Embed Size (px)

Citation preview

CHAPTER IV

COST AND RETURNS FROM MANGO CULTIVATION

4.1 INTRODUCTION

In this chapter, an attempt has been made to analyse cost and returns

from mango cultivation. For this purpose, the collected data have been

analysed and compared with reference to costs and returns including various

components of cost between two taluks namely, Shenkottai and Tenkasi in

Thirunelveli district. The varieties of mango mainly raised by the farmers are

Banganapalli, Alphonso, Neelam, Banglore and Sendhura in these two taluks

neither of them exclusively but in the same orchard. Hence, in the present

study, costs were worked out for mango crop as such and there is no separate

cost estimates for different varieties. Yield and returns were calculated

separately for each variety on the basis of the information collected from the

questionnaire. Then the pooled gross income was worked out for further

analysis.

4.2 COST COMPONENTS

Mango being a perennial horticultural crop, cost of production of mango

has been classified into direct and indirect costs. Direct cost included the

128

operation and maintenance costs and indirect cost included the annual share of

establishment cost, interest on fixed capital, interest on working capital and

depreciation.

4.1.1 Cost of Establishment of Mango Orchard

The pre-bearing costs incurred in the establishment of mango crop up to

bearing stage formed the establishment cost. The establishment cost included

all the costs incurred from the initial establishment i.e., seed material and

planting, fencing and gap filling up to the stage of bearing, i.e., 5th

and 6th

year.

The total establishment cost included that of initial establishment, plant

protection, fertilizer and manures, human labour, tillage, watch and ward, land

tax up to the stage of bearing and repair and upkeep of farm implements. The

implement cost for five years was accordingly estimated at the prevailing

prices of inputs during the period under study.

The cost of establishment of mango in Shenkottai and Tenkasi taluks is

presented in the following Table 4.1. Total cost of establishment of mango

orchard per acre for five years was found to be Rs.22328 in Shenkottai taluk

and Rs.19532 in Tenkasi taluk. The net establishment of mango orchard per

129

acre was Rs.20778 for Shenkottai orchard and Rs.18082 in the case of Tenkasi

orchard. The break-up details of costs are given in Table 4.1.

TABLE 4.1

COST OF ESTABLISHMENT OF MANGO ORCHARD PER ACRE

FOR 5 YEARS

Sl.

No.

Cost Components Shenkottai Taluk Tenkasi Taluk

In Rs. Percent In Rs. Percent

1. Initial Establishment

i) Seed material and Planting 1200 5.37 960 4.92

ii) Gap filling 48 0.21 72 0.37

iii) Fencing 680 3.05 760 3.89

2. Fertilizer and manures 600 2.69 400 2.05

3. Human labour 3,400 15.22 1140 5.84

4. Bullock labour 3,000 13.44 1800 9.22

5. Watch and ward 1000 4.48 1000 5.12

6. Interest on land value and land

tax

12,150 54.42 13,150 67.32

7. Recent and upkeep of farm

implements

250 1.12 250 1.27

8. Total establishment cost 22,328 100.00 19,532 100.00

9. Income from intercrop 1550 1450

10. Net establishment cost 20,778 18,082

130

The initial establishment costs such as seed material and planting, gap

filling and fencing account for 8.63 per cent of the total establishment cost in

Shenkottai taluk and 9.18 per cent in Tenkasi taluk. The average initial

establishment cost varied from Rs.1792 in Tenkasi taluk to Rs.1928 in

Shenkottai taluk.

Seed material and planting cost was Rs.1200 in Shenkottai and Rs.960 in

Tenkasi taluk. Fencing and gap filling costs were slightly higher in Tenkasi

than Shenkottai. The cost figures were Rs.680 for fencing and Rs.48 for gap

filling in Shenkottai and Rs.760 and Rs.72 for fencing and gap filling in

Tenkasi.

The life cycle of mango may be divided into five stages, i.e., the nursery,

the establishment in the field, the non-bearing period, the bearing period and

the ageing trees. The nutritional requirements in each of these periods would

normally differ. At the time of establishment in the field it is necessary to

ensure least mortality. Normally at the time of planting manures and fertilizers

were not applied since the application of manures would prove harmful.

Application of fertilizers and manures was not unique to all orchards. The cost

of fertilizer and manures was lowest in Tenkasi is more congenial than

131

Shenkottai for mango cultivation. Cost of fertilizers and manures was Rs.600

in Shenkottai and Rs.400 in Tenkasi and their percentage share in the total

establishment cost was 2.69 per cent and 2.05 per cent respectively.

The cost of human labour charges per acre for five years was worked out

to Rs.3,400 and Rs.1140 and it was accounted 15.22 per cent and 5.84 per cent

in the total cost of establishment in Shenkottai and Tenkasi taluks respectively.

The cost of human labour and its percentage share in total establishment cost is

higher in Shenkottai compared to Tenkasi. Cost of human labour included the

expenditure on labour for digging pits, filling the digs, planting, application of

manures and fertilizers, de blossoming, after cultivation such as weeding,

hoeing, guiding the water, etc. In Shenkottai more men and women were used

for proper watering up to six months than in Tenkasi and further wage rates are

higher for both men and women in Shenkottai compared to Tenkasi. The cost

of human labour was calculated at the price of Rs.40 per man-day in

Shenkottai and Rs.30 per man-day in Tenkasi which are the prevailing wage

rate during the period under study. This is why the reason for higher human

cost in Shenkottai than in Tenkasi. But, in the case of women labour in both

the taluks, 2 women-days of eight hours each were considered as one man-day

in the basis of the prevailing wage rate.

132

Inter cultivation was the main tillage operation in establishing and

established plantations. The main practice followed was ploughing. During the

period of establishment of orchards, six ploughings were common per year.

The cost of bullock labour per pair per day was Rs.100 and Rs.40 in Shenkottai

and Tenkasi respectively. It includes the cost of human labour engaged along

with the bullock pairs. Bullock labour cost per year per acre was worked out to

be Rs.600 in Shenkottai and Rs.360 in Tenkasi. The cost of bullock labour in

the total establishment cost was 13.44 per cent in Shenkottai and 9.22 per cent

in Tenkasi.

Watch and ward cost and repair and upkeep of farm implements were

found to be Rs.1000 and Rs.250 respectively in both Shenkottai and Tenkasi

taluks. But the percentage share of these costs in the total establishment cast

varies in these two taluks. The percentage share was 5.60 per cent in

Shenkottai and 6.39 per cent in Tenkasi.

The interest on land value and tax were substantial and it shared 54.42

percent and 67.32 per cent of the total establishment cost in Shenkottai and

Tenkasi taluk respectively. An interest rate of 10.50 per cent was charged on

the market value of land. The interest on land was lowest in Shenkottai taluk

133

with Rs.2,410 per annum and highest in Tenkasi taluk with Rs.2,610. The land

tax in both taluks was the same and the land tax per annum was Rs.20. the

variation in the value of land indicated the difference in their fertility levels

and their proximity to the market and the approach roads. The land values

during the period under study were Rs.22,952 and Rs.24,858 per acre in

Shenkottai and Tenkasi taluks respectively.

The mango orchards, especially in the first 3 to 5 years of their life are

intercropped with minor millets and pulses to utilise profitably the vacant

space lying between the trees. Here, the income from intercrop in the two

taluks was almost the same. The average net cost per acre to establish a mango

orchard was worked by deducting the average per acre income from intercrop

from the total establishment cost. The average total establishment cost per acre

of mango orchard amounted to Rs.22,328 in Shenkottai orchard and Rs.9,766

in Tenkasi orchard. The net establishment cost for establishing one acre in

Shenkottai mango orchard was Rs.20,378 and in the case of Tenkasi it was

amounted to Rs.18,082.

Mango being a perennial crop, its life time extends over a period of 50

years. The annual share of cost of establishment in the total cost of production

134

was Rs.415.56 Shenkottai taluk and Rs.361.64 in Tenkasi taluk. The annual

share of establishment cost was worked out based on the assessment that the

life time of mango is 50 years.1

4.1.2 Operation and Maintenance Cost of Mango Orchard

Operation and maintenance costs were those costs which were incurred

during the bearing stage. Expenditure on labour, tillage practices in terms of

bullock labour, manures and fertilizers, plant protection, watch and ward and

land tax form the cost of operation and maintenance of mango orchard.

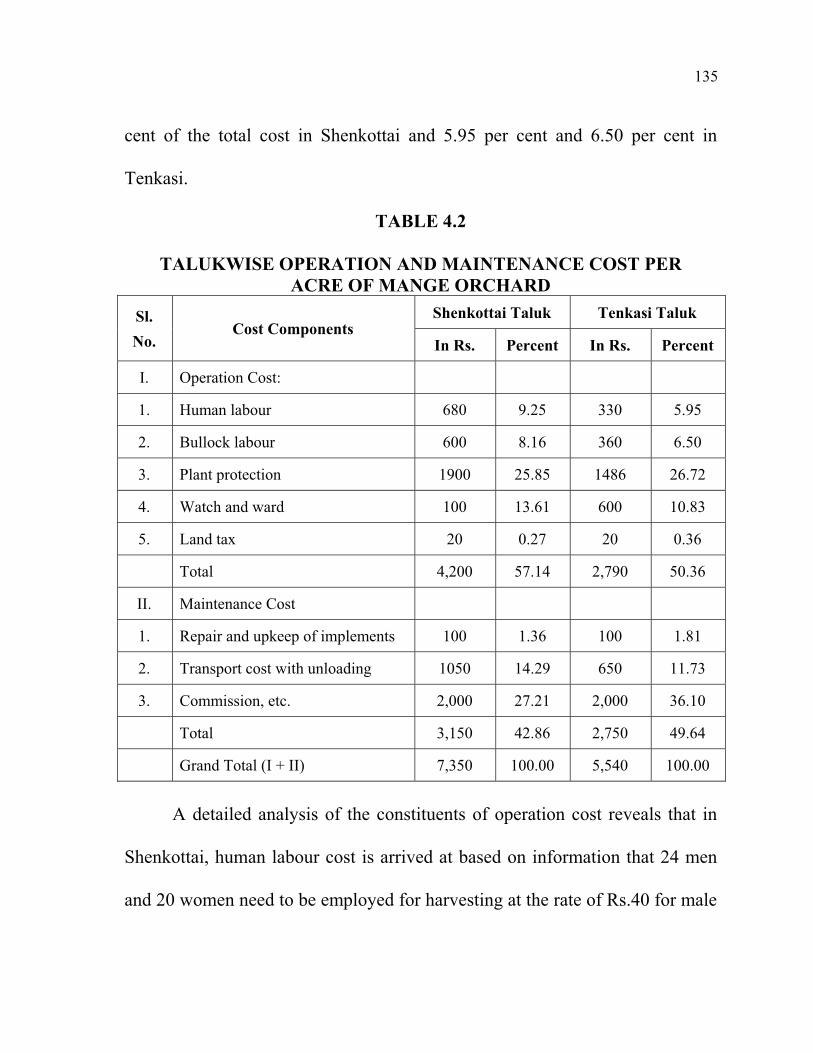

The taluk wise break-up of operation and maintenance cost is presented

in the following Table 4.2. It is evident from the Table that operation cost

which includes labour cost both human and bullock, cost on plant protection

and watch and ward cost plus land taxes accounts for 57.14 per cent of the total

cost on operation and maintenance on Shenkottai and 50.36 per cent in

Tenkasi. Of this, cost on plant protection ranks high with a percentage of 25.85

in Shenkottai taluk and 26.72 per cent in Tenkasi. Watch and ward cost ranks

next with a percentage of 13.61 and 10.83 in Shenkottai and Tenkasi taluks

respectively. Human and bullock labour cost form 9.25 per cent and 8.16 per

1 D.Singh, et.al., Survey on Fresh Fruits in Tamil Nadu (1971-73), Institute of

Agricultural research Statistics, New Delhi, 1976, p.38.

135

cent of the total cost in Shenkottai and 5.95 per cent and 6.50 per cent in

Tenkasi.

TABLE 4.2

TALUKWISE OPERATION AND MAINTENANCE COST PER

ACRE OF MANGE ORCHARD

Sl.

No.Cost Components

Shenkottai Taluk Tenkasi Taluk

In Rs. Percent In Rs. Percent

I. Operation Cost:

1. Human labour 680 9.25 330 5.95

2. Bullock labour 600 8.16 360 6.50

3. Plant protection 1900 25.85 1486 26.72

4. Watch and ward 100 13.61 600 10.83

5. Land tax 20 0.27 20 0.36

Total 4,200 57.14 2,790 50.36

II. Maintenance Cost

1. Repair and upkeep of implements 100 1.36 100 1.81

2. Transport cost with unloading 1050 14.29 650 11.73

3. Commission, etc. 2,000 27.21 2,000 36.10

Total 3,150 42.86 2,750 49.64

Grand Total (I + II) 7,350 100.00 5,540 100.00

A detailed analysis of the constituents of operation cost reveals that in

Shenkottai, human labour cost is arrived at based on information that 24 men

and 20 women need to be employed for harvesting at the rate of Rs.40 for male

136

and Rs.20 for female labour. Hence, the cost of human labour was worked to

be Rs.680.

Similarly six bullocks were hired at the rate of Rs.100 with the cost of

bullock labour amounting to Rs.600.

For plant protection chemicals worth Rs.100 was purchased and for

spraying 24 men and 24 women were employed at the rate of Rs.40 and Rs.20

respectively.

The total cost on plant protection including cost of chemicals (i.e.,

Rs.1000), cost of human labour (i.e., Rs.720) and cost of sprayers (i.e., Rs.180)

was Rs.1900.

In Tenkasi taluk, for harvesting 12 men and 20 women were employed

at the rate of Rs.30 and Rs.15 respectively and the total cost on human labour

was Rs.330.

Six bullocks were hired at the rate of Rs.60 with the cost of bullock

labour amounting to Rs.360.

137

Plant protection cost included the cost of chemicals (Rs.1000), cost of

human labour (Rs.360) i.e., the cost of employing 12 men and 24 women for

spraying at the rate of Rs.30 and Rs.15 respectively and cost of sprayers

(Rs.120). The total cost of plant protection was Rs.1480.

The cost of maintenance like repair and upkeep of implements, transport

and commission charges formed 42.86 per cent of the total cost in Shenkottai

and 49.64 per cent in Tenkasi of which commission charges alone accounted

for 27.21 per cent and 36.10 per cent in Shenkottai and Tenkasi respectively.

Transport and unloading cost is 14.29 per cent in Shenkottai and 11.73 per cent

in Tenkasi. Repair and upkeep of implements was less than two per cent in

both taluks.

On the whole the operation and maintenance cost together amounted to

Rs.7,350 in Shenkottai taluk and Rs.5,540 in Tenkasi.

4.1.3 Cost of Production

The cost of production of mangoes included (i) direct costs and (ii)

indirect costs. The direct costs included annual operation and maintenance

costs incurred during the reference year i.e., the agricultural year during which

138

primary data collection was made. The indirect costs included the annual share

of establishment cost up to bearing, interest on fixed and working capital and

depreciation of fixed assets. The detailed break-up of these costs is presented

in Table 4.3 for Shenkottai and Tenkasi taluks.

TABLE 4.3

COST OF PRODUCTION OF MANGO PER ACRE IN RADHAPURAM

AND NANGUNERI TALUKS

Sl.

No.

Cost Components Shenkottai Taluk Tenkasi Taluk

In Rs. Percent In Rs. Percent

I. Direct Cost:

Operation and Maintenance cost 7,350.00 68.84 5,540.00 66.06

II. Indirect Cost:

1. Annual share of establishment

cost

415.56 3.89 361.64 4.31

2. Depreciation 500.00 4.68 400.00 4.77

3. Interest on fixed capital 1530.00 14.33 1420.00 16.93

4. Interest on working capital 882.00 8.26 664.00 7.93

Total 3,327.56 31.16 2,845.64 33.94

Total cost (I + II ) 10,677.56 100.00 8,385.64 100.00

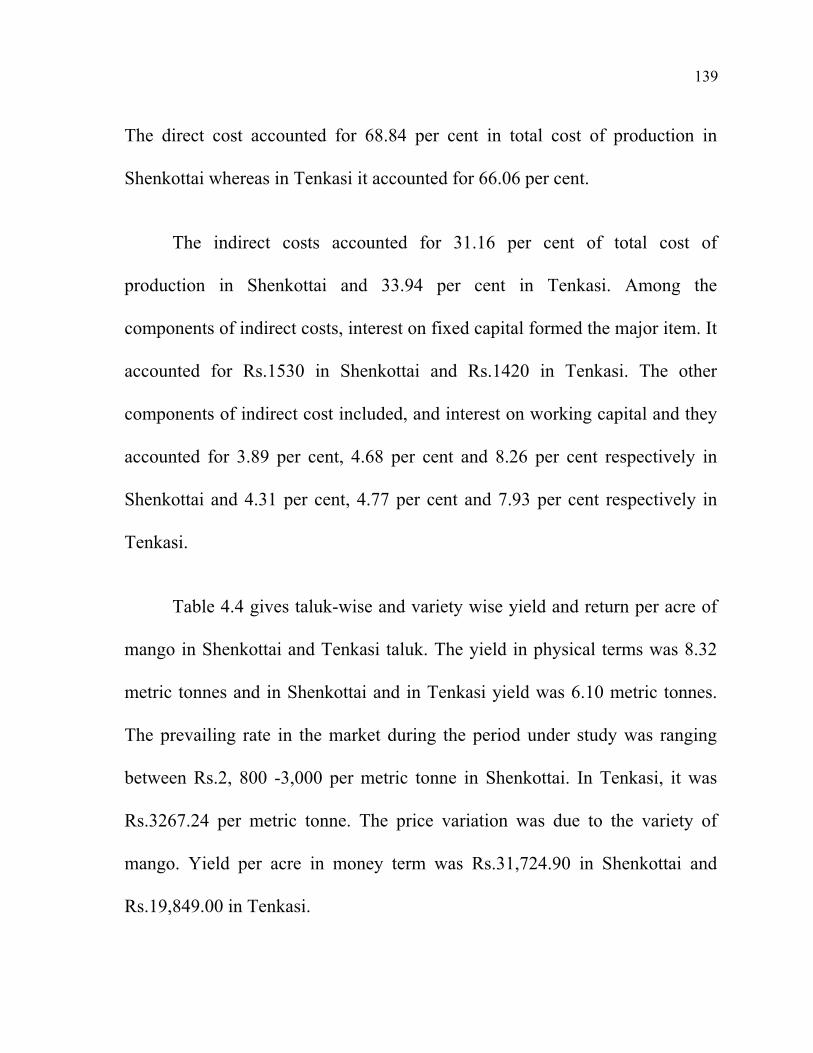

It could be seen from the Table 4.3 that the total cost of production was

Rs.10,677.56 in Shenkottai whereas in Tenkasi, it amounted to Rs.8,385.64.

139

The direct cost accounted for 68.84 per cent in total cost of production in

Shenkottai whereas in Tenkasi it accounted for 66.06 per cent.

The indirect costs accounted for 31.16 per cent of total cost of

production in Shenkottai and 33.94 per cent in Tenkasi. Among the

components of indirect costs, interest on fixed capital formed the major item. It

accounted for Rs.1530 in Shenkottai and Rs.1420 in Tenkasi. The other

components of indirect cost included, and interest on working capital and they

accounted for 3.89 per cent, 4.68 per cent and 8.26 per cent respectively in

Shenkottai and 4.31 per cent, 4.77 per cent and 7.93 per cent respectively in

Tenkasi.

Table 4.4 gives taluk-wise and variety wise yield and return per acre of

mango in Shenkottai and Tenkasi taluk. The yield in physical terms was 8.32

metric tonnes and in Shenkottai and in Tenkasi yield was 6.10 metric tonnes.

The prevailing rate in the market during the period under study was ranging

between Rs.2, 800 -3,000 per metric tonne in Shenkottai. In Tenkasi, it was

Rs.3267.24 per metric tonne. The price variation was due to the variety of

mango. Yield per acre in money term was Rs.31,724.90 in Shenkottai and

Rs.19,849.00 in Tenkasi.

140

TABLE 4.4

TALUK WISE YIELD AND RETURN PER ACRE

Particulars Shenkottai Taluk Tenkasi Taluk

Yield (in metric tonnes) 9.25 7.32

Return (in Rs.) 31,724.90 19,849.00

Source: Survey Data.

A higher yield and return are observed in Shenkottai taluk compared to

Tenkasi. The reasons for higher yield in Shenkottai taluk are: since long back

mango cultivation practice was set at Shenkottai taluk, a full pledged bearing

tree between the age of 20 to 35 years are more in each orchard. The second

main reason for higher yield is that in Shenkottai more number of trees is

planted per acre compared to Tenkasi. It has been observed that averages of 50

trees were planted per acre in Shenkottai whereas the average number of trees

per acre planted in Tenkasi was only 40. This is because of expecting a wide

spread canopy due to congenial soil and humidity in Tenkasi a more space

between the trees was given at the time of planting. It was observed that the

space between the trees was 10 m x 10 m in Tenkasi and 9 m x 9 m in

Shenkottai.

141

It may also be observed as one of the reasons that cultivators of mango

in Shenkottai are taking special care compared to Tenkasi cultivators as far as

certain cultivation practices are concerned such as watering the trees at

extraordinary drought situations, regular pruning, bunding, etc.

Higher return in Shenkottai was due to the fact that market was

diversified extending beyond the state i.e., Kerala, Karnataka, Gujarat, etc.,

whereas market was realised in Tenkasi only within the State i.e., Madurai,

Trichy, Karur and Dindigul. This is the main reason why the price differs for

the same variety in Shenkottai and Tenkasi.

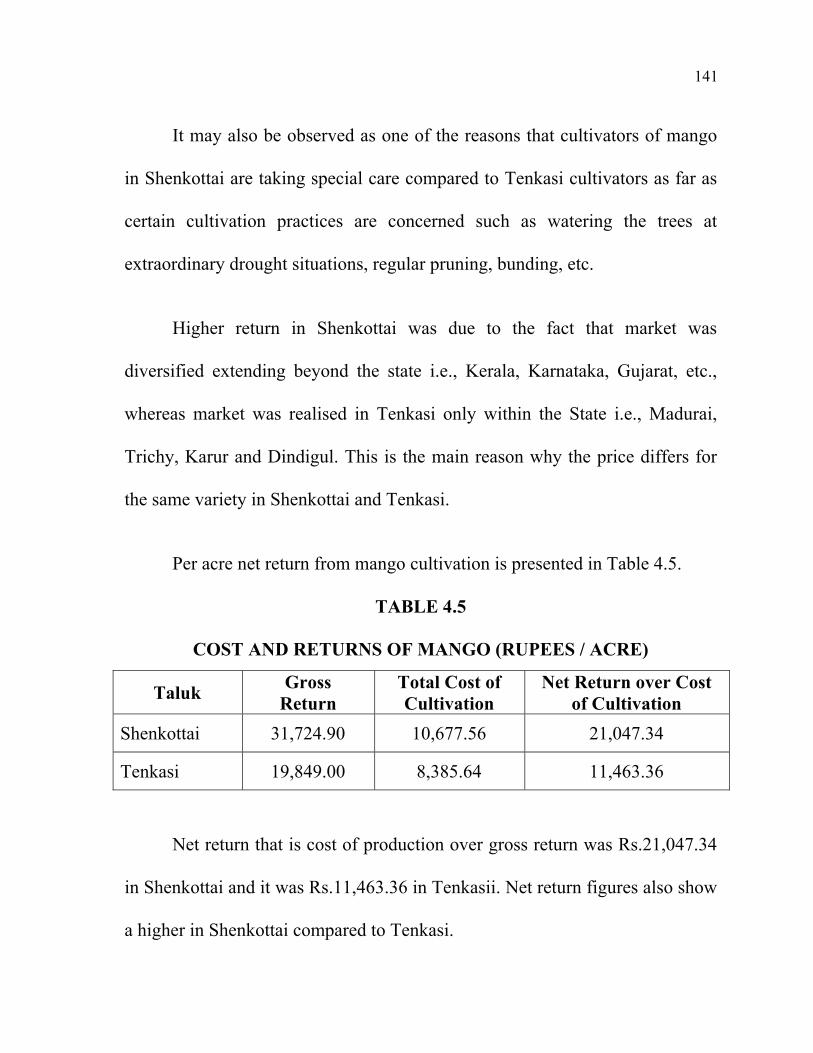

Per acre net return from mango cultivation is presented in Table 4.5.

TABLE 4.5

COST AND RETURNS OF MANGO (RUPEES / ACRE)

Taluk Gross

Return

Total Cost of

Cultivation

Net Return over Cost

of Cultivation

Shenkottai 31,724.90 10,677.56 21,047.34

Tenkasi 19,849.00 8,385.64 11,463.36

Net return that is cost of production over gross return was Rs.21,047.34

in Shenkottai and it was Rs.11,463.36 in Tenkasii. Net return figures also show

a higher in Shenkottai compared to Tenkasi.

142

4.3 AGE-WISE ANALYSIS OF MANGO ORCHARD

Mango being a perennial crop, its life time extends over a long period of

time. Various stages of cost of production could be estimated only if the cost

and yield figures during the entire span are taken into account. For the purpose

of analysis, life span of mango was classified into three stages, such as the

initial bearing stage, peak bearing stage and declining stage depending on the

yield potential of the orchard. Upon the 5th

year, establishment of the orchard

involves cost and no yield takes place.

Cost of production of one kilogram of mango in Shenkottai taluk is

presented in Table 4.6.

TABLE 4.6

COST OF PRODUCTION OF ONE KILOGRAM OF MANGO IN

SHENKOTTAI TALUK

Sl.

No.

Stage of the

Orchard

Cost of

Production

(in Rs.)

Per acre Yield

(in kg.)

Cost per

kilogram

(in Rs.)

1. 6th

to 20th

year 11,360.90 9,640.80 1.18

2. 21st to 35

th year 10,730.64 21,960.74 0.49

3. 36 and above 9,881.24 18,201.26 0.54

143

Cost of production is observed to decrease with the age of the orchard

and yield has increased from 9640.80 kg / acre to 21,960.74 kg / acre and has

declined to 18,201.26 kg / acre beyond 35 the year.

Cost of production per kilogram of mango has declined from Rs.1.18 to

Rs.0.49 in the second stage and increased to Rs.0.54 in the third stage. A

higher initial cost the reason why the yield of mango is raised to the maximum

only in the second stage and during the first and third stage yield is

comparatively low.

Cost of production per kilogram of mango in Tenkasi taluk is given in

table 4.7.

TABLE 4.7

COST OF PRODUCTION OF ONE KILOGRAM OF MANGO IN

TENKASI TALUK

Sl.

No.

Stage of the

Orchard

Cost of

Production

(in Rs.)

Per acre

yield

(in kg.)

Cost per

kilogram

(in Rs.)

1. 6th

20th

year 8,930.94 8740.24 1.02

2. 21st to 35

th year 8,280.00 16,300.70 0.50

3. 36 and above 7,941.18 11,480.96 0.69

144

From the Table 4.7, it is evident that even though cost per kilogram of

mango on the whole is less than the cost in Shenkottai taluk the same trend is

noticed i.e., higher cost and low yield in the first stage is followed by slightly

low cost and maximum yield in the second stage. During third stage cost of

production is very low and yield has started declining.

The cost per kilogram was Rs.1.02 in the initial period (6th 20th year)

and it has come down to Rs.0.50 in the second stage and increased to Rs.0.69

in the third stage.

4.3.1 Netted benefit – Cost ratio

The cost and return for the perennial orchard crops over the entire life

span is analysed in different stages since the returns are spread over a long

period. It would be more appropriate of net benefit and cost was taken into

account by giving due weight age to the time value of money.

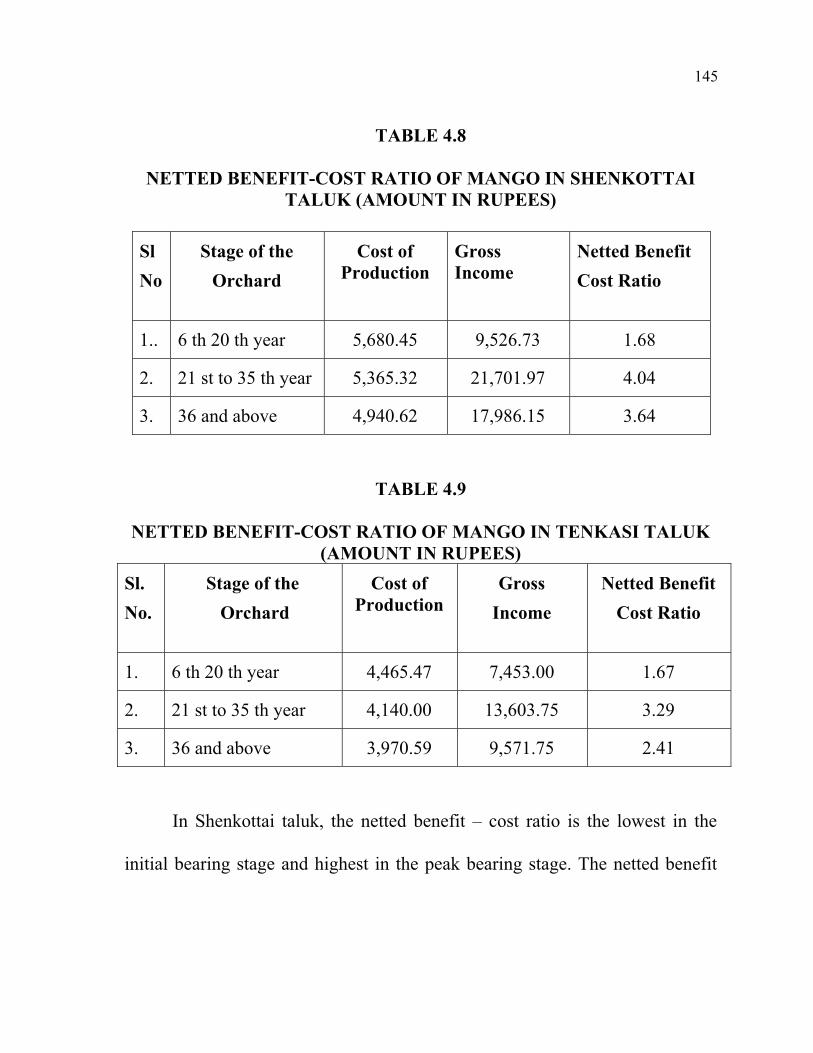

The netted benefit-cost ratio calculated for initial bearing, peak bearing

and declining stages of mango orchard in Shenkottai and Tenkasi taluks are

presented in Table 4.8 and 4.9.

145

TABLE 4.8

NETTED BENEFIT-COST RATIO OF MANGO IN SHENKOTTAI

TALUK (AMOUNT IN RUPEES)

Sl

No

Stage of the

Orchard

Cost of

Production

Gross

Income

Netted Benefit

Cost Ratio

1.. 6 th 20 th year 5,680.45 9,526.73 1.68

2. 21 st to 35 th year 5,365.32 21,701.97 4.04

3. 36 and above 4,940.62 17,986.15 3.64

TABLE 4.9

NETTED BENEFIT-COST RATIO OF MANGO IN TENKASI TALUK

(AMOUNT IN RUPEES)

Sl.

No.

Stage of the

Orchard

Cost of

Production

Gross

Income

Netted Benefit

Cost Ratio

1. 6 th 20 th year 4,465.47 7,453.00 1.67

2. 21 st to 35 th year 4,140.00 13,603.75 3.29

3. 36 and above 3,970.59 9,571.75 2.41

In Shenkottai taluk, the netted benefit – cost ratio is the lowest in the

initial bearing stage and highest in the peak bearing stage. The netted benefit

146

cost ratio was 1.68 in the first stage, 4.04 during the second stage and 3.64

during the third or declining stage.

In Tenkasi taluk, the netted benefit-cost ratio is less than in Shenkottai

taluk. Orchards in the age group of 6 to 20 shows netted benefit-cost ratio is

1.67 and for orchards in the age group 21 to 35 to the netted benefit-cost ratio

was 3.29 and to orchards above the age group 36 it was 2.41.

4.4 PRODUCTION PROBLEMS

4.4.1 Several problems make mango cultivation uncertain. Of these, the

major obstacles in mango production are given below:

(i) Incidence of Pests and Diseases

Mango is subject to a number of diseases during its development, right

from plants in the nursery with the fruits in storage or transit. When some of

these diseases assumed to be a virulent form these may be even a complete

crop failure. Among the various pests and diseases, the following are the most

important ones in the study area.

147

Pests

(a) Mango Stem Borer

It attacks the main trunk and the branches resulting tin their complete

drying. The borer is the fruit of a large, shout, long corn beetle. External

symptoms of attack are not always clear. It takes place either at ground level or

at the roots. The attacked trunk of the branches becomes hollow and breaks

very easily.

(b) Mango Hopper

This pest was prevalent in the mango flowering season, when it

multiplied in large numbers and proved devastating to the crop. Due to

recurrent annual damage by the orchards, some orchards fail altogether to

blossom.

(c) Mites

Among non-insect, pests, mites were of importance. They cause damage

not only to growing trees but also at seedling stages.

Diseases

a) Anthracnose of mango is prevalent in the study area. The tender shoots

and foliage were readily affected brown or dark circular or irregular

148

spots were formed on the leaves. Consequently, normal development

was prevented and they became crinkled.

b) Powdery mildew has been yet another common disease of mango. The

affected flowers or fruit drop prematurely reducing the crop

considerable or preventing the fruits set.

c) Bangalora variety was found to be more susceptible to black stem

disease.

(ii) Irregular Bearing

The mango tree is known to be an erratic bearer. Normally it crops

heavily in one year and stays sterile in the following year. In the study area,

almost all the orchardists raised mainly two varieties of mango namely,

Bangalora and Neelum. These two varieties are the most famous of the regular

annual bearers. In the study region, it is reported, that there are only an erratic

crop production and no rhythmic bearing tendency.

(iii) High velocity of Wind during Fruiting

Prevalence of strong winds especially at the onset of flowering would

result in the reduction of quantum of fruits. Similarly, strong winds at the early

stage of fruiting would also reduce the yield considerably.

149

(iv) Fruit crop

The fruit drop is another most important obstacle in mango production.

It could be observed in the study area that the most of the mango fruits drop in

very early stages i.e., occurred in the first three weeks of April after which it

was very little. The causes of fruit drop are climatic factors such as high

temperature, heavy wind etc., and disturbed water relations, lack of nutrition

and diseases and pests.

(v) Needs Heavy Investment

The mango orchards are mostly established in dry lands and hence

depended upon rainfall. The initial investment cost was high for the

establishment of mango orchards. Those farmers who cannot afford to meet the

initial expenditure heavily relied on money lenders and contractors.

Sometimes, orchards will be leased but to the contractors for getting credit and

the price offered by them is also very low.

4.4.2 Problems of Production of Mango

The mango cultivators identified five major problems of mango

production and they were ranked by using Garret’s scoring technique. The

results of Garret’s scoring and ranking are presented in Table 4.10.

150

TABLE 4.10

PRODUCTION PROBLEMS IN MANGO CULTIVATION

Sl.

No.

Factors Shenkottai Tenkasi

Mean Score Rank Mean Score Rank

1. Needs heavy

investment

53.48 I 47.16 II

2. Pest and disease 47.47 II 58.36 I

3. Climate Factors 32.30 III 38.16 III

4. Fruit drop 29.62 IV 31.48 IV

5. Irregular bearing 15.30 V 28.91 V

A perusal of the table shows that the orchardists encountered with five

problems for production of mango. In Shenkottai taluk, the most important

problems in the production of mango were heavy investments, pest and disease

and climatic factors which were ranked as first, second and third respectively.

In Tenkasi Taluk, it was clear from the analysis that the most important factor

which severely affected mango production was the pest and disease, needs

heavy investment and climate factors which were ranked 1st, 2

nd and 3

rd places.

151

An overall glance of this chapter is given below:

The varieties of mango viz., Banganapalli, Neelum, Bangalore and

Sendhura are mainly cultivated by the farmers in the selected taluks namely,

Shenkottai and Tenkasi which are situated at Tirunelveli district and neither of

them exclusively but in the same orchard. Hence, there were no separate cost

estimates derived for the different varieties; costs were worked out of the

mango crop as such. But in the case of yield per tree and yield per acre has

been calculated on the basis of information collected from the questionnaire.

Then the pooled gross income was used for further analysis.

As a perennial crop, cost of production of mango has been classified into

direct and indirect costs. Direct cost included the operation and maintenance

cost and indirect cost included the annual share of establishment cost, interest

on fixed capital, interest on working capital and depreciation.

The taluk wise average establishment cost per acre worked out to

Rs.22,328 and Rs.19,532 in Shenkottai and Tenkasi respectively. The costs

incurred on human labour, bullock labour and the interest on land value and

land tax were substantial and they shared 83.08 per cent of the total

establishment cost in Shenkottai and 82.38 per cent in Tenkasi. Among these

152

three, the share alone of interest on land value and land tax was 54.42 per cent

in Shenkottai and 67.32 per cent in Tenkasi.

In the case of human labour, cost incurred was Rs.3,400 in Shenkottai

and Rs.1140 in Tenkasi and constituted 15.22 per cent and 5.84 per cent of the

total establishment cost respectively. The cost of human labour is higher in

Shenkottai compared to Tenkasi the variation in human cost between two

taluks was due to the reason that more men and women are used for irrigation

purposes at Shenkottai compared to Tenkasi because in Shenkottai proper

water is given for young plant up to 6 months. Further, the prevailing wage

rates for men and women are higher in Shenkottai compared to Tenkasi. The

percentage share of cost of fertilizer and manures in the total establishment

cost was 2.69 per cent and 2.05 per cent in Shenkottai and Tenkasi

respectively.

The average net cost of establishment of a mango orchard per acre was

Rs.20,778 in Shenkottai and Rs.18,082 in Tenkasi. Here, the income from

intercrop in the two taluks was almost the same. The life time of mango crop

was assessed as 50 years according to various literatures and local enquires and

this period was adopted for working out the annual share of establishment cost

153

while calculating the cost of cultivation. The annual share of establishment

cost in the total cost of production was Rs.415.56 in Shenkottai taluk and

Rs.361.64 in Tenkasi taluk.

Regarding the operation and maintenance cost, the average operation

and maintenance cost for mango amounted to Rs.3,675 in Shenkottai and

Rs.2,770 in Tenkasi. The operation costs, which included human labour,

bullock labour, plant protection, watch and ward and land tax accounted for a

large share of 57.14 per cent and 50.36 per cent in Shenkottai and Tenkasi

respectively. The amount spent on plant protection was higher in both

Shenkottai and Tenkasi compared to other operational costs. The maintenance

costs constituted 42.86 per cent and 49.64 per cent of total operation and

maintenance cost in Shenkottai and Tenkasi respectively.

The average total cost of cultivation amounted to Rs.10,677.56 in

Shenkottai and Rs.82,385.64 in Tenkasi. Of this, 65 to 70 per cent was

incurred on direct cost and worked out to Rs.7,350 in Shenkottai and Rs.5,540

in Tenkasi. Next to direct cost, interest on fixed capital amounted for nearly 14

to 17 per cent of the total cost. The interest on working capital was worked out

to Rs.882 in Shenkottai and Rs.664 in Tenkasi.

154

The return per acre from mango orchard in Shenkottai taluk was

Rs.31,724.90 whereas in Tenkasi, it was Rs.19849. The net return was worked

out to Rs.21,049.34 in Shenkottai and it was Rs.11,462.56 in Tenkasi. Both

gross income and net return are higher in Shenkottai compared to Tenkasi

because of the following reasons:

(i) Higher yield in Shenkottai due to more number of well bearing

stage trees compared to Tenkasi.

(ii) Special intensive care of mango orchard taking as far as certain

cultivation practice such as watering the trees at an

extraordinary drought situations, regular pruning, bunding,

etc., and

(iii) The prices per metric tonne of mango are higher in Shenkottai

compared to Tenkasi mainly because of diversified marketing

of Shenkottai mango beyond the State of Tamil Nadu.

Mango, being a perennial crop its cost of production varies with the age

of the trees; likewise, the yield also varies much with the changes in the age.

For the purpose of analysis, life time of mango was classified into three stages,

155

viz., and the initial bearing stage from 6th year to 20th

year, peak bearing stage

from 21st year to 35

th year and declining stage from 36 and above.

It could be observed that the cost of production per kilogram of mango

during the age of 20 years was Rs.1.18 in Shenkottai and Rs.1.02 in Tenkasi.

As the average yield after 20th

year increased from 9,640.80 kilograms to

21,960.74 kilograms in Shenkottai and from 8,740.24 kilograms to 16,300.70

kilograms in Tenkasi, the cost of production between 21 – 35 years was

Rs.0.49 and 0.50 in Shenkottai and Tenkasi respectively. During the peak

bearing stage, the cost of production of mango per kilogram is almost the same

in both taluks. During the last declining stage, i.e., from 36th

year onwards, cost

per kilogram was higher and yield was also declined compared to peak bearing

stage in both taluks. The cost of production was declined in each stage of both

taluks.

The worked out netted benefit-cost ratio was 4.04 and 3.29 for orchards

having an age of 21 – 35 years in Shenkottai and Tenkasi respectively. The

higher netted benefit-cost ratio at this stage was expected as the production

was maximum at this period. It could also be noticed that the netted benefit-

cost ratio was declining after 36th

year in both taluks. However, the ratio was

156

comparatively higher as compared to the initial bearing stage. But in all the

three stages, netted benefit-cost ratios are higher in Shenkottai than in Tenkasi

taluk.

Regarding the problems of mango production, it was found that the most

important problems were heavy investment, pest and disease and climatic

factors.