Embed Size (px)

Citation preview

Commodity Derivatives Desk, London

April 2007

Strictly Private and Confidential

Why the interest ?

Strategic rationale Return - Historical absolute returns on commodity indices are higher than government bonds,

credit and comparable with those of equity markets Diversification - Returns generally have negative correlation with equities Insurance - Commodity exposure has historically provided a good hedge against Geopolitical

risk and inflation surprises

Tactical Rationale Global growth China and India industrial growth USD weakness

2 [Section Title]

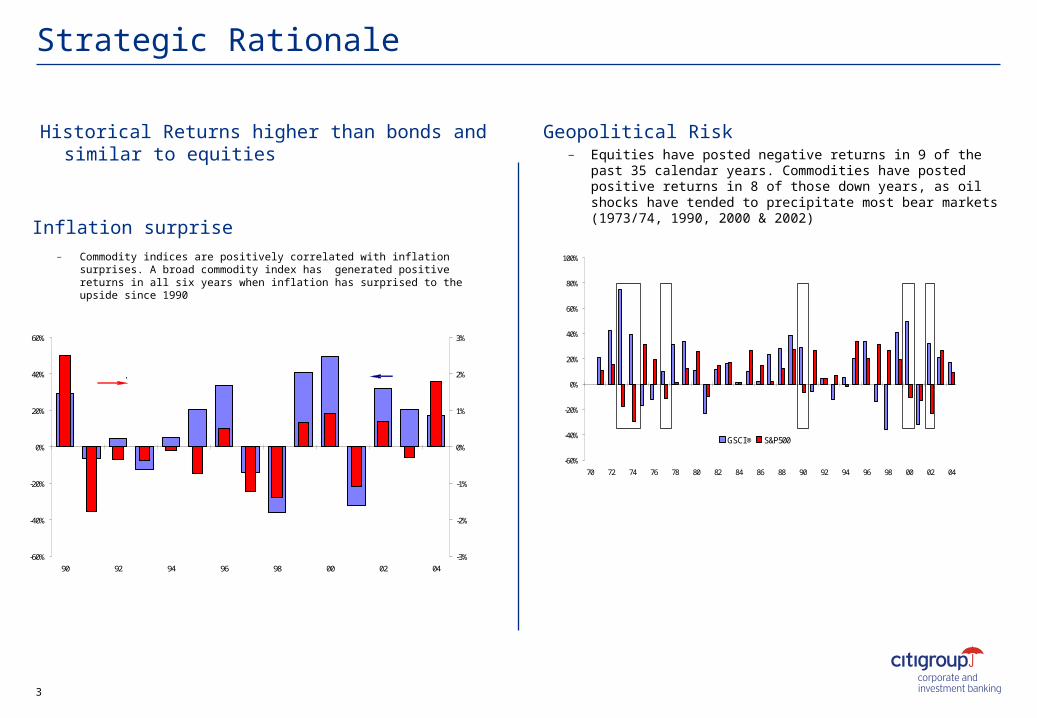

Strategic Rationale

Historical Returns higher than bonds and similar to equities

Geopolitical Risk– Equities have posted negative returns in 9 of the past 35

calendar years. Commodities have posted positive returns in 8 of those down years, as oil shocks have tended to precipitate most bear markets (1973/74, 1990, 2000 & 2002)

Inflation surprise– Commodity indices are positively correlated with inflation surprises. A

broad commodity index has generated positive returns in all six years when inflation has surprised to the upside since 1990

3

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04

GSCI ® S&P500

-60%

-40%

-20%

0%

20%

40%

60%

90 92 94 96 98 00 02 04-3%

-2%

-1%

0%

1%

2%

3%

Inflation surpriseGSCI return

Tactical Rationale

Chinese commodity use as % of world consumption

▲ China accounts for only 10% of global GDP but a much larger share of demand for certain commodities

▲ Industrial metals: 10%-20%

▲ Bulk commodities: 20%-30%

▲ Chinese demand growth is also more rapid than other countries’

Global growth and USD weakness

▲ Industrial metals have exhibited the strongest and most consistent correlation with the global business cycle

▲ Metals’ cyclicality is even stronger than equities’

▲ Energy prices also exhibit some cyclicality, but are strongly influenced by geopolitics

▲ Commodities are generally denominated in USD. A USD depreciation makes commodities cheaper for non US based investors/consumers and should attract more demand. Therefore commodities tend to be negatively correlated with the USD. Gold in particular has a strong negative correlation with the USD

4 [Section Title]

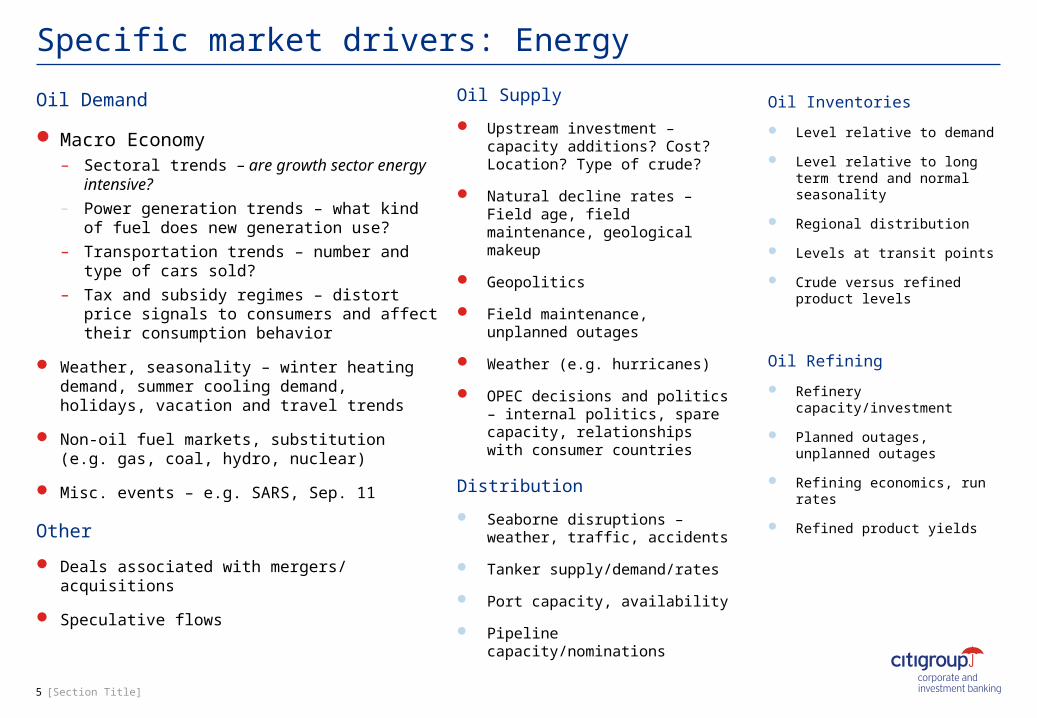

Specific market drivers: Energy

Oil Demand

Macro Economy– Sectoral trends – are growth sector energy

intensive?– Power generation trends – what kind of fuel

does new generation use?

– Transportation trends – number and type of cars sold?

– Tax and subsidy regimes – distort price signals to consumers and affect their consumption behavior

Weather, seasonality – winter heating demand, summer cooling demand, holidays, vacation and travel trends

Non-oil fuel markets, substitution (e.g. gas, coal, hydro, nuclear)

Misc. events – e.g. SARS, Sep. 11

Other

Deals associated with mergers/ acquisitions

Speculative flows

5 [Section Title]

Oil Supply

Upstream investment – capacity additions? Cost? Location? Type of crude?

Natural decline rates – Field age, field maintenance, geological makeup

Geopolitics

Field maintenance, unplanned outages

Weather (e.g. hurricanes)

OPEC decisions and politics – internal politics, spare capacity, relationships with consumer countries

Distribution

Seaborne disruptions – weather, traffic, accidents

Tanker supply/demand/rates

Port capacity, availability

Pipeline capacity/nominations

Oil Inventories

Level relative to demand

Level relative to long term trend and normal seasonality

Regional distribution

Levels at transit points

Crude versus refined product levels

Oil Refining

Refinery capacity/investment

Planned outages, unplanned outages

Refining economics, run rates

Refined product yields

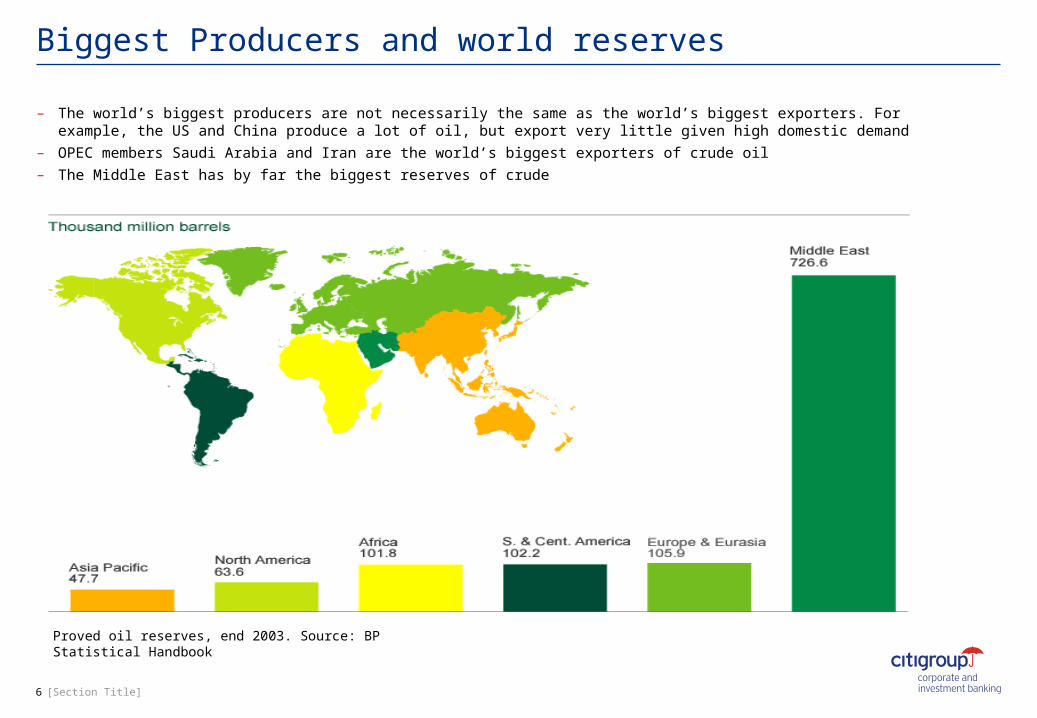

Biggest Producers and world reserves

6 [Section Title]

– The world’s biggest producers are not necessarily the same as the world’s biggest exporters. For example, the US and China produce a lot of oil, but export very little given high domestic demand

– OPEC members Saudi Arabia and Iran are the world’s biggest exporters of crude oil– The Middle East has by far the biggest reserves of crude

Proved oil reserves, end 2003. Source: BP Statistical Handbook

So what happened to oil over the past few years

– Tight refining capacity in a strong oil demand environment tops the list of supportive fundamentals

– Infrastructural and distributional constraints also feature prominently

– Speculative investment in energy magnified prices moves

– Potential geopolitical supply-side risks generated market ‘noise’ – Iraq, Venezuela, Nigeria, Lebanon

7 [Section Title]

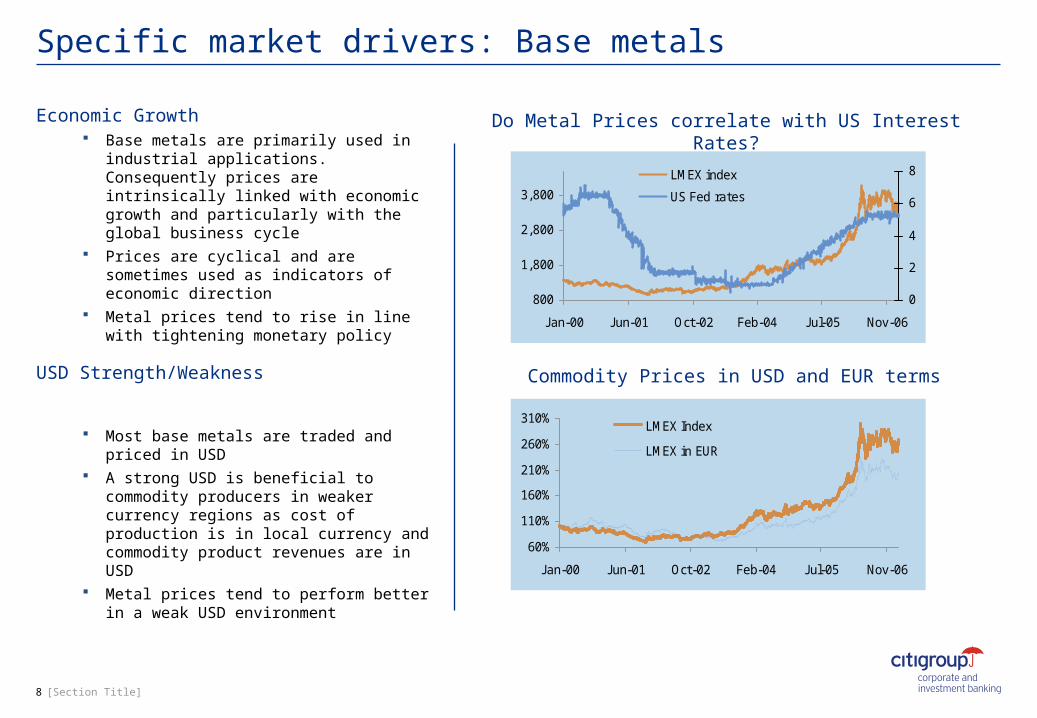

Economic Growth Base metals are primarily used in

industrial applications. Consequently prices are intrinsically linked with economic growth and particularly with the global business cycle

Prices are cyclical and are sometimes used as indicators of economic direction

Metal prices tend to rise in line with tightening monetary policy

USD Strength/Weakness

Most base metals are traded and priced in USD

A strong USD is beneficial to commodity producers in weaker currency regions as cost of production is in local currency and commodity product revenues are in USD

Metal prices tend to perform better in a weak USD environment

Specific market drivers: Base metals

8 [Section Title]

Do Metal Prices correlate with US Interest Rates?

Commodity Prices in USD and EUR terms

800

1,800

2,800

3,800

J an-00 J un-01 Oct-02 Feb-04 J ul-05 Nov-06

0

2

4

6

8LMEX index

US Fed rates

60%

110%

160%

210%

260%

310%

J an-00 J un-01 Oct-02 Feb-04 J ul-05 Nov-06

LMEX Index

LMEX in EUR

Base metals inventories

9 [Section Title]

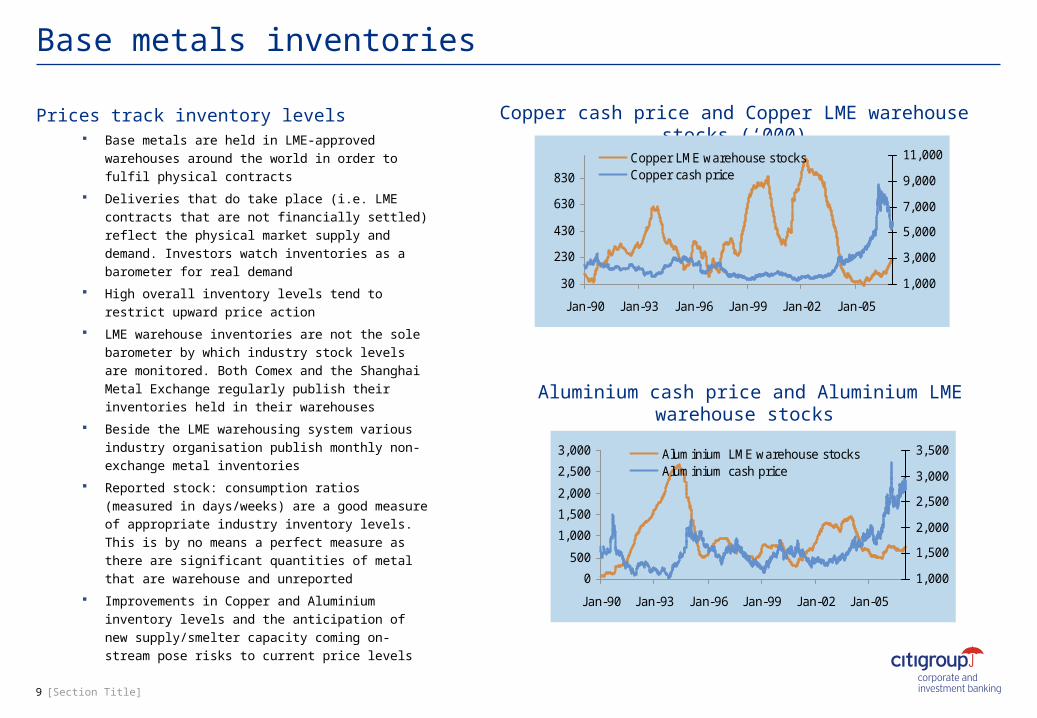

Prices track inventory levels Base metals are held in LME-approved

warehouses around the world in order to fulfil physical contracts

Deliveries that do take place (i.e. LME contracts that are not financially settled) reflect the physical market supply and demand. Investors watch inventories as a barometer for real demand

High overall inventory levels tend to restrict upward price action

LME warehouse inventories are not the sole barometer by which industry stock levels are monitored. Both Comex and the Shanghai Metal Exchange regularly publish their inventories held in their warehouses

Beside the LME warehousing system various industry organisation publish monthly non-exchange metal inventories

Reported stock: consumption ratios (measured in days/weeks) are a good measure of appropriate industry inventory levels. This is by no means a perfect measure as there are significant quantities of metal that are warehouse and unreported

Improvements in Copper and Aluminium inventory levels and the anticipation of new supply/smelter capacity coming on-stream pose risks to current price levels

Copper cash price and Copper LME warehouse stocks (‘000)

Aluminium cash price and Aluminium LME warehouse stocks

30

230

430

630

830

J an-90 J an-93 J an-96 J an-99 J an-02 J an-05

1,000

3,000

5,000

7,000

9,000

11,000Copper LME warehouse stocksCopper cash price

0

500

1,000

1,500

2,000

2,500

3,000

J an-90 J an-93 J an-96 J an-99 J an-02 J an-05

1,000

1,500

2,000

2,500

3,000

3,500Aluminium LME warehouse stocksAluminium cash price

Supply– Mine output and scrap were the predominant

sources of supply historically Majority of output comes from South Africa,

North America, Australia and China– Hedging / De-Hedging

Gold producers have been reducing their hedge books significantly in the past years driven by industry consolidation and a lower contango (determined by the difference between gold lease rates and LIBOR) which made forward selling less attractive

Producer hedging traditionally was an accelerated source of metal into the spot market, but now producer hedge reductions have added to demand for gold

– Central Banks Central banks sell from or lend reserves as

part of portfolio management 15 Central Banks are signatories to the 2004

Gold Agreement which limits annual sales to 500 tonnes and total sales to 2,500 tonnes in the 5 years to Sep-09

Specific market drivers: Gold

10 [Section Title]

Demand– Fabrication demand

Carat jewellery is dominated by India while Italy is a major manufacturer that sells finished goods to other Western countries

Other fabrication (dentistry, electronics) Gold Bar Hoarding and gold coin sales

– Investor demand Gold has traditionally been viewed as a

“safe haven” asset Recent turmoil in financial markets,

weakening global economies, and geopolitical developments have turned investor interest back to gold

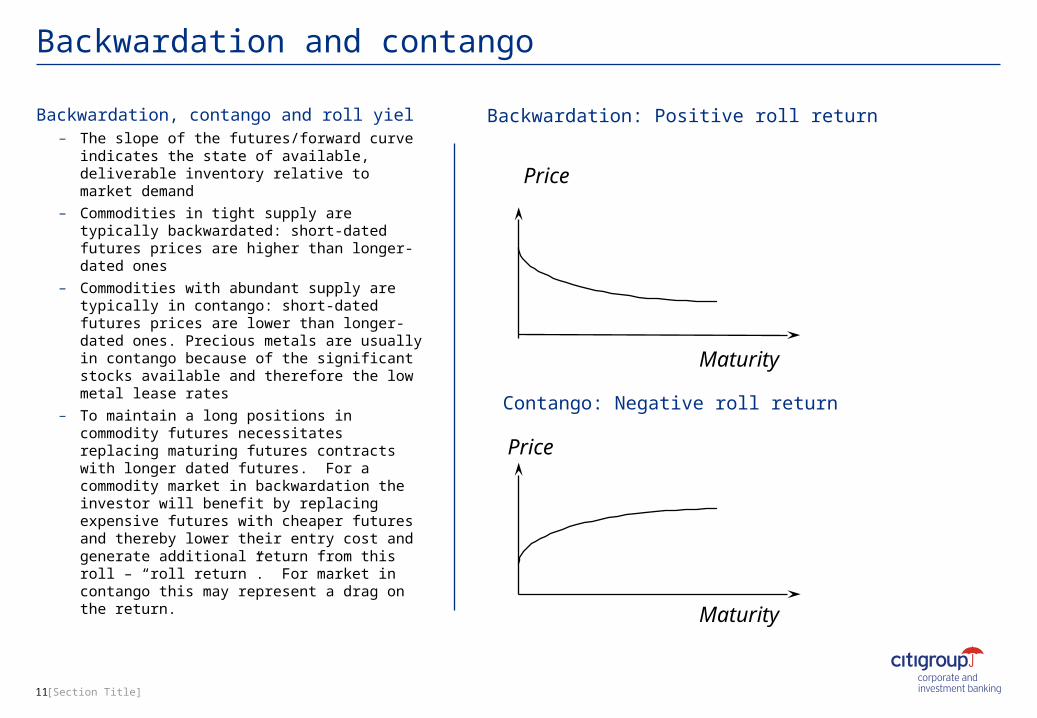

Backwardation, contango and roll yiel– The slope of the futures/forward curve

indicates the state of available, deliverable inventory relative to market demand

– Commodities in tight supply are typically backwardated: short-dated futures prices are higher than longer-dated ones

– Commodities with abundant supply are typically in contango: short-dated futures prices are lower than longer-dated ones. Precious metals are usually in contango because of the significant stocks available and therefore the low metal lease rates

– To maintain a long positions in commodity futures necessitates replacing maturing futures contracts with longer dated futures. For a commodity market in backwardation the investor will benefit by replacing expensive futures with cheaper futures and thereby lower their entry cost and generate additional return from this roll – “roll return”. For market in contango this may represent a drag on the return.

Backwardation and contango

11 [Section Title]

Backwardation: Positive roll return

Contango: Negative roll return

Price

Price

Maturity

Maturity

Current contango and backwardation in metals and energy

12 [Section Title]

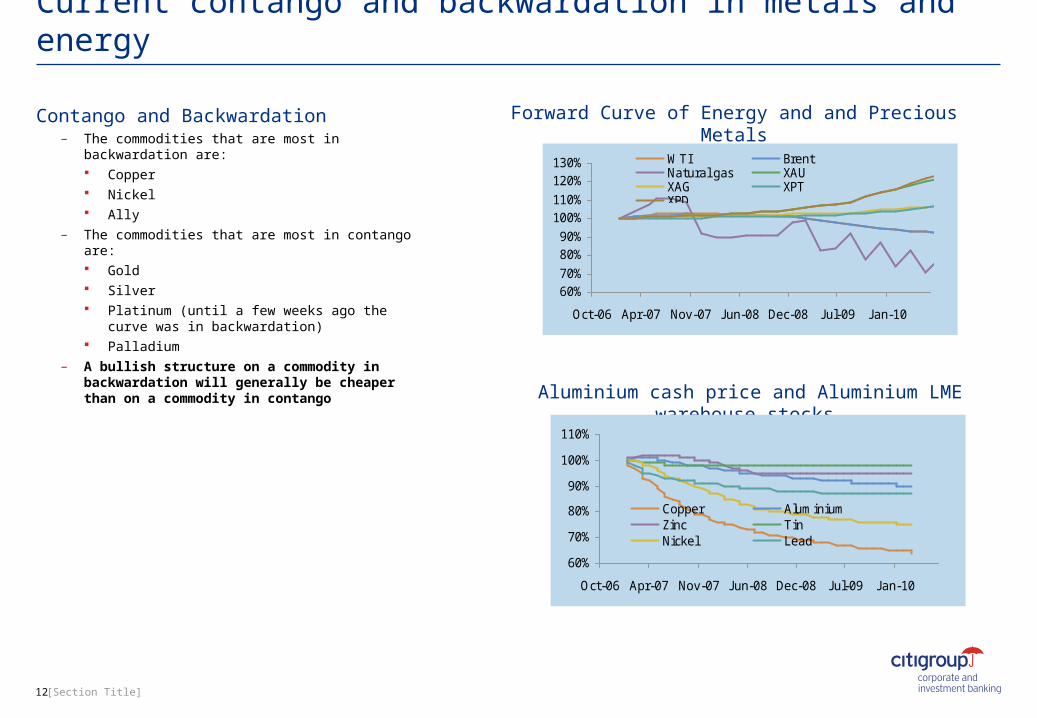

Contango and Backwardation– The commodities that are most in backwardation

are: Copper Nickel Ally

– The commodities that are most in contango are: Gold Silver Platinum (until a few weeks ago the curve was

in backwardation) Palladium

– A bullish structure on a commodity in backwardation will generally be cheaper than on a commodity in contango

Forward Curve of Energy and and Precious Metals

Aluminium cash price and Aluminium LME warehouse stocks

60%70%

80%90%

100%110%

120%130%

Oct-06 Apr-07 Nov-07 J un-08 Dec-08 J ul-09 J an-10

WTI BrentNatural gas XAUXAG XPTXPD

60%

70%

80%

90%

100%

110%

Oct-06 Apr-07 Nov-07 J un-08 Dec-08 J ul-09 J an-10

Copper AluminiumZinc TinNickel Lead

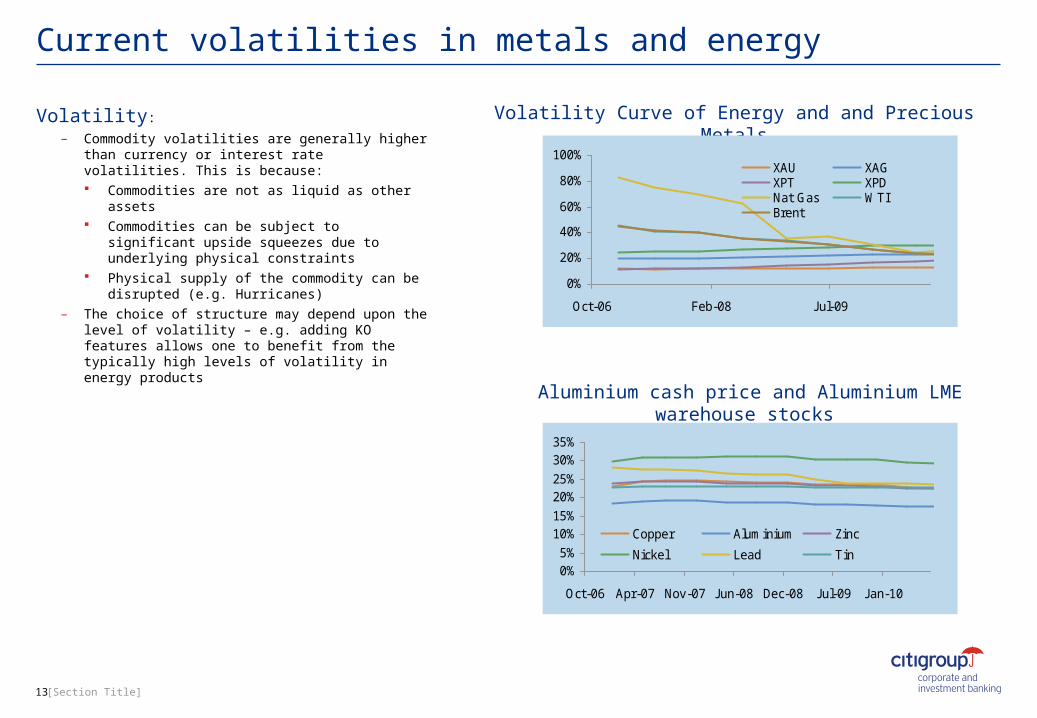

Current volatilities in metals and energy

13 [Section Title]

Volatility:

– Commodity volatilities are generally higher than currency or interest rate volatilities. This is because: Commodities are not as liquid as other assets Commodities can be subject to significant

upside squeezes due to underlying physical constraints

Physical supply of the commodity can be disrupted (e.g. Hurricanes)

– The choice of structure may depend upon the level of volatility – e.g. adding KO features allows one to benefit from the typically high levels of volatility in energy products

Volatility Curve of Energy and and Precious Metals

Aluminium cash price and Aluminium LME warehouse stocks

0%

20%

40%

60%

80%

100%

Oct-06 Feb-08 J ul-09

XAU XAGXPT XPDNat Gas WTIBrent

0%5%

10%15%

20%25%

30%35%

Oct-06 Apr-07 Nov-07 J un-08 Dec-08 J ul-09 J an-10

Copper Aluminium Zinc

Nickel Lead Tin

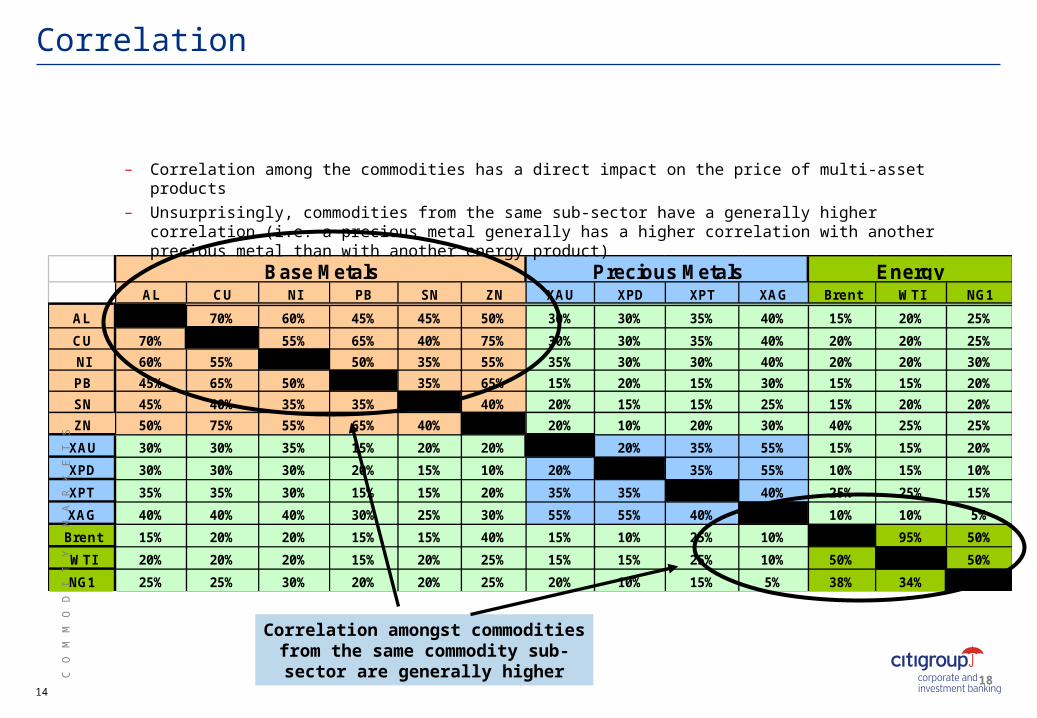

AL CU NI PB SN ZN XAU XPD XPT XAG Brent WTI NG1

AL 70% 60% 45% 45% 50% 30% 30% 35% 40% 15% 20% 25%

CU 70% 55% 65% 40% 75% 30% 30% 35% 40% 20% 20% 25%

NI 60% 55% 50% 35% 55% 35% 30% 30% 40% 20% 20% 30%

PB 45% 65% 50% 35% 65% 15% 20% 15% 30% 15% 15% 20%

SN 45% 40% 35% 35% 40% 20% 15% 15% 25% 15% 20% 20%

ZN 50% 75% 55% 65% 40% 20% 10% 20% 30% 40% 25% 25%

XAU 30% 30% 35% 15% 20% 20% 20% 35% 55% 15% 15% 20%

XPD 30% 30% 30% 20% 15% 10% 20% 35% 55% 10% 15% 10%

XPT 35% 35% 30% 15% 15% 20% 35% 35% 40% 25% 25% 15%

XAG 40% 40% 40% 30% 25% 30% 55% 55% 40% 10% 10% 5%

Brent 15% 20% 20% 15% 15% 40% 15% 10% 25% 10% 95% 50%

WTI 20% 20% 20% 15% 20% 25% 15% 15% 25% 10% 50% 50%

NG1 25% 25% 30% 20% 20% 25% 20% 10% 15% 5% 38% 34%

Base Metals Precious Metals Energy

Correlation

– Correlation among the commodities has a direct impact on the price of multi-asset products

– Unsurprisingly, commodities from the same sub-sector have a generally higher correlation (i.e. a precious metal generally has a higher correlation with another precious metal than with another energy product)

Correlation amongst commodities from the same commodity sub-sector are

generally higher18C

O M

M O

D I

T Y

M A

R K

E T

S

14

How can we help clients take exposure in the commodity space?

15 [Section Title]

– Global Commodities have had recently the rollout of the new models for the Investor Product Business. Baskets (incl. quanto) American observations of single or basket underlying (quanto), ie KI/KO options (call, put, digi-call, digi-

put) Single/double touch KI/KO for single or basket underlying (incl. quanto) Rainbow structures (incl. quanto) [i.e. where weighting is allocated according to final performance]

– Over the coming weeks, we will be adding further features such as autocallables, resettables and quantoed range accruals.

– Underlyings that we can trade are: Oil Precious Metals Base Metals Commodity Indices (eg GSCI, DJAIG) and Sub Indeces Refined Products (e.g Jet Fuel, Gasoil, Gasoline, Propane) US Gas and Power Coal

– Over the coming months, this will expand into European Power & Gas, and Carbon Emissions.

This material has been prepared by individual sales and/or trading personnel of Citigroup or its subsidiaries or affiliates and not by Citigroup's research department. Citigroup are pleased to present to you the proposed transaction or transactions described herein. All material contained herein, including proposed terms and conditions, are indicative and for discussion purposes only, is strictly confidential, may not be reproduced and is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. Finalised terms and conditions are subject to further discussion and negotiation. Information and opinions presented in this material have been obtained or derived from sources believed by Citigroup to be reliable, but Citigroup makes no representation as to their accuracy or completeness. Citigroup accepts no liability for loss (whether direct or consequential) arising from the use of this material. Citigroup does not provide legal, tax or accounting advice; such matters should be discussed with your independent advisors. The ultimate decision to proceed with any transaction rests solely with you. Citigroup is not acting as your advisor or agent. Therefore, prior to entering into any proposed transaction, you should determine, without reliance upon Citigroup or its affiliates, the economic risks and merits, as well as the legal, tax and accounting characterizations and consequences, of the transaction and that you are able to assume these risks. This material is directed exclusively at Citigroup's market professional and institutional investor customers ie market counterparties and intermediate customers as defined by the rules of the Financial Services Authority. It is not intended for private customers and such persons should not rely on this material. Moreover, any investment or service to which this material may relate, will not be made available by Citigroup to such private customers. This document and its contents are proprietary information and products of Citigroup and may not be reproduced or otherwise disseminated in whole or in part without Citigroup’s written consent.

Copyright © Citigroup 2005. All Rights Reserved

Disclaimer