Embed Size (px)

Citation preview

Checking Accounts

3rd Period STEPMs. Gikas 2009-2010

The Convenience of Checking Check – a written order to

pay someone takes money directly out of the

persons checking account who wrote the check

Keep track of your expenses Keeps your money safe If lost or stolen, you can stop

payment Pay bills with and show proof of

payment

Where to Open an Account

Select a financial institution or bankConsider the following factors when

choosing the right bank:Convenience ServicesTypes of accounts offeredFees

Opening a Bank Account

Convenience near home or work Store hours

Services Checking & Savings ATM machines Drive up banking Bank statement Credit/debit cards

Debit – take money directly from checking account

Loans Safe-deposit boxes Certified/cashier/traveler

checks Money orders

Types of Accounts Individual account

Only your signature Joint account

1-2 owners can sign on the account

Interest paying account Like a savings account Interest is paid to you

depending on the amount Fees

Costs Money Differs, depending on bank Free checking Pay fee for each check Order checkbooks Huge fee for bounced

checks

Opening a Checking Account Find a Bank/Financial Institution &

Open a Checking Account Go in and just ask, “I want to Open a

Checking Account” Fill out an application You will be asked to sign a signature

card Helps them read your signature on checks

Prevents forgery

Need to bring ID and Social Security Card

Making a DepositMaking a Deposit Must have money Must have money

in your checkingin your checking– Needed to write Needed to write

checkschecks Bank teller will ask Bank teller will ask

you to complete a you to complete a deposit slipdeposit slip

Deposit SlipDeposit Slip– Records how Records how

much money you much money you are putting into are putting into your checkingyour checking

Spaces are Spaces are provided to list provided to list either cash or either cash or checkcheck

Deposit money Deposit money electronicallyelectronically– Transfer money Transfer money

From account to From account to accountaccount

Have your job send Have your job send your checks directly your checks directly

Deposit SlipDeposit Slip

1. Write the date you are making the deposit.1. Write the date you are making the deposit.2. If you are depositing currency (paper bills), write the total amount here.2. If you are depositing currency (paper bills), write the total amount here.3. If you are depositing coins, write the total amount here.3. If you are depositing coins, write the total amount here.4. If you are depositing a check, write the bank transit number here, which is 4. If you are depositing a check, write the bank transit number here, which is

the top portion of the two-part number printed in the upper corner of the the top portion of the two-part number printed in the upper corner of the check.check.

5. Write the amount of the check here.5. Write the amount of the check here.6. If you are depositing more checks than can be listed on the front, continue to 6. If you are depositing more checks than can be listed on the front, continue to

list them on the back, and write the total amount of the checks on back here.list them on the back, and write the total amount of the checks on back here.7. Write the total amount you are depositing here.7. Write the total amount you are depositing here.8. If you are making a deposit inside a bank with a teller and you want to 8. If you are making a deposit inside a bank with a teller and you want to

receive cash back from your deposit, write the amount you want.receive cash back from your deposit, write the amount you want.9. Write the total amount (less cash back) of your deposit. 9. Write the total amount (less cash back) of your deposit.

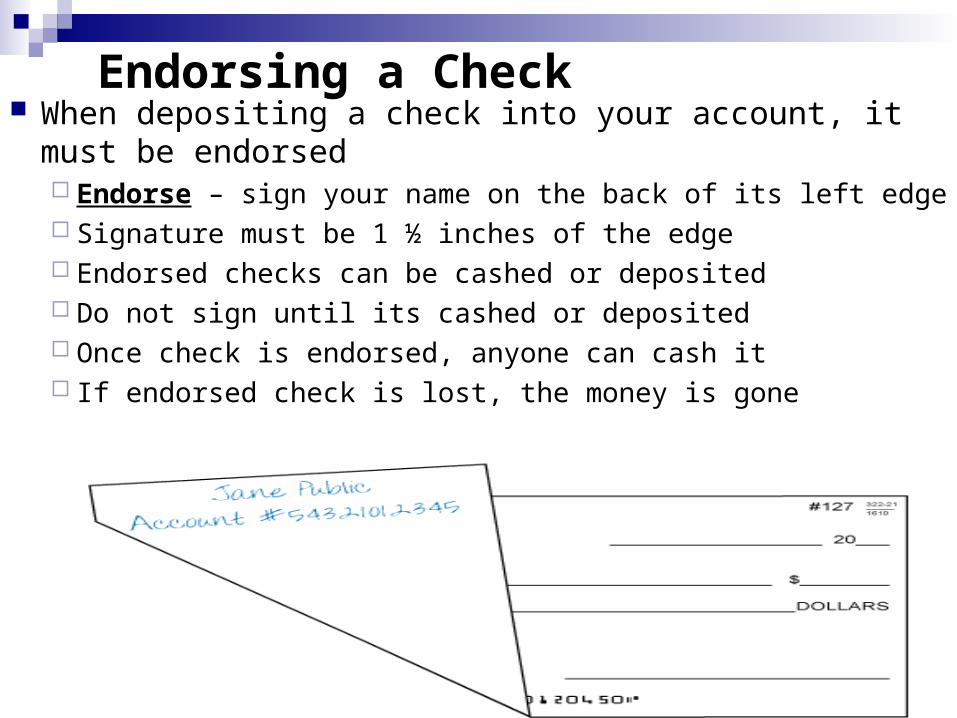

Endorsing a Check When depositing a check into your account, it must be

endorsed Endorse – sign your name on the back of its left edge Signature must be 1 ½ inches of the edge Endorsed checks can be cashed or deposited Do not sign until its cashed or deposited Once check is endorsed, anyone can cash it If endorsed check is lost, the money is gone

Writing a Check

Checks should be written in ink Prevents others from changing the

amount or name

Bank will return checks unpaid with information that’s been erased, crossed out, or changed in any way

Using Check Registers

Most checks come w/ Check Registers Register – place to record all deposits,

check purchases & credits that affect your account Helps keep track of how much money you

have in the account Complete every time you write a check or

deposit Check and service fees are subtracted from your

balance

Check Register Sample

Using Check Registers Comes with stubs or

carbon Written record of check

numbers, dates, amounts & parties to whom checks are written to

Used to avoid overdrawing your account

checks will bounce if you do not have enough money in your account Bank will charge a fee against

inefficient funds

Using Electronic Checking

Electronic Checking – allows to pay bills using the computer or internetPay bills or view checking account onlineBills can be paid automatically

Balancing your Checkbook

Monthly/quarterly statement from bank Bank Statement – lists all your deposits, cash

withdrawals, check withdrawals, service charges, & interest payments Lists your beginning & ending balances

1. Bank account details and sort code

2. Balance at the beginning of statement period

3. Date of transaction 4. Type of transaction 5. Amount of transaction 6. Running balance after each

transaction7. Balance at the end of the

statement period

8. This denotes a regular payment from your account by Direct Debit

9. This denotes a regular payment from your account to another account by Standing Order

10. This shows where you have taken money out at an ATM at an extra cost of $1.50

11. This shows where you have taken money out at an ATM at no extra cost

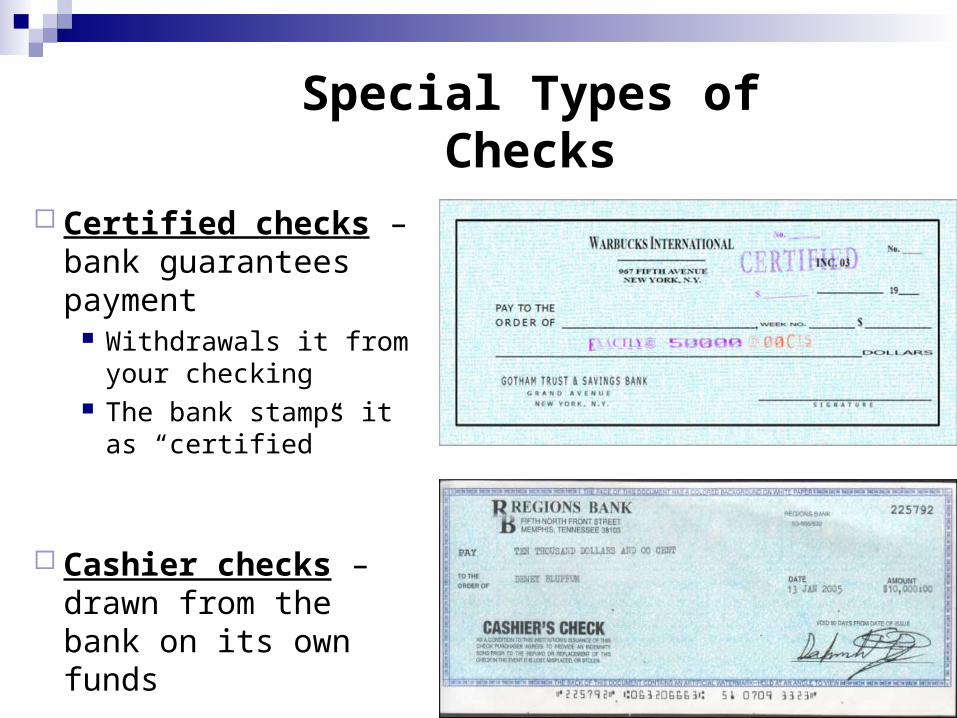

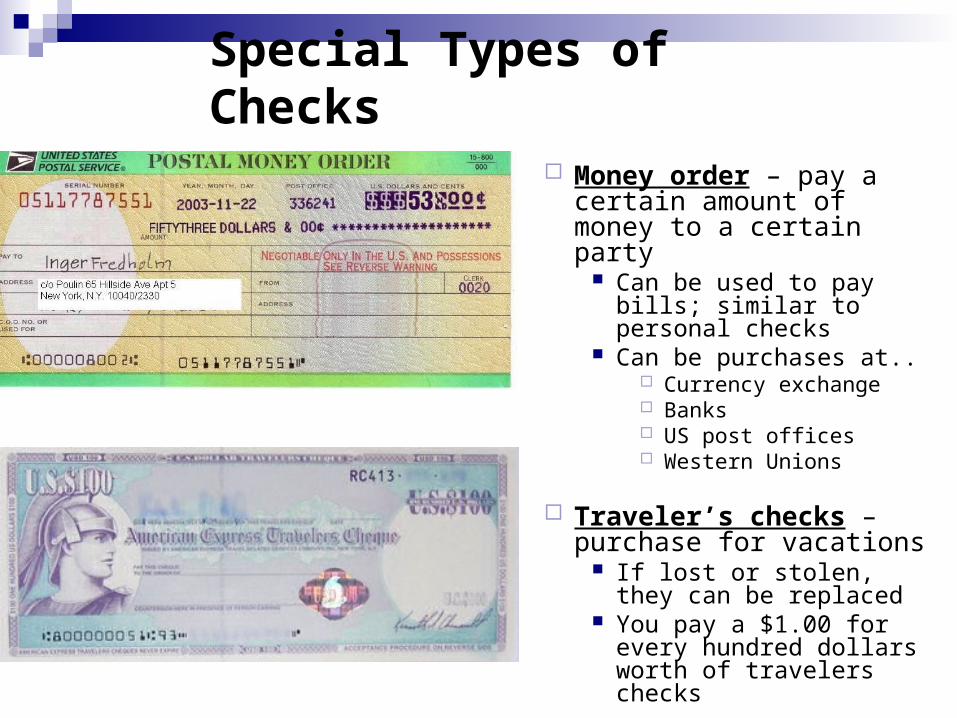

Special Types of Checks

Certified checks – bank guarantees payment

Withdrawals it from your checking

The bank stamps it as “certified”

Cashier checks – drawn from the bank on its own funds

Special Types of Checks

Money order – pay a certain amount of money to a certain party

Can be used to pay bills; similar to personal checks

Can be purchases at.. Currency exchange Banks US post offices Western Unions

Traveler’s checks –purchase for vacations

If lost or stolen, they can be replaced

You pay a $1.00 for every hundred dollars worth of travelers checks

Saving Accounts

3rd Period STEP

Ms. Gikas 2009-2010

Reasons for Saving

Money managementSave a portion from each paycheckMain Reasons for saving money:

Emergencies Future loss of income Travel and recreation Advanced education Major purchases such as car or home Retirement Financial security

Where to Save

Several options for saving your money

Become familiar with banks that offer saving accounts

Find out how much interest they will pay

WHERE TO SAVE (CONT.)

Decide where you want to deposit your money Commercial banks

Department stores of finance. Provide a variety of banking services and financial

advice Offer savings accounts

Savings and loan associations Loans money to home buyers Pay higher interest rates on savings accounts than

commercial banks Credit Unions

Non profit banks Owned by and operated for their members

People who belong to a trade union, church, company, professional organization

Will your Savings be Safe?

Banks that are insured are safe places to keep your money Offers protection Make sure you choose a bank that’s insured

2 agencies are responsible for insuring the banks money Federal Deposit Insurance Corporation (FDIC)

– protects deposits, savings, loans for most banks National Credit Union Association (NCUA) –

protects deposits on most credit unions

Ways to be Safe

Most common ways to save Savings accounts Savings clubs Certificates of deposits US savings bonds

Saving Accounts Open an account at

a local bank Statement savings

account – type of account where you receive monthly or quarterly statement all statements &

withdrawals are recorded

Earn Interest Interest – money paid to

you for allowing a bank to have & use your money the longer you keep your

money in savings, the more interest you earn

Interest is paid… Daily Quarterly (4 times a year) Semiannually (twice a year) Annually (once a year)

Savings Accounts Cont. Interest is added to a

savings account Earns interest

Both the principle & earned interest continue to earn interest, known as compound interest Principle – savings account

deposit Compound Interest – interest

figured in the principle plus the earned interest of financial account

Opening a Savings Account & Comparing Fees

Open a Savings account Convenience

Select a bank near home Hours that meet your

needs Check for how interest

they will pay choose the highest

interest rate Pick bank that you can

have both your checking and savings account

Comparing Fees Some banks require

a fee Must maintain a

certain balance in your account

Be aware the fees your bank may charge

Making a DepositMaking a Deposit

To put money in your savings, you must fill out a To put money in your savings, you must fill out a deposit formdeposit form

Fill them out correctly by following these stepsFill them out correctly by following these steps Write name, date & account numberWrite name, date & account number On currency line, list paper money totalOn currency line, list paper money total On coin line, list total amount of coinsOn coin line, list total amount of coins List each check separatelyList each check separately List amount of cash you want to receive from accountList amount of cash you want to receive from account Subtract the amount of cash to be from amountSubtract the amount of cash to be from amount Present deposit to tellerPresent deposit to teller

Savings Deposit SlipSavings Deposit Slip

Using Direct Deposit

Some employers offer a direct deposit plan

Direct Deposit – allows your employer to deposit your paycheck into your accountYou can deposit your paychecks either in

your checking, savings or bothMust complete a direct deposit from with

your employerMoney goes directly in your account

Withdrawing Money from your Savings You can withdraw money out of your savings Follow this steps

Write your name, date, & account number Write amount of money you wish to withdraw Sign your name on withdraw form Present complete withdraw slip to teller with an ID

Savings ClubSavings Club – encourages you to form a

habit of saving money Savings plan You set up an amount of money every week or month You are given a savings club book with your account

number At the end of your savings period, you receive a check

for the amount you saved plus the interest you earned People use savings clubs for Christmas present or

vacations

Certificates of DepositCertificate of Deposit

(CD) – a savings certificate earning a fixed rate of interest that is purchased for a specific amount of money and held for a set period of time Can be bought at a bank You decide how much you want

to purchase & for how long CDs are usually sold for $500

or more Money is held for a set period

of time Interest rates vary

Money Market Accounts

Money Market Account – A type of savings account that is similar to a CD, but has not time period restrictions

U.S. Savings Bonds U.S. savings bond – A certificate of debt issued by

the federal government that serves as a safe and profitable way for citizens to save money way to save because they are issued by the government. If

lost or stolen, they can be replaced Easy way to save and are given at most banks They earn higher interest rates. The longer they are kept,

the more money you make on them When purchased, they must be kept for 6 months

Mutual Funds & Annuities

Mutual Fund – a long term investment that provides a way to invest in stocks and bonds Gives professional

assistance on where to invest your money

Money can rise or fall; takings risks/gamble

Annuity – a form of investment that lasts 10-15 years and provides insurance & savings Similar to life insurance Used for retirement or

future financial security

![GIKAS ESCAR-2010final.ppt [Kompatibilitätsmodus]](https://img.dokumen.tips/doc/110x75/61aa8e052c881147c835918b/gikas-escar-kompatibilittsmodus.jpg)