Embed Size (px)

Citation preview

CHERRY Discussion Paper Series CHERRY DP 12/02

Discount rate policy under the Classical Gold Standard:core versus periphery (1870s – 1914)

By

Matthias Morys

1

Discount rate policy under the Classical Gold Standard:core versus periphery (1870s – 1914)

Matthias MorysDepartment of Economics

University of [email protected]

March, 2012

AbstractDrawing on a new data set of monthly observations, this paper investigates similaritiesand differences in discount rate policy of 12 European countries under the Classical GoldStandard; it asks, in particular, whether bank rate policy followed different patterns incore and peripheral countries. Based on OLS, ordered probit and pooled estimations ofcentral bank discount rate behaviour, two main findings emerge: first, the discount ratedecisions of core countries were motivated by keeping the exchange-rate within the goldpoints. In stark contrast, the discount rate decisions of peripheral countries reflectedchanges in the domestic cover ratio. The main reason for the different behaviour was thelimited effectiveness of the discount rate tool for peripheral countries which resulted inmore frequent gold point violations. Consequently, peripheral countries relied on highreserve levels and oriented their discount rate policy towards maintaining the reservelevel. Second, interest rate decisions were influenced by Berlin and London to a similardegree, suggesting that the European branch of the Classical Gold Standard was lessLondon-centered than hitherto assumed. In establishing general patterns of discount ratepolicy, this paper aims to contribute to the wider question of monetary policy under thegold standard and the core-periphery dichotomy.

Keywords: gold standard, rules of the game, balance-of-payment adjustment,central banking

JEL classification: E4, E5, E6, F3, N13

________________________Earlier versions of this paper were presented at the AEA, EHES, EHS and IEHA meetings; at seminars in Antwerp,Berkeley, Glasgow, Leuven, NYU, Oxford, Paris, Rutgers, York; and at the EABH Young Scholars Workshop inRotterdam and the SEEMHN Annual Conference in Bucharest. I am grateful to all participants for their spiriteddiscussion and helpful suggestions, and in particular to Dion Bongaerts, Michael Bordo, Barry Eichengreen, ClemensJobst, Chris Meissner, Larry Neil, Jaime Reis, Alan Taylor and Marc Weidenmier. I owe a special thanks to thefollowing people in helping me collect the data: Ivo Maes and Arnold de Schepper (National Bank of Belgium), KathBegley (Bank of England), Alfredo Gigliobianco (Bank of Italy), Mrs Beex (De Nederlandsche Bank), all members ofthe data collection task force of the South-East European Monetary History Network, Erik Buyst, Jan Tore Kloveland,Larry Neal, Giuseppe Tattara, Anders Ogren and Marc Weidenmier. The usual disclaimer applies.

2

CHAPTER ONE INTRODUCTION

The Classical Gold Standard (1870s – 1914) has attracted the interest of economists, economic

historians and policy-makers ever since its foundation. The exchange-rate stability among most

countries of the world for some forty years was unprecedented and remained an inspiration for

policy-makers after both world wars. At the time, adherence to gold was not entirely

uncontroversial, as the international bimetallic movement of the mid-1870s to mid-1890s

demonstrates.1 But the perspective soon changed as a result of monetary instability following World

War I and high exchange-rate volatility in the 1930s; policy-makers came to idealize the pre-World

War I gold standard as a benchmark against which any international monetary system should be

measured – hence the label Classical Gold Standard.

Economists and economic historians, aware of costs and benefits of adhering to a system of

fixed exchange-rates, have tended to avoid the eulogistic tone of policy-makers; they have

contributed to the gold standard myth, however, by producing a highly stereotypical account of its

working. Some of the stereotypes have surely been overturned by more recent research. Following

Hume’s price-specie mechanism (1752), the textbook account of the gold standard had it that

physical gold was shipped between countries to settle balance-of-payments disequilibria. Recent

research, following earlier leads2, has demonstrated the importance and sophistication of foreign

exchange policy.3 In other cases, recent research has provided the empirical basis to verify or reject

some of the claims made in the older gold standard literature. This would be the case for the

discussion on the benefits of gold standard adherence which are seen in improved access to global

1 Reti, Silver and Gold: The Political Economy of International Monetary Conferences. 1867-1892 (Westport (CT),London: Greenwood, 1998).

2 Lindert, Key Currencies and Gold. 1900-1913, Princeton Studies in International Finance 24 (Princeton1969).3 Jobst, "Market Leader: The Austro-Hungarian Bank and the Making of Foreign Exchange Intervention, 1896-1913,"

European Review of Economic History 13, no. 3 (2009).

3

capital markets and reduced transaction costs with other gold standard countries.4 Yet another

strand of the recent literature has highlighted conditions crucial to the workings of the Classical

Gold Standard which had been neglected so far, such as the importance of labour mobility and

remittances in smoothing the adjustment mechanism.5

While the gold standard myth has given way to a broader empirical analysis in some

debates, in other areas it stubbornly persists. One of them is the alleged core-periphery dichotomy.

It is argued that the adjustment process to balance-of-payments disequilibria was much smoother

for the industrialised core countries of North-Western Europe as opposed to the peripheral

economies. Different authors have emphasised different factors in explaining the alleged advantages

of the core countries in the adjustment process. Drawing on the theory of optimum currency areas,

one school of thought has argued that core countries were better suited for monetary integration.6

Others have argued that central banks7 of core countries helped each other in times of crisis, but did

not help peripheral economies for the lack of self-interest.8 The more recent literature has

emphasized differences in credibility9, whereas an older school of thought highlighted the

peripheral countries’ role as debtors in the global financial system which made them vulnerable to

sudden withdrawals of funds in times of financial strain.10

4 Bordo and Rockoff, "The Gold Standard as a 'Good Housekeeping Seal of Approval'," Journal of Economic History56(1996). Lόpez-Cόrdova and Meissner, "Exchange-Rate Regimes and International Trade: Evidence from the Classical Gold Standard Era," American Economic Review 93(2003).

5 Esteves and Khoudour-Castéras, "A Fantastic Rain of Gold: European Migrants' Remittances and Balance ofPayments Adjustment During the Gold Standard Period," Journal of Economic History 69, no. 4 (2009). Khoudour-Castéras, International Adjustment During the Classical Gold Standard: The Migration Nexus, Working PaperChaire Finances Internationales, Science Po (Paris2005).

6 Martín Aceña and Reis, eds., Monetary Standards in the Periphery: Paper, Silver, and Gold. 1854-1933 (London,New York: MacMillan Press, St. Martin's Press,2000).

7 We will use the word “central bank” in the following, even though the transition to modern central banking had notyet been completed and the terminology “banks of note issue” would be more appropriate.

8 Eichengreen, "Central bank cooperation and exchange rate commitments: the classical and interwar gold standardscompared," Financial History Review 2(1995). Flandreau, "Central Bank Cooperation in Historical Perspective: ASceptical View," Economic History Review 50, no. 4 (1998).

9 Hallwood, MacDonald, and Marsh, "Credibility and fundamentals: Were the Classical and Interwar Gold StandardsWell-Behaved Target Zones?," in Modern Perspectives on the Gold Standard, ed. Bayoumi, Eichengreen, andTaylor (Cambridge: Cambridge University Press, 1996). Bordo and MacDonald, "Interest Rate Interactions in theClassical Gold Standard, 1880-1914: Was there any Monetary Independence?," Journal of Monetary Economics52(2005).

10 de Cecco, Money and Empire: The International Gold Standard, 1890-1914 (Oxford: Blackwell, 1974).

4

Although the existing literature allures to the core-periphery dichotomy, it is surprising to see that

little effort has gone into analyzing what exactly these differences consist of. A number of

publications of recent years on the experience of individual countries has greatly expanded our

knowledge of the European periphery under the Classical Gold Standard11; but case studies, by

design, can never substitute for a cross-country study analyzing similarities and differences between

countries based on the same methodology. Such comparative studies on different aspects of

monetary policy under the Classical Gold Standard exist, but they are mostly confined to comparing

core countries with each other.12

In this paper we aim to provide the first systematic comparison of discount rate policy under

the Classical Gold Standard based on the concept of a central bank reaction function. The discount

rate was the most important monetary policy instrument at the time; Bagehot’s famous description

of the London money market, for instance, is almost exclusively concerned with the discount rate.13

Modern research, going back to Bloomfield’s path-breaking 1959 study14, has followed this

approach. Drawing on a sample of 12 European countries (Austria-Hungary, Belgium, Bulgaria,

England, France, Germany, Italy, the Netherlands, Norway, Romania, Serbia, Sweden) and relying

on monthly data – the highest frequency available for all countries simultaneously –, we will

analyse the determinants of discount rate policy; in particular, we will ask whether core and

peripheral countries followed different patterns and, if so, explain why this was the case.

In the process of collecting the data required for this analysis, it became clear to us why a

comparative study of similar size and data frequency had never been conducted before: with the

11 Esteves, Reis, and Ferramosca, "Market Integration in the Golden Periphery: The Lisbon/London Exchange, 1854-1891," Explorations in Economic History 46, no. 3 (2009). Jobst, "Market Leader: The Austro-Hungarian Bank andthe Making of Foreign Exchange Intervention, 1896-1913." Reis, "An "Art" and not a "Science"? Central BankManagement in Portugal under the Gold Standard, 1863-1887," Economic History Review 60, no. 4 (2007). Tattara,"Paper money but a gold debt: Italy on the gold standard," Explorations in Economic History 40(2003). Ögren andOksendal, eds., The gold standard peripheries: monetary policy, adjustment and flexibility in a global setting(London: Palgrava Macmillan,2012).

12 Giovannini, "'Rules of the Game' during the International Gold Standard: England and Germany," Journal ofInternational Money and Finance 5(1986). Contamin and Denise, "Quelle autonomie pour les politiques monétairessous l'étalon-or, 1880-1913?," Economie Internationale. La Revue di CEPII 78(1999).

13 Bagehot, Lombard Street. A Description of the Money Market, 6th ed. (London: Kegan Paul, 1878).14 Bloomfield, Monetary Policy under the International Gold Standard, 1880-1914 (New York: Federal Reserve Bank

of New York, 1959), p. 27.

5

exception of England, Italy and Norway, the central banks have not made their historical balance

sheet data publicly available. Most of the data (though not all) could be found in the Annual Reports

of the time, but copies of these reports can nowadays only be found in the archives of the respective

central banks.15 Hence intensive collaboration with the central banks’ historical archives was

needed to reconstruct the time series.16

Which countries do we view as core and which ones as periphery? This dichotomy is often

used in the literature but rarely defined based on rigorous foundations. A classification based on

GDP per capita appears problematic in this context, as some countries considered peripheral by

most scholars would need to be classified as core (Argentina comes to mind and Ford’s famous

comparison with the UK17). In our context, any definition should rather capture the position in the

international economy and, in particular, the international financial system. Liquidity in the foreign

exchange market, for instance, provides evidence on the ability to attract short-term capital; another

potential indicator might relate to the ability to attract long-term capital: raising long-term capital is

more difficult for countries suffering from original sin than for those able to access global capital

markets in domestic currency.

Classifying countries into core and periphery along these two (or other similar) criteria

might lead to conflicting results; the example of the US comes to mind, which Morgenstern and

Schwartz classify as core, while Bordo and Eichengreen tend to see it as peripheral in the pre-WW I

financial architecture.18 Fortunately, our sample of 12 countries poses little risk of unclear

15 The only exception to this rule is the Bank of England which holds all of the German and many of the FrenchAnnual Reports. Interestingly enough, national libraries and university libraries did not even collect the AnnualReports of the bank of note issue of their own country (as they do today). Banks of note issue at the time wereprivately owned and the evolution towards a central bank was so gradual that librarians apparently judged thesereports to be akin to the Annual Reports of conventional commercial banks and hence did not deem holding thereports to be in the public interest.

16 I owe a special thanks to the following people in helping me collect the data: Ivo Maes and Arnold de Schepper(National Bank of Belgium), Kath Begley (Bank of England), Alfredo Gigliobianco (Bank of Italy), Mrs Beex (DeNederlandsche Bank), all members of the data collection task force of the South-East European Monetary HistoryNetwork, Erik Buyst, Jan Tore Kloveland, Larry Neal, Giuseppe Tattara, Anders Ogren and Marc Weidenmier.

17 Ford, Britain and Argentina (Oxford: Clarendon Press, 1962).18 We thank Michael Bordo for discussion on how the view of the US in the pre-World War I financial architecture has

changed over time in historiography.

6

classification: based on an analysis of foreign exchange-market liquidity, Flandreau&Jobst19

classify England, France, Germany, Belgium and the Netherlands as “key countries”20 of the

international monetary system in 1880, a year which conveniently coincides with the beginnings of

our estimation period; we would choose exactly the same five countries if we looked at the second

criterion allured to above, i.e., the ability to issue sovereign bonds in terms of their own currency:

from the 12 countries in our sample, Bordo&Flandreau show that it is the same five countries who

were in a position to issue debt abroad in their own currency.21 In the following, we will therefore

treat Belgium, England, France, Germany and the Netherlands as core countries and the other seven

countries as periphery.

The remainder of the paper is organized as follows. In the second chapter we will estimate central

bank reaction functions for core and peripheral countries. Having established that the two types of

countries reacted to different variables in setting their discount rate, chapter three aims at explaining

the differences; based on published sources and internal documents of the time, we will show that

peripheral countries adapted the “English” gold standard to suit their needs; a modification which

also impinged on how exactly the discount rate was be used. Chapter four summarizes and

concludes.

19 Flandreau and Jobst, "The ties that divide: a network analysis of the international monetary system, 1890-1910,"Journal of Economic History 65, no. 4 (2005): p. 997.

20 Flandreau&Jobst have a classification into key-internediary-periphery in mind rather than a dichotomy between coreand periphery only; the implication for our research is that we merge the second and the third group into a singlegroup labelled “periphery”.

21 Bordo and Flandreau, "Core, periphery, exchange rate regimes, and globalization," in Globalization in historicalperspective, ed. Bordo, Taylor, and Williamson (Chicago: University of Chicago Press, 2003), p. 439.

7

CHAPTER TWO DETERMINANTS OF DISCOUNT RATE DECISIONS

Components of a central bank reaction function

Adherence to the gold standard implied two main constraints. First, in order to maintain confidence

in the domestic monetary system, banks of note issue were required to hold a certain minimum level

of reserves against bank notes in circulation; if the ratio between the two – usually referred to as the

cover ratio – fell below some statutory level (typically 30% - 40%), some sort of sanction would be

applied. In extremis, this could lead to the complete loss of the note issuing privilege granted by the

government.22

The second constraint relates to the international dimension of the gold standard, i.e., the

need to keep the exchange-rate within the gold points. As the vast majority of transactions in the

late 19th century were settled by bills of exchange23, the exchange-rate (i.e., the price of a bill of

exchange drawn on a foreign country) could deviate from mint parity (i.e., the “standard” exchange-

rate implied by the respective mint ratios); only over and above some level of deviation – known as

the gold export point -, it will be advantageous to settle debt with (physical) gold, transaction costs

notwithstanding (mainly shipping and insurance). As such withdrawal of gold from domestic

circulation led, directly or indirectly, to a loss in reserves, central banks used the discount rate to

prevent the exchange-rate from breaking out of the gold points.

Third, discount rate decisions might be explained by patterns of interest rate followership

vis-à-vis England, France and Germany. In a world of fixed exchange-rates and capital mobility, the

macroeconomic policy trilemma implies that “small countries” have to follow the interest rates set

by “large countries”.24

22 Reichsbank, Vergleichende Notenbank-Statistik. Organisation und Geschäftsverkehr wichtiger europäischerNotenbanken 1876-1913 statistisch dargestellt (Berlin: Reichsdruckerei, 1925).

23 Denzel, "The European Bill of Exchange. Its Development from the Middle Ages to 1914," in Cashless Paymentsand Transactions from the Antiquity to 1914, ed. Chaudhuri and Denzel (Stuttgart: Franz Steiner Verlag, 2008).

24 Obstfeld, Shambaugh, and Taylor, "The Trilemma in History: Tradeoffs among Exchange Rates, Monetary Policies,and Capital Mobility," Review of Economics and Statistics 87, no. 3 (2005).

8

In an ideal world, we would also include real economic variables such as output,

unemployment or whether the economy is in an expansionary or contractionary phase of the

business cycle; for, after all, central bank reaction functions are meant to shed light on the trade-off

between the external constraint (or, in today’s setting, the inflation target) and the incentive to

stimulate the domestic economy. This approach is well exemplified by Eichengreen&Watson&

Grossman’s study on the Bank of England interwar discount rate policy, where real economic

conditions are captured by monthly series on output and unemployment.25 Real economic data on

such frequency are available for our period not even for England, France and Germany26, let alone

for the other 9 countries (for many of which we would not even have decent annual GDP estimates).

We can therefore only point out to the problem and move on.

Modelling a central bank reaction function

Our model emerges naturally from our previous discussion. The discount rate is perceived as a

function of the exchange-rate, the cover ratio and interest rates set abroad. As for exchange-rate and

interest rate, we choose England, France and Germany as the reference point, following widespread

practice in the literature.27

Two more decisions need to be taken: first, shall we model specific discount rate changes or,

more generally, discount rate behaviour? In the first case, we wish to explain why, for instance, the

Bank of England increased its discount rate by 100 basis points on 31st October 1907 (the American

Banking Crisis reaches England). Some of the literature follows exclusively this approach28, but in

confining our sample to actual discount rate changes we miss an important dimension: if central

banks leave the discount rate unchanged at their monthly meeting, this also constitutes a decision

25 Eichengreen, Watson, and Grossman, "Bank Rate Policy under the Interwar Gold Standard: A Dynamic ProbitModel," Economic Journal 95(1985).

26 Bordo and MacDonald, "Interest Rate Interactions in the Classical Gold Standard, 1880-1914: Was there anyMonetary Independence?." are faced with the same problem and are forced to rely on an interpolated series forEngland, France and Germany. As our sample of countries is larger, we cannot go down that road.

27 Tullio and Wolters, "Monetary policy in Austria-Hungary, 1876-1913: an econometric analysis of the determinantsof the central bank's discount rate and the liquidity ratio," Open Economy Review 18(2007). Contamin and Denise,"Quelle autonomie pour les politiques monétaires sous l'étalon-or, 1880-1913?."

28 Tullio and Wolters, "Monetary policy in Austria-Hungary, 1876-1913: an econometric analysis of the determinantsof the central bank's discount rate and the liquidity ratio."

9

worth investigating. Consequently, we will model discount rate changes as well as monthly

discount rate behaviour. The frequency of the second approach will be monthly; this is the highest

frequency available (for all countries simultaneously), but it also seems justified, as our sources

suggest most central banks at the time had one (regular) meeting each month.

Second, shall we pool the data or conduct country-specific regressions? The appeal of the

latter option is to pursue a general-to-specific approach, thereby establishing which regressors

mattered for which country. On the other hand, direct comparability of results is better ensured by

pooling the data with country-specific (or group-specific) regressors; moreover, country-specific

regressions might constitute a case of seemingly unrelated regressions (SUR) and hence be

econometrically questionable. As each approach has its own advantages, we decided to pursue both.

This leads to four sets of equations of which we shall discuss the two country-specific

equations first. We propose the following equation for the actual discount rate changes:

(Eq. 1) Δi = α0 * constant + α1 * crm=-1 + α2 * (crm=-1 – crm=-2) +

+ ß1 * xr_em=-1 + ß2 * xr_fm=-1 + ß3 * xr_gm=-1 +

+ γ1 * (i_ed=-1 – i_ed=-31) + γ2 * (i_fd=-1 – i_fd=-31) + γ3 * (i_gd=-1 – i_gd=-31) + ε

The dependent variable Δi captures the interest rate change (in per cent) on a given day of base rate

change (which we arbitrarily set at day d=0 in month m=0). α-coefficients then relate to the cover

ratio: (crm=-1 – crm=-2) measures the change in the cover ratio, comparing the month prior to the

discount rate change (m=-1) to the month preceding it (m=-2).

crm=-1 measures the level of the cover ratio (in m=-1) and is included in addition to the

change in the cover ratio for the following reason: a decline in the cover ratio is more likely to

result in a discount rate increase, if the central bank is faced with already low reserve levels.

Including a constant is a consequence: while the variables for the discount rate change, the

exchange-rate deviation and the interest rate changes (as well as the dependent variable itself) all

10

have an expected value of zero, crm=-1 is positive; implying we require the constant as an offset.

Assuming the central bank targets a specific reserve level, we would expect this level to be close to

– (α1 / α0). We will return to this issue later.

ß-coefficients relate to the exchange-rates vis-à-vis England, France and Germany. They

measure deviations from mint parity, with a positive value implying a depreciated exchange-rate;

for instance, a value of 0.01 for xrEngland means that the exchange-rate vis-à-vis England was

depreciated by 1% with respect to mint parity.

Finally, γ-coefficients relate to potential patterns of interest rate followership vis-à-vis

England, France and Germany. While data on cover ratio and exchange-rate are available only on

monthly frequency, we exploit the daily character of our discount rate data by measuring the

(potential) discount rate change of England, France and Germany as the difference between the

discount rate level the day before the discount rate decision of the country in question (d=-1)

compared to a month before (d=-31).

What signs do we expect? A declining cover ratio should lead to a discount rate increase;

similarly, a discount rate increase is more likely at low reserve levels. Hence, α1 and α2 are expected

to be negative; α0 as an offset should then be positive. ß-coefficients are expected to be positive, as

a depreciation puts upward pressure on the bank rate; similarly, the concept of interest rate

followership implies that γ-coefficients should be positive.

Modelling monthly discount rate behaviour entails two changes: first, we estimate this equation as

an ordered probit with three entries: comparing the last day of the current month (m=0) with the last

day of the previous month (m=-1), the discount rate was either increased (Δi= +1), decreased (Δi=-

1) or remained at the same level (Δi=0).

Second, adaptation is required for the interest rate. As the dependent variable looks at a one-

month horizon (as opposed to a specific day in the first set of equations), i_e, i_f and i_g refer to

potential interest rate changes between the last day of the previous month (m=-1) compared to the

11

last day of the month before (m=-2). Sign expectations remain unchanged but refer to marginal

effects (or, in the case of interest rate changes, differential effects).

(Eq. 2) Δi = δ1 * crm=-1 + δ2 (crm-1 – crm-2) +

+ ε1 * xr_em=-1 + ε2 * xr_fm=-1 + ε3 * xr_gm=-1 +

ζ1 * (i_em=-1 – i_em=-2) + ζ2 * (i_fm=-1 – i_fm=-2) + ζ3 * (i_gm=-1 – i_gm=-2) + ε

How do eqs. 1 and 2 compare to central bank reaction functions estimated in earlier research? For

all their minor differences, most estimations include the same variables as we do, with the possible

exception of the exchange-rate deviation which is only captured by Tullio&Walters29. The main

difference lies in the high frequency of our data as well as the large sample. Most earlier studies do

not venture beyond England, France and Germany30 (and often involve only one31 or two32 of them)

and there is really only one study dedicated to a peripheral country (Austria-Hungary in the event).

The pooled estimations follow the same principle with one modification: exchange-rate data on

England, France and Germany was highly multi-collinear so that it seemed prudent to replace the

individual series by a principal component series. We first estimate a separate pool for core

countries and for peripheral countries (eqs. 3A and 3B for actual discount rate changes and eqs. 4A

and 4B for monthly discount rate behaviour). In another estimation (3C and 4C), we then merge

29 Ibid; ———, The Objectives of French Monetary Policy during the Classical Gold Standard, 1876-1913: aneconometric analysis of the determinants of the Banque de France's official discount rate, Diskussionsbeiträge desFachbereichs Wirtschaftswissenschaft der Freien Universität Berlin, Nr. 12 (2003); ———, The Objectives ofBritish Monetary Policy during the Classical Gold Standard, 1876-1913: an econometric analysis of domestic andforeign determinants of bank rate, Diskussionsbeiträge des Fachbereichs Wirtschaftswissenschaft der FreienUniversität Berlin, Nr. 13 (2003); ———, The Objectives of German Monetary Policy during the Classical GoldStandard, 1876-1913: an econometric analysis of the determinants of the Reichsbank's discount rate,Diskussionsbeiträge des Fachbereichs Wirtschaftswissenschaft der Freien Universität Berlin, Nr. 14 (2003).

30 Contamin and Denise, "Quelle autonomie pour les politiques monétaires sous l'étalon-or, 1880-1913?."31 Goodhart, The Business of Banking, 1891-1914 (London1972). Dutton, "The Bank of England and the Rules of the

Game under the International Gold Standard: New Evidence," in A Retrospective on the Classical Gold Standard,1821-1931, ed. Bordo and Schwartz (Chicago: Chicago University Press, 1984). Pippenger, "Bank of EnglandOperations, 1893-1913," in A Retrospective on the Classical Gold Standard, 1821-1931, ed. Bordo and Schwartz(Chicago: Chicago University Press, 1984). Davutyan and Parke, "The Operations of the Bank of England, 1890-1908: A Dynamic Probit Approach," Journal of Money, Credit and Banking 27(1995).

32 Giovannini, "'Rules of the Game' during the International Gold Standard: England and Germany."

12

both pools and use group-specific regressors for those variables which delivered substantially

different results in 3A vs. 3B and 4A vs. 4B.

As for eqs. 1 and 2, we follow a general-to-specific approach by eliminating successively all

variables that are not statistically significant at the 10 percent level. This often implied the exclusion

of multi-collinear regressors. Low variance inflation factors for the final results (presented in tables

4 and 5) indicate that multi-collinearity no longer poses a problem. As for eqs. 3 and 4 (tables 6 and

7), we report results for different weights (pooled least squares versus pooled EGLS) as well as for

different coefficient covariances (standard, cross-section SUR and period SUR). All equations pass

conventional residual tests for white noise, normal distribution and heteroskedasticity as well as

tests against misspecification. Details results are available upon request.

We were not in a position to include Bulgaria and Serbia in the country-specific regressions

due to degree of freedom constraints; as they adhered to the gold standard only for short periods of

time (Bulgaria: 1906-1912; Serbia: 1905-1912), they changed their discount rates only two and four

times, respectively. Both countries are, however, included in the pooled regressions.

13

Summary statistics on the independent and the dependent variables

Before presenting the estimation results, it seems worthwhile exploring our raw data on the

exchange-rate performance, the discount rate behaviour and the cover ratio. Some summary

statistics of these three indicators alone are suggestive of substantial differences in monetary policy

between core and peripheral countries.

(a) Exchange-rate performance

Available gold point estimates33 mainly cover intra-core country pairs and range between 0.367

percent (Germany to England) and 0.645 percent (Austria-Hungary to England).34 For core-

periphery pairs, we expect gold points to be further away from mint parity, as transportation costs

for gold shipping between, say, Bucharest and Berlin were higher than between Paris and Berlin.

Fortunately, we can avoid calculating gold points, as peripheral countries did normally not

introduce specie convertibility; this is well documented for Austria-Hungary and Italy, but recent

research on Bulgaria, Romania, Serbia and Sweden suggests the same for other peripheral

economies.35 Stabilising the exchange-rate with respect to England, France and Germany is often

referred to as shadowing the gold standard and is conventionally seen as another form of gold

standard adherence.36 Crucial in our context is that if the peripheral countries wanted to stabilize

their exchange-rate, they had to conceive of “virtual” gold points which would trigger some kind of

central bank reaction. We have therefore assumed two such points at 0.6 percent and 1.0 percent.

33 It should be emphasized that gold points were not time-invariant; they grew smaller over time due to decliningtransportations costs and they could also change during financial crises, as shown byCanjels, Prakash-Canjels, andTaylor, "Measuring market integration: foreign exchange-arbitrage and the gold standard, 1879-1913," Review ofEconomics and Statistics 86, no. 4 (2004). For the argument advanced here, however, it seems justified to operatewith an average gold point taken from contemporary calculations.

34 Cf. sources of table 1.35 Morys, "The Classical Gold Standard in the European Periphery: A Case Study of Austria-Hungary and Italy, 1870-

1913" (PhD Diss., London School of Economics, 2006), pp. 23-27. Fratianni and Spinelli, Storia Monetaria d'Italia.Lira e politica monetaria dall'Unità all'Unione Europea, 2nd ed. (Milan: Mondadori, 2001). Tattara, "Was ItalyEver on Gold?," in Monetary Standards in the Periphery: Paper, Silver, and Gold, 1854-1933, ed. Martín Acenaand Reis (London, New York: MacMillan Press, St. Martin's Press, 2000). Monetary Time Series of SoutheasternEurope from the 1870s to 1914, Bank of Greece Working Paper Nr. 94 (Athens2009), p. 29. We thank AndersOgren for providing similar insight for the Swedish case.

36 Inter alia Obstfeld, Shambaugh, and Taylor, "The Trilemma in History: Tradeoffs among Exchange Rates, MonetaryPolicies, and Capital Mobility." who do not even differentiate between de jure and de facto adherence to gold.

14

Table 1 provides us with the relevant statistics, based on exchange-rate data with respect to

England, France and Germany. For each of the three exchange-rates, we provide the maximum

deviation and the standard deviation. The information is then “condensed” into three indicators: the

maximum deviation with respect to all three countries, the average maximum deviation and the

average standard deviation. The lower part of table 1 shows how often (in percent) the gold export

point was violated with respect to England, France, and Germany, as well as how often the

exchange-rate was depreciated by more than 0.6% and 1.0%, respectively. We also provide an

additional statistic in which we look at gold export violations without taking into account periods of

global financial strain before World War I. These periods were identified as the onset of the Boer

War (1899-1902), the crisis of 1907, and the Balkan Wars (1912/13). We will return to these crises

– and their importance in understanding the core-periphery dichotomy – in chapter 3.

England, Germany, France and the Netherlands are the only countries whose exchange-rate

never depreciated by more than 1 percent. Only slightly below we find Belgium (1.19 percent). At

the other end of the spectrum, Italy and Romania stand out with maximum deviations of 2.83

percent and 5.27 percent, respectively. The middle field is occupied by Sweden, Norway, and

Austria-Hungary (in this order). The average standard deviation gives a similar picture, even though

Sweden, Norway and Austria-Hungary (again in this order) are more similar to the core countries

on this measure. The five core countries and Sweden, Norway and Austria-Hungary all have

average standard deviations between 0.22 percent and 0.36 percent. This contrasts strongly with

Italy and Romania with average standard deviations of approximately double the size.

Focusing on the middle and lower part of table 1, we first consider export point violations of

those countries for which we have gold export point estimates (England, Germany, France, the

Netherlands, Austria-Hungary). Such violations were rare but did occur. The only country without

any such violation in our sample is the Netherlands, but England and Germany, for instance, had

more than the occasional gold point violation. In their bilateral relationship, they had, on average,

one violation every year. This might not sound much, but we have to take into account that we are

15

relying on monthly averages; consequently, the number of gold point violations reported in table 1

only constitutes a lower bound of the actual number of violations if data of higher frequency were

used. A similar picture emerges for the German exchange-rate vis-à-vis France.

Austria-Hungary is the only peripheral country for which we have contemporary gold point

estimates and we find that gold export point violations were more frequent (7.0 percent) than for

England, France, Germany, and the Netherlands (2.7 percent on average). We now turn to Sweden,

Norway, Italy and Romania for which we do not have gold point estimates. When applying the 0.6

percent benchmark (a criterion milder than any of the gold point estimates we have bar the one for

Austria-Hungary), we find that only Sweden’s exchange-rate performance comes close to England,

France, Germany and the Netherlands (2.8 percent). Next come Norway (5.6 percent) and Austria-

Hungary (6.5 percent), to be followed – with a wider margin – by Italy (27.2 percent) and Romania

(30.6 percent). If we allow for a 1 percent depreciation, fewer gold point violations occur but the

broad patterns remains unchanged: Sweden, Norway, and Austria-Hungary had substantially fewer

gold points violations than Italy and Romania.

A closer observation of the exchange-rate data show that most gold point violations

happened during three well-defined events: the early period of the Boer War (1899-1902), the crisis

of 1907, and the Balkan Wars (1912/13). For the purposes of this section, we will confine ourselves

to pointing out how our statistics change when leaving the three episodes out of consideration (more

on the implications for discount rate policy in chapter 3). The exchange-rate performance of both

core and periphery improves but improvements are more pronounced for the periphery (lower part

of table 1). Sweden, Norway and Austria-Hungary have no (on the 1 percent benchmark) or

virtually no (on the 0.6 percent benchmark) gold point violations, and Italy’s and Romania’s

exchange-rate performance now appears in a different light; Italy, for instance, does not exhibit a

single gold point violation vis-à-vis Germany (at the 1.0 percent benchmark).

We can summarize our findings on exchange-rate performance as follows: first, peripheral

countries exhibited higher exchange-rate volatility, which, in turn, led to more frequent and more

16

sizeable violations of the gold points; second, differences in the ability to keep the exchange-rate

close to mint parity were particularly acute in times of global financial strain.

(b) Discount rate behaviour

Table 2 provides data on the average discount rate and the frequency of discount rate changes. As

Austria-Hungary and Italy joined the gold standard only in 1896 and 1904, respectively, we

distinguish between three periods for the average discount rate: 1883-1913, 1896-1913, and 1904-

1913. For some countries, we were able to collect data for the private discount rate. It relates to the

interest rate applied to bills of exchange discounted on the private market; which usually (especially

in the English case which we understand best thanks to Bagehot) meant discounting at banks

specialised on discounting bills. We failed to locate such data for Bulgaria, Italy, Norway, Romania,

Serbia and Sweden, which suggests that the money market in these places was less mature and

most, if not all, of the discounting took place at the central bank.

France enjoyed both the lowest bank rate and the lowest private discount rate. As for the

bank rate, England does not even come in the second position which is taken by the Netherlands.

Only if we look at the private discount rate, we find England in second place. The spread among

core countries was low, but it is interesting to note that Germany had the highest discount rate of the

five core countries.

Peripheral countries had substantially higher interest rates. Sweden, Norway, and Romania –

all of which adhered to gold for the entire period – exhibit a discount rate spread of more than 150

basis points (4.97 percent versus 3.41 percent). If we include Austria-Hungary, Italy, Bulgaria, and

Serbia – all of which adhered to gold only for parts of the 1883-1913 period -, the interest rate

spread increases to more than 200 basis points (5.48 percent versus 3.41 percent).

Turning to the frequency of discount rate changes, table 2 shows that core countries had a

more active discount rate policy; core countries changed their discount rate 2.9 times per annum,

compared to 1.6 times per annum for the periphery. We will be able to give a full explanation only

17

in chapter 3, but two factors should be mentioned at this stage: peripheral countries were, on

balance, under more government pressure, and hence more reluctant to change the discount rate (in

particular in cases where formal government approval was required). This argument, which is often

found in the literature37, probably goes some way towards explaining the differences but fairly

independent central banks could also come under intense pressure: Bagehot, for instance, wrote:

“The Bank directors now fear public opinion exceedingly; probably no kind of persons are so

sensitive to newspaper criticism.”38 Presumably more important was how dominant the central

bank’s position was in the money market: If faced with heavy competition from discount houses,

the central bank had to adjust frequently its bank rate to the market rate so as to get its share of the

discount market. If the central bank dominated the money market – which was presumably the case

in the periphery –, fewer discount rate changes were needed.

(c) Cover ratio

The cover ratio represents the fraction of reserves to liquid liabilities and served as an indicator of

the central bank’s liquidity. The legal requirement to publish the cover ratio on a monthly or even

weekly basis aimed at retaining confidence in the domestic monetary system. We show a

standardized central bank balance sheet to illustrate which items might potentially constitute

“reserves” and “liquid liabilities”.

[INSERT FIGURE 1 ABOUT HERE]

Rules as to what exactly defined the cover ratio differed across countries and over time, but the

broad pattern is as follows: Initially, the reserve ratio was defined as gold (bullion or specie) over

bank notes39; gold was the quintessential store of value, and the convertibility requirement referred

only to bank notes but not deposits. As time went on, the cover ratio matured from this somewhat

37 Reis, "An "Art" and not a "Science"? Central Bank Management in Portugal under the Gold Standard, 1863-1887,"pp. 712-22.

38 Bagehot, Lombard Street. A Description of the Money Market, p. 72.39 The cover ratio of the Bank of England was defined differently as a result of the 1844 Bank Act. The Issue

Department only issued notes. There was a limited fiduciary note issue, but any additional note issue had to be fullybacked by gold. The cover ratio – often referred to as the “proportion” in the English case – refers to the BankingDepartment and represents its reserves (largely bank notes) to its liquid liabilities. For details cf. appendix.

18

legalistic perspective into a more economic concept. This was largely the result of foreign exchange

holdings becoming more important relative to gold holdings. Consequently, countries amended

their bank acts in order to include foreign exchange into the note cover.40 As far as we can see, a

similar process did not take place on the liabilities side. While deposits grew as a share of liquid

liabilities, bank acts were not changed to provide cover for both bank notes as well as deposits. This

is probably explained by the fact that the share of deposits never grew larger than 15 percent – 20

percent of liquid liabilities.

Table 3 shows the average, the minimum, the maximum and the standard deviation of the

cover ratio. Core countries had a substantially lower average reserve ratio than the periphery (56.0

percent versus 69.6 percent). The minimum reserve ratio shows a similar dichotomy: England,

Germany, and Belgium, for instance, let their reserve ratio decline to 30 percent and below. This

contrasts strongly with a minimum cover ratio of 66.1 percent for Italy. So while neither core nor

periphery violated their bank acts (which normally stipulated a 30 percent - 40 percent minimum

cover41), our findings suggest that peripheral countries felt the need to have substantially higher

reserve levels.

In sum: Core countries had few gold point violations (which allowed them to introduce specie

convertibility), changed their discount rate frequently and had a low cover ratio. Peripheral

countries, by contrast, had a worse exchange-rate performance (especially in periods of global

financial strain), changed their discount rate infrequently and relied on a high cover ratio. Do these

pronounced differences in independent and dependent variables translate into different central bank

reaction functions for core and peripheral countries? This is what we turn to now.

40 Morys, "The Classical Gold Standard in the European Periphery: A Case Study of Austria-Hungary and Italy, 1870-1913", p. 136. Monetary Time Series of Southeastern Europe from the 1870s to 1914.

41 Reichsbank, Vergleichende Notenbank-Statistik. Organisation und Geschäftsverkehr wichtiger europäischerNotenbanken 1876-1913 statistisch dargestellt.

19

Results of country-specific estimations (eq. 1 and eq. 2)

(a) Cover ratio

Results for eq. 1 (actual discount rate changes) show that England, Germany, the Netherlands and

Belgium did not respond to changes in the cover ratio by adjusting their discount rate. By contrast,

for all peripheral countries (with the exception of Sweden), we find the expected negative sign. For

some peripheral countries (Italy, Norway and Sweden), we can detect an additional role for the

level of the cover ratio.42

Our findings for eq. 2 (monthly discount rate behaviour) are supportive. Given that more

observations are now available for each equation, we do find a role for the cover ratio in all

equations (except for Belgium); crucially, however, marginal effects for core countries are much

smaller than for peripheral countries (and in some cases only marginally significant). Germany, for

instance, has a marginal effect ten times smaller than Italy (-0.34 versus -3.42).

(b) Exchange-rates

ß- and ε-coefficients on the exchange-rate reveal another core-periphery divide. Counteracting

exchange-rate deviations by means of discount rate changes was crucial for England, Germany, the

Netherlands, and Belgium, but not for peripheral countries. In eq. 2 – which should allow more

precise estimation given the higher number of observations – the exchange-rate does not come out

as significant for any of the five peripheral countries; only in eq. 1 we find a role for the exchange-

rate in the cases of Sweden and Norway. This intra-periphery difference is in line with our findings

for the exchange-rate performance, where the two Scandinavian countries performed better than

Austria-Hungary, Italy and Romania.

42 In these cases, - (α0 / α1) ≈ average cover ratio, vindicating our interpretation of the intercept as an offset to the level of the cover ratio; e.g., Italy: - (α0 / α1) = 74.53% ≈ 75.0% (cf. table 3).

20

(c) Interest rates

Eq. 1 and eq. 2 demonstrate that all countries track the interest rate of at least one of the large core

countries. While differences prevail between core and periphery regarding cover ratio and

exchange-rate, similarities are strong as far as the interest rate is concerned: most countries follow

either England or Germany and coefficients/differential effects are of comparable magnitude.

While interest rate followership can clearly be detected, the size of the

coefficients/differential effects is probably not as large as one would expect given the

macroeconomic policy trilemma. In eq. 1, none of the coefficients comes even close to unity (which

would mean perfect interest rate pass through). Similarly, differential effects in eq. 2 are low: for

example, when the Bank of England increases its discount rate by 1%, the Reichsbank’s probability

to increase its discount rate in response is only raised by 9%; even the highest value in this context

(a 22%-increase in probability for Italy in response to Germany) is far away from an “automatic”

interest rate response. Thus, γ- and ζ-coefficients suggest that a considerable amount of monetary

autonomy was retained under the Classical Gold standard, even for peripheral countries.

Taken together, eq. 1 and eq. 2 show similarities and differences between core and periphery. An

element of interest rate followership was common to both, though not as strong as we would expect

under fixed exchange-rates and capital mobility. Core and periphery differ, however, in the

importance they attach to cover ratio and exchange-rate deviations. Core countries use their

discount rate changes to target specifically the exchange-rate; and they do so with great success, as

evidenced by the superior exchange-rate performance compared with peripheral countries. In turn,

they pay little attention to the cover ratio which was allowed to fall close to the minimum level

required by the bank act. Peripheral countries pursue the opposite strategy: paying little attention to

exchange-rate deviations (hence their poor performance on this account), they target the cover ratio

and successfully manage to keep it at levels approximately twice as high as required by the bank

act.

21

The only country which escapes this clear-cut core-periphery dichotomy seems to be France.

Neither eq. 1 nor eq. 2 suggest that discount rate policy was motivated by exchange-rate deviations;

similarly, the high cover ratio and low frequency of discount rate changes set it apart somewhat

from England, Germany, Belgium and the Netherlands. Yet its exchange-rate performance was

stellar. This seeming contradiction is probably best reconciled by a well-established body of

research which has stressed the sophistication and effectiveness of French gold devices, thereby

substantially reducing reliance on the discount rate tool.43

Results of pooled estimations (eqs. 3 A, B, C and eq. 4 A, B, C)

Our results obtained from country-specific regressions are confirmed by pooled estimations. We

first discuss the pooled estimates for core countries vs. peripheral countries (3A vs. 3B and 4A vs.

4B) and then proceed to a common pool with group-specific regressors.

(a) Cover ratio

Changes in the cover ratio are important for core and periphery but peripheral countries react more

strongly in eq. 3. Moreover, the level of reserves is significant for peripheral countries but not for

the core (the same is true for the constant, see our discussion above on the constant as an offset for

the level of reserves). Both findings are in line with eq. 1 and 2 and underline the specific

importance attached to the cover ratio – both in levels and first differences – by peripheral

countries.

(b) Exchange-rates

Core countries target the exchange-rate but peripheral countries do not, confirming earlier results.

43 For a recent contribution see Contamin, "Interdépendences financières et dilemma de politique monétaire: la Banquede France entre 1880 et 1913," Revue Economique 54(2003).

22

(c) Interest rates

3A, 3B, 4A, 4B all show patterns of interest rate followership vis-à-vis England and Germany but

there is some difference between core and periphery: core countries follow the English interest rate

more strongly, as evidenced by a higher coefficient.44 By contrast, peripheral countries follow

Germany more strongly, with some specifications not even indicating any role for the London bank

rate.

It is worth exploring this difference in some more detail by referring back to the country-

specific equations. Leaving England and Germany aside for obvious reasons, eq. (1) and (2) suggest

the same interest rate setter in seven out of eight cases: Sweden follows both England and Germany,

with the size of the coefficient/differential effect suggesting similar dependence on London and

Berlin. The remaining six countries either follow the Bank of England or the Reichsbank, with

France and Romania following England and the Netherlands, Norway, Austria-Hungary and Italy

following Germany. Only Belgium seems to follow the German bank rate in eq. (1) and the French

bank rate in eq. (2). Combining our findings of eq. (1) – (4), we find that the Reichsbank had a

much bigger role in setting interest rates under the Classical Gold Standard – at least vis-à-vis

countries on the European periphery – than is conventionally acknowledged.45

Pooling core and peripheral countries with group-specific regressors (esq. 3C and 4C)

Eq. 3A, 3B, 4A and 4B have shown that the main difference lies in the importance attached to the

reserve level and the exchange-rate. We therefore pool core and peripheral countries and form

group-specific regressors for the level of the cover ratio and the exchange-rate.

The fundamental difference is confirmed in 3C and 4C: while all other coefficients can

easily be pooled for all countries (and then take on an intermediate value compared to the separate

44 Moreover, in the case of eq. 4A, the coefficient on Germany is not significant at conventional levels.45 Eichengreen, "Conducting the International Orchestra: Bank of England Leadership under the Classical Gold

Standard," Journal of International Money and Finance 6(1987). Tullio and Walters, "Was London the Conductorof the International Orchestra, the Second Violinist or the Triangle Player? A Survey of the Literature onAsymmetries in Balance of Payments Adjustment during the Classical Gold Standard," Scottish Journal of PoliticalEconomy 43(1996).

23

equations reported before), the coefficient for the exchange-rate is only significant for core

countries, while the reserve level is significant only for peripheral countries.46

In conclusion, we found similarities and differences between core and periphery. A strong element

of interest rate followership was common to both. They differ, however, in the importance they

attach to cover ratio and exchange-rate deviations. Core countries used their frequent discount rate

changes to target the exchange-rate. Little attention was paid to the cover ratio which occasionally

fell close to the minimum level required by the bank act. Peripheral countries, by contrast, targeted

the cover ratio and successfully managed to keep it at levels approximately twice as high as

required by the bank act.

But why, then, did peripheral countries not attach more importance to exchange-rate

deviations in setting the discount rate? Was this out of choice or out of necessity? We recall that the

exchange-rate performance of peripheral countries was not much worse than that of core countries

for most of the time, but deteriorated quickly during periods of global financial strain.

Understanding central bank behaviour during these periods will enable us to give an answer to this

question. This is what we turn to now.

46 In some specifications, the reserve level is not significant at the 10%-level for the peripheral countries, as opposed to3B and 4B. This is owed to the circumstance that we cannot have a group-specific constant (which would allow theconstant to assume the function as an offset to the reserve level as argued above) in a country-fixed-effectsestimation, the reason being: country-fixed effects imply adding dummy-variables for each cross-sectional unit; agroup-specific constant means adding (in our case) two dummy variables. If both types of dummy variables areadded simultaneously, each group-specific dummy variable can be written as a linear combination of some of thecountry-specific dummy variables, thereby resulting in a non-full-rank matrix (which can hence not be inverted).

24

CHAPTER THREE. CENTRAL BANK BEHAVIOUR DURING THE PERIODS OF GLOBAL

FINANCIAL STRAIN

As indicated earlier, there were three periods of sustained gold point violations by peripheral

countries: the Boer War, starting in 1899; the crisis of 1907; and the Balkan wars of 1912/13. We

briefly explain each episode and then analyse the discount rate behaviour of core and peripheral

countries during these crises. Subsequently, we will support our analysis of the data by a study of

the internal protocols and the Annual Reports of the Austro-Hungarian bank.

(a) The Boer War began in October 1899. Early successes of the Boers culminated in the so-

called “Black Week” (10th – 15th December 1899). As the British Empire grew increasingly

determined to win the war, major reinforcements were sent; by January 1900 it became clear

that England would, at least, not lose the war (even though hostilities continued for a long

time and peace was only achieved in May 1902). For the purpose of our study it is important

to keep in mind that South-Africa at the time was the world’s largest supplier of gold for a

rapidly growing world economy connected to the gold standard. The chronology of military

events is mirrored by three discount rate increases of the Bank of England from 3.5 percent

to 6 percent (3.10., 5.10. and 30.11.) before it fell to 5 percent on 11th January 1900. We

observe a similar pattern for the Reichsbank which raised its discount rate by 2 percent to 7

percent (3.10. and 15.11.) before reducing it to 6 percent on 12th January 1900.

(b) The crisis of 1907 is often erroneously reduced to the American Banking Crisis of the same

year but in fact it was a much wider phenomenon. It followed the upswing of the first years

after the turn of the century in which many countries had participated. Bubbles burst in

different places at different times. European discount rate data suggests two waves. The first

one began in September 1906 and ran until January 1907 when the first central banks start

lowering their discount rates. This was then followed by a second wave in late 1907. The

25

failure of the Knickerbocker Trust Company in New York on 22nd October 1907 soon led to

a general suspension of cash payments by the entire American banking system. A week

later, Germany (29th October) and England (31st October) started raising their discount rate

from 5.5 percent and 4.5 percent, respectively, to 7.5 percent and 7 percent. These were the

highest values for both countries during the Classical Gold Standard era which underlines

the severity of the crisis. On 2nd January 1908 the Bank of England became the first major

central bank to decrease its discount rate again.

(c) The third episode relates to the Balkan Wars of 1912/13. Great power rivalries had

manifested itself on the Balkans since the congress of Berlin (1878), which explains why

every new crisis led to increased anxiety worldwide. In the event, the so-called Balkan

League was established as an alliance between Greece, Serbia, Bulgaria, and Montenegro

with the aim of conquering the European lands of the Ottoman Empire. Established in early

1912, the outbreak of war was likely as soon as summer 1912 (even though it broke out only

on 8th October 1912). The Bank of England was the first central bank to raise its discount

rate, increasing it by 2 percent to 5 percent (29.8. and 17.10.) before decreasing it on the 17th

April. Germany also increased its discount rate by 1.5 percent to 6 percent (24.10. and

14.11.).

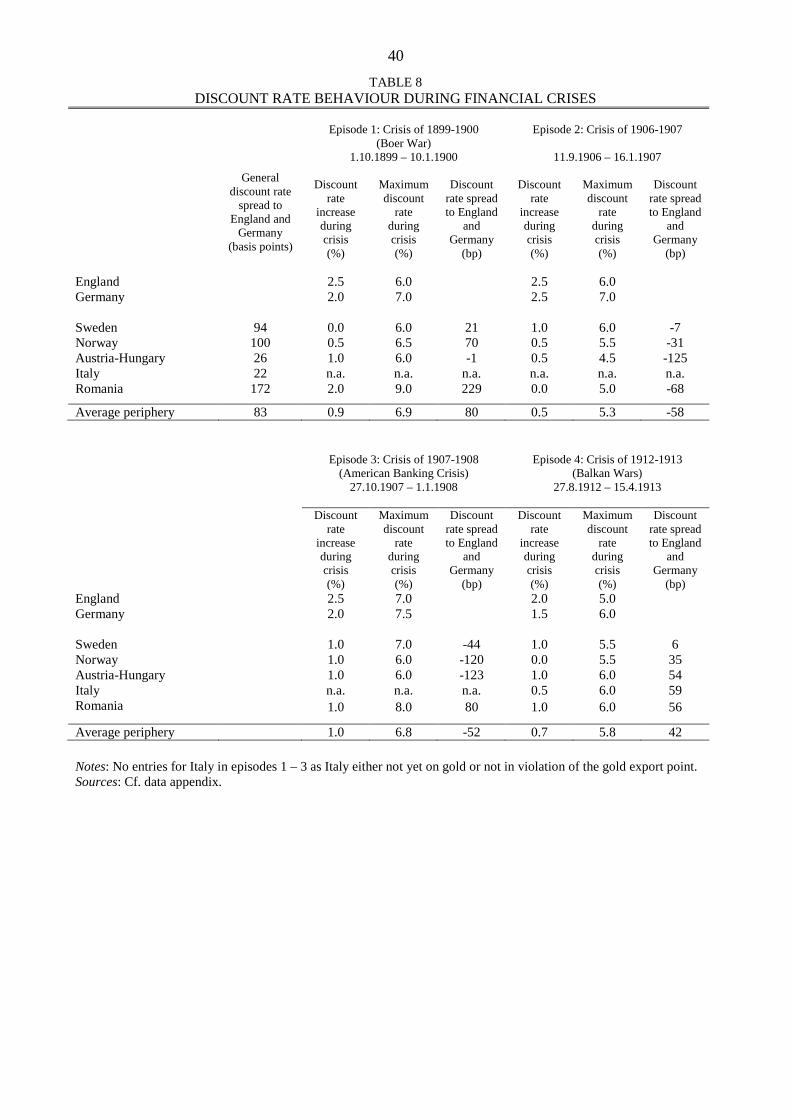

Table 8 compares the discount rate policy of England and Germany with peripheral countries. The

time window is defined by two days in advance of the first central bank raising the discount rate and

ends the day prior to the first central bank lowering it again. Table 8 shows by which margin

discount rate changes were made and to which level they were raised. We also report the discount

rate differentials to England and Germany (represented by the arithmetic average of their respective

discount rates) during the time window as opposed to the normal discount rate spread.

England and Germany engaged in competitive discount rate increases early on but

peripheral countries reacted late and increased their discount rates by substantially lower margins.

26

Consequently, the discount rate differential between core and periphery actually declined during

crises. The peripheral economies had an average discount rate spread of 83 basis points. The spread

declined during all four crises episodes and even turned negative during the crisis of 1907. We are

hence confronted with a paradox: in crisis situations with prolonged violations of the gold export

point, peripheral countries decreased rather than increased their discount rate spread to the core

countries.

This paradox might be explained as follows: as the general discount rate level was higher for

peripheral countries, there was limited room for manoeuvre during periods of global financial

strain. Moreover, a signalling problem might have prevented peripheral economies from raising the

discount rate by a wide margin. Sizeable discount rate increases could be interpreted as signs of

weakness and hence deter rather than encourage the inflow of much-needed short-term capital. Last

but not least, the discount rate increases could have been a less effective tool in peripheral countries.

In order to provide some qualitative evidence, we studied the annual reports of the Austro-

Hungarian bank and the protocols of the general council. The Annual Reports were mainly meant

for the shareholders of the Austro-Hungarian Bank, whereas the protocols of the general council

were internal documents. The internal discussions in particular provide an answer as to why

peripheral countries used the discount rate tool so sparingly during crises. First, there was a general

sense that discount rate increases would be unpopular and to the detriment of domestic business, an

argument particularly often advanced by government representatives on the general council.47 The

Austro-Hungarian bank could be very explicit about this; when describing discount rate policy

during the Boer War (i.e., our first crisis episode), for instance, they write that “... we should not

forget that the bank’s duties do not only consist of defending mint parity. It is of no less importance

to protect and promote all the other interests of our national economy which is beset with so many

difficulties…”48.

47 General council meeting #523, held 27th June 1907, pp. 5-6. The Austro-Hungarian bank had two governmentrepresentatives, one for Austria and one for Hungary.

48 Report to the 22nd General Meeting of the Austro-Hungarian Bank (1900), p. 11. A very similar statement can befound in the Report to the 32nd General Meeting of the Austro-Hungarian Bank (1910).

27

Second, members of the governing council doubted the effectiveness of discount rate

increases. From a general council meeting held at the height of the American Banking crisis (28th

November 1907), we learn that Austria-Hungary did contemplate increasing the discount rate

further (at this point it was 100 basis points below England and 150 basis points below Germany),

but failed to do so because “even a higher interest rate would not have made a difference”49 (i.e., the

exchange-rate would have remained substantially depreciated).

If raising the discount rate was difficult and, in times of global financial strain, potentially not even

effective, what was the alternative? The annual reports and protocols give several hints which help

explain the different discount rate policies established in the second chapter. First, accumulating

large reserves in “good times” and returning them slowly to the market when necessary was seen as

a good way of keeping interest rates low and stable: „The enormous increase of our metallic

holdings … and, more importantly, the vast stock of foreign bills of exchange and foreign deposits

has proven beneficial to the domestic economy. As a result, we could offer relatively low interest

rates throughout the year despite adverse interest rates abroad… “50 The concept that a policy of

infrequent discount rate changes required high reserve levels can be found elsewhere51 and provides

qualitative evidence in support of our econometric findings.

Second, not introducing specie convertibility provided important “breathing space” during

periods of prolonged exchange-rate depreciations. As indicated earlier, one of the key institutional

differences between core and peripheral countries was that the latter only “shadowed” the gold

standard, i.e., they were not constrained by the rather narrow gold points implied by specie

convertibility. Austria-Hungary was a case in point, where, despite a long and intense discussion,

specie convertibility remained suspended.52 It is therefore interesting to note that during the 1907

49 General council meeting #528, held 28th November 1907, p. 4.50 Report to the 29th General Meeting of the Austro-Hungarian Bank (1907), pp. 10-11.51 Report to the 30th General Meeting of the Austro-Hungarian Bank (1908).52 Hemetsberger-Koller, "Die suspendierte Goldkonvertibilität. Barzahlungskrise in Österreich-Ungarn zu Beginn des

20. Jahrhunderts," in Auf Heller und Cent. Beiträge zur Finanz- und Währungsgeschichte, ed. Bachinger and Stiefel(Frankfurt, Vienna: Überreuter, 2001).

28

crisis, one of the council members states how helpful it proved in the current financial crisis that

Austria-Hungary had not introduced specie convertibility, thus giving more flexibility to the

monetary authority.53

Third, “moral suasion” on behalf of the central bank probably played a much bigger role in

peripheral money markets. The London money market, due to its size and anonymity54, was to

react to the price of money; in the much smaller and less developed money markets of the periphery

(where, probably for the lack of it, we could not even find data for open market discount rates for

most countries, cf. above), by contrast, it was potentially feasible to reduce, if only temporarily,

demand for foreign currency by other means. By the informal nature of “moral suasion”, it is

difficult to provide an abundance of hard evidence to support this claim, but from the sources

available to us it seems that the Austro-Hungarian bank did make use of it.55

In conclusion, the qualitative evidence is supportive of our statistical analysis. Peripheral countries

adapted the “English” gold standard in two crucial aspects to suit their needs: first, they did not

introduce specie convertibility, thus widening the exchange-rate bands and hence providing more

flexibility; second, peripheral countries came to rely on high reserve levels and oriented their

discount rate policy towards maintaining the reserve level rather than targeting more narrowly the

exchange-rate.

53 General council meeting #527, held 9th November 1907, p. 9.54 A factor emphasized by Capie in the functioning of the London money market. Capie, "Banking in Europe in the

Nineteenth and Twentieth Centuries: The Role of the Central Bank," in The State, the Financial System andEconomic Modernization, ed. Sylla, Tilly, and Tortella (Cambridge: Cambridge University Press, 1999).

55 We thank Clemens Jobst for this insight and sharing the following newspaper entry with us: “Budapest, 29.September (Der Devisen und Geldmarkt.) Heute war eine ruhige Strömung auf dem Devisenmarkte vorhanden. DemWunsche der Oesterreichisch-Ungarischen Bank Rechnung tragend, haben einzelne Wiener Institute die bei ihnenvom Auslande einlaufenden Orders auf Beschaffung von Gold und Devisen zur Ausführung nicht mehrangenommen. Englische und französische Zahlmittel blieben zwar begehrt, doch waren die Transaktionen nicht soumfangreich wie in den letzten Tagen. Deutsche Zahlmittel haben eine mäßige Abschwächung erfahren.“ (PesterLloyd, 30th September 1911, p. 11)

29

CHAPTER FOUR CONCLUSION

In this paper we provided the first systematic comparison of discount rate policy under the Classical

Gold Standard based on the concept of a central bank reaction function. Drawing on a new data set

of monthly observations for 12 European countries, we analysed the determinants of discount rate

policy; in particular, we asked whether core and peripheral countries followed different patterns and

why this was the case.

Two key findings emerged: first, core and periphery differ in the importance they attach to

cover ratio and exchange-rate deviations. Core countries use their discount rate changes to target

specifically the exchange-rate; and they do so with great success, as evidenced by the superior

exchange-rate performance compared with peripheral countries. In turn, they pay little attention to

the cover ratio which was allowed to fall close to the minimum level required by the bank act.

Peripheral countries pursue the opposite strategy: paying little attention to exchange-rate deviations

(hence their poor performance on this account), they target the cover ratio and successfully manage

to keep it at levels approximately twice as high as required by the bank act.

Second, an element of interest rate followership vis-à-vis England and Germany was

common to core and periphery, though not as strong as one would expect under fixed exchange-

rates and capital mobility. Core countries followed more strongly the bank rate set in London,

whereas countries on the European periphery were more influenced by the Reichsbank. Thus, our

findings suggest that the European branch of the Classical Gold Standard was less London-centered

than hitherto assumed.

We then turned to explaining the differences between core and peripheral countries. The key

difference was the effectiveness of the discount rate tool: In the case of core countries, a discount

rate increase quickly led to short-term capital inflows and hence an improvement of the exchange-

rate. This mechanism did not operate as smoothly for peripheral countries, resulting in more

30

frequent violations of the gold export point. This core-periphery dichotomy was particularly

pronounced in periods of global financial strain, when peripheral countries had to live with

prolonged periods of unfavourable exchange-rates. As a result, peripheral countries adapted the

gold standard in two crucial aspects to suit their needs. First, they did, for the most part, not

introduce specie convertibility, thus widening the exchange-rate bands and hence providing more

flexibility; second, peripheral countries came to rely on high reserve levels and they oriented their

discount rate policy towards maintaining the reserve level rather than targeting more narrowly the

exchange-rate.

If peripheral countries modified the “English” gold standard to suit their needs, this probably

entails a wider lesson for the functioning of the Classical Gold Standard: there was not only one

gold standard but a variety of gold standards; peripheral countries apparently followed a version

different from the one pioneered by England. Perhaps it is precisely this institutional flexibility

which explains why the Classical Gold Standard remains to this day the longest-ever system of

fixed exchange-rates.

DATA APPENDIX

Austria-Hungary, Bulgaria, Romania and Serbia

All data except for private discount rates (cf. below) from Monetary Time Series of South-Eastern

Europe from the 1870s to 1914.

Belgium

- Exchange rates: Neal-Weidenmier-Gold Standard data base (England),

Schneider&Schwarzer&Zellfelder 1991, Europäische und nordamerikanische Devisenkurse

1777-1914, vol. 2, pp. 239-240 & vol. 3, pp. 354-356 (France, Germany)

- Bank rate: Kauch, La Banque Nationale de Belgique, pp. 148-152

- Reserves and monetary base: “Assemblée Générale des Actionnaires de la Banque

Nationale. Rapport fait par le Gouverneur au nom du Conseil d’Administration”, section

“Extrait des situations publiées au moniteur belge en …”, Brussels 1878 – 1914

31

England

- Exchange rates: Neal-Weidenmier-Gold Standard data base (Germany), NBER

Macrohistory database #14107 (France)

- Bank rate: Hawtrey, A Century of Bank Rate, pp. 281-296

- Reserves and monetary base: Capie&Webber, A Monetary History of the United Kingdom,

pp. 408-431.

France

- Exchange rates: Neal-Weidenmier-Gold Standard data base (England),

Schneider&Schwarzer&Zellfelder 1991, Europäische und nordamerikanische Devisenkurse

1777-1914, vol. 2, pp. 351-352 (Germany)

- Bank rate: Hawtrey, A Century of Bank Rate, pp. 302

- Reserves and monetary base: “Compte rendu des operations de la Banque de France et de

ses succursales pendant l’année 1889” etc., Paris 1890-1914, section “Situation

hebdomadaire des principaux comptes de la Banque”

Germany

- Exchange rates: Neal-Weidenmier-Gold Standard data base (England), NBER Macrohistory

database #14071 (France)

- Bank rate: Reichsbank, Vergleichende Notenbankstatistik, pp. 186-189.

- Reserves and monetary base: “Verwaltungs-Bericht der Reichsbank fuer das Jahr 1876” etc.,

Berlin 1876-1914, section “Zusammenstellung der … veroeffentlichten Wochen-

Uebersichten”

Italy

- Exchange rates: Spinelli, Per la storia monetaria dell'Italia, vol. 2, pp. 45-94 (England),

Schneider&Schwarzer&Zellfelder 1991, Europäische und nordamerikanische Devisenkurse

1777-1914, vol. 3, pp. 22-23 & pp. 69-71 (France, Germany)

- Bank rate: kindly communicated by Alfredo Gigliobianco, Historical Archive of the Bank of

Italy

- Reserves and monetary base: de Mattia, I bilanci degli istituti di emissione italiani dal 1845

al 1936, vol. 2, pp. 619-753 and pp. 446-454

Netherlands

32

- Exchange rates: Neal-Weidenmier-Gold Standard data base (England),

Schneider&Schwarzer&Zellfelder 1991, Europäische und nordamerikanische Devisenkurse

1777-1914, vol. 2, pp. 122-123, 126-127, 188-189 (France, Germany)

- Bank rate: de Jong, Geschiedenis van de Nederlandsche Bank, vol. 3, pp. 537-543

- Reserves and monetary base: “Verkorte Balans der Nederlandsche Bank”, 1875-1913

(Nationaal Archief, The Hague)

Norway

- Bank rate: Annual Report of Norges Bank 1979, p. E10

- All other data: downloaded from www.norges-bank.no

Sweden

- Exchange rates: Schneider&Schwarzer&Schnelzer 1993, Statistik der Gold- und

Wechselkurse in Deutschland und im Ostseeraum, 18. und 19. Jahrhundert, pp. 299-300,

337-338, 318-320, 348 (England, France, Germany)

- Bank rate: Sveriges Riksbank, Sveriges Riksbank 1668-1924-1931, pp. 136-138.

- Reserves and monetary base: “Sammandrag af Bankernas Uppgifter”, Stockholm 1878-1912

and “Sveriges Riksbank Årsbook”, Stockholm 1913-1915

Private discount rates for Austria-Hungary, Belgium, England, France, Germany, the Netherlands

Reichsbank, Vergleichende Notenbankstatistik, pp. 212-231

FIGURE 1CENTRAL BANK BALANCE SHEET

Assets Liabilities

International assets Liquid liabilitiesGold (bullion and specie) Bank notes in circulationSilver (bullion and specie) Bank depositsForeign exchange and otherinternational assets

Other liabilities payable on demand

Domestic assetsBills of exchangeCash advances

Other assets (real estate etc.) Other liabilities

33

TABLE 1

EXCHANGE RATE PERFORMANCE (MEASURED AGAINST MINT PARITY) WITH RESPECT TOENGLAND, FRANCE AND GERMANY

England France Germany NetherlandsXR w.r.t. France Germany England Germany England France England France Germany

Maximum deviation 1.0051 1.0059 1.0043 1.0037 1.0063 1.0062 1.0041 1.0068 1.0023Standard deviation 0.0026 0.0024 0.0022 0.0050 0.0024 0.0032 0.0023 0.0039 0.0024

Max. dev. 1.0059 1.0043 1.0063 1.0068Avg. max. dev. 1.0055 1.0040 1.0062 1.0044Avg. st. dev. 0.0025 0.0036 0.0028 0.0029