Embed Size (px)

Citation preview

www.colliers.comwww.colliers.com

US Real Estate Review 2007

COLL IERS INTERNATIONAL

Colliers Research Services Group is recognized as a knowledge leader in thecommercial real estate industry, and provides clients with valuable marketintelligence to support business decisions. Colliers researchers provide multi-level support across all property types, ranging from data collection to comprehensive market analysis.

Colliers Research has developed powerful technological tools to provideclients with valuable market intelligence. Our expansive databases housedetailed information on properties nationwide, including historical supply,demand, absorption data, and transaction comparables. Research uses thisinformation to produce quarterly surveys of office and industrial markets in over 70 North American metropolitan areas.

Colliers research reports provide standardized information for each market.Market Highlights reports based upon quarterly surveys include inventory,vacancy, absorption and rental rates in side-by-side comparisons for North American markets as well as quarter-to-quarter comparisons and aggregated national statistics. Investment sales prices and cap rates are reported as well.

Research groups across the country also have expertise in location and site analysis, geographic information systems, and financial modeling. To ensure that our clients’ real estate decisions are thoroughly informed,our researchers perform numerous financial analyses. Options include comprehensive occupancy cost comparisons for potential lease locations and complex lease vs. own scenarios.

The information contained herein has been obtained from sources deemed reliable. While every reasonableeffort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

COLLIERS RESEARCH

TABLE OF CONTENTS

UNITED STATES REAL ESTATE REVIEW

Letter from the President and CEO 1Letter from the Director of Market and Economic Research 2US Real Estate 3Linking Real Estate to Company Objectives – The Role of Personal Beliefs, Decision Context and Business Integration, Sven Govaars 9

Glossary 72Colliers USA Office Locations 73

US CITY ANALYSES AND FORECASTS

Atlanta, GA 13Bakersfield, CA 14Baltimore, MD 15Boise, ID 16Boston, MA 17Charleston, SC 18Charlotte, NC 19Chicago, IL 20Cincinnati, OH 21Cleveland, OH 22Columbia, SC 23Columbus, OH 24Dallas/Ft. Worth, TX 25Denver, CO 26Detroit, MI 27Ft. Lauderdale/Broward County, FL 28Fresno, CA 29Greenville, SC 30Hartford, CT 31Honolulu, HI 32Houston, TX 33Indianapolis, IN 34Jacksonville, FL 35Kansas City, MO-KS 36Las Vegas, NV 37Little Rock, AR 38Los Angeles, CA 39Los Angeles/Inland Empire, CA 40

Los Angeles/Orange County, CA 41Louisville, KY 42Memphis, TN 43Miami/Dade County, FL 44Milwaukee, WI 45Minneapolis, MN 46Nashville, TN 47New Jersey – Central 48New Jersey – Northern 49New York, NY 50 – 52Oakland, CA 53Orlando, FL 54Philadelphia, PA 55Phoenix, AZ 56Pleasanton/Walnut Creek, CA 57Portland, OR 58Raleigh/Durham, NC 59Reno, NV 60Sacramento, CA 61San Diego, CA 62San Francisco, CA 63San Francisco/San Mateo Peninsula, CA 64San Jose/Silicon Valley, CA 65Seattle/Puget Sound, WA 66St. Louis, MO 67Tampa Bay, FL 68Washington, DC 69 – 70West Palm Beach, FL 71

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

www.colliers.com

To our clients and colleagues:

Colliers has long been recognized for its in-depth, forward looking market andeconomic information which provides a valuable vantage point in solvingcomplex real estate challenges. As such, I’m pleased to present the 2007 USReal Estate Review, an analysis of over 55 commercial real estate markets.

In addition to being an acknowledged leader in providing information,Colliers has built a powerful platform for achieving our clients’ goals. Our collaborative affiliation works like no other organization in the industry.We are an owner-managed company, which means that principals of Colliersfirms are deeply involved in our clients’ activities. Colliers is also recognizedwithin the industry as a leader and an innovator. Once again, Colliers hasbeen named to the prestigious Global Outsourcing 100 list of the country’stop outsourcing firms, one of the few commercial real estate firms to receive this honor.

2006 was a very robust year in nearly every commercial real estate market in the United States, and we expect most markets to maintain similar momentum in 2007, although there are increasing signs that economic growthwill be somewhat more sluggish. The labor market is expected to remainhealthy, and we expect commercial rents to rise in many markets as the inventory of available space continues to diminish. The retail sector will continue to drive the southern and western markets, and the appetite for Class A investment sales properties is set to continue unabated. We continueto believe the US real estate market offers many opportunities and we lookforward to helping you take advantage of what we consider very exciting timesfor our industry.

We wish you continued success and hope you enjoy the following report.

Margaret WigglesworthPresident and CEOColliers USA

LETTER FROM THE PRESIDENT

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

www.colliers.com 1

LETTER FROM THE DIRECTOR OF RESEARCH

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

2

A year ago I wrote how our industry was in store foranother very robust year marked by healthy levels ofleasing, development and investment activity. With 2006 behind us it is now safe to say that we didindeed enjoy a near perfect year, almost goldilocks like,not too hot and certainly not too cold. The vast majority of our projections were spot on with the exception of the investment sales market which wethought would cool, which of course it didn’t and marksthe second consecutive year where we got it wrong. The balance of this year’s letter is to try and explain whyour forecasts were right, and wrong, which will hopefullyshed some light on what we can expect in 2007 and perhaps more importantly what we can expect over thecoming two, three, four and five years – keeping in mindreal estate is a long term investment.

Let me start with what we got wrong. Our year-ago forecast was “With considerable trepidation our 2006forecast is that it (the investment sales market) will cool somewhat from 2005 as pricing appears to be discouraging new investment. This does not mark acomplete withdrawal of buyers from the marketplace butrather sufficient headwinds may now exist to keep someinvestors on the sidelines.” With hindsight it is nowobvious that the weight of money was far in excess of what we thought was the case. A relatively new phenomenon was at work, that being the private capitalcraze that is now prevalent in virtually all investmentarenas, whether it be equities, commodities, infrastructure investment or currencies. This thirst foryield has now reached a fevered pitch. Private capitalwas behind almost every large transaction and through abetter understanding and measurement of risk and moreuse of leverage these groups were able bid up prices tolevels unimaginable even 12 months ago. However, if we strip away some of the large portfolio sales and a few of the high profile Manhattan office transactions,investment actively and pricing did indeed plateau in2006 so at least we can take some comfort that our projections weren’t completely wrong.

If we now focus of what we got right, virtually everyother projection was on target. We anticipated a healthyeconomy, both domestic and global, a reasonably robust

labor market and continued low long-term interest rates.All of these key ingredients added up to healthy leasingmarkets for all the major real estate sectors and a corresponding increase in lease rates with rental spikesin a limited number of markets. Construction, as anticipated increased, but still not to dangerous levels.

Again, with hindsight this now appears somewhat obvious but as is always the case the future is never easyto forecast. Our view of the coming 12 months, andindeed for the next few years, is the real estate marketwill be the recipient of a relatively buoyant economyagainst still modest amounts of new construction. This does not mean certain markets will get overbuilt,but for the nation as whole we are not headed towardsan oversupply situation. An abundance of capital andrecord high sales prices normally leads to developmentbut many of the markets with these characteristics alsohave significant barriers to entry. Rising constructioncosts and a more difficult entitlement process will alsoslow development.

Against this rosy outlook are the usual concerns.Geopolitical issues, terrorism, an energy crisis, a hedgefund crisis, a debt crisis, a China crisis and the list goeson. The point to keep in mind is many of these possibleevents have been with us for some time, but the globaleconomy is experiencing a period of rapid growth almostunmatched in history. Federal regulators both here andabroad are far better equipped to keep the global economy chugging a long and in many respects theUnited States is better positioned to take advantage ofthis rapidly growing global economy than ever before.Real estate markets will ebb and flow over the comingyears but the general direction will be up as businessestake advantage of the many opportunities that are sureto come their way. The road ahead no doubt offersmany opportunities, but as always, keeping your eye onwhat could go wrong is always the best policy. We hopeyou enjoy this year’s Colliers US Real Estate Review.

Ross MooreSenior Vice President, Director of Market & Economic [email protected]

U.S. Real Estate Still Looks Like a Good Bet – With the Usual Caveats

www.colliers.com 3

US REAL ESTATE

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

OfficeThose expecting a significant cool down in the officemarket were largely disappointed as demand for officespace remained relatively robust in 2006. To the surpriseof some, the year was characterized by significantly higheroffice rents although this was mostly the case in downtownmarkets. Though higher rents were anticipated, the sudden jump reflected sufficient tightening in a handfulof markets rather than a surge across all markets thatpushed up the national average. Still, rents are destinedto continue rising, with no downturn in sight. Office space is sure to become more expensive as demandremains strong, and supply relatively lean. Upcoming newconstruction deliveries could alter the course slightly as2007 plays out but for the immediate term more andmore markets will offer few alternatives for tenants.

A Quick Review of 2006Vacancy rates fell further in 2006 to finish the year at 12.56% down 103 basis points over the prior year’s13.59%. Vacant available sublease space moved marginally lower to 9.9% of total vacant space.Downtown and suburban markets both showed improvement during the year with the Central BusinessDistrict (CBD) vacancy rate falling to 11.50%, and non-CBD markets recorded vacancy at 13.08%.Absorption also followed suit with a fairly robust year,ending on a particularly high note with full year

downtown occupied space increasing by 32.3 millionsquare feet (MSF), and suburban office 63.1 MSF. These levels easily topped the ten year average of 70.5 MSFwith full year occupied space increasing by 95.4 MSF,which exceeded Colliers’ 90 million square feet forecast.

For the third consecutive year asking rents continued toclimb for downtown Class A space, while suburban ClassA space registered a second year of positive growth.Downtown Class A rents in particular increased duringall four 2006 quarters, with a substantial spike in thefourth quarter to $41.01 per square foot, a 6.6% rise.Comparatively, suburban Class A lease rates rose 3.6%to $25.83. For the year, downtown rents marked a substantial 18.2% increase over 2005, and suburbanrents registered 7.4%.

Construction activity continued unabated, with 2006bringing 58.6 million square feet of new space to themarket. This marked a substantial rise over 2005’s 46.7million square feet. The trend appears to be spillingheadlong into 2007 as evidenced by the amount of spacecurrently under construction. At year-end constructionactivity clocked 106.9 million square feet compared with73.2 million square feet at year-end 2005.

Executive SummaryU.S. real estate markets enjoyed yet another banner year and look set to put in a similar performance in 2007. A combination of healthy, but more importantly, sustainable economic growth and low long-term interest rates madealmost all forms of income producing real estate very attractive to investors. An abundance of capital, both debt andequity, continued to support record levels of investment transactions and valuations that even just a few years agoseemed in-comprehensible.

Office assets remained the most sought after, but industrial and retail were not far behind and multi-family was quicklyregaining its position as favored property type particularly amongst smaller investors. The coast markets remained highlysought after by a wide spectrum of investors including off-shore, institutional and perhaps most importantly private equity investors who continue to push up prices in these very liquid and dynamic markets.

Two trends worth watching were the rapid growth in “green” buildings, “green” leasing and “green” development andsecondly the substantial transfer of ownership from public to private hands. The “privatization” of real estate is discussedin detail in the following pages, but the trend towards green or sustainable development is something we have begun to monitor as all aspects of real estate are beginning to be affected by this global movement towards addressing globalwarming or climate change depending on your point of view.

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

IndustrialThe industrial market closed 2006 on a slightly lowernote but the overall trend was still largely positive.Construction activity continued to push higher withcompletions anticipated to outpace demand as 2007unfolds. Industrial rents overall rose steadily during2006 increasing by 6.0% over the year with a similarincrease expected over the next 12 months.

The NumbersAbsorption for the year fell short of anticipated levels tototal 183.6 million square feet, somewhat shy of Colliers’projected 200 million square feet. This marked a substantial 17.6% drop over 2005’s 222.8 million squarefeet. Looking closer, the fourth quarter slide to just 36.9million square feet, down from the third quarter’s 48.4million square feet, and 20.6 million square feet lessthan year-end 2005, illustrated a substantial slowdown at year-end. The disappointing fourth quarter ended astring of robust quarters going back to 2004, whereabsorption had remained between 40 and 60 millionsquare feet.

New construction however, still crept upward registering184.1 million square feet for the year, a rise of

39.6 million square feet over 2005 levels. Quarterly numbers for new construction hovered around 50 million square feet. At year-end, new constructiondropped slightly to 48.8 million square feet from 49.4 million square feet in the third quarter. Still construction activity is expected to remain elevatedthroughout 2007. This was already impacting industrialvacancy rates with the fourth quarter seeing rates bumpupward for the first time in eleven quarters. The twobasis point rise left rates at 8.21% at year-end, the firstincrease since the first quarter of 2004. This rise wasanticipated, due to relatively high levels of constructionactivity and may suggest the low point for vacancy ratesin this cycle may now have been reached.

However, industrial rents forged ahead despite highervacancy and new availability. At year-end rents registered $5.28 per square foot, a 6% rise over year levels, and the highest level in four years. The most significant rent increases occurred in the second andthird quarters, with a marginal rise of 0.38% in the fourth.

Outlook 2007The slowing housing sector and a cutback in productionby the big three automakers foreshadows a mixed

Outlook 2007Demand for office space in 2007 is expected to almostmatch the robust levels seen in 2006 despite a softeningeconomy. The financial, professional, and business services sectors will again lead leasing activity. Rents areanticipated to increase significantly with central businessdistrict (CBD) lease rates set to jump 12 to 15 percent,due to several factors. Some of the rise is due to healthydemand and still only modest amounts of new construction, but spikes in expenses such as insurance,maintenance and property taxes also play a part. Indeed, four markets: Midtown Manhattan, San Francisco,Chicago and Seattle are expected to see rents rise byover twice the national average. Suburban rents will alsorise but at a more modest rate of five to seven percent.

Office construction is anticipated to jump 25 percentand should ultimately total approximately 75 millionsquare feet. Absorption is expected to remain flat, ordrop slightly to 90 to 95 million square feet, comparedwith 95 million square feet in 2006. The anticipatedrise in new construction will take the pressure off tenants, though demand is expected to remain strong for some time with the national vacancy rate remainingsteady with just half a percent decline to 12.5 percent by year-end 2007 at the outside.

4

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 1,230,562,000 12,040,000 17,507,400 8.4 36.812000 1,370,397,508 15,689,000 27,008,000 7.5 42.832001 1,402,263,508 11,416,000 -51,353,000 11.8 38.102002 1,464,575,508 19,993,000 -18,255,000 14.3 33.202003 1,484,411,508 16,701,000 3,839,000 14.9 32.002004 1,521,648,508 9,946,000 14,311,000 14.4 33.252005 1,533,449,508 11,801,000 29,022,000 13.1 34.692006 1,545,443,508 11,994,000 32,282,000 11.5 41.01

Source: Colliers Research Services

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 2,385,032,000 113,452,000 88,330,000 10.0 26.532000 2,528,431,000 96,757,000 161,931,000 9.4 27.232001 2,838,532,000 114,955,000 -20,070,000 14.5 26.402002 2,979,709,000 70,243,000 -9,376,000 16.8 23.902003 3,024,817,000 38,617,000 21,830,000 17.2 23.602004 3,086,602,000 36,177,000 65,268,000 15.7 23.482005 3,119,305,000 33,491,000 75,703,000 13.7 24.042006 3,169,448,000 46,571,000 63,088,000 13.1 25.83

Source: Colliers Research Services

5

Retail Despite a year-end slump, retail sales grew by 6.0% in2006, and excluding motor vehicles and parts, that number jumps to 7.3%. Despite a soft finish for the year,2007 is anticipated to be another good year for retailersas the economy is set to post steady growth.

The Retail LandscapeThe retail landscape remained relatively benign withmarket fundamentals favoring neither retailers nor landlords. As is always the case, the demand side continues to change as consumer’s tastes change and onthe supply side, construction continues to move awayfrom large regional centers to lifestyle and urban infilldevelopment. Relative equilibrium continues to be thecase with only a limited number of exceptions.

For owners and developers of retail real estate the twomost pressing issues remain finding land available fordevelopment and second how the American consumerwill react to a pullback in the housing market and theresulting psychological “loss of wealth.” Added on top of this were high debt levels, which restrict furthergrowth in retail sales. Important to keep in mind, however, is continued healthy job creation, rising wages and still relatively low short-term and long-terminterest rates. The combined effect will leave retail salesgrowth at levels similar to that experienced in 2006 but

a more uneven retail landscape with more pronouncedwinners and losers.

Outlook 2007Looking ahead, all the gloom and doom talk about aslowing economy led by a slump in housing, plus themuch-publicized difficulties in the auto sector, mayprove much ado about nothing. The combined Januaryand February job reports were surprisingly good, theConference Board’s consumer confidence index hit a 56-month high, and the forecast is favorable for mostretail sectors.

Apparel sales should match 2006’s growth of 6.0% andFood Services along with Drinking Places are expectedto register another strong year, though may fall slightlyshy of 2006’s 8.1% growth. Spending trends seen overthe last several years, are expected to continue through2007 with the anticipated winners likely to remain discount retailers, luxury retailers, and lifestyle stores.Retailers such as Costco, Target, Nordstrom’s, NeimanMarcus, Starbucks and a multitude of restaurant groupsare the probable beneficiaries of both macro economicand demographic trends, which only show signs of persisting. This relatively healthy backdrop for retaillandlords will help to keep occupancies at healthy levelsand push lease rates upward.

upcoming year. Conversely, distribution should remain robust due to a rising trade sector and ensuingtransportation activity, plus manufacturing is expected to stay relatively buoyant through the year.

Industrial rents are again anticipated to increase in2007. A predicted 10 percent rise or $0.50 per squarefoot hike is likely on the way, with some of this increasedue to a higher percentage of first generation space listed for lease.

Absorption is not expected to keep pace with new supply, which will leave the year-end 2007 vacancy rateup a quarter of a percent, registering approximately8.5%. This will be the first increase since 2003. Still, steady absorption of on average 40-50 millionsquare feet per quarter is expected, as growing domesticand global economies will sustain strong leasing activity.

The main concern for forward-looking investors is construction. Both completions and projects under construction have been on the rise since 2005.Construction activity is expected to remain robust,

with an anticipated 15% increment over 2006 levelswith the year-end totals reaching approximately 205 million square feet. At year-end construction activity was up 25% relative to year-end 2005, so it isreasonable to expect a similar increase in completionsfor the year ahead. Such levels will likely leave 30 million square feet of excess space given currentdemand, triggering a rise in vacancy.

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 8,981,911,000 201,510,000 177,676,000 6.8 4.81 3.382000 9,602,904,000 203,695,000 212,717,000 6.3 5.51 3.502001 9,954,236,000 221,336,000 6,312,000 8.9 4.90 4.74200210,692,426,000 129,084,000 13,016,000 10.1 4.63 4.82200310,793,452,000 101,027,000 84,917,000 10.1 4.72 5.96200410,973,029,000 131,822,000 193,883,000 9.5 4.74 6.17200511,115,743,000 154,433,000 242,905,000 8.4 5.00 8.03200611,335,815,000 184,853,000 183,571,000 8.2 5.28 9.94

Source: Colliers Research Services

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

A two-tier market may ultimately emerge, where primestrips and high-end centers will enjoy strong sales andhealthy occupancies while more average properties willexperience only modest growth. Tourism fueled retailmarkets such as; Midtown Manhattan, San Francisco,Los Angeles, Chicago, Las Vegas and Honolulu areexpected to flourish with record rental rates.

The biggest success stories in the coming year are likelyto be high-end retailers and those with a strong brandimage, as well as apparel retailers, which should alsohave a solid year. Overall, owners of retail real estate canexpect another solid year, similar to 2006 – with steadyoccupancies and a 3-4 percent increase in rents.

Investment SalesNew investment capital continued to find a home inreal estate continuing a five-year trend. Though a slumphad been predicted for 2006, as the year unfolded, itbecame apparent the investment market would stayrobust for some time to come. Clearly, investorsremained attracted to real estate because of tighteningleasing markets and rising rents. This was reflected in a number of prime office buildings selling for theunprecedented level of over $1,000 per square foot.

In 2006 investment sales volume totaled $310 billion, adouble-digit increase of 11%. As predicted, long-terminterest rates remained steady and institutional investorscontinued to increase their real estate portfolios whenever and wherever possible. Rising constructioncosts and the increasingly difficult entitlement processremained favorable trends for the investment market.

Securitizing Begs PrivatizingOne of the major themes running throughout 2006 and into 2007 was the velocity of portfolio sales and privatizations. Most of the 11% rise in transaction

volume came through privatizations, which rose dramatically, from $7 billion in 2005 to $29 billion in2006. Even though portfolio sales garnered significantattention during the year, the year-end total of $52 billion was unchanged from 2005 levels. Still, therewas a massive abundance of capital, on both the debtand equity side, resulting in a blizzard of privatizations.Private investors seized the opportunity to arbitrage thepricing differential between the public and private markets. These portfolios or real estate companies,mainly listed on NYSE, were bought outright; privatecapital came in and purchased the whole companyrather than just the property. Upon taking ownership,many properties were then sold off, often with a substantial profit.

Historically, real estate has been a very inefficient market but over the last 15 years it has been securitized,and as a result it is now far more transparent. It hasbeen a natural evolution beginning with the savings and loans crisis of the early 90’s. Out of that downturncame real estate investment trusts, or REITs, and also apublic debt market, the commercial mortgage backed

6

YEAR-TO-DATE SALES ENDING DECEMBER 2006 2005 % CHANGE

All Stores 4,364,542 4,115,815 6.0%Motor Vehicle and Parts Dealers 909,127 895,250 1.6%Gasoline Stations 425,166 388,261 9.5%Food and Beverage Stores 544,581 519,292 4.9%Grocery Stores 482,797 463,905 4.1%Health and Personal Care Stores 224,341 208,376 7.7%Building Material and Garden Equipment Stores 355,002 326,993 8.6%General Merchandise Stores 553,191 525,726 5.2%Department Stores (excluding leased departments) 212,799 214,658 -0.9%Clothing and Accessories Stores 214,009 201,682 6.1%Furniture, Home Furnishings, Electronics and Appliance Stores 227,701 211,733 7.5%Furniture and Home Furnishing Stores 120,201 111,293 8.0%Electronics and Appliance Stores 107,500 100,440 7.0%Sporting Goods, Hobby, Book and Music Stores 86,684 81,853 5.9%Miscellaneous Store Retailers 118,833 111,001 7.1%Nonstore Retailers 277,064 249,011 11.3%Food Services and Drinking Places 428,843 396,637 8.1%

Source: US Census Bureau.All Values are expressed in millions of US dollars and are not seasonally adjusted.

7

securities market, or CMBS. Though 15 years in themaking, what is new is the enormous amount of privateequity targeting these public real estate vehicles with theintent of returning ownership to private hands.

Returning to the issue of transparency, these privateequity investors are very much aware that the tremendous abundance of readily available research anddata inherent in the securities market allowed risk to be more easily identified, and measured. In today’sinvestment world it is the ability to measure risk thatallows investors to pay prices that seemingly make littleor no sense. Investors and experts now measure risk in ways many people find difficult to comprehend. The result is prices that to many in the commercial real estate industry can’t make sense.

Examples of private equity transactions include the threetop portfolio sales in 2006. Trizec Properties was boughtby Blackstone Investors and Brookfield Properties for$7.2 billion, CarrAmerica sold for $5.6 billion, toBlackstone Investors and Tishman Speyer, and BeaconCapital Partners, went for $3.3 billion to Broadway RealEstate Partners. Also, following year-end 2006,Blackstone Investors acquired Equity Office Propertiesfor $39 billion including debt. The trend is clear – realestate is undergoing a change in ownership, transferringfrom public markets to private ownership, all driven bythe glut of investment capital available worldwide.

Real estate is now experiencing a whole new buyergroup and these private equity investors have a tremendous amount of capital to draw on. A new chapter in real estate investing is in progress, as privateequity is quickly becoming the most dominant force inreal estate investing. It was reported private equityinvestors poured nearly $60 billion into real estate fundsin 2006, with early indication that this was a record, butthe figure could be surpassed in 2007 if the funds raisingcapital for real estate meet their aggregate target: $80billion. Groups such as Blackstone were understood tobe raising a $10 billion fund and Morgan Stanley wasraising an $8 billion fund. And Lone Star was rumoredto be raising a $6 billion fund.

However, this trend also signifies a marked move towardless inefficiency in the overall market, which could spelldisappointment for more average investors. All this efficiency and transparency ultimately may mean it will become much more difficult to make super-normalprofits. So while real estate has returned to its place as a viable investment alternative for institutional investorsand offshore buyers, smaller investors could see dwindlingprofit margins as price discrepancies become more rare.

Cap Rates PlateauAfter coming down during the 2002-2005 period, caprates finally plateaued. With hindsight it is fair to saycap rate compression peaked in late 2005. Cap ratesremained steady through 2006, with numbers changingjust a couple of basis points.

Office cap rates, both CBD and suburban, finished the year up just 10 basis points to 7.0% and 7.6% respectively. Warehouse cap rates also increased duringthe year, increasing by 20 basis points to 7.1%. R&D caprates, however, bucked the trend, dropping by 20 basispoints to 7.6%. Cap rates for retail as demonstrated by neighborhood centers held steady at 6.8% whilemulti-family cap rates fell by 10 basis points to 6.20%.Many investors realized that with the privately ownedresidential market slowing, would-be buyers might opt to rent, making multi-family a strategic option. As apartment buildings fill up, owners can hike rents,allowing them to pay more with the anticipation of rising rent rolls in the future.

Price Per Square FootOverall, pricing increased throughout the U.S. realestate market, with one exception. The greatest riseoccurred in downtown office properties. Average priceper square foot for downtown markets rose 24% from$225 to $279 per square foot. Suburban office valuesalso increased, growing by 13.2% from $167 to $189 persquare foot. Industrial warehouse prices climbed 13%,from $54 to $61 per square foot. Looking at combinedretail, the average price per square foot rose to $157 per square foot, up from $149, a 5.3% increase.Only Multi-family fell with price per unit going from$101,500 down to $96,400, marking a 5.1% decline.This, the result of the condo conversion craze thatoccurred in 2005 which more or less disappeared in2006 and brought prices down to more sustainable levels.

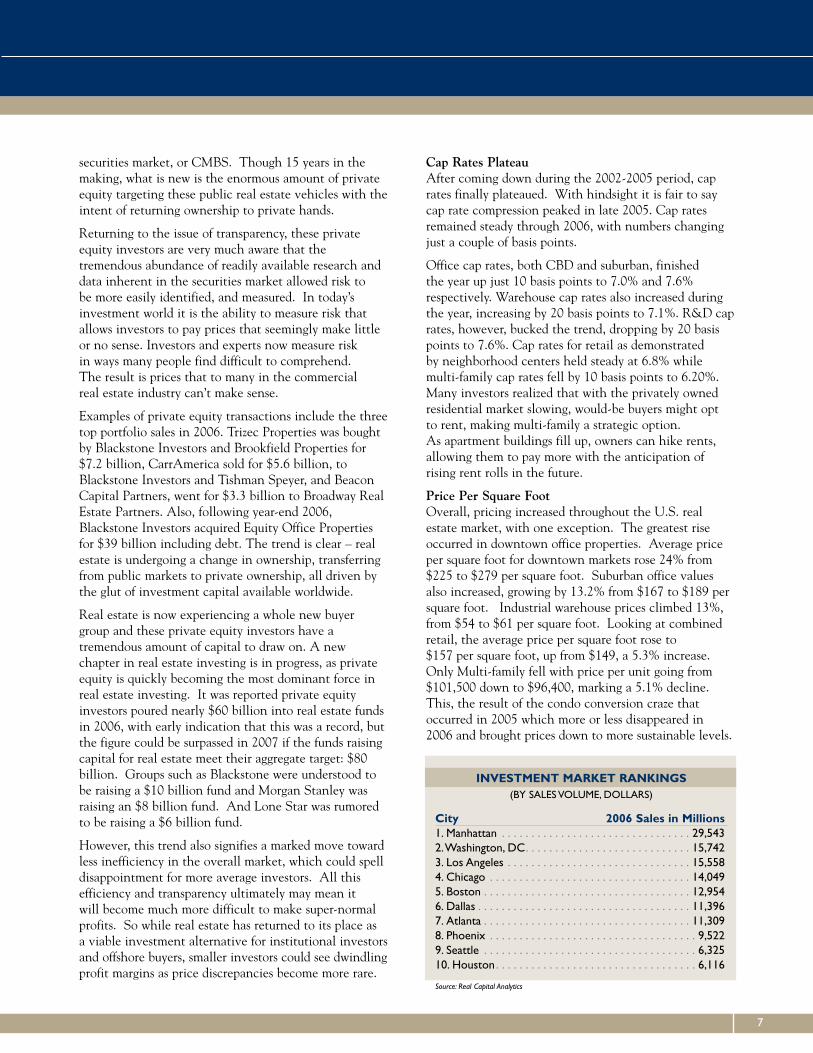

INVESTMENT MARKET RANKINGS(BY SALES VOLUME, DOLLARS)

City 2006 Sales in Millions1. Manhattan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29,5432.Washington, DC. . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,7423. Los Angeles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,5584. Chicago . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14,0495. Boston . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12,9546. Dallas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,3967. Atlanta . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,3098. Phoenix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,5229. Seattle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,32510. Houston . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,116

Source: Real Capital Analytics

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

Outlook 20072007 looks set to be another robust year, with a continuing surge in M&A activity one of the the primary drivers. The mountain of private capital willcontinue to scour the world, looking for a home andmuch of it will see commercial real estate as an attractive home. The enormous interest by these relatively new investors will force many long-timeinvestors to think outside the box for opportunities.The days of easy investing in traditional institutional-grade real estate are dwindling. As long as REITs trade at a discount to net asset value, privatizations are likelyto occur – and as REITs begin trading in the UK andGermany, global investing is poised to grow exponentially.Going “global” will be the buzzword for 2007.

Interest in multi-family rental real estate will experiencea boost as the owner-occupied residential market softens. That said, with interest rates staying low andfundamentals improving, 2007 will be another year ofstrong performance by virtually all property types.

Coastal markets will again be the strongest performersbut even traditionally weak markets will benefit fromthe abundance of capital seeking to invest in real estate.Property values will increase, more due to a spike in netoperation income, rather than cap rate compression.Except for the very top tier, that dynamic is over.

Cross-border investment is expected to accelerate asdomestic investors seek superior returns abroad, and foreign investors view the weakened dollar as an opportunity to enter or expand their U.S. portfolios. All six major buyer groups (institutions, REITs, equityfunds, foreign investors, private investors and syndicators) will be active, with no one group accounting for more than 20 percent of the market. In addition, many pension funds will continue to growtheir real estate portfolio in 2007, and should be some of the most aggressive buyers in the coming year. A yearfrom now we will almost certainly be writing about howreal estate continues to be a preferred investment type.

8

10.00

9.75

9.50

9.25

9.00

8.75

8.50

8.25

8.00

7.75

7.50

7.25

7.00

6.75

6.50

6.25

6.00

Capi

taliz

atio

nRa

tes

(%)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2001 2002 2003 2004 2005 2006

Multi-Family Industrial Office-CBD Office-Sub Retail (Neighborhood)

CAP RATE TRENDS

Source: Real Estate Research Corp.

www.colliers.com 9

LINKING REAL ESTATE TO COMPANY OBJECTIVES –THE ROLE OF PERSONAL BELIEFS, DECISIONCONTEXT AND BUSINESS INTEGRATION

SVEN GOVAARS

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

IntroductionIt is very difficult for an organization to consciouslychange how it makes real estate decisions. Millions ofdollars are spent every year in the pursuit of changethrough the hiring and firing of consultants, implementing training programs and undertaking corporate restructuring.

Decisions bring change and changing the way an organization does business is hard and we all know it.Without a systematic decision process throughout anorganization, a broad based business context, and understanding the role our personal beliefs play, corporate real estate risk will be controlled more by the risk tolerance of individuals than by the organization’s strategy.

By embracing change and understanding the influenceof these decision factors, we have a better chance ofresolving issues that reinforce company objectives andprovide future opportunities. These issues include thosematters relating to corporate real estate. Finding betterways to link real estate to a company’s overall objectivesis a critical success factor for many businesses today.

Personal BeliefsBy being aware of our personal limitations, especially our strongly held beliefs developed over a lifetime, we can hopefully avoid some common danger signs. Because real estate decisions often have long term outcomes and delayed feedback, it is important that the decisions be resolved correctly the first time. Just knowing how we personally influence the decisionprocess will make it easier to safeguard against and dispel potential mistakes.

BiasesEveryone has biases and companies display them as well.We have all witnessed well meaning individuals whoshow excessive optimism and enthusiasm for a solutiononly to realize the diagnosis was prepared too quicklyand not sufficiently verified. It is common for individuals and teams to develop over confidence without allowing sufficient time for important

information to surface. Sometimes data may be screened out by an unrealized bias and we inadvertentlyavoid data that may be present but did not support the business case. We sometimes make the choice toexclude information without consciously realizing it.

ShortcutsThe real estate environment today forces us to findfaster, better, and cheaper ways to make decisions.Those new to real estate decision support often look forshortcuts to speed up the process. At the other end ofthe spectrum, after years of experience we develop rulesof thumb and can move quickly through diagnosis andanalysis, sometimes second guessing the outcome. Many times we are wrong and we pay a high price when challenged and we realize it would have beenmore prudent to take the time to work through each step.

PerspectiveOne of the most powerful inhibitors to successful decision making is our personal point of view. Where acolleague can sometimes point out a bias before it unduly affects a decision, or a shortcut can be tested by alternative means to ensure its validity, the role ofperspective is more difficult to handle. How a project isposed influences the outcome. Think about what itwould take to change your view on a real estate decisionthat you have already made. We are also influenced by our organizational structure and experience communicating across departmental lines. Different personality types have different perspectivesand develop different problem statements depending ontheir role and position in the organization. The way a situation is described has an already embedded viewpoint and it is important to not let it drive the final result. We should explore multiple ways to thinkthrough a problem. We intuitively know we have apoint of view but we often fail to realize its impact onour decisions and resistance to change. We need tobroaden our analysis to create a larger context to address opportunities and constraints that we might otherwise miss.

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

Decision ContextOne way to combat our long held beliefs is to use simpletools and apply them consistently in our decisionprocess. We tend to emphasize the outcome of the work and spend too little time gathering data to set the context for decision-making.

Our experience facilitating teams led us to use a simplefour square chart during discovery and diagnosis toassemble information and broaden the decision context.The chart is used from the outset and presented alongwith the final results. By categorizing information intohow we come to know it, we can better realize what wemay not know to provide clues for additional research.

Four areas are explored (see Figure 1):

(1) We begin with what we know from our information gathering,interviews, data researchand so on.

(2) Next we prepare a list ofwhat we do not know.Some of these items we will research and other items will remain unknown.

(3) As we probe deeper wediscover information anddata we did not know atthe beginning and chartit here, some from step 2.

(4) This square is usually not filled in.Sometimes referred to as a “wildcard,” it is an unexplained event that might change the course of any decision. We use scenario planning to thinkabout the implications.

We have used this chart as an internal tool and whenworking with external teams. In our alignment worksessions we present the chart early in the planning stageand encourage its use in later forecasting and decisionsupport. It also serves as a reminder that we may neverhave all the information we desire and that most decisions are made in a point in time and need to bereexamined periodically.

Business IntegrationSince real estate is often considered non-core, howevernecessary to a company’s mission, the decision processand business context employed typically falls short ofcurrent business practices. It is not uncommon for solutions reached by real estate professionals to end upbeing too narrow in scope and do not readily integratewith other critical business drivers. To avoid this, realestate professionals need to align real estate issues to thecompany objectives and bring an enterprise view to theirdiscussions. This linkage should be based on the degreeto which organizational, operational and capital factorsaffect and align with real estate decisions to serve the objectives of the company. It is not enough todemonstrate cost reduction benefits; these must be

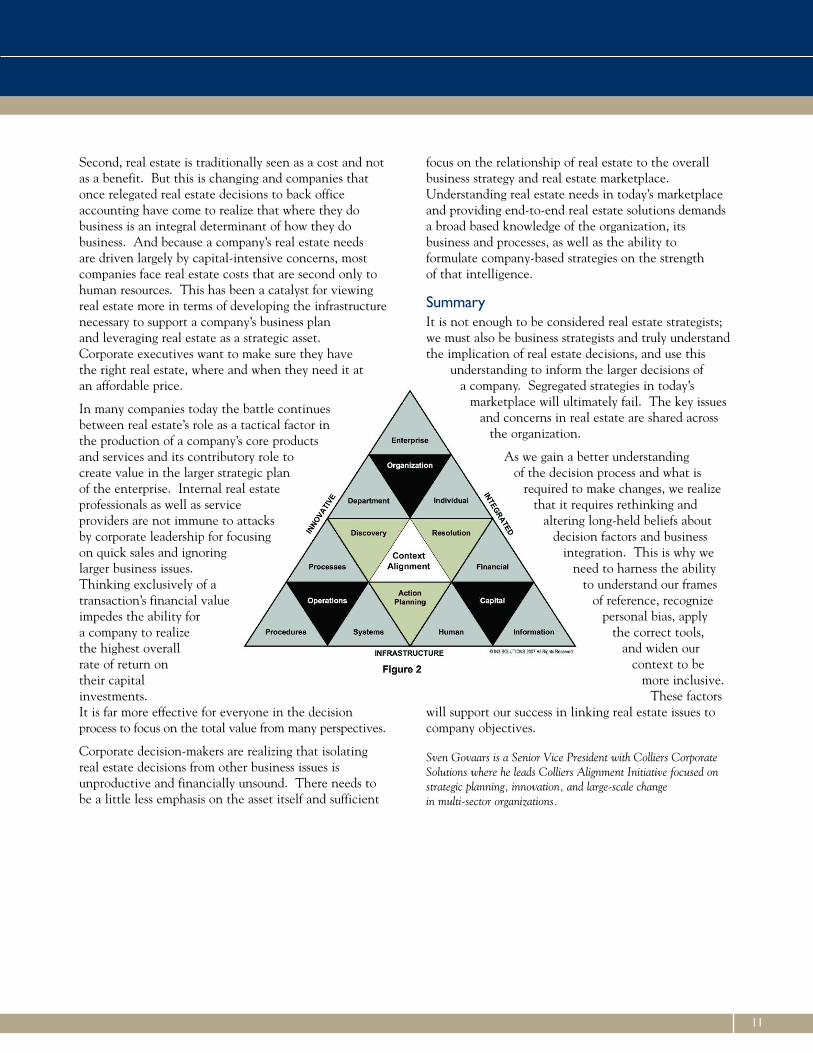

coupled with value-based initiatives that drive integratedresults. We use a simple context alignment model(Figure 2), which outlines first and second level factors to be considered in real estate decisions.

We know that decisions made today have tremendousconsequences for the future ofour organization. Given therapid changes in the businessclimate, a seemingly straightforward decisioninvolves balancing a multitudeof organizational, legal, financial, and stakeholder

risks. How we make decisions and the required changesthat follow those decisions force us to look closer at our choices.

So, what are the reasons that real estate has not beenbetter integrated into the overall business decisions of a company? First, the difficulty and complexity ofintegrating real estate is a direct result of marketplacecycles. When times are good, real estate is acquired and when times are tough real estate is disposed of orcommitted to some form of alternative use. This sets up a continued mismatch with the longer term businesscycles of most companies.

10

11

Second, real estate is traditionally seen as a cost and notas a benefit. But this is changing and companies thatonce relegated real estate decisions to back officeaccounting have come to realize that where they dobusiness is an integral determinant of how they do business. And because a company’s real estate needs are driven largely by capital-intensive concerns, mostcompanies face real estate costs that are second only tohuman resources. This has been a catalyst for viewingreal estate more in terms of developing the infrastructurenecessary to support a company’s business plan and leveraging real estate as a strategic asset. Corporate executives want to make sure they have the right real estate, where and when they need it at an affordable price.

In many companies today the battle continuesbetween real estate’s role as a tactical factor in the production of a company’s core products and services and its contributory role to create value in the larger strategic plan of the enterprise. Internal real estate professionals as well as service providers are not immune to attacks by corporate leadership for focusingon quick sales and ignoring larger business issues. Thinking exclusively of a transaction’s financial valueimpedes the ability for a company to realizethe highest overallrate of return ontheir capitalinvestments. It is far more effective for everyone in the decisionprocess to focus on the total value from many perspectives.

Corporate decision-makers are realizing that isolatingreal estate decisions from other business issues is unproductive and financially unsound. There needs tobe a little less emphasis on the asset itself and sufficient

focus on the relationship of real estate to the overallbusiness strategy and real estate marketplace.Understanding real estate needs in today’s marketplaceand providing end-to-end real estate solutions demandsa broad based knowledge of the organization, its business and processes, as well as the ability to formulate company-based strategies on the strength of that intelligence.

SummaryIt is not enough to be considered real estate strategists;we must also be business strategists and truly understandthe implication of real estate decisions, and use this

understanding to inform the larger decisions of a company. Segregated strategies in today’s

marketplace will ultimately fail. The key issuesand concerns in real estate are shared across

the organization.

As we gain a better understanding of the decision process and what is

required to make changes, we realizethat it requires rethinking and

altering long-held beliefs aboutdecision factors and business

integration. This is why weneed to harness the ability

to understand our frames of reference, recognize

personal bias, apply the correct tools,

and widen our context to be

more inclusive. These factors

will support our success in linking real estate issues tocompany objectives.

Sven Govaars is a Senior Vice President with Colliers CorporateSolutions where he leads Colliers Alignment Initiative focused onstrategic planning, innovation, and large-scale change in multi-sector organizations.

ATLANTA, GA

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 46,943,000 290,000 -113,000 7.4 22.202000 47,593,000 650,000 1,405,000 5.7 24.202001 50,443,000 2,850,000 -164,000 11.4 24.902002 51,668,000 1,225,000 79,000 13.3 23.502003 52,156,000 488,000 187,000 13.8 23.302004 52,710,000 554,000 327,000 14.1 21.902005 53,029,000 319,000 695,000 13.3 21.702006 53,740,000 711,000 601,000 13.3 21.90

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 136,250,000 10,396,000 8,559,000 10.7 23.002000 143,995,000 7,745,000 6,724,000 10.8 23.302001 151,626,000 7,631,000 445,000 15.0 23.802002 155,856,000 4,230,000 281,000 17.1 22.502003 158,660,000 2,804,000 1,185,000 17.8 21.502004 159,845,000 1,185,000 3,872,000 16.0 21.402005 162,243,000 2,398,000 3,620,000 14.9 21.402006 164,651,000 2,408,000 3,470,000 14.0 22.00

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 450,600,000 18,629,000 15,507,000 8.5 3.75 – 2000 467,289,000 16,689,000 16,064,000 8.3 3.70 – 2001 486,710,000 19,421,000 3,504,000 11.2 3.60 2.502002 493,957,000 7,247,000 -1,550,000 12.9 3.35 2.872003 496,986,000 3,029,000 1,369,000 13.1 3.30 3.802004 504,632,000 7,646,000 13,946,000 11.7 3.50 1.402005 514,033,000 9,401,000 11,800,000 11.0 3.75 1.852006 534,363,000 20,330,000 12,882,000 11.9 3.80 1.95

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 3.4

• Total Employment Increase/Decrease: 41,900Percent Change: 1.8

• Unemployment Rate: 4.0

• Population (000): 5,137.8

Source: Moody’s Economy.com

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

CONTACT: Mike Spears • [email protected] l RESEARCH: Scott Amoson • [email protected] 13

OFFICE

• Office absorption in 2006 reached 3.7 million SF, in line with levelsover past two years.

• Delivered office space totaled 3 million SF, second highest in four years.• Top three office leases were: CompuCredit consolidating into

400,000 SF in Central Perimeter; Newell Rubbermaid signing for350,000 SF headquarters expansion; and American Cancer Societymoving to 270,000 SF downtown.

• Rental rates on the rise. The market transitioning from tenant’s market to landlord’s market, however some pockets of tenant control remain.

• Atlanta experienced record investments with first ever Class A trophy tower topping $400 per SF and commercial land in midtownselling for over $12.8 million per acre.

Office Outlook• Atlanta will continue to add jobs at faster pace than nation.

Office absorption should remain steady at 3-4 million SF in 2007.• Service, hospitality, and technology industries will have greatest

impact on office market growth for 2007.• Like much of nation, housing market will experience downturn,

however effects will be shorter-lived and less damaging than overcooked markets.

• Population migration will continue into city’s urban core where mostcommercial development taking place.

• Investment activity for office buildings in Atlanta will remain solid in 2007.

INDUSTRIAL

• Absorption of 13 million SF consistent with previous two years, butstill off from levels reached in late 90s.

• Overall vacancy rate up from 2005 at 11.9% mainly due to slowdemand from big box users and 20 million SF of deliveries.

• Largest transactions were Kimberly-Clark leasing 1.3 million SF,PetSmart signing for 877,500 SF, and Progressive Lighting leasing 796,663 SF.

• Land scarcity and higher prices continue pushing development further from city.

• Investment activity remained strong with portfolio sales hottest investments.

Industrial Outlook• 2007 absorption will be between 6-8 million SF, slightly off

2006 levels.• Logistics companies could reemerge as major space users around

airport and multi-modal facilities as port activity, rail activity, andtrucking remain high.

• South Atlanta will experience greatest growth in 2007 and accountfor most of absorption.

• Construction levels declining, however funding available for development. Eight million SF expected to deliver in 2007 androughly 4-5 million SF expected next year.

• Two unknowns regard the Ford and GM plant closings and whattakes their place.

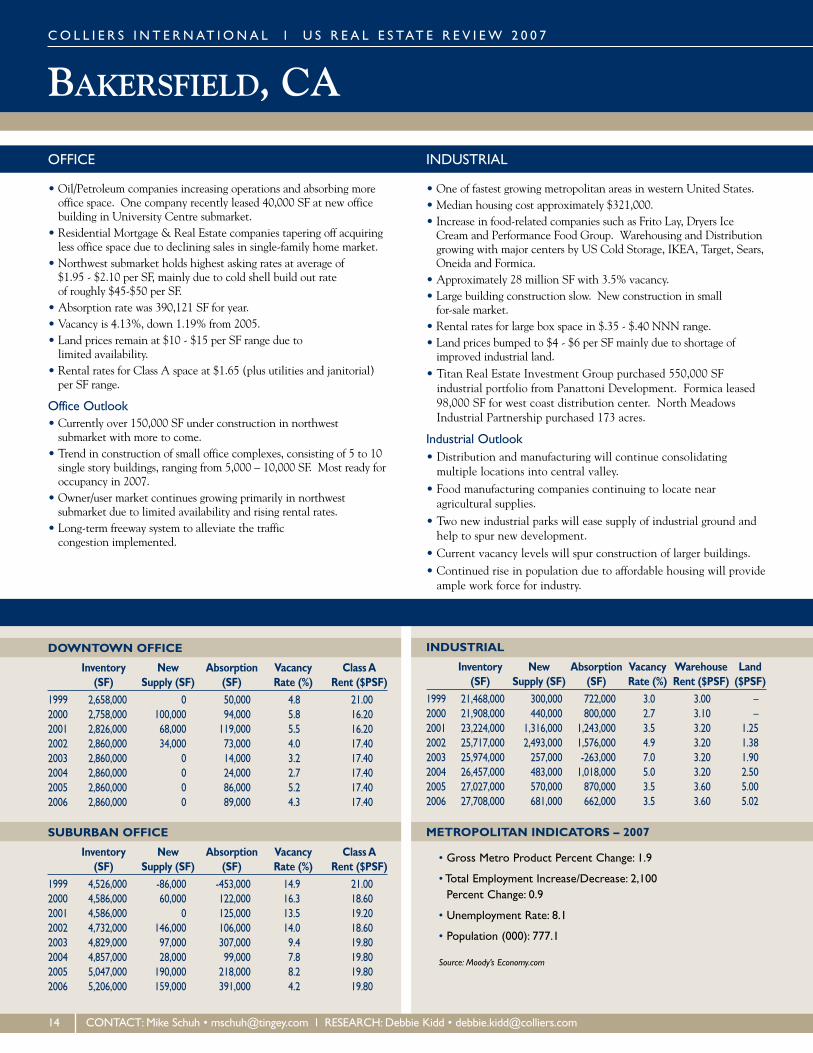

BAKERSFIELD, CAC O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 2,658,000 0 50,000 4.8 21.002000 2,758,000 100,000 94,000 5.8 16.202001 2,826,000 68,000 119,000 5.5 16.202002 2,860,000 34,000 73,000 4.0 17.402003 2,860,000 0 14,000 3.2 17.402004 2,860,000 0 24,000 2.7 17.402005 2,860,000 0 86,000 5.2 17.402006 2,860,000 0 89,000 4.3 17.40

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 4,526,000 -86,000 -453,000 14.9 21.002000 4,586,000 60,000 122,000 16.3 18.602001 4,586,000 0 125,000 13.5 19.202002 4,732,000 146,000 106,000 14.0 18.602003 4,829,000 97,000 307,000 9.4 19.802004 4,857,000 28,000 99,000 7.8 19.802005 5,047,000 190,000 218,000 8.2 19.802006 5,206,000 159,000 391,000 4.2 19.80

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 21,468,000 300,000 722,000 3.0 3.00 – 2000 21,908,000 440,000 800,000 2.7 3.10 – 2001 23,224,000 1,316,000 1,243,000 3.5 3.20 1.252002 25,717,000 2,493,000 1,576,000 4.9 3.20 1.382003 25,974,000 257,000 -263,000 7.0 3.20 1.902004 26,457,000 483,000 1,018,000 5.0 3.20 2.502005 27,027,000 570,000 870,000 3.5 3.60 5.002006 27,708,000 681,000 662,000 3.5 3.60 5.02

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 1.9

• Total Employment Increase/Decrease: 2,100Percent Change: 0.9

• Unemployment Rate: 8.1

• Population (000): 777.1

Source: Moody’s Economy.com

14 CONTACT: Mike Schuh • [email protected] l RESEARCH: Debbie Kidd • [email protected]

OFFICE

• Oil/Petroleum companies increasing operations and absorbing moreoffice space. One company recently leased 40,000 SF at new officebuilding in University Centre submarket.

• Residential Mortgage & Real Estate companies tapering off acquiringless office space due to declining sales in single-family home market.

• Northwest submarket holds highest asking rates at average of $1.95 - $2.10 per SF, mainly due to cold shell build out rate of roughly $45-$50 per SF.

• Absorption rate was 390,121 SF for year.• Vacancy is 4.13%, down 1.19% from 2005. • Land prices remain at $10 - $15 per SF range due to

limited availability. • Rental rates for Class A space at $1.65 (plus utilities and janitorial)

per SF range.

Office Outlook• Currently over 150,000 SF under construction in northwest

submarket with more to come. • Trend in construction of small office complexes, consisting of 5 to 10

single story buildings, ranging from 5,000 – 10,000 SF. Most ready foroccupancy in 2007.

• Owner/user market continues growing primarily in northwest submarket due to limited availability and rising rental rates.

• Long-term freeway system to alleviate the traffic congestion implemented.

INDUSTRIAL

• One of fastest growing metropolitan areas in western United States. • Median housing cost approximately $321,000.• Increase in food-related companies such as Frito Lay, Dryers Ice

Cream and Performance Food Group. Warehousing and Distributiongrowing with major centers by US Cold Storage, IKEA, Target, Sears,Oneida and Formica.

• Approximately 28 million SF with 3.5% vacancy. • Large building construction slow. New construction in small

for-sale market. • Rental rates for large box space in $.35 - $.40 NNN range.• Land prices bumped to $4 - $6 per SF mainly due to shortage of

improved industrial land.• Titan Real Estate Investment Group purchased 550,000 SF

industrial portfolio from Panattoni Development. Formica leased98,000 SF for west coast distribution center. North MeadowsIndustrial Partnership purchased 173 acres.

Industrial Outlook• Distribution and manufacturing will continue consolidating

multiple locations into central valley. • Food manufacturing companies continuing to locate near

agricultural supplies.• Two new industrial parks will ease supply of industrial ground and

help to spur new development. • Current vacancy levels will spur construction of larger buildings.• Continued rise in population due to affordable housing will provide

ample work force for industry.

BALTIMORE, MD

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 12,963,000 161,000 593,000 9.2 25.002000 13,187,000 224,000 171,000 9.3 26.502001 13,795,000 608,000 299,000 11.4 24.102002 15,485,000 1,690,000 33,000 19.6 21.402003 15,650,000 165,000 296,000 18.4 24.302004 16,031,000 381,000 294,000 17.7 24.002005 16,214,000 183,000 316,000 17.2 23.202006 16,739,000 525,000 511,000 17.0 23.80

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 30,598,000 1,856,000 1,400,000 8.4 23.502000 33,044,000 2,446,000 1,913,000 9.9 23.702001 35,252,000 2,208,000 418,000 14.6 22.502002 36,253,000 1,001,000 14,000 17.4 18.402003 36,902,000 649,000 1,114,000 16.0 21.302004 38,577,000 1,675,000 2,213,000 14.2 22.502005 40,641,000 2,064,000 1,797,000 14.0 24.302006 42,392,000 1,751,000 1,847,000 13.4 24.55

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 75,749,000 2,529,000 2,608,000 11.6 4.75 – 2000 77,050,000 1,301,000 3,616,000 7.7 4.70 – 2001 80,951,000 3,901,000 917,000 13.3 4.50 3.452002 82,258,000 1,307,000 -322,000 16.8 5.00 6.002003 84,590,000 2,332,000 2,250,000 17.0 5.60 4.902004 85,728,000 1,138,000 -814,000 18.7 5.40 5.172005 88,255,000 2,527,000 3,924,000 16.5 5.90 5.752006 89,242,000 987,000 1,169,000 15.2 6.46 6.31

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 1.9

• Total Employment Increase/Decrease: 9,800Percent Change: 0.8

• Unemployment Rate: 4.1

• Population (000): 2,677.9

Source: Moody’s Economy.com

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

CONTACT: Peter McGill • [email protected] l RESEARCH: Jay Wellschlager • [email protected] 15

OFFICE

• Absorbed and built over 2 million SF for third consecutive year, surpassing any three-year period.

• Activity strong with absorption exceeding construction in most markets.

• Buyers looking for stabilized income and redevelopment opportunities. CBD properties, acquired for redevelopment to residential or hotel uses. Others acquired as income producing office buildings.

• Construction costs for new mid-rises exceed $200 per SF. Tenant improvement allowances for Class A range from $25-$35 per SF, depending on lease term and market.

• Operating expenses increasing, driven by rising utility costs, taxes,and services.

• Growing healthcare, educational, financial, and professional servicefirms drove performance.

Office Outlook• Positive, but demand likely to level off in 2007. Job growth

appears to be slowing for information, financial, professional and business services.

• Only 27% pre-leased of 2.19 million SF under construction.• 68% of deliveries expected in Baltimore-Washington corridor,

including largest project, Johns Hopkins’ 243,000 SF build-to-suit.

INDUSTRIAL

• Record absorption cooled. Two submarkets posted positive whileCorridor flat.

• bulk distribution, warehouse, and flex space absorption unremarkable,still exceeded new space. Vacancy rate dropped to 15.2%.

• Bulk distribution vacancy at 16.5%, down from 17.8%. Vacancy forindustrial flex (13.5%) and office warehouse (11.1%) also dropped for year.

• Robust investment sales. RREEF acquired Calpers’ eight buildingportfolio for $57 per SF; Patuxent Range LLC acquired portfolio inCorridor for $66 per SF.

• Port of Baltimore expanded capacity and warehousing. • Redevelopment of former General Motors site into port-related

multi-modal hub.

Industrial Outlook• Land more expensive with development options further north in

@ 95 Corridor. The GM site, the 1,000-acre Crossroads, andTradeCenter @ 95 highlight options.

• Three large distribution buildings under construction, 600,000 SF in TradeCenter at @ 95, two buildings in Corridor, plus 176,000 SF in Preston Gateway, and 215,000 SF in Lincoln Crossroads.

• Limited new construction, especially for bulk distribution warehouses. Slowing state economy, may continue to moderate leasing activity in 2007.

BOISE, IDC O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 1,935,000 242,000 181,000 8.9 19.002000 1,975,000 40,000 17,000 9.1 18.802001 – – – – –2002 – – – – –2003 3,210,000 75,000 -4,000 10.6 18.902004 3,462,000 252,000 187,000 11.7 18.802005 3,551,000 89,000 206,000 7.6 18.902006 3,731,000 180,000 88,000 9.7 20.00

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 4,833,000 331,000 244,000 15.3 17.002000 5,034,000 201,000 234,000 12.6 17.002001 – – – – –2002 – – – – –2003 6,933,000 442,000 323,000 15.6 16.602004 7,102,000 169,000 157,000 19.2 17.602005 7,981,000 879,000 1,068,000 13.4 16.902006 8,157,000 176,000 197,000 12.9 16.20

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 20,858,000 396,000 345,000 2.3 4.90 – 2000 22,219,000 1,361,000 1,558,000 1.5 5.00 – 2001 22,300,000 81,000 -712,000 5.0 4.50 – 2002 22,445,000 145,000 -476,000 7.7 3.50 – 2003 22,532,000 87,000 -468,000 10.1 4.40 – 2004 22,669,000 137,000 146,000 10.0 4.60 5.002005 22,757,000 88,000 288,000 9.1 4.60 4.002006 22,937,000 180,000 754,000 5.7 6.03 3.94

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 4.2

• Total Employment Increase/Decrease: 8,100Percent Change: 3.0

• Unemployment Rate: 2.7

• Population (000): 563.2

Source: Moody’s Economy.com

16 CONTACT: Pete Draper • [email protected] l RESEARCH: Cory Read • [email protected]

OFFICE

• Tenants are getting used to the $19 and above rents in Boise CBD,demonstrated by consistent downtown absorption.

• Office absorption backed down from high 2005 levels due mostly tosuburban slowdown, but still consistent and positive.

• National tenant activity has increased over the last year.• Building in downtown has returned with the completion of a

new 11 story 180,000 SF building during 2006 and the current construction of another large project.

• CBD will see most leasing activity in valley if current levels continuethrough 2007.

Office Outlook• Absorption should remain consistent and positive.• National tenant activity will continue as companies look to gain

position in response to the high growth of the valley.• New construction continuing on 84,000 SF project.• Average CBD Class A rents will more than likely crest the $20 for

the first time during 2007.

INDUSTRIAL

• Speculative development slow due to land prices and constructioncosts increasing at faster rate than rental rates.

• Landlords currently hold bargaining chips because vacancies arebelow 6% across valley with very few choices for tenants looking forspaces 20,000 or greater.

• Average rents have crested the $6 annual rate for warehouse space for first time during the latter part of 2006.

• The 2006 industry slowdown in expansion (which had supported residential construction) did not have much effect on industrial leasing and vacancy.

• Over 1 million SF were absorbed across the Valley during 2006.

Industrial Outlook• Speculative building may increase slightly during 2007, but will

probably not meet demand. • Rents are going to rise throughout 2007. • Developers will spend much of 2007 planning and positioning

themselves while looking for rents and land costs to fall in line.

BOSTON, MA

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 58,904,000 844,000 812,000 5.5 50.502000 60,754,000 1,850,000 2,290,000 4.5 72.002001 62,928,000 2,174,000 -1,935,000 11.9 55.302002 64,660,000 1,732,000 -860,000 16.2 43.702003 65,914,000 1,254,000 368,000 17.4 38.402004 66,722,000 808,000 -61,000 17.9 38.202005 66,942,000 220,000 2,045,000 12.6 41.402006 66,942,000 0 1,773,000 9.8 46.00

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 90,941,000 5,599,000 7,904,000 12.3 25.602000 95,894,000 4,953,000 9,241,000 6.2 38.902001 102,727,000 6,833,000 -6,570,000 21.0 31.002002 106,177,000 3,450,000 -1,766,000 26.0 25.002003 108,561,000 2,384,000 -290,000 28.2 21.002004 108,383,000 -178,000 1,810,000 25.6 20.802005 107,341,000 -1,042,000 3,363,000 18.8 20.102006 108,091,000 750,000 2,616,000 12.7 24.00

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 142,309,000 795,000 2,170,000 9.7 6.00 – 2000 144,744,000 2,435,000 3,030,000 8.2 7.00 – 2001 146,806,000 2,062,000 -1,726,000 14.6 7.00 1.952002 147,664,000 858,000 -60,000 15.9 6.00 1.952003 148,421,000 757,000 -1,248,000 19.2 6.00 1.702004 149,036,000 615,000 -1,767,000 23.0 5.50 2.872005 151,142,000 2,106,000 503,000 23.7 5.50 –2006 152,380,000 1,238,000 488,000 22.8 5.84 –

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 2.3

• Total Employment Increase/Decrease: 11,300Percent Change: 1.0

• Unemployment Rate: 5.0

• Population (000): 1,804.8

Source: Moody’s Economy.com

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

CONTACT: Margaret Wigglesworth • [email protected] l RESEARCH: Robert Sammons • [email protected] 17

OFFICE

• Boston closes 2006 in relatively good condition though not yet at pre-2001 levels due to shakiness in financial services.

• Vacancy continues declining especially for Downtown and Back Bayas well as 128 West suburban markets.

• Few large blocks available Downtown or Back Bay, one exception isGillette placing 325,000 SF on market at Prudential Center.

• Average asking rents steadily rising across submarkets but especiallyDowntown, Cambridge and 128 West.

• CBD investment sales strong with several key properties closing atwell over $400 per SF (1 Lincoln Street at $838 per SF and 265Franklin Street for $486 per SF).

Office Outlook• Jobs expected to climb again in 2007, especially in law and

accounting fields. Financial services is mixed bag with some growth (Bank of America adding jobs) and some cutbacks due to relocations (Fidelity).

• Little new office construction in metro area, so the vacancy rateexpected to decline in 2007 across most submarkets.

• Average asking rents in key submarkets will increase at or slightlyhigher than 2006 levels, especially for Class A.

• High-Tech/Bio-Tech/Pharma firms will continue desiring office andlab space, especially in Cambridge and 128 West submarkets.

• Expect 128 West to be hot, due to increasing popularity withinvestors and developers with several long-term speculative projectsto be announced in 2007.

INDUSTRIAL

• Industrial/warehouse activity space picked up but remains weakerthan other major metro markets.

• Most leasing and sales transactions on smaller side, less than 100,000 SF.

• 128 West and North submarkets closed 2006 with tightest availability, both near 10.0% and highest average asking rents, both near $10.00 per SF NNN).

• R&D and Flex remained hottest subset in 2006.• Major construction underway includes 200,000 SF warehouse near

Port of Boston, 50% pre-leased.• Gillette renewed for just over 1-million SF in Ayer after threatening

to relocate away from Boston market completely.

Industrial Outlook• Demand for industrial/warehouse/R&D will lag behind other

major markets in 2007. With little new construction, vacanciesshould continue declining.

• Activity greater in submarkets furthest from CBD in 2007.• Average asking rents will climb slightly, especially in submarkets with

new product. Possibly some pricing weakness in areas with significantolder stock.

• Investment activity should remain steady in 2007 especially amongmodern properties along I-495 and Bristol County.

• Expect distribution facilities development to spread further from traditional submarkets toward Providence and Worcester.

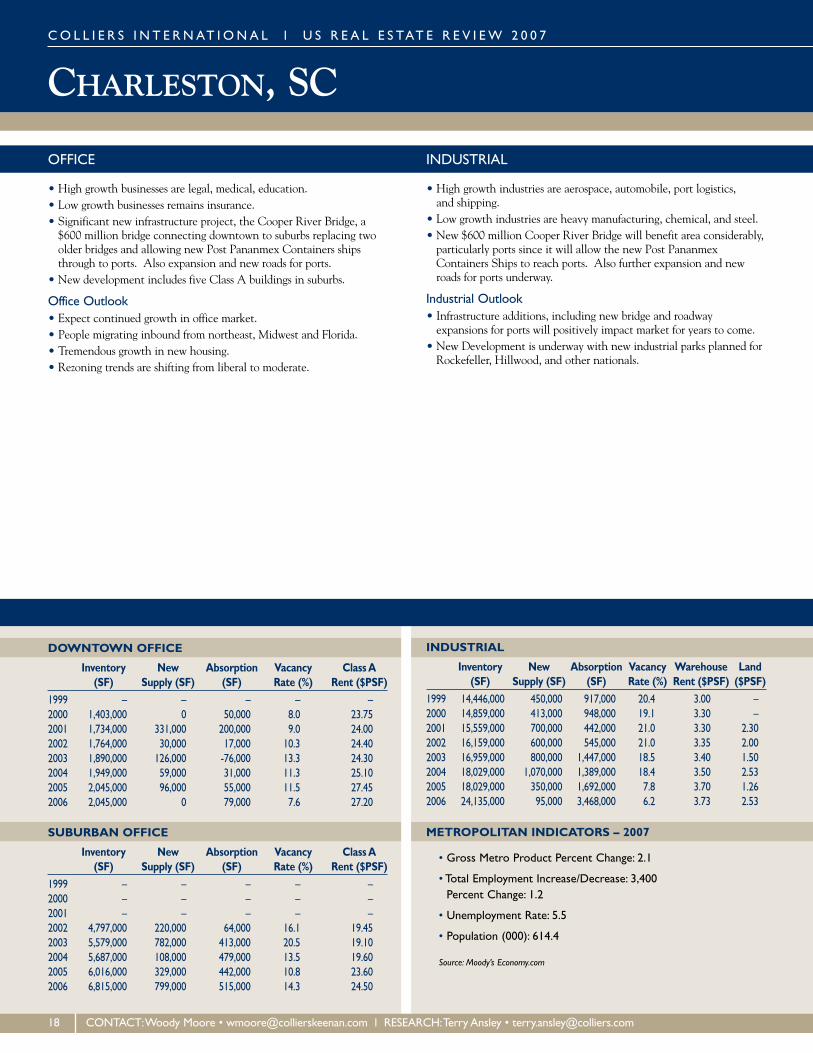

CHARLESTON, SCC O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 – – – – –2000 1,403,000 0 50,000 8.0 23.752001 1,734,000 331,000 200,000 9.0 24.002002 1,764,000 30,000 17,000 10.3 24.402003 1,890,000 126,000 -76,000 13.3 24.302004 1,949,000 59,000 31,000 11.3 25.102005 2,045,000 96,000 55,000 11.5 27.452006 2,045,000 0 79,000 7.6 27.20

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 – – – – –2000 – – – – –2001 – – – – –2002 4,797,000 220,000 64,000 16.1 19.452003 5,579,000 782,000 413,000 20.5 19.102004 5,687,000 108,000 479,000 13.5 19.602005 6,016,000 329,000 442,000 10.8 23.602006 6,815,000 799,000 515,000 14.3 24.50

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 14,446,000 450,000 917,000 20.4 3.00 – 2000 14,859,000 413,000 948,000 19.1 3.30 – 2001 15,559,000 700,000 442,000 21.0 3.30 2.302002 16,159,000 600,000 545,000 21.0 3.35 2.002003 16,959,000 800,000 1,447,000 18.5 3.40 1.502004 18,029,000 1,070,000 1,389,000 18.4 3.50 2.532005 18,029,000 350,000 1,692,000 7.8 3.70 1.262006 24,135,000 95,000 3,468,000 6.2 3.73 2.53

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 2.1

• Total Employment Increase/Decrease: 3,400Percent Change: 1.2

• Unemployment Rate: 5.5

• Population (000): 614.4

Source: Moody’s Economy.com

18 CONTACT:Woody Moore • [email protected] l RESEARCH:Terry Ansley • [email protected]

OFFICE

• High growth businesses are legal, medical, education.• Low growth businesses remains insurance.• Significant new infrastructure project, the Cooper River Bridge, a

$600 million bridge connecting downtown to suburbs replacing twoolder bridges and allowing new Post Pananmex Containers shipsthrough to ports. Also expansion and new roads for ports.

• New development includes five Class A buildings in suburbs.

Office Outlook• Expect continued growth in office market.• People migrating inbound from northeast, Midwest and Florida.• Tremendous growth in new housing.• Rezoning trends are shifting from liberal to moderate.

INDUSTRIAL

• High growth industries are aerospace, automobile, port logistics, and shipping.

• Low growth industries are heavy manufacturing, chemical, and steel.• New $600 million Cooper River Bridge will benefit area considerably,

particularly ports since it will allow the new Post PananmexContainers Ships to reach ports. Also further expansion and newroads for ports underway.

Industrial Outlook• Infrastructure additions, including new bridge and roadway

expansions for ports will positively impact market for years to come.• New Development is underway with new industrial parks planned for

Rockefeller, Hillwood, and other nationals.

CHARLOTTE, NC

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 17,251,000 1,145,000 938,000 5.1 28.002000 18,003,000 752,000 947,000 3.2 25.302001 18,670,000 667,000 126,000 5.4 24.502002 19,668,000 998,000 364,000 9.5 22.902003 19,768,000 100,000 -7,000 10.2 23.802004 19,768,000 0 77,000 9.7 23.802005 19,858,000 90,000 463,000 5.2 21.302006 19,858,000 0 157,000 4.7 22.80

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 33,835,000 420,000 1,558,000 13.0 24.002000 34,972,000 1,137,000 1,423,000 11.8 21.802001 36,825,000 1,853,000 215,000 17.8 20.302002 37,682,000 857,000 98,000 19.8 20.002003 38,074,000 392,000 539,000 18.9 19.302004 38,737,000 663,000 89,000 20.7 19.302005 39,690,000 953,000 1,551,000 15.3 19.402006 41,250,000 1,560,000 1,273,000 15.7 19.70

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 145,584,000 1,959,000 2,044,000 13.0 4.30 – 2000 146,934,000 1,350,000 1,712,000 9.7 3.80 – 2001 147,738,000 804,000 -644,000 14.4 3.60 1.492002 148,941,000 1,203,000 -486,000 17.2 3.40 1.502003 149,115,000 174,000 76,000 18.2 3.40 1.702004 149,478,000 363,000 981,000 17.0 4.10 1.752005 150,714,000 1,236,000 2,224,000 11.1 4.10 –2006 151,429,000 715,000 1,962,000 10.4 4.11 –

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 3.0

• Total Employment Increase/Decrease: 13,300Percent Change: 1.6

• Unemployment Rate: 5.1

• Population (000): 1,607.1

Source: Moody’s Economy.com

C O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

CONTACT: Rob Cochran • [email protected] l RESEARCH: Matt Russell • [email protected] 19

OFFICE

• Availability at 2-4% vacancy downtown, 12-14% suburbs. Very healthy.

• High growth includes financial services, legal, government, anddefense-related. Real estate and construction strong in residentialand commercial.

• High growth are all major homebuilders, Bank of America,Wachovia, BB&T banks and startup community banks.

• Sports, especially NASCAR are economic driver and growing.• First leg of light rail line from Pineville to Charlotte’s CBD, estimated

at $475 million.• New towers under construction include BOA and Wachovia, also

NASCAR office building; City Park is large 175-acre mixed-use redevelopment of former Charlotte Convention Center.

• Outer belt residential and commercial exploding.• Housing market strong. Top end slowed, time on market longer,

prices steady.

Office Outlook• NASCAR Hall of Fame arrives in 2008. Expect large economic impact.• Anticipate unabated migration over next 20-50 years. Great weather,

good government. Transplants mainly from northeast.• IT and Tech treading water. Textile waning.• First light rail line to open late 2007-2008. Additional interest

in north line to University area. Project has 25-year timeline. Other projects are I-485, with 2013 completion, and western legbetween I-85 and I-77 to connect 2008-2009.

• Land rates rising. Infill spiked considerably. Trend pushing developers further out.

INDUSTRIAL

• By year-end 1.77 million SF bulk distribution space delivered.• Overall vacancy rate slightly down at 10.4% over last year’s 10.5%.• Top growth includes logistics, automotive parts, machine, medical

equipment, construction, and NASCAR. • Retailers are high growth, including Ross Dress for Less, Crate &

Barrel, Target, West Marine, Black & Decker. • Old buildings, especially former textile mills, converted to residential

condos and apartments.• Bulk land sales at $45,000 to $85,000 per acre with individual sites

w/utilities at $75,000 to $125,000 per acre.• Becoming increasingly difficult to rezone land to light and heavy

industrial, diminishing supply, resulting in rapid continued price acceleration.

• Largest sale 1.08 million SF former Winn Dixie Distribution Centerat $24,500,000.

• Largest lease West Logistics at 251,000 SF.

Industrial Outlook• Charlotte’s outer belt (I-485) under construction with 75% delivered

end 2007.• Third runway and runway extension will increase business for largest

cargo jets. Runways and Norfolk Southern's rail extension intomulti-modal yard at airport will spur more logistics growth.

• Early 2007 expect delivery of approximately 500 million SF.• Comparatively low house prices will continue to fuel migration from

non-traditional areas such as Midwest, Florida, and California.

CHICAGO, ILC O L L I E R S I N T E R N AT I O N A L l U S R E A L E S TAT E R E V I E W 2 0 0 7

DOWNTOWN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 116,112,000 2,600,000 -156,000 10.7 34.302000 116,916,000 804,000 2,140,000 10.2 36.002001 119,147,000 2,231,000 -685,000 12.7 35.002002 119,977,000 830,000 -3,404,000 16.6 32.002003 122,802,000 2,825,000 -945,000 16.9 32.002004 124,660,000 1,858,000 1,544,000 17.0 32.002005 126,316,000 1,656,000 207,000 19.5 34.002006 126,795,000 479,000 3,795,000 15.2 36.00

SUBURBAN OFFICE

Inventory New Absorption Vacancy Class A(SF) Supply (SF) (SF) Rate (%) Rent ($PSF)

1999 93,130,000 3,984,000 1,681,000 11.7 27.002000 97,059,000 3,929,000 1,383,000 13.8 28.502001 101,232,000 4,173,000 -3,010,000 20.7 29.002002 102,945,000 1,713,000 -793,000 23.4 25.002003 103,347,000 402,000 -1,283,000 23.9 25.002004 103,886,000 539,000 2,501,000 21.8 22.002005 104,112,000 226,000 1,365,000 21.1 23.602006 104,245,000 133,000 1,385,000 18.9 22.30

INDUSTRIAL

Inventory New Absorption Vacancy Warehouse Land(SF) Supply (SF) (SF) Rate (%) Rent ($PSF) ($PSF)

1999 988,381,000 22,227,000 24,189,000 5.6 5.20 – 2000 1,007,524,000 19,143,000 15,680,000 5.8 5.60 – 2001 1,017,872,000 10,348,000 -10,978,000 8.0 5.10 4.682002 1,031,233,000 13,361,000 1,305,000 8.9 4.40 3.902003 1,044,699,000 13,466,000 7,392,000 9.4 4.60 4.802004 1,061,977,000 17,278,000 13,221,000 9.5 4.50 4.202005 1,080,869,000 18,892,000 19,349,000 9.0 4.60 5.172006 1,098,495,000 17,626,000 14,077,000 9.0 4.56 6.01

METROPOLITAN INDICATORS – 2007

• Gross Metro Product Percent Change: 2.4

• Total Employment Increase/Decrease: 39,700Percent Change: 1.0

• Unemployment Rate: 4.6

• Population (000): 7,975.2

Source: Moody’s Economy.com

20 CONTACT: David Bercu • [email protected] l RESEARCH: George Cutro • [email protected]

OFFICE

• Downtown demand set records for investment sales with high-quality,well-leased product. New record with 1 S. Dearborn sale at $422 per SF.

• Two new CBD deliveries and ground broken on two towers totaling 2 million SF, expected delivery 2009.

• Largest leases include Kirkland & Ellis’ 600,000 SF; Jenner & Block’s412,000 SF; and Mesirow Financial’s 390,000 SF.

• CBD vacancy steadily decreased nearly 2.0%, absorption remainedpositive every quarter.

• CBD growth in office conversions to office-condos or residential-condos, particularly East Loop due to Millennium Park.

• Suburban Class A successful attracting tenants, causing rents to rise10% to 15% over 2005 levels.

• Four speculative projects broke ground in suburban markets.

Office Outlook• Demand remaining strong in 2007 for top-tier assets as leasing

improves and vacancy rates continue falling.• Mixed-use delivery set for Q4 2007, adds 400,000 SF. • Leasing expected strong with continued absorption and vacancy

likely dipping below 15%.• Conversion trend expected to continue for assets challenged with

high vacancy.• Suburban freeze on electrical rates terminates at year-end.

Anticipate jump from 40% to 80% over 2006.• Land prices to continue climbing. Reached $16.00 per SF in 2006,

four times higher than decade ago.• Landlords scaling back concessions 5% to 10%. Already fewer free

rents and tenant allowances for Class A.

INDUSTRIAL

• Major absorption in warehouse/distribution. End users signed leasesfor majority of large transactions.

• Infill development robust at O’Hare International Airport. Nine speculative warehouse/distribution facilities broke ground, 1.2 million SF total, with 706,100 SF available.