Embed Size (px)

Citation preview

January 13, 2016 Mr. Brent J. Fields Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 Subject: Comments on Proposed Rule 30e-3, Investment Company Reporting Modernization, File Number S7-08-15 Dear Mr. Fields: Broadridge appreciates the opportunity to submit additional comments to the Securities and Exchange Commission (“SEC”) on its proposed rule 30e-3 which outlines a notice and access delivery option (“notice and access”) for the dissemination of annual and semiannual shareholder reports of mutual funds and ETFs (“fund reports”). 1 As explained in our first comment letter and in further detail below, proposed rule 30e-3 fails to advance the goals of better reaching and informing investors through electronic delivery or realizing greater cost efficiencies. Significant progress on these goals is being made, however, under the SEC’s existing guidance for e-delivery and by NYSE regulated incentive fees for technology development. There is widespread alignment on the importance of these goals among virtually all industry participants. Broadridge has sought to be scrupulously objective in our comments, which are driven by data we possess as the largest shareholder communications services provider in the United States. We have relied on SEC surveys as well as studies we commissioned, as described in our first comment letter. If rule 30e-3 were approved as proposed, it would have a neutral-to-positive economic impact on Broadridge. However, the alternatives to proposed rule 30e-3 create greater savings for investment companies and, at the same time, better inform investors of their fund information. Regardless of the path that the SEC decides to take, Broadridge is committed to work constructively to implement the most efficient and effective means possible.

1 As the largest provider of shareholder communications services, Broadridge has regularly provided the SEC and other interested parties with factual information on the technology and processing implications of potential regulatory changes in areas we serve. Broadridge is committed to pursuing innovations and implementing changes in ways that provide more efficiency, greater use of technology, and increased investor participation. Broadridge’s business model is founded upon the pursuit of increasing levels of participation and efficiency in serving broker-dealers, investment companies, individual investors, and other market participants.

Charles V. Callan SVP Regulatory Affairs Broadridge Financial Solutions, Inc. 51 Mercedes Way Edgewood, NY 11717

Page 2 January 13, 2016

I. EXECUTIVE SUMMARY a. Proposed rule 30e-3 would have a negative impact on viewing levels of millions of investors and a disproportionate impact on seniors and lower income investors. Its comparatively low and diminishing cost savings would benefit only a narrow segment of funds. By proposing to flip the “switch” so that investors will have to affirmatively elect to receive fund reports in paper format, the SEC will have to make a finding that the negative impact on millions of investors will outweigh the low and declining cost savings benefits to a narrow segment of funds.2 The additional data and analysis we provide below show that it would do disproportionate harm to seniors and those who annually earn less than $50,000 – without a meaningful offsetting benefit. The SEC’s prior approval of the notice and access method for proxy materials provides a useful comparison. In that situation the data showed that there was a dramatic reduction in shareholder participation, accompanied by very large cost savings to issuers. In contrast, the proposed rule 30e-3 for fund reports would result in neither significant cost savings nor any investor benefits. Indeed in comparison to notice and access for proxy materials, proposed rule 30e-3 would negatively impact over four times as many investors and produce less than 10% of the printing and postage cost savings.3 b. Technology use by investors is widespread and expanding rapidly. Investors show strong and growing preferences for electing e-delivery, a less expensive alternative to a mailed notice. E-delivery technologies “push” fund reports directly to investors and make them available on enhanced broker Internet platforms (“EBIPs”) and personal cloud solutions, the very places where individuals go to receive communications. These technologies can also send communications through mobile apps that funds and brokers provide. 2 As amply demonstrated by specific survey data, quantitative analysis, and demographic information, proposed rule 30e-3 would negatively impact fund report viewing levels of tens of millions of fund investors. Refer to Broadridge’s August 11, 2015 comment letter and attachments in SEC File No. S7-08-15. 3 In fiscal year 2015, a total of 53.9 million proxy notices were mailed to retail investors and over 240 million fund reports were mailed to fund holders. Based on National Investor Relations Institute surveys of the median unit cost to print proxy materials and actual postage rates (USPS), the estimated cost savings to issuers exceeded $350 million, net of notice and access processing fees, in fiscal year 2015. The median unit cost for printing and postage of a full set of proxy materials can exceed $6.00, while that of a digest-sized fund report is less than $0.50 on average across all funds. Broadridge estimated that if notices were mailed instead of fund reports to investors holding funds in street name, the savings in fiscal year 2015 would have been $36 million, excluding the added costs of fulfillment and of sending Initial Statements.

Page 3 January 13, 2016

By contrast, proposed rule 30e-3 defines a different type of mailed document which, as a practical matter, adds costs and diverts modernization efforts that are based on investors’ actual preferences. It would require investment companies and broker-dealers to make substantial first-year outlays in order to avail themselves of an option whose cost savings are small and diminishing. As a result, a relatively small number of funds would use it. For example, only 5% of funds would realize printing and postage cost savings of $10,000 or more, and this figure excludes the additional costs to build the technology to implement notice and access, the costs of sending Initial Statements, and the costs of fulfilling an unknown number of requests for mailed copies on demand. The data also clearly confirms the SEC’s wisdom and foresight in enabling electronic delivery to investors through its long-standing rules and guidance, including its recent approval of NYSE rules for EBIPs (enhanced brokerage Internet platforms). Together with the SEC’s support for electronic delivery, NYSE incentive fees for technology innovation have helped foster an ongoing digital transformation in how investor communications are delivered and consumed. Investors’ ever-growing adoption of e-delivery is resulting in greater efficiencies each year, and e-delivery is far more efficient than mailing a fund report notice. Moreover, new advancements in electronic delivery can improve the user experience with fund reports in ways that a mailed notice cannot. These advancements can further engage investors who are now on the sidelines rather than disengage them by sending a notice few want -- and even fewer will use. c. Broadridge welcomes collective efforts to further foster the digital transformation that is now underway. The digital transformation now underway is occurring without the large first-year outlays that notice and access entails, without the ongoing fees of a notice and access process, and without harm to individual investors. Working with the industry, individual investors, and regulators, we believe that it is possible to reach levels of technology use and cost savings not deemed likely just a few years ago and not contemplated by proposed rule 30e-3. Broadridge will continue to play a leadership role by investing in technologies and intellectual capital to support efforts to create more participation and more efficiency. For example, Broadridge welcomes the opportunity to work with brokers and funds to send a dual distribution of a “re-imagined” fund report facility to email addresses of investors who have not yet consented to e-delivery of fund reports in order to educate them on the signature benefits of e-delivery and encourage more viewing of fund report information. Broadridge and other stakeholders will continue to monitor the adoption of e-delivery. We welcome the opportunity to report periodically to the SEC with objective data and analysis of progress made.

Page 4 January 13, 2016

II. PROPOSED RULE 30e-3 HAS A DISPROPORTIONATE DEMOGRAPHIC IMPACT ON THOSE WHO ARE MOST VULNERABLE TO A CHANGE IN THE DEFAULT.

The data below further substantiates the findings of the survey information, behavioral studies, and quantitative analyses we provided in our comment letter on August 11, 2015.4 It offers additional evidence that proposed rule 30e-3 would not only impact millions of investors but would also have a disproportionate impact on seniors and on investors who annually earn less than $50,000. This is especially significant because the surveys indicate that by a factor of over four to one, respondents over the age of 65 prefer their current method of receipt over the proposed notice and access method. Our analysis was undertaken in November and December 2015 using the following approach:

• On the assumption that funds are more likely to use the notice and access method for distributions (“jobs”) where the cost savings are significant, we identified 120 jobs where the estimated savings would exceed $100,000. Together, these jobs mailed nearly 32.8 million fund reports to investors. (Had the analysis considered a lower cost savings threshold, far greater numbers of investors would be impacted by the proposal.) 5

• Within this set of jobs, we identified individuals who received fund reports by mail. These individuals would be the most directly impacted by the proposed rule because they would receive mailed notices instead of reports. We excluded investors who received reports electronically, as the proposal does not change the method by which e-delivery recipients receive their reports. We also excluded fund positions held in managed accounts.

• We eliminated duplicate names and addresses from the list of 32.8 million reports sent by mail in order to derive the unique number of names and addresses involved. The result was over 8.3 million unique names and addresses. For these purposes, an investor that holds multiple funds for which she received multiple mailed

4 The information we submitted on August 11, 2015 indicated that the proposal would have a disproportionate impact on seniors. Refer to Forrester Research’s report, “How Might the Proposed Rule on Accessing Annual and Semiannual Fund Reports Affect Investor Behavior,” August 7, 2015, pages 8, 21, and 36. Refer also to report by True North Market Insights, “Annual and Semiannual Report Notification Study: Understanding the Impact of Providing Investors with Mutual Fund and ETF Report Notifications,” June, 2015, pages 7, 21, 25 and 29. 5 Based on Broadridge estimates for fiscal year 2018, if notices are mailed to every investor that would otherwise receive a fund report, a total of 115 million investor positions would be impacted. Based on the Experian analysis, each unique name and address held four funds on average in the fiscal year 2015 data. Assuming that this ratio continues into 2018, the 115 million fund positions would be held by approximately 29 million unique individuals. For any given CUSIP, our analysis considered only the mailing of an annual report or a semiannual report, and not both.

Page 5 January 13, 2016

reports was counted as one impacted investor. (Account numbers, brokerage affiliation, and shareholding information were excluded from the list.)

• A random sample was drawn, comprising over 240,000 name and address records. The records were matched against Experian’s demographic databases. Information is aggregated and reported on the basis of age and annual income.6

• We compared the aggregated results to demographic baseline data on all mutual

fund investors as a group. Baseline data on all mutual fund investors as a group is based on ICI Research Perspective, 2014. Refer to Investment Company Institute 2015 Investment Company Fact Book.7

Age: Fund investors in the 51-69 and 70+ year old age brackets comprise 54% of all fund investors and almost 74% of the impacted group.8

Age in Years All Fund Investors (composition)

Impacted Group (composition)

<35

15%

9%

35-50

31%

18%

51-69

42%

50%

70+ 12% 23%

6 Experian is a leading provider of credit services, consumer information, marketing and data analytics. Experian provides certain aggregated data analysis services to Broadridge. 7 Investment Company Institute 2015 Investment Company Fact Book, June 9, 2015, pages 117 and 119. Source: ICI Research Perspective, “Characteristics of Mutual Fund Investors, 2014” and ICI Research Perspective, “Ownership of Mutual Funds, Shareholder Sentiment, and Use of the Internet, 2014.” 8 Differences are due to rounding.

Page 6 January 13, 2016

Income: Fund investors earning less than $50,000 annually comprise 20% of all mutual fund owners and 25% of the impacted group.9

Annual Income (categories)

All Fund Investors (composition)

Impacted Investors (composition)

< $49,999

20%

25%

$50,000 - $99,999

40%

39%

$100,000 - $199,999

31%

27%

> $200,000

9%

10%

9 The annual income of impacted investors is based on a definition of individual and household data that is highly predictive of a living unit. It is closely aligned with national census data.

Page 7 January 13, 2016

III. PROPOSED RULE 30e-3 PROVIDES COST SAVINGS BENEFITS TO ONLY A SMALL SEGMENT OF FUNDS.

The data below is based on a detailed analysis of the industry-level data we provided on August 11, 2015. It shows that the cost savings of proposed rule 30e-3 would benefit only a small segment of funds. The analysis looks at each of the 10,428 fund report distribution “jobs” that Broadridge processed in fiscal year 2015. We grouped the underlying jobs into their respective cost savings ranges. Approximately two-thirds of the total number of jobs would have no net cost savings or incur greater costs (i.e., 6,633 jobs out of a total of 10,428). Another 15% of the jobs (or 1,575 in number) would save less than $100 each.10 The cost savings of proposed rule 30e-3 would benefit a relatively small segment of mutual funds. These estimates exclude the start-up costs to investment companies (e.g., mailing Initial Statements) and the unknown costs associated with fulfilling on-demand requests for mailed reports.

Estimated Cost Savings (Ranges)

Number of Jobs within Each Range

No cost savings (or a net cost incurred)

6,633

< $100 1,575 $100 - $1,000 933

$1,000 - $5,000 544 $5,000 - $10,000 210 $10,000 - $25,000 230

$25,000 - $100,000 183 > $100,000 120

Total Number of Jobs Processed (FY15)

10,428

The percentage of funds that might choose to use the notice and access option would likely be small in comparison to the percentage of companies that use notice and access

10 The information covers distributions to investors that held funds in street name in fiscal year 2015. It is based on NYSE regulated rates, including tiered rates for notice and access. We excluded estimates of other costs that investment companies and/or broker-dealers would incur in using notice and access such as for the fulfillment of investor requests for hard copies and the costs of sending Initial Statements.

Page 8 January 13, 2016

for proxy deliveries. Only 5% of the fund report distribution jobs have a benefit of $10,000 or more, and this excludes the added costs of start-up, Initial Statements, and fulfillment. By comparison, in the 12 months ending June 30, 2015, a total of 39% of operating companies utilized the notice and access method for annual meeting proxy solicitations.11 The far higher average unit costs of proxy materials provide a total savings opportunity that simply does not exist for most fund reports whose average unit costs are far lower. The notice and access method is not designed to create delivery savings for documents whose unit costs of printing and postage are low to begin with.12 Moreover, distributing notices adds work and, therefore, additional cost to the process. Examples of the added work include the following activities: developing, handling, and merging a third distribution method; handling new fulfillment requirements; coding and processing new consent types; and, among other examples, providing services to analyze and process a variety of mail consolidation strategies. A list of examples of the operational details involved with notice and access processing was provided in our earlier comment letter. Proposed rule 30e-3 is largely silent on the essential role broker-dealers play in efficiently and effectively serving the fund report communications needs of their client account holders. Recently, we sampled the document fulfillment processes of 20 investment companies to better understand whether these processes might be up to the task of fulfilling on-demand requests for fund reports of funds held in street name. The results are found in Attachment A, “Sample of Fulfillment Results for Document Requests.” Investors contacted fund companies directly using toll-free numbers and/or email addresses provided on summary prospectuses or found on the contact page of the fund’s website. The contacts were initiated to request printed information by mail. The results showed that the process was neither uniform nor efficient in serving the needs of investors holding funds in street name. In several cases, no materials were received.

11 This figure includes equity issuers and excludes mutual funds, ADRs and contested solicitations. 12 Approximately 5% of the fund report mailings in FY15 involved a relatively expensive 9”x12” flat that had a unit postage rate of $1.00 or more.

Page 9 January 13, 2016

IV. THE ALTERNATIVES PROVIDE SIGNIFICANT COST SAVINGS TO INVESTMENT COMPANIES, WITHOUT THE NEGATIVE IMPACT ON INVESTORS. a. Electronic Delivery As electronic delivery grows, the percentage of physical mailings shrinks and this erodes the potential savings from mailing notices instead of printed copies of fund reports. For funds held in street name, e-delivery has grown from 19% of all report deliveries in 2010 to 43% of all deliveries in 2015. Broadridge projects that e-deliveries will comprise 59% of deliveries in three years’ time without a change in the rules.

Our growth-rate assumptions are based on recent (5-year) momentum, experience with existing technologies, and internal projections for new developments. These include the following factors and examples, among others:

• EBIPs are now made available by brokers who as a group have over 50% of all beneficial shareholder accounts. All but one of these installations provide access to fund reports at no additional charge to investment companies.13 Prior analyses have shown that the rates of consent to e-delivery are greater at the group of brokers offering EBIPs than at brokers not offering EBIPs.

• Capabilities to electronically deliver investor communications to individuals’ personal cloud solutions, such as Dropbox™, Evernote, Microsoft OneDrive and Amazon Cloud Drive. 14

13 Under NYSE rules, the EBIP incentive fee is paid on a one-time basis when a full set of proxy materials is converted to an e-delivery. 14 Broadridge’s Inlet technology provides communications from participating brokers and funds to individuals upon consent of the user.

19% 23% 30%

37% 40% 43% 48% 54% 59%

0% 10% 20% 30% 40% 50% 60% 70%

2010 2011 2012 2013 2014 2015 2016 est. 2017 est. 2018 est.

E - Delivery Is a Significant and Growing Percentage of All Deliveries

Page 10 January 13, 2016

• Capabilities to electronically delivery investor communications to individuals through broker-dealer or fund company mobile apps.

• New, more-flexible email templates are available with the redesign of proxyvote.com (September 2015), Broadridge’s communications, e-consent, and proxy voting platform for individual investors. These new templates are being used to enhance branding efforts and encourage open rates and ‘clicking-thru.”

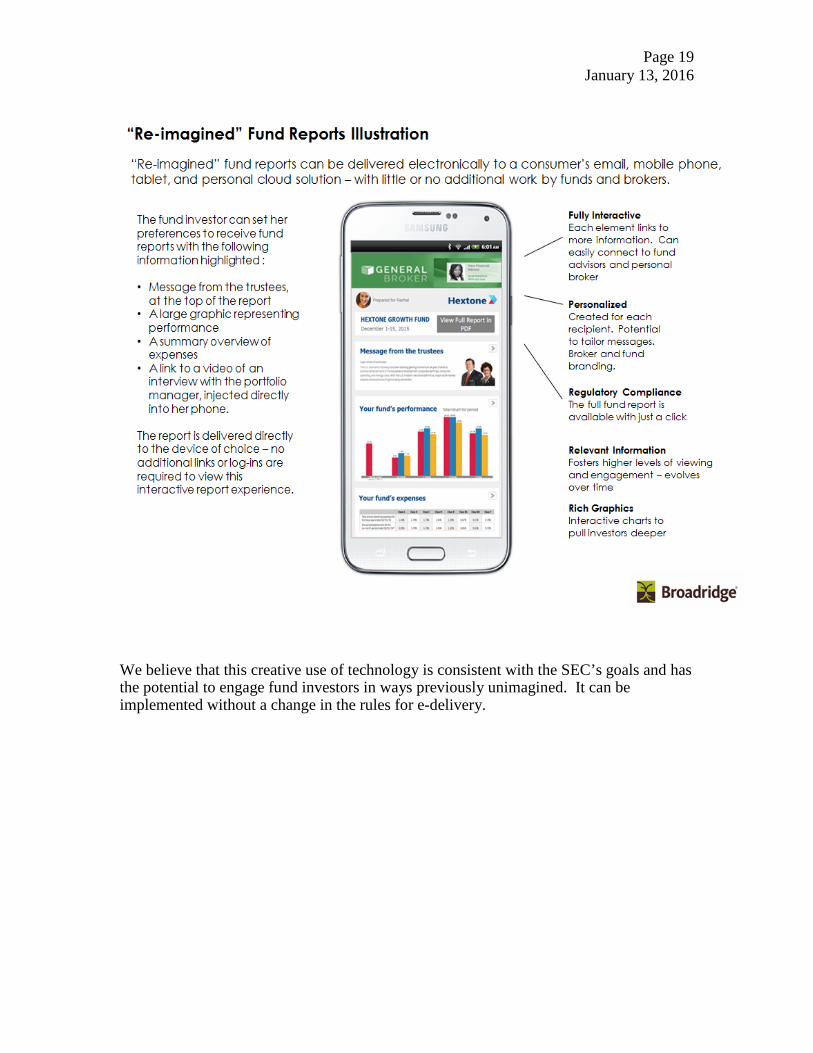

• Technology developments that can “re-imagine” how annual and semiannual reports are presented by providing a facility for individual investors to choose to see displayed the fund information that is of most interest to them. (Refer to Attachment B for an illustration)

• The combined efforts of brokers, funds, and Broadridge to drive greater levels of

electronic delivery of virtually all document types. Examples include, among others: adding invitations to e-delivery on most mailed communications, provision of a central enrollment site, and processing to encourage enrollments by account holders in e-delivery for each communication.

Page 11 January 13, 2016

Recently, we sought third-party involvement with the calculations we performed in arriving at estimates of the delivery cost savings of the proposal and its alternatives.15 We also sought third-party confirmation of the applicable NYSE fees.16 Schedule of Comparative Estimated Delivery Cost Savings for Alternatives to Proposed Rule 30e-3

Industry Spending (Printing, Postage and Fees)

FY18 Savings Opportunity

(vs. FY18 baseline)

Net Savings Per Report (vs. FY18 baseline)

FY15 ($m) FY18 est. ($m) FY18 est. ($m) FY18 est. ($)

Baseline 354 382 - -

Notice and Access Option

318 364 18 0.02

Comparison of the Alternatives

E-Delivery Option

144 179 203 0.28

Summary Report Option

221 252 130 0.18

As shown in the analysis (which is described in detail in our first comment letter), e-delivery is the least costly of any of the alternatives, and it results in the greatest savings. If all mailed reports in 2018 were instead sent electronically, the savings are estimated to be $203 million. In comparison to mailing notices, e-delivery creates incremental savings of approximately $185 million. By growing from 43% of deliveries, currently, to 59% of deliveries, as projected, e-delivery creates an incremental savings of over $100 million to investment companies. b. Summary Reports (as an alternative to mailed notices) Use of summary reports would also provide significant savings to fund companies, while meeting the desires of investors. SEC studies have consistently identified strong interest 15 The schedule was subjected to certain agreed-upon procedures performed by a “Big Four” independent accounting firm. 16 Refer to Attachment C, Memorandum from Davis Polk, “Cost-Savings Estimates in Broadridge’s Comment Letter Concerning Proposed Rule 30e-3, January 13, 2016”

Page 12 January 13, 2016

among individual investors in receiving user-friendly summary information with links to additional or “layered” information for more detail.17 In our earlier comment letter, Broadridge determined that the benefits of mailing summary reports rather than full reports were approximately $130 million. In comparison to mailing notices, sending summary reports creates an incremental savings of approximately $112 million in fiscal year 2018. Summary reports do not entail the added fees of notice and access.

17 Refer to the SEC’s Dodd-Frank-mandated “Study Regarding Financial Literacy Among Investors.” Specifically, refer to “Investor Testing of Selected Mutual Fund Annual Reports (Revised),” Siegel + Gale, Submitted to: The U.S. Securities and Exchange Commission February 9, 2012. Earlier studies were conducted in connection with SEC rulemaking for an enhanced (i.e., summary) prospectus delivery option, File No. S7-28-07.

Page 13 January 13, 2016

V. CONCLUSION At its heart, proposed rule 30e-3 changes the underlying default on fund report delivery. It flips the “switch” so that investors will have to affirmatively elect to receive fund reports in paper format. Based on the data, the SEC will have to make a finding that the negative impact on millions of investors will outweigh the low and declining cost savings benefits to a narrow segment of funds. The well-known behavioral economist Eric Johnson framed this tradeoff in the context of the SEC’s then-proposed rules for proxy notice and access:

If defaults make a difference, how do we know what is the right default? Economists and legal scholars have started to ask this question, and developed an interesting answer: Defaults should encourage the behavior that makes the most people better off. This approach (Camerer, Issacharoff, Loewenstein, O'Donoghue, and Rabin, 2003; Thaler and Sunstein, 2003) makes the following argument: If defaults have an effect, they should be used to improve peoples’ average outcomes. In a case like retirement savings, where Americans are typically described as under-saving toward their retirement, changing the default from zero to some positive number seems to make sense. Choice is not taken away in these cases; people with strong feelings can always change the default. The argument is that it helps people who are unreasonably lazy or suffer from loss aversion, and in fact, makes the correct implied endorsement. If the sole goal of SEC information provision was consumer consumption of information and participation in voting, it would appear that the current system of mailing information unless investors opt-out and select electronic forms would be the better default. The proposed rule takes something away. 18

The SEC’s prior approval of the notice and access method for proxy materials provides a useful comparison. In that situation, the data showed that there was a dramatic reduction in shareholder participation, accompanied by very large cost savings to issuers. In contrast, the proposed rule 30e-3 for fund reports would result in neither significant cost savings nor any investor benefits. Indeed in comparison to notice and access for proxy materials, proposed rule 30e-3 would negatively impact over four times as many investors and produce less than 10% of the printing and postage cost savings As detailed in our first comment letter, and further herein, the data shows that proposed rule 30e-3 does not advance the goals of better informing investors and providing greater cost efficiencies. These goals are being fostered very successfully under the SEC’s existing guidance for e-delivery and by NYSE regulated fees that encourage technology development. 18 “Defaults and Deciding to Use Information, A White Paper Reviewing the Role of Defaults in Decision Making: Implications for Investor Participation in the Proposed Notice and Access Scenario,” Eric Johnson, Columbia Business School, February 9-10, 2006.

Page 14 January 13, 2016

As always, regardless of the position that the SEC adopts, Broadridge stands ready to work in an efficient and effective manner. We appreciate the opportunity to submit comments and to provide additional information where helpful. Sincerely,

cc: Mary Jo White, Chair, U.S. Securities and Exchange Commission Michael Piwowar, Commissioner

Kara Stein, Commissioner David Grim, Director, Division of Investment Management Diane Blizzard, Associate Director, Division of Investment Management Sara Cortes, Senior Special Counsel, Division of Investment Management Jennifer McHugh, Senior Advisor to the Director, Division of Investment Management Andrew Donohue, Chief of Staff to the Chair

ATTACHMENTS

A. Sample of Fulfillment Results for Document Requests B. Illustration of How Technology Can Be Utilized to “Re-Imagine” the User Experience with Fund Reports Delivered Electronically C. Memorandum from Davis Polk on the Cost-Savings Estimates in Broadridge’s Comment Letter Concerning Proposed Rule 30e-3, January 13, 2016

Page 15 January 13, 2016

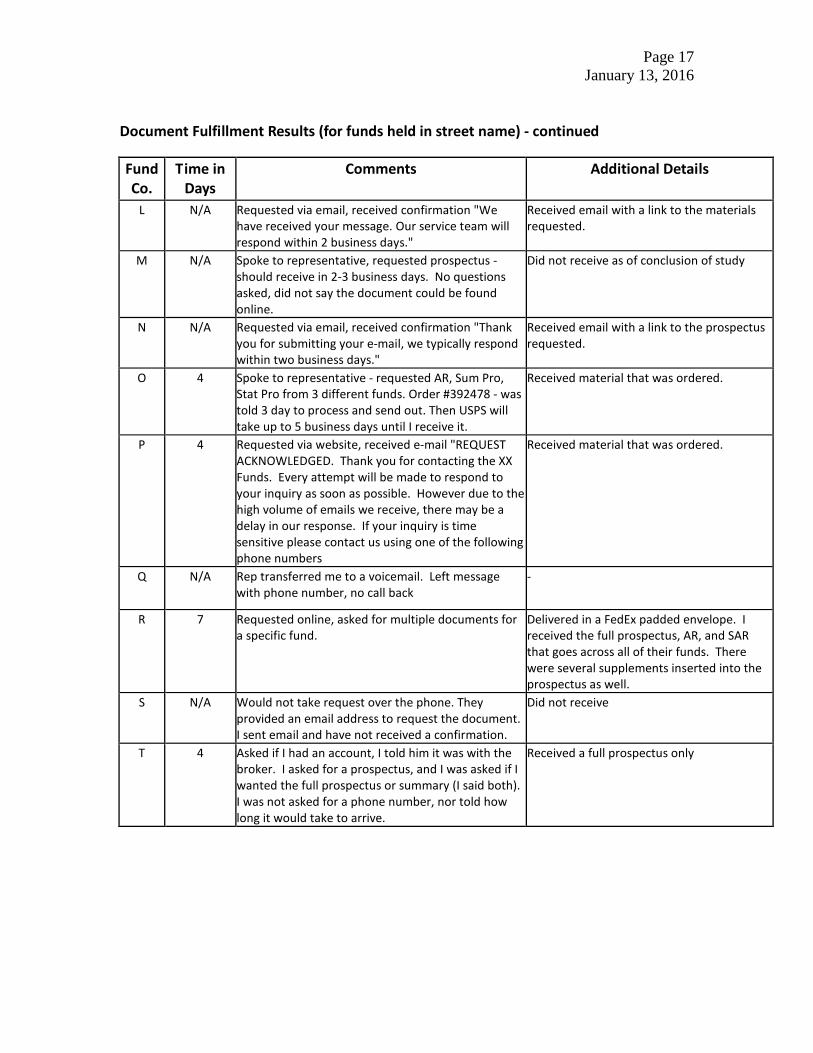

Attachment A Sample of Fulfillment Results for Document Requests Proposed rule 30e-3 was largely silent on the essential role broker-dealers provide in efficiently and effectively serving the fund report communications needs of their client account holders. Our first comment letter discussed why a “control number process” and central site would be essential elements of making the notice and access process operate efficiently and effectively. We asked investors holding funds in street name to contact their fund companies to request printed materials by mail. In most cases, they used the toll-free number found on the fund’s summary prospectus; in some cases, they used the email address provided or the contact page provided on the fund’s website. Contacts were initiated in November and December, 2015. The investors took notes on their interactions with fund company representatives and counted the days it took to receive the requested materials. The results are reported in the following charts. In eight of the cases, no printed materials were received as requested; in one case, a request was pending at the time of reporting. Materials typically arrived in 4 to 7 days. In a few cases, the materials received were not the materials requested. In five cases, materials were sent by overnight postage. In one case, the investor’s high-net worth financial advisor became involved, and yet materials were not received. In several cases, fund company representatives asked for account numbers, social security numbers, and other brokerage information which they were not in a position to verify. Under proposed rule 30e-3, there would likely be a far higher volume of requests for printed materials for several reasons, among others. First, the volume of fund reports sent annually exceeds the volume of prospectuses, typically by a factor of two or more, and this could logically result in more requests being made. Second, because a summary prospectus provides an investor with useful information in hand that may be sufficient for their purposes, they may not feel the need to request additional printed information. In contrast, the proposed printed notice does not contain the key details of information found in fund reports – investors would need to request to receive printed reports.

Page 16 January 13, 2016

Document Fulfillment Results (for funds held in street name)

Fund Co.

Time in Days

Comments Additional Details A 7 Sent via UPS Asked for acct # B 4 Sent via UPS Asked for acct # C N/A Sent a request to the email address listed. Received

an automated acknowledgement by email of the message sent. My high net worth advisor sent me an email to follow up – telling me to look at the website or call her.

First asked me for account # or SS# (held in a brokerage account)

D 13 Received out-of-date prospectus w/ supplement (POD) via UPS - never received annual report; called on 11/17 - annual report still pending, will reorder and find out why it wasn't sent; will also have the correct prospectus sent to me.

Received final pieces via UPS (13 days later)

E 5 Spoke to representative - requested AR, Sum Pro from 4 different funds. Asked who my dealer was & then my SS#. Took my address and stated they will be sent out shortly and then disconnected.

Representative was annoyed and suggested I obtain the information online. When I advised I didn't have a computer, they asked how did I get this number?

F 5 Called the representative, took my information and advised a hard copy will be mailed directly to my home with 3-5 business days.

Received UPS. Material received 5 days later Prospectus and October 2015 Quarterly Statistical update.

G 7 Spoke to representative, requested an investment kit - will be mailing out over the next few days.

Requested one prospectus, received an entire kit containing Summary Pros for 6 different funds, a letter, several different account applications, a BRE, a performance sheet covering all funds, a quarterly report, an article reprint, and a marketing piece.

H 5 Ordered 4 Pros at Fund’s website and received a popup - You will receive your order in approximately 3-7 business days.

Received photocopies of material stapled

I 4 Didn't ask if I owned the fund. Did tell me that the latest annual report covers up to 9/30/15, and that it will take 5 to 7 business days to receive material. Requested a phone number.

Received a personalized letter, A/R dated 12/31/14, SAR dated 6/30/15, and a fact sheet dated 9/30/15. Sent in a plain envelope.

J N/A It took 3 attempts to get live person on the phone. They asked a lot of questions, but finally agreed to mail the hard copy material to me.

Did not receive

K N/A Rep said he could not send me the document (I requested an AR) because my account was not with the Fund company directly. I explained I owned the fund, through my broker, and he directed me to download it and/or print it off the website. He said I could contact my broker if I wanted to receive a hard copy.

Did not receive

Page 17 January 13, 2016

Document Fulfillment Results (for funds held in street name) - continued

Fund Co.

Time in Days

Comments Additional Details

L N/A Requested via email, received confirmation "We have received your message. Our service team will respond within 2 business days."

Received email with a link to the materials requested.

M N/A Spoke to representative, requested prospectus - should receive in 2-3 business days. No questions asked, did not say the document could be found online.

Did not receive as of conclusion of study

N N/A Requested via email, received confirmation "Thank you for submitting your e-mail, we typically respond within two business days."

Received email with a link to the prospectus requested.

O 4 Spoke to representative - requested AR, Sum Pro, Stat Pro from 3 different funds. Order #392478 - was told 3 day to process and send out. Then USPS will take up to 5 business days until I receive it.

Received material that was ordered.

P 4 Requested via website, received e-mail "REQUEST ACKNOWLEDGED. Thank you for contacting the XX Funds. Every attempt will be made to respond to your inquiry as soon as possible. However due to the high volume of emails we receive, there may be a delay in our response. If your inquiry is time sensitive please contact us using one of the following phone numbers

Received material that was ordered.

Q N/A Rep transferred me to a voicemail. Left message with phone number, no call back

- R 7 Requested online, asked for multiple documents for

a specific fund. Delivered in a FedEx padded envelope. I received the full prospectus, AR, and SAR that goes across all of their funds. There were several supplements inserted into the prospectus as well.

S N/A Would not take request over the phone. They provided an email address to request the document. I sent email and have not received a confirmation.

Did not receive

T 4 Asked if I had an account, I told him it was with the broker. I asked for a prospectus, and I was asked if I wanted the full prospectus or summary (I said both). I was not asked for a phone number, nor told how long it would take to arrive.

Received a full prospectus only

Page 18 January 13, 2016

Attachment B

Illustration of How Technology Can Be Utilized to “Re-Imagine” the User Experience with Fund Reports Delivered Electronically Unlike a summary prospectus delivery option, a “re-imagined” fund report does not need to require a change in the rules. It can be provided to investors with comparatively little additional work by broker-dealers and investment companies. It has the potential to substantially improve the investor’s experiences in ways a mailed notice cannot. Technology facilities can be developed to enable each investor to easily choose the summary information he or she most wants to see in fund reports that are subsequently e-delivered. These facilities can be made available from the website of a fund- or broker for all investors that have consented to e-delivery (including on “EBIPs,” i.e., enhanced broker Internet platforms). Because individual investors would be afforded a more customized user experience, the technology could spur more individuals to opt-in for e-delivery to view information on their investments. As an alternative to choosing, a fund or broker could offer key information to investors, for starters. As learning builds, the information can be modified based on the needs and viewing habits of each individual. The illustration below shows an example of the individualized summary report an illustrative investor can create from the information fund companies file. The technology can present different sections of a fund report, together with examples of user-friendly graphics that display essential information. When fund reports are subsequently delivered electronically that information is prominently displayed. Individual content selections would be indexed and processed each time a fund report is delivered. In all cases, these distributions function in ways that are similar to e-deliveries; that is, they provide compliance links to complete reports. For example, the investor wishes to see information that highlights her fund’s performance, expenses, and messages from the trustees in each of the fund reports she subsequently receives. The technology enables her to create her own user-friendly summary report. The facility can also display broker and fund messages and branding, and provide an easy means to connect to her broker or financial advisor. The entire experience can be delivered directly to her device of choice – no additional links or log-ins are required to view this interactive report experience.

Page 19 January 13, 2016

We believe that this creative use of technology is consistent with the SEC’s goals and has the potential to engage fund investors in ways previously unimagined. It can be implemented without a change in the rules for e-delivery.

Page 20 January 13, 2016

Attachment C