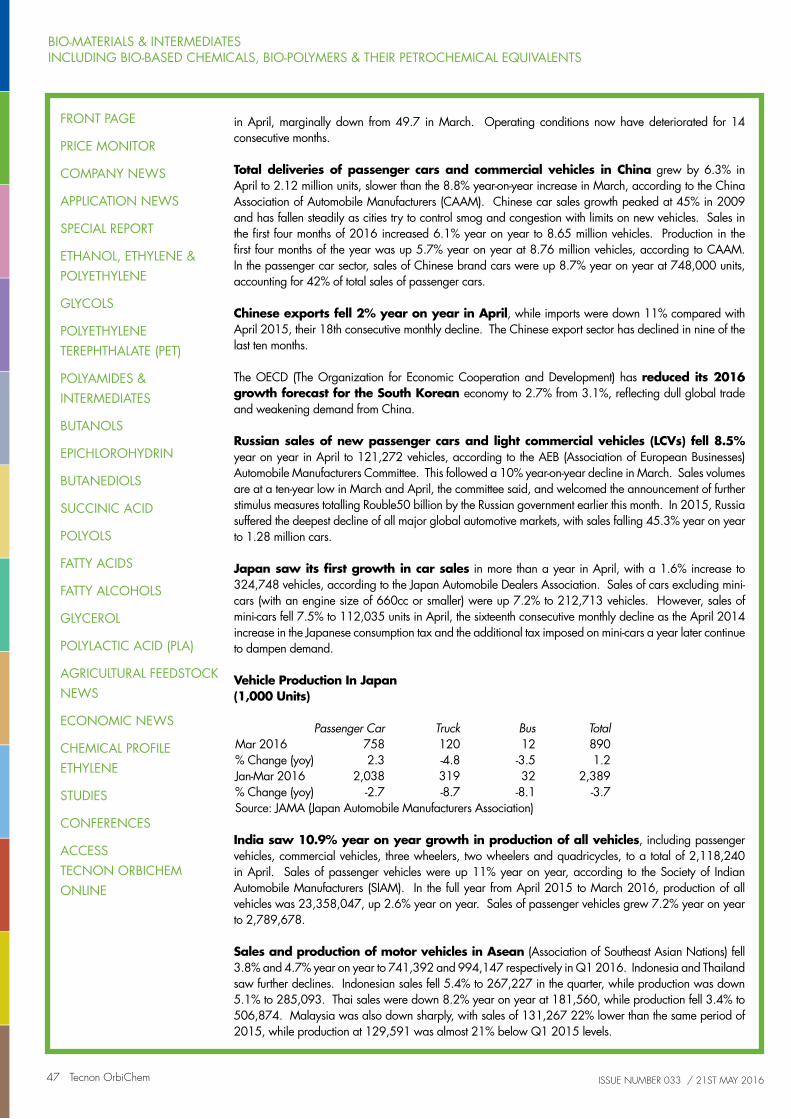

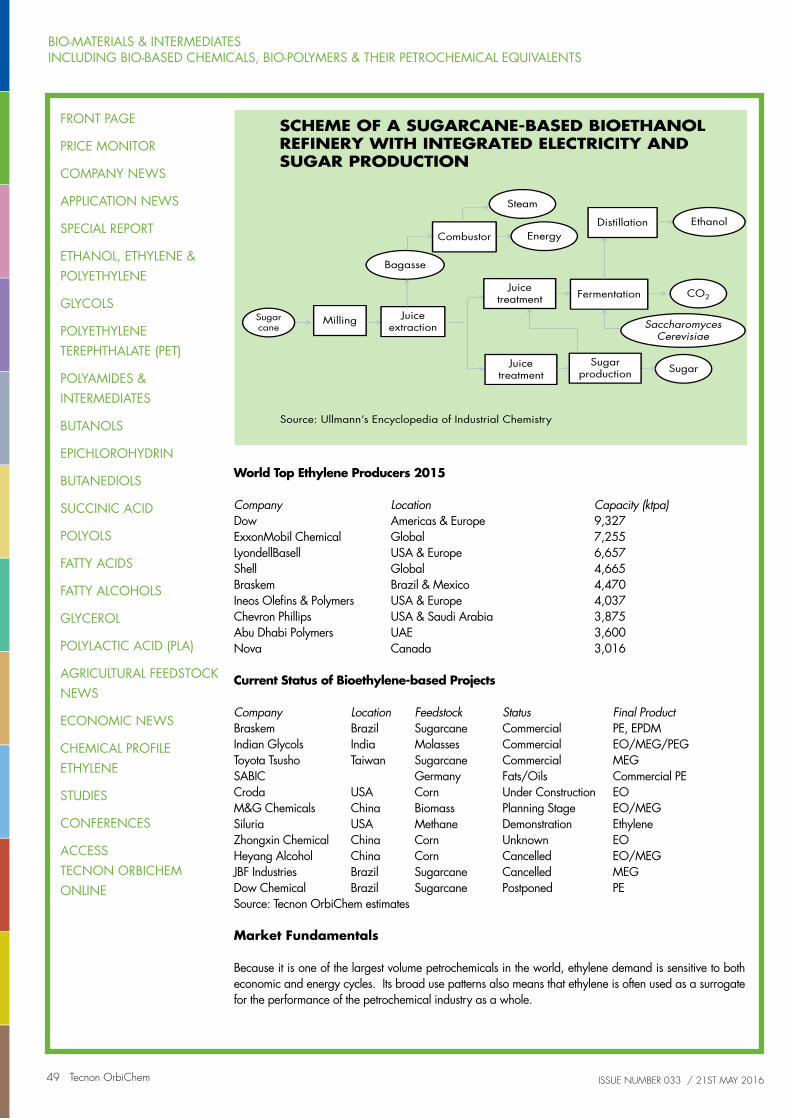

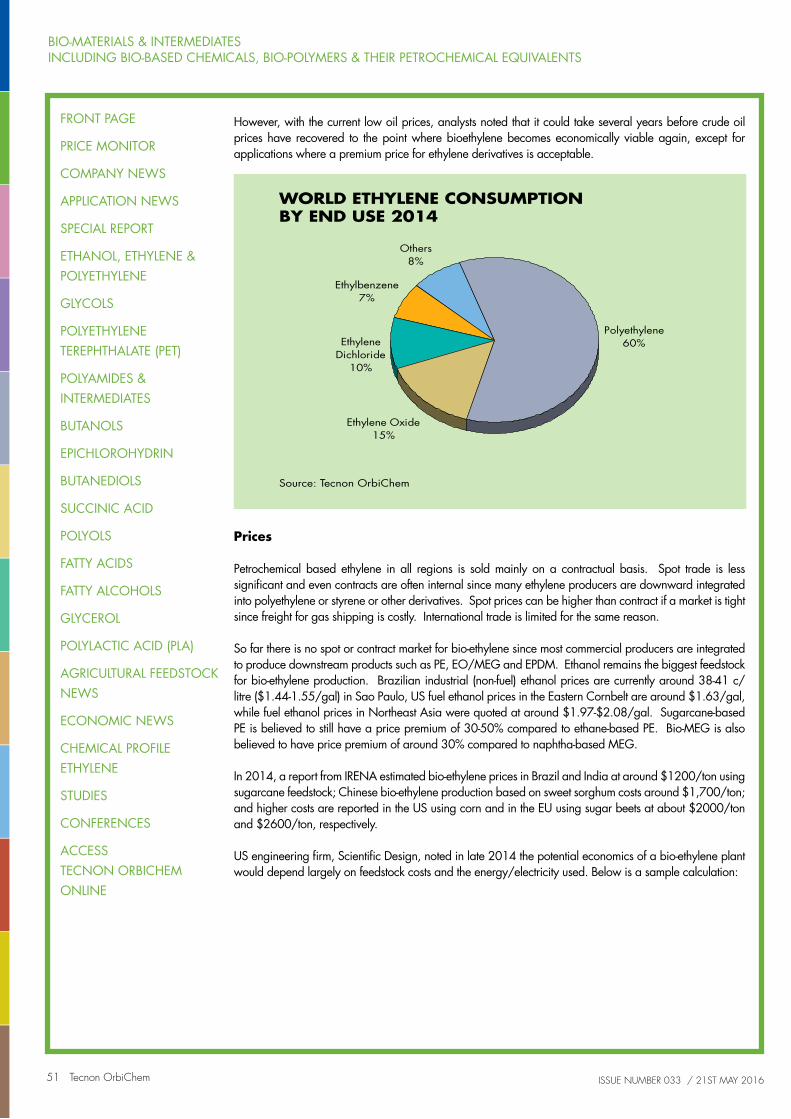

Embed Size (px)

Citation preview

BIO-M

ATERIALS &

INTERM

EDIATESIN

CLU

DIN

G BIO

-BASED

CH

EMIC

ALS, BIO

-POLYM

ERS & TH

EIR PETROC

HEM

ICA

L EQU

IVALEN

TS

A MONTHLY ROUNDUP AND ANALYSIS OF THE KEY FACTORS SHAPING WORLD CHEMICAL MARKETS

CHEMICAL BUSINESS FOCUS

CONTACT: PHILIPPA DAVIESEmail: [email protected] Follow us on

ISSUE NUMBER 3331ST MAY 2016

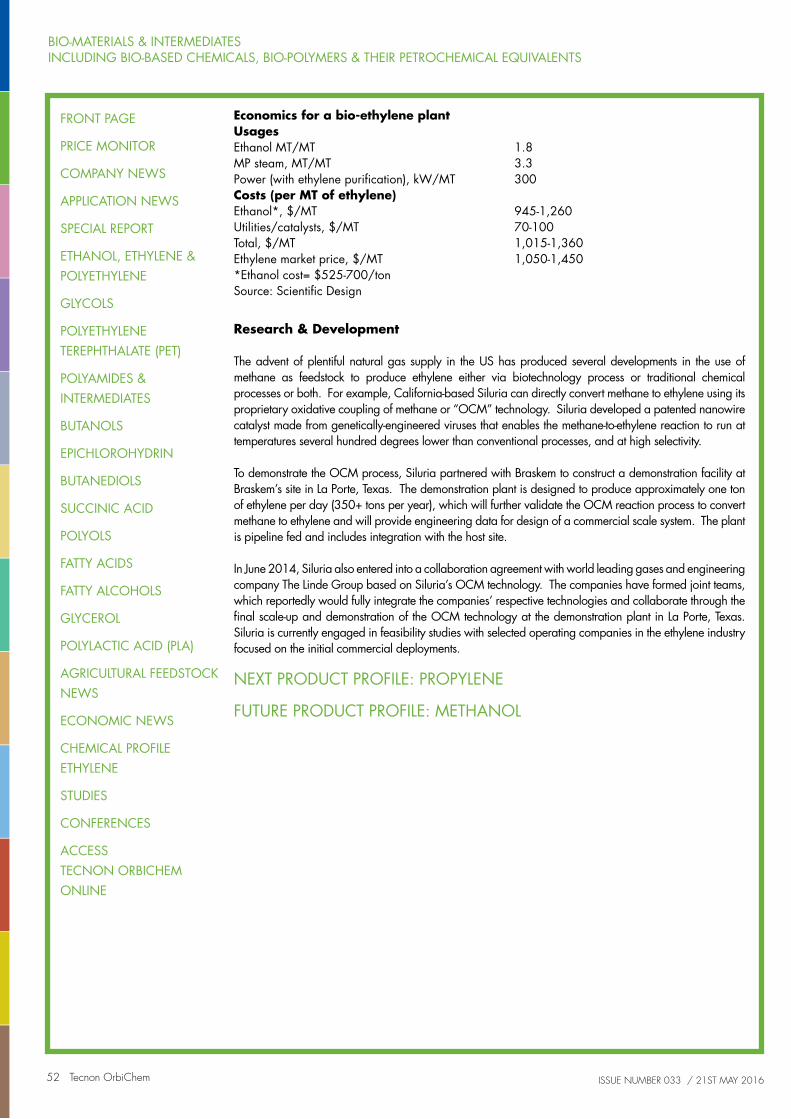

SPECIAL REPORTSBio-based surfactants continue to see growth opportunities

Malonic Acid: Lygos, Sirrus in malonates R&D

Ethanol, Ethylene & PolyethyleneClariant to scale-up Gevo’s ethanol-to-olefins technology

GlycolsAvatherm launches bio-based heat transfer fluid as alternative to petro-glycols

Polyethylene Terephthalate (PET)Valmet and Biochemtex collaborate on developing lignin-derived chemicals

Polyamides & IntermediatesStora Enso and Rennovia in bio-based chemicals partnership

ButanolsGevo ships a railcar of bio-isobutanol in the first quarter

Epichlorohydrin & Epoxy ResinsToyota uses biohydrin rubber in engine and drive system hoses

ButanediolsUS petro-BDO market buoyant on strong demand from automotive industry

Succinic AcidReverdia, Wageningen UR collaborate on bio-PBS compounds development in durables

Polyols & PolyurethanesFord to use CO2-based polyols in vehicles

Fatty AcidsGlobal fatty acid prices remain stable despite oversupplied Asian market

Fatty AlcoholsSynthetic mid-cut alcohols continue to gain market share in the US

GlycerolUS glycerine supply is getting long due to imports, competition

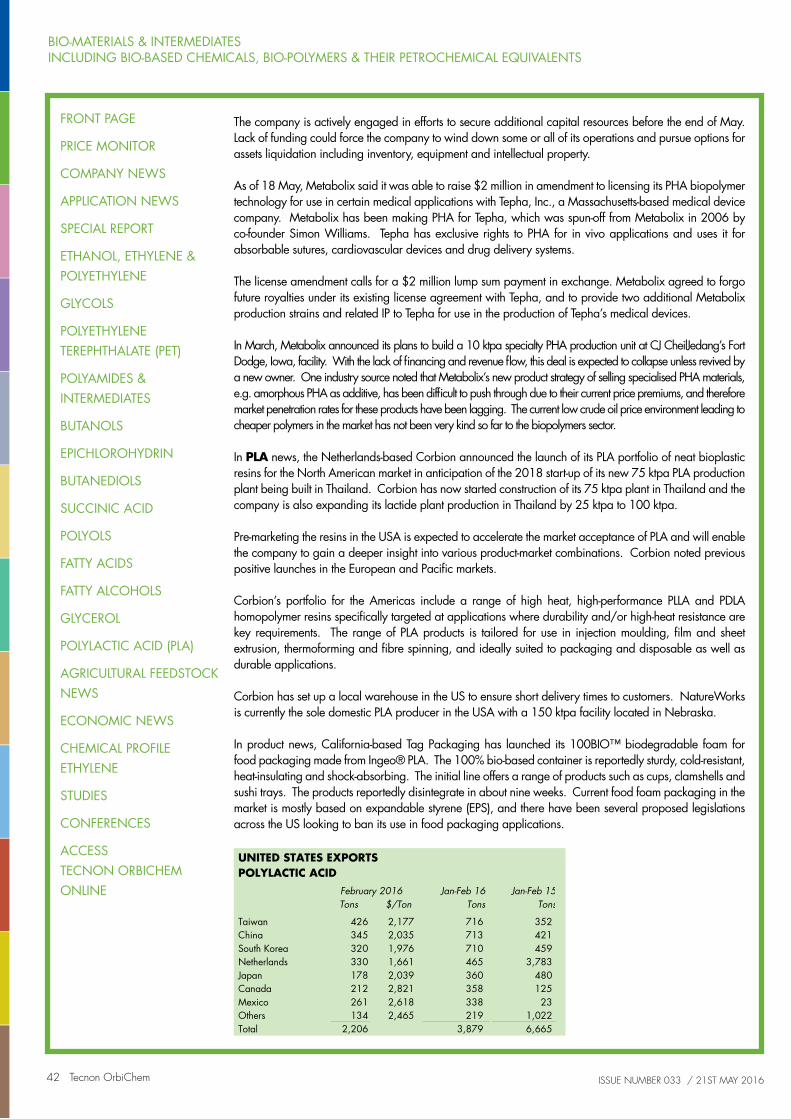

PLA & PHAMetabolix plans to divest its PHA business and Yield10 Bioscience program

CHEMICAL PROFILE: ETHYLENE

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

2 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

PRICE MONITORUS PRICES

Feb-2016 Mar-2016 31-May-2016Apr-2016 31-May-2016

¢/lb ¢/lb $/ton¢/lb ¢/lb

25.75 29.75 DDP N.A.Contract MonthlyEthylene 30.50 N.A.

22.00 - 25.00 26.00 - 29.00 FOB 551 - 661SpotMEG 29.00 - 33.00 25.00 - 30.00

28.6 - 32.5 30.8 - 35.0 FOB 772 - 926Bio-based 37.7 - 42.9 35.0 - 42.0

$/ton $/ton $/ton$/ton $/ton

640 - 665 690 - 720 FOB 710 - 730SpotParaxylene 700 - 720 710 - 730

¢/lb ¢/lb $/ton¢/lb ¢/lb

38.90 39.73 DDP 917ContractPTA 41.27 ¶ 41.60 ¶

66.00 - 69.50 66.75 - 70.00 DDP 1499 - 1554Bottle PolymerPolyester 68.50 - 71.50 ‡ 68.00 - 70.50

77.10 - 80.50 80.40 - 84.00 DDP 1799 - 1865Bottle Polymer Bio-based 82.80 - 87.60 81.60 - 84.60

70 - 80 70 - 80 DDP 1764 - 1874ContractAdipic Acid 75 - 85 80 - 85

70 - 76 70 - 76 EXW 1587 - 1698Industrial Grade ContractMonopropylene Glycol 72 - 77 72 - 77

$/ton $/ton $/ton$/ton $/ton

620 N.A. FOB N.A.Exportn-Butanol N.A. N.A.

¢/lb ¢/lb $/ton¢/lb ¢/lb

59.4 - 69.4 61.5 - 71.5 DDP 1371 - 1592ContractEpichlorohydrin 62.2 - 72.2 62.2 - 72.2

107 - 110 107 - 110 DDP 2293 - 2359Contract Quarterly1,4-Butanediol 104 - 107 104 - 107

86.5 - 103.0 86.5 - 103.0 DDP 1907 - 2271ContractSuccinic Acid 86.5 - 103.0 86.5 - 103.0

91.0 - 109.0 91.0 - 109.0 DDP 2006 - 2403Bio-based 91.0 - 109.0 91.0 - 109.0

90 - 95 88 - 94 DDP 2050 - 2161Flexible, slabstockPolyether Polyols 89 - 95 93 - 98 †

$/ton $/ton $/ton$/ton $/ton

850 - 1025 850 - 1025 DDP 950 - 1100Stearic Acid ContractFatty Acids (Bio-based) 950 - 1100 950 - 1100

1200 - 1300 1200 - 1300 DDP 1290 - 1400Oleic Acid Contract 1290 - 1400 1290 - 1400

1250 - 1350 1100 - 1500 DDP 1200 - 1900C12-C15 ContractFatty Alcohols (Bio-based) 1100 - 1900 ‡ 1200 - 1900

1200 - 1300 1200 - 1300 DDP 1350 - 1500C16-C18 Contract 1350 - 1500 1350 - 1500

650 - 800 600 - 750 DDP 650 - 750Refined Glycerine ContractGlycerol (Bio-based) 650 - 800 650 - 750

150 - 200 130 - 170 DDP 130 - 170Crude Glycerine Spot 130 - 170 130 - 170

€: 0.898 £: 0.684 (1/1.462)

US$: 1.114 £: 0.762 (1/1.313) Yen: 123.7

Current one US dollar equivalent (30-May-2016)

Current one € equivalent (30-May-2016)

Yen: 111.1 NT$: 32.64 Won: 1191.80 Rmb: 6.58 Rs: 67.22

N.A. = Not Available † = Provisional ‡ = Revised ¶ = Provisional and See Text

Information contained in this report is obtained from sources believed to be reliable, however no responsibility nor liability will be accepted by Tecnon OrbiChem for commercial decisions claimed to have been based on the content of the report.

Reproduction of any part of this work by any process whatsoever without written permission of Tecnon OrbiChem is strictly forbidden.

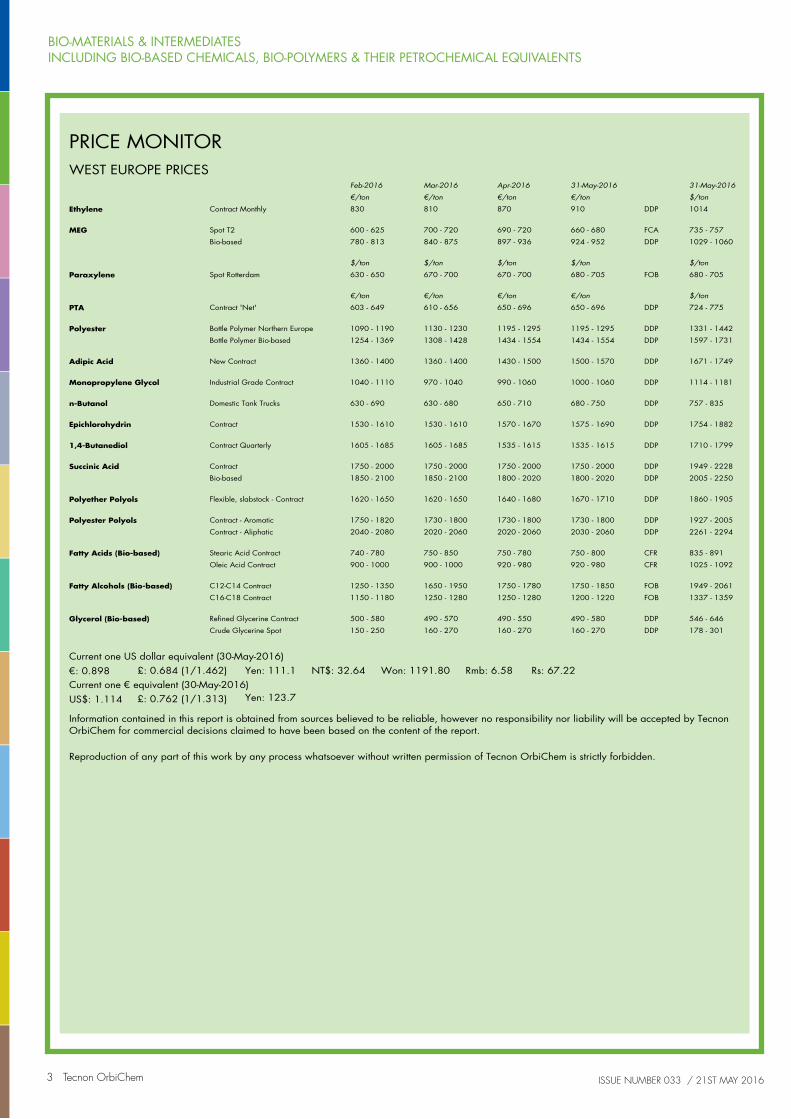

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

3 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

PRICE MONITORWEST EUROPE PRICES

Feb-2016 Mar-2016 31-May-2016Apr-2016 31-May-2016

€/ton €/ton $/ton€/ton €/ton

830 810 DDP 1014Contract MonthlyEthylene 870 910

600 - 625 700 - 720 FCA 735 - 757Spot T2MEG 690 - 720 660 - 680

780 - 813 840 - 875 DDP 1029 - 1060Bio-based 897 - 936 924 - 952

$/ton $/ton $/ton$/ton $/ton

630 - 650 670 - 700 FOB 680 - 705Spot RotterdamParaxylene 670 - 700 680 - 705

€/ton €/ton $/ton€/ton €/ton

603 - 649 610 - 656 DDP 724 - 775Contract 'Net'PTA 650 - 696 650 - 696

1090 - 1190 1130 - 1230 DDP 1331 - 1442Bottle Polymer Northern EuropePolyester 1195 - 1295 1195 - 1295

1254 - 1369 1308 - 1428 DDP 1597 - 1731Bottle Polymer Bio-based 1434 - 1554 1434 - 1554

1360 - 1400 1360 - 1400 DDP 1671 - 1749New ContractAdipic Acid 1430 - 1500 1500 - 1570

1040 - 1110 970 - 1040 DDP 1114 - 1181Industrial Grade ContractMonopropylene Glycol 990 - 1060 1000 - 1060

630 - 690 630 - 680 DDP 757 - 835Domestic Tank Trucksn-Butanol 650 - 710 680 - 750

1530 - 1610 1530 - 1610 DDP 1754 - 1882ContractEpichlorohydrin 1570 - 1670 1575 - 1690

1605 - 1685 1605 - 1685 DDP 1710 - 1799Contract Quarterly1,4-Butanediol 1535 - 1615 1535 - 1615

1750 - 2000 1750 - 2000 DDP 1949 - 2228ContractSuccinic Acid 1750 - 2000 1750 - 2000

1850 - 2100 1850 - 2100 DDP 2005 - 2250Bio-based 1800 - 2020 1800 - 2020

1620 - 1650 1620 - 1650 DDP 1860 - 1905Flexible, slabstock - ContractPolyether Polyols 1640 - 1680 1670 - 1710

1750 - 1820 1730 - 1800 DDP 1927 - 2005Contract - AromaticPolyester Polyols 1730 - 1800 1730 - 1800

2040 - 2080 2020 - 2060 DDP 2261 - 2294Contract - Aliphatic 2020 - 2060 2030 - 2060

740 - 780 750 - 850 CFR 835 - 891Stearic Acid ContractFatty Acids (Bio-based) 750 - 780 750 - 800

900 - 1000 900 - 1000 CFR 1025 - 1092Oleic Acid Contract 920 - 980 920 - 980

1250 - 1350 1650 - 1950 FOB 1949 - 2061C12-C14 ContractFatty Alcohols (Bio-based) 1750 - 1780 1750 - 1850

1150 - 1180 1250 - 1280 FOB 1337 - 1359C16-C18 Contract 1250 - 1280 1200 - 1220

500 - 580 490 - 570 DDP 546 - 646Refined Glycerine ContractGlycerol (Bio-based) 490 - 550 490 - 580

150 - 250 160 - 270 DDP 178 - 301Crude Glycerine Spot 160 - 270 160 - 270

€: 0.898 £: 0.684 (1/1.462)

US$: 1.114 £: 0.762 (1/1.313) Yen: 123.7

Current one US dollar equivalent (30-May-2016)

Current one € equivalent (30-May-2016)

Yen: 111.1 NT$: 32.64 Won: 1191.80 Rmb: 6.58 Rs: 67.22

Information contained in this report is obtained from sources believed to be reliable, however no responsibility nor liability will be accepted by Tecnon OrbiChem for commercial decisions claimed to have been based on the content of the report.

Reproduction of any part of this work by any process whatsoever without written permission of Tecnon OrbiChem is strictly forbidden.

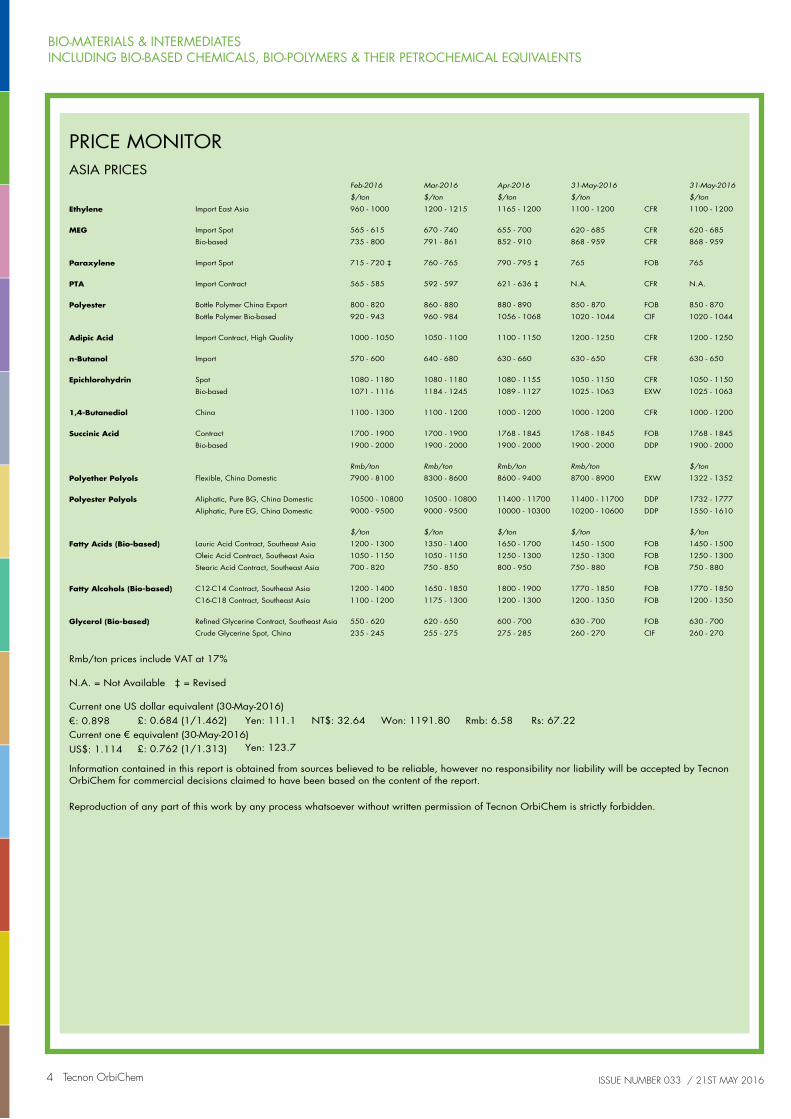

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

4 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

PRICE MONITORASIA PRICES

Feb-2016 Mar-2016 31-May-2016Apr-2016 31-May-2016

$/ton $/ton $/ton$/ton $/ton

960 - 1000 1200 - 1215 CFR 1100 - 1200Import East AsiaEthylene 1165 - 1200 1100 - 1200

565 - 615 670 - 740 CFR 620 - 685Import SpotMEG 655 - 700 620 - 685

735 - 800 791 - 861 CFR 868 - 959Bio-based 852 - 910 868 - 959

715 - 720 ‡ 760 - 765 FOB 765Import SpotParaxylene 790 - 795 ‡ 765

565 - 585 592 - 597 CFR N.A.Import ContractPTA 621 - 636 ‡ N.A.

800 - 820 860 - 880 FOB 850 - 870Bottle Polymer China ExportPolyester 880 - 890 850 - 870

920 - 943 960 - 984 CIF 1020 - 1044Bottle Polymer Bio-based 1056 - 1068 1020 - 1044

1000 - 1050 1050 - 1100 CFR 1200 - 1250Import Contract, High QualityAdipic Acid 1100 - 1150 1200 - 1250

570 - 600 640 - 680 CFR 630 - 650Importn-Butanol 630 - 660 630 - 650

1080 - 1180 1080 - 1180 CFR 1050 - 1150SpotEpichlorohydrin 1080 - 1155 1050 - 1150

1071 - 1116 1184 - 1245 EXW 1025 - 1063Bio-based 1089 - 1127 1025 - 1063

1100 - 1300 1100 - 1200 CFR 1000 - 1200China1,4-Butanediol 1000 - 1200 1000 - 1200

1700 - 1900 1700 - 1900 FOB 1768 - 1845ContractSuccinic Acid 1768 - 1845 1768 - 1845

1900 - 2000 1900 - 2000 DDP 1900 - 2000Bio-based 1900 - 2000 1900 - 2000

Rmb/ton Rmb/ton $/tonRmb/ton Rmb/ton

7900 - 8100 8300 - 8600 EXW 1322 - 1352Flexible, China DomesticPolyether Polyols 8600 - 9400 8700 - 8900

10500 - 10800 10500 - 10800 DDP 1732 - 1777Aliphatic, Pure BG, China DomesticPolyester Polyols 11400 - 11700 11400 - 11700

9000 - 9500 9000 - 9500 DDP 1550 - 1610Aliphatic, Pure EG, China Domestic 10000 - 10300 10200 - 10600

$/ton $/ton $/ton$/ton $/ton

1200 - 1300 1350 - 1400 FOB 1450 - 1500Lauric Acid Contract, Southeast AsiaFatty Acids (Bio-based) 1650 - 1700 1450 - 1500

1050 - 1150 1050 - 1150 FOB 1250 - 1300Oleic Acid Contract, Southeast Asia 1250 - 1300 1250 - 1300

700 - 820 750 - 850 FOB 750 - 880Stearic Acid Contract, Southeast Asia 800 - 950 750 - 880

1200 - 1400 1650 - 1850 FOB 1770 - 1850C12-C14 Contract, Southeast AsiaFatty Alcohols (Bio-based) 1800 - 1900 1770 - 1850

1100 - 1200 1175 - 1300 FOB 1200 - 1350C16-C18 Contract, Southeast Asia 1200 - 1300 1200 - 1350

550 - 620 620 - 650 FOB 630 - 700Refined Glycerine Contract, Southeast AsiaGlycerol (Bio-based) 600 - 700 630 - 700

235 - 245 255 - 275 CIF 260 - 270Crude Glycerine Spot, China 275 - 285 260 - 270

€: 0.898 £: 0.684 (1/1.462)

US$: 1.114 £: 0.762 (1/1.313) Yen: 123.7

Current one US dollar equivalent (30-May-2016)

Current one € equivalent (30-May-2016)

Yen: 111.1 NT$: 32.64 Won: 1191.80 Rmb: 6.58 Rs: 67.22

Rmb/ton prices include VAT at 17%

N.A. = Not Available ‡ = Revised

Information contained in this report is obtained from sources believed to be reliable, however no responsibility nor liability will be accepted by Tecnon OrbiChem for commercial decisions claimed to have been based on the content of the report.

Reproduction of any part of this work by any process whatsoever without written permission of Tecnon OrbiChem is strictly forbidden.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

5 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

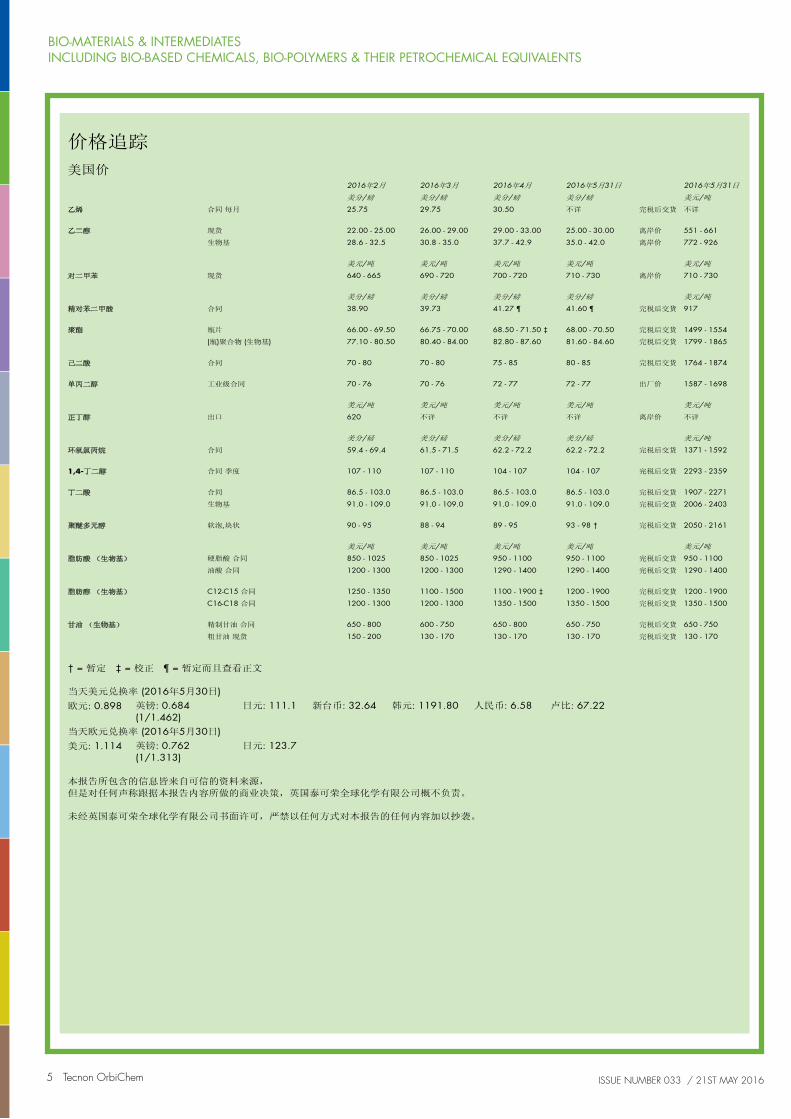

价格追踪

美国价2016年2月 2016年3月 2016年5月31日2016年4月 2016年5月31日

美分/磅 美分/磅 美元/吨美分/磅 美分/磅

25.75 29.75 完税后交货 不详合同 每月乙烯 30.50 不详

22.00 - 25.00 26.00 - 29.00 离岸价 551 - 661现货乙二醇 29.00 - 33.00 25.00 - 30.00

28.6 - 32.5 30.8 - 35.0 离岸价 772 - 926生物基 37.7 - 42.9 35.0 - 42.0

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

640 - 665 690 - 720 离岸价 710 - 730现货对二甲苯 700 - 720 710 - 730

美分/磅 美分/磅 美元/吨美分/磅 美分/磅

38.90 39.73 完税后交货 917合同精对苯二甲酸 41.27 ¶ 41.60 ¶

66.00 - 69.50 66.75 - 70.00 完税后交货 1499 - 1554瓶片聚酯 68.50 - 71.50 ‡ 68.00 - 70.50

77.10 - 80.50 80.40 - 84.00 完税后交货 1799 - 1865(瓶)聚合物 (生物基) 82.80 - 87.60 81.60 - 84.60

70 - 80 70 - 80 完税后交货 1764 - 1874合同己二酸 75 - 85 80 - 85

70 - 76 70 - 76 出厂价 1587 - 1698工业级合同单丙二醇 72 - 77 72 - 77

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

620 不详 离岸价 不详出口正丁醇 不详 不详

美分/磅 美分/磅 美元/吨美分/磅 美分/磅

59.4 - 69.4 61.5 - 71.5 完税后交货 1371 - 1592合同环氧氯丙烷 62.2 - 72.2 62.2 - 72.2

107 - 110 107 - 110 完税后交货 2293 - 2359合同 季度1,4-丁二醇 104 - 107 104 - 107

86.5 - 103.0 86.5 - 103.0 完税后交货 1907 - 2271合同丁二酸 86.5 - 103.0 86.5 - 103.0

91.0 - 109.0 91.0 - 109.0 完税后交货 2006 - 2403生物基 91.0 - 109.0 91.0 - 109.0

90 - 95 88 - 94 完税后交货 2050 - 2161软泡,块状聚醚多元醇 89 - 95 93 - 98 †

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

850 - 1025 850 - 1025 完税后交货 950 - 1100硬脂酸 合同脂肪酸 (生物基) 950 - 1100 950 - 1100

1200 - 1300 1200 - 1300 完税后交货 1290 - 1400油酸 合同 1290 - 1400 1290 - 1400

1250 - 1350 1100 - 1500 完税后交货 1200 - 1900C12-C15 合同脂肪醇 (生物基) 1100 - 1900 ‡ 1200 - 1900

1200 - 1300 1200 - 1300 完税后交货 1350 - 1500C16-C18 合同 1350 - 1500 1350 - 1500

650 - 800 600 - 750 完税后交货 650 - 750精制甘油 合同甘油 (生物基) 650 - 800 650 - 750

150 - 200 130 - 170 完税后交货 130 - 170粗甘油 现货 130 - 170 130 - 170

本报告所包含的信息皆来自可信的资料来源,

但是对任何声称跟据本报告内容所做的商业决策,英国泰可荣全球化学有限公司概不负责。

未经英国泰可荣全球化学有限公司书面许可,严禁以任何方式对本报告的任何内容加以抄袭。

欧元: 0.898 英镑: 0.684 (1/1.462)

美元: 1.114 英镑: 0.762 (1/1.313)

日元: 123.7

当天美元兑换率 (2016年5月30日)

当天欧元兑换率 (2016年5月30日)

日元: 111.1 新台币: 32.64 韩元: 1191.80 人民币: 6.58 卢比: 67.22

† = 暂定 ‡ = 校正 ¶ = 暂定而且查看正文

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

6 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

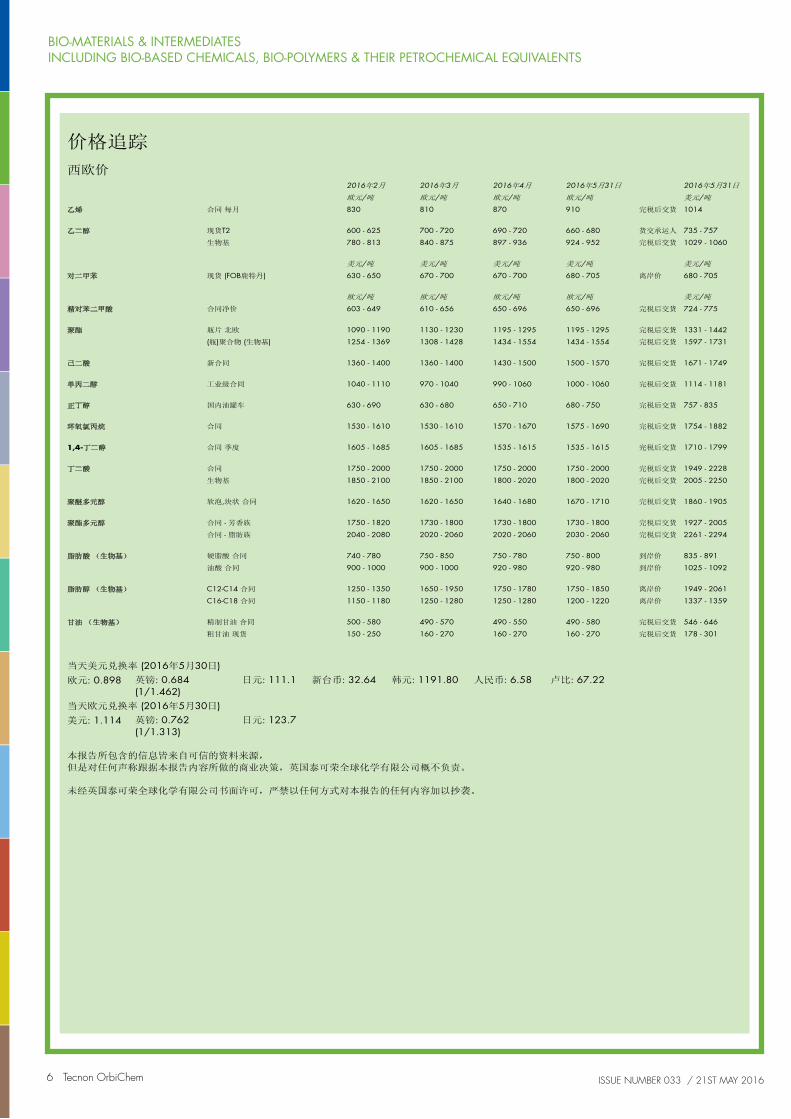

价格追踪

西欧价2016年2月 2016年3月 2016年5月31日2016年4月 2016年5月31日

欧元/吨 欧元/吨 美元/吨欧元/吨 欧元/吨

830 810 完税后交货 1014合同 每月乙烯 870 910

600 - 625 700 - 720 货交承运人 735 - 757现货T2乙二醇 690 - 720 660 - 680

780 - 813 840 - 875 完税后交货 1029 - 1060生物基 897 - 936 924 - 952

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

630 - 650 670 - 700 离岸价 680 - 705现货 (FOB鹿特丹)对二甲苯 670 - 700 680 - 705

欧元/吨 欧元/吨 美元/吨欧元/吨 欧元/吨

603 - 649 610 - 656 完税后交货 724 - 775合同净价精对苯二甲酸 650 - 696 650 - 696

1090 - 1190 1130 - 1230 完税后交货 1331 - 1442瓶片 北欧聚酯 1195 - 1295 1195 - 1295

1254 - 1369 1308 - 1428 完税后交货 1597 - 1731(瓶)聚合物 (生物基) 1434 - 1554 1434 - 1554

1360 - 1400 1360 - 1400 完税后交货 1671 - 1749新合同己二酸 1430 - 1500 1500 - 1570

1040 - 1110 970 - 1040 完税后交货 1114 - 1181工业级合同单丙二醇 990 - 1060 1000 - 1060

630 - 690 630 - 680 完税后交货 757 - 835国内油罐车正丁醇 650 - 710 680 - 750

1530 - 1610 1530 - 1610 完税后交货 1754 - 1882合同环氧氯丙烷 1570 - 1670 1575 - 1690

1605 - 1685 1605 - 1685 完税后交货 1710 - 1799合同 季度1,4-丁二醇 1535 - 1615 1535 - 1615

1750 - 2000 1750 - 2000 完税后交货 1949 - 2228合同丁二酸 1750 - 2000 1750 - 2000

1850 - 2100 1850 - 2100 完税后交货 2005 - 2250生物基 1800 - 2020 1800 - 2020

1620 - 1650 1620 - 1650 完税后交货 1860 - 1905软泡,块状 合同聚醚多元醇 1640 - 1680 1670 - 1710

1750 - 1820 1730 - 1800 完税后交货 1927 - 2005合同 - 芳香族聚酯多元醇 1730 - 1800 1730 - 1800

2040 - 2080 2020 - 2060 完税后交货 2261 - 2294合同 - 脂肪族 2020 - 2060 2030 - 2060

740 - 780 750 - 850 到岸价 835 - 891硬脂酸 合同脂肪酸 (生物基) 750 - 780 750 - 800

900 - 1000 900 - 1000 到岸价 1025 - 1092油酸 合同 920 - 980 920 - 980

1250 - 1350 1650 - 1950 离岸价 1949 - 2061C12-C14 合同脂肪醇 (生物基) 1750 - 1780 1750 - 1850

1150 - 1180 1250 - 1280 离岸价 1337 - 1359C16-C18 合同 1250 - 1280 1200 - 1220

500 - 580 490 - 570 完税后交货 546 - 646精制甘油 合同甘油 (生物基) 490 - 550 490 - 580

150 - 250 160 - 270 完税后交货 178 - 301粗甘油 现货 160 - 270 160 - 270

本报告所包含的信息皆来自可信的资料来源,

但是对任何声称跟据本报告内容所做的商业决策,英国泰可荣全球化学有限公司概不负责。

未经英国泰可荣全球化学有限公司书面许可,严禁以任何方式对本报告的任何内容加以抄袭。

欧元: 0.898 英镑: 0.684 (1/1.462)

美元: 1.114 英镑: 0.762 (1/1.313)

日元: 123.7

当天美元兑换率 (2016年5月30日)

当天欧元兑换率 (2016年5月30日)

日元: 111.1 新台币: 32.64 韩元: 1191.80 人民币: 6.58 卢比: 67.22

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

7 Tecnon OrbiChem ISSUE NUMBER 033 / 21ST MAY 2016

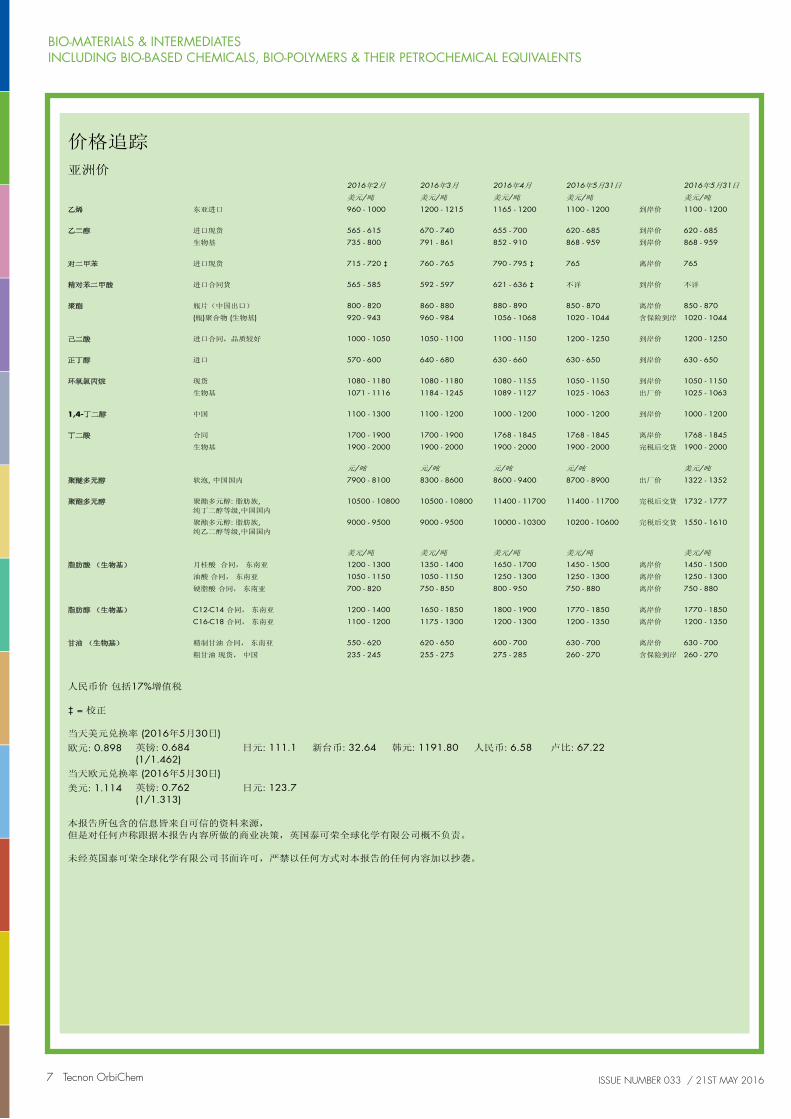

价格追踪

亚洲价2016年2月 2016年3月 2016年5月31日2016年4月 2016年5月31日

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

960 - 1000 1200 - 1215 到岸价 1100 - 1200东亚进口乙烯 1165 - 1200 1100 - 1200

565 - 615 670 - 740 到岸价 620 - 685进口现货乙二醇 655 - 700 620 - 685

735 - 800 791 - 861 到岸价 868 - 959生物基 852 - 910 868 - 959

715 - 720 ‡ 760 - 765 离岸价 765进口现货对二甲苯 790 - 795 ‡ 765

565 - 585 592 - 597 到岸价 不详进口合同货精对苯二甲酸 621 - 636 ‡ 不详

800 - 820 860 - 880 离岸价 850 - 870瓶片(中国出口)聚酯 880 - 890 850 - 870

920 - 943 960 - 984 含保险到岸 1020 - 1044(瓶)聚合物 (生物基) 1056 - 1068 1020 - 1044

1000 - 1050 1050 - 1100 到岸价 1200 - 1250进口合同,品质较好己二酸 1100 - 1150 1200 - 1250

570 - 600 640 - 680 到岸价 630 - 650进口正丁醇 630 - 660 630 - 650

1080 - 1180 1080 - 1180 到岸价 1050 - 1150现货环氧氯丙烷 1080 - 1155 1050 - 1150

1071 - 1116 1184 - 1245 出厂价 1025 - 1063生物基 1089 - 1127 1025 - 1063

1100 - 1300 1100 - 1200 到岸价 1000 - 1200中国1,4-丁二醇 1000 - 1200 1000 - 1200

1700 - 1900 1700 - 1900 离岸价 1768 - 1845合同丁二酸 1768 - 1845 1768 - 1845

1900 - 2000 1900 - 2000 完税后交货 1900 - 2000生物基 1900 - 2000 1900 - 2000

元/吨 元/吨 美元/吨元/吨 元/吨

7900 - 8100 8300 - 8600 出厂价 1322 - 1352软泡, 中国国内聚醚多元醇 8600 - 9400 8700 - 8900

10500 - 10800 10500 - 10800 完税后交货 1732 - 1777聚酯多元醇: 脂肪族, 纯丁二醇等级,中国国内

聚酯多元醇 11400 - 11700 11400 - 11700

9000 - 9500 9000 - 9500 完税后交货 1550 - 1610聚酯多元醇: 脂肪族, 纯乙二醇等级,中国国内

10000 - 10300 10200 - 10600

美元/吨 美元/吨 美元/吨美元/吨 美元/吨

1200 - 1300 1350 - 1400 离岸价 1450 - 1500月桂酸 合同, 东南亚脂肪酸 (生物基) 1650 - 1700 1450 - 1500

1050 - 1150 1050 - 1150 离岸价 1250 - 1300油酸 合同, 东南亚 1250 - 1300 1250 - 1300

700 - 820 750 - 850 离岸价 750 - 880硬脂酸 合同, 东南亚 800 - 950 750 - 880

1200 - 1400 1650 - 1850 离岸价 1770 - 1850C12-C14 合同, 东南亚脂肪醇 (生物基) 1800 - 1900 1770 - 1850

1100 - 1200 1175 - 1300 离岸价 1200 - 1350C16-C18 合同, 东南亚 1200 - 1300 1200 - 1350

550 - 620 620 - 650 离岸价 630 - 700精制甘油 合同, 东南亚甘油 (生物基) 600 - 700 630 - 700

235 - 245 255 - 275 含保险到岸 260 - 270粗甘油 现货, 中国 275 - 285 260 - 270

本报告所包含的信息皆来自可信的资料来源,

但是对任何声称跟据本报告内容所做的商业决策,英国泰可荣全球化学有限公司概不负责。

未经英国泰可荣全球化学有限公司书面许可,严禁以任何方式对本报告的任何内容加以抄袭。

欧元: 0.898 英镑: 0.684 (1/1.462)

美元: 1.114 英镑: 0.762 (1/1.313)

日元: 123.7

当天美元兑换率 (2016年5月30日)

当天欧元兑换率 (2016年5月30日)

日元: 111.1 新台币: 32.64 韩元: 1191.80 人民币: 6.58 卢比: 67.22

人民币价 包括17%增值税

‡ = 校正

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

8 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

COMPANY NEWS

Americas

Amyris has signed a MOU with South Korea-based CJ Cheiljedang for the large-scale manufacturing of Amyris’s farnesene in existing CJ facilities. The partnership is also expected to include the opportunity for CJ Bio (a division of CJ Cheiljedang) to market select Amyris products in Asian markets as well as the potential for Amyris to develop several products for CJ Bio. The companies expect to complete a definitive agreement by the first week of August.

Bolt Threads, a California-based biotechnology company, has raised $50 million in series C financing. The company reportedly attracted the interest of new investors and partners, including Patagonia, a sports apparel company. Bolt Threads has partnered with Patagonia to further develop the company’s fabric using Bolt Threads’ Engineered Silk™ protein and the company is moving into yarn manufacturing this summer. Bolt’s silk protein is made primarily of sugar, water, salts and yeast, and through a process called wet spinning, this liquid is spun into fibre, similar to the way fibres like acrylic and rayon are made. Other companies in this space include Japanese start-up Spiber, and German company, Amsilk.

CO2 Solutions Inc. and Mojonnier Limited, have partnered to integrate Mojonnier’s GTS rotating packing bed (RPB) mass transfer technology now used in Mojonnier’s beverage equipment, with CO2 Solutions’ enzyme based carbon capture process. Mojonnier has an established client list in the beverage industry and with CO2 Solutions, they will jointly market a low-cost and environment-friendly solution for the supply of CO2 to this sector. Bottlers typically have to purchase CO2 for their beverages from commercial sources at a substantial cost. The joint solution closes the loop and allows for the reuse of the boiler-emitted CO2 from bottling sterilisation operations.

Eastman Chemical Company has entered a definitive agreement with Solvay to sell its 50% stake in the Kingsport, Tennessee, cellulose acetate flake joint venture named Primester. The transaction will allow Eastman to eliminate costs associated with the excess cellulose acetate flake capacity of the JV. Eastman has completed a small capital investment to increase flake capacity at the site. The company said it is no longer necessary for Eastman to support the fixed costs of Primester to have sufficient cellulose acetate flake capacity in order to reliably supply its acetate tow capacity around the world. Eastman has also shut down its UK acetate tow site last year. Eastman will continue to supply certain services, utilities and raw materials to Primester for Solvay’s operation of the former JV assets. The sale is expected to close in second quarter 2016.

The US Department of Energy (DOE) announced up to $90 million funding focused on designing, constructing and operating integrated biorefinery facilities under the Project Development for Pilot and Demonstration Scale Manufacturing of Biofuels, Bioproducts and Biopower program. The funding is meant to assist in the construction of bioenergy infrastructure to integrate cutting-edge pretreatment, process, and convergence technologies.

Weyerhauser Company will sell its cellulose fibres pulp mill to International Paper for $2.2 billion in cash. The transaction includes five pulp mills located in Mississippi, North Carolina, two mills in Georgia, and one in Alberta, Canada, with a total combined capacity of nearly 1.9 million tons. The sale also includes two modified fibre mills in Mississippi and Gdansk, Poland. The transaction does not include Weyerhauser’s liquid packaging board facility or newsprint and publishing papers joint venture, which are currently being reviewed by the company. The deal is expected to close in the fourth quarter of 2016.

West Europe

AkzoNobel and Royal Cosun, an agro-industrial cooperative based in the Netherlands, have formed a new partnership to develop novel products from cellulose side streams of sugar beet processing. The partnership will combine Cosun’s specialist knowledge in separation and purification of agricultural process side streams with AkzoNobel’s expertise in the chemical modification of cellulose. The companies did not disclose specific chemical products targeted by the collaboration.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

9 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

Deinove, a France-based biotechnology company, has partnered with Toulouse White Biotechnology to optimise Deinove’s Deinococcus production. The project aims to map the metabolic fluxes of the Deinococcus chassis, i.e. to create an inventory of all the potentialities of the microorganism in the production of molecules of interest. This mapping will serve as reference to identify and optimise all the metabolic pathways of the Deinoccocus model to rapidly reach the target yield and productivity of industrial processes developed by Deinove.

Hempel A/S, a Denmark-based coatings supplier, has developed a renewable-based anti-fouling marine coating under a research project sponsored by EEA Grants, which represents the contribution of Iceland, Liechtenstein, and Norway with the goal of reducing economic and social disparities in 16 EU countries. The company did not disclose raw materials used for the bio-based coating formulations. The anti-fouling coatings can reduce a vessel’s fuel consumption and associated emissions by 4-8%/year.

Pentair Haffmans, the Netherlands-based manufacturer of quality control and process equipment has introduced its skid CO2 recovery system that can be connected to any existing biogas upgrading plant, thus preventing a considerable amount of CO2 and methane to be expelled into the air. The recovered CO2 can be used in a variety of applications including gaseous fertiliser in greenhouses or for the production of dry ice. Additional options include selling liquefied CO2 to a third party. With capacities up to 1,000 kg/h, the compact enclosed CO2 recovery system is delivered as a stand-alone unit.

SABIC has inaugurated a new research facility at the Brightlands Chemelot Campus in Geleen, the Netherlands, which will support an extension of SABIC’s research in the area of innovative chemistry and materials such as its development of lightweight foamed polyolefins and renewable polymers for packaging. The company is looking to develop new and sustainable solutions together with customers and partners in markets such as transportation, packaging and building industries.

Wageningen UR Food & Bio-based Research is working on the development of environmentally-friendly resins alternatives for isocyanate-based components used for elastic rail fastening systems. The goal is to develop new resins from biomass, which cure into an elastic rubber-like compound within a limited time. The polymers can be applied as elastic sound and vibration-reducing materials. The final material should be less moisture-sensitive in processing and have a short curing time. It must meet specific mechanical material requirements and adhere well to rails and concrete.

Asia

Innovia Group, a UK-based plastic film products manufacturer, has agreed to sell its Cellophane business and assets to Futamura Chemicals Co. Ltd. based in Nagoya, Japan. Futamura is a major manufacturer of plastic and cellulose films, principally servicing the food packaging industry. Cellophane films are made from regenerated cellulose obtained from wood pulp. The Innovia Cellophane™ films have thickness ranging from 19 to 42 microns. The films are said to be naturally biodegradable but the coatings usually used in the films provide the important barrier and sealing properties that prevent Cellophane™ from being truly compostable. Uncoated Cellophane™ can be composted.

Sunlight Fuels Private Limited based in New Delhi, India, has entered a Front End Loading FEL-2 license agreement for IH2 Technology with a Singapore-based affiliate of CRI Catalyst Company LT, a global catalyst technology company of the Shell Group. IH2 is a continuous catalytic thermochemical process which produces fungible hydrocarbon transportation fuels from agriculture, forest and sorted municipal residues. The agreement is the first IH2 FEL-2 license granted in India for a commercial plant that will be designed to convert 500 tpd of dry bagasse into 150 tpd of liquid hydrocarbon transportation fuels. The plant will be adjacent to an operating sugar mill.

The Vietnam Saigon Plastic Association will reportedly focus on research to develop renewable raw materials for making plastics in the 2016-2020 period. The association will work to enable more members to join the industry’s human resource training programs arranged by the city in collaboration with French and South Korean partners. Vietnam’s plastic sector’s exports reportedly great at an average 12.9% in 2011-2015 to reach nearly $2 billion last year.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

10 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

APPLICATION NEWS

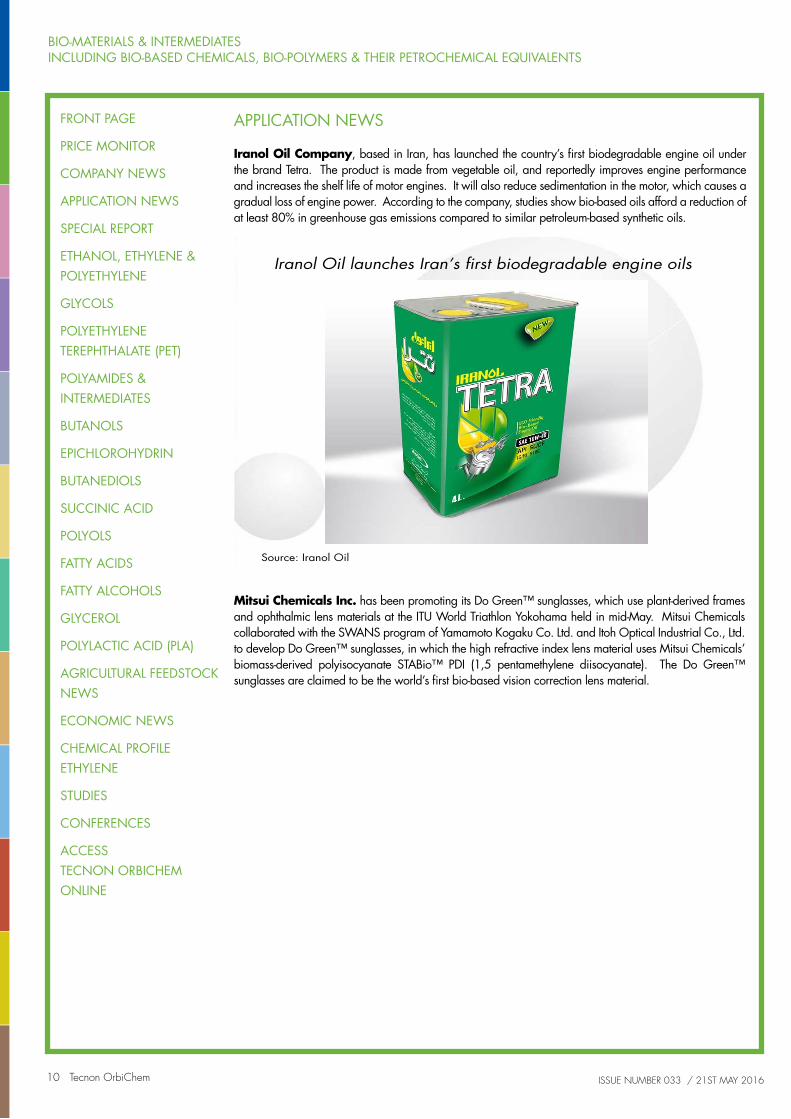

Iranol Oil Company, based in Iran, has launched the country’s first biodegradable engine oil under the brand Tetra. The product is made from vegetable oil, and reportedly improves engine performance and increases the shelf life of motor engines. It will also reduce sedimentation in the motor, which causes a gradual loss of engine power. According to the company, studies show bio-based oils afford a reduction of at least 80% in greenhouse gas emissions compared to similar petroleum-based synthetic oils.

Iranol Oil launches Iran’s first biodegradable engine oils

Source: Iranol Oil

Mitsui Chemicals Inc. has been promoting its Do Green™ sunglasses, which use plant-derived frames and ophthalmic lens materials at the ITU World Triathlon Yokohama held in mid-May. Mitsui Chemicals collaborated with the SWANS program of Yamamoto Kogaku Co. Ltd. and Itoh Optical Industrial Co., Ltd. to develop Do Green™ sunglasses, in which the high refractive index lens material uses Mitsui Chemicals’ biomass-derived polyisocyanate STABio™ PDI (1,5 pentamethylene diisocyanate). The Do Green™ sunglasses are claimed to be the world’s first bio-based vision correction lens material.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

11 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

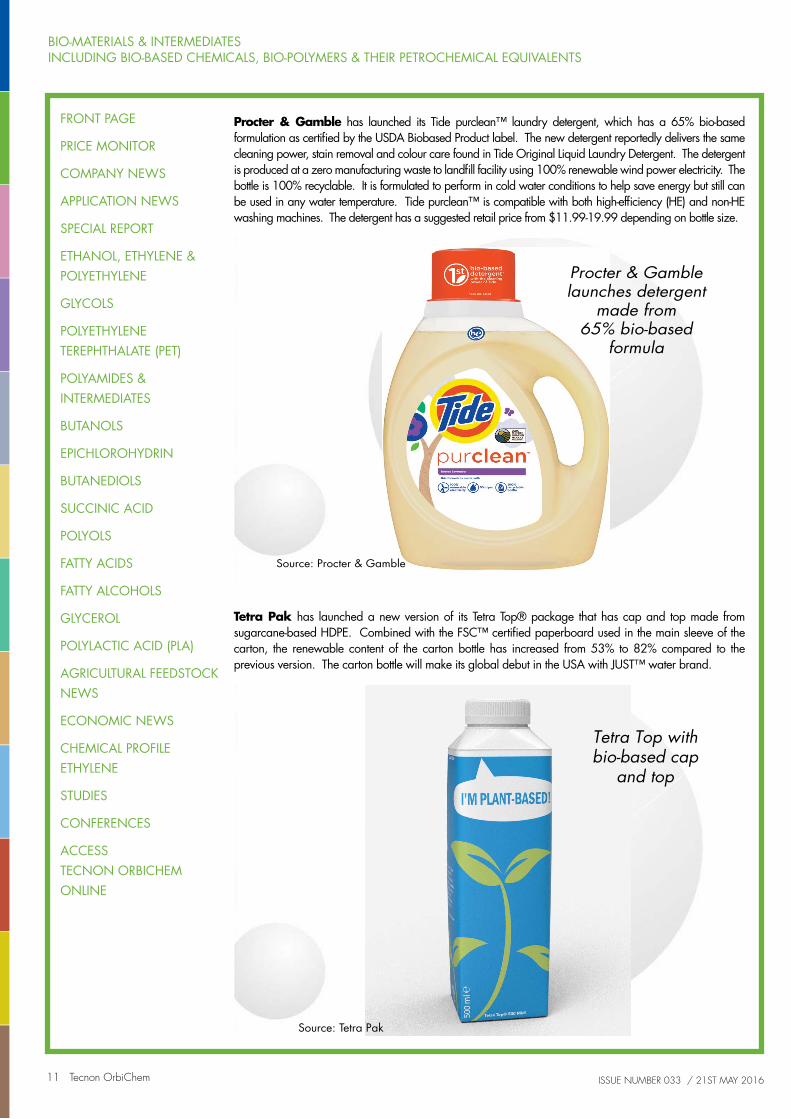

Tetra Pak has launched a new version of its Tetra Top® package that has cap and top made from sugarcane-based HDPE. Combined with the FSC™ certified paperboard used in the main sleeve of the carton, the renewable content of the carton bottle has increased from 53% to 82% compared to the previous version. The carton bottle will make its global debut in the USA with JUST™ water brand.

Procter & Gamble launches detergent

made from 65% bio-based

formula

Source: Procter & Gamble

Tetra Top with bio-based cap

and top

Source: Tetra Pak

Procter & Gamble has launched its Tide purclean™ laundry detergent, which has a 65% bio-based formulation as certified by the USDA Biobased Product label. The new detergent reportedly delivers the same cleaning power, stain removal and colour care found in Tide Original Liquid Laundry Detergent. The detergent is produced at a zero manufacturing waste to landfill facility using 100% renewable wind power electricity. The bottle is 100% recyclable. It is formulated to perform in cold water conditions to help save energy but still can be used in any water temperature. Tide purclean™ is compatible with both high-efficiency (HE) and non-HE washing machines. The detergent has a suggested retail price from $11.99-19.99 depending on bottle size.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

12 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

SPECIAL REPORTS

Bio-based surfactants continue to see growth opportunities

The recently held ICIS World Surfactants conference in New Jersey, USA, revealed the continued growing opportunities for bio-based surfactants especially in the areas of oilfield applications, agriculture and in cleaning products.

In an annual survey held by Neil A. Burns LLC, the co-producer of the surfactants conference, around 115 surfactants-related companies (buyers and sellers) noted the top three biggest opportunities within the surfactants market are the growth of emerging markets, lower crude oil prices, and bio-based products and feedstocks. Other opportunities include regulatory changes, increasing availability of shale, information technology innovations and growth of online vs physical retail,.

Bio-based feedstocks for surfactants are expected to be the fourth most important trend after regulations in the surfactants market over the next ten years. Downstream integration by bio-feedstock suppliers is expected to be a trend as the market for bio-based products grows along with changes in product preferences. However, when comparing survey data between 2015 and 2016 there was a noticeable decline of companies choosing bio-based products as an important trend for the next 10 years, from around 54% last year to 41% this year. One reason is the steep decline in crude oil prices, which has made petroleum-based surfactants more competitive. Surfactant consumers have reportedly been worried about increasing cost pressure coming from their own customers, volatility in surfactant pricing as well as a cost/performance benefit trade-off especially when trying to reformulate existing products. Surfactant manufacturers have also been worried first and foremost about the volatility in raw material pricing as well as the difficulty in coming up with new/innovative offerings.

Based on the survey, surfactant manufacturers are spending most of their R&D efforts on new applications or application technology as well as customer-specific projects and process improvements to lower costs. Surfactant users are also spending their R&D efforts first on customer-specific projects and in brand new/improved end products as well as process improvements. Surfactant users pointed out that they want pricing stability from their suppliers for more than three months, price indexing to raw materials and tailored innovations. At the conference, Johnson & Johnson, a well-known consumer packaged goods manufacturer, noted its increasing use of the Principles of Green Chemistry approach when designing formulations and products. The company pointed out its use of a biodegradable polymeric surfactant product, NATRASURF™, which is a 90% renewable product based on potato starch, and is reportedly produced using a low-energy, solvent-free process that yields zero waste. The surfactant is said to be producing a milder cleanser formulation. NATRASURF™ products, such as AVEENO® Pure Renewal™ shampoo and conditioner line, have already been rolled out within the company’s baby and adult skin care lines since December 2015.

Johnson & Johnson said it has been encouraged by the developments in biotechnology-based surfactants pointing to Evonik’s sophorolipid surfactant, Rewoferm® SL 446, which was introduced last year. Johnson & Johnson is monitoring the fermentation-based surfactants market but cautioned that bio-based alone is not a benefit citing an example that plant-based coco-betaine is more irritating to skin than its synthetic counterpart, cocamidopropyl betaine. Alkylpolyglucoside (APG) is 100% bio-based and relatively non-irritating to skin, but unfortunately, it readily solubilise skin barrier lipids and therefore not as good in providing moisturisation in skin care products.

In a panel discussion at the conference, another well-known consumer products company, Unilever, also noted its interest in biotechnology-based surfactants but pointed out that manufacturers in this space have to first prove the safety of new products as well as compliance with various regulatory requirements worldwide before Unilever can incorporate bio-surfactants into its global supply chain. A representative from Procter & Gamble Chemicals pointed out that bio-surfactants have to be cost competitive with their petrochemical counterparts, noting the company’s initial cost projections for bio-surfactants use have not even included the possibility of crude oil costs at $50/bbl or less.

Seventh Generation, another US company that specialises in cleaning and personal care products designed with human health and the environment in mind, noted its use of plant-based surfactants such as

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

13 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

75% bio-based sodium laureth sulfate and 46% bio-based laureth-7 in the period from 1990 to 1998. The company is aiming for a higher plant-based content level and started using 100% bio-based sodium lauryl sulfate and APG between 1999-2001. In 2002-2008, the company used 75% bio-based sodium laureth sulfate that has low 1,4 dioxane (5ppm) by-product, and 46% bio-based laureth-7. Since then the ultimate goal for the company is to use 100% bio-based with zero 1,4 dioxane byproduct.

Seventh Generation said it has already started using 100% bio-based laureth-6 supplied by Solvay’s Rhodasurf-6 NAT, which contains palm kernel oil-based lauryl alcohol and sugarcane-based ethylene oxide. It has also been using 100% bio-based sodium lauryl sulfate surfactant. For the future, it is also looking into the use of 76% bio-based lauryl dimethylamine oxide and 21% bio-based Ppg-10-laureth-7 (alcohol alkoxylate) for some of its products as an alternative to methyl-based feedstock. Other future goals are to replace palm kernel oil with algal oil and to use more sustainable sugarcane feedstock in the company’s supply chain.

Household and industrial and institutional (HI&I) cleaning products and personal care are the two key surfactants consuming applications, accounting for 65% of global surfactant consumption in 2015, according to Kline & Company, a US market research firm. Surfactants account for around 60% of the $17.7 billion total ingredients consumed in HI&I cleaning applications. Europe and the US represent about two-thirds of the consumption of HI&I cleaning ingredients last year. Anionic and nonionic surfactants represent the bulk of the $11bn, 5.7 million-ton global specialty surfactant market. According to Kline & Company, the move towards surfactants that have more a favourable environmental profile remains one of the key trends at the finished products level.

In industrial applications, surfactant consumption in the US was valued at $2 billion, with food, crop protection and lubricants representing the largest markets accounting for half of the total consumption. Surfactant consumption in industrial applications is expected to grow at rates close to that of GDP at slightly over 2%, but large differences exist within each application. BASF is said to the leading supplier in the US market for industrial applications, however, the market is said to be fragmented, with more than 30 companies having over $10 million in surfactant sales in the US.

In the agchemicals sector, a representative from US agbiotech company, Monsanto, noted the regulatory challenges in Europe on using glyphosate, which contains polyethoxylated tallow amines, a surfactant that is drawing heavy criticism from consumer advocates because of of its alleged toxicity to humans, animals and the environment. Glyphosate is one of the most widely-used herbicides in the world. While Monsanto claims that tallow amines do not pose an imminent risk for human health, the company said it has been preparing for a gradual transition away from tallow amines to other types of surfactants for commercial reasons. Tallow amines, when mixed with herbicides, help active ingredients to be absorbed efficiently by crops. Monsanto said there has been increasing interest in green surfactant options for the agchemicals market. The company has already looked into the use of APG surfactant, however, this is said to bring slow uptake and excludes high-load formulations. The biological-based surfactant category is expected to create new product opportunities and Monsanto is said to be looking heavily at this market. Agricultural biologicals, often referred to as bio-pesticides, represent a growing market segment of roughly $1.7 billion in annual sales, and are used to complement or replace agricultural chemical products.

The company noted the high growth of the global crop protection market between 2009 and 2019, and stated that herbicides remain the most important application for surfactant consumption in this sector. Global surfactants use in the agriculture sector was estimated to be worth around $1.1 billion.

In the oilfield sector, the issue with surfactants use is in the supply chain and logistics arena as surfactants production is not co-located in oilfields. In EOR applications, Shell noted that it is difficult to support investment in modern EOR surfactants production if oil prices are below $50-60/bbl. Around 2-4 lbs of EOR surfactants are required per barrel of oil that can be accessed. Instead of drilling new wells, Shell pointed out that it is better to create new surfactants that can recover the rest of the oil in existing wells.

Shell noted the use of its NEOFLO® surfactants in drilling, NEODOL® alcohol ethoxylates in the fracking process, and ENORDET® surfactants in enhanced oil recovery.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

14 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

Typical Surfactant Chemistries in Oilfield applications

Well & Reservoir Surfactants Use Function Drilling Fatty acid amines Emulsifiers and dispersants for AOS, AES, soaps, lignosulfates drilling mud formulations tall oil acid Fracture, Initial Production Mainly nonionics Flowback aids, initial frack (anionics at R&D stage) fluids, emulsifiers Enhanced Oil Recovery Alcohol alkoxysulfates, IFT reduction, mobility control, IO sulfonates, alkyl aryl sulfonates wettability alteration Source: Shell Chemicals

MALONIC ACID: Lygos, Sirrus in Malonates R&D

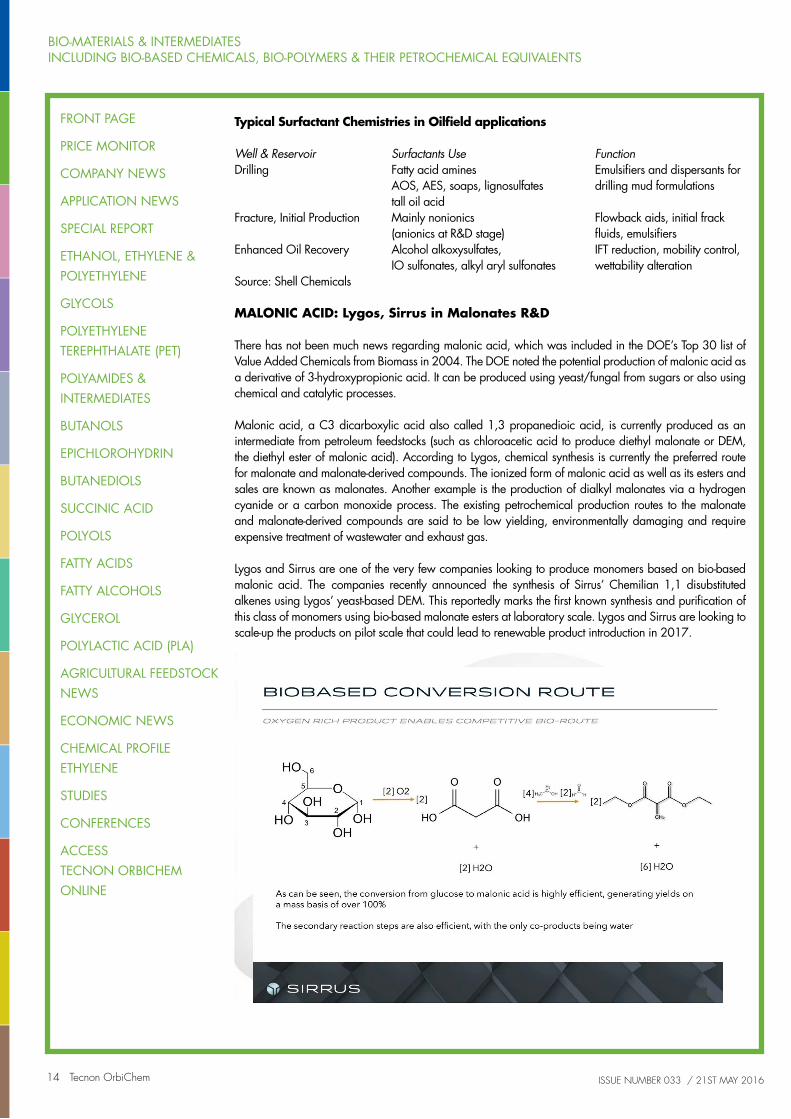

There has not been much news regarding malonic acid, which was included in the DOE’s Top 30 list of Value Added Chemicals from Biomass in 2004. The DOE noted the potential production of malonic acid as a derivative of 3-hydroxypropionic acid. It can be produced using yeast/fungal from sugars or also using chemical and catalytic processes.

Malonic acid, a C3 dicarboxylic acid also called 1,3 propanedioic acid, is currently produced as an intermediate from petroleum feedstocks (such as chloroacetic acid to produce diethyl malonate or DEM, the diethyl ester of malonic acid). According to Lygos, chemical synthesis is currently the preferred route for malonate and malonate-derived compounds. The ionized form of malonic acid as well as its esters and sales are known as malonates. Another example is the production of dialkyl malonates via a hydrogen cyanide or a carbon monoxide process. The existing petrochemical production routes to the malonate and malonate-derived compounds are said to be low yielding, environmentally damaging and require expensive treatment of wastewater and exhaust gas.

Lygos and Sirrus are one of the very few companies looking to produce monomers based on bio-based malonic acid. The companies recently announced the synthesis of Sirrus’ Chemilian 1,1 disubstituted alkenes using Lygos’ yeast-based DEM. This reportedly marks the first known synthesis and purification of this class of monomers using bio-based malonate esters at laboratory scale. Lygos and Sirrus are looking to scale-up the products on pilot scale that could lead to renewable product introduction in 2017.

Newlight to supply IKEA with AirCarbon PHA resins

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

15 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

Lygos announced early this year that it has achieved a critical breakthrough in the cleaner production of malonic acid using engineered yeast, and has since then produced sample quantities of high-quality malonic acid to customers and partners in pilot scale manufacturing under a program funded in part by the DOE’s Bioenergy Technologies Office (BETO). Lygos performed scale-up production in the Advanced Biofuels Process Demonstration Unit (ABPDU) at Lawrence Berkeley National Laboratory. BETO’s Biochemical Conversion Technology Area, along with its other technology areas across the biomass supply chain, aims to find cost-effective pathways to sustainably produce biofuels, bioproducts, and biopower.

Lygos has also been awarded a $300,000 Small Business Voucher from the DOE in March to help accelerate scale-up and commercialization of the malonic acid technology. The voucher is being used to run Lygos’ bio-malonic acid fermentation process at up to a 7,000-liter scale at NREL and to validate process performance using cellulose-derived sugars at the ABPDU. Lygos will purify the malonic acid produced at NREL and the ABPDU, producing high-purity bio-malonic acid derived from cellulose sugars and CO2.

Lygos said its malonic acid IP portfolio covers its engineered microbes, metabolic pathways, engineered enzymes, methods to produce malonic acid, and methods to purify malonic acid, among others. (Published U.S. patent application PCT/US2013/029441)

Sirrus was formerly called Bioformix led by then CEO Adam Malofsky. Ohio-based Bioformix was first founded in 2009 by mostly ex-employees of super glue developer, Loctite Company, which was acquired by Henkel in 1997. The company has been working on high performance resins and polymers that provide epoxy-like bonds with high-speed curing at ambient temperatures, and at the same time compostable and metabolically compatible. The polymers reportedly exhibit excellent UV and light resistance, as well as thermal, solvent and water-resistance.

The company’s monomer feedstock uses petro-derived acetic acid, but Malofsky already hinted the possibility of using a sugar-derived monomer, which the company had started looking into by 2012. BioFormix’s first target application back then was in light assembly adhesives that could include consumer electronics assembly and consumer adhesives. These are low-volume, high margin applications where the polymers could demand prices anywhere between $25/lb to $1000/lb.

Today, Sirrus is marketing this new chemical platform based on 1,1-disubstituted alkene monomers under the tradenames, Chemilian and Forza, which were first launched in 2014. Chemilian-enabled adhesive, coatings and inks reportedly do not require external energy sources such as ovens or solvents to activate, and can cure ambiently and bond in minutes, saving time, money and simplifying production. Chemilian-based products can reportedly deliver superior chemical and temperature resistance, low odour, optical clarity and no blooming, all the while meeting the demand for environmental suitability including reducing the need for building block materials including BPA, formaldehyde or styrene.

Also in 2014, Sirrus has partnered with Elmer’s Products for the development of consumer products based from Chemilian and Forza monomer platforms. While Chemilian products have one alkene group, the Forza products contain multiple alkene groups allowing cross-linking for the development of polymers exhibiting high strength, thermal and chemical resistance.

In a presentation during the BIO World Congress in 2014, Sirrus noted the possibility of either replacing acetic acid or malonic acid to produce a bio-based alternative for its platform monomers. Sirrus said that the conversion of glucose to malonic acid is already highly efficient, generating yields on a mass basis of over 100%, and the secondary reaction steps are also efficient, with water the only co-products.

The DOE’s 2004 Top Value Added Chemicals from Biomass report noted the malonic acid market at only around 453 tons and was estimated to be worth at EUR24,000/ton. Third party sourced prices for malonic acid resulted at varying prices ranging between $7-20/kg and $30/100g. Lygos is looking to produce its malonic acid at a cheaper price.

The US DOE also recently awarded a grant to Lygos to develop microbial catalysts that can convert renewable cellulosic sugars into aspartic acid, which has several end uses including biodegradable polymers, fertilisers, and even cosmetics.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

16 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

ETHANOL, ETHYLENE & POLYETHYLENE

North America – Petrochemical

The US Gulf spot market was very active in the second half of May with more than 100 trades concluded. Spot pricing was consistently in the range of 25.0-25.5 c/lb. The weighted average price up to 20 May was 25.21 c/lb, nearly a cent below the April average. Ethane traded mainly around 19.5 c/gal during the month, about 0.5 c/gal higher than the April average. Various shutdowns – mainly for planned maintenance – restricted cracker operating rates during May to 90-91% of capacity.

The Americas - Bio-based

Gevo announced this month that it has entered into an agreement with Clariant Corp. to develop catalysts that will enable Gevo’s ethanol-to-olefins (ETO) technology, which uses ethanol as a feedstock to produce tailored mixes of propylene, isobutylene and hydrogen. ETO is a chemical process unlike Gevo’s biological process of converting sugars to isobutanol. Underpinning the ETO technology is Gevo’s patent of proprietary mixed-metal oxide catalysts that can produce polymer-grade propylene or high purity isobutylene, along with hydrogen in high yields in a single process step from conventional fuel grade ethanol.

For one million gallons of ethanol feedstock, the Gevo technology reportedly could produce around 1.5 kt of acetone or 1.1 kt of propylene, which can also be converted into 1.7 kt of n-butanol and/or 300,000 gallons of diesel or jet fuel. Alongside acetone or propylene, it could also produce 0.18-0.2 kt of hydrogen depending on co-products. This equates to around 0.5 MW of electricity or can be sold as renewable hydrogen.

Gevo said the technology has the potential to address a variety of markets such as automobile parts, packaging, durable goods made of plastics, renewable diesel fuel and renewable hydrogen for the chemical, energy and fuel cell markets. Once the ETO technology has been successfully developed and scaled up, Clariant will be in a position to produce quantities of the catalyst needed to meet commercial production requirements. Gevo expects to license the technology in the same way it did with its bio-isobutanol process. Partnerships are also expected to come from ethanol, chemical, hydrogen, and end-user markets.

Gevo also emphasised that the ETO technology can produce cost-competitive renewable propylene and hydrogen.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

17 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

In cellulosic ethanol news, Aemetis Inc. announced that it will acquire the privately-owned California-based Edeniq, which has developed a Pathway technology that includes equipment called Cellunator™ that can convert corn kernel fibre to cellulosic ethanol using cellulase enzymes. The Pathway technology can use existing fermentation and distillation equipment to produce up to 2.5% cellulosic ethanol and a 7% increase in ethanol yield. Aemetis will acquire all of Edeniq’s shares in a stock plus cash merger transaction to be paid over the next 5 years in an amount of up to $20 million (up to $18 million if Edeniq stockholders elect all stock consideration). Edeniq generated around $20 million in revenue and $6 million in positive EBITDA in 2015.

Edeniq’s technology is already commercially proven with 29 of the company’s Cellunators™ installed in 6 US ethanol plants. Upon completion of the deal, which is expected during the second quarter, Edeniq will operate as a wholly-owned subsidiary of Aemetis.

Meanwhile, POET-DSM noted late last month that it’s Emmetsburg, Iowa, cellulosic ethanol Project LIBERTY plant, is still in the process of ramping up to its full 20 million gallon/year capacity. Project LIBERTY came online in late 2014, and can convert 770 tons/day of biomass using enzymatic hydrolysis followed by fermentation. The company said it has produced and shipped several tank cars of cellulosic ethanol since its start-up phase began last year. Besides ethanol, the facility produces biogas from its anaerobic digester and steam from its solid fuel boiler to produce power to run its own processes, and export energy to the adjacent grain-based ethanol plant.

It was reported that just over 1 million gallons of cellulosic ethanol were produced during the first quarter of 2016 as announced by the US Environmental Protection Agency (EPA). Production this year is said to be well ahead of the pace in 2015, when 2.2 million gallons of cellulosic ethanol were produced for the entire year. Key cellulosic ethanol players in the US include Ineos Bio, POET-DSM, Quad County Corn Processors, Abengoa Bioenergy, and DuPont Industrial Biosciences. However, Ineos Bio’s facility is reportedly not producing any ethanol while Abengoa shut down its plant last December. Quad County’s potential is reportedly currently limited to a small amount of residual ethanol production at existing corn ethanol plants.

West Europe – Petrochemical

Problems at various European crackers, including both Total plants at Antwerp and Dow at Terneuzen, tightened ethylene supply in late April and early May. Spot prices rose to 3-5% above contract. The May contract settled up by €40/ton at €910/ton ddp. The June contract will be €25/ton higher. Supply eased around the middle of May and spot prices fell to more normal levels of 3-5% below contract in the second half of the month. Strikes in France affecting all forms of transport have led to force majeure declarations on ethylene and propylene at Feyzin, and Gonfrevillle and Lavera.

West Europe – Bio-based

Switzerland-based specialty chemicals company, Clariant, and its partner Scania, one of the world’s top heavy-duty vehicle manufacturers, have announced the one-year milestone in the use of Scania’s cellulosic ethanol-powered Ecotrucks, which Clariant uses at its Suzano plant in Brazil. In mid-2015, Clariant acquired three Scania P 270 model trucks, which run on ethanol and are the first of their kind to be sold by Scania in Latin America. The Ecotrucks transport ISO tanks with a 25,000 litre (6,604 gallon) capacity for Clariant’s chemical products coming from its plant in Suzano, Sao Paulo, Brazil, which is the company’s largest industrial complex in Latin America.

After a year of using the Ecotrucks, Clariant can verify a reduction in CO2 emission by around 90% compared to the diesel engines that were used before. The ethanol fuel is manufactured with the Master Batch ED 95 additive produced by Clariant in Brazil. The additive allows engines designed to run on diesel to run on hydrous ethanol because it adjusts the characteristics of the fuel to the engines’ requirements.

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

18 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

In the second phase of this project, Clariant said it has now started using cellulosic ethanol manufactured from sugarcane bagasse using the company’s sunliquid® technology. Clariant noted that the total cost per litre of its cellulosic ethanol including feedstock, conversion and depreciation using the sunliquid® technology is price competitive with sugarcane ethanol pricing in Brazil. The company has conducted tests on over 40 containers of sugarcane bagasse, tops and leaves from Brazil and converted them into cellulosic ethanol at Clariant’s pilot and pre-commercial facilities in Straubing, Germany. Clariant has been operating a pre-commercial plant in Straubing since July 2012, producing up to 1 ktpa of cellulosic ethanol from around 4.5 ktpa of raw materials.

Alkol Biotech said it has sold 500 kilos of its EUnergyCane sugarcane bagasse for Clariant’s sunliquid® cellulosic ethanol testing. Alkol Biotech has been developing this hybrid sugarcane variety, which is grown in the company’s fields in Motril, Spain. The company claimed it is the only genuine native sugarcane variety in Europe and Alkol Biotech is improving it to grow in UK and Europe.

Asia – Petrochemical

Ethylene spot prices in Asia weakened in May especially in the second half of the month. From $1165-1200/ton cfr at the beginning of May they fell to $1100-1120/ton cfr by the 26 May. Supply increased with offers from Taiwan together with deep-sea imports from Europe and the Middle East. Chinese buyers pushed hard for lower numbers as demand weakened. The Shell Bukom cracker is expected to re-start in late July or early August. Petro Rabigh in Saudi Arabia is offering regular parcels of ethylene by tender – 6,000 tons early in March and 9,000 later in the month.

GLYCOLS

North America – Petrochemical

Benchmark MEG prices in the US fell by 2 c/lb and may do so again in June on lower ACPs. All turnarounds are now complete, although Pemex is having ethane supply problems and has cut back operations, resulting in higher MEG imports from the US. Demand from PET resin remained slow due to the weather affecting bottled water and CSD sales.

The benchmark price for DEG in the US was raised by 2.0 c/lb this month to give the new range of 37.0-41.0 c/lb ($816-904/ton) fob US Gulf. Since demand last month was not all that exciting, the general expectation from the market was for prices to drop in line with MEG prices, i.e. by 2.0 c/lb. However,

Scanla trucks use cellulosic ethanol produced via Clariant’s technology

Source: Clariant

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

19 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

as the attempt to increase levels last month fell on stony ground, US producers decided that they would get their wish this month. Not all producers or suppliers were of the same mind. Indorama, for instance, probably felt that demand was still not robust enough to bear an increase and so announced a roll-over at last month’s levels of 35.0-39.0 c/lb ($772-860/ton) fob Gulf. A couple of the others, such as Formosa Plastics, were also of this persuasion and therefore the 2.0 c/lb increase attempt foundered for the second month in succession.

The North American MPG market is stable in May, with little change seen in market conditions since May. Supply is balanced this month, following a period where PG availability was restricted by planned turnarounds. Demand from the principal derivatives is still running well. The food, pharma and personal care side of the market is described as stable, which is to be expected in these sectors which are not as volatile as more cyclical MPG derivatives. Pricing this month is largely holding steady at a rollover, following a set of price increases which went through to a varying degree last month. This month’s propylene settlement has settled at a rollover. Looking ahead, market players will be keeping an eye on supply and demand in order to determine any further price movement.

North America – Bio-based

Archer Daniels Midland (ADM), the sole producer of bio-based MPG in the Americas, is planning to leave the de-icing and antifreeze market due to its low margins. Like petro-based MPG producers, ADM has also faced downward price pressure due to lower crude prices that have lingered for more than a year since late 2014. ADM’s bio-based MPG price has to be competitive with propylene-based MPG although there are certain applications where the company can get slight premiums in exchange for the value-added sustainability and renewability claims that customers can use as marketing tools. ADM’s bio-based MPG is usually negotiated in long-term supply contracts.

ADM’s high-purity MPG materials (greater than 99.5%) can be used in applications such as heat transfer fluids; fragrance, cosmetics and personal care; food and flavourings; pet food and animal feed; and pharmaceutical excipient. Its industrial grade bio-MPG can be used in UPRs; hydraulic and brake fluid, and in paints and coatings.

The company produces its glycerol-based MPG at its 100 ktpa facility in Decatur, Illinois, using refined biodiesel-derived glycerine feedstock. The company sources the crude glycerine from its own biodiesel plant, and further refines it to USP grade glycerine as feedstock for MPG production; or sells the refined glycerine as is into the open market. ADM also has the capability of sourcing cheaper crude glycerine from its biodiesel plants in South America, especially as the bio-MPG plant consumes significant quantities of US glycerine. The company has disclosed that it has been exporting its bio-MPG into the European market.

West Europe – Petrochemical

One MEG contract settlement in Europe was announced at a drop of €25/ton, but a second has not been announced yet. Demand has not reached its peak and PET resin producers are faced with growing imports. Spot prices weakened by some €30-40/ton as demand for industrial solvent uses was poor and antifreeze blenders are not yet thinking of buying.

The DEG market is rather stable at the moment, since not much movement has been noticeable in the offtakes into the polyester polyols area, although those for UPR are thought to have dipped, but only very slightly. The continued low demand from the construction and house-building sectors has seen inventories throughout the chain fall and the downstream consumers are only just now coming into the market with increased interest. This has also made UPR and polyester polyols producers unwilling to make any more purchases other than hand to mouth and has tended to make them keep their inventories extremely low. This, of course, puts the working capital cost onto the suppliers as well as the burden of having to deliver on time. Fortunately for European suppliers there were several turnarounds on EO in April, which forced a re-arrangement in internal EO allocation away from glycols, and this month Ineos has a shutdown at its Antwerp plant.

The European MPG market is stable, supported by a firmer feedstock market, as well as a tighter supply situation during April and May. A number of shutdowns are taking place in the PO/PG sector, and this

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

20 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

has supported a somewhat firmer MPG market in Europe. Demand is currently at reaching its peak for construction applications such as UPR, whilst other downstream sectors were stable. Overall demand is in line with forecast, but still remains fairly flat year on year. Prices have moved up by around €10-20/ton in May, following last month’s price negotiations which resulted in a €20-40/ton increase. There have been cases of larger increases this month, but this is thought to be only in cases where buyers’ requirements are above forecast. Once the current round of maintenance outages has come to an end, MPG availability is likely to return to the normal seasonal position. The DPG market is short and prices have firmed as a result.

West Europe – Bio-based

Avatherm, based in Sweden, has launched its new line of Heat Transfer Media products using Neste’s renewable isoalkane that is produced as a co-product from Neste’s renewable diesel production based on hydrotreated fats and oils. Avatherm claims to be one of the first companies in the world to market heat transfer media produced from renewable raw materials. One of the first lines of products is a coolant to replace glycol. Future products include transformer oil and release fluids among others that are currently being developed.

The Heat Transfer Media products will have low sulphur and aromatic content, which is a specific concern to sensitive environments such as forestry and agriculture. The chemical composition of Neste’s Renewable Isoalkane is said to be comparable to the fossil equivalents, but it outperforms conventional fossil-based products in terms of quality, performance and environmental impact.

Neste has been selling its renewable isoalkane as is to customers directly and to partners, such as Haltermann Carless Solutions and Total Fluides, that further process and market isoalkane-derived products according to industry needs. Neste produces the bio-based isoalkane using its NEXBTL technology at its refineries in Singapore, the Netherlands and Finland.

Avatherm’s products have been tested in cooperation with the Royal Institute of Technology in Stockholm, the Saybolt Laboratory in Gothenburg, and with research partners in Europe.

China – Petrochemical

Polyester operating rates in China remained above 80%, the PET resin season picked up, inventories and imports dropped, some producers cut back on negative margins and the spot prices came down, which

0

250

500

750

1000

1250

1500

1750

2000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

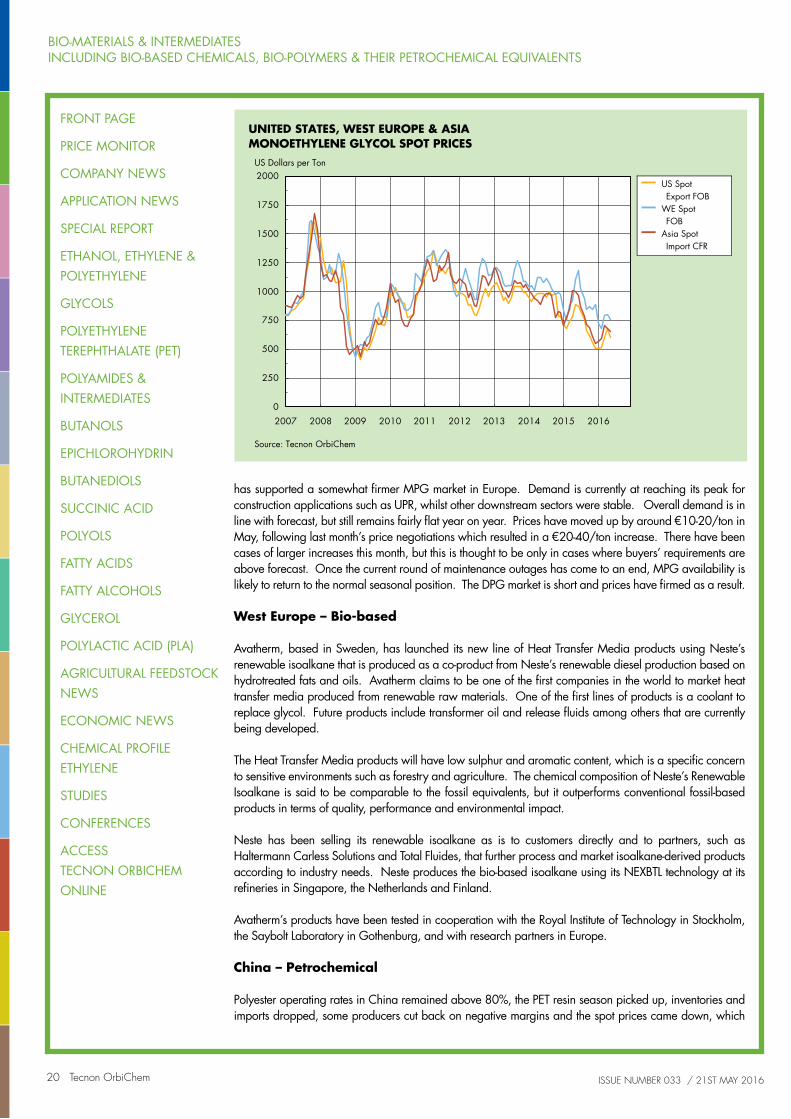

UNITED STATES, WEST EUROPE & ASIA

Source: Tecnon OrbiChem

MONOETHYLENE GLYCOL SPOT PRICESUS Dollars per Ton

US Spot

WE Spot

Asia Spot

Export FOB

FOB

Import CFR

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

21 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

can only be due to speculation on the futures market. Spot levels fell by some $60-70/ton to $620/ton cfr and MEGlobal announced its MEG ACP for June at a decrease of $40/ton.

The consumption of DEG into UPR remained on the weak side again this month, with the estimated operating rate put at 40-50%. Much of the cause of this continued poor performance on UPR has come from the dire state of the house-building and construction sector, where DEG itself has previously been used in concrete accelerator mixes. This has also affected the downstream consumption of polyester polyols, although not to the same extent. Supply is amble for as virtually all the scheduled shutdowns have now finished and so it is expected that the inventories may well start to increase going into June. To some extent this will be alleviated by the enforced shutdowns of the #1 and #2 plants of Nan Ya at Mailiao and the turnaround of its #4 plant, the larger one, until early June. This should also be helped by the continued closure of the Shell plant at Singapore, the Mitsubishi lengthy turnaround at Kashima and some operating cutbacks due to low margins. The domestic prices dropped by some Rmb250/ton to Rmb4400-4450/ton exw in East China and the import spot levels came down by $20/ton to $560-590/ton cfr.

Asia – Bio-based

Bio-MEG producer, India Glycols, noted the increased prospects for bio-PET and bio-MEG demand in a recent presentation at the Biobased World Chemicals and Plastics conference held in Bangkok, Thailand. The global PET/fibre demand this year is expected at around 70 million tons, with an estimated growth rate of around 6%. At a conservative level assuming 3% of this demand is for bio-PET/fibre, the total demand then works out at 2 million tons. This converts to bio-MEG requirement at around 600 ktpa against today’s world bio-MEG capacity of around 250 ktpa.

According to India Glycols, bio-PET fibre demand is further expected to increase to 5% or around 4 million tons by 2018. The challenges for bio-MEG, however, are the current low cost of petro-MEG vs bio-MEG; smaller volume and capacity availability for bio-MEG; feedstock availability and options; supply chain management and also increased use of bio-ethanol as biofuel, which will continue to have impact on availability and costs of ethanol-based MEG.

India Glycols noted its collaborative project with DBT-ICT and the Government of India’s Ministry of Science & Technology, for the conversion of cellulosic waste to bio-ethanol, where a 10 tpd demonstration plant at India Glycol’s Kashipur site has recently been commissioned. India Glycols has its own ethanol distilleries at Kashipur as well as in Gorakhpur, India, with a combined capacity of around 200 ktpa of hydrous ethanol.

India Glycols expects bio-MEG availability worldwide would increase as new capacities are being added. The use of cellulosic waste could also lead to reduce bio-ethanol costs as well as give boost bio-MEG’s availability and competitiveness.

India Glycols’ current bio-MEG capacity is reportedly 175 ktpa and can be further expanded at its current location. Bio-EO derivatives capacity is around 100-125 ktpa in another facility. There are reportedly 3-4 Chinese producers currently active in bio-MEG production with a combined totally capacity of around 50-100 ktpa. Greencol Taiwan is considered to be the only serious competitor of India Glycols for bio-MEG.

It was reported that a significant volume of bio-MEG is also being consumed in anti-freeze products, driven by players in the automotive industry such as Toyota, and in fibre for sport clothes from companies such as Nike and Puma. Some in the petro-MEG markets doubt the significant use of bio-MEG in anti-freeze due to much more competitive pricing for petro-glycols in the de-icing and antifreeze sectors, and note that the current premiums for bio-MEG are prohibiting its use in these markets.

POLYETHYLENE TEREPHTHALATE (PET)

North America – Petrochemical

North American PET resin volumes continued to improve modestly in May. Producers reported high production levels and well controlled inventories. Imports from countries not included in the recent US

BIO-MATERIALS & INTERMEDIATESINCLUDING BIO-BASED CHEMICALS, BIO-POLYMERS & THEIR PETROCHEMICAL EQUIVALENTS

22 Tecnon OrbiChem

FRONT PAGE

PRICE MONITOR

COMPANY NEWS

APPLICATION NEWS

SPECIAL REPORT

ETHANOL, ETHYLENE & POLYETHYLENE

GLYCOLS

POLYETHYLENE TEREPHTHALATE (PET)

POLYAMIDES & INTERMEDIATES

BUTANOLS

EPICHLOROHYDRIN

BUTANEDIOLS

SUCCINIC ACID

POLYOLS

FATTY ACIDS

FATTY ALCOHOLS

GLYCEROL

POLYLACTIC ACID (PLA)

AGRICULTURAL FEEDSTOCK NEWS

ECONOMIC NEWS

CHEMICAL PROFILE ETHYLENE

STUDIES

CONFERENCES

ACCESS TECNON ORBICHEM ONLINE

ISSUE NUMBER 033 / 21ST MAY 2016

dumping ruling including Mexico, Taiwan, Brazil and Thailand are gaining share in US markets and US imports through the first three months of the year are flat compared to the same period a year ago.

North America – Bio-based

Texas-based, Wholesome Sweeteners Inc., has announced the transition of its Wholesome! Organic Blue Agave line into using bio-PET bottles designed in partnership with Berlin Packaging’s Studio One Eleven. The new bottles which contain up to 30% plant-based PET, will be available in 11.75, 23.5 and 44 ounces, and will start flowing through store shelves in late summer 2016. The bottles are moulded with the #1 SPI coding for PETE.

Wholesome Sweeteners has also partnered with How2Recycle, a standardised labelling program designed to make recycling easier to understand and act upon for consumers. The company said it is the first organic sweetener brand to join the How2Recycle movement, which has created a universal recycling language for consumers through the use of special on-package logos that provide clear instructions for each piece of recyclable packaging.

According to the company, bottle sizes and pricing will remain the same as they were in their previous packaging. Wholesome Sweeteners is looking to incorporate bio-PET bottles for its other liquid sweeteners.