Embed Size (px)

Citation preview

Charteris Treasury Portfolio Managers Ltd

Goodacre Gold & Silver Presentation

March 2014

For Professional advisers only. Not to be shown or given to any retail investors

1. Seasonal Pattern – Gold & Silver tend to bottom around July and rise for the rest of the year2. GOFO (Forward Rate) and Futures in backwardation – very unusual – signalling massive shortage of physical Gold for

immediate delivery which is why holders of Gold seem unwilling to do the normal risk free arbitrage (sell spot & buy back cheaper in 3 months time) . The other problem with the Arbitrage is that you might not get your Gold back (see point 3)

3. COMEX vaults being rapidly emptied of Gold – If too many holders ask for delivery, a large problem will arise (see also point 2 abo t Asia)point 2 about Asia)

4. Major Cycle lows – the 10-10½ year cycle in Silver bottomed on 28th June 2013 – this cycle bottomed with a text-book capitulation sell off

5 Investor sentiment – this is universally bearish towards Gold & Silver Assets – sentiment acts as a reverse indicator – when5. Investor sentiment this is universally bearish towards Gold & Silver Assets sentiment acts as a reverse indicator when the herd is this bearish – BUY – See slide 12 – COT report shows record speculator short positions in Gold & Silver.

6. Gold’s replacement cost is around £1,500 an ounce – Gold is currently $1,300 an ounce, it is not possible for Gold to stay below its replacement cost for very long

7. Selling from Gold ETF’s (finite amount anyway) by Americans is drying up – Buying from Asia & the Middle East continues on a massive scale

8. Global Money printing continues unabated despite tapering by the Fed, but massive printing still taking place in Japan & quite possibly China, if that economy starts to fade

9. Supply/Demand fundamentals very, bullish – Net Global mine output is 2,200 Tonnes. Demand from China (1,200), India (800) and Japan (250) tonnes means that three Asian countries will take entire 2013 Global Mine Output

10 Ratio of Miners relative to Bullion recently at all time record since XAU Index formed in 1984 (miners cheap relative to

For professional intermediaries only 2

10. Ratio of Miners relative to Bullion recently at all time record since XAU Index formed in 1984 (miners cheap relative to Bullion) (see Slide 18)

Source: Bloomberg

For professional intermediaries only 3

(as at 28th Feb ‘14)Last Price 1,326.44

Source: Bloomberg

For professional intermediaries only 4

(as at 28th Feb ‘14)Last Price 21.2275

Source: Bloomberg(as at 28th Feb ‘14)

For professional intermediaries only 5

Source: Bloomberg(as at 28th Feb ‘14)

Silver in BlackGold in YellowHUI in Green

For professional intermediaries only 6

For professional intermediaries only 7

Source: United Nations

Source: ezilon.com

More people live insidethe red circle than outside the circle

For professional intermediaries only 8

For professional intermediaries only 9

Source: Bloomberg

Source: Bloomberg

For professional intermediaries only 10

Peaks in the Gold/Silver ratio – correlate to 10 year cycle in SILVER (see previous slide P.9)

(as at 31st Oct ‘13)

For professional intermediaries only 11

Source: Kitco

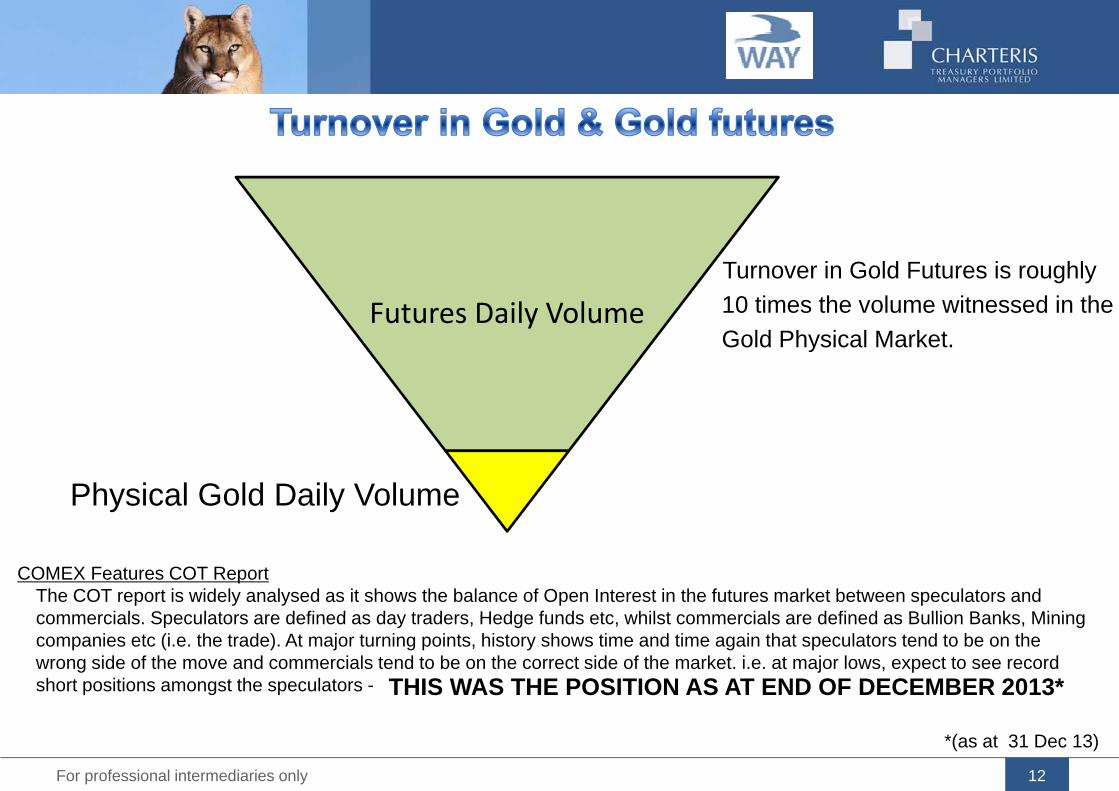

T i G ld F t i hl

Futures Daily VolumeTurnover in Gold Futures is roughly 10 times the volume witnessed in the Gold Physical Market. y

Physical Gold Daily Volume

COMEX Features COT ReportThe COT report is widely analysed as it shows the balance of Open Interest in the futures market between speculators and commercials Speculators are defined as day traders Hedge funds etc whilst commercials are defined as Bullion Banks Miningcommercials. Speculators are defined as day traders, Hedge funds etc, whilst commercials are defined as Bullion Banks, Miningcompanies etc (i.e. the trade). At major turning points, history shows time and time again that speculators tend to be on thewrong side of the move and commercials tend to be on the correct side of the market. i.e. at major lows, expect to see recordshort positions amongst the speculators - THIS WAS THE POSITION AS AT END OF DECEMBER 2013*

For professional intermediaries only 12

*(as at 31 Dec 13)

For professional intermediaries only 13

For professional intermediaries only 14

For professional intermediaries only 15

For professional intermediaries only 16

Source: Bloomberg

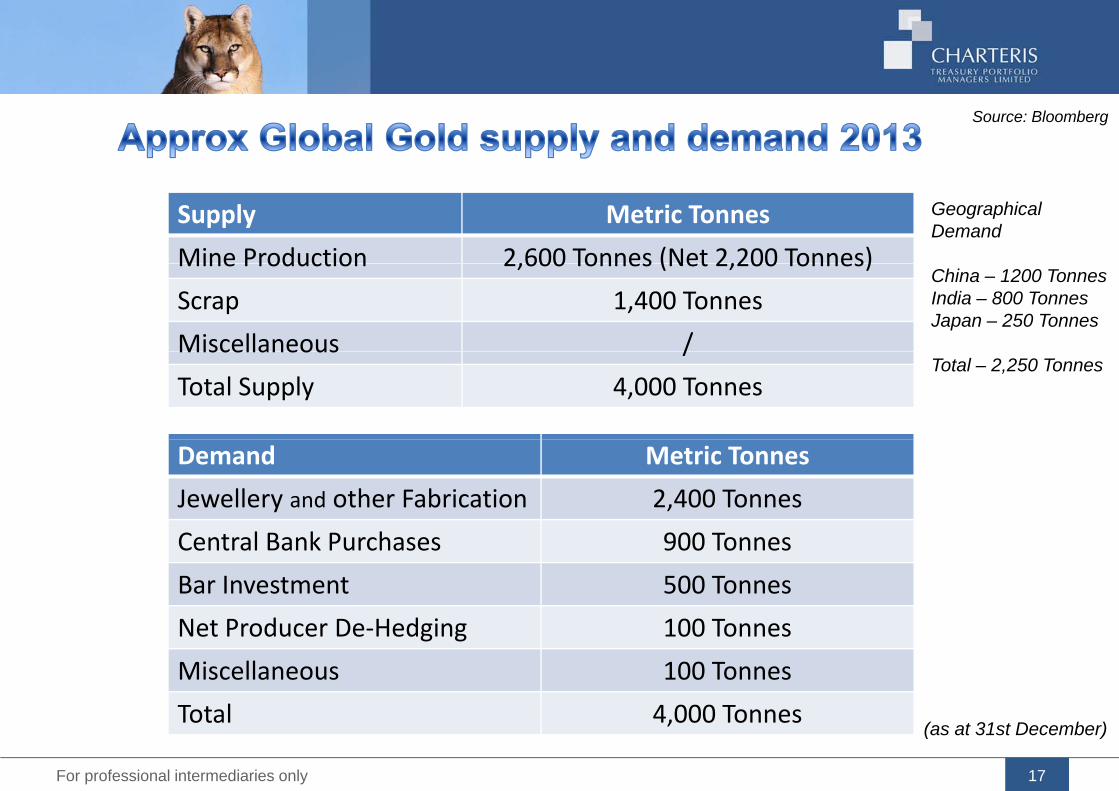

Supply Metric Tonnes

Mine Production 2,600 Tonnes (Net 2,200 Tonnes)

Geographical Demand

Mine Production 2,600 Tonnes (Net 2,200 Tonnes)

Scrap 1,400 Tonnes

Miscellaneous /

China – 1200 TonnesIndia – 800 TonnesJapan – 250 Tonnes

Miscellaneous /

Total Supply 4,000 TonnesTotal – 2,250 Tonnes

Demand Metric Tonnes

Jewellery and other Fabrication 2,400 Tonnes

Central Bank Purchases 900 Tonnes

Bar Investment 500 Tonnes

Net Producer De‐Hedging 100 Tonnes

Miscellaneous 100 Tonnes

For professional intermediaries only 17

(as at 31st December)Total 4,000 Tonnes

Source: Bloomberg(as at 17th Mar ‘14)

For professional intermediaries only 18

This chart shows the Gold shares ratio relative to the Gold price, showing that gold shares are the cheapest they have been in history.

Last Price 13.0902

For professional intermediaries only 19

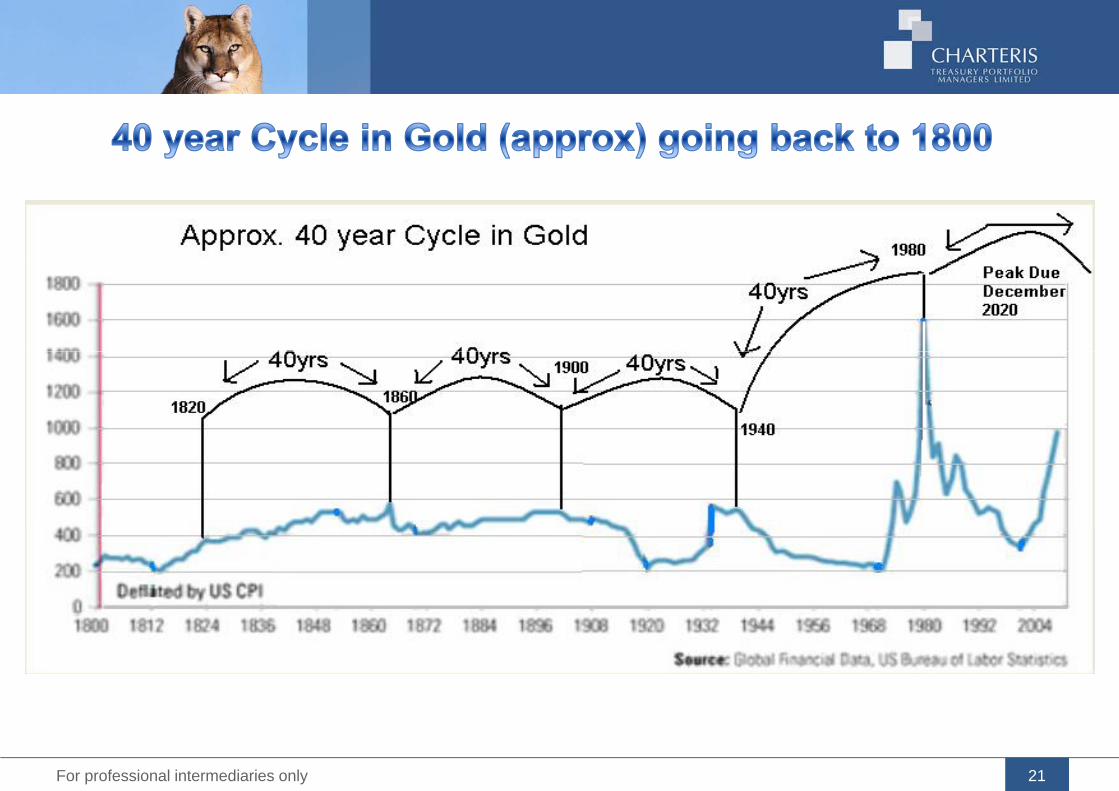

G ld C lGold Cycles

Year Month Weekly Day

40 480 2080 14600

3.36 40.4 173 1212

2.7 33.6 404 2828

.83 10 43 300

.52 6.3 27 190.52 6.3 27 190

Bold print denotes the cycle under which it is commonly known asBold print denotes the cycle under which it is commonly known as.

For professional intermediaries only 20

For professional intermediaries only 21

For professional intermediaries only 22

1. Gold and Silver bullion are amongst the most volatile assets on Earth2. Gold & Silver mining shares are even more volatile2. Gold & Silver mining shares are even more volatile3. Silver is more volatile than Gold – therefore, if an investor is bullish and wants

exposure to Precious metals, Silver will rise much more than Gold in a Bull p ,Market

4. Cycle and GOFO analysis points to a major multi-year low – ideal buying levely y p j y y g5. Mining Shares at record levels of cheapness to Bullion6. WAY Charteris Gold and Precious Metals Fund has 70% exposure to Silver

miners7. This fund has the ability to outperform every other mutual fund in the UK. IF a

Bull market in Silver and Gold develops (see separate presentation on the fund)

For professional intermediaries only 23

Ian Williams – Chartered FCSI & Chartered Wealth Manager

Ian has spent the past 35 years trading equities, commodities and G7 government b d i l h k t

Nick Taylor – Chartered FCSI & Head of Private Client Wealth Management

Nick Taylor has 38 years of international investment management experience, gained at Morgan

bonds, covering sales, research, market making and proprietary trading. He was a member of the London Stock Exchange for many years before joining Chase Manhattan

B k ( JP M ) H h k d f D d Kl i

Grenfell, Invesco, and was Managing Director at Cigna International Investment Advisors and Matheson Investment Management. An award‐winning manager,

Bank (now JP Morgan). He then worked for Dresdner Kleinwort Benson and Guinness Mahon (now Investec) before becoming Chairman & Chief Executive of Charteris Treasury Portfolio Managers. Ian also manages the WAY Charteris Gold Fund (

Nicholas has run equity portfolios for a broad range of investors, including institutional pension funds, such as the Cadbury Schweppes Pension Fund alongside running several million pounds of private client portfolios and investment trusts. Nick is also a

(which was the top Fund in the country across all sectors in its first four months of trading, City Financial Strategic Gilt Fund (which was the top UK Gilt Fund in 2007 & 2009*) & The Elite Charteris Premium Income Fund. Ian Williams awarded

p pChartered Fellow of the Chartered Securities Institute.

Mark WilliamsTrustnet Alpha Manager in 2011 & accomplished a CityWire A rating in 2009, 2010 & 2011. Mark graduated from Surrey University with a BA in

2005 and began his career in Investment Management with Forsyth Partners. He joined Charteris in November 2008 as a Junior Fund Manager assisting with the management of both individual private client portfolios as well as the management of the in‐house Charteris funds.

For professional intermediaries only 24

London Office8-9 Lovat Lane, London EC3R 8DW

Exeter OfficeSouthernhay Lodge,

Head of Sales and MarketingMoritz Langlotz,

T: +44 (0) 20 7220 9780Tel: +44 (0)20 7220 9780F 44 (0)20 7929 6925

1a Barnfield Crescent,Exeter, EX1 1QTTel: +44 (0)1392 422 184

Moritz LanglotzE. [email protected]. +44 (0)20 7220 9780

Fax: +44 (0)20 7929 6925www.charteris.co.uk

Tel: +44 (0)1392 422 184Fax: +44 (0)1392 413 222

Gibraltar OfficeGibraltar Office66a Main StreetGibraltarEnquiries – [email protected]

You can find us on Twitter, LinkedIn, Facebook and YouTube

For professional intermediaries only 25

Authorised and regulated by the Financial Conduct Authority & the Gibraltar Financial Services Commission

This presentation is issued by Charteris Treasury Portfolio Management Ltd which is authorised and regulated by the Financial Conduct Authority & the Gibraltar Financial S i C i iServices Commission

• Past performance is not a guide to future performance and investors may not get back the full amount invested

• The price of shares and any income from them may fall as well as rise

• On redemption of holdings investors may not receive back the full amount invested. Management and other fees may reduce the capital investedManagement and other fees may reduce the capital invested

• The information provided does not constitute advice or a personal recommendation for which the duty of suitability would be owed by us and you should seek your own advice as to the suitability of any investment matter mentioned heresuitability of any investment matter mentioned here

• Professional advisers should be aware that this document is intended for their use only and this document is not to be shown or given to any retail investors

• The presentation is made on the basis of our current understanding of United Kingdom Tax laws, which may be subject to change in the future

For professional intermediaries only 26