Embed Size (px)

Citation preview

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

Communicatingand Interpreting

AccountingInformation

Chapter 5

5-2

Learning Objectives

Recognize the people involved in the accounting communication process

(regulators, managers, directors, auditors, information intermediaries and users), their role in the process and the guidance they

receive from legal and professional standards.

5-3

Players in the Accounting

Communication Process

An An unqualifiedunqualified opinion states opinion states that the financial statements are that the financial statements are fair presentations in all material fair presentations in all material

respects in conformity with respects in conformity with GAAP.GAAP.

Independent AuditorsIndependent AuditorsVerificationVerification

Partners, Managers, StaffPartners, Managers, StaffGuided by GAASGuided by GAAS

ManagementManagementPreparationPreparation

CEO, CFO, Accounting StaffCEO, CFO, Accounting StaffGuided by GAAPGuided by GAAP

5-4

Information Information IntermediariesIntermediaries

Analysis and AdviceAnalysis and AdviceFinancial analysis, Financial analysis,

Information servicesInformation services

Financial analysts Financial analysts make predictions make predictions

concerning concerning companies’ future companies’ future earnings and stock earnings and stock

prices.prices.

Independent AuditorsIndependent AuditorsVerificationVerification

Partners, Managers, StaffPartners, Managers, StaffGuided by GAASGuided by GAAS

ManagementManagementPreparationPreparation

CFO, CEO, Accounting StaffCFO, CEO, Accounting StaffGuided by GAAPGuided by GAAP

Players in the Accounting

Communication Process

5-5

Information Information IntermediariesIntermediaries

Analysis and AdviceAnalysis and AdviceFinancial analysis, Financial analysis,

Information servicesInformation services

Financial analysts Financial analysts make predictions make predictions

concerning concerning companies’ future companies’ future earnings and stock earnings and stock

prices.prices.

Independent AuditorsIndependent AuditorsVerificationVerification

Partners, Managers, StaffPartners, Managers, StaffGuided by GAASGuided by GAAS

ManagementManagementPreparationPreparation

CFO, CEO, Accounting StaffCFO, CEO, Accounting StaffGuided by GAAPGuided by GAAP

Web Info Services:Web Info Services:www/sec/govwww/sec/gov

www.compustat.comwww.compustat.comwww.djnr.comwww.djnr.com

www.bloomberg.comwww.bloomberg.comwww.firstcall.comwww.firstcall.comwww.hoover.comwww.hoover.com

Players in the Accounting

Communication Process

5-6

Government Government RegulatorsRegulatorsVerificationVerification

SEC MembersSEC MembersGuided by SEC regs.Guided by SEC regs.

UsersUsersAnalysis and DecisionAnalysis and Decision

Investors, Lenders, etc.Investors, Lenders, etc. Public companies only

ManagementManagementPreparationPreparation

CFO, CEO, Accounting StaffCFO, CEO, Accounting StaffGuided by GAAPGuided by GAAP

Information Information IntermediariesIntermediaries

Analysis and AdviceAnalysis and AdviceFinancial analysis, Financial analysis,

Information servicesInformation services

Independent AuditorsIndependent AuditorsVerificationVerification

Partners, Managers, StaffPartners, Managers, StaffGuided by GAASGuided by GAAS

Players in the Accounting

Communication Process

5-7

Ensuring the Integrity of Financial Information Communication Process

RegulatorsRegulatorsStandard Setting and Standard Setting and

VerificationVerificationSECSEC

ManagementManagementPrimary ResponsibilityPrimary Responsibility

CFO, CEO, Accounting StaffCFO, CEO, Accounting Staff

Auditors (CPAs)Auditors (CPAs)VerificationVerification

Partners, Managers, StaffPartners, Managers, Staff

DirectorsDirectorsOversightOversight

Audit Committee Audit Committee (Independent directors)(Independent directors)

5-8

Using Financial Reports

ManagementManagementPrimary ResponsibilityPrimary Responsibility

CFO, CEO, Accounting StaffCFO, CEO, Accounting Staff

Information Information IntermediariesIntermediaries

Analysis and AdviceAnalysis and AdviceFinancial analysts, Financial analysts,

Information servicesInformation services

UsersUsersAnalysis and DecisionAnalysis and DecisionInstitutional and private Institutional and private

investors, Lenders, investors, Lenders, Suppliers, Customers, etc.Suppliers, Customers, etc.

5-9

Guiding Principles for Communicating Useful Information

Primary Objective of External Financial ReportingPrimary Objective of External Financial Reporting To provide economic information to external users To provide economic information to external users

for decision making. for decision making.

Primary Qualitative CharacteristicsPrimary Qualitative Characteristics

Relevance:Relevance: Timely and Predictive Feedback ValueTimely and Predictive Feedback Value

Reliability:Reliability: Accurate, Unbiased, and VerifiableAccurate, Unbiased, and Verifiable

Secondary Qualitative CharacteristicsSecondary Qualitative Characteristics

Comparability:Comparability: Across businessesAcross businesses

Consistency:Consistency: Over timeOver time

5-10

Guiding Principles for Communicating Useful Information

Primary Objective of External Financial ReportingPrimary Objective of External Financial Reporting To provide economic information to external users To provide economic information to external users

for decision making.for decision making.

Primary Qualitative CharacteristicsPrimary Qualitative Characteristics

Relevance:Relevance: Timely and Predictive and Feedback ValueTimely and Predictive and Feedback Value

Reliability:Reliability: Accurate, Unbiased, and VerifiableAccurate, Unbiased, and Verifiable

Secondary Qualitative CharacteristicsSecondary Qualitative Characteristics

Comparability:Comparability: Across businessesAcross businesses

Consistency:Consistency: Over timeOver time

The full-disclosure principles require . . .The full-disclosure principles require . . .

3.3.A complete set of financial statements,A complete set of financial statements,andand

• Notes to the financial statementsNotes to the financial statements

5-11

International Accounting Standards Board and Global Differences in Accounting

Difference in Accounting Standards US GAAP IFRSExtraordinary items Permitted ProhibitedLIFO for inventory Permitted ProhibitedReversal of inventory write-downs Prohibited RequiredBasis of property, plant, and equipment Historical cost Fair Value or

Historical cost

IInternational nternational FFinancial inancial RReporting eporting SStandardstandards

5-12

Learning Objectives

Identify the steps in the accounting communication process, including the issuance

of press releases, annual reports, quarterly reports and SEC filings as well as the role of

electronic information services in this process.

5-13

The Disclosure Process

Press ReleasesPress Releases are used to announce are used to announce quarterly and annual earnings as soon as quarterly and annual earnings as soon as

the verified figures are available.the verified figures are available.

Earnings Press Release Excerpt for Callaway GolfEarnings Press Release Excerpt for Callaway Golf

Callaway® Golf

CARLSBAD, Calif. -- Jan. 22, 2004-- Callaway Golf Company (NYSE:ELY) today reported record sales for the full year ended December 31, 2003, announcing net sales of $814 million compared with $793 million for the prior year. Net income for the full year was $46 million versus . . . .

5-14

Annual Reports

For For privatelyprivately held companies, annual reports held companies, annual reports are simple documents that include:are simple documents that include:

1.1. Four basic financial statements.Four basic financial statements.

2.2. Related notes (footnotes).Related notes (footnotes).

3.3. Report of independent accountants Report of independent accountants (auditor’s opinion) if the statements are (auditor’s opinion) if the statements are audited.audited.

5-15

Annual Reports

For For publicpublic companiescompanies, annual reports are , annual reports are elaborate due to SEC reporting elaborate due to SEC reporting

requirements:requirements:1.1. A Nonfinancial SectionA Nonfinancial Section

A letter to the stockholders, a description of A letter to the stockholders, a description of management’s philosophy, products, management’s philosophy, products, successes, etc.successes, etc.

2.2. A Financial SectionA Financial Section See next slide for a detailed listing . . . See next slide for a detailed listing . . .

5-16

Annual Reports - Financial Section

• Summarized financial Summarized financial data for 5- or 10-years.data for 5- or 10-years.

• Management Discussion Management Discussion and Analysis (MD&A).and Analysis (MD&A).

• The four basic financial The four basic financial statements.statements.

• Notes (footnotes).Notes (footnotes).• Independent Independent

Accountant’s Report and Accountant’s Report and the Management the Management Certification.Certification.

1.1. Recent stock price Recent stock price information.information.

2.2. Summaries of the Summaries of the unaudited quarterly unaudited quarterly financial data.financial data.

3.3. Lists of directors and Lists of directors and officers of the company officers of the company and relevant addresses.and relevant addresses.

5-17

Quarterly Reports

Usually begin with short letter to stockholdersUsually begin with short letter to stockholders Condensed Condensed unauditedunaudited income statement and income statement and

balance sheet for the quarter.balance sheet for the quarter. Often, cash flow statement and statement of Often, cash flow statement and statement of

stockholders’ equity are stockholders’ equity are omittedomitted. Some notes to . Some notes to the financial statements also may be omitted.the financial statements also may be omitted.

5-18

SEC Reports

Form 10-K Annual ReportForm 10-K Annual Report•Due within 90 days of the fiscal year-end.Due within 90 days of the fiscal year-end.•Contains audited financial statements.Contains audited financial statements.

Form 10-Q Quarterly ReportForm 10-Q Quarterly Report•Due within 45 days of the end of the quarter.Due within 45 days of the end of the quarter.•Financial statements can be unaudited.Financial statements can be unaudited.

Form 8-K Current ReportForm 8-K Current Report•Due within 15 days of the major event date.Due within 15 days of the major event date.•Financial statements can be unaudited.Financial statements can be unaudited.

5-19

Learning Objectives

Recognize and apply the different financial statement and disclosure formats used by

companies in practice.

5-20

Financial Statement Formats

Let’s take aLet’s take acloser lookcloser lookat the assetat the asset

section of thesection of thebalance balance sheet!sheet!

5-21

5-22

Current assets Current assets are assets that are assets that

will be turned into will be turned into cash or expire cash or expire (be used up) (be used up)

within the longer within the longer of one year or the of one year or the operating cycle.operating cycle.

5-23

Property, plant and Property, plant and equipment includes equipment includes assets with useful assets with useful lives of more than lives of more than one year acquired one year acquired

for use in the for use in the business rather business rather

than for resale. The than for resale. The amount is reported amount is reported net of net of accumulated accumulated

depreciationdepreciation..

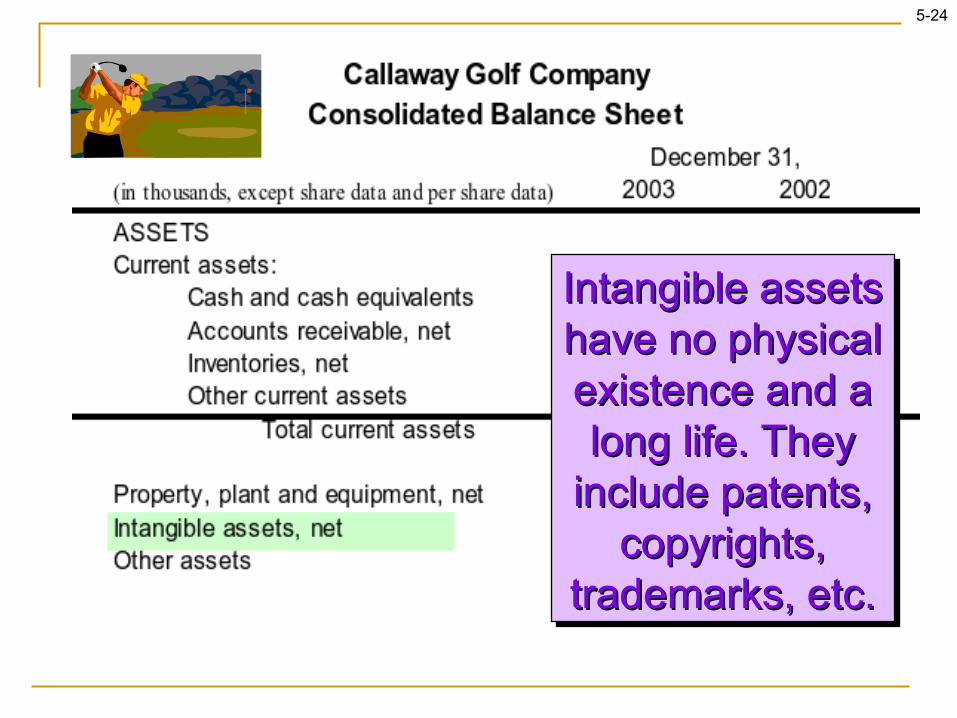

5-24

Intangible assets Intangible assets have no physical have no physical existence and a existence and a long life. They long life. They

include patents, include patents, copyrights, copyrights,

trademarks, etc.trademarks, etc.

5-25

Let’s now look Let’s now look at the liability at the liability section of a section of a classified classified

balance sheet.balance sheet.

5-26

5-27

Current liabilities Current liabilities are obligations are obligations that will be paid that will be paid

with current with current assets, normally assets, normally within one year.within one year.

5-28

Long-term liabilities are debts that have Long-term liabilities are debts that have maturity dates extending beyond one maturity dates extending beyond one

year from the balance sheet date.year from the balance sheet date.

5-29

Finally, we get to the

stockholders’ equity section of

a classified balance sheet.

5-30

Contributed capital is often shown in Contributed capital is often shown in two separate accountstwo separate accounts

2.2. Common stock.Common stock.

3.3. Additional paid-in capital.Additional paid-in capital.

5-31

Retained earnings is the total Retained earnings is the total earnings of the company less the earnings of the company less the

total dividends declared since total dividends declared since inception of operations.inception of operations.

5-32

Balance Sheet Ratios andDebt Contracts

When a company borrows money, it often agrees to certain restrictions on activity.

Ratios typically part of the borrowing agreement include:

Total Liabilities÷ Stockholders' Equity= Debt-to-Equity Ratio

Current Assets÷ Current Liabilities= Current Ratio

5-33

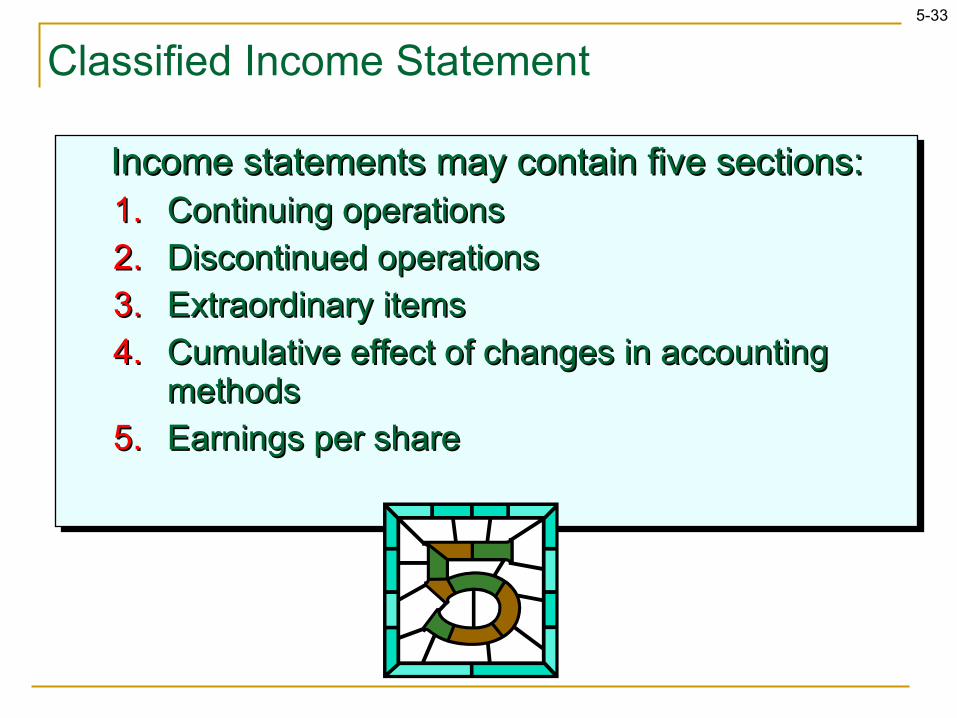

Classified Income Statement

Income statements may contain five sections:Income statements may contain five sections:1.1. Continuing operationsContinuing operations

2.2. Discontinued operationsDiscontinued operations

3.3. Extraordinary itemsExtraordinary items

4.4. Cumulative effect of changes in accounting Cumulative effect of changes in accounting methodsmethods

5.5. Earnings per shareEarnings per share

5-34

Classified Income Statement

Net sales− Cost of goods sold

Gross profit− Operating expenses

Income from operations± Nonoperating revenues/expenses and gains/losses

Income before income taxes− Income tax expense

Net income

General Format for the Classified Income StatementGeneral Format for the Classified Income Statement

Gross sales minus any Gross sales minus any discounts, returns, and discounts, returns, and

allowances during the period.allowances during the period.

5-35

Net sales− Cost of goods sold

Gross profit− Operating expenses

Income from operations± Nonoperating revenues/expenses and gains/losses

Income before income taxes− Income tax expense

Net income

General Format for the Classified Income StatementGeneral Format for the Classified Income Statement

Classified Income Statement

Cost of inventory sold.Cost of inventory sold.

5-36

Net sales− Cost of goods sold

Gross profit− Operating expenses

Income from operations± Nonoperating revenues/expenses and gains/losses

Income before income taxes− Income tax expense

Net income

General Format for the Classified Income StatementGeneral Format for the Classified Income Statement

Classified Income Statement

Not related to the company’s primary Not related to the company’s primary operations. Usually includes interest income or operations. Usually includes interest income or

expense and any gains or losses from the expense and any gains or losses from the retirement of equipment.retirement of equipment.

5-37

Common-Size Income Statement

Total revenue isequal to 100%.

5-38

Earnings Per Share

EPS =Net Income Available to Common Shareholders

Weighted Average Number of Shares Outstanding During the Reporting Period

Basic EPSBasic EPS

5-39

Earnings Per Share

EPS =Net Income Available to Common Shareholders

Weighted Average Number of Shares Outstanding During the Reporting Period

Diluted EPSDiluted EPSStock options, debt securities, Stock options, debt securities,

equity securities are assumed to equity securities are assumed to be converted into common stock be converted into common stock at the beginning of the period.at the beginning of the period.

5-40

Statement of Cash Flows

Recall that the Statement of Cash Flows is Recall that the Statement of Cash Flows is divided into divided into threethree major sections. major sections.

2.2. Cash flows from operating activities.Cash flows from operating activities.

3.3. Cash flows from investing activities.Cash flows from investing activities.

4.4. Cash flows from financing activities.Cash flows from financing activities.

We will examine the indirect method of We will examine the indirect method of preparing the statement. This format begins preparing the statement. This format begins

with a with a reconciliationreconciliation of accrual income to of accrual income to cash flows from operations.cash flows from operations.

5-41

This is the operating activities section of Callaway using theThis is the operating activities section of Callaway using the indirect indirect methodmethod. Begin with accounting net income and arrive at cash . Begin with accounting net income and arrive at cash

provided by operating activities.provided by operating activities.

5-42

While these While these items are on items are on the income the income

statement, they statement, they have no have no

current cash current cash effect.effect.

5-43

This table This table provides provides

guidance for guidance for adjustments adjustments

related to related to changes in changes in

current assets current assets and current and current liabilities.liabilities.

5-44

Here is the rest Here is the rest of Callaway’s of Callaway’s Statement of Statement of Cash Flows Cash Flows showing the showing the

cash balance cash balance on the on the

company’s company’s balance sheet.balance sheet.

5-45

Notes to Financial Statements

Descriptions of the key accounting rules Descriptions of the key accounting rules that apply to the company’s statements.that apply to the company’s statements.

Additional detail supporting reported Additional detail supporting reported numbers.numbers.

Relevant financial information not Relevant financial information not disclosed on the statements.disclosed on the statements.

5-46

Learning Objectives

Analyze a company’s performance based on return on equity and its components.

5-47

Return on Equity (ROE)

1(beginning equity + ending equity) ÷ 2

Return Return onon

EquityEquity==

Net IncomeNet IncomeAverage Stockholders’ EquityAverage Stockholders’ Equity11

ROE measures how much the firm earned for each dollar of stockholders’ investment.

5-48

ROE Profit Driver Analysis

ROE Net ProfitMargin

AssetTurnover

FinancialLeverage= ××

Net IncomeAverage

Stockholders’Equity

Net IncomeNet Sales

Net SalesAverage

Total Assets

AverageTotal Assets

AverageStockholders’

Equity

× ×=

5-49

Profit Drivers and Business Strategy

High-value or product-differentiation.High-value or product-differentiation.Rely on R&D and product promotion to convinceRely on R&D and product promotion to convince

customers of the superiority of your product.customers of the superiority of your product.

Low-Cost.Low-Cost.Rely on efficient management of accounts receivable,Rely on efficient management of accounts receivable,

inventory and productive assets to produceinventory and productive assets to producehigh asset turnover.high asset turnover.

5-50

Other Items Reported on the Income Statement

Chapter Supplement A

5-51

Net sales− Cost of goods sold

Gross profit− Operating expenses

Income from operations± Nonoperating revenues/expenses and gains/losses

Income before income taxes− Income tax expense

Net income

General Format for the Classified Income StatementGeneral Format for the Classified Income Statement

Classified Income Statement

In addition, companies may have nonrecurring items. In addition, companies may have nonrecurring items. These nonrecurring items may include:These nonrecurring items may include:

1. 1. Discontinued operations,Discontinued operations,2. 2. Extraordinary items,Extraordinary items,3. 3. Cumulative effect of changes in accounting methods.Cumulative effect of changes in accounting methods.

These items are reported separately because they are These items are reported separately because they are not useful in predicting future income of the company.not useful in predicting future income of the company.

5-52

Discontinued Operations

Income or loss on Income or loss on segment’s operation for segment’s operation for

the period.the period.

Gain or loss on Gain or loss on disposal of the disposal of the

segment.segment.

Sale or abandonment of a Sale or abandonment of a segmentsegment of a of a business.business.

Show net of applicable taxes.Show net of applicable taxes.

5-53

Extraordinary Items

UnusualUnusual InfrequentInfrequent

Show net of applicable taxes.Show net of applicable taxes.

5-54

Cumulative Effect of Changes in Accounting Methods

The change must be to a The change must be to a preferable preferable methodmethod and must be disclosed in notes and must be disclosed in notes

to financial statements.to financial statements.

GAAP GAAP MethodMethod

Change to

AlternativeGAAP GAAP

MethodMethod

Show net of applicable taxes.Show net of applicable taxes.

5-55

End of Chapter 5