)Implementaproactiveapproachtoforestrydevelopmentinareasthathavesubstantialopportunitiesforafforestation,namelyaco-operativegovernmentinitiativetoauthoriseswiftafforestationlicensinginareas thathavebeenidentifiedanddemarcatedasbeingsuitableforafforestationintheEasternCapeandKwaZulu-Natal.ThiswillbeprovidedforintheMemorandumofUnderstandingreferredtoinpar(d)above.

(f)DevelopaprotocoltobeincludedintheMemorandumofUnderstandingreferredtoinpar.(d)abovetofacilitatelawfulconversionoftreegenusorspecies,specifiedasapermitorlicencecondition,wherethischangeshouldbeinformedbyforestrypracticeoreconomics.Thekeyprinciplegoverningsuchchangewillbethewateruseconditionoftheapplicableauthorisation.

(g)MakeprovisionforwaterusebysubsistenceandhomesteadwoodlotsbyprovidingfortheconsiderationofaSchedule1provisionand/orGeneralAuthorisationforsuchsmall-scalewoodlots.

(h)Facilitatethetransferortradeofawateruseallocationorexistinglawfuluseofwater,andtheissuingoflicencesintheeventofconversionofalandusefromirrigatedcropping(includingsugarcane)totimberplantations.

(i)Allowwaterusebydrylandsugarcanetobeallocatedtotimberplantations,basedonanequitablewateruseexchangeratioforthesecrops,providedthatsuchdrylandsugarcanehasbeenanexistinglandusepracticeforatleastfiveyears,andthatthisdoesnotcompromisetheavailabilityofwatertotheReserveandotherlawfulwaterusers.

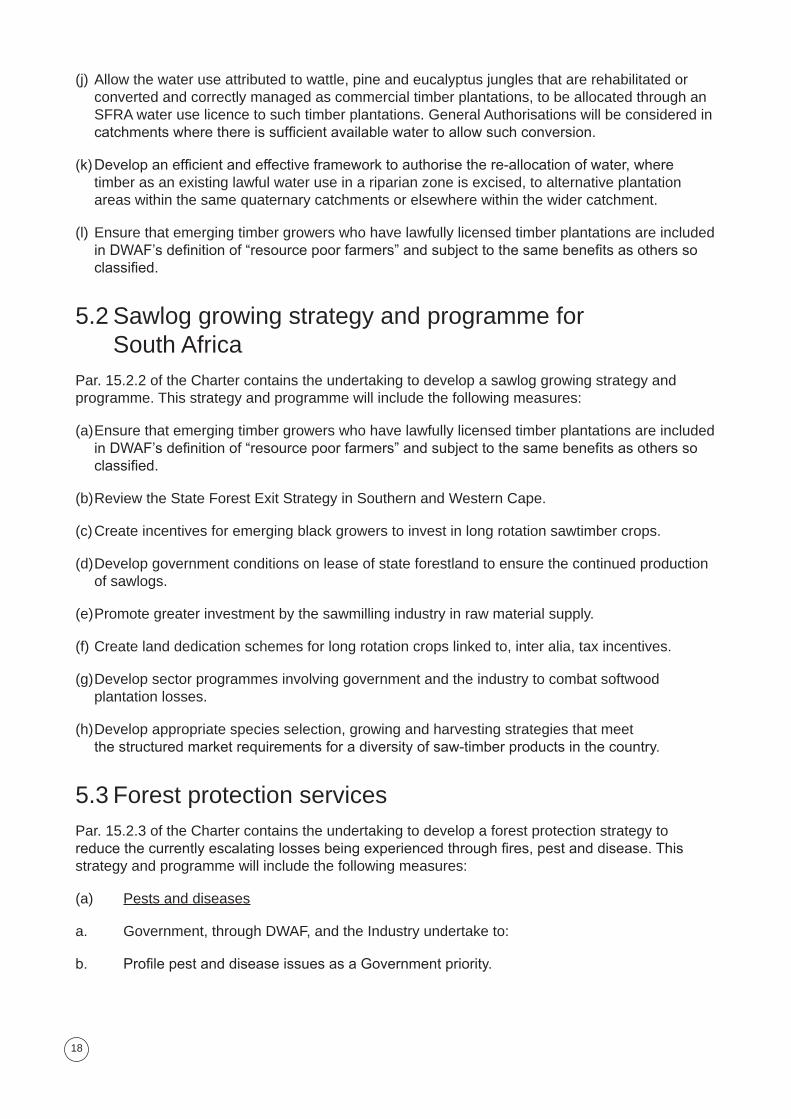

18

(j)Allowthewateruseattributedtowattle,pineandeucalyptusjunglesthatarerehabilitatedorconvertedandcorrectlymanagedascommercialtimberplantations,tobeallocatedthroughanSFRAwateruselicencetosuchtimberplantations.GeneralAuthorisationswillbeconsideredincatchmentswherethereissufficientavailablewatertoallowsuchconversion.

(k)Developanefficientandeffectiveframeworktoauthorisethere-allocationofwater,wheretimberasanexistinglawfulwateruseinariparianzoneisexcised,toalternativeplantationareaswithinthesamequaternarycatchmentsorelsewherewithinthewidercatchment.

(l)EnsurethatemergingtimbergrowerswhohavelawfullylicensedtimberplantationsareincludedinDWAF’sdefinitionof“resourcepoorfarmers”andsubjecttothesamebenefitsasotherssoclassified.

5.2SawloggrowingstrategyandprogrammeforSouthAfrica

Par.15.2.2oftheChartercontainstheundertakingtodevelopasawloggrowingstrategyandprogramme.Thisstrategyandprogrammewillincludethefollowingmeasures:

(a)EnsurethatemergingtimbergrowerswhohavelawfullylicensedtimberplantationsareincludedinDWAF’sdefinitionof“resourcepoorfarmers”andsubjecttothesamebenefitsasotherssoclassified.

(b)ReviewtheStateForestExitStrategyinSouthernandWesternCape.

(c)Createincentivesforemergingblackgrowerstoinvestinlongrotationsawtimbercrops.

(d)Developgovernmentconditionsonleaseofstateforestlandtoensurethecontinuedproductionofsawlogs.

(e)Promotegreaterinvestmentbythesawmillingindustryinrawmaterialsupply.

(f)Createlanddedicationschemesforlongrotationcropslinkedto,interalia,taxincentives.

(g)Developsectorprogrammesinvolvinggovernmentandtheindustrytocombatsoftwoodplantationlosses.

(h)Developappropriatespeciesselection,growingandharvestingstrategiesthatmeetthestructuredmarketrequirementsforadiversityofsaw-timberproductsinthecountry.

5.�ForestprotectionservicesPar.15.2.�oftheChartercontainstheundertakingtodevelopaforestprotectionstrategytoreducethecurrentlyescalatinglossesbeingexperiencedthroughfires,pestanddisease.Thisstrategyandprogrammewillincludethefollowingmeasures:

(a) Pestsanddiseases

a. Government,throughDWAF,andtheIndustryundertaketo:

b. ProfilepestanddiseaseissuesasaGovernmentpriority.

19

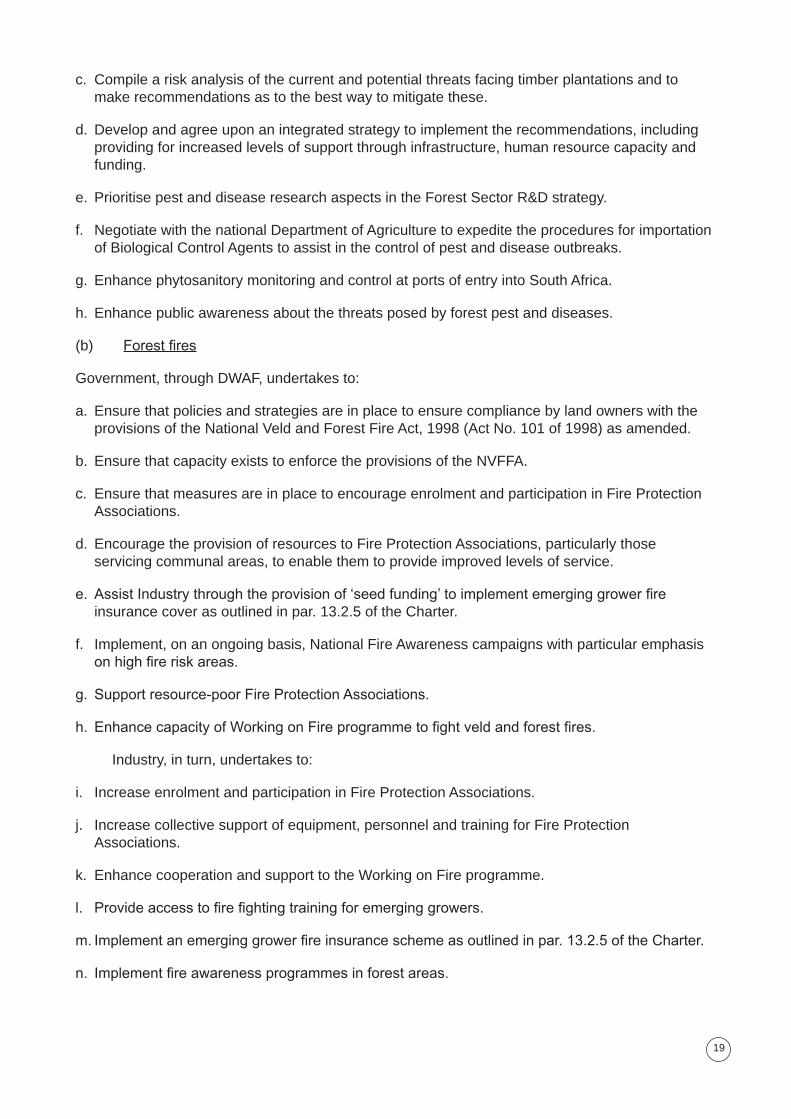

c. Compileariskanalysisofthecurrentandpotentialthreatsfacingtimberplantationsandtomakerecommendationsastothebestwaytomitigatethese.

d. Developandagreeuponanintegratedstrategytoimplementtherecommendations,includingprovidingforincreasedlevelsofsupportthroughinfrastructure,humanresourcecapacityandfunding.

e. PrioritisepestanddiseaseresearchaspectsintheForestSectorR&Dstrategy.

f. NegotiatewiththenationalDepartmentofAgriculturetoexpeditetheproceduresforimportationofBiologicalControlAgentstoassistinthecontrolofpestanddiseaseoutbreaks.

g. EnhancephytosanitorymonitoringandcontrolatportsofentryintoSouthAfrica.

h. Enhancepublicawarenessaboutthethreatsposedbyforestpestanddiseases.

(b) Forestfires

Government,throughDWAF,undertakesto:

a. EnsurethatpoliciesandstrategiesareinplacetoensurecompliancebylandownerswiththeprovisionsoftheNationalVeldandForestFireAct,1998(ActNo.101of1998)asamended.

b. EnsurethatcapacityexiststoenforcetheprovisionsoftheNVFFA.

c. EnsurethatmeasuresareinplacetoencourageenrolmentandparticipationinFireProtectionAssociations.

d. EncouragetheprovisionofresourcestoFireProtectionAssociations,particularlythoseservicingcommunalareas,toenablethemtoprovideimprovedlevelsofservice.

e. AssistIndustrythroughtheprovisionof‘seedfunding’toimplementemerginggrowerfireinsurancecoverasoutlinedinpar.1�.2.5oftheCharter.

f. Implement,onanongoingbasis,NationalFireAwarenesscampaignswithparticularemphasisonhighfireriskareas.

g. Supportresource-poorFireProtectionAssociations.

h. EnhancecapacityofWorkingonFireprogrammetofightveldandforestfires.

Industry,inturn,undertakesto:

i. IncreaseenrolmentandparticipationinFireProtectionAssociations.

j. Increasecollectivesupportofequipment,personnelandtrainingforFireProtectionAssociations.

k. EnhancecooperationandsupporttotheWorkingonFireprogramme.

l. Provideaccesstofirefightingtrainingforemerginggrowers.

m.Implementanemerginggrowerfireinsuranceschemeasoutlinedinpar.13.2.5oftheCharter.

n. Implementfireawarenessprogrammesinforestareas.

20

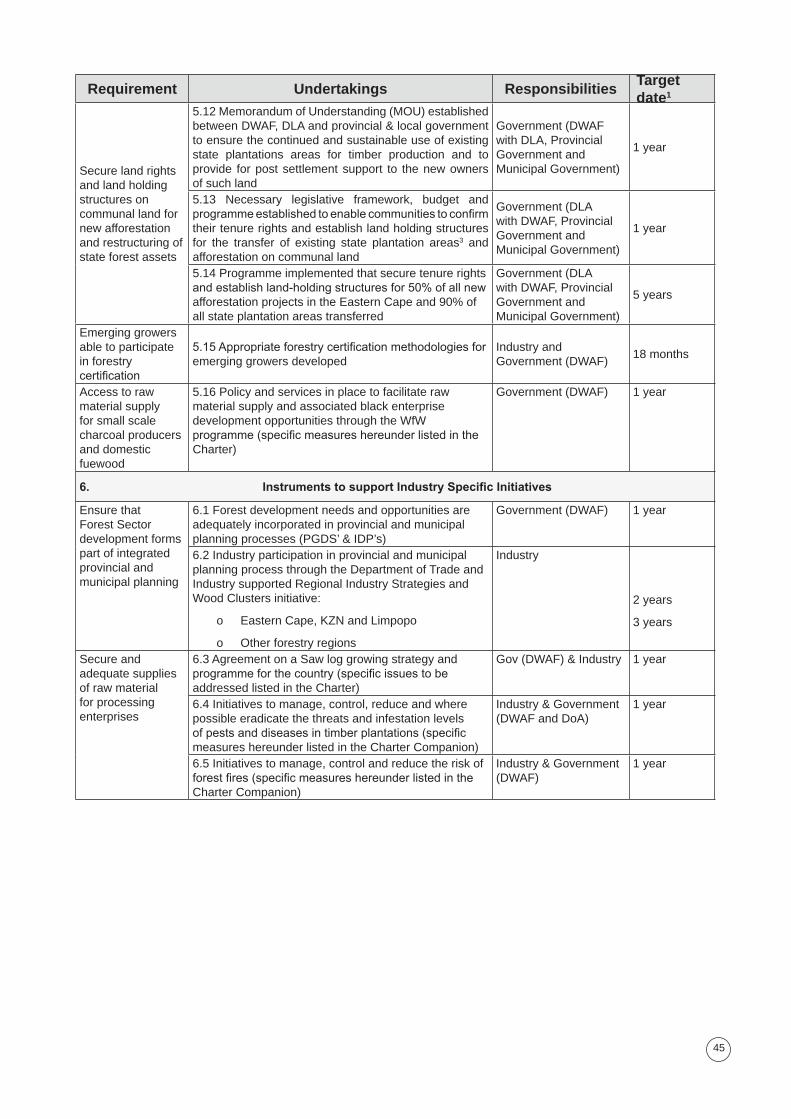

5.4CharterCouncilPar.16.1oftheChartercontainstheundertakingtoestablishaForestSectorCharterCouncilthatwilloverseeandfacilitatetheimplementationoftheCharter.Thefunctions,composition,constitutionandfundingarrangementsfortheCouncilareoutlinedhereunder:

(a) Functions

a. MonitortheimplementationoftheCharterandreviewtheCharterasoutlinedinpar.16.2oftheCharter.

b. ProvideinterpretationandguidancewithrespecttotheCharter.

c. FacilitatethecommunicationandpopularisationoftheCharter.

d. Facilitatecross-industryandgovernmentnegotiationstopromotetheapplicationandimplementationoftheCharter.

e. Provideguidanceonsector-specificmattersaffectingB-BBEEinentitieswithintheSector.

f. ShareinformationwiththenationalmonitoringmechanismandapprovedaccreditationagenciesthatarerelevanttotheSector.

g. ImplementprogrammestoensurethatsufficientindependentcapacityofverificationagenciesexisttosupporttheCharter.

h. InitiateprocedurestoconverttheForestCharterintoSectorCodes.

i. Issueguidelinesforsector-specificenterprisedevelopmentandsocio-economicdevelopmentcontributionsundertheScorecard.

(b) Composition

a. TheCouncilshallconsistof19members,withthefollowingcomposition:

oAChairperson,whoshallbeanindependentperson,appointedbytheMinisterofWaterAffairsandForestryinconsultationwithstakeholderconstituencies.

oAChiefExecutiveOfficer,whoshallberesponsibleforthedailyadministrationandoperationsoftheCouncilandserveontheCouncilinanex-officiocapacity.

oNine(9)membersrepresentingindustry,appointedfromthevarioussub-sectorsintheForestSector.

oTwo(2)membersrepresentingorganisedlabour.

oThree(�)membersrepresentingbroaderstakeholdersassignedbytheMinisterofWaterAffairsandForestryinconsultationwiththestakeholderconstituencies.

oThree(�)membersrepresentinggovernment,oneeachfromtheDepartmentsofWaterAffairsandForestry,TradeandIndustry,andLandAffairs.

b. ThecompositionoftheCouncilshallfairlyreflectthestakeholdersintheSectorandberaciallyandgenderrepresentative.

21

c. ThetermsofofficeformembersoftheCouncilshallbe3years,andmembersshallbeeligibleforre-appointment.

d. TheChiefExecutiveOfficershallbeappointedjointlybythepartiesthatfundtheCharterCouncilasoutlinedinpar.5.4(d)below.

e. TheChiefExecutiveOfficersshallmakeotherstaffappointments.

(c) Constitution

a. TheCouncilshallbeguidedbythefollowingfivebasicprinciples:

o Transparency

o Fairness

o CorporateGovernance

o Consultationandinclusivity

o Socio-economictransformation

b. DecisionsoftheCouncilshallbetakenonaconsensusbasis.IfonanyissuetheCouncilisunabletoachieveconsensus,therewillbeadisputebreakingmechanismasspecifiedintheConstitutionreferredtoinpar.ebelow.

c. TheCouncilmaycreatesub-committeestodealwithspecificmattersasandwhenrequired.

d. TheCouncilmayco-optexpertstoserveonoradvisesub-committeesascontemplatedabove.

e. AConstitutionoftheCouncilshallbetabledforadoptionatthefirstmeetingoftheCouncilandmustbeadoptedbyatwo-thirdmajoritywithin60workingdaysafterthegazettingofthisCharter.

f. TheCouncilmayamendtheConstitutionoftheCouncilfromtimetotime.

g. TheCouncilshall,inconsultationwiththeBEEAdvisoryCouncilandbyresolution,formulaterulestofurtherregulateitsproceedings.

(d)Funding

a. TheForestIndustryandGovernmentshallfundtheCounciljointly,withGovernmentcontributing60%andIndustry40%ofthebudgetrequirements.

b. Thefundingarrangementasoutlinedinpar.aaboveissubjecttoagreementbetweenthesepartiesontheinitialbudgetrequirementsfortheCouncilandanannualescalationofthebudgetbasedontheSouthAfricanConsumerPriceIndex,unlessotherwiseagreedtobytheparties.

c. TheCouncilshallprepareanannualbusinessplanthatwillincludeabudgetfortheworkoftheCouncil.

22

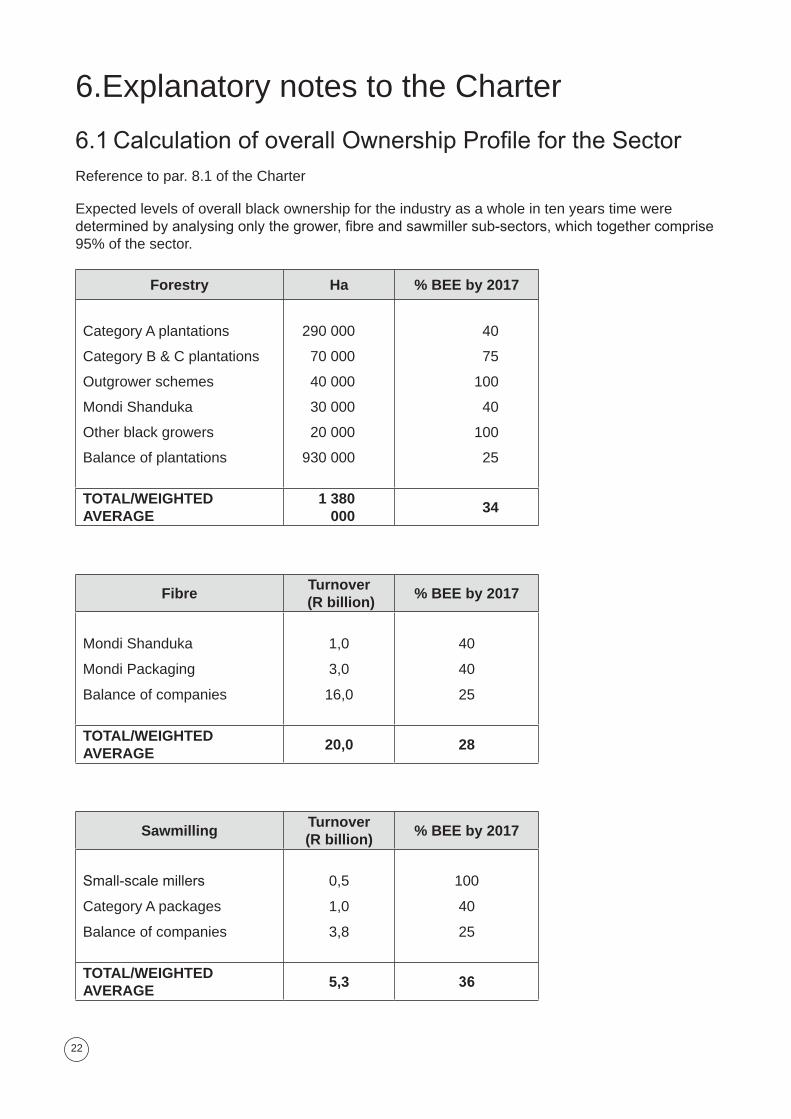

6.ExplanatorynotestotheCharter

6.1CalculationofoverallOwnershipProfilefortheSectorReferencetopar.8.1oftheCharter

Expectedlevelsofoverallblackownershipfortheindustryasawholeintenyearstimeweredeterminedbyanalysingonlythegrower,fibreandsawmillersub-sectors,whichtogethercomprise95%ofthesector.

Forestry Ha % BEE by 2017

CategoryAplantations

CategoryB&Cplantations

Outgrowerschemes

MondiShanduka

Otherblackgrowers

Balanceofplantations

290000

70000

40000

�0000

20000

9�0000

40

75

100

40

100

25

TOTAL/WEIGHTED AVERAGE

1 380 000

34

FibreTurnover

(R billion)% BEE by 2017

MondiShanduka

MondiPackaging

Balanceofcompanies

1,0

�,0

16,0

40

40

25

TOTAL/WEIGHTED AVERAGE

20,0 28

SawmillingTurnover (R billion)

% BEE by 2017

Small-scalemillers

CategoryApackages

Balanceofcompanies

0,5

1,0

�,8

100

40

25

TOTAL/WEIGHTED AVERAGE

5,3 36

2�

Theweightedaverageexpectedlevelofoverallblackownershipfor2017fortheForestSectoristhusabout30%(weightingaccordingtosectorturnover;usingR5billionforthegrowersub-sector).Theapplicationofbonuspointstoincreaseblackownershipinexistingenterpriseswithablackownershiptargetof25%byafurther5%hasnotbeenincludedinthesecalculations

6.2ComparisonbetweenScorecardfortheForestSectorandtheGenericScorecard

ChangesfromtheGenericScorecardintheCodesofGoodPracticeandthejustificationforthesechangesarelistedbelow.

6.2.1QualificationsforESMEs

CompliancewiththeIndustryCodesofGoodConductisalsoappliedtoESMEs.ESMEsmust,whentheysubmitproofoftheirESME-status,alsosignacommitmentofcompliancewiththeIndustryCodesofGoodConduct.ESMEsthatdon’tcomplywilllosetheBEEstatusaffordedtothem,namelytheLevel�contributorforthosethatare50%ownedbyblackpeopleorbyblackwomenorLevel4contributorforotherESMEs.

6.2.2Bonuspoints

Additionalbonuspointshavebeenallocated(11insteadof7formediumandlargeenterprisesand10insteadof7forQSE)asanincentivetoachievehighersector-specifictargetsasfurtheroutlinedbelow.

6.2.�Medium/largeenterprises

Ownershiptargets

a)Thetargetforeconomicinterestinthehandsofbroad-basedblackownershipschemeshasbeenincreasedfrom2.5%to7.5%.ThisisjustifiedonthebasisthattheForestSector,asaruralbasedindustry,canmakeasignificantcontributiontobroad-basedBEEinthisregard.Thisdoesnotaffecttheoverallownershiptargets.

b)Twobonuspointshavebeenallocatedasanincentivetoachievehigheroverallownershiptargetsintermsofeconomicinterestinthehandsofblackpeople(�0%)andinthehandsofblackwomen(15%).

c) Therealizationpointsfornetequityinterestsforgrowersisbasedonfullpaymentinequaltranchesoverthecroprotationperiodandnotthe10-yearrepaymentperiodthatappliestotherestoftheSectorandtheeconomy.Thisreflectstherealityintreefarmingwherereturnoninvestmentisrealizedatharvesting.

ManagementControl

Theallocationofonebonuspointasanincentivetoappointnon-executiveboardmembershasnotbeenappliedintheForestSector.GreaterBEEimpactcanbeobtainedbyusingthisbonuspointasanincentivetosupportahigheroverallownershiptarget.

24

EmploymentEquitytargetsandweightings

ThereisaneedtoensureequitableandsustainablecontractingandemploymentpracticesintheForestSectorthroughtheintroductionofIndustryCodesofGoodConduct.Thisisnecessarytoensurethatnotonlythequantitybutalsothequalityofblackparticipationintheindustryisimproved.CompliancewithIndustryCodesofGoodConductonemploymentpracticeshasbeensetasaminimumrequirementforscoringontheEmploymentEquityelementoftheScorecard.Notethatcontractingpracticeisdealtwithunderthepreferentialprocurementelement.

Preferentialprocurementtargetsandweightings

TheneedforIndustryCodesofGoodConducthasbeenhighlightedinthepreviousparagraph.Three(3)pointshavebeenre-allocatedtopromotecompliancewithIndustryCodesofGoodConductasitrelatestocontractingpracticesforenterprisesthatareengagedinforestrycontractingandcharcoalproductioncontractingandemerginggrowercontractingschemes.ForestenterprisesthatarenotinvolvedinanyofthesecontractingpracticeswillbesubjecttotheGenericScorecardweightingsforthepreferentialprocurementelement.

EnterpriseDevelopmentandSocio-economicDevelopmenttargetsandweightings

a)TheemphasisplacedintheGenericScorecardonpreferentialprocurementisbasedonthenotionofademand-driveneconomy.However,dueashortageofrawmaterialsupply,theforestproductsindustryinSouthAfricaislargelysupply-driven.ShortagesinlogandsawtimbersuppliesenableforestenterprisestoleverageB-BBEEthroughthesaleoftheseproductstoBEEenterprises.Forthisreasonthree(3)ofthefifteen(15)pointshavebeenre-allocatedtosupportthesaleoflogsandsawtimbertoBEE-compliantandblack-ownedenterprises.

b)Three(�)bonuspointshavebeenallocatedforadditionalspend(onebonusforevery0.25%NPATonsector-specificinitiativesinenterprisedevelopmentorsocio-economicdevelopment.ThisisaimedatdirectingB-BBEEinitiativestoaddresssector-specificchallengesfacingtheindustry,inparticular:

oTosupport,encourageandnurtureemergingblackenterprisesthatwillcontributeto:(a)increasedtimbersupply;and(b)beneficiationintheforestryvaluechain.

oToimprovethelivingconditionsandlivelihoodopportunitiesfortheruralpoor,includingForestSectorworkersandtheirfamilies,inforestryareas.Mostforestenterprisesarelocatedinruralareaswherethemajorityofthecountry’spoorlive.Thelong-termgrowthandstabilityintheForestSectorcanonlybesecuredifalignedwithbroad-basedpovertyalleviationandlocaleconomicdevelopment.

6.2.4QualifyingSmallEnterprises

Sector-specificmeasureshavebeenincludedinthisScorecardintandemwithwhatisproposedfortheScorecardformediumandlargeenterprises.TheneedforthisisunderscoredbythefactthattheQSEthresholdhassubstantiallyincreasedandthatamuchgreaterrangeofenterpriseswouldneedtobeadequatelycoveredbythisScorecard.

EmploymentEquity

TheneedtoensureequitableandsustainablecontractingandemploymentpracticesintheForestSectorthroughtheintroductionofIndustryCodesofGoodConduct(refertoinpar.9.2.�)alsoappliestoQSEs.Five(5)ofthetwenty-five(25)pointshavebeenre-allocatedintheScorecardtopromotecompliancewithIndustryCodesofGoodConductonemploymentpractices.Notethat

25

complyingwiththeseCodesislessdemandingformediumandlargeenterprisesandcompliancehasbeensetasaminimumrequirementforscoringontheEmploymentEquityelementoftheirScorecard.

Preferentialprocurementtargetsandweightings

Five(5)ofthetwenty-five(25)pointshavebeenre-allocatedtopromotecompliancewithIndustryCodesofGoodConductasitrelatestoforestrycontractingandcharcoalproductioncontractingandemerginggrowercontractingschemes.ForestenterprisesthatarenotinvolvedinanyofthesecontractingpracticeswillbesubjecttotheGenericScorecardweightingsforthepreferentialprocurementelement.

EnterpriseDevelopmentandSocio-economicDevelopmenttargetsandweightings

a)ShortagesinlogandsawtimbersuppliesenableforestenterprisestoleverageB-BBEEthroughthesaleoftheseproductstoBEEenterprises.Forthisreasonfive(5)ofthetwenty-five25pointshavebeenre-allocatedtosupportthesaleoflogsandsawtimbertoBEE-compliantandblack-ownedenterprises.

b)Aswithmedium/largeenterprises,threebonuspointshavebeenallocatedforadditionalspend(onebonusforevery0.25%NPAT)onsector-specificinitiativesinenterprisedevelopmentorsocio-economicdevelopment.

6.�FurtherdetailsonSkillsDevelopmentStrategy/PlanRefertopar.11.2.1oftheCharter

Keyelementstobeaddressedthroughaskillsdevelopmentstrategy/planfortheForestSectorincludethefollowing:

6.�.1Strengthenthenationalframeworkforskillsdevelopment

Theframeworkforskillsdevelopmentcomprisesofseveralelementsthatarenecessaryfortheoverallsystemtowork.Additionaleffortisneededtoensurethatthefollowingelementsareinplace:

a. Identifyscarce,criticalandcoreskills.Skillsdevelopmentgrantscanbeclaimedfortrainingthatmeetsidentifiedscarceandcriticalskills.ChambersneedtosubmitlistsofscarceandcriticalskillstotheDepartmentofLabourforthesepurposes.SomescarceandcriticalskillsfalloutsidethedirectinfluenceoftheFIETAe.g.1stlinesupervisionandLeadership/Managementdevelopment.ThesewillthereforequalifyasCoreskills.

b.Conductskillsneedsanalysisforeachsub-sector.ThestrategyandprogrammeforreachingScorecardtargetsneedstobebasedonananalysisofexistingskillsandskillsgapsforthespecifiedgroups.

c. DevelopmentofappropriateOutcomesBasedUnitStandards. Sub-sectorStandardGeneratingBodiestocontinuewiththeprocessofdevelopingandfacilitatingtheregistrationofUnitStandards,QualificationsandLearnershipsinaccordancewiththeirneeds.

d.QualificationstomatchtrainingneedsregisteredwithSAQA. RegistrationofUnitStandardsandQualificationsthroughSAQAhasbeenunacceptablyslow,aproblemcommontomostsectors.Theprocessneedstobeaccelerated.WithoutthisregistrationtheDepartmentofLabourcannot

26

registerLearnerships,whileregistrationalsoformsthebasisforthedevelopmentofcreditbearingshortcoursesandskillsprogrammes.

e. SectorwideABETinitiative. ABETisanationalimperative,andthereisaneedforadedicatedandsector-wideapproachtoensureeffectivenessandsustainabilityofsuchaninitiative.TheDepartmentofLabourhascommissionedaninvestigationintotheABETprogrammeandrecommendationsarenowavailable.Thisoffersabasisfordesigningasector-wideinitiativeonABET.

6.�.2Strengthensectorcapacityforskillsdevelopmentdelivery

a. StrengthencapacityofFIETA. Only10%ofSkillsLeviesmaybespentonAdministration.MoreandmoredemandsarebeingmadeonSETAsandthesmallerSETA’s,includingFIETA,arestretchedbeyondcapacity.MeasuresareneededtostrengthenthecapacityofFIETA,toenableittomeetitsstatutoryrequirementsinregisteringlearningprogrammesandtrainingserviceproviders.

b. Implementationmechanismsfortheadditionalskillsdevelopmentspend.Theskillsdevelopmentstrategy/planneedstoidentifyanddeploystreamlinedimplementationmechanismsfortheadditional�%skillsdevelopmentspendprovidedforinthisCharter.ItmustbenotedthatthisneednotbeimplementedthroughtheFIETAinthesamewayasthestatutoryskillsdevelopmentlevy.

c. Expandtraininginfrastructure.Thenetworkoftrainingserviceproviders,inparticularABETserviceproviders,needstobeexpanded.

6.�.�Promoteskillsdevelopmentopportunitiesforyouthandnew entrantsintheForestSector

SpecificmeasuresareneededtoattracttheyouthintotertiarystudiesinforestryandtoensurehigherpassratestoensureaflowofskillednewentrantsintotheSector.

a. Planforthepromotionofforestryascareerofchoice.ItisnecessarytoraisetheprofileoftheForestSectoras“EmployersofChoice”toprocurequalitystudentsandemployeesinthefuture.

b. Planfornewandenhancedbridgingcourses.Currentdropoutrateofstudentsfromsecondarytotertiaryeducationishighduetopoorsecondaryeducation.Bridgingcoursestopreparelearnersfortherequirementsoftertiaryeducationareneededtoreducethedropoutrate.

c. Enhancequalityofsecondaryeducationinmathsandsciences.ThequalityandquantityofMathematicsandPhysicalSciencelearnersatsecondarylevelneedsattention.WithoutqualitylearnersinthesesubjectstheSectorwillnotbeabletotraintherequirednumbersintotechnicalandmanagementfieldsspecifictotheSector.InitiativesinthisregardshouldlinkwiththoseunderASGI-SAandJIPSA.

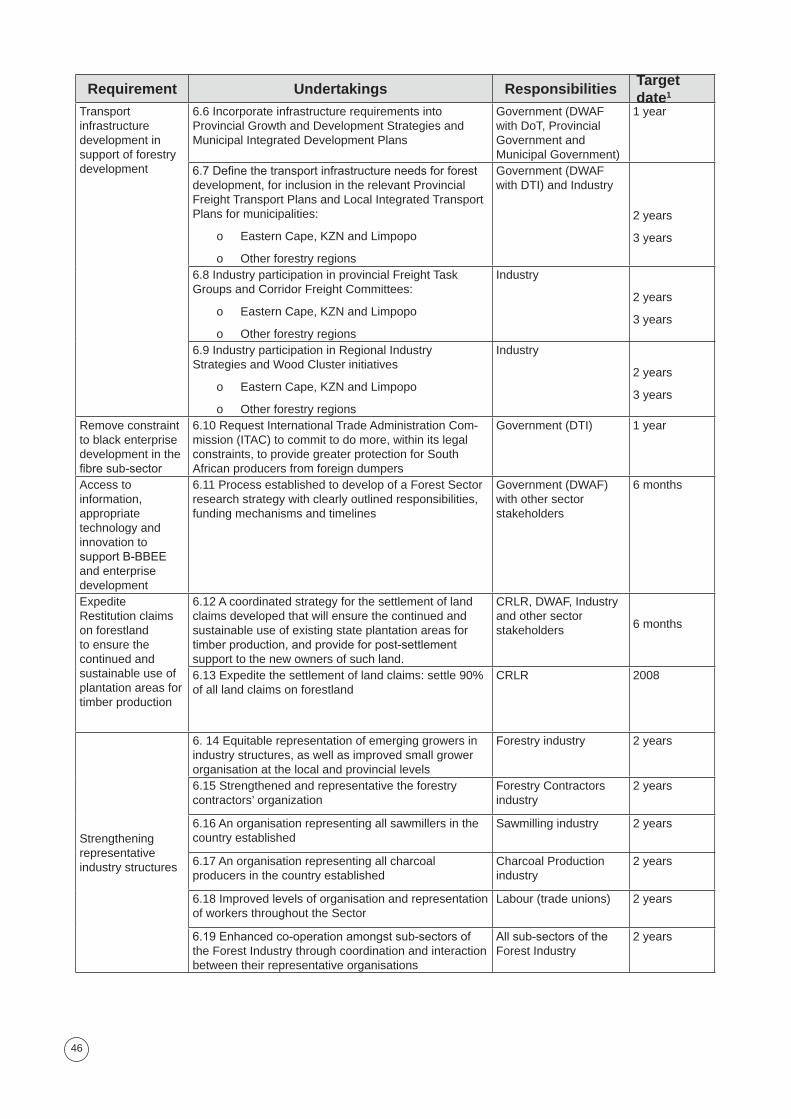

6.4 FurtherdetailsonIndustryCodesofConductonContractingandEmployment

Refertopar.12.2.1oftheCharter.

TheForestCharterSteeringCommitteehaspreparedthefollowingguidelinesforthepreparationoftheIndustryCodesofConductfortheForestSector:

27

6.4.1Codesforforestrycontracting

TheaimoftheseCodesistoensurelonger-termstability,sustainablegrowthandequitablepracticesintheforestrycontractingsub-sector.TheseCodeswillcontrolanddirecttherelationshipbetweencontractingcompaniesandcontractors,andbetweencontractorsandsub-contractors.TheCodeswillprovideforlargerandlonger-termcontractsenablingcontractorstoimprovemarginsandinvestintheirbusinessesandstaff.Itwillalsoprovidefortransparentandaccessibletenderingsystemsandfairpricingthatwillsupportgoodgovernanceandfairlabourpractices.ThefollowingelementswillbedealtwithintheseCodes:

a. Contractualarrangements

• Theforestryindustrywilldevelopandfollowstandard(model)contractsthatspecifycontractterms,paymenttermsandcontractduration,risksharing,terminationandconflictresolution.

• ForestryenterpriseswillensurethatcontractconditionsenableandspecifycompliancewiththeCodesonemploymentpracticesintheForestSectorandthatmeasuresarestipulatedtomonitorandenforcecompliancewiththesecodes.

• ForestryenterpriseswillensurethatcontractconditionsenableandspecifycompliancewiththeCodesonhealthandsafetystandardsforforestrycontractworkandthatmeasuresarestipulatedtomonitorandenforcecompliancewiththesecodes.

• Forestryenterpriseswillsecureacontractingenvironmentthatisconducivetosuccessfulmeetingofcontractconditions(e.g.maintainingforestryroadstoreasonablestandard).

• Contractingpartieswillmaintainconfidentialityofcontractsandcontractterms.

b. Contractnegotiations

• Associationsrepresentinggrowersandforestrycontractorswillprovideaccesstoindustrydevelopedbestoperatingpracticesforstandardforestryoperations.Theseguidelinesareaimedatenablingcontractorstodeterminetheirmarketrelatedcostsintenderingforcontracts.

• Forestryenterpriseswillensurethatcontractorrateadequatelyreflectminimumstatutorylabourcostsandotherreasonableexpensestobeincurredinperformingtheworkandthatcontractorratesarenotestablishedattheexpenseoffairlabourandsustainablebusinesspractices.

• Contractingpartieswillprovideaccesstoperformancestandardsandunitpaymentinformationbyforestryenterprises,contractorsandworkers.

c. Tenderingandprocurement

• Forestryenterpriseswillestablishopen,transparentandaccessibletenderingandprocurementsystem.

• Forestryenterpriseswillincludeclearselectionandappraisalcriteriaintenderdocuments.

• Forestryenterpriseswill,whereverpossible,givepreferencetolocaloperatorsandcommunities.

• Theforestrycontractorsassociationwillestablishadatabaseofavailablecontractors(indicatingkeyskills).

28

d. Mediationandarbitration

• Associationsrepresentinggrowersandforestrycontractorswillformulateandimplementguidelinesforarbitrationandmediationintheforestrycontractingsector.

• Associationsrepresentinggrowersandforestrycontractorswillestablishanindependentdisputeresolutionmechanismand/orForestryContractors’ombudsman.

e. Safety,healthandenvironment

• Theforestrycontractorsassociationwillprovideaccesstobest-practicestandardsandworkmethodsforkeycontractingoperationsandequipment.Contractorswillcomplywiththesestandards.

• Theforestrycontractorsassociationwillprovideaccesstominimumacceptablestandardsforprovidingaccesstohousingfacilities(includingtransporttoandfromwork)andbasicfoodstuffforworkerswhohavetoliveon-site.Contractorswillcomplywiththesestandards.

• CertificationagencieswillensureadherencetocertificationrequirementsandimplementationofPrinciples,Criteria,IndicatorsandStandardsofSustainableForestManagement.

f. Industrygovernance

• AssociationsrepresentinggrowersandforestrycontractorswillsecureagreementthroughaMemorandumofUnderstanding(MOU)tojointlystabiliseandgrowtheforestsectorcontractingindustry.

• Thecapacityoftheforestrycontractorsassociationtoprovideadviceandsupporttosmallscalecontractorsoncontractnegotiations,labourlawsandallotheraspectsrelatingtotheeffectiveimplementationoftheCodesforestrycontractorswillbestrengthened.

• Theforestrycontractorsassociationwillimplementasystemofmembershipaccreditationandgradingofallcontractors.

g. Supportandtraining

• Theforestrycontractorsassociationwillestablishguidelinesformentorshipsupportandtraining.

• Forestryenterpriseswillmaintaincontractingconditionsthatfacilitateaccesstofundingsources.

6.4.2Codesforemergingforestgrowerschemes(EFGS)

ThepromotionofEmergingForestGrowerSchemesbycompaniesandcooperativesisanimportantmeanstosupportB-BBEEinforestry.Thereisaneedtoensurethatgoodpracticeisappliedinimplementingtheseschemesthatsupporttheaims,principlesandtargetssetoutintheForestSectorTransformationCharter.TheseCodeswillcontrolanddirectcontractswithemerginggrowersincompany-affiliatedschemes.TheCodeswillprovidetransparencyinthecostingofsupportservicesandmarketrelatedpricingarrangementsfortimberthatwillsupportsustainablebusinesspractices,goodgovernanceandfairlabourpractices.ThefollowingelementswillbedealtwithintheseCodes:

29

a. Fundingandcontractualarrangements

• TheorganizationpromotingEFGSmayinclude,amongthecontractingobligationsofthegrower,anundertakingbindingthegrowerto,inthefirstinstance,selltimberoranyotherproducttotheorganizationpromotingEFGS.Forestenterprisesnotpartytotheagreementwillrespectsucharrangements.

• Thepricepaidforthetimberorotherforestproductsmustbeafairmarketprice.Intheeventofapricedisputethematterwillbereferredtoanexpert.

• Ifrequiredbyanexternalfundingagency,theorganizationpromotingEFGSwillagreetoaminimumguaranteedpriceforthetimberandanyotherproductsatmaturityofthedevelopment.

• TheorganizationpromotingEFGScannotuse“statefundingagency’s”capitalaspartoftheirEnterpriseDevelopmentcosts.

• IftheorganizationpromotingEFGSguaranteesrepaymentoftheloansonbehalfoftheEFGS,thatportionnotrepaid–i.e.defaultby‘EFGS’canbeaddedtoEnterpriseDevelopmentcosts.

b. Transparency

•Allaccumulatedcoststobeincurredtodeterminethesellingpriceforthetimberorotherforestproductsmustbemadeknowninwritingandbeproperlyexplainedtotheemerginggrower.

•IntheprocessofimplementationoftheEFGS,theremustbetotaltransparencywithregardtothetermsofloansandanyotheraspectofthefinancialagreement.Effectivemeasurestoensureclearunderstandingamongstpartiestofinancialagreementoftheconditionsitcontainsandtheirimplications,needtobespelledoutintheEFGSCodeofConduct.

•Atharvest,afullandclearstatementofpricesandproductioncostsmustbecommunicatedtoallparties.

c. Plantationinsurance

• DuringthedevelopmentoftheEGFSandoverthefullrotation,the“promoter”mustensureadequateplantationinsurancecoverattheoptionoftheemerginggrowertomeettheemerginggrowers’plantationexpectationvaluethroughouttherotation.Ifthefundingagenciesrequireinsuranceasaconditionoffunding,theoptionwillfallaway,andinsurancebecomescompulsory.

6.4.�Codesforcharcoalcontracting

TheaimoftheseCodesistoensurelonger-termstability,sustainablegrowthandequitablecontractingpracticesinthecharcoalsub-sector.TheseCodeswillcontrolanddirecttherelationshipbetweensmallblackcharcoalproducersandthebrandnameproducersandindustrialusersofcharcoal.TheCodeswillprovideforjointventuresandpartnershipsbetweensmallscalesuppliersandlargescalebuyersofcharcoalandafair,transparentandstablepricingsystemthatwillsupportsustainablebusinesspractices,goodgovernanceandfairlabourpractices.ThefollowingelementswillbedealtwithintheseCodes:

a. JointVenturesandPartnerships

• Thecharcoalindustrywillprovideforjointventureandpartnershiparrangementsthatwillencouragetheestablishmentofviablecharcoalproductionenterprises.

�0

• Contracttermsandconditionsforjointventuresandpartnershipswillresultinthetransferofskillsandproductivecapacitytocharcoalproductionenterprises.

• Contracttermsandconditionsforjointventuresandpartnershipswillleadtotheestablishmentofindependentoperators(withoutlimitationsastoitsclientsandcustomers)withinadefinedperiodoftime.

b. Contractualarrangements

• Thecharcoalindustrywilldevelopandfollowstandard(model)contractsforprocurementfromsmallcharcoalproducersthatspecifycontractterms(suchasthesupplyofrawmaterialandequipment,transportofcharcoal,siteestablishmentandintellectualpropriety),paymenttermsandcontractduration,risksharing,terminationandconflictresolution.

• Thecharcoalindustryassociationwillprovideaccesstoindustrydevelopedbestoperatingpracticesforcharcoalproductionoperations.Theseguidelinesareaimedatenablingcharcoalproducerstodeterminetheirmarketrelatedcostsintenderingforcontracts.

• Largescalebuyersofcharcoalwillensurethatcontractorratesadequatelyreflectminimumstatutorylabourcostsandotherreasonableexpensestobeincurredinperformingtheworkandthatcontractorratesarenotestablishedattheexpenseoffairlabourandsustainablebusinesspractices.

• LargescalebuyersofcharcoalwillensurethatcontractconditionsenableandspecifycompliancewiththeCodesonemploymentpracticesintheForestSectorandthatmeasuresarestipulatedtomonitorandenforcecompliancewiththesecodes.

• LargescalebuyersofcharcoalwillensurethatcontractconditionsenableandspecifycompliancewiththeCodesonenvironmental,healthandsafetystandardsforcharcoalproductionandthatmeasuresarestipulatedtomonitorandenforcecompliancewiththeseCodes.

• Largescalebuyersofcharcoalwillmaintaincontractingconditionsthatfacilitateaccesstocapitalinvestmentincharcoalproduction.

c.Safety,healthandenvironment

• Thecharcoalindustryassociationwillprovideaccesstobest-practicestandardsandworkmethodstocomplywithsafetyhealthandenvironmentalstandardsforcharcoalproduction.Charcoalproducerswillcomplywiththesestandards.

• Thecharcoalindustryassociationwillprovideaccesstominimumacceptablestandardsinprovidingaccesstohousingfacilities(includingtransporttoandfromwork)andbasicfoodstuffforworkerswhohavetoliveon-site.Charcoalproducerswillcomplywiththesestandards.

• CertificationagencieswillensureadherencetocertificationrequirementsandimplementationofPrinciples,Criteria,IndicatorsandStandardsofSustainableForestManagement.

d. Industrygovernance

• ThecharcoalindustryassociationwillbestrengthenedwithkeycapabilitiesrelatingtotheeffectiveimplementationoftheCodesforestrycontractors.

• Thecharcoalindustryassociationwillimplementasystemofmembershipaccreditationandgradingofallmembers.

�1

6.4.4Codesforemploymentpractices:

TheaimoftheseCodesistoensureequitableemploymentpracticesintheForestSector.TheseCodeswillgivepracticaleffectandweighttofairlabourpracticesasprovidedforundertheBasicConditionsofEmploymentAct,1997,andotherlabourlegislationasitappliestoemployees,includingcontractworkers.ThefollowingelementswillbedealtwithintheseCodes:

a. Contractsandwages

• Employerswillensurewrittenemploymentcontractsforallworkers,includingcontractorworkers,thatcomplyingwithallrelevantlabourlegislationandregulations.

• Employerswillinformworkersoftheiremploymentrights,translatetheBasicConditionsofEmploymentActandtheSectoralDeterminationagreementintolanguagesunderstoodbytheworkforceanddisplaythesedocuments.

• Employerswillclearlyinformworkersofthetasksthatareexpectedfromthem.

• Employerswilladheretominimumwagestipulations.

b.LabourRelationsAct

• Employerswillrespectandpromotetherightofallworkerstojoinorganisationsoftheirchoiceandtocreateanenablingenvironmentfortheestablishmentandgrowthofworkerorganisations.

• EmployerswillinformworkersoftheirrightundertheLabourRelationsAct.

c. OccupationalInjuriesanddiseases

• EmployerswillregisterwiththeCompensationFundsothattheirworkerscanclaimcompensationforoccupationalinjuriesanddiseases.

• EmployerswillinformworkersoftheirrightundertheCompensationforOccupationalInjuriesandDiseasesAct.

d. UnemploymentInsurance

• EmployerswillregisterwiththeUnemploymentInsuranceFund(UIF).

• EmployerswillinformworkersoftheirrightundertheUnemploymentInsuranceAct.

e. OccupationalHealthandSafety

• EmployerswillensurecompliancewithOccupationalSafetyandHealthAct(OSHA),e.g.basicrequirementsregardingprotectiveclothing,noiseprotection,andquickaccesstoemergencytreatment.

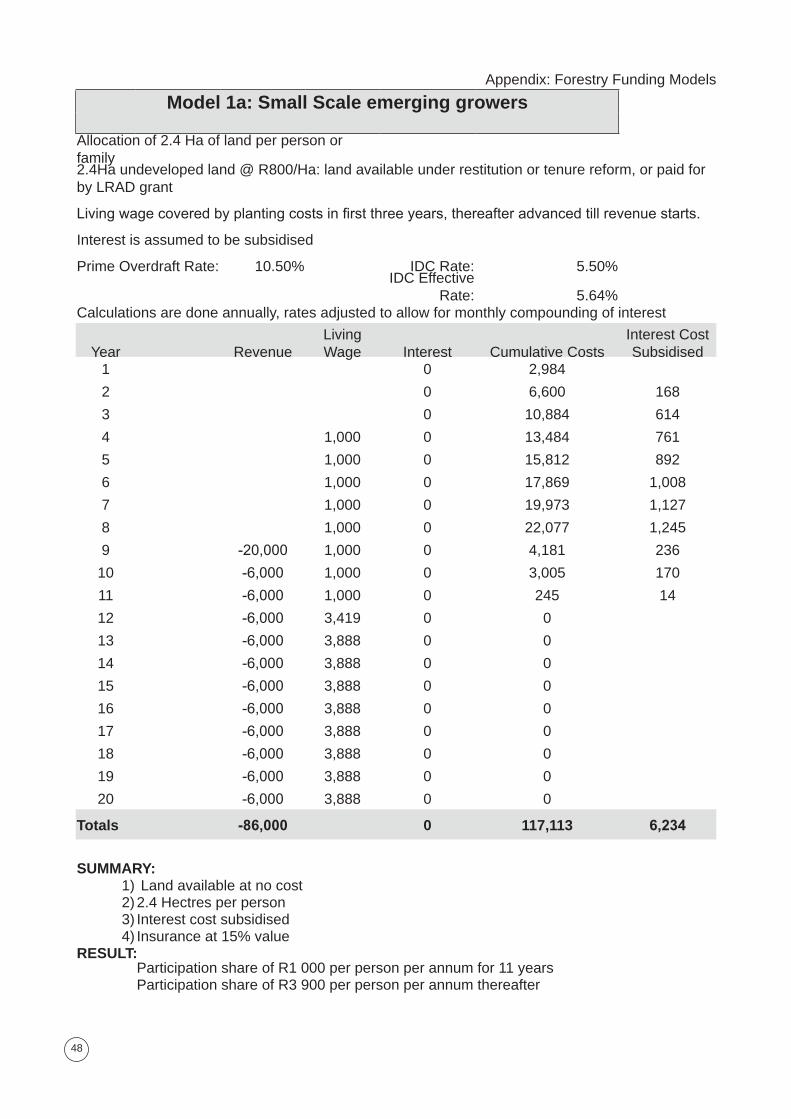

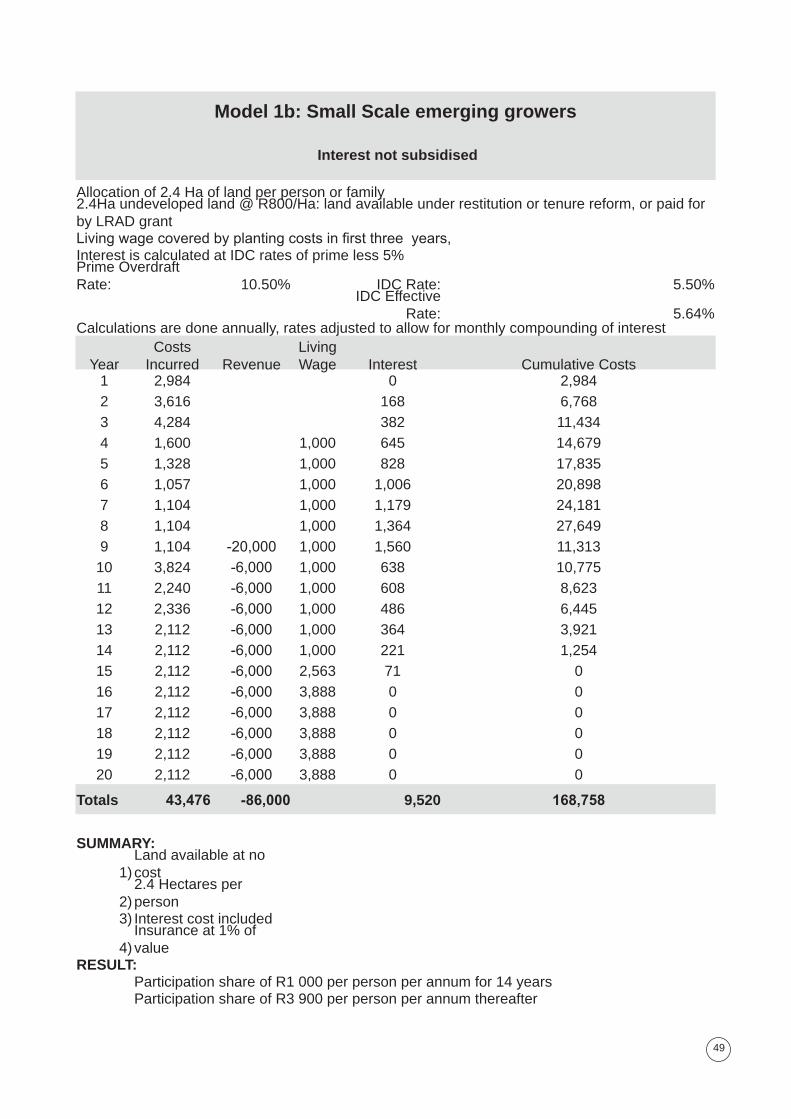

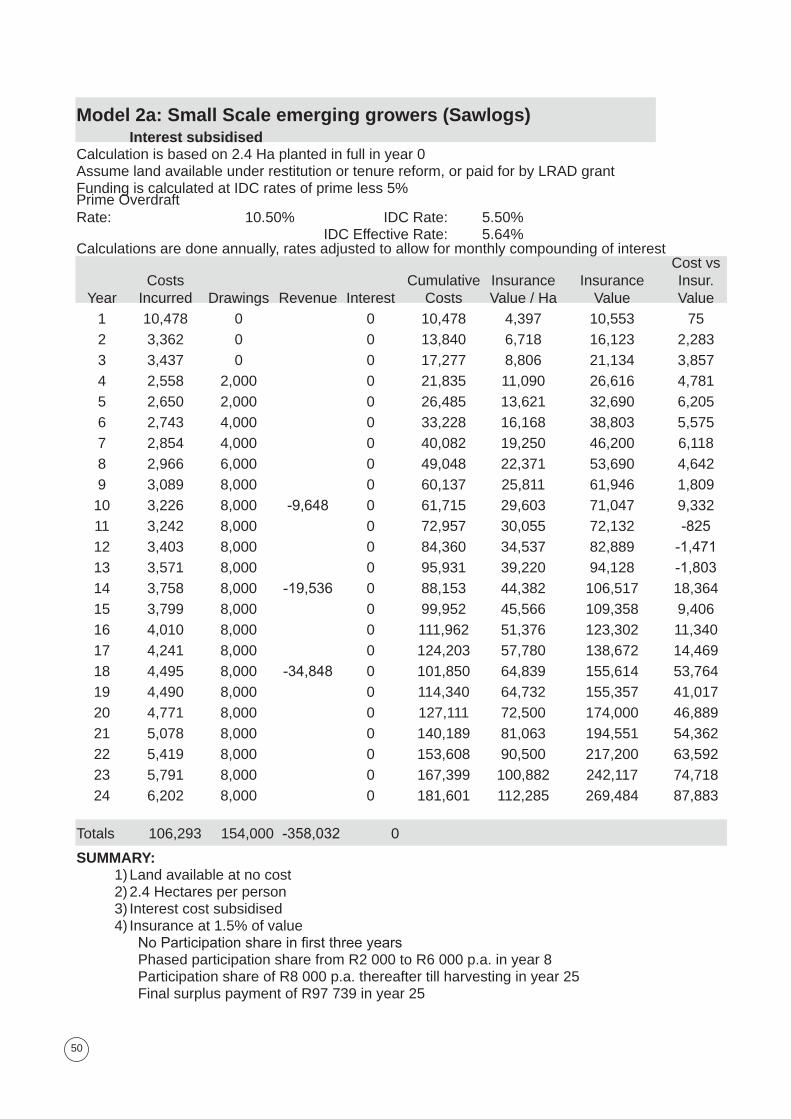

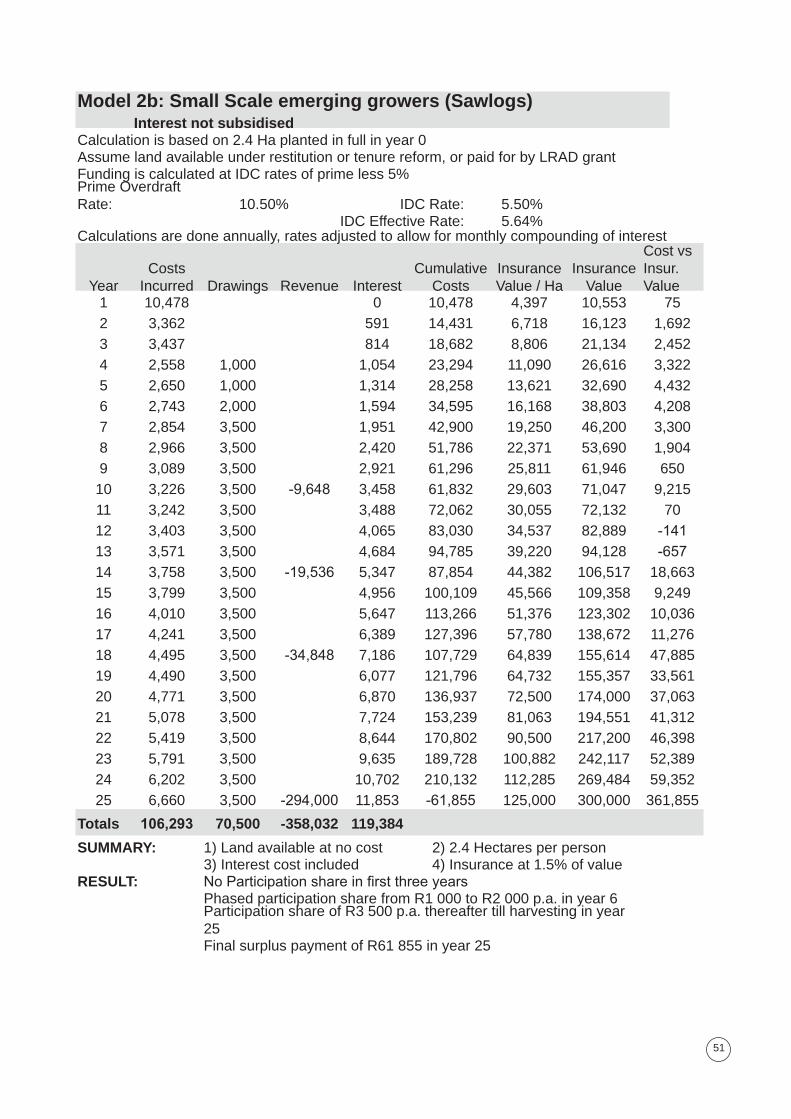

6.5 Motivationtofundand/orsubsidisetheinterestburdentodevelopemergingforestryenterprises

Refertopar.8.2.1and1�.2.1(e)oftheCharter.

Thecost-of-capitalforemerginggrowerenterprisesisoftenprohibitivetotheenterprisebecause

�2

ofthelongcroprotation(oftenexceeding10years),andhencedeferredrevenue.Subsidisingthecost-of-capitalreducesthecashflowobligationoftheemerginggrowerenterpriseresultingfromcapitalloans.

Anumberofmodelshavebeenanalysed(refertoAppendix:ForestryFundingModels)todeterminetheeffectofinterestcostsonafforestationschemesandB-BBEEequitytransfersintheForestrySector.Alloftheseshowthat,ifinterestcostsaresubsidised,themodelsbecomesubstantiallymoreviableandarelikelytoimprovethechancesofsuccessofBroad-basedBlackEmpowerment.

6.5.1Rationaleforinterestsubsidisationforemerginggrowerschemes

a. Thesmallgrowerinitiativeisintendedtoprovideanincometopoorerpeople.Bytheirnature,povertyalleviationschemesaretargetedatpeoplewhodonothaveresourcestofundtheirlivingexpensesforthelengthoftimetimbertakestogrowtomaturity.Interestsubsidiesarerequiredtoimprovetheprofitabilityandcash-flowpositionforblackemerginggrowers.

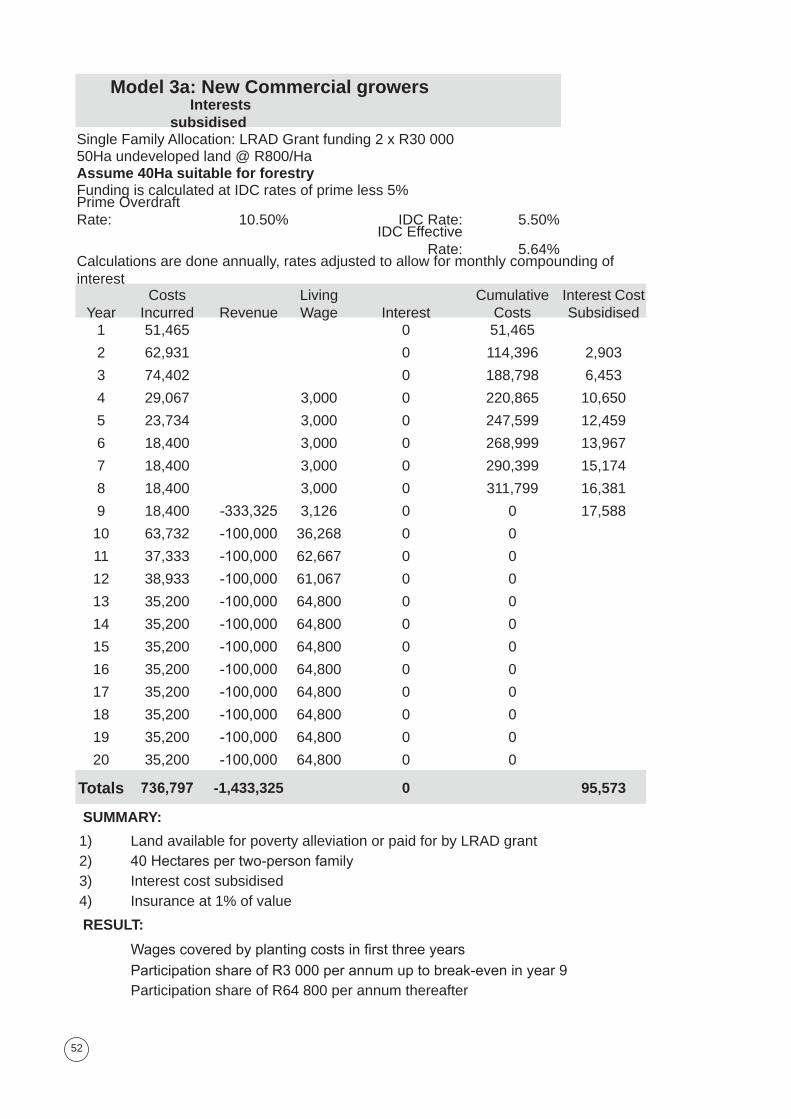

b. Refertoappendedmodel1a(interestsubsidised)andmodel1b(interestnotsubsidised)forshort-rotationprojects(GumandWattle).Ifinterestisnotsubsidisedforemerginggrowers(2.4haperentity),suchschemesonlybecomeprofitableinyear16.Thismeansthatthecapitalandinterestrepaymentsareextendedto6yearsaftertherotationperiod.Itisunrealistictoexpectpeopletowaitthislongbeforethefullbenefitintheformofalivingwageispayable.

c. Refertoappendedmodel2a(interestsubsidised)andmodel2b(interestnotsubsidised)forlong-rotationprojects(sawlogs).Thesemodelsarebasedona25-yearrotation;400cubicmetresperhectareatclearfelling;anoverallpriceofR325-00percubicmetrestandingatmaturityorR125000netperhectarestanding;incomefromthinningscoversthecostofpruningandpartofannualmaintenance.Atthese(current)sawlogpricesthisrepresentsthebestpovertyalleviationmodel,butrequiresfundingat2.5timesthatofshortrotationcrop.

Withoutanyinterestsubsidybeingapplied(model2b)thisallowsdrawingsofR�500perannum(per2.4ha)fromyearfouronwards,withanadditionalR61855profitonclearfelling.Withinterestsubsidybeingapplied(model2a),thedrawingscanbeincreasedtoR6000perannum,withanadditionalR97739profitonclearfelling.Thismodelcouldworkwithoutinterestsubsidisation,butwiththecomplexitiesandriskassociatedwithraisingsuchalargeinvestmentoveralongperiod,wouldgreatlybenefitfromsomelevelofinterestsubsidisation.

d. Foremergingcommercialgrowers(40haperentity),theinterestratesubsidydoesnothaveasdramaticaneffectbutstillreducesthetimeperiodtobreakeven,andbringsthisclosertoafullrotation.Theeffectontheparticipantissignificantinthatitbringsthefullearningspotentialseveralyearsearlier.

Refertoappendedmodel�a(interestsubsidised)comparedtomodel�b(interestnotsubsidised),wherethebreak-evenincreasesfrom9yearsto12years.

e. Iftheinterestissubsidizeditwillreducetheriskcarriedbythefinancingbody,andwillpromotemoreoftheschemesthanwouldotherwisehavebeenthecase.

f. Finally,theneedforinterestsubsidizationisdemonstratedbythefactthatpresentout-growerschemesincludesubsidisationoftheinterestfactor.Theforestindustryhasacceptedtheneedbothinwordandactionforinterestsubsidizationtoensurethatemergingforestgrowerschemessucceed.

��

6.5.2Rationaleforinterestsubsidisationforemergingforestgrower schemes:

Existingsmallforestenterprisesintheformofacompanyortrustarenotlargeenoughtoaccessfavourablefundinginthesamemanneraslargegrowers(Corporates).Inaddition,theydonothavethemeanstoself-fundB-BBEEinitiativesanddonothavetheresourcestocarrytheinterestloadonloansovertherotation.TheconsequenceoftheseshortcomingsisthatsuchenterpriseswillbeforcedtoseekeliteBEEpartnerswhoarecapableofcarryingthecostoftheinvestment.ThishastheeffectofunderminingtheGovernment’sobjectiveofensuringthatownershiptransferisbroad-based.

Twomodelsofownershiptransferwereconsidered:

a. Outrightpurchaseof25%ofequityinenterprise

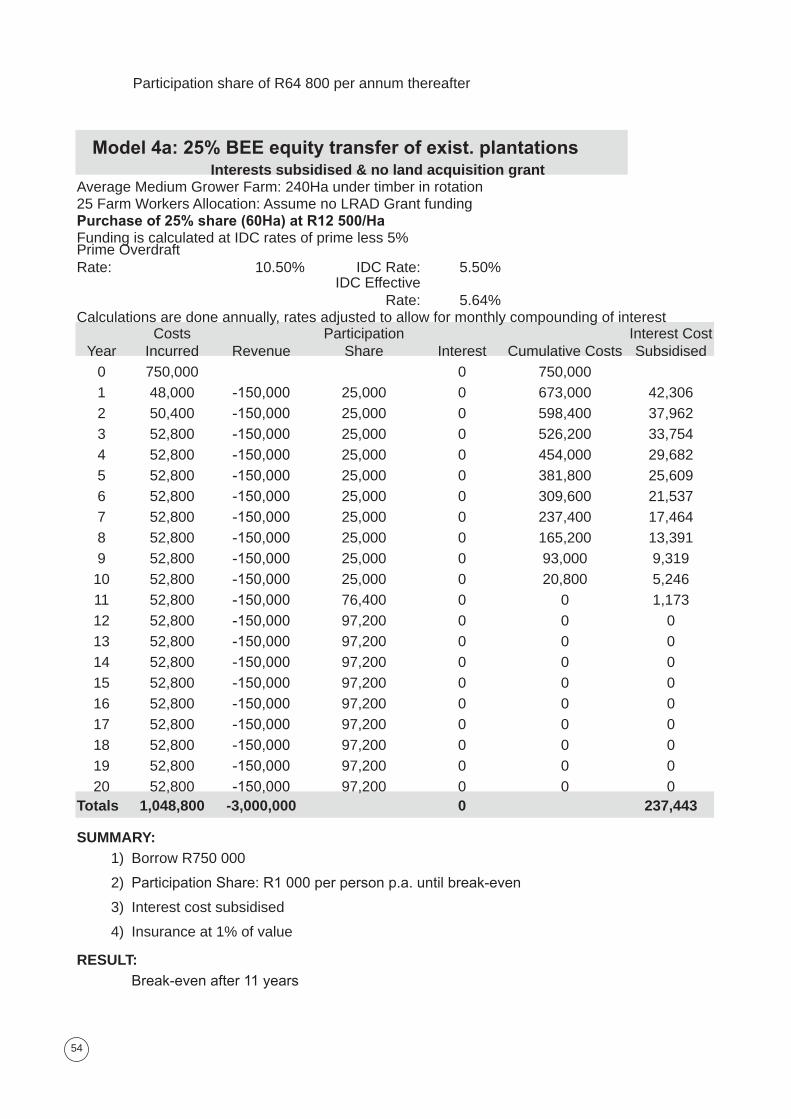

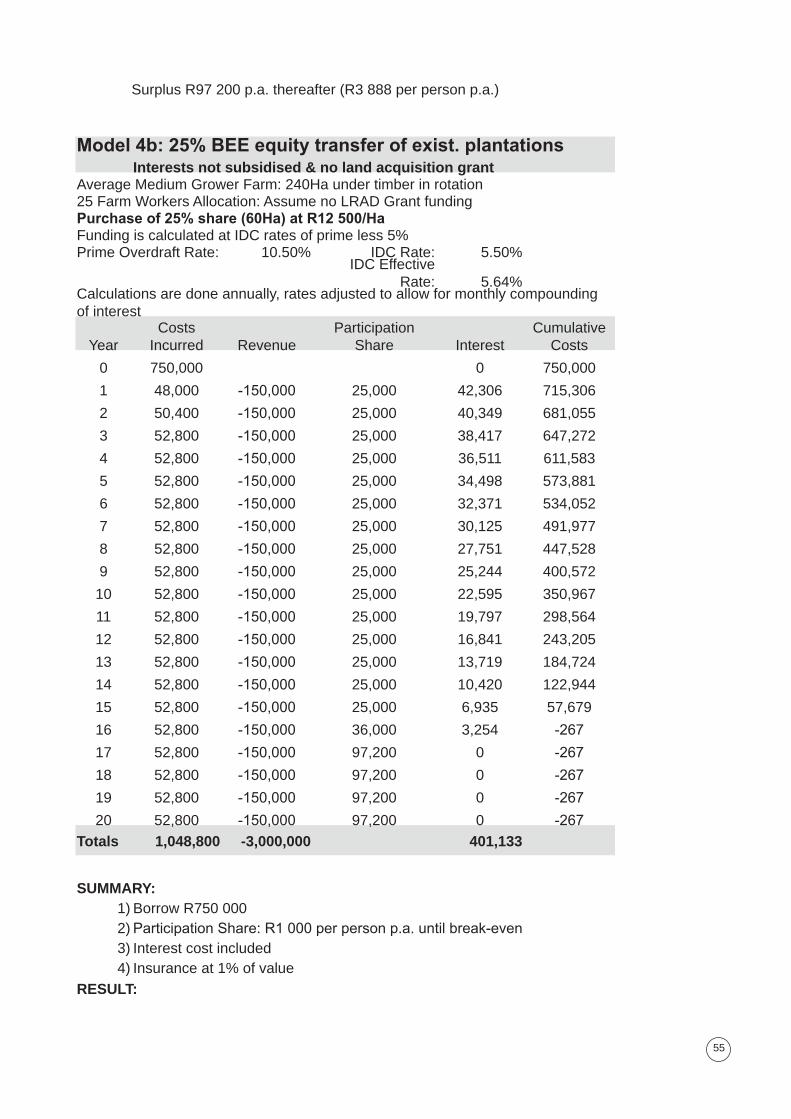

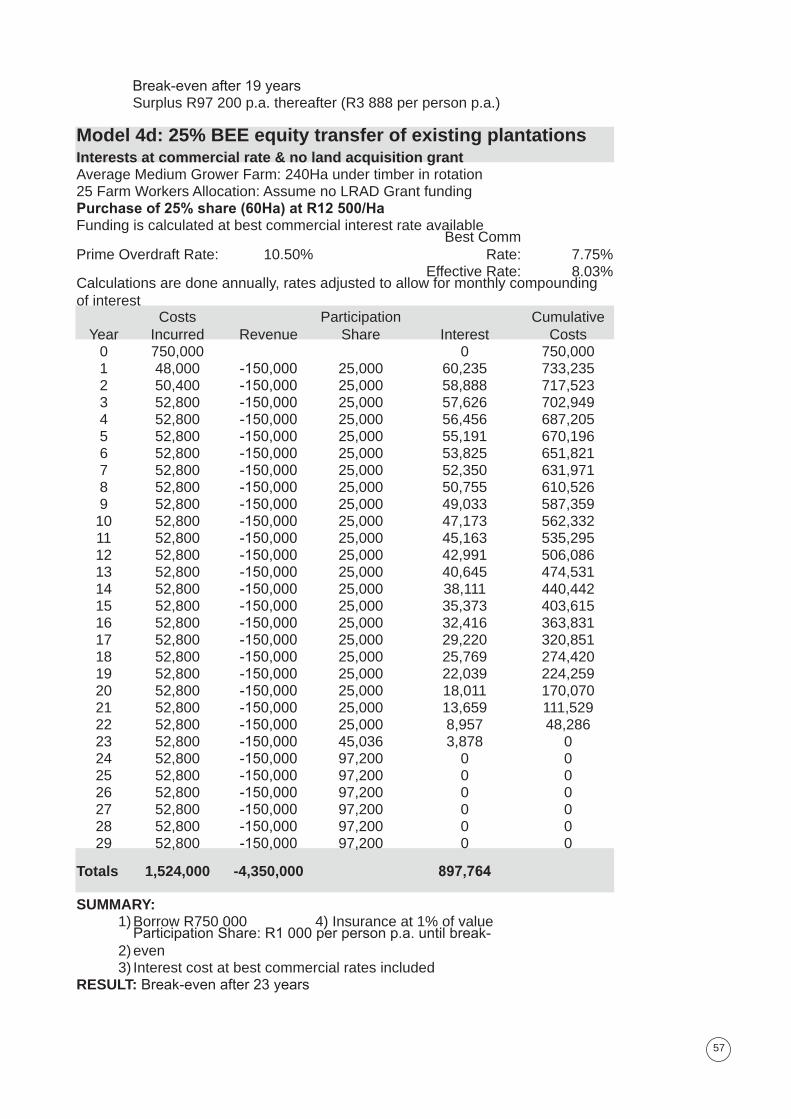

• Theappendedmodel4a(interestsubsidised)andmodel4b(interestnotsubsidised)showthatthebreak-evenincreasesfrom11yearsto16yearsifinterestisnotsubsidised.

• Theimplicationofthisisthatthe25farmworkers,whoareearningaminimalR1000perannumeachforthefirsttenyears,wouldnowearnR1000eachfor15years,whichstretchestherepaymentofcapitalbeyondtherotationage.

• TheabovetwomodelswerebasedontheassumptionthattheIDCPro-Jobschemeat5%belowprimewouldbeapplicableor,failingthat,asimilarschemeatthesameratewouldbeapplicable.

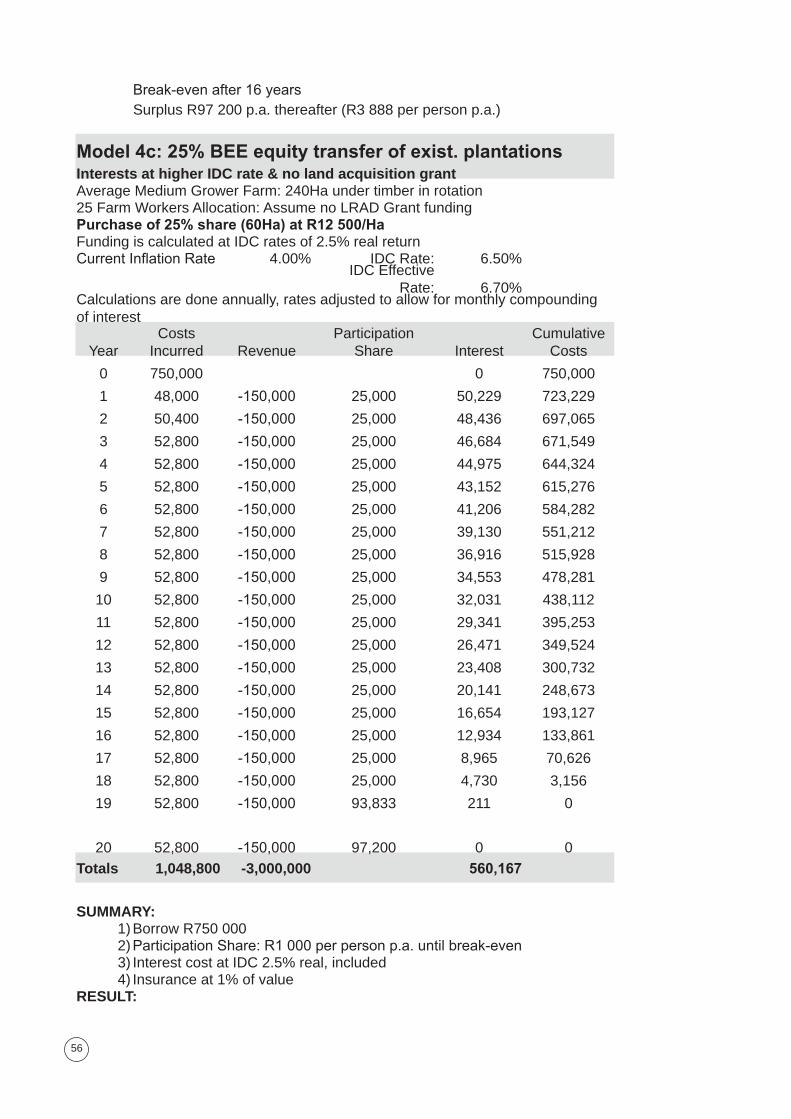

• Atpresent,however,theonlyfundingforthistypeofprojectfromtheIDCistheProForestryschemeatarealrateofreturnof2.5%.WiththecurrentlevelofCPI,thistranslatestoaneffective6.5%interest.Thebreak-evenfortheProForestryschemewouldbeinyear19(model4c)comparedtobreak-eveninyear11withinterestsubsidy(model4a).

• IfIDCfundingisnotavailable,thebestcommercialrateavailableis2,75%belowprimeandatthisinterest(model4d),break-evenextendsto24years,morethantworotations.

• Fromtheaboveitisclearthatwithoutinterestsubsidisation,theB-BBEE25%shareownershipmodelcannotwork.

b. PhasedtransferofB-BBEE25%participationinasmallcompanyortrustoveronerotation(10years)

Ananalysiswascarriedoutusingthismodel,andwasfoundtobecompletelyunworkableevenwiththesubsidisationofinterest.Thismodelisthusnotdiscussedfurther.

6.6 Motivationforseedfundingtodevelopfireinsuranceschemesforemergingforestryenterprises

Refertopar.1�.2.1(e)oftheCharter.

Thereisatpresenteffectiveplantationfireinsuranceavailable,whichiscurrentlyprovidingcoverforapproximately200,000hectaresoftimber.However,thereisaneedtoprovideseedcapitalforthedevelopmentofafireinsuranceschemeforemerginggrowers,tosupport10000haofafforestationannually,overtenyears.Theseedcapitalisrequiredtoreducetheinsurancepremium,requiredtocoverexpectedannualandcatastrophiclosses,toamoreaffordablelevel

�4

fortheemerginggrowersector.Growerswillcollectivelypooltheirrisk.Theseedmoneywillberequiredduringthefirst9years,whereafterthepoolwillbebigenoughtosustainthesebeneficialpremiumlevels.Forsuchaschemetobesuccessful,pre-planningandfireriskmanagementareessential.Pre-planningentailstheidentification,carefulconsiderationandmitigationoffirerisksbeforethetreesareevenplanted.Furthermore,thereisaneedforongoingfireriskmanagementafterthetreeshavebeenplanted.Pre-planningandfireriskmanagementarevitaltoensuretheviabilityoftheafforestationprojectandtoaccrueunderwritingprofitsforthebenefitoftheemerginggrowers.

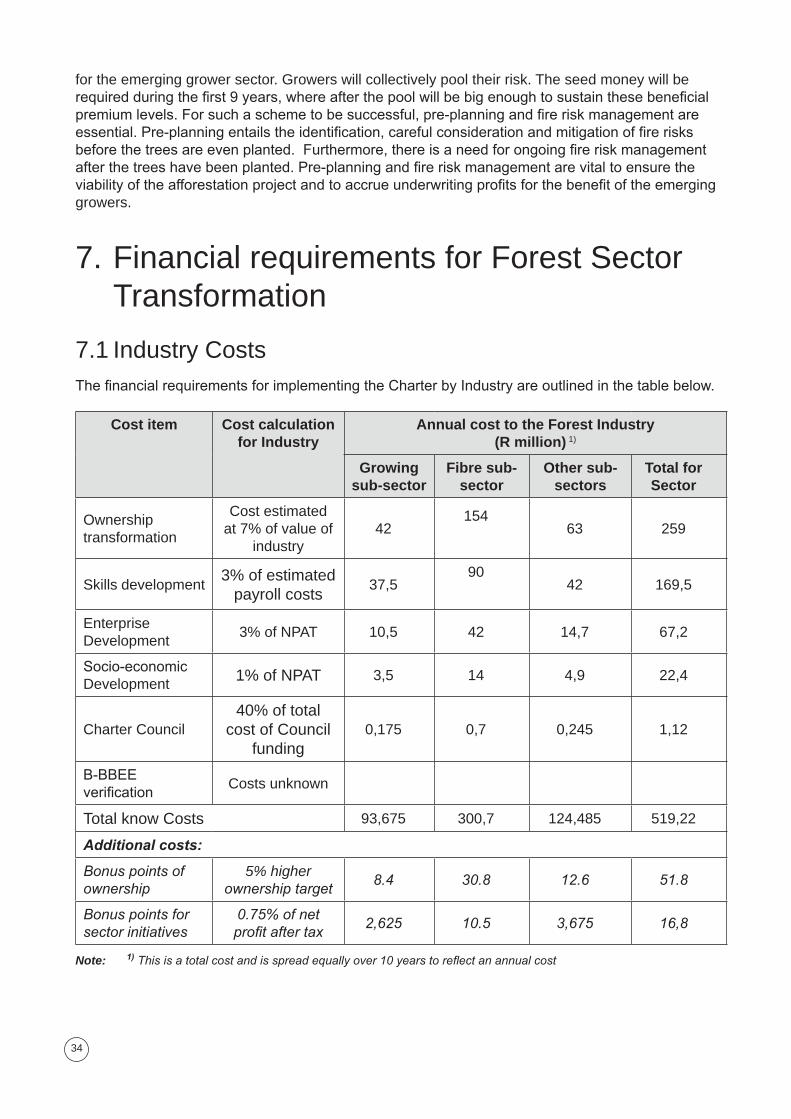

7.FinancialrequirementsforForestSectorTransformation

7.1IndustryCostsThefinancialrequirementsforimplementingtheCharterbyIndustryareoutlinedinthetablebelow.

Cost item Cost calculation for Industry

Annual cost to the Forest Industry (R million)1)

Growing sub-sector

Fibre sub-sector

Other sub-sectors

Total for Sector

Ownershiptransformation

Costestimatedat7%ofvalueof

industry42

1546� 259

Skillsdevelopment�%ofestimated

payrollcosts�7,5

9042 169,5

EnterpriseDevelopment

�%ofNPAT 10,5 42 14,7 67,2

Socio-economicDevelopment

1%ofNPAT �,5 14 4,9 22,4

CharterCouncil40%oftotal

costofCouncilfunding

0,175 0,7 0,245 1,12

B-BBEEverification

Costsunknown

TotalknowCosts 9�,675 �00,7 124,485 519,22

Additional costs:

Bonus points of ownership

5% higher ownership target

8.4 30.8 12.6 51.8

Bonus points for sector initiatives

0.75% of net profit after tax

2,625 10.5 3,675 16,8

Note: 1) This is a total cost and is spread equally over 10 years to reflect an annual cost

�5

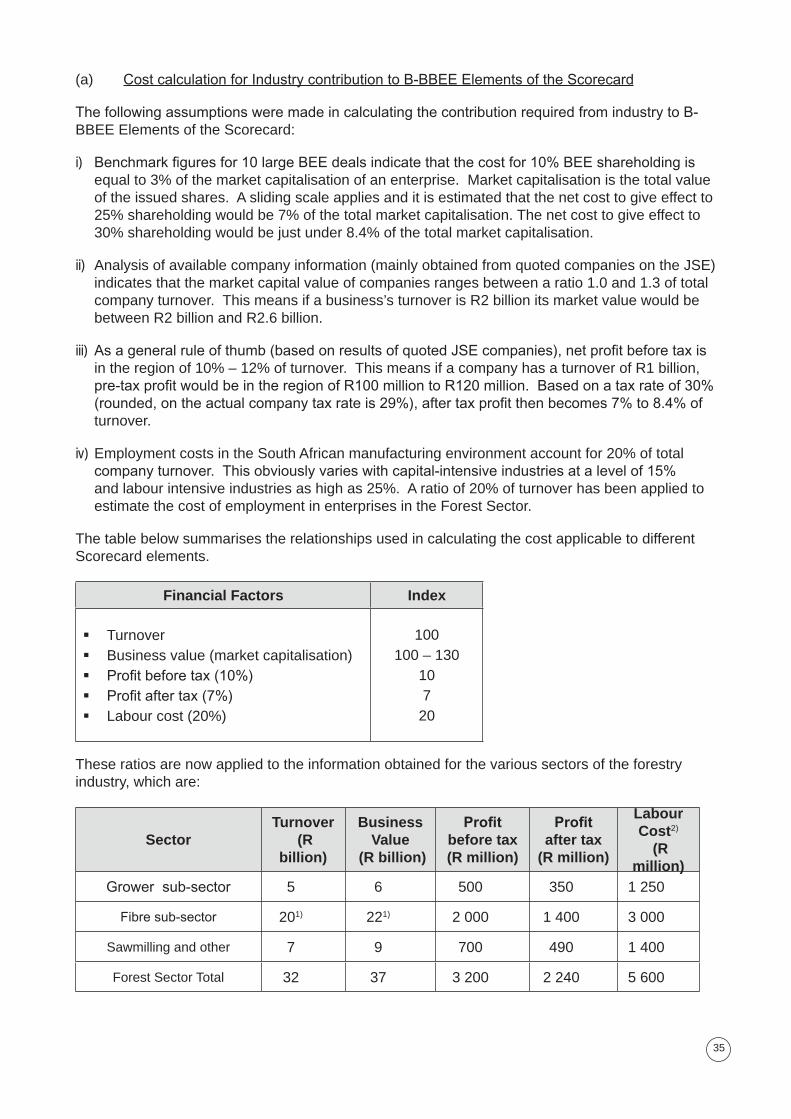

(a) CostcalculationforIndustrycontributiontoB-BBEEElementsoftheScorecard

ThefollowingassumptionsweremadeincalculatingthecontributionrequiredfromindustrytoB-BBEEElementsoftheScorecard:

i) Benchmarkfiguresfor10largeBEEdealsindicatethatthecostfor10%BEEshareholdingisequalto�%ofthemarketcapitalisationofanenterprise.Marketcapitalisationisthetotalvalueoftheissuedshares.Aslidingscaleappliesanditisestimatedthatthenetcosttogiveeffectto25%shareholdingwouldbe7%ofthetotalmarketcapitalisation.Thenetcosttogiveeffectto�0%shareholdingwouldbejustunder8.4%ofthetotalmarketcapitalisation.

ii) Analysisofavailablecompanyinformation(mainlyobtainedfromquotedcompaniesontheJSE)indicatesthatthemarketcapitalvalueofcompaniesrangesbetweenaratio1.0and1.�oftotalcompanyturnover.Thismeansifabusiness’sturnoverisR2billionitsmarketvaluewouldbebetweenR2billionandR2.6billion.

iii) Asageneralruleofthumb(basedonresultsofquotedJSEcompanies),netprofitbeforetaxisintheregionof10%–12%ofturnover.ThismeansifacompanyhasaturnoverofR1billion,pre-taxprofitwouldbeintheregionofR100milliontoR120million.Basedonataxrateof30%(rounded,ontheactualcompanytaxrateis29%),aftertaxprofitthenbecomes7%to8.4%ofturnover.

iv) EmploymentcostsintheSouthAfricanmanufacturingenvironmentaccountfor20%oftotalcompanyturnover.Thisobviouslyvarieswithcapital-intensiveindustriesatalevelof15%andlabourintensiveindustriesashighas25%.Aratioof20%ofturnoverhasbeenappliedtoestimatethecostofemploymentinenterprisesintheForestSector.

ThetablebelowsummarisestherelationshipsusedincalculatingthecostapplicabletodifferentScorecardelements.

Financial Factors Index

ßTurnoverßBusinessvalue(marketcapitalisation)ßProfitbeforetax(10%)ßProfitaftertax(7%)ß Labourcost(20%)

100100–1�0

107

20

Theseratiosarenowappliedtotheinformationobtainedforthevarioussectorsoftheforestryindustry,whichare:

SectorTurnover

(R billion)

Business Value

(R billion)

Profit before tax (R million)

Profit after tax

(R million)

Labour Cost2)

(R million)

Growersub-sector 5 6 500 �50 1250

Fibresub-sector 201) 221) 2000 1400 �000

Sawmillingandother 7 9 700 490 1400

ForestSectorTotal �2 �7 �200 2240 5600

�6

Notes:1) LHAestimates 2) Differentratiosassumed,i.e.25%forgrowers,15%forfibreand20%forsawmilling

EstimatesofaggregateturnoverofEnterprisesineachsub-sectorareasfollows

a. Growersector–annualharvest(2005)of20millionm³@R250/m³delivered=R5billion

b. Fibresector

ßPulpandPaper-PAMSAestimate: R14billion

ßBoardproducts: R�billion

ßChipexports: R�billion

c. Sawmillingandother

ßSawmilling(2,7millionm³@R1600/m³):R4,�billion

ßMiningtimber(0,8millionm³@R1200/m³): R1,0billion

ßCharcoal: R0,5billion

ßPoles(800000m³@R1000/m³):R0,8billion

ßMatches,other: R0,4billion

�7

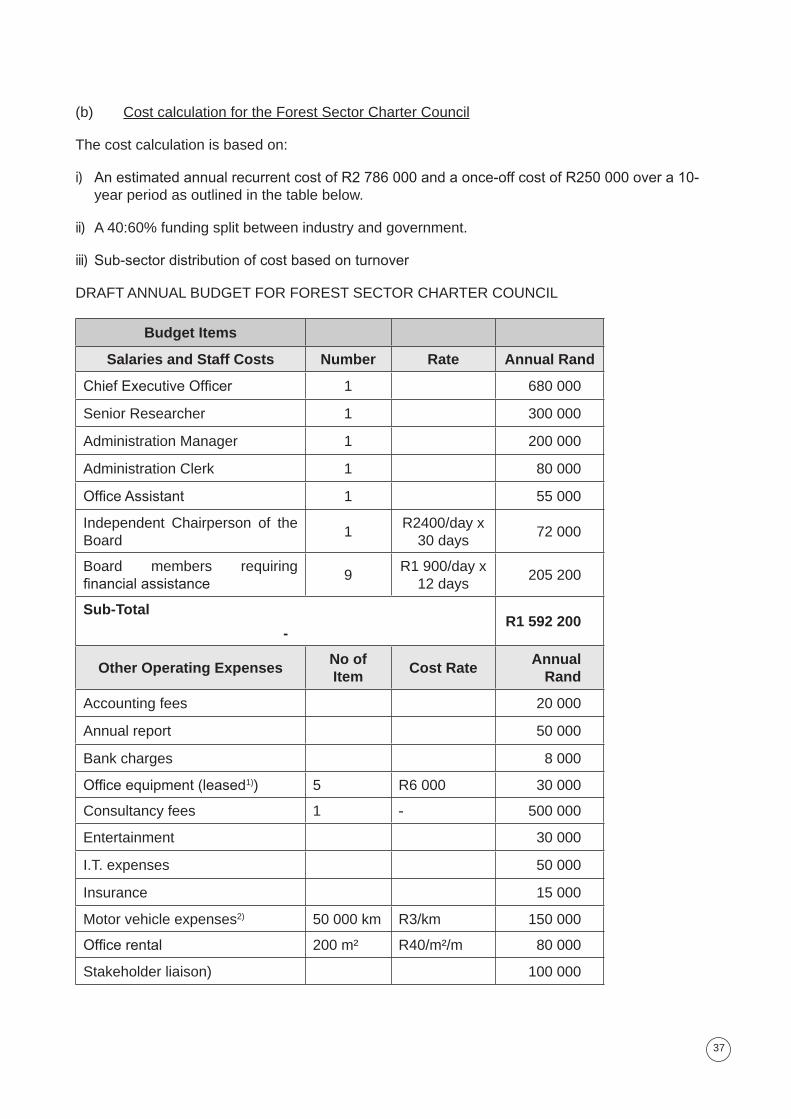

(b) CostcalculationfortheForestSectorCharterCouncil

Thecostcalculationisbasedon:

i) AnestimatedannualrecurrentcostofR2786000andaonce-offcostofR250000overa10-yearperiodasoutlinedinthetablebelow.

ii) A40:60%fundingsplitbetweenindustryandgovernment.

iii) Sub-sectordistributionofcostbasedonturnover

DRAFTANNUALBUDGETFORFORESTSECTORCHARTERCOUNCIL

Budget Items

Salaries and Staff Costs Number Rate Annual Rand

ChiefExecutiveOfficer 1 680000

SeniorResearcher 1 �00000

AdministrationManager 1 200000

AdministrationClerk 1 80000

OfficeAssistant 1 55000

Independent Chairperson of theBoard

1R2400/dayx

�0days72000

Board members requiringfinancialassistance

9R1900/dayx

12days205200

Sub-Total

-R1 592 200

Other Operating ExpensesNo of Item

Cost RateAnnual

Rand

Accountingfees 20000

Annualreport 50000

Bankcharges 8000

Officeequipment(leased1)) 5 R6000 �0000

Consultancyfees 1 - 500000

Entertainment �0000

I.T.expenses 50000

Insurance 15000

Motorvehicleexpenses2) 50000km R�/km 150000

Officerental 200m² R40/m²/m 80000

Stakeholderliaison) 100000

�8

Photocopying, printing andstationery

25000

Publicity,circulars,etc 50000

Stafftravel R4000/ea 80000

Flights

Accommodationandmeals

CarHire

24trips

24nights

24cardays

R2000/trip

R600/night

R�00/day

48000

14400

7200

Counciltravel(GovtandIndustryAssociationspayforthemselves)

Flights(6meetingsX8flights)

Accommodationandmeals

Carhire

48flights

6meetings

48carhires

R2000/trip

R8000/meeting

R�00/day

96000

48000

14400

Telecommunication 65000

Sub-Total R1 480 600

TOTAL BUDGET R3 072 800

Notes: 1) Office establishment costs (once-off) are excluded. The following should be budgeted for:

- Officefurniture = R120000-00

- ComputersandITinfrastructure = R100000-00

- Boardroom,etc = R30000-00

= R250000-00

2)Assumenocompanyvehicles,onlyre-imbursementforownvehicletravelexpenses

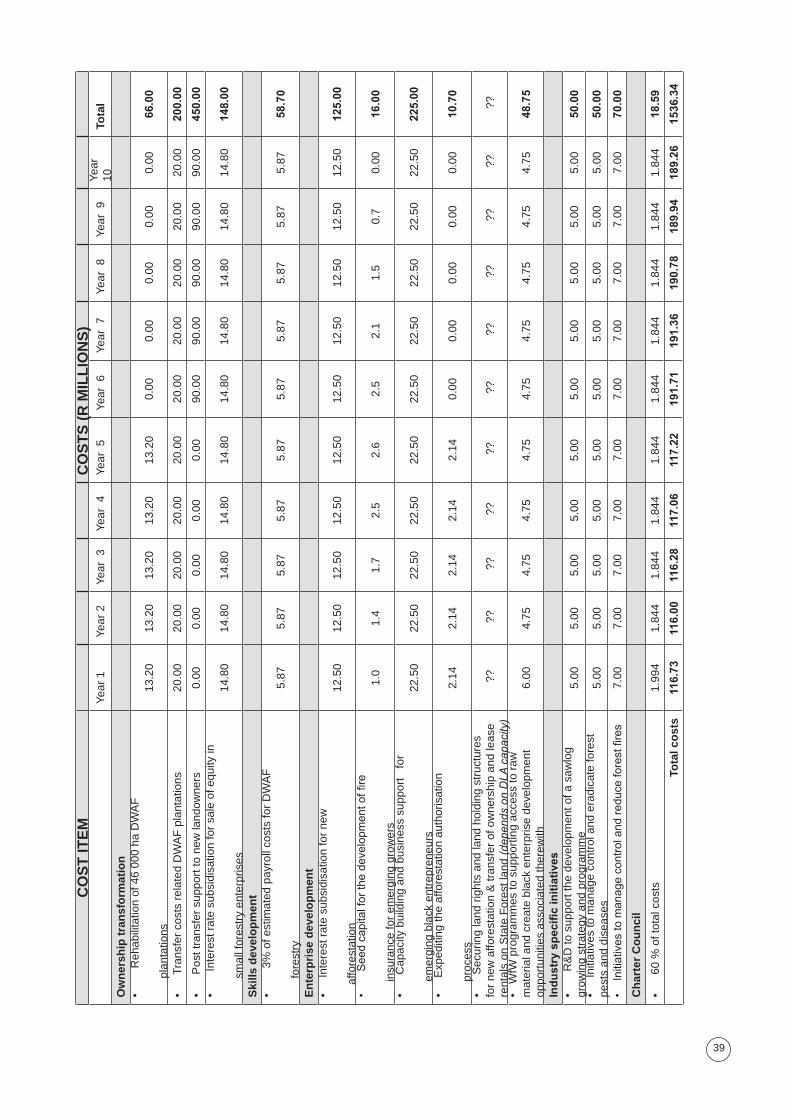

7.2 GovernmentCosts

ThefinancialrequirementsforimplementingtheCharterbyGovernmentareoutlinedinthetablebelow.TheactualbudgetavailablewillbesubjecttoParliamentaryapproval.

(a) CostcalculationforGovernmentcontributiontoOwnershipTransformation

ThecalculationofGovernmentcoststoeffectownershiptransformationrelatestotherehabilitationandtransferoftheremainingDWAFplantations.ThisamountstoR716millionoveraten-yearperiod,basedonthefollowing:

i) Rehabilitationof46000haplantationsatatotalcostofR66millionoveraperiodoffiveyears.

ii) Costoftransfer(transfercostsfacilitationsupportandestablishmentoflegalentities)atR10millionpertransferpackagefor20packagesoverthe10-yearperiod.

iii)PosttransfersupporttonewownersatR90million/yearfromyear6-10.

iv)Theinterestratesubsidisationfor25%blackequityownershipin300000haof“small”forestry

�9

CO

ST

ITE

MC

OS

TS

(R

MIL

LIO

NS

)

Yea

r1

Yea

r2

Yea

r�

Yea

r4

Yea

r5

Yea

r6

Yea

r7

Yea

r8

Yea

r9

Yea

r

10To

tal

Ow

ner

ship

tra

nsf

orm

atio

n

•

Reh

abili

tatio

nof

46

000

haD

WA

F

plan

tatio

ns1�

.20

1�.2

01�

.20

1�.2

01�

.20

0.00

0.00

0.00

0.00

0.00

66.0

0

•

Tra

nsfe

rco

sts

rela

ted

DW

AF

pla

ntat

ions

20.0

020

.00

20.0

020

.00

20.0

020

.00

20.0

020

.00

20.0

020

.00

200.

00

•

Pos

ttra

nsfe

rsu

ppor

tto

new

land

owne

rs0.

000.

000.

000.

000.

0090

.00

90.0

090

.00

90.0

090

.00

450.

00•

Inte

rest

rat

esu

bsid

isat

ion

for

sale

ofe

quity

in

smal

lfor

estr

yen

terp

rises

14.8

014

.80

14.8

014

.80

14.8

014

.80

14.8

014

.80

14.8

014

.80

148.

00

Ski

lls d

evel

op

men

t

•

�

%o

fest

imat

edp

ayro

llco

sts

for

DW

AF

fore

stry

5.87

5.87

5.87

5.87

5.87

5.87

5.87

5.87

5.87

5.87

58.7

0

En

terp

rise

dev

elo

pm

ent

•

In

tere

str

ate

subs

idis

atio

nfo

rne

w

a

ffore

stat

ion

12.5

012

.50

12.5

012

.50

12.5

012

.50

12.5

012

.50

12.5

012

.50

125.

00

•Seedcapitalforthedevelopm

entoffire

i

nsur

ance

for

emer

ging

gro

wer

s1.

01.

41.

72.

52.

62.

52.

11.

50.

70.

0016

.00

•

Cap

acity

bui

ldin

gan

dbu

sine

sss

uppo

rt

for

e

mer

ging

bla

cke

ntre

pren

eurs

22.5

022

.50

22.5

022

.50

22.5

022

.50

22.5

022

.50

22.5

022

.50

225.

00

•

Exp

editi

ngth

eaf

fore

stat

ion

auth

oris

atio

n

p

roce

ss2.

142.

142.

142.

142.

140.

000.

000.

000.

000.

0010

.70

•

Sec

urin

gla

ndr

ight

san

dla

ndh

oldi

ngs

truc

ture

sfo

rne

wa

ffore

stat

ion

&tr

ansf

ero

fow

ners

hip

and

leas

ere

ntal

son

Sta

teF

ores

tlan

d(d

epen

ds o

n D

LA c

apac

ity)

??

??

??

??

??

??

??

??

??

??

??

•W

fWp

rogr

amm

esto

sup

port

ing

acce

ssto

raw

m

ater

iala

ndc

reat

ebl

ack

ente

rpris

ede

velo

pmen

top

port

uniti

esa

ssoc

iate

dth

erew

ith6.

004.

754.

754.

754.

754.

754.

754.

754.

754.

7548

.75

Ind

ust

ry s

pec

ific

init

iati

ves

•

R&

Dto

sup

port

the

deve

lopm

ento

fas

awlo

ggr

owin

gst

rate

gya

ndp

rogr

amm

e5.

005.

005.

005.

005.

005.

005.

005.

005.

005.

0050

.00

•

Initi

ativ

esto

man

age

cont

rola

nde

radi

cate

fore

st

pest

san

ddi

seas

es5.

005.

005.

005.

005.

005.

005.

005.

005.

005.

0050

.00

•Initiativestomanagecontrolandreduceforestfires

7.00

7.00

7.00

7.00

7.00

7.00

7.00

7.00

7.00

7.00

70.0

0

Ch

arte

r C

ou

nci

l

•

60

%o

ftot

alc

osts

1.99

41.

844

1.84

41.

844

1.84

41.

844

1.84

41.

844

1.84

41.

844

18.5

9

Tota

l co

sts

116.

7311

6.00

116.

2811

7.06

117.

2219

1.71

191.

3619

0.78

189.

9418

9.26

1536

.34

40

enterprisesamountstoR920millionover10years,basedonR2�744�per60hatransferred(R�957/ha)-refertoModel4a,par.6.5.2a.Itisfurtherassumedthathalfoftheemergingforestryenterpriseswouldnotparticipate insuchanarrangement.Governmentcontribution to interestsubsidisationisthereforebasedon25%equityownershipof150000ha,whichamountstoR148million.

(b) CostcalculationforGovernmentcontributiontoSkillsDevelopment

Thecostofskillsdevelopmentisbasedon�%spendofpayrollbyDWAF,basedonaforestrypersonnelbudgetofR195552000in2006-07(approximately4200posts)

(c) CostcalculationforGovernmentcontributiontoEnterpriseDevelopment

Thisisbasedonthefollowingcalculationsandassumptions:

i) Interestratesubsidisationfor100000hanewafforestationover10-yearsiscalculatedatR6234per2.4hafamilyfarm(refertoModel1a,par.6.5.1b.),whichamountstoR2597/ha,orR9557�per50hacommercialfarmingoperation(refertoModel�a,par.6.5.1d.),whichamountstoR2�89/ha.AtanaveragecostofR2500/hathisamountstoR250millionrequiredforthe100000ha.Itisfurtherassumedthat50%ofthiscostwillbebornebytheprivatesectoreitheraspartoftheirenterprisedevelopmentcontributionsorlinkedtocontractualagreementsforthesupplyofrawmaterial.GovernmentcontributiontointerestratesubsidisationthereforeamountstoR125millionover10years.