Embed Size (px)

Citation preview

Colorado Health Care

Reform: The Path

Ahead

Senator Irene Aguilar, MD

Where we’ve been

Distribution of Health Plan Enrollment for Covered Workers, by Plan Type, 1988-2012

Note: Information was not obtained for POS plans in 1988. A portion of the change in plan type enrollment for 2005 is likely attributable to incorporating more recent Census Bureau estimates of the number of state and local government workers and removing federal workers from the weights. See the Survey Design and Methods section from the 2005 Kaiser/HRET Survey of Employer-Sponsored Health Benefits for additional information.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2012; KPMG Survey of Employer-Sponsored Health Benefits, 1993, 1996; The Health Insurance Association of America (HIAA), 1988.

2%

<1%

1%

1%

1%

Average Annual Premiums for Single and Family Coverage,

1999-2012

* Estimate is statistically different from estimate for the previous year shown (p<.05).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2012.

$15,745*

Cumulative Increases in Health Insurance Premiums, Workers’ Contributions to Premiums, Inflation, and

Workers’ Earnings, 1999-2011

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2011. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 1999-2011; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1999-2011 (April to April).

Job-based health insurance premiums rise sharplyBy Tony Pugh, McClatchy NewspapersPosted: 09/28/2011

Government Insurance

4 Million

CO Medicaid = 560,722

CHP + = 69,008

Government Insurance

4 Million

CO Medicaid = 560,722

CHP + = 69,008

2011: 48.6 Million Uninsured2011: 48.6 Million Uninsured

2011 Colorado:

829,180 uninsured

16% of population

2011 Colorado:

829,180 uninsured

16% of population

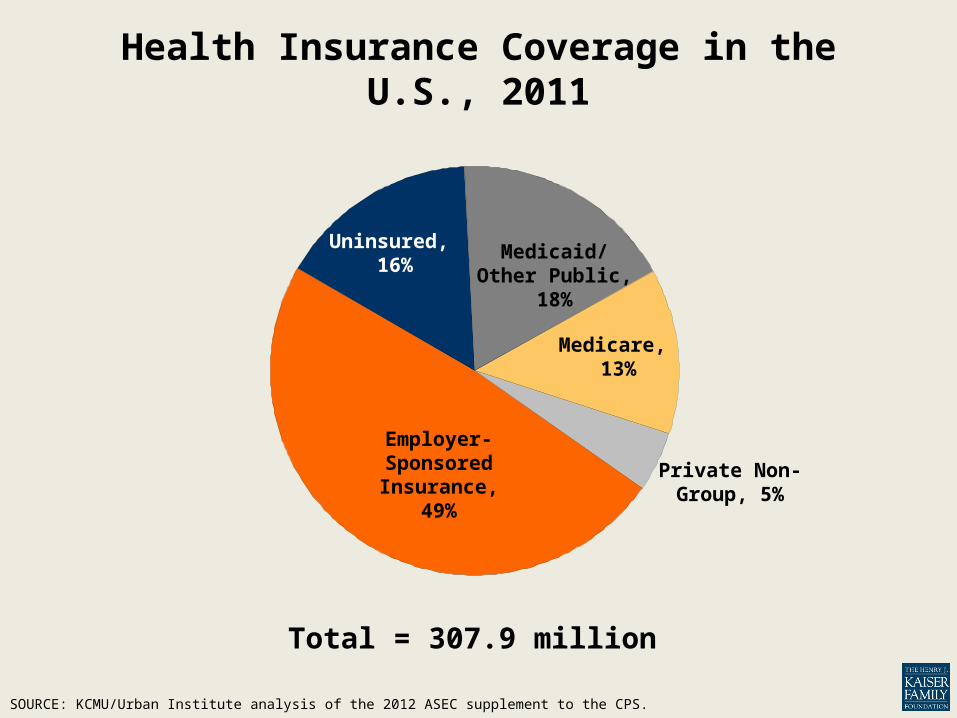

Health Insurance Coverage in the U.S., 2011

SOURCE: KCMU/Urban Institute analysis of the 2012 ASEC supplement to the CPS.

Total = 307.9 million

Employer-Sponsored Insurance,

49%

Medicaid/Other Public,

18%

Medicare, 13%

Private Non-Group, 5%

Uninsured, 16%

Where we’re going

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2010Prohibited RescissionProhibited denial of coverage to children with

pre-existing conditionsEliminated lifetime limits on coverageRequired Free Preventive CareAllowed children under 26 to stay on parents’

plans

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2010Medicare donut hole rebate of $250 Required insurance companies to justify

premium increases

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2011Implemented Medical Loss Ratio of 80/85%Prescription drug discounts for seniorsFree preventive care for seniorsCenter for Medicaid & Medicare InnovationIndependent Payment Advisory BoardCommunity First Choice Program

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2012-2013Streamline Administrative FunctionPayment reformIncrease Medicaid payment for Primary Care

and preventive health services

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2014Prohibits discrimination due to pre-existing

conditions or genderRequires the purchase of Insurance (individual

mandate) Eliminate annual limits on insurance coveragePremiums in the individual and small group markets

may vary only by family structure, geography, the actuarial value of the benefit, age (3:1) and tobacco use (1.5:1)

2013 Federal Poverty Levels

PATIENT PROTECTION AND AFFORDABLE CARE ACT

2014 (continued)Allows expansion of Medicaid to 133% FPLPremium Tax credits for 133 – 400% FPLCost sharing subsidies for those at < 250% FPLInsurance Exchanges are source for premium

assistance : Connect for Health Colorado1-855-PLANS-4-You

www.ConnectforHealthCO.com

Brings together buyers and sellers of insuranceCompare health insurance options and shop for

coverage that will take effect as early as January 1, 2014Open enrollment will continue until March 31, 2014.

Choice of up to 150 different private health insurance plans from ten carriers

Financial assistance based on income available to close to 500,000 Coloradans

Shoppers may claim the tax credit on their taxes or apply for an advance tax credit to use up-front to reduce the monthly premium Customer Service Center are available to guide the

processReviews and approves insurance products

(Qualified Health Plans )Essential health Benefits Plan

Small employers can create small group plans from as many as 92 health insurance plans provided by six carriers

For the first time, they can offer their employees a choice of health insurance carriers and health plans

Small employers can apply for tax credits based on the size and average wages of the business, to help cover the cost of health insurance premiums

Customer service representatives are available to help

As of October 4th

Over 15,000 accounts created

8,781 calls and chats in the Service Center

145,000 unique visitors

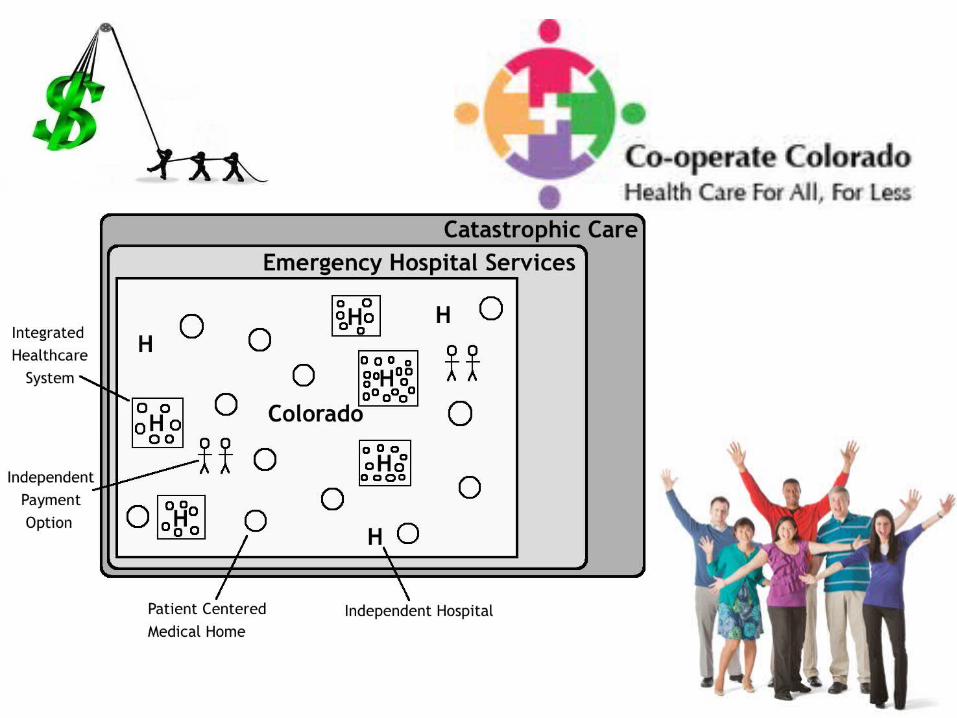

Colorado’s Next Steps:

1. Connect for Health Colorado – opened 10.1.13 Monitor for “gaming” of exchange

2. Medicaid will be expanded to 133% of FPL Identify ways to reduce Medicaid “churn”

3. Continue to work on Cost Control

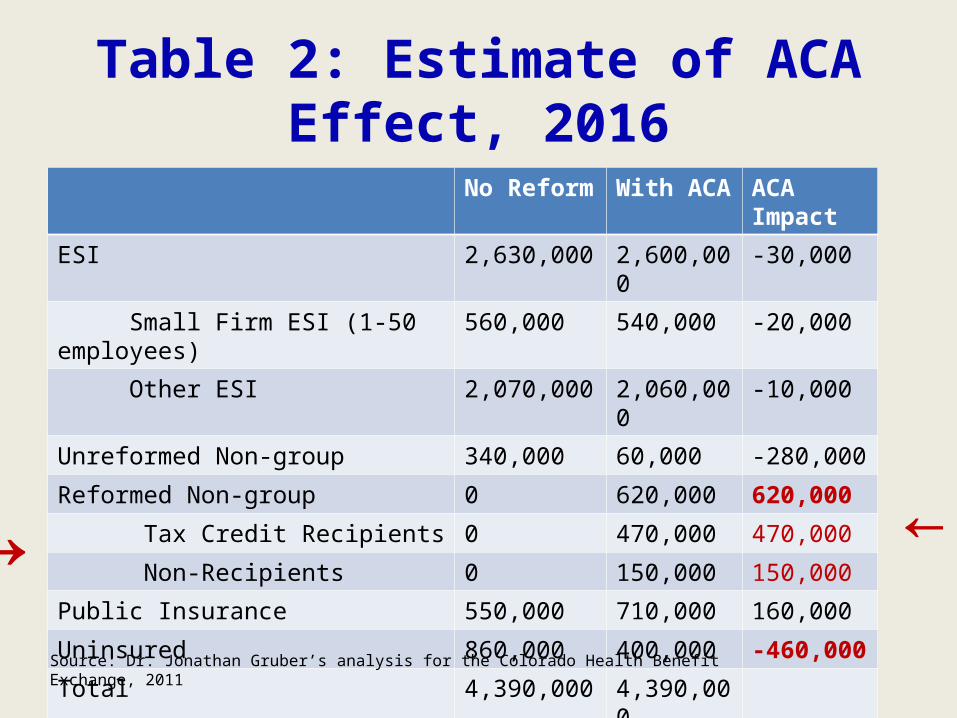

Table 2: Estimate of ACA Effect, 2016

No Reform With ACA ACA Impact

ESI 2,630,000 2,600,000 -30,000

Small Firm ESI (1-50 employees) 560,000 540,000 -20,000

Other ESI 2,070,000 2,060,000 -10,000

Unreformed Non-group 340,000 60,000 -280,000

Reformed Non-group 0 620,000 620,000

Tax Credit Recipients 0 470,000 470,000

Non-Recipients 0 150,000 150,000

Public Insurance 550,000 710,000 160,000

Uninsured 860,000 400,000 -460,000

Total 4,390,000 4,390,000→ →

→

Source: Dr. Jonathan Gruber’s analysis for the Colorado Health Benefit Exchange, 2011

Dr. Jonathan Gruber 9/16/11

22%

39%

10%

29%

24

Since 2006, the cost of the state’s insurance program has increased by 42 percent, or almost $600 million. According to an analysis by the Rand Corporation, “in the absence of policy change, health care spending in Massachusetts is projected to nearly double to $123 billion in 2020, increasing 8 percent faster than the state’s gross domestic product (GDP).”

ORIGINAL BY: John A. Nyman, PhDUniversity of Minnesota

27

US v. Other G7 Countries Updated

Canada France Germ. Italy Japan UK Avg USA

MD visits (2009)per capita

6.5 6.9 8.2 NA 13.2* 5.0 6.3 3.9

Hosp dischargesper 100 pop (2009)

8.4 17.0 26.3 NA NA 13.3 16.0 13.1

Avg hospitalLOS (2009)

7.7 5.2 7.5 NA NA 6.8 5.9 5.4

Hospital days per 100 population

144.0 83.2

HC spending (2010)

per capita (PPP)

$4,445

$3,974

$4,338

$2,964

NA $3,433

$3,831

$8,232

HC spending as % of GDP (2010)

11.4 11.6 11.6 9.3 NA 9.6 10.6 15.8

LE at birth (2010)

80.8 (08)

80.2 80.5 82 (09) 83 80 81.1 78.7

Infant deaths per 1000 live births (2010)

NA 3.6 3.4 3.4 2.3 4.2 3.4 6.1OECD website : http://stats.oecd.org/index.aspx

The spending per capita numbers were converted from the currency of the country to US dollars by a PPP index.

American Ingenuity at Work

Drug Prices for 30 Most Commonly Prescribed Drugs, 2006–07

US is set at 1.0

0.34

0.440.450.490.51

0.63

0.760.77

1.00

0.0

0.2

0.4

0.6

0.8

1.0

US CAN GER SWIZ UK AUS NETH FR NZ

Source: IMS Health.

New HampshireInsurers Disparate Payments

What is the Price? Range for What Insurance Pays to Health Care Provider Per Procedure

Colonoscopy Mammogram MRI (back)(Outpatient)

Insurer A 1,353 - 4,611 227 - 881 645 - 2,790

Insurer B 1,270 - 3,121 161 - 564 640 – 2,292

Insurer C 1,195 - 3,524 129 - 612 732 - 2,659

Source: CMWF analysis of data retrieved October 2010 from: http://www.nhhealthcost.org/costByProcedure.aspx

Advanced primary care networks

Variations Among Academic Medical CentersUCLA Mass

General Mayo Clinic

CMS Inpatient Quality Score

81.5 85.9 90.4

Source: Elliot Fisher, Dartmouth Medical School

Care Delivery & Spending, last 6 months of life

Total Medicare Spending

$50,522 $40,181 $26,330

Hospital Days

Physician Visits19.2

52.1

17.7

42.2

12.9

23.9Specialist/ Primary Care Ratio

2.9 1.0 1.0

Source: The Dartmouth Atlas of Health Care.

DENOMINATOR DEFINITION:A 20% random sample of the enrollment file for beneficiaries age 65-99 enrolled in both Medicare Parts A and B, selected on the basis of the terminal digits in the Social Security number. Patients enrolled in risk-bearing health maintenance organizations (HMOs) are excluded.ADJUSTMENTS:Rates are adjusted for age, sex and race using the indirect method, using the U.S. Medicare population as the standard. Gender-specific rates are age and race adjusted; race-specific rates are age and sex adjusted.

Medicare Payments per Enrollee, by Hospital Referral Region, 2009

Research shows significant variation in health care spending.

Massachusetts: Private, Medicare & Medicaid Payment for Professional Procedures

MinPrice

Max Price

Office Visit

$45 $330

MRI Brain

$104 $646

Colon-oscopy

$203 $1,045

Private Payer Payment Variation

Source: Massachusetts Division of Health Care Finance and Policy, Massachusetts Health Care Cost Trends: Price Variation in Massachusetts Health Care Services, May 2011.

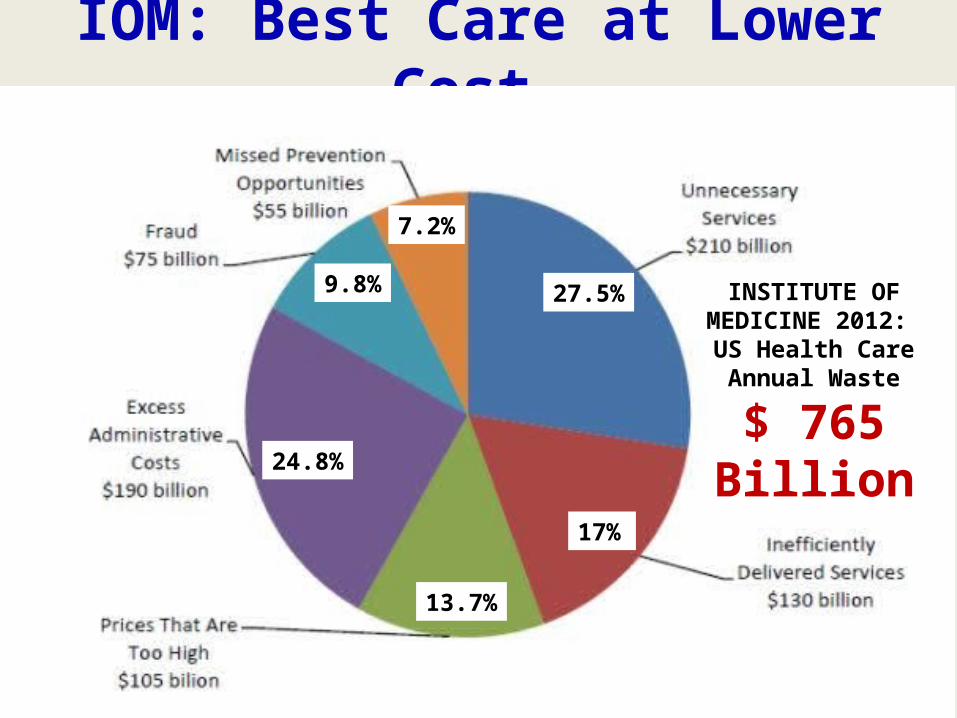

IOM: Best Care at Lower Cost

9.8%

7.2%

27.5%

17%

13.7%

24.8%

INSTITUTE OF MEDICINE 2012: US Health Care Annual Waste

$ 765 Billion

Determinants of Health

2011 U.S.

Healthcare Spending:

$2.7 Trillion

Number of U.S. Deaths from Behavioral Causes

Note: Dollar amounts in parentheses are the annual expenses per person in each percentile. Population is the civilian noninstitutionalized population, including those without any health care spending. Health care spending is total payments from all sources (including direct payments from individuals and families, private insurance, Medicare, Medicaid, and miscellaneous other sources) to hospitals, physicians, other providers (including dental care), and pharmacies; health insurance premiums are not included.

Source: Kaiser Family Foundation calculations using data from U.S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey (MEPS), Household Component, 2009.

Concentration of Health Care Spending in the U.S. Population, 2009

(≥$51,951) (≥$17,402) (≥$9,570) (≥$6,343) (≥$4,586) (≥$851) (<$851)

Perc

ent o

f Tot

al H

ealth

Car

e Sp

endi

ng

Distribution of Medicaid enrollment & expenditures by eligibility category,

FY 2010-2011

Figure 4. Share of Colorado population without health insurance coverage, alternative funding

programs, 2015-24.

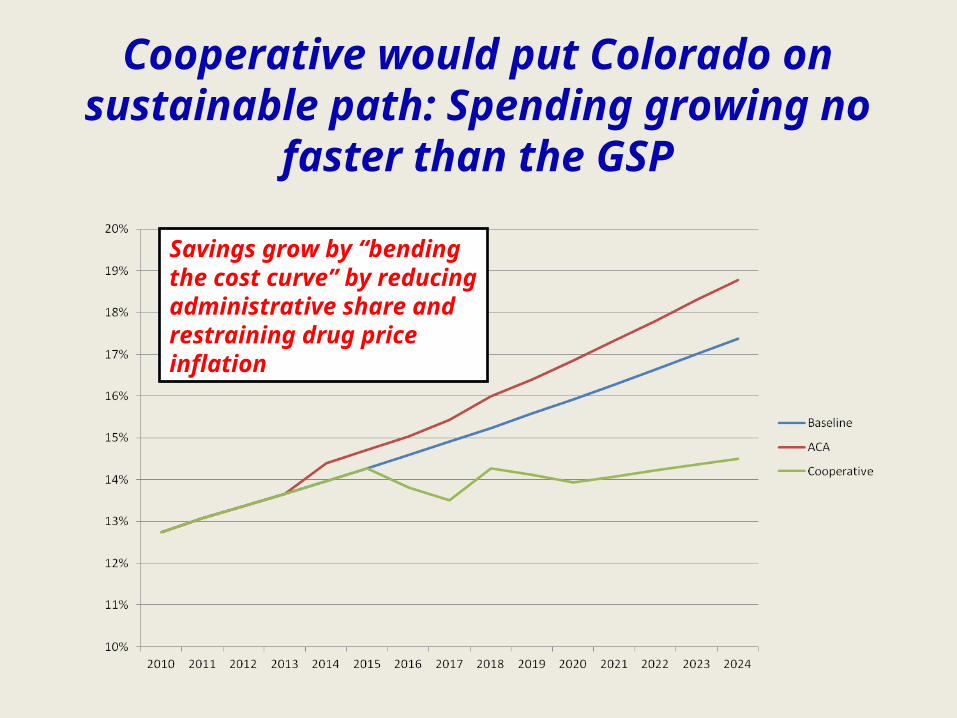

Cooperative would put Colorado on sustainable path: Spending growing no

faster than the GSP

Savings grow by “bending the cost curve” by reducing administrative share and restraining drug price inflation

Savings under the Cooperative come from reducing administrative waste

SAVINGS: 2016: $7.7 billion @ 16% 2024: $ 24 billion @ 28%