Embed Size (px)

Citation preview

143

Chapter-VI

REVENUES OF THE SAMPLE GRAMA PANCHAYATS

6.1 Introduction:

This chapter is focused on the analysis of the different sources of revenue of

the GPs in the selected talukas of Koppal district. Based on the time series data

covering a period of 6 years i.e., from 2002-03 to 2007-08, the trends in the revenue

of the GPs is examined. Further, an analysis of the individual components of revenue

is made so as to understand the structure of revenue mobilisation. A complete

examination of the revenue sources of the GPs will provide an insight into its fiscal

strength. Analysis of the fiscal trends is necessary to evaluate the performance of the

GPs. An examination of the trends in the various sources of revenue will reveal the

strengths and weakness and will help to identify appropriate solutions.

Despite the availability of human resources such as elected representatives and

bureaucrats, many panchayats may not succeed for the simple reason that they may

not have adequate material resources. The major problem of panchayat finance is the

inadequate resources of GPs for an effective discharging of their functions. The

balance between obligations and resources is essential to ensure efficient working of

GPs. Inadequate resources are the main impediments in the way of the GPs to render

services efficiently and effectively. Lack of funds makes them unpopular. If the GPs

are to render services at reasonable standards, they should have enough resources.

Hence, like any other institution, panchayats also need sufficient financial resources.

Mobilisation of financial resources and ensuring that they are available continuously

without any break are very important components. Hence, the financial resource

mobilisation has received the foremost attention in the discussion that follows.

6.2 Revenue Powers of Panchayati Raj Institutions in Karnataka:

The Karnataka Panchayat Raj Act, 1993 specifies own revenue sources of the

three levels of Panchayats in the state. According to the Act, only GPs have the

144

powers to raise revenue from taxes and neither the TPs nor ZPs have independent tax

powers. The ZPs and TPs have to depend upon the transfers made from the central

and state governments. The own revenues of ZPs and TPs are minor; they consist of

fees charged by them, gifts and contributions received by them, rents charged on the

shops, establishments and buildings rented by them and sale proceeds of movable and

immovable properties owned by them. The ZPs too do not have significant own

sources of revenue. In the main, these consist of fees and penalties levied by ZPs, rent

from land and other properties let out by ZPs, interests and profits of ZPs, gifts and

contributions made to ZPs and revenue from sale proceeds of land and other

properties of ZPs.

Under clause 199 of the Karnataka Panchayat Raj Act, 1993, the GPs can levy

tax on land and buildings within the limits of their respective geographical area that

are not subject to agricultural assessment. This levy is subject to the exemptions and

maximum rate specified by the state government. In addition, GPs may also levy

water rate for the supply of water for drinking and other purposes. The Act also

specifies some other taxes to be levied subject to the exemptions and maximum rates

prescribed by the state government. These are: (i) tax on entertainment other than

cinematograph shows; (ii) taxes on vehicles other than motor vehicles; (iii) taxes on

advertisements and hoarding; (iv) pilgrim fees on persons attending jatras, festivals

etc., when GPs make arrangement for water supply, health and sanitation; (v) market

fee; (vi) fees on the registration of cattle brought for sale in the market (vii) fees on

buses and taxies and auto-stands provided the GP, and (viii) fee on grazing cattle in

the grazing lands.

The Act also provides that taxes, rates or fees payable by the owners of any

factory or Industry established in any panchayat area may be compounded into an

annual lump sum payment as agreed upon by the owner and the GP. If such an

agreement is not possible, the concerned ZP, after hearing both the GP and the owner

of the factory, may determine the lump sum payable and this will be binding on the

145

GP and the owner of the factory. Collection of taxes, fees or other revenues may be

done by the GP or any agency entrusted with the task by the GP. In addition to these,

the state government may levy a cess equivalent to the rate of land revenue on all

items of land revenue, and the proceeds will be passed on to the GPs in the respective

areas. Similarly, the state government may levy additional stamp duty imposed by the

Karnataka Stamp Act, 1957 on the transfer of immovable property at a rate not

exceeding 3 per cent on the market value of property, and in the case of lease, the

value of rent for 10 years. The proceeds of the additional stamp duty will be

transferred to the TPs based on the collections in their respective jurisdictions.

Apart from these, provisions for statutory and discretionary transfers and

borrowings have been provided. Another important provision made in almost all the

state PR Acts is constitution of a Finance Commission by the states once in five years

in conformity with Article 243-I of the Indian constitution.

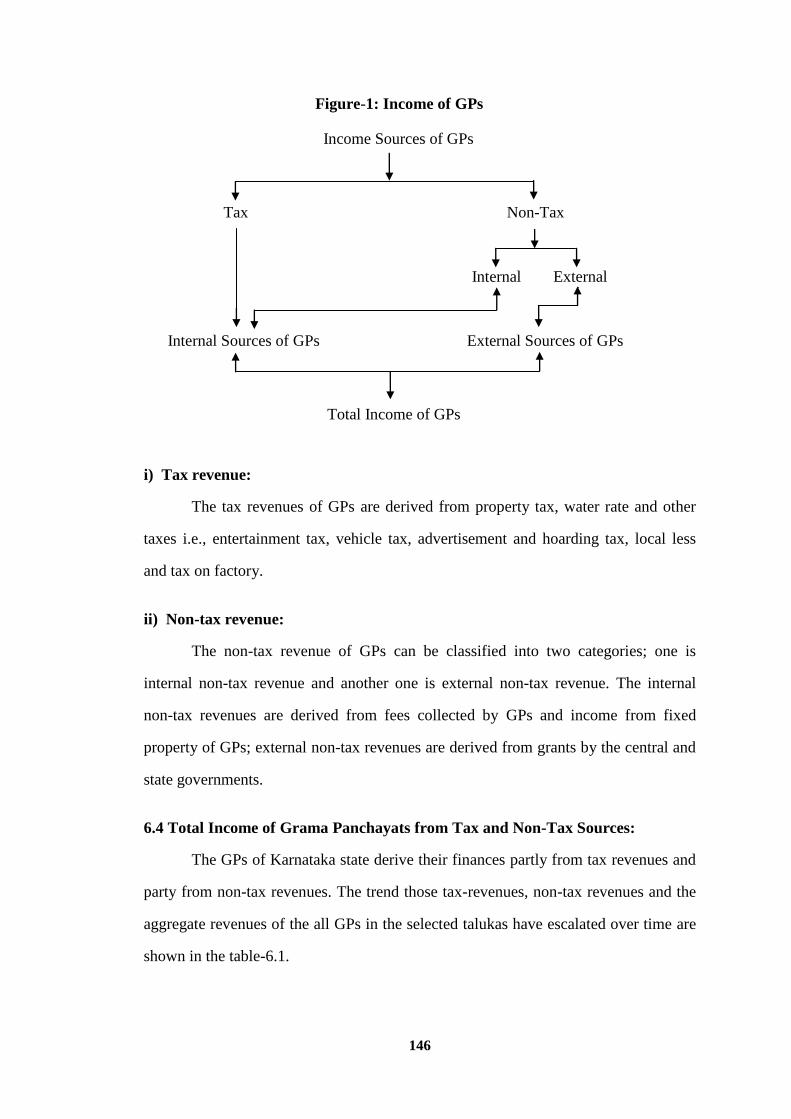

6.3 Revenues of Grama Panchayats:

The GPs although autonomous in character but largely are subordinate to state

government, which create them. Their revenues are also limited to the sources

assigned to them under the state law. Their income is derived from taxation and

services, people inhabited within the limits of panchayats. The GPs levy taxes from

the residents within the area of panchayat. Direct taxation is common in Panchayat

fiscal administration. They also receive assistance in form of grants from state and

central governments for discharging their functions. The income or revenue2 of

Grama Panchayats can be classified in the following broad heads as depicted in the

figure-1.

2 For the sake of convenience, the words ‘income’ and ‘revenue’ are herein after referred

interchangeably.

146

Figure-1: Income of GPs

Income Sources of GPs

Tax Non-Tax

Internal External

Internal Sources of GPs External Sources of GPs

Total Income of GPs

i) Tax revenue:

The tax revenues of GPs are derived from property tax, water rate and other

taxes i.e., entertainment tax, vehicle tax, advertisement and hoarding tax, local less

and tax on factory.

ii) Non-tax revenue:

The non-tax revenue of GPs can be classified into two categories; one is

internal non-tax revenue and another one is external non-tax revenue. The internal

non-tax revenues are derived from fees collected by GPs and income from fixed

property of GPs; external non-tax revenues are derived from grants by the central and

state governments.

6.4 Total Income of Grama Panchayats from Tax and Non-Tax Sources:

The GPs of Karnataka state derive their finances partly from tax revenues and

party from non-tax revenues. The trend those tax-revenues, non-tax revenues and the

aggregate revenues of the all GPs in the selected talukas have escalated over time are

shown in the table-6.1.

147

Table-6.1: Total Income of the GPs from Tax & Non-Taxes

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Tax Non- Tax Total Percentage

Variation Tax Non-Tax Total

Percentage

Variation

2002-03 46.88 275.85 322.73 - 20.75 188.98 209.73 -

2003-04 71.35 189.32 260.67 -19.23 14.24 194.72 208.96 -0.37

2004-05 81.97 480.41 562.38 115.74 46.04 292.11 338.15 61.83

2005-06 86.47 549.24 635.71 13.04 50.34 573.32 623.66 84.43

2006-07 112.58 736.69 849.27 33.59 41.64 997.23 1038.87 66.58

2007-08 69.25 586.21 655.46 -22.82 59.52 1176.32 1235.84 18.96

Average 78.08 469.62 547.70 24.06 38.76 570.45 609.20 46.29

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 588.60 1026.88

B) Net increase in percentage 225.80 491.42

C) Net increase in annual average percentage 37.63 81.90

D) Highest growth rate 115.74 84.43

E) Lowest growth rate -22.82 -0.37

The time series data relating to total income of the all GPs in the both talukas

for the six years period i.e., from 2002-03 to 2007-08 are presented in the table-6.1. It

indicates that the gross income of all 38 GPs in Gangavathi taluk increased from Rs.

322.73 lakhs to Rs. 849.27 lakhs except 2003-04 and 2007-08 in which years decline

trend is observed; it has thus risen by 225.80% during the study period. On the other

hand, the gross income of all 33 GPs in Yelburga taluk has increased from Rs. 209.73

lakhs to Rs. 1235.84 lakhs except 2003-04 in which year a small amount decline is

perceived; it has thus risen by 491.42%. Whopping of the non-tax income is the main

reason for increase in the aggregate income of the GPs.

148

The average amount of Rs. 609.20 lakhs of total receipts of the all GPs in

Yelburga taluk for the six years is greater than the average total receipts of Rs. 547.70

lakhs of the all GPs in Gangavathi taluk. Hence, average total receipts of (Rs. 609.20

lakhs ÷ 33 GPs) Rs. 18.46 lakhs of each GP in Yelburga taluk for the six years are

greater than that of (Rs. 547.70 lakhs ÷ 38 GPs) Rs. 14.41 lakhs of each GP in

Gangavathi taluk. The average annual growth rate of 46.29% of the GPs in Yelburga

taluk is better than that of 24.06% of the GPs in Gangavathi taluk. The erratic

variations are found in the growth rates of gross income. In terms of percentage, very

wide fluctuations can be easily observed pertaining to the growth rates of gross

income ranging from - 22.82% to 115.74% and from -0.37% to 84.43% in the GPs of

Gangavathi and Yelburga talukas respectively. As for the average amount and the

average annual growth rates of the total income, the GPs of Yelburga taluk displayed

the better performance than the GPs of Gangavathi taluk.

Graph-6.1

Total Income of the GPs from Tax & Non-Taxes (Rs. in Lakhs)

The graph-6.1 reveals that the minimum gross income of Rs. 260.67 lakhs in

2003-04 of the GPs in Gangavathi taluk is higher than the Rs. 188.98 lakhs in

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

1300

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Rs.

in

Lak

hs

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount Amount

Average Line Average Line

149

2002-03 of the GPs in Yelburga taluk. The maximum gross income of Rs. 1235.84

lakhs in 2007-08 of the GPs in Yelburga taluk is higher than the Rs. 849.27 lakhs in

2006-07 of the GPs in Gangavathi taluk. The total receipts of the GPs in Gangavathi

taluk has crossed the average line for four years i.e., from 2004-05 to 2007-08; while

it has crossed the average line for three years i.e., from 2005-06 to 2007-08 in respect

of the GPs in Yelburga taluk.

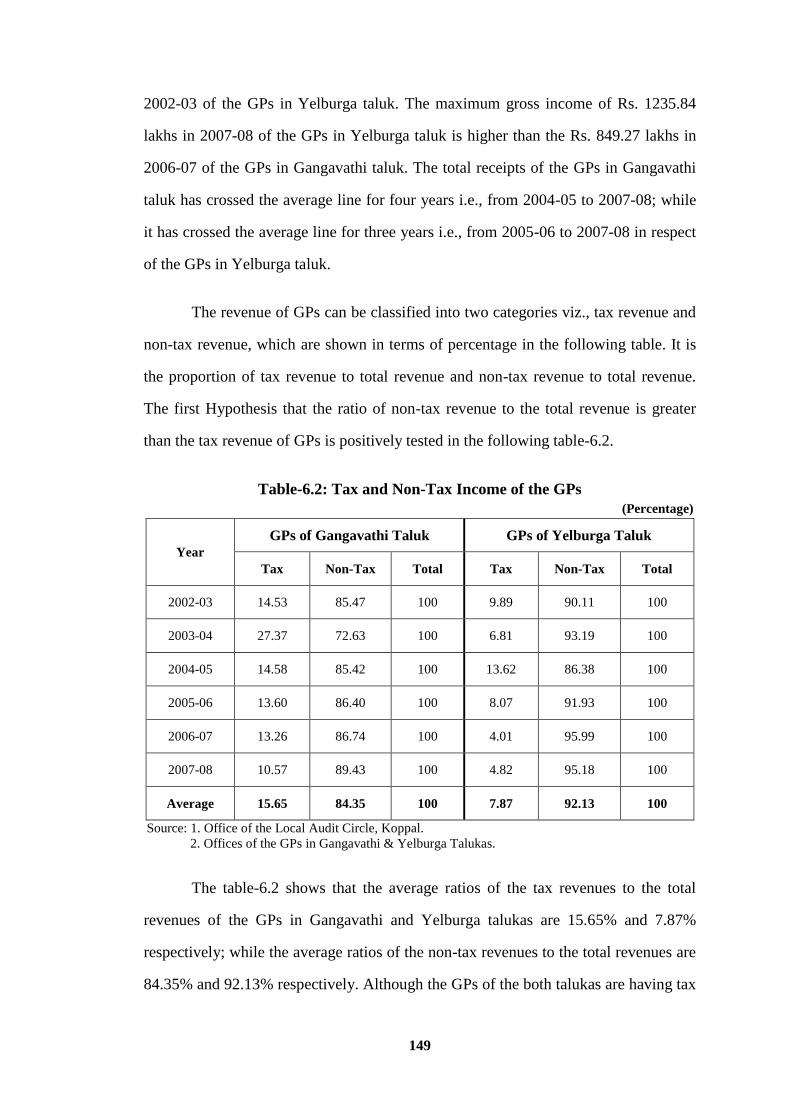

The revenue of GPs can be classified into two categories viz., tax revenue and

non-tax revenue, which are shown in terms of percentage in the following table. It is

the proportion of tax revenue to total revenue and non-tax revenue to total revenue.

The first Hypothesis that the ratio of non-tax revenue to the total revenue is greater

than the tax revenue of GPs is positively tested in the following table-6.2.

Table-6.2: Tax and Non-Tax Income of the GPs

(Percentage)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Tax Non-Tax Total Tax Non-Tax Total

2002-03 14.53 85.47 100 9.89 90.11 100

2003-04 27.37 72.63 100 6.81 93.19 100

2004-05 14.58 85.42 100 13.62 86.38 100

2005-06 13.60 86.40 100 8.07 91.93 100

2006-07 13.26 86.74 100 4.01 95.99 100

2007-08 10.57 89.43 100 4.82 95.18 100

Average 15.65 84.35 100 7.87 92.13 100

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

The table-6.2 shows that the average ratios of the tax revenues to the total

revenues of the GPs in Gangavathi and Yelburga talukas are 15.65% and 7.87%

respectively; while the average ratios of the non-tax revenues to the total revenues are

84.35% and 92.13% respectively. Although the GPs of the both talukas are having tax

150

revenue much lesser than that of non-tax revenue, the tax revenue of the GPs in

Yelburga taluk is much lower than that of the GPs in Gangavathi taluk. The ratios of

tax revenue are not only low but also showed the declining trend for the several years

and vice versa in case of non-tax ratios. The share of tax revenue in the total revenue

of the GPs in the both talukas approximately stands at 16% and even less. The GPs

finance is mainly derived from non-tax revenue sources; the tax revenue sources did

not make any significant contribution during the study period. This is evident from the

graphs-6.2 and 6.3.

Graph-6.2

Tax Revenue of the GPs % to Total Income

The above graph-6.2 reveals the ratios of tax revenue to total revenue. The

ratio for only one year i.e., 2003-04 crossed the average line (15.65%) in the GPs of

Gangavathi taluk; while the ratios for three years i.e., 2002-03, 2004-05, and 2005-06

crossed the average line (7.87%) in the GPs of Yelburga taluk. The highest and lowest

ratios in the GPs of Gangavathi taluk are shown in 2003-04 and 2007-08 respectively.

In case of the GPs in Yelburga taluk the highest and lowest ratios are shown in

2004-05 and 2006-07 respectively. From the above graph, it is evident that the

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Per

cen

tage

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

Year

151

contribution of tax revenue to total revenue of the GPs in Gangavathi taluk is better

than the GPs in Yelburga taluk.

Graph-6.3

Non-Tax Revenue of the GPs % to Total Income

The graph-6.3 reveals the ratios of non-tax revenue to total revenue. The ratios

for five years except 2003-04 crossed the average line (84.35%) in the GPs of

Gangavathi taluk; while the ratios for three years i.e., 2003-04, 2006-07, and 2007-08

crossed the average line (92.13%) in the GPs of Yelburga taluk. The highest and

lowest ratios in the GPs of Gangavathi taluk are recorded in 2007-08 and 2003-04

respectively. In case of the GPs in Yelburga taluk the highest and lowest ratios are

recorded in 2006-07 and 2004-05. As revealed in the graph, though the contribution

of non-tax revenue to total revenue of the GPs in Yelburga taluk is higher than the

GPs in Gangavathi taluk, the ratios are significantly higher in the both cases. The

share of non-tax revenue in total revenue of the GPs in the both talukas roughly stands

at 84% and even more.

0

10

20

30

40

50

60

70

80

90

100

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Year

Per

cen

tag

e

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

152

6.5 Income of Grama Panchayats from Taxes:

1) According to section 199 of the Karnataka Panchayat Raj (KPR) Act, 1993, the

GPs can levy following taxes;

a) Property Tax on buildings and lands which are not subject to agricultural

assessment, within the limits of the panchayat area.

b) Tax on water (drinking water).

c) Tax on entertainment other than cinematography shows.

d) Tax on vehicles other than motor vehicles.

e) Tax on advertisement and hoarding.

2) Section 202 provides for levy of tax on factory / industry by the GP.

The revenue mobilisation from taxes by the all GPs in the both talukas is

presented in the following table-6.3.

Table-6.3: Income of the GPs from Taxes

(Rs. in Lakhs)

Yea

r

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Pro

per

ty

Ta

x

Wa

ter

Ra

te

Oth

er

Ta

xes

To

tal

Ta

x

Rev

enu

e

Per

cen

tag

e

Va

ria

tio

n

Pro

per

ty

Ta

x

Wa

ter

Ra

te

Oth

er

Ta

xes

To

tal

Ta

x

Rev

enu

e

Per

cen

tag

e

Va

ria

tio

n

2002-03 33.13 6.30 7.45 46.88 - 10.39 7.94 2.42 20.75 -

2003-04 62.19 7.66 1.50 71.35 52.20 6.69 7.55 NA 14.24 -31.37

2004-05 68.75 13.22 NA 81.97 14.88 20.33 9.76 15.95 46.04 223.31

2005-06 76.86 8.95 0.66 86.47 5.49 41.15 3.03 6.18 50.34 9.34

2006-07 95.42 17.16 NA 112.58 30.20 28.61 13.03 NA 41.64 -17.28

2007-08 58.95 10.30 NA 69.25 -38.49 38.82 18.37 2.33 59.52 42.94

Average 65.88 10.60 1.60 78.08 12.86 24.33 9.95 4.48 38.76 37.82

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

Note: NA – Data Not Available.

153

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 65.70 45.28

B) Net increase in percentage 140.15 317.98

C) Net increase in annual average percentage 23.36 52.99

D) Highest growth rate 52.20 223.31

E) Lowest growth rate -38.49 -31.37

The table-6.3 indicates that the gross tax income of the all 38 GPs in

Gangavathi taluk increased from Rs. 46.88 lakhs to 112.58 lakhs between 2002-03

and 2006-07, declined sharply to 69.25 lakhs in 2007-08; it has thus risen by 140.15%

during the study period. On the other side, the gross tax income of the all 33 GPs in

Yelburga taluk has increased from Rs. 20.75 lakhs to 50.34 lakhs between 2002-03

and 2005-06, deteriorated to Rs. 41.64 lakhs in 2006-07, again increased to Rs. 59.52

lakhs in 2007-08; it has thus risen by 317.98%.

The average amount of Rs. 78.08 lakhs of total tax income of the all GPs in

Gangavathi taluk is much greater than that of the average of Rs. 38.76 lakhs of the all

GPs in Yelburga taluk. Hence, average total tax receipt of (Rs. 78.08 lakhs ÷ 38 GPs)

Rs. 2.05 lakhs of each GP in Gangavathi taluk is greater than that of the average of

(Rs. 38.76 lakhs ÷ 33 GPs) Rs. 1.17 lakhs of each GP in Yelburga taluk. As for

generation of total tax income, the GPs in Gangavathi taluk showed the better

performance than the GPs in Yelburga taluk.

The graph-6.4 exhibits that the minimum gross tax income of Rs. 46.88 lakhs

in 2002-03 of the GPs in Gangavathi taluk is higher than that of the Rs. 14.24 lakhs in

2003-04 of the GPs in Yelburga taluk. The maximum gross tax income of Rs. 112.58

lakhs in 2006-07 of the GPs in Gangavathi taluk is higher than that of the Rs. 59.52

lakhs in 2007-08 of the GPs in Yelburga taluk. The gross tax income of the GPs in the

former taluk has crossed the average line (Rs. 78.08 lakhs) for three years i.e., from

154

2004-05 to 2006-07; while it has crossed the average line (Rs. 38.76 lakhs) for four

years i.e., from 2004-05 to 2007-08 in respect of the GPs in the latter taluk.

Graph-6.4: Income of the GPs from Taxes (Rs. in Lakhs)

6.6 Income of Grama Panchayats from Non-Taxes:

The non-tax revenue of GPs can be classified in two categories, viz., internal

non-tax revenue and external non-tax revenue. The total of internal and external non-

tax revenues are equal to the total non-tax revenue which is symbolically represented

as follows;

Total Internal Total External Total

Non -Tax Revenue Non-Tax Revenue Non-Tax Revenue

The internal non-tax revenues are derived from own accounts and the external

non-tax revenues are derived from other than own accounts of GPs.

6.6 (i) The Internal Non-Tax Revenues of Grama Panchayats:

They are generated by the GPs through different means viz., pilgrim fees, Jatra

fees, market fees, license fees, mutation fees, notice fees, warrant fees, fees on buses,

0

10

20

30

40

50

60

70

80

90

100

110

120

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Rs.

in

La

kh

s

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount Amount

Average Line Average Line

+ =

155

taxis and auto stands, fees on grazing lands, rent or income from own buildings and

assets, interest earned on deposits, sale proceeds of movable and immovable assets,

auction of trees, fruits, etc. The KPR Act permits the PRIs including GPs to receive

contributions, gifts and aid from different sources. These are mainly from local

people, philanthropists, charitable institutions, voluntary and non-governmental

organisations. In some of the GPs closer to the major cities and towns, rents from

shops and establishments constructed and let out by the panchayats also generate

significant revenues.

6.6 (ii) The External Non-Tax Revenues of Grama Panchayats:

They are mainly in form of grants from higher level governments. The grants

occurring to PRIs including the GPs are mainly from three sources, namely, (i) the

state government, (ii) the central government and (iii) on the recommendations of the

central finance commission. The state grants consist of plan and non-plan grants,

whereas the central grants constitute only plan grants that are conditional and

matching in nature. The grants recommended by CFCs (Tenth and Eleventh) are non-

plan and are thus again conditional and matching.

The KPR Act under section 214, 220 and 229 empowers the GPs, TPs and ZPs

respectively to raise loans for the execution of the any developmental work or for the

purpose of carring out any of the provisions of the Act. However, there was no

evidence of any panchayat making use of this statutory power. The main reason for

this was stiff conditions laid down for raising loans. The KPR Act stipulates that: (i)

the panchayat that intend to raise loans (development purpose only) must seek prior

permission / guarantee from the state government, and (ii) provide for ‘Sinking Fund’.

In the first place, the chances of state governments giving guarantee to local

government borrowings are highly doubtful and as far as the second condition is

concerned, it requires sufficient own revenues so that they could apportion a portion

of that to the sinking fund account. However, it is highly improbable from the present

local governments’ fiscal powers to fulfill the second condition.

156

The trends relating to internal non-tax revenue, external non-tax revenue and

total non-tax revenue are presented in the following table-6.4.

Table-6.4: Income of the GPs from Non-Taxes

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk In

tern

al

No

n-T

ax

Ex

tern

al

No

n-T

ax

To

tal

No

n-T

ax

Per

cen

tag

e

Va

ria

tio

n

Inte

rna

l

No

n-T

ax

Ex

tern

al

No

n-T

ax

To

tal

No

n-T

ax

Per

cen

tag

e

Va

ria

tio

n

2002-03 8.15 267.70 275.85 - 4.58 184.40 188.98 -

2003-04 6.44 182.88 189.32 -31.37 11.71 183.01 194.72 3.04

2004-05 14.61 465.80 480.41 153.76 15.47 276.64 292.11 50.02

2005-06 12.50 536.74 549.24 14.33 9.98 563.34 573.32 96.27

2006-07 9.47 727.22 736.69 34.13 5.13 992.10 997.23 73.94

2007-08 15.07 571.14 586.21 -20.43 19.15 1157.17 1176.32 17.96

Average 11.04 458.58 469.62 30.08 11.00 559.44 570.45 48.25

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 547.37 987.34

B) Net increase in percentage 289.12 522.46

C) Net increase in annual average percentage 48.19 87.08

D) Highest growth rate 153.76 96.27

E) Lowest growth rate -31.37 3.04

The time series data relating to the non-tax revenue of the all GPs in the both

talukas is presented in the table-6.4. It shows that the gross non-tax revenue of the

GPs in Gangavathi taluk increased from Rs. 275.85 lakhs to 736.69 lakhs during the

study period except 2003-04 and 2007-08 in which years decline trend is noticed; it

has thus risen by 289.12%. On the other side, the gross non-tax revenue of the GPs in

157

Yelburga taluk increased from 188.98 lakhs to 1176.32 lakhs between 2002-03 and

2007-08; it has thus risen by 522.46%.

The average amount of Rs. 570.45 lakhs of gross non-tax revenue of the all

GPs in Yelburga taluk for the six years is higher than the average of Rs. 469.62 lakhs

of the all GPs in Gangavathi taluk. Consequently, the average gross non-tax revenue

of (Rs. 570.45 lakhs ÷ 33 GPs) Rs. 17.29 lakhs of each GP in Yelburga taluk for the

six years is greater than the average of (Rs. 469.62 lakhs ÷ 38 GPs) Rs. 12.36 lakhs of

each GP in Gangavathi taluk. The average annual growth rate of 48.25% of the GPs in

Yelburga taluk is higher than that of 30.08% of the GPs in Gangavathi taluk. With

respect to generation of the gross non-tax income, the GPs of Yelburga taluk showed

the better performance than the GPs of Gangavathi taluk.

Graph-6.5

Income of the GPs from Non-Taxes (Rs. in Lakhs)

The above graph-6.5 shows that the minimum gross non-tax income of Rs.

189.32 lakhs in 2003-04 of the GPs in Gangavathi taluk is higher than that of the Rs.

188.98 lakhs in 2002-03 of the GPs in Yelburga taluk. The maximum gross non-tax

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Rs.

in

Lak

hs

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount Amount

Average Line Average Line

158

income of Rs. 1176.32 lakhs in 2007-08 of the GPs in Yelburga taluk is much higher

than that of the Rs. 736.69 lakhs in 2006-07 of the GPs in Gangavathi taluk. The gross

non-tax income of the GPs in Gangavathi taluk has crossed the average line (Rs.

469.62 lakhs) for the last four years; while it has crossed the average line (Rs. 570.45

lakhs) for the last three years in case of the GPs in Yelburga taluk.

The second hypothesis that the proportion of external non-tax revenue is

greater than the internal non-tax revenue in the non-tax structure of GPs is proved in

the following table-6.5.

Table-6.5: Income of the GPs from Non-Taxes

(Percentage)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Internal

Non- Tax

External

Non-Tax

Total

Non-Tax

Internal

Non- Tax

External

Non-Tax

Total

Non-Tax

2002-03 2.95 97.05 100 2.42 97.58 100

2003-04 3.40 96.60 100 6.01 93.99 100

2004-05 3.04 96.96 100 5.30 94.70 100

2005-06 2.28 97.72 100 1.74 98.26 100

2006-07 1.29 98.71 100 0.51 99.49 100

2007-08 2.57 97.43 100 1.63 98.37 100

Average 2.59 97.41 100 2.94 97.06 100

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

The table-6.5 discloses that the average percentage of internal non-tax revenue

of the GPs in Gangavathi and Yelburga talukas for the six years are 2.59% and 2.94%

respectively; while the average percentage of external non-tax revenue are 97.41%

and 97.06% respectively. The ratios of internal non-tax revenue are not only low but

also showed the declining trend for the several years and vice versa in respect of

external non-tax ratios. Although the GPs’ finance is mainly derived from non-tax

sources, external non-tax revenue is so much greater than the internal non-tax

159

revenue. The external non-tax revenue has a lion share and internal non-tax revenue

has a lean share in the GPs’ finance.

Graph-6.6

Internal Non-Tax Revenue of the GPs % to Total Income

The above graph-6.6 exhibits the ratios of internal non-tax revenue to total

revenue. The ratios for the first three years crossed the average line (2.59%) in the

GPs of Gangavathi taluk; while the ratios for two years i.e., 2003-04 and 2004-05

crossed the average line (2.94%) in the GPs of Yelburga taluk. The highest and lowest

ratios in the GPs of the both talukas are shown in 2003-04 and 2006-07 respectively.

From the graph it is obvious that the internal non-tax revenue sources did not make

any signification contribution to GPs’ finance in the both talukas.

The graph-6.7 exhibits that the ratios of external non-tax revenue for the last

three years continuously crossed the average line (97.41%) in the GPs of Gangavathi

taluk; while the ratios for four years i.e., 2002-03, 2005-06, 2006-07, and 2007-08

crossed the average line (97.06%) in the GPs of Yelburga taluk. The highest and

lowest ratios in the GPs of the both talukas are recorded in 2006-07 and 2003-04

0

1

2

3

4

5

6

7

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

Per

cen

tag

e

Year

160

respectively. From the graph, it is evident that the external non-tax sources made very

significant contribution to the GPs’ finance in the both talukas.

Graph-6.7

External Non-Tax Revenue of the GPs % to Total Income

6.6. ii (a) Income of Grama Panchayats from Internal Non-Tax Sources:

The internal non-tax revenue is the income which is generated by own account

of GPs other than tax revenue. It is derived from fees and revenue from GPs’ fixed

property. The income of the all GPs in the both talukas from the internal non-tax

sources is shown in the table-6.6.

The time series data as shown in the table-6.6 indicates that the gross internal

non-tax revenue of all 38 GPs in Gangavathi taluk decreased from Rs. 8.15 lakhs in

2002-03 to Rs. 6.44 lakhs in 2003-04, rose to Rs. 14.61 lakhs in 2004-05, again fell to

Rs. 12.50 lakhs and 9.47 lakhs in 2005-06 and 2006-07 respectively, again showed

the increasing tendency to Rs. 15.07 lakhs in 2007-08; it has thus risen by 134.01%.

On the contrary, the gross internal non-tax revenue of all 33 GPs in Yelburga taluk

has increased from Rs. 4.58 lakhs to Rs. 15.47 lakhs between 2002-03 and 2004-05,

10

20

30

40

50

60

70

80

90

100

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

Year

Per

cen

tag

e

161

decreased to Rs. 9.98 lakhs and 5.13 lakhs in 2005-06 and 2006-07 respectively, again

rose to Rs. 19.15 lakhs in 2007-08; it has thus risen by 318.12%. Fluctuations in the

revenue from internal non-tax revenue are greater in the GPs of Yelburga taluk than

the GPs of Gangavathi taluk.

Table-6.6: Income of the GPs from Internal Non-Taxes

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Fee

s

Co

llec

ted

by

GP

s

Rev

enu

e fr

om

GP

s’ F

ixed

Pro

per

ty

To

tal

Inte

rna

l

No

n -

Ta

x

Per

cen

tag

e

Va

ria

tio

n

Fee

s

Co

llec

ted

by

GP

s

Rev

enu

e fr

om

GP

s’ F

ixed

Pro

per

ty

To

tal

Inte

rna

l

No

n -

Ta

x

Per

cen

tag

e

Va

ria

tio

n

2002-03 3.33 4.82 8.15 - 3.13 1.45 4.58 -

2003-04 4.29 2.15 6.44 -20.98 10.82 0.89 11.71 155.68

2004-05 11.50 3.11 14.61 126.86 13.63 1.84 15.47 32.11

2005-06 8.01 4.49 12.50 -14.44 8.23 1.75 9.98 -35.49

2006-07 6.12 3.35 9.47 -24.24 3.62 1.51 5.13 -48.60

2007-08 12.14 2.93 15.07 59.13 15.26 3.89 19.15 273.29

Average 7.57 3.47 11.04 25.27 9.11 1.89 11.00 75.40

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 8.63 14.57

B) Net increase in percentage 134.01 318.12

C) Net increase in annual average percentage 22.34 53.02

D) Highest growth rate 126.86 273.29

E) Lowest growth rate -24.24 -48.60

The average amount of Rs. 11.04 lakhs of receipts from gross internal non-tax

sources of the all GPs in Gangavathi taluk for the six years is slightly higher than that

162

of Rs. 11.00 lakhs of the all GPs in Yelburga taluk. However, the average of

(Rs. 11.00 lakhs ÷ 33 GPs) Rs. 0.33 lakhs of each GP in Yelburga taluk for the six

years is greater than that of the average of (Rs. 11.04 lakhs ÷ 38 GPs) Rs. 0.29 lakhs

of each GP in Gangavathi taluk. The average annual growth rate of 75.40% of the

GPs in Yelburga taluk is better than that of 25.27% of the GPs in Gangavathi taluk.

As far the average revenue from internal non-taxes is concerned the GPs in the both

talukas exhibits more or less same position.

6.6. ii (b) Income of Grama Panchayats from External Non-Tax Sources:

The external non-tax revenue is obtained by other than own accounts (other

than tax revenue) of GPs. They are in forms of different grants as shown in the

following table-6.7.

Table-6.7: Income of the GPs from External Non-Taxes

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Gra

nts

fro

m

the

Sta

te G

ov

t.

Gra

nts

fro

m

the

CF

Cs

Gra

nts

fro

m

Cen

tra

lly

& /

or

Sta

te S

po

nso

red

Sch

emes

To

tal

Ex

tern

al

No

n-T

ax

Per

cen

tag

e

Va

ria

tio

n

Gra

nts

fro

m

the

Sta

te G

ov

t.

Gra

nts

fro

m

the

CF

Cs

Gra

nts

fro

m

Cen

tra

lly

& /

or

Sta

te S

po

nso

red

Sch

emes

To

tal

Ex

tern

al

No

n-T

ax

Per

cen

tag

e

Va

ria

tio

n

2002-03 82.49 74.33 110.88 267.70 - 60.10 50.50 73.80 184.40 -

2003-04 70.65 1.74 110.49 182.88 -31.68 76.67 6.31 100.03 183.01 -0.75

2004-05 49.74 40.53 375.53 465.80 154.70 40.60 40.33 195.71 276.64 51.16

2005-06 191.21 25.80 319.73 536.74 15.23 179.47 22.84 361.03 563.34 103.64

2006-07 192.50 73.10 461.62 727.22 35.49 167.76 121.56 702.78 992.10 76.17

2007-08 50.75 40.25 480.14 571.14 -21.46 218.72 68.09 870.36 1157.17 16.64

Average 106.22 42.63 309.73 458.58 30.46 123.89 51.60 383.95 559.44 49.36

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

163

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 544.34 974.16

B) Net increase in percentage 297.65 532.30

C) Net increase in annual average percentage 49.61 88.72

D) Highest growth rate 154.70 103.64

E) Lowest growth rate -31.68 -0.75

The time series data as shown in the above table reveals that the gross external

non-tax revenue of the all 38 GPs in Gangavathi taluk rose from Rs. 267.70 lakhs to

Rs. 727.22 lakhs except 2003-04 and 2007-08 in which years decrease is observed; it

has thus risen by 297.65%. Whereas the gross external non-tax revenue of the all 33

GPs in Yelburga taluk rose from Rs. 184.40 lakhs to Rs. 1157.17 lakhs except 2003-

04 in which year small amount of decline is noticed; it has thus raised by 532.30%

which is much higher than the GPs in the other taluk.

The average amount of Rs. 559.44 lakhs of total external non-tax revenue of

the all GPs in Yelburga taluk for the six years is higher than the average of Rs. 458.58

lakhs of the all GPs in Gangavathi taluk. Accordingly, the average of (Rs.559.44

lakhs ÷ 33 GPs) Rs. 16.95 lakhs of each GP in Yelburga taluk is greater than that of

the average of (Rs.458.58 lakhs ÷ 38 GPs) Rs.12.07 lakhs of each GP in Gangavathi

taluk. The GPs in Yelburga taluk be provided with more grants than the GPs in

Gangavathi taluk. Hence, the average annual growth rate of 49.36% of the GPs in

Yelburga taluk is much better than that of 30.46% of the GPs in Gangavathi taluk.

6.7 Income of Grama Panchayats from Internal (Own) Sources:

The internal sources of GPs can be classified into two categories viz., tax and

internal non-tax. The total of tax and internal non-tax revenue is equal to total internal

revenue, which are symbolically presented as;

164

Total Internal Total

Tax Revenue Non-Tax Revenue Internal Revenue

The tax and internal non-tax revenue are derived from own accounts of the

GPs which are presented in the following table-6.8.

Table-6.8: Income of the GPs from Internal (Own) Sources

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Total

Tax

Internal

Non-Tax

Total

Internal

Income

%

Variation

Total

Tax

Internal

Non-Tax

Total

Internal

Income

%

Variation

2002-03 46.88 8.15 55.03 - 20.75 4.58 25.33 -

2003-04 71.35 6.44 77.79 41.36 14.24 11.71 25.95 2.45

2004-05 81.97 14.61 96.58 24.15 46.04 15.47 61.51 137.03

2005-06 86.47 12.50 98.97 2.47 50.34 9.98 60.32 -1.93

2006-07 112.58 9.47 122.05 23.32 41.64 5.13 46.77 -22.46

2007-08 69.25 15.07 84.32 -30.91 59.52 19.15 78.67 68.21

Average 78.08 11.04 89.12 12.08 38.76 11.00 49.76 36.66

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 67.02 53.34

B) Net increase in percentage 121.79 210.58

C) Net increase in annual average percentage 20.30 35.10

D) Highest growth rate 41.36 137.03

E) Lowest growth rate -30.91 -22.46

The time series data as shown in the above table represents the gross income

from internal sources of all 38 GPs in Gangavathi taluk increased from Rs. 55.03

lakhs to 122.05 lakhs between 2002-03 to 2006-07, but fall to Rs. 84.32 lakhs in

+ =

165

2007-08; it has thus increased by 121.79% during the study period. On the other hand,

the gross income from internal sources of all 33 GPs in Yelburga taluk increased from

Rs. 25.33 lakhs to Rs. 61.51 lakhs in the first three years, but fall to Rs. 60.32 lakhs

and Rs. 46.77 lakhs in the next two years, again rose to Rs.78.67 lakhs in the last year;

it has thus increased by 210.58%.

The average amount of Rs. 89.12 lakhs of receipts from internal sources of the

all GPs in Gangavathi taluk for the six years is higher than the average of Rs. 49.76

lakhs of the all GPs in Yelburga taluk. Consequently, the average of (Rs.89.12 lakhs ÷

38 GPs) Rs. 2.35 lakhs of each GP in the former taluk is greater than that of average

of (Rs. 49.76 lakhs ÷ 33 GPs) Rs. 1.51 lakhs of each GP in the latter taluk. In terms of

amount, the GPs of Gangavathi taluk showed better performance than the GPs of

Yelburga taluk in generating the income from internal (own) sources. Nevertheless,

the annual average growth rate of 36.66% of the GPs in Yelburga taluk is much better

than that of 12.08% of the GPs in Gangavathi taluk.

6.8 Income of Grama Panchayats from External Sources:

Table-6.9: Income of the GPs from External Sources

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

External Non-Tax =

Total External Income

Percentage

Variation

External Non-Tax =

Total External Income

Percentage

Variation

2002-03 267.70 - 184.40 -

2003-04 182.88 -31.68 183.01 -0.75

2004-05 465.80 154.7 276.64 51.16

2005-06 536.74 15.23 563.34 103.64

2006-07 727.22 35.49 992.10 76.17

2007-08 571.14 -21.46 1157.17 16.64

Average 458.58 30.46 559.44 49.36

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

166

GPs of

Gangavathi Taluk

GPs of

Yelburga Taluk

A) Net increase in amount 303.44 972.77

B) Net increase in percentage 113.35 527.53

C) Net increase in annual average percentage 18.89 87.92

D) Highest growth rate 154.70 103.64

E) Lowest growth rate -31.68 -0.75

As presented in the table-6.9 the revenue from external sources of the GPs

received by them are solely in form of grants i.e., external non-tax revenue. Hence,

grants received by GPs are equal to total external revenue, symbolically presented as

follows;

Total External Total

Non-Tax Revenue External Revenue

The table-6.9 is a derivative of table-6.7 on which the observations have been

made already.

6.9 Total Income of Grama Panchayats from Internal and External Sources:

The income of GPs can be classified into two categories viz., internal sources

and external sources. The total of internal and external income is equal to total

income, which is symbolically presented as;

Total Total Total

Internal Income External Income Income

The internal income is derived from own accounts and the external income is

derived from other than own accounts of GPs which are presented in the following

tables. The third hypothesis that resources of GPs are mainly derived from external

sources i.e., grants from higher level governments is verified in the tables- 6.10 and

6.11.

=

+ =

167

Table-6.10: Total Income of the GPs from Internal & External Sources

(Rs. in Lakhs)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Internal

Income

External

Income

Total

Income

Internal

Income

External

Income

Total

Income

2002-03 55.03 267.70 322.73 25.33 184.40 209.73

2003-04 77.79 182.88 260.67 25.95 183.01 208.96

2004-05 96.58 465.80 562.38 61.51 276.64 338.15

2005-06 98.97 536.74 635.71 60.32 563.34 623.66

2006-07 122.05 727.22 849.27 46.77 992.10 1038.87

2007-08 84.32 571.14 655.46 78.67 1157.17 1235.84

Average 89.12 458.58 547.70 49.76 559.44 609.20

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

Table-6.11: Total Income of the GPs from Internal & External Sources

(Percentage)

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Internal

Income

External

Income

Total

Income

Internal

Income

External

Income

Total

Income

2002-03 17.05 82.95 100 12.08 87.92 100

2003-04 29.84 70.16 100 12.42 87.58 100

2004-05 17.17 82.83 100 18.19 81.81 100

2005-06 15.57 84.43 100 9.67 90.33 100

2006-07 14.37 85.63 100 4.50 95.50 100

2007-08 12.86 87.14 100 6.37 93.63 100

Average 17.81 82.19 100 10.54 89.46 100

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

The table-6.10 reveals the amount and table-6.11 reveals the ratios of internal

revenue and external revenue to the total revenue of all GPs in the both talukas. The

average ratios of internal revenue of the all GPs in Gangavathi and Yelburga talukas

168

are 17.81% and 10.54% respectively; while the average ratios of external revenue of

all GPs in these talukas are 82.19% and 89.46% respectively. The GPs in Gangavathi

taluk are better placed than the GPs of Yelburga taluk as for the average ratio of

internal revenue is concerned or it can also be assertively said that the reliance of the

GPs in Yelburga taluk on the external revenue is enormously high than the GPs in

Gangavathi taluk.

The most identifiable trend of the whole episode is that the ratios of internal

revenue are descending downwards while those of the external revenue are ascending

upwards except 2003-04 in the GPs of Gangavathi taluk; 2003-04 and 2004-05 in the

GPs of Yelburga taluk. The overall average share of internal sources for the six years

tenure comes to not so appreciable level of 18%. In other words, the GPs of the

sample talukas are depended upon the external sources to the extent of 82% and even

more. The inference has drawn from the above figures are that the GPs reliance on the

external sources is predominantly high. The GPs resources are mainly derived from

external sources i.e., the internal sources did not make any significant contribution to

the GPs of the sample talukas during the study period. Moreover the GPs are either

unwilling to tap the internal sources fully or the internal sources are very inflexible in

yielding the expected revenues.

The graph-6.8 reveals the ratios of internal revenue to total income of the GPs

in the sample talukas. In the GPs of Gangavathi taluk the ratios crossed the average

line (17.81%) for 2003-04; while in the GPs of Yelburga taluk the ratios crossed the

average line (10.54%) for first three years. The average line of the GPs in the former

taluk is higher than that of the GPs in the latter taluk. Therefore, the contribution of

internal sources to total income of the GPs in Gangavathi taluk is better than the GPs

in Yelburga taluk.

169

Graph-6.8

Internal Revenue of the GPs % to Total Income

Graph-6.9

External Revenue of the GPs % to Total Income

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

0

10

20

30

40

50

60

70

80

90

100

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Per

cen

tag

e P

erce

nta

ge

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

170

The graph-6.9 shows the ratios of external revenue to total income of the GPs

in the selected talukas. In the GPs of Gangavathi taluk the ratios crossed the average

line (82.19%) for first one year and last four years; whereas in the GPs of Yelburga

taluk the ratios crossed the average line (89.46%) for last three years. The average line

of the GPs in Yelburga taluk is higher than that of the GPs in Gangavathi taluk.

Therefore, the contribution of external sources to total income of the GPs in Yelburga

taluk is higher than the GPs in Gangavathi taluk.

6.10 Grama Panchayat Fund:

It is a fact that every organisation requires money to manage its affairs and to

meet its requirements. All governmental organisations (central, state and local) meet

their expenditures by imposing various taxes and non-taxes. This is a universal

practice and GPs were not exceptions to this system. The resources of GPs come from

the following revenue components;

I. Sources of Tax Revenue;

1. Property Tax

2. Water Rate

3. Other Taxes

II. Sources of Non-Tax Revenue;

(a) Internal Non-Taxes;

4. Fees Collected by GPs

5. Revenue from GPs’ Fixed Property

(b) External Non-Taxes;

6. Grants from Karnataka State Government

7. Grants from Central Finance Commission

8. Grants from Centrally and / or State Sponsored Schemes

171

6.11 Tax Rates:

The rates at which the tax can be levied on various components laid down in

the IV schedule of Karnataka Panchayati Raj Act, 1993 are shown in the following

table-6.12.

Table-6.12: Taxes and Their Rates

Sl.

No. Particulars

Tax Rate

(In Rupees) Description Section

1.

Tax on lands not

subject to

agricultural

assessment

Re.1 for every

100 square

meter

Re.1 per annum for every 100

square meter.

199 of

KPR

Act,1993

2 Tax on buildings

10% of annual

letting value

(per annum)

Tax may be levied on the basis of

10% of annual letting value of huts,

temporary and permanent houses. If

building is used for own living, tax

rate should be decided on the basis

of its value.

199 of

KPR

Act,1993

3

Tax on

entertainment

other than

cinematography

shows.

Rs. 20 per

entertainment

For a circus, drama exhibition,

amusements, games or sports and

magic show which generates

income.

199 of

KPR Act

1993

4

Tax on vehicles

other than motor

vehicles.

Rs. 25 Per

annum

For every 4 wheeled vehicle with

springs constructed to be drawn by

two or more horses, bulls, or

bullocks.

199 of

KPR

Act,1993 Rs. 10 per

annum

i) For every 2 wheeled vehicle with

springs constructed to be drawn by

one or more horses, bulls, or

bullocks.

ii) For every other vehicle with

springs.

iii) For every cart or vehicle without

springs.

Rs. 5 Per

annum For every bicycle or tricycle

5

Tax on

advertisement and

hoarding.

Rs. 5 for every

square meter

Per month

For advertisement other than

premises of trade institutions, ex:

advertisements at road side, on

buildings wall.

199 of

KPR

Act,1993

6 Water rate

General water

rate Rs. 10 per

month

For providing water facility through

street taps or water supply schemes. 199 of

KPR

Act,1993 Special water

rate Rs. 25 per

month

For supplying water to houses

through taps.

Source: Prajaprabutva, Vikendrikarana Matthu Abivrudhi, ANSSIRD, Mysore, 2009.

172

6.12 The Property Tax:

Separate figures for tax on lands not subject to agricultural assessment and tax

on buildings could not be ascertained as records are showing consolidated collection

for these taxes. Hence, for the present study data of tax on lands not subject to

agricultural assessment and tax on buildings are presented in a united source of

income as a property tax.

6.12 (i) Rate of the Property Tax:

The tax shall be levied;

(a) On the building at the rate of 10 per cent of the annual letting value of such

building, per annum; and

(b) On the land, at the rate of 1 rupee per annum for every 100 square meter.

6.12 (ii) Exemption:

The following buildings and lands shall be exempted from the levy of tax

under sub-section (1) of Section 199 of KPR Act namely;

(a) Buildings and lands belonging to the Zilla Panchayats, Taluk Panchayats and

Grama Panchayats.

(b) Buildings and lands belonging to Central Government or any State Government

and used for the purposes of such Government and not used for intended to be

used for residential or commercial purposes;

(c) Buildings and lands, used solely for charitable or public religious purposes and not

let out for rent; and

(d) Lands measuring less than 100 square meter and buildings having an annual

letting value of less than rupees twenty-five.

6.12 (iii) Assessment List:

The Secretary shall, as soon as may be after the publication of the notice of

resolution under KPR (Panchayat Taxes and Fees) Rule 3 but not later than the 1st

173

day of December next following, prepare an assessment list relating to the buildings

and lands in the Panchayat area showing the-

(a) Serial number of each house or land;

(b) Name of the owner and occupier, if any;

(c) Annual letting value of the buildings; and

(d) Amount of tax assessed thereon.

6.12 (iv) Objection to the Assessment List:

When the assessment list is completed, a notice shall be published by affixing

it on the notice board of the office of the Grama Panchayat, and also by beat of drum

in the Panchayat area, stating that the list is open for inspection at the office of the

Grama Panchayat and that objections will be considered and decided by the Grama

Panchayat on a date which shall not be earlier than thirty days from the date of

publication of the aforesaid notice.

6.12 (v) Inspection of Assessment List:

Every person whose name appears in the assessment list, every person

claiming to be the owner or occupier of any building or land, and the agent of any

such person shall be at liberty to inspect the list and to make extracts there from

without any charge.

6.12 (vi) Authentication of Assessment List:

(1) All objections to the assessment shall be considered and decided by the Grama

Panchayat on the date specified in the notice published under KPR (Panchayat

Taxes and Fees) Rule 8 or on any later date and the decision of the Grama

Panchayat shall be communicated to the person objecting to the assessment.

(2) The Grama Panchayat shall cause to be made necessary amendments, if any, in the

assessment list in accordance with the orders under the KPR sub-rule (1) or the

orders of the Zilla Panchayat under the Rule 39 and thereafter the assessment list

shall be authenticated by the Adhyaksha.

174

(3) The entries in the list authenticated under the sub-rule (2) shall be conclusive

evidence of the amount of tax leviable.

6.12 (vii) Alteration of the Assessment List:

(1) Grama Panchayat may at any time alter the assessment list by inserting or deleting

an entry-

(a) In respect of any building or land, if such entry has been omitted from, or

erroneously made in, the assessment list through fraud, accident or mistake;

(b) In respect of any building constructed, altered, added to or reconstructed after

preparation of the assessment list, after giving the person interested in the

alteration of the list, a notice of not less than one month calling upon to file

objections, if any, to such alteration.

(2) An objection made under the sub-rule (1) before the time specified in such notice

shall be considered and decided by the Grama Panchayat.

(3) Any entry or alteration made under this rule shall be deemed to have been made-

(a) In the case of building constructed, altered, added to or reconstructed, on the date

on which such construction, alteration, addition or reconstruction was completed or

of the date on which the building was first occupied after such construction,

alteration, addition or reconstruction, whichever is earlier; and

(b) In other cases, on the date of which the circumstances justifying the entry or

alteration existed.

(4) The tax or the enhanced tax, as the case may be, which becomes leviable on

account of alteration of the assessment and after the first day of April of a year,

shall be levied in respect of the remaining period of such year as nearly as may be

in the same proportion in which the remaining period bears to the whole year.

175

6.12 (viii) Liability to Pay the Tax:

(1) Where the owner of any building or land assessed to tax transfers such building or

land to any person, such owner as well as the transferee shall, within two months

from the date of such transfer, give a notice of the same to the Grama Panchayat.

(2) Where the owner of any building or land assessed to tax dies, his heirs who

succeed to the building or land shall, within two months from the date of the

death of such person give notice of the same to the Grama Panchayat.

(3) Where such transfer of ownership of the building or land or the death of the owner

of the building or land comes to the knowledge of the Grama Panchayat, either

through a notice under the sub-rule (1) or (2) or otherwise it shall, after such

enquiry as it may deem fit, substitute the names of the transferee or the legal heirs

of the deceased owner, as the case may be, in the records of the Grama Panchayat.

6.12 (ix) Liability to Give Notice in Case of Demolition or Removal of a Building:

Owner of the building or any portion of the building assessed to tax under

these rules shall, if such building or part thereof, is demolished give notice of the

same in writing to the Secretary failing which he shall continue to be liable to pay the

tax in respect of such building till it is communicated to the Grama Panchayat:

Provided that nothing in this rules shall apply in respect of a building or portion of a

building which has fallen down or is burnt.

6.12 (x) Revision of the Assessment List:

(1) It shall not be necessary to prepare a new assessment list every year but every part

of the assessment list shall be completely revised not less than once in every four

years.

(2) Grama Panchayat may adopt the valuation and assessment in the list of the

previous year for the year immediately following with such alteration as may be

deemed necessary.

176

6.12 (xi) Occupier’s Right to Recover the Tax Paid by Him:

Where the occupier of any building or land has paid the tax under sub-section

(2) of Section 199 of the KPR Act, in respect of such building or land, he shall be

entitled to be reimbursed by the owner of such building or land and may in addition

to, any other remedy open to him deduct the amount of tax so paid from the rent or

any other amount payable by him to the owner.

6.12 (xii) Remission of Assessment when Done:

Where any building or land assessed to tax has remained vacant and

unproductive for the whole or part of a year the Grama Panchayat shall remit or

refund proportionately the amount of tax in respect of the period of such vacancy:

Provided that no such remission or refund shall be granted unless the building or land

is vacant and underproductive for not less than sixty consecutive days and that notice

in writing of the fact of the building or land being vacant and unproductive has been

given to the Secretary: Provided further that no remission or refund shall be granted

for any period prior to the date of the receipt of the notice.

Table-6.13: Income of the GPs from Property Tax

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

2002-03 33.13 70.67 10.27 10.39 50.07 4.95

2003-04 62.19 87.16 23.86 6.69 46.98 3.20

2004-05 68.75 83.87 12.22 20.33 44.16 6.01

2005-06 76.86 88.89 12.09 41.15 81.74 6.60

2006-07 95.42 84.76 11.24 28.61 68.71 2.75

2007-08 58.95 85.13 8.99 38.82 65.22 3.14

Average 65.88 83.41 13.11 24.33 59.48 4.44

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

177

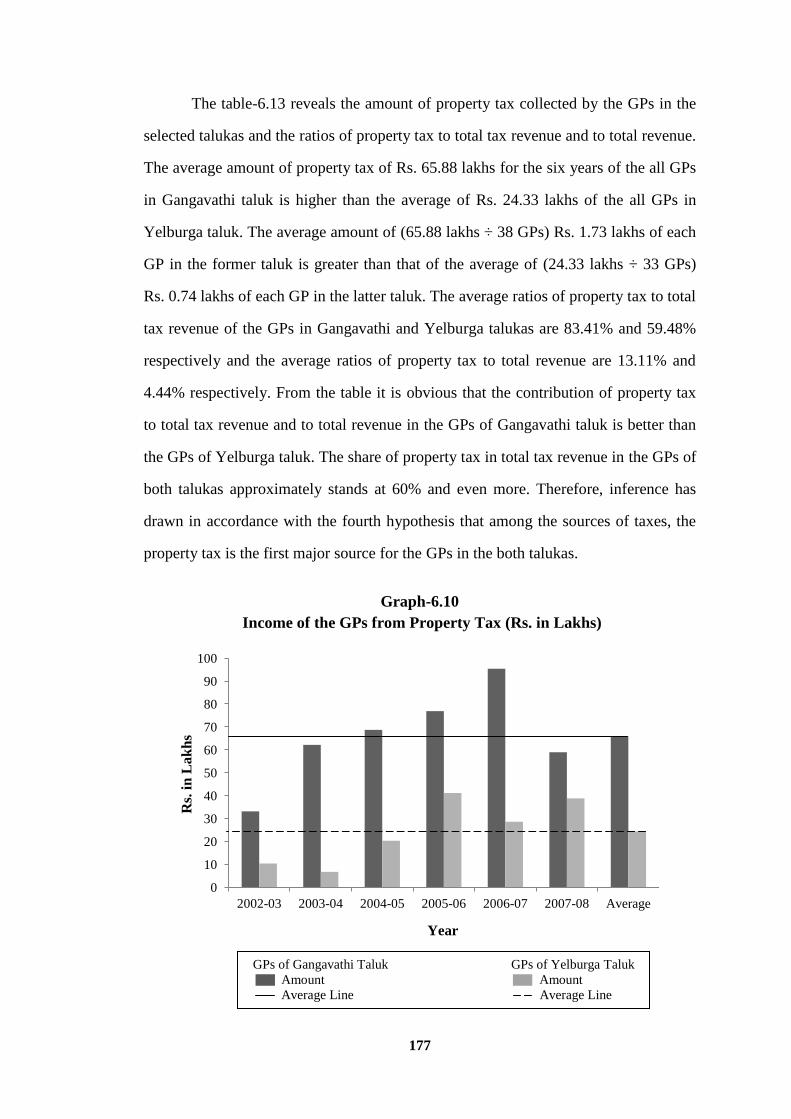

The table-6.13 reveals the amount of property tax collected by the GPs in the

selected talukas and the ratios of property tax to total tax revenue and to total revenue.

The average amount of property tax of Rs. 65.88 lakhs for the six years of the all GPs

in Gangavathi taluk is higher than the average of Rs. 24.33 lakhs of the all GPs in

Yelburga taluk. The average amount of (65.88 lakhs ÷ 38 GPs) Rs. 1.73 lakhs of each

GP in the former taluk is greater than that of the average of (24.33 lakhs ÷ 33 GPs)

Rs. 0.74 lakhs of each GP in the latter taluk. The average ratios of property tax to total

tax revenue of the GPs in Gangavathi and Yelburga talukas are 83.41% and 59.48%

respectively and the average ratios of property tax to total revenue are 13.11% and

4.44% respectively. From the table it is obvious that the contribution of property tax

to total tax revenue and to total revenue in the GPs of Gangavathi taluk is better than

the GPs of Yelburga taluk. The share of property tax in total tax revenue in the GPs of

both talukas approximately stands at 60% and even more. Therefore, inference has

drawn in accordance with the fourth hypothesis that among the sources of taxes, the

property tax is the first major source for the GPs in the both talukas.

Graph-6.10

Income of the GPs from Property Tax (Rs. in Lakhs)

0

10

20

30

40

50

60

70

80

90

100

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Rs.

in

Lak

hs

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount Amount

Average Line Average Line

178

The graph-6.10 reveals that the highest and lowest yields from the property tax

are in the years of 2006-07 and 2002-03 respectively in the GPs of Gangavathi taluk;

while the highest and lowest yields from this tax are in the years of 2005-06 and

2003-04 respectively in the GPs of Yelburga taluk. The collection of the tax in the

GPs of the former taluk crossed the average line (Rs. 65.88 lakhs) for three years

i.e., 2004-05, 2005-06 and 2006-07; in case of the GPs in the latter taluk it has crossed

the average line (Rs. 24.33 lakhs) for last three years. The average line of the GPs in

Gangavathi taluk is much higher than that of the GPs in Yelburga taluk.

Graph-6.11

Property Tax of the GPs % to Total Tax Revenue

The above graph-6.11 shows the ratios of property tax to total tax revenue of

the GPs in the both talukas. The ratios of the GPs in Gangavathi taluk crossed the

average line (83.41%) for last five years; whereas in case of the GPs in Yelburga taluk

the ratios crossed the average line (59.48%) for last three years. From the graph, it is

evident that the contribution of property tax to total tax revenue of the GPs in

Gangavathi taluk is better than that of the GPs in Yelburga taluk. Therefore, the

0

10

20

30

40

50

60

70

80

90

100

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Year

Per

cen

tage

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

179

revenue component of property tax made significant contribution in the GPs of

Gangavathi taluk during the study period.

6.13 The Water Rate:

A GP may levy the water rate for supply of water for drinking and other

purposes. It is the revenue component of tax sources that is derived from own

accounts of GPs and collected from the residents living within the limits of

panchayats area.

6.13 (i) Period of Levy:

(1) The water rate under sub-section (2) of Section 199 of KPR Act may be levied on

the owner of a building for a year or part thereof and shall be paid every quarterly

commencing from the 1st day of April, 1st day of July, 1st day of October and 1st

day of January of such year.

(2) Where such owner has left the Panchayat area or cannot otherwise be found the

occupier of such building shall be liable for the water rate levied under KPR

(Panchayat Taxes and Fees) sub-rule (1).

(3) The occupier of the building who has paid the water rate under the sub-rule (2)

shall be entitled to be reimbursed by the owner of such building and may, in

addition to any other remedy open to him, deduct the amount of water rate so paid

from the rent or any other amount payable by him to the owner.

6.13 (ii) Remission for Temporary Stoppage of Water Supply:

If through any accident in the water works arrangements or due to any other

cause there is a temporary stoppage in the water supply, no reduction shall be claimed

in the water rate nor the Grama Panchayat shall be liable for damages for any loss or

inconvenience sustained by the rate payer; so, however, the Grama Panchayat may

grant proportionate remission in water rate if there is a stoppage of water supply

continuously for more than a month.

180

Alignment of water rate with total tax revenue and total revenue is presented

for the all GPs of the sample talukas in the following table.

Table-6.14: Income of the GPs from Water Rate

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

2002-03 6.30 13.44 1.95 7.94 38.27 3.79

2003-04 7.66 10.74 2.94 7.55 53.02 3.61

2004-05 13.22 16.17 2.35 9.76 21.20 2.89

2005-06 8.95 10.35 1.41 3.03 6.02 0.49

2006-07 17.16 15.24 2.02 13.03 31.29 1.25

2007-08 10.30 14.87 1.57 18.37 30.86 1.49

Average 10.60 13.46 2.04 9.95 30.11 2.25

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

The above table-6.14 shows the amount of water rate collected by the all GPs

in the both talukas and the ratios of water rate to total tax revenue and to total

revenue. The average amount of water rate of Rs. 10.60 lakhs for the six years of the

all GPs in Gangavathi taluk is higher than the average of Rs. 9.95 lakhs of the all GPs

in Yelburga taluk. However, the average amount of (9.95 lakhs ÷ 33 GPs) Rs. 0.30

lakhs of each GP in Yelburga taluk is greater than that of the average of (10.60 lakhs

÷ 38 GPs) Rs. 0.28 lakhs of each GP in Gangavathi taluk. As for the average amount

is concered the GPs in the both talukas exhibits more or less same position. The

average ratios of water rate to total tax revenue of the GPs in Gangavathi and

Yelburga talukas are 13.46% and 30.11% respectively and the average ratios of water

rate to total revenue are 2.04% and 2.25% respectively. From the table it is evident

that the contribution of water rate to total tax revenue and to total revenue in the GPs

of Yelburga taluk is better than the GPs of Gangavathi taluk. The share of water rate

in total tax revenue of the GPs in the both the talukas approximately stands at 30%

181

and even less. Therefore, inference has drawn in accordance with the fourth

hypothesis that among the sources of taxes, the water rate is the second major source

for the GPs in the both the talukas.

Graph-6.12

Income of the GPs from Water Rate (Rs. in Lakhs)

The graph-6.12 shows that highest and lowest yields from the water rate are in

the years of 2006-07 and 2002-03 respectively in the GPs of Gangavathi taluk; while

the highest and lowest yields are in the years of 2007-08 and 2005-06 respectively in

the GPs of Yelburga taluk. The collection of the water rate in the GPs of the former

taluk crossed the average line (Rs. 10.60 lakhs) for two years i.e., 2004-05 and 2006-

07; in case of the GPs in the latter taluk it has crossed the average line (Rs. 9.95 lakhs)

for the last two years. The average line of the GPs in Gangavathi taluk is just higher

than the GPs in Yelburga taluk.

The graph-6.13 reveals the ratios of water rate to total tax revenue of the GPs

in the both talukas. The ratios of the GPs in Gangavathi taluk crossed the average line

(13.46%) for three years i.e., 2004-05, 2006-07, and 2007-08; whereas in case of the

0

2

4

6

8

10

12

14

16

18

20

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Rs.

in

La

kh

s

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount Amount

Average Line Average Line

182

GPs in Yelburga taluk the ratios crossed the average line (30.11%) for four years

i.e., 2002-03, 2003-04, 2006-07 and 2007-08. From the graph, it is evident that the

contribution of water rate to total tax revenue of the GPs in Yelburga taluk is better

than the GPs in Gangavathi taluk. Therefore, the revenue component of water rate

made significant contribution in the GPs of Yelburga taluk during the study period.

Graph-6.13

Water Rate of the GPs % to Total Tax Revenue

6.14 The Other Taxes:

For the present study, low revenue yielding taxes are classified as other taxes

viz., entertainment tax, vehicle tax, advertisement and hoarding tax, tax on factory.

6.14 (i) Tax on Entertainment Other than Cinematograph Shows:

6.14. i (a) Interpretation:

(1) 'Entertainment' means and includes a drama, exhibition, amusements, games or

sports to which persons are entertained on payment for admission;

(2) ‘Payment for admission’ means and includes-

(a) Any payment for seats or other accommodation, a place of entertainment; and

0

5

10

15

20

25

30

35

40

45

50

55

60

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Average

Per

cen

tag

e

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Percentage Percentage

Average Line Average Line

183

(b) Any payment for a programme or synopsis of an entertainment;

(3) 'Proprietor' in relation to any entertainment includes owner, manager, agent or any

other person responsible for the management thereof.

6.14. i (b) Exemptions:

No tax on entertainment shall be levied in respect of an entertainment-

(a) Which is not open to the general public.

(b) The proceeds of which are intended to be utilised for the public, educational,

cultural or charitable purposes.

6.14. i (c) Levy and Recovery of Entertainment Tax:

The tax on entertainment shall be levied before the beginning of an

entertainment and shall be recovered from the proprietor.

6.14. i (d) Refund of Entertainment Tax:

(1) If after the payment of tax on entertainment the entertainment is not held on

account of any extenuating or unavoidable circumstances the amount of tax paid

shall be refunded to the proprietor.

(2) Grama Panchayat shall, unless there are reasons to believe that a claim for refund

under KPR (Panchayat Taxes and Fees) sub-rule (1) is not admissible sanction the

refunds of tax if- (i) an application in writing is made to the Adhyaksha within

three days from the date fixed for the entertainment; and (ii) The receipt for

having paid the entertainment tax is produced.

6.14 (ii) Tax on Vehicles Other than Motor Vehicles:

6.14. ii (a) Exemptions:

No tax under chapter VI of the KPR Act shall be levied on-

(a) Vehicles belonging to Central or State Government;

(b) Vehicles kept solely for sale by vehicle makers and dealers;

184

(c) Vehicles which are under repairs or kept at a vehicle maker for a period not

exceeding six months;

(d) Vehicles belonging to the Grama Panchayat, Taluk Panchayat or Zilla Panchayat.

6.14. ii (b) Levy of Vehicle Tax:

(l) Grama Panchayat may levy vehicle tax on the person having possession, custody

or control of any vehicle specified in Schedule IV to the Act, if such vehicle has

been kept or used within the Panchayat area for an aggregate period of not less

than 120 days in a year. Provided that no tax shall be levied on a vehicle for any

year-

(a) If full tax for that year in respect of such vehicles has already been paid to the

Grama Panchayat by some other person; or

(b) If the tax equal to or in excess of the amount payable in the Panchayat area in

respect of such vehicle for that year has already been paid to any other Grama

Panchayat.

(2) If during the middle of the year any person having possession, custody or control

of any vehicle liable to tax replaces such vehicle being incapable of use, by another

vehicle of the same description, no tax shall be levied again on the replacing

vehicle for the rest of the year.

6.14 (iii) Tax on Factory:

The tax on factory under Section 202 of KPR Act may be levied if a factory or

industry owner provides sanitary and other ameneties for buildings and land used by

the industry, the GP may in lieu of taxes, rates, fees receive such amount annually as

may be agreed between the GP and the factory / industry owner. If such agreement

cannot be reached, the CEO shall determine the amount payable by such owner.

Alignment of other taxes with total tax revenue and total revenue is presented

for the all GPs of the sample talukas in the table-6.15.

185

Table-6.15: Income of the GPs from Other Taxes

Year

GPs of Gangavathi Taluk GPs of Yelburga Taluk

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

Amount (Rs. in Lakhs)

% to

Total Tax

Revenue

% to

Total

Revenue

2002-03 7.45 15.89 2.31 2.42 11.66 1.15

2003-04 1.50 2.10 0.58 NA - -

2004-05 NA - - 15.95 34.64 4.72

2005-06 0.66 0.76 0.10 6.18 12.24 0.99

2006-07 NA - - NA - -

2007-08 NA - - 2.33 3.92 0.19

Average 1.60 3.13 0.49 4.48 10.41 1.17

Source: 1. Office of the Local Audit Circle, Koppal.

2. Offices of the GPs in Gangavathi & Yelburga Talukas.

Note: NA - Data Not Available.

The above table shows the amount of other taxes collected by the all GPs in

the both talukas and the ratios of other taxes to total tax revenue and to total revenue.

The average amount of other taxes of Rs. 4.48 lakhs of the all GPs in Yelburga taluk

is much higher than the average of Rs. 1.60 lakhs of the all GPs in Gangavathi taluk.

The average amount of (Rs. 4.48 lakhs ÷ 33 GPs) Rs. 0.14 lakhs of each the GP in

Yelburga taluk is much greater than that of the average of (1.60 lakhs ÷ 38 GPs) Rs.

0.04 lakhs of the each GP in Gangavathi taluk. The average ratios of other taxes to

total tax revenue of the GPs in Gangavathi and Yelburga talukas are 3.13% and

10.41% respectively; the average ratios of other taxes to total revenue are 0.49% and

1.17% respectively. From the table it is evident that the contribution of other taxes to

total tax and to total revenue in the GPs of Yelburga taluk is better than the GPs of

Gangavathi taluk. The share of other taxes in total tax revenue of the GPs in the both

talukas approximately stands at 10% and even less. Therefore, inference has drawn