Embed Size (px)

Citation preview

City of Douglas Downtown Revitalization Plan

Community Meeting

June 22, 2010

Agenda

1. Introductions 2. Project Information

1. Scope 2. Schedule

3. Work Accomplished To Date 1. Economic Study 2. Phelps Dodge Building Update 3. Community Research

4. Downtown Planning Collaboration 5. Pin Up

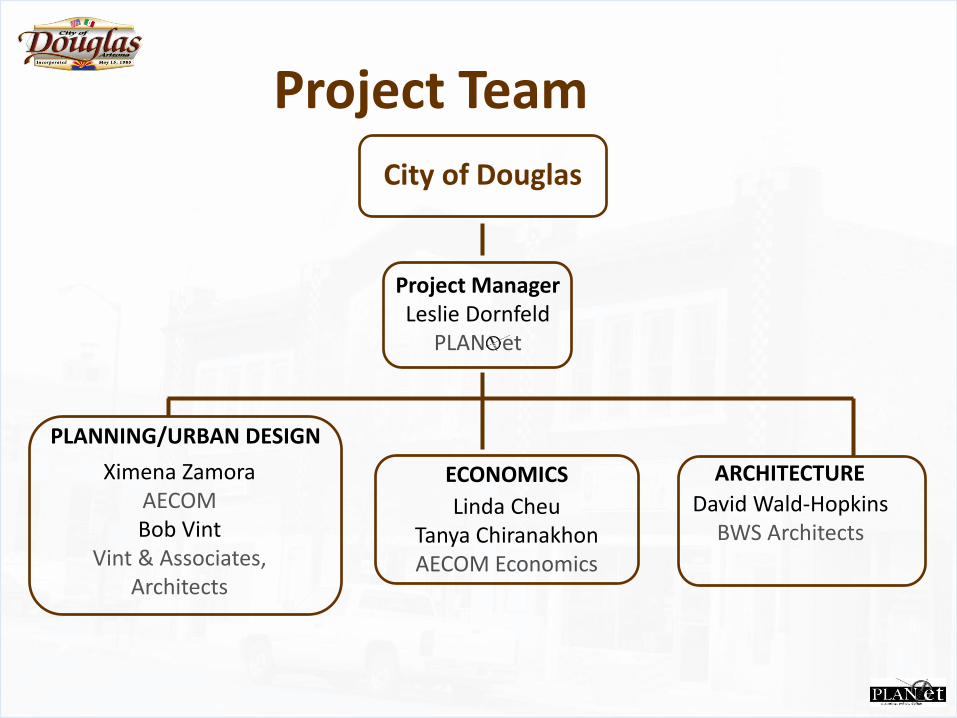

Project Team

City of Douglas

Ximena Zamora AECOM Bob Vint

Vint & Associates, Architects

Linda Cheu Tanya Chiranakhon AECOM Economics

ECONOMICS

PLANNING/URBAN DESIGN

Project Manager Leslie Dornfeld

PLAN et

David Wald-Hopkins BWS Architects

ARCHITECTURE

PROJECT SCOPE

Reconnaissance Economic Study Focus Groups (May 13, 2010) Research

Develop Concepts Public Workshop (June 22, 2010) Concept Development Meet with City Staff (Late Summer)

Refine Concept Community Meeting (Early Fall)

Finalize Concept City Council Meeting (Late 2010/Early 2011)

City of Douglas Downtown Redevelopment Plan Economic Study

Community Meeting June 22, 2010

I. Economic and Retail Trends

II. Relevant Findings from Stakeholder Interviews

III. SWOT Analysis

1. Strengths

2. Weaknesses

3. Opportunities

4. Threats

IV. Economic Development Strategies

I. Economic Trends

Cochise County Employment Growth, 2001-2010

1,475

600

6,250 5,625

4,425 3,800

2,450

12,475

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mining and Construction Manufacturing

Trade, Transportation, and Utilities Professional and Business Services

Educational and Health Services Leisure and Hospitality

Services2 Government

I. Economic Trends

Em

plo

ym

en

t

Source: State of Arizona, Department of Commerce, Research Administration

Cochise County Employment, 2010

Mining and Construction

4%

Manufacturing 2% Trade,

Transportation, and Utilities

17%

Professional and Business

Services 15%

Educational and Health Services

12%

Leisure and Hospitality

10%

Services2 6%

Government 34%

I. Economic Trends

Source: State of Arizona, Department of Commerce, Research Administration

Cochise County Population Growth, 2001-2009

The City of Douglas’ share of Cochise County’s population has ranged from 13.7% in

2001 to 12.7% in 2009.

I. Economic Trends

Po

pu

lati

on

38

,70

0

40

,40

0

40

,40

0

42

,70

0

43

,70

0

44

,90

0

44

,70

0

45

,90

0

46

,60

0

16,600 17,000 17,100 17,100 17,200 17,700 18,200 18,200 17,800

65

,50

0

66

,40

0

68

,10

0

69

,90

0

70

,90

0

72

,70

0

74

,30

0

75

,30

0

75

,90

0

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

Sierra Vista Douglas Remainder of Cochise County

120,800 123,800 125,600

129,700 131,800 135,300 137,200 139,400 140,300

Source: Arizona Department of Economic Security, Population Statistics Unit; Arizona Department of Commerce, 2009 Population

Estimates

City of Douglas Population Growth, 2001-2009

16

,60

0 1

6,9

90

17

,07

5

17

,08

0

17

,19

5 1

7,6

60

18

,15

2

18

,20

7

17

,75

8

15,500

16,000

16,500

17,000

17,500

18,000

18,500

2001 2002 2003 2004 2005 2006 2007 2008 2009

According to The Arizona Department of Corrections, these population figure includes

approximately 2,000 inmates at the Arizona State Prison Complex in Douglas. The

household population in 2009 is estimated to be approximately 15,760.

I. Economic Trends

Po

pu

lati

on

Douglas and Agua Prieta Population Comparison, 2001 and 2005

16,600 17,195

60,269

68,402

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2001 2005

Douglas Agua Prieta City

I. Economic Trends

The population figures shown above for Agua Prieta are sourced from INEGI, the Mexican

government’s National Institute of Statistics and Geography. Unofficial sources have cited

the population anywhere from 60,000 to 200,000. In either case, the population of Agua

Prieta is at least 4 times greater than that of Douglas.

Po

pu

lati

on

$501,000 $528,000 $513,400 $504,400

$150,800 $155,800 $156,900

$139,500

$132,700 $112,900 $104,800

$103,500

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

2006 2007 2008 2009

Sierra Vista Douglas Remainder of Cochise County

Cochise County, Douglas and Sierra Vista Retail Sales, 2006-2009 G

ros

s T

axa

ble

Re

tail

Sa

les

(Th

ou

sa

nd

s)

$784,500 $796,700

$775,100 $747,400

Gross taxable retail sales in Douglas roughly mirrored those of Cochise County from 2006 through

2009. Sales in Douglas consistently accounted for approximately 19% to 20% of the county’s.

I. Economic Trends

$5

,79

9

$5

,80

7

$5

,56

0

$5

,32

8

$1

1,1

59

$1

1,8

12

$1

1,1

85

$1

0,8

25

$9

,60

7

$9

,61

8

$9

,68

5

$8

,83

1

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2006 2007 2008 2009

Cochise County Sierra Vista Douglas

Cochise County, Douglas, Sierra Vista Per Capita Retail Sales P

er

Ca

pit

a R

eta

il S

ale

s

Per capita retail in Douglas are significantly higher than those of Cochise County and lower that than of

Sierra Vista. Because Douglas’ median household income is below the countywide median, these

figures indicate considerable retail sales to non-residents, including cross-border shoppers.

Per capita retail

sales in Douglas

that exceed the

countywide

average indicate

sales to Mexican

shoppers.

* In 2007 the median household income for Douglas was $25,597 compared to $40,656 for Cochise County.

Indicate possible

retail leakage to

Sierra Vista

I. Economic Trends

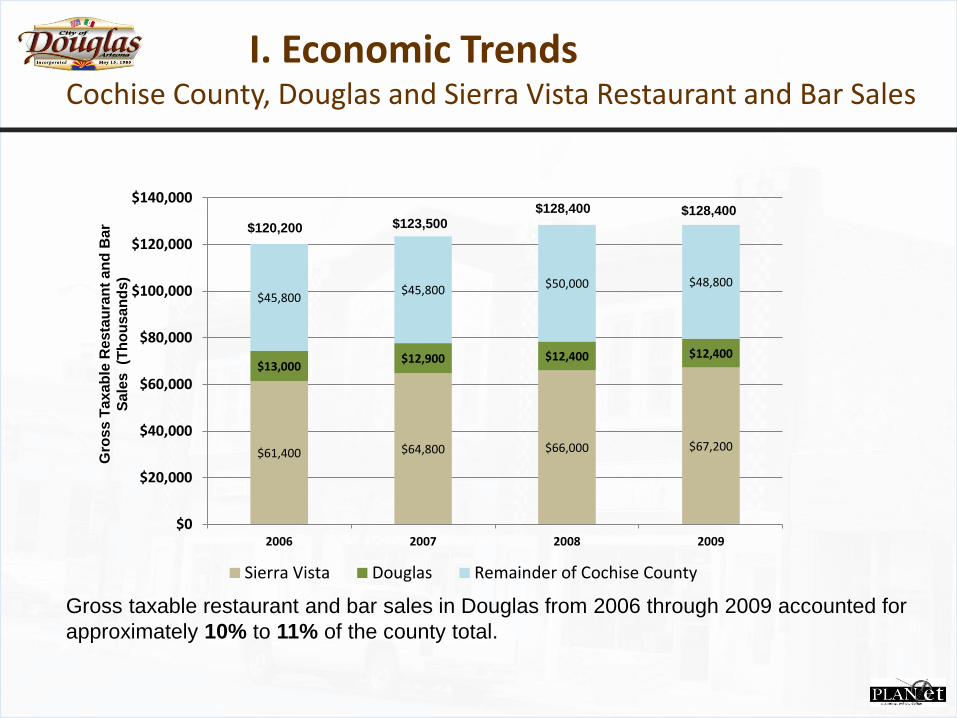

$61,400 $64,800 $66,000 $67,200

$13,000 $12,900 $12,400 $12,400

$45,800 $45,800 $50,000 $48,800

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

2006 2007 2008 2009

Sierra Vista Douglas Remainder of Cochise County

Cochise County, Douglas and Sierra Vista Restaurant and Bar Sales G

ros

s T

axa

ble

Re

sta

ura

nt

an

d B

ar

Sa

les

(T

ho

usa

nd

s)

$120,200 $123,500 $128,400 $128,400

Gross taxable restaurant and bar sales in Douglas from 2006 through 2009 accounted for

approximately 10% to 11% of the county total.

I. Economic Trends

$8

88

$9

00

$9

22

$9

15

$1

,36

7

$1

,45

0

$1

,43

9

$1

,44

1

$8

25

$7

98

$7

68

$7

88

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2006 2007 2008 2009

Cochise County Sierra Vista

Cochise County, Douglas, Sierra Vista Per Capita Restaurant Sales P

er

Ca

pit

a R

esta

ura

nt

an

d B

ar

Sa

les

Per capita restaurant and bar sales calculated using the household population in Douglas

are only half of Sierra Vista’s and lower than those of Cochise County. These figures

indicate considerable restaurant and bar sales leakage.

* In 2007 the median household income for Douglas was $25,597 compared to $40,656 for Cochise County.

Lower per capita

restaurant and bar

sales in Douglas

indicate

considerable

leakage.

I. Economic Trends

Douglas Resident Retail Out-Shopping

• Highest percentage of retail out-shopping by Douglas

residents:

1. 30.1% Computer hardware / software

2. 29.4% Books

3. 29.3% Furniture

• Weaknesses of Douglas retail stores:

1. Too few stores and lack of variety of retail goods

2. Prices in Douglas are too high

3. Poor customer service (language barrier?)

Source: 2006 survey conducted by Cochise College Center for Economic Research

I. Economic Trends

Douglas POE Cross Border Traffic from Mexico, 2009

Source: US Department of Transportation, Research and Innovative Technology Administration

1,190 999 1,391 1,432 1,019 972 1,561 1,338 962 1,155 525 1,028

385,590

344,964

367,920 366,441

389,196

366,650 388,155

261,387 248,864 250,339 249,847

273,977

112,294 110,984 113,719 112,332 112,346

86,160 103,612

114,402 104,837 101,391

111,531 131,137

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Bus Passengers Personal Vehicle Passengers Pedestrians

Pe

rso

n C

ros

sin

gs

I. Economic Trends

Economic Impact of Mexican Shoppers in Cochise County

• Direct Economic Impacts of Mexican visitor spending in

Cochise County from 2007-2008:

1. 1,498 jobs

2. Over $28 million in income from these jobs

3. $186 million in sales

Source: Mexican Visitors to Arizona: Visitor Characteristics and Economic Impacts 2007-2008

Reason for Visit % of Parties # of Parties

Leisure 89.9% 1,616,066

Health 0.4% 6,471

Vacation 0.7% 12,943

Friends / Relatives 8.2% 147,585

Shopping 79.2% 1,423,361

Other 1.4% 25,706

Business 10.1% 181,560

Health0.4%

Vacation0.7%

Friends / Relatives8.2%

Shopping79.2%

Other1.4%

Business10.1%

I. Economic Trends

Characteristics of Mexican Shoppers in Douglas

• Monthly HH income distribution of Mexican Shoppers in

Douglas

• Top 10 stores where Mexican visitors to Douglas shop

Shopping Centers / Stores % of Parties

Wal-Mart 54.3%

Safeway 33.2%

Factory 2-U 24.9%

Family Dollar 18.3%

Food City 16.8%

JC Penney 13.3%

Gas Station 12.6%

Dollar Tree 9.3%

Radio Shack 4.8%

Payless Shoes 3.0%

Under $929 $929-$1,393 $1,394-$1,859 $1,860-$2,787 $2,788-$3,716 $3,717-$4,646 $4,647-$7,434 $7,435 or Over

Douglas 45.7% 36.2% 13.0% 3.3% 0.9% 0.3% 0.3% 0.3%

Port of Entry

Income Range (US Dollars)

Source: Mexican Visitors to Arizona: Visitor Characteristics and Economic Impacts 2007-2008

* Average monthly household income for Mexico as a whole was $952 in 2005.

I. Economic Trends

II. Findings from Stakeholder Interviews

Key Findings II. Findings from Stakeholder Interviews

• Cross border traffic accounts for between 25% to 75% of client

base for Downtown businesses

• Downtown Douglas lacks variety in dining options – need nicer

restaurants, bars, cafes, ice cream shops

• Ideas for Downtown stores? Hobby shops, a sporting goods

store, card store, bookstore, and hair and nail salon

• Parking is a problem – inconveniently located and not enough

• Downtown should be more of a social hub - music events,

parades and street festivals would be big draws

• Need to improve the aesthetic of downtown storefronts and

streetscape with signage, coordinated color scheme, etc.

• Grand Theatre and YMCA are key buildings to renovate.

Gadsden Hotel could be further improved.

III. Strengths, Weaknesses, Opportunities and Threats

Strengths

III. SWOT Analysis

• Location across border from significant population

center in Agua Prieta

• Cross border visitors come specifically for shopping

• Historic downtown buildings with authentic character

• Long standing small, local businesses provide

unique commercial core

• Call center, hospital and expanded border patrol

provide stable employment opportunities

III. SWOT Analysis

• Relatively small local population, low income, and

low growth

• Large, spread out downtown area is not very

cohesive and lacks intimacy

• Existing vacancies contribute to lack of cohesion

• Douglas lacks marquee event, brand, or icon to

attract tourism

• Current tourism limited to cross border shoppers

• Downtown buildings in need of renovation and repair

• Restaurant and dining options are limited

• Parking challenges

Weaknesses

III. SWOT Analysis

• Three target market segments to capitalize on

• New PD building and government center could focus

spending downtown

• Key projects centered around one node – PD

building, Grand Theatre, Gadsden Hotel

• Gadsden Hotel and Grand Theatre should be

centerpieces of the tourism strategy

• Active community college with potential for

partnership

• Douglas history – there are authentic stories from

which to build tourism sector

• New, reenergized Chamber of Commerce with

downtown events, promotion activities, etc.

• Preliminary planning for development of economic

development corporation

Opportunities

III. SWOT Analysis

• Local competition from Walmart and surrounding

businesses

• Regional competition from Sierra Vista and retail

leakage

• Proposed bypass could further divert traffic

• Conservatism towards change by long standing

business owners

• Frustration with past planning efforts that were not

economics driven, “study fatigue”

• Perception of border safety issues

• Perception about new immigration law

Threats

IV. Economic Development Strategy

Three Target Market Segments IV. Economic Development Strategy

1. Douglas resident market

2. Cross-border visitor market

3. Tourism market

15

,90

0

16

,00

0

16

,20

0

16

,40

0

16

,60

0

16

,80

0

17

,10

0

17

,40

0

17

,70

0

18

,00

0

18

,30

0

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Douglas Household Population

Douglas Household Population

Douglas Household Population Projection, 2010-2020

Ho

us

eh

old

Po

pu

lati

on

Three Target Market Segments IV. Economic Development Strategy

3,2

00

3,2

00

3,3

00

3,3

00

3,4

00

3,5

00

3,5

00

3,6

00

3,7

00

3,7

00

3,8

00

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Non-US Citizen Person Crossings

Non-US Citizen Person Crossings

Non-US Citizen Border Crossings Projection, 2010-

2020

1. Douglas resident market

2. Cross-border visitor market

3. Tourism market N

on

-US

Cit

ize

n B

ord

er

Cro

ss

ing

s

(Th

ou

sa

nd

s)

Supportable Retail Space Based on Projected Growth

IV. Economic Development Strategy

Sources of Retail Demand:

1. Additional capture of existing cross-border spending

2. Growth of cross-border spending

3. Growth of Douglas residents and spending

4. Attract tourism already visiting Tombstone and Bisbee

IV. Economic Development Strategy 10 Year Retail and Restaurant Demand

• Demand for nearly 100,000 additional SF of restaurant and retail space

in downtown Douglas over the next 10 years.

• Approximately 40% to 50% of this space should be restaurants, bars

and food-related retail.

• 50% to 60% should be other types of retail, with 50% serving the cross

border market and 50% serving the local and tourist market.

• Should target one or two nationally known restaurant chains – may have

to provide incentives.

Current 2010-2015 2015-2020 TOTAL SF % of Total SF

10,000 3,500 4,600 18,100 20%

7,800 5,000 5,900 18,700 21%

29,800 10,500 13,900 54,200 60%

47,600 19,000 24,400 91,000 100%

Estimated Supportable Square Feet in Downtown Douglas

Supportable Downtown Retail Space Based on Projected Growth

IV. Economic Development Strategy

Additional Capture of Existing

Spending

2010 - 2015 2015 - 2020

Food Related Retail SF

10,000 21%

Restaurant and Bar SF7,800 16%

Other Retail SF29,800 63%

Food Related Retail SF

3,500 19%

Restaurant and Bar SF

5,000 26%

Other Retail SF10,500 55%

Food Related Retail SF

4,600 19%

Restaurant and Bar SF

5,900 24%

Other Retail SF13,900 57%

Tourism Strategy (mid- to long-term)

“Southwest Trail”

• Over 400,000 tourists

go to Tombstone

annually

• The Kartchner

Caverns in Benson

and Bisbee also

attract tourists

• Strategic positioning

for Douglas

Tombstone

Bisbee Douglas

IV. Economic Development Strategy

Tucson

Benson

Market Positioning / Branding

• Tombstone – Wild west image, OK Corral gunfight

• Bisbee – Unique landscape, cooler climate, arts and

culture

• Douglas

• History of Southwest from the Mexican perspective,

legends of Pancho Villa in Douglas

• Gateway to Mexico

• Carne Asada Capital of the World?

“

IV. Economic Development Strategy

Strategic Partnerships / Key Catalyst Projects

• PD Building

• Partnership with Cochise College - culinary, nursing,

computers and language programs

• Gadsden Hotel

• Grand Theatre

IV. Economic Development Strategy

Marketing and Events

• Regular events that bring people downtown

• Mexican music festival at the Grand Theatre

• Promote the cross border shuttle bus Parking

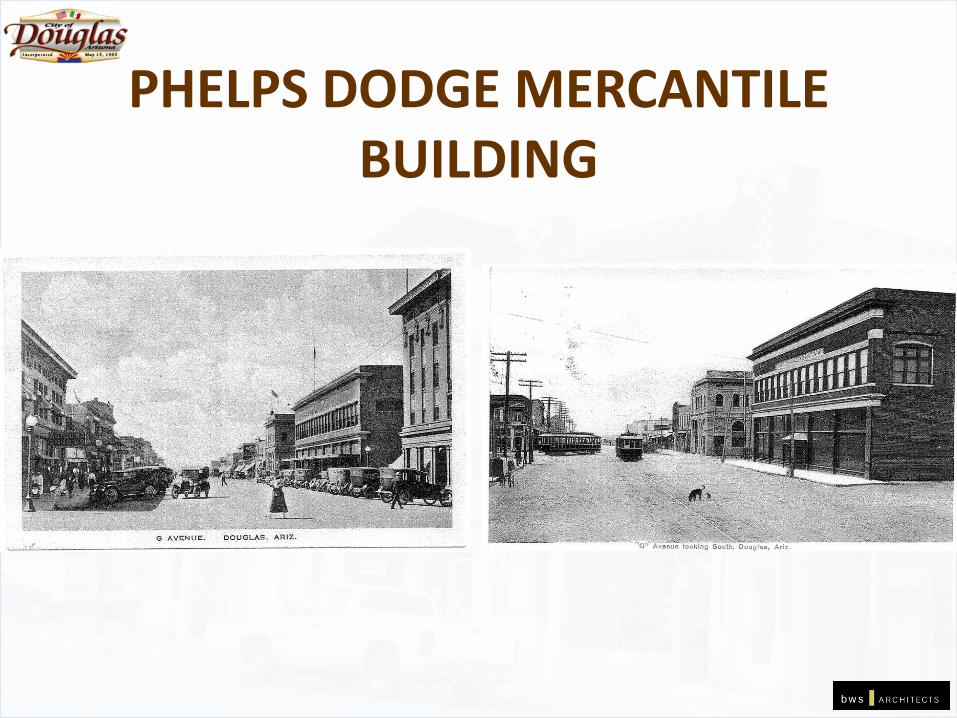

PHELPS DODGE MERCANTILE BUILDING

PHELPS DODGE MERCANTILE BUILDING

ENTRANCE

STAIRWAY

INTERIORS

NEW FLOOR PLAN

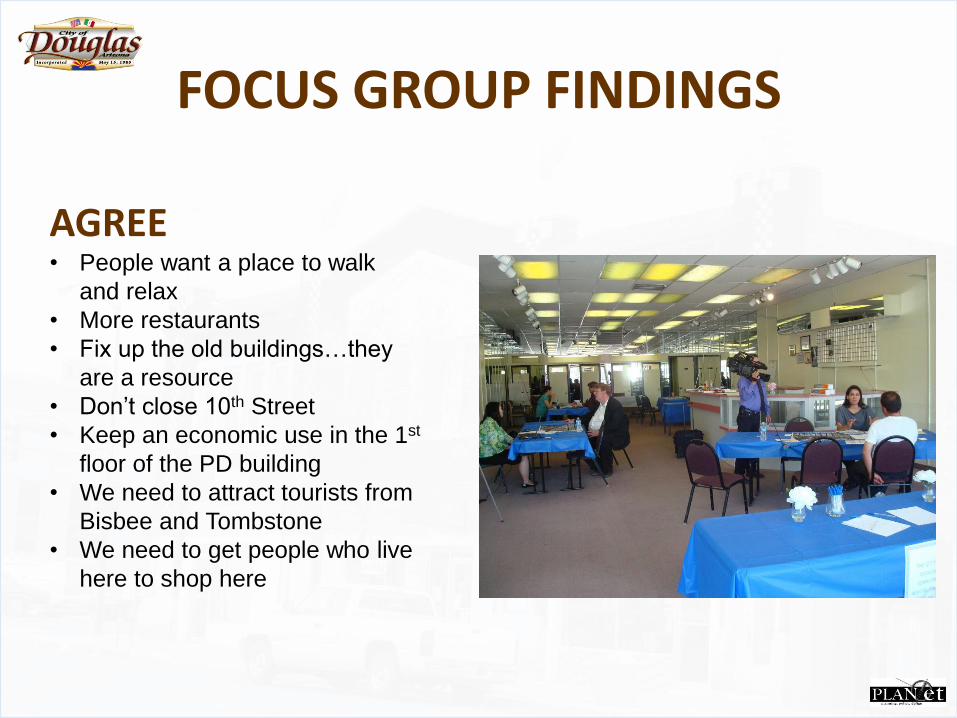

FOCUS GROUP FINDINGS

AGREE • People want a place to walk

and relax

• More restaurants

• Fix up the old buildings…they

are a resource

• Don’t close 10th Street

• Keep an economic use in the 1st

floor of the PD building

• We need to attract tourists from

Bisbee and Tombstone

• We need to get people who live

here to shop here

FOCUS GROUP FINDINGS

VARIETY OF IDEAS • Activities for youth in the

Downtown (renovate the YMCA

for them?)

• The role of the City in

Downtown redevelopment

(extent of code enforcement,

extent of regulations)

• Parking (not enough?)

• Role of Mexican Market

(depend on it more or less?)

1.Zones/Zone Elements 2.Circulation 3.Access/Gateways 4.Streetscape 5.Architecture

WHAT DO YOU THINK?

ZONE IDEA: Education

Main Mall, Poughkeepsie NY Douglas, Arizona

ZONE IDEA: Ramblas

Santa Monica Pier Ramblas, Spain Winslow, Arizona

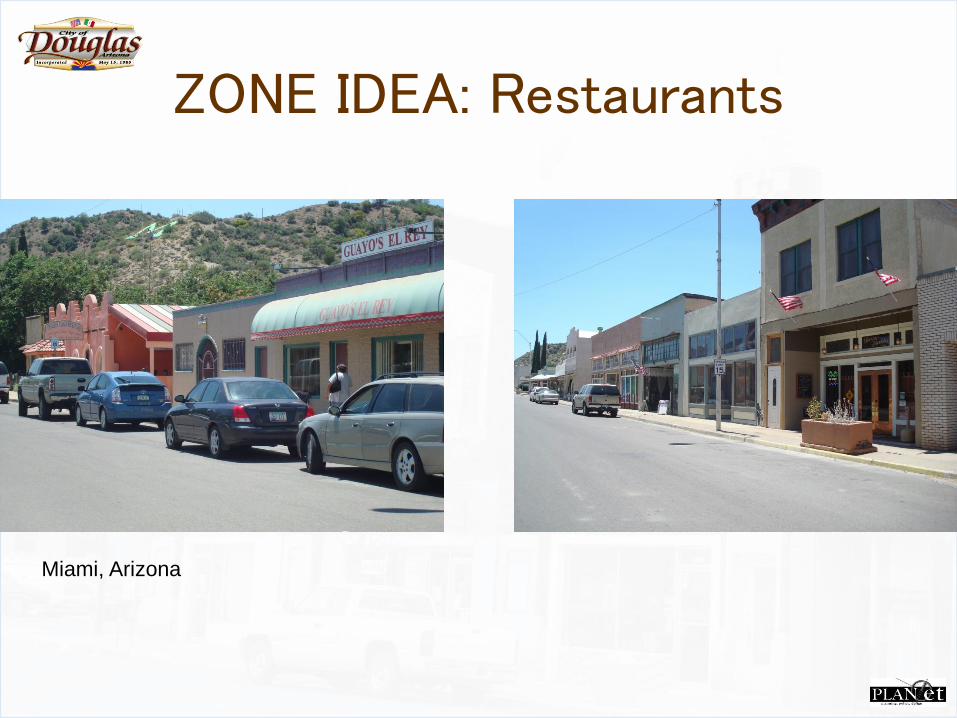

ZONE IDEA: Restaurants

Miami, Arizona

ZONE IDEA: Old West History

Slaughter Ranch, Arizona Pancho Villa George Washington Taverns

Pancho Villa

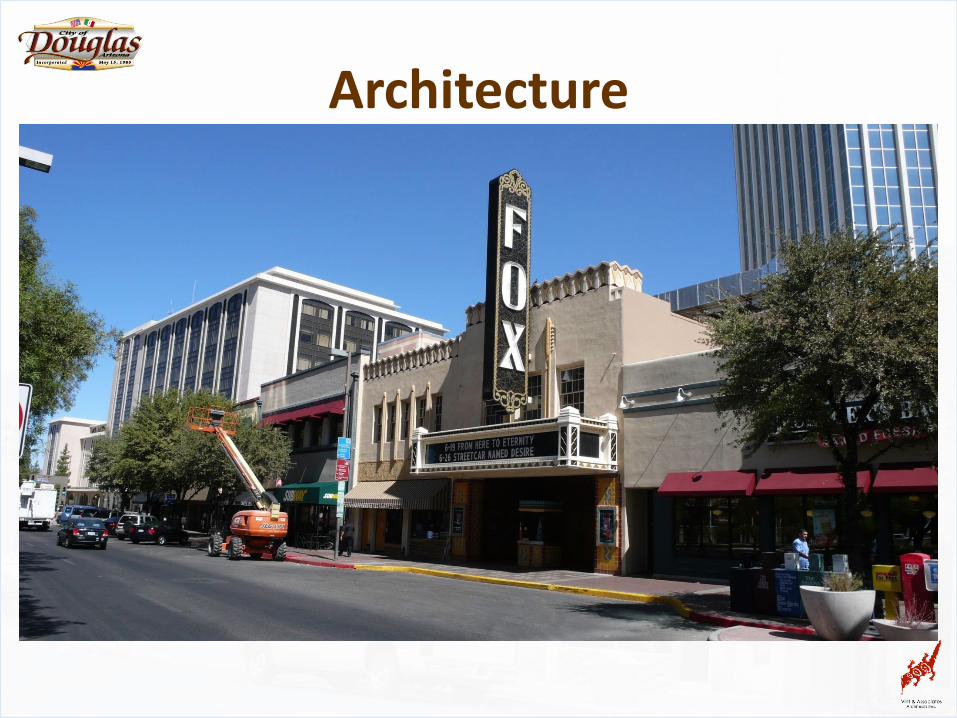

ZONE IDEA: Architecture

Globe, Arizona Tombstone, Arizona

ZONE IDEA: Arts/Culture

Tucson, Arizona Globe, Arizona

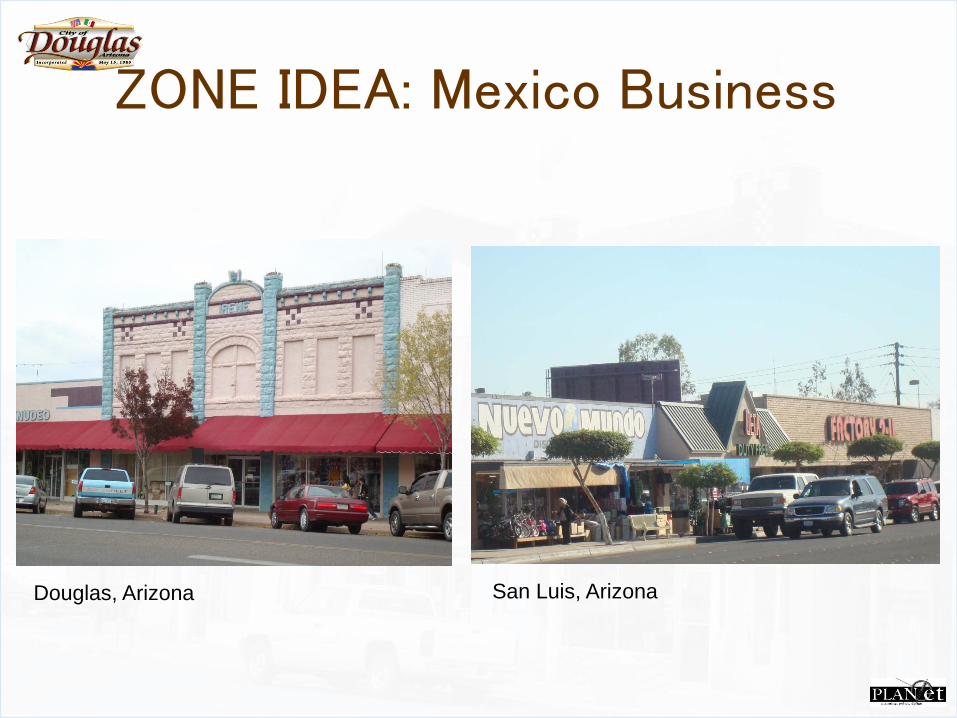

ZONE IDEA: Mexico Business

Douglas, Arizona San Luis, Arizona

ZONE IDEA: Mixed Use/Residential

Douglas, Arizona Miami, Arizona

ZONE: Government Center

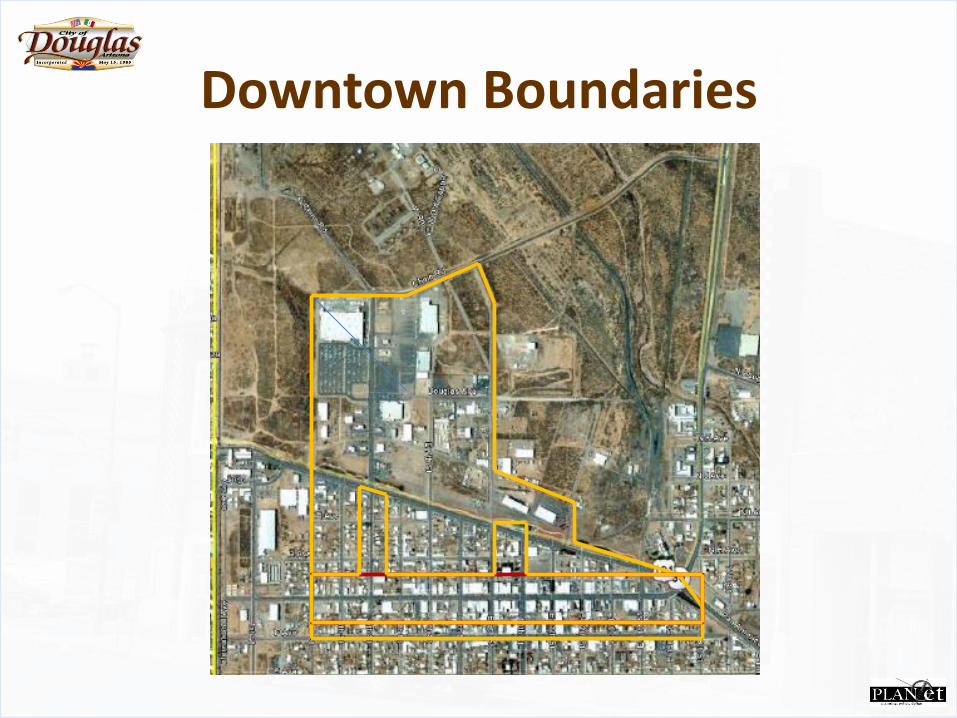

Downtown Boundaries

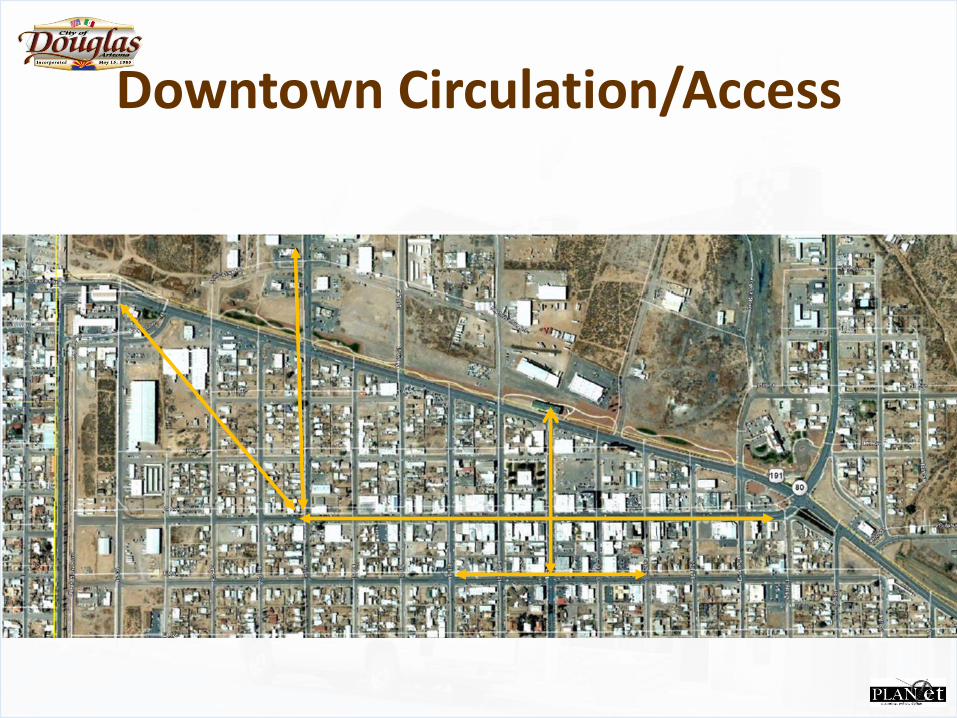

Downtown Circulation/Access

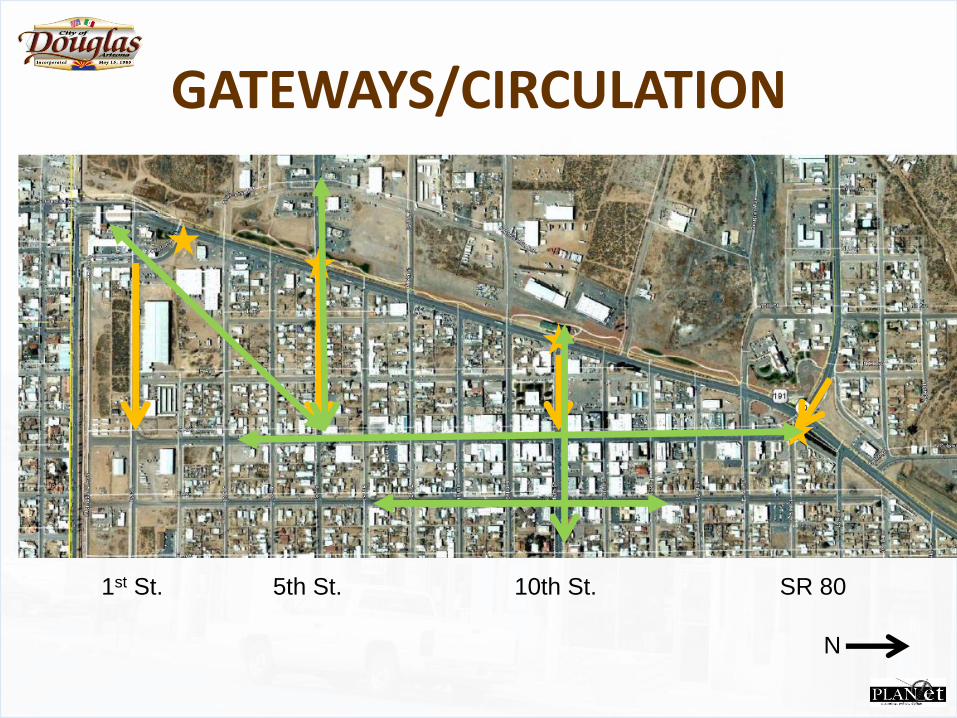

Downtown Gateways

1st St. 5th St. 10th St. SR 80

N

GATEWAYS/CIRCULATION

Downtown Gateways

McDowell Road, Phoenix Arizona Downtown Scottsdale, Arizona Globe, Arizona

Downtown Streetscape…

….establishes

a unique

identity & visual

character,

strengthens

community

sense of place,

is catalyst for

economic

development

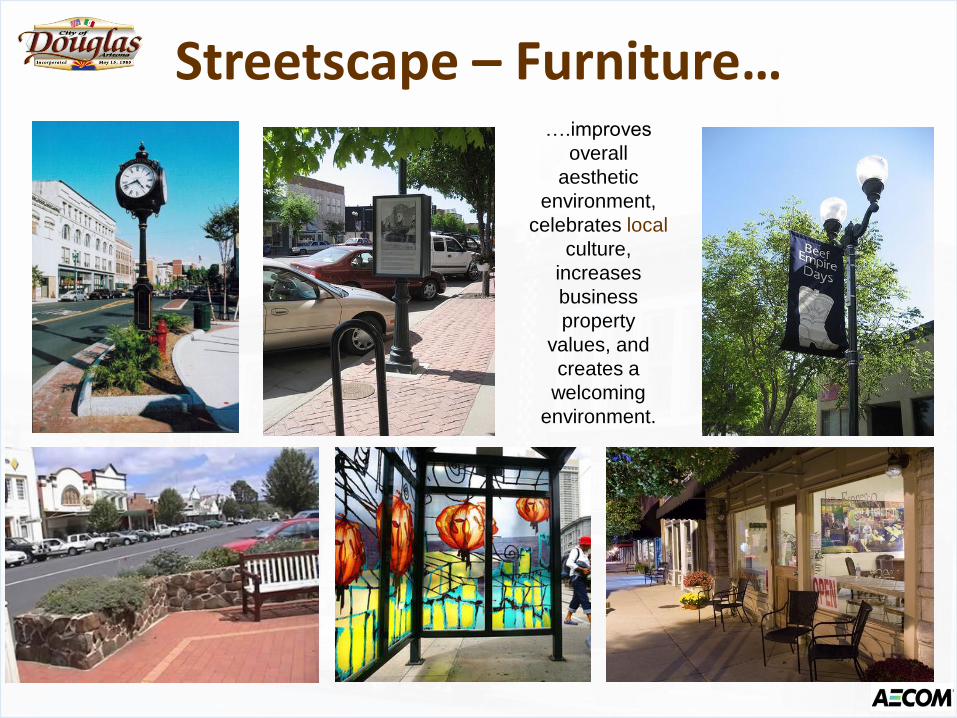

Streetscape – Furniture… ….improves

overall

aesthetic

environment,

celebrates local

culture,

increases

business

property

values, and

creates a

welcoming

environment.

Streetscape – Landscaping…

….adds value to the shopping and visiting

experience. Shrubs, trees, planters and parks are

essential to the downtown.

Streetscape - Colors

Mexican

inspired or

vibrant colors

for facades and

awnings

![Populärversion [100622]](https://img.dokumen.tips/doc/110x75/5486206fb4af9f586c8b45ff/populaerversion-100622.jpg)