Embed Size (px)

Citation preview

COMMERCIALDEPOSIT ACCOUNT

TERMS AND CONDITIONSAlso for use by FIDUCIARIES

WELCOME TO M&TOn November 1, 2015, Hudson City Savings Bank (“HCSB”) merged into and became

part of M&T Bank (“M&T”). As a result, your company’s Hudson City deposit accountsbecame M&T accounts. Soon, we will be transferring those accounts and any accountsopened at our Hudson City division* onto M&T computer systems. We sometimes referto the date on which this transfer takes place as the “conversion date.” The exactconversion date is set forth in the cover letter accompanying this booklet.

This booklet includes information about the names and features of your company’sHudson City deposit accounts after the conversion. Please note that provisions that applyonly to new customers or only to newly opened accounts will not apply to convertedaccounts.

The features and terms of your company’s deposit accounts, as described in thisbooklet, do not necessarily reflect the standard features and terms of M&T depositaccounts. This means that any deposit account your company may open with M&Tbefore, on, or after the conversion date may have features and terms that are differentfrom those that will apply to your company’s converted Hudson City deposit accounts.

*The Hudson City division refers to the former HCSB locations, which were acquired by M&T inthe merger. We also refer to the accounts opened at HCSB before the merger and the accountsopened through our Hudson City division after the merger collectively as Hudson City accountsor Hudson City deposit accounts and we use the term “Hudson City” to refer to the processingand systems for those accounts prior to the conversion.

THE COMMERCIAL DEPOSIT ACCOUNT AGREEMENT IN THIS BOOKLET(BEGINNING ON PAGE 20) INCLUDES AN ARBITRATION PROVISION INTHE SECTION ENTITLED “DISPUTES INVOLVING YOUR ACCOUNT.”

2 B

OverdraftsBank’s Right of SetoffPower of AttorneyLiabilities and ExpensesServices Fees and Negative Available Balance Fees....................p. 26Closing AccountsStatements, Notices, Advices and Changes of AddressAbandoned AccountsAmendmentsNonwaiver by BankWaiver of RightsAssignment of AccountJoint Accounts..............................................................................p. 27Reasonable Time to ActOverdraft Fees Imposed Based on Available BalanceDisclosure of InformationSuccessors and AssignsLegal Proceedings and DisputesDisputes Involving Your AccountEvidence ......................................................................................p. 28Conflicts with Applicable LawSeverabilityWhat Law AppliesMore Information

Special Provisions for Commercial Checking, NOW and Savings Accounts ..........................................................p. 28

DepositsLimitations on WithdrawalsNotice of WithdrawalRefusal to Permit WithdrawalPassbooksStale and Postdated Checks..........................................................p. 29Stopping Payment of CheckCheck Cashing at Bank BranchesCheck Cashing FeesCheck Cashing Identification RequirementsElectronic Presentment of ChecksCertain Interest-Bearing Checking AccountsCertain Non-Interest-Bearing Checking Accounts ......................p. 30

Special Provisions for Commercial Time Deposit Accounts.............................................p. 30

No Change in Maturity Date by Additional DepositAutomatic RenewalBook Entry AccountsDelay in WithdrawalOn and After Final Maturity DateNotice of Maturity DateLimitation on Early WithdrawalPast Policies on Early WithdrawalLimitations on WithdrawalsPenalty for Early Withdrawal

Commercial Deposit Account Fee Schedule .....................................p. 31

TABLE OF CONTENTS

Checking Account Conversion Information .......................................p. 3Savings and Money Market Account Conversion Information.........p. 3Time Deposit Account Conversion Information.................................p. 4

Specific Features and Terms..........................................................pp. 5-11M&T Simple Checking for Business Account ...................................p. 5Commercial Checking Account .........................................................p. 5M&T Business Interest Checking Account ........................................p. 6IOLTA NOW Account (New Jersey) ..................................................p. 7IOLTA NOW Account (Connecticut) .................................................p. 7IOLA NOW Account (New York) ......................................................p. 8Commercial Money Market Savings Account....................................p. 9Commercial Savings Account ............................................................p. 9Commercial Certificate of Deposit......................................................p. 10

Notice Regarding Overdrafts .............................................................p. 12

Availability Disclosure for Commercial Deposit Accounts ......................................................pp. 13-14

Electronic Banking Agreement for Businesses.............................pp. 15-19

Commercial Deposit Account Agreement .................................pp. 20-30

Introduction ...................................................................................................p. 20DefinitionsGoverning DocumentsKinds of Commercial Accounts

General Terms and Conditions for Commercial Deposit Accounts ......................................................p. 20

General Use of AccountsDepositsMissing Endorsements ................................................................p. 21Limitations on DepositsInitial Deposit Amounts

And Error CorrectionCollection and Cashing of Checks and Other ItemsCrediting of DepositsWithdrawalsInformation about Transactions Made with Your

Debit Card and Authorization HoldsAuthorized Signatures and Identification.....................................p. 22Telephone InstructionsPreauthorized and Automatic Transfers .......................................p. 23ACH Payments ProvisionalNotice of ChangesIndemnity of Bank as EscroweeFiduciariesCustomer SecurityNotice of Suspected ErrorsStandard of CareCharging of Withdrawals .............................................................p. 24Order in Which We Post and Pay Debit Items for Checking,

NOW, Savings (Other than Passbook Savings), and Money Market Accounts

Posting Order for Time Deposit and Passbook Accounts ............p. 25

3 B

After the conversion, the governing documents for your company’s account willinclude:• Commercial Deposit Account Agreement• Notice Regarding Overdrafts – Business Checking Accounts• Availability Disclosure for Commercial Deposit Accounts• Specific Features and Terms for the specific type of account you will have after

conversion• Commercial Deposit Account Fee Schedule • Electronic Banking Agreement for Businesses

These documents will apply to your account as though your company signed aCommercial Deposit Account Opening Request for that account on the conversiondate.

Your account will automatically become the type of account indicated in thechart, but we would be happy to discuss account options with you after theconversion. Simply stop by any branch or call us.

For interest-bearing accounts, the Annual Interest Rates have not yet beendetermined. Please call 1-800-724-6070 after the conversion to find out the AnnualInterest Rate applicable to your account. Rates are variable and subject to changedaily. For tiered rate accounts, if your balance falls within a particular tier, M&Twill pay the Annual Interest Rate corresponding to that tier on the entire balanceeligible to earn interest in your account.

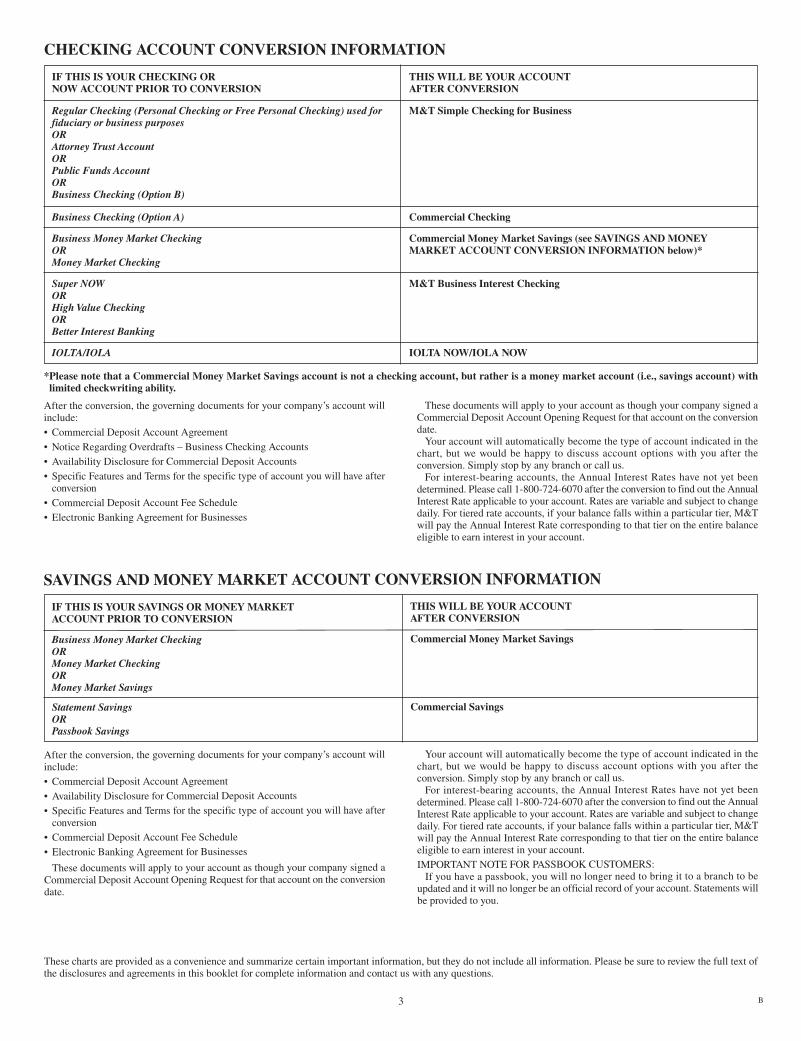

CHECKING ACCOUNT CONVERSION INFORMATION

IF THIS IS YOUR CHECKING OR NOW ACCOUNT PRIOR TO CONVERSION

THIS WILL BE YOUR ACCOUNTAFTER CONVERSION

Regular Checking (Personal Checking or Free Personal Checking) used forfiduciary or business purposesORAttorney Trust AccountORPublic Funds AccountORBusiness Checking (Option B)

M&T Simple Checking for Business

Business Checking (Option A) Commercial Checking

Business Money Market CheckingORMoney Market Checking

Commercial Money Market Savings (see SAVINGS AND MONEYMARKET ACCOUNT CONVERSION INFORMATION below)*

Super NOW OR High Value Checking OR Better Interest Banking

M&T Business Interest Checking

IOLTA/IOLA IOLTA NOW/IOLA NOW

After the conversion, the governing documents for your company’s account willinclude:• Commercial Deposit Account Agreement

• Availability Disclosure for Commercial Deposit Accounts

• Specific Features and Terms for the specific type of account you will have afterconversion

• Commercial Deposit Account Fee Schedule

• Electronic Banking Agreement for Businesses

These documents will apply to your account as though your company signed aCommercial Deposit Account Opening Request for that account on the conversiondate.

Your account will automatically become the type of account indicated in thechart, but we would be happy to discuss account options with you after theconversion. Simply stop by any branch or call us.

For interest-bearing accounts, the Annual Interest Rates have not yet beendetermined. Please call 1-800-724-6070 after the conversion to find out the AnnualInterest Rate applicable to your account. Rates are variable and subject to changedaily. For tiered rate accounts, if your balance falls within a particular tier, M&Twill pay the Annual Interest Rate corresponding to that tier on the entire balanceeligible to earn interest in your account.

IMPORTANT NOTE FOR PASSBOOK CUSTOMERS:If you have a passbook, you will no longer need to bring it to a branch to be

updated and it will no longer be an official record of your account. Statements willbe provided to you.

SAVINGS AND MONEY MARKET ACCOUNT CONVERSION INFORMATION

IF THIS IS YOUR SAVINGS OR MONEY MARKET ACCOUNT PRIOR TO CONVERSION

THIS WILL BE YOUR ACCOUNT AFTER CONVERSION

Business Money Market CheckingORMoney Market Checking ORMoney Market Savings

Commercial Money Market Savings

Statement SavingsORPassbook Savings

Commercial Savings

*Please note that a Commercial Money Market Savings account is not a checking account, but rather is a money market account (i.e., savings account) withlimited checkwriting ability.

These charts are provided as a convenience and summarize certain important information, but they do not include all information. Please be sure to review the full text ofthe disclosures and agreements in this booklet for complete information and contact us with any questions.

4 B

Until your company’s CD renews as a Commercial Certificate of Deposit, its termswill remain unchanged. Note, however, that the availability of funds deposited intothat account will be governed by M&T’s Availability Disclosure for CommercialDeposit Accounts. If your account pays simple interest, interest will compoundmonthly.

After the first maturity date of your company’s CD on or after the first businessday following the conversion date, the governing documents for your company’saccount will include:• Commercial Deposit Account Agreement• Availability Disclosure for Commercial Deposit Accounts

• Specific Features and Terms for Commercial Certificate of Deposit• Commercial Deposit Account Fee Schedule

These documents will apply to your account as though your company signed aCommercial Deposit Account Opening Request for that account at renewal.IMPORTANT NOTE FOR PASSBOOK CUSTOMERS:

If you have a passbook, you will no longer need to bring it to a branch to beupdated and it will no longer be an official record of your account.

TIME DEPOSIT ACCOUNT CONVERSION INFORMATION

IF THIS IS YOUR CD ACCOUNT ON THE CONVERSION DATE

AT YOUR CD’S FIRST MATURITY DATE ON OR AFTER THEFIRST BUSINESS DAY FOLLOWING THE CONVERSION DATE

Certificate of Deposit with automatic renewal Your account will renew as a Commercial Certificate of Deposit

Single-maturity Certificate of Deposit That maturity date will be the final maturity date of the Certificate of Depositand the account will not be automatically renewed. Upon maturity, the balancein the account will cease to earn interest and will remain in the accountuninvested until your company provides us with instructions for payment ordeposit into another account.

These charts are provided as a convenience and summarize certain important information, but they do not include all information. Please be sure to review the full text ofthe disclosures and agreements in this booklet for complete information and contact us with any questions.

5 B

SPECIFIC FEATURES AND TERMS

M&T SIMPLE CHECKING FOR BUSINESS ACCOUNT

KIND OF ACCOUNTChecking

ACCOUNT CAN BE OPENED BYAll Non-Consumer

MINIMUM OPENING DEPOSITNone

LEDGER BALANCEAt the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against theAccount.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

AVAILABLE BALANCEThe balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCE An Available Balance less than zero.

AVERAGE NEGATIVE AVAILABLE BALANCE

The sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that AnalysisPeriod.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

STATEMENT CYCLEMonthly cycle unless otherwise requested.

OTHER FEESSee separate schedule as amended from time to time.

ANALYSIS PERIODCalendar month

ACCESS AT ELECTRONIC FACILITIESYes

*The Annual Negative Available Balance Rate will be set by M&T at M&T’sdiscretion without reference to any index, formula or schedule.

COMMERCIAL CHECKING ACCOUNT

KIND OF ACCOUNT Analyzed Checking

ACCOUNT CAN BE OPENED BY All Non-Consumer

MINIMUM OPENING DEPOSITNone

ANNUAL EARNINGS CREDIT RATEVariable, subject to change daily.*

LEDGER BALANCE At the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against theAccount.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCEThe Ledger Balance reduced by Items in the process of collection.

AVERAGE LEDGER BALANCE The sum of all Ledger Balances at the end of each day in the Analysis Period, dividedby the number of calendar days in that period.

AVERAGE FLOATThe sum of checks and other Items deposited in the Account but not yet collectedon each day in the Analysis Period, divided by the number of calendar days in thatperiod.

AVERAGE COLLECTED BALANCEThe result of subtracting the Average Float from the Average Ledger Balance.

AVERAGE POSITIVE COLLECTED BALANCEThe sum of all positive end-of-day Collected Balances which occur during theAnalysis Period, divided by the number of calendar days in that period.

RESERVE REQUIREMENTA percentage reduction equal to the highest percentage reserve requirementapplicable to net transaction accounts (as defined in 12 CFR 204.2(j)) withoutregard to whether M&T is actually subject to a reserve requirement or the actualamount of any applicable reserve requirement with respect to M&T’s nettransaction accounts or any category or class of its net transaction accounts(including any category or class of demand deposit or NOW accounts that wouldinclude the Account).

NET AVERAGE POSITIVE COLLECTED BALANCE

The Average Positive Collected Balance less the Reserve Requirement.

EARNINGS ALLOWANCE COMPUTATIONThe Net Average Positive Collected Balance for the Analysis Period, multipliedby the Annual Earnings Credit Rate in effect on the last day of the Analysis Period,divided by 365 (or 366 in a leap year), multiplied by the number of calendar daysin that Analysis Period. The Earnings Allowance will be used to offset eligiblefees posted to the Account.

BALANCE REQUIREMENTTotal charges multiplied by 365 (or 366 in a leap year), divided by the number ofdays in the Analysis Period, divided by the Annual Earnings Credit Rate. Thebalance required to offset fees posted to the Account.

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCEAn Available Balance less than zero.

6 B

AVERAGE NEGATIVE AVAILABLE BALANCEThe sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that AnalysisPeriod.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

STATEMENT CYCLEMonthly cycle unless otherwise requested.

ANALYSIS PERIODCalendar month

OTHER FEESSee separate schedule as amended from time to time.

ACCESS AT ELECTRONIC FACILITIESYes

*The Annual Earnings Credit Rate and Annual Negative Available Balance Ratewill be set by M&T at M&T’s discretion without reference to any index, formulaor schedule.

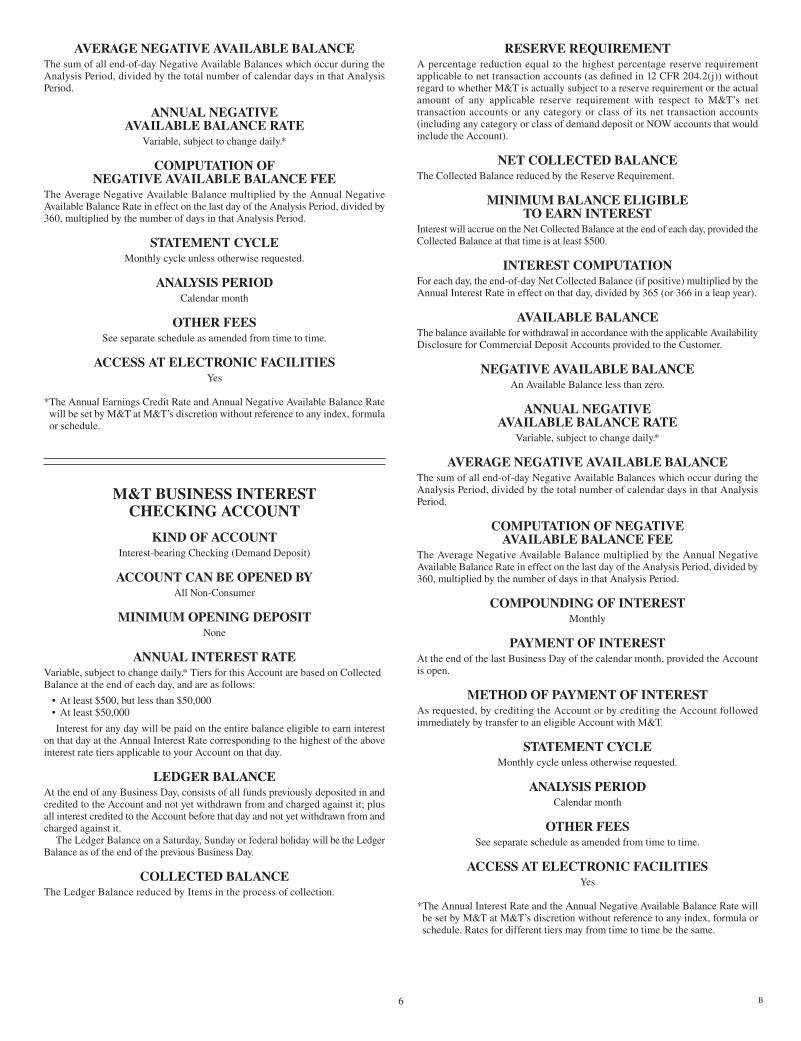

M&T BUSINESS INTEREST CHECKING ACCOUNT

KIND OF ACCOUNT Interest-bearing Checking (Demand Deposit)

ACCOUNT CAN BE OPENED BY All Non-Consumer

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATE Variable, subject to change daily.* Tiers for this Account are based on CollectedBalance at the end of each day, and are as follows:

• At least $500, but less than $50,000• At least $50,000

Interest for any day will be paid on the entire balance eligible to earn intereston that day at the Annual Interest Rate corresponding to the highest of the aboveinterest rate tiers applicable to your Account on that day.

LEDGER BALANCE At the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against it; plusall interest credited to the Account before that day and not yet withdrawn from andcharged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

RESERVE REQUIREMENT A percentage reduction equal to the highest percentage reserve requirementapplicable to net transaction accounts (as defined in 12 CFR 204.2(j)) withoutregard to whether M&T is actually subject to a reserve requirement or the actualamount of any applicable reserve requirement with respect to M&T’s nettransaction accounts or any category or class of its net transaction accounts(including any category or class of demand deposit or NOW accounts that wouldinclude the Account).

NET COLLECTED BALANCE The Collected Balance reduced by the Reserve Requirement.

MINIMUM BALANCE ELIGIBLE TO EARN INTEREST

Interest will accrue on the Net Collected Balance at the end of each day, provided theCollected Balance at that time is at least $500.

INTEREST COMPUTATION For each day, the end-of-day Net Collected Balance (if positive) multiplied by theAnnual Interest Rate in effect on that day, divided by 365 (or 366 in a leap year).

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCE An Available Balance less than zero.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

AVERAGE NEGATIVE AVAILABLE BALANCE The sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that AnalysisPeriod.

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

COMPOUNDING OF INTEREST Monthly

PAYMENT OF INTEREST At the end of the last Business Day of the calendar month, provided the Accountis open.

METHOD OF PAYMENT OF INTEREST As requested, by crediting the Account or by crediting the Account followedimmediately by transfer to an eligible Account with M&T.

STATEMENT CYCLE Monthly cycle unless otherwise requested.

ANALYSIS PERIOD Calendar month

OTHER FEES See separate schedule as amended from time to time.

ACCESS AT ELECTRONIC FACILITIESYes

*The Annual Interest Rate and the Annual Negative Available Balance Rate willbe set by M&T at M&T’s discretion without reference to any index, formula orschedule. Rates for different tiers may from time to time be the same.

7 B

IOLTA NOW ACCOUNT(for accounts open in New Jersey)

KIND OF ACCOUNT IOLTA (Interest on Lawyers Trust) accounts are a special type of NOW (negotiableorder of withdrawal) account which can be opened only as an attorney trust accountfor qualified commingled client funds bearing interest for the benefit of the IOLTAFund of the Bar of New Jersey.

ACCOUNT CAN BE OPENED BY Attorney or Law Firm

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATE Variable, subject to change daily.* Tiers for this Account are based on CollectedBalance at the end of each day, and are as follows:

• At least $500, but less than $50,000• At least $50,000

Interest for any day will be paid on the entire balance eligible to earn intereston that day at the Annual Interest Rate corresponding to the highest of the aboveinterest rate tiers applicable to your Account on that day.

LEDGER BALANCE At the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against it; plusall interest credited to the Account before that day and not yet withdrawn from andcharged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

RESERVE REQUIREMENT A percentage reduction equal to the highest percentage reserve requirementapplicable to net transaction accounts (as defined in 12 CFR 204.2(j)) withoutregard to whether M&T is actually subject to a reserve requirement or the actualamount of any applicable reserve requirement with respect to M&T’s nettransaction accounts or any category or class of its net transaction accounts(including any category or class of demand deposit or NOW accounts that wouldinclude the Account).

NET COLLECTED BALANCE The Collected Balance reduced by the Reserve Requirement.

MINIMUM BALANCE ELIGIBLE TO EARN INTEREST

Interest will accrue on the Net Collected Balance at the end of each day, provided theCollected Balance at that time is at least $500.

INTEREST COMPUTATION For each day, the end-of-day Net Collected Balance (if positive) multiplied by theAnnual Interest Rate in effect on that day, divided by 365 (or 366 in a leap year).

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCE An Available Balance less than zero.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

AVERAGE NEGATIVE AVAILABLE BALANCE The sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that Analysis Period.

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

COMPOUNDING OF INTEREST Monthly

PAYMENT OF INTEREST At the end of the last Business Day of the calendar month, provided the Accountis open.

METHOD OF PAYMENT OF INTEREST By crediting the Account; with periodic remittances to the account of the IOLTAFund of the Bar of New Jersey after deduction of permissible service charges andother fees.

STATEMENT CYCLE Monthly cycle unless otherwise requested.

ANALYSIS PERIOD Calendar month

OTHER FEES See separate schedule as amended from time to time.

*The Annual Interest Rate and the Annual Negative Available Balance Rate willbe set by M&T at M&T’s discretion without reference to any index, formula orschedule. Rates for different tiers may from time to time be the same.

IOLTA NOW ACCOUNT(for accounts open in Connecticut)

KIND OF ACCOUNT IOLTA (Interest on Lawyers Trust) accounts are a special type of NOW (negotiableorder of withdrawal) account which can be opened only as an attorney trust accountfor qualified commingled client funds bearing interest for the benefit of theConnecticut Bar Foundation.

ACCOUNT CAN BE OPENED BY Attorney or Law Firm

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATE Variable, subject to change daily.* Tiers for this Account are based on CollectedBalance at the end of each day, and are as follows:

• At least $500, but less than $50,000• At least $50,000

Interest for any day will be paid on the entire balance eligible to earn intereston that day at the Annual Interest Rate corresponding to the highest of the aboveinterest rate tiers applicable to your Account on that day.

LEDGER BALANCE At the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against it; plusall interest credited to the Account before that day and not yet withdrawn from andcharged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

8 B

RESERVE REQUIREMENT A percentage reduction equal to the highest percentage reserve requirementapplicable to net transaction accounts (as defined in 12 CFR 204.2(j)) withoutregard to whether M&T is actually subject to a reserve requirement or the actualamount of any applicable reserve requirement with respect to M&T’s nettransaction accounts or any category or class of its net transaction accounts(including any category or class of demand deposit or NOW accounts that wouldinclude the Account).

NET COLLECTED BALANCE The Collected Balance reduced by the Reserve Requirement.

MINIMUM BALANCE ELIGIBLE TO EARN INTEREST

Interest will accrue on the Net Collected Balance at the end of each day, provided theCollected Balance at that time is at least $500.

INTEREST COMPUTATION For each day, the end-of-day Net Collected Balance (if positive) multiplied by theAnnual Interest Rate in effect on that day, divided by 365 (or 366 in a leap year).

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCE An Available Balance less than zero.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

AVERAGE NEGATIVE AVAILABLE BALANCE The sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that AnalysisPeriod.

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

COMPOUNDING OF INTEREST Monthly

PAYMENT OF INTEREST At the end of the last Business Day of the calendar month, provided the Accountis open.

METHOD OF PAYMENT OF INTEREST By crediting the Account; with periodic remittances to the account of theConnecticut Bar Foundation after deduction of permissible service charges andother fees.

STATEMENT CYCLE Monthly cycle unless otherwise requested.

ANALYSIS PERIOD Calendar month

OTHER FEES See separate schedule as amended from time to time.

*The Annual Interest Rate and the Annual Negative Available Balance Rate willbe set by M&T at M&T’s discretion without reference to any index, formula orschedule. Rates for different tiers may from time to time be the same.

IOLA NOW ACCOUNT(for accounts open in New York)

KIND OF ACCOUNT IOLA (Interest on Lawyers) accounts are a special type of NOW (negotiable orderof withdrawal) account which can be opened only as an attorney trust account forqualified commingled client funds bearing interest for the benefit of the New YorkState IOLA Fund pursuant to Section 97-v of the State Finance Law and Section 497of the Judiciary Law of the State of New York.

ACCOUNT CAN BE OPENED BYAttorney or Law Firm

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATEVariable, subject to change daily.* Tiers for this Account are based on CollectedBalance at the end of each day, and are as follows:

• At least $500, but less than $50,000• At least $50,000

Interest for any day will be paid on the entire balance eligible to earn intereston that day at the Annual Interest Rate corresponding to the highest of the aboveinterest rate tiers applicable to your Account on that day.

LEDGER BALANCE At the end of any Business Day, consists of all funds previously deposited in andcredited to the Account and not yet withdrawn from and charged against it; plusall interest credited to the Account before that day and not yet withdrawn from andcharged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

RESERVE REQUIREMENT A percentage reduction equal to the highest percentage reserve requirementapplicable to net transaction accounts (as defined in 12 CFR 204.2(j)) withoutregard to whether M&T is actually subject to a reserve requirement or the actualamount of any applicable reserve requirement with respect to M&T’s nettransaction accounts or any category or class of its net transaction accounts(including any category or class of demand deposit or NOW accounts that wouldinclude the Account).

NET COLLECTED BALANCE The Collected Balance reduced by the Reserve Requirement.

MINIMUM BALANCE ELIGIBLE TO EARN INTEREST

Interest will accrue on the Net Collected Balance at the end of each day, provided theCollected Balance at that time is at least $500.

INTEREST COMPUTATION For each day, the end-of-day Net Collected Balance (if positive) multiplied by theAnnual Interest Rate in effect on that day, divided by 365 (or 366 in a leap year).

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

NEGATIVE AVAILABLE BALANCE An Available Balance less than zero.

ANNUAL NEGATIVE AVAILABLE BALANCE RATE

Variable, subject to change daily.*

9 B

AVERAGE NEGATIVE AVAILABLE BALANCE The sum of all end-of-day Negative Available Balances which occur during theAnalysis Period, divided by the total number of calendar days in that AnalysisPeriod.

COMPUTATION OF NEGATIVE AVAILABLE BALANCE FEE

The Average Negative Available Balance multiplied by the Annual NegativeAvailable Balance Rate in effect on the last day of the Analysis Period, divided by360, multiplied by the number of days in that Analysis Period.

COMPOUNDING OF INTEREST Monthly

PAYMENT OF INTEREST At the end of the last Business Day of the calendar month, provided the Accountis open.

METHOD OF PAYMENT OF INTEREST By crediting the Account; with periodic remittances to the account of the NewYork State IOLA Fund pursuant to Section 497(6)(c) of the Judiciary Law of theState of New York.

STATEMENT CYCLE Monthly cycle unless otherwise requested.

ANALYSIS PERIOD Calendar month

OTHER FEES See separate schedule as amended from time to time.

*The Annual Interest Rate and the Annual Negative Available Balance Rate willbe set by M&T at M&T’s discretion without reference to any index, formula orschedule. Rates for different tiers may from time to time be the same.

COMMERCIAL MONEY MARKET SAVINGS ACCOUNT

KIND OF ACCOUNT Statement Savings

ACCOUNT CAN BE OPENED BY All Non-Consumer

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATE Variable, subject to change daily.* Tiers for this Account are based on CollectedBalance at the end of each day, and are as follows:

• At least $500, but less than $2,500• At least $2,500, but less than $10,000• At least $10,000, but less than $25,000• At least $25,000, but less than $50,000• At least $50,000, but less than $75,000• At least $75,000, but less than $100,000• At least $100,000

Interest for any day will be paid on the entire balance eligible to earn intereston that day at the Annual Interest Rate corresponding to the highest of the aboveinterest rate tiers applicable to your Account on that day.

LEDGER BALANCE At the end of any Business Day, consists of:

1. All funds deposited in and credited to the Account and not yet withdrawnfrom and charged against it; plus

2. All interest credited to the Account before that day and not yet withdrawnfrom and charged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

BALANCE ELIGIBLE TO EARN INTEREST As of any time during any day, will consist of:

1. The Collected Balance as of that time; plus 2. All interest earned on funds in the Account before that day, but not yet paid.

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

COMPOUNDING OF INTEREST Daily

INTEREST COMPUTATION For each day, the Balance Eligible to Earn Interest as of the end of that daymultiplied by the Annual Interest Rate in effect on that day, divided by 365 (or 366in a leap year).

PAYMENT OF INTEREST At the end of the last day of the statement cycle, provided the Account is open.

METHOD OF PAYMENT OF INTEREST As requested:

1. By crediting the Account, or 2. By crediting the Account followed immediately by transfer to a checking,

NOW or statement savings Account with M&T.

MINIMUM BALANCE TO EARN INTEREST To earn interest on any day, the Collected Balance must be at least $500 as of theend of that day.

STATEMENT CYCLE Monthly cycle

OTHER FEES See separate schedule as amended from time to time.

TRANSFER LIMITATIONS During any calendar month, a total of no more than 6 withdrawals and transferscan be made to another account with M&T or to a third party by means of apreauthorized or automatic transfer or telephonic (including data transmission)agreement, order or instruction (including Internet, online banking and othercomputer transactions), or by check, draft, debit card or similar order payable toa third party.

ACCESS AT ELECTRONIC FACILITIESYes

NOT TRANSFERABLE (as defined in 12 CFR 204)

* The Annual Interest Rate will be set by M&T at M&T’s discretion withoutreference to any index, formula or schedule. Rates for different tiers may fromtime to time be the same.

COMMERCIAL SAVINGS ACCOUNT

KIND OF ACCOUNT Statement Savings

ACCOUNT CAN BE OPENED BY All Non-Consumer

MINIMUM OPENING DEPOSITNone

ANNUAL INTEREST RATE Variable, subject to change daily.*

10 B

LEDGER BALANCE At the end of any Business Day, consists of:

1. All funds deposited in and credited to the Account and not yet withdrawnfrom and charged against it; plus

2. All interest credited to the Account before that day and not yet withdrawnfrom and charged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

COLLECTED BALANCE The Ledger Balance reduced by Items in the process of collection.

BALANCE ELIGIBLE TO EARN INTEREST As of any time during any day, will consist of:

1. The Collected Balance as of that time; plus 2. All interest earned on funds in the Account before that day, but not yet paid.

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

COMPOUNDING OF INTEREST Daily

INTEREST COMPUTATION For each day, the Balance Eligible to Earn Interest as of the end of the daymultiplied by the Annual Interest Rate in effect on that day, divided by 365 (or 366in a leap year).

PAYMENT OF INTEREST At the end of the last day of the statement cycle, provided the Account is open.

METHOD OF PAYMENT OF INTEREST As requested:

1. By crediting the Account, or 2. By crediting the Account followed immediately by transfer to a checking,

NOW or statement savings Account with M&T.

MINIMUM BALANCE TO EARN INTERESTTo earn interest on any day, the Collected Balance must be at least $100 as of theend of that day.

STATEMENT CYCLE Monthly cycle

OTHER FEESSee separate schedule as amended from time to time.

TRANSFER LIMITATIONS During any calendar month, a total of no more than 6 withdrawals and transferscan be made to another account with M&T or to a third party by means of apreauthorized or automatic transfer or telephonic (including data transmission)agreement, order or instruction (including Internet, online banking and othercomputer transactions), or by debit card or similar order payable to a third party.No withdrawal can be made by check.

ACCESS AT ELECTRONIC FACILITIESYes

NOT TRANSFERABLE (as defined in 12 CFR 204)

*The Annual Interest Rate will be set by M&T at M&T’s discretion withoutreference to any index, formula or schedule.

COMMERCIAL CERTIFICATE OF DEPOSIT

KIND OF ACCOUNT Automatically Renewable Time Deposit

ACCOUNT CAN BE OPENED BY All Non-Consumer

MINIMUM OPENING DEPOSIT $500

MATURITY NOTICEYou will receive a maturity notice with information about the initial term, firstmaturity date, and how you can inquire about the Annual Interest Rate,* AnnualPercentage Yield** and Daily Percentage Rate*** for the Account.

LEDGER BALANCE At the end of any Business Day, consists of:

1. All funds deposited in and credited to the Account and not yet withdrawnfrom and charged against it; plus

2. All interest credited to the Account before that day and not yet withdrawnfrom and charged against it.

The Ledger Balance on a Saturday, Sunday or federal holiday will be the LedgerBalance as of the end of the previous Business Day.

BALANCE ELIGIBLE TO EARN INTEREST As of any time during any day, will consist of:

1. The Ledger Balance; plus 2. All interest earned on funds in the Account before that day, but not yet paid.

AVAILABLE BALANCE The balance available for withdrawal in accordance with the applicable AvailabilityDisclosure for Commercial Deposit Accounts provided to the Customer.

FREQUENCY OF COMPOUNDING AND PAYMENT OF INTEREST****

Interest is compounded daily and paid at the end of the day before each maturitydate and, if requested, approximately every month, every 3 months, every 6 months,or every year.

INTEREST COMPUTATION For each day, the Balance Eligible to Earn Interest as of the end of that daymultiplied by the Annual Interest Rate in effect on that day, divided by 365 (or 366in a leap year).

METHOD OF PAYMENT OF INTEREST As requested:

1. By crediting the Account, or 2. By crediting the Account followed immediately by transfer to an eligible

Account with M&T, or 3. By crediting the Account followed immediately by withdrawal and payment

by check.

TRANSACTION LIMITATIONSCertain deposit and withdrawal limitations apply to your Account. After theAccount is opened, no deposit may be made to your Account except on a maturitydate or as permitted during a grace period. Please see the “Penalty for EarlyWithdrawal” section for information about withdrawals.

PENALTY FOR EARLY WITHDRAWAL You have contracted to keep your funds on deposit for the term of your Account.This means that you may not withdraw deposited funds from the Account exceptat maturity, as permitted during a grace period (see the “Renewal Policy/AutomaticRenewal” section), or as provided in these terms.

In our discretion, we may allow you to withdraw money from the Account attimes other than at maturity or as permitted during a grace period. However, if youmake such a withdrawal, we may charge you a penalty in our discretion unless thewithdrawal is due to an owner’s death or incompetency as determined by a courtor administrative body.

The penalty will be:1. $50 plus 182 days’ interest on the amount of the withdrawal, computed

without compounding, at the Annual Interest Rate in effect when thewithdrawal is made, if the term of the Account during which the withdrawalis made is more than 364 days; or

2. $25 plus 91 days’ interest on the amount of the withdrawal, computedwithout compounding, at the Annual Interest Rate in effect when thewithdrawal is made, if the term of the Account during which the withdrawalis made is less than 365 days.

Please note that the penalty may invade principal, and the term of your Accountis the period of time during which you have contracted to keep your funds ondeposit from the opening deposit or renewal date until the next maturity date.

During each term of your Account, you may withdraw interest that has beencredited to your Account during that term. However, after the next maturity dateof your Account, that interest cannot be withdrawn from your Account without ourconsent or as permitted during a grace period.

We can close the Account any time the balance falls below the minimum depositthat was required to open that Account or, if we automatically renew the Account,that was required to open the same type of Account on the most recent maturitydate of the Account. We can require the closing of your Account as a condition ofallowing any withdrawal from it.

RENEWAL POLICY/AUTOMATIC RENEWALYour Account will renew automatically on each of its maturity dates unless, beforethat maturity date, you notify us not to renew it, we send you notice that we willnot renew it, or we are prohibited by applicable law from renewing it. Each timeyour Account automatically renews, there will be a grace period of 10 calendardays after the maturity date (“grace period”), during which you may make awithdrawal without penalty, make a deposit, or change the length of your term.Funds withdrawn from your Account during the grace period will not earn anyinterest during the grace period. The interest rate for your Account at the time ofrenewal will be set by us at our discretion and will not be tied to any index.

If your Account does not automatically renew for any reason, on its maturitydate (or on our next Business Day if that maturity date is not a Business Day),money in the Account will stop earning interest unless you renew the Account orreinvest the money.

CHANGE OF TERM On or within 10 days after any maturity date of the Account.

NOT TRANSFERABLE (as defined in 12 CFR 204)

****The Annual Interest Rate is subject to change each time the Account isrenewed and will be set by M&T at M&T’s discretion without reference to anyindex, formula or schedule.

****The Annual Percentage Yield is an annual rate that is subject to change eachtime the Account is renewed and is based on the assumptions that the Accountis renewed on each maturity date, that interest earned on the funds in theAccount is not withdrawn from the Account and that the Annual Interest Ratefor the initial Term does not change for subsequent Terms.

****The Daily Percentage Rate is subject to change each time the Account isrenewed.

****The availability of particular periodic interest payment options for the Accountdepends on the Term of the Account. Not all of the interest payment optionsare available for all Terms.

11 B

12 B

This notice provides general information concerning what may occur and whatfees may be charged when you withdraw, or try to withdraw, more money fromyour checking account* than you have available for withdrawal from that account.More detailed information on these and other important topics may be found inthe Commercial Deposit Account Agreement, applicable fee schedule, ElectronicBanking Agreement for Businesses, and Availability Disclosure for CommercialDeposit Accounts.

MEANING OF SOME TERMS WE USE IN THIS NOTICE

A Debit Item means any withdrawal, transfer or other transaction made orattempted including, but not limited to, any withdrawal, transfer or other transactionmade or attempted by check, in person, ATM or other electronic means.

An Overdraft Arrangement means either (i) a line of credit account tied to youraccount or (ii) another account you have with us that is linked to your account suchthat it covers overdrafts.

GENERAL INFORMATION ABOUT OVERDRAFTS

When we receive a Debit Item for payment from your account and your accountdoes not contain sufficient available funds to pay that Debit Item, we may decideto pay the Debit Item or not to pay it.** We make this decision in our sole discretionand our decision to pay a particular Debit Item does not obligate us to pay otherDebit Items if your account does not contain sufficient available funds to coversuch other Debit Items. If your account becomes overdrawn (that is, has a negativebalance), you must immediately pay to us the total amount overdrawn.

INSUFFICIENT FUNDS (NSF)/OVERDRAFT FEEIf you withdraw, or try to withdraw, more money from your account than you haveavailable for withdrawal from that account, you will be charged an insufficientfunds (NSF)/overdraft fee*** unless the money is paid under an OverdraftArrangement.** This is true regardless of:

1. Whether we pay or decline to pay the Debit Item; or 2. How you withdraw or attempt to withdraw the funds.

EXTENDED OVERDRAFT FEEIn addition to any insufficient funds (NSF)/overdraft fees and negative availablebalance charges*** that may apply to your checking account, if we pay a DebitItem and, as a result, your checking account becomes overdrawn (that is, thebalance is negative) or becomes further overdrawn, you will be charged a single$40 extended overdraft fee after 5 consecutive business days if the account remainsoverdrawn.

CHANGES TO INSUFFICIENT FUNDS (NSF)/OVERDRAFT OR EXTENDED OVERDRAFT FEES

If we change the amount of or manner of assessing our insufficient funds(NSF)/overdraft fees or extended overdraft fees or implement any new fees inconnection with overdrafts, we will send a notice explaining this change to you.

* This notice applies only to Commercial Checking, M&T Business InterestChecking, Non-Profit Checking, M&T Advanced Business Checking, M&TSimple Checking for Business, M&T Medical Services Checking, M&TProfessional Services Checking, Business FlexChecking, BusinessProChecking, Business Sweep Checking I, and Business Sweep Checking II.

** NOTE: If you have an Overdraft Arrangement with us that fully covers theamount of any Debit Item posted against insufficient available funds, the DebitItem will be paid, the account will not be treated as overdrawn and theinsufficient funds (NSF)/overdraft fees and extended overdraft fees andnegative available balance charges will not be assessed. However, you mustpay any charges related to using that Overdraft Arrangement.

*** Insufficient funds (NSF)/overdraft fees and negative available balance chargesare described in the fee schedule and Specific Features and Terms for youraccount, respectively.

NOTICE REGARDING OVERDRAFTSBUSINESS CHECKING ACCOUNTS*

13 B

Funds deposited in a commercial account at M&T Bank become available forwithdrawal according to the following schedule. Prior to the availability date, fundsdeposited are unavailable for withdrawal in the form of cash or for payment ofchecks, except for instances marked by an asterisk below.

DETERMINING THE AVAILABILITY OF A DEPOSIT

The availability of your deposit is counted in business days from the day of yourdeposit. Every day is a business day except Saturdays, Sundays and federalholidays. If you make a deposit before our business day cutoff time on a businessday that we are open, that day will be considered to be the day of your deposit.However, if you make a deposit after our business day cutoff time, or at any timeon a day that is not a business day or is a day we are not open, we will consider thedeposit made on the next business day we are open. Our business day cutoff timemay vary by location, but is no earlier than 2 p.m. for deposits made to a branchemployee, and no earlier than noon for deposits made at our ATMs. Please ask forspecifics at your branch.

The availability schedule depends on the type of deposit, as explained below.

SAME-DAY AVAILABILITY Funds from the following deposits are available on the same business day as theday we receive the transfer or deposit:• Cash.• Wire transfers via Fedwire or CHIPS.• ACH credit entries in which a party initiates a transfer of funds from its account

to your account, including electronic direct deposits such as payroll and SocialSecurity payments; however, funds received for deposit by means of aninternational ACH transaction (IAT) may not be made available until certainmonitoring and review procedures are completed and, therefore, may not be madeavailable on the same business day as we receive the transaction.

NEXT-DAY AVAILABILITYFunds from the following deposits are available on the first business day after theday of your deposit:• Checks drawn on M&T Bank.*• U.S. Treasury checks that are payable to your company.• Traveler’s checks.• Federal Reserve Bank checks, Federal Home Loan Bank checks and postal

money orders, if these items are payable to your company.If the item is payable to your company, and you make the deposit in person to

one of our employees, using a special deposit slip available from the customerservice representatives at our branch offices, funds from the following deposits arealso available on the first business day after the day of your deposit:• Checks drawn by the state or by a unit of the local government in the state in

which the deposit is made.• Cashier’s, certified or teller’s checks.

*Funds from deposits of checks drawn on M&T Bank, other than controlleddisbursement checks, will be available on the same business day as the day wereceive the deposit to pay checks and certain other items drawn on your account.(Funds from the deposit of controlled disbursement checks drawn on M&T Bankare available on the first business day after the day of your deposit to pay checksdrawn on your account. A controlled disbursement check drawn on M&T Bank –which is a check drawn on either a Corporate Checking Account or a CommercialChecking Account that has controlled disbursement services – is distinguishablefrom other checks drawn on M&T Bank by its 9-digit routing number located atthe bottom of the check. If the routing number on a check drawn on M&T Bankis 021907577, 221370632, 031100173, 031318619 or 055000110, that check is acontrolled disbursement check. Checks drawn on M&T Bank that have differentrouting numbers are not controlled disbursement checks.)

OTHER CHECK DEPOSITSThe availability of funds from the deposit of other domestic checks depends on

whether the check is a Category A or Category B check. To see whether a checkis classified as Category A or Category B, look at the routing number on the check.The routing number appears as the first group of encoded numbers on the bottomof a personal check, and as the second group of encoded numbers on the bottomof a business check. Find the first four digits of the routing number on your checkand if they are listed in the chart, the check is a Category A check. If they are notlisted in the chart, the check is a Category B check.

For example, if the first four digits of the routing number are 0220, then thecheck is a Category A check; if the first four digits of the routing number are 1250,since they do not appear in the chart, the check is a Category B check.

Some checks are marked “payable through” and have a four- or nine-digitnumber nearby. For these checks, use the four-digit number (or the first four digitsof the nine-digit number), not the routing number on the bottom of the check, todetermine if these checks are Category A or Category B checks. For example, ona credit union share draft marked “payable through” use the four-digit number (orthe first four digits of the nine-digit number) following the name and location ofthe credit union.

Our policy is to make funds from these checks available as follows:1. Category A checks. The funds from a deposit of Category A checks will be

available on the first business day after the day of your deposit.For example, if you deposit a Category A check of $700 on a Monday, $700 of

the deposit is available on Tuesday.2. Category B checks. The first $250 from a day’s deposits of Category B checks

will be available on the first business day after the day of your deposit. Theremaining funds will be available on the second business day after the day ofyour deposit.For example, if you deposit a Category B check of $700 on a Monday, $250 of

the deposit is available on Tuesday. The remaining $450 is available on Wednesday.If you deposit checks from both of the above categories, the funds from your

Category A checks, or $250, whichever is greater, will be available on the firstbusiness day after the day of your deposit.

DEPOSITS AT AUTOMATED TELLER MACHINES

An automated teller machine (ATM) is an electronic facility that either is usedwithout the assistance of an operator or is used with the assistance of an operatorsuch as a retail store clerk. An ATM we own or operate is called a proprietary ATM.An ATM we do not own or operate is called a non-proprietary ATM.

PROPRIETARY ATM DEPOSITSFunds from deposits made at proprietary ATMs are available in accordance withthe normal schedule set forth above.

NON-PROPRIETARY ATM DEPOSITSDeposits to your account are not permitted to be made at non-proprietary ATMs.

EXCEPTIONSAvailability of funds from check deposits may be delayed under the followingcircumstances:• If M&T doubts that a particular check will be paid; for instance, if

• the check has previously been returned unpaid; or• the check bears multiple endorsements.

• If deposits of checks and other items total more than $5,000 on any one day.

AVAILABILITY DISCLOSURE FOR COMMERCIAL DEPOSIT ACCOUNTS

Category A

0110 0210 0212 0213 0214 0219

0220 0223 0260 0280 0310 0311

0312 0313 0319 0360 0410 0420

0430 0432 0433 0434 0440 0510

0514 0519 0520 0521 0522 0530

0539 0540 0550 0560 0570 0610

0660 0810 0830

2110 2210 2212 2213 2214 2219

2220 2223 2260 2280 2310 2311

2312 2313 2319 2360 2410 2420

2430 2432 2433 2434 2440 2510

2514 2519 2520 2521 2522 2530

2539 2540 2550 2560 2570 2610

2660 2810 2830

14 B

• If your account has been overdrawn repeatedly in the last six months and theoverdrafts were not paid with funds that were lent under a line of credit accountor made available from another deposit account you have with us that is linkedto your account as part of an overdraft arrangement.

• If there is an emergency, such as failure of communications or computerequipment.M&T will notify you if such an exception hold applies to a check deposited in

your account. The notice will explain when the funds will be available. They willgenerally be available no later than the fourth business day after the day on whichthey would otherwise have been available.

HOLDS ON OTHER FUNDS (CHECK CASHING; OTHER ACCOUNTS)

If M&T cashes a check which is drawn on another bank, or makes funds from sucha check available to you immediately upon deposit, a hold for a correspondingamount may be placed on available funds on deposit in one of your M&T accounts.The hold will be released on the business day on which the funds would havebecome available according to the schedule set forth above.

SPECIAL RULES FOR NEW ACCOUNTSIf your company is a new customer at M&T, the following special rules will applyduring the first 30 days your account is open:

Funds from wire transfers via Fedwire or CHIPS and ACH credit entries to youraccount will be available on the same business day on which M&T receives thetransfer with complete instructions.

Funds from deposits of cash, checks drawn on M&T Bank and the first $5,000of a day’s total deposits of checks drawn by the state or by a unit of the localgovernment in the state in which the deposit is made, cashier’s, certified, teller’s,traveler’s and federal government checks will be available on the first business dayafter the day of deposit if the deposit meets certain conditions. For example, thechecks must be payable to your company and may require a special deposit slip.The excess over $5,000 will be available on the seventh business day after the dayof deposit.

Funds from all other check deposits will be available on the fourth business dayafter the day on which they would otherwise have become available.

OTHER EXCEPTIONSThis availability schedule does not affect M&T’s right to refuse to accept an itemfor deposit or M&T’s right to charge your company’s account or otherwise obtaina refund from you for any item that is not fully paid, regardless of the reason fornonpayment.

INSUFFICIENT FUNDS (NSF)/OVERDRAFTFEES ASSESSED BASED ON BALANCE

AVAILABLE FOR WITHDRAWALSubject to and in accordance with the fee schedule applicable to your checking orsavings account, we will charge an insufficient funds fee or overdraft fee whenyou make or attempt to make a transaction but do not have sufficient availablefunds to pay for the transaction. Funds subject to hold or otherwise encumberedfor any reason are not available for withdrawal or payment, including funds pledgedas collateral for indebtedness, subject to legal process (e.g., tax levy or restraint),held to pay for a transaction made using a debit card, or held to make apreauthorized payment on a line of credit or online bill payment.

15 B

MEANING OF SOME TERMSIn this agreement (1) “we,” “us,” “our” and “ours” mean M&T Bank, One M&TPlaza, Buffalo, New York 14203; (2) “you” and “your” mean the sole proprietoror business entity issued one or more access devices pursuant to an application forsame made to us by such sole proprietor or business entity; (3) “your card” meanseach M&T ATM Card for Business and each Visa® debit card tied to a comm ercialdeposit account with us that we have issued to someone who has been authorizedby you to use the card, and any Virtual Card that we have issued to someone whohas been authorized by you to use the Virtual Card; (4) “our VRU” means theM&T Business Tele phone Banking Center auto mated voice response unit; (5)“access device” means your card, card number, card data, or such other informationassociated with your card that is used to access your account; (6) “your PIN” meansthe secret personal identi fication number assigned to an authorized user of yourcard; (7) “your Checking Account” means any commercial checking account orNOW account with us to which your card is linked; (8) “your Savings Account”means any commercial savings account with us to which your card is linked; (9)“your Line of Credit Account” means any commercial line of credit account withus to which your card and your Checking Account or your Savings Account aretied; (10) your “Virtual Card” means the multi-digit number issued to you that canbe used alone or in conjunction with other information (such as a PIN) to identifyyou for purposes of accessing our VRU or enrolling in certain of our services; and(11) “E-Banking Services” means electronic banking services not provided atelectronic facilities covered by this agreement which we may make available toyou from time to time via the Internet or other electronic medium, including,without limitation, M&T Online Banking for Busi ness. Except as set forth herein,the terms and conditions of such E-Banking Services are not covered by thisagreement.

INTRODUCTION TO ELECTRONIC BANKING SERVICES

We offer a variety of services that allows you and your authorized employees,agents and representatives to access certain of your commercial deposit accountswith us and/or your commercial credit accounts with us or with our affiliates, bywhat is called an electronic funds transfer (“EFT”). For purposes of this agreement,an EFT is a transfer of funds from or to a commercial deposit account you maintainwith us or a commercial credit account you maintain with us or with our affiliatesthrough use of your access device at electronic facilities covered by this agreement.This agreement describes the EFT and other services available to you through useof your access device and sets forth the terms and conditions applicable to youruse of all such services, including, among other things, your and our respectiverights and liabilities that arise from such use. By using your access device or PINor authorizing someone else to use either, you agree to be bound by all terms andconditions of this agreement, and with regard to E-Banking Services, you agree tobe bound by all of the terms and conditions of the applicable E-Banking Servicesagreement.

AUTHENTICATIONYou acknowledge that use of an access device and, where required, correspondingPIN (i) is the equi valent of the signature of the authorized user of the access device,(ii) authenticates and validates the directions given at any electronic facility coveredby this agreement or the directions given in connection with any E-BankingServices as the directions of an authorized user of the access device to the sameextent as the actual signature and proof of identity of such authorized user of theaccess device and (iii) identifies the party using the access device and, whererequired, corresponding PIN as the authorized user of the access device, or assomeone who has been delegated the rights of an authorized user, with the powerand authority to enter into contracts on your behalf, including entering intocontracts over the Internet or other electronic medium, and to transact businessand bind you as set forth herein or in any applicable E-Banking Services agreement.You further acknowledge that the use of the PIN in conjunction with the accessdevice is a commercially reasonable security procedure for use in authenticatingtransactions or enrolling in E-Banking Services.

ISSUANCE OF CARDS AND PINSWe will deliver to you the number of cards that you request in writing. A separatecard will be issued to each person authorized by you to use your card. You mustfurnish us with the full name of each person whom you authorize to use your card.Each of your cards will be imprinted with your name and the name of the employee,agent or other representative authorized to use such card. Each authorized user ofyour card must sign his or her name on the reverse side of the card issued to suchauthorized user. A separate PIN will be assigned to each card and told to theauthorized user of such card, or, each authorized user, if he or she prefers, canchoose his or her own PIN.

ELECTRONIC FACILITIES COVERED BY THIS AGREEMENT

Electronic facilities covered by this agreement are our own automated tellermachines (ATMs), electronic facilities owned or operated by any of our affiliates,our VRU, ATMs and point-of-sale terminals in networks of shared electronicfacilities in which we directly or indirectly participate (for example, the PLUS®,STAR® or Visa network) and any means of electronic communication throughwhich you may communicate instructions to make transfers to or from your accountusing your access device (e.g., telephone or Internet).

USE OF YOUR ACCESS DEVICEThe type of transactions that a user of your access device will be permitted toperform and where they can be performed depends on whether your card is anM&T ATM Card for Business, a Visa debit card or an M&T Virtual Card, and, ifyour card is an M&T ATM Card for Business, whether you have the “BalanceInquiry” option or the “All Activity” option for the authorized user of your card.The Visa debit card and the All Activity option for the M&T ATM Card forBusiness are available to an authorized user of your card only if such person is alsoan authorized signer on each deposit account and credit account linked to yourcard.

A. M&T ATM CARD FOR BUSINESS1. Balance Inquiry Option. If you elect this option for an authorized user

of your card, such authorized user will be able to (a) make a deposit inyour Checking Account or your Savings Account, (b) make a deposit ina comm ercial deposit account of yours with us other than your CheckingAccount and Savings Account, (c) find out the balance of your CheckingAccount, your Savings Account or your Line of Credit Account, (d) payan amount owing under an account with us or someone else for whom wecollect payments, and (e) find out the amount of credit available underyour Line of Credit Account.

2. All Activity Option. If you elect this option for an auth orized user of yourcard, such authorized user will be able to (a) make a withdrawal of cashfrom your Checking Account or your Savings Account, (b) make a depositin your Checking Account or your Savings Account, (c) make a transferto an account linked to your card, (d) make a transfer from an accountlinked to your card to another account that you or someone else has withus or with another bank, (e) make a deposit in a commercial depositaccount of yours with us other than your Checking Account and yourSavings Account, (f) find out the balance of your Checking Account, yourSavings Account or your Line of Credit Account, (g) pay an amount owingunder an account with us or someone else for whom we collect payments,(h) find out the amount of credit available under your Line of CreditAccount, and (i) obtain credit under your Line of Credit Account to borrowmoney in cash.

B. VISA DEBIT CARDAn authorized user of your Visa debit card will be able to perform all of thetransactions listed in the paragraph of this agreement entitled “All ActivityOption.” In addition, the auth orized user will be able to make a transfer fromyour Checking Account to pay for the purchase or lease of goods or servicesat any merchant that honors Visa debit cards without the use of an elec tronicfacility.

ELECTRONIC BANKING AGREEMENT FOR BUSINESSES

16 B

Please note, whether your card is an M&T ATM Card for Business or a Visa debitcard, not all types of transactions that an authorized user of your access device ispermitted to perform can be performed at all electronic facilities at which youraccess device may be used. For example, there may be restrictions on the types oftransactions that can be made with your card at certain of our ATMs or at any otherATM or point-of-sale terminal at which your card may be used. Also, telephonetransactions made with your access device using our VRU are limited to transfersbetween your Checking Account and your Savings Account as well as betweenthose accounts and your Line of Credit Account.

C. VIRTUAL CARDThe Virtual Card can only be used to access our VRU and to enroll in andaccess certain services at our E-Banking Service, M&T Online Banking forBusiness.

TRANSACTION LIMITATIONS1. During any day, the total transactions in which your access device is used at

an ATM to obtain cash, whether the cash is obtained through a withdrawalfrom your Check ing Account or your Savings Account or through anothertransaction (for example, a transaction in which a check is cashed or credit isobtained under your Line of Credit Account to borrow money in cash) cannotexceed (i) 9 in number (15 if your card is a Visa debit card) or (ii) $500 inamount ($1,000 if your card is a Visa debit card). We may, but we do not haveto, from time to time allow trans actions that exceed these limits.

2. During any day, the total transactions in which your access device associatedwith your Visa debit card is used to access your Checking Account to (a) payfor a purchase of goods or services, (b) pay bills for services provided bycompanies authorized to process bill payment transactions through STAR,Visa or other networks in which we participate or (c) perform a cash advancethrough Visa, cannot exceed (i) 20 in number or (ii) $7,500 in amount. Wemay, but we do not have to, from time to time allow transactions that exceedthese limits.

3. Deposits in or transfers to your Checking Account or your Savings Accountat some shared electronic facilities may be limited by the operators of thosefacilities or by the networks in which they participate.

4. No coins may be deposited and no more than 50 items may be deposited at anyone time at any electronic facility covered by this agreement at which depositsmay be made.

5. If you have multiple accounts of the same type linked to your card (i.e.,multiple checking accounts), some locations at which you can use your accessdevice may not offer the ability to select which of those accounts you wishto use to effect your transaction, and some locations may offer the ability toselect some, but not all, of those accounts. When no such choice is offered,the transaction will be processed in connection with your primary account,as designated by you and reflected in our records.

6. During any calendar month, no more than 6 withdrawals can be made fromyour Savings Account by a check, by a preauthorized, automatic or telephonictransfer to another deposit account with us or to a third party (including atransfer made via the Internet using E-Banking Services) or by a transfer toa third party made using your access device (for example, a transfer to paythe purchase price of goods or services).

7. To help avoid disruptions in the use of your access device, please let us knowin advance if you are planning to travel away from home. We may (but arenot obligated to) prohibit, restrict or limit the use of your access device if wesuspect potential or increased risk of fraud, unauthorized transfers, or otherillicit activity. In addition, we may (in our discretion) prohibit, restrict or limitthe use of your access device in some jurisdictions outside the United States.

Other limitations on the use of your access device can be imposed. For purposesof any limitation on the use of your access device, a day does not necessarily haveto begin at midnight. For reasons of security, we are not describing exactly whenthe day begins for purposes of any limitation on the use of your access device.

FOREIGN TRANSACTIONSIf your access device is used to conduct a transaction in a foreign country, thetransaction may be in a foreign currency. For purchases made through the Visanetwork with your access device, Visa will convert the purchase price into a U.S.dollar amount. The conversion rate will be (a) a rate selected by Visa from therange of rates available in wholesale currency markets on the date (based onGreenwich Mean Time) Visa receives the transaction for processing, which ratemay vary from the rate Visa itself receives, or (b) the government-mandated ratein effect for the date (based on Greenwich Mean Time) on which Visa receives thetransaction for processing. For other transactions, we will post the transaction inU.S. dollars based on the currency exchange rate in effect on the day we settle forthe transaction. The currency exchange rate may be different on that day than onthe day of the transaction. Also, there may be special currency exchange charges,which you agree to pay. We have no control over the exchange rate or the date orplace of exchange or the amount of any special currency exchange charges.

MERCHANT TRANSACTIONSIf your access device is used to pay for goods or services and/or to obtain cash backfrom a merchant or service provider, you are requesting that we withdraw funds inthe amount of such payment (including any cash received from the merchant orservice provider) from your Checking Account or your Savings Account anddirecting us to pay such funds to the merchant or service provider. We will haveno liability if a merchant or service provider refuses to honor your access device.We are not responsible for any injury to you or to anyone else caused by any goodsor services purchased or leased with your access device. You are responsible forresolving all disputes concerning the purchase or lease of goods or services withthe merchant or service provider who accepted your access device. We are notsubject to any claim or defense you may have regarding any dispute with anymerchant or service provider involving a transaction conducted with the use ofyour access device.

TELEPHONE TRANSACTIONSWith a Visa debit card, a Virtual Card or an M&T ATM Card for Business that isissued with the All Activity option, your access device may be used by telephonethrough our VRU to make transfers of funds between accounts linked to your card.To initiate a transfer of funds through our VRU, you must use a touchtone telephoneand have available your access device and any other information we may requireto establish the identification of the authorized user of your access device. You areresponsible for the accuracy and completeness of all information and directionssupplied to us in connection with a transaction made using our VRU. For yourprotection and ours, you agree that we may, but we do not have to, record yourinstructions for EFTs made using our VRU.

TIME OF INFORMATIONWhen your access device is used at any electronic facility covered by this agreementto find out the balance of your Checking Account or your Savings Account or theamount of credit available under your Line of Credit Account, the information willgenerally, but not necessarily, be as of a time no earlier than the start of our mostrecent business day beginning before the inquiry is made.

OBLIGATIONS WITH RESPECT TO ACCESS DEVICES AND PINS

You agree to safeguard your access device(s) and PIN(s) issued to authorized accessdevice users pursuant to this agreement and to cause each person you authorize touse or to whom you give your access device and/or corresponding PIN to safeguardyour access device and/or corresponding PIN by adopting security measures toprevent any unauthorized person from obtaining possession of your access deviceand/or corresponding PIN, and by taking all reasonable precautions, including, butnot limited to: (i) not keeping your access device and corresponding PIN in thesame place; (ii) not writing the PIN on your card or on any document carried alongwith your card or in the area of your PC that may be used to engage in E-BankingServices; (iii) memorizing the PIN and destroying or keeping under lock and keyany paper on which the PIN is written; and (iv) not disclosing any PIN to anyoneexcept any person to whom your access device to which the PIN applies is givenor such person that you have authorized to gain access to, or enroll in, E-BankingServices. If any person for whom you have requested a card ceases to have yourpermission to use your card, whether because of termination of employment orotherwise, you must return that card to us or request that we deactivate the cardand PIN immediately. You must do this even if the person to whom your card isissued is an authorized signer on any deposit account or credit account linked toyour card and at your request, we have noted in our records that such person’ssignature authority over any such account has been terminated. If an authorizeduser of your Visa debit card, your M&T ATM Card for Business issued with theAll Activity option or your Virtual Card ceases to be an authorized signer on anydeposit account or credit account linked to your card, you agree that we may, butshall have no obligation to, de activate such person’s card and PIN. Deacti vationof the card and the PIN shall not void or otherwise repudiate any agreement we mayhave entered into with you for E-Banking Services in reliance on the PIN andaccess device prior to the date of such deactivation unless you separately requestthat we terminate such E-Banking Services in accordance with the terms of therespective E-Banking Services agreement. If any card, access device or PINassociated with your card (or any cellular phone or other device on which youraccess device is stored) is or is believed by you to be lost, stolen or in the possessionof any un authorized person, or if you believe that any transaction involving yourChecking Account or your Savings Account or an E-Banking Service may havebeen or may be made using your access device or the correspond ing PIN withoutyour authorization, or if you suspect there has been any compromise of any securitymeasures adopted to prevent unauthorized use of your access device or thecorresponding PIN, you must immediately notify us of that fact and we will de -activate the card and the corresponding PIN. You must notify us by telephoning1-800-724-1552, or by writing to M&T Bank, P.O. Box 767, Buffalo, New York14240-0767, Attention: M&T Business Tele phone Banking Center. Please note

17 B