Embed Size (px)

Citation preview

China and India – Outlook and Implicationsfor the Global Automotive Industry

Ashvin ChotaiDirector, Asian Automotive Industry Research

2Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Asian Auto Industry: Key Areas of Industry Attention in the Last Decade

1995/1996: Growth in Japan,ASEAN and India

1997/1998: ASEAN and Korean slump

1999: Post crisis recovery and restructuring. Foreign companies start taking control in ASEAN

2000: Nissan and Mitsubishi restructuring

2001: ASEAN Integration and September 11 Events

2002: September 11th impact. Start of China Boom GM takes over Daewoo, starts revival

2003: China Boom - concerns over policy and capacitySince 2004: China continues to boom ... changing dynamics

Asian OEMs dominating global markets.Start of a boom in India ?

3Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Asian Automotive Industry: Key Highlights and Topics of Debate: 2006/2007

• How big will China become?– Winners and Losers … Foreign Brands vs Chinese Brands

• Will India be the next China?– What is behind the rising level of interest in India– What is Tata’s “1lakh rupee car”? Is it for real?– Potential and Obstacles to Growth ?– Winners and Losers

• How rapidly will Chinese and Indian exports grow?– Can they make the same impact as Japanese and Korean brands ?

• Resurgence in Japanese Domestic Production– Strong exports encouraging capacity expansion for first time since early

1990s– Japan Production Surpassed U.S. production in 2006– Global production by Japanese brands estimated at 22.3 million in 2006

• Korean Industry Hit by Strong Currency and Strikes– Overseas Expansion Will Accelerate … Limited Growth in South Korea

• ASEAN Rapidly Losing Ground to India and China– Mini slump in 2006 …Mixed Outlook for 2007

4Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Presentation Outline

• Overview– OEM financial comparison– Asian developments in a global perspective

• Focus on China and India– Sales, exports and production outlook– Product and segmentation trends– Key challenges / obstacles for exporters from China and India

Chinese brands and their global ambitionsGlobal OEM export plans from India

– Key players and performance outlook• Developments in Asian Medium and Heavy Truck Market

– Focus on China and India• Global Implications

5Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Japanese Big 3 Accounted for ~84% of Global Industry Level Operating Profits Last Year

-20-15-10-505

10152025

Toyo

taH

onda

Nis

san

Maz

daM

itsub

ishi

Suzu

kiD

aiha

tsu

GM

Ford

BM

W

DC

XVW

Ren

ault

PSA

Fiat

Hyu

ndai

Kia

Bill

ion

US$

Operating income excluding special itemsFor Japanese companies: Fiscal year ending March 2007. Exchange rate of 1US$ =116 YenFor U.S. and European companies: Calendar year 2006. Exchange rate of 1 Euro = US$1.3

Combined operating profits of Toyota, Honda and Nissan were US$ 33.3 billion

Operating ProfitsJapanese OEMS: $36.7 bnEuropean OEMs: $24.4 bnU.S. OEMs: Lost $22.7 bnKorean OEMs: $1.2bn

Operating Profits Before Special items: Total of Top 17 OEMs: $39.6 bn

6Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

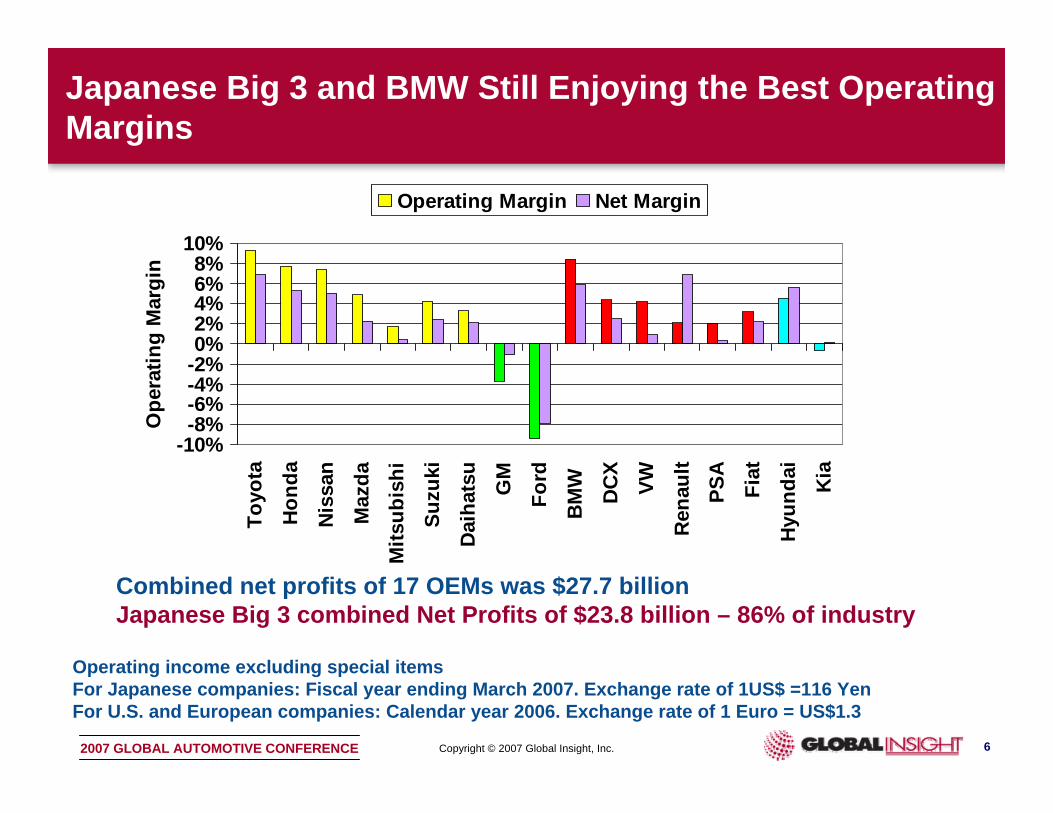

Japanese Big 3 and BMW Still Enjoying the Best Operating Margins

Operating income excluding special itemsFor Japanese companies: Fiscal year ending March 2007. Exchange rate of 1US$ =116 YenFor U.S. and European companies: Calendar year 2006. Exchange rate of 1 Euro = US$1.3

-10%-8%-6%-4%-2%0%2%4%6%8%

10%To

yota

Hon

da

Nis

san

Maz

daM

itsub

ishi

Suzu

ki

Dai

hats

u

GM

Ford

BM

W

DC

X

VW

Ren

ault

PSA

Fiat

Hyu

ndai

Kia

Ope

ratin

g M

argi

n

Operating Margin Net Margin

Combined net profits of 17 OEMs was $27.7 billionJapanese Big 3 combined Net Profits of $23.8 billion – 86% of industry

7Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

2006: All Vehicles Sales of 68.7 Million Units …Global Growth of 2.57 Million Units … China Again the Main Growth Engine

Strongest Performers

Global 2.57m units, Asian 1.2m units…China:1.42m units

0 200 400 600 800 1000 1200 1400 1600

SAUDI ARABIA

COLOMBIA

ARGENTINA

IRAN

SOUTH AFRICA

ITALY

UKRAINE

VENEZUELA

GERMANY

BRAZIL

INDIA

RUSSIA

CHINA

Change in Vehicle Sales (Thousand units)

2006 Sales Growth/Declines By Country

Most significant declines in U.S., Indonesia and Taiwan

-400 -300 -200 -100 0

UNITED STATES

INDONESIA

TAIWAN

JAPAN

UNITED KINGDOM

TURKEY

MALAYSIA

FRANCE

AUSTRALIA

THAILAND

HUNGARY

PORTUGAL

ECUADOR

Change in Vehicle Sales (Thousand units)

Weakest Performers

8Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

2006: Production Growth of 2.9 Million Units in Asia …China Again the Main Growth Engine

Strongest Performers

Global 2.9m units, Asian 2.33m units…China:1.54m units

0 400 800 1200 1600

BRAZILGERMANY

SOUTH AFRICATHAILANDUKRAINE

COLOMBIAIRAN

SLOVAKIAPOLANDTURKEY

ARGENTINASOUTH KOREA

RUSSIAITALY

CZECH REPUBLICINDIA

MEXICOJAPANCHINA

Change in Vehicle Production (Thousand units)

Most significant declines in U.S., France, Indonesia and UK

-800 -600 -400 -200 0

UNITED STATESFRANCEINDONESIAUKTAIWANCANADAAUSTRALIAMALAYSIASLOVENIANETHERLANDSPHILIPPINESSERBIASWEDENCHILE

Change in Vehicle Production (Thousand units)

2006 Production Growth/Declines By CountryWeakest Performers

9Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Market: Key Trends

• Changing customer mix– Traditionally SOEs, government, taxi firms– Then private buyers in big cities– Motorisation now spreading to small cities– Ageing population will become a more dominant theme after 2010

• Government encouraging independent brands– Encouraging supply development in budget segments– Further intensification in price competition– Chinese brands accelerating motorisation rather than taking significant share

from foreign JVs• Market and consumer dynamics entering first stage of maturity

– Development of used car market now gathering momentum– Brand experience and better brands consciousness in Tier 1/2 cities

• Energy and environmental concerns … fuel prices still low– Limited impact on short term demand– Fuel consumption and environmental factors will constrain long term growth in

motorisation– Fuel efficiency standards will encourage move to smaller cars

• Parallel production of more than one generation of same model – Repositioning of older models to lower price point or different consumer

segment

10Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China in Regions

Yantai

Chongqing

MacauHong Kong

Xining

Chengdu Wuhan

Guiyang

Tianjin

Hefei

Nanjing Shanghai

Ha ng

z ho u

Nanchang

Fuzhou

Guangzhou

Nanning

S h en y an g

Changchun

Harbin

Beijing

Guangdong

Fuj i a

n

Taiwan

Sichuan

Hubei

Hunan Jiangxi

H eilon gjiang

Inner Mongolia

Heb

ei

Henan Jiangsu

Anhui

Guangxi

Guizhou

Jilin

Gansu

Shaanxi

Shanxi

Qinghai

Xinjiang

Tibet

N ingx ia

Liaon in

g

Zhe

jian

g

Yunnan

Haikou

Hainan

11Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

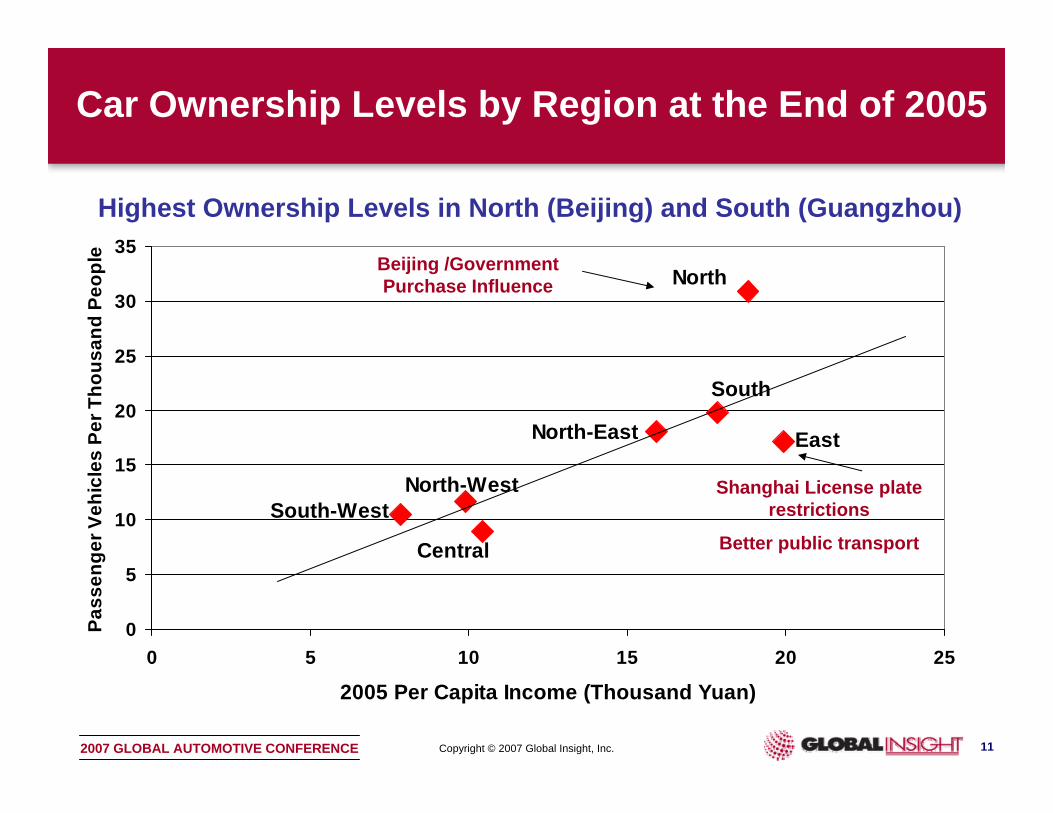

Car Ownership Levels by Region at the End of 2005

0

5

10

15

20

25

30

35

0 5 10 15 20 25

2005 Per Capita Income (Thousand Yuan)

Pass

enge

r Veh

icle

s Pe

r Tho

usan

d Pe

ople

North

South

East

North-West

North-East

South-West

Central

Highest Ownership Levels in North (Beijing) and South (Guangzhou)

Beijing /Government Purchase Influence

Shanghai License plate restrictions

Better public transport

12Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

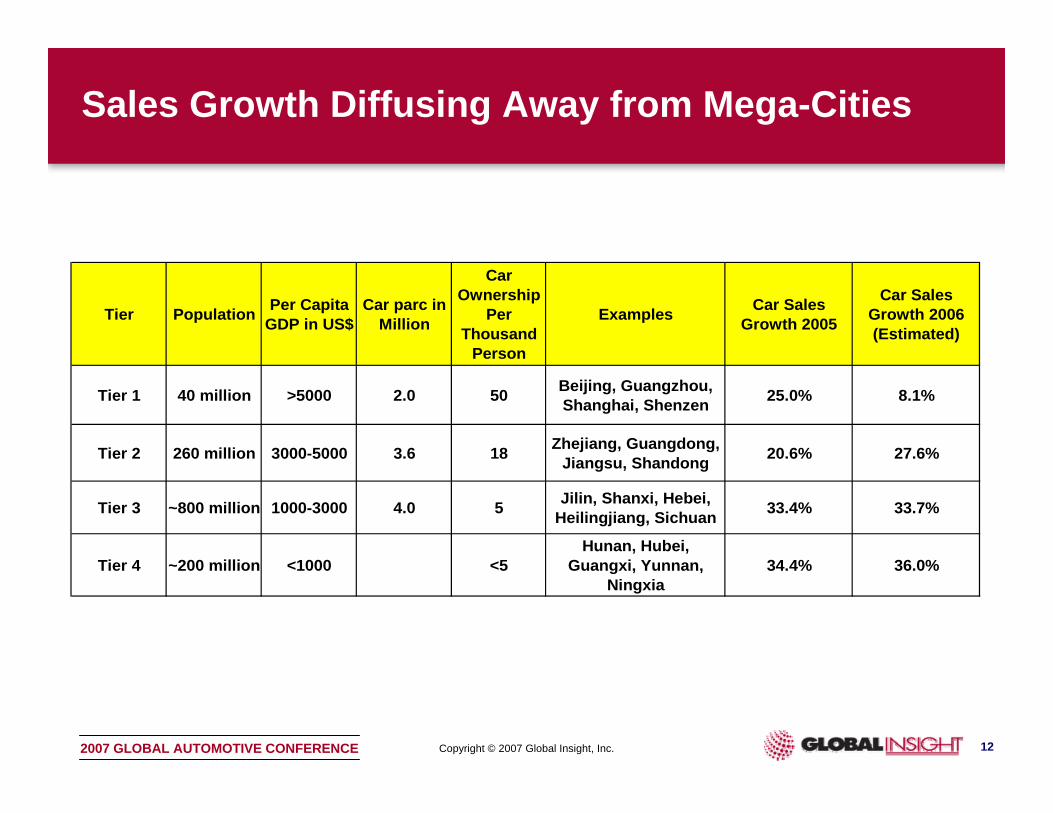

Sales Growth Diffusing Away from Mega-Cities

Tier Population Per Capita GDP in US$

Car parc in Million

Car Ownership

Per Thousand

Person

Examples Car Sales Growth 2005

Car Sales Growth 2006 (Estimated)

Tier 1 40 million >5000 2.0 50 Beijing, Guangzhou, Shanghai, Shenzen 25.0% 8.1%

Tier 2 260 million 3000-5000 3.6 18 Zhejiang, Guangdong, Jiangsu, Shandong 20.6% 27.6%

Tier 3 ~800 million 1000-3000 4.0 5 Jilin, Shanxi, Hebei, Heilingjiang, Sichuan 33.4% 33.7%

Tier 4 ~200 million <1000 <5Hunan, Hubei,

Guangxi, Yunnan, Ningxia

34.4% 36.0%

13Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Production Will Overtake Japan and U.S. by 2010/2011 … But Profits Under Pressure

0

2000

4000

6000

8000

10000

12000

1998

2000

2002

2004

2006

2008

2010

2012

2014

Prod

uctio

n (T

hous

and

Uni

ts)

Car

LCV

Truck and Bus

Cars 9.1 million, LCV 3.5 million,HCV : 843K

Total output of $128 billion in 2005

Total 2012 Production: 13.4 million units

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Mill

ion

Uni

ts

Incremental Year-Over Year Growth

• Rapid spread of motorisation in second and third tier cities from 2005/2006

• Aggressive product and market strategies by domestic brands

• Fuel consumption and environment will be major obstacles

CAGR 2001-2006: 24.6%

CAGR 2007-2012: 9.8%

14Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Consumers Still Have Strong Appetite for Cars …But What Could Go Wrong?• Economic hard landing

– Focus on controlling investments and exports– Long term solution – boost domestic consumption– Government unlikely to adopt anti-consumption policies

• Social or political backlash– Regional disparities– Can the government achieve more balanced development

• Environmental disaster– Loss of confidence and impact on FDI– Would trigger clampdown on industrial growth

• Oil supply squeeze– Pump prices will need to be hiked up more aggressively– Chinese oil companies investing to secure oil supplies

• Banking crisis– Lower probability now as banks are better capitalised

• Trade backlash … especially from U.S.– But U.S. multinationals are the major exporters– Will force a more rapid yuan appreciation

15Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China: Total Vehicle Exports of 343K Units in 2006 …Small Trucks Account for the Bulk of Exports

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006

Thou

sand

s U

nits Others (Mainly Chassis)

Buses

Trucks

Passenger Cars

2000: US$ 200.8 million

2005: US$ 1.58 billion

2006: US$ 3.13 billionExcludes engines, components and motorcycles

Average price of exported passenger car $7400

0

10

20

30

40

50

60

CH

ERY

HA

RB

INH

AFE

I

GR

EAT

WA

LL

HO

ND

A

CH

AN

GA

N

FAW

GEE

LY

JIA

NG

LIN

G

AN

HU

IJI

AN

GH

UA

I

CH

AN

GH

E

Thou

sand

s U

nits

Top Exporter in 20062000: US$ 2 billion

2005: US$ 16.8 billion (13% of output) All Automotive Exports including vehicles, engines, components and motorcycles

Around 1,175 organisations exported vehicles in 2006Over 669 of these exported less than 10 units204 companies exported just 1 unit

16Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Exports: Still Significant Obstacles …Growth Unlikely to be Spectacular

Foreign OEMs• Restrictions on foreign ownership of assembly ventures

– Does not encourage global OEMs to hike vehicle exports– Complicated to integrate China operations into regional and global networks under current

ownership structure– India, Thailand, Mexico, Brazil and S. Africa are attractive alternatives with fewer restrictions– Current focus of exports is on components

Chinese OEMs• Chinese brands still have major hurdles to overcome

– Upstream: Product quality and refinements– Regulatory: Homologation, Safety and Emissions– Downstream: Branding, Distribution Network, After-Sales, Warranties

• So far … an opportunistic approach by Chinese brands– Deals with inexperienced operators …unable to grapple with all the product, regulatory, brand-

building issues– Need a coherent strategy and greater direct OEM presence in key export regions– International mindset

• Alliances and rebadging relationships will provide learning experience and reduce risks e.g.

– Chery and Chrysler Chery and Fiat

17Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Chinese Assemblers Striving to Develop Independent Development Capability: Key Development Stages

Globally Competitive Development Capability &

Product Portfolio and Renewal

Copying Generally use of many of the original suppliers of copied models

Reverse Engineering and Adapting of China

Use of Local Suppliers to commodity partsRelationship with foreign suppliers for critical parts

Use of Design Houses to Develop Own Platform and Powertrain Development

E.g. AVL, Ricardo. Lotus, Magna,Tier 1 Suppliers

Use of Design Houses for Interior and Exterior Styling e.g. Pininfarina, Bertone, IDEA, Guigaro

Powertrain generally outsourced

In-house Capability to Manage Design and

Development of All Core Parts of the Vehicle

Build Up Low Cost Development Capability

Geely

Chery

Great Wall

ChanganBrilliance

Changfeng Zhongxing

Many players still at this stage

18Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Chinese Brands: Examples of Other Development Strategies

Acquisition of foreign companies to accelerate development

SAIC purchase of Rover and Ssangyong

Nanjing acquisition of some Rover technology

Rely on foreign JV partner to transfer technology

FAW obtaining access to VW, Toyota, Mazda platform

19Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Exports: Commercial Vehicles Dominate ….Passenger Car Export Take-off from 2009/2010

0

200

400

600

800

1000

1200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Thou

sand

s

Others (Mainly Chassis)BusesTrucksPassenger Cars

Total Exports: 343K in 2006 ….Around 1 Million in 2011

20Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

0 200 400 600 800 1000 1200

DAIMLERCHRYSLER

MAZDASUZUKI

FORD

PSANISSAN

HONDAHYUNDAI

SGM WULINGGM

TOYOTA

VW GROUP

Increase in Vehicle Production (000 units) 2012 vs 2007

2006 Production

Production Growth 2007-2012

Sino-Foreign JVs: LV Production Increase of 2.6 Million Units* in the Period 2007-2012

Growth Prospects by Company: 2007-2012 Sino-Foreign JVs

Based on Ownership of Technology * SGM Wulin counted under Domestic Brand Total

21Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

0 200 400 600 800 1000

BYD AUTONANJING AUTOMOTIVE

CHINA BRILLIANCELIFAN GROUP

AVICHINABEIJING AUTOMOTIVE

DONGFENGANHUI JIANGHUAI

SGM-WULINSAIC

GREAT WALLGEELY

FAWCHERY

CHANGAN

Increase in Vehicle Production (000 units) 2012 vs 2007

2006 Production

Production Growth 2007-2012

Domestic Brands LV Production Increase of 3.3 Million Units* in the Period 2007-2012

Growth Prospects by Company: 2007-2012 Domestic Brands

Based on Ownership of Technology * SGM Wulin counted under Domestic Brand Total

All Light Vehicles < 6 Tonnes GVW

22Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Component Industry: Opportunities and Challenges for Global Suppliers

• OE competitive dynamics changing rapidly – Unique mix of OE customer base in China– U.S., European, Japanese, Korean and Chinese platforms in production– Challenge is to have diversified customer base and leverage regionally and

globally• Greater competition and concerns of intellectual property

– Investment by Japanese and Korean suppliers has accelerated significantly in recent years

– Tread carefully between protecting strategic technologies and maintaining good relations with jv partners and government

– Logistics Management and Tier 2/3 Supply Management are becoming key success factors

• Component trade surplus of around $8.7 billion in 2006– Trade surplus in suspension and electronic parts ….deficit in Driveline and

engine components– Surplus vs U.S. but deficit vs Japan, Korea, Germany

• Integration into regional and global supply chain– China’s role rising rapidly– Bosch, Delphi, Visteon, Borg-Warner, Conti-Teves, Federal Mogul, PPG,

Goodyear all have their Asia-Pacific HQ in Shanghai

23Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Revival of Interest in India

• Strong economic performance– Real GDP growth of >8% for four consecutive years

• After years of underperformance …healthy signs that vehicle market growth is accelerating

• Many companies have made investments in China and now regard India as the next natural step

– Also reflects some disillusionment with China• Greater focus on fuel efficiency and small cars

Bottom line• India will not match China’s auto industry growth rates

– Only companies with strong small car product line will achieve significant scale • India will be the second biggest growth market on 5 and 10 year horizons• Greater transparency and level playing field

– More attractive to establish export strategy and integration with global supply chain

• Offers significant scope for leveraging on low cost component production and engineering services for global operations

24Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Tata Plans to Target 2-Wheeler Owners with its Microcar (1 Lakh Car) …Other OEMs Now Beginning to Take Note

• Styling work completed … Prototypes being tested– Rear engine 4-5 seat car with 600cc

Euro IV compliant 30hp engine– Planning a diesel version

• Innovative production concept and supplier relationship– Mother plant in West Bengal and

satellite assembly locations across India

• Target price of base version expected to be $2500 (125,000 rupees) … about half the price of the Maruti Alto

• Attractive financing will play a key role in supporting sales– Tata expanding its vehicle finance

network in rural areas

Tata Microcar will targetbuyers of Two-Wheelers

Tata targeting 1 million units

25Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

India Gaining Popularity as an Attractive Export Base for Global OEMs

• Few restrictions on foreign ownership of assembly ventures– Full management control– Easier to integrate into global strategy and supply chain

• India gradually positioning itself as global production hub for small cars

• Several global OEMs planning large export operations– Hyundai already the largest exporter … raising exports levels– Suzuki will ramp up exports post 2009– GM will commence Matiz/Spark exports from 2009– Renault and Nissan have ambitious export plans– Toyota and Honda most likely export small cars post 2010

• Poor infrastructure and logistics costs are main obstacles

26Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

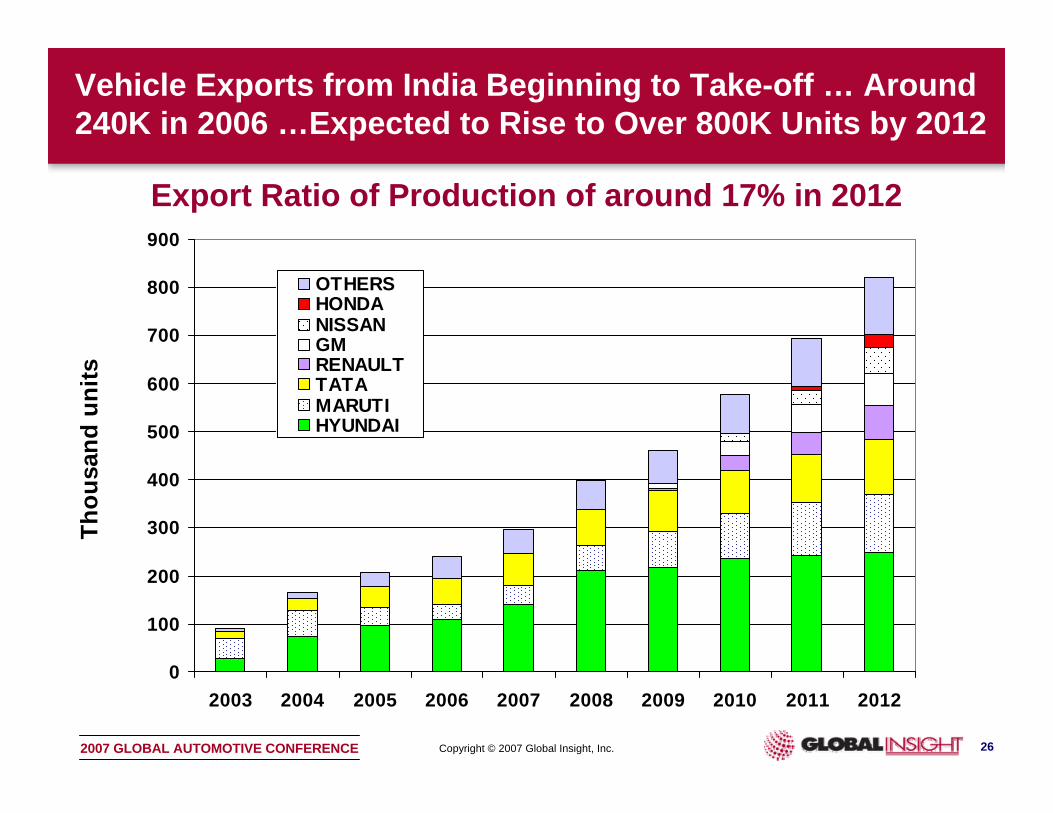

Vehicle Exports from India Beginning to Take-off … Around 240K in 2006 …Expected to Rise to Over 800K Units by 2012

0

100

200

300

400

500

600

700

800

900

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Thou

sand

uni

ts

OTHERSHONDANISSANGMRENAULTTATAMARUTIHYUNDAI

Export Ratio of Production of around 17% in 2012

27Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

0 200 400 600 800 1000 1200 1400

FIAT GROUPFORD

VW GROUPHONDA

TOYOTARENAULT

MAHINDRAGM

HYUNDAISUZUKI

TATA

Production (000 units)

2006 Production Production Growth 2006-2012

Light Vehicle Production Increase of 2.7 million units in the period 2006-2012 … Tata “1 lakh Car” Provides a Major Boost Post 2009

India: Small Car Makers Best Placed for Growth

Logan plus its derivatives

Microcar, Ace

New Plant, More Export Production

New Plant, Diesel Engines,SX4 sedan, Zen Estillo, New Wagon R

New Plant, Add Aveo and SparkIngenio in 2008

Plans to Launch Small Car Delayed to 2009

New plant and Small Car in 2010

28Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Indian Auto Industry: Opportunities and Challenges for Global Suppliers

• Significant scale disadvantage versus China– $11 billion output in 2005-2006 vs $57 billion in China in 2005– Major reason for cost disadvantage in many component areas– Strong growth in component imports from China

• More attractive for engineering and development activities• More stable OE competitive dynamics …but small cars mean thin margins

– Consolidated industry dominated by Maruti, Tata and Hyundai– Other companies now raising their profile– Other OEMs to watch … GM, Honda, Renault-Nissan

• Challenge is to scale up for global sourcing demands– $4.4 billion (component industry) investment in the last fiscal year

• Global Tier 1 suppliers now accelerating expansion plans– Bosch, Delphi, Visteon have significant presence– Japanese suppliers have weak direct presence– A competitive engineering and development base

• Indian suppliers are becoming global forces– Bharat Forge, Taco

29Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

394617

865999 1006

11781320

741

0300600900

12001500

'00 '02 '05 '06 '07 '09 '12 '17

Asia (excl. JPN) Sales (000 units)Japan and Korea:• Legislation

Driven• Cyclical

Medium and Heavy Trucks: Key Developments

• Technically and economically outdated

• “Crude” Trucks, operated by owner-drivers

• Focus on Medium Trucks

• New generation, technically and commercially upgraded

• Professional fleet usage• Life-cycle costing• High "value for money"• Focus on Heavy Trucks

New ModelsOld Models

Western OEMs “testing waters” in India and China Define Product Benchmark

85 76111

92108 98 103109

0

50

100

150

'00 '02 '05 '06 '07 '09 '12 '17

Japan Truck Sales (000 units

India and China• Infrastructure

Development

• Haulage Fleet Formation

• Tighter control on overloading

• Upgrade from farm vehicles

• Tighter Emissions

• Aggressive Product Renewal of Major OEMs

30Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China: Truck Demand Recovering Since Second Half of 2006 …Gradual Investment Slowdown

0

50

100

150

200

250

300

350

400

450

500

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Truc

k an

d B

us S

ales

(Tho

usan

d U

nits

)

Trucks6-15T GVW

Trucks >15T GVW

Medium and Large Buses

Key Trends• Overloading restriction

fuelled boom in 2004• Some scrappage

incentives• Correction in 2005 and

recovery in 2H of 2006• Strong investments and

infrastructure construction supporting demand

• Demand for large (>25t) Artic tractors especially strong

• Migration from farm vehicles supporting medium truck sales

31Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

China Heavy Truck Market Share Outlook … Fragmentation at Top End…Foreign Cab, Engine, Driveline Technology

0

100

200

300

400

500

600

700

800

2000 2004 2006 2007 2012

Prod

uctio

n (T

hous

and

units

)

DONGFENG FAWCNHTC SHAANXI AUTOMOTIVEAUMAN ANHUI JIANGHUAICHONGQING HONGYAN NORTH BENZCHENGDU WANGPAI SICHUAN HIGHWAY MACHINERYLIFAN HUALINGOTHERS NANJING AUTOMOTIVEOTHER

CNHTC and Shaanxi gaining share in heavy segment Beijing Automotive (Auman) entered in 2004

Farm truck companies (e.g. Chengdu Wangpai) entering medium truck segment

32Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

India Truck Sales: Strong Up Cycle Continuing …New Entrants Will Struggle to Build up Volumes

0

50

100

150

200

250

1996

1998

2000

2002

2004

2006

2008

2010

2012

HC

V Sa

les

(Tho

usan

d U

nits

)

Heavy Trucks

Medium Trucks

Bus

TATA

ASHOK LEYLAND

MAHINDRAEICHERSWARAJFORCE/MAN

0

100

200

300

400

500

2002

2004

2006

2008

2010

2012

2014H

CV

Prod

uctio

n (T

hous

and

units

)

Key New Players• Force Motor -- MAN: Joint Venture:

Aiming for high local content• Mahindra & Mahindra and

International: Joint Venture: Aiming for high local content

• Volvo 100% Owned Subsidiary: low volume

• DaimlerChrysler 100% Subsidiary: Very low volume

Key Trends• Infrastructure development a

major driver• Strong industrial performance• Overloading restrictions boosted

2006 performance• Less dependent on agricultural

sector and monsoons

33Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Top Six Countries Will Account for 60% of Global Production in 2012 … Major Markets for OEM Parts

-3000 0 3000 6000 9000 12000 15000

TURKEYIRAN

ITALYUK

THAILANDRUSSIAMEXICO

SPAINBRAZIL

CANADAFRANCE

S KOREAINDIA

GERMANYJAPAN

UNITED STATESCHINA

Vehicle Production (Million units)

2006 ProductionProduction Growth 2006-2012

17 Countries with production over 1m units in 2012 …will account for 90% of global production in 2012

China, Japan, Korea and India will account for nearly 40% of global

vehicle production in 2012

Including Passenger Cars And Commercial Vehicles

Global production: 69.8 in 2006 85.7 Million units in 2012 …15.9 Million Units of Growth …India and China will account for 57%

34Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

-1000 -500 0 500 1000 1500 2000 2500 3000

MITSUBISHIMAZDA

BMWSUZUKI

FIAT GROUPRENAULT

NISSANPSA

HONDA HYUNDAI

DAIMLERCHRYSLER VW GROUP FORD

GMTOYOTA

Increase in Vehicle Production (000 units)

North America South America West Europe East EuropeJapan China Rest of Asia Middle East/Africa

Total Production(Excluding Double Counting)

2006: 69 million units2012: 84.7 million units

15.6 Million Units (Net of Double Count) Increase in the Period 2006-2012 …. 10.8 Million Units in Asia

Global Production Growth Performance (2012 vs 2006)

35Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

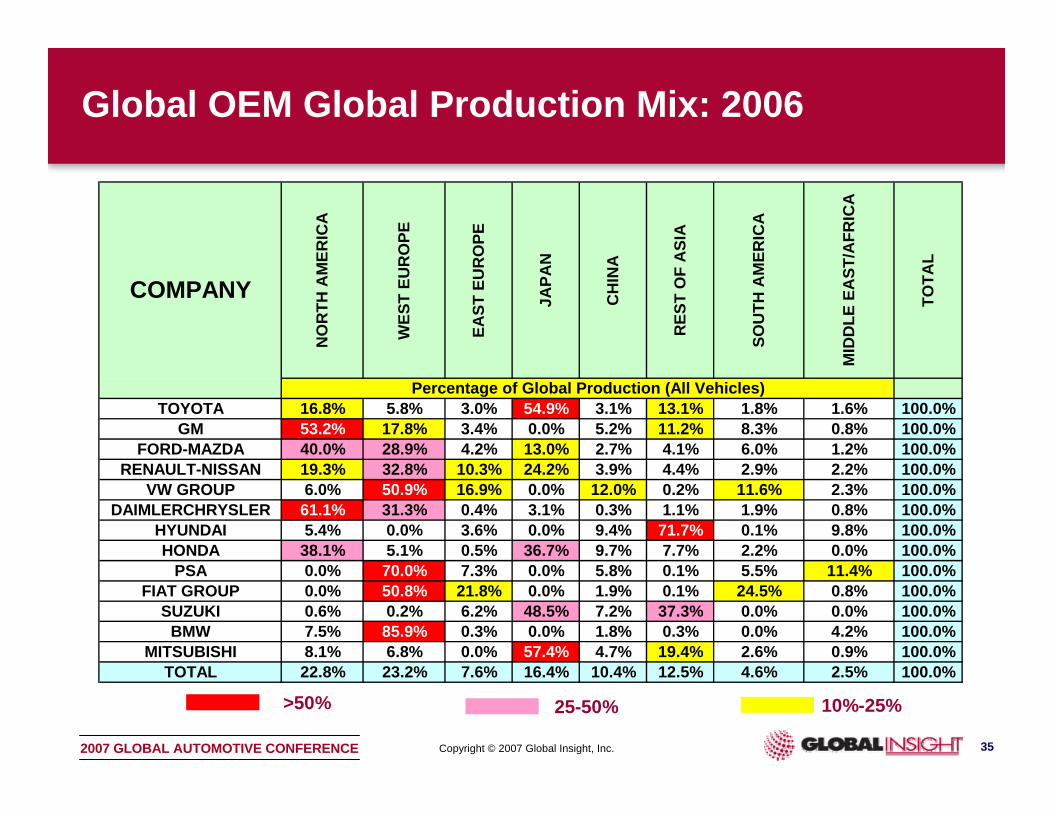

Global OEM Global Production Mix: 2006

>50% 25-50% 10%-25%

NO

RTH

AM

ERIC

A

WES

T EU

RO

PE

EAST

EU

RO

PE

JAPA

N

CH

INA

RES

T O

F A

SIA

SOU

TH A

MER

ICA

MID

DLE

EA

ST/A

FRIC

A

TOTA

L

TOYOTA 16.8% 5.8% 3.0% 54.9% 3.1% 13.1% 1.8% 1.6% 100.0%GM 53.2% 17.8% 3.4% 0.0% 5.2% 11.2% 8.3% 0.8% 100.0%

FORD-MAZDA 40.0% 28.9% 4.2% 13.0% 2.7% 4.1% 6.0% 1.2% 100.0%RENAULT-NISSAN 19.3% 32.8% 10.3% 24.2% 3.9% 4.4% 2.9% 2.2% 100.0%

VW GROUP 6.0% 50.9% 16.9% 0.0% 12.0% 0.2% 11.6% 2.3% 100.0%DAIMLERCHRYSLER 61.1% 31.3% 0.4% 3.1% 0.3% 1.1% 1.9% 0.8% 100.0%

HYUNDAI 5.4% 0.0% 3.6% 0.0% 9.4% 71.7% 0.1% 9.8% 100.0%HONDA 38.1% 5.1% 0.5% 36.7% 9.7% 7.7% 2.2% 0.0% 100.0%

PSA 0.0% 70.0% 7.3% 0.0% 5.8% 0.1% 5.5% 11.4% 100.0%FIAT GROUP 0.0% 50.8% 21.8% 0.0% 1.9% 0.1% 24.5% 0.8% 100.0%

SUZUKI 0.6% 0.2% 6.2% 48.5% 7.2% 37.3% 0.0% 0.0% 100.0%BMW 7.5% 85.9% 0.3% 0.0% 1.8% 0.3% 0.0% 4.2% 100.0%

MITSUBISHI 8.1% 6.8% 0.0% 57.4% 4.7% 19.4% 2.6% 0.9% 100.0%TOTAL 22.8% 23.2% 7.6% 16.4% 10.4% 12.5% 4.6% 2.5% 100.0%

Percentage of Global Production (All Vehicles)

COMPANY

36Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE

Global OEM Global Production Mix: 2012

>50% 25-50% 10%-25%

NO

RTH

AM

ERIC

A

WES

T EU

RO

PE

EAST

EU

RO

PE

JAPA

N

CH

INA

RES

T O

F A

SIA

SOU

TH A

MER

ICA

MID

DLE

EA

ST/A

FRIC

A

TOTA

L

TOYOTA 20.2% 5.8% 2.7% 45.0% 6.7% 15.8% 2.2% 1.5% 100.0%GM 48.6% 16.6% 4.9% 0.0% 7.0% 13.9% 8.4% 0.6% 100.0%

FORD-MAZDA 33.5% 27.8% 5.9% 11.8% 6.6% 7.4% 5.9% 1.2% 100.0%RENAULT-NISSAN 16.0% 26.3% 10.7% 19.4% 5.7% 12.7% 3.6% 5.7% 100.0%

VW GROUP 6.9% 46.5% 17.6% 0.0% 14.9% 2.4% 8.9% 2.9% 100.0%HYUNDAI 7.2% 0.0% 13.5% 0.0% 12.6% 63.1% 0.2% 3.5% 100.0%

DAIMLERCHRYSLER 53.8% 34.0% 0.4% 3.5% 2.7% 1.7% 2.1% 1.7% 100.0%HONDA 38.5% 4.1% 2.0% 30.4% 11.8% 11.1% 2.1% 0.0% 100.0%

PSA 0.0% 61.6% 13.0% 0.8% 9.6% 0.2% 6.2% 8.5% 100.0%FIAT GROUP 0.0% 48.1% 21.5% 0.0% 4.0% 1.6% 22.0% 2.9% 100.0%

SUZUKI 1.4% 0.0% 5.4% 40.7% 9.3% 43.0% 0.0% 0.2% 100.0%BMW 13.0% 79.8% 0.6% 0.0% 3.0% 0.6% 0.0% 3.0% 100.0%TATA 0.0% 0.0% 0.1% 0.0% 0.0% 99.7% 0.1% 0.2% 100.0%

TOTAL 20.0% 20.3% 8.2% 13.6% 15.7% 15.6% 4.2% 2.4% 100.0%

Percentage of Global Production (All Vehicles)

COMPANY