Embed Size (px)

Citation preview

CHAPTER FIVEMeasuring And Evaluating The

Performance Of Banks And Their Principal Competitors

The purpose of this chapter is to discover what analytical tools can be applied to a bank’s financial statements so that management and the public can identify the most critical problems inside each bank and develop ways to deal with those problems

5-3

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Value of the Bank’s Stock

0ttr) (1

)E(D P

t

0

5-4

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Value of a Bank’s Stock Rises When:

Expected Dividends Increase

Risk of the Bank Falls

Combination of Expected Dividend Increase and Risk Decline

5-5

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Value of Bank’s Stock if Earnings Growth is Constant

g -r

D P

1

0

5-6

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Key Profitability Ratios in Banking

CapitalEquity Total

TaxesAfter IncomeNet (ROE) CapitalEquity on Return

Assets Total

TaxesAfter IncomeNet (ROA) Assetson Return

Assets Total

IncomeInterest Net Margin Interest Net

Assets Total

Incomet NoninteresNet Margin t NoninteresNet

5-7

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Key Profitability Ratios in Banking (cont.)

Assets Total

Expenses Operating Total

- Revenues Operating Total

Margin OperatingBank Net

gOutstandin SharesEquity Common

TaxesAfter IncomeNet (EPS) SharePer Earnings

5-8

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Breaking Down ROE

N e t P ro fit M a rg in =N e t In com e /T o ta l O pe ra tin g R e ve n ue

A sse t U tiliza tio n =T o ta l O p era ting R eve n ue /T o ta l A sse ts

R O A =N e t In co m e /T ota l A sse ts

E q u ity M u lt ip lie r =T o ta l A sse ts /E q u ity C a p ita l

R O E = N e t In co m e / T o ta l E qu ity Ca p ita l

x

x

5-9

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

ROE Depends On:

Equity MultiplierLeverage or Financing Policies

Net Profit MarginEffectiveness of Expense Management

Asset UtilizationPortfolio Management Policies

5-10

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Components of ROE for All Insured U.S. Banks (1991-2002)

Year ROE = NPM X AU X EM2002 14.51 = 17.16 X 7.82 X 10.822000 14.48 = 12.20 X 9.32 X 12.741999 14.92 = 14.01 X 8.91 X 11.951997 11.94 = 13.32 X 8.86 X 11.941995 14.19 = 12.68 X 8.93 X 12.531993 15.13 = 13.47 X 8.87 X 12.661991 8.00 = 5.32 X 10.17 X 14.77

5-11

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Bank Risks

Credit RiskLiquidity RiskMarket RiskInterest Rate RiskEarnings RiskCapital Risk

5-12

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Credit Risk

The Probability that Some of the Bank’s Assets Will Decline in Value and Perhaps Become Worthless

5-13

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

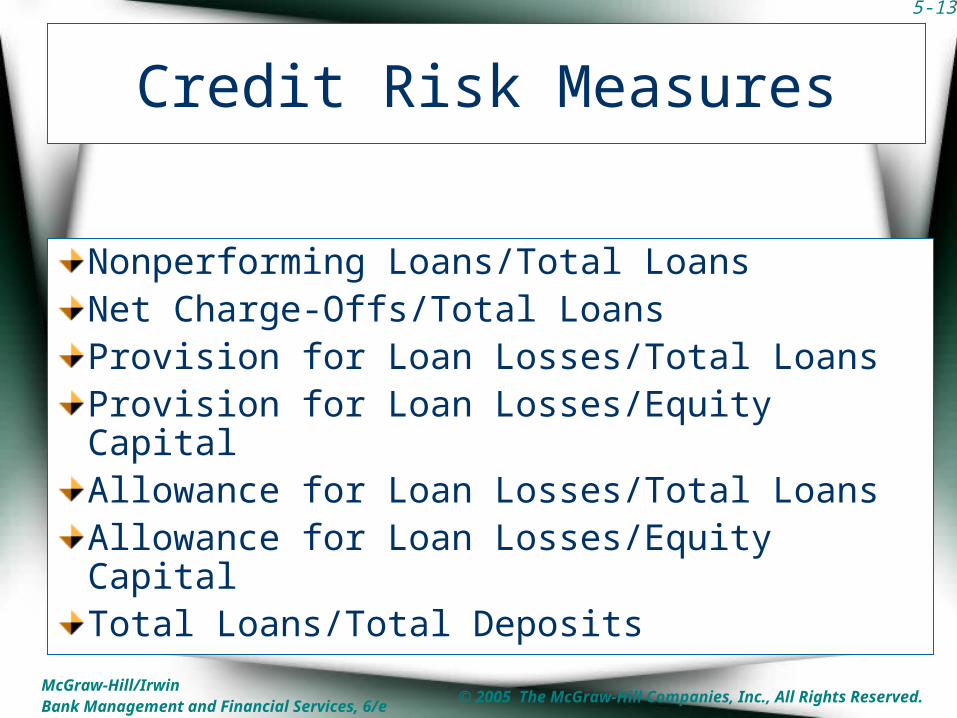

Credit Risk Measures

Nonperforming Loans/Total LoansNet Charge-Offs/Total LoansProvision for Loan Losses/Total LoansProvision for Loan Losses/Equity CapitalAllowance for Loan Losses/Total LoansAllowance for Loan Losses/Equity CapitalTotal Loans/Total Deposits

5-14

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Liquidity Risk

Probability the Bank Will Not Have Sufficient Cash and Borrowing Capacity to Meet Deposit Withdrawals and Other Cash Needs

5-15

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Liquidity Risk Measures

Purchased Funds/Total Assets

Net Loans/Total Assets

Cash and Due from Banks/Total Assets

Cash and Government Securities/Total Assets

5-16

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Market Risk

Probability of the Market Value of the Bank’s Investment Portfolio Declining in Value Due to a Rise in Interest Rates

5-17

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Market Risk Measures

Book-Value of Assets/ Market Value of Assets

Book-Value of Equity/ Market Value of Equity

Book-Value of Bonds/Market Value of Bonds

Market Value of Preferred Stock and Common Stock

5-18

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Interest Rate Risk

The Danger that Shifting Interest Rates May Adversely Affect a Bank’s Net Income, the Value of its Assets or Equity

5-19

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Interest Rate Risk Measures

Interest Sensitive Assets/Interest Sensitive Liabilities

Uninsured Deposits/Total Deposits

5-20

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Earnings Risk

The Risk to the Bank’s Bottom Line – Its Net Income After All Expenses

5-21

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Earnings Risk Measures

Standard Deviation of Net Income

Standard Deviation of ROE

Standard Deviation of ROA

5-22

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Capital Risk

Probability of the Value of the Bank’s Assets Declining Below the Level of its Total Liabilities. The Probability of the Bank’s Long Run Survival

5-23

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Capital Risk Measures

Stock Price/Earnings Per Share

Equity Capital/Total Assets

Purchased Funds/Total Liabilities

Equity Capital/Risk Assets

5-24

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

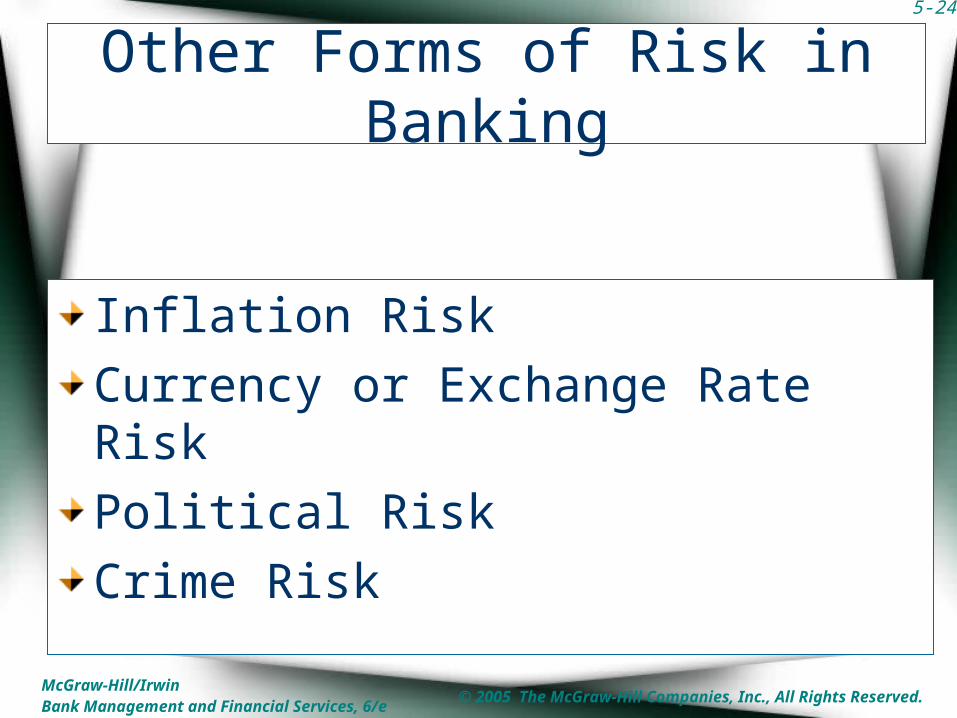

Other Forms of Risk in Banking

Inflation Risk

Currency or Exchange Rate Risk

Political Risk

Crime Risk

5-25

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Bank Performance Indicators Related to Size 2002

Performance IndicatorsAll

Banks

Under $100 Mill.

$100 Mill. To $1 Bill.

$1 Bill. To $10

BillOver

$10 Bill.ROA 1.37 1.05 1.26 1.48 1.38ROE 14.85 9.55 12.89 14.69 15.57

Net Operating Margin/TA 1.33 1.03 1.25 1.45 1.33Net Interest Margin/EA 4.13 4.32 4.44 4.32 4.03

Net Noninterest Margin/EA -1.03 -2.57 -1.29 -0.68 -2.16Operating Exp./Operating Rev. 55.03 68.19 61.85 55.65 53.35

PLL/Net Charge Offs 127.22 123.08 151.26 173.24 118.51Net Charge Offs/Total Loans 1.10 0.28 0.37 0.82 1.34

ALL/Total Loans 1.87 1.44 1.45 1.81 1.99Noncurrent Assets + Real Estate/TA 0.96 0.88 0.75 0.73 1.04

Net Loans/TotalDeposits 87.61 72.37 78.92 89.10 90.25Equity Capital/TA 9.24 11.12 9.91 10.29 8.84

Yield on Earning Assets 6.32 6.84 6.85 6.51 6.15Cost of Funding Earning Assets 2.18 2.52 2.41 2.18 2.12

5-26

McGraw-Hill/IrwinBank Management and Financial Services, 6/e

© 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

UBPR

The Uniform Bank Performance Report Provided by U.S. Federal Regulators so that Analysts Can Compare the Performance of One Bank Against Another