Embed Size (px)

Citation preview

www.ubs.com/investmentresearch

This report has been prepared by UBS Securities Asia Limited. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 44. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Global Research 10 April 2019

Chinese Wind Power Sector No winners in this rush installation era

No one benefits from rush installation; downgrade Goldwind from Buy to Sell We cut our earnings forecasts and price targets for both wind turbine generator (WTG) manufacturers and wind farm operators, taking an anti-consensus cautious view on Goldwind, and being neutral on the operators. We expect new wind farm additions will surge in 2019 and 2020 before subsidy cancellation, as major wind farm operators aggressively raised capacity addition guidance in their 2018 results briefings. Contrary to consensus, we think this can hardly benefit Goldwind, as margin pressure eroded the volume benefits, and may be negative to wind farm operators as curtailment, earnings, subsidy payments, balance sheets, and cash flow will be under substantial pressure for two years. We downgrade Goldwind to Sell as the current high valuation multiples reflect volume upside but not margin pressure. We are neutral on wind farm operators as we think the impact of rush installation is largely priced in.

Rush installation ahead, but Goldwind can hardly benefit We raise our 2019/20 wind power connection forecasts from 22/23GW to above 30GW, suggesting large growth from 21GW in 2018. We think rush installation is justified as, even allowing for delays in grid connection and subsidies, project internal rates of return (IRR) in southern China are still better at 7.4% if installed now, than 5% if installed after 2020. However, we expect Goldwind's gross margin erosion could be worse than we had expected, from 25% in 2017 to 15/17% in 2019/20E. This will lower its WTG EBIT margin to 2-4%.

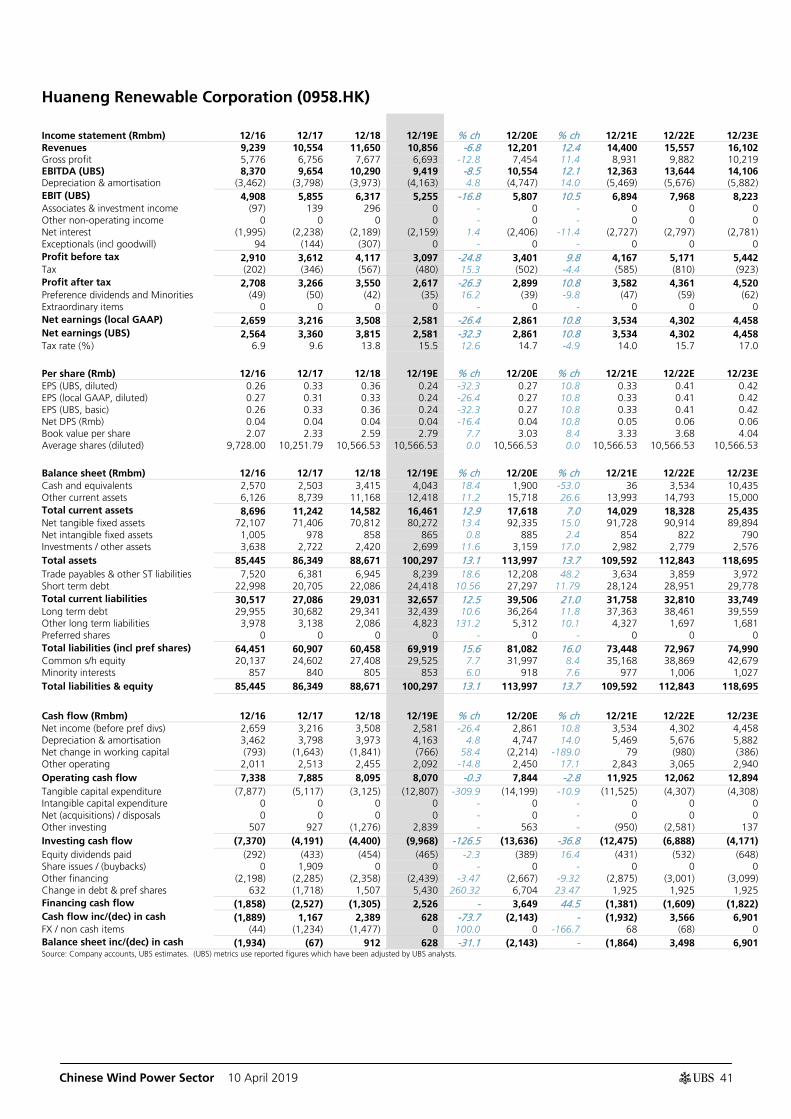

Two dark years for wind farm operators; downgrade Longyuan and Huaneng We believe wind farm operators will suffer from 1) reduced earnings as curtailment will likely worsen; 2) deteriorating cash flow with larger subsidy deficits and increased capex; 3) increased gearing. We cut our 2019/20 earnings forecasts by cutting utilisation hours from 2,200 to 2,000. We expect they generate negative FCF for 2019/20E from positive FCF in 2018. We downgrade Longyuan and Huaneng Renewable from Buy to Neutral.

What's priced in? We see valuation downside for Goldwind as the implied 2020E PE for its WTG business has already exceeded that of the 2015 upper cycle. For wind farm operators, we estimate that the returns profiles for 2019/20 will be similar to that in 2015. We believe valuations could remain close to the 2015 trough for some time at 0.7x P/BV, close to current valuations. Figure 1: Valuation summary and rating changes

Rating Current Price target Upside 2019E EPS 2020E EPS 2021E EPS

New Old price New Old Chg

New Old Chg New Old Chg New Old Chg

Goldwind-A Sell Buy Rmb13.80 Rmb11.50 Rmb17.00 -32% -17% 0.51 0.66 -22% 0.67 0.82 -19% 0.61 0.88 -31%

Goldwind-H Sell Buy HK$10.28 HK$8.50 HK$12.00 -29% -17% 0.51 0.71 -28% 0.67 0.88 -25% 0.61 0.95 -35%

Longyuan Neutral Buy HK$5.47 HK$6.00 HK$8.70 -31% 10% 0.48 0.80 -40% 0.52 0.88 -41% 0.67 0.97 -30%

HNR Neutral Buy HK$2.24 HK$2.40 HK$3.00 -20% 7% 0.24 0.36 -31% 0.27 0.38 -28% 0.33 0.40 -16% Region Reuters Mkt cap PE P/BV ROE Dividend yield

code Rating Rmb m 19E 20E 19E 20E 19E 20E 19E 20E

Goldwind-A CN 002202.SZ Sell 58,306 26.9x 20.7x 1.9x 1.8x 8.1% 9.0% 1.8% 1.9%

Goldwind-H CN 2208.HK Sell 37,172 17.2x 13.2x 1.2x 1.1x 8.1% 9.0% 2.7% 2.9%

Longyuan CN 0916.HK Neutral 37,621 9.8x 8.9x 0.8x 0.7x 8.4% 8.6% 2.0% 2.2%

HNR CN 0958.HK Neutral 20,257 7.9x 7.1x 0.7x 0.6x 9.1% 9.3% 1.9% 2.1% Source: Company data, UBS estimates. Note: price as of 9 April 2019; Goldwind-A's EPS change contains changes in share outstanding.

Equities

China

Electric Utilities

Abigail Sun Analyst

S1460518040002 [email protected]

+86-213-866 8637

Ken Liu Analyst

[email protected] +852-2971 7516

Simon Powell Analyst

[email protected] +852-2971 7772

Chinese Wind Power Sector 10 April 2019

2

Contents

OUR THESIS IN PICTURES .................................................................... 4

PIVOTAL QUESTIONS ........................................................................... 5

Q: Will wind power installation volume surge in 2019/20? .......................... 5

Q: Will curtailment continue to ease or turn worse? .................................... 8

Q: Can wind farm operators speed up the collection of subsidy receivables?

.................................................................................................................. 10

WHAT'S PRICED IN? .......................................................................... 13

Company pages .............................................................................. 14

Xinjiang Goldwind Science & Technology .................................................. 15

Xinjiang Goldwind Science & Technology-A ............................................... 28

China Longyuan Power .............................................................................. 29

Huaneng Renewable Corporation .............................................................. 36

Abigail Sun Analyst

S1460518040002 [email protected]

+86-213-866 8637

Ken Liu Analyst

[email protected] +852-2971 7516

Simon Powell Analyst

[email protected] +852-2971 7772

Chinese Wind Power Sector 10 April 2019

3

Chinese Wind Power Sector

P2

UBS Research THESIS MAP a guide to our thinking and what's where in this report OUR THESIS IN PICTURES

MOST FAVOURED LEAST FAVOURED

Longyuan Goldwind A/H

PIVOTAL QUESTIONS Q: Will wind power installation volume surge in 2019/20? Yes. We think wind power installation could surge significantly in 2019/20 ahead of the subsidy cancellation at end-2020. We forecast 30/32GW wind power connection and 31GW/33GW wind power installation in 2019/20. more

Q: Will curtailment continue to ease or become worse? Worse. We believe the glut of new wind farm supply is likely to increase the pressure for the grid to absorb the renewable power. Utilization is likely to be suppressed in 2019/20, which would be bad for earnings. We think curtailment may go back to the 2016 level of around 15%. more

Q: Can wind farm operators speed up the collection of subsidy receivables? Unlikely. The rush installation for new wind farms in 2019/20 will likely exacerbate the subsidy deficits from the current one year or eighteen months to almost two years. We expect balance sheets and cash flows for wind farm operators to further deteriorate. more

UBS VIEW We believe the operating environment for wind farm operators will significantly worsen in 2019/20 as most companies rush ahead to install new wind projects. We believe they will suffer from 1) reduced earnings as curtailments will likely worsen; 2) deteriorating cash flows, with larger subsidy deficits and increased capex; and 3) increased gearing.

EVIDENCE 1) Most managements of wind farm operators have increased their guidance for expansion plans in 2019 and 2020; 2) our renewable subsidy funds calculation shows that deficits will escalate in the next two years as capacity expansion is accelerating.

WHAT'S PRICED IN? The implied 2020E PE for Goldwind's WTG business has already gone above the level in 2015 upper cycle; we think market has priced in volume upside but not margin contraction. Trading at 0.7x 12-month forward P/BV for wind farm operators, we believe the market has priced in most of the negatives potentially brought by rush installations. Our 2019/20 ROE forecasts are similar to the levels in 2015. The current valuation multiples are similar to those back in 2015. more

Installation and connection could surge to over 30GW in 2019/20E

Source: Reuters, Company data, UBS estimates

17 15 15

20

34

20

16

21

30 32

25 25 25 25 25

18

13 16

23

31

23

20 21

31 33

24 25 25 25 25

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

GW

New connection New installation

Chinese Wind Power Sector 10 April 2019

4

Chinese Wind Power sector UBS Research

P3

OUR THESIS IN PICTURES return

China's wind power capacity addition should surge in 2019/20E

Rush installation could drive curtailment ratio to increase again

And subsidy receivable days will also increase, leading to deteriorated cash flows for wind farm operators

However, Goldwind can hardly benefit due to significant margin contraction

Sources for exhibits above: Company data, UBS Research

0

5

10

15

20

25

30

35

2011

2012

2013

2014

2015

2016

2017

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

GW Wind farm capacity addition

New connection New installation

0%

5%

10%

15%

20%

25%

30%

Q11

4

Q21

4

Q31

4

Q41

4

Q11

5

Q21

5

Q31

5

Q41

5

Q11

6

Q21

6

Q31

6

Q41

6

Q11

7

Q21

7

Q31

7

Q41

7

Q11

8

Q21

8

Q31

8

Q41

8

2019

E

2020

EWind power curtailment ratio

(10,000)

(5,000)

0

5,000

10,000

15,000

2017 2018 2019E 2020E 2021E 2022E

Free cash flow of wind farm operators (Rmb m)

Longyuan Huaneng Renewable China Resources Power

0

2,000

4,000

6,000

8,000

10,000

0%

5%

10%

15%

20%

25%

30%

35%

40%

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

E

2020

E

MW Goldwind's WTG sales volume and margin

WTG external sales volume EBIT margin Gross margin

Chinese Wind Power Sector 10 April 2019

5

Chinese Wind Power sector UBS Research

Sector Q1

PIVOTAL QUESTIONS return

Q: Will wind power installation volume surge in 2019/20? UBS VIEW

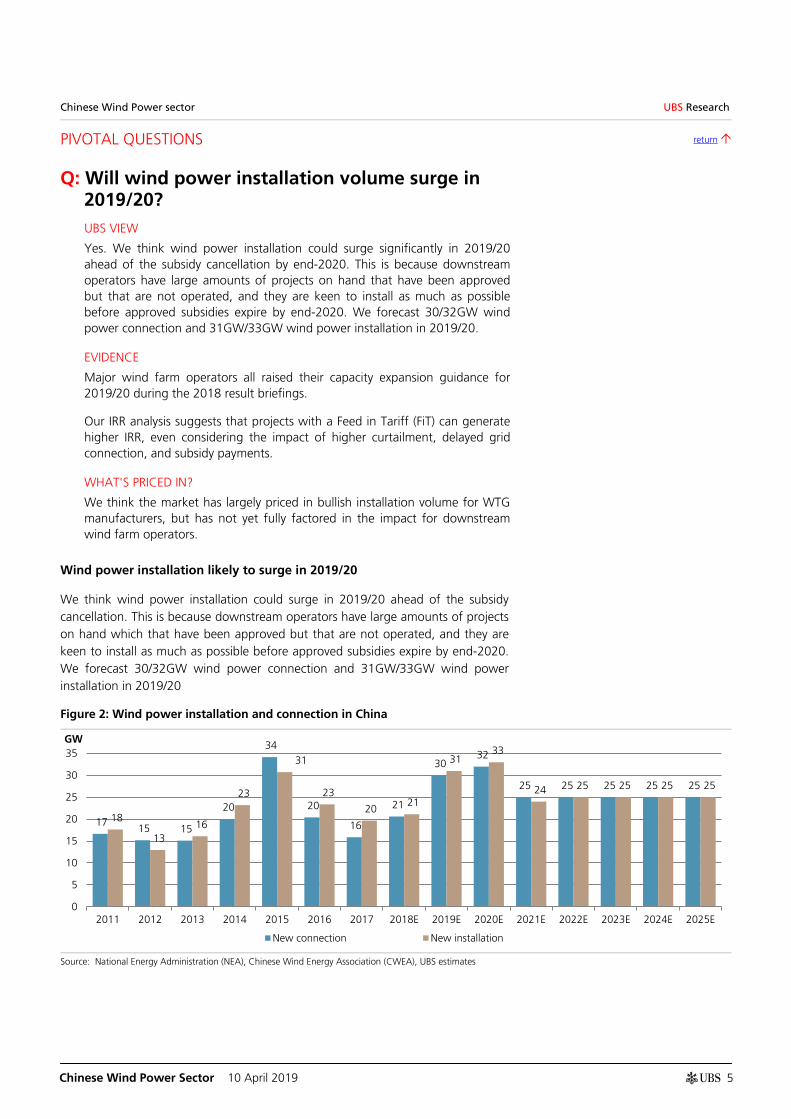

Yes. We think wind power installation could surge significantly in 2019/20 ahead of the subsidy cancellation by end-2020. This is because downstream operators have large amounts of projects on hand that have been approved but that are not operated, and they are keen to install as much as possible before approved subsidies expire by end-2020. We forecast 30/32GW wind power connection and 31GW/33GW wind power installation in 2019/20.

EVIDENCE

Major wind farm operators all raised their capacity expansion guidance for 2019/20 during the 2018 result briefings.

Our IRR analysis suggests that projects with a Feed in Tariff (FiT) can generate higher IRR, even considering the impact of higher curtailment, delayed grid connection, and subsidy payments.

WHAT'S PRICED IN?

We think the market has largely priced in bullish installation volume for WTG manufacturers, but has not yet fully factored in the impact for downstream wind farm operators.

Wind power installation likely to surge in 2019/20

We think wind power installation could surge in 2019/20 ahead of the subsidy cancellation. This is because downstream operators have large amounts of projects on hand which that have been approved but that are not operated, and they are keen to install as much as possible before approved subsidies expire by end-2020. We forecast 30/32GW wind power connection and 31GW/33GW wind power installation in 2019/20

Figure 2: Wind power installation and connection in China

Source: National Energy Administration (NEA), Chinese Wind Energy Association (CWEA), UBS estimates

17 15 15

20

34

20

16

21

30 32

25 25 25 25 25

18

13 16

23

31

23

20 21

31 33

24 25 25 25 25

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

GW

New connection New installation

Chinese Wind Power Sector 10 April 2019

6

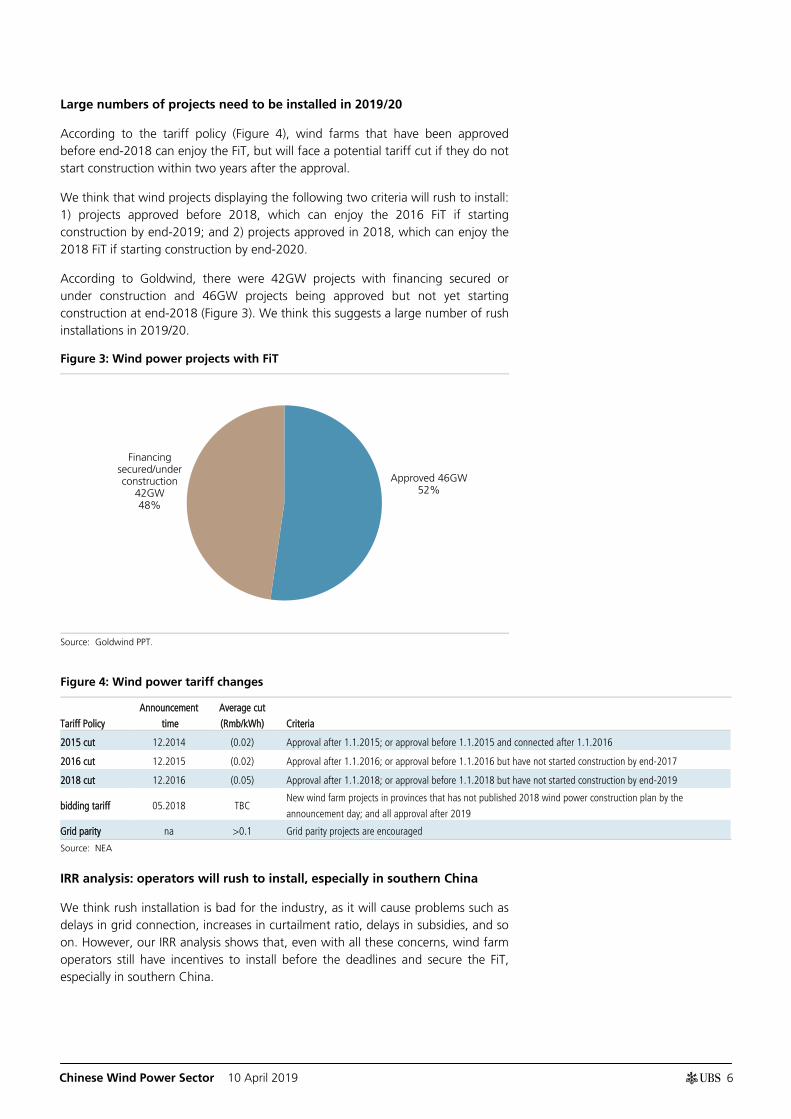

Large numbers of projects need to be installed in 2019/20

According to the tariff policy (Figure 4), wind farms that have been approved before end-2018 can enjoy the FiT, but will face a potential tariff cut if they do not start construction within two years after the approval.

We think that wind projects displaying the following two criteria will rush to install: 1) projects approved before 2018, which can enjoy the 2016 FiT if starting construction by end-2019; and 2) projects approved in 2018, which can enjoy the 2018 FiT if starting construction by end-2020.

According to Goldwind, there were 42GW projects with financing secured or under construction and 46GW projects being approved but not yet starting construction at end-2018 (Figure 3). We think this suggests a large number of rush installations in 2019/20.

Figure 3: Wind power projects with FiT

Source: Goldwind PPT.

Figure 4: Wind power tariff changes

Tariff Policy

Announcement

time

Average cut

(Rmb/kWh) Criteria

2015 cut 12.2014 (0.02) Approval after 1.1.2015; or approval before 1.1.2015 and connected after 1.1.2016

2016 cut 12.2015 (0.02) Approval after 1.1.2016; or approval before 1.1.2016 but have not started construction by end-2017

2018 cut 12.2016 (0.05) Approval after 1.1.2018; or approval before 1.1.2018 but have not started construction by end-2019

bidding tariff 05.2018 TBC New wind farm projects in provinces that has not published 2018 wind power construction plan by the

announcement day; and all approval after 2019

Grid parity na >0.1 Grid parity projects are encouraged

Source: NEA

IRR analysis: operators will rush to install, especially in southern China

We think rush installation is bad for the industry, as it will cause problems such as delays in grid connection, increases in curtailment ratio, delays in subsidies, and so on. However, our IRR analysis shows that, even with all these concerns, wind farm operators still have incentives to install before the deadlines and secure the FiT, especially in southern China.

Approved 46GW 52%

Financing secured/under construction

42GW 48%

Chinese Wind Power Sector 10 April 2019

7

In Figure 5 and Figure 6, we analyse wind projects’ IRRs under different scenarios, for regions in southern and northern China (we use Inner Mongolia as an example), respectively.

We assume that 1) if the projects are constructed before a deadline, it could enjoy FiT but will face a one-year delay in grid connection and subsidy payment, and a higher curtailment ratio in northern China; 2) if the projects are constructed after 2020, it is applied to local coal-fired tariffs with no subsidy, but they will face no curtailment or delays in grid connection.

Our analysis shows that wind farms in southern China will have large incentives to install in a rush, as their project IRR may drop by 2.4ppts under grid parity. But in areas such as Inner Mongolia, where curtailment is a concern and current subsidies are low, wind farms will not be hurt much under grid parity.

Figure 5: Wind project IRR under different scenarios – South (Region IV)

Capex

(Rmb

m/MW)

Tariff

(Rmb/kWh)

Subsidy

(Rmb/kWh)

Utilization

hours Delay in connection? Delay in subsidy? IRR

Normal case 8.0 0.570 0.180 2,100 No 1 year 9.10%

Constructed by 2020 8.0 0.570 0.180 2,100 1 year 2 year 7.40%

Construct after 2020 7.5 0.390 - 2,100 No No 5.00%

Source: UBS estimates

Figure 6: Wind project IRR under different scenarios – Inner Mongolia (Region I)

Capex

(Rmb

m/MW)

Tariff

(Rmb/kWh)

Subsidy

(Rmb/kWh)

Utilization

hours Delay in connection? Delay in subsidy? IRR

Normal case 7.0 0.400 0.107 3,000 No 1 year 11.00%

Constructed by 2020 7.0 0.400 0.107 2,850 1 year 2 year 8.30%

Construct after 2020 6.5 0.293 - 3,150 No No 8.20%

Source: UBS estimates

Downstream operators have all raised installation targets for 2019/20

Major wind farm operators all raised their installation targets for 2019/20 during the 2018 result briefings (Figure 7), as they all have large number of projects on hand that have been approved but that are not operated yet. And over 50% of these projects are in southern China.

Figure 7: Major operators plan to accelerate installation in 2019/20

Company Projects – approved but not operated Guidance on capacity expansion

Longyuan 7GW 1.2-1.5GW in 2019, more in 2020

Huaneng Renewable 4.2GW 1.6GW in 2019, more in 2020

Huaneng Power Na >2GW in 2019

CR Power 9GW 1.7GW in 2019, 2.3GW in 2020

Source: Company guidance

Chinese Wind Power Sector 10 April 2019

8

Chinese Wind Power sector UBS Research

Sector Q2

PIVOTAL QUESTIONS return

Q: Will curtailment continue to ease or turn worse? UBS VIEW

Worse. We believe the glut of new wind farm supply is likely to increase the pressure for the grid to absorb the renewable power. Utilisation is likely to be suppressed in 2019/20, which would be bad for earnings. We expect the curtailment ratio to go back to the 2016 level of around 15%.

EVIDENCE

We looked at the level of curtailment relative to power demand and the new capacity additions for renewables, and believe that curtailment may turn to be as bad as the level of 2016.

WHAT'S PRICED IN?

We believe investors have priced in modest curtailment risks.

The curtailment ratio is usually a function of overall power demand growth and the speed of capacity additions. Weak power demand growth and high capacity additions usually could result in a high curtailment ratio, and vice versa.

Figure 8 and Figure 9 show the historical curtailment ratio for wind farms compared with power demand growth and wind farm additions. As we expect new additions in 2019/20 could reach levels similar to those in 2015 with weakening power demand to potentially 4-5%, we believe the curtailment ratio for 2019/20 could be similar to that in 2016 at around 15%. This is a substantial increase from the latest Q418 curtailment ratio of only 5%.

We therefore believe that utilisation hours for wind farms will be under pressure, at least for two consecutive years. We expect utilisation hours for 2019/20 to be similar to the levels in 2016 for listed companies, at around 2,000 hours.

Figure 8: Curtailment ratio for wind farms Figure 9: National capacity addition for wind farms versus national power demand growth

Source: NEA Source: CEIC, UBS estimates

0%

5%

10%

15%

20%

25%

30%

Q11

4

Q21

4

Q31

4

Q41

4

Q11

5

Q21

5

Q31

5

Q41

5

Q11

6

Q21

6

Q31

6

Q41

6

Q11

7

Q21

7

Q31

7

Q41

7

Q11

8

Q21

8

Q31

8

Q41

8

2019

E

2020

E

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

5

10

15

20

25

30

35

40

2014 2015 2016 2017 2018 2019E 2020E

Capacity additions (MW) Power demand (YoY, RHS)

Chinese Wind Power Sector 10 April 2019

9

Zone IV means no curtailment?

Although most of the new projects added are in Zone IV, where curtailment was almost zero, we believe the inflow of new projects in Zone IV developed regions could likely crowd out the demand of renewable power imports in Zones I to III. This situation could be similar to those in 2015 and 2016, when most of the new projects added were at non-curtailment regions in Zone IV, and the overall wind power curtailment ratio still increased substantially.

Chinese Wind Power Sector 10 April 2019

10

Chinese Wind Power sector UBS Research

Sector Q3

PIVOTAL QUESTIONS return

Q: Can wind farm operators speed up the collection of subsidy receivables? UBS VIEW

Unlikely. The rush installation for new wind farms in 2019/20 is likely to exacerbate the subsidy deficits. We expect balance sheets and cash flows for wind farm operators to further deteriorate.

EVIDENCE

Our calculation shows that the annual subsidy deficit will continue to escalate to around Rmb108bn in 2020E, from Rmb66bn in 2018, with an increase of 63% in two years. It will be increasingly difficult for the wind farm operators to receive subsidies in a timely manner, and we expect receivable days to further increase from the current one year or eighteen months to close to two years.

WHAT'S PRICED IN?

We believe investors have largely priced in long receivable days, but may not have expected this to further exacerbate.

Annual subsidy deficit could increase by 48% from 2018 to 2020

As shown in Figure 2, the annual subsidy deficit grew from Rmb27bn in 2016 to Rmb66bn in 2018. We estimate that the annual deficit could rise to and peak out at Rmb105bn by the end of 2020, before it gradually grinds down to below Rmb100bn by 2025E.

This exercise shows that 1) in 2019/20E, the annual subsidy deficit will increase to Rmb88/98bn p.a., almost 33%/48% increases compared to that of 2018, This implies the subsidy receivable days will likely lengthen from currently around a year or eighteen months to almost two years; 2) cash flow will likely deteriorate substantially for wind farm operators because the capex they spent is unlikely to have cash coming back, at least for the subsidies, until two years later.

Our estimate assumes that the capacity addition will accelerate to 30/32GW p.a. for 2019/20 for wind farms, and that the subsidies for new projects in 2021 and after will be completely gone, such that the subsidy deficit will start to shrink in 2022 as the utilisation rate stabilises in the long term.

Chinese Wind Power Sector 10 April 2019

11

Figure 10: Renewable subsidy account calculation

(Rmb/kWh) 2016 2017 2018 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Surcharge income (cash inflow)

Renewable energy surcharge (Rmb/kWh)

Non-residential/agricultural 0.019 0.019 0.019 0.019 0.019 0.019 0.019 0.019 0.019 0.019

Residential 0.001 0.001 0.001 0.001 0.001 0.001 0.001 0.001 0.001 0.001

Agricultural - - - - - - - - - -

Power consumption (kWh bn)

Non-residential/agricultural 5,007 5,323 5,750 6,066 6,339 6,592 6,856 7,130 7,415 7,712

Residential 805 870 969 1,022 1,068 1,110 1,155 1,201 1,249 1,299

Agricultural 108 116 127 134 140 145 151 157 164 170

Implied surcharge income (Rmb bn) 96 102 110 116 122 126 131 137 142 148

Subsidy paid (cash outflow)

Wind power generation (kWh bn) 241 305 366 384 443 523 602 655 708 760

Solar power generation (kWh bn) 68 119 155 244 307 379 456 537 621 708

Wind subsidy (Rmb/kWh) 0.22 0.22 0.21 0.21 0.20 0.18 0.17 0.15 0.14 0.13

Solar subsidy (Rmb/kWh) 0.57 0.51 0.46 0.40 0.33 0.27 0.23 0.19 0.17 0.15

Total subsidy required (91) (127) (148) (175) (189) (197) (204) (205) (206) (207)

Actual surcharge collected 65 71 83 87 91 95 99 103 107 111

Collection rate 68% 69% 75% 75% 75% 75% 75% 75% 75% 75%

Annual surplus / (deficit), based on actual collection rate (27) (56) (66) (88) (98) (102) (105) (103) (100) (96)

Accumulated (51) (107) (173) (261) (359) (462) (567) (670) (769) (865)

Wind capacity - year-end (GW) 151 167 188 218 250 275 300 325 350 375

New additions (GW) 20 16 21 30 32 25 25 25 25 25

Solar capacity - year end (GW) 77 127 172 217 272 332 395 461 529 599

New additions (GW) 35 50 44 45 55 60 63 66 68 70 Source: UBS estimates

A key challenge is the delay of subsidies to renewables in China. China renewable energy operators, wind and solar mostly, are entitled to tariff subsidies that have been in place since 2009 and 2011, respectively. The tariffs that renewable energy operators are entitled to are made of two parts—benchmark coal-fired tariffs (around Rmb0.4/kWh) and the tariff subsidies on top of this, which add up to the total tariffs. The benchmark coal-fired tariffs are settled by the grid company in a timely manner, but the tariff subsidies, which are roughly Rmb0.2/kWh for wind and Rmb0.6/kWh for solar, are settled by the Ministry of Finance via the renewable energy subsidies fund.

According its original plans, the Ministry of Finance was supposed to pass on the tariffs subsidy burden to end-users, as end-users have to pay a renewable energy surcharge whenever they consume a unit of electricity. This surcharge should form an inflow of funds to the renewable energy subsidies fund, while the tariffs subsidies are the outflow of funds from it.

However, over the past few years, the fund has been facing severe deficits. This is because the amount of fund inflow has been growing slowly at the pace of overall power demand growth in the mid-single digits, while the end-user surcharge per one unit of electricity has remained unchanged. On the other hand, the amount of fund outflow has grown significantly, in the double digits, given strong growth in solar and wind capacity. In addition, some end-users have avoided paying the surcharge to the renewable energy fund. These are mostly captive power plants that do not pay electricity bills to the grid companies—thus, they have been able to indirectly avoid the surcharge payments.

Chinese Wind Power Sector 10 April 2019

12

Cash flow for wind farm operators will deteriorate

We believe cash flow for wind farm operators will be under substantial pressure in 2019 and 2020. This is because operating cash flow could be suppressed, as wind farm utilisation hours were reduced and the current subsidies receivable days of around a year to eighteen months could surge to close to two years. In addition, investing cash outflow will increase as most wind farm operators under our coverage have increased their capacity expansion plans for 2019/20 to get their projects completed before the subsidies are cut.

Figure 11 shows the free cash flow projection for wind farm operators; most of them will turn negative in 2019 and 2020 before recovering in 2021 and 2022. Figure 12 shows the accelerated capacity addition plan in 2019/20 for most operators.

Figure 11: Free cash flows for major wind farm operators under UBS coverage (Rmb m)

Source: Company data, UBS estimates

Figure 12: Capacity addition (MW) for major listed wind farm operators

Source: Company data, UBS estimates

(10,000)

(5,000)

0

5,000

10,000

15,000

2017 2018 2019E 2020E 2021E 2022E

Longyuan Huaneng Renewable China Resources Power

0

500

1,000

1,500

2,000

2,500

2017 2018 2019E 2020E 2021E 2022E

Longyuan Huaneng Renewable China Resources Power

Chinese Wind Power Sector 10 April 2019

13

Chinese Wind Power sector UBS Research

Sector priced in

WHAT'S PRICED IN? return

For wind equipment makers, please refer to the link below for the separate What's Priced In? section given the A- and H-share valuation differences (link)

Wind farm operators are trading at around 0.7x forward P/BV at around 8-9% ROE; this is similar to the levels when curtailment was relatively a serious issue in 2015-16 and the companies delivered similar ROE. As we forecast ROE for wind farm operators to stay low at least for 2019 and 2020, we believe the current valuations multiples are justified and most of the concerns are largely priced in.

Figure 13: Longyuan 12-month forward P/BV vs ROE Figure 14: Huaneng Renewable 12-month forward P/BV vs ROE

Source: Company data, Bloomberg, UBS estimates Source: Company data, Bloomberg, UBS estimates

Figure 15: Earnings sensitivity of Chinese wind farm operators

Longyuan Huaneng Renewable

2019E 2020E 2019E 2020E

Wind segment

50 hours (0.5ppt) increase in wind utilisation rate 8.0% 7.7% 7.9% 8.1%

1% cut in wind tariffs for new wind farms -0.2% -0.7% -0.4% -0.4%

1% cut in wind tariffs for all wind farms -11.7% -22.9% -12% -12.5%

25bps increase in interest costs -2.7% -5.5% -3.6% -3.8%

Source: Company data, UBS estimates

Chinese Wind Power Sector 10 April 2019

14

Company pages

abc Global Research 10 April 2019

Chinese Wind Power Sector 10 April 2019

15

Xinjiang Goldwind Science & Technology No gold from this rush; downgrade to Sell

Downgrade to Sell on WTG margin concerns We downgrade Goldwind-H from Buy to Sell, as we think the market has priced in the wind turbine generator (WTG) volume surge in 2019 but ignored margin contractions. While Goldwind's external WTG sales volume could increase to over 8GW in 2019/20 due to rush installation, we think larger-than-expected margin contraction could fully offset the benefit. We forecast Goldwind's recurring earnings to decline 3% in 2019, and to peak in 2020E with 30% YoY growth. We also think its net gearing could reach 80% in 2020E, from 65% in 2015, due to lower cash inflow from WTG, higher downstream capex and longer subsidy delays. The current valuation of its WTG business has already exceeded that in the 2015 cycle, and we think that risk is skewed to the downside.

2019 WTG gross margin could be lower than expected Goldwind's 2018 WTG gross margin was down 6ppts, larger than our expectation, and we think this trend will continue in 2019. This is because industry average bidding prices for 2.0MW/2.5MW WTG dropped by 14/13% YoY in 2018, and most of these orders will be delivered in 2019. We estimate this will pressure down Goldwind's overall ASP by 6% in 2019E, driving its gross margin to go down by another 4ppts to 15% in 2019E. This suggests its WTG EBIT margin could drop to 2% in 2019E, making any impact from volume growth almost irrelevant.

Valuation for peak year does not look attractive Goldwind-H is now trading at 17x/13x 2019/20E PE. While this still looks reasonable, we think investors need to notice that about 40% of Goldwind's net profit will come from its wind farm business, which deserves a lower PE. Our analysis shows that implied PE for Goldwind's WTG business in 2019/20E is already 28x/18x, much higher than the 15.5x in 2015. That means, even for its peak earnings in 2020E, the PE has already exceeded the historical peak, not mentioning that 1) Goldwind's earnings will decline in 2021E, and 2) its WTG EBIT margin is 2-4% in 2019/20E versus 13% in 2015.

Valuation: downgrade to Sell; lower price target from HK$12.00 to HK$8.50 We base our price target on a sum-of-the-parts (SOTP) methodology, with valuation of each segment based on DCF. We cut our price target by about 30% due to 1) larger WTG margin contraction; 2) higher curtailment and longer subsidy delay in 2019-21. Our price target implies 14.5x 2020E PE for WTG sales, close to the 2015 peak, and 6x 2020E PE for wind farms, similar to other operators.

Equities

China

Electric Components & Equipment

12-month rating Sell Prior: Buy

12m price target HK$8.50

Prior: HK$12.00

Price HK$10.28

RIC: 2208.HK BBG: 2208 HK

Trading data and key metrics 52-wk range HK$13.98-5.30

Market cap. HK$43.4bn/US$5.54bn

Shares o/s 4,225m (ORD)

Free float 85%

Avg. daily volume ('000) 10,252

Avg. daily value (m) HK$93.9

Common s/h equity (12/19E) Rmb30.2bn

P/BV (12/19E) 1.2x

Net debt / EBITDA (12/19E) 4.1x

EPS (UBS, diluted) (Rmb) From To % ch Cons.

12/19E 0.71 0.51 -28 0.81 12/20E 0.88 0.67 -25 0.99 12/21E 0.95 0.61 -35 1.18

Abigail Sun Analyst

S1460518040002 [email protected]

+86-213-866 8637

Wenzhuo Du Analyst

S1460516050001 [email protected]

+86-213-866 8960

Alex Liu Analyst

S1460515080001 [email protected]

+86-213-866 8857

Highlights (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Revenues 26,174 24,971 28,590 36,857 40,161 33,060 34,957 35,756 EBIT (UBS) 3,685 3,310 3,360 3,423 4,381 4,388 4,784 5,103 Net earnings (UBS) 2,681 2,271 2,241 2,166 2,810 2,581 2,933 3,208 EPS (UBS, diluted) (Rmb) 0.70 0.60 0.59 0.51 0.67 0.61 0.69 0.76 DPS (Rmb) 0.15 0.20 0.30 0.24 0.26 0.39 0.43 0.46 Net (debt) / cash (11,320) (15,650) (18,779) (20,741) (30,230) (28,007) (26,727) (25,147)

Profitability/valuation 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E EBIT margin % 14.1 13.3 11.8 9.3 10.9 13.3 13.7 14.3 ROIC (EBIT) % 14.9 10.7 9.3 8.0 8.3 7.5 8.2 8.7 EV/EBITDA (core) x 7.5 8.8 9.9 10.6 9.3 9.4 8.4 7.7 P/E (UBS, diluted) x 9.9 13.1 13.9 17.2 13.2 14.4 12.7 11.6 Equity FCF (UBS) yield % (9.2) (6.6) (8.9) (14.7) (21.5) 10.6 9.3 10.4 Net dividend yield % 2.1 2.6 3.6 2.8 2.9 4.4 4.8 5.2 Source: Company accounts, Thomson Reuters, UBS estimates. Metrics marked as (UBS) have had analyst adjustments applied. Valuations: based on an average share price that year, (E): based on a share price of HK$10.28 on 09 Apr 2019 18:27 HKT

Chinese Wind Power Sector 10 April 2019

16

Goldwind - H Sell (Price target HK$8.50)

CO1 P2

UBS-S Research THESIS MAP

a guide to our thinking and what's where in this report

PIVOTAL QUESTIONS Q: Will wind power installation volume surge in 2019/20? Yes. We think wind power installation could surge significantly in 2019/20 ahead of the subsidy cancellation. We forecast 30/32GW wind power connection and 31GW/33GW wind power installation in 2019/20. We expect Goldwind's external WTG sales volume to reach 8.4GW and 8.9GW in 2019E and 2020E, respectively. more

Q: Will WTG margin contraction fully offset the impact from volume growth in 2019? Likely. We think Goldwind's 2019 WTG gross margin faces large pressure because the industry average WTG bidding price dropped by over 10% YoY in 2018, and most of these orders will be delivered in 2019. We estimate the price pressure will bring down its WTG gross margin to around 15% and EBIT margin to around 2% in 2019E. more

Q: Will curtailment continue to ease or worsen? Worsen. We believe the glut of new wind farm supply is likely to increase the pressure for the grid to absorb the renewable power. Utilisation is likely to be suppressed in 2019/20 which is bad for earnings. We expect receivable days to surge from a year or eighteen months to almost two years. more

UBS-S VIEW

We downgrade Goldwind-H to Sell on margin concerns. We expect its external WTG sales volume to increase to over 8GW in 2019/20E due to rush installation, but larger-than-expected margin contraction could fully offset the benefit. Its wind farm business should face strong growth in capacity, but higher curtailment ratios and subsidy delays. We forecast Goldwind's recurring earnings to decline 3% in 2019, and to peak in 2020E with 30% YoY growth.

EVIDENCE

Our IRR analysis shows that even with delays in subsidy and grid connection, the operators are still incentivized to rush install to secure the FiT. Our margin analysis shows that Goldwind's WTG sales volume growth in 2019E will be fully offset by a margin squeeze.

WHAT'S PRICED IN? Current share price-implied PE for WTG business is 18x for 2020E peak earnings, much higher than the 15x in 2015, suggesting the market has priced in the upside in volume but not downside in margin.

more

UPSIDE / DOWNSIDE SPECTRUM

Value drivers 2019

WTG external sales volume

WTG gross margin

Wind farm utilization hours

Wind farm attributable capacity addition

HK$12.50 upside 9.5GW 17% 2,300 1.5GW HK$8.50 base 8.4GW 15% 2,244 1.1GW HK$6.50 downside 7.5GW 13% 2,150 0.8GW Source: UBS estimates

more

COMPANY DESCRIPTION Xinjiang Goldwind Science & Technology (Goldwind) is a leading manufacturer of wind turbine generators (WTG) in China. Goldwind was established in 1998 and had the largest WTG market share in China over 2011-18. more

Abigail Sun, Analyst, S1460518040002, [email protected], +86-213-866 8637

Chinese Wind Power Sector 10 April 2019

17

Goldwind – H UBS-S Research CO1 Q1

PIVOTAL QUESTIONS return

Q: Will WTG margin contraction fully offset the impact from volume growth in 2019?

UBS-S VIEW

Likely. We think Goldwind's 2019 WTG gross margin faces large pressure because the industry average WTG bidding price dropped by over 10% YoY in 2018, and most of these orders will be delivered in 2019. We estimate the price pressure will bring down its WTG gross margin to around 15% and EBIT margin to around 2% in 2019E. We expect Goldwind's WTG EBIT to drop 11% YoY in 2019E, despite a 43% increase in WTG sales volume.

EVIDENCE

WTG industry average bidding price dropped over 10% in 2018, and our analysis shows that it is highly related to Goldwind's WTG ASP with a one-year lag.

Our sensitivity analysis shows that Goldwind's net profit is not sensitive to WTG sales volume with WTGs’ current low margin.

WHAT'S PRICED IN?

We think investors know that Goldwind's gross margin will drop in 2019E, but do not expect it to fully offset the impact of WTG volume growth.

WTG margin drop could be larger than expected.

Goldwind's 2018 WTG gross margin dropped 6ppts to 19% due to the ASP drop and cost increases. We expect ASP pressure to push down its gross margin by another 4ppts, to 15% in 2019E, and gradually recover afterwards.

Figure 16 shows that historically Goldwind's WTG ASP is highly correlated to industry average bidding prices, with a one-year lag. The 2018 industry average bidding price for 2.0MW WTG dropped 14% YoY (Figure 17), and we estimate this could transfer to a 10% decline in its 2019 ASP, leading to a 6% decline in Goldwind's average WTG ASP.

Figure 16: Goldwind's WTG ASP vs. industry average bidding price (2.0MW, assuming a one-year lag)

Rmb/kw 2015 2016 2017 2018 2019E

Goldwind's WTG ASP – excl. VAT 3,709 3,568 3,476 3,302 2,972

YoY -4% -3% -5% -10%

Goldwind's WTG ASP – incl. VAT 4,340 4,174 4,067 3,830 3,358

Pre-year bidding average 4,170 4,244 4,144 3,847 3,323

Difference 4% -2% -2% 0% 1%

Note: We assume 17% VAT in 2015-17, 16% VAT in 2018 and 13% VAT in 2019. Source: Company data, UBS-S estimates

Chinese Wind Power Sector 10 April 2019

18

Figure 17: Historical industry average bidding price

Source: Company data.

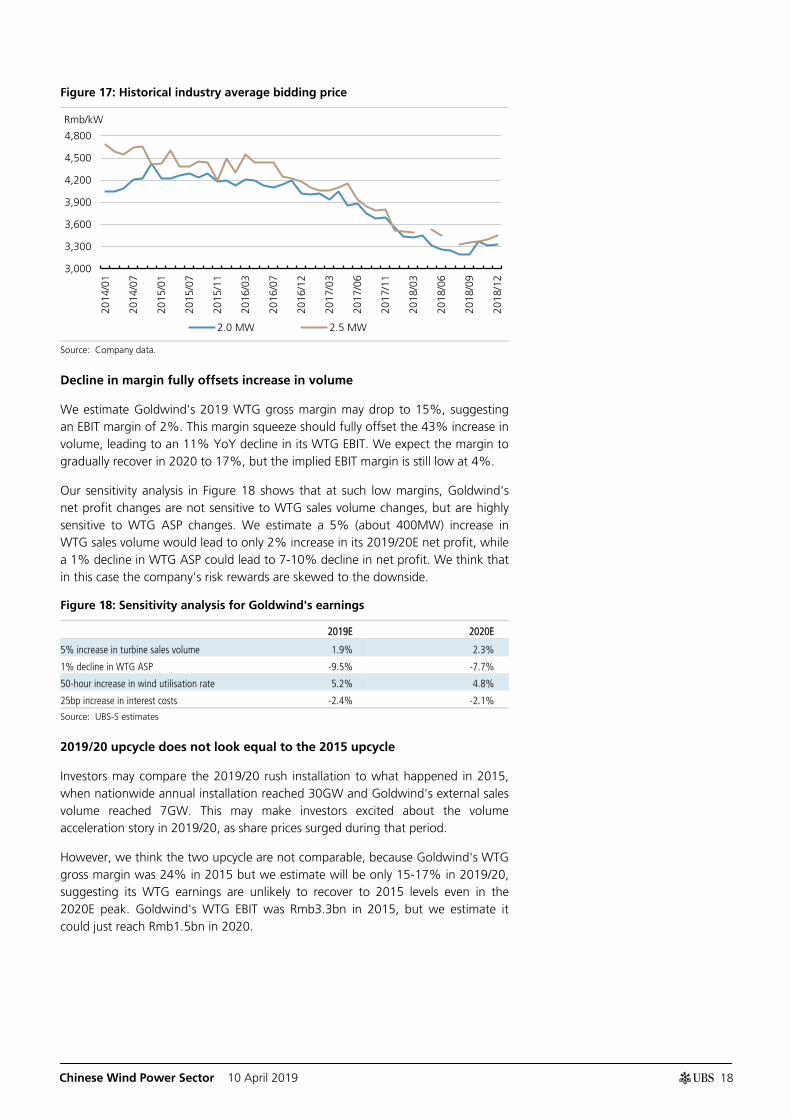

Decline in margin fully offsets increase in volume

We estimate Goldwind's 2019 WTG gross margin may drop to 15%, suggesting an EBIT margin of 2%. This margin squeeze should fully offset the 43% increase in volume, leading to an 11% YoY decline in its WTG EBIT. We expect the margin to gradually recover in 2020 to 17%, but the implied EBIT margin is still low at 4%.

Our sensitivity analysis in Figure 18 shows that at such low margins, Goldwind's net profit changes are not sensitive to WTG sales volume changes, but are highly sensitive to WTG ASP changes. We estimate a 5% (about 400MW) increase in WTG sales volume would lead to only 2% increase in its 2019/20E net profit, while a 1% decline in WTG ASP could lead to 7-10% decline in net profit. We think that in this case the company's risk rewards are skewed to the downside.

Figure 18: Sensitivity analysis for Goldwind's earnings

2019E 2020E

5% increase in turbine sales volume 1.9% 2.3%

1% decline in WTG ASP -9.5% -7.7%

50-hour increase in wind utilisation rate 5.2% 4.8%

25bp increase in interest costs -2.4% -2.1%

Source: UBS-S estimates

2019/20 upcycle does not look equal to the 2015 upcycle

Investors may compare the 2019/20 rush installation to what happened in 2015, when nationwide annual installation reached 30GW and Goldwind's external sales volume reached 7GW. This may make investors excited about the volume acceleration story in 2019/20, as share prices surged during that period.

However, we think the two upcycle are not comparable, because Goldwind's WTG gross margin was 24% in 2015 but we estimate will be only 15-17% in 2019/20, suggesting its WTG earnings are unlikely to recover to 2015 levels even in the 2020E peak. Goldwind's WTG EBIT was Rmb3.3bn in 2015, but we estimate it could just reach Rmb1.5bn in 2020.

3,000

3,300

3,600

3,900

4,200

4,500

4,800

2014

/01

2014

/07

2015

/01

2015

/07

2015

/11

2016

/03

2016

/07

2016

/12

2017

/03

2017

/06

2017

/11

2018

/03

2018

/06

2018

/09

2018

/12

Rmb/kW

2.0 MW 2.5 MW

Chinese Wind Power Sector 10 April 2019

19

Figure 19: Goldwind’s WTG sales volume and margin changes

Note: Margin includes sales of spare parts. Source: Company data, UBS estimates

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0%

5%

10%

15%

20%

25%

30%

35%

40%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019E 2020E

MW

WTG external sales volume EBIT margin Gross margin

Chinese Wind Power Sector 10 April 2019

20

Goldwind – H UBS-S Research CO1 WPI

WHAT'S PRICED IN? return

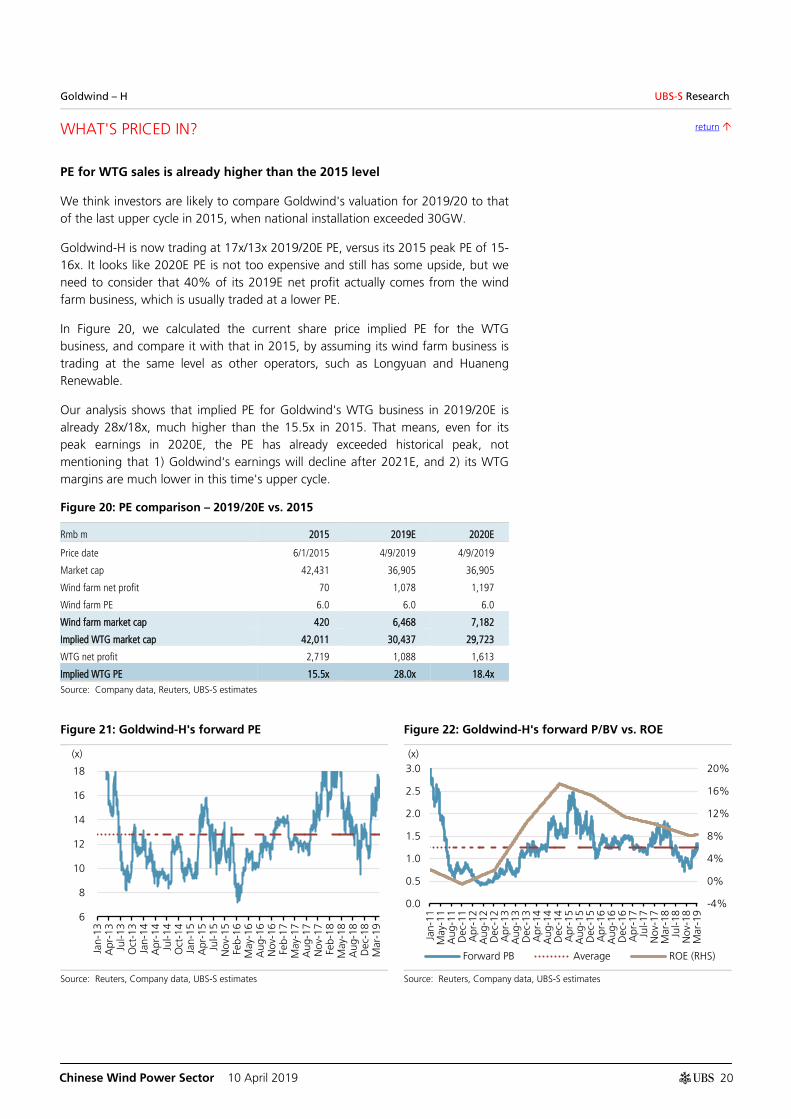

PE for WTG sales is already higher than the 2015 level

We think investors are likely to compare Goldwind's valuation for 2019/20 to that of the last upper cycle in 2015, when national installation exceeded 30GW.

Goldwind-H is now trading at 17x/13x 2019/20E PE, versus its 2015 peak PE of 15-16x. It looks like 2020E PE is not too expensive and still has some upside, but we need to consider that 40% of its 2019E net profit actually comes from the wind farm business, which is usually traded at a lower PE.

In Figure 20, we calculated the current share price implied PE for the WTG business, and compare it with that in 2015, by assuming its wind farm business is trading at the same level as other operators, such as Longyuan and Huaneng Renewable.

Our analysis shows that implied PE for Goldwind's WTG business in 2019/20E is already 28x/18x, much higher than the 15.5x in 2015. That means, even for its peak earnings in 2020E, the PE has already exceeded historical peak, not mentioning that 1) Goldwind's earnings will decline after 2021E, and 2) its WTG margins are much lower in this time's upper cycle.

Figure 20: PE comparison – 2019/20E vs. 2015

Rmb m 2015 2019E 2020E

Price date 6/1/2015 4/9/2019 4/9/2019

Market cap 42,431 36,905 36,905

Wind farm net profit 70 1,078 1,197

Wind farm PE 6.0 6.0 6.0

Wind farm market cap 420 6,468 7,182

Implied WTG market cap 42,011 30,437 29,723

WTG net profit 2,719 1,088 1,613

Implied WTG PE 15.5x 28.0x 18.4x

Source: Company data, Reuters, UBS-S estimates

Figure 21: Goldwind-H's forward PE Figure 22: Goldwind-H's forward P/BV vs. ROE

Source: Reuters, Company data, UBS-S estimates Source: Reuters, Company data, UBS-S estimates

6

8

10

12

14

16

18

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Nov

-15

Feb-

16M

ay-1

6A

ug-1

6N

ov-1

6Fe

b-17

May

-17

Aug

-17

Nov

-17

Feb-

18M

ay-1

8A

ug-1

8D

ec-1

8M

ar-1

9

(x)

-4%

0%

4%

8%

12%

16%

20%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-

11M

ay-1

1A

ug-1

1D

ec-1

1A

pr-1

2A

ug-1

2D

ec-1

2A

pr-1

3A

ug-1

3D

ec-1

3A

pr-1

4A

ug-1

4D

ec-1

4A

pr-1

5A

ug-1

5D

ec-1

5A

pr-1

6A

ug-1

6D

ec-1

6A

pr-1

7Ju

l-17

Nov

-17

Mar

-18

Jul-1

8N

ov-1

8M

ar-1

9

(x)

Forward PB Average ROE (RHS)

Chinese Wind Power Sector 10 April 2019

21

Figure 23 shows our revenue and earnings forecast versus consensus.

We are different from consensus in that: 1) our revenues are 23% below consensus in 2021E, because the market may expect rush installation to last to 2021, but we think it is unlikely that the grid/government can afford a three-year continuous rush installation; and 2) our earnings are much below consensus’s because we look at the recurring earnings, excluding disposal gains, while consensus may look at the reported earnings. Since about 30% of Goldwind's 2018 earnings are from disposal-related gains, we think this makes a big difference.

Figure 23: UBS versus consensus net profit (Rmb m)

Consensus UBS Difference

2019E 2020E 2021E 2019E 2020E 2021E 2019E 2020E 2021E

Revenue 37,696 43,141 43,899 36,857 40,161 33,060 -2% -7% -25%

Net profit 3,311 4,231 4,702 2,166 2,810 2,581 -35% -34% -45%

Source: Reuters, UBS-S estimates

Chinese Wind Power Sector 10 April 2019

22

Goldwind - H UBS-S Research CO1 UD

UPSIDE / DOWNSIDE SPECTRUM return

Value drivers 2019

WTG external sales volume

WTG gross margin

Wind farm utilization hours

Wind farm attributable capacity addition

HK$12.50 upside 9.5GW 17% 2,300 1.5GW HK$8.50 base 8.4GW 15% 2,244 1.1GW HK$6.50 downside 7.5GW 13% 2,150 0.8GW Source: UBS estimates

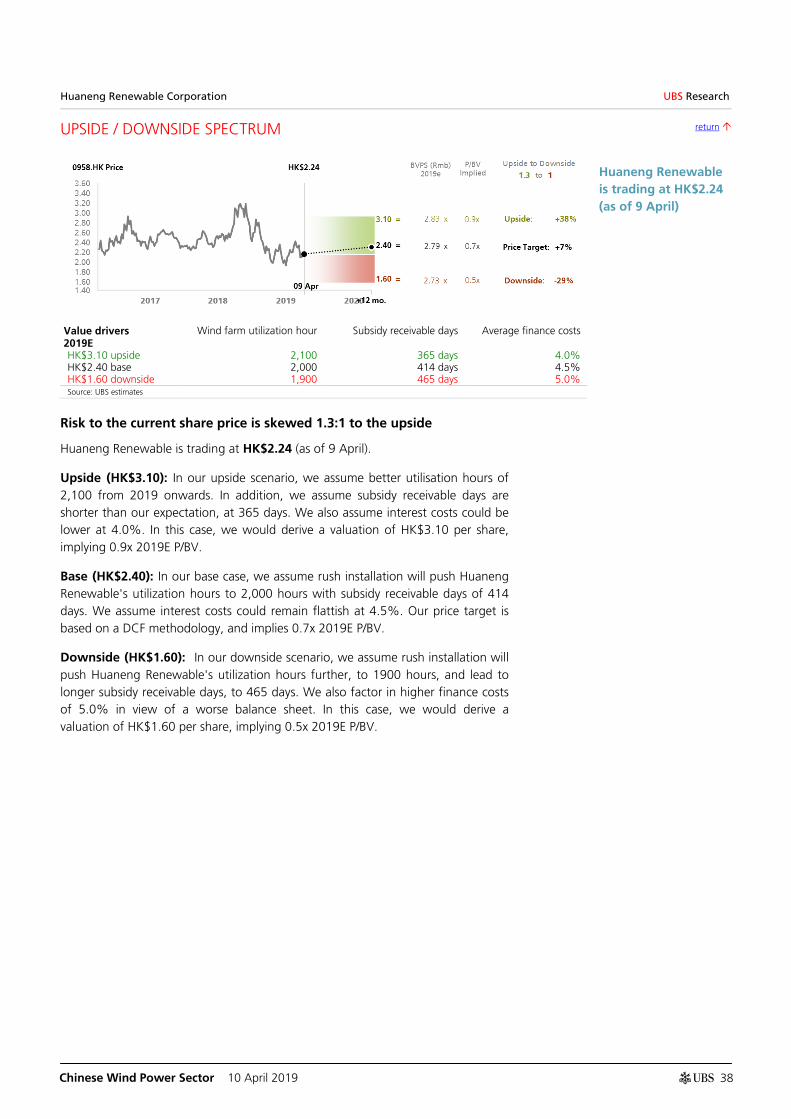

Goldwind is trading at HK$10.28 (as of 9 April 2019)

Risk to the current share price is skewed (1:1.7) to the downside

Goldwind-H is trading at HK$10.28 (as of 9 April 2019).

Upside (HK$12.50): In our upside scenario, we assume the total wind power installation in 2019 is higher than our expectation and reaches 38GW, suggesting about 9.5GW external sales for Goldwind given a 25% market share. The surge in volume may lead to some recovery in Goldwind's WTG gross margin, and we assume the margin contraction narrows to 2ppts YoY in 2019E. For wind farm operations, we factor in: 1) higher utilisation hours, assuming the curtailment issue in western China is solved; and 2) a higher capacity addition plan. In this scenario, we derive a valuation of HK$12.50 per share, implying 15x 2020E PE.

Base (HK$8.50): In our base case, we assume Goldwind's WTG volume could increase by 43%/7% to 8.4GW/8.9GW in 2019/20E, due to the rush installation of downstream operators. But we expect its WTG gross margin to contract by another 4ppts in 2019E and recover by 2ppts in 2020E, due to the delivery of 2018 cheap orders. For wind farms, we assume utilization hours can remain flattish in 2019E but drop to 2,200/2,100 in 2020/21E, as a result of rush installation in 2019/20E. We also assume Goldwind will accelerate its downstream investment, leading to 1.1/1.4GW net increases in its wind farm attributable capacity in 2019/20E.

Downside (HK$6.50): In our downside scenario, we assume wind power installation is lower than our expectation, at 30GW, as the power grid/government cannot support so much installation in one year. This will lead to 7.5GW external sales volume for Goldwind. We also assume Goldwind's WTG unit cost does not change in 2019, leading to a 5ppt drop in the WTG gross margin. For the wind farms, we assume higher curtailment ratio and smaller installations in 2019. In this case, we derive a downside valuation of HK$6.50 per share, implying 9x 2020E PE.

Chinese Wind Power Sector 10 April 2019

23

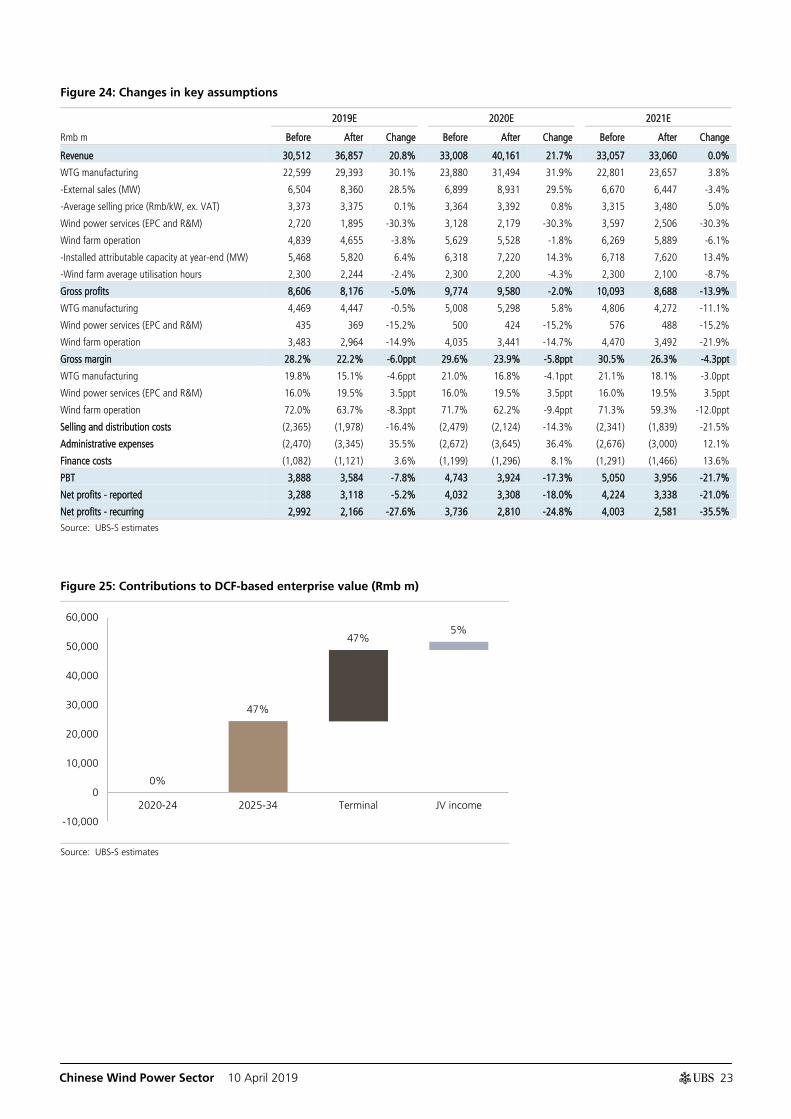

Figure 24: Changes in key assumptions

2019E 2020E 2021E

Rmb m Before After Change Before After Change Before After Change

Revenue 30,512 36,857 20.8% 33,008 40,161 21.7% 33,057 33,060 0.0%

WTG manufacturing 22,599 29,393 30.1% 23,880 31,494 31.9% 22,801 23,657 3.8%

-External sales (MW) 6,504 8,360 28.5% 6,899 8,931 29.5% 6,670 6,447 -3.4%

-Average selling price (Rmb/kW, ex. VAT) 3,373 3,375 0.1% 3,364 3,392 0.8% 3,315 3,480 5.0%

Wind power services (EPC and R&M) 2,720 1,895 -30.3% 3,128 2,179 -30.3% 3,597 2,506 -30.3%

Wind farm operation 4,839 4,655 -3.8% 5,629 5,528 -1.8% 6,269 5,889 -6.1%

-Installed attributable capacity at year-end (MW) 5,468 5,820 6.4% 6,318 7,220 14.3% 6,718 7,620 13.4%

-Wind farm average utilisation hours 2,300 2,244 -2.4% 2,300 2,200 -4.3% 2,300 2,100 -8.7%

Gross profits 8,606 8,176 -5.0% 9,774 9,580 -2.0% 10,093 8,688 -13.9%

WTG manufacturing 4,469 4,447 -0.5% 5,008 5,298 5.8% 4,806 4,272 -11.1%

Wind power services (EPC and R&M) 435 369 -15.2% 500 424 -15.2% 576 488 -15.2%

Wind farm operation 3,483 2,964 -14.9% 4,035 3,441 -14.7% 4,470 3,492 -21.9%

Gross margin 28.2% 22.2% -6.0ppt 29.6% 23.9% -5.8ppt 30.5% 26.3% -4.3ppt

WTG manufacturing 19.8% 15.1% -4.6ppt 21.0% 16.8% -4.1ppt 21.1% 18.1% -3.0ppt

Wind power services (EPC and R&M) 16.0% 19.5% 3.5ppt 16.0% 19.5% 3.5ppt 16.0% 19.5% 3.5ppt

Wind farm operation 72.0% 63.7% -8.3ppt 71.7% 62.2% -9.4ppt 71.3% 59.3% -12.0ppt

Selling and distribution costs (2,365) (1,978) -16.4% (2,479) (2,124) -14.3% (2,341) (1,839) -21.5%

Administrative expenses (2,470) (3,345) 35.5% (2,672) (3,645) 36.4% (2,676) (3,000) 12.1%

Finance costs (1,082) (1,121) 3.6% (1,199) (1,296) 8.1% (1,291) (1,466) 13.6%

PBT 3,888 3,584 -7.8% 4,743 3,924 -17.3% 5,050 3,956 -21.7%

Net profits - reported 3,288 3,118 -5.2% 4,032 3,308 -18.0% 4,224 3,338 -21.0%

Net profits - recurring 2,992 2,166 -27.6% 3,736 2,810 -24.8% 4,003 2,581 -35.5%

Source: UBS-S estimates

Figure 25: Contributions to DCF-based enterprise value (Rmb m)

Source: UBS-S estimates

0%

47%

47% 5%

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

2020-24 2025-34 Terminal JV income

Chinese Wind Power Sector 10 April 2019

24

Figure 26: Valuation summary – Wind farm Figure 27: Valuation summary – WTG & others

Source: UBS-S estimates Source: UBS-S estimates

Chinese Wind Power Sector 10 April 2019

25

Goldwind - H UBS-S Research CO1 Co des

COMPANY DESCRIPTION return

Xinjiang Goldwind Science & Technology (Goldwind) is a leading manufacturer of wind turbine generators (WTG) in China. Goldwind was established in 1998 and had the largest WTG market share in China in 2011-18. It developed and began operating its own wind farm in 2012 and had 4.7GW of attributable connected wind farms as of end-2018. The company was listed on the Shenzhen Stock Exchange in December 2007 and on the Hong Kong Stock Exchange in October 2010.

Industry outlook

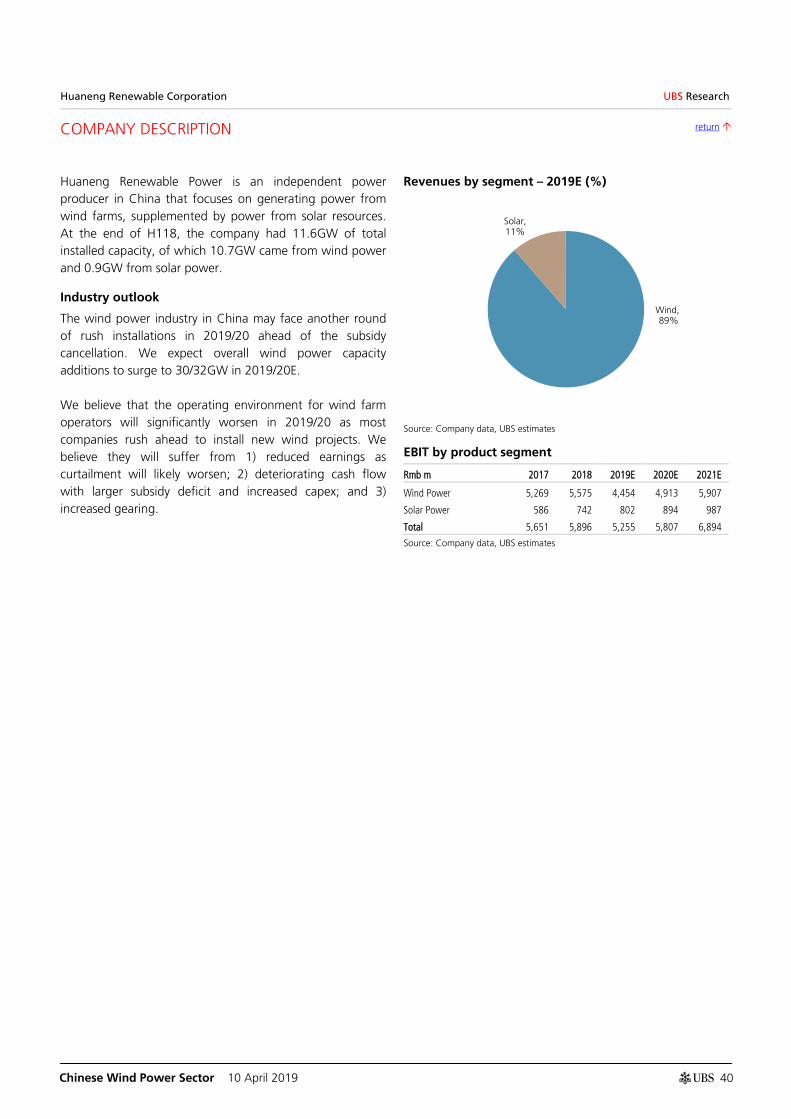

We think wind power installation will accelerate in 2019-20E to over 30GW p.a. because wind projects with fixed tariffs were all approved before end-2018 and need to start construction within two years. In the longer term, we think annual installation may maintain at an average of 24GW under bidding tariff/grid parity, as we expect development of large wind farms in north China together with UHV lines to drive future demand growth.

We expect WTG manufacturers' margins will trough in 2019E, and further downside under bidding tariff /grid parity is limited, as: 1) the already-published bidding tariff rule suggests regulators do not encourage fierce price competition; 2) downstream operators will focus more on LCOE instead of WTG price; and 3) WTG manufacturers' profitability under the current price environment is already thin, leaving them no incentive for another price war, in our view.

For downstream wind farm operators, we think they will suffer from reduced earnings as curtailment will likely worsen, deteriorating cash flow with larger subsidy deficit and increased capex as well as increasing gearing.

Revenues by segment (%)

Source: Company data, UBS-S estimates

EBIT by product segment

Rmb m 2016 2017 2018 2019E 2020E

WTG manufacturing 2,690 1,455 958 848 1,529

Wind farm operation 1,040 2,227 2,687 2,979 2,727

Others 239 341 620 477 552

Total EBIT 3,969 4,023 4,265 4,304 4,808

Non-recurring item (285) (713) (904) (882) (427)

Adjusted EBIT 3,685 3,310 3,360 3,423 4,381

Source: Company data, UBS-S estimates

WTG manufacturing

80%

Wind farm operation

13%

Others 7%

Chinese Wind Power Sector 10 April 2019

26

Xinjiang Goldwind Science & Technology (2208.HK)

Income statement (Rmbm) 12/16 12/17 12/18 12/19E % ch 12/20E % ch 12/21E 12/22E 12/23E Revenues 26,174 24,971 28,590 36,857 28.9 40,161 9.0 33,060 34,957 35,756 Gross profit 7,558 7,466 7,344 8,176 11.3 9,580 17.2 8,688 9,264 9,630 EBITDA (UBS) 4,609 4,434 4,741 5,086 7.3 6,407 26.0 6,707 7,246 7,707 Depreciation & amortisation (924) (1,124) (1,381) (1,663) 20.4 (2,026) 21.8 (2,319) (2,461) (2,604) EBIT (UBS) 3,685 3,310 3,360 3,423 1.9 4,381 28.0 4,388 4,784 5,103 Associates & investment income 192 210 266 314 18.0 354 12.5 323 334 344 Other non-operating income 0 0 0 0 - 0 - 0 0 0 Net interest (609) (743) (849) (1,035) -21.9 (1,238) -19.7 (1,441) (1,359) (1,283) Exceptionals (incl goodwill) 0 0 0 0 - 0 - 0 0 0 Profit before tax 3,267 2,778 2,778 2,703 -2.7 3,497 29.4 3,270 3,760 4,164 Tax (446) (342) (400) (387) 3.1 (522) -34.7 (519) (651) (777) Profit after tax 2,821 2,436 2,378 2,315 -2.6 2,975 28.5 2,751 3,108 3,387 Preference dividends and Minorities (140) (165) (137) (150) -8.9 (164) -9.9 (171) (175) (179) Extraordinary items 285 713 904 882 -2.5 427 -51.6 686 673 661 Net earnings (local GAAP) 2,966 2,984 3,145 3,047 -3.1 3,237 6.2 3,267 3,606 3,869 Net earnings (UBS) 2,681 2,271 2,241 2,166 -3.4 2,810 29.8 2,581 2,933 3,208 Tax rate (%) 13.7 12.3 14.4 14.3 -0.4 14.9 4.1 15.9 17.3 18.7

Per share (Rmb) 12/16 12/17 12/18 12/19E % ch 12/20E % ch 12/21E 12/22E 12/23E EPS (UBS, diluted) 0.70 0.60 0.59 0.51 -12.9 0.67 29.8 0.61 0.69 0.76 EPS (local GAAP, diluted) 0.78 0.78 0.83 0.72 -12.7 0.77 6.2 0.77 0.85 0.91 EPS (UBS, basic) 0.70 0.60 0.59 0.51 -12.9 0.67 29.8 0.61 0.69 0.76 Net DPS (Rmb) 0.15 0.20 0.30 0.24 -18.5 0.26 6.2 0.39 0.43 0.46 Book value per share 4.85 5.56 6.16 7.15 16.1 7.69 7.6 8.23 8.71 9.22 Average shares (diluted) 3,809.40 3,809.40 3,809.40 4,225.07 10.9 4,225.07 0.0 4,225.07 4,225.07 4,231.88

Balance sheet (Rmbm) 12/16 12/17 12/18 12/19E % ch 12/20E % ch 12/21E 12/22E 12/23E Cash and equivalents 8,267 7,730 5,050 6,560 29.9 1,179 -82.0 1,906 1,765 1,995 Other current assets 24,830 25,352 27,867 36,424 30.7 38,070 4.5 29,823 30,588 30,151 Total current assets 33,097 33,081 32,918 42,984 30.6 39,249 -8.7 31,729 32,353 32,146 Net tangible fixed assets 19,479 22,838 25,509 32,455 27.2 40,699 25.4 41,947 43,029 43,945 Net intangible fixed assets 1,250 2,752 3,965 3,830 -3.4 3,695 -3.5 3,561 3,426 3,291 Investments / other assets 10,612 14,116 18,973 19,287 1.7 19,641 1.8 19,964 20,298 20,642 Total assets 64,437 72,788 81,364 98,556 21.1 103,285 4.8 97,201 99,106 100,024 Trade payables & other ST liabilities 21,991 23,601 28,130 35,043 24.6 33,315 -4.9 26,413 27,629 27,691 Short term debt 2,672 5,999 3,470 3,470 0.00 3,470 0.00 3,470 3,470 3,470 Total current liabilities 24,663 29,600 31,601 38,513 21.9 36,786 -4.5 29,883 31,099 31,161 Long term debt 15,419 15,886 18,865 22,336 18.4 26,443 18.4 24,948 23,527 22,177 Other long term liabilities 3,656 3,827 4,424 4,424 0.0 4,424 0.0 4,424 4,424 4,424 Preferred shares 1,495 1,495 1,495 1,495 0.00 1,495 0.00 1,495 1,495 1,495 Total liabilities (incl pref shares) 45,233 50,808 56,384 66,768 18.4 69,148 3.6 60,749 60,545 59,257 Common s/h equity 18,481 21,192 23,466 30,221 28.8 32,506 7.6 34,756 36,800 38,937 Minority interests 723 788 1,514 1,567 3.5 1,631 4.1 1,695 1,761 1,830 Total liabilities & equity 64,437 72,788 81,364 98,556 21.1 103,285 4.8 97,201 99,106 100,024

Cash flow (Rmbm) 12/16 12/17 12/18 12/19E % ch 12/20E % ch 12/21E 12/22E 12/23E Net income (before pref divs) 3,003 3,055 3,217 3,118 -3.1 3,308 6.1 3,338 3,677 3,940 Depreciation & amortisation 924 1,124 1,381 1,663 20.4 2,026 21.8 2,319 2,461 2,604 Net change in working capital (807) (885) (856) (1,759) -105.5 (3,374) -91.8 1,345 451 499 Other operating (18) (270) (588) 708 - 858 21.2 1,065 984 908 Operating cash flow 3,103 3,023 3,153 3,730 18.3 2,818 -24.4 8,066 7,573 7,951 Tangible capital expenditure (5,501) (4,843) (5,943) (9,177) -54.4 (10,795) -17.6 (4,135) (4,105) (4,075) Intangible capital expenditure (152) (63) (83) 0 - 0 - 0 0 0 Net (acquisitions) / disposals (1,405) (2,313) (4) 864 - 714 -17.3 724 717 711 Other investing 47 120 (84) 178 - 178 - 178 178 178 Investing cash flow (7,011) (7,098) (6,114) (8,136) -33.1 (9,903) -21.7 (3,234) (3,210) (3,186) Equity dividends paid (1,313) (547) (711) (1,056) -48.5 (1,023) 3.1 (1,087) (1,633) (1,803) Share issues / (buybacks) 1,495 0 0 4,693 - 0 - 0 0 0 Other financing (699) (883) 304 (1,193) - (1,380) -15.72 (1,522) (1,450) (1,381) Change in debt & pref shares 5,763 4,812 1,609 3,472 115.81 4,107 18.30 (1,496) (1,421) (1,350) Financing cash flow 5,247 3,382 1,201 5,916 392.4 1,704 -71.2 (4,105) (4,504) (4,534) Cash flow inc/(dec) in cash 1,338 (693) (1,759) 1,510 - (5,381) - 727 (141) 230 FX / non cash items 628 156 (920) 0 100.0 0 - 0 0 0 Balance sheet inc/(dec) in cash 1,966 (537) (2,679) 1,510 - (5,381) - 727 (141) 230 Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts.

Chinese Wind Power Sector 10 April 2019

27

Xinjiang Goldwind Science & Technology (2208.HK)

Valuation (x) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E P/E (local GAAP, diluted) 9.0 9.9 9.9 12.2 11.5 11.4 10.3 9.6 P/E (UBS, diluted) 9.9 13.1 13.9 17.2 13.2 14.4 12.7 11.6 P/CEPS 7.4 8.7 8.6 9.7 7.7 7.6 6.9 6.4 Equity FCF (UBS) yield % (9.2) (6.6) (8.9) (14.7) (21.5) 10.6 9.3 10.4 Net dividend yield (%) 2.1 2.6 3.6 2.8 2.9 4.4 4.8 5.2 P/BV x 1.4 1.4 1.3 1.2 1.1 1.1 1.0 1.0 EV/revenues (core) 1.3 1.6 1.6 1.5 1.5 1.9 1.7 1.7 EV/EBITDA (core) 7.5 8.8 9.9 10.6 9.3 9.4 8.4 7.7 EV/EBIT (core) 9.4 11.8 13.9 15.8 13.6 14.3 12.7 11.6 EV/OpFCF (core) 7.7 9.0 10.1 10.9 9.4 9.5 8.5 7.8 EV/op. invested capital 1.4 1.3 1.3 1.3 1.1 1.1 1.0 1.0

Enterprise value (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Market cap. 27,859 28,461 32,375 37,179 37,179 37,179 37,179 37,179 Net debt (cash) 8,757 13,485 17,215 19,760 25,486 29,118 27,367 25,937 Buy out of minorities 676 755 1,151 1,541 1,599 1,663 1,728 1,795 Pension provisions/other 0 0 0 0 0 0 0 0 Total enterprise value 37,291 42,701 50,741 58,480 64,264 67,960 66,274 64,912 Non core assets (2,622) (3,693) (3,974) (4,326) (4,748) (5,198) (5,674) (5,674) Core enterprise value 34,669 39,008 46,767 54,155 59,516 62,763 60,600 59,237

Growth (%) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Revenue -12.3 -4.6 14.5 28.9 9.0 -17.7 5.7 2.3 EBITDA (UBS) 17.4 -3.8 6.9 7.3 26.0 4.7 8.0 6.4 EBIT (UBS) 8.9 -10.2 1.5 1.9 28.0 0.2 9.0 6.7 EPS (UBS, diluted) -2.4 -15.3 -1.3 -12.9 29.8 -8.2 13.7 9.2 Net DPS -58.2 37.5 48.5 -18.5 6.2 50.2 10.4 7.3

Margins & Profitability (%) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Gross profit margin 28.9 29.9 25.7 22.2 23.9 26.3 26.5 26.9 EBITDA margin 17.6 17.8 16.6 13.8 16.0 20.3 20.7 21.6 EBIT margin 14.1 13.3 11.8 9.3 10.9 13.3 13.7 14.3 Net earnings (UBS) margin 10.2 9.1 7.8 5.9 7.0 7.8 8.4 9.0 ROIC (EBIT) 14.9 10.7 9.3 8.0 8.3 7.5 8.2 8.7 ROIC post tax 12.7 9.3 7.8 6.7 6.9 6.2 6.6 6.9 ROE (UBS) 15.2 11.4 10.0 8.1 9.0 7.7 8.2 8.5

Capital structure & Coverage (x) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Net debt / EBITDA 2.5 3.5 4.0 4.1 4.7 4.2 3.7 3.3 Net debt / total equity % 58.9 71.2 75.2 65.2 88.6 76.8 69.3 61.7 Net debt / (net debt + total equity) % 37.1 41.6 42.9 39.5 47.0 43.4 40.9 38.2 Net debt/EV % 32.7 40.1 40.2 38.3 50.8 44.6 44.1 42.5 Capex / depreciation % NM NM NM NM NM 189.4 176.5 165.1 Capex / revenue % 21.0 19.4 20.8 24.9 26.9 12.5 11.7 11.4 EBIT / net interest 6.0 4.5 4.0 3.3 3.5 3.0 3.5 4.0 Dividend cover (UBS) 4.8 3.0 2.0 2.1 2.6 1.6 1.6 1.7 Div. payout ratio (UBS) % 20.7 33.6 50.5 47.3 38.7 63.3 61.5 60.3

Revenues by division (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Wind turbine generator business and others

22,264 19,346 22,169 29,393 31,494 23,657 24,866 24,924

Wind farm development 2,414 3,247 3,904 4,655 5,528 5,889 6,152 6,408 Others 1,496 2,377 2,518 2,808 3,138 3,513 3,939 4,424 Total 26,174 24,971 28,590 36,857 40,161 33,060 34,957 35,756

EBIT (UBS) by division (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Wind farm development 562 1,191 1,590 1,852 2,076 2,066 2,140 2,211 Wind turbine generator business and others 2,802 1,450 845 660 1,319 1,282 1,476 1,598

Others 321 669 925 911 987 1,041 1,168 1,295 Total 3,685 3,310 3,360 3,423 4,381 4,388 4,784 5,103 Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts.

abc Global Research 10 April 2019

Chinese Wind Power Sector 10 April 2019 28

Xinjiang Goldwind Science & Technology-A No gold from this rush; downgrading to Sell

Downgrading to Sell on concern over wind turbine generator margins We downgrade Goldwind-A [Link] from Buy to Sell, as we think the market has priced in the wind turbine generator (WTG) volume surge in 2019E but ignored the margin contraction. While Goldwind's external WTG sales volume could increase to over 8GW pa in 2019/20E due to an installation rush, we think larger than expected margin contraction will fully offset the benefit. We forecast recurring earnings to decline 3% YoY in 2019 and reach peak growth of 30% YoY in 2020E. We expect net gearing to rise to 80% in 2020 from 65% in 2015 due to lower cash inflow from WTGs, higher downstream capex and longer subsidy delays. The valuation of its WTG business has exceeded that of the 2015 peak cycle, and we believe risk is skewed to the downside.

2019 WTG gross margin could be lower than expected Goldwind's 2018 WTG gross margin was down 6ppt, a stepper decline than we expected, and we think this trend will continue in 2019. The industry average bidding price for 2.0/2.5MW WTG dropped by 14/13% YoY in 2018, and most of these orders will be delivered in 2019. We estimate this will lower overall WTG ASP by 6% and GPM by 4ppt to 15% in 2019. This suggests Goldwind's WTG EBIT margin could decline to 2% in 2019E, making any impact from volume growth almost irrelevant.

Valuation for peak year does not look attractive Goldwind - A is trading at 27x/21x 2019/20E PE. While this valuation looks reasonable, we note that c.40% of Goldwind's net profit will come from its wind farm business, which deserves a lower PE. Our analysis shows the implied 2019/20E PE of Goldwind's WTG business is already 44x/29x, much higher than the 24x seen in 2015. This means that its PE even for peak earnings in 2020E has already exceeded the historical peak. On top of that, we estimate: 1) Goldwind's earnings will decline in 2021; and 2) its 2019/20E WTG EBIT margins will be 2-4% versus 13% in 2015.

Valuation: Downgrading to Sell with new price target of Rmb11.50 Our PT is based on sum-of-the-parts methodology, with the valuation of each segment based on DCF. We cut our 2019-21E earnings by 19-31% and PT by c.30% due to: 1) larger than expected WTG margin contraction; and 2) higher curtailment and a longer subsidy delay in 2019-21E. Our PT implies 24x 2020E PE for WTG, close to the 2015 peak, and 8x 2020E PE for wind farms, close to other operators.

Equities

China

Electric Components & Equipment

12-month rating Sell Prior: Buy

12m price target Rmb11.50

Prior: Rmb17.00

Price Rmb13.80

RIC: 002202.SZ BBG: 002202 CH

Trading data and key metrics 52-wk range Rmb17.05-8.05

Market cap. Rmb58.3bn/US$8.68bn

Shares o/s 4,225m (ORDA )

Free float 49%

Avg. daily volume ('000) 42,126

Avg. daily value (m) Rmb552.9

Common s/h equity (12/19E) Rmb30.2bn

P/BV (12/19E) 1.9x

Net debt / EBITDA (12/19E) 4.1x

EPS (UBS, diluted) (Rmb) From To % ch Cons.

12/19E 0.66 0.51 -22 0.86 12/20E 0.82 0.67 -19 1.07 12/21E 0.88 0.61 -31 1.31

Abigail Sun Analyst

S1460518040002 [email protected]

+86-213-866 8637

Wenzhuo Du Analyst

S1460516050001 [email protected]

+86-213-866 8960

Alex Liu Analyst

S1460515080001 [email protected]

+86-213-866 8857

Highlights (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Revenues 26,174 24,971 28,590 36,857 40,161 33,060 34,957 35,756 EBIT (UBS) 3,685 3,310 3,360 3,423 4,381 4,388 4,784 5,103 Net earnings (UBS) 2,681 2,271 2,241 2,166 2,810 2,581 2,933 3,208 EPS (UBS, diluted) (Rmb) 0.70 0.60 0.59 0.51 0.67 0.61 0.69 0.76 DPS (Rmb) 0.15 0.20 0.30 0.24 0.26 0.39 0.43 0.46 Net (debt) / cash (11,320) (15,650) (18,779) (20,741) (30,230) (28,007) (26,727) (25,147)

Profitability/valuation 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E EBIT margin % 14.1 13.3 11.8 9.3 10.9 13.3 13.7 14.3 ROIC (EBIT) % 14.9 10.7 9.3 8.0 8.3 7.5 8.2 8.7 EV/EBITDA (core) x 11.1 12.9 13.4 14.6 12.4 12.4 11.2 10.5 P/E (UBS, diluted) x 16.6 20.5 22.5 26.9 20.7 22.6 19.9 18.2 Equity FCF (UBS) yield % (5.7) (4.0) (5.7) (9.3) (13.7) 6.7 5.9 6.6 Net dividend yield % 1.2 1.6 2.2 1.8 1.9 2.8 3.1 3.3 Source: Company accounts, Thomson Reuters, UBS estimates. Metrics marked as (UBS) have had analyst adjustments applied. Valuations: based on an average share price that year, (E): based on a share price of Rmb13.80 on 09 Apr 2019 18:35 HKT

Global Research 10 April 2019

Chinese Wind Power Sector 10 April 2019

29

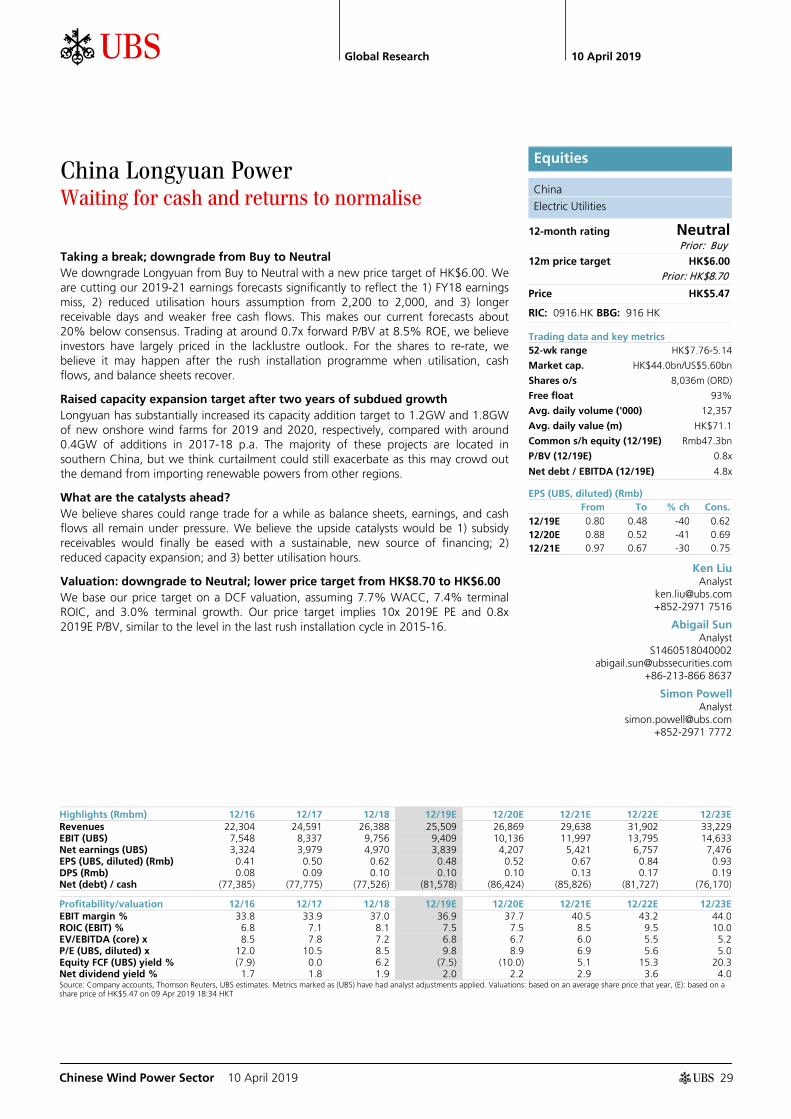

China Longyuan Power Waiting for cash and returns to normalise

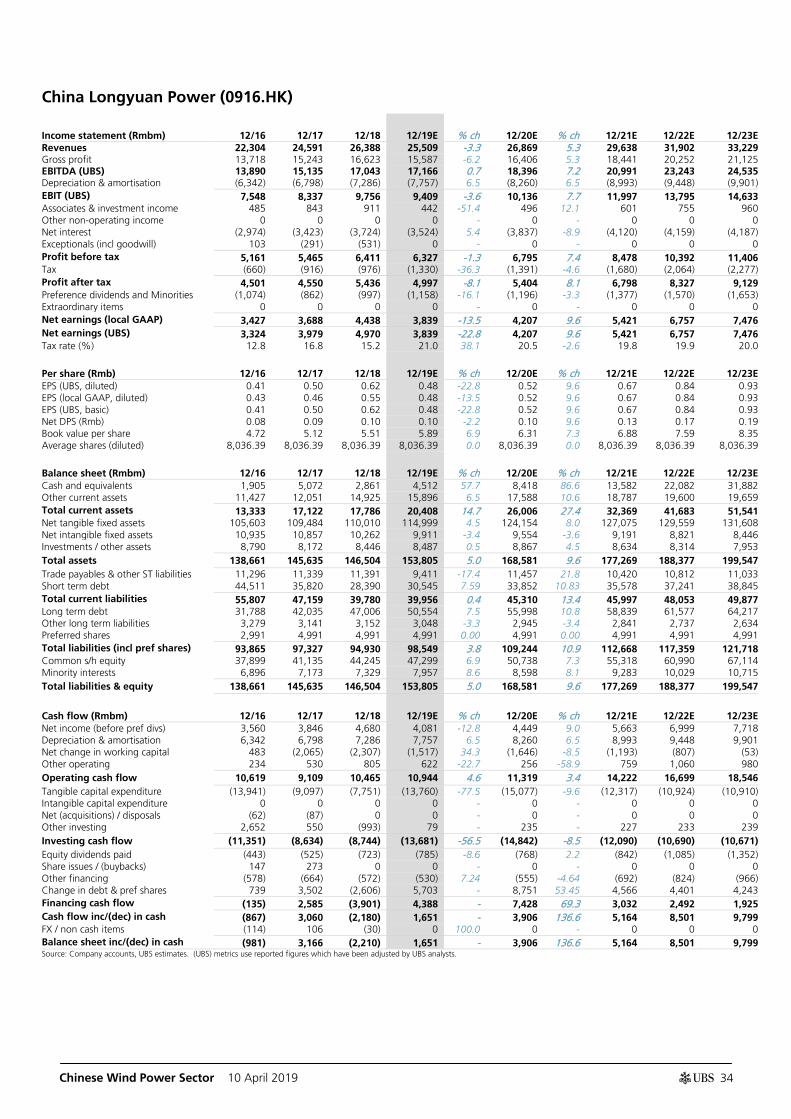

Taking a break; downgrade from Buy to Neutral We downgrade Longyuan from Buy to Neutral with a new price target of HK$6.00. We are cutting our 2019-21 earnings forecasts significantly to reflect the 1) FY18 earnings miss, 2) reduced utilisation hours assumption from 2,200 to 2,000, and 3) longer receivable days and weaker free cash flows. This makes our current forecasts about 20% below consensus. Trading at around 0.7x forward P/BV at 8.5% ROE, we believe investors have largely priced in the lacklustre outlook. For the shares to re-rate, we believe it may happen after the rush installation programme when utilisation, cash flows, and balance sheets recover.

Raised capacity expansion target after two years of subdued growth Longyuan has substantially increased its capacity addition target to 1.2GW and 1.8GW of new onshore wind farms for 2019 and 2020, respectively, compared with around 0.4GW of additions in 2017-18 p.a. The majority of these projects are located in southern China, but we think curtailment could still exacerbate as this may crowd out the demand from importing renewable powers from other regions.

What are the catalysts ahead? We believe shares could range trade for a while as balance sheets, earnings, and cash flows all remain under pressure. We believe the upside catalysts would be 1) subsidy receivables would finally be eased with a sustainable, new source of financing; 2) reduced capacity expansion; and 3) better utilisation hours.

Valuation: downgrade to Neutral; lower price target from HK$8.70 to HK$6.00 We base our price target on a DCF valuation, assuming 7.7% WACC, 7.4% terminal ROIC, and 3.0% terminal growth. Our price target implies 10x 2019E PE and 0.8x 2019E P/BV, similar to the level in the last rush installation cycle in 2015-16.

Equities

China

Electric Utilities

12-month rating Neutral Prior: Buy

12m price target HK$6.00

Prior: HK$8.70

Price HK$5.47

RIC: 0916.HK BBG: 916 HK

Trading data and key metrics 52-wk range HK$7.76-5.14

Market cap. HK$44.0bn/US$5.60bn

Shares o/s 8,036m (ORD)

Free float 93%

Avg. daily volume ('000) 12,357

Avg. daily value (m) HK$71.1

Common s/h equity (12/19E) Rmb47.3bn

P/BV (12/19E) 0.8x

Net debt / EBITDA (12/19E) 4.8x

EPS (UBS, diluted) (Rmb) From To % ch Cons.

12/19E 0.80 0.48 -40 0.62 12/20E 0.88 0.52 -41 0.69 12/21E 0.97 0.67 -30 0.75

Ken Liu Analyst

[email protected] +852-2971 7516

Abigail Sun Analyst

S1460518040002 [email protected]

+86-213-866 8637

Simon Powell Analyst

[email protected] +852-2971 7772

Highlights (Rmbm) 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E Revenues 22,304 24,591 26,388 25,509 26,869 29,638 31,902 33,229 EBIT (UBS) 7,548 8,337 9,756 9,409 10,136 11,997 13,795 14,633 Net earnings (UBS) 3,324 3,979 4,970 3,839 4,207 5,421 6,757 7,476 EPS (UBS, diluted) (Rmb) 0.41 0.50 0.62 0.48 0.52 0.67 0.84 0.93 DPS (Rmb) 0.08 0.09 0.10 0.10 0.10 0.13 0.17 0.19 Net (debt) / cash (77,385) (77,775) (77,526) (81,578) (86,424) (85,826) (81,727) (76,170)

Profitability/valuation 12/16 12/17 12/18 12/19E 12/20E 12/21E 12/22E 12/23E EBIT margin % 33.8 33.9 37.0 36.9 37.7 40.5 43.2 44.0 ROIC (EBIT) % 6.8 7.1 8.1 7.5 7.5 8.5 9.5 10.0 EV/EBITDA (core) x 8.5 7.8 7.2 6.8 6.7 6.0 5.5 5.2 P/E (UBS, diluted) x 12.0 10.5 8.5 9.8 8.9 6.9 5.6 5.0 Equity FCF (UBS) yield % (7.9) 0.0 6.2 (7.5) (10.0) 5.1 15.3 20.3 Net dividend yield % 1.7 1.8 1.9 2.0 2.2 2.9 3.6 4.0 Source: Company accounts, Thomson Reuters, UBS estimates. Metrics marked as (UBS) have had analyst adjustments applied. Valuations: based on an average share price that year, (E): based on a share price of HK$5.47 on 09 Apr 2019 18:34 HKT

Chinese Wind Power Sector 10 April 2019

30

China Longyuan Power Neutral (Price target HK$6.00)

CO1 P2

UBS Research THESIS MAP a guide to our thinking and what's where in this report

PIVOTAL QUESTIONS Q: Will wind power installation volume surge in 2019/20?

Yes. We think wind power installation could surge significantly in 2019/2020 ahead of the subsidy cancellation by end-2020. We forecast 30/32GW wind power connection and 31GW/33GW wind power installation in 2019/20.

more

Q: Will curtailment continue to ease or become worse?

Worse. We believe the glut of new wind farm supply is likely to increase the pressure for the grid to absorb the renewable power. Utilisation is likely to be suppressed in 2019/20, which would be bad for earnings. We expect curtailment ratio to go back to the 2016 level of around 15%.

more

Q: Can wind farm operators speed up the collection of subsidy receivables?

Unlikely. The rush installation for new wind farms in 2019/20 will likely exacerbate the subsidy deficits. We expect balance sheet and cash flows for wind farm operators to further deteriorate. We think subsidy receivable days may increase from one year or eighteen months to almost two years.

more

UBS VIEW We believe the operating environment for Longyuan will significantly worsen in 2019/20 as most companies rush ahead to install new wind projects. We believe it will suffer from 1) reduced earnings as curtailment will likely worsen; 2) deteriorating cash flow with larger subsidy deficit and increased capex; and 3) increased gearing.

EVIDENCE 1) Most managements of wind farm operators have increased their guidance for expansion plans in 2019 and 2020; and 2) our renewable subsidy funds calculation shows that deficits will escalate in the next two years as capacity expansion is accelerating.

WHAT'S PRICED IN? Trading at around 0.7x forward P/BV at 8.5% ROE, we believe investors have largely priced in the lacklustre outlook. For shares to re-rate, we believe it may happen after the rush installation programme when utilisation, cash flows, and balance sheets recover.

UPSIDE / DOWNSIDE SPECTRUM

Value drivers 2019E

Onshore wind farm utilization hour

Subsidy receivable days Average finance costs

HK$7.00 upside 2,100 500 days 5.0% HK$6.00 base 2,000 546 days 5.3% HK$4.50 downside 1,900 600 days 5.6% Source: UBS estimates

more

COMPANY DESCRIPTION China Longyuan is the largest wind power developer and operator in China and one of the largest wind power operators in the world. more

Ken Liu, Analyst, [email protected], +852-2971 7516

Chinese Wind Power Sector 10 April 2019

31

China Longyuan Power UBS Research CO1 UD

UPSIDE / DOWNSIDE SPECTRUM return

Value drivers 2019E

Onshore wind farm utilization hour

Subsidy receivable days Average finance costs

HK$7.00 upside 2,100 500 days 5.0% HK$6.00 base 2,000 546 days 5.3% HK$4.50 downside 1,900 600 days 5.6% Source: UBS estimates

Longyuan is trading at HK$5.47 (as of 9 April)

Risk to the current share price is skewed 1.6:1 to the upside

Longyuan is trading at HK$5.47 (as of 9 April).

Upside (HK$7.00): In our upside-case scenario, we assume better utilisation hours of 2,100 from 2019E onwards. In addition, we assume subsidy receivable days just increase from 476 days in 2018 to 500 days. We also factor in lower interest costs of 5.0%. In this case, we derive a valuation of HK$7.00 per share, implying 1.0x 2019E P/BV.

Base (HK$6.00): In our base case, we expect utilization hours to decline to 2,000 hours in 2019, with subsidy receivable days increasing by 80 days to 546 days. We assume interest rate will maintain flattish at 5.3%.

Our price target is based on a DCF methodology and implies 0.9x 2019E P/BV.

Downside (HK$4.50): In our downside-case scenario, we assume the rush installation could lead to a larger decline in utilization hours to 1,900. We also assume subsidy receivable days will surge to 600 days. In addition, we factor in higher interest costs given the company's worse financial situation. In this case, we derive a valuation of HK$4.50 per share, implying 0.7x 2019E P/BV.

Chinese Wind Power Sector 10 April 2019

32

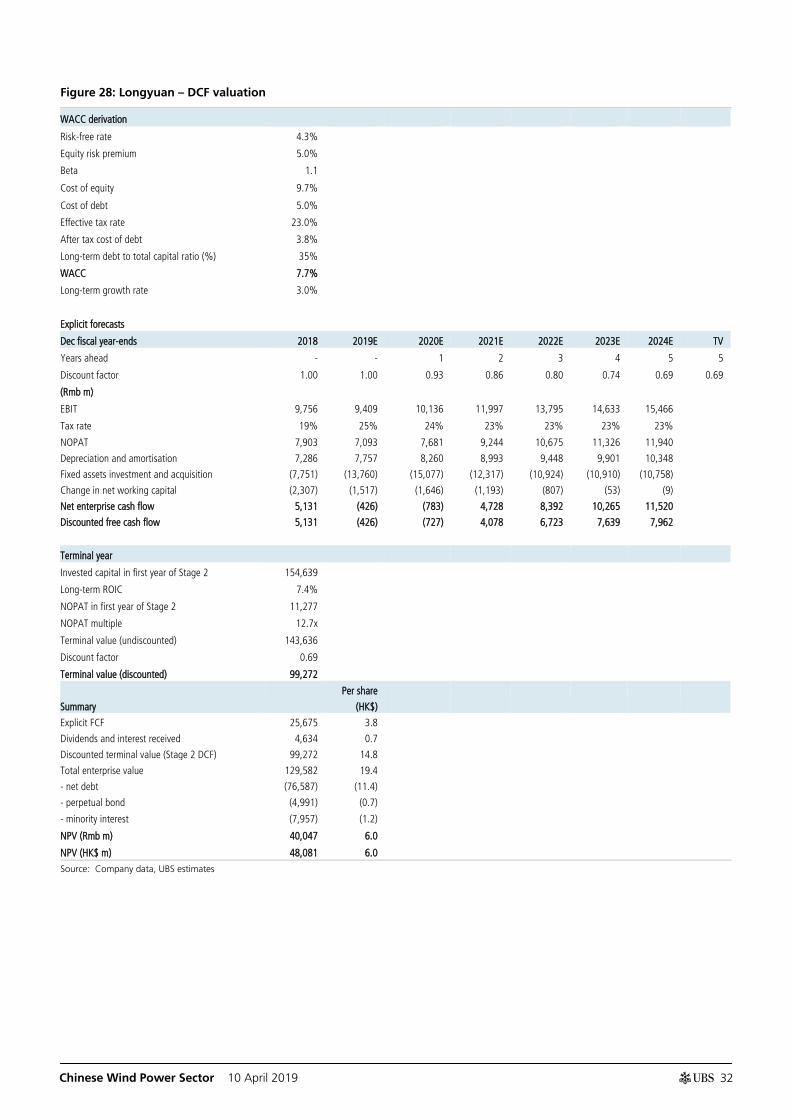

Figure 28: Longyuan – DCF valuation

WACC derivation

Risk-free rate 4.3%

Equity risk premium 5.0%

Beta 1.1

Cost of equity 9.7%

Cost of debt 5.0%

Effective tax rate 23.0%

After tax cost of debt 3.8%

Long-term debt to total capital ratio (%) 35%

WACC 7.7%

Long-term growth rate 3.0%

Explicit forecasts

Dec fiscal year-ends 2018 2019E 2020E 2021E 2022E 2023E 2024E TV

Years ahead - - 1 2 3 4 5 5

Discount factor 1.00 1.00 0.93 0.86 0.80 0.74 0.69 0.69

(Rmb m)

EBIT 9,756 9,409 10,136 11,997 13,795 14,633 15,466

Tax rate 19% 25% 24% 23% 23% 23% 23%

NOPAT 7,903 7,093 7,681 9,244 10,675 11,326 11,940

Depreciation and amortisation 7,286 7,757 8,260 8,993 9,448 9,901 10,348

Fixed assets investment and acquisition (7,751) (13,760) (15,077) (12,317) (10,924) (10,910) (10,758)

Change in net working capital (2,307) (1,517) (1,646) (1,193) (807) (53) (9)

Net enterprise cash flow 5,131 (426) (783) 4,728 8,392 10,265 11,520

Discounted free cash flow 5,131 (426) (727) 4,078 6,723 7,639 7,962

Terminal year

Invested capital in first year of Stage 2 154,639

Long-term ROIC 7.4%

NOPAT in first year of Stage 2 11,277

NOPAT multiple 12.7x

Terminal value (undiscounted) 143,636

Discount factor 0.69

Terminal value (discounted) 99,272

Summary

Per share

(HK$)

Explicit FCF 25,675 3.8

Dividends and interest received 4,634 0.7

Discounted terminal value (Stage 2 DCF) 99,272 14.8

Total enterprise value 129,582 19.4

- net debt (76,587) (11.4)

- perpetual bond (4,991) (0.7)

- minority interest (7,957) (1.2)

NPV (Rmb m) 40,047 6.0

NPV (HK$ m) 48,081 6.0

Source: Company data, UBS estimates

Chinese Wind Power Sector 10 April 2019

33

China Longyuan Power UBS Research CO1 Co des

COMPANY DESCRIPTION return

China Longyuan is the largest wind power developer and operator in China and one of the largest wind power operators in the world. In most provinces of China that have significant wind resources, Longyuan is the market leader. The company also owns minority stakes in two coal-fired power plants.

Industry outlook

The wind power industry in China may face another round of rush installations in 2019/20 ahead of the subsidy cancellation. We expect overall wind power capacity additions to surge to 30/32GW in 2019/20E. We believe that the operating environment for wind farm operators will significantly worsen in 2019/20 as most companies rush ahead to install new wind projects. We believe they will suffer from 1) reduced earnings as curtailment will likely worsen; 2) deteriorating cash flow with larger subsidy deficit and increased capex; and 3) increased gearing.

NPV by segment – 2019E (%)

Source: Company data, UBS estimates

Net profit by product segment

Rmb m 2016 2017 2018 2019E 2020E

Wind 3,067 3,877 4,413 3,746 4,117

Coal power and others 257 103 42 93 90

Total 3,324 3,979 4,455 3,839 4,207

Source: Company data, UBS estimates

Wind 89%

Coal 11%

Chinese Wind Power Sector 10 April 2019

34

China Longyuan Power (0916.HK)