Embed Size (px)

DESCRIPTION

Chapter Five Appendix. DEPRECIATION METHODS. DEPRECIATION METHODS. Straight-Line Sum-of-the-Years’-Digits Double-Declining-Balance Modified Accelerated Cost Recovery System. EXAMPLE:. - PowerPoint PPT Presentation

Citation preview

Chapter Five Appendix

DEPRECIATION METHODS

DEPRECIATION METHODS

• Straight-Line

• Sum-of-the-Years’-Digits

• Double-Declining-Balance

• Modified Accelerated Cost Recovery System

EXAMPLE:

For all illustrations in this appendix, we will assume that a delivery van was purchased for $40,000. It has a five year useful life and salvage value of $4,000.

STRAIGHT-LINE METHOD

Under this method, an equal amount of depreciation will be taken each period.

STEP #1: Compute the depreciable cost

COST SALVAGE VALUE

= DEPRECIABLE COST

$40,000 $4,000 = $36,000

STRAIGHT-LINE METHOD

STEP #2: Divide the depreciable cost by the expected life of the asset.

Depreciation Expense per year=Depreciable Cost

Years of Life

$36,0005 years

= $7,200 per year

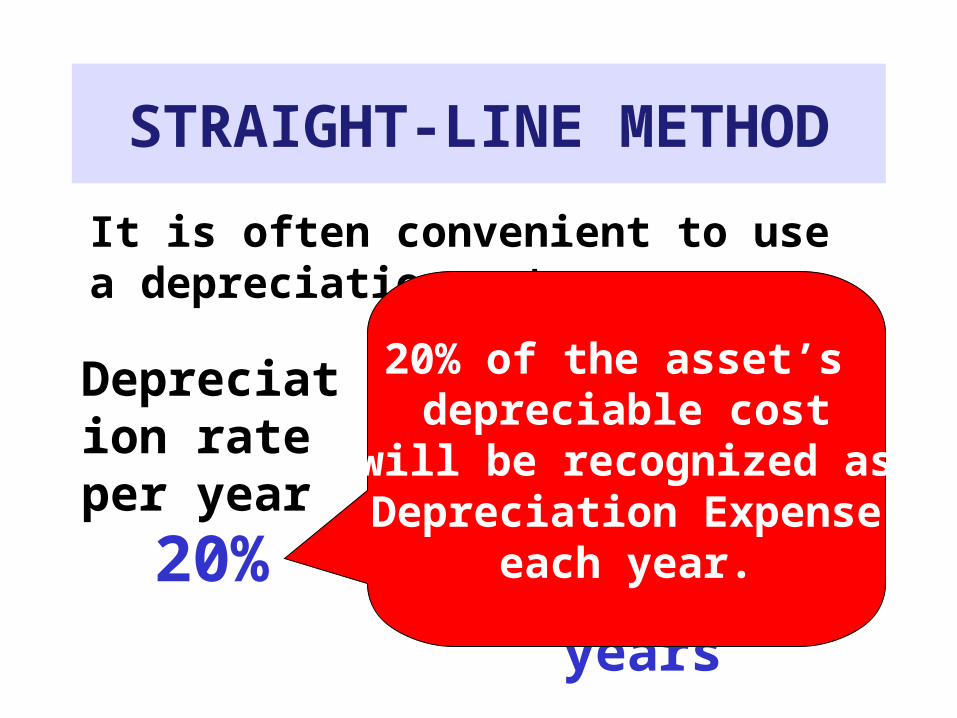

STRAIGHT-LINE METHOD

It is often convenient to use a depreciation rate per year.

Depreciation rate per year =

100%Years of Life

100%5 years=20%

20% of the asset’s depreciable cost

will be recognized asDepreciation Expense

each year.

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000x =

Original Cost minus Salvage Value $40,000 - $4,000

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

100% / Years of Life100% / 5 year life

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Depreciable Cost x Depreciation Rate$36,000 x 20%

$7,200

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Since this is the first year of the asset’s life, only this year’s

depreciation has accumulated.

$7,200 $7,200

STRAIGHT-LINE DEPRECIATION SCHEDULE

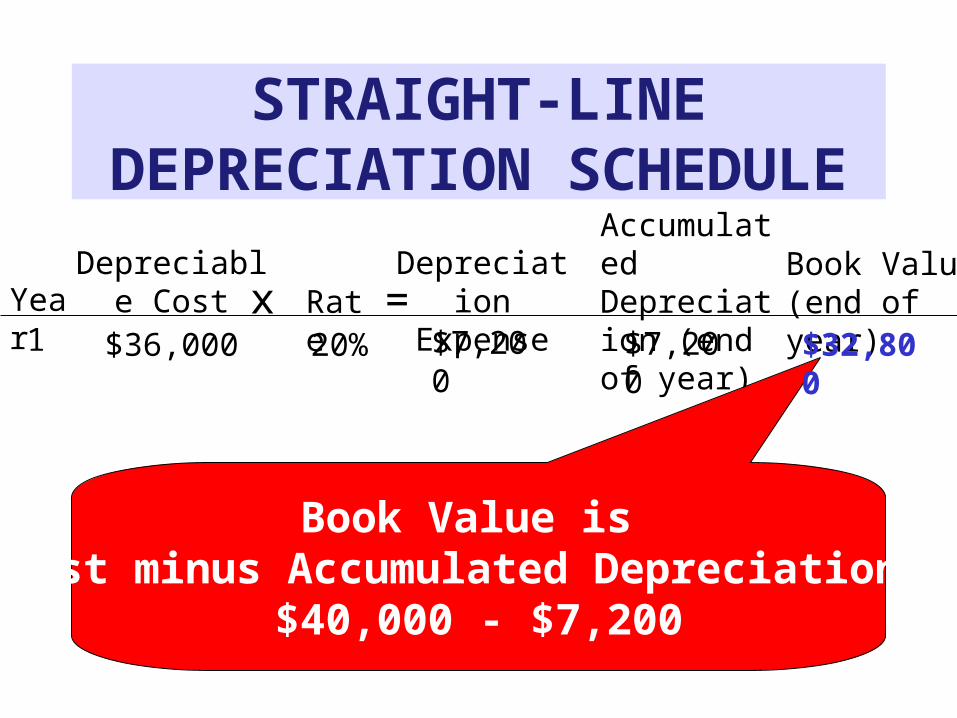

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Book Value is Cost minus Accumulated Depreciation.

$40,000 - $7,200

$7,200 $7,200 $32,800

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Depreciable Cost does not change.

$7,200 $7,200 $32,800

2 $36,000

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Depreciation Rate does not change.

$7,200 $7,200 $32,800

2 $36,000 20%

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Depreciation Expense remainsthe same each year.

$7,200 $7,200 $32,800

2 $36,000 20% $7,200

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Now two years of depreciation has accumulated.

$7,200 + $7,200

$7,200 $7,200 $32,800

2 $36,000 20% $7,200 $14,400

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Cost - Accumulated Depreciation$40,000 - $14,400

$7,200 $7,200 $32,800

2 $36,000 20% $7,200 $14,400 $25,600

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

Book Value declines overthe life of the asset.

$7,200 $7,200 $32,800

2 $36,000 20% $7,200 $14,400 $25,600

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

$7,200 $7,200 $32,800

2 $36,000 20% $7,200 $14,400 $25,600

3 $36,000 20% $7,200 $21,600 $18,400

4 $28,800$36,000 20% $7,200 $11,200

5 $36,000 20% $7,200 $36,000

The entire Depreciable Cost has now beenrecognized as Depreciation Expense.

STRAIGHT-LINE DEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 20%x =

$7,200 $7,200 $32,800

2 $36,000 20% $7,200 $14,400 $25,600

3 $36,000 20% $7,200 $21,600 $18,400

4 $28,800$36,000 20% $7,200 $11,200

5 $36,000 20% $7,200 $36,000

Book Value has fallen to the Salvage Value.

$4,000

SUM-OF-THE-YEARS’-DIGITS

• Depreciation is determined by multiplying the depreciable cost by a schedule of fractions.

• The numerator (top) of the fraction for a specific year is the number of years of remaining useful life.

• The denominator (bottom) of the fraction is determined by adding the digits of the years of the estimated life of the asset.

SUM-OF-THE-YEARS’-DIGITS

FORMULA:

DEPRECIABLE COST

Remember, Depreciable Cost isOriginal Cost minus Salvage Value.

SUM-OF-THE-YEARS’-DIGITS

FORMULA:

DEPRECIABLE COST X

YEARS REMAINING

This is measured from the beginning of the year. For example, to calculate

the first year’s depreciation….we would say there are 5 years remaining.

SUM-OF-THE-YEARS’-DIGITS

FORMULA:

DEPRECIABLE COST X

YEARS REMAINING

5 YEAR LIFE = 5+4+3+2+1 OR 15 10 YEAR LIFE =

10+9+8+7+6+5+4+3+2+1 OR 55

SUM-OF-THE-YEARS’-DIGITS

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000x =

Original Cost minus Salvage Value $40,000 - $4,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000x =

Five years remaining divided by sum-of-years’-digits of 15

(5+4+3+2+1)

5/15

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000x =

$36,000 X 5/15

5/15 $12,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Sum-of-the-years’-digits method recognizeslarge amounts of depreciation in the first

year of the asset’s life and smaller amounts each subsequent year.

5/15 $12,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Only this first year of depreciation has accumulated so far.

5/15 $12,000 $12,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Original Cost minus Accumulated Depreciation$40,000 - $12,000

5/15 $12,000 $12,000 $28,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Depreciable Costdoes not change.

5/15 $12,000 $12,000 $28,0002 $36,000

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Now there are 4 years remaining.

5/15 $12,000 $12,000 $28,0002 $36,000 4/15

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Since the rate (fraction) is smaller, the depreciation expense is also

smaller in the 2nd year.

5/15 $12,000 $12,000 $28,0002 $36,000 4/15 $9,600

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

There are now two years of depreciation accumulated.

$12,000 + $9,600

5/15 $12,000 $12,000 $28,0002 $36,000 4/15 $9,600 $21,600

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

Book Value falls as the asset ages.

5/15 $12,000 $12,000 $28,0002 $36,000 4/15 $9,600 $21,600 $18,400

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

5/15 $12,000 $12,000 $28,0002 $36,000 4/15 $9,600 $21,600 $18,400

3 $36,000 3/15 $7,200 $28,800 $11,200

4 $36,000 2/15 $4,800 $33,600 $6,400

5 $36,000 2/15 $2,400 $36,000

The entire depreciable cost has been recognized as Depreciation Expense.

SUM-OF-THE-YEARS’-DIGITSDEPRECIATION SCHEDULE

YearDepreciable

Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $36,000 x =

5/15 $12,000 $12,000 $28,0002 $36,000 4/15 $9,600 $21,600 $18,400

3 $36,000 3/15 $7,200 $28,800 $11,200

4 $36,000 2/15 $4,800 $33,600 $6,400

5 $36,000 2/15 $2,400 $36,000

Book value now matches the Salvage Value.

$4,000

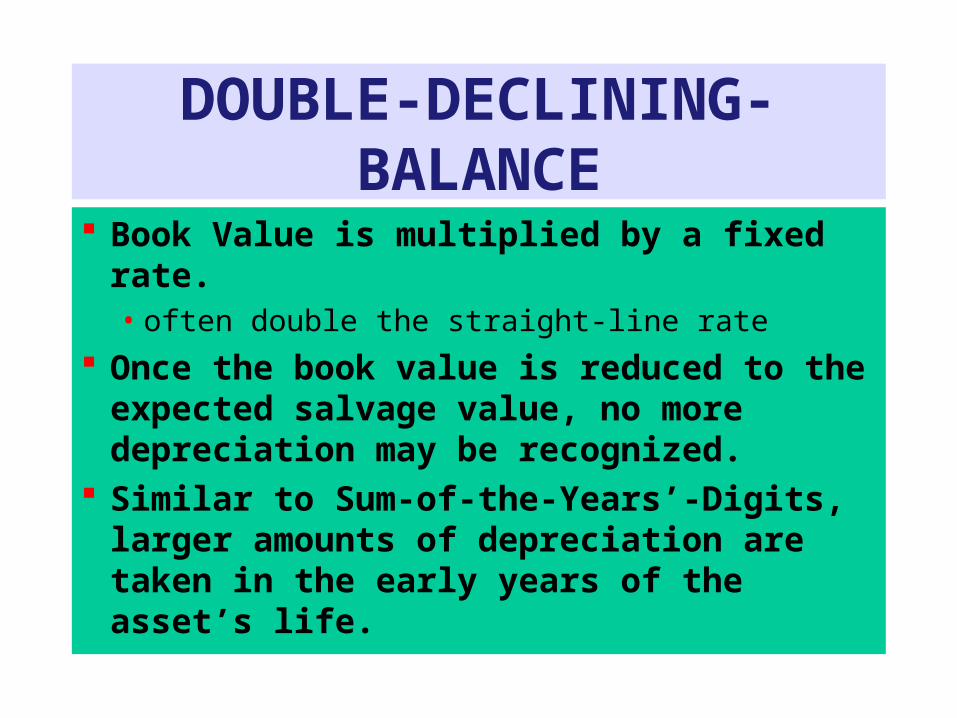

DOUBLE-DECLINING-BALANCE

Book Value is multiplied by a fixed rate.• often double the straight-line rate

Once the book value is reduced to the expected salvage value, no more depreciation may be recognized.

Similar to Sum-of-the-Years’-Digits, larger amounts of depreciation are taken in the early years of the asset’s life.

DOUBLE-DECLINING-BALANCE

FORMULA:

Book Value

Cost minus Accumulated Depreciation equals Book Value.

For an asset’s first year depreciation,Book Value equals Original Cost.

DOUBLE-DECLINING-BALANCE

FORMULA:

Book Value x (Straight-Line Rate)2

100% / Useful LifeFor our example……100%/5years = 20%

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

Original Cost minus Accumulated Depr. $40,000 - $0

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

Twice the Straight-Line Rate 2 (100%/5) or 2 x 20%

40%

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

Book Value x twice the Straight-Line Rate$40,000 x 40%

40% $16,000

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

First year’s depreciation is all that has accumulated.

40% $16,000 $16,000

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

Original Cost minus Accumulated Depreciation$40,000 - $16,000

40% $16,000 $16,000 $24,000

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

40% $16,000 $16,000 $24,0002 $24,000

The Book Value at the end of one year becomes the next year’sbeginning Book Value.

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Rate will be the same every year. Always twice the straight-line rate

40%40%

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Depreciation Expense will be smaller each year because the book value

is declining each year.

40%40% $9,600

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Two years’ depreciation has accumulated….$16,000 + $9,600

40%40% $9,600 $25,600

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Original Cost - Acc. Depreciation$40,000 - $25,600

40%40% $9,600 $25,600 $14,400

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

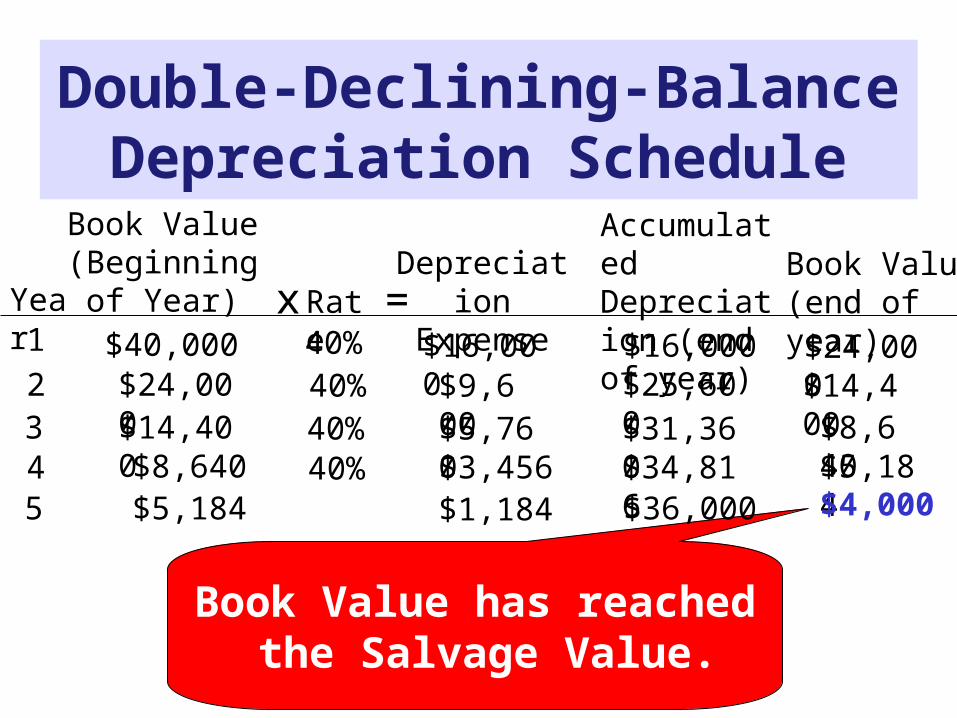

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Book Value can fall only to the amount of the Salvage Value.$5,184 - $4,000 = $1,184 to go!!

40%40% $9,600 $25,600 $14,400

3 $14,400 40% $5,760 $31,360 $8,6404 $8,640 40% $3,456 $34,816 $5,184

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Book Value x Rate = $2,073This would be too much depreciation.

Can recognize only $1,184

40%40% $9,600 $25,600 $14,400

3 $14,400 40% $5,760 $31,360 $8,6404 $8,640 40% $3,456 $34,816 $5,1845 $5,184 $1,184

Double-Declining-BalanceDepreciation Schedule

Year

Book Value (Beginning of

Year) RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000 x =

$16,000 $16,000 $24,0002 $24,000

Book Value has reached the Salvage Value.

40%40% $9,600 $25,600 $14,400

3 $14,400 40% $5,760 $31,360 $8,6404 $8,640 40% $3,456 $34,816 $5,1845 $5,184 $1,184 $36,000 $4,000

MODIFIED ACCELERATED COST RECOVERY SYSTEM Used for Tax Purposes Internal Revenue Service classifies

various assets according to useful life and sets depreciation rates for each year of the asset’s life.

Rates are then multiplied by the cost of the asset.

Abbreviated MACRS

MACRS example

A delivery van was purchased for $40,000. It has a five year useful life and salvage value of $4,000.

The IRS would give this vana 6-year life and no salvage

value.

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

IRS doesn’t allow a Salvage Value for this asset.

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

IRS sets the first year rate at 20%.

20%

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

Cost x Rate$40,000 x 20%

20% $8,000

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

Cost - Accumulated Depreciation$40,000 - $8,000

20% $8,000 $8,000 $32,000

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

IRS has a larger 2nd year rate.

20% $8,000 $8,000 $32,000

2 $40,000 32%

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

20% $8,000 $8,000 $32,000

2 $40,000 32% $12,800 $20,800 $19,200

3 $40,000 19.20%

Each year has a different rate.

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

20% $8,000 $8,000 $32,000

2 $40,000 32% $12,800 $20,800 $19,200

3 $40,000 19.20% $7,680 $28,480 $11,520

4 $40,000 11.52% $4,608 $33,088 $6,912

5 $40,000 11.52% $4,608 $37,696 $2,304

6 $40,000 5.76%

100%

At the end of the6 years, 100% of

the asset’s costwill have been recognized as

Depreciation Expense.

MACRSDepreciation Schedule

Year Cost RateDepreciation

Expense

Accumulated Depreciation (end of year)

Book Value (end of year)

1 $40,000x =

20% $8,000 $8,000 $32,000

2 $40,000 32% $12,800 $20,800 $19,200

3 $40,000 19.20% $7,680 $28,480 $11,520

4 $40,000 11.52% $4,608 $33,088 $6,912

5 $40,000 11.52% $4,608 $37,696 $2,304

6 $40,000 5.76%

100%

$2,304 $40,000 $0

$40,000