Embed Size (px)

Citation preview

Claiming Scientific Research andExperimental DevelopmentGuide to Form T661

T4088(E) Rev. 01

Advisory ServicesThere are a number of advisory services provided toSR&ED claimants to enhance awareness of programrequirements and to help SR&ED claimants submitsuccessful claims. These services are described in the“General Information” section of this guide.

Project informationWe recommend that you submit a summary of each of yourprojects in four pages or less.

Application policiesThe following new application policies have been issued inyear 2000:

SR&ED 2000-01 – Cost of materials for SR&ED

SR&ED 2000-02 – Guidelines for resolving claimants’ SR&EDconcerns

SR&ED 2000-03 – Government Assistance – Treatment ofProvincial and Territorial R&D Assistance

SR&ED 2000-04 – Recapture of Investment Tax Credit

Other application policies will be developed in 2001 andwill be available on the SR&ED Web site as soon as they arefinalized. Also, a list of application policies issued inprevious years can be found on the Web site.

Internet site – www.ccra.gc.ca/sred/A number of papers have been developed to clarify SR&EDissues and are available on the Web site:

n SR&ED Project Definition – Principles

n Action Plan: Consultation to Implementation

n Software/Information Technology Sector Guidance

n Claim Review Process Letter

n Guide to Conducting a Scientific Research and ExperimentalDevelopment Review

Revision of Interpretation BulletinInterpretation Bulletin IT-151R5 – Scientific Research andExperimental Development Expenditures was released onOctober 17, 2000. The new version of the bulletin cancelsInterpretation Bulletin IT-151R3 dated June 24, 1988. Thecomments in this bulletin generally apply to expenditureson scientific research and experimental developmentincurred in taxation years ending after December 2, 1992.Interpretation Bulletin IT-151R4 will continue to apply,subject to certain transitional provisions, to thoseexpenditures incurred in taxation years ending before thattime and after December 15, 1987.

SR&ED coordinating officesA list of the SR&ED coordinating tax services offices andthe offices they serve is provided at the end of this guide.

February 28, 2000 budget proposal,Government assistance – Provincialsuper-deductions programProvincial SR&ED investment tax credits (ITCs) areconsidered to be government assistance for federal taxpurposes. These provincial and territorial ITCs reduce thefederal expenditure base on which federal ITCs aredetermined.

For taxation years commencing after February 2000, thebudget proposes to treat a specified percentage ofprovincial deductions for SR&ED in excess of the actualamount of the expenditure as government assistance. Thespecified percentage will be based on the provincial taxrates applicable to income earned in the province by acorporation for the year.

La version française de cette publication est intitulée Demande pour la recherche scientifique et le développement expérimental –Guide pour le formulaire T661.

What’s New

3

Page Page

General Information.......................................................... 4

How to Complete Form T661 ........................................... 5Filing requirement .............................................................. 5How Form T661 is structured............................................ 6

Line-by-Line Explanations ............................................... 7Part 1 – General Information............................................ 7Part 2 – Scientific or Technological Project

Information ...................................................................... 9Step 1 – Project summary information ......................... 10Step 2 – Detailed project description ............................ 10

Part 3 – Summary of SR&ED Expenditures ..................... 11Step 1 – Allowable SR&ED expenditures for

SR&ED carried on in Canada ..................................... 11Step 2 – Pool of deductible SR&ED expenditures ....... 17Step 3 – Qualified SR&ED expenditures for ITC

purposes ........................................................................ 19Part 4 – Background Information ...................................... 27

Glossary................................................................................ 30

Tax services offices............................................................. 31

Blind or visually-impaired persons can get this publication inbraille and large print, and on audio cassette and computerdiskette. To order, please call 1-800-267-1267 weekdays between8:15 a.m. and 5:00 p.m. (Eastern Time).

In this guide, legislative references are to the Income Tax Act (the Act) and regulatory references are to the Income TaxRegulations (the Regulations).

Contents

4

Legislative referencesIncome Tax ActSections 37, 127.1 and 248(1)

Subsections 96(2.4), 96(3), 127(5), 127(8), 127(9), 127(10.1),127(10.3), 127(10.4), 127(11.1) to (11.8), 127(13) to (35),and 194(2)

Paragraphs 12(1)(t), 12(1)(v), 12(1)(x), 20(1)(hh), 96(1)(e.1),and 96(1)(g)

See other references in the current version of InterpretationBulletin IT-151, Scientific Research and ExperimentalDevelopment Expenditures.

Income Tax RegulationsSections 2900, 2902, 2903 and 8201

Paragraph 1102(1)(d)

Internet accessYou can find SR&ED Program information, policies,publications, draft papers for comments, and other usefulinformation on our Web site at www.ccra.gc.ca/sred/.

Our publicationsThe following publications will help you determine yourSR&ED claim. We recommend that you review the currentversion of these publications.

T4052, An Introduction to the Scientific Research andExperimental Development Program – This brochure describesthe scope of the incentive program and explains how toreceive the program’s benefits.

Interpretation Bulletin IT-151, Scientific Research andExperimental Development Expenditures – This bulletindiscusses the provisions of the Act and the Regulationsdealing with SR&ED expenditures and ITC.

Information Circular 86-4, Scientific Research andExperimental Development – The information circular clarifieswhat constitutes SR&ED under subsection 248(1) of the Act.

Information Circular 97-1, Scientific Research andExperimental Development – Administrative Guidelines forSoftware Development – The information circular assistsclaimants and our staff in interpreting how the taxincentives apply to software development.

Provincial and territorial tax incentivesProvincial and territorial incentives may also be availablefor your SR&ED expenditures. Contact your provincial taxauthority to determine if such incentives exist. You willfind the telephone number of the provincial and territorialauthority in the government section of your and telephonebook.

Advisory servicesThere are a number of advisory services provided toSR&ED claimants to enhance awareness of programrequirements and to help SR&ED claimants submitsuccessful claims. These services include:

1. First time SR&ED claimant service – This serviceprovides information and assistance for companies newto the program. Prospective claimants may visitCCRA’s Web site at www.ccra.gc.ca/sred/ for access toSR&ED publications or request an information kit inwhich many of these publications are included. Onrequest, one of SR&ED’s representatives will call newclaimants to answer questions. If necessary, a SR&EDrepresentative can arrange a personal visit to explainthe program and documentation requirements in moredetail.

2. Public information seminars – New claimants areinvited to attend one of SR&ED Program’s regularpublic information seminars that are held at locationsthroughout Canada. Please contact your local taxservices office if you wish to attend a seminar. The firsttime claimant service and public information seminarsgreatly aid new or potential claimants to betterunderstand their entitlements under the SR&EDProgram.

3. Preclaim Project Review (PCPR) – PCPR serviceprovides a business with an up-front review and apreliminary opinion on the eligibility of projects forSR&ED investment tax credits, before the claim is filed.A key aspect of the service is direct communicationbetween a claimant’s personnel, who understand thetechnical issues of the project, and a SR&ED scienceadvisor. The service helps claimants understand theSR&ED Program, including substantiationrequirements, and it addresses concerns before a claimis made.

4. Account Executive service – This service providesclaimants with a designated contact person. A claimantcan call the account executive for help with variousSR&ED Program areas, including technical or financialissues, as well as access to other services such as PCPR.The account executive will ensure that the appropriateassistance is provided. Through ongoing contact, theaccount executive helps the claimant better understandthe program.

You are encouraged to use these services which areavailable through most CCRA tax services offices across thecountry.

Simplified claim Form T665A simplified claim Form T665 is available and is part of ourinitiatives to streamline paperwork, particularly for smallbusinesses. This measure is designed to reduce theadministrative burden for companies claiming investmenttax credits for SR&ED.

General Information

5

You may use the simplified claim Form T665 if you are acorporation and you meet the following conditions:

n The total allowable expenditures for SR&ED carried on inCanada are $200,000 or less for the year;

n The corporation elects to use the proxy method for theyear; and

n There are no non-arm’s length SR&ED transactions.

There are also other conditions to be met. For more details,read the instructions attached to the simplified claimForm T665 available on the CCRA’s Web site or at your taxservices office.

Your opinion countsWe review this guide regularly. If you have comments orsuggestions that would help us improve the explanations inthis guide, we would like to hear from you.

Please send your comments to:

SR&ED DirectorateCanada Customs and Revenue Agency875 Heron RoadOttawa ON K1A 0L8

Filing requirementIf you have expenditures for SR&ED carried on in Canada,you must complete Form T661 and should send it withyour tax return, along with any related schedules andattachments. You have to file Form T661 whether or not,you claim an investment tax credit (ITC) in the current year.

NotesForm T661 applies only to SR&ED carried on in Canada.Expenditures for SR&ED conducted outside Canadashould not be claimed on Form T661. They should beclaimed with other business expenditures. If you wantmore information on how to treat these expenditures,read the current version of Interpretation Bulletin IT-151,Scientific Research and Experimental DevelopmentExpenditures, which is available on the CCRA’s Web site.

Generally, these out of country expenditures aredeductible under subsection 37(2) and are treated in thesame way as other business expenditures (i.e., youdeduct current expenditures in the year you incur them,and add capital expenditures to the appropriate capitalcost allowance class). Expenditures for SR&EDconducted outside Canada do not earn an ITC.

Technical personnel should complete Part 1 and Part 2 ofthe form, and the financial personnel should completePart 3. Part 4 may need information from both financial andtechnical personnel.

You have to file an original or revised Form T661 andSchedule T2SCH31 or Form T2038(IND.) for the year, nolater than the day that is 12 months after the filing-due date

of the return of income for the year. For a corporation, as ageneral rule, you have 18 months from the end of thetaxation year in which you incurred the expenditures toreport such expenditures. If you do not report anexpenditure by the reporting deadline on Form T661, youcannot deduct the expenditures for SR&ED purposes. Aswell, if you do not report your SR&ED expenditures withinthe same reporting deadline on Schedule T2SCH31 orForm T2038 (IND.), you will not be allowed to claim anyITC for the expenditures.

However, a corporation exempt from Part I tax underparagraph 149(1)(j) has to file Form T661 on or before thefiling-due date for the year. A corporation exempt from taxunder paragraph 149(1)(j) that does not file Form T661 ontime is subject to a penalty.

Under exceptional circumstances, if your claim is late-filed,you may apply to the Director of your tax services officeunder fairness provisions to have your claim accepted.

Information circulars 92-1, 92-2, and 92-3 containinformation and guidelines concerning the fairnessprovisions and examples of how they may be applied. Ingeneral, the comments in these circulars also apply to caseswhere the deadline prescribed in subsection 37(11) of theAct has not been met.

In general, this discretionary authority is exercised whenexceptional circumstances beyond the claimant’s controlhave prevented the claimant from meeting a legalrequirement or paying a required amount by the requireddeadline. The claimant must have shown reasonablediligence in his efforts to comply with the requirements ofthe Act.

General filing requirements for partnershipsIf the partnership’s members have to file Form T5013Summary, Partnership Information Return, the partnership’sT661 form and accompanying information should be filedwith the Partnership Information Return. A T5013 slip,Statement of Partnership Income, must be filed with eachpartner’s tax return. For more information, see the Guide forthe Partnership Information Return (T4068) which is availableon the CCRA’s Web site or at any tax services office.

When the partnership’s members do not have to file thePartnership Information Return, each partner has to fileForm T661 and financial statements for the partnershipwith his or her income tax return for the year. Each partneralso has to file an explanation of how the SR&ED allocationof income or loss was calculated for each partner for taxpurposes, and for the ITC.

The expenditures listed in Part 3 are the total SR&EDexpenditures at the partnership level, and not just aparticular partner’s prorata share of those expenditures.

Partnerships cannot carry forward an SR&ED expenditurepool balance to a later year. For more information onSR&ED expenditures and ITC of a partnership, read thecurrent version of Interpretation Bulletin IT-151, ScientificResearch and Experimental Development Expenditures.

How to Complete Form T661

6

How to speed up the processing of yourclaimTo ensure we can process your current year claim asquickly as possible:

n use the latest version of Form T661 (see the CCRA’sWeb site);

n file a complete claim. Filing an incomplete claim, or usinga previous version of Form T661 to file a current yearclaim will delay the processing of your return;

n place the complete Form T661 on top of your corporatetax return for quick identification;

n keep all technical and financial information to supportyour claim;

n file the SR&ED claim at the tax centre (filing your claimat your local tax services offices may delay the processingof your claim);

n respond in a timely manner to our requests for moreinformation; and

n check off the appropriate box on the T2 return requestinga direct deposit of your refundable ITC.

Complete claimSubsections 37(1) and 127(9) (definition of “qualifiedexpenditure”) require that the claimant supply theprescribed information on the prescribed forms.

A complete claim is one that supplies the information askedfor on Form T661 and Schedule T2SCH31 orForm T2038(IND.) (used to claim ITC on qualified SR&EDexpenditures) on the version of the forms that apply to theyear of the claim. Form T2 is also required in order to havea complete claim.

You must complete all parts of Form T661, the schedules,and all parts of Schedule T2SCH31 or Form T2038(IND.),and you must sign where required. For Form T661, youmust indicate whether you use the proxy or traditionalmethod to determine the SR&ED expenditures and relatedITC. A checklist of most of the required key information isprovided on page 1 of Form T661.

Even if a claim is complete, it must meet the requirementsof the definition of “scientific research and experimentaldevelopment” contained in subsection 248(1) of the Act,and also meet the rules under sections 37 and 127 of theAct.

Classified projectsIf a federal agency has designated one of your projectdescriptions as “classified information” for nationalsecurity reasons, please follow these instructions:

n Prepare and keep on file a fully completed T661 form,including all project descriptions in Part 2, Step 2.

n Send a letter to the Research and Technology Section atthe following address:

SR&ED DirectorateCanada Customs and Revenue Agency875 Heron RoadOttawa ON K1A 0L8

n In the letter, explain that certain project descriptions areclassified information, and that they are available onrequest.

n With your income tax return, send a copy of theabove-mentioned letter and the completed Form T661,without the descriptions of the classified project(s).

How Form T661 is structuredWe have divided the form into four parts:

Part 1 – General InformationProvide the information required and sign the“Certification and Election” area on page 1 of the form.

Part 2 – Scientific or Technological ProjectInformationStep 1 – Project Summary InformationProvide information for each SR&ED project you claim inthe taxation year. You have to indicate the total currentexpenditures and the capital expenditures you claimed foreach project.

Step 2 – Detailed Project DescriptionProvide project descriptions for the expenditures youclaimed in Part 3. Remember to have the individualresponsible for technical work complete this part.

Part 3 – Summary of SR&ED ExpendituresProvide expenditure information on all claims for SR&EDcarried on in Canada. This part represents the total cost forall projects. Keep in mind that you also have to provideindividual project cost information in Part 2 of the form.

All claimants should keep records of costs and explanationsof cost allocations associated with individual projects.These records should be made available during the claimreview.

Step 1 – Allowable SR&ED expenditures for SR&EDcarried on in Canada – In this section, list the totalallowable SR&ED expenditures that you made inthe year, both current and capital, for SR&EDcarried on in Canada.

Step 2 – Pool of deductible SR&ED expenditures – In thissection, you will calculate the SR&ED expenditurepool deduction that is available in the year, startingwith the amount of allowable expenditures forSR&ED carried on in Canada determined online 400, the deduction claimed in the year, andany balance of the SR&ED expenditure pooldeduction you can deduct in future years.

7

Step 3 – Qualified SR&ED expenditures for ITCpurposes – In this section, you will determine theSR&ED expenditures that qualify for a federal ITC.

Part 4 – Background InformationThis information on your business is needed to processyour SR&ED claim.

he following section explains the information you haveto provide on each line of Form T661. We recommend

that you read each explanation as you complete the form.

Part 1 – General InformationName, business address, Web site addressand postal codeEnter the registered business name, address, Web siteaddress (if available), and postal code. If you have to file aPartnership Information Return (Form T5013 Summary), enterthe name of the partnership.

Return for taxation yearWrite the dates of the beginning and the end of the taxationyear for which you are submitting the claim.

Business number, social insurance number,or partnership identification numberIn this area, enter the appropriate identification numberthat pertains to you.

Lines 100, 105, and 110Contact-personWrite the name, telephone number, and fax number of theperson best suited to provide information about the overallsubmission.

Lines 142, 145, and 150Answer questions on lines 142, 145, and 150 if you areentitled to a share of the SR&ED expenditures incurred by apartnership, and the partnership does not file a PartnershipInformation Return (Form T5013 Summary).

Lines 160 and 162Choice of methodYou can choose the traditional method and claim allSR&ED expenditures you incurred during the year, or youcan elect under clause 37(8)(a)(ii)(B) to use the proxymethod for the year. The proxy method provides analternative way to determine your SR&ED expendituresand investment tax credit (ITC) for overhead expenditures.

The proxy method involves calculating a substitute amountfor overhead expenditures using a formula, rather thanspecifically identifying and allocating these expenditures,as you would with the traditional method.

To determine your qualified SR&ED expenditures for ITCpurposes, calculate the amount representing the overheadexpenditures (the prescribed proxy amount (PPA)) as afixed percentage (65%) of the salaries or wages of theemployees directly engaged in SR&ED. Special rules applyto restrict the amount of salaries or wages of specifiedemployees you can include in the salary base. For moredetails, see the explanation for line 502. The PPA may beeligible for the 100% ITC refund.

You do not include the PPA in the SR&ED expenditurepool, and you do not deduct it when calculating income. Itrepresents the amount of overhead expenditures forSR&ED, and is used to determine your ITC for theseoverhead expenditures. The PPA is treated as a qualifiedexpenditure for ITC purposes. The actual overheadexpenses represented by the PPA are ordinary businessexpenses.

If you elect to use the proxy method, you will continue toclaim certain expenses separately. For example, you claimexpenditures for materials consumed for SR&EDseparately.

Lines 165 and 170Authorization and dateThe individual, an authorized signing officer of thecorporation, or an authorized partner will certify theinformation on Form T661, the related schedules, and theattachments. That person also has to indicate the choice ofmethod to calculate the SR&ED expenditures for the year.

Line-by-Line Explanations

T

8

Treatment of expenses under the proxy and traditional methods

Expenditure Traditional method Proxy method

Direct SR&ED salaries or wages n eligible for ITCn deductible under 37(1)(a)

(see line 300)

n eligible for ITC and base for proxyamount (see line 502)

n deductible under 37(1)(a)(see line 300)

n Overhead expenditures directlyrelated and incremental to SR&ED

n eligible for ITC (see line 360) n not specifically identifiedn covered in prescribed proxy amount

(see examples below)—PPA is eligiblefor ITC.

n deductible as regular businessexpenses only—not deductibleunder 37(1)(a)

n Materials transformed in performingSR&ED

n deductible under 37(1)(a) (seeline 325)

n not deductible under 37(1)(a)

Other expenditures claimedseparately:

n materials consumed in performingSR&ED

n lease costs of SR&ED equipmentn expenditures for SR&ED directly

undertaken on your behalfn third-party payments

n eligible for ITCn deductible under 37(1)(a)

n eligible for ITCn deductible under 37(1)(a)

The proxy amount covers overhead expenditures such as:

n office suppliesn general purpose office equipmentn heat, water, electricity, and telephonesn support staff salaries or wagesn travel and trainingn property taxesn maintenance and upkeep of SR&ED premises, facilities or equipmentn any other eligible expenditures directly related to the prosecution of SR&ED that you would not have incurred if the

SR&ED had not occurred

You have to elect or choose a method for each taxation yearyou want to use it. You have to make your choice of amethod when you first file Form T661 for the year.Therefore, whether you elect to use the proxy method oryou choose the traditional method, your choice of a methodis irrevocable for the year.

If you are a member of a partnership that elects to use theproxy method to calculate the income from the partnership,the election is only valid if you made it on behalf of all themembers of the partnership and, as an authorized partner,you had the authority to act for the partnership.

9

The following chart gives the advantages and disadvantages of each method.

Method Advantages Disadvantages

Proxy method You get ITC on the prescribedamount (PPA) which is 65% ofdirectly engaged SR&ED salariesand wages in the salary base.

It is easier to determine the PPAonce you establish the salary base.You will establish the PPA in mostcases.

No need to track SR&ED overheadexpenditures.

The PPA may be less than theactual overhead expensesincurred.

You have to calculate the salarybase on which a 65% rate willapply.

You may have to calculate anoverall cap on the PPA.

You cannot include in the SR&EDexpenditure pool the expenditureswhich the PPA represents.

No expenditures nor any ITC onmaterials transformed

Traditional method You calculate ITC on the actualoverhead expenditures youincurred.

The actual overhead expendituresmay be greater than the PPA.

There is no salary base to calculateand no PPA to determine.

There is no overall cap tocalculate.

Overhead expenditures areadded to the SR&ED expenditurepool.

You have to demonstrate that theoverhead expenditures areincremental to the SR&ED.

Using this method could be acomplex and uncertain exercise,especially when SR&ED and otherwork are carried out in the samefacility (e.g. shop-floor SR&ED).

You have to specifically identifyand allocate which overheadexpenditures are for SR&ED work.

You have to explain how youdetermined the amount and youhave to provide support for thedetermination.

Your allocation of overhead mustbe reasonable.

Part 2 – Scientific or TechnologicalProject InformationWhen we use the term project, we are referring to a SR&EDproject. A SR&ED project includes only the work that fallswithin the definition of SR&ED contained in the Act. Abasic principle of SR&ED is that the work is a systematicinvestigation or search that is carried out in a field ofscience or technology by means of experiment or analysis.Furthermore, for the purposes of experimentaldevelopment, the work must be undertaken to achieve atechnological advancement for the company.

The work claimed must be structured as a SR&ED project.The project description must contain the objective orobjectives in scientific or technological terms stating clearlythe advance or advances to be sought for the company. Itshould be clear that the work performed on the SR&EDproject was directed towards the attempt to achieve thatscientific or technological advancement for the company.

Paragraph 2.11 of Information Circular 86-4R3 discusseshow the CCRA applies the three criteria of projecteligibility in the claimant’s business environment.

SR&ED projects generally fall into two categories: distinctand well-defined projects with a clear beginning and endand a set of well-defined specific scientific and/ortechnological objectives and uncertainties; and larger,long-term multi-year projects. The latter contains aninterrelated work that may include routine development,routine engineering, routine programming, design, etc. Thisinterrelated work is characterised by being an integral partof the larger project and commensurate with its needs.These activities will not necessarily qualify as stand-aloneindependent SR&ED projects but could qualify as supportwork by virtue of their contribution to the overall project.

Generally, a program dedicated to advancing a particulartechnology by experimentation will inherently be SR&ED.A program’s technological objectives are broader and,conceptually, the advancement sought is described at ahigher level than that of a project. At this time, claimantsare required to contact the CCRA prior to filing their workat the program level. In these situations, the issue iswhether the allocation of the work attributed to theprogram reflects the contribution to its objectives. It isimportant that claimants establish the relationship andcontribution of the work claimed as SR&ED to theprogram’s technological objectives. In addition, claimants

10

must be able to explain the process they use to differentiateSR&ED from non-eligible work. The CCRA will work withclaimants to establish how they are to proceed.

The discussion that follows assumes that the claimant isfiling on a project basis.

Step 1 – Project summary informationProvide the information requested in Step 1 and Step 2 onseparate sheets of paper, and submit them with theT661 form.

Line 680Provide the total number of projects being claimed in thisfiscal year.

Line 206 – Industrial Research Assistance Program(IRAP) – The National Research Council of Canada offerstechnical and financial assistance through its IRAP to smalland medium-sized Canadian companies (up to500 employees) that already have technological capabilitiesand wish to strengthen and enhance them. Indicate theamount of assistance, if any, received by the corporationfrom IRAP for the project(s) claimed in the year.

Table of projects claimedProject identification: code and name – Please list all theSR&ED projects claimed. The internal reference code is thecode used to track the project and its costs. If you do notuse a code to track the projects and costs, then give anequivalent identifier. The project name is the internal nameor title you have given the claimed project.

NoteIf you do not have an established system of projectcoding, please number them in sequence and use thesenumbers throughout your claim.

Start date – The date when you started work on the SR&EDproject.

Finish date – The date when the SR&ED project’s initialscientific or technological objectives were achieved. If theproject is not finished in this taxation year, give theexpected finish date.

Total labour expenditures – This may be an actual amountor a reasonable cost allocation and relates to the amountreported on line 300 to 310.

Other information such as the names of the qualifiedpersonnel and the amounts of material and capitalexpenditures must be maintained and provided uponrequest.

Step 2 – Detailed project descriptionThe specific project information essential to yoursubmission is made up of five questions. The answers tothese questions should provide the appropriate technicalinformation we need to do an initial review of the claim.We recommend that personnel who are familiar with thetechnical content of the work you are claiming prepare thispart of the submission. Your answers should concentrate onthe relevant technical facts, that illustrate the experimentalnature of the work. Most project information can beprovided in four pages or less.

Please note that you must provide the informationrequested in the five questions (A to E) for every projectlisted in Step 1 of Part 2 of the T661 form. If your companyis not claiming by program and conducted more than20 projects during the course of your fiscal year, providedescriptions for the 20 largest projects with yoursubmission. You are required to provide descriptions forany of the remaining projects when we review your claim.

To the extent possible, if you used the Preclaim ProjectReview (PCPR) service, utilise the information prepared forthat purpose in submitting this claim.

If you continue projects from a previous year, simplyupdate the previous year’s submission and especially forquestion D, describe what work performed is being claimedthis year.

HintWhen providing this technical information, you mustensure that the relevant SR&ED project informationfocuses on the science or technology necessary for theattempt to achieve a scientific or technologicaladvancement for your company. If your work wasexperimental development to create new, or improveexisting, materials, devices, products or processes,describe how the work contributes to a scientific ortechnological advancement for your company ratherthan simply describing the development of a newproduct or process. Explain how the new or improvedproduct or process represents a technologicaladvancement for the company.

Activities such as financing, marketing, customerdemonstration and consumer acceptance testing, qualitycontrol testing, patent search and registration, andpreparation of submission or documents for licensingagencies, certification agencies, or regulatory authorities arenot eligible.

A. Scientific or technological objectives – For eachproject, state the overall scientific or technologicalobjectives. The objectives must be scientific ortechnological, not financial or marketing goals. Thescientific or technological objectives put the workclaimed into the proper technical perspective of what itwill mean for your company. These objectives alsoprovide an indication of when the project is complete.The scientific or technological objectives you state mustbe specific and verifiable.

State the indicators or measures you will use todetermine if you meet the scientific or technologicalobjectives. If this project continues from a previous yearand has not changed in direction, simply restate thescientific or technological objectives. However, if youmade a change in direction, you must explain andclarify the new objectives.

B. Scientific or technological advancement – State thescientific or technological advancement you are seekingfor your company. Give the field of science ortechnology in which you expect to achieve the scientificor technological advancement. Indicate how this is anadvancement for your company.

11

With experimental development, the scientific ortechnological advancement can be manifested in newproducts, new features of existing products, processes,improvements to processes or the knowledge acquiredin the attempt to achieve these. Even if you triedsomething unsuccessfully, this can be an advancementin the sense that you gained new knowledge useful forguiding future work. Note that novelty, innovation,uniqueness, feature enhancement, or increasedfunctionality in the product or process alone does notindicate technological advancement.

C. Scientific or technological uncertainty – Scientific ortechnological uncertainty is whether or not a givenresult or objective can be achieved, and/or how toachieve it, is not known or cannot be determined on thebasis of generally available scientific or technologicalknowledge or experience. See meaning of “commonlyavailable sources of knowledge or experience in theglossary (p. 28) of Information Circular IC 86-4R3”. Theuncertainty must be of a scientific or technologicalnature. Scientific or technological uncertainty ariseswhen knowledge generally available to your companydoes not provide you the necessary information on howto achieve the technological advancement. Generally,achieving scientific or technological advancementwould require removing the element of scientific ortechnological uncertainty through a process ofsystematic investigation.

In describing the scientific or technological uncertaintyit is not enough to state, “it is technologically uncertainhow to achieve the technological advancement.” Youhave to explain why there exists a scientific ortechnological uncertainty. Therefore, you must supportyour statement of scientific or technological uncertaintywith an analysis and discussion of the relevantunderlying technological issues and problems.

D. Description of work in this taxation year – Eligibility isgenerally determined at the project level. For multi-yearprojects, when the work extends beyond one taxationyear, eligibility of the project work ceases when thespecific scientific or technological objectives are met.Therefore, it is important that you describe what workwas actually carried out in this taxation year. In thisdescription the focus should be on the pursuit of thescientific or technological advancement. It must alsoinclude the results you obtained and the conclusionsyou made. If the project continued from the previousyear, state both the work and the progress madetowards the scientific or technological advancementstated in Part B above. Work in each year can qualify asSR&ED if it supports eligible work done in a previousyear.

E. Supporting information – To substantiate that yourwork was carried out as described in Step 2 of Part 2,you must have evidence of the work done to supportyour claim. List the information that you could use tosubstantiate the work described in Step 2. Technicalrecords that were created at the time the work wasperformed provide the most ready form ofdocumentation. Examples are planning documents,documents describing project objectives, descriptions ofthe problems to be solved, contract work statements,

notes of discussions dealing with unexpected obstaclesencountered, minutes of the meetings, records of trials,observations, project notebooks, lab notebooks, testrecords, and quantitative measurement data. Even thenew products, hardware, prototypes, pictures ofprototypes, or a combination of any of these, newgenetic material, business records, employee activityrecords, etc., can serve to substantiate the work.Usually, the information produced over the course ofdoing the SR&ED will be sufficient. It should not benecessary to specifically prepare additional documentsto substantiate the work claimed.

Part 3 – Summary of SR&EDExpendituresWe have divided Part 3 of this form into three steps. Youmust round all amounts you report in this part to thenearest dollar.

Step 1Allowable SR&ED expendituresfor SR&ED carried on in Canada (lines 300to 400)Usually, SR&ED current expenditures are those that do notresult in the acquisition of land, a leasehold interest in land,or property that would otherwise have been yourdepreciable property.

Current SR&ED expenditures involve three types ofexpenditures:

1. Cost for performing SR&ED: costs you incurred whenyou directly undertake the SR&ED (in-house SR&ED).These costs are basically wages, materials, andoverhead costs.

2. Cost for SR&ED on your behalf: costs associated withhaving SR&ED performed on your behalf (“contractpayments”).

3. Third-party payments: payments to certain thirdparties, such as approved associations or approvedinstitutions (“third-party payments”) to be used forSR&ED undertaken by these third parties. See line 370for more details.

Lines 300 to 315On lines 300 and 305, include in your pool of deductibleSR&ED expenditures the portion of salaries or wages andtaxable benefits you incurred for your employees who aredirectly engaged in SR&ED in Canada, which canreasonably be considered to relate to the time they spent inthe prosecution of SR&ED in Canada.

Determine the SR&ED portion of the employee’s salaryaccording to the time that person spends on SR&ED work.Employees directly engaged all or substantially all of theirtime (at least 90% of the time) in SR&ED will be consideredto spend all of their time in SR&ED.

12

ExampleIf you incur $100,000 in wages for an employee who spent90% of his or her time directly engaged in SR&ED, then$100,000 is considered to be directly engaged wages for thatemployee.

We explain below the meaning of salary or wages anddirectly engaged in SR&ED.

Separate the amount of salaries or wages for employeeswho are specified employees (see glossary) and those whoare not.

For a specified employee, do not include bonuses orremuneration based on profits in your pool of SR&EDexpenditures.

For SR&ED purposes, the maximum amount of salaries andwages per specified employee is limited to five times theyear’s maximum pensionable earnings (YMPE) determinedfor purposes of the Canada Pension Plan. The YMPE are$38,300 for year 2001 and $37,600 for year 2000. Therefore,the maximum amount of salaries and wages per specifiedemployee that you can include on line 305 is $191,500 for ataxation year that ends in year 2001 and $188,000 for ataxation year that ends in year 2000. The maximum amountis prorated by the number of days in the taxation year inwhich the employee is a specified employee. If a specifiedemployee is also performing SR&ED for an associatedcorporation, the maximum amount must be allocatedbetween the associated corporations using Form T1174,Agreement Among Associated Corporations to Allocate Salariesor Wages of Specified Employees for Scientific Research andExperimental Development (SR&ED) Expenditures.

Unpaid salaries, wages, and other remunerationSubsection 78(4) generally applies to accrued salaries,wages, and other remuneration that you still have not paid180 days after the end of the year in which you incurred theexpense. It deems the expense not to have been incurred inthe year, but rather in the year the amount is paid.

Enter unpaid subsection 78(4) amounts on line 315 ofForm T661, even though the expense is not deductible forthe year. Make sure you do not include the amount enteredon line 315 to line 300 or 305. Later, in a following taxationyear, if you satisfy the reporting requirement, you candeduct such an expense on line 310 of Form T661 for thetaxation year in which you actually paid the expense.

Definition of “salary or wages”“Salary or wages” as defined in subsection 248(1) is incomefrom an office or employment as calculated in sections 5 to8 of the Act. Therefore, salary or wages of an employeeincludes such amounts as vacation pay, statutory holidaypay, sick leave pay, as well as a taxable benefit to theemployee under section 6. Since you have to incur theexpenditure to claim it as SR&ED, do not include benefitsfor which you have not incurred an expenditure such asbenefits under subsection 6(9) for interest-free loans.

Do not include as salary or wages an expenditure forrelated benefits. Related benefits include the employer’sshare of payments to the Canada Pension Plan (CPP) orQuebec Pension Plan (QPP), Employment Insurance (EI),

Worker’s Compensation Board (WCB) or the Commissionquébécoise de la santé et de la sécurité au travail (CSST), anapproved employee pension plan, and employee medical,dental, or optical insurance plans.

You may be able to deduct related benefits on line 360 ifyou use the traditional method.

Do not include as salary or wages an expenditure forextended vacation or extended sick leave of an employee.We consider extended leave to be leave in excess of theusual annual leave an employee earns.

Directly engaged in SR&EDWhether an employee is directly engaged in SR&ED is aquestion of fact based on the duties the employee performsand not on the employee’s job title.

We consider the time employees, including supervisors andmanagers, spend to carry out the following tasks as timeduring which the employee is directly engaged in SR&ED:

n preparing equipment and materials for experiments,tests, and analyses, but not for maintaining equipment;

n experimenting, testing, and analyzing;

n collecting data for experimentation and analysis; and

n directing the course of the ongoing SR&ED work beingclaimed in the year.

We consider time other employees spend to carry out thefollowing tasks, to the extent that the tasks are required aspart of an SR&ED project, to be time during which theemployee is directly engaged in SR&ED:

n recording measurements, making calculations, andpreparing charts and graphs;

n conducting statistical surveys and interviews;

n preparing computer programs; and

n working in the areas of engineering or design, operationsresearch, mathematical analysis, computer programming,data collection, testing or psychological research.

We do not consider employees providing a service toSR&ED staff, including clerks, secretaries, and receptionistsengaged in activities in such areas as accounting, payroll,finance, legal, purchasing, sales, human resources,shipping, inventory control, maintenance, and wordprocessing, to be directly engaged in SR&ED.

We consider the time supervisors or managers are directlyinvolved in the technical aspects of the ongoing SR&EDwork as time spent directly engaged in SR&ED.

We do not consider the time managers and supervisorsspend on the non-technological management aspect ofwork, such as long-term strategic planning, contractadministration, and other decision-making functions thatdo not directly influence the ongoing SR&ED work, to betime during which they are directly engaged in SR&ED.

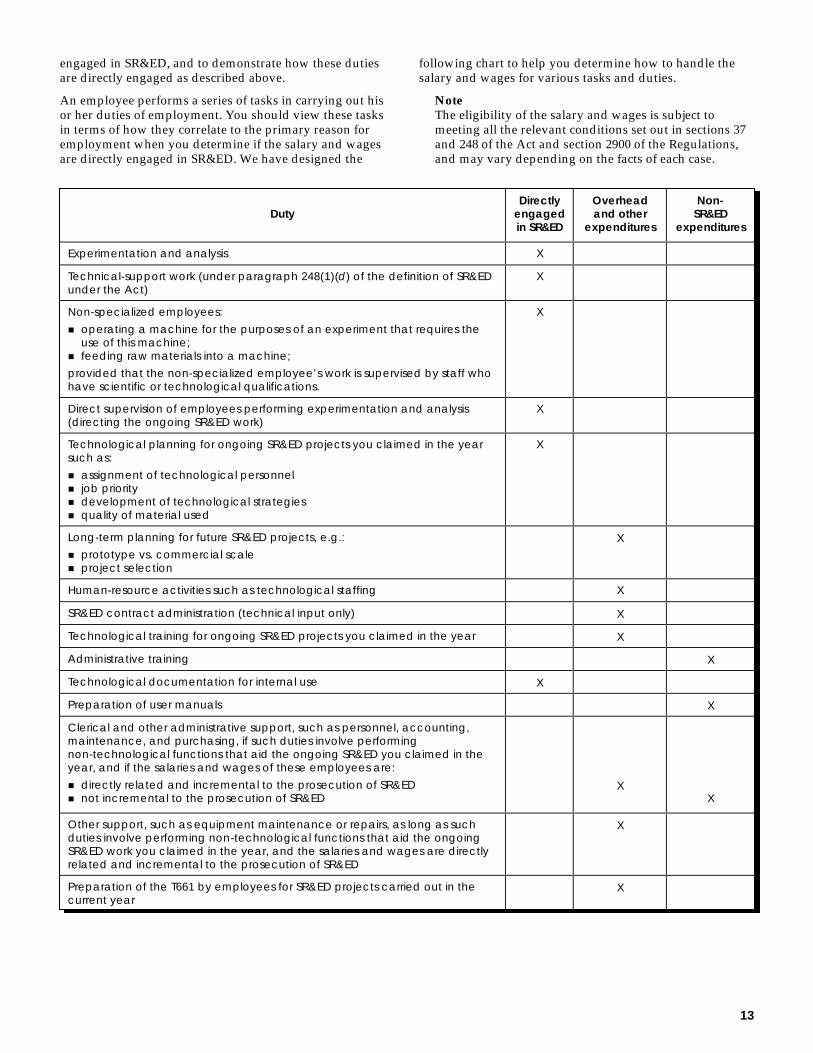

Usually, we do not consider work performed beyond thefirst-line supervision level as directly engaged. If you claimtime for employees beyond the first-line supervision level,you will be asked to provide details of the duties theemployee performed in the time claimed as directly

13

engaged in SR&ED, and to demonstrate how these dutiesare directly engaged as described above.

An employee performs a series of tasks in carrying out hisor her duties of employment. You should view these tasksin terms of how they correlate to the primary reason foremployment when you determine if the salary and wagesare directly engaged in SR&ED. We have designed the

following chart to help you determine how to handle thesalary and wages for various tasks and duties.

NoteThe eligibility of the salary and wages is subject tomeeting all the relevant conditions set out in sections 37and 248 of the Act and section 2900 of the Regulations,and may vary depending on the facts of each case.

DutyDirectly

engagedin SR&ED

Overheadand other

expenditures

Non-SR&ED

expenditures

Experimentation and analysis X

Technical-support work (under paragraph 248(1)(d) of the definition of SR&EDunder the Act)

X

Non-specialized employees:

n operating a machine for the purposes of an experiment that requires theuse of this machine;

n feeding raw materials into a machine;

provided that the non-specialized employee’s work is supervised by staff whohave scientific or technological qualifications.

X

Direct supervision of employees performing experimentation and analysis(directing the ongoing SR&ED work)

X

Technological planning for ongoing SR&ED projects you claimed in the yearsuch as:

n assignment of technological personneln job priorityn development of technological strategiesn quality of material used

X

Long-term planning for future SR&ED projects, e.g.:

n prototype vs. commercial scalen project selection

X

Human-resource activities such as technological staffing X

SR&ED contract administration (technical input only) X

Technological training for ongoing SR&ED projects you claimed in the year X

Administrative training X

Technological documentation for internal use X

Preparation of user manuals X

Clerical and other administrative support, such as personnel, accounting,maintenance, and purchasing, if such duties involve performingnon-technological functions that aid the ongoing SR&ED you claimed in theyear, and if the salaries and wages of these employees are:

n directly related and incremental to the prosecution of SR&EDn not incremental to the prosecution of SR&ED

XX

Other support, such as equipment maintenance or repairs, as long as suchduties involve performing non-technological functions that aid the ongoingSR&ED work you claimed in the year, and the salaries and wages are directlyrelated and incremental to the prosecution of SR&ED

X

Preparation of the T661 by employees for SR&ED projects carried out in thecurrent year

X

14

Supporting documentsYou must be able to explain how you determined theamount you claimed and to provide supportingdocumentation (e.g., time sheets, T4 slips, job descriptions).For salary and wages, this involves identifying the time youallocated to SR&ED and the work the employee performedduring that time. Keep in mind that the amounts youallocate to SR&ED must be reasonable.

Line 320Enter the cost of materials consumed in the prosecutionof SR&ED. If you incur a liability for materials that you willuse later for SR&ED, we consider the cost of these materialsto be an SR&ED expenditure in that later year in which youwill consume the materials. Be sure all costs are the netlaid-down price after you deduct trade discounts and addacquisition costs (e.g., transportation costs). Refer toApplication Policy SR&ED 2000-01 – Cost of materials forSR&ED, issued March 1, 2000.

The phrase “materials consumed in the prosecution ofSR&ED” basically means that you destroyed the materialsor rendered them virtually valueless as a result of theSR&ED. For example, in the following situations, not allmaterials were consumed in the prosecution of SR&ED (seeline 325):

n developing assets to sell (custom products);

n developing assets to use in the commercial operations ofthe performer (commercial assets); and

n sale of experimental production.

Line 325 – Cost of materials transformed into anotherproductIf you use the traditional method, you can claim the costs ofmaterials transformed into another product, if theexpenditure is all or substantially all or directly attributableto the SR&ED. The costs of materials transformed into aproduct is considered directly attributable to theprosecution of SR&ED if the materials are transformed inthe prosecution of eligible SR&ED work. There will be anITC recapture as an addition to your tax payable underPart I when you sell the property or convert it tocommercial use after February 23, 1998.

Lines 340 and 345Enter expenditures you incurred for contractors orsubcontractors carrying on SR&ED on your behalf(i.e., other parties performing SR&ED services directly foryou). See the explanation for line 370 if you need detailsabout the difference between third-party payments forSR&ED and SR&ED undertaken on your behalf.

It is important that you separate the SR&ED contractexpenditures between arm’s length contractors andnon-arm’s length contractors. Expenditures you incur forSR&ED performed on your behalf by a person orpartnership (the performer) at a time when you and theperformer do not deal with each other at arm’s length arenot qualified expenditures for ITC purposes. In addition,the amount received or receivable by the performer will notbe considered to be a contract payment. For more details,see the explanations for lines 526 (expenditures fornon-arm’s length SR&ED contracts), 534 (contract

payments), and 508 and 510 (transfer of qualified SR&EDexpenditures between non-arm’s length parties).

SR&ED performed on behalf of a personThe key element for determining an amount as a contractpayment is whether the payer requested the contractor toperform SR&ED on behalf of the payer under the contractterms. You can only make this determination based on theterms of the contract read as a whole, and by reviewing allthe facts surrounding the particular situation.

Meaning of “arm’s length”The current version of Interpretation Bulletin IT-419,Meaning of Arm’s Length, expresses in general terms thecriteria we consider when determining whether or notpersons deal with each other at arm’s length.

NoteWhen an expenditure relates to a contract for services tobe performed after the year-end, the amount for thoseservices does not qualify as an SR&ED expenditure untilthe year in which the services are actually performed.

Line 350 – Lease costs of equipment: allowable SR&EDexpendituresOn line 350, enter a lease expense that was all orsubstantially all (90%) attributable to the use of equipmentfor the prosecution of SR&ED in Canada. If you use theproxy method, do not include expenditures for generalpurpose office equipment or furniture (see glossary).

We consider a current expenditure for the lease ofequipment to be all or substantially all attributable to theuse of equipment for the prosecution of SR&ED if you usedit 90% or more for SR&ED. You must determine the SR&EDusage as a percentage of the total operating time. Generally,operating time means the time the equipment usually runsor functions.

Lease costs of building: not an allowable SR&EDexpenditureA building lease expense you incur does not qualifyfor SR&ED. A lease expense for a building is any outlay orexpense you made or incurred to use a building, or to havethe right to use a building.

OtherIn certain cases, a lease expense that was all or substantiallyall attributable to using premises or facilities other than abuilding may be allowable. For example, the lease expensefor a structure may be allowable.

Line 355On line 355, if you use the proxy method, enter 50% of thelease costs of equipment other than general purpose officeequipment or furniture, which is primarily used (morethan 50%, but less than 90%) for SR&ED.

You should determine the SR&ED usage as a percentage ofthe total operating time. Generally, operating time meansthe time the equipment usually runs or functions.

15

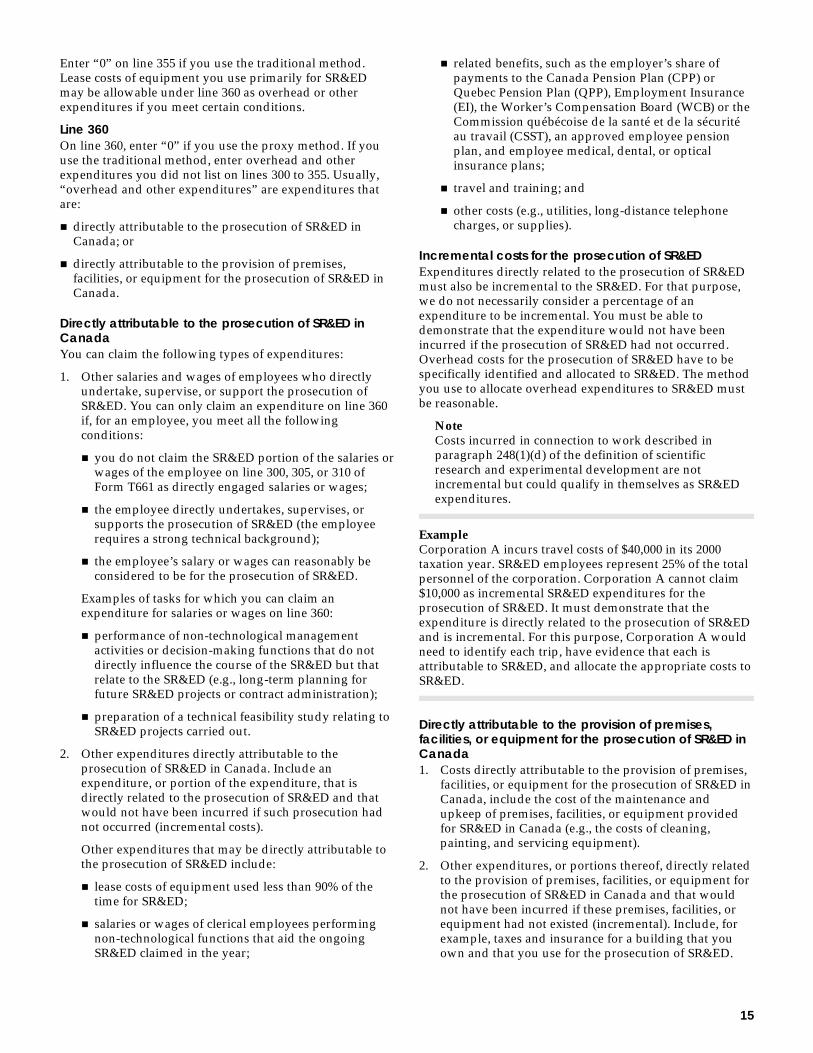

Enter “0” on line 355 if you use the traditional method.Lease costs of equipment you use primarily for SR&EDmay be allowable under line 360 as overhead or otherexpenditures if you meet certain conditions.

Line 360On line 360, enter “0” if you use the proxy method. If youuse the traditional method, enter overhead and otherexpenditures you did not list on lines 300 to 355. Usually,“overhead and other expenditures” are expenditures thatare:

n directly attributable to the prosecution of SR&ED inCanada; or

n directly attributable to the provision of premises,facilities, or equipment for the prosecution of SR&ED inCanada.

Directly attributable to the prosecution of SR&ED inCanadaYou can claim the following types of expenditures:

1. Other salaries and wages of employees who directlyundertake, supervise, or support the prosecution ofSR&ED. You can only claim an expenditure on line 360if, for an employee, you meet all the followingconditions:

n you do not claim the SR&ED portion of the salaries orwages of the employee on line 300, 305, or 310 ofForm T661 as directly engaged salaries or wages;

n the employee directly undertakes, supervises, orsupports the prosecution of SR&ED (the employeerequires a strong technical background);

n the employee’s salary or wages can reasonably beconsidered to be for the prosecution of SR&ED.

Examples of tasks for which you can claim anexpenditure for salaries or wages on line 360:

n performance of non-technological managementactivities or decision-making functions that do notdirectly influence the course of the SR&ED but thatrelate to the SR&ED (e.g., long-term planning forfuture SR&ED projects or contract administration);

n preparation of a technical feasibility study relating toSR&ED projects carried out.

2. Other expenditures directly attributable to theprosecution of SR&ED in Canada. Include anexpenditure, or portion of the expenditure, that isdirectly related to the prosecution of SR&ED and thatwould not have been incurred if such prosecution hadnot occurred (incremental costs).

Other expenditures that may be directly attributable tothe prosecution of SR&ED include:

n lease costs of equipment used less than 90% of thetime for SR&ED;

n salaries or wages of clerical employees performingnon-technological functions that aid the ongoingSR&ED claimed in the year;

n related benefits, such as the employer’s share ofpayments to the Canada Pension Plan (CPP) orQuebec Pension Plan (QPP), Employment Insurance(EI), the Worker’s Compensation Board (WCB) or theCommission québécoise de la santé et de la sécuritéau travail (CSST), an approved employee pensionplan, and employee medical, dental, or opticalinsurance plans;

n travel and training; and

n other costs (e.g., utilities, long-distance telephonecharges, or supplies).

Incremental costs for the prosecution of SR&EDExpenditures directly related to the prosecution of SR&EDmust also be incremental to the SR&ED. For that purpose,we do not necessarily consider a percentage of anexpenditure to be incremental. You must be able todemonstrate that the expenditure would not have beenincurred if the prosecution of SR&ED had not occurred.Overhead costs for the prosecution of SR&ED have to bespecifically identified and allocated to SR&ED. The methodyou use to allocate overhead expenditures to SR&ED mustbe reasonable.

NoteCosts incurred in connection to work described inparagraph 248(1)(d) of the definition of scientificresearch and experimental development are notincremental but could qualify in themselves as SR&EDexpenditures.

ExampleCorporation A incurs travel costs of $40,000 in its 2000taxation year. SR&ED employees represent 25% of the totalpersonnel of the corporation. Corporation A cannot claim$10,000 as incremental SR&ED expenditures for theprosecution of SR&ED. It must demonstrate that theexpenditure is directly related to the prosecution of SR&EDand is incremental. For this purpose, Corporation A wouldneed to identify each trip, have evidence that each isattributable to SR&ED, and allocate the appropriate costs toSR&ED.

Directly attributable to the provision of premises,facilities, or equipment for the prosecution of SR&ED inCanada1. Costs directly attributable to the provision of premises,

facilities, or equipment for the prosecution of SR&ED inCanada, include the cost of the maintenance andupkeep of premises, facilities, or equipment providedfor SR&ED in Canada (e.g., the costs of cleaning,painting, and servicing equipment).

2. Other expenditures, or portions thereof, directly relatedto the provision of premises, facilities, or equipment forthe prosecution of SR&ED in Canada and that wouldnot have been incurred if these premises, facilities, orequipment had not existed (incremental). Include, forexample, taxes and insurance for a building that youown and that you use for the prosecution of SR&ED.

16

Incremental costs for the provision of premises,facilities or equipmentThese other expenditures directly related to the provisionof premises, facilities, or equipment for the prosecution ofSR&ED in Canada must also be incremental to the SR&ED.For that purpose, we consider a reasonable percentage of anexpenditure to be incremental.

ExampleIf you own a building and use it for the prosecution ofSR&ED, we consider a reasonable portion of the municipaltaxes or the cost of insurance for the building to be directlyattributable to the provision of premises, facilities, orequipment for the prosecution of SR&ED.

The method you use to determine the portion that isdirectly related to the SR&ED has to be reasonable. You canbase it, for example, on the square meters of the buildingyou used for SR&ED over the total square meters of thebuilding. You can use other methods to determine theportion of an expenditure that is directly related to theprovision of premises, facilities, or equipment for theprosecution of SR&ED, as long as they are reasonable in thecircumstances. In all cases, whichever method you use, youhave to be able to provide support that it is reasonable.

On line 360, do not include capital cost allowance, generaladministrative expenses, or factory overhead expenses thatyou would have incurred if you had not conducted theSR&ED.

Supporting documentsYou have to identify each overhead expenditure specificallyand allocate a reasonable amount to SR&ED. At the time ofthe financial review, you may be asked to explain how youdetermined the amount, provide support for thisdetermination, and be able to demonstrate that theoverhead expenditures are incremental to the SR&ED.

Line 370On line 370, include third-party payments you made to thefollowing organizations if the payments are to be used forSR&ED carried on in Canada that is related to yourbusiness, and only if you are entitled to exploit the resultsof the SR&ED:

a) approved associations that undertake SR&ED;

b) an approved university, college, research institute, orother similar institution;

c) non-profit SR&ED corporations resident in Canada andexempt from tax under paragraph 149(1)(j) of the Act;

d) an approved organisation (granting councils) thatmakes payments to an association, institution, orcorporation described in a) to c) above;

e) corporations resident in Canada provided the SR&EDwas performed.

NoteTo determine whether the Minister of National Revenuehas approved an institution or association, you mustcontact the organization in question.

The amounts you report on line 370 are usually referred toas third-party payments for SR&ED. They do not includepayments for SR&ED undertaken on your behalf which youreport on lines 340 or 345. For example, third-partypayments for SR&ED could include payments to participatein arrangements such as industry-wide SR&ED undertakenby SR&ED associations, non-profit SR&ED corporations, oruniversities. In such cases, the payer does not control theactual work performed.

The following chart shows the usual differences betweenthe two concepts:

SR&ED contracts or Third-party payments

Characteristics SR&ED contractsThird-partypayments

Control ofSR&ED

payer performer

Rights exclusive non-exclusive(generallypublished)

Number offunders

usually limited toone payer

multiple funders

Type of SR&ED commerciallyfocused

often basic orappliedresearch

Tax treatment accrual cash basis

You cannot include all payments to organizations such asSR&ED associations and universities as expenditures online 370, since you could contract with such organizationsto perform SR&ED on your behalf. For example, if youneed a particular type of expertise, you can contract withthese organizations to perform specific tasks for you. In thiscase, the work is performed on your behalf, and you shouldreport the expenditures on line 340 or 345.

For a corporation, include on line 370 any payments youmade to a non-profit SR&ED corporation resident inCanada for basic or applied research carried on in Canada.For more details on such payments, see the current versionof Interpretation Bulletin IT-151, Scientific Research andExperimental Development Expenditures.

The amount of your payment eligible for SR&ED may bereduced if the recipient uses the funds to acquire abuilding, a leasehold interest in a building, or to pay rentfor a building.

See instructions for Schedule A below.

Line 390Capital expenditures for SR&ED carried on in CanadaOn line 390, include in the pool of deductible SR&EDexpenditures under paragraph 37(1)(b) any capitalexpenditures for SR&ED carried on in Canada and relatedto a business of yours. Capital expenditures on SR&ED areonly those expenditures that result in the acquisition ofdepreciable property other than buildings and leaseholdinterest in buildings. Generally, only capital expendituresfor new equipment are allowable. You cannot includenon-depreciable assets in the pool. A list of capital itemsacquired in the year should be available for review.

17

ExampleA claimant acquires land, building, and equipment to beused all or substantially all for the prosecution of SR&ED.The expenditure pool will only be affected by theequipment expenditure, as land is a non-depreciable asset,and buildings are generally excluded (see below).

The only difference in determining capital expendituresunder the traditional method and the proxy method is thatyou cannot include general purpose office equipment orfurniture if you use the proxy method.

An SR&ED capital expenditure is an expenditure you madeto acquire property that would otherwise be depreciableproperty if, when you acquired it, you intended either to:

n use the property during all or substantially all (90% ormore) of its operating time in its expected useful life forthe prosecution of SR&ED in Canada; or

n consume all or substantially all of the value of theproperty in the prosecution of SR&ED in Canada.

You determine a property’s eligibility when you make theexpenditure. However, when determining eligibility, welook beyond the use of the property in the year you makethe expenditure, to the intended use over the life of theasset.

We cannot consider you as having made a capitalexpenditure until the property you acquired as a result ofthe expenditure becomes available for your use.

NoteIf you are allowed an SR&ED deduction for thedepreciable property, you cannot also claim capital costallowance on the same property.

When you sell the SR&ED property, the tax treatment ofthe proceeds may vary. What you do depends on whetheror not you have previously claimed a deduction for theproperty. For more details, see the explanation for line 440.

ITC recaptureThere will be an addition to your tax payable under Part Iwhen you sell an ASA equipment or convert it tocommercial use after February 23, 1998. For more details,see Application Policy SR&ED 2000-04 – Recapture ofInvestment Tax Credit, issued December 7, 2000.

Buildings and landExpenditures you incurred to acquire buildings andleasehold interests in buildings (other than prescribedspecial-purpose buildings) do not qualify as SR&EDexpenditures. In addition, expenditures to acquire land andleasehold interests in land are also excluded.

Prescribed special-purpose buildings are defined insection 2903 of the Regulations. They are buildings theDepartment of Finance Canada approves on abuilding-by-building basis.

Line 400Allowable SR&ED expenditures are the total current andcapital expenditures you made in the year. On line 400,enter the total of the amounts on lines 380 and 390.

Step 2Pool of deductible SR&ED expenditures(lines 430 to 470)In this section, starting with the amount of allowableexpenditures for SR&ED carried on in Canada determinedon line 400, you will calculate the SR&ED expenditure pooldeduction that is available in the year, the deductionclaimed in the year, and any balance of the SR&EDexpenditure pool deduction you can deduct in future years.

Line 430Assistance refers to both government and non-governmentassistance for SR&ED. Government assistance includesforgivable loans, grants, subsidies, deductions from tax,investment allowances, or any other form of assistance,excluding the federal ITC. It also includes assistance forSR&ED from a provincial government, a municipality, or apublic authority. This includes provincial SR&ED taxcredits when they apply. Non-government assistanceincludes inducements and assistance you obtained fromother persons that you do not include in your taxableincome because of some other provision (e.g., the generalprovisions of section 9).

Certain provinces have introduced “super-deductions”which allow corporations to deduct over 100% of SR&EDexpenditure costs for provincial tax purposes. Even thoughthese deductions provide for a similar level of provincialassistance, as compared to provincial ITCs, they were notconsidered to be government assistance and did not reducethe expenditures for federal ITC purposes.

For taxation years commencing after February 2000, thebudget proposes to treat a specified percentage ofprovincial deductions for SR&ED in excess of the actualamount of the expenditure as government assistance. Thespecified percentage is based on the provincial tax ratesapplicable to income earned in the province by acorporation for the year and is:

n the maximum provincial tax rate applicable to activebusiness income, where the corporation’s federal ITCexpenditure limit (relevant for the purposes of theenhanced ITC rate of 35%) for the year is nil;

n the provincial tax rate applicable to small businessincome, in any other case;

The amount calculated will be added to the corporation’sPart I tax payable in the year. For more details, refer toApplication Policy SR& ED 2000-03 – Government Assistance– Treatment of Provincial and Territorial R&D Assistance,issued October 31, 2000).

Assistance amounts will reduce the pool of deductibleSR&ED expenditures if, at the filing-due date of your taxreturn for the taxation year, you have received, are entitledto receive, or can reasonably expect to receive the amounts.

If you are using the proxy method, do not deduct theassistance for expenditures that the prescribed proxyamount replaces.

18

Line 435An ITC for SR&ED expenditures that you claimed in theyear (including ITC refunds, an ITC you carried back toprevious years, an ITC on the prescribed proxy amount, anITC on qualified SR&ED expenditures transferred to youfrom a non-arm’s length performer underparagraph 127(13)(e), but not an ITC on shared-usedequipment) does not reduce your pool of deductibleSR&ED expenditures for the current year. Rather, it will bededucted from the pool of deductible SR&ED expendituresin the next year.

To the extent that an ITC deducted or refunded mayreasonably be considered to relate to a property acquired ina preceding year as shared-use equipment, it will reducethe capital cost of the property acquired.

For partnerships, you have to reduce the balance in the poolof deductible SR&ED expenditures by the amount of ITC inthe same year the partnership makes the related SR&EDexpenditures.

Line 440If you sold an SR&ED asset (capital equipment youpurchased for SR&ED) during the year, and the line 450amount includes unclaimed expenditures for the asset,include on line 440 the sale proceeds or the amount ofunclaimed expenditures for the asset, whichever amount isless.

If the sale proceeds are more than the unclaimed balance ofSR&ED expenditure for the asset, include the difference inyour income up to the amount of recapture of capital costallowance (CCA). If the sale proceeds are more than theoriginal cost of the asset, the difference is either a capitalgain or income, depending on the facts of each case.

ExampleFacts (1) Unclaimed SR&ED expenditures

balance carried forward from theprevious year (line 450) ......................... $ 500

(2) Asset you sold during the year:Original cost............................................ $1,000Proceeds of disposition ......................... $ 100Unclaimed expenditures for the assetthat are included in the line 450amount..................................................... $ 50

Solution (1) Determine the line 440 amount,whichever amount is less: theproceeds of disposition ......................... $ 100

orthe amount of unclaimedexpenditures for the asset ..................... $ 50The line 440 amount............................... $ 50

(2) Determine the recaptured CCA,whichever amount is less: cost ............. $1,000

orproceeds of disposition ......................... $ 100

$ 100Minus the reduction to the line 440amount..................................................... $ 50Recapture of CCA (include thisamount in your income for the year)... $ 50

NoteIn certain cases, other deductions may be required to bemade to the SR&ED expenditure pool (e.g., expendituresa corporation renounced for the purposes of Part VIIItax, and amounts deducted under section 61.3).

Line 445If an amount of assistance has reduced your balance in thepool of deductible SR&ED expenditures (see line 430), addany repayments of that assistance to the pool on line 445. Inaddition, if an amount of assistance receivable has reducedyour expenditure pool balance and you did not receive itand it ceased to be an amount you can reasonably expect toreceive, the amount is considered to be a repayment ofassistance that you can add to the pool on line 445.

Line 450Enter the unclaimed balance in the pool of deductibleSR&ED expenditures you are carrying forward from theprevious year. For a partnership, enter “0” on line 450.

Line 452For information on amalgamation and winding-up and theimpact on the pool of deductible SR&ED expenditures readInterpretation Bulletin IT-151, Scientific Research andExperimental Development Expenditures.

Line 453 – Recapture of ITCAny ITC recaptured under new subsections 127(27), (29),(30) or (34) for the previous taxation year, will increase theamount of the taxpayer’s subsection 37(1) SR&ED pool forthe current year.

Generally, the circumstances which will cause the reductionin a taxpayer’s SR&ED ITCs are disposition or conversionto commercial use of a property (after February 23, 1998),where the cost of that property was previously claimed asan SR&ED cost for SR&ED ITC purposes. Refer toApplication Policy SR&ED 2000-04 for more information onITC recapture.

Line 454If the amount on line 454 is positive, enter that amount online 455. If the amount on line 454 is negative, enter “0” onlines 455, 460, and 470, and include the line 454 amount inyour income for the year.

Line 460Enter the deduction you claim in the year from the pool ofdeductible SR&ED expenditures. You can deduct all or aportion of your expenditures for SR&ED carried on inCanada in the year you make the expenditures, or you canaccumulate them and carry them forward to deduct infuture years. The deduction is optional, and can be anyamount up to the current year’s line 455 amount, subject tothe following restrictions:

n If the claimant is a corporation and an acquisition ofcontrol has previously occurred, the total amount online 455 may not be available for deduction in the year orin a later year. You have to use special rules to determinethe amount you can deduct. Usually, these rules operatelike the non-capital loss restrictions in subsection 111(5)for an acquisition of control. For more details, see the

19

current version of Interpretation Bulletin IT-151, ScientificResearch and Experimental Development Expenditures.

n A partnership cannot carry forward SR&ED expendituresto a subsequent year.

Line 470This amount is your unclaimed balance in the pool ofdeductible SR&ED expenditures at the end of the year and,subject to the restrictions noted at line 460, you can deductit in future years. For a partnership, enter “0” on line 470.

Step 3Qualified SR&ED expenditures for ITCpurposes (lines 500 to 570)In this section, you will determine the SR&ED expendituresthat qualify for a federal ITC. Not all expendituresfor SR&ED carried on in Canada will earn an ITC. UseStep 3 to determine the base of SR&ED expenditures thatearn an ITC.

You should break down your expenditures between currentand capital expenditures. This will help you calculate yourrefundable ITC.

Line 500On line 500, enter unpaid amounts from previous years youpaid in the year and that are deemed to be an expenditureyou incurred in the year under subsection 127(26).

Under subsection 127(26), SR&ED current expenditures thatyou do not pay within 180 days of the end of the taxationyear in which you incurred them are deemed not to havebeen incurred in that year for ITC purposes but only at thetime you paid them. This applies to all unpaid amounts forSR&ED current expenditures except unpaid salaries, wages,or other remuneration under subsection 78(4). Seeexplanation for line 310.

On line 520, deduct unpaid amounts deemed not to be anexpenditure incurred in the year under subsection 127(26).

NoteEven if your unpaid subsection 127(26) amounts do notqualify for ITC until the time you paid them, they arestill allowable SR&ED expenditures deductible in theyear you otherwise incurred the expenditures. Makesure to include your unpaid subsection 127(26) amountsin your allowable SR&ED expenditures within theperiod allowed to file Form T661. Otherwise, they willnot be qualified expenditures in the year you pay them.

ExampleIn its 2000 taxation year ending on December 31, 2000,Corporation A incurs SR&ED expenditures of $100,000 forconsulting fees payable to Corporation B. Corporation Astill has not paid the expenditure 180 days after the end ofthe 2000 taxation year. The expenditure is only paid inNovember 2001.

n Corporation A must identify the expenditure in theSR&ED expenditure pool on Form T661 within thereporting deadline. It is an allowable SR&EDexpenditure deductible in 2000.

n Corporation A has to deduct the unpaid amount online 520 of Form T661 for the 2000 taxation year. For ITCpurposes, the expenditure is deemed not to have beenincurred in 2000.

n When Corporation A pays the expenditure in the 2001taxation year, enter the amount that is paid on line 500 ofForm T661 for that year.

Line 502 – Prescribed proxy amountEnter “0” on line 502 if you use the traditional method.

The prescribed proxy amount (PPA) for a taxation year is65% of the salary base. In certain situations, an overall capon the prescribed proxy amount may limit the amount youwould otherwise determine.

Use Table 1 below to help you calculate the PPA inaccordance with the Act.

Salary base – The salary base for the proxy method iscomprised of salaries and wages of employees who aredirectly engaged in SR&ED in Canada. The directlyengaged salaries and wages are those you entered online 300 of Form T661 for non-specified employees, andline 305 for specified employees. However, special rulesapply to restrict the amount of salaries or wages ofspecified employees that you can include in the salary base.

The salary base does not include taxable benefits undersections 6 and 7of the Act, bonuses, remuneration based onprofits, or an amount deemed incurred in the year undersubsection 78(4).

The following chart illustrates the differences between thesalaries or wages expenditure you include in the SR&EDexpenditure pool, and the salary base you use to calculatethe PPA:

Salaries or wagesexpenditure Salary base

Directly engaged salaries orwages other than taxablebenefits under sections 6and 7, bonuses,remuneration based onprofits, an amount deemedincurred undersubsection 78(4)

– for non-specifiedemployee

– for specified employee

Taxable benefits (section 6)incurred

Remuneration based onprofits, bonuses

Amount deemed incurredin the year undersubsection 78(4)

Related benefits(employer’s contributions tocertain plans)

yes (included online 300)

yes (on line 305)amount isrestricted *

yes (lines 300and 305)

yes fornon-specifiedemployees(line 300)

yes (line 310)

no (seeexplanations forlines 300 to 315)

yes

yes, amountis restricted**

no

no

no

no

* 5 x YMPE** 2.5 x YMPE

20

Section A of Table 1Enter the amount from line 300 to line 1 of Table 1. Thisamount is the total wages or salaries of personnel directlyengaged in SR&ED, for employees other than specifiedemployees.