Embed Size (px)

Citation preview

Clerical Medical Managed Funds

Annual FSA Insurance Returns for the year ended

31 December 2010

IPRU(INS) Appendices 9.1, 9.3, 9.4, 9.6

Contents

Balance Sheet and Profit and Loss Account

Form 2 Statement of solvency - long-term insurance business 1Form 3 Components of capital resources 3Form 13 Analysis of admissible assets 6Form 14 Long term insurance business liabilities and margins 12Form 15 Liabilities (other than long term insurance business) 13Form 16 Profit and loss account (non-technical account) 14Form 17 Analysis of derivative contracts 15

Long Term Insurance Business: Revenue Account and Additional Information

Form 40 Revenue account 16Form 41 Analysis of premiums 17Form 42 Analysis of claims 18Form 43 Analysis of expenses 19Form 44 Linked funds balance sheet 20Form 45 Revenue account for internal linked funds 21Form 46 Summary of new business 22Form 47 Analysis of new business 23Form 48 Assets not held to match linked liabilities 26Form 50 Summary of mathematical reserves 27Form 51 Valuation summary of non-linked contracts (other than

accumulating with-profits contracts)28

Form 53 Valuation summary of property linked contracts 31Form 54 Valuation summary of index linked contracts 35Form 55 Unit prices for internal linked funds 36Form 57 Analysis of valuation interest rate 38Form 58 Distribution of surplus 39Form 60 Long-term insurance capital requirement 40

Supplementary notes to the return 41

Additional information on derivative contracts 48

Additional information on controllers 49

Abstract of the Valuation Report 50

Directors' Certificate 58

Auditor's Report 59

23032011:13:19:23

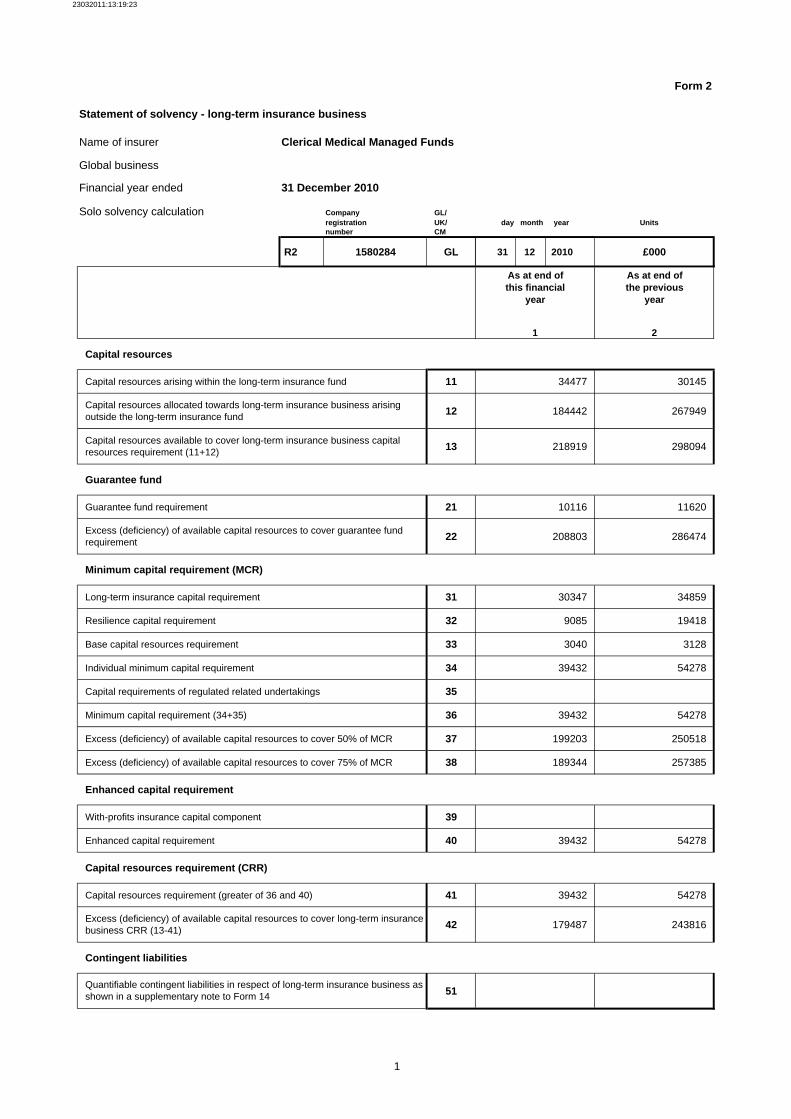

Form 2

Statement of solvency - long-term insurance business

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Solo solvency calculation Company GL/registration UK/ day month year Units number CM

R2 1580284 GL 31 12 2010 £000

As at end of As at end ofthis financial the previous

year year

1 2

Capital resources

Capital resources arising within the long-term insurance fund 11 34477 30145

12 184442 267949

13 218919 298094

Guarantee fund

Guarantee fund requirement 21 10116 11620

22 208803 286474

Minimum capital requirement (MCR)

Long-term insurance capital requirement 31 30347 34859

Resilience capital requirement 32 9085 19418

Base capital resources requirement 33 3040 3128

Individual minimum capital requirement 34 39432 54278

Capital requirements of regulated related undertakings 35

Minimum capital requirement (34+35) 36 39432 54278

Excess (deficiency) of available capital resources to cover 50% of MCR 37 199203 250518

Excess (deficiency) of available capital resources to cover 75% of MCR 38 189344 257385

Enhanced capital requirement

With-profits insurance capital component 39

Enhanced capital requirement 40 39432 54278

Capital resources requirement (CRR)

Capital resources requirement (greater of 36 and 40) 41 39432 54278

42 179487 243816

Contingent liabilities

51Quantifiable contingent liabilities in respect of long-term insurance business as shown in a supplementary note to Form 14

Capital resources allocated towards long-term insurance business arising outside the long-term insurance fund

Capital resources available to cover long-term insurance business capital resources requirement (11+12)

Excess (deficiency) of available capital resources to cover guarantee fund requirement

Excess (deficiency) of available capital resources to cover long-term insurance business CRR (13-41)

1

23032011:13:19:23

Form 2

Covering Sheet to Form 2

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

P D Loney Director

K Luscombe Director

A G Kane Director

Date : 28 March 2011

2

23032011:13:19:23

Form 3(Sheet 1)

Components of capital resources

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010Company GL/registration UK/ Units number CM

R3 GL 31 12 2010 £000

General Long-term Total as at Total as atinsurance insurance the end of the end of business business this financial the previous

year year1 2 3 4

Core tier one capital

Permanent share capital 11 375500 375500 375500

Profit and loss account and other reserves 12 (80058) (80058) (96592)

13

Positive valuation differences 14

15

16

Core tier one capital (sum of 11 to 16) 19 295442 295442 278908

Tier one waivers

21

Implicit Items 22

Tier one waivers in related undertakings 23

24

Other tier one capital

25

26

27

28

31 295442 295442 278908

32

33

34

35 2738 2738 1251

36

37 2738 2738 1251

39 292704 292704 277657

day month year

1580284

Share premium account

Fund for future appropriations

Core tier one capital in related undertakings

Unpaid share capital / unpaid initial funds and calls for supplementary contributions

Total tier one waivers as restricted (21+22+23)

Perpetual non-cumulative preference shares as restricted

Perpetual non-cumulative preference shares in related undertakings

Innovative tier one capital as restricted

Innovative tier one capital in related undertakings

Total tier one capital before deductions (19+24+25+26+27+28)

Investments in own shares

Intangible assets

Amounts deducted from technical provisions for discounting

Other negative valuation differences

Deductions in related undertakings

Deductions from tier one (32 to 36)

Total tier one capital after deductions (31-37)

3

23032011:13:19:23

Form 3(Sheet 2)

Components of capital resources

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010Company GL/registration UK/ Units number CM

R3 GL 31 12 2010 £000

General Long-term Total as at Total as atinsurance insurance the end of the end of business business this financial the previous

year year1 2 3 4

Tier two capital

41

42

43

44

45

46 100000

Upper tier two capital in related undertakings 47

Upper tier two capital (44 to 47) 49 100000

Fixed term preference shares 51

Other tier two instruments 52

Lower tier two capital in related undertakings 53

Lower tier two capital (51+52+53) 59

61 100000

Excess tier two capital 62

63

69 100000

day month year

1580284

Implicit items, (tier two waivers and amounts excluded from line 22)Perpetual non-cumulative preference shares excluded from line 25

Innovative tier one capital excluded from line 27

Tier two waivers, innovative tier one capital and perpetual non-cumulative preference shares treated as tier two capital (41 to 43)

Perpetual cumulative preference shares

Perpetual subordinated debt and securities

Total tier two capital before restrictions (49+59)

Further excess lower tier two capital

Total tier two capital after restrictions, before deductions (61-62-63)

4

23032011:13:19:23

Form 3(Sheet 3)

Components of capital resources

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010Company GL/registration UK/ Units number CM

R3 GL 31 12 2010 £000

General Long-term Total as at Total as atinsurance insurance the end of the end of business business this financial the previous

year year1 2 3 4

Total capital resources

71

72 292704 292704 377657

73 73785 73785 79563

74

75

76

77

79 218919 218919 298094

Available capital resources for GENPRU/INSPRU tests

81 218919 218919 298094

82 218919 218919 277657

83 218919 218919 298094

Financial engineering adjustments

91

92

93

94

95

96

day month year

1580284

Positive adjustments for regulated non-insurance related undertakingsTotal capital resources before deductions (39+69+71)

Inadmissible assets other than intangibles and own shares

Assets in excess of market risk and counterparty limits

Deductions for related ancillary services undertakings

Deductions for regulated non-insurance related undertakings

Deductions of ineligible surplus capital

Total capital resources after deductions (72-73-74-75-76-77)

Available capital resources for guarantee fund requirement

Available capital resources for 50% MCR requirement

Available capital resources for 75% MCR requirement

Implicit items

Financial reinsurance - ceded

Financial reinsurance - accepted

Outstanding contingent loans

Any other charges on future profits

Sum of financial engineering adjustments(91+92-93+94+95)

5

23032011:13:19:23

Form 13(Sheet 1)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total other than long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 1

As at end of this financial year

As at end of the previous year

1 2

Land and buildings 11

21222324252627282930

Other financial investments

Equity shares 41Other shares and other variable yield participations 42Holdings in collective investment schemes 43 184280 271826

Rights under derivative contracts 4445464748

Participation in investment pools 49Loans secured by mortgages 50

51

52Other loans 53

54 1

55Other financial investments 56Deposits with ceding undertakings 57

5859

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Variable interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Loans to public or local authorities and nationalised industries or undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial institution deposits

One month or less withdrawal

More than one month withdrawal

6

23032011:13:19:23

Form 13(Sheet 2)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total other than long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 1

As at end of this financial year

As at end of the previous year

1 2

60

61

62

63

717273747576777879

80

81 97 19

82

83

84 92 100

85

86

87

89 184470 271945

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approvedinstitutions

Cash in hand

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assetsin excess of market risk and counterparty limits (11 to 86 less 87)

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

Deferred acquisition costs (general business only)

Other prepayments and accrued income

7

23032011:13:19:23

Form 13(Sheet 3)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total other than long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 1

As at end of this financial year

As at end of the previous year

1 2

91 184470 271945

92

93 30

94

95

96

97

98

99

100

101

102 184500 271945

103

Reconciliation to asset values determined in accordance with the insurance accounts rules or international accounting standards as applicable to the firm for the purpose of its external financial reporting

Total admissible assets after deduction of admissible assetsin excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related undertakings

Ineligible surplus capital and restricted assets in regulated related insurance undertakings

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Total assets determined in accordance with the insurance accountsrules or international accounting standards as applicable to the firmfor the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from relatedinsurers, other than those under contracts of insurance or reinsurance

Other differences in the valuation of assets (other than for assetsnot valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

8

23032011:13:19:23

Form 13(Sheet 1)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 10

As at end of this financial year

As at end of the previous year

1 2

Land and buildings 11

21222324252627282930

Other financial investments

Equity shares 41Other shares and other variable yield participations 42Holdings in collective investment schemes 43 76066 165149

Rights under derivative contracts 44 617

45 272515 219872

46 37195

47 14829

48Participation in investment pools 49Loans secured by mortgages 50

51

52Other loans 53

54 218 72

55Other financial investments 56Deposits with ceding undertakings 57

58 19538 17399

59 9673324 9387868

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Variable interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Loans to public or local authorities and nationalised industries or undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial institution deposits

One month or less withdrawal

More than one month withdrawal

9

23032011:13:19:23

Form 13(Sheet 2)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 10

As at end of this financial year

As at end of the previous year

1 2

60

61

62

63

71 124 144

727374 202

75767778 36678 33908

79

80

81 3868 2483

82

83

84 2829 3164

85

86

87

89 10100808 9867254

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approvedinstitutions

Cash in hand

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assetsin excess of market risk and counterparty limits (11 to 86 less 87)

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

Deferred acquisition costs (general business only)

Other prepayments and accrued income

10

23032011:13:19:23

Form 13(Sheet 3)

Analysis of admissible assets

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R13 1580284 GL 31 12 2010 £000 10

As at end of this financial year

As at end of the previous year

1 2

91 10100808 9867254

92

93

94

95

96

97

98

99 101760 110504

100 65303 71334

101 19563 6499

102 10287434 10055591

103

Reconciliation to asset values determined in accordance with the insurance accounts rules or international accounting standards as applicable to the firm for the purpose of its external financial reporting

Total admissible assets after deduction of admissible assetsin excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related undertakings

Ineligible surplus capital and restricted assets in regulated related insurance undertakings

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Total assets determined in accordance with the insurance accountsrules or international accounting standards as applicable to the firmfor the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from relatedinsurers, other than those under contracts of insurance or reinsurance

Other differences in the valuation of assets (other than for assetsnot valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

11

23032011:13:19:23

Form 14Long term insurance business liabilities and margins

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Total business/Sub fund CMMF LONG TERM BUSINESS FUND

Units £000 As at end of As at end ofthis financial the previous

year year1 2

Mathematical reserves, after distribution of surplus 11 10027100 9730855

12

Balance of surplus/(valuation deficit) 13 34477 30148

Long term insurance business fund carried forward (11 to 13) 14 10061577 9761003

Gross 15 Reinsurers' share 16 Net (15-16) 17 Taxation 21 Other risks and charges 22 1600

Deposits received from reinsurers 23 Direct insurance business 31 Reinsurance accepted 32 37386 106011

Reinsurance ceded 33 Secured 34 Unsecured 35

Amounts owed to credit institutions 36 Taxation 37 Other 38 245 243

Accruals and deferred income 3941

Total other insurance and non-insurance liabilities (17 to 41) 49 39231 106254

Excess of the value of net admissible assets 51Total liabilities and margins 59 10100808 9867257

61

62 9673324 9387868

71 10066331 9837109

Increase to liabilities - DAC related 72Reinsurers' share of technical provisions 73 65303 71334

Other adjustments to liabilities (may be negative) 74 44830 36189

Capital and reserves and fund for future appropriations 75 110970 110960

76 10287434 10055591

Cash bonuses which had not been paid to policyholders prior to end of the financial year

Claims outstanding

Provisions

Creditors

Amounts included in line 59 attributable to liabilities in respect of property linked benefits

Total liabilities (11+12+49)

Total liabilities under insurance accounts rules or international accounting standards as applicable to the firm for the purpose of its external financial reporting (71 to 75)

Debenture loans

Creditors

Provision for "reasonably foreseeable adverse variations"

Amounts included in line 59 attributable to liabilities to related companies, other than those under contracts of insurance or reinsurance

12

23032011:13:19:23

Form 15

Liabilities (other than long term insurance business)

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Company GL/registration UK/ day month year Unitsnumber CM

R15 1580284 GL 31 12 2010 £000As at end of As at end ofthis financial the previous

year year1 2

Technical provisions (gross amount)

Provisions for unearned premiums 11Claims outstanding 12Provision for unexpired risks 13

Credit business 14 Other than credit business 15

Other technical provisions 16Total gross technical provisions (11 to 16) 19

Provisions and creditors

Taxation 21 Other risks and charges 22

Deposits received from reinsurers 31 Direct insurance business 41 Reinsurance accepted 42 Reinsurance ceded 43 Secured 44 Unsecured 45

Amounts owed to credit institutions 46 Taxation 47 Foreseeable dividend 48 Other 49 28 3996

Accruals and deferred income 51Total (19 to 51) 59 28 3996

Provision for "reasonably foreseeable adverse variations" 61Cumulative preference share capital 62Subordinated loan capital 63 100000

Total (59 to 63) 69 28 103996

71 28 100000

Amounts deducted from technical provisions for discounting 82Other adjustments (may be negative) 83Capital and reserves 84 184472 167948

85 184500 271944

Creditors

Amounts included in line 69 attributable to liabilities to related insurers, other than those under contracts of insurance or reinsurance

Total liabilities under insurance accounts rules or international accounting standards as applicable to the firm for the purpose of its external financial reporting (69-82+83+84)

Equalisation provisions

Provisions

Creditors

Debenture loans

13

23032011:13:19:23

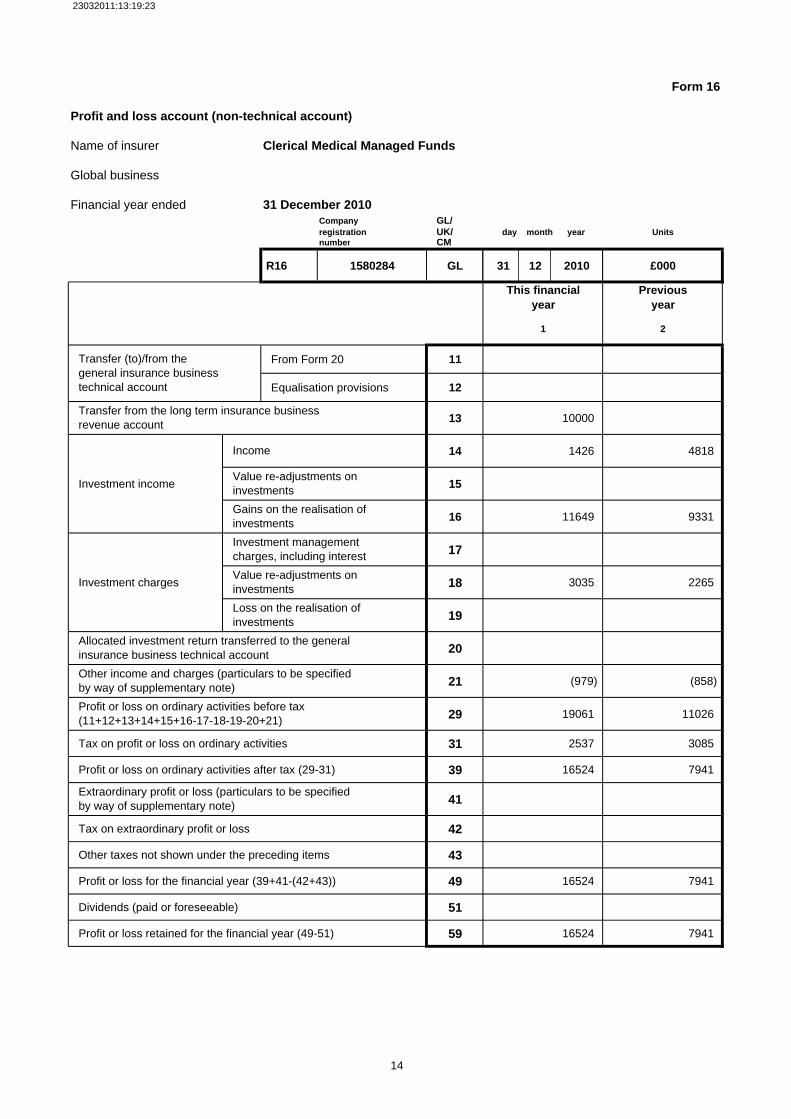

Form 16

Profit and loss account (non-technical account)

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010Company GL/registration UK/ day month year Unitsnumber CM

R16 1580284 GL 31 12 2010 £000

This financial Previousyear year

1 2

From Form 20 11

Equalisation provisions 12

13 10000

14 1426 4818

Investment income 15

16 11649 9331

17

Investment charges 18 3035 2265

19

20

21 (979) (858)

29 19061 11026

Tax on profit or loss on ordinary activities 31 2537 3085

Profit or loss on ordinary activities after tax (29-31) 39 16524 7941

41

Tax on extraordinary profit or loss 42

Other taxes not shown under the preceding items 43

Profit or loss for the financial year (39+41-(42+43)) 49 16524 7941

Dividends (paid or foreseeable) 51

Profit or loss retained for the financial year (49-51) 59 16524 7941

Transfer (to)/from the general insurance business technical account

Transfer from the long term insurance businessrevenue account

Income

Value re-adjustments on investmentsGains on the realisation of investmentsInvestment management charges, including interestValue re-adjustments on investmentsLoss on the realisation of investments

Allocated investment return transferred to the general insurance business technical accountOther income and charges (particulars to be specified by way of supplementary note)Profit or loss on ordinary activities before tax (11+12+13+14+15+16-17-18-19-20+21)

Extraordinary profit or loss (particulars to be specified by way of supplementary note)

14

23032011:13:19:23

Form 17

Analysis of derivative contracts

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010

Category of assets Total long term insurance business assets

Company GL/ Categoryregistration UK/ day month year Units ofnumber CM assets

R17 1580284 GL 31 12 2010 £000 10

Derivative contracts

Assets Liabilities Bought / Long Sold / Short

1 2 3 4

11

Interest rates 12 568 102171

Inflation 13 49 139 5601 22862

Credit index / basket 14

Credit single name 15

16

Equity stock 17

Land 18

Currencies 19

Mortality 20

Other 21

31

Equity index calls 32

Equity stock calls 33

Equity index puts 34

Equity stock puts 35

Other 36

Swaptions 41

Equity index calls 42

Equity stock calls 43

Equity index puts 44

Equity stock puts 45

Other 46

Total (11 to 46) 51 617 139 5601 125033

52

53 617 139

Value as at the endof this financial year

Notional amount as at the endof this financial year

Futures and contracts for differences

Fixed-interest securities

Equity index

Total (51 + 52)

THE NOTIONAL AMOUNTS IN COLUMNS 3 AND 4 ARE NOT A MEASURE OF EXPOSURE. Please see instructions 11 and 12 to this Form for the meaning of these figures.

In the money options

Swaptions

Out of the money options

Adjustment for variation margin

15

23032011:13:19:23

Form 40

Long-term insurance business : Revenue account

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

Financial year Previous year

1 2

Income

Earned premiums 11 693494 (681034)

12 269108 556268

13 14076 (37311)

14 822143 1145744

Other income 15 9163 9207

Total income 19 1807984 992874

Expenditure

Claims incurred 21 1400879 5604513

22 92035 115388

23

24 4495 (12428)

Other expenditure 25

Transfer to (from) non technical account 26 10000

Total expenditure 29 1507409 5707474

Business transfers - in 31

Business transfers - out 32

Increase (decrease) in fund in financial year (19-29+31-32) 39 300575 (4714600)

Fund brought forward 49 9761002 14475602

Fund carried forward (39+49) 59 10061577 9761002

Interest payable before the deduction of tax

Taxation

Investment income receivable before deduction of tax

Increase (decrease) in the value of non-linked assets brought into account

Increase (decrease) in the value of linked assets

Expenses payable

16

23032011:13:19:23

Form 41

Long-term insurance business : Analysis of premiums

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life UK Pension Overseas Total Financial year

Total Previous year

1 2 3 4 5

Gross

Regular premiums 11 11150 482998 494148 551578

Single premiums 12 305 210512 210817 718206

Reinsurance - external

Regular premiums 13

Single premiums 14 11471 11471 22786

Reinsurance - intra-group

Regular premiums 15

Single premiums 16 1928032

Net of reinsurance

Regular premiums 17 11150 482998 494148 551578

Single premiums 18 305 199041 199346 (1232613)

Total

Gross 19 11455 693510 704965 1269784

Reinsurance 20 11471 11471 1950819

Net 21 11455 682039 693494 (681034)

17

23032011:13:19:23

Form 42

Long-term insurance business : Analysis of claims

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life UK Pension Overseas Total Financial year

Total Previous year

1 2 3 4 5

Gross

Death or disability lump sums 11 8421 38787 47208 35054

Disability periodic payments 12

Surrender or partial surrender 13 29 1180974 1181003 5288160

Annuity payments 14 799 3824 4623 128829

Lump sums on maturity 15 43 185381 185424 160561

Total 16 9292 1408966 1418258 5612603

Reinsurance - external

Death or disability lump sums 21

Disability periodic payments 22

Surrender or partial surrender 23 17379 17379 8090

Annuity payments 24

Lump sums on maturity 25

Total 26 17379 17379 8090

Reinsurance - intra-group

Death or disability lump sums 31

Disability periodic payments 32

Surrender or partial surrender 33

Annuity payments 34

Lump sums on maturity 35

Total 36

Net of reinsurance

Death or disability lump sums 41 8421 38787 47208 35054

Disability periodic payments 42

Surrender or partial surrender 43 29 1163595 1163624 5280070

Annuity payments 44 799 3824 4623 128829

Lump sums on maturity 45 43 185381 185424 160561

Total 46 9292 1391587 1400879 5604513

18

23032011:13:19:23

Form 43

Long-term insurance business : Analysis of expenses

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life UK Pension Overseas Total Financial year

Total Previous year

1 2 3 4 5

Gross

Commission - acquisition 11

Commission - other 12

Management - acquisition 13

Management - maintenance 14 493 91542 92035 90038

Management - other 15 25350

Total 16 493 91542 92035 115388

Reinsurance - external

Commission - acquisition 21

Commission - other 22

Management - acquisition 23

Management - maintenance 24

Management - other 25

Total 26

Reinsurance - intra-group

Commission - acquisition 31

Commission - other 32

Management - acquisition 33

Management - maintenance 34

Management - other 35

Total 36

Net of reinsurance

Commission - acquisition 41

Commission - other 42

Management - acquisition 43

Management - maintenance 44 493 91542 92035 90038

Management - other 45 25350

Total 46 493 91542 92035 115388

19

23032011:13:19:23

Form 44

Long-term insurance business : Linked funds balance sheet

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

Financial year Previous year

1 2

Internal linked funds (excluding cross investment)

11 4967135 4833350

12 2692379 351265

13 2033157 4223655

14 9692671 9408269

Provision for tax on unrealised capital gains 15

Secured and unsecured loans 16

Other liabilities 17 14266 19219

Total net assets (14-15-16-17) 18 9678405 9389050

Directly held linked assets

Value of directly held linked assets 21

Total

31 9678405 9389050

Surplus units 32 5451 4028

Deficit units 33 370 2846

Net unit liability (31-32+33) 34 9673324 9387868

Value of directly held linked assets and units held (18+21)

Directly held assets (excluding collective investment schemes)

Directly held assets in collective investment schemes of connected companies

Directly held assets in other collective investment schemes

Total assets (excluding cross investment) (11+12+ 13)

20

23032011:13:19:23

Form 45

Long-term insurance business : Revenue account for internal linked funds

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

Financial year Previous year

1 2

Income

11 481313 945701

12 256938 434560

13 822143 1145743

14

Total income 19 1560394 2526004

Expenditure

21 1194222 2042041

22 76815 72625

23 2 17861

24

25

26

Total expenditure 29 1271039 2132527

39 289355 393477

49 9389050 8995573

59 9678405 9389050

Value of total creation of units

Investment income attributable to the funds before deduction of tax

Increase (decrease) in the value of investments in the financial year

Other income

Value of total cancellation of units

Charges for management

Charges in respect of tax on investment income

Taxation on realised capital gains

Internal linked funds carried forward (39+49)

Increase (decrease) in amount set aside for tax on capital gains not yet realised

Other expenditure

Increase (decrease) in funds in financial year (19-29)

Internal linked fund brought forward

21

23032011:13:19:23

Form 46

Long-term insurance business : Summary of new business

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

UK Life UK Pension Overseas Total Financial year

Total Previous year

1 2 3 4 5

Regular premium business 11

Single premium business 12

Total 13

Amount of new regular premiums

Direct insurance business 21

External reinsurance 22

Intra-group reinsurance 23 66501 66501 94905

Total 24 66501 66501 94905

Amount of new single premiums

Direct insurance business 25 9318 9318 20576

External reinsurance 26 754 754 1037

Intra-group reinsurance 27 180201 180201 673660

Total 28 190273 190273 695273

Number of new policyholders/ scheme members for direct insurance business

22

23032011:13:19:23

Form 47

Long-term insurance business : Analysis of new business

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

UK Pension / Direct Insurance Business

Number of policyholders /

scheme membersAmount of premiums

Number of policyholders /

scheme membersAmount of premiums

1 2 3 4 5 6

765 Group managed fund 9318

Single premium business

23

Product code

numberProduct description

Regular premium business

23032011:13:19:23

Form 47

Long-term insurance business : Analysis of new business

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

UK Pension / Reinsurance accepted external

Number of policyholders /

scheme membersAmount of premiums

Number of policyholders /

scheme membersAmount of premiums

1 2 3 4 5 6

735 Group money purchase pension property linked ELAS 754

Single premium business

24

Product code

numberProduct description

Regular premium business

23032011:13:19:23

Form 47

Long-term insurance business : Analysis of new business

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

UK Pension / Reinsurance accepted intra-group

Number of policyholders /

scheme membersAmount of premiums

Number of policyholders /

scheme membersAmount of premiums

1 2 3 4 5 6

435 Miscellaneous non-profit HLL 18489 5370

725 Individual pensions property linked CMIGL 17378 110623

735 Group money purchase pension property linked CMIGL 30633 52015

750 Income drawdown property linked CMIGL 11955

755 Trustee investment plan CMIGL 238

Single premium business

25

Product code

numberProduct description

Regular premium business

23032011:13:19:23

Form 48

Long-term insurance business : Assets not held to match linked liabilities

Name of insurer Clerical Medical Managed Funds

Category of assets 10 Total long term insurance business assets

Financial year ended 31 December 2010

Units £000

Unadjusted assets

Economic exposure

Expected income from

assets in column 2

Yield before adjustment

Return on assets in

financial year

1 2 3 4 5

Land and buildings 11

Approved fixed interest securities 12 274671 285403 11500 4.00

Other fixed interest securities 13 366 3 0.86

Variable interest securities 14 14845 18768 186 3.52

UK listed equity shares 15

Non-UK listed equity shares 16

Unlisted equity shares 17

Other assets 18 118431 103409 547 0.53

Total 19 407946 407946 12237 3.10

Land and buildings 21

Approved fixed interest securities 22

Other fixed interest securities 23

Variable interest securities 24

UK listed equity shares 25

Non-UK listed equity shares 26

Unlisted equity shares 27

Other assets 28

Total 29

Overall return on with-profits assets

Post investment costs but pre-tax 31

Return allocated to non taxable 'asset shares' 32

Return allocated to taxable 'asset shares' 33

Assets backing non-profit liabilities and non-profit capital requirements

Assets backing with-profits liabilities and with-profits capital requirements

26

23032011:13:19:23

Form 50

Long-term insurance business : Summary of mathematical reserves

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life UK Pension Overseas Total Financial year

Total Previous year

1 2 3 4 5

GrossForm 51 - with-profits 11

Form 51 - non-profit 12 (2524) 319573 317049 292384

Form 52 13

Form 53 - linked 14 9734727 3900 9738627 9459202

Form 53 - non-linked 15 730 13779 14509 33204

Form 54 - linked 16 17399

Form 54 - non-linked 17 19538 19538

Total 18 (1794) 10087617 3900 10089723 9802188

Reinsurance - externalForm 51 - with-profits 21

Form 51 - non-profit 22 (2680) (2680)

Form 52 23

Form 53 - linked 24 65303 65303 71334

Form 53 - non-linked 25

Form 54 - linked 26

Form 54 - non-linked 27

Total 28 62623 62623 71334

Reinsurance - intra-groupForm 51 - with-profits 31

Form 51 - non-profit 32

Form 52 33

Form 53 - linked 34

Form 53 - non-linked 35

Form 54 - linked 36

Form 54 - non-linked 37

Total 38

Net of reinsuranceForm 51 - with-profits 41

Form 51 - non-profit 42 (2524) 322253 319729 292384

Form 52 43

Form 53 - linked 44 9669424 3900 9673324 9387868

Form 53 - non-linked 45 730 13779 14509 33204

Form 54 - linked 46 17399

Form 54 - non-linked 47 19538 19538

Total 48 (1794) 10024994 3900 10027100 9730855

27

23032011:13:19:23

Form 51

Long-term insurance business : Valuation summary of non-linked contracts (other than accumulating with-profits contracts)

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

435 Miscellaneous non-profit HLL 3504843 9194 (2524)

28

23032011:13:19:23

Form 51

Long-term insurance business : Valuation summary of non-linked contracts (other than accumulating with-profits contracts)

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Pension / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

390 Deferred annuity non-profit HLL 13038 296472

400 Annuity non-profit (CPA) 45 75 769

435 Miscellaneous non-profit HLL 1669572 4426 22332

29

23032011:13:19:23

Form 51

Long-term insurance business : Valuation summary of non-linked contracts (other than accumulating with-profits contracts)

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Pension / Reinsurance ceded external

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

435 Miscellaneous non-profit (2680)

30

23032011:13:19:23

Form 53

Long-term insurance business : Valuation summary of property linked contracts

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Life / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

795 Miscellaneous property linked HLL 1636 730 730

31

23032011:13:19:23

Form 53

Long-term insurance business : Valuation summary of property linked contracts

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Pension / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

725 Individual pensions property linked CMIGL 240581 6723047 6723047 6723047

735 Group money purchase pensions property linked CMIGL 112080 2395486 2395486 2395486

735 Group money purchase pensions property linked ELAS 39899 39899 61 39960

755 Trustee investment plan CMIGL 280911 280911 280911

765 Group managed fund 295384 295384 295384

795 Miscellaneous property linked HLL 16319 13718 13718

32

23032011:13:19:23

Form 53

Long-term insurance business : Valuation summary of property linked contracts

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Pension / Reinsurance ceded external

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

725 Individual pensions property linked CMIGL 65303 65303 65303

33

23032011:13:19:23

Form 53

Long-term insurance business : Valuation summary of property linked contracts

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

Overseas / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

725 Individual pensions property linked CMIGL 453 3900 3900 3900

34

23032011:13:19:23

Form 54

Long-term insurance business : Valuation summary of index linked contracts

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

UK Pension / Gross

Product code

numberProduct description

Number of policyholders /

scheme members

Amount of benefit

Amount of annual office

premiums

Nominal value of units

Discounted value of units Other liabilities

Amount of mathematical

reserves

1 2 3 4 5 6 7 8 9

905 Index linked annuity HLL 618 19538 19538

35

23032011:13:19:23

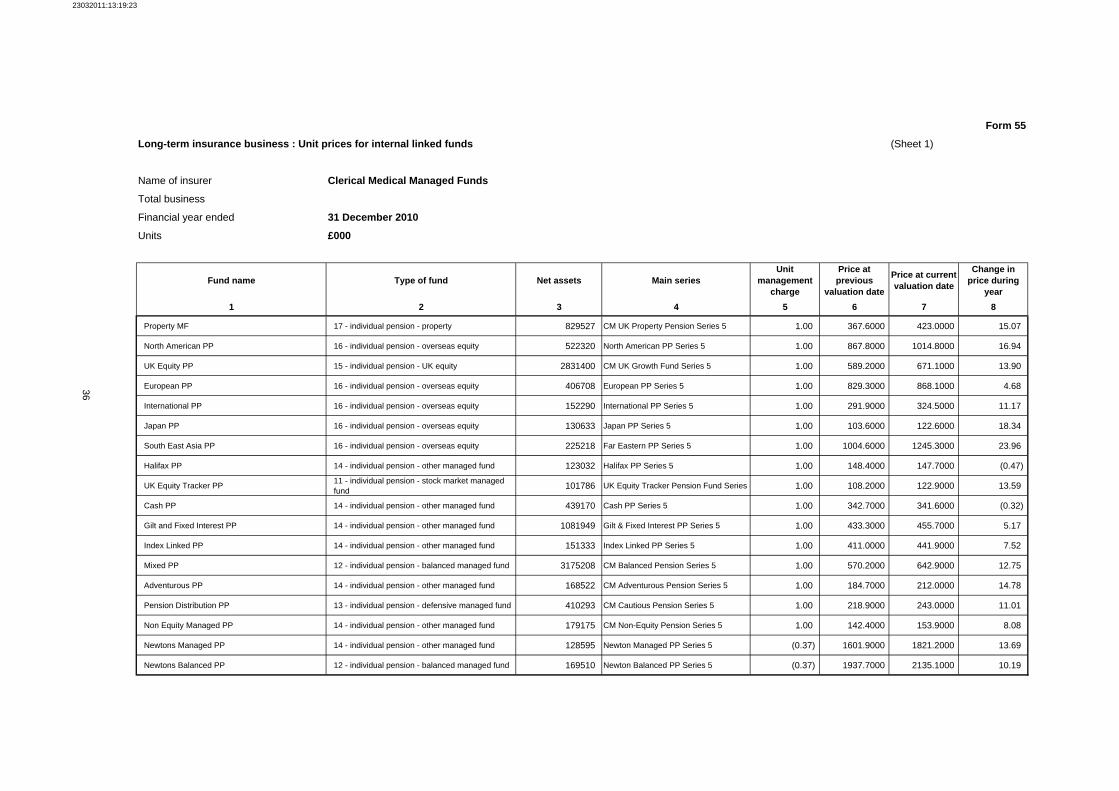

Form 55

Long-term insurance business : Unit prices for internal linked funds (Sheet 1)

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

Fund name Type of fund Net assets Main seriesUnit

management charge

Price at previous

valuation date

Price at current valuation date

Change in price during

year1 2 3 4 5 6 7 8

Property MF 17 - individual pension - property 829527 CM UK Property Pension Series 5 1.00 367.6000 423.0000 15.07

North American PP 16 - individual pension - overseas equity 522320 North American PP Series 5 1.00 867.8000 1014.8000 16.94

UK Equity PP 15 - individual pension - UK equity 2831400 CM UK Growth Fund Series 5 1.00 589.2000 671.1000 13.90

European PP 16 - individual pension - overseas equity 406708 European PP Series 5 1.00 829.3000 868.1000 4.68

International PP 16 - individual pension - overseas equity 152290 International PP Series 5 1.00 291.9000 324.5000 11.17

Japan PP 16 - individual pension - overseas equity 130633 Japan PP Series 5 1.00 103.6000 122.6000 18.34

South East Asia PP 16 - individual pension - overseas equity 225218 Far Eastern PP Series 5 1.00 1004.6000 1245.3000 23.96

Halifax PP 14 - individual pension - other managed fund 123032 Halifax PP Series 5 1.00 148.4000 147.7000 (0.47)

UK Equity Tracker PP 11 - individual pension - stock market managed fund 101786 UK Equity Tracker Pension Fund Series 5 1.00 108.2000 122.9000 13.59

Cash PP 14 - individual pension - other managed fund 439170 Cash PP Series 5 1.00 342.7000 341.6000 (0.32)

Gilt and Fixed Interest PP 14 - individual pension - other managed fund 1081949 Gilt & Fixed Interest PP Series 5 1.00 433.3000 455.7000 5.17

Index Linked PP 14 - individual pension - other managed fund 151333 Index Linked PP Series 5 1.00 411.0000 441.9000 7.52

Mixed PP 12 - individual pension - balanced managed fund 3175208 CM Balanced Pension Series 5 1.00 570.2000 642.9000 12.75

Adventurous PP 14 - individual pension - other managed fund 168522 CM Adventurous Pension Series 5 1.00 184.7000 212.0000 14.78

Pension Distribution PP 13 - individual pension - defensive managed fund 410293 CM Cautious Pension Series 5 1.00 218.9000 243.0000 11.01

Non Equity Managed PP 14 - individual pension - other managed fund 179175 CM Non-Equity Pension Series 5 1.00 142.4000 153.9000 8.08

Newtons Managed PP 14 - individual pension - other managed fund 128595 Newton Managed PP Series 5 (0.37) 1601.9000 1821.2000 13.69

Newtons Balanced PP 12 - individual pension - balanced managed fund 169510 Newton Balanced PP Series 5 (0.37) 1937.7000 2135.1000 10.19

36

23032011:13:19:23

Form 55

Long-term insurance business : Unit prices for internal linked funds (Sheet 2)

Name of insurer Clerical Medical Managed Funds

Total business

Financial year ended 31 December 2010

Units £000

Fund name Type of fund Net assets Main seriesUnit

management charge

Price at previous

valuation date

Price at current

valuation date

Change in price during

year1 2 3 4 5 6 7 8

Schroder UK Mid 250 PP 15 - individual pension - UK equity 109661 Schroder UK Mid 250 PP Series 5 0.19 127.3000 154.5000 21.37

High Income IP 14 - individual pension - other managed fund 254060 CM High Income IP Series 5 0.11 151.0000 167.5000 10.93

BGI UK Equity PP 15 - individual pension - UK equity 169600 BGI UK Eq PP Series 5 1.00 99.0000 115.0000 16.16

BGI World (Ex UK) Equity PP 16 - individual pension - overseas equity 160601 BGI World (ex UK) PP Series 5 0.99 102.5000 118.1000 15.22 37

23032011:13:19:23

Form 57Long-term insurance business: Analysis of valuation interest rate

Name of insurer Clerical Medical Managed Funds

Total business CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

Net mathematical reserves

Net valuation interest rate

Gross valuation interest rate

Risk adjusted yield on

matching assets

2 3 4 5

316010 3.96 4.18

6662 1.89 1.94

31104 n/a n/a

Total 353776

Product group

1

UK Pensions Form 51 Deferred annuity non-profit (HLL)

Uk Pensions Form 51 term assurances non profit (HLL)

Misc

38

23032011:13:19:23

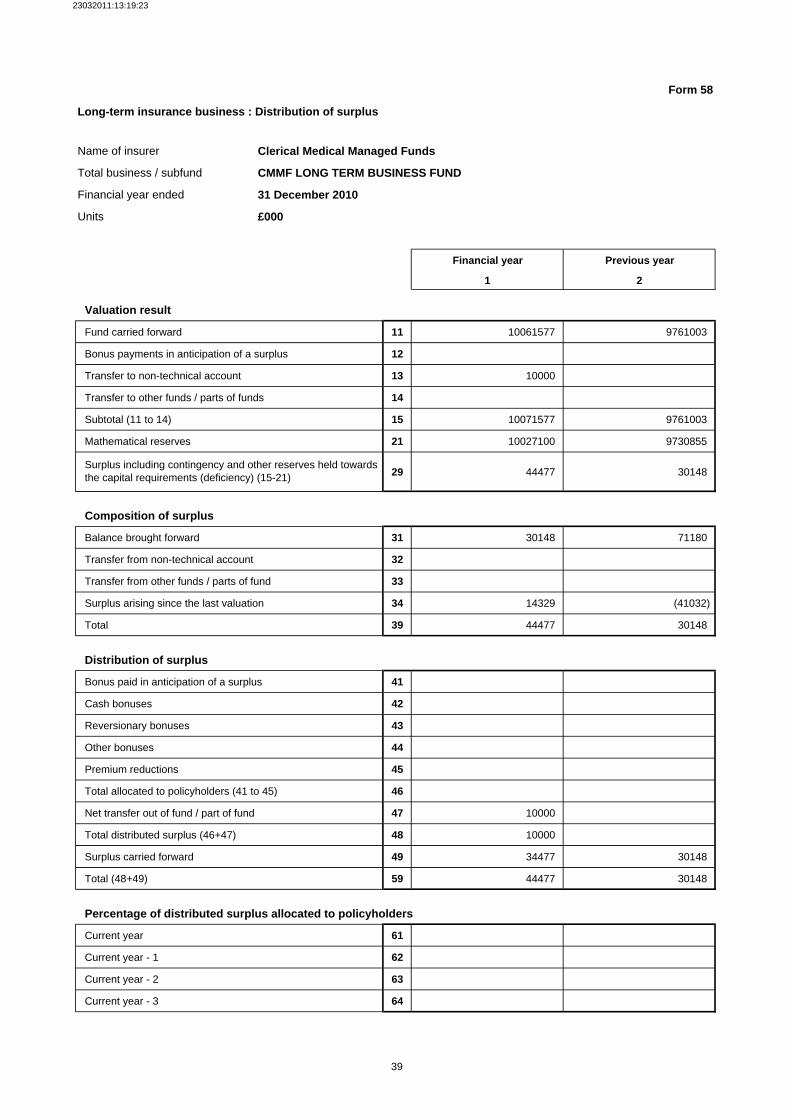

Form 58

Long-term insurance business : Distribution of surplus

Name of insurer Clerical Medical Managed Funds

Total business / subfund CMMF LONG TERM BUSINESS FUND

Financial year ended 31 December 2010

Units £000

Financial year Previous year

1 2

Valuation result

Fund carried forward 11 10061577 9761003

Bonus payments in anticipation of a surplus 12

Transfer to non-technical account 13 10000

Transfer to other funds / parts of funds 14

Subtotal (11 to 14) 15 10071577 9761003

Mathematical reserves 21 10027100 9730855

29 44477 30148

Composition of surplus

Balance brought forward 31 30148 71180

Transfer from non-technical account 32

Transfer from other funds / parts of fund 33

Surplus arising since the last valuation 34 14329 (41032)

Total 39 44477 30148

Distribution of surplus

Bonus paid in anticipation of a surplus 41

Cash bonuses 42

Reversionary bonuses 43

Other bonuses 44

Premium reductions 45

Total allocated to policyholders (41 to 45) 46

Net transfer out of fund / part of fund 47 10000

Total distributed surplus (46+47) 48 10000

Surplus carried forward 49 34477 30148

Total (48+49) 59 44477 30148

Percentage of distributed surplus allocated to policyholders

Current year 61

Current year - 1 62

Current year - 2 63

Current year - 3 64

Surplus including contingency and other reserves held towards the capital requirements (deficiency) (15-21)

39

23032011:13:19:23

Form 60Long-term insurance capital requirement

Name of insurer Clerical Medical Managed Funds

Global business

Financial year ended 31 December 2010Units £000

LTICR factor

Gross reserves / capital at

risk

Net reserves / capital at

risk

Reinsurance factor

LTICR Financial

year

LTICR Previous

year

1 2 3 4 5 6

Insurance death risk capital component

Life protection reinsurance 11 0.0%

Classes I (other), II and IX 12 0.1%

Classes I (other), II and IX 13 0.15%

Classes I (other), II and IX 14 0.3% 5193242 5193242 15580 19769

Classes III, VII and VIII 15 0.3%

Total 16 5193242 5193242 15580 19769

Insurance health risk and life protection reinsurance capital componentClass IV supplementaryclasses 1 and 2 and life protection reinsurance

21

Insurance expense risk capital componentLife protection and permanenthealth reinsurance 31 0%

Classes I (other), II and IX 32 1% 336587 339267 1.01 3393 3098

Classes III, VII and VIII(investment risk) 33 1% 14509 14509 1.00 145 332

Classes III, VII and VIII(expenses fixed 5 yrs +) 34 1%

Classes III, VII and VIII(other) 35 25% 616 1370

Class IV (other) 36 1%

Class V 37 1%

Class VI 38 1%

Total 39 4154 4800

Insurance market risk capital componentLife protection and permanenthealth reinsurance 41 0%

Classes I (other), II and IX 42 3% 336587 339267 1.01 10178 9293

Classes III, VII and VIII(investment risk) 43 3% 14509 14509 1.00 435 996

Classes III, VII and VIII(expenses fixed 5 yrs +) 44 0%

Classes III, VII and VIII(other) 45 0% 9738627 9673324

Class IV (other) 46 3%

Class V 47 0%

Class VI 48 3%

Total 49 10089723 10027100 10613 10290

Long term insurance capital requirement 51 30347 34859

1.00

40

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

41

*0201* Waiver and modification rules

The FSA, on the application of the firm, made a direction under section 148 of the Financial Services and Markets Act 2000 in December 2010. The effect of the direction is to modify the provisions of INSPRU 3.1.35R and IPRU(INS) Appendix 9.3 so that a more appropriate rate of interest is used for assets taken in combination.

*0301* Reconciliation of net admissible assets to total capital resources after deductions

£’000

Total of admissible assets after deduction of market risk and counterparty

limits - Other than long term business assets – Form 13 (SH) line 89 184,470

Total of admissible assets after deduction of market risk and counterparty

limits - long term business assets – Form 13 (NP) line 89 10,100,808

Mathematical reserves, after distribution of surplus – Form 14 line 11 (10,027,100)

Cash bonuses which had not been paid to policyholders prior to end of the

financial year – Form 14 line 12 -

Total other insurance and non-insurance liabilities – Form 14 line 49 (39,231)

Total liabilities - other than long term insurance business – Form 15 line 69 (28)

218,919

Components of capital resources treated as a liability in Form 15 -

Total capital resources after deductions – Form 3 Line 79 218,919

*0310* Details of positive and negative valuation differences

£’000Negative valuation differences on liabilities (2,738)

Positive valuation differences on liabilities

Net positive valuation difference – Form 3 line 35 (2,738)

Valuation differences arise as a result of changes in the valuation of long-term liabilities.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

42

*0313* Reconciliation of profit and loss and other reserves to Form 16

£’000 Profit and Loss Account and other reserves as at 31 December 2009 Form 3 Line 12 Column 4 (96,592)Profit and Loss Account and other reserves as at 31 December 2010 Form 3 Line 12 Column 3 (80,058)Movement in Profit and Loss Account and Other Reserves 16,534

Reporting basis differences (4,339)

Long Term Business Fund profit / (loss) retained for the financial year 4,329

Profit retained for the financial year – Form 16 line 59 16,524 *1301* and 1308 Aggregate Value of Certain Investments

The company has no investments meeting the specified criteria. *1304* and 1310 Set off of amounts – long term insurance business Amounts have been set off to the extent permitted by generally accepted accounting principles. *1305* and 1319 Maximum permitted counterparty limits

The Company’s investment guidelines set maximum counterparty limits in order to maintain the admissibility of assets in accordance with INSPRU 2.1.22. Shareholder and Non Profit funds have mandates which are reviewed annually. The Company's maximum approved counterparty limits for the SWIP Defensive Gilt fund (0-5 year Gilts) and SWIP GLF (stable NAV cash fund) are £1bn and £6bn respectively across the Lloyds Banking Group Insurance Division as a whole. The table below considers the remaining Shareholder and Non Profit fund limits for approved and unapproved counterparties.

Credit rating of bond Maximum percentage of fund Maximum absolute amount

AAA Sovereigns/AAA Supranationals/AAA Government Agencies

10% £200m

AAA 5% £60m AA 3% £50m A 2% £40m BBB or below 0% £0m

During the year, there was 1 instance of a breach in a lower limit that had been applied to a counterparty due to a downgrading in its credit rating. Action was taken to resolve the breach within 24 hours of identification. There were 6 instances of breaches where dispensation was given to maintain the position due to the expectations of the counterparty.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

43

*1306* and 1312 Exposure to large counterparties

There were no counterparty exposures held at year end that were greater than 5% of the sum of the base capital resources requirements and long term insurance liabilities, excluding property linked liabilities and net of reinsurance ceded (2009 £nil).

*1318* Details of other adjustments to assets

Long term insurance business – Non Profit £’000

Difference between tax on IFRS account reserves and FSA 63

Linked liabilities included in net asset value on FSA Form 13 Line 59 included as liability

in IFRS accounts) 19,500

19,563

*1401* No provision for adverse changes under either GENPRU 1.3.30R to GENPRU 1.3.33R or INSPRU 3.2.17R and INSPRU 3.2.18R has been made. The Company considers asset valuations in the context of the requirements of GENPRU 1.3.30R to GENPRU 1.3.33R. The need for a provision for adverse variation is also considered by the Actuarial Function Holder. The Company's mark to model valuations are formally reviewed and signed off to provide additional comfort over robustness. The Company reviews any potential liquidity issues on assets on a regular basis and incorporates valuation adjustments if required. The Company reviews its investments to identify whether any provisions are required pursuant to INSPRU 3.2.17R and INSPRU 3.2.18R. Sufficient cover is held for all positions to match reasonably foreseeable adverse variations and no non-approved derivatives or quasi-derivatives are held.

*1402* Liabilities

a) Charges over assets

There are no charges over assets.

b) Potential capital gains tax liability

There is no potential capital gains tax liability should the Company dispose of its assets at 31 December 2010.

c) Contingent liabilities

There are no contingent liabilities.

d) Guarantees, indemnities or other contractual commitments affected other than in the ordinary

course of insurance business and in respect of related companies.

There are no such items.

e) Other fundamental uncertainties

The company is not aware of any fundamental uncertainties affecting its business.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

44

*1405* Details of other adjustments to liabilities £’000

Linked liabilities included in net asset value on FSA Form 13 Line 59 (included as

liability in IFRS accounts) 19,500

Deferred Tax on IFRS account and FSA differences 28,003

Difference between IFRS account reserves and FSA mathematical reserves (2,736)

Difference between tax on IFRS account reserves and FSA 63

44,830

*1501* No provision for adverse changes under either GENPRU 1.3.30R to GENPRU 1.3.33R or INSPRU

3.2.17R and INSPRU 3.2.18R has been made. The Company considers asset valuations in the context of the requirements of GENPRU 1.3.30R to GENPRU 1.3.33R. The need for a provision for adverse variation is also considered by the Actuarial Function Holder. The Company's mark to model valuations are formally reviewed and signed off to provide additional comfort over robustness. The Company reviews any potential liquidity issues on assets on a regular basis and incorporates valuation adjustments if required. The Company reviews its investments to identify whether any provisions are required pursuant to INSPRU 3.2.17R and INSPRU 3.2.18R. Sufficient cover is held for all positions to match reasonably foreseeable adverse variations and no non-approved derivatives or quasi-derivatives are held.

*1502* Liabilities

a) Charges over assets

There are no charges over assets.

b) Potential capital gains tax liability

There is no potential capital gains tax liability should the Company dispose of its assets at 31 December 2010.

c) Contingent liabilities

There are no contingent liabilities.

d) Guarantees, indemnities or other contractual commitments affected other than in the ordinary

course of insurance business and in respect of related companies.

There are no such items.

e) Other fundamental uncertainties There are no other uncertainties which it is necessary to disclose.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

45

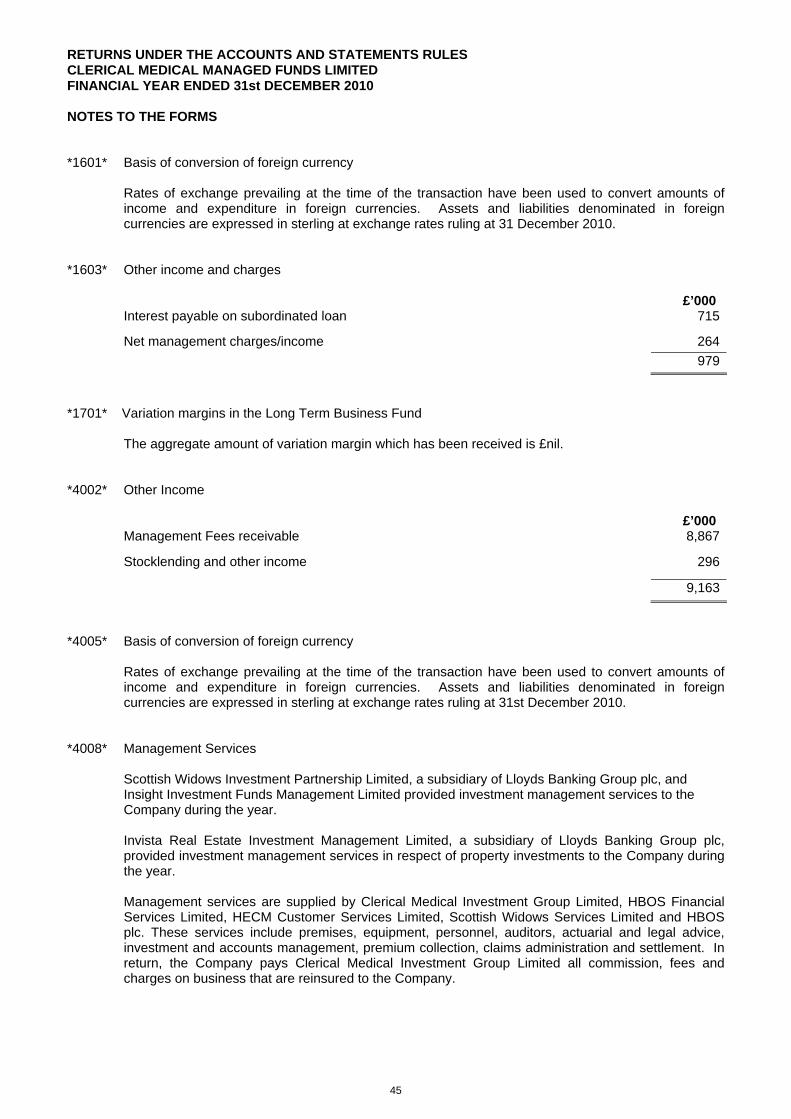

*1601* Basis of conversion of foreign currency

Rates of exchange prevailing at the time of the transaction have been used to convert amounts of income and expenditure in foreign currencies. Assets and liabilities denominated in foreign currencies are expressed in sterling at exchange rates ruling at 31 December 2010.

*1603* Other income and charges

£’000 Interest payable on subordinated loan 715

Net management charges/income 264 979

*1701* Variation margins in the Long Term Business Fund

The aggregate amount of variation margin which has been received is £nil.

*4002* Other Income

£’000

Management Fees receivable 8,867

Stocklending and other income 296

9,163

*4005* Basis of conversion of foreign currency

Rates of exchange prevailing at the time of the transaction have been used to convert amounts of income and expenditure in foreign currencies. Assets and liabilities denominated in foreign currencies are expressed in sterling at exchange rates ruling at 31st December 2010.

*4008* Management Services

Scottish Widows Investment Partnership Limited, a subsidiary of Lloyds Banking Group plc, and Insight Investment Funds Management Limited provided investment management services to the Company during the year.

Invista Real Estate Investment Management Limited, a subsidiary of Lloyds Banking Group plc, provided investment management services in respect of property investments to the Company during the year.

Management services are supplied by Clerical Medical Investment Group Limited, HBOS Financial

Services Limited, HECM Customer Services Limited, Scottish Widows Services Limited and HBOS plc. These services include premises, equipment, personnel, auditors, actuarial and legal advice, investment and accounts management, premium collection, claims administration and settlement. In return, the Company pays Clerical Medical Investment Group Limited all commission, fees and charges on business that are reinsured to the Company.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

46

*4009* Material Connected Party Transactions

Name of connected party

Relationship with connected party

Amount £000

Description of transaction

Clerical Medical Investment Group Limited

Parent undertaking 686,301 Premiums reassured inwards

Clerical Medical Investment Group Limited

Parent undertaking 1,307,865 Claims reassured inwards

HIFM European Special Situations Institutional Income Shares

Fellow group undertaking

267,521

Net investment in OEIC subsidiary during year

HIFM Japanese OEIC Institutional Income Shares

Fellow group undertaking

130,690 Net investment in OEIC subsidiary during year

HIFM North American OEIC Institutional Income

Fellow group undertaking

522,403 Net investment in OEIC subsidiary during year

HIFM UK Property Fund Fellow group undertaking

48,414 Net investment in OEIC subsidiary during year

*4401* Bases of asset valuation

Linked assets are valued using the FSA Handbook Rules in GENPRU 1.3. Financial assets and Instruments used to cover linked liabilities are stated at market value. Stock exchange securities and investments in collective investment schemes have been valued at bid prices. Investment property is shown at open market value as determined by independent valuation. Investment property valuations are carried out by persons who are members of the Royal Institute of Chartered Surveyors and were conducted in accordance with the "RICS Statement of Asset Valuation and Guidance Notes". Other assets have been valued using appropriate international financial reporting standards applicable to the firm for the purpose of its external financial reporting. The Rules in GENPRU 1.3.30 to GENPRU 1.3.33 may require management to make adjustments to these valuations

*4402* Aggregate value of derivative contracts

Gross VariationMargin

Net

£000 £000 £000 Derivative Rights 496 (722) (226) Derivative Liabilities (2,886) (2,886) Net (2,390) (722) (3,112)

*4701* New group schemes

No new group schemes commenced in 2010.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 NOTES TO THE FORMS

47

*4900* Form 49 has been omitted on account of de minimis limits as per IPRU(INS) Rule 9.11. *4901* Rating agencies used Standard and Poor's and Moody's Credit ratings have been used. *5103* Details of Miscellaneous contracts

Product code 435 – Life – Miscellaneous non-profit HLL Reinsurance of Equitable Life Assurance Society business accepted under the R2 treaty with Halifax

Life Limited. Reserve -£2.524m.

*5103* Details of Miscellaneous contracts continued

Product code 435 – Pension – Miscellaneous non-profit HLL Reinsurance of Equitable Life Assurance Society business accepted under the R2 treaty with Halifax Life Limited. Reserve £22.332m. Product code 435 – Pension – Miscellaneous non-profit Default reserve held in relation to business reinsured to Suffolk Life. Reserve £2.680m

*5301* Treatment of administration funds

Product code 765 – Pension

Managed Funds number of schemes under administration is 51. This number is made up of 41 investment only schemes and 10 full administration schemes.

*5303* Details of Miscellaneous contracts

Product code 795 – Life – Miscellaneous property linked HLL Reinsurance of Equitable Life Assurance Society business accepted under the R2 treaty with Halifax Life Limited. Reserve £0.730m.

Product code 795 – Pension – Miscellaneous property linked HLL Reinsurance of Equitable Life Assurance Society business accepted under the R2 treaty with Halifax Life Limited. Reserve £13.718m.

*5600* Form has been omitted on account of de minimis limits as per IPRU(INS) Rule 9.11.

*5701* Negative mathematical reserves

Negative mathematical reserves on Life term assurance (miscellaneous non-profit HLL) have been used to offset positive reserves on deferred annuity business (deferred annuity non profit HLL). These negative reserves total -£6.5m.

*6001* Insurance Health Risk Capital Component

The gross annual premiums for this class of business are less than 1% of the gross annual premiums of the company so Forms 11 and 12 are not needed. The Insurance Health Risk Capital Component is calculated as the greater of 18% of annual premiums and 26% of gross claims. The capital required for PHI business is the same as if Forms 11 and 12 had been completed.

RETURNS UNDER THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31st DECEMBER 2010 ADDITIONAL INFORMATION REQUIRED BY RULE 9.29 OF THE ACCOUNTS AND STATEMENTS RULES

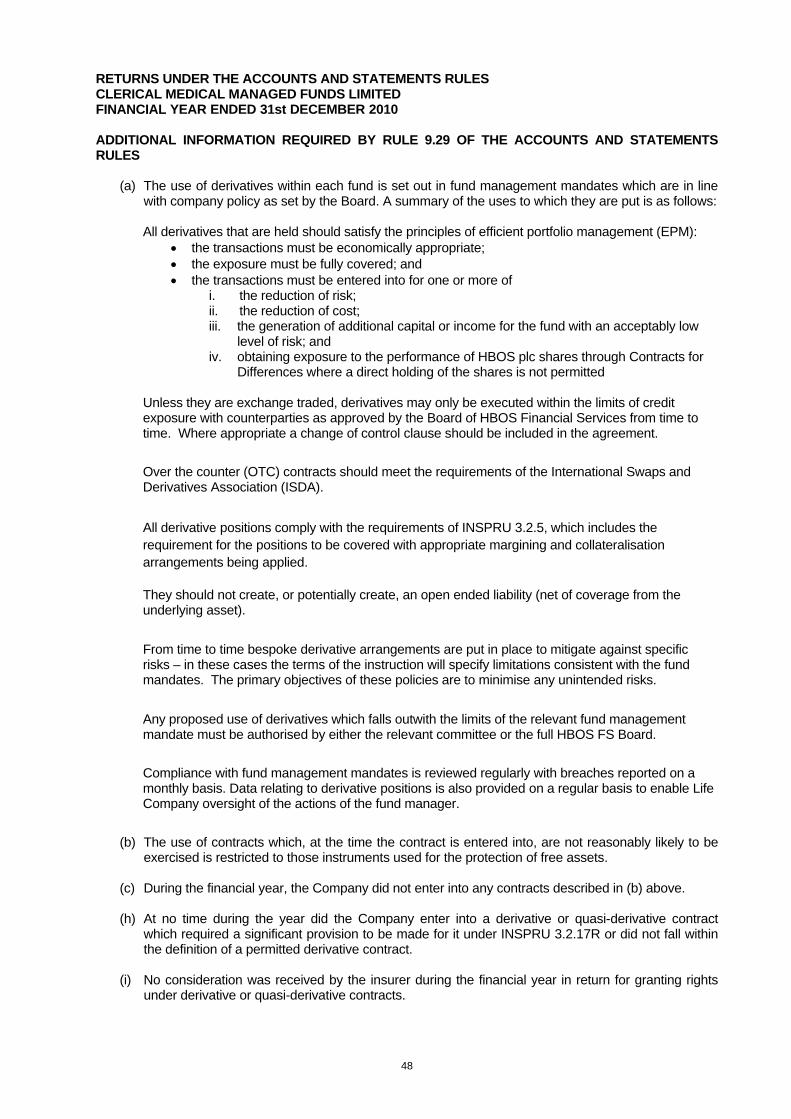

(a) The use of derivatives within each fund is set out in fund management mandates which are in line with company policy as set by the Board. A summary of the uses to which they are put is as follows:

All derivatives that are held should satisfy the principles of efficient portfolio management (EPM):

• the transactions must be economically appropriate; • the exposure must be fully covered; and • the transactions must be entered into for one or more of

i. the reduction of risk; ii. the reduction of cost; iii. the generation of additional capital or income for the fund with an acceptably low

level of risk; and iv. obtaining exposure to the performance of HBOS plc shares through Contracts for

Differences where a direct holding of the shares is not permitted

Unless they are exchange traded, derivatives may only be executed within the limits of credit exposure with counterparties as approved by the Board of HBOS Financial Services from time to time. Where appropriate a change of control clause should be included in the agreement.

Over the counter (OTC) contracts should meet the requirements of the International Swaps and Derivatives Association (ISDA).

All derivative positions comply with the requirements of INSPRU 3.2.5, which includes the requirement for the positions to be covered with appropriate margining and collateralisation arrangements being applied. They should not create, or potentially create, an open ended liability (net of coverage from the underlying asset).

From time to time bespoke derivative arrangements are put in place to mitigate against specific risks – in these cases the terms of the instruction will specify limitations consistent with the fund mandates. The primary objectives of these policies are to minimise any unintended risks.

Any proposed use of derivatives which falls outwith the limits of the relevant fund management mandate must be authorised by either the relevant committee or the full HBOS FS Board.

Compliance with fund management mandates is reviewed regularly with breaches reported on a monthly basis. Data relating to derivative positions is also provided on a regular basis to enable Life Company oversight of the actions of the fund manager.

(b) The use of contracts which, at the time the contract is entered into, are not reasonably likely to be exercised is restricted to those instruments used for the protection of free assets.

(c) During the financial year, the Company did not enter into any contracts described in (b) above.

(h) At no time during the year did the Company enter into a derivative or quasi-derivative contract

which required a significant provision to be made for it under INSPRU 3.2.17R or did not fall within the definition of a permitted derivative contract.

(i) No consideration was received by the insurer during the financial year in return for granting rights

under derivative or quasi-derivative contracts.

48

49

STATEMENT OF INFORMATION ON SHAREHOLDER CONTROLLER AS REQUIRED BY RULE 9.30 OF THE ACCOUNTS AND STATEMENTS RULES CLERICAL MEDICAL MANAGED FUNDS LIMITED FINANCIAL YEAR ENDED 31 DECEMBER 2010 The immediate shareholder controller of the Company during the financial year was Clerical Medical Investment Group Limited. Clerical Medical Managed Funds Limited is a wholly owned and controlled subsidiary of Clerical Medical Investment Group Limited. Clerical Medical Investment Group Limited is a wholly owned and controlled subsidiary of HBOS Financial Services Limited.

HBOS Financial Services Limited is a wholly owned and controlled subsidiary of HBOS Insurance & Investment Group Limited. HBOS Insurance & Investment Group Limited is a wholly owned and controlled subsidiary of HBOS plc.

HBOS plc is a wholly owned and controlled subsidiary of Lloyds Banking Group plc. Clerical Medical Investment Group Limited holds all the issued shares of the Company and is thereby entitled to exercise all the associated voting powers at any general meeting of the Company.

CLERICAL MEDICAL MANAGED FUNDS LIMITED APPENDIX 9.4 FOR PERIOD ENDED DECEMBER 2010 ABSTRACT OF VALUATION REPORT

50

1. Introduction (1) Date of Investigation The valuation was made at 31 December 2010 (2) Date of Previous Investigation The previous valuation was made at 31 December 2009 (3) Date of Interim Investigation Not applicable. 2. Product Range (1) Direct Written Business There have been no changes to products in 2010. (2) Reinsurance Accepted There have been no significant changes to products in 2010 which would affect the reserves held under the reinsurance treaties. 3. Discretionary Charge and Benefits (1) There is no with-profit business in Clerical Medical Managed Funds Limited (CMMF) and therefore no option to apply a market value adjuster. (2) There have been no changes to premiums on reviewable protection policies.

(3) Not applicable.

(4) There are no service charges on direct written business in CMMF

(5) There are no benefit charges on direct written business in CMMF

(6) Not applicable. (7) Unit Pricing for Internal Linked Funds (a) (i) Creation and cancellation of units of internal linked funds:

The Company’s policy is to match the units allocated for policies (the “liability units”) closely to the units available within each corresponding unit fund (the “asset units”). The excess of asset units over the liability units is called the box of units. The Company’s policy is to avoid negative unit boxes, however, for practical reasons these can arise from time to time. The Company's policy also places a limit on the maximum size of the box of units for each fund, after allowing for any units reserved for new policies which have already been accepted but have yet to be issued. Whenever units in a fund are created or cancelled, cash or assets of equivalent value at the bare price are added or deducted respectively.

Within the above policy, the Company’s practice is to create or cancel units such that each fund’s box size is the smallest practical commensurate with efficient dealing in the investments permitted under the guidelines for the fund.

(ii) Unit Prices:

The unit prices make allowance for the actual or expected outgoings from the fund, actual tax charges and prospective tax liabilities attributable to the fund and are computed for each fund normally each working day as follows:-

CLERICAL MEDICAL MANAGED FUNDS LIMITED APPENDIX 9.4 FOR PERIOD ENDED DECEMBER 2010 ABSTRACT OF VALUATION REPORT

51

i) The assets of the fund are valued, together with any accrued income and uninvested cash as

follows:- a) The maximum value of any asset may not exceed the market value at which it may be

purchased, increased by any charges which may be expected; and b) The minimum value of any asset may not be less than the market value at which it may be

sold, reduced by any charges which may be expected. c) The mid-market value of any asset is the average of the maximum and minimum values.

ii) For listed securities, prices quoted on a recognised Stock Exchange are used. Otherwise, the value of

assets is determined by the Company in conjunction with its investment managers.

iii) Any other charges incurred or expected are deducted or added. iv) For single priced funds, the price of the units is the sum of the mid-market values of the assets

divided by the number of units in issue. v) For dual priced funds, the price will be on a bid or offer basis as appropriate.